Abstract

Residential aged care providers rely on refundable accommodation deposits (RADs) to finance capital expenditure, but changing consumer accommodation payment preferences may reduce their access. Our study evaluated the potential impact of a significant reduction in provider RAD balances. We surveyed 300 providers across Australia in 2020 and conducted focus groups and interviews with stakeholder executives, to develop key themes using an inductive constant comparative method couched within grounded theory. We found preferences for RADs vary across providers, with those seeking to undertake capital expenditure mostly preferring RADs. Stakeholder views suggested RADs facilitate low cost capital investment for some providers and allow banks to offer more debt to more providers. However, stakeholders suggested RADs may also create a more volatile financial structure and impose barriers to entry for equity. Stakeholders suggested a significant and sustained reduction in RADs would negatively impact capital expenditure and increase provider financial risk. Our study proposes that government intervention to stop a significant reduction in provider RAD balances should only occur if access to care is threatened. Intervention options could include enforcing liquidity and capital adequacy requirements, increasing investor returns to attract more equity and facilitate more commercial debt and establishing a government backed accommodation capital facility.

1. Introduction

The number of Australians aged 65 years and older is projected to double to 8.9 million by 2060–2061, with 5% aged 85 years and over (The Treasury, 2021). With the population ageing, increased prevalence of chronic disease and reduced supply of informal care, the demand from older Australians for aged care services is expected to increase. This is already reflected by the recent increase in home care packages and residential aged care places funded by the Australian Government.

Building residential accommodation requires sustainable capital financing. In many European countries, aged care providers mostly rely on government grants to fund capital expenditure. In the United States and the United Kingdom, governments and residents pay accommodation fees that generate provider revenue, which is used to support capital expenditure financed by equity and commercial debt. Real Estate Investment Trusts (REITs) have become a large source of capital expenditure finance in both these countries (Harrington et al., 2011; Omokhomion et al., 2018).

Australia has a unique capital financing system for residential aged care accommodation. While residents with low means have their accommodation paid for by the Australian Government, other residents must contribute towards their accommodation costs. Aged care residents can make a lump sum payment to providers known as a refundable accommodation deposit (RAD), which is refunded to the resident or estate upon leaving the facility. Residents can also pay a rental style payment known as a daily accommodation payment (DAP) or any combination of a RAD and DAP.

RADs are ubiquitous throughout the Australian residential aged care sector. The total value of RADs held by providers was AUD$33.6 billion as of 30 June 2021 (Department of Health and Aged Care, 2022), with RAD balance increases positively correlated with a US$10.5 billion capital expenditure increase since 2013–2014. Shifts in consumer preferences from RADs to DAPs have concerned the sector. The proportion of new residents that paid an RAD fell from 43% in 2014–2015 to 35% in 2018–2019 (Aged Care Financing Authority (ACFA), 2020). Providers suggest they may become insolvent because of their reduced ability to replace an outgoing RAD with an incoming RAD. These financial viability concerns are exacerbated by reduced average occupancy rates, from 93.1% in 2011 to 86.8% in 2021 (Productivity Commission, 2022), and a substantial reduction in average earnings before interest, tax and depreciation per resident per annum between 2016–2017 and 2020–2021 (Department of Health and Aged Care, 2022).

Our study systematically analysed stakeholder views on the importance of RADs to the residential aged care sector and the potential risks from a significant reduction in RAD balances. We sought the perspectives of providers, lenders, valuers and peak industry groups to answer whether a potential substantial reduction in RADs, due to a shift in consumer preferences towards DAPs, would significantly negatively impact residential aged care providers.

We conducted focus groups and interviews with provider chief executive officers (CEOs), managing directors and chief financial officers (CFOs), and conducted an online survey of 300 providers in 2020 to gather perspectives on the use of RADs, the potential impact of a significant reduction in RADs and alternative capital financing options. We used an inductive constant comparative method in grounded theory to analyse stakeholder responses and to develop key themes to understand the importance of RADs (Madsen et al., 2007).

Our article is derived from a broader study on the role of RADs in residential aged care (Cutler et al., 2021b) conducted on behalf of the (now defunct) Aged Care Financing Authority to inform the Commonwealth Minister for Health (Aged Care Financing Authority (ACFA), 2021a). ACFA recommended retaining RADs because they noted there was no obvious and immediate non-government finance for capital expenditure that could replace RADs. ACFA also noted the financial risks associated with RADs and recommended strengthening prudential regulations and financial performance monitoring.

Several government-initiated inquiries have explored specific components of RADs, including whether adjustments should be made to either the accommodation payment regulation (Productivity Commission, 2011), the Accommodation Payment Guarantee Scheme or the prudential regulation of RADs. The Royal Commission into Aged Care Quality and Safety recommended phasing out RADs for new residents, establishing an aged care accommodation capital facility, introducing liquidity and capital adequacy standards and improving financial reporting (Royal Commission into Aged Care Quality and Safety, 2021). In 2021, the Australian Government improved prudential and financial monitoring of residential aged care providers (Department of Health, 2021b).

To our knowledge, no previous literature has explored the role of RADs in residential aged care, despite their somewhat controversial introduction (Senate Community Affairs Reference Committee, 1997). RADs have created a substantial Australian Government financial risk through the Accommodation Payment Guarantee Scheme, which guarantees the Australian Government will repay an owing RAD to the consumer or the estate when the consumer leaves a facility if the provider cannot repay (Department of Health, 2022).

Our study investigates the important issue of a substantial reduction in RADs and its potential impact on residential aged care financial viability. We find that many providers believe a substantial reduction in RADs could negatively impact them financially and reduce capital expenditure within the sector. However, other providers noted they would benefit from a reduction in RADs due to an associated increase in DAP income, allowing them to spend more on care services and daily living expenses. We highlight the imperfect nature of RADs to finance capital expenditure and the need for the Australian Government to consider the benefits and costs of any intervention that seeks to reduce provider reliance on RADs.

2. Background

Residential aged care consumers with low means, as determined by an income and means assessment administered by Services Australia, have their accommodation costs paid for by the Australian Government. All other consumers must pay for their accommodation using an RAD, DAP or a combination of both. Maximum accommodation prices are set by the residential aged care provider but lower prices can be negotiated between the provider and consumer. Accommodation prices in the same residential aged care facility can also differ due to differences in room size and amenities.

Accommodation prices are published as an RAD and converted to a DAP using the maximum permissible interest rate (MPIR) set by the Australian Government every 3 months. The MPIR can be volatile as it is based on a base interest rate that reflects the monthly average yield of 90 day Bank Accepted Bills. A change in the MPIR impacts the DAP and therefore the choice between an RAD and DAP. A decrease in the MPIR will reduce the DAP, potentially making it more attractive to the consumer.

