Abstract

Scandals show that ethics is an important topic in financial planning. Our research analyses 212 financial ombudsman decisions (2013–2018) to understand the nature of financial planning misconduct in complaint decisions. We develop a coding structure to ascertain what professional conduct involves and then use content analysis and cluster analysis to identify the aspects of professional conduct occurring in these misconduct decisions. Diligence, acting in the client’s best interest and having no reasonable basis for advice are interconnected elements in over half of these decisions. Secondary elements are misleading statements, conflicts of interest and disclosure. Analysis of decisions involving fiduciary duty showed that financial planners failed to ascertain a client’s circumstances and did not form advice based on their client’s information. As financial planning professionalises, future research, financial planning education, policy and practice should address these issues.

JEL Classification:

1. Introduction

Financial services scandals in Australia involving alleged unethical behaviour, misleading advice and deceptive conduct highlight governance and cultural challenges within the financial planning industry (Hayne, 2019; Steen et al., 2016). There have been significant regulatory reforms to improve trust in the financial planning profession, including the development of an industry-wide code of ethics (Financial Adviser Standards and Ethics Authority (FASEA), 2019) and a protocol for ensuring that financial advice is provided in a client’s best interest (Australian Government, 2018). A fiduciary duty is entrenched in the code of ethics and legislation, so a fiduciary duty is triggered when personal financial advice is provided (Richards and Morton, 2020). However, creating codes of ethics and fiduciary duty protocols alone is insufficient to build trust in a profession (Brien, 1998) and the financial planning profession (Cull and Bowyer, 2017). Instead, research is needed to investigate pertinent ethical issues in financial planning and ascertain how these ethical issues reconcile with the professional conduct espoused by the ethical elements in codes of ethics and fiduciary duty protocols.

One method to understand ethical issues in financial planning is to analyse instances of misconduct in the financial advice industry (Camarda, 2017; Egan et al., 2018). Research on misconduct has illustrated the prevalence of misconduct, how repeat misconduct continues and adviser-based factors associated with misconduct. However, the research is quantitative and could be complemented by qualitative research on the inherent nature of the misconduct and how it impedes the expected delivery of financial advice. To build trust in financial advice through developing codes of ethics and fiduciary protocols, it is important to gather rich information on unethical behaviour in financial planning. This article addresses that need by reviewing financial ombudsman decisions to identify the types of misconduct most apparent in financial planning. The two research questions are as follows:

RQ1. What aspects of professional conduct are violated in financial planning misconduct decisions?

RQ2. What are the key breaches in fiduciary duty in financial planner misconduct decisions?

Professional conduct of financial planners refers to the collective ethical elements outlined in codes of ethics and steps in a fiduciary duty protocol.

A combination of content analysis, cluster analysis and qualitative analysis of financial ombudsman decisions from 2013 to 2018 was undertaken to answer these questions. Content analysis coded each decision for ethical elements and conduct type in the provision of financial advice. Cluster analysis was used to identify emergent themes from these data, and qualitative analysis draws a richer picture of the nature of the misconduct. In total, 212 financial ombudsman decisions were analysed, representing a large sample from which to draw conclusions. An amalgamation of codes of conduct espoused by professional bodies was used to create a coding structure for the ethical elements. A coding structure for conduct type was created from prior literature and analysis of the data. Finally, a coding structure for fiduciary duty was created using the legislated client’s best interest protocol. The codes of ethics and the client’s best interest protocol represent the professional conduct to which financial planning should adhere to professionalise and improve trust in this industry.

Our findings illustrate facets of misconduct in financial advice complaint decisions. Descriptive analyses found that investment products, especially those with higher risk, feature frequently in financial ombudsman decisions when compared to industry revenue data. The cluster analysis identified two recurring ethical elements: diligence and acting in a client’s best interest. These were inherently linked with the conduct type of not having a reasonable basis for advice, and our analysis elaborates the interconnectedness of these ideas. Other ethical elements in the decisions included objectivity, fairness and conflicts of interest and the conduct type of misleading statements. As the issue of acting in a client’s best interest occurred frequently, we analysed this more thoroughly using a seven-step fiduciary duty process legislated in Australia. Results show that where a client’s best interests were impeded in the financial planning process, financial planners were not ascertaining the clients’ circumstances, not basing decisions on these circumstances and recommending products that were not justified.

Overall, our analysis of the ethical elements, types of conduct and steps in fiduciary duty suggests a need for improved communication between financial planners and clients. This is a concern because communication issues arose in fiduciary duty cases where the financial planner was not ascertaining a client’s circumstances and could not base financial advice on the (unknown) circumstances. Our findings contribute to developing a richer understanding of the types of unethical behaviour in financial planning and can serve as the starting point for education and regulation in financial planning. Our results shape a narrative to accompany the codes of ethics to make them effective tools in building trust for this developing profession.

2. Literature review

2.1. Ethics and trust in financial planning

Bigel (1998) examined the benefits of certification and the merits of various compensation systems on ethics in financial planning. The study was limited to financial planners practising in the United States. It found that Certified Financial Planner® (CFP®) designees achieved higher ethical orientation scores than non-holders of this qualification, suggesting that codes of practice influence ethical decision-making. Lower ethical orientation scores were noted among planners whose career tenure exceeded 10 years, but a comparison between fee-based planners and their counterparts remunerated via commissions found no significantly different results. However, experimental research on financial planning has illustrated that commission-based remuneration reduces truth-telling and lowers the priority given to a client’s interest in financial planning (Angelova and Regner, 2013; Chen and Richardson, 2018). Also, Steen et al. (2016) found that remuneration structures driving sales of unsuitable products, poor management and lack of experience coupled with inadequate compliance oversight caused scandals in financial planning in Australia.

For financial planning to professionalise, the sector needs to embrace the role of ethics in financial advice. Bruhn and Asher (2020) conduct a qualitative analysis of parliamentary inquiries and in-depth interviews surrounding the Storm Financial Services scandal 1 and find a need for professional financial advice and that ethics needs to take a primary role in professional advice. That is, the ethical disposition in providing financial advice is inherently linked to the quality of financial advice provided. Other research finds that ethics is lacking in the financial advice sector. Smith (2009) observed that ethical reasoning levels among financial planners and compliance managers were lower than the level required to effectively resolve the complex ethical dilemmas associated with the provision of advice. Smith finds that a lack of integrity was one of the most common ethical issues. Murphy and Watts (2009) surveyed financial planners to determine whether their attitudes towards professionalism would meet the level required to convert financial planning into a profession. Their findings showed that financial planners failed to exhibit a satisfactory level of professionalism considering the attributes of professionalism. Finally, Cull and Bowyer (2017) used a mixed method approach to investigate the ethical behaviour of financial advisers considering changes in the economic environment (post-Global Financial Crisis) and regulatory changes (post-Future of Financial Advice reforms). They found that clients ranked their financial planners’ technical skills highly but were less impressed with their ethical skills. However, when ranking the importance of different aspects of financial advice, clients ranked ethical skills above technical skills.

The concept of trust is inherently linked to ethics and is relevant to financial planning (Bruhn and Asher, 2020) because trust is an important determinant of seeking financial advice (Burke and Hung, 2019; Lachance and Tang, 2012; Monti et al., 2014). Hunt et al. (2011) found that Australian financial planners do not realise how important trust is from the client’s perspective and overestimate clients’ trust in them. Cull and Sloan (2016) found that affective elements of trust are essential in the financial planner–client relationship where clients feel emotional bonds, benevolence and likeability in their financial planner. The trust clients have in the financial services sector has decreased since the Global Financial Crisis (Ahmed et al., 2020). This decrease in trust has been exacerbated in Australia, where the Royal Commission illustrated the pervasiveness of misconduct in this sector (Hayne, 2019).

2.2. Misconduct in financial planning

While there is limited research into financial planner misconduct in the Australian context (Steen et al., 2016), two studies in the United States provide insights into the extent of this misconduct. In the United States, financial advisers are registered by the Financial Industry Regulatory Authority (FINRA). In the first study, Camarda (2017) measured the relationship between having a financial advisory professional designation and misconduct and found that having at least one professional designation is associated with lower misconduct. In the second study, Egan et al. (2018) constructed a database of financial advisers in the United States from 2005 to 2015, representing approximately 10% of those employed in the finance and insurance sector. This study examined the economy-wide extent of misconduct among financial advisers and the associated labour market consequences of misconduct. Seven percent of advisers had misconduct records, but this increased to 15% at large advisory firms. Around one-third of advisers with misconduct convictions are repeat offenders, and prior offenders are 5 times more likely to engage in new misconduct than are average financial planners. Approximately half of the financial planners lose their jobs after misconduct, yet firms rehire many of these planners despite their history of misconduct. The results show the prevalence of misconduct in this industry.

