Abstract

Drawing on a Gramscian Regulation Approach and Harvey’s accumulation by dispossession thesis, this article discusses the structural and hegemonic mechanisms of the neoliberal transformation of Sweden’s welfare sectors. Providing new longitudinal data on welfare retrenchment, corporate governance, wealth shares, and private economic power, the article further analyzes how the transformation of the Swedish post-war universal welfare model is related to class struggle and accumulation regime change in the Swedish economy. Following a decade-long countermobilization of Swedish capital and a severe economic crisis in the early 1990s, neoliberal economic common sense was cemented among social democratic policy elites that manifested itself in an institutionalized austerity polity, leading to a slow but steady dismantling of the Swedish welfare project. Roughly a fifth of employees in the three largest welfare sectors work in private welfare companies that generate tax-financed profits on politically created welfare markets. Welfare profits are in turn defended by a welfare–industrial complex and undergirded by a hegemonic bloc consisting of capital elites and sympathetic policymakers. In the virtual absence of vocal antihegemonic forces, many social democratic leaders have limited criticism against welfare profits throughout the last decades. On the contrary, austerity measures practiced by Swedish social democrats have thereto led to deteriorating social cohesion and spawned distrust among core social democratic voters.

Keywords

Introduction

Following the development of its post-war universal welfare model, Sweden is often perceived as the most equal country in the world regarding economic equality, access to welfare, and general living standards. Post-war welfare policy was guided by the exclusion of private interests from welfare services, universal and equal welfare services to all citizens, and democratic governance that resulted in the most egalitarian Western society in the post-war period. However, from the 1980s onward, the Swedish welfare model, and the Swedish economy at large, has undergone profound neoliberal changes (e.g. Baccaro & Pontusson 2016; Belfrage & Kallifatides 2018; Buendía & Palazuelos 2014; Hein et al. 2021; Ryner 2013; Svallfors & Tyllström 2019). Government spending has been cut, welfare services have been privatized, and stock listed companies now constitute a significant share of the welfare sector. Significantly, The Economist (2013) has noted Sweden’s notorious neoliberal welfare reforms. Despite being one of Europe’s richest economies, Sweden has had fewer hospital beds per capita than Greece, Italy, and Spain throughout the Covid-pandemic (OECD 2022).

This article further explores how the neoliberal transformation of the Swedish welfare model is related to class struggle, hegemonic strife, and long-term structural changes in the Swedish economy. Drawing on a Gramsci-inspired Regulation Approach (e.g. Aglietta 1979; Bieling 2014; Boyer 1990; Jessop 2013; Lipietz 1988) and Harvey’s (2005) accumulation by dispossession thesis, the article sheds light on the underlying mechanisms behind the increasing presence of private business activities in the welfare sector, the shrinkage of the public sector in relation to the private sector, and how the size and scope of welfare institutions have changed and been integrated into global financial circuits in recent decades. We highlight that the accumulation by dispossession of welfare assets is both undergirded by force, that is, the structural power of globalized and financialized capitalist structures, as well as consent in the Gramscian (2003) sense through the hegemonic status of neoliberal ideas in the realm of economic policymaking. More specifically, three coevolving mechanisms – one ideological and political, one economic or structural, and one hegemonic – have been at play in these processes. The ideological mechanism implies right-wing neoliberal governments on national, regional, and local levels that ideologically perceive privatizations of welfare institutions as an end in itself. The economic mechanism comprises economic crises and drawn-out recessions (including on the regional and municipality level) that exert downward pressures on tax income, which opens up new opportunities for capital to enter the recommodified welfare sector following privatizations (cf. Harvey 2003: 141). The third and last mechanism, neoliberal common sense, with its roots in the 1970’s crisis of Fordism, was cemented among social democratic elites in the last three decades under the perception that hostile globalized financial market forces hold policymakers hostage and render anything but public sector retrenchment futile (Brenton & Pierre 2017; Erixon 2015; Göteborgsposten 1995; Harvey 2014: 91; Jonung 1999: 67; Persson 1997: 43; Pierre 1999; Wolrath 1995: 3–4). During the concomitant emergence of a neoliberal hegemonic bloc and a private welfare-industrial complex throughout the 21st century, neoliberal common sense has contributed to the unwillingness among social democratic elites to mobilize voters and resources to counter welfare retrenchment and privatizations (Peck 2010). Instead, the social wage has deteriorated, unemployment has persisted above average OECD figures, while a significant amount of public financial net wealth has accumulated through excessive government debt amortization and public financial asset hoarding.

A number of scholars have contributed to important research on Swedish welfare reform. However, few have discerned the coevolution of structural and semiotic changes that have enabled this neoliberal transformation. Buendía and Palazuelos (2014) provide a valuable historical account from a structural lens, but they black-box the social-democratic party and its important role in the coproduction of hegemony. Likewise, Hort et al. (2019) neglect the impact of hegemony, semiotic mechanisms, and societal alliances when describing changes in the Swedish welfare sector. Other researchers overtly focus on ‘ideational power’ while downplaying material factors, including how structural changes in the domestic and global economy (i.e. accumulation regime change) alter the power resources and strategies for labor and capital. Svallfors and Tyllström (2019) downplay such structural factors to focus on how private interests defend their stakes in the welfare sector through political means. Selling (2021) likewise provides an idealistic account of welfare regime change by focusing on the ideational power of Swedish capital and its effect on policy. The ideological change in the Swedish social democratic party has been scrutinized by Ryner (2003, 2018) and Mudge (2018) among others, but welfare state change is often absent in such accounts. In contrast, apart from presenting a more thorough empirical testimony of Sweden’s neoliberal welfare transformation, we present a more holistic and historically sensitive account, weighing in material as well as constructivist aspects and their coevolutionary dynamics (Sum & Jessop 2013) when explaining welfare regime change.

Given the broad popular support for welfare institutions (Svallfors 1997), the high trust in public institutions, and its social democratic post-war legacy (in total, Social Democrats have been in government for 60 years since 1945), Sweden could be viewed as a least likely case for welfare regime change (Eckstein 2000). Most welfare studies focusing on Sweden conclude that it was around 1980 that the universal model was most comprehensive (SOU 1988:38). Thus, public and private sector sources of macroeconomic, wealth, and welfare statistics have been surveyed in this article between 1980 and 2020. Economic data are expressed in nominal values in the Swedish currency (SEK). In today’s currency, 10 SEK corresponds to approximately 1 Euro.

The next section presents the article’s theoretical approaches, which is followed by a historical account of the post-war class-compromise, and the Swedish universal welfare regime from a Regulation Approach. The subsequent section presents and analyzes empirical results on regulation regime changes, public sector retrenchment, and the transformation of the Swedish welfare model, which is followed by a concluding analysis.

A Gramscian Regulation Approach, the power mechanisms of capital, and accumulation by dispossession

According to the Regulation Approach (e.g. Aglietta 1979; Bieling 2014; Boyer 1990; Jessop 2013; Jessop & Sum 2006; Lipietz 1988), resting on Marxist and other heterodox economic foundations, the capitalist market economy is characterized by two ‘laws’ that are fundamentally tied to the historical formation of economic and social relations: class struggle between wage-earners and capitalists and competition between capitalists. The Regulation Approach analyzes the stability and changes in these relations through three institutionally crystallized modes of social organization that reflect the underlying balance of social forces: accumulation regimes, modes of regulation, and growth models. Accumulation regimes are stabilized modes of production, consumption, and remuneration that are reproduced through norms, habits, laws, and networks (Lipietz 1987: 14). Modes of regulation are ensembles of institutions, norms, organizational forms, and social networks that mutually support and temporarily stabilize accumulation regimes by smoothing social and economic contradictions inherent in the accumulation process. Finally, growth models are coherent combinations of modes of regulation and accumulation regimes (Sum & Jessop 2013: 246).

Taking a Gramscian view of the Regulation Approach, changes in modes of regulation, accumulation regimes, and growth models take place through shifting constellations of long-term societal alliances. Historical blocs imply the structural unity of a social formation as an outcome of the strength between different forces striving for hegemonic status (Jessop 2016: 106). Gramsci (2003) showed how historical blocs are created and consolidated through intellectual, moral/ethical, and political practices and how ethical–political practices coconstitute economic structures and give them legitimacy (Jessop 2016). Hegemonic blocs are understood as alliances where political agendas are articulated by and implemented to the advantage of certain social groups but are recognized to be in the general interest of society. Dominant fractions in a hegemonic bloc retain hegemony, that is exercises ideological (political, intellectual as well as moral) leadership as acknowledged by subaltern classes (Bieling 2013; Bieling et al. 2016; Jessop 2016). While integral hegemony implies a hegemonic order where large parts of consenting masses materially profit, minimal hegemony implies a state of affairs where public discontent increasingly amasses, but subaltern classes, and crucially the leaders that nominally represent then, are too weak and disorganized to perform or articulate any significant form of counterhegemonic visions or strategies (Cafruny & Ryner 2007: 143–144). Class domination rests on a combination of coercion and consent, where the latter is reified through the creation and diffusion of a hegemonic common sense (Sum & Jessop 2013: 206) as a ‘set of ideas that are taken for granted and accepted as unproblematic truth’ (Stahl 2021: 4) that constrains the perceived viability of alternative policies.

