Abstract

We examine the effect of chief financial officer (CFO) turnover on the likelihood and size of asset impairments. Using Australian data, we find evidence consistent with incoming CFOs recording larger asset impairments, particularly when they are external hires with prior listed experience, or receive equity-based compensation. Our results also indicate that outgoing CFOs report higher profits in the year prior to their departure by reporting fewer and smaller asset impairments. This effect is larger when outgoing CFOs move to another listed firm or receive equity-based compensation, consistent with reputational and compensation incentives to maximise earnings. Overall, our results provide evidence of the independent influence CFOs have on financial reporting.

1. Introduction

The objective of this study is to extend prior research on asset impairments (Bond et al., 2016) by examining the effect of chief financial officer (CFO) turnover on the likelihood and size of non-current asset impairments, including both goodwill and other assets, in the period prior to, during, and immediately after CFO turnover. 1 Despite evidence regarding the significance of CFO turnover on firms’ reported results (e.g. Bamber et al., 2010; Brochet et al., 2011; Dejong and Ling, 2013; Demerjian et al., 2013; Ge et al., 2011; Geiger and North, 2006), whether outgoing and incoming CFOs use asset write-offs as a vehicle to manipulate accounting profit remains unexplored. 2 This lack of research is surprising given that the evaluation of the recoverability of non-current asset carrying values provides substantial discretion for CFOs to influence firms’ accounting numbers.

The motivation for this study is threefold. First, prior research largely attributes the ‘big bath’ phenomenon to a change in a firm’s chief executive officer (CEO) (e.g. Moore, 1973; Murphy and Zimmerman, 1993; Pourciau, 1993; Strong and Meyer, 1987; Wells, 2002). CEO turnover is, therefore, considered to be an important determinant of asset impairments (e.g. Bond et al., 2016). However, the primary responsibility for decisions involving sophisticated financial judgement is delegated to the CFO, and it is widely acknowledged that CFOs influence a firm’s reported results. 3 Prior evidence also suggests that CFO career opportunities are hindered by the arrival of a new CEO, increasing the likelihood of CFO replacement following CEO turnover (Collins et al., 2009; Fee and Hadlock, 2004; Mian, 2001). Therefore, the ‘big bath’ phenomena may be partly driven by concurrent CEO-CFO appointments and/or CFO turnover alone, which have been overlooked in prior research.

The second motivation for this study is to provide evidence on whether CFOs serve as ‘monitors’ of financial reporting integrity or act in self-interest around their turnover. This examination is important for firm stakeholders, as CFOs are legally expected to uphold financial reporting integrity and suffer labour market penalties for financial reporting failures (Bedard et al., 2014; Collins et al., 2009; Engel et al., 2015; Haislip et al., 2015). However, outgoing CFOs may act in self-interest due to compensation and career concerns, aiming to increase earnings in the year prior to their replacement. Specifically, departing CFOs have incentives to achieve performance targets in order to maximise their final pay (e.g. Geiger and North, 2006), maintain their position within the firm (e.g. Fee and Hadlock, 2004; Feng et al., 2011; Mian, 2001; Park et al., 2014) and increase the value of their human capital in the managerial labour market (e.g. Brickley et al., 1999; Fama, 1980; Mian, 2001). Similarly, incoming CFOs may engage in ‘big bath’ accounting in their year of appointment (e.g. Geiger and North, 2006) attributing poor results to their predecessors.

The final motivation for this study is to extend limited prior research on the factors associated with the recognition of non-current asset impairments. While Bond et al. (2016) find that impairment decisions appear to be discretionary, and Vanza et al. (2018) document asset impairment recognition is not associated with information asymmetry or the uncertainty about future returns, there is currently no evidence on whether non-accounting factors such as CFOs and executive turnover are associated with impairment decisions.

Our analysis is conducted using an Australian sample of 463 CFO changes over the period 1 July 2007 to 30 June 2015. We focus on firm-year observations around CFO turnover to limit the need to control for the endogenous nature of CFO turnover events. 4 We also investigate all asset impairments as opposed to just goodwill impairments, as Bond et al. (2016) find that non-goodwill asset impairments are dominant in the Australian environment. We find that incoming CFOs initiate significantly larger asset impairments in the year of appointment. 5 Conversely, we find that prior to their departure, outgoing CFOs are significantly less likely to record an asset impairment, and if they record one, it is significantly smaller in size.

Prior research indicates that the incentives and ability to manipulate earnings varies with the circumstances of the appointment (Geiger and North, 2006; Murphy and Zimmerman, 1993; Pourciau, 1993; Wells, 2002); therefore, we partition our sample based on various characteristics associated with the CFO turnover event. We document that when the outgoing CFO continues employment with the firm in another capacity, there is no evidence of impairments around the turnover. In contrast, when the outgoing CFO does not remain with the firm, obtains employment with another listed firm, or has equity incentives, there is a decrease in the likelihood and size of asset impairments prior to their departure. In terms of incoming CFOs, we document an increase in the size of impairments in their appointment year when they are an external hire, have prior experience with a listed firm, or receive equity compensation. Internally recruited CFOs, however, appear to wait until the year after their appointment to record asset impairments.

Additional testing demonstrates that CFOs exercise significant independent influence on firms’ financial reporting. Specifically, when we compare subsamples of firm-years with CEO turnover to those with CFO turnover, the likelihood and size of non-current asset impairments does not differ across the two groups. We also find, after dropping years with CEO turnover, that the likelihood and size of asset impairment increases in the year following a CFO turnover. The evidence in this study is therefore similar to Geiger and North (2006), who document incoming CFOs recognise income decreasing discretionary accruals in the year following a CFO change. The results also indicate that CFOs exert independent influence on financial reporting decisions.

This study makes a number of important contributions. First, it extends the existing literature on ‘big bath’ accounting by emphasising the significance of CFO turnover on firm financial reporting (e.g. Dejong and Ling, 2013; Demerjian et al., 2013; Ge et al., 2011; Geiger and North, 2006). While the majority of the literature focuses on CEO turnover and documents ‘big bath’ accounting in the year of a new CEO’s appointment, our study highlights the independent role of CFOs in earnings management. We demonstrate that the judgement required in estimating the recoverability of non-current asset carrying values provides opportunities for earnings manipulation by CFOs, irrespective of concurrent CEO turnover. Specifically, we show that CFOs can independently manage earnings through their decisions to recognise asset write-offs, with the size and timing of these write-offs appearing to align with their self-interest. This finding underscores the influence of CFO turnover on financial reporting practices and informs stakeholders about the potential for opportunistic behaviour by CFOs during executive transitions.

Second, while goodwill impairments have been studied extensively in prior research (Hayn and Hughes, 2006; Li et al., 2011), there is currently limited literature on the determinants of non-current asset impairments (Bond et al., 2016; Vanza et al., 2018). We contribute to and extend this literature by examining whether executive turnover is an additional factor influencing asset impairment decisions. Our results indicate that both CFO and CEO turnover independently drive asset impairments, suggesting that these factors should be included as controls in studies examining the recognition of non-current asset impairments. This inclusion enhances the understanding of the determinants of asset impairments and provides a more comprehensive view of the factors influencing financial reporting.

Third, our findings have implications for regulators (e.g. ASIC), auditors, and audit committees by suggesting that heightened scrutiny is needed for firms making CFO changes, as our evidence indicates these impairments are not justified by firm fundamentals. Specifically, ASIC may consider increasing surveillance of firms experiencing CFO turnover to identify unjustified asset impairments. Similarly, additional audit effort may be necessary around CFO turnover events to assess the validity of asset impairment decisions. Increasing the scrutiny of asset impairments is important for shareholders, as prior research highlights the negative market reaction to asset write-offs (Bens et al., 2011; Riedl, 2004).

The remainder of this study is structured as follows. Section 2 reviews prior literature and develops hypotheses. The regression models, which estimate the effect of CFO turnover on the likelihood and size of non-current asset impairments, are detailed in Section 3. Section 4 describes the sample selection process, while the empirical results are discussed in Section 5 along with additional analyses. Finally, Section 6 provides concluding remarks.

2. Literature review and hypotheses development

It is widely acknowledged that the CFO is the leader of the finance and accounting function. The growing importance of CFOs’ stewardship responsibilities is reflected in the US Sarbanes-Oxley Act and similar Australian regulatory reforms (i.e. CLERP 9), which require both the CEO and CFO to personally certify the accuracy and completeness of financial information. Following this legislative elevation of CFO financial oversight responsibility, an emerging literature recognises the rise of CFO visibility, power and importance beyond that of other executives (e.g. Aier et al., 2005; Bedard et al., 2014; Wang et al., 2012; Wang, 2010). As top-level managers with the capacity to exert control over the financial reporting process, CFO turnover is expected to be an important determinant of financial reporting integrity (e.g. Bamber et al., 2010; Brochet et al., 2011; Dejong and Ling, 2013; Demerjian et al., 2013; Ge et al., 2011; Geiger and North, 2006). The ability of CFOs to independently influence a firm’s accounting choices is particularly pertinent in complex financial reporting areas such as asset impairment, which requires the exercise of substantial judgement, professional scepticism, and discretion.

2.1. Outgoing CFOs’ Financial Reporting Incentives

CFOs may be motivated to maximise reported income prior to their departure for several reasons. First, compensation incentives may motivate CFOs to engage in earnings management particularly in the case of routine retirement (i.e. the horizon problem). It is well-established that bonus-based compensation contingent on financial measures provides top-level management with motivations to manipulate income (e.g. Healy, 1985) and prior research has found that CFO equity awards are positively associated with accruals management (Jiang et al., 2010), the likelihood of beating analyst forecasts (Jiang et al., 2010), the manipulation of information flow to capital market participants (Kim et al., 2011), and insider trading (Wang et al., 2012). Therefore, CFOs may use accounting discretion to reach performance targets to maximise their pay in the year preceding their departure (e.g. Geiger and North, 2006). Second, CFOs are also susceptible to career and reputational pressure to avoid reporting poor performance (e.g. Engel et al., 2015; Graham et al., 2005; Mian, 2001). For example, when CFO turnover is disciplinary, it is preceded by weak stock price (Mian, 2001) and/or operating performance (Engel et al., 2015; Mian, 2001). CFOs dismissed in these circumstances are also penalised in the labour market (Fee and Hadlock, 2004). 6 Therefore, outgoing CFOs have incentives to use their accounting discretion to maximise firm performance.

These career, reputation and compensation payoffs potentially serve as significant motivating factors in the financial reporting decisions of outgoing CFOs. In summary, outgoing CFOs are expected to bias earnings upwards in the year prior to departure leading to a lower likelihood and size of non-current asset impairments.