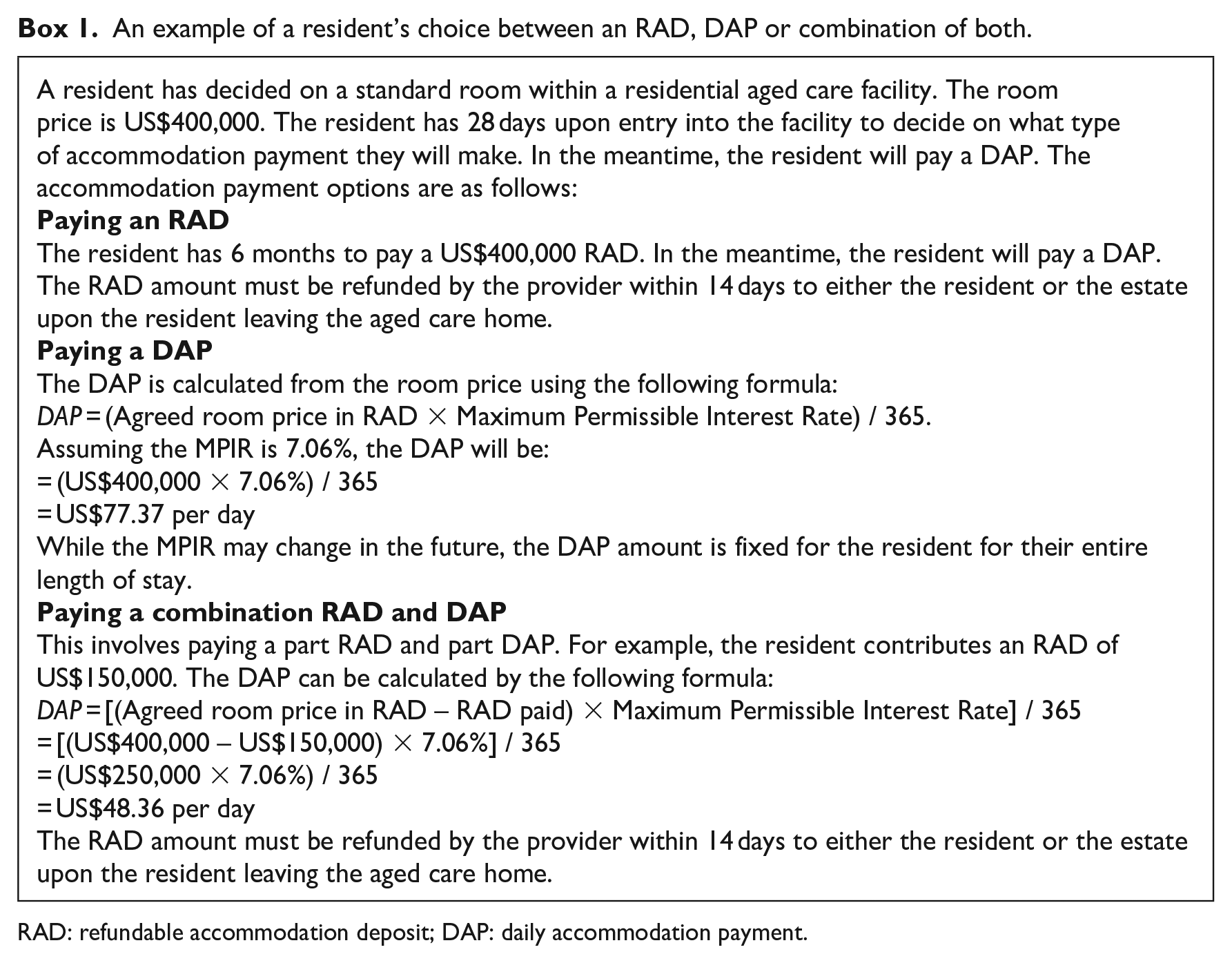

Box 1 shows an example of an accommodation payment choice faced by a consumer and highlights the potential financial risk to residential aged care providers associated with different resident payment choices. If a resident leaving a facility had paid a US$400,000 RAD upon entry, the provider must refund that RAD from some liquid asset, typically cash in the bank, within 14 days. The Accommodation Payment Guarantee Scheme means an RAD is a risk free investment to the resident with a return equivalent to the MPIR. If the new resident chooses to pay a DAP, the provider cannot immediately replace the US$400,000. This could reduce provider solvency if additional residents that paid an RAD also leave the facility and are replaced by residents that pay a DAP.

An example of a resident’s choice between an RAD, DAP or combination of both.

RAD: refundable accommodation deposit; DAP: daily accommodation payment.

Several factors also impact the probability of choosing an RAD, including the value of assets upon entry, expected length of stay, assessed level of care required, accommodation price, age of the consumer and whether the consumer is married (Cutler et al., 2021b). The value of assets upon entry has the greatest impact on choosing an RAD. This reflects the increased ability to pay an RAD with more assets, and also the financial incentive for residents to pay an RAD given its value is excluded from the Age Pension asset and income test.

Providers use RADs to mostly finance significant refurbishment, renovations and to build new residential aged care facilities. There is a strong positive correlation between total RAD balances and the annual value of private sector building jobs for aged care facilities. Capital expenditure is also financed through equity, commercial debt, donations, endowments and capital grants, although RADs comprised 59% of total assets and 71% of total liabilities as on 30 June 2021 (Department of Health and Aged Care, 2022).

Despite consumer preferences shifting towards DAPs, total provider RAD balances doubled between 2013–2014 and 2018–2019 (Aged Care Financing Authority (ACFA), 2020). This increase mostly came from allowing providers to charge all new residents an RAD after the Living Longer Living Better (LLLB) reforms were introduced. Prior to the LLLB reforms, providers could only charge residents receiving low care or residents receiving high care with extra services. Other factors that increased total RAD balances were an increase in accommodation prices and an increase in the total number of operational beds (Aged Care Financing Authority (ACFA), 2020).

Annual growth in the total value of RADs has since declined as growth in the number of RADs held by providers has plateaued (Department of Health and Aged Care, 2022). This occurred when some providers were already experiencing liquidity risk. Around US$9.6 billion worth of lump sum accommodation payments were held by providers on 30 June 2018 that were considered as having a high liquidity risk rating (between 5% and 8%) or very high liquidity risk rating (lower than 5%). Coupled with poor financial returns for residential aged care providers, there was a significant risk that providers holding a significant proportion of lump sum accommodation payments could default (StewartBrown, 2019).

A substantial increase in RADs is needed to ensure accommodation supply keeps up with demand and resident preferences. ACFA projected that approximately 80,000 new beds are required to meet demand over the next decade (Aged Care Financing Authority (ACFA), 2020). This includes refurbishing and rebuilding the current stock of aged care facilities for a combined required total investment of US$51 billion. Most of this capital expenditure will require an increase in RAD balances if the structure of aged care financing remains unchanged. The Australian Government also accepted a recommendation made by the Royal Commission into Aged Care Quality and Safety to develop and implement a set of National Aged Care Design Principles and Guidelines on accessible and dementia-friendly design (Department of Health, 2021a). This will require some providers to substantially renovate their facilities to meet these guidelines.