The ontological Strategic-Relational Approach (Jessop 2005; Sum & Jessop 2013) underlines the coevolution of structural change on the one hand and common sense and political strategies on the other hand. Different capitalist structures, whether Fordist, post-Fordist, or otherwise, are strategic in their form and favor some actors, identities, interests, agents, spatiotemporal horizons, and strategies over others in different spatiotemporal conjunctures. This does not imply that agency should be reduced to structures as action is both structured but also structuring, path-shaping as well as path-dependent (Jessop 2005; Ryner 2013; Sum & Jessop 2013). A Strategic-Relational Approach may be fruitful when discerning how social democratic third-wayism has evolved against the reinforced instrumental and structural power of capital under financialized neoliberal growth models. Instrumental power refers to a business sector’s political power, including lobbying resources. As states are dependent on capitalists for tax revenue, growth, and employment (Offe & Ronge 1975: 140; Przeworski & Wallerstein 1988), structural power ‘generally refers to the influence business has through their capacity to withdraw investment and thus reduce levels of funding, production and employment, affecting overall economic growth’ (Woll 2016). Concurrently, states are not neutral to social forces but ‘. . . “more open to capitalist influences and more readily mobilized for capitalist policies” rather than “equally accessible to all social forces and equally adaptable to all ends”’ (Jessop 1990: 147–148, cited by Milonakis et al. 2021: 498–499). Speaking in terms of the ‘augmented power mechanism’ (Trampusch & Fastenrath 2021) or the ‘augmented power resource approach’ (Svallfors & Tyllström 2019), a number of scholars argue that instrumental power reinforces structural power and vice versa (cf. Fairfield 2015; Woll 2016) with significant impact on the evolution and persistence of hegemony and neoliberal common sense.

As ‘[t]he general thrust of any capitalistic logic of power is not that territories should be held back from capitalist development, but that they should be continuously opened up’ (Harvey 2003: 139), integral to neoliberalized growth models is the ongoing accumulation by dispossession (Harvey 2003) where private capital accumulates by dispossessing the public sector of its assets. More specifically, accumulation by dispossession comprises four components: (1) privatization and commodification, (2) financialization, or the use of increasingly sophisticated financial markets as a tool for accumulation by dispossession (Harvey 2003: 147), (3) the creation and/or use of economic crises and recessions to further enhance accumulation by dispossession, and (4) the state and the international state system as key institutions in these processes (Harvey 2003: 145). A main feature of the finance-dominated accumulation regime is thus the invasion by private capital into spaces formerly occupied by the welfare state (Nölke et al. 2013: 212; Vercelli 2013: 40).

Welfare state expansion, the crisis of Fordism, and the formation of neoliberal common sense

After hostile industrial relations in the first decades of the century, labor and capital signed the Saltsjöbaden industrial peace agreement of 1938 that laid the post-war period based on mutual understanding rather than hostility. According to Korpi (2006: 188), instrumental to this historical compromise was the social democrat’s claim to governmental power in 1932, at the time understood as a long-term tenure that shifted the policy alternatives leftward and markedly decreased the power disadvantage of labor vis-a-vis capital. The dominance of the Social Democratic party, in government between the 1930s until 1976 and the majority of the years since then, lacks precedence in Europe, including in Scandinavia (Mjøset 1987: 417). The Saltsjöbaden agreement should be understood as a starting point of a Fordist historical bloc, a historical class compromise between two societal forces consisting of a social democratic labor movement holding governmental power and an internationally oriented politically organized Swedish capitalist class. Amid this power balance (Korpi 2006), capitalists accepted centralized wage negotiations, full employment, financial regulation, and welfare state expansion in exchange for retaining ownership and control of Sweden’s major industries (Johansson & Ekdahl 1996).

Following the social democratic four-decade-long claim to power, societal development in post-war Sweden was driven by a Fordist growth model akin to other Western states at the time, characterized by a combination of financial regulation, intensive and industrial accumulation, and a ‘monopolistic’ mode of regulation (Buendía & Palazuelos 2014; Erixon 1996). The industry-intensive accumulation regime was mutually reinforced by a regulating bureaucratic universal welfare state, social safety nets, reformist mass movements and parties, and the corporatist ‘Fordist compromise’ between capital and labor, with the state as a mediator of institutionalized conflicts and regulator of the financial system (Belfrage & Kallifatides 2018; Sjöberg & Dube 2014). Equally important for the various national Fordist growth models was that Keynesianism served as the economic theory for understanding, managing, and controlling economies and mitigating crises and social conflicts, hence stabilizing the reigning class compromise (Boyer 2000; Jessop 2013; Jessop & Sum 2006).

The Swedish welfare model was rapidly developed and embedded in the Fordist growth model in the post-war period by social democratic governments (Denvall et al. 2016; Esping-Andersen 1999; Olsen 1994; Olson 1990). According to Esping-Andersen (1990), the welfare models of Scandinavian countries were characterized as universal, implying a comparatively extensive public sector along with decommodification, that is, a situation where free market mechanisms and profit motives were prohibited. Decommodification was based on the argument that unequal welfare service provision would occur if market forces and private interests would govern. Democratic public sector governance, regulation of the private sector, and tax-based redistribution of welfare resources were considered essential for equal and universal access to welfare. Esping-Andersen (1990) also differentiated between two other welfare models, that is, the selective or means-tested/liberal model and the corporatist/conservative model. In the market-based welfare model exemplified by the United States, private actors provide services on welfare markets. Within this model, schools, health care, and elderly care are primarily run by private actors and often financed through commissions from the welfare recipients, viewed as ‘customers’. Social insurance is likewise distributed by private actors and paid by customers through fees (Esping-Andersen 1990, 1999; Greve 2007). In its heyday, the Swedish welfare state accomplished significant degrees of decommodification along four dimensions; full employment as an overarching political objective, housing as a social right, universal social insurance protection, and universal welfare services such as health care, child care, and elderly care.

Major opposition to the Fordist growth model originally stemmed from labor rather than capital. After two decades of the Fordist golden age, a ‘red wave’ formed internationally (Mjøset 1987) and also in Sweden in the late 1960s, where workers voiced critique over capitalist exploitation and alienation, Western imperialism (not least connected to the Vietnam War), and Taylorist work organization (Lipietz 1987) as well as gender inequality reproduced by the Swedish model. Amid decent gross domestic product (GDP) and productivity growth, this was articulated by a series of wild-cat strikes at mining and industrial sites in northern Sweden and Gothenburg in 1969 and the early 1970s. The red wave culminated when the social democratic trade union (LO) proposed collective capital accumulation through trade union-controlled employee funds in 1975, where 10%–20% of major companies’ profits would be transferred as stocks to democratically elected trade union funds each year. The aim was to counteract the concentration of private ownership and fortunes and to develop collective ownership and economic democracy (see Meidner et al. 1978). The proposal reinforced the Swedish capitalist class’ neoliberal counterattack led by the employers’ federation (SAF) and influenced by international neoliberal currents, which became a ‘hegemonic turning point’ in Swedish socio-political development through which the Fordist historical bloc came to dissolve (Högfeldt 2005; Sjöberg & Dube 2014). By 1976, SAF initiated a neoliberal ideological public campaign, directly undermined corporatist institutions, and formed a 100,000 strong ‘employers’ demonstration protesting the wage-earner funds’ proposal on 4 October 1981, that was repeated throughout the decade (Ahrne & Clement 1992: 471–474; Westerberg 2020).

Meanwhile, global Fordism was disrupted by decreasing overall profitability, several oil crises, labor unrest, and sociopolitical conflicts across Western capitalism throughout the 1970s (Hameiri 2020; Harvey 2005). The failure of Keynesian economic policies in the 1970s was soon replaced by the neoliberal mode of development, a willful intellectual, ideological, and political project pushed by capitalist elites (Neilson 2020). Amid one of the deepest nationwide recessions in the OECD, Swedish bourgeois governments (1976–1982) initially maintained full employment and welfare quality through expansionary Keynesian fiscal stimulus and active labor market policies. In the absence of an expected global economic boom, a period of ‘fumbling’ followed, characterized by incoherent sets of expansionary and austerity policies until the summer of 1980, whereafter the policy became more ardently austere (Mjøset 1987: 449). From then on, unemployment was allowed to rise following a reduction in public transfers and labor market expenditures. Keynesian economic thinking and especially Sweden’s vast public sector had by then been increasingly questioned by leading Swedish economists (Blyth 2001: 16; Erixon 2020: 6, 1; Korpi 2002; Mjøset 1987: 433; Ryner 2003: 162). Similar developments can be seen in several other North European economies (Andersson & Mjøset 1987: 238; Mjøset 1987: 420–422).

When the Social Democrats returned to power in 1982 after 6 years in opposition, strategically and ideologically weakened by the countermobilization of Swedish capital while inheriting a profitability crisis, losing export market shares, trade imbalances, and structural public deficits, they abandoned the original employee funds plan and embarked on a set of neoliberal policies that had become common sense in Northern Europe by the early 1980s (Andersson & Mjøsset 1987: 238; Erixon 2020: 6; Mjøset 1987: 420–422; Ryner 2003: 175–187). Based on supply-side economics, neo-mercantilism, and crowding out reasoning, the government intended to restore private sector profitability and improve net exports through currency devaluation; lowering labor ’s income share vis-a-vis capital; and shrinking the public sector through fiscal restraint. The government also preceded the financial deregulation initiated by the previous liberal-conservative government, which was done in a badly timed and executed manner, leading to a homegrown real-estate, banking, and currency crisis in the early 1990s (Englund 1999; Erixon 2015). The public bailout of the financial sector that followed sent public debt levels to new heights, turned full employment into mass unemployment (1.6% in 1990 to 8.2% in 1993), and paved new ground for neoliberal restructuring and serious attacks on Sweden’s universal welfare regime and its working and middle classes.

In what follows, accumulation regime change and data on wealth inequality, including the power of Sweden’s 15 major financial families, are presented in the next chapter. This is followed by an excursus on how neoliberal hegemony was cemented in the 1990s, which has enabled the accumulation by dispossession of the Swedish welfare sector assets. These two empirical chapters serve as a precursor to how Sweden’s welfare sector specifically has been commodified, including how collective agential forces are undergirding its continuous metamorphosis, antithetical to the post-war welfare regime that was based on decommodification.

