Abstract

This article examines Venezuelan migrants’ remittance practices in Madeira and Trinidad & Tobago (T&T) to highlight how similar-sounding remittance methods diverge sharply across contexts. In Madeira, it identifies a novel remittance system termed ‘reciprocal remittances’ whereby friends enable transfers through parallel domestic transactions in both countries. Unlike systems like hawala, these exchanges are bidirectional, non-profit, and enabled by reciprocity as an integral feature of the mechanics of the transfer itself. Conversely, in T&T, migrants rely on ‘friends’ who operate as profit-seeking informal agents. Here, Venezuelan migrants must pay high fees while remaining unaware of the multiple intermediaries involved. They face limited alternatives due to their undocumented status as well as T&T’s restrictive banking regulation. By comparing the contexts of Madeira and T&T, the article reveals how migrants’ legal status and local fintech environments shape the availability of different remittance practices. While reciprocal remittances exemplify an alternative economy rooted in reciprocity, their dependence on documentation and access to diverse infrastructures is thus an important limitations. The article concludes by challenging the assumption that formalisation improves remittance efficiency, calling instead for greater recognition of migrant-devised remittance practices.

Introduction

In their work on alternative economies, Gibson-Graham and Roelvink (2011) show that, ‘the economy can be a space of ethical action, not a place of submission to . . . the “imperatives of capital”’ (p. 39). In response, this article critically explores alternative economic practices used to enable remittances. It is based on qualitative research conducted with Venezuelan migrants in Madeira and Trinidad & Tobago (T&T). Venezuelans in Madeira are either Portuguese citizens or the spouses thereof. In T&T, most are undocumented, and even when documented are usually still restricted from accessing mainstream financial services. But in both locations, alternative remittance methods are popular. For reasons such as historical sanctions, Venezuelan government interference, high inflation, and lack of bank account access, many Venezuelan migrants use alternative remittance methods (Chaves-González and Echeverría-Estrada, 2020; Chaves-González et al., 2021).

The main argument of the paper is that remittance research must focus more closely on the concrete transfer mechanisms through which remittances move, and on the social ties that make these mechanisms possible. It follows Rodima-Taylor and Grimes’ (2019) interest in ‘inventive practices’ – novel workarounds that remitters employ in the face of restrictions to access so-called formal remittance methods. Inventive practices are a ‘recombination of existing tools and repertoires’ (p. 19) showing that ‘remittance infrastructure is neither monolithic nor (at least in whole) intentional in nature’ (p. 4). The article focuses on inventive practices that migrants often refer to as ‘using friends’. By closely examining the methods of transfer in different geographical contexts, we find that the practice of ‘using friends’ can in fact constitute fundamentally different economic systems depending on migrants’ legal status and the regulatory and financial environment in which they are embedded. These differences have significant theoretical and policy implications.

In Madeira, using friends signified a highly informal remittance method which I term ‘reciprocal remittances’ to emphasise the simultaneous bidirectional nature of the benefits to all parties. This article’s analytic contribution lies in showing that reciprocity in remittances can be embedded in the mechanics of transfer itself, rather than emerging as a social outcome of remittances being sent. Further, the most informal, disintermediated, and non-profit remittance practices paradoxically depend on migrants’ access to formal legal and financial infrastructures. This challenges conventional policy wisdom.