The limited research on ethics in Australian financial planning research suggests that the ethical capabilities of Australian financial planners could be improved (Bruhn and Asher, 2020; Murphy and Watts, 2009). Research based in the United States illustrates the prevalence of misconduct in the financial advice sector. It would seem reasonable to suggest that this occurrence of misconduct is also present in Australia, and some misconduct was highlighted by the government inquiry (Hayne, 2019). However, it remains unknown what common unethical practices occur in this environment. There is a need for research into the behaviour of financial planners when ethical issues are raised; this is a topic we pursue.

2.3. Codes of ethics

A code of ethics, sometimes referred to as a code of conduct or a code of practice, is created to ensure a minimum level of ethical standards among peers in a profession. Abbott (1983) identified that the creation of codes of ethics and their application is essential in the development of a profession. A purpose of a code of ethics is to create trust in a profession because it acts like a mission statement, quality assurance management strategies or promise of service and contains sensible guides for action for clients and the public (Bonvin and Dembinski, 2002; Mackay, 2011). This is essential for the emerging financial planning profession, where client trust in their financial planner is crucial (Bruhn, 2019a, 2019b; Calcagno et al., 2017).

Australian financial planning professional bodies have developed codes of ethics (Accounting Professional & Ethical Standards Board (APESB), 2013; Association of Financial Advisers (AFA), 2018; Financial Planning Association of Australia (FPA), 2013). While not all financial planners belong to professional organisations, they have been governed by contract and tort laws that require professionals to have a duty of care (Glover, 2002). A duty of care requires that professional services ‘must be rendered with reasonable care according to prevailing community standards’ (Glover, 2002: 224). These community standards are set by the codes of ethics espoused by various professional bodies (discussed in further detail in Section 3). Thus, those providing financial advice in Australia have a legal requirement to provide advice in line with the professional bodies’ codes of ethics. More recently, the FASEA (2019) code of ethics was legislated into the Corporations Act, 2001 Section 921E, making this code a legal requirement.

Nonetheless, developing a code of ethics will not compel professionalisation and inherent trust by clients in a vocation, including financial planning. Brien (1998) argued that a profession’s adoption of a code of ethics, self-regulation and legislation alone does not control unethical behaviour. Instead, a culture of trust in each individual and the profession is required. Research by Kaptein and Schwartz (2008) on the effectiveness of codes of ethics supports Brien’s (1998) argument. They report that only 35% of the studies found that codes are effective, 16% of studies found that the relationship is weak, 33% found no significant relationship between the two, 14% presented mixed results and one study found that codes are counterproductive.

To create an effective code of ethics, and thereby increase the trust in a profession, a code needs to be accepted and incorporated by individuals in the profession (Schwartz, 2013; Statler and Oliver, 2016). However, there is a dearth of research to ascertain which ethical issues exist in the financial planning industry. With no clear knowledge of ethical issues in financial advice, codes of ethics are ineffective tools to build trust because some financial planners cannot see the folly in their practices. This study builds knowledge on the types of misconduct involved in financial advice and how such misconduct is classified using the codes of ethics espoused by financial planning professional bodies.

2.4. Fiduciary duty

A key ethical element in financial planning codes of ethics is that the financial planner acts in the client’s best interest (Richards and Morton, 2020). This stems from the concept of fiduciary duty. Boatright (2000) states, ‘Fiduciary duties are the duties of a fiduciary to act in that other person’s interest without gaining any material benefit except with the knowledge and consent of that person’ (p. 202). This concept is relevant for the financial services industry, where fund managers and trustees act as custodians of clients’ investments (Palazzo and Rethel, 2008). In financial planning, the concept of fiduciary duty is often equated to acting in the best interest of one’s clients and is a key characteristic of clients’ trust in their financial planner (Cull and Sloan, 2016). However, ‘best interests’ is a difficult concept to define.

The collapse of Storm Financial Services provides significant insight into the understanding of fiduciary duty and acting in a client’s best interest. Bruhn and Miller (2014) researched the high-profile collapse of Storm Financial and examined factors that constitute good advice, couched in terms of a ‘best interests’ duty from adviser to customer. The authors concluded that the key aspects of best interest are that advice is personalised to the client, explicitly accounts for a customer’s goals and risk tolerance, is communicated clearly and allows for alternative advice to be sought (Bruhn and Miller, 2014). They add that extra precautions should be taken when recommending debt and additional borrowing and that a client’s choice to proceed does not remove the adviser’s duty to consider the client’s best interest in future courses of action.

Many countries have legislated the need to uphold a client’s best interest when giving financial advice (Angel and McCabe, 2013; Batten and Pearson, 2013; McMeel, 2013). In Australia, the Corporations Amendment Act 2012 (Commonwealth of Australia, 2012) amended the Corporations Act, 2001 (Cth) to include a statutory fiduciary duty for financial advisers to act in the best interests of their clients, which is essentially a codification of the existing common law fiduciary duty owed by all advisers. Specifically, advice providers are required to act in a client’s best interests under s961B of the Corporations Act. Australian Securities and Investments Commission (ASIC, 2021b) provides guidance on the best interests duty in Regulatory Guide 75 – Licensing: Financial product advisers – Conduct and disclosure. RG 175.254 of this guide sets out the processes for complying with the best interests duty, and this includes an appropriate scope of advice that meets the client’s objectives, financial situation and needs; that these objectives, financial situation and needs are identified through appropriate enquiry; and that the advice provider focuses on providing advice that is not product specific (ASIC, 2021a).

There is some academic argument about how financial planners should act to ensure their compliance with their fiduciary duty. Richards and Morton (2020) argue that the business models adopted in many financial planning practices impede a fiduciary duty. Martin (2009) analyses whether the fiduciary duty of a financial adviser is compatible with socially responsible investing (SRI). Drawing on legal, religious and professional arguments, Martin (2009) argues that the two are not incompatible and that advisers should follow 27 standards, 7 standards of care and a five-step investment process. Martin’s (2009) argument is theoretical and does not constitute empirical research evidence on whether financial planners adhere to these processes. The current research investigates this topic by examining the processes where financial planners are most likely to falter when they do not act in accordance with a fiduciary duty.

In summary, ethics are of concern in financial planning as the profession tries to build clients’ trust in an industry where misconduct occurs. Two methods of building trust are to create a code of ethics and enforce a requirement to act in a client’s best interest. Both methods have been legislated in the Australian financial planning industry. However, it is unknown what elements of these codes of ethics are impeded or what types of behaviour occur in financial planning misconduct. The current research investigates this topic through content analysis of financial ombudsman decisions. The following section outlines the research method, the research findings and finally, a discussion of the implications of this research method.

3. Method

3.1. Data

All financial service institutions that are Australian Financial Services (AFS) licensees are required to offer both internal and external complaint services for clients. The unit of analysis for this research is the adjudication of external consumer complaints, called decisions. This study focuses on an analysis of 212 decisions that pertain to personal financial advice. Decisions are selected from the three financial ombudsman services in Australia (Financial Ombudsman Service (FOS), Credit and Investments Ombudsman and the Superannuation Complaints Tribunal) over the period 8 August 2013 to 9 August 2018. This time frame was chosen as the cases will incorporate the Future of Financial Advice legislation, which was voluntary on 1 July 2012 but became mandatory as of 1 July 2013 (Australian Government, 2018). There were 719 decisions available over this time frame. Selection of the 212 decisions involved a stratified sampling approach where the subgroups were the type of products advised on (details on products are in Section 4.1). Subgroup proportions were ascertained using the search function on the ombudsman’s websites for the research time frame. Selection of decisions within each subgroup was made by assigning random numbers. FOS had more financial advice decisions than the other ombudsman services, so based on proportionality, FOS decisions are 98% of our data.

Lodging a complaint with FOS is free for clients because the AFS licensee pays for this service via annual fees. When a complaint has been lodged with FOS, the decision can be resolved by referring it back to the internal complaint service, negotiation, conciliation/mediation or by decision. In our research, we review the decisions because the ombudsman organisations published them after they were anonymised. A decision is determined by a panel (an ombudsman, a client representative and an industry representative) and offers detail about the reason and nature of the dispute and the elements involved (FOS, 2015). The decision is made regarding legal principles, applicable industry codes of ethics, good industry practice and previous relevant decisions. This illustrates that ombudsman decisions blend legal and moral duties when making a ruling. Each decision is binding on the financial service provider (FSP) but not on the client. In 2018, FOS accepted complaints where the dispute is less than US$500,000 and could award a maximum of US$323,500 in a decision (FOS, 2018).