3. Data and methods

Our study employed grounded theory to explore the residential aged care sector’s understanding of the advantages and risks associated with RADs. Qualitative methods are popular in health services research because they provide rich descriptions of complex phenomena and illuminate the experience and interpretation of events by stakeholders with widely different stakes and roles. Grounded theory is used to develop a theory grounded in the behaviour, words and actions of those being studied. It involves an iterative process, interrelated planning, data collection, data analysis and theory development (Vollstedt and Rezat, 2019).

Grounded theory was first developed by Glaser and Strauss (1967), and has evolved into different variations to the original ‘Classic Grounded Theory’: Strauss and Corbin’s Basics of Qualitative Research, Charmaz’s Constructivist Grounded Theory and Clarke’s postmodern Situational Analysis. We followed the general principles of grounded theory with a modified practical approach in carrying out the analysis.

Purposive sampling was used to start the sampling process, where we identified stakeholders with substantial experience and knowledge about aged care financing. We recruited providers, lenders, valuers and peak body representatives for providers and consumers. These stakeholders held senior management positions in their organisations, with extensive experience operating residential aged care homes, lending to / valuing of residential aged care providers, or interacting with residents who make decisions relating to accommodation payments.

Stakeholder interviews were 60 minutes and started with semi-structured and open-ended interview questions tailored to the type of stakeholders being interviewed. Questions were designed to encourage discussion with the senior researcher leading the interviews, the latter probing the stakeholders to ensure their thoughts and perspectives were fully understood (see Appendix 1 for the interview questions). We interviewed six lenders, three peak providers representatives, two peak consumer representatives and three valuers. We sought to achieve heterogeneity in sample perspectives rather than representativeness to increase the broadness of concepts and scope of theory (Corbin and Strauss, 2008).

We also recruited 25 senior executives from 23 providers based on the size of their RAD balances, number of occupational beds and ownership type (profit, not for profit and government) to participate in five focus groups lasting 90 minutes each. Of the participating senior executives, 56% were either a CEO or managing director, 24% were CFOs, 16% were senior managers and one was an owner and non-executive director. Providers were a mix of mid-to-large sized for-profit and not-for-profit organisations. Focus group sessions were facilitated by a senior researcher with semi-structured and open-ended questions to allow interactions and free flowing discussions among the participants (see Appendix 2 for the focus group questions). Each session was kept to a maximum of six provider participants to promote equal contribution. Interviews and focus groups were conducted via Zoom in September and October 2020.

We followed the idea of theoretical sampling in grounded theory to supplement the interview and focus group data with an online survey of approved residential aged care providers between 26 October 2020 and 13 November 2020. The survey questionnaire was developed around the research questions and refined from the information collected within the focus groups (see Appendix 3 for the online survey questions). It was designed to extend information and corroborate perspectives collected from the interviews and focus groups. Providers were recruited through advertising by the Department of Health, which sent out online survey invites to all 845 approved residential aged care providers in Australia.

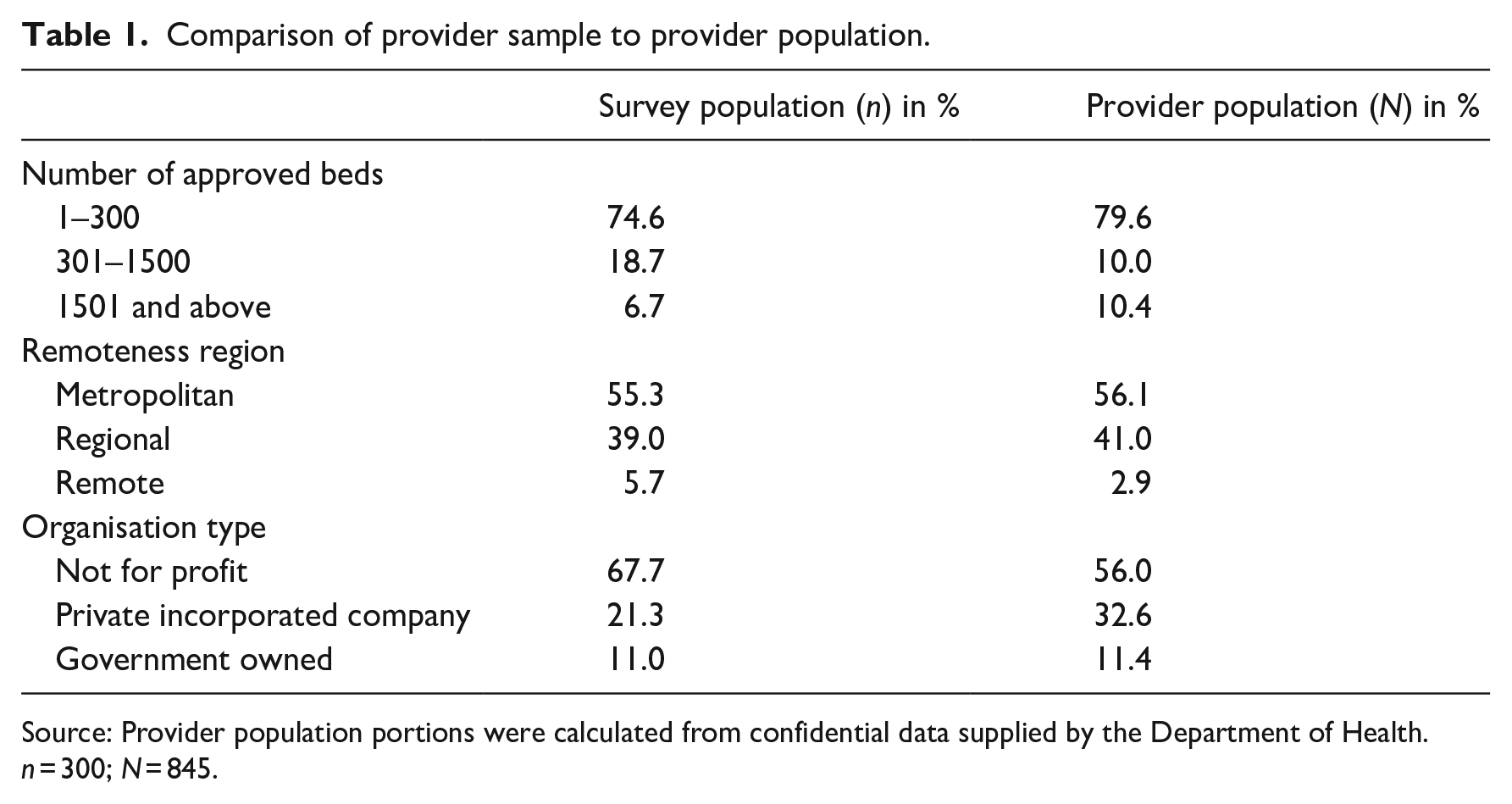

A review of survey responses was undertaken to identify incomplete questionnaire responses and illogical relationships between question responses. These questionnaire responses were discarded from the analysis of survey results. Responses were also checked for potential speeders, finding the minimum time to complete the questionnaire was 4.9 minutes, with the fastest 2.5% of the sample completing the survey in 8.1 minutes. These responses were kept, as dropping them did not significantly impact the mean results. A total of 300 completed survey questionnaires were included in the analysis, representing a 36% response rate. Respondents broadly reflected the sector’s composition, capturing providers of all size, ownership type and location of facilities across regional areas, states and territories (see Table 1).