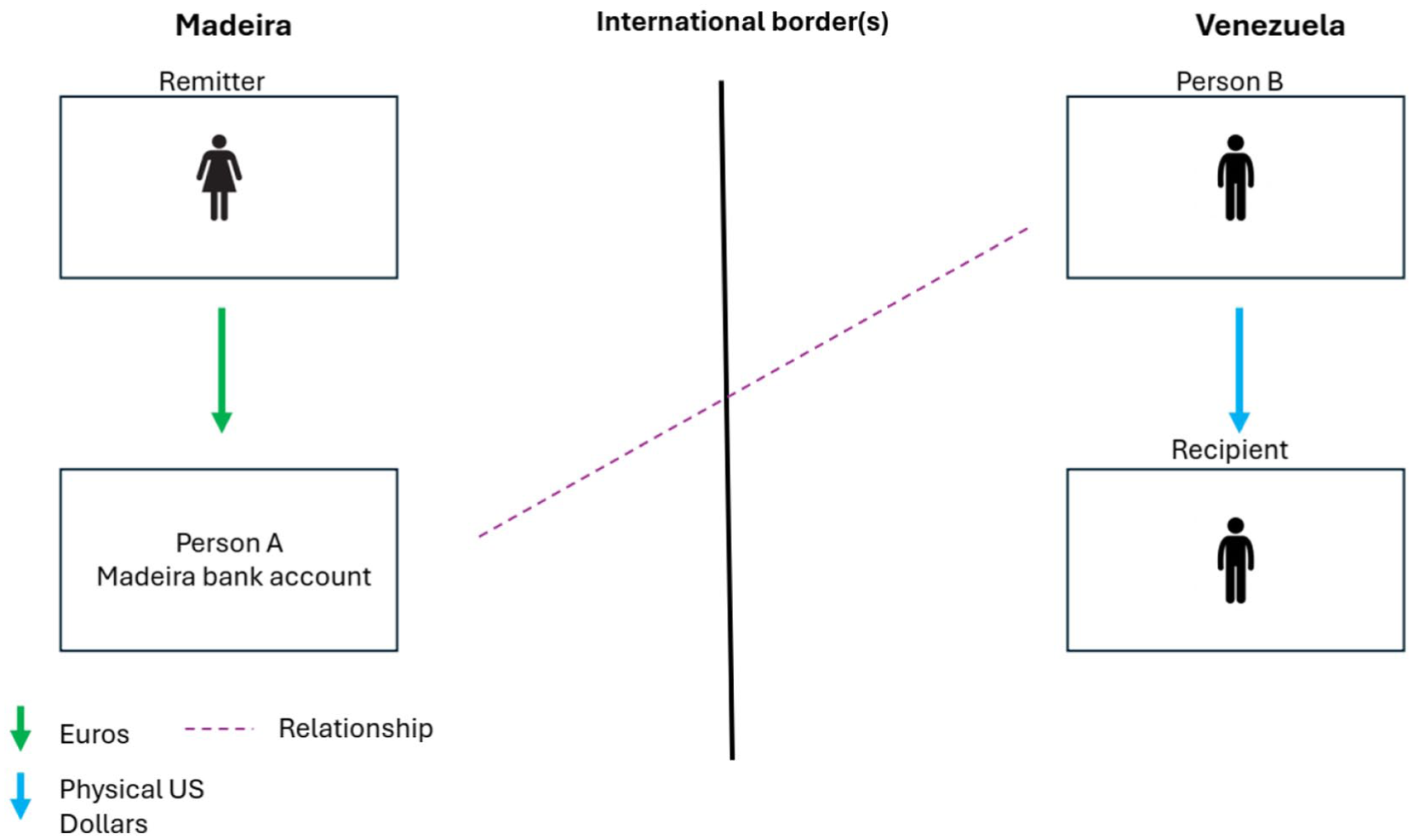

What do reciprocal remittances involve? Here is an example of a reciprocal remittance sent from Madeira to Venezuela (see Figures 1–3). The remitter transfers, for example, 100 euros into the Portuguese account of person A. Person B in Venezuela transfers the equivalent of 100 euros in bolívars to the Venezuelan bank account of the recipient (Figure 1). Or they give 100 euros worth of physical US dollars to the remitter’s family member (Figure 2). Person A and person B may be linked by family connection. However, Person A can also perform both roles by possessing bank accounts in Madeira and Venezuela (Figure 3). Those familiar with informal transfer mechanisms will note that this method resembles hawala 1 systems. Yet rather than relying on professional, commission-charging, hawala agents, the senders are themselves one of the agents of the transfer alongside their close friends and family. Again, unlike hawala, this feature also enables the transaction to be settled directly and instantly, illuminating the technical novelty of this remittance medium.

The remitter transfers euros into the Portuguese account of person A. Person B in Venezuela transfers the equivalent amount in bolívars to the Venezuelan bank account of the remittance recipient.