3.2. Content analysis: coding decisions

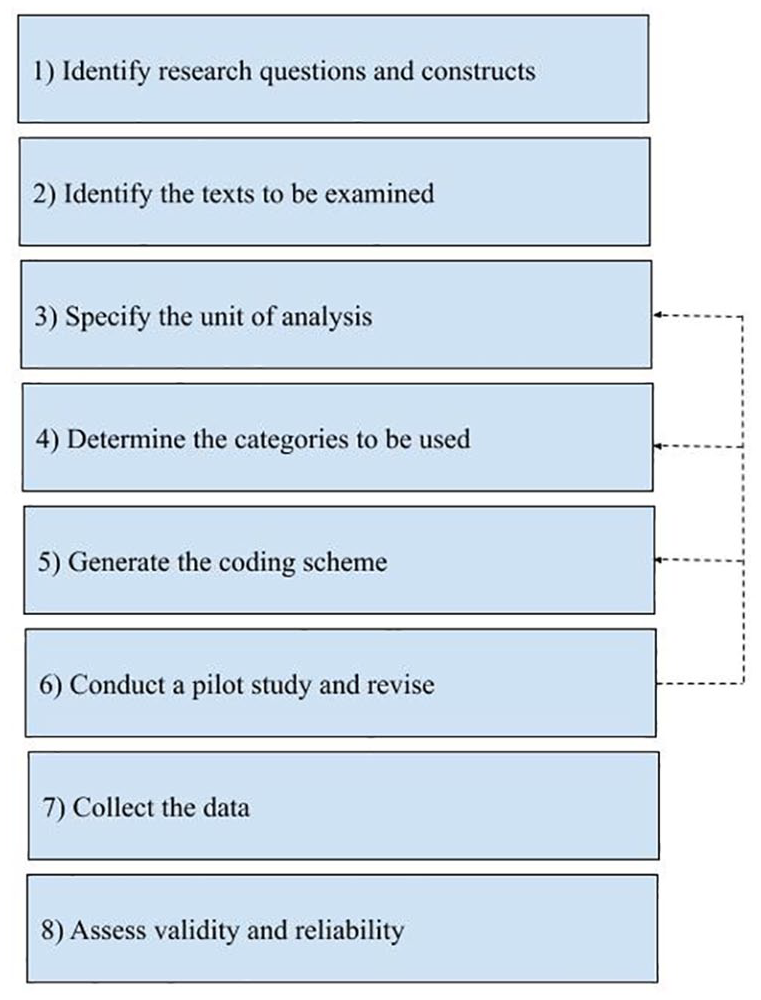

To investigate the two research questions of this study, a content analysis method, as outlined by Harris (2001), was undertaken to ensure validity and reliability. Figure 1 shows a graphical depiction of the stages in content analysis employed to code data (Harris, 2001: 194). We used this content analysis to construct codes in three steps. The first step was to assess the professional standards financial planners are required to adhere to. As outlined in the literature review above, financial advice is required to be delivered at professional standards under contract and tort laws (Glover, 2002), and recently, FASEA (2019) legislated a code of ethics for financial advice. For this reason, our coding framework was derived by reviewing the codes of ethics adopted by the financial planning professional bodies and the code of ethics legislated by FASEA for financial advice in Australia.

Process of content analysis from Harris (2001: p. 194).

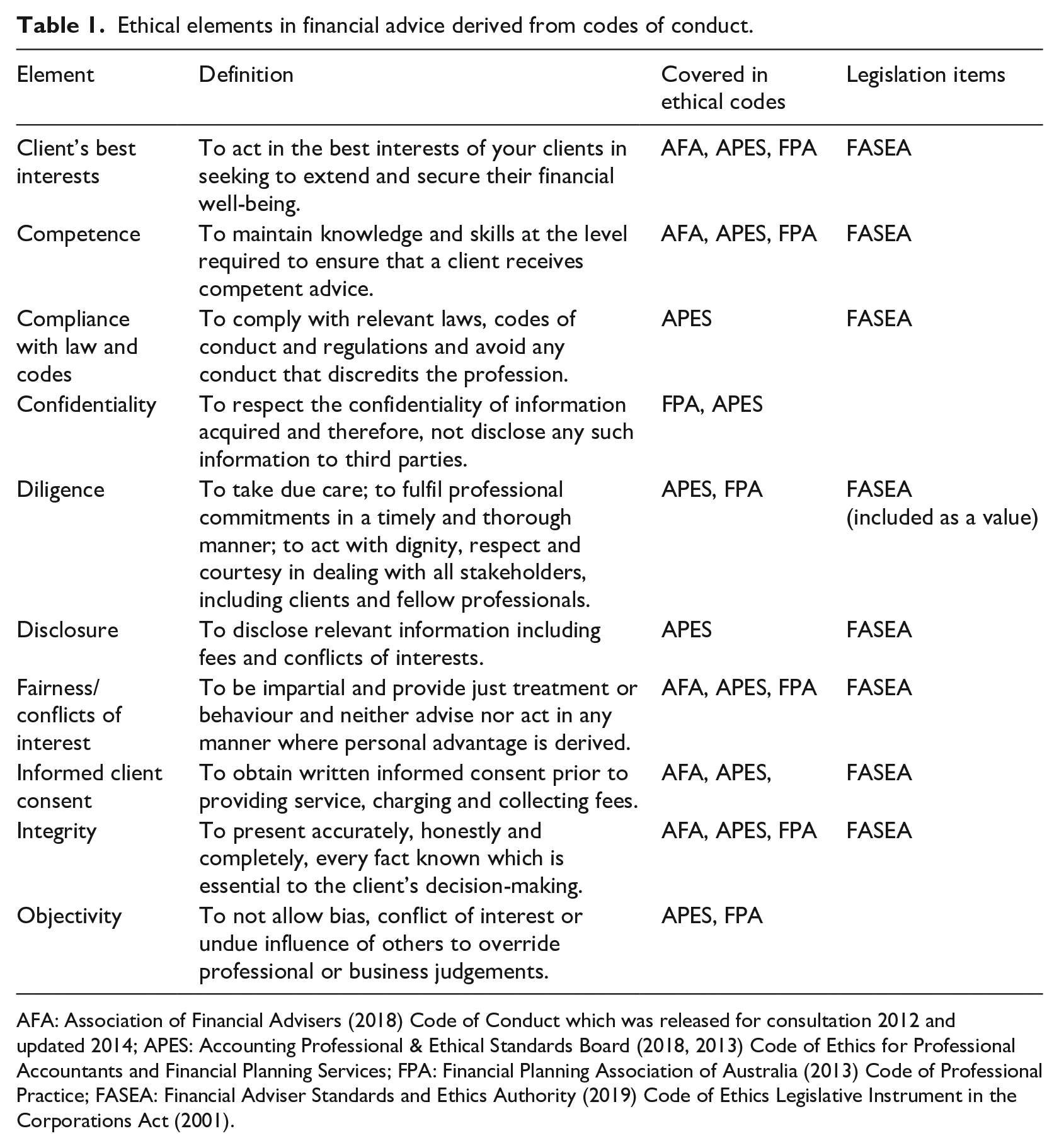

At a broad level, we coded for the ethical element apparent in each decision. We use the term ‘ethical element’ to refer to key ethical concepts espoused by codes of ethics in financial planning. There were considerable overlaps between the content of these codes of ethics, so the codes were synthesised to develop common ethical elements. We do not use the term ‘ethical value’ because an ethical element is specific to financial planning, whereas values have generic applicability. Table 1 outlines the ethical elements, their definition and the relevant code of ethics and legislation. Missing from Table 1 is the term ‘professionalism’, defined as ‘being professional’. This element was omitted because it was vague. Professionalism could be applied to all ethical elements in the code, as ethics and professionalism are inherently linked (Bruhn and Asher, 2020).

Ethical elements in financial advice derived from codes of conduct.

AFA: Association of Financial Advisers (2018) Code of Conduct which was released for consultation 2012 and updated 2014; APES: Accounting Professional & Ethical Standards Board (2018, 2013) Code of Ethics for Professional Accountants and Financial Planning Services; FPA: Financial Planning Association of Australia (2013) Code of Professional Practice; FASEA: Financial Adviser Standards and Ethics Authority (2019) Code of Ethics Legislative Instrument in the Corporations Act (2001).

The second step involved creating a coding framework for specific conduct types because this allowed more specific analysis than the ethical elements. Conduct types were initially derived from academic literature and then generated from the data. Although there is a dearth of academic literature on this topic, the research by Smith (2009) was pertinent, as it contained a thorough review of the types of unethical behaviour detected in Australia. In addition to the academic literature, the research project used content analysis to generate conduct types from the data. The open-ended development of this framework involved reviewing 20 decisions from one ombudsman, the FOS; details on FOS are in Section 3.2. The researchers met to discuss these decisions and refine the coding framework. The process was repeated in two more pilot coding analysis sessions which involved applying the coding structure to another 15 FOS decisions and 10 FOS decisions.