Structural changes in regulation, ownership, and welfare, 1980 to 2020

Accumulation regime change, widening income and wealth inequality, and the 15 families

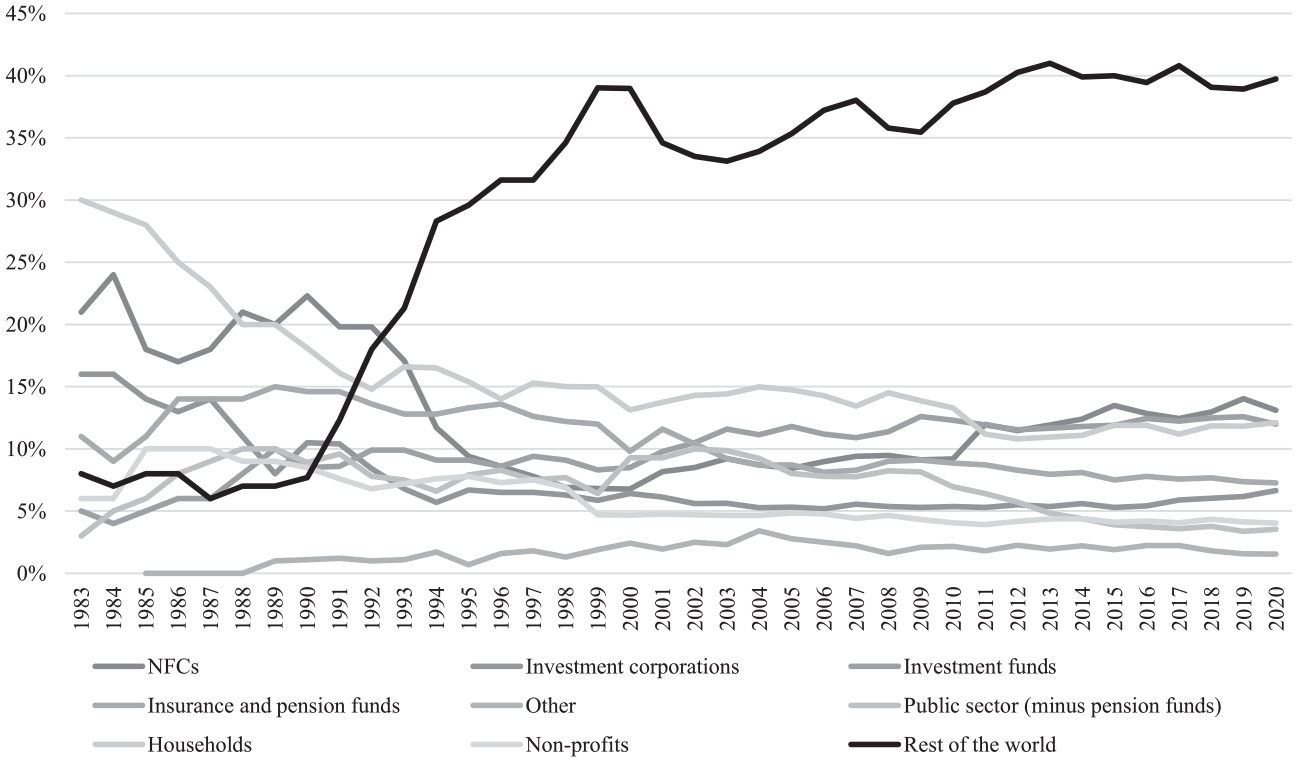

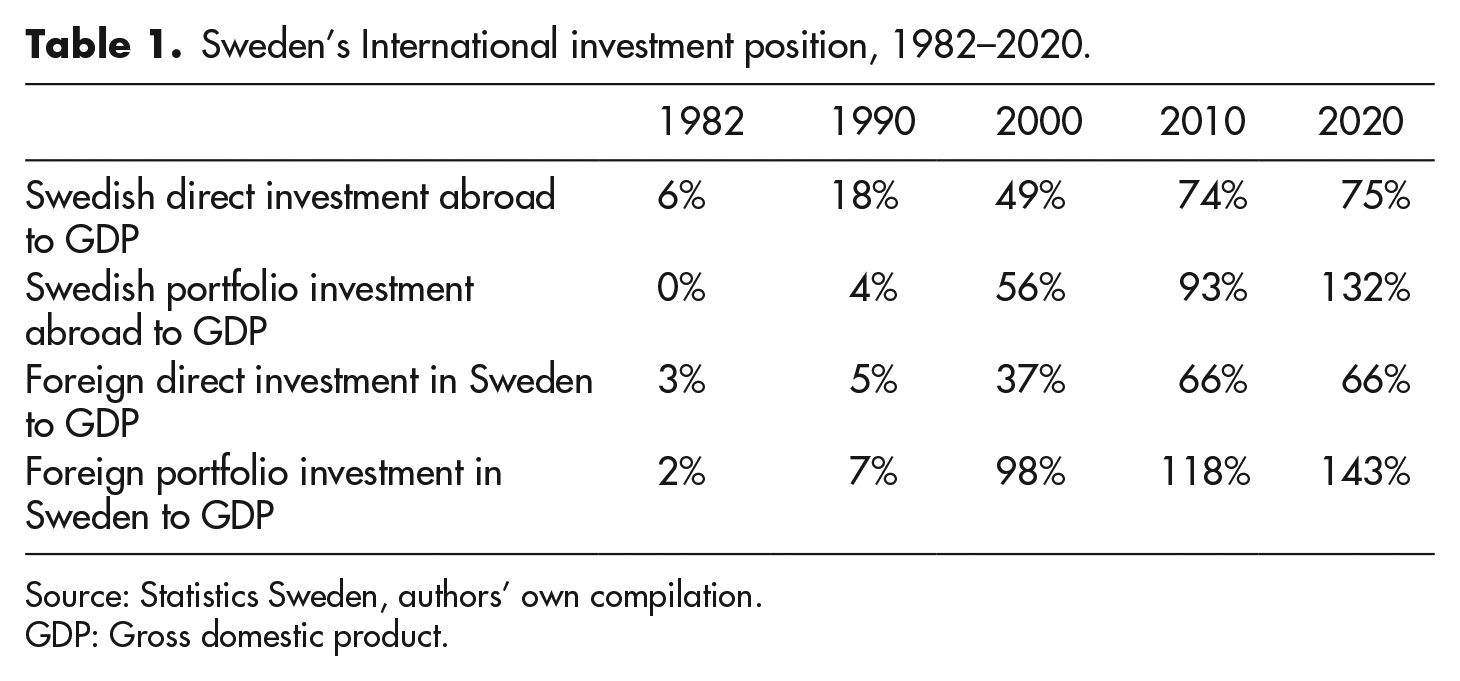

Financial market deregulation from the late 1970s coupled with the elimination of currency controls in 1989 quickly immersed Swedish industry into transnational ownership structures (Allelin et al. 2018a; Henrekson & Jakobsson 2008). Foreign ownership of publicly traded companies rapidly increased from 7% in 1990 to 40% in 2000 as indicated in Figure 1 and Table 1. Deregulation, liberalization, and political encouragement of households to invest in mutual funds from the late 1970s (Jonsson & Lounsbury 2004) also made dormant Swedish equity markets booming, as turnover increased from approximately 1% in 1980 to 16% in 1985 to 133% in 1999 (Ryner 2018). Shareholder value ideology likewise penetrated corporate governance practices in the 1990s, resulting in increased short-sightedness among management at listed firms (Brodin et al. 2000), increased shareholder remuneration as well as accelerated CEO pay. In 1980, the 50 best-paid CEOs had an equivalent income of 9 industry wage-earners on average, down from 26 in 1950. In 2019, CEOs made on average as much as 60 blue-collar wage-earners combined (LO 2021).

Sectoral ownership of Swedish publicly-traded companies, 1983–2020.

Sweden’s International investment position, 1982–2020.

Source: Statistics Sweden, authors’ own compilation.

GDP: Gross domestic product.

When ownership of entities outside the stock exchange is included, foreign ownership currently amounts to about half of the Swedish economy (SVCA 2015). While the largest foreign institutional owners are primarily American and British, the 18 largest Swedish institutional investors owned 21% of the total market value of the Swedish stock exchange in 2015 (Nachemson-Ekwall 2016). Most Swedish institutional capital is allocated outside Sweden as current legislation aims to limit public ownership and influence over domestic and foreign industries by collectively owned institutions to the benefit of private actors.

Despite the emergence of domestic and international institutional ownership, the majority of the Swedish economy is still controlled by a few financial family dynasties. Ownership concentration, a fundamental aspect of the Swedish economy, is an important reason for this outcome. Swedish companies have historically been controlled by one or two owners, often but not always by Swedish financial families, which is possible due to vote differentiation (‘A shares’ and ‘B shares’) (Henrekson & Jakobsson 2008). In 1978, the largest owner controlled 26.8% on average of the nation’s 31 largest conglomerates (Hermansson 1989: 120; SOU 1988:38). When surveying ownership control of 88 largest companies on the Swedish stock exchange in 2017, we found that the largest owner controlled 31.2% of the voting power, the two largest owners had a combined voting power of 41.3%, and the three largest owners had a combined voting power of 46.4% on average. In other words, the power of Swedish capitalists over Swedish corporate control remains intact.