The remitter transfers euros into the Portuguese account of person A. Person B in Venezuela gives the equivalent amount in physical US dollars to the remittance recipient.

The remitter transfers euros into the Portuguese account of person A. Person A also possesses an account in Venezuela and transfers the equivalent amount in bolívars to the Venezuelan bank account of the remittance recipient.

Reciprocal benefits are key to understanding person A’s and person B’s motivation to enable this method on behalf of the remitter and recipient, beyond just ‘altruism’. Reciprocal benefits can include it being a way for person B in Venezuela to save money in euros in an EU bank account that they either own or are otherwise tied to via a familial bond. Person B can also use this method to simultaneously send a ‘reverse remittance’ to person A. This is because money that person A receives from the remitter in Madeira stands in for the money that person B has sent to the recipient in Venezuela (even though it is not literally the same money). Crucially, these reciprocal remittances only depend on domestic bank transfers which are repurposed to enable international transfers. In T&T, the data revealed another inventive practice but one that was exploitative. Venezuelans in T&T also relied on friends but the meaning of ‘friend’ in that context was quite different. Rather than using friends to enable reciprocal remittances, in T&T friends served as profit seeking remittance agents who were able to help the migrant send money home. This method involved using a chain of intermediaries, cryptocurrency exchanges, and domestic bank transactions in Venezuela. 2 Remitters in T&T were usually unaware of how the money was actually transferred. They only knew that their ‘friend’ was capable of making transfers. The web of intermediaries at the back end of these transfers was invisible to the remitter.

Unlike the examples of reciprocal remittances from those in Madeira, they also needed to pay high fees to account for the multiple, invisible, profit-seeking intermediaries in this remittance chain amidst a lack of competing alternatives.

Why Madeira and T&T? This article explores these two different methods from each place to make two points. First, paying attention to the mechanics of a remittance medium reveals the descriptive weakness of stating that in both contexts, Venezuelans used friends to send remittances. Second, the two cases highlight the importance of the legal status of migrants and the liberal regulatory status of fintech (things which migrants in Madeira enjoy and those in T&T lack) in, ironically, enabling the cheapest, most informal method of remitting – reciprocal remittances. In other words, because Venezuelans in T&T are usually undocumented and situated in a difficult regulatory environment for banking and fintech, their range of remittance options is dramatically reduced so they must use friends. Conversely, in Madeira, they are usually fully documented and have a range of options. In this situation they choose to use friends.

This article is structured as follows. Section two establishes a theoretical framework through the literature on alternative economies, reciprocity, the social meaning of remittances, and the importance of studying remittance methods. Section three explains the research context and methodology of the article. Section four provides the empirical data. Section five discusses what makes reciprocal remittances distinct and what the limitations of this method are. Section six explores the policy implications of the empirical findings.

Theoretical framework: Alternative economies, solidarity economies, and reciprocity

This article approaches remittances by treating economies and monetary practices as heterogeneous social fields starting with broader theories that challenge dominant understandings of ‘the economy’ and ‘money’ themselves. Gibson-Graham’s work on diverse and alternative economies provides a foundational intervention. Rather than understanding the economy as a singular, profit-driven system, they conceptualise it as a space composed of multiple coexisting economic forms, many of which may fall outside of capitalist logic. This allows us to recognise so-called informal remittance flows as economically meaningful in their own right rather than dismissing them as non-productive or inefficient. The World Bank (Freund and Spatafora, 2005) once estimated that only 35%–75% of remittances to the Global South are sent by formal means.