2.2. Incoming CFOs’ Financial Reporting Incentives

It has long been recognised that a change in leadership provides an incentive for incoming CEOs to bias earnings downwards (e.g. through large asset write-offs) in the initial year of appointment. This poor firm performance is then blamed on previous management and the subsequent improvements in performance (paper profits from accrual reversals) are attributed to the new management. This behaviour is what the literature describes as an ‘earnings bath’ (e.g. Moore, 1973; Murphy and Zimmerman, 1993; Pourciau, 1993; Strong and Meyer, 1987; Wells, 2002). It is plausible that incoming CFOs engage in similar behaviours, and Geiger and North (2006) use discretionary accruals to provide evidence consistent with this rationale. 7

The discussion above suggests that the likelihood and size of impairments are expected to decrease/(increase) in the period before/(after) CFO turnover. This leads to Hypothesis One:

H1(a): There is a decrease in the likelihood and size of non-current asset impairments in the period prior to CFO turnover.

H1(b): There is an increase in the size and likelihood of non-current asset impairments in the period(s) at or after CFO turnover.

2.3. The Nature of CFO Turnover and Impairment Decisions

Prior research investigating the effect of new executives on financial reporting identifies that the impetus and opportunities for earnings manipulation vary with the circumstances of the appointment. For example, the results by Geiger and North (2006) are predominantly driven by externally appointed CFOs, consistent with outsiders bringing in new perspectives and having less commitment to the status quo (e.g. Büttner et al., 2013; Geiger and North, 2006; Karaevli, 2007). Conversely, internal successions convey continuity in leadership dependent on existing practices, firm-specific knowledge, and established networks within the firm (Büttner et al., 2013; Karaevli, 2007). Given these findings, we also investigate if certain aspects of CFO turnover are driving impairment decisions. This is described in Section 4 below.

3. Research design

The model below, based on Bond et al. (2016), is estimated to test the association between CFO turnover (CFOTURN) and the likelihood (IMPAIR) and size (IMPAIRSIZE) of non-current asset impairments: 8

Model (1) is estimated (CFOTURN) separately for the year prior (CFOTURN_PY), the year of (CFOTURN) and following CFO turnover (CFOTURN_FY), consistent with Bond et al. (2016). IMPAIR is defined as a binary variable coded as one if a non-current asset impairment is recognised, zero otherwise. IMPAIRSIZE represents the total non-current asset impairment loss (excluding any impairment reversals) recognised by the firm in the current financial year scaled by prior year total assets. 9 Following Bond et al. (2016), model (1) includes controls for the factors that AASB 136 identifies as potential indicators of impairment. A book value in excess of market value is an external indicator of impairment (AASB 136, paragraph 12(d)) and therefore is included as an independent variable (BM) and measured as the ratio of the book value of equity (adjusted for the recognition of asset impairments) to the market value of equity at the end of the prior financial year. As a decline in market value is potentially not temporary for firms where BM > 1 or BM < 0 for more than 1 year, the model also includes a binary variable coded as one if BM > 1 or BM < 0 for two consecutive reporting periods prior to the current financial year end, zero otherwise (YRS). Both BM and YRS are expected to have a positive relation to IMPAIR and IMPAIRSIZE. Consistent with significant declines in market value being an external indicator of impairment (AASB 136, paragraph 12(a)), model (1) also controls for the buy-hold return of the stock over the prior financial year (BHR). A negative relation between BHR and the likelihood and size of impairments is expected. Given prior evidence we also add a control for CEO turnover (Wells, 2002) (CEOTURNOVER).

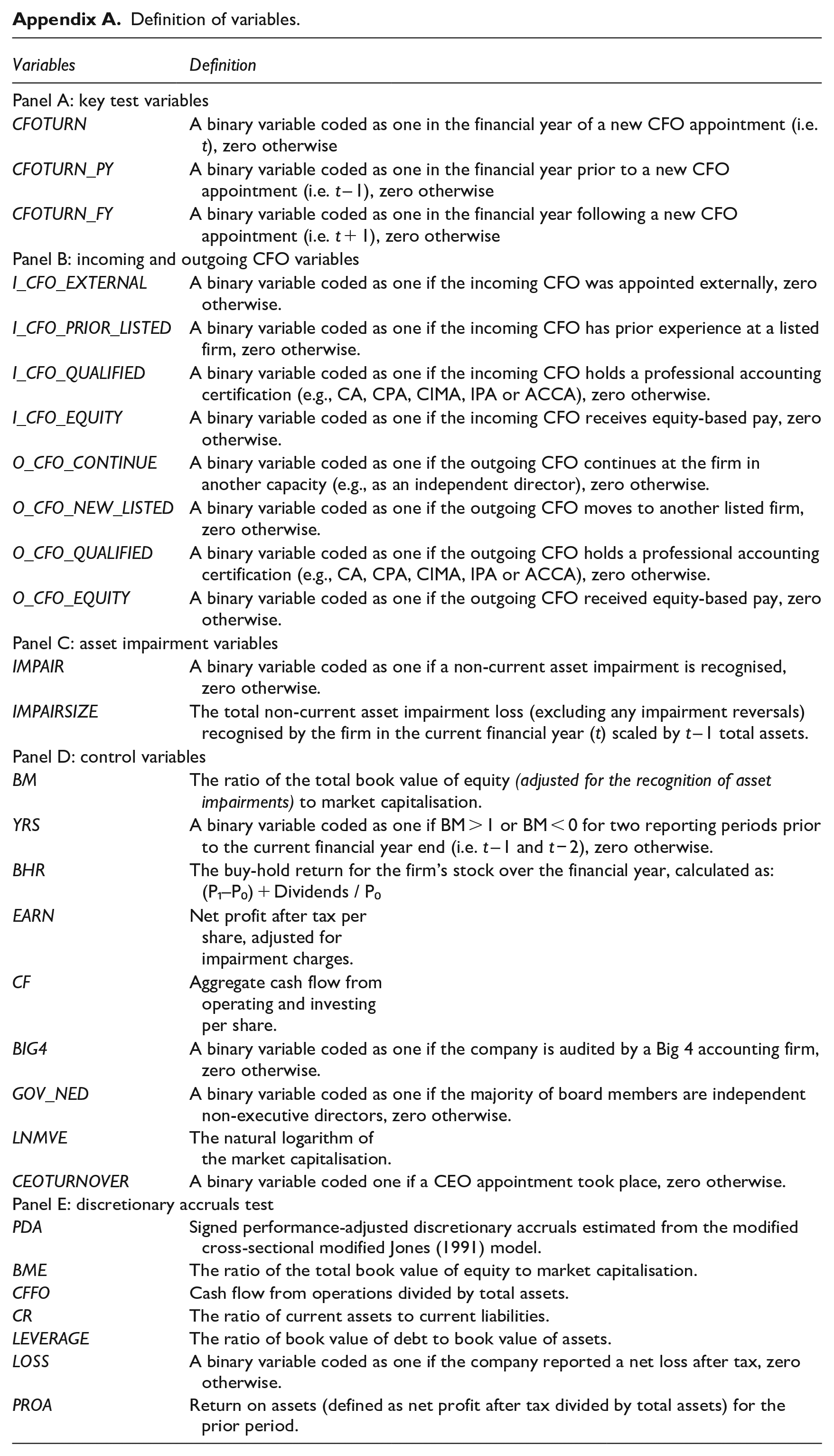

Model (1) also includes net profit after tax per share adjusted for impairment charges (EARN), and aggregate cash flow from operating and investing activities per share (CF). These variables control for internal indicators of impairment (AASB 136, paragraph 14(a)-(d)) and are expected to be negatively related to IMPAIR and IMPAIRSIZE. To control for effective corporate governance and external monitoring, the model includes controls for board independence (GOV_NED) and the use of a Big 4 audit firm (BIG4). Finally, the natural logarithm of market capitalization (LNMVE) is included to control for firm size and industry-fixed effects are included to control for factors that vary across industry. Appendix A provides definitions of all variables.

4. Sample selection and characteristics of CFO turnover

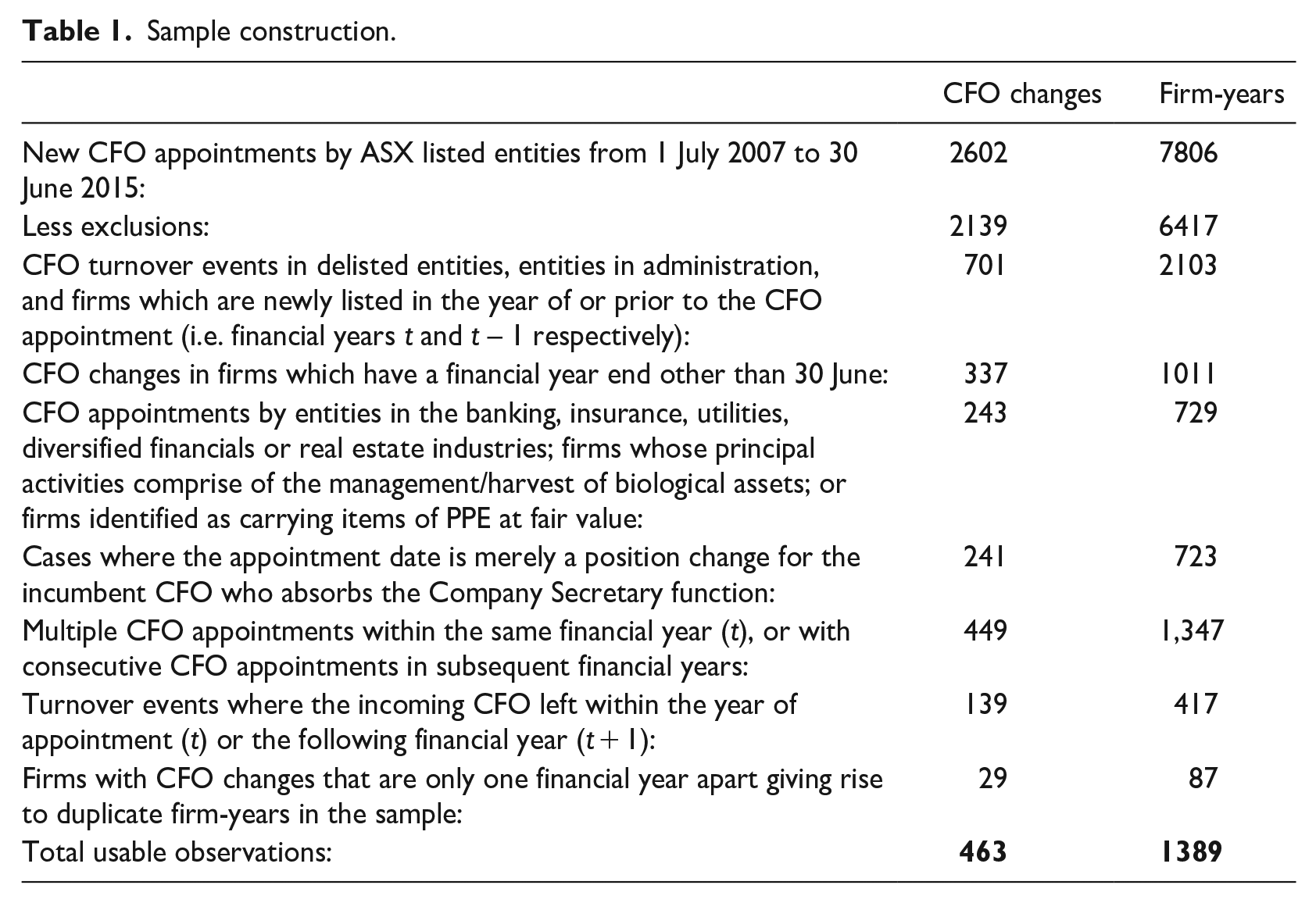

The Connect 4 Boardroom database is used to identify 2602 CFO appointments by ASX-listed entities between 1 July 2007 and 30 June 2015. 10 We exclude 701 observations relating to delisted companies, entities in administration and companies newly listed in the year of or prior to a CFO appointment. To maintain uniformity surrounding the timing of disclosures and impairments assessments, 337 CFO appointments in firms with financial reporting periods ending on a date other than 30 June are removed. Lu et al. (2013) document that over 80% of Australian firms have a June year end, and there are systematic differences between firms with June and non-June year-ends. The exclusion of non-June year-end firms thus reduces the likelihood that such differences impact our analysis. Also, the uniformity in financial year-end ensures all sample firms are assessing impairment at the same time and based on identical market conditions.