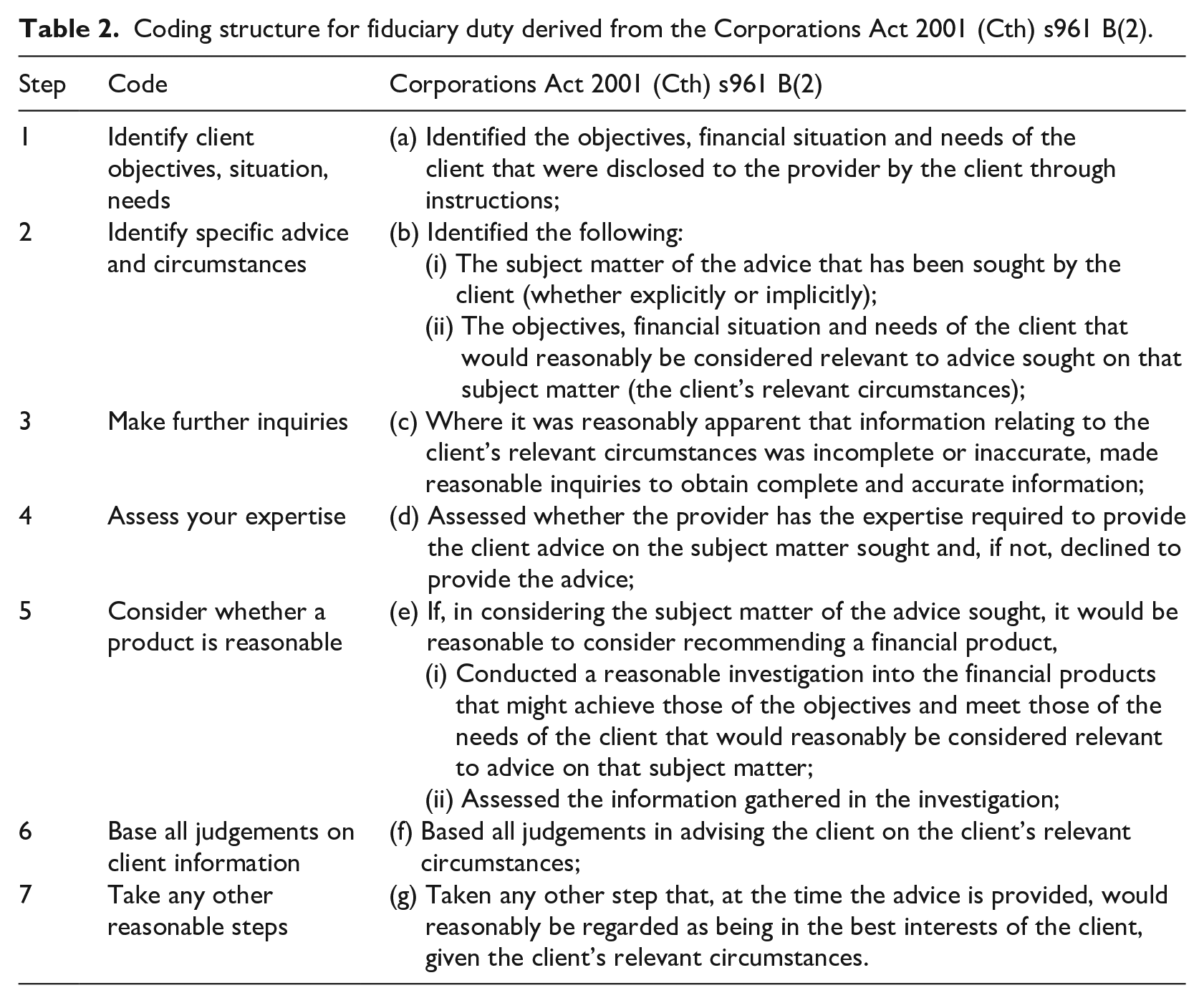

The final step of coding specifically relates to fiduciary duty. In Australia, fiduciary duty moved from being a duty to a legal requirement when it was included in the Corporations Act, 2001, s961B. This legislation outlines a seven-step process financial planners should undertake to fulfil their fiduciary duty. Industry participants refer to the seven steps as providing a ‘safe harbour’. Using these steps, seven codes were created to identify each step a financial planner should follow to achieve a fiduciary duty; these seven steps are outlined in Table 2 regarding the Corporations Act, 2001 (Cth) s961B.

Coding structure for fiduciary duty derived from the Corporations Act 2001 (Cth) s961 B(2).

ASIC has treated the ‘safe-harbour’ provisions as the only way to comply with a client’s best interest duty. This is evidenced by ASIC (2017, 2018) reports, where if the adviser’s client file did not demonstrate compliance with all seven safe harbouring steps, then the adviser had failed to comply with a client’s best interest duty. However, FASEA’s (2019) Code of Ethics Guidance asserts that the client’s best interest duty (Standard 2) in its code of ethics has a broader ethical obligation than contained in s961B of the Corporations Act. This broader duty is that the adviser must look more widely at the client’s best interests. FASEA’s Guidance (FASEA, 2019) states, ‘So, even if you follow the steps set out in section 961B of the Act, you may still not have complied with the duty under the Code [of ethics] to act in the client’s best interests’ (p. 14). FASEA’s involvement in regulating the client’s best interests duty is in doubt because Treasury (2020) announced that FASEA is being wound up, and the Financial Services and Credit Panel (FSCP) will take on this regulatory function.

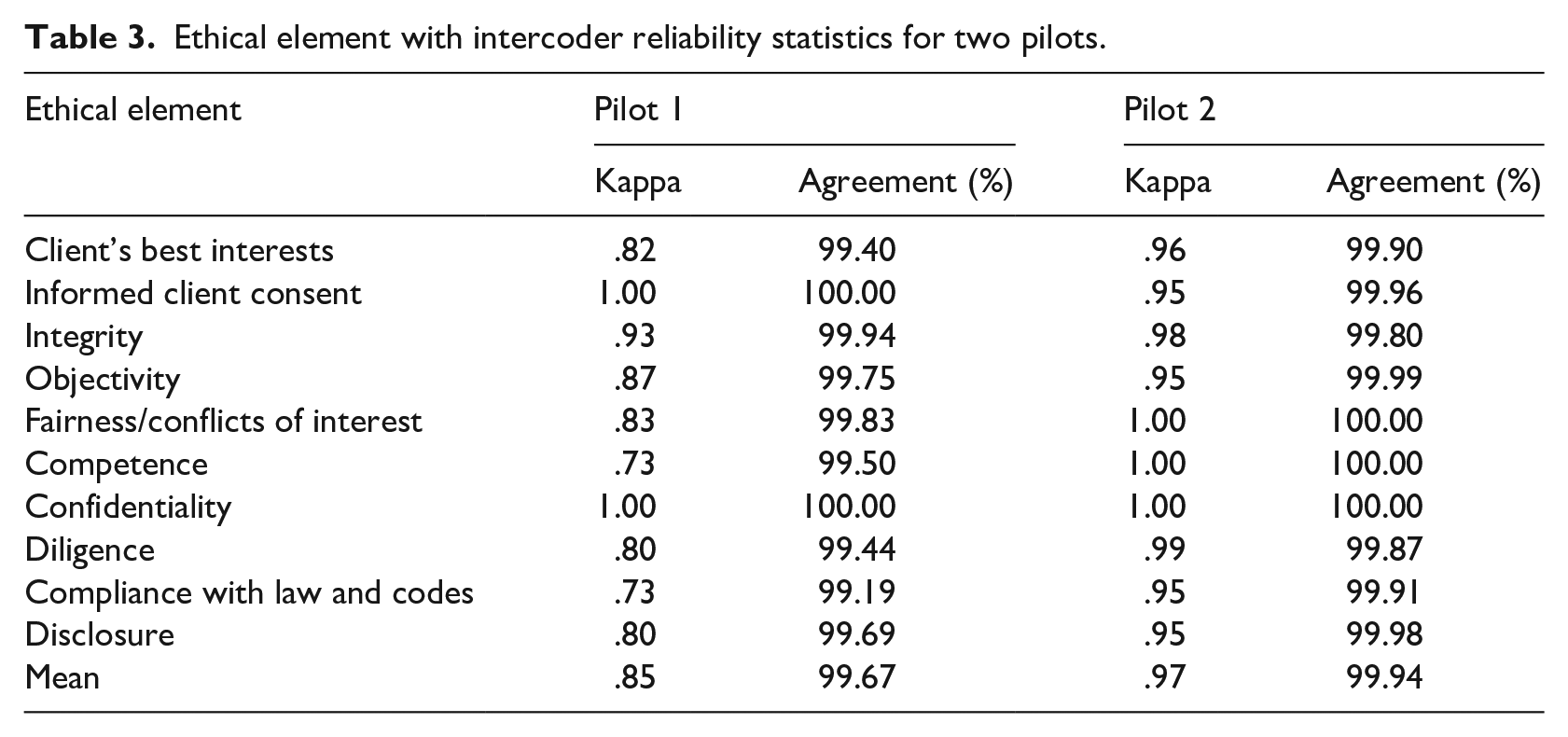

All coding was conducted using NVivo 12, and tests of reliability and accuracy of the two pilots were completed by running a coder-to-coder comparison. Table 3 outlines the Kappa reliability statistics and percentage of agreement from the two pilot trials for the ethical elements. It demonstrates an improvement in the Kappa score between the trials and an overall high level of reliability. The final coding structure for the study is available on request. Once the coding framework was established, the coding of the data was completed by one researcher. The ethical elements conduct type and fiduciary steps are not mutually exclusive. This meant there could be multiple ethical elements and conduct types in each case. After coding was completed, a second researcher conducted checks to establish the validity and reliability of the analysis. The second researcher reviewed the selection of text for each code to ensure accurate judgements were made. Any discrepancies between the coder and reviewer were discussed until an agreement could be made.