3

Given the sizeable volume of remittances sent outside of the mainstream, we should follow Gibson-Graham (2006) and learn to read this kind of economic activity ‘for difference rather than dominance’ (p. 55). Here a ‘diverse economies framing’ (Gibson-Graham and Roelvink, 2011) is useful. They write: When people speak of ‘the economy’ they tend only to think of formal . . . markets . . . and . . . enterprises focused on . . . profit. [But] . . . There are . . . not only formal market transactions, but alternative markets where considerations other than supply and demand influence the terms of exchange . . . [T]here are different modes of economic organisation . . . other forms of enterprise where private accumulation of surplus is not, or not the only, core business. (Gibson-Graham and Roelvink, 2011: 29)

Reading remittance transfers in this way ‘has the potential to offer new subject positions and prompt novel identifications’ (Gibson-Graham, 2006: p. xxxv). We must transform economic subjects – ‘subordinated’ and ‘disciplined’ by a hegemonic ‘economy’ – to what they term ‘economic becoming’. This requires economic activity to be read for diversity so that ‘fleeting energies can be organized and amplified within alternative enactments of economy’ (Gibson-Graham, 2006: 51). Complementing this approach, Zelizer (1989, 2014) demonstrates that money and payments are never socially neutral. Zelizer has consistently foregrounded the social meaning of different payment forms, objects, and transactions, and the relational processes through which they are constituted. This article extends beyond an analysis of payment forms to examine the social and regulatory processes that enable particular payment infrastructures to exist in the first place, and the social meanings attached to those infrastructures themselves, independent of the specific payment forms they process. This shift from transactions to infrastructures marks a subtle but important analytical distinction. Extending Zelizer’s approach shows that remittance transfer methods are not merely market transactions and that, like remittances themselves, these methods carry distinct social meaning. Ultimately, all economic practices should be analysed through their relational architectures, transactional forms, and the infrastructures that enable them. This insight is crucial for remittance research.

Remittances scholars have criticised attempts by financial elites to frame remittances as market transactions to be formalised, financialised, and optimised. Mullings (2022) and Smyth (2022) show how global institutions seek to appropriate remittance flows by recoding them as development tools. Smyth’s ethnography of Indigenous women in Mexico reveals how such logics impose binaries such as ‘productive versus non-productive’ that erase local moral economies. Recent work by Menon also shows how remittances can be reconstituted as ‘intimate infrastructures of finance’, with banks acting as shadow intermediaries that package remittances into standardised debt instruments for urban development (Menon, 2025).

But reciprocal remittances circulate value outside of formal remittance channels and hence cannot be controlled by formal institutions. In fact, the existence of reciprocal remittances undermines the very concept of ‘the remittance market’ (Kunz et al., 2020: 1616) as a hegemonic financial conglomeration. Referring singularly to ‘the remittance market’ obscures the diversity of economic practices that make up ‘remittance-scapes’ (Guermond, 2022b). We should spotlight ‘remittance markets’: remittance transfer practices that can be grouped by similarity of transfer method into ‘markets’, loosely defined. Formal remittance transfers are just one amongst a series of methods, one amongst several remittance markets, each with their own economy and each with their own financial logic, intermediaries, and advocates. Guermond (2022a, 2022b) and Zapata (2013) illuminate such diverse alternative economies. Through remittances, ‘multiple alternative socioeconomic practices and imaginaries are being articulated’ (Zapata, 2013: 95). Guermond (2022a) describes collective meso-level efforts to create community owned savings and credit associations (funded by remittances). These are ‘collective self-organised financial spaces that are established in direct opposition to mainstream financial systems’ (p. 815). These community savings and credit associations are formalised and still charge fees and/or interest for their use. But ‘interest payments were accepted because they came out of collective decisions and were subsequently redistributed to all members of the group at the end of the cycle’ (Guermond, 2022a: 815). One of Guermond’s (2022a) interviewees remarked, ‘we don’t call it interest, we call it solidarity’.

Solidarity frequently underpins alternative economic practices and is intricately linked to reciprocity. Dacheux and Goujon (2011) argue for reciprocity as a third pillar of ‘the solidarity economy’ (p. 205) beyond redistribution and profit. Elsewhere, Datta shows how reciprocity shapes migrants’ financial practices. She characterises migrants borrowing and lending from each other as ‘“balanced reciprocity,” whereby there is a recognition that participants are both borrowers and lenders’ (p. 124). These loans are interest free since they are ‘embedded within wider social relations’ (p. 124). Åkesson uses Zelizer’s ideas to argue that remittances are ‘embedded in the transactional relation between the migrants and those left behind’ (Åkesson, 2011: 327). She records how sending remittances creates an expectation amongst recipients that they should reciprocate in various (non-monetary) ways. Smyth (2017) also applies reciprocity specifically to remittances. She shows that Mexican hometown associations (HTAs) practise a solidarity-economy logic grounded in reciprocity. This ethos both motivates their collective transfers to Mexico and in return shapes services organised for migrants in New York City. Others have used the term ‘reverse remittances’ to describe remittances or other forms of help sent back in response to the original remittance. These reverse remittances are often explored as evidence of the reciprocal nature of the relationship between migrants and stayers (Ampah, 2016; Mazzucato, 2011; Ran and Liu, 2023; Yeboah et al., 2021).