A further 243 observations are excluded due to industry or firm-specific financial reporting issues. That is, entities that re-value items of property, plant and equipment, as well as firms in the agriculture and real-estate investment sectors that may not recognise declines in asset values as impairments due to the application of fair value accounting. Financial and utilities firms operate in a different regulatory environment with distinct reporting requirements and are therefore also excluded.

In 241 cases, the CFO appointment is merely a position change for the incumbent CFO who absorbs the Company Secretary function, hence these observations are removed. A further 449 firms are deleted where multiple CFO appointments occur within the same financial year (year t) or recurrent CFO appointments in consecutive financial years. In 139 cases, the incoming CFO ceased employment within the appointment financial year (t) or the following financial year (t + 1) and are therefore excluded. Finally, 29 firms with CFO changes that are only one financial year apart are also removed. These exclusions result in a final sample of 463 unique CFO changes. Data are collected for three financial years surrounding each CFO turnover event (i.e. the period prior to (t – 1), during (t) and immediately following (t + 1) the CFO appointment) resulting in a sample of 1389 firm-years. A summary of the sample selection process is documented in Table 1.

Sample construction.

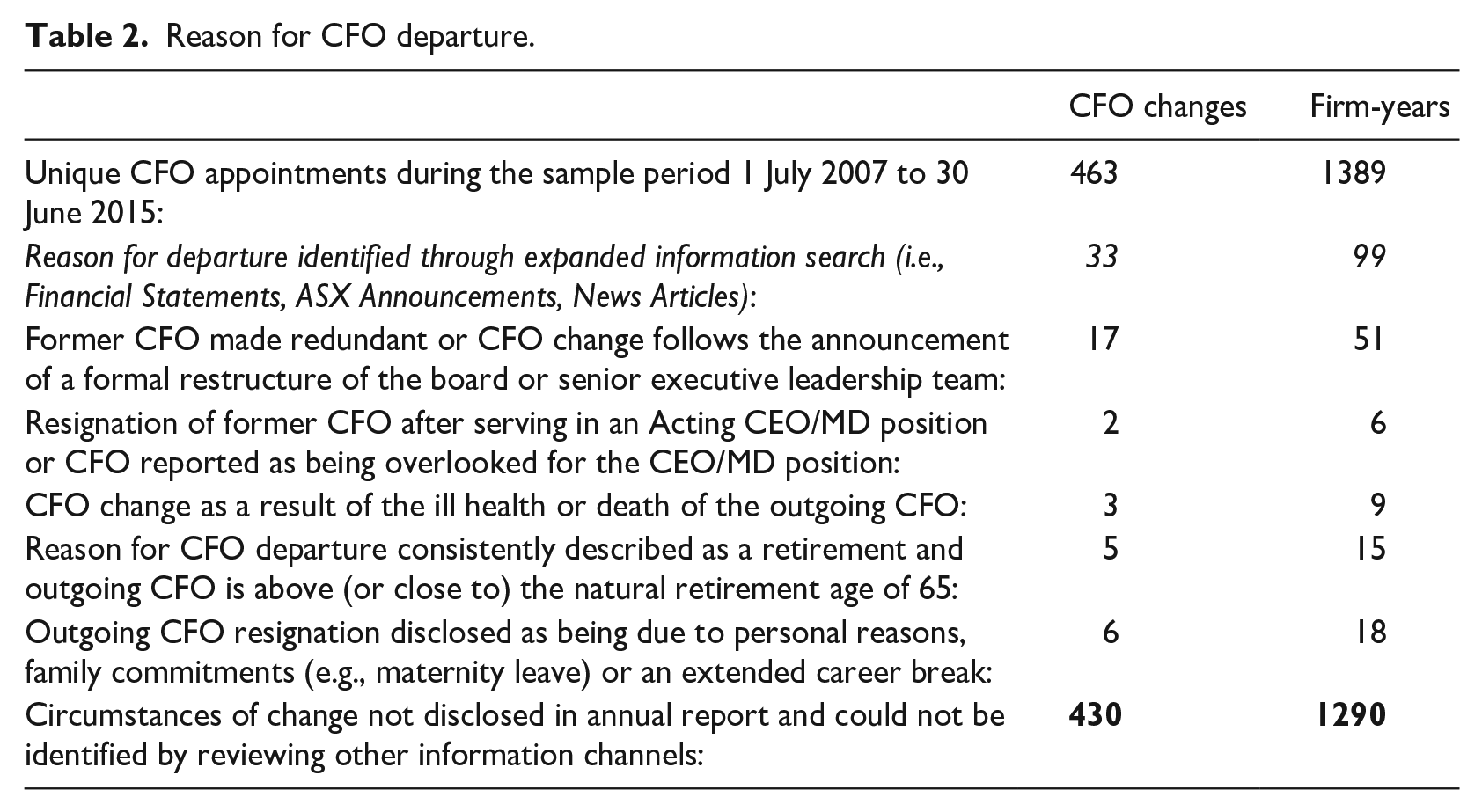

Table 2 documents the reason for CFO departures in cases where available information sources (e.g. annual reports, ASX announcements and news articles) provide relevant commentary. There are 17 CFO changes that follow a formal restructuring of the board or senior executive leadership team. In only five cases (i.e. 15 firm-years) was the reason for CFO departure consistently described as a retirement and the outgoing CFO was above (or close to) the natural retirement age of 65. Other departures were due to ill health or death (three events), family related (six events) or because the former CFO was overlooked for the CEO position (two events). The reluctance on the part of the directors to candidly discuss the reason for CFO changes is recognised in prior literature (e.g. Park et al., 2014). Therefore, it is unsurprising that in most cases (430 events), disclosures regarding the reason for CFO turnover are absent.

Reason for CFO departure.

To address this disclosure deficiency and identify characteristics of CFO turnover, we conduct an information search of ASX announcements, news articles, financial statement disclosures and the executives’ LinkedIn profiles. Research into Australian CFOs of ASX 100 listed firms shows that the ratio of internally and externally hired CFOs has been near identical over several years: 52% are hired externally and 48% are hired from within the firm (Chiswick, 2018, 2022); Therefore, an external hire alone is likely not enough to imply a suspicious turnover event which may lead to subsequent write-downs (Büttner et al., 2013; Mian, 2001; Vafeas and Vlittis, 2015). As such, we hand collect the following information which may affect the propensity to record an impairment surrounding CFO turnover: (1) qualifications and prior experience of the incoming CFO, (2) if the incoming CFO is awarded equity-based compensation, and (3) if the outgoing CFO continues with the firm in a different capacity or moves to another listed firm.

First, firms typically bring in ‘bigger and better’ talent, such as a CFO from a listed company, when they wish to overhaul a negative image or improve processes significantly, which could result in impairments. This view is supported by facts showing that 53% of CFO appointments in Australian ASX 100 firms are first-time group CFOs and only 32% of appointed CFOs have prior public company CFO experience (Chiswick, 2022). Second, if the incoming CFO is awarded equity-based compensation, it provides an incentive to make write-downs that will result in greater subsequent performance. Third, career progression and promotion are positive signals of CFO quality consistent with ex-post settling up in the labour market (Haislip et al., 2015). Therefore, if the outgoing CFO is appointed to another listed firm, there is likely an incentive to record fewer write-downs prior to departure.

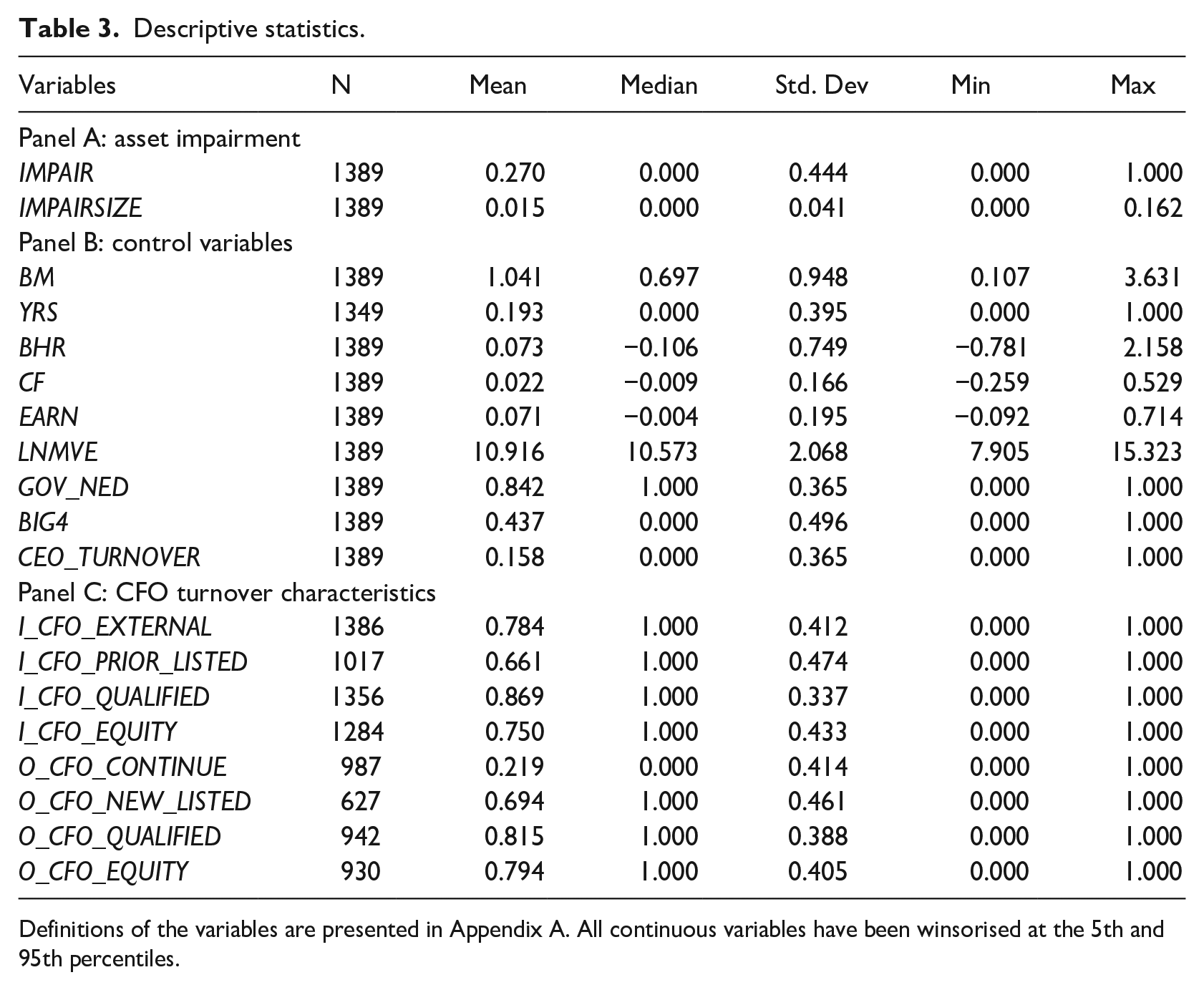

Panel C of Table 3 provides a breakdown of the above characteristics of CFO turnover.