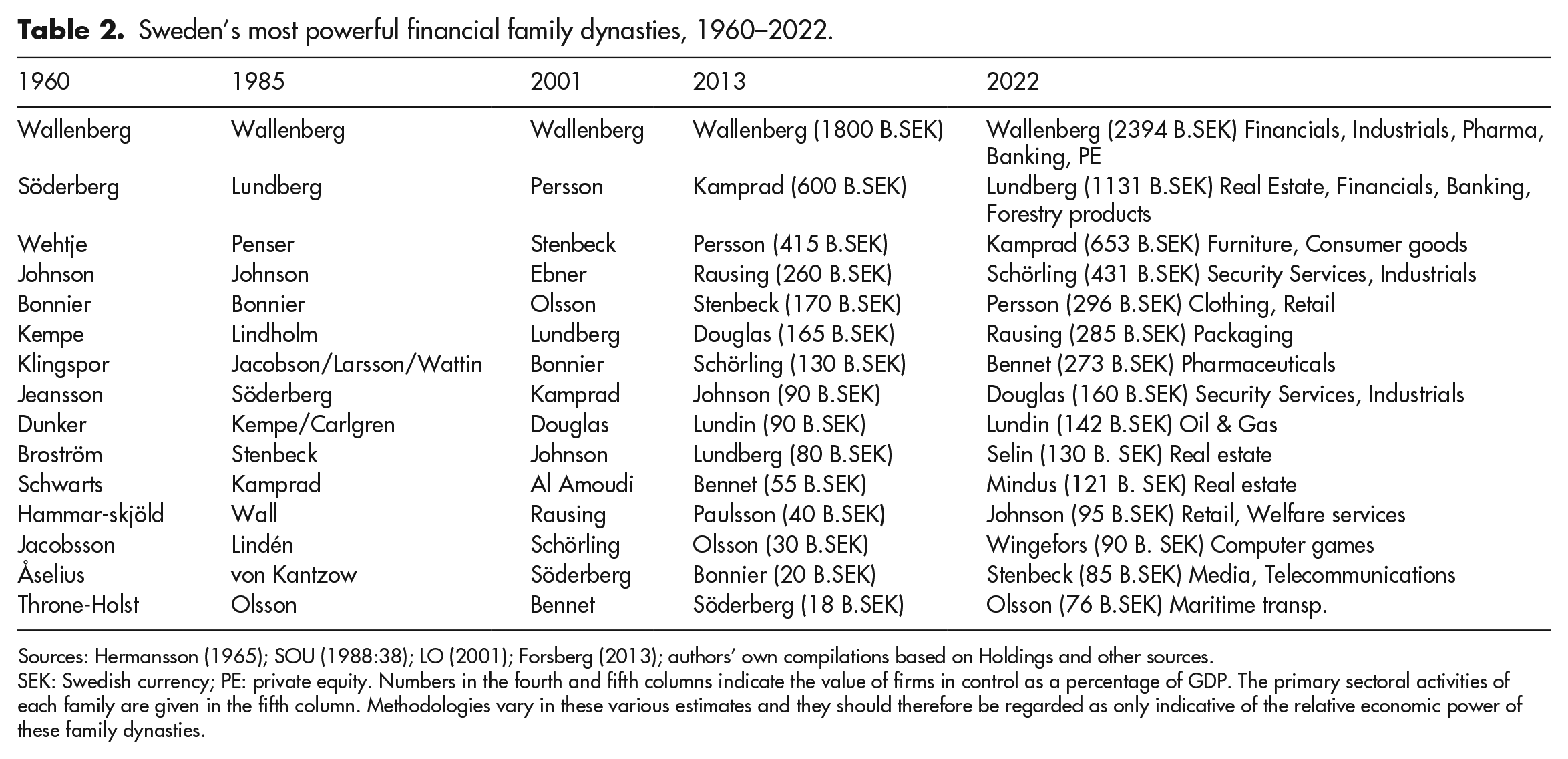

About 50 Swedish large-cap companies as well as significant corporate and non-corporate resources outside the stock exchange are controlled by the 15 financial family dynasties (cf. Hermanson 1965) that have been present on the Stockholm stock exchange for a long period. Table 2 shows the 15 most powerful financial families and their assets controlled since the early 1960s, according to different sources including our own calculations for 2022. The 15 largest financial families controlled companies worth 6312 billion SEK in 2022, corresponding to 47% of the Stockholm stock exchange or 112% of GDP. The 15 families’ penetration of the welfare sector and the strategies used by Swedish capital to defend their interests in the welfare sector will be brought up later in this article. Before that, we show how the structural power of capital coupled with a neoliberal elite mobilization and new economic common sense has contributed to austerity executed by right-wing as well as social democratic governments.

Sweden’s most powerful financial family dynasties, 1960–2022.

Sources: Hermansson (1965); SOU (1988:38); LO (2001); Forsberg (2013); authors’ own compilations based on Holdings and other sources.

SEK: Swedish currency; PE: private equity. Numbers in the fourth and fifth columns indicate the value of firms in control as a percentage of GDP. The primary sectoral activities of each family are given in the fifth column. Methodologies vary in these various estimates and they should therefore be regarded as only indicative of the relative economic power of these family dynasties.

Redistribution from the public sector to the private sector

The transformation of the universal welfare regime must be seen in the light of the early 1990s financial crisis that was enabled and exacerbated by policy mistakes undertaken by social democratic and liberal-conservative governments alike. The first significant policy mistake was the lifting of lending regulations in 1985 which took place without any public inquiry or explicit impact assessment, amid a tax system that fostered debt-funded real estate speculation and crisis. A second policy mistake took place in the early 1990s following policymakers’ recalcitrance to let the fixed domestic currency (the krona) float amid foreign currency speculation. Amid the Swedish central bank’s interest rate climbing to double- and even triple-digit numbers, eventually peaking at 500%, right-wing parties and social democrats alike agreed to cut public budgets in desperate attempts to gain market confidence in order to preserve the fixed exchange rate regime (Edin et al. 2012). While the krona was finally set to float in November of 1992, the real and perceived threat of the structural power of financial markets, or more specifically ‘bondholder power’ (Harvey 2014: 91), continued to loom. In June 1994, the CEO of the Swedish insurance company Skandia publicly stated that the company would boycott Swedish government debt instruments due to the country’s weak public finances. Apart from temporarily impacting capital markets, interest rates, and the Swedish currency, Wolrath’s statements had significant political effects. According to the social democratic economic–political spokesperson at the time, Göran Persson (1997: 43), ‘the election [in September the same year] came to almost exclusively focus on austerity’ following the boycott (see also Wolrath 1995: 3–4). In the spring of 1995, new rounds of exchange rate and capital market turbulence again led to heightened criticism from social democrats of the market’s ‘undemocratic influence’ over Swedish politics (Jonung 1999: 67; Pierre 1999). As the former prime minister Ingvar Carlsson claimed: ‘[if we] try a bolder economic policy, the market will strike, push up interest rates, lower the krona and force us to back down’ (Göteborgsposten 1995).

A parliamentary consensus subsequently emerged that ‘Sound finances are the best way to curb the market [pressures]’, as according to one politician (Pierre 1999). Between 1997 and 2006, the Social Democrats institutionalized ‘the surplus goal’ (‘överskottsmålet’, or more informally ‘the Persson doctrine’) that aimed for a 2% government surplus over the business cycle (Erixon 2015: 570) under the mantra ‘If you are in debt, you are not free’, as explicated by then prime minister Göran Persson. While the target was reduced to 1% between 2007 and 2019, Sweden was among the top three European Union economies with the strictest fiscal rules in 2000 to 2012; Swedish fiscal conservatism was radical from an international perspective (Erixon 2015: 571–573). Fiscal restraint was likewise defended by neoclassical thinking among MoF economists in the 1990s, who maintained that only increased labor market flexibility could reduce the ‘natural rate’ of unemployment and that austerity actually could have expansionary effects (Erixon 2015: 570). By the early 21st century, the size of the government budget surplus had become a common sensical measure for a government’s economic skills (Brenton & Pierre 2017).