Ethical element with intercoder reliability statistics for two pilots.

3.2. Sampling and cluster analysis

There are no strict rules about the sample size necessary for cluster analysis with qualitative data. Siddiqui (2013) offers a comprehensive summary of sample size advice for quantitative statistical techniques, including cluster analysis, but concludes that no sample size guidelines exist for cluster analysis. Given this concern, our sample size should be considered relative to the number of variables. Hence, we consider whether the dimensionality is too high for the number of cases to be grouped, following Dolnicar (2002). Here, 212 ombudsman decisions were analysed and clustered with a dimensionality of 24 variables across ethical elements and codes of conduct. In comparison, Macia (2015) had a sample of 195 decisions across 59 variables. Thus, our sample of 212 decisions is sufficient to draw conclusions. In relation to the second research question, decisions relating to fiduciary duty were selected from the initial sample for further analysis (n = 54).

After the 212 decisions were coded for ethical elements and ethical conduct, cluster analysis was used to organise decisions into clusters based on their similarity. The benefit of cluster analysis is identifying patterns in qualitative data where numerous cases are studied (Macia, 2015). The cluster analysis was performed by constructing a table that listed each decision and identified the presence or absence of each ethical element and conduct. These data are binary data, where 1 represents when a code was present and 0 when it was absent. Since there are more 0s than there are 1s, these data are asymmetric.

A hierarchical clustering method was adopted as appropriate for qualitative binary data (Everitt et al., 2011; Macia, 2015). The data analysis was conducted using SPSS 27. The specific hierarchical clustering method used was the agglomerative approach, where each code starts with its own cluster, and clusters are compared using contingency tables to identify the similarity between them (Macia, 2015). It is important to adopt a clustering measure that suits the data; we adopted the Jaccard (1908) coefficient because it prioritises similarity over dissimilarity (Everitt et al., 2011). Specifically, it omits decisions where both decisions do not have a code (e.g. both have 0s) and focuses on decisions that do have a match (both or one decision has a 1). The linkage method adopted to classify decisions into clusters using the Jaccard measure is the group average linkage, which offers a compromise between other more extreme linkage methods and is relatively robust (for details, refer to Everitt et al., 2011: 77–79).

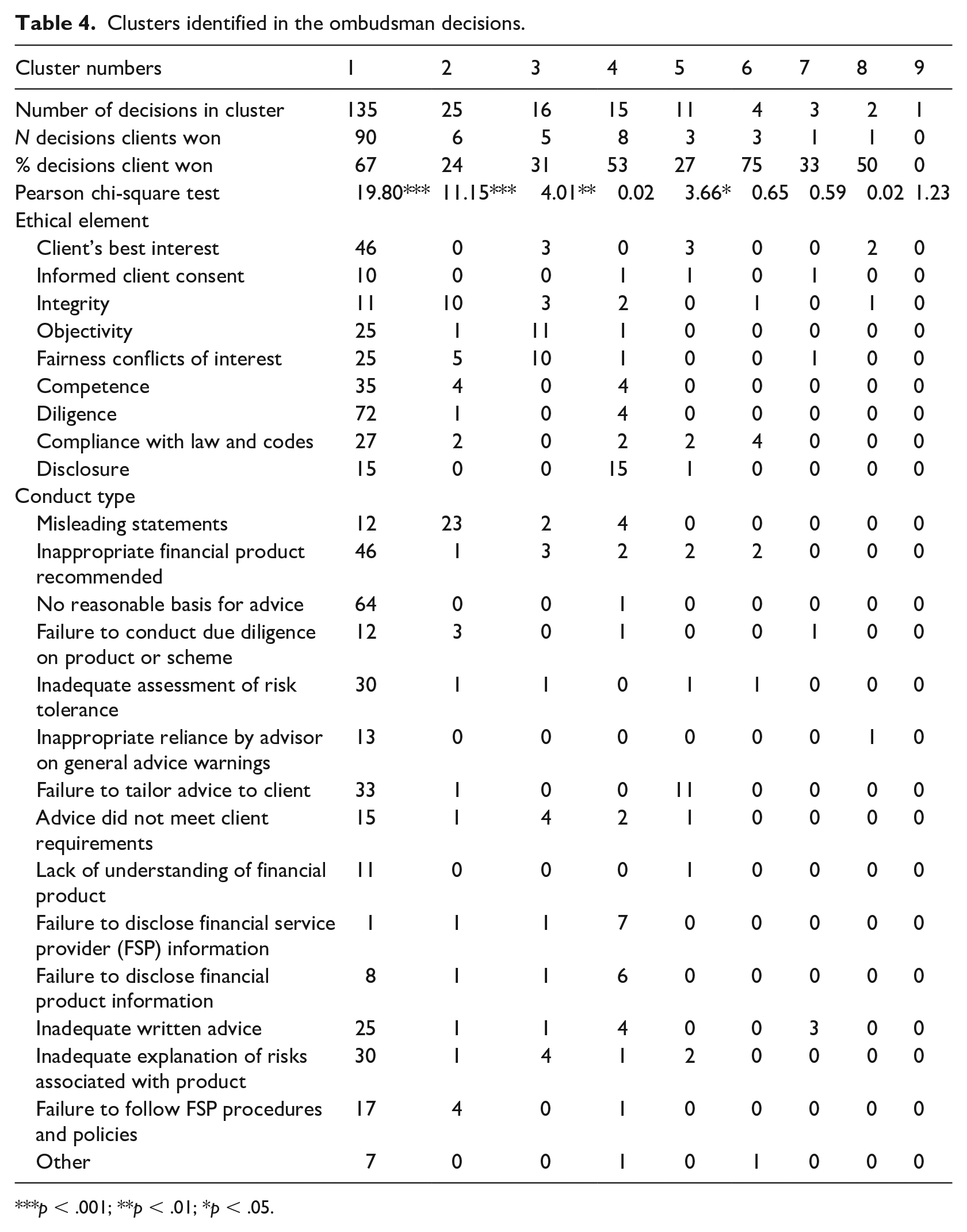

The appropriate number of clusters was identified by running the analysis using a range of clusters (from 3 to 15) using this method. There is no established number of clusters research should adopt; instead, researchers should investigate the data to make sense of how clusters are formed in relation to the codes in the data (Macia, 2015). Through an iterative process of analysing the qualitative data to ascertain whether the clustering made coherent structures, nine clusters were identified as optimal for these data. It grouped 135 decisions into one large cluster and created eight other distinct clusters. Adopting more clusters separated this large cluster and created differences that were not supported in the qualitative data. Adopting fewer clusters combined unrelated decisions into this large cluster.

Table 4 shows the nine clusters arranged by the number of cases in each cluster and how the ethical elements and conduct types are allocated to clusters. Clusters 1–4 were analysed to show what they illustrate relative to financial advice (see next section). Cluster 1 contains the most cases of the clusters and is characterised by two ethics elements: diligence and client’s best interest, and one conduct: no reasonable basis for the advice was provided. Cluster 2 focuses on misleading statements, Cluster 3 is objectivity and integrity and finally, Cluster 4 focuses on disclosure. Clusters 5–9 were not analysed, as the number of cases was deemed too small to reach meaningful conclusions.

Clusters identified in the ombudsman decisions.

p < .001; **p < .01; *p < .05.