Descriptive statistics.

Definitions of the variables are presented in Appendix A. All continuous variables have been winsorised at the 5th and 95th percentiles.

Despite our advanced search, we were unable to identify all characteristics for every CFO turnover event due to lack of disclosure; therefore, the number of observations differs across characteristics. Within our sample, most CFO appointments are from candidates external to the firm (78%) (I_CFO_EXTERNAL) and more than half have prior experience with listed firms (66%) (I_CFO_PRIOR_LISTED) which is higher than recent research from the ASX 100 (Chiswick, 2018, 2022); not surprisingly, most are qualified accountants (87%) (I_CFO_QUALIFIED) and receive equity-based compensation as part of their remuneration package (75%) (I_CFO_EQUITY). In terms of outgoing CFOs, roughly 22% continue with the firm in some capacity (O_CFO_CONTINUE) (e.g. as a non-executive director), and 69% take up a position on another publicly listed firm (O_CFO_NEW_LISTED). The majority are also qualified accountants (82%) and receive equity-based compensation (79%).

5. Empirical results

5.1. Descriptive Statistics

Director and other governance data required to estimate model (1) are obtained from the SIRCA Corporate Governance database. Financial data other than asset impairments are obtained from the Morningstar DatAnalysis Premium database. Asset impairments are hand collected from annual reports. Appendix A provides detailed variable definitions. All continuous variables are winsorised at the 5th and 95th percentile to reduce the influence of outliers. 11 Table 3 presents descriptive statistics for the variables used in the analysis for the full sample. Mian (2001) documents that CFO turnover is preceded by abnormally high CEO turnover. It is, therefore, unsurprising that CEO turnover is observed in roughly 16% of the sample (CEOTURNOVER). Asset impairments are recognised in 27% of firm-years (IMPAIR) and represent 1.5% of total prior period assets (IMPAIRSIZE) on average.

Significant variation across the financial variables is observed. The average market capitalization is $470.7 million with the median being $39.1 million. The mean (median) BM is 1.041 (0.697) which indicates skewness in the distribution of this variable. An indicator of impairment is present in a significant percentage (36.2%) of firm-years, which have a BM > 1 or BM < 0. Furthermore, 19.3% of firm-years have had a BM > 1 or BM < 0 for two consecutive prior financial reporting periods (YRS). Substantial skewness in both market (BHR) and accounting (EARN) returns is also evident with negative values apparent at the 50th percentile. The mean (median) value of BHR is 0.073 (−0.106). EARN has a mean (median) value of 0.071 (−0.004). A negative value of CF is also evident at the median (−0.009), the mean being 0.022. A material percentage of firm-years, therefore, exhibit both internal and external indicators of impairment. Big 4 accounting firms audit 43.7% of the sample (BIG4) and 84.2% of firm-years have a majority of non-executive directors on the board (GOV_NED).

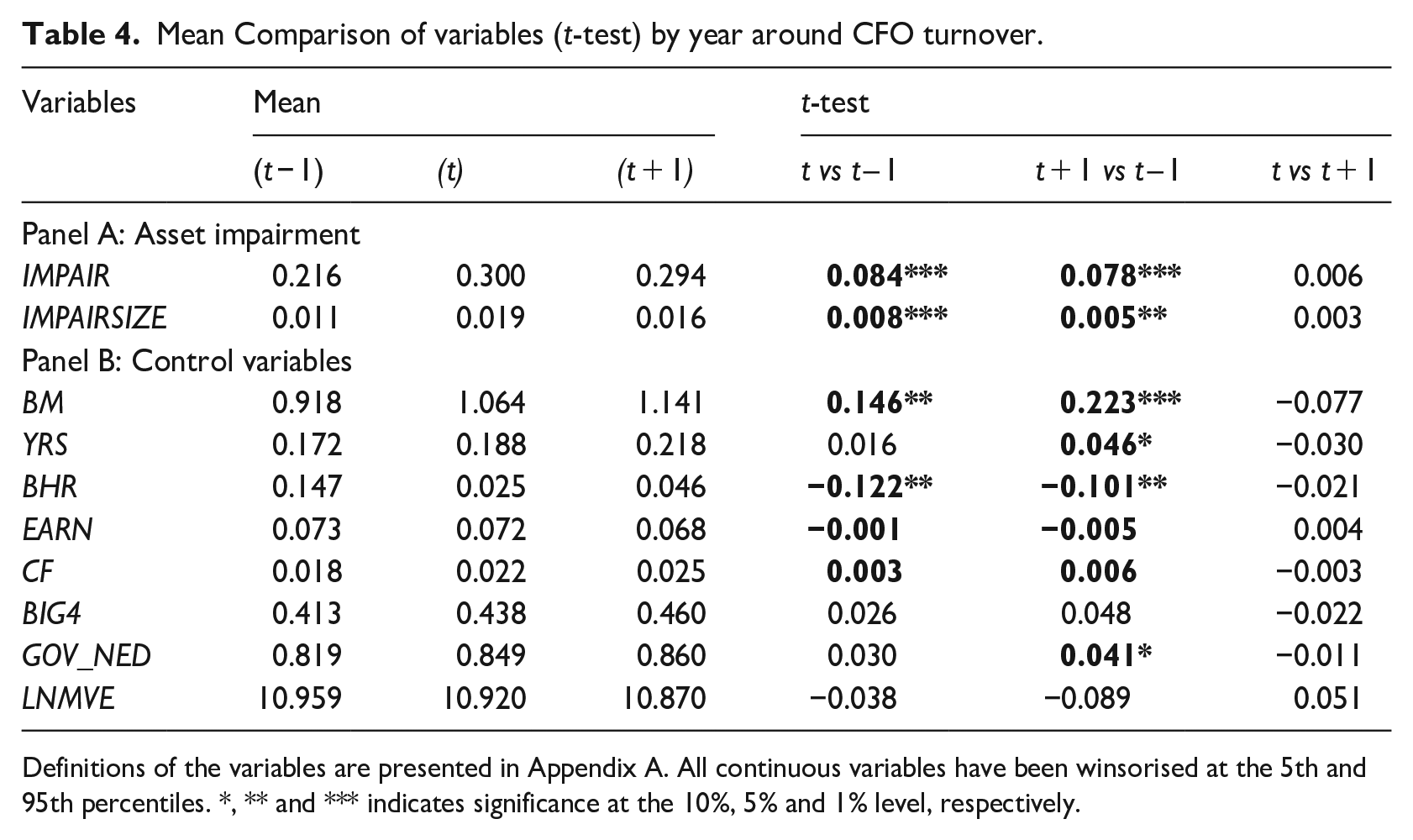

Table 4 presents a comparison of means for the years t – 1, t and t + 1 surrounding CFO turnover. A greater percentage of firms recognise asset impairments in year t (30%) and t + 1 (29.4%) compared to t − 1 (21.6%). Larger asset impairments are also recognised in year t (1.9% of total prior year assets) and t + 1 (1.6% of total prior year assets) versus t – 1 (1.1% of total prior year assets). The differences are statistically significant at the 1% level.

Mean Comparison of variables (t-test) by year around CFO turnover.

Definitions of the variables are presented in Appendix A. All continuous variables have been winsorised at the 5th and 95th percentiles. *, ** and *** indicates significance at the 10%, 5% and 1% level, respectively.

Table 4 indicates that indicators of impairment may be present in year t and t + 1 which exhibit significantly lower/(higher) BHR/(BM) than t – 1. There is also evidence that a BM > 1 or BM < 0 has persisted for two consecutive prior financial reporting periods (YRS) for a larger percentage of firms in year t + 1 (21.8%) compared to t – 1 (17.2%). A higher GOV_NED in year t + 1 (86.0%) versus t – 1 (81.9%) suggests that CFO appointments are accompanied by changes in board composition. Overall, the absence of statistically significant differences across most of the control variables indicates that, year to year, firm characteristics are relatively similar.