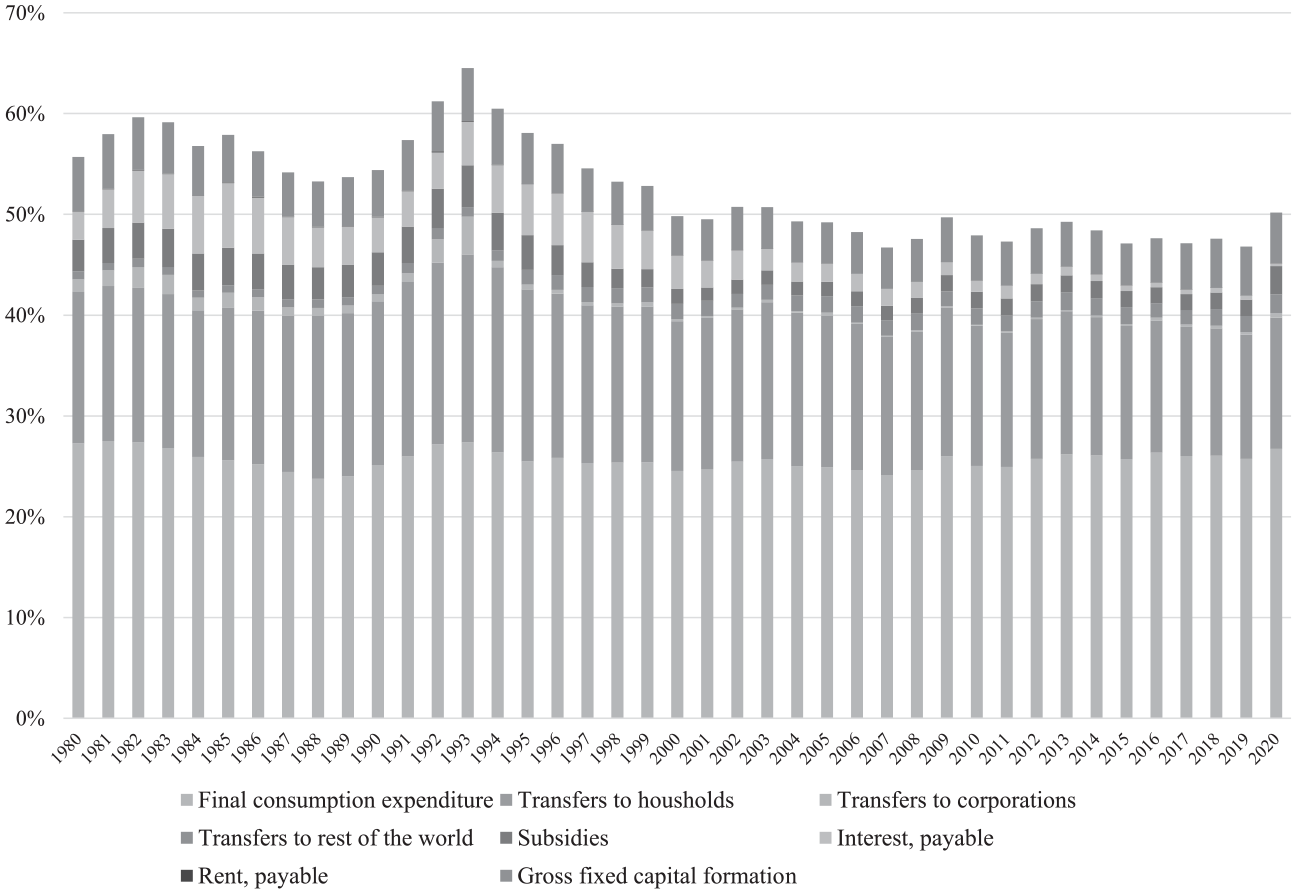

Against this background, the public sector’s total expenditures to GDP decreased from 60% of GDP in the 1980s to 50% in the 2010s (Figure 2). Public expenditure on social protection has been reduced from 33% in 1980 to 27.7% in 2019 (Statistics Sweden) meaning that social protection spending is 266 billion SEK lower in 2019 than if it would have constituted 33% of BNP as in 1980. A final reason for the decreased public sector spending is the early 1990s abandonment of the public housing program, a cornerstone of Sweden’s post-war welfare model. Together with Sweden’s dysfunctional housing market, the abandonment of this program has resulted in a structural housing shortage, runaway prices, and rampant household indebtedness for the upper half of households that can afford to take part in this process (Blackwell 2019).

Public sector expenditure as a share of GDP, 1980–2020.

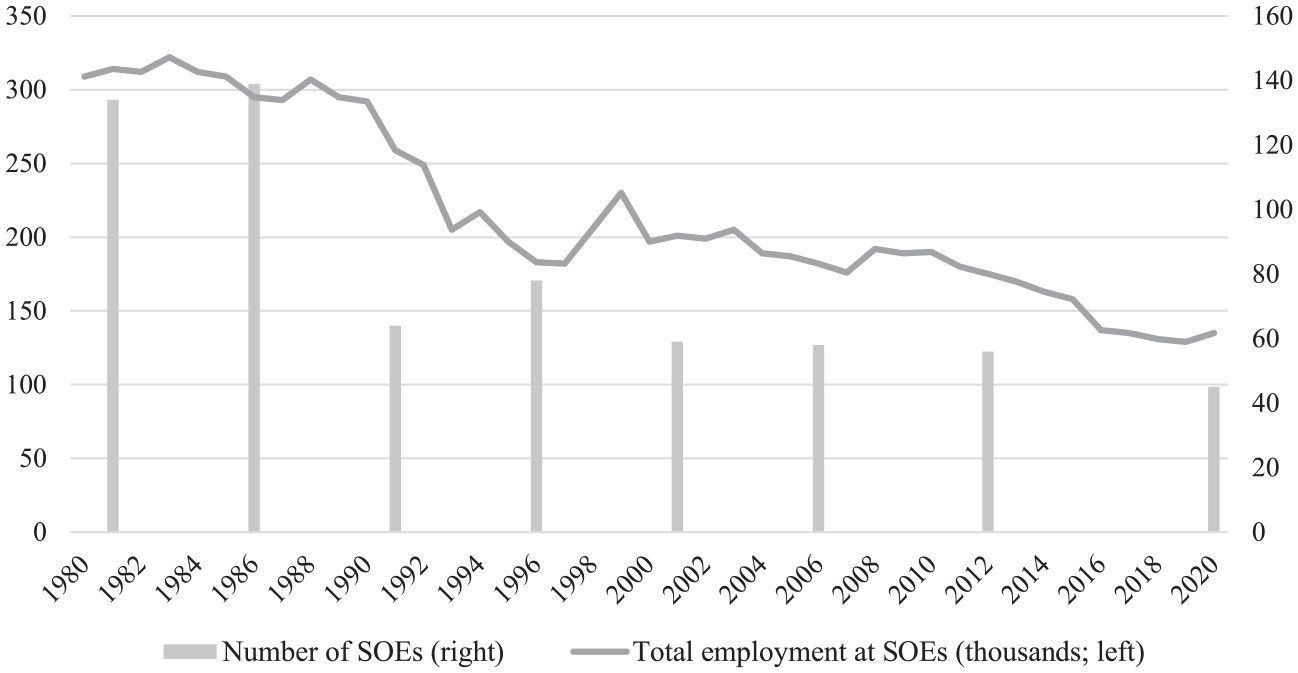

Sweden moreover ranks high internationally in privatizations as a share of GDP (Jordahl 2008, see also Allelin et al. 2018b: 15–17). The public sector’s share of all employees amounted to 33% in 1980, reached a peak of 39% in 1985, decreased rapidly in the 1990s, and currently amounts to 30% with a corresponding private sector share of 70%. State-owned enterprises (SOEs) decreased from 134 in 1981 to 46 in 2019, while SOE employment has shrunk from 314,000 to 129,000 (Figure 3). The combined value of privatizations of SOEs between 1980 and 2017 amounts to more than 400 billion SEK or around 6% of the GDP of 2017 (author’s compilation based on the Privatization Barometer 2019).

Number of SOEs and employment (hundreds of thousands) in SOEs, 1980–2020.

Adding to public sector retrenchment, tax income to GDP decreased from around 50% in 1990 to 44% in 2017, following lowered income and corporate taxes, cancellation of wealth, gift, inheritance, and property taxation, and the implementation of a wide range of tax deductions including on private pension savings and mortgage interest rates that disproportionately benefit wealthier households. It is clear from Figure 4 how the tax income share dropped after early 1990s tax reform, financial crises, and during right-wing governments of 1991–1994 and 2006–2014. The decrease in 1997–2001 during a social democratic government is perhaps a more surprising one.

Tax revenue as share of GDP and unemployment, 1980–2020.

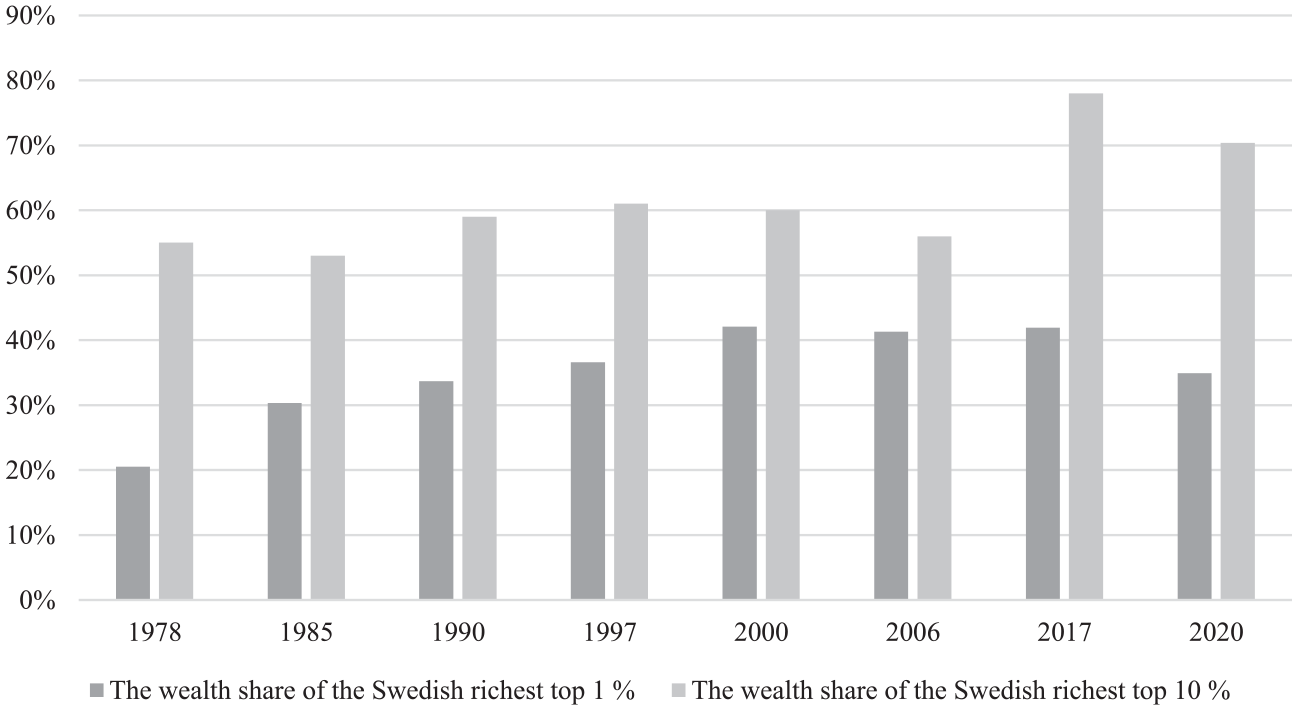

The cancellation of numerous capital taxes mentioned above, coupled with accumulation regime change, have significantly contributed to the increased wealth share held by the Swedish top 1% over the last 40 years (Figure 5). The estimated total wealth share of the richest 1%, including assets that citizens hold in hidden assets in tax havens and non-listed firms abroad, has increased from around 20% in 1978 to 35% in 2020 (Credit Suisse Research Institute 2020; Roine & Waldenström 2009). The large increase after 2006 has much to do with low interest rates and unconventional monetary policies following the financial crisis of 2008, which have fueled capital markets around the world. The significant rise of the wealth share of the 10% after 2006 may also have to do with Sweden’s significant house price inflation. Sweden ranks eighth in wealth inequality out of 53 comparable countries in 2020 (Allianz Research 2020: 49), while ranking higher than most other Western nations when it comes to billionaire wealth as a share of GDP (Sharma 2021). The number of Sweden’s SEK billionaires has increased from 83 in 2001 to 187 in 2017 possessing a combined wealth amounting to 47% of GDP in 2017 (Veckans Affärer 2014–2017).