The medium is the message: Differentiating between the remittance itself and the method of transfer

McLuhan (1964) showed that how things are sent is often just as important as what is sent. In a reciprocal remittance, reciprocity is understood as an integral feature of the mechanics of the remittance transfer itself. This is fundamentally different to how reciprocity is normally characterised in the literature. Further, the enjoyer of the reciprocal benefit is different. Again, there are three or four agents involved in a reciprocal remittance transfer: the remitter, the recipient, and the friend(s) who enable the transfer on either end. By providing the means for the remittance to be sent, the provider(s) of this service (the friends) receive a reciprocal benefit within that very exchange. It is this reciprocal benefit to the friend(s), acting as they are as informal non-profit seeking remittance agents, which constitutes the reciprocal compensation for enabling the remittance. This is what makes the use of the term ‘reciprocal remittances’ novel in this context. Reciprocity is not a social outcome of remitting, but a constitutive feature of the transfer method itself. But in the literature, reverse remittances are always a separate set of transfers to those that run from remitter to recipient. 4 The difference in the examples from Madeira here is that the reciprocal or ‘reverse’ remittance is enabled simultaneously as an integral feature of the original remittance. The reciprocal element is not a later reward in exchange for receiving the remittance. Instead, the ‘reverse’ remittance and the original remittance are contained within a single transaction.

This has been overlooked because the majority of research has focused on the role and meaning of remittances once they are received (Datta, 2017). With some exceptions (Datta, 2012; Lindley, 2009), scholars rarely focus on the social meaning of the methods by which remittances are transferred. This is a wider phenomenon that extends to much monetary social science research (Nelms et al., 2018: 17). Even the quantitative data suffers from this problem. The global scale of informal remittances is by its nature very difficult to quantify but Chaves-González et al. (2021) give some insight into the situation amongst Venezuelans in Latin America. In Ecuador and Peru, ‘the principal channel for transfers was through family or friends (43 percent)’ (p. 21). Elsewhere, ‘more than 20% of those in . . . Trinidad and Tobago said they transferred resources via acquaintances’ (Chaves-González and Echeverría-Estrada, 2020). In Brazil, ‘76 percent of respondents . . . said they sent remittances informally, followed by 16 percent who sent them through friends and acquaintances’ (p. 21). One will note the inconsistency in terminology in all this survey data. It also says nothing about what actually constitutes a transfer that is ‘sent informally’ compared to a transfer that is sent ‘through a friend’ or ‘through an acquaintance’. This is a good illustration of how the methods by which remittances are transmitted are often insufficiently examined. Indeed, the method of remittance transfer is itself often a socially meaningful practice, shaped by legal status, regulatory environments, and social relations. It is at this level that the concept of reciprocal remittances is presented. Reciprocal remittances are not defined by the meanings of and social relations connected to what is sent, but instead by the infrastructures that enable the remittance to be sent: through simultaneous, bidirectional domestic transactions that substitute for international transfers and embed reciprocity directly into the mechanics of exchange.