5.2. Likelihood and Size of Non-Current Asset Impairments around CFO Turnover

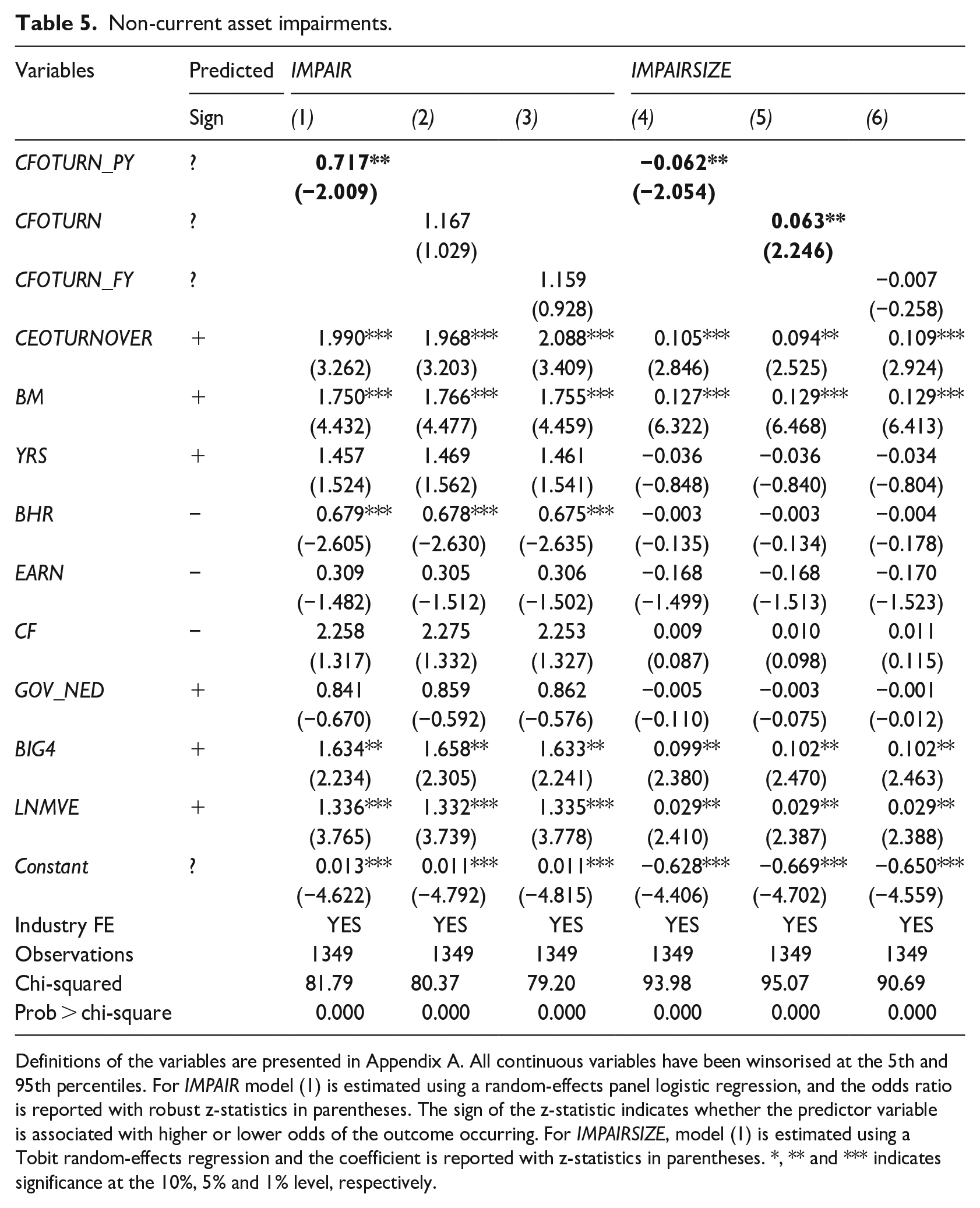

Table 5 presents the results of estimating regression model (1) for the full sample of CFO turnover events.

Non-current asset impairments.

Definitions of the variables are presented in Appendix A. All continuous variables have been winsorised at the 5th and 95th percentiles. For IMPAIR model (1) is estimated using a random-effects panel logistic regression, and the odds ratio is reported with robust z-statistics in parentheses. The sign of the z-statistic indicates whether the predictor variable is associated with higher or lower odds of the outcome occurring. For IMPAIRSIZE, model (1) is estimated using a Tobit random-effects regression and the coefficient is reported with z-statistics in parentheses. *, ** and *** indicates significance at the 10%, 5% and 1% level, respectively.

Columns (1) to (3) present results for the likelihood of non-current asset impairments and columns (4) to (6) present results for the size of asset impairment. Given that IMPAIR is a binary variable, a random-effects panel logistic regression is used, and odds ratios are reported along with robust z-statistics in parentheses. The sign of the z-statistic indicates whether the predictor variable is associated with higher or lower odds of the outcome occurring. 12 For IMPAIRSIZE, a Tobit random-effects model is used. 13

The results in column (1) indicate that firms are 28.3% less likely to recognise asset impairments in the year prior to a CFO change (CFOTURN_PY) (odds ratio = 0.717, p < 0.05). Meanwhile column (4) reports that the value of asset impairments recognised in this period are also lower (β = −0.062, p < 0.05). While there is no evidence that the recognition of asset impairments is more probable in the year of or following a new CFO appointment compared to other years surrounding CFO turnover, column (5) reports that the size of asset write-downs increases by 6.3% of total assets in the year of a new CFO appointment (CFOTURN) (β = 0.063, p < 0.05). Overall, the findings are consistent with Hypothesis 1(a) and provide partial support for hypothesis H1(b).

Turning to the control variables, CEO turnover is also associated with a higher likelihood and size of asset impairment consistent with prior literature (e.g. Moore, 1973; Murphy and Zimmerman, 1993; Pourciau, 1993; Strong and Meyer, 1987; Wells, 2002). As expected, a significant positive association is found between BM and the likelihood (IMPAIR) and size (IMPAIRSIZE) of asset impairments, while BHR significantly reduces the likelihood of asset impairments but not the size. Larger firms (LNMVE) and those audited by one of the Big 4 accounting firms (BIG4) are also more likely to recognise (and record higher) asset impairments. In addition, a significant negative association is observed between firm profitability and asset impairment size.

In assessing the results in Table 5, it is important to consider whether CFOs’ accounting choices are justifiable by indicators of financial impairment. In separate analysis (not tabulated), the CFO turnover variable is interacted with each of the variables capturing indicators of impairment. Consistent with ‘big bath’ theory, there is no evidence that the likelihood or size of asset impairments in the years surrounding CFO turnover are in response to indicators of impairment. Instead, the only significant results are that in year t + 1, the likelihood and size of asset impairments decreases in the presence of a BM > 1 or BM < 0 that has persisted for two consecutive years, but increases with higher earnings. 14

5.3. Characteristics of CFO turnover

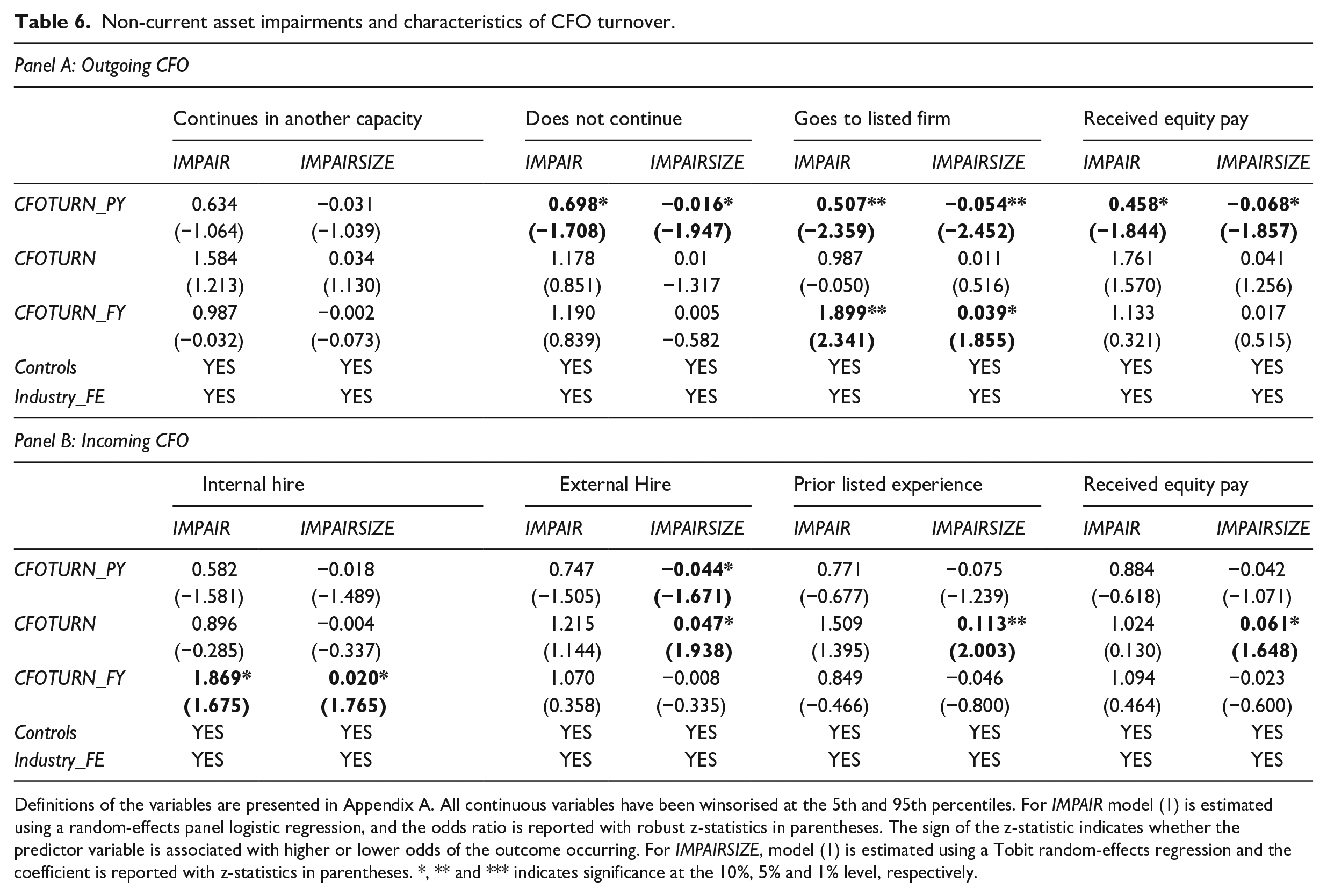

We next examine whether characteristics of CFO turnover impact on the impairment decision. To do so, we estimate model (1) on subsamples of firms depending upon the characteristic of the outgoing or incoming CFO. The results are summarised in Table 6.

Non-current asset impairments and characteristics of CFO turnover.

Definitions of the variables are presented in Appendix A. All continuous variables have been winsorised at the 5th and 95th percentiles. For IMPAIR model (1) is estimated using a random-effects panel logistic regression, and the odds ratio is reported with robust z-statistics in parentheses. The sign of the z-statistic indicates whether the predictor variable is associated with higher or lower odds of the outcome occurring. For IMPAIRSIZE, model (1) is estimated using a Tobit random-effects regression and the coefficient is reported with z-statistics in parentheses. *, ** and *** indicates significance at the 10%, 5% and 1% level, respectively.

We include all control variables and fixed effects as previously discussed and displayed in Table 5 but report only the coefficients, odds ratios and z-stats of the main test variables for brevity. Panel A displays the results for subsamples based on characteristics surrounding the outgoing CFO. In cases where the CFO does not continue with the firm in some capacity, moves on to another listed firm or received equity pay, the likelihood and size of non-current asset impairments are all negative and significantly associated with the year prior to CFO turnover (CFOTURN_PY). Intuitively, this makes sense since departing CFOs have reputational and compensation incentives to maximise performance prior to departure, consistent with Hypothesis 1(a). These results are also consistent with those reported in Table 5. All other years remain insignificant in relation to outgoing CFOs apart from when the CFO goes to another listed firm. In this instance, the likelihood (odds ratio 1.899) and size (β = 0.039) of non-current asset impairments are higher in the year following a new CFO appointment (CFOTURN_FY). 15

Panel B displays results for characteristics surrounding the incoming CFO. In contrast to panel A, there are no significant associations for the year prior to turnover (CFOTURN_PY) except when the incoming CFO is an external hire, in which case the size of impairment is smaller (β = −0.044, p < 0.10). These results suggest that the impairment decision in the year prior to CFO turnover is influenced by the incumbent CFO at the time and not the incoming CFO. In contrast, when the CFO is an internal replacement, there is a greater likelihood (odds ratio 1.869) and size (β = 0.020) of impairment in the year following but not the year of CFO turnover (CFOTURN_FY). This finding is consistent with internal successors requiring time to establish authority over financial reporting. Another possible explanation is internal CFOs not wanting to blame write-offs on a predecessor who was likely a mentor. When the incoming CFO is an external replacement, has prior listed experience or receives equity-based compensation, the size of non-current asset impairments is higher in the year of appointment. These results are consistent with hypothesis 1(b) and the results in Table 5.