Estimated share of private wealth held by the richest 1% and 10% of the Swedish citizens, 1978–2020.

Recommodification of the Swedish welfare sectors

Amid the Social Democratic accelerating neoliberalization (Ryner 2018), a changing attitude toward the public sector became visible among party elites. Under finance minister Feldt, ‘virtually all publications from the ministry of finance came to advocate the introduction of various types of so-called “quasi-markets” in the social services sector’ in the late 1980s (Blomqvist 2004: 144–145). Between 1986 and 1991, social democrats decentralized and dismantled much of government regulatory control of central state agencies that were handed down to the regional and municipality level. Public funding became available to nonprofit providers in 1984 and onwards to increase the share of parental cooperatives, staff cooperatives, and nonprofit foundations in Swedish welfare (Blomqvist 2004; Lapidus 2019: 194).

Major changes in the welfare sector followed when the conservative government (1991–1994) opened the doors to for-profit companies in the midst of the country’s deep economic crisis. New legislation stipulated municipalities and counties to procure welfare services under free bidding competition between public and private actors (LOU 1992). A school voucher system was implemented in 1992, enabling public funding of for-profit companies to run and students to choose schools, public or private, with the public funding connected to and following the student. Amid deteriorating municipality budgets, welfare services were increasingly carried out by private actors within the (still tax-financed) sectors of education, elderly care, and health care (Larsson et al. 2012; Righard et al. 2015). The social democratic governments which followed in 1994–2006 did not abolish these reforms but ‘sought to consolidate and improve on them [. . .] consistent with the ideational shift that had taken place within the party leadership’ (Selling 2021: 56). The liberal-conservative government of 2006–2014 continued neoliberal reforms by introducing a care system based on individual choice in 2008 and brought forward reforms that legally forced counties to allow citizens to choose between different welfare providers in 2010.

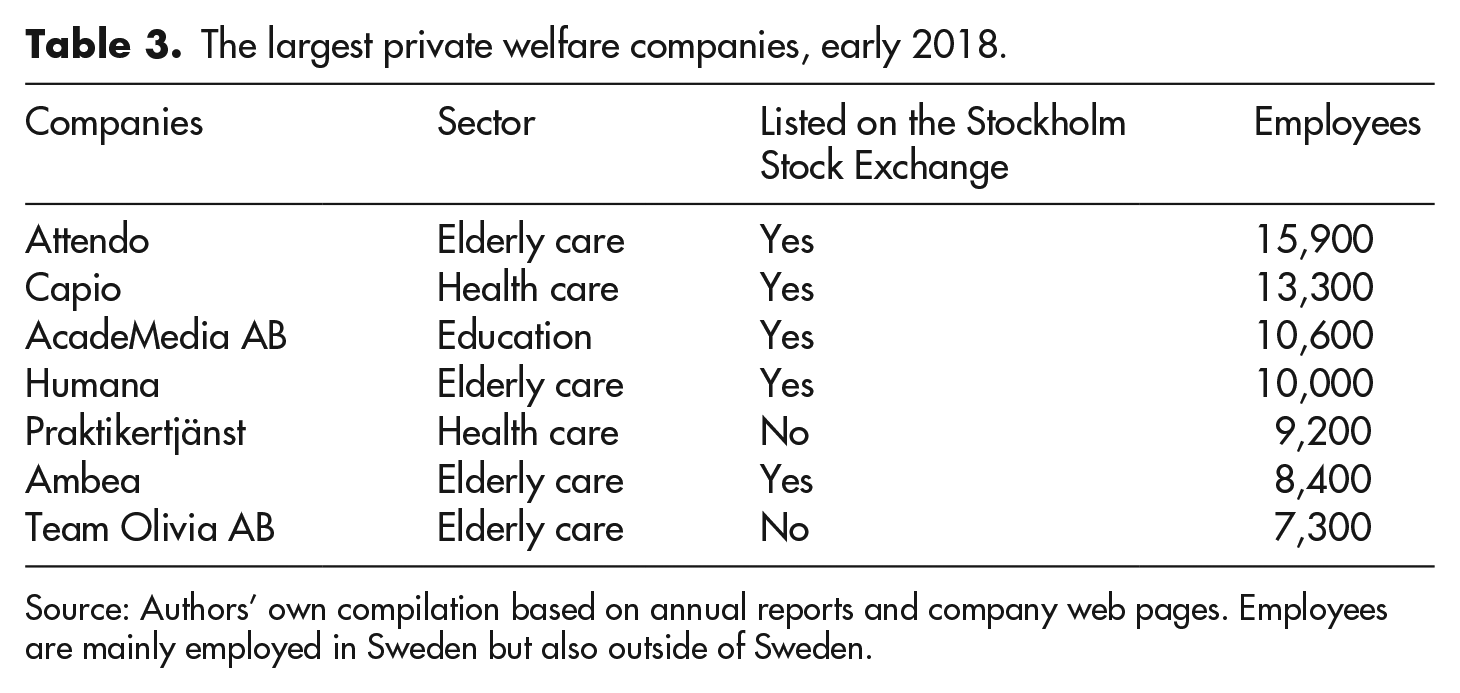

Corporate actors, including the Swedish financial families (see Table 2) started to significantly penetrate the welfare sector by the turn of the century. According to a government report, ‘During the 2000s, ownership concentration has increased as national business groups buy up smaller actors’ (SOU 2016: 78, Table 3). In 2016, 91% of private elderly care, 96% of private healthcare, and 75% of private education was run by for-profit companies (Werne 2018). The Wallenberg family previously controlled healthcare giant Aleris and owned 30% of Kunskapsskolan. The Douglas and Schörling families previously owned Attendo before selling it to British Bridgepoint. The company was listed on the Stockholm stock exchange in 2015 and is today controlled by the Johnson family through its investment company Nordstjernan. As ownership through private equity (PE) has increased significantly over the past decades corresponding to 8% of GDP in 2013 (Skyrman 2020: 40–41; SVCA 2017), a series of welfare companies were taken over by Swedish and British PE firms in the mid-2000s (Werne & Unsgaard 2014). One of Europe’s largest PE firms is the Wallenberg-controlled EQT that ‘has invested in several companies that provide welfare services largely financed with taxes, such as education and health care’ (EQT Group 2013) including the education giant AcadeMedia until 2017, the fourth largest welfare company at the time.

The largest private welfare companies, early 2018.

Source: Authors’ own compilation based on annual reports and company web pages. Employees are mainly employed in Sweden but also outside of Sweden.

To defend welfare profits and fend off counteractive regulation, a welfare-industrial complex consisting of industry groups, consultancies, specialized PR firms, think tanks, welfare companies, law firms, and sympathetic policymakers, of which some are tied to SAP, has emerged as a ‘formidable power bloc’ the last two decades (Svallfors 2016; cf. Reformisterna 2020: 29–31). Concrete lobby measures have included targeting municipal governments susceptible to privatization due to voter preferences or poor economic conditions; threatening to exit welfare operations and thus leaving the everyday needs of elderly, students, and clients behind, as well as the workers employed in welfare companies; organizing industry actors and sympathizing policymakers; and persuading uncertain or indifferent policymakers (Svallfors & Tyllström 2019: 755–761). This has created new forms of demands on private actors, which, compared to the historical dependence relationship between labor and capital, has become more intertwined in people’s everyday life. While large parts of center-right voters are skeptical about welfare profits (SOM 2021), almost all center-right parliamentarians vote in favor of profits according to one survey. The key in obtaining majority parliamentary approval has been to lobby the populist right-wing Sweden democrats, roughly comprising a fifth of the national parliament, in the mid-2010s (Wingborg 2016). Despite the negative public opinion of welfare profits, also social democrats and union officials have been targeted, and some have even been recruited by the welfare-industrial complex (Svallfors & Tyllström 2019: 758–759).