4. Results

4.1. Descriptive results

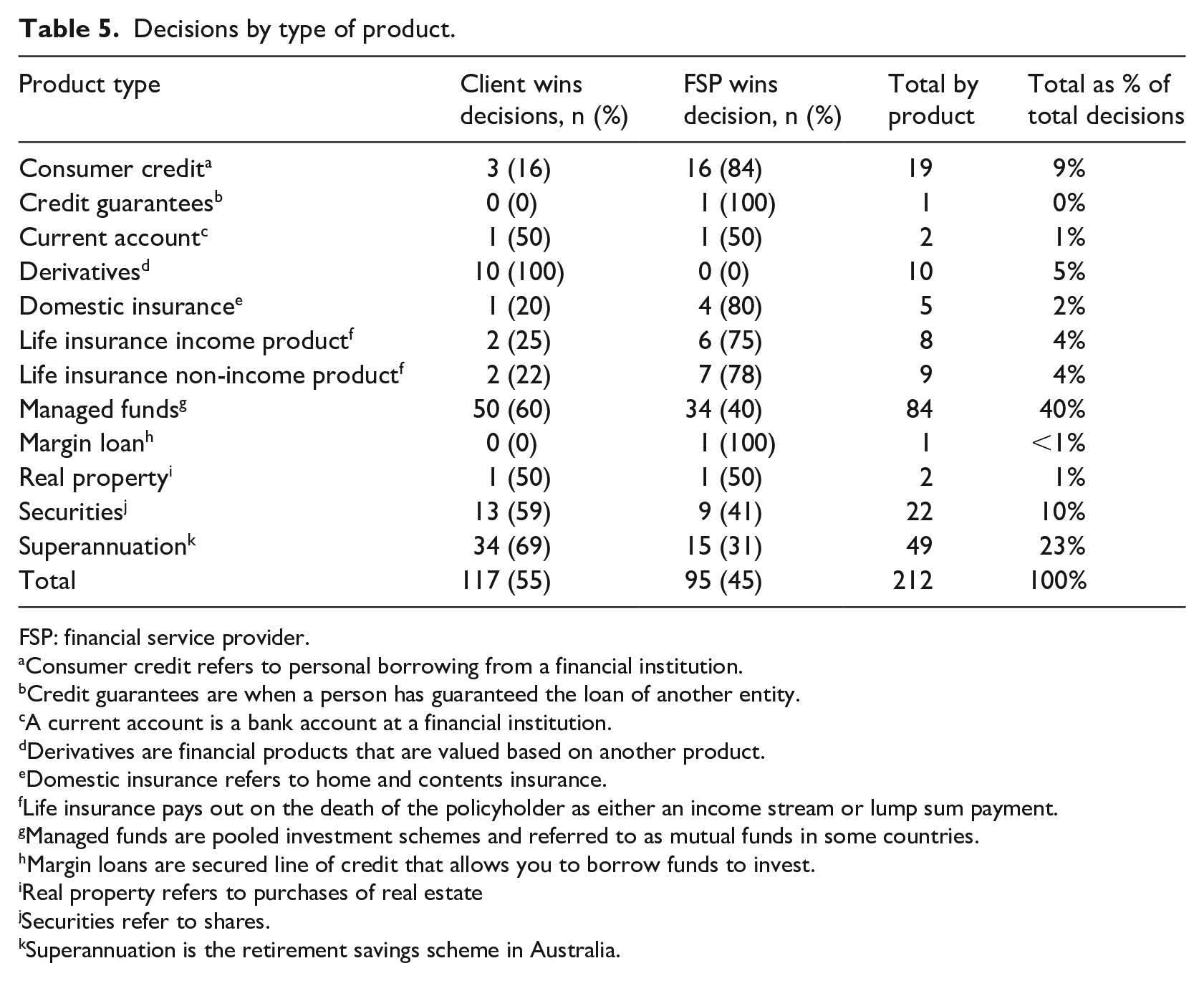

Table 5 presents an overview of these results, which show that clients win 55% of decisions, and the FSP wins 45%. This indicates a slight advantage to clients when complaints are elevated to this level. The mean value of settlement awarded to a client was US$91,269.80 AUD, the median value was US$51,417.20 AUD and the standard deviation was US$96,480. The value of the settlements is positively skewed, with a few settlements valued above the mean and the majority below it. Table 5 splits decisions depending on product type and by whether the client or FSP won the case. The two most common products represented in the cases were managed funds (40%) and superannuation (23%), which constitute slightly under two-thirds of all decisions. For 2016–2017, it was estimated that revenue in the financial planning industry was derived from the following areas: one-third relates to retirement and superannuation, one-quarter relates to loan and investment advice, one-fifth relates to self-managed superannuation funds, one-tenth relates to tax advice and one-tenth relates to other activities (Commonwealth of Australia, 2018). A major difference between the complaint decision data in this study and the industry revenue data is the high amount of investment products (managed funds, securities, derivatives, real property and margin loans), which constitute over half of the data. This is not as prevalent in the industry-wide data, even if these products are classified in the ‘retirement and superannuation’ category.

Decisions by type of product.

FSP: financial service provider.

Consumer credit refers to personal borrowing from a financial institution.

Credit guarantees are when a person has guaranteed the loan of another entity.

A current account is a bank account at a financial institution.

Derivatives are financial products that are valued based on another product.

Domestic insurance refers to home and contents insurance.

Life insurance pays out on the death of the policyholder as either an income stream or lump sum payment.

Managed funds are pooled investment schemes and referred to as mutual funds in some countries.

Margin loans are secured line of credit that allows you to borrow funds to invest.

Real property refers to purchases of real estate

Securities refer to shares.

Superannuation is the retirement savings scheme in Australia.

There are some interesting insights regarding the percentage of decisions awarded to clients across product type. First, the percentage of decisions won by clients is high when the products are derivatives (100%), superannuation (69%), managed funds (60%) and securities (59%) in comparison with the overall percentage (55%). Overall, these products are higher risk investment products than most other product types (excluding margin loans). FSPs are more likely to be successful in decisions where the products are not investment related and less risky such as consumer credit (84%), insurance products – domestic (80%), life income (75%) and life – non-income based (78%). When investment products are high risk, the client is more likely to win the decision than the FSP.

4.2. Analysis of clusters

4.2.1 Cluster 1: diligence, client’s best interest and no reasonable basis for advice

Cluster 1 contains 135 out of 212 decisions; clients win 67% of these cases, and this is higher than the average win percentage of 55 at a statistically significant level (χ2 = 19.80, df = 1, N = 212, p < .001). This cluster is characterised by a high proportion of decisions involving the ethical elements diligence and client’s best interest and conduct type no reasonable basis for advice.

Diligence. Here we analyse how a lack of diligence manifests in financial planning misconduct cases. In this research, we define diligence as having three inter-related elements: taking due care; fulfilling professional commitments in a timely and thorough manner; and acting with dignity, respect and courtesy in dealing with all stakeholders, including clients and fellow professionals. The first two elements of diligence occurred in the decisions. The first finding regarding diligence is that financial planners were not taking due care. Case 255263 typified this, where the ombudsman found that the financial planner ‘failed to meet its duty to provide advice in response to Ms P’s requests’. Other cases illustrated that advice provided was not timely, such as a ‘delay of more than six months before the adviser provided specific share and investment recommendations’ (Case 407625). There were also situations where clients expected advice, but the financial planner had reasons for not providing advice, such as when the clients stopped paying the ongoing advice fee.

A second aspect regarding lack of diligence is where the financial planner did not complete all facets of the work with thoroughness. The financial planner provided advice but failed to complete the necessary tasks required to form that advice. This is illustrated in a case where a financial planner recommended that a client purchase an investment property using their superannuation (retirement) funds, but the ombudsman found that The SOA (statement of advice) contained no cash flow projections and did not stress test the strategy for various possibilities such as:

Periods where the property may be untenanted

Interest rates increasing

One of the applicants becoming unemployed and therefore not contributing to superannuation. Case 477767

In other situations, financial planners provided advice and completed the necessary facets of their work but made significant errors in conducting those tasks. The ombudsman could see these errors, referred to as factual errors, in the adviser’s notes. This quote illustrates how diligence did not occur when providing financial advice on mortgages to a client: Reasonable budgeting for a one-income family with 2-3 dependants living in Sydney would have shown that the repayments were not viable. Case 326089

Client’s best interest. While Cluster 1 contains decisions on 72 cases with diligence as an ethical element, it also contains 46 cases with the client’s best interest as an ethical element. Here the interconnectedness of these themes is explored. Situations where a client’s circumstances were not ascertained show a lack of diligence by the financial planner and a deficit in the client’s best interest element. When the client’s circumstances are unknown to the financial planner, it is difficult for the adviser to meet their responsibilities as a fiduciary (refer Section 4.2.5 for further analysis on fiduciary duty). The following quote shows how a financial planner has not ascertained the client’s information to act in their best interest: In all of the circumstances, it would have been appropriate for the adviser to insist on the wife’s participation in the advice process and to obtain information from her about her relevant personal circumstances. Case 332797

This quote also suggests that the financial planner was not acting with dignity and respect towards the wife’s involvement in decision-making. In other situations, financial planners have ascertained but not carefully considered a client’s circumstances when providing advice. Consider this quote from a decision where a financial planner advised a client to borrow money to invest: SOA 1 and SOA 2 did not provide any analysis of the Applicant’s capacity to service the cost of the increased debt, despite one of their stated objectives being to reduce their level of borrowings. Case 301430

No reasonable basis for advice. There is also overlap between the no reasonable basis for advice conduct and the ethical elements diligence and client’s best interest. In the first cluster, there are 64 decisions where the code no reasonable basis for advice occurred; this shows the overlap between these concepts. Reasonable basis for financial advice covers the client’s intentions and willingness to accept risk. Thus, a frequent failing for not having a reasonable basis for advice was that the client’s objectives and risk profile were either not ascertained or considered, as highlighted in these quotes: The FSP has failed to provide documents (such as a fact find) to show the adviser made reasonable enquiries about the applicants’ circumstances and risk appetite. The FSP provided an extract of three pages from an SOA which only sets out the recommendations and the applicants’ signed authority to proceed. No information has been provided to show the basis for the adviser’s recommendations. Case 448102 There is no evidence to show Mr RP considered the applicant’s goals and objectives or his risk tolerance. Case 435068