Carling’s notion of remittances as ‘scripts’ shows how remittances bundle material, emotional, and relational elements, yet even here the transfer mechanism itself remains analytically underdeveloped. Still, we can use Carling’s (2014) ideas to understand the idea of a reciprocal benefit acting as compensation for enabling the transfer. Reciprocal remittances make sense within the logic of a combination of remittances ‘scripted’ as Carling’s concepts of ‘compensation’ and ‘pooling’. He writes, ‘when remittance recipients provide services for migrants, the money that is sent can represent compensation, or payment, for the service rendered’ (p. 232). ‘Pooling’, on the other hand, refers to how resources within a family are often shared even when that family is spread across space. Compensation and pooling capture how money used in reciprocal remittances can circulate in both directions balancing relations in real time. In Carling’s terms, reciprocal remittances are a balanced-exchange script. But it is not just remitters and recipients who are engaged in this script. Instead, there is a script governing the transfer method itself that involves three or four agents: the remitter, the recipient, and the friend(s). Bolívars received in Venezuela by the recipient are offset with euros received by the friend or the friend’s family the same day. This two-way simultaneous transfer process directly settles the balance of favours between the remitter-recipient on one side and the friend(s) on the other. This shows how there is no limit to the number of scripts one could ascribe to remittance practices, which has been raised as a criticism of remittance scripts as an analytical concept (Hoye and Robins, forthcoming). Still, there are structural limitations that confine the performance of certain scripts to specific contexts.

This section has shown how by situating reciprocal remittances at the intersection of diverse economies theory, the social meaning of money and payments, and critical remittance scholarship, we can reframe remittance transfer methods themselves as relational infrastructures rather than market transactions. This theoretical positioning allows the subsequent empirical sections to be read as evidence of migrants’ capacity to use social ties to reconfigure financial infrastructures under specific legal and regulatory conditions.

Madeira and T&T: Research context and methodology

The scale of Venezuelan emigration is unparalleled in the region’s history. Around 8 million people have left (Chughtai, 2026). This mass emigration has been attributed to increasing crime, hyperinflation, and shortages of food and medicine, which in turn have been caused by a combination of government incompetence and repression and worsened by US sanctions (Bull and Rosales, 2020). Most receiving countries have been operating a de facto ‘open door’ policy (Chaves-González and Echeverría-Estrada, 2020). Yet there are significant differences in how countries have received Venezuelan immigrants. Regarding Madeira and T&T, both are small island states with high Venezuelan populations per capita. Both also have a history as ‘sending’ countries to Venezuela (Baptiste, 2002; da Silva Isturiz, 2020). The differences in legal recognition and legal status as well as the differences in local banking regulations and resulting availability of fintech services mean that the remittance options in each country are also different.

Madeira

Around 1.3 million Venezuelans are of Portuguese descent, many tracing their origins to Madeiran migration to Venezuela between the late nineteenth and mid-20th century (Dinneen, 2011; Gabaldón, 2017; Vieira, 2022). As conditions in Venezuela deteriorated, many Luso-Venezuelans returned, with a notable share settling in Madeira rather than mainland Portugal, despite Venezuelans comprising a small proportion of Portugal’s overall immigrant population. In Madeira, Venezuelans constitute the largest foreign-born group on an island of around 250,000 residents. Precise demographic data are limited because most Venezuelans are registered as Portuguese citizens (Padilla et al., 2024: 14), but in 2022 the population was estimated at around 10,000, approximately three quarters registered as Portuguese and the remainder likely spouses of Luso-Venezuelans (DREM, 2023; Pacifico, 2022). Portugal is progressive regarding fintech (Leitão et al., 2023). There are a range of remittance options available.

T&T

T&T has one of the highest numbers of Venezuelan migrants per capita (Herbert, 2021). T&T’s handling of Venezuelan immigration has been criticised for its ambivalence towards Venezuelans and unwillingness to formally document arrivals (Peters and Berkeley, 2021). Greenidge (2023) cautions against seeing the lack of response as a sign of ineptitude or governmental paralysis. He suggests it is a policy of ‘strategic indifference’ that aims ‘neither to exclude nor fully integrate refugees or migrants’ (p. 161). This reflects two considerations: political sensitivity to the unpopularity of Venezuelan migration among voters (Mohan, 2019), and a reluctance to jeopardise relations with Venezuela: a strategically important trading partner (Greenidge, 2023). There have been recent efforts to formally recognise Venezuelan migrants but many of the Venezuelans in T&T remain undocumented (Herbert, 2021). Sixty-nine percent of documented Venezuelans have registered as refugees (Chaves-González and Echeverría-Estrada, 2020). Banking in T&T is notoriously restrictive even for citizens (Kowlessar-Alonzo, 2023). Few Venezuelans in T&T have access to banking or formal Money Transfer Operators (MTOs) like Western Union.