Comparison of provider sample to provider population.

Source: Provider population portions were calculated from confidential data supplied by the Department of Health.

n = 300; N = 845.

We used inductive constant comparative method in grounded theory to analyse responses within the interviews, focus groups and online survey. Two researchers independently analysed and coded the interview and focus group transcripts using NVivo (v.12) to link the survey data with developing a theory. We first started with one interview/focus group discussion transcript, decomposed it into small components to identify categories and concepts and made notes on their meaning. Questions about these concepts were used as a starting point to examine and code the next set of transcripts. These codes were re-examined and regrouped to form core themes.

We systematically categorised and compared themes to identify similarities and differences in the patterns of data. We also analysed online survey results, and notes taken within interviews and focus groups by researchers, to find common or emerging themes to those developed from the interview and focus group data. This was an iterative process until the themes became more developed and refined to link the initial categories and concepts to form unified explanations of the research questions. Saturation was achieved when all concepts were well defined and explained and no new information could be identified (Corbin and Strauss, 2008), which occurred in our case after 14 interviews and five focus groups. This saturation point aligns with empirical literature, which has shown themes become saturated on average after 12 interviews (Guest et al., 2006).

4. Results

4.1. Access and use of RADs vary by providers

Use of RADs varied across provider characteristics. Several providers stated they maintain a 10%–15% RAD balance in a liquid asset to comply with prudential requirements and use the remainder to finance capital expenditure, while others kept their RADs as cash to ensure they have enough liquidity to meet the outflow of RADs. Some providers noted they used RADs to avoid the need for commercial debt or paying back commercial debt quickly. Provider survey results suggest this view may not reflect the experience of most providers, with 65% of respondents using between 1% and 20% of their RADs for either capital expenditure or to repay a debt incurred for capital expenditure.

If an RAD surplus remained, some providers acquired land for their next development project. This can potentially increase equity from greater land valuation over time, but could also reduce liquidity given the land may not be easily converted into cash if there was an urgent need to pay back RADs. Other providers noted they used RADs to generate income through interest-earning term deposits. Provider survey results found 80% of RAD balances that were not used for capital expenditure were held in a deposit account. Providers noted this RAD income was used to fund facility administration and to cross subsidise daily living expenses and care services. Around 15% of survey respondents noted a potential impact on daily living activities if they experienced a 10% reduction in their RAD balances, while 14% noted a potential impact on delivering care activities and 10% noted a potential impact on delivering extra service activities.

Providers noted within the focus groups that service costs were greater than the basic daily fee and Aged Care Funding Instrument (ACFI) prices they received for their residents. This claim is supported by Department of Health data, which showed the revenue received from the basic daily fee was short of the cost to provide hoteling, utilities and maintenance by $19-$24 per bed day across all regions (Aged Care Financing Authority, 2021). The Australian Government has since sought to rectify this funding gap by introducing a basic daily fee supplement of US$10 per day, per resident in 2021.

One peak body suggested that some providers may use their RADs to fund daily costs, which is not a permitted use of RADs as defined by Section 52 N.1 of the Aged Care Act 1997.

‘I would say that there are services out there who are using their RADs to cross-subsidise, so to keep afloat the care component of their business to fund the care component and the care delivery.’ (A peak body representing providers)

A review of the use of RADs in 2019 found that 164 providers were at risk of not complying with the permitted use rules, with around US$1.6 billion of lump sum accommodation payments being used for other purposes (StewartBrown, 2019).

Banks suggested that management quality was one critical area that providers were assessed against when deciding to lend. Banks placed emphasis on the governance structure and the integrity and experience of the entire management team, including the director of nursing, management team track records, history of adaptability to government regulation changes, and history of dealing with industry sanctions. Banks suggested larger providers were more likely to have better governance systems in place.

Banks noted they were more willing to provide funding to large and multi-site providers given their economies of scale, their ability to spread the investment risk over several sites and their increased ability to attract RADs. One lender noted 200 beds was the minimum number of beds to meet their lending criteria, while another lender noted their clients have 1500 beds on average. It was unclear what banks meant when suggesting large and multi-site providers have a greater ability to attract RADs as consumers have control over their accommodation payment choice. Bank views may reflect where large and multi-site providers choose to locate their facilities, which is in capital cities where the number of RADs available and their values are greater compared to smaller metropolitan, rural and remote regions.

Bankers and valuers suggested large providers mostly used RADs to redevelop or build new buildings in metropolitan regions. This is supported by multivariate regression analysis that estimated the relationship between RADs and provider financial performance using government administration data (Cutler et al., 2021b). It found a positive and significant relationship between RADs and capital expenditure, which was greatest for providers with four or more facilities. Larger providers typically have most of their facilities located in metropolitan regions. Banks also suggested that large providers are more likely to attract higher value RADs by acquiring small providers and refurbishing their rooms.

Banks suggested there were fewer opportunities for small providers to use RADs for capital expenditure as many have facilities located in non-metropolitan locations where RAD prices are lower and residents are more likely to be government supported. This is reflected in the provider survey results, with 74% of providers with less than 300 beds using between 1% and 20% of their RADs for capital expenditure. Provider survey results also suggest RADs were less likely to be used for capital expenditure if the provider was mainly located in regional or remote regions and was government owned.

4.2. Preferences for RADs vary by providers

Providers suggested their preference for RADs depended on their past and future capital expenditure. Providers relied on RADs to build new facilities and undertake major refurbishments or renovations. The promise of RADs allowed providers to access initial debt from banks and to repay that debt within a short period (up to 5 years) once the facility opened and RAD balances increased. Providers noted they prefer DAPs when not planning to undertake capital expenditure because DAPs generated more operational cashflow and earnings compared to the return on investing RADs in permittable assets. This view is supported by historical trends, with the MPIR typically greater than returns from low-risk assets, such as bank deposits.

About four or five years ago it was all about RADs. When we renewed most of our assets, we really had a RAD focus and that was the path we’ve taken. We’re kind of at the end of that program and we’ve built up a significant RAD balance. We’ve lost the appetite for new construction. And so there is a preference now to shift towards DAPs to boost profitability, which is struggling a little bit at the moment. (A provider)

Some providers preferred a more balanced RAD and DAP mix to reduce the operational and capital investment risk associated with relying on one type of accommodation payment.