5.4. Additional testing and robustness

5.4.1. Classifying turnovers into routine versus non-routine

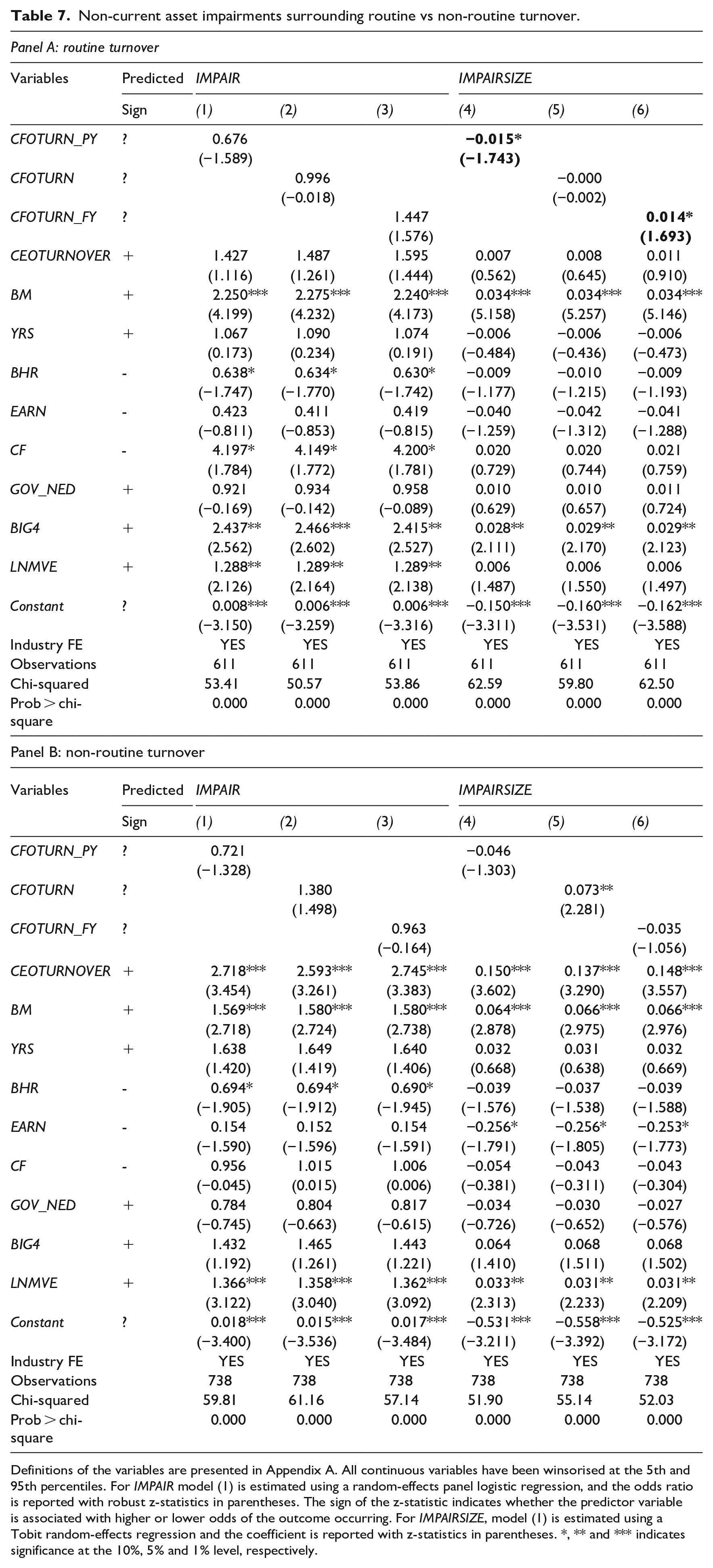

As additional analyses, we consider all factors surrounding CFO turnover to distinguish routine versus non-routine CFO changes. Prior literature has generally classified CFO turnover as routine if the outgoing CFO has continuing involvement with the firm (i.e. in another executive position or as a member of the board of directors) or an internal replacement is hired (Geiger and North, 2006; Wells, 2002). Therefore, we begin by classifying CFO turnover as ‘routine’ if the above two criteria are met. Second, we consider if the outgoing CFO is appointed to another listed firm since career progression and promotion is a positive signal of CFO quality (Haislip et al., 2015). Third, any CFO turnovers that do not meet the above criteria are classified as routine if there is an internal replacement and non-routine if there is an external replacement or the former CFO cannot be identified. Using this criteria, 206 (44%) of the 463 CFO turnover events are classified as routine. Table 7 reports the results of estimating model (1) on subsamples based on this classification.

Non-current asset impairments surrounding routine vs non-routine turnover.

Definitions of the variables are presented in Appendix A. All continuous variables have been winsorised at the 5th and 95th percentiles. For IMPAIR model (1) is estimated using a random-effects panel logistic regression, and the odds ratio is reported with robust z-statistics in parentheses. The sign of the z-statistic indicates whether the predictor variable is associated with higher or lower odds of the outcome occurring. For IMPAIRSIZE, model (1) is estimated using a Tobit random-effects regression and the coefficient is reported with z-statistics in parentheses. *, ** and *** indicates significance at the 10%, 5% and 1% level, respectively.

Panel A displays results for the routine subsample, and Panel B displays results for the non-routine subsample. The results for routine CFO appointments are largely consistent with those documented in Table 6 regarding internal CFO appointments, and if the outgoing CFO goes to another listed firm, both of which are reflected in the routine classification criteria. Specifically, the size of impairment is smaller in the year prior to turnover (column 4) and larger in the year following turnover (column 6). BM is positive and significant across all columns.

In regard to non-routine CFO turnover, Panel B shows that the size of asset impairments is larger in the year of appointment, reflecting the results documented in Panel B of Table 6. The controls for CEO turnover and BM are positive and significant across all columns. Overall, our results are consistent with our main findings using this holistic approach to classifying CFO turnover into routine versus non-routine. However, unlike CEO turnover, the paucity in disclosure regarding CFO turnovers means that this method of classifying turnovers into routine versus non-routine is particularly noisy. Therefore, we believe that investigating the characteristics of outgoing and incoming CFOs separately (as displayed in Table 6) provides greater insight into the reasons behind impairment decisions than subjectively classifying CFO turnovers into routine and non-routine.

5.4.2. Effect of concurrent appointments

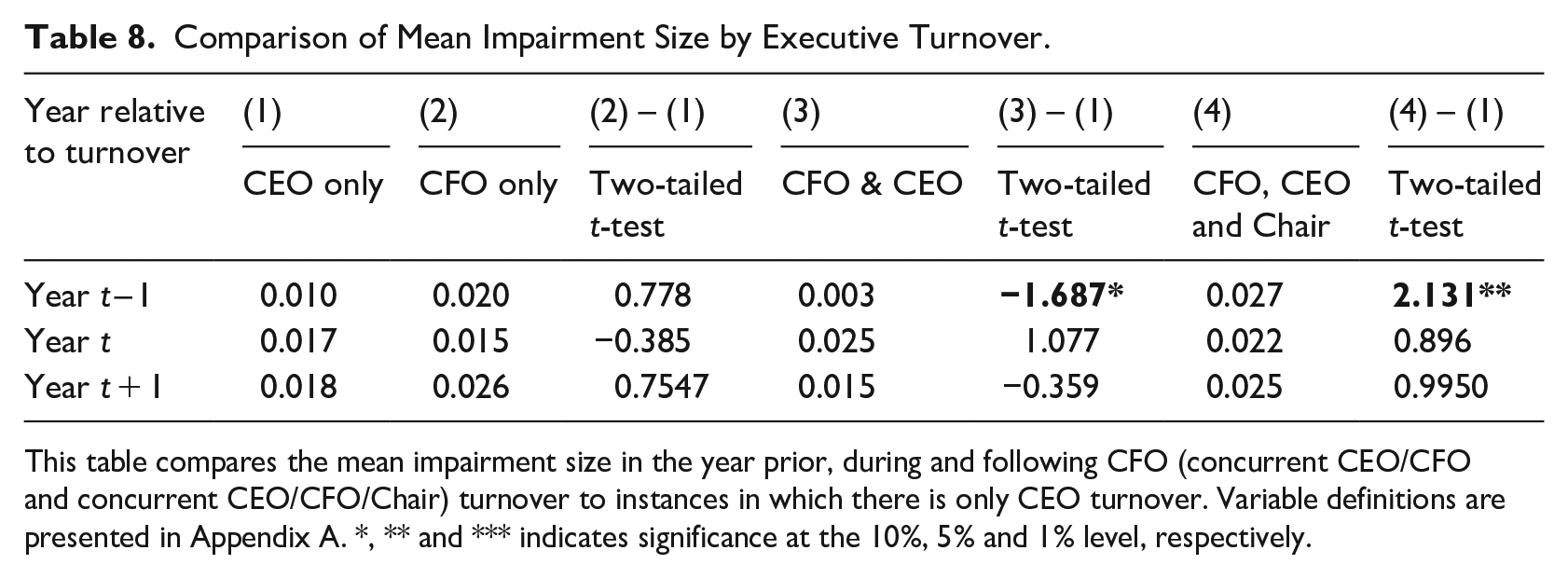

Prior research documents that CEO turnover is often accompanied by a ‘big-bath’ in the year of appointment (Wells, 2002). As a result, in our main findings, we control for CEO turnover that occurs prior to, during or following the CFO turnover. To provide additional insight, we compare the size of impairments surrounding CFO, concurrent CFO/CEO and concurrent CFO/CEO/Chair turnover to years in which only the CEO changes. The results are displayed in Table 8.

Comparison of Mean Impairment Size by Executive Turnover.

This table compares the mean impairment size in the year prior, during and following CFO (concurrent CEO/CFO and concurrent CEO/CFO/Chair) turnover to instances in which there is only CEO turnover. Variable definitions are presented in Appendix A. *, ** and *** indicates significance at the 10%, 5% and 1% level, respectively.