Methodology

Sixteen interviews were conducted with Venezuelans in T&T and twelve with Venezuelans in Madeira. In T&T, interviewees were sourced via contacts at the UNHCR and a research assistant. Interviews were semi-structured. They were conducted in Spanish or Portuguese in Madeira and English and Spanish in T&T. In T&T, interviews were online only. In Madeira, interviews were in person with two online. Participants were recruited in person by ‘hanging out’ (Woodward, 2008) at various Venezuelan owned cafes and with the owners’ permission, approaching customers and asking them if they would be willing to be interviewed. In both fieldwork sites there were no specific criteria for choosing interviewees, only that they were willing to be interviewed. The data from T&T was collected from October 2023 to January 2024. The data from Madeira was collected from February to March 2024. Ages ranged from 18 to 51. In line with Chaves-González and Echeverría-Estrada’s (2020) research, interviewees from T&T tended to have lower educational attainment and a flatter trajectory in terms of former occupation in Venezuela compared to current occupation in T&T. The exceptions were two long-term residents who had skilled occupations. In Madeira, educational attainment was slightly higher, and many had experienced downward mobility since migrating to Madeira.

No interviewees were directly asked about their legal status, and all interviewees were paid for their time (Warnock et al., 2022). In T&T, interviewees were paid 70 TTD and in Madeira 20 EUR (reflecting the differences in cost of living). All names are pseudonymous. Interviews were transcribed using Maestra AI and then manually verified for accuracy by the researcher. Interviews were coded using NVivo. Grounded Theory Analysis was employed: an inductive ‘open’ approach whereby the researcher observes patterns in responses, recording them and then building theorisations. All fieldwork was cleared by the University of Oxford’s ethical approval board and in compliance with the ethical standards of countries in which fieldwork took place.

Remittances to Venezuela from T&T and Madeira

This section explores the remittance methods employed in each country. It shows how access to these methods is coloured by access to transnational forms of mobility. It also highlights the importance of qualitative investigation in detailing the mechanics of remittances by showing that ‘using friends’ to send remittances has radically different meanings in different contexts. The section begins by exploring the formal and semi-formal options available to remitters in Madeira and T&T. It then addresses the remittance methods that relied on friends. Friends and friendship play a pivotal role in enabling remittances in Madeira and T&T but in diverse ways.

Formal and ‘semi-formal’ options: Western Union and cryptocurrency exchanges

Many interviewees in T&T expressed a desire to use formal MTOs but were frustrated by their inability to obtain the correct identity documents that would enable their use. They were obliged to use alternative methods. Vincent, 51, in T&T explained: The problem is [the] parallel market imposes a much lower rate than the real one for transfers. [A]fter the migratory flow of 2016, the regulations tightened, for example . . . you cannot send [through Western Union] if you do not have a valid passport . . . Venezuelans here do not have access. (Interview in Spanish, 23/01/2024)

Even the few interviewees who did have the necessary documents found it difficult due to the restrictions from sanctions that had been historically imposed. Officially, these restrictions had been recently lifted for Western Union at least. But in many Western Union outlets, agents were still wary of processing transfers to Venezuela. One interviewee who had been living in T&T for 7 years and was documented described it as ‘a whole process’ to use Western Union as a Venezuelan. Another, Ricardo, 27, in T&T, who was also documented, explained further: They don’t allow us as a migrant to send money through them. The passport must be up to date [and] has to have a work permit stamp but the government of T&T will not give it to you . . . they want the background of where you obtained the money . . . so if you don’t have anything to show you’re working, you withdrew the money from your bank and now you’ve come to Western Union . . . that lack, that makes us not eligible. (Interview in English, 13/11/23)

In Madeira, Western Union was not considered a favourable option for the opposite reasons. Although it was a straightforward process, the exchange rate offered was worse than that available through friends. Martina, 50, in Madeira, could only use Western Union since she no longer knew anyone who could enable informal transfers.