The consequence of poor diligence and not acting in a client’s best interests is that clients receive an inappropriate financial product recommendation. This is a common theme in Cluster 1, where 34% of cases involved the code inappropriate products. A typical example would be where a high-risk product was recommended to a client with a low risk tolerance. Consider this quote: The Applicants and the SMSF (self-managed super fund) were balanced investors. The WI portfolio was chosen on Mr R’s advice. That advice was inappropriate because the proportion of growth investments chosen was too high. Case 347397

An inference of these findings questions why the financial planner is recommending an inappropriate product. While we did not specifically research the motivations for conflicts of interest, our findings suggest that they exist in this industry. On one hand, financial planners provide clients with the information they need, and on the other hand, financial planners sell products for financial product providers. The prominence of no reasonable basis for advice suggests that balancing client and corporation interests is an area of concern for this industry. Future research could investigate conflicts of interest further; it an essential issue for financial planning, as it professionalises and addresses ethical concerns (Bruhn and Asher, 2020).

4.2.2 Cluster 2: misleading statements

Cluster 2 shows a distinct difference from Cluster 1, where clients won 24% of the decisions, which is less than the other decisions at a statistically significant level (χ2 = 11.15, df = 1, N = 212, p = .001). The cluster is also characterised by the conduct of misleading statements. This suggests an issue with communication between financial planners and clients, where clients interpret information differently than financial planners intended it. Furthermore, evidence shows that it is difficult for clients to prove a misleading statement if the communication was made orally and not documented. This is illustrated by the quote: The Applicant says the FSP had verbally pre-approved finance to purchase a second property but then declined it . . . The information available does not show that the FSP misled the Applicant that Loan 2 would be granted. Case 383730

However, other instances showed that clients interpreted written communication as misleading, but the financial planner and ombudsman did not. Consider this quote: I therefore do not accept that the Website was misleading in the manner suggested by the Applicants. Case 379107

4.2.3 Objectivity, fairness and conflicts of interest

Cluster 3 is like Cluster 2, in that clients are less likely to win these cases (χ2 = 4.01, df = 1, N = 212, p < .01). In this cluster, two-thirds of the decisions pertain to the ethical elements of objectivity or fairness/conflicts of interest. These two elements are related where fairness/conflicts of interest refer to preventing personal gain from influencing financial advice. Objectivity includes conflicts of interest but also other bias and undue influence that may occur when providing financial advice. This cluster contained situations where a financial planner appeared to be impelling a client into a course of action. Some of this influence is unwarranted, such as ‘forcing’ a client to sign documentation: The Applicant says that the FSP ‘forced’ him to sign the varied loan contracts such that he signed under duress. Case 365522

Some cases showed that perceived or actual conflicts of interest influenced the adviser’s coercion: The applicant maintains that this demonstrates excessive trading and that Mr W ‘bombarded’ her with suggestions for investments. She has claimed that his motivation in doing so was for personal profit, without consideration to her best interests. Case 414519

In other decisions, particularly where the client lost the decision, it is evident that the financial adviser had a different opinion. The financial adviser did not follow the client’s wishes and distanced themselves from the client’s stipulations after considering them. The ombudsman agreed with this approach. For example, one client believed they should have invested in a product, but the ombudsman found the following: The adviser fulfilled his obligations to understand the Investec product and, on considering the objectives of the Applicants, advised against investing in it. Case 332991

4.2.4 Disclosure

Cluster 4 is the final cluster analysed and is notable due to all the cases involving the ethical element disclosure. Disclosure also occurred in Cluster 1, where the disclosure often related to providing information about the risks involved with the recommendation and explanations of those risks. This is in line with the client’s best interest element in Cluster 1, where the decisions pertain to not providing advice specific to the client’s needs. However, Cluster 4’s analysis of disclosure is related to information about the financial product or the financial planner’s services, relationships or fees. As an example, consider this quote regarding selective disclosure: The adviser told the Applicants about benefits of the insurer’s policies. The adviser did not tell them the FSP and the insurer were related companies. Case ID 390100

4.2.5 Fiduciary duty analysis

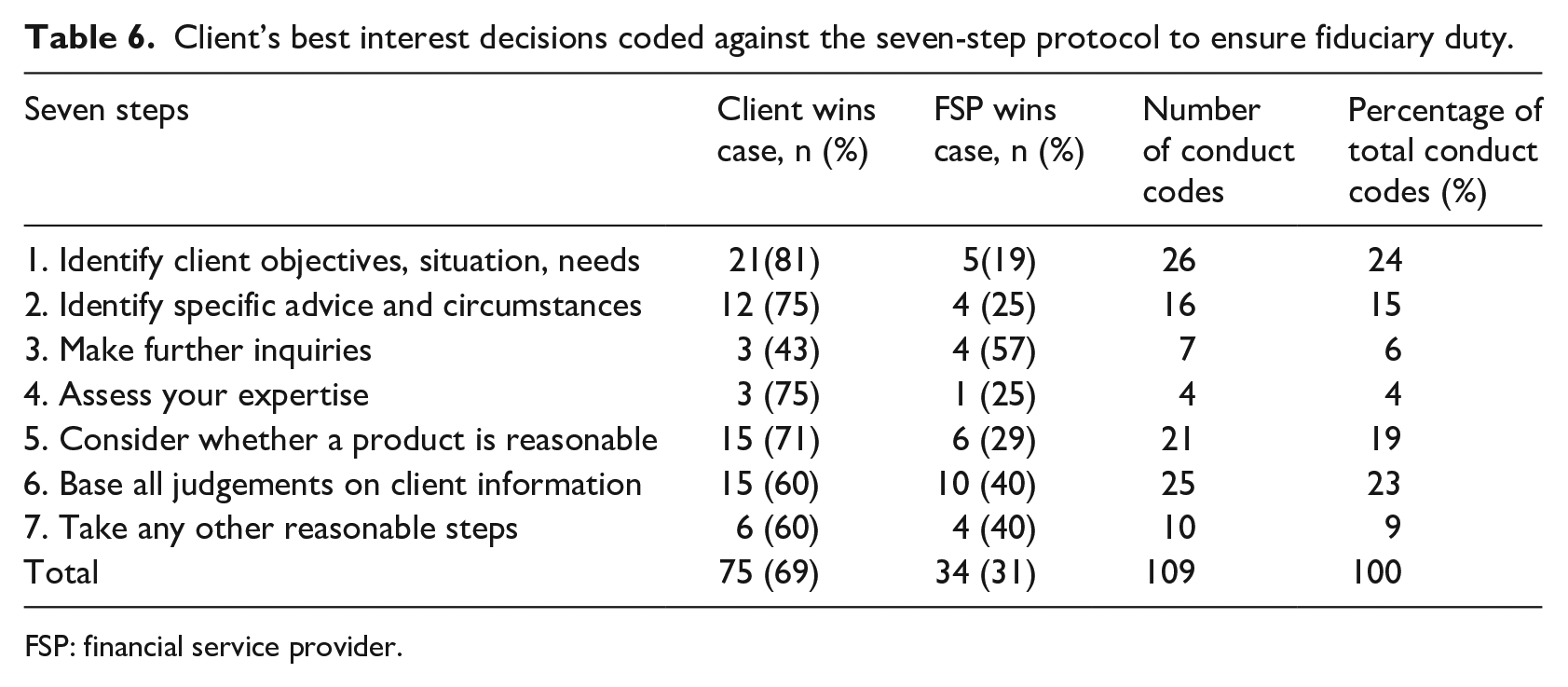

In this section, decisions that contained the client’s best interest element (n = 54) were analysed further. The analysis was conducted separately from the previous cluster analysis and involved coding these decisions using the codes based on the seven-step process of fiduciary duty (refer Table 6). It should be noted that the codes are not mutually exclusive, so more than one code could arise in each case. The results presented in Table 6 highlight that three steps were often apparent in decisions that involved fiduciary duty. These are the following: Step 1 (identify a client’s objects, situation or needs), Step 5 (consider whether a product is reasonable) and/or Step 6 (base all judgements on client information). One of these three steps occurred in just under two-thirds of the decisions, but Steps 1 and 6 are inherently related. That is, if a financial planner did not ascertain the client’s circumstances properly, then it is difficult for them to base their recommendations on this information. These two steps highlight the importance of communication between a financial planner and a client because ascertaining a client’s objectives, situation and needs derives from client interaction. The adverse finding for financial planners in relation to Step 5 may stem from a financial planner having a conflict of interest to recommend a product as required by their employer, rather than by the client.