. . . it’s a balanced approach you have to have. I don’t think you can have one or the other anymore. There’s not sufficient care funding to cover the underlying operating costs of the business anymore. So providers are being forced to supplement or complement that cash flow from accommodation income which traditionally was used purely for refurbishment or a rebuild. A simple DAP approach does help but one is harder than the other. A pure RAD approach does make a financier nervous because they know the regulatory risk and RADs could change tomorrow. The government guarantee could just disappear that would change consumer sentiment towards it. And at the end of day cash flow is really what is most important, it drives valuations for these sites that allows you to get borrowing. So you need to have a really balanced approach to it. (A provider)

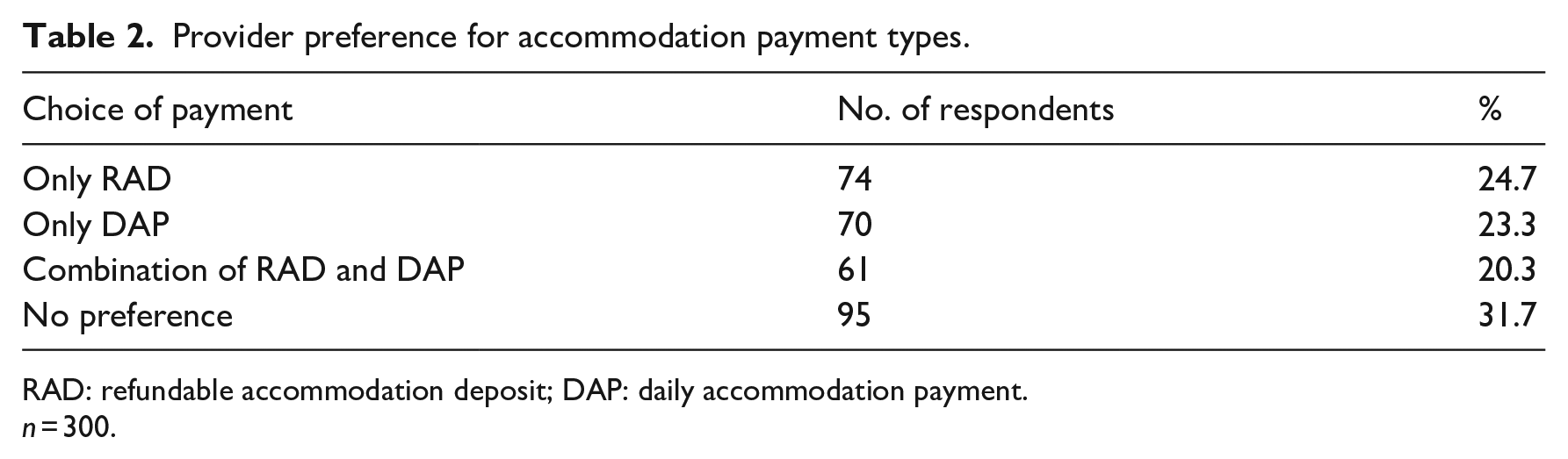

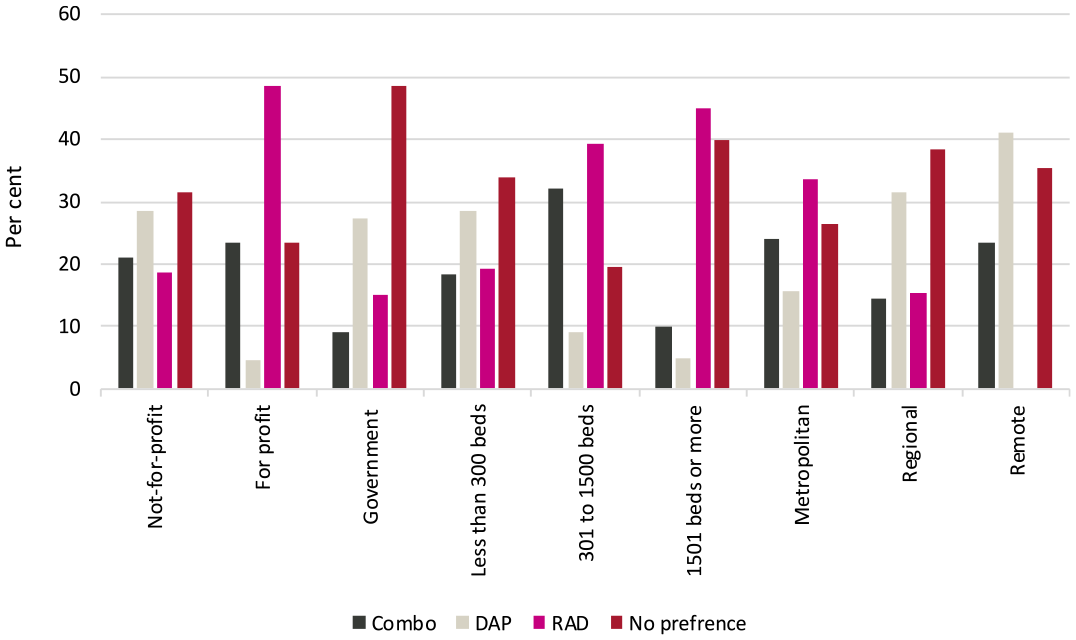

Provider survey results suggested most providers (32%) do not have an accommodation payment preference (see Table 2). Preferences for RADs also differ across provider characteristics. Large providers (1500 beds or more), those with facilities mostly located in metropolitan regions and for-profit providers mostly preferred an RAD, however 40% of large providers also had no preference (see Chart 1). Around half of government providers, and a third of not-for-profit providers had no preference. The relatively low preference for RADs from government providers reflects their greater access to capital finance from government.

Provider preference for accommodation payment types.

RAD: refundable accommodation deposit; DAP: daily accommodation payment.

n = 300.

Provider preference for accommodation payment type by provider characteristic.

4.3. RADs are a low-cost form of capital finance for some providers

All stakeholders suggested RADs allow providers to access commercial debt not otherwise obtainable. Banks suggested that many smaller providers may not easily access commercial debt even if they have good access to RADs. Banks noted that attracting RADs reduces the risk of provider default, and allows banks to better meet their minimum capital adequacy ratios because loans can be repaid quickly. Stakeholders noted that when providers borrow for capital expenditure, the expected RAD value is a key driver of valuation, along with the proportion of residents likely to pay an RAD and the proportion of supported residents. Banks noted their loans are structured around the loan-to-value ratio based on the forecasted value of incoming RADs:

And this is where the role of the RAD is really important [to the construction of facilities] because the majority of times we want RADs to be paying down the debt, or a portion of that debt. And usually we make it 90 per cent because we want providers to keep 10 per cent minimum from a liquidity point of view. (A bank)

Stakeholders therefore saw RADs as a vehicle for providers to undertake greater amounts of capital expenditure, through financing from the RADs and the ability to leverage RADs for short-term borrowing from banks. Banks noted they preferred RADs from a new build (once residents have moved in) to cover the entire amount of bank debt, with the provider having some RADs left over to ensure it can pay residents back when they leave the facility. Stakeholders also saw RADs as an essential component of long-term aged care financing within the sector because banks noted they mostly only lend up to a maximum of 5 years.