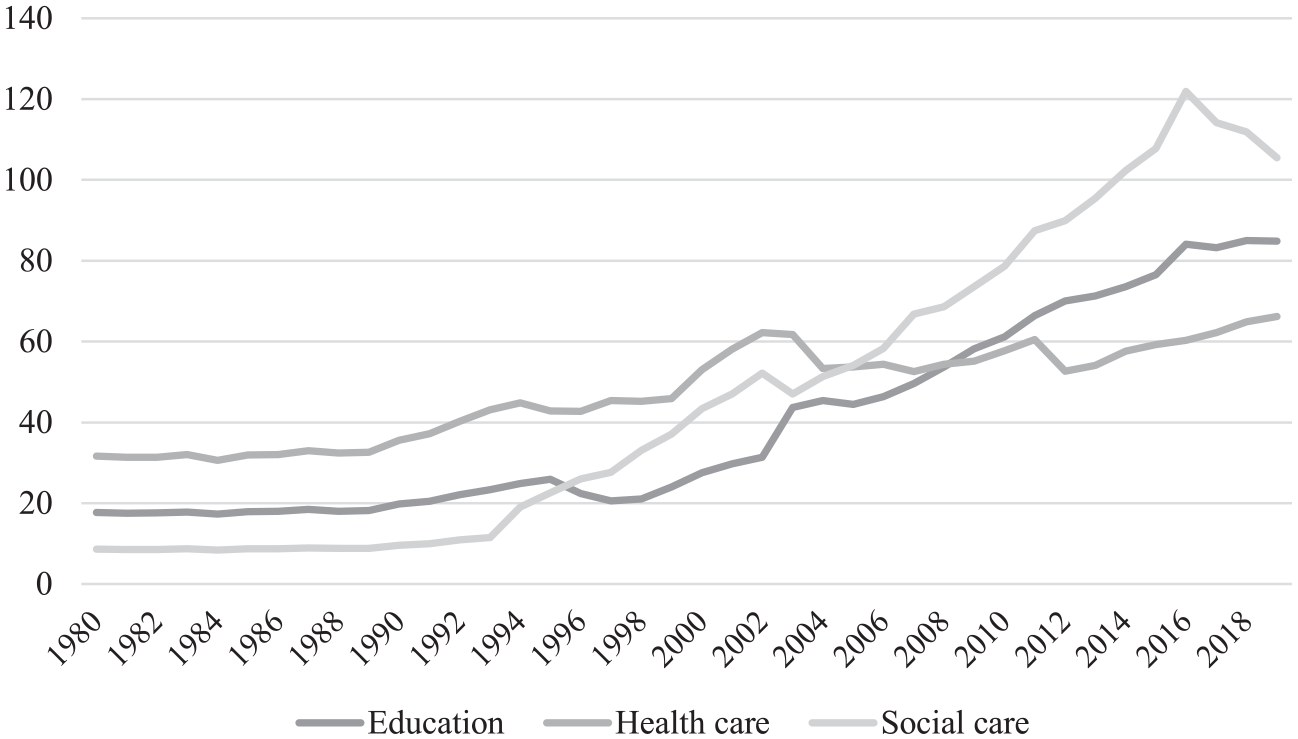

The combination of extensive budget cuts and far-reaching neoliberal reforms has had a transformative effect on the Swedish welfare model (Figure 6). The number of employees in the three largest private welfare sectors has quadrupled from 60,000 in 1980 to 260,000 in 2018. In all, 20% of all employees in the welfare sector work in the private sector and 40% of all primary health clinics were privately run in 2019, up from 25% in 2007 (Ekonomifakta). In 2014, private elderly care accounted for 23% of the total working hours and housed 21% of all recipients (Ekonomifakta 2019a). By 2013, some 16% of comprehensive schools and 25% of upper secondary high schools were privately owned (Statistics Sweden).

Number of employees (thousands) in tax-funded privately executed welfare operations, 1980–2019.

While privatizations have comprised management and ownership, funding of private welfare operations is predominantly tax based. Municipalities and counties purchased 180 Billion SEK worth of welfare services from private suppliers in 2019, up from 50 billion in 2007 (SOU 2016: 78, Statistics Sweden; Table 4). In 2016, 13,6% of the total costs of municipalities and 11.5% county costs were spent on the procurement of welfare services (Ekonomifakta 2019b). Welfare companies received on average 87% of their revenues from tax-based public financial means in 2013 (SOU 2016:78). After Chile canceled public subsidies to for-profit private education in 2016, Sweden is, to our knowledge, currently the only country in the world that subsidizes for-profit primary and secondary education.

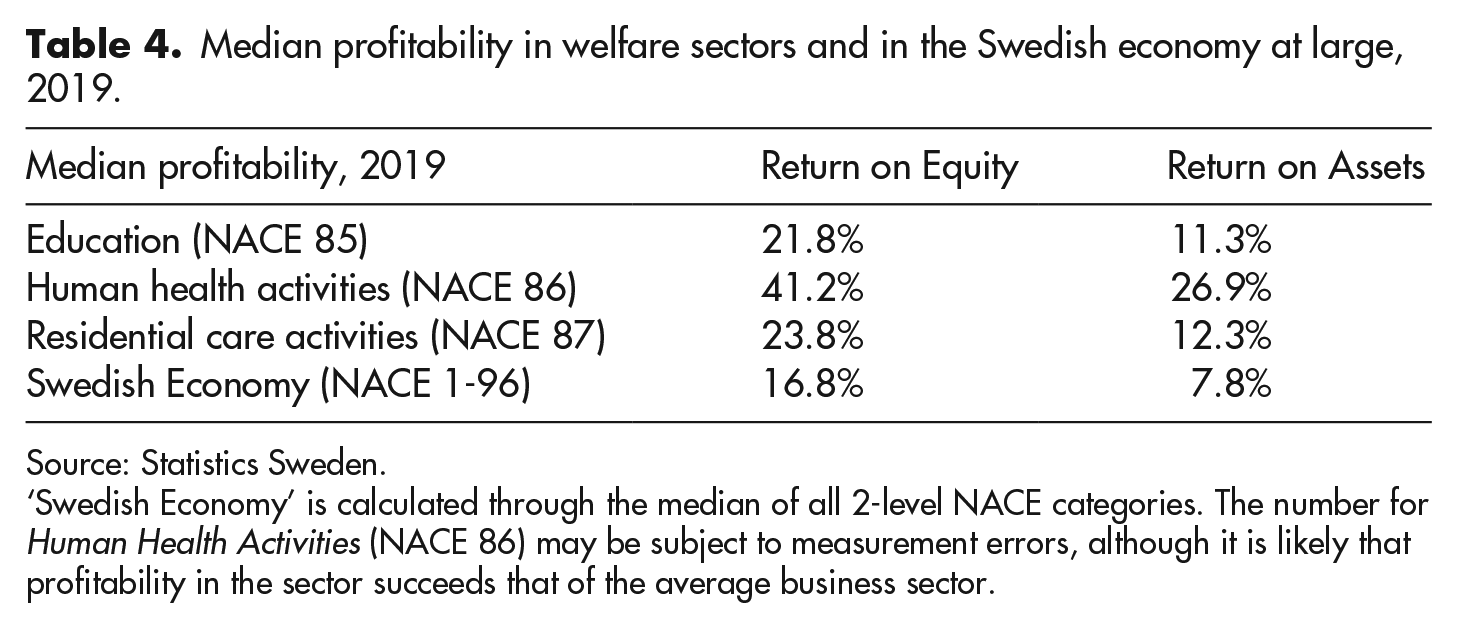

Median profitability in welfare sectors and in the Swedish economy at large, 2019.

Source: Statistics Sweden.

‘Swedish Economy’ is calculated through the median of all 2-level NACE categories. The number for Human Health Activities (NACE 86) may be subject to measurement errors, although it is likely that profitability in the sector succeeds that of the average business sector.

New regulation of the welfare model through accumulation by dispossession

Since the 1980s, policymakers throughout Western economies have seen the public sector as a cost rather than a source of demand (Jessop 2007: 53). Consequently, Sweden’s contemporary growth model is based on fostering profits in the private sector and maintaining macroeconomic and monetary stability, while the public sector is downsized, following a North-European pattern to reduce the social wage for competitive purposes (Buendía & Palazuelos 2014; cf. Harvey 2014: 91; Kalecki 1943; Korpi 2002; Ryner 2018; Van Apeldoorn & Horn 2007). As ‘capitalism always requires a fund of assets outside of itself if it is to confront and circumvent pressures of overaccumulation’ (Harvey 2003: 143), such assets include mature welfare institutions developed in the post-war period, that by the late 20th and early 21st century are to be reaped for profits ‘at very low (and in some instances zero) cost’ (Harvey 2003: 149). The institutionalized fisco-financial polity and the hegemony it rests upon provide the foundation for accumulation of dispossession, as one policy entrepreneur and former financial CEO notices, pointing to Europe’s gradual but accelerating erosion of state-supported systems for education, health and medical care, social security and pensions. Some of these needs can be met through the private sector and indeed represent significant and well-documented market opportunities for the insurance industry. (Wolrath 1998: 501)

Since the 1980s, the welfare sector has become a profit source for capitalists and institutional investors searching for yields.