The average size of impairment is not statistically different between subsamples of CEO turnover and CFO turnover, implying that CFOs have just as much influence over the size of impairment as CEOs. When examining concurrent CFO and CEO turnover, the mean size of impairment is smaller in year t – 1, which could be driven by motives to maximise performance prior to departure. Conversely, the mean size of impairment is larger in the year prior to concurrent CFO, CEO and Chair turnover (column 4). Firms generally restructure the senior leadership team following poor firm performance (Mian, 2001) or events which signal financial reporting failures (Arthaud-Day et al., 2006; Collins et al., 2009; Leone and Liu, 2010), larger impairments in year t – 1 are likely to reflect such circumstances. All other years are not statistically different from years surrounding CEO turnover. As an extra additional test, we eliminate all CEO turnover years. The results (not tabulated show) show that both the likelihood and size of asset impairments in the year following a CFO appointment are greater, consistent with Geiger and North (2006) and with results for internal CFO replacements in Table 6. 16 Overall, results of these additional tests confirm that CFOs can exert independent and additional influence over financial reporting choices surrounding turnover, similar to that of CEOs.

5.4.3. Other impairment sensitivity tests

We undertake several other additional tests (not tabulated), to confirm our results. First, we partition the sample according to whether there is a change in CFO qualification (i.e. qualified accountant) arising from CFO turnover. 17 The results for the sample of firms in which there is no change in qualification show lower likelihood and size of impairment in the year prior to turnover, consistent with the results reported in Table 5. This is unsurprising given that there is little variation in qualification within our sample (as shown in Panel C of Table 3). When testing instances in which the outgoing CFO is not qualified and is replaced with a qualified CFO (n = 130), or vice versa (n = 83), we find no significant results and the regressions are largely insignificant due to the small sample sizes. When we combine all changes in CFO qualifications (n = 213) we also find no results. Therefore, qualification does not appear to impact on the impairment choice.

Second, we attempt to analyse the effect of CFO equity incentives on impairment decisions around CFO turnover by focusing on a sub-group of the sample where the incoming CFO’s pay package includes an equity reward mechanism that is not in place for the outgoing CFO (n = 102). The results show a significant decrease in the likelihood and size of impairments in year t – 1, and a significant increase in impairment likelihood in year t + 1. We also analyse the subsample in which the outgoing CFO’s pay package includes an equity reward mechanism that is not in place for the incoming CFO (n = 135). The results show a significant decrease in the likelihood and size of impairments in year t – 1, and a significant increase in impairment in likelihood and size in year t. 18 Overall, the results suggest that fewer (higher) asset impairments in year t – 1 (t and t + 1) occur regardless of whether the outgoing CFO has equity incentives. It is therefore reasonable that other concerns (e.g. career) in addition to equity reward mechanisms, serve as significant motivating factors in departing CFOs’ financial reporting decisions.

Third, we investigate if a change in external auditor in the year of CFO turnover is associated with the likelihood or size of impairments. The findings indicate that in firms with a concurrent CFO and auditor change (n = 293), there is an insignificant effect of CFO turnover on asset impairment likelihood and size. In contrast, the results for firms without an auditor change are consistent with those for the full sample reported in Table 5. These results suggest that a new auditor may mitigate earnings management in the year of a CFO appointment. 19

5.4.4. CFO turnover and impairments relative to all firm-years

This study examines whether there is a change in the likelihood and size of non-current asset impairments surrounding CFO turnover; hence, the sample is constructed from new CFO appointments. An investigation of the effect of CFO turnover on asset write-offs more broadly requires non-current asset impairment data for all ASX listed entities. This examination is problematic because non-current asset impairments are not electronically available and need to be hand collected from annual reports. Moreover, due to the frequency of CFO turnover, it is difficult to isolate firm-years, which are impervious to CFO turnover events occurring within neither the year prior to (t – 1) nor immediately after (t + 1) a CFO change.

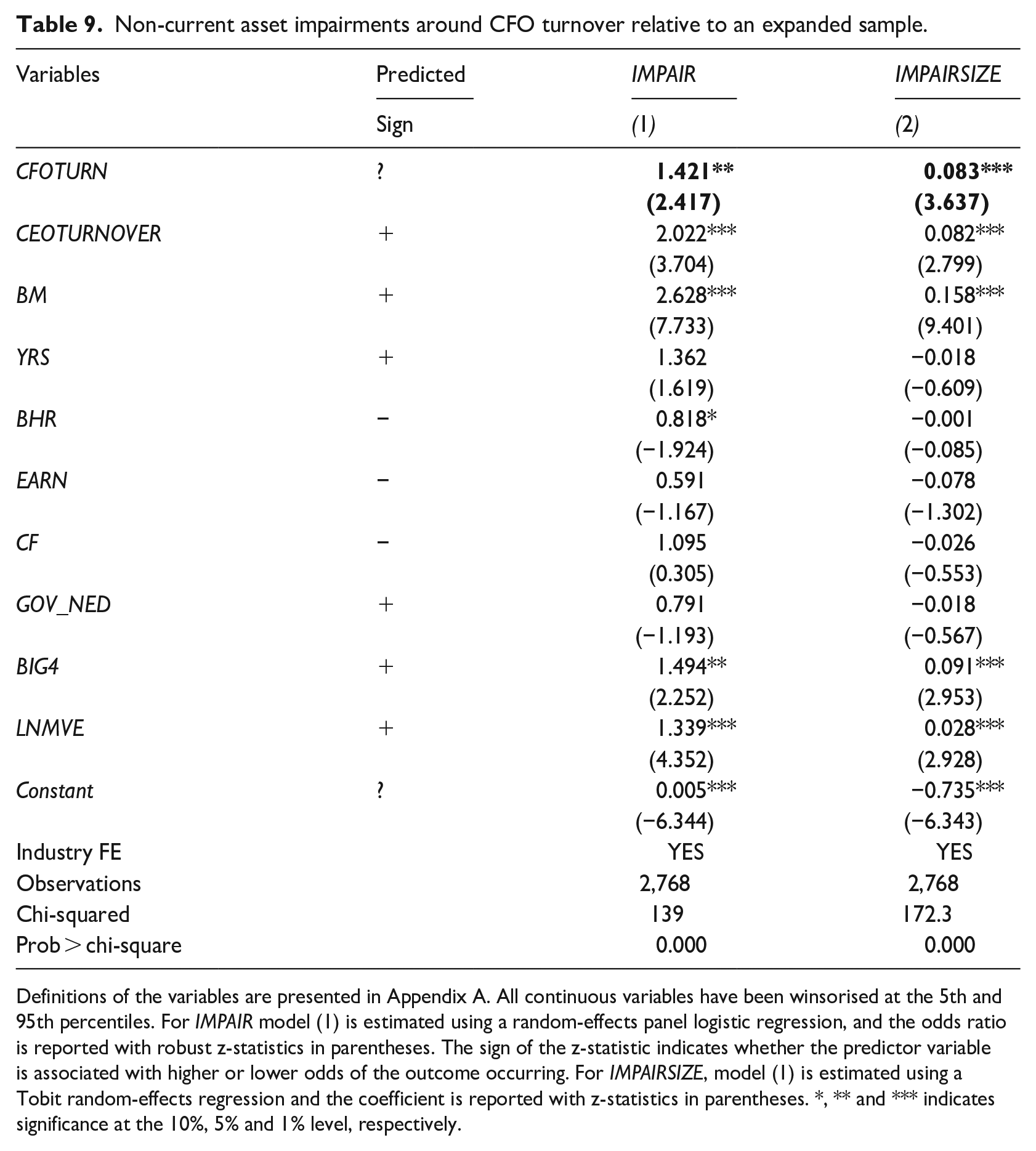

Within the bounds of these limitations, we perform additional analyses by combining the test sample with 1379 firm-year observations for Top 500 ASX listed entities for the period 2007 to 2015. 20 Model (1) is then estimated for this expanded sample with the results presented in Table 9.

Non-current asset impairments around CFO turnover relative to an expanded sample.

Definitions of the variables are presented in Appendix A. All continuous variables have been winsorised at the 5th and 95th percentiles. For IMPAIR model (1) is estimated using a random-effects panel logistic regression, and the odds ratio is reported with robust z-statistics in parentheses. The sign of the z-statistic indicates whether the predictor variable is associated with higher or lower odds of the outcome occurring. For IMPAIRSIZE, model (1) is estimated using a Tobit random-effects regression and the coefficient is reported with z-statistics in parentheses. *, ** and *** indicates significance at the 10%, 5% and 1% level, respectively.

The evidence reported in Table 9 indicates that a new CFO appointment is significantly positively associated with the likelihood (odds ratio = 1.421, p < 0.05) and size (β = 0.083, p < 0.01) of non-current asset impairments. Asset impairments are also more likely and increase around CEO turnover (CEOTURNOVER). The results for BM are significant and in line with predictions; however, the two other external indicators of impairment (BHR and YRS) are insignificant, apart from BHR which is positive and significantly related to the likelihood of impairment. As expected, BIG4 and LNMVE are also positive and significantly related with asset impairment likelihood and size. Due to the concern that the merged sample may include firm-years before (t – 1) or after (t + 1) a CFO change, only CFO (i.e. year t) is included as the key test variable in the model. In additional analyses (not tabulated), we include CFOTURN_PY, CFOTURN and CFOTURN_FY in the model simultaneously and document positive and significant relations between CFOTURN and CFOTURN_FY and IMPAIR and IMPAIRSIZE.