RADs are so integral to actually getting either equity or commercial debt approved that with a continued downward trend in RADs it’s becoming significantly harder for services to borrow if they don’t have those RADs essentially as collateral against those services. (A provider peak body)

Stakeholders suggested that RADs provide access to cheaper debt compared to commercial debt and that required rates of return for equity were higher than the MPIR. Stakeholders therefore saw RADs as a unique financing vehicle for providers that could not be easily replaced by bank debt or increased equity without substantial reductions in capital expenditure.

. . . the benefit of the RAD is that it has no interest cost, therefore it is a cheap form of funding for an operator versus other potential forms of funding. So, if I have to replace a cheaper form of funding with a more expensive form of funding, my capacity for capital investment will reduce. (A bank)

These views expressed by stakeholders do not hold universally. As some large providers can borrow more cheaply than the MPIR, RADs can represent a more expensive form of debt because of the income forgone from using an RAD for capital expenditure. An RAD only represents low-cost debt to a provider that cannot access commercial debt at a rate lower than the MPIR.

4.4. RADs create a volatile capital structure

Most stakeholders agreed that RADs could create a more volatile capital structure because they are beholden to resident choices. Stakeholders also noted that providers continuously need to monitor and manage RAD balances to ensure they remain liquid. Banks suggested that there is a mismatch between RADs and capital expenditure, as RADs are a current liability while capital is a non-current asset. Banks suggested this can impose a potential risk to providers’ capital structure because an outflow of RADs may need to be replaced with commercial debt if capital cannot be converted into cash quickly, or is converted quickly but below market rates.

They are [RADs] a short term liability. And they are being used to provide assistance in funding the construction of a long term asset. So there is a mismatch between those two. And whenever you have a mismatch between a liability and an asset, it can create a potential risk to a capital structure. (A bank)

Stakeholders suggested that a provider’s capital expenditure, liquidity and solvency are exposed to shifting consumer preferences away from RADs, creating a challenge for providers to manage a sustainable RAD balance. For some providers, a substantial reduction in RADs could reduce liquidity and solvency because they could struggle to replace those RADs with commercial debt, or payoff their commercial debt if they had recently undertaken substantial capital expenditure. However, while less RADs mean providers have lower cash balances, they may also have less capacity to access commercial debt or undertake capital expenditure. Multivariate analysis found less RADs are associated with more liquidity and greater solvency on average across the sector (Cutler et al., 2021b). A reduction in RADs could improve solvency if DAPs provide a greater return to EBITDA through the MPIR relative to returns earned by investing RADs, or interest paid on commercial debt. This relationship is heterogeneous across the sector. Cutler et al. (2021b) found no significant relationship existed between RADs and solvency for providers with less than four facilities. This potentially reflects their reduced access to RADs and commercial debt, on average.

Several providers were concerned about an outflow of RADs from a decline in occupancy rates and consumer preference shift from RADs to DAPs. These perspectives were supported by results from the provider survey, although not to the extent suggested within the focus groups. Most providers in the survey were concerned about a decline in housing prices, with around 46% of providers agreeing that their RAD balances were significantly exposed to a reduction in housing prices. Only 21% of providers thought their RAD balances were exposed to reduced occupancy rates, 21% thought their RAD balances were exposed to reduced interest rates and 20% thought their RAD balances were exposed to a further shift in consumer preferences from RADs to DAPs.

4.5. RADs incur administrative costs for providers

Stakeholders suggested RADs incur administration costs for providers as they must actively monitor and manage their RAD balance to ensure financial viability. Stakeholders were confident that larger providers understood the permitted uses of RADs and their prudential obligations. They suggested the size and scale of larger providers enabled them to develop strong governance frameworks, and to employ qualified staff to understand the prudential requirements and adhere to the regulations. Stakeholders also noted that small operators might struggle with understanding prudential standards and compliance, given they have limited resources.

‘. . . about 600 providers are single-site operators, relatively small businesses. I think it’s fair to say that their ability would vary with regards to the depth of understanding of the prudential requirements.’ (A provider peak body)

Provider survey results suggest this view may not accurately reflect the sector. Around 97% of respondents noted they ‘completely’ understood the prudential requirements for using lump sum accommodation payments.

While the Accommodation Bond Guarantee Scheme means consumers will always receive their RADs once they leave a facility, stakeholders suggested low liquidity increased the risk of providers defaulting on their RAD obligations. This increased the risk to either the Australian Government or other providers for paying back the RAD debt, given the Australian Government can impose a levy on all other providers to recover lost RADs through the Aged Care (Bond Security) Levy Act 2006.

4.6. The choice between RADs and DAPs is not well understood by consumers

Stakeholders suggested the choice between an RAD or DAP can be complex for consumers and their choice can significantly impact a consumer’s wealth. A consumer peak body noted that many consumers have a limited understanding of the financial implications of their accommodation payment choice and are not fully aware of how the Accommodation Payment Guarantee Scheme works. It suggested consumers are hesitant to hand over their life savings to a provider, with an emotional attachment to the family home and inheritance further complicating the decision:

Even though there is a guarantee on RADs, consumers don’t understand how it all works properly and they fear they’re not going to get the money back. And that kind of goes back into that inheritance side of things as well, so that complicates things. (A consumer peak body)

This view is supported by Cutler et al. (2021a), who surveyed 589 informal carers that either made or substantially influenced the accommodation payment decision. The study found that 40% reported the accommodation payment decision as complex and 33% were not certain that the accommodation payment decision was best for the resident financially. Only 48% of informal carers were considered financially literate.

Some stakeholders observed that many people do not consult a financial advisor even though they are confused about RADs and DAPs. Stakeholders suggested consumers are price sensitive and there was limited pricing transparency for financial advice. Cutler et al. (2021a) found only 37% of informal carers consulted a financial advisor when making an accommodation payment decision. Stakeholders also noted that many consumers do not fully trust financial advisors:

‘. . . they’re not willing to go to financial advisors because they don’t trust financial advisors. So trust is a really big factor for consumers I think.’ (A consumer peak body)

A limited understanding of RADs and DAPs increases the likelihood that a consumer will make a sub-optimal accommodation payment choice. Stakeholders suggested that some providers try to manipulate consumer choice towards RADs to suit their preferences. Provider survey results support these views, with around 27% of providers noting that they had a strategy to maintain or increase RAD balances, including offering fee rebates for a consumer to pay an RAD and keeping accommodation prices low.