Client’s best interest decisions coded against the seven-step protocol to ensure fiduciary duty.

FSP: financial service provider.

5. Discussion and policy implications

This article investigates misconduct in financial planning to understand the ethical elements and types of conduct in this industry. The Australian financial planning industry has been marred by scandals and has undergone significant parliamentary investigation and regulatory reform. Two methods used to build trust in financial planners have been the use of codes of ethics and a protocol to ensure that financial planners adhere to their fiduciary duty. Codes of ethics serve as a cornerstone in developing a profession (Abbott, 1983), act as a mission statement to communicate quality assurance and promises of service, and as guides for the public (Mackay, 2011). In addition, codes of ethics can increase clients’ trust in that profession (Bonvin and Dembinski, 2002). However, the creation of a code of ethics alone cannot create trust in a profession. According to Brien (1998), a culture of ethics must be cultivated in individuals within the profession. Schwartz (2013) and Statler and Oliver (2016) argue that alongside a code, there needs to be information and sensemaking by the individuals in a profession about what the code means for a code to be effective. In financial planning, there is a limited amount of knowledge about the ethical issues within this industry, making it difficult for sensemaking and cultivation of ethics to occur.

Our first finding comes from the descriptive analysis, where we find a prominence of investments (including managed funds, securities and derivatives) associated with over half of the decisions in the dataset. This is not so prevalent in the industry-wide data. The Australian financial planning industry draws one-third of its revenue from retirement and superannuation advice, one-quarter from loan and investment advice and one-fifth from self-managed superannuation funds (Commonwealth of Australia, 2018). In addition to this disparity, when the products being recommended were high-risk products, such as derivatives, managed funds or securities, the client was much more likely to win the decision than the financial planner. This highlights a need for the financial planning industry to address ethics in investments, particularly high-risk investments.

We used cluster analysis to categorise decisions based on the commonality between them in terms of ethical elements and conduct types. The cluster analysis identified nine clusters, but one large cluster contained over half of the decisions, and clients were more likely to win these decisions. The largest cluster was characterised by two ethical elements: diligence and client’s best interest, and the conduct type no reasonable basis for advice. Both elements present challenges for restoring trust in the financial planning industry. Diligence illustrated that financial planners were not performing the tasks to the level required to give reliable financial advice. The lack of diligence observed in the cases ranged from the extreme of not providing advice to a smaller mistake of incorrect analysis when providing financial advice. The frequency with which diligence occurred in our research links with the fee-for-no-service scandal where financial institutions were charging clients but not conducting the services paid for (Hayne, 2019).

A lack of diligence can occur due to factors at the individual, organisational or industry level or a combination of all three. For example, a financial planner could underestimate the time required to professionally complete work; organisations could encourage financial planners to attract new clients (revenue) rather than work diligently for existing clients; and the industry requirements (disclosure, record keeping) could be excessive. A lack of diligence is problematic for rebuilding trust in the financial planning industry because it directly impedes reliability, which is an essential aspect of trust (Ahmed et al., 2020; Cull and Sloan, 2016). Cull and Sloan (2016) also identify that client vulnerability is a characteristic of trust in financial planning, as clients have limited knowledge or ability to make a financial decision. A financial planner who fails to diligently provide accurate financial advice exacerbates trust in vulnerable clients who most require it.

Diligence is also related to acting in a client’s best interest, where financial planners did not consider the client’s circumstances or risk profile when providing financial advice. Thus, the financial planner could not prioritise a client’s best interest because the client’s interests are either unknown or not used to form the basis of advice. Consequently, a conduct type most frequently occurring in this large cluster was that there was no reasonable basis for the advice. This relates to the application of fiduciary duty in financial services (Boatright, 2000). Research has shown that prioritising a client’s best interest is an essential aspect of trust (Cull and Sloan, 2016) and that clients largely do trust their financial planners (Bruhn, 2019a, 2019b; Calcagno et al., 2017). However, conflicts of interest are common in financial planning, where financial institutions that employ financial planners have interests that are not always compatible with the client’s best interest duty (Ahmed et al., 2020; Richards and Morton, 2020). Our research implies that the occurrence of diligence and fiduciary duty in misconduct contradict the financial planning industry’s goal of building trust.

AFS legislation has attempted to resolve the issue of conflicts of interest and improve trust by having financial planners follow a seven-step fiduciary duty protocol (s961B Batten and Pearson, 2013; Corporations Act, 2001). Our research used this protocol as a coding framework to investigate the steps where breaches in fiduciary duty occurred in a financial planner’s misconduct. We found that the breaches occurred in three areas: identifying the client’s circumstances, basing judgement on client information and considering whether it is reasonable to recommend a product. The first two reasons are inherently related because it is impossible to base judgements on client circumstances if those circumstances are not ascertained. It points towards communication being an essential part of fiduciary duty that needs to be focused on; financial planners require communication skills and effective data-gathering techniques with clients to build the knowledge required to act as a fiduciary. They then need to base advice solely on this information.

The second and third clusters involved decisions where clients were less likely to win. Cluster 2 was characterised by conduct involving misleading statements and Cluster 3 by the ethical elements of objectivity and fairness/conflicts of interest. The themes in the clusters and the low win percentage for clients could imply that these topics are hard to prove in an ombudsman decision. However, they could also imply a gap between the client’s expectations and the financial planner’s services. In Cluster 2, it seems clients believe they are being misled, and in Cluster 3, they believe the financial planner is conflicted and not being impartial. Overall, these results imply that a breakdown in client expectations has occurred and that for the financial planning industry to improve trust, the communication of expectations needs to be improved.

Important policy implications can be drawn from the results of this study. From a policy perspective, the findings of this research will be useful to AFS licensees, financial planners, professional bodies and regulators. The prevalence of investment-based products in client complaints, particularly high-risk investment products, highlights a clear need for the financial services industry to educate financial planners on ethics around high-risk investments. In addition, high-risk products are more likely to result in a loss for a client, increase the chance of client dissatisfaction and lead to consumer complaints at an ombudsman service. This study highlighted that the ethical elements diligence and fiduciary duty were the most common, and these elements were synthesised from relevant codes of ethics. From an industry-level perspective, there is a need to focus on training in skills and behaviours related to these areas (such as how to provide assiduous, conscientious financial advice with attention to detail). There is also a need to address how diligence pertains to a client’s best interest. In the seven-step protocol of fiduciary duty, a step often impeded was failing to identify a client’s objectives, situation and needs. We contend that this occurs due to poor communication and information gathering in financial planning. Have financial planners taken sufficient time to understand their clients’ situation and objectives, or do they lack the skills to extract this information? Our research suggests that the lack of communication is a common theme arising from many of the decisions analysed.

Our research highlights the need for future research in this area. Under FASEA, financial planning has increased the educational requirements and training in ethics. Future research could investigate how these changes have changed the provision of financial advice and whether this has resulted in improved financial outcomes for consumers. In addition, financial planning is undergoing a process of professionalisation. Research is needed on the influences on professionalisation and how these relate to the ethical concerns raised in our research, including client’s best interest, diligence, conflicts of interest and disclosure. Finally, our research also has education implications where financial planning education could focus on the issues we address and use ombudsman decisions as case studies. Likewise, existing financial planners undertaking professional development could benefit from this research as it highlights areas to focus on.

6. Conclusion

The financial planning industry has been plagued by scandals that highlight the significance of unethical behaviour among some financial planners. Despite the many laws and ethical codes of conduct that guide how a financial planner should act, the industry is still beset by misconduct. This study investigated the practical aspect of ethics in financial planning through an in-depth analysis of recent financial ombudsman decisions to discover the types of misconduct found. Instances of misconduct were measured against ethical elements in financial advice with reference to the types of conduct involved and the fiduciary duty of financial planners. The findings contribute to an emerging field of research on ethics in financial planning (Chen and Richardson, 2018; Cull and Bowyer, 2017).

This study has potential limitations. First, this study is based on content analysis of financial ombudsman decisions that represent only a sample of all decisions. Prior to complaints being reviewed by an ombudsman, they may have been through several stages of a financial firm’s internal dispute resolution (IDR) process. This study has not looked at IDR decisions and may be subject to sample selection bias. IDR data are not publicly available, but ASIC has public consultation on new standards to make firms’ complaint-handling performance transparent (ASIC, 2019). The publication of these data may provide an opportunity for future research. Another limitation is that we research misconduct cases only. The findings cannot be generalised to all financial planning. Further, it should be noted that this research only covered the situation where poor financial advice has been either perceived or occurred. Finally, a limitation of this research is that it is restricted to 5 years of data (2013–2018) and 212 cases. As the financial planning industry evolves, the content of ombudsman decisions will likely change with it.

Footnotes

Final transcript accepted 14 May 2021 by Millicent Chang (AE Finance).

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors would like to thank Financial Planning Education Committee (FPEC) for the financial support received to undertake this project.