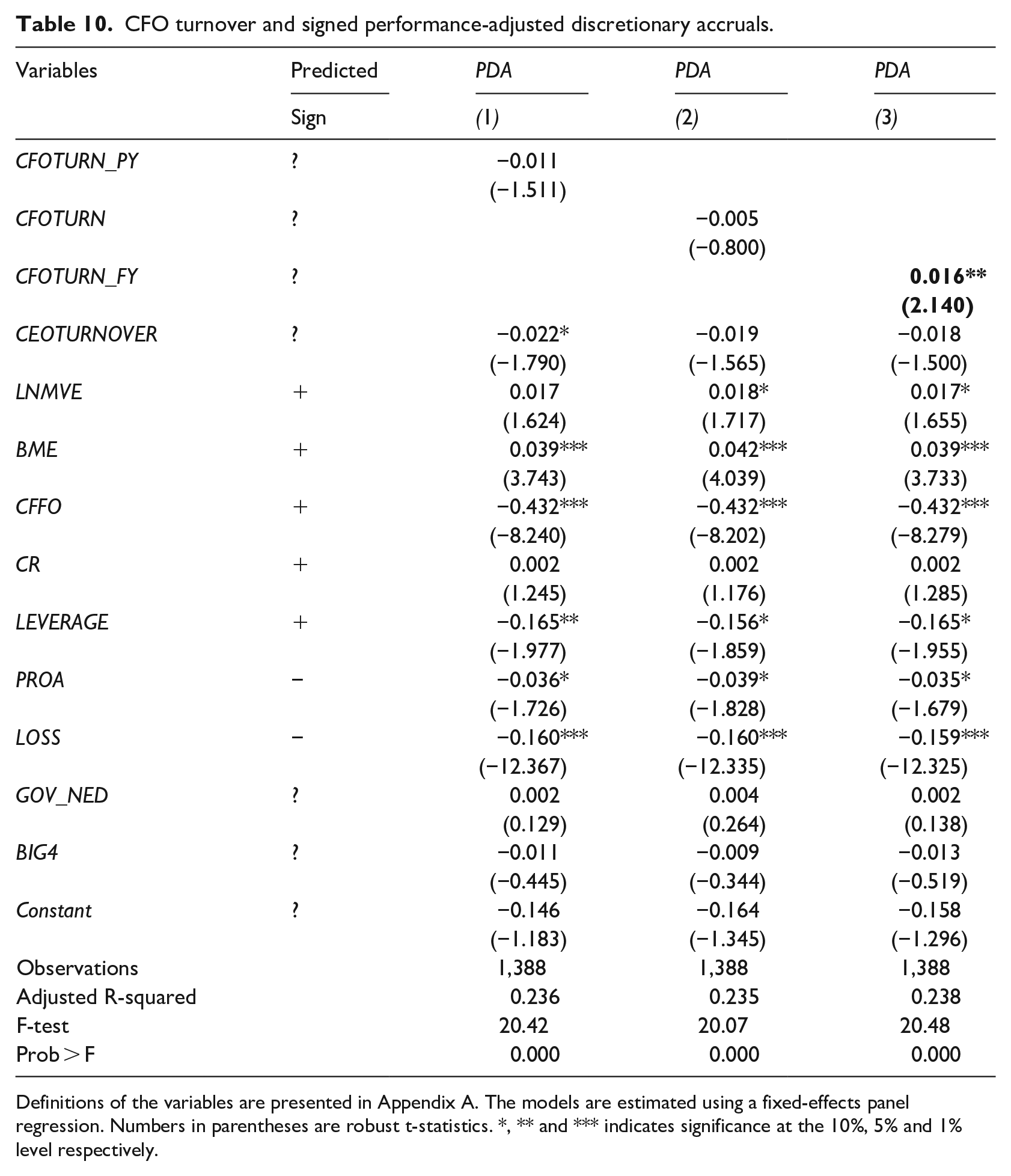

5.4.5. CFO turnover and discretionary accruals

Given the absence of a single comprehensive proxy for accounting quality, the hypotheses are also tested by examining the effect of CFO turnover on signed performance-adjusted discretionary accruals (PDA). Financial data for all ASX-listed companies between 2007 and 2016 are retrieved from the Morningstar DatAnalysis Premium database. These data are used to estimate the cross-sectional, performance-matched, modified Jones (1991) model (DeFond and Jiambalvo, 1994; Kothari et al., 2005). 21 Expected accruals are estimated cross-sectionally for this sample of firm-years based on year groupings using the following model:

where TA (total accruals) is defined as net profit (loss) after tax before special items less cash flow from operations for firm i in period t.

The estimated coefficients from the yearly regressions of model (2) are used to calculate the value of expected accruals for sample firms. Discretionary accruals (DA) are defined as the difference between total accruals and expected accruals. The firm’s estimated discretionary accruals (DA

The following equation is estimated to examine the association between CFO turnover and PDA. The model includes controls for factors found to relate to discretionary accruals in prior research:

Table 10 presents the results from estimating regression model (3).

CFO turnover and signed performance-adjusted discretionary accruals.

Definitions of the variables are presented in Appendix A. The models are estimated using a fixed-effects panel regression. Numbers in parentheses are robust t-statistics. *, ** and *** indicates significance at the 10%, 5% and 1% level respectively.

The results provide evidence of greater income increasing discretionary accruals in year t + 1 after CFO turnover. To ensure discretionary accruals are not substituting for impairments, we also run our tests after including PDA as a control variable in our original models. The results (not tabulated) show that PDA reduces the likelihood of impairment across all subsamples, while the coefficients on CFOTURN_PY CFOTURN and CFOTURN_FY are consistent with our main results across all subsamples. 23

6. Conclusion

Based on a sample of 463 Australian CFO changes between 1 July 2007 to 30 June 2015 (i.e. 1389 firm-years), this study examines the effect of CFO turnover on the likelihood and size of non-current asset impairments. The evidence indicates that incoming CFOs often initiate large asset write-offs in the initial or subsequent period of their appointment. The effect is largest for external hires with prior listed experience, and those receiving equity-based compensation. Therefore, the financial reporting motives maintained by CFOs surrounding a turnover event are similar to those of CEOs.

For outgoing CFOs, the results indicate that they are less likely to recognise (and record smaller) asset write-offs in the year prior to their departure. These findings are consistent with outgoing CFOs acting in self-interest, suggesting that CFOs are motivated to manage earnings upwards to maximise their final pay (e.g. Geiger and North, 2006) or enhance their reputation before joining another firm. Prior research indicates that the value of CFOs’ human capital in a competitive managerial market is influenced by the performance of the CFO’s firm (Brickley et al., 1999; Fama, 1980; Mian, 2001). Our results support this view, suggesting that CFOs’ motives to pursue post-retirement and other executive progression career prospects may also serve as an incentive to manipulate income prior to their departure.

The results in this study indicate that CFOs’ incentives to manipulate earnings through asset write-offs exist irrespective of concurrent CEO turnover. This evidence demonstrates that CFOs independently influence the timing and magnitude of asset write-offs to bias earnings surrounding a turnover event. As the impairment of non-current assets continues to be a focus area of ASIC’s inquiries, these results suggest that heightened scrutiny should be directed at firms appointing a new CFO. The findings are also relevant to the impairment literature, indicating that CFO turnover should be considered a key determinant of non-current asset impairments in addition to CEO turnover.

Key practical and research implications

• Outgoing CFOs are less likely to record asset impairments prior to their departure if they obtain employment with another listed firm or received equity incentives, highlighting the role of career concerns and compensation incentives in asset impairment decisions.

• Incoming CFOs often initiate larger asset impairments in the year of their appointment, particularly when they are an external hire with prior listed experience or receive equity incentives. These results are similar to those in the ‘big bath’ literature.

• Firm stakeholders, including investors and analysts, need to be aware of the potential for opportunistic behaviour by CFOs during transitions. Understanding that CFOs may engage in earnings management through asset impairments, either to maximise final pay or to attribute poor results to predecessors, can lead to more informed investment decisions.

• Auditors and audit committees should allocate additional resources and attention to firms experiencing CFO changes, and regulatory bodies like ASIC should increase surveillance of firms experiencing CFO turnover to help protect the interests of shareholders.

• Both CFO and CEO turnover independently drive asset impairments; therefore, researchers examining non-current asset impairments should incorporate CFO and CEO turnover as control variables.

Footnotes

Appendix

Definition of variables.

| Variables | Definition | ||

|---|---|---|---|

| Panel A: key test variables | |||

| CFOTURN | A binary variable coded as one in the financial year of a new CFO appointment (i.e. t), zero otherwise | ||

| CFOTURN_PY | A binary variable coded as one in the financial year prior to a new CFO appointment (i.e. t – 1), zero otherwise | ||

| CFOTURN_FY | A binary variable coded as one in the financial year following a new CFO appointment (i.e. t + 1), zero otherwise | ||

| Panel B: incoming and outgoing CFO variables | |||

| I_CFO_EXTERNAL | A binary variable coded as one if the incoming CFO was appointed externally, zero otherwise. | ||

| I_CFO_PRIOR_LISTED | A binary variable coded as one if the incoming CFO has prior experience at a listed firm, zero otherwise. | ||

| I_CFO_QUALIFIED | A binary variable coded as one if the incoming CFO holds a professional accounting certification (e.g., CA, CPA, CIMA, IPA or ACCA), zero otherwise. | ||

| I_CFO_EQUITY | A binary variable coded as one if the incoming CFO receives equity-based pay, zero otherwise. | ||

| O_CFO_CONTINUE | A binary variable coded as one if the outgoing CFO continues at the firm in another capacity (e.g., as an independent director), zero otherwise. | ||

| O_CFO_NEW_LISTED | A binary variable coded as one if the outgoing CFO moves to another listed firm, zero otherwise. | ||

| O_CFO_QUALIFIED | A binary variable coded as one if the outgoing CFO holds a professional accounting certification (e.g., CA, CPA, CIMA, IPA or ACCA), zero otherwise. | ||

| O_CFO_EQUITY | A binary variable coded as one if the outgoing CFO received equity-based pay, zero otherwise. | ||

| Panel C: asset impairment variables | |||

| IMPAIR | A binary variable coded as one if a non-current asset impairment is recognised, zero otherwise. | ||

| IMPAIRSIZE | The total non-current asset impairment loss (excluding any impairment reversals) recognised by the firm in the current financial year (t) scaled by t – 1 total assets. | ||

| Panel D: control variables | |||

| BM | The ratio of the total book value of equity (adjusted for the recognition of asset impairments) to market capitalisation. | ||

| YRS | A binary variable coded as one if BM > 1 or BM < 0 for two reporting periods prior to the current financial year end (i.e. t – 1 and t − 2), zero otherwise. | ||

| BHR | The buy-hold return for the firm’s stock over the financial year, calculated as: (P₁–P₀) + Dividends / P₀ | ||

| EARN | Net profit after tax per share, adjusted for impairment charges. | ||

| CF | Aggregate cash flow from operating and investing per share. | ||

| BIG4 | A binary variable coded as one if the company is audited by a Big 4 accounting firm, zero otherwise. | ||

| GOV_NED | A binary variable coded as one if the majority of board members are independent non-executive directors, zero otherwise. | ||

| LNMVE | The natural logarithm of the market capitalisation. | ||

| CEOTURNOVER | A binary variable coded one if a CEO appointment took place, zero otherwise. | ||

| Panel E: discretionary accruals test | |||

| PDA | Signed performance-adjusted discretionary accruals estimated from the modified cross-sectional modified Jones (1991) model. | ||

| BME | The ratio of the total book value of equity to market capitalisation. | ||

| CFFO | Cash flow from operations divided by total assets. | ||

| CR | The ratio of current assets to current liabilities. | ||

| LEVERAGE | The ratio of book value of debt to book value of assets. | ||

| LOSS | A binary variable coded as one if the company reported a net loss after tax, zero otherwise. | ||

| PROA | Return on assets (defined as net profit after tax divided by total assets) for the prior period. | ||

Acknowledgements

The authors wish to acknowledge the comments received from Peter Clarkson, Andrew Jackson and Stephen Taylor and seminar participants at the University of Technology Sydney, University of Queensland and Curtin University of Technology. They also thank the two anonymous reviewers for their valuable comments and suggestions.

Final transcript accepted 18 July 2024 by Andrew Jackson (Editor-in-Chief ).

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data availability

The data that support the findings of this study are available from Connect4, SIRCA and Morningstar DatAnalysis Premium databases. Restrictions apply to the availability of these data, which were used under licence for this study. Data regarding classification of CFO turnovers as routine and non-routine are available from the authors upon request.