Some providers noted within the focus groups that their strategy to maintain RAD balances was to increase occupancy through marketing or applying for additional bed licences. One provider noted they worked with consumers on the potential financial benefits of an RAD. This approach could be contrary to legislation as direct financial advice can only be provided by a registered financial planner.

Overall, providers suggested they had little control over accommodation payment choices. Providers argued that allowing consumers to choose freely created increased uncertainty for capital expenditure planning and could reduce the sector’s attractiveness to equity investors. Several providers believed they should have more influence over the consumer’s accommodation payment choice, using a process of mutual agreement with consumers:

But currently it’s [accommodation payment arrangement] swayed too much towards the consumer. Where else would you normally pay for accommodation say okay, well you know what, we’ll settle on a piece of accommodation, but you have a choice to make it a lump sum payment or rent and it’s completely at your disposal. There should be a fairer process whereby the provider and the consumer actually have a bit more of a conversation and come up with what works for both. (A provider)

One provider suggested that the Australian Government should enforce a minimum proportion of RADs that must be offered to the market by a provider, relative to their total number of accommodation payments received, but beyond that the provider can dictate the accommodation payment type paid by consumers. While this would be attractive to providers, it would reduce consumer choice and their ability to match their accommodation payment choice to their financial circumstances. It could also reduce access to care if consumers cannot afford an accommodation payment type sought by a provider.

4.7. RADs impose barriers to entry for equity investment

Stakeholders suggested that RADs impose barriers to entry for equity investment. They suggested there was limited publicly available information on the residential aged care sector for equity research, given the small number of providers listed on the Australian stock exchange, which made investment risk assessment opaque. Stakeholders suggested that assessing the value of providers was further complicated by the lack of investor understanding of RADs and how they are treated on the balance sheet.

. . . what you really need is for there to be sufficient companies that are large enough on the stock exchange to be followed by credible equity research analysts who then present back appropriate analysis on what’s going on in the business. This creates better information dissemination and, therefore, creates a more efficient equity capital market. That doesn’t quite exist for Australian aged care businesses and one reason is the complications that RADs create. (A valuer)

Bankers and valuers largely agreed that RADs are not well understood by international investors as there is no comparable system outside Australia. They suggested this imposes a barrier to entry for international investors as they must become familiar with RADs first to minimise their perceived investment risk.

It [RADs] does discourage investment. So, we represent overseas acquirers. And large groups that are interested in investing in Australia. And the two things that are challenging is that it takes a long time for us to get their heads around RADs because they don’t exist anywhere else in the world . . .. So, it’s very hard to sell that concept to someone from overseas. (A valuer)

One bank questioned whether categorising RADs as a current liability could reduce equity investment in the sector:

I guess the other thing to think about is the structure of a RAD as a liability on the balance sheet. It’s a short term liability. Notwithstanding they’re interest free. But does that have an impact in terms of their capacity to provide equity? (A bank)

Some providers also felt that RADs created a barrier for REITs to enter the market in a substantial way. It was suggested that RADs increase large loan-to-asset ratios because the building asset sits on the REIT balance sheet while the RAD liability sits on the provider balance sheet. Stakeholders noted that if RADs are misappropriated by the provider, and the provider enters bankruptcy, there is no building asset to draw upon for collateral under an REIT arrangement.

4.8. No viable alternative to RADs currently exist

Banks felt they did not have enough lending capacity to replace a substantial reduction in RADs because their lending was restricted due to capital requirements. They suggested many smaller providers would not gain access to bank debt because they would be considered too risky. Even if interest rates on debt were increased and could be met by the provider, banks suggested they would be hesitant to lend due to unacceptable liquidity risk rating:

‘There isn’t a lot more debt capacity the sector could currently take on. Bank debt capacity is almost exhausted, particularly given the margin erosion we’re seeing, and the emerging liquidity issue through a change to DAPs.’ (A bank) It goes back to the capital requirements. There is a premium put on liquidity and so lending outside a certain point becomes challenging because we need to maintain a fair bit of liquidity in our funding sources to meet the capital requirements. (A bank)

Several possible financial alternatives to RADs were discussed by stakeholders. Stakeholders suggested private equity investors are interested in the residential aged care sector, given ageing of the Australian population offers potential growth opportunities. However, stakeholders suggested they are reluctant to enter the market due to low profitability and uncertainty around regulatory change.

Several stakeholders noted that REITs are common in aged care markets in other countries. Banks noted that healthcare REITs are keen to invest in aged care but the current MPIR would not generate enough yield for healthcare REITs to invest, given there were better returns from other healthcare properties. The option for the Australian Government to invest in the residential aged care sector was also raised by stakeholders, with some suggesting an Australian Government-backed loan facility to providers, or as an investor of last resort if providers could not obtain commercial debt.

5. Discussion

Interviews, focus groups and the provider survey identified perceived advantages and disadvantages associated with RADs, which differed across provider types and their position in their capital expenditure cycle. This is reflected in the ongoing debate around whether RADs are fit for purpose in the future of residential aged care in Australia. Some stakeholders felt RADs are not sustainable due to the potential liability created for the Australian Government through the Accommodation Payment Guarantee Scheme. While this risk could be mitigated by imposing a levy on providers to recoup government costs, the levy would increase provider costs when many providers are already operating with low margins.

Interview and focus group respondents suggested that RADs provide access to debt that may not otherwise be available from a bank, thereby allowing for more capital expenditure. They also noted RADs offer cheaper debt compared to bank debt for those providers who cannot access debt more cheaply than the MPIR. However, some providers indicated they are exposed to shifting consumer preferences for RADs, which potentially increases their liquidity and solvency risk, although most providers within the survey were more concerned about the negative impact of a reduction in house prices, given they are correlated with RAD prices. There are also administrative costs associated with managing RAD balances and maintaining adequate liquidity and solvency.

Our representative survey of providers suggests most providers do not prefer an accommodation payment type. A substantial shift from RADs to DAPs would impact residential aged care providers differently, depending on their reliance on RADs. It could benefit some providers not looking to undertake capital expenditure. Given the provider survey found RADs are mostly invested in bank deposits if not used for capital expenditure, a consumer preference shift to DAPs could increase provider incomes because the MPIR is typically greater than bank deposit returns. Similarly, providers with little reliance on RADs may not be substantially negatively affected by a significant reduction in RAD balances. These providers are typically government owned, small or located in remote regions. Providers most negatively affected are likely to be those with most of their RADs used for capital expenditure, or providers that require RADs for significant future capital expenditure. Results from the provider survey suggests these are large, for-profit providers with most of their facilities located in metropolitan regions.

Whether the Australian Government should intervene if there was a decline in RAD balances depends on the size and timing of that decline. Provider survey results suggest the residential aged care sector could mostly absorb a small reduction in RAD balances over a long period of time. Most providers (68%) believed that a 10% reduction in their RADs balance due to a shift to DAPs would not impact their capital investment decisions, and around 53% of providers noted that it would not impact other parts of their business.