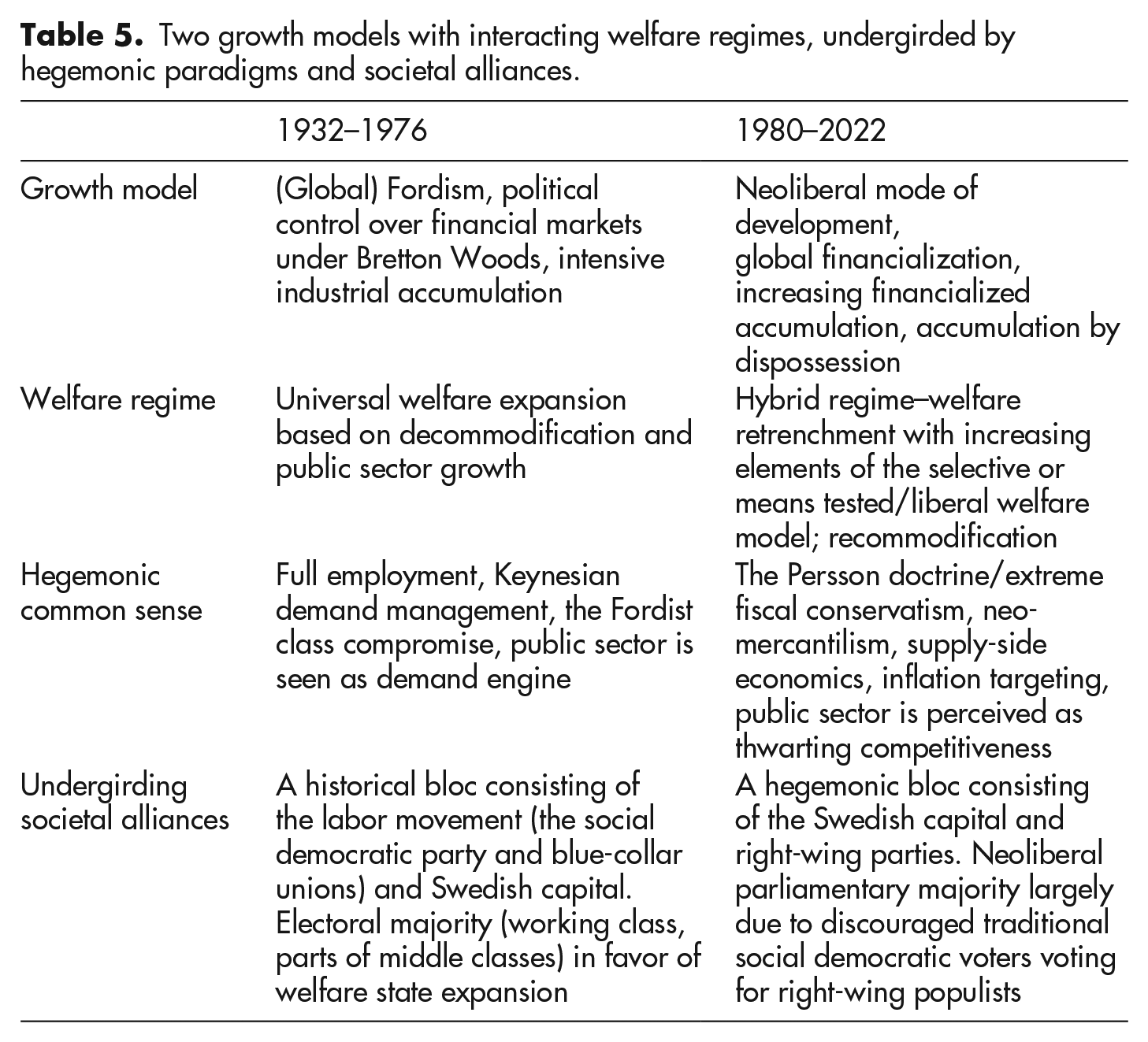

This article highlights that accumulation by dispossession in Sweden rests on three coevolving mechanisms – one ideological and political, one economic or structural, and one hegemonic. The ideological mechanism implies governments that on ideological grounds perceive privatizations as an end in itself. A key example is right-wing governments that have carried out almost all privatizations of SOEs in the last decades. The economic/structural mechanism comprises economic crises and drawn-out recessions (including on the regional and municipality level) that exert downward pressures on tax income, which opens up new opportunities for capital to enter the recommodified welfare sector following privatizations (cf. Harvey 2003: 141). The third and last mechanism can be viewed as neoliberal common sense in the field of economic policy, which is both as a result of structural factors and conscious efforts by capital elites and organic intellectuals to generate neoliberal hegemony (Ahrne & Clement 1992: 471–474, Westerberg 2020). While social democratic policymakers bought into neoliberal ideas in the 1980s (Andersson & Mjøsset 1987; Mjøset 1987; Ryner 2003, 2018; Mudge 2018), neoliberal common sense was further cemented by the financial crisis and the perceived structural power of financial markets by policymakers in the 1990s (Brenton & Pierre 2017; Erixon 2015; Göteborgsposten 1995; Harvey 2014: 91; Jonung 1999: 67; Persson 1997: 43, Pierre 1999; Wolrath 1995: 3–4). The extreme fiscal conservatism that followed has become a perpetual state-administered austerity program that has debilitated municipalities’ balance sheets and thereby reinforced privatization tendencies and private welfare governance. Austerity measures practiced by Swedish social democrats have thereto led to deteriorating social cohesion and spawned distrust among core social democratic voters, as highlighted by an outgoing social democratic minister in 2006 (Dagens Nyheter 2006) which has resulted in the party’s continual electoral shrinking. This void has primarily been filled by neoliberal parties prone to further welfare retrenchment and privatization, including the rise of a previously neo-Nazi right-wing populist party garnering roughly 20% of votes in popular elections (Table 5).

Two growth models with interacting welfare regimes, undergirded by hegemonic paradigms and societal alliances.

Following regulation regime change, Sweden’s transformed welfare model is best described as a mixed model with increasing market liberal characteristics. Welfare privatization and retrenchment have resulted in a considerably smaller public sector, reduced social security, and increasingly individually financed pension and social security insurance schemes. While the Swedish universal welfare model was based on redistribution from the private to the public sector, the overarching societal development in Sweden from the beginning of 1980s has been characterized by a large-scale reverse redistribution from the public to the private sector. The number of public sector employees has decreased by 25%, employees in SOEs have more than halved, while private welfare firm employment has quadrupled. In 2018, 20% of the employees in the three largest welfare sectors worked in the private welfare companies that generated tax-financed profits on politically created welfare markets. The allocation of welfare resources is increasingly determined by private welfare companies and their relatively well-to-do consumers, while inequality and polarization increase between socioeconomic groups and communities within cities and between urban and rural areas. Meanwhile, the 15 largest financial family dynasties, in control of industries worth 112% of Sweden’s GDP, are important actors in the ongoing financialization of the Swedish welfare sector, where welfare companies are continuously bought and sold on and outside of the stock market. Various constellations of the Wallenberg, Douglas, Schörling, and Johnson families have been in control of welfare giants such as Attendo, AcadeMedia, and Aleris. Welfare firm operations are increasingly transnational in scale as Swedish welfare firms expand primarily in Europe, while ownership of Swedish welfare companies is swapped between domestic, North European, British, French, and Australian owners. Welfare neoliberalization is likewise defended by societal alliances. The post-war social democratic historical bloc has largely been replaced by a neoliberal hegemonic bloc as the driving hegemonic force of societal development, led by the Swedish business elites and center-right wing parties. In the virtual absence of vocal anti-hegemonic forces, many social democratic leaders have limited criticism against welfare profits as much as possible throughout most of the last decades. On the contrary, Sweden’s neoliberalized welfare model has received open support from several political elites tied to the social democratic party, as well as from the white-collar unions, one of the largest blue-collar union, and affluent citizens that benefit from exclusive private welfare access (Lapidus 2019: 174–175, 187–188, 195; Svallfors & Tyllström 2019: 758–759).

While the social wage has been lowered under bourgeois and social democratic governments alike, Sweden simultaneously enjoys among the best government finances in the OECD. Public gross debt has decreased from 70% in 1995 to 35% in 2019 and rose only marginally during the Covid-19 pandemic. Government net wealth subsequently rose from negative 29% in 1997, turned positive in 2005, and amounted to 21.4% of GDP in 2020 (Regeringen 2020: 68, and Statistics Sweden, authors’ own compilation). Policymakers have seemingly engaged in internal devaluation by reducing Sweden’s social wage on competition arguments (cf. Regeringen 2018: 8). To no avail, the International Monetary Fund (IMF) has called upon surplus and creditor countries in the European North to stimulate their economies (and hence European aggregate demand) for about a decade (Cafruny 2015; IMF 2019).

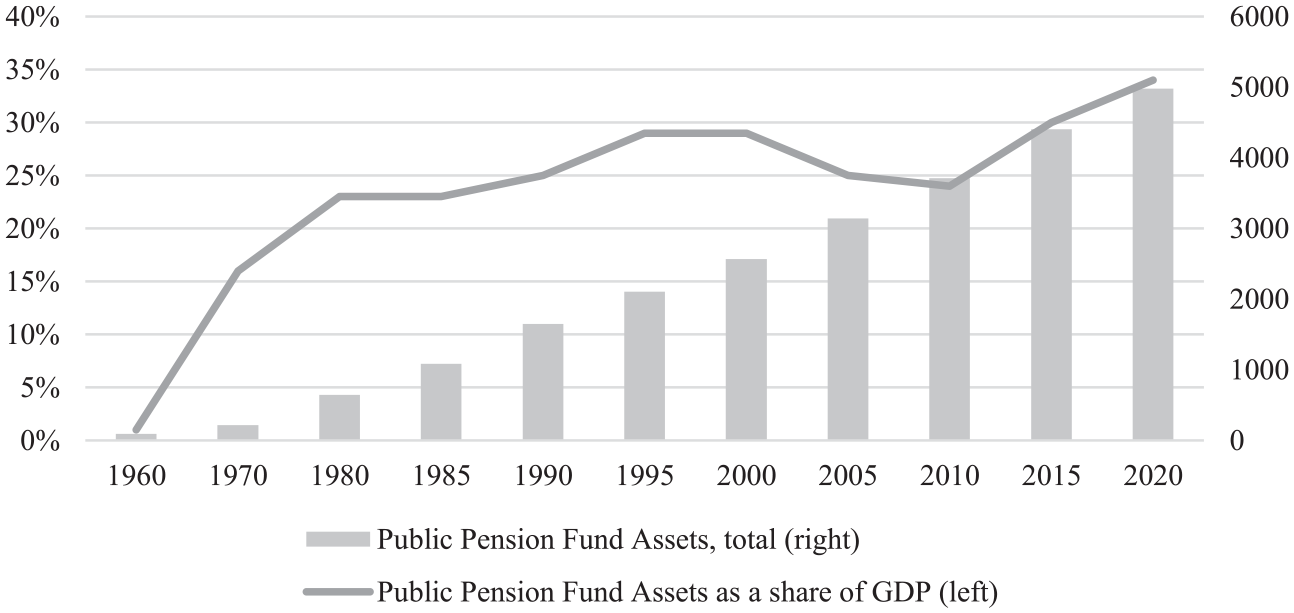

To reverse these neoliberal trends, labor, and progressive movements in Sweden and internationally must articulate counterhegemonic strategies and present new forms of sustainable accumulation strategies that can contribute to green growth, wealth redistribution, and universal welfare (e.g. Durand & Légé 2013; Neilson 2021). The Swedish finance-led accumulation regime has resulted in an immense accumulation of assets into wealth funds, including the public pension funds (‘AP-fonderna’), with total assets amounting 34% of GDP in 2020 (Figure 7). While the aim of these sovereign wealth funds is to maximize yields through passive portfolio ownership, Sweden’s collective wealth could be used for increased democratic control and influence over the economy; a crucial objective for the green transition away from fossil fuel dependence. Amid Sweden’s extraordinary public finances, large sums of capital could also be borrowed to negative real interest rates, compared to nominal interest rates on 10-year government bonds equaling 10% in 1995 (Kallifatides & Skyrman 2021). Amid increasing calls from Swedish society, including mainstream economists (Dagens Arena 2015; SvD 2013) and business media, leading social democrats have ardently opposed and termination of government debt amortization that could free up tax resources for welfare expenditures in later years, which indicates the deep entrenchment of neoliberal common sense in Swedish politics. The shackles that are tormenting the Swedish labor movement are seemingly of hegemonic rather than structural/fisco-financial nature.

Total assets of public pension funds in billion SEK (left axis), and as a percentage of GDP (right axis), 1960–2020.

Footnotes

Acknowledgements

Author Note

Majsa Allelin is now affiliated to Halmstad University, Sweden