Around 65% of providers responding to the survey noted that a 10% reduction in RADs could be covered by additional debt or equity. Providers also noted there were other financing options available, besides equity or commercial debt, which could replace a reduction in RAD balances. These included disposing of assets, such as an investment portfolio or surplus property, or using funding from other business streams, such as retirement living. Some providers noted they had access to state government contributions, while others noted they would seek funding from the Australian Government or through donations, while some providers stated they could raise funds through their association members.

The Australian Government announced extensive aged care reforms in the 2021–2022 Budget. It pledged US$17.7 billion to address most recommendations made by the Royal Commission into Aged Care Quality and Safety. Within the reform package, the Australian Government announced it will spend US$55.3 million to introduce a new financial and prudential monitoring, compliance and intervention framework, commencing over three phases from July 2021 (Department of Health, 2021b). The Framework will include minimum liquidity requirements and capital adequacy requirements applied to providers, quarterly financial reporting and improved Aged Care Financial Report and Annual Prudential Compliance Statement reporting (Department of Health, 2021b). The objective is to reduce the Australian Government’s contingent liability associated with the Accommodation Payment Guarantee Scheme.

Another way to reduce the financial risk associated with a substantial reduction in RADs is to attract a greater proportion of equity within the capital financing mix of providers. Stakeholders suggested this would require a significant increase in funding from the Australian Government for care services and daily living expenses, given many providers are struggling to cover these costs with current revenue streams. The Royal Commission into Aged Care Quality and Safety suggested the residential aged care sector was extensively underfunded (Royal Commission into Aged Care Quality and Safety, 2021). Stakeholders noted that increased provider returns are required to attract more REITs into the sector; however, they also suggested that low levels of financial sophistication and the unwillingness to shift towards an unfamiliar financial product may limit the use of REITs by many providers.

The Australian Government has recently changed the funding quantum and approach for care services and daily living expenses. Under the reforms announced in the 2021–2022 Budget, the Australian Government is providing additional funding to increase the amount of frontline care delivered by providers and an additional basic daily fee supplement to help providers deliver better food. The Australian Government has also introduced a new funding model for care services and giving responsibility to the newly formed Independent Health and Aged Care Pricing Authority (IHACPA) to recommend care prices.

There was no consensus among stakeholders on whether RADs are an appropriate source of finance for a future aged care system. Some felt that the residential aged care sector should be without RADs due to the volatility they can create for providers. The Australian Government has not committed to removing RADs, instead promising to consult with the sector on new ways to raise capital expenditure finance (Department of Health, 2021b). Stakeholders noted that the Australian Government has a potential role to play in transitioning to a sector without RADs. Some stakeholders suggested one way to transition away from RADs is to develop an Australian Government backed loan facility for providers. Alternatively, they suggested the Australian Government could act as an investor of last resort if providers could not obtain commercial debt.

If the Australian Government were to guarantee providers’ commercial debt, this would reduce lending risk for banks, allowing them to provide more debt and more providers to access commercial debt. This approach is not without precedent. The Australian Government provided loan guarantees under the Small to Medium Enterprise Recovery Loan Scheme during the COVID-19 pandemic. (Australian Government, 2021). The US Department of Housing and Urban Development’s (HUD) Section 232 programmes provide mortgage insurance to finance the purchase, refinance, new construction or substantial rehabilitation of nursing home facilities in the United States (Federal Housing Administration, 2020).

An Australian Government loan facility for providers to access capital could be attractive. The Australian Government has access to relatively cheap debt from their current AAA credit rating (Chalmers, 2023). The Australian Government could also allow providers to invest their surplus RADs into the loan facility, which could give them access to higher returns than bank deposits.

6. Conclusion

RADs have allowed providers to refurbish old facilities and build new facilities to better meet consumer preferences. Providers that prefer RADs have used their RADs for capital expenditure or are looking to undertake further significant capital expenditure. The value of RADs to a provider can be contingent on their capital expenditure plans.

A substantial reduction in RAD balances would impact residential aged care providers differently. Providers most negatively affected would likely be those with most of their RADs used to finance capital expenditure. In general, these are large, for-profit providers with most facilities located in metropolitan regions. A substantial reduction in RAD balances would likely reduce capital expenditure undertaken by non-government providers but would have little impact on government providers.

Transitioning the residential aged care sector from RADs to commercial debt and equity would align the residential aged care sector financing with other countries, such as the United States, United Kingdom and Canada (Cutler et al., 2021b). These countries rely more on debt and equity through REITs to fund residential aged care accommodation. If the Australian Government chooses that path to reduce the reliance on RADs, providers may need to generate a greater return on investment to attract more equity.

Alternatively, an accommodation capital facility could be established with some form of assistance from the Australian Government, whether through guaranteeing providers’ commercial debts or forming its own loan facility for providers to access capital. Any intervention must ensure the Australian Government has a detailed understanding of provider financial positions and their drivers, and the financial impact of moving away from RADs, to ensure any transition can be undertaken with minimal risk to residential aged care access.

Supplemental Material

sj-docx-1-aum-10.1177_03128962241230665 – Supplemental material for The role of refundable accommodation deposits in financing aged care capital expenditure: Views from the sector

Supplemental material, sj-docx-1-aum-10.1177_03128962241230665 for The role of refundable accommodation deposits in financing aged care capital expenditure: Views from the sector by Megan Gu, Henry Cutler, Mona Aghdaee, Yuanyuan Gu and Anam Bilgrami in Australian Journal of Management

Supplemental Material

sj-docx-2-aum-10.1177_03128962241230665 – Supplemental material for The role of refundable accommodation deposits in financing aged care capital expenditure: Views from the sector

Supplemental material, sj-docx-2-aum-10.1177_03128962241230665 for The role of refundable accommodation deposits in financing aged care capital expenditure: Views from the sector by Megan Gu, Henry Cutler, Mona Aghdaee, Yuanyuan Gu and Anam Bilgrami in Australian Journal of Management

Supplemental Material

sj-docx-3-aum-10.1177_03128962241230665 – Supplemental material for The role of refundable accommodation deposits in financing aged care capital expenditure: Views from the sector

Supplemental material, sj-docx-3-aum-10.1177_03128962241230665 for The role of refundable accommodation deposits in financing aged care capital expenditure: Views from the sector by Megan Gu, Henry Cutler, Mona Aghdaee, Yuanyuan Gu and Anam Bilgrami in Australian Journal of Management

Footnotes

Acknowledgements

We acknowledge guidance provided by the Aged Care Financing Authority when undertaking this study.

Final transcript accepted on 4 January 2024 by Phong Ngo (AE Finance).

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the Commonwealth Department of Health through the Aged Care Financing Authority. The views expressed in this article are wholly those of the authors.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.