I used to send it to a friend. But it stopped . . . he can’t send anymore because . . . he had a business [in Venezuela], and it went bankrupt . . . [Now I use Western Union] because I don’t know anyone else who does transfers. And it’s safer there. At least, I know it’s a well-known company. (Interview in Spanish, 07/03/24)

Similarly, Maria, 23, lacked the transnational social connections to engage in informal transfers, so she used a cryptocurrency exchange which although it incurred fees was still far cheaper than Western Union. She remarked, ‘I find it better to send through a crypto exchange than any other agency [but] . . .. I don’t know people who [help] send money to Venezuela’ (Interview in Spanish, 07/03/24). Finally, alternatives to friends were used in cases where the highly informal circumstances of the transfer method meant it was unavailable. Petra, 28, in Madeira, also used cryptocurrency platforms when her friends were unable to help. She explained: It’s not so constant. When I am going to send the money, I ask them if they have bolívars available for exchange or if they are interested at that moment. The answer can be positive or negative. When they don’t need the exchange, I use Binance [the leading cryptocurrency exchange]. (Interview in Spanish, 20/03/2024)

More formalised methods of remitting such as through cryptocurrency platforms could be used to fill gaps when friends were unavailable. The next section reveals that in T&T the majority of those using friends were indirectly using cryptocurrencies unawares. Their options were limited not only due to their legal status but also due to low awareness of cryptocurrencies and an underdeveloped regulatory environment for fintech.

Friends as remittance agents

Because most were unable to access formal remittance services, using friends was by far the most popular reported method amongst interviewees in T&T. However, these ‘friends’ were usually closer to acquaintances and in all cases the friends would profit from providing this service. Further, the method by which friends would enable money to arrive in the bank accounts of the migrants’ families was often mysterious to the remitter. Closer investigation revealed that the friends were acting as semi-professional remittance transfer agents, employed within a wider hierarchy of agents. One interviewee, Bella, 47, in T&T, had worked as one of these agents. She explained the process: There is always a person in Venezuela who has an account [with] a large sum of money. You make the request to another person [in T&T] who works for that person [in Venezuela] . . .. And that person . . . in T&T earns a percentage. You give the Venezuelan account details [of your family] . . . but you give him [the person in T&T] the money. That person communicates with the person in Venezuela. The person in Venezuela will make the transfer from bank to bank . . . directly there. Now, how does someone who is there get their money back [from T&T to Venezuela]? They . . . send it through cryptocurrencies . . . [I]t is a monopoly. They take advantage of [Venezuelans] everywhere. (Interview in Spanish, 12/01/24)

Relying on friends was usually perceived to be the sole method available, resulting, as Bella says, in a monopoly. This meant that the exchange rates and fees were much higher than those available through Western Union or directly via a cryptocurrency exchange. In Madeira, this method of using acquaintances who worked as informal profit-seeking remittance transfer agents did exist. However, it sat within a greater variety of formal or ‘semi formal’ (Datta, 2012) options. Petra, in Madeira, described her experience with using one of these informal agents.

There is a person here, [but] she gives me much less. The same with Western Union. So, I find alternatives that don’t devalue as much. (Interview in Spanish, 20/03/24)

By comparing T&T and Madeira, this difference in preference for formal options compared to the friends-based options shows that in each country context, the term ‘friend’ was being used very differently. While the friends in T&T would take some kind of commission, in Madeira, interviewees were keen to emphasise that this was not the case.

Reciprocal benefits for enabling remittances: Inflation protection, access to goods, and reverse remittances

The reciprocal remittance method found in Madeira is a non-profit hawala style method of transfer that has removed any professional intermediary and uses friends and the remitters themselves as their own intermediaries. The motivation to enable these transfers lies in reciprocity rather than altruism. The reciprocal benefits are: (i) protection from bolívar inflation; (ii) transnational access to goods; (iii) enabling reverse remittances and transnational mobility between Venezuela and Madeira. These motivations are explored in order. The benefit to friends who have a bank account in both countries is that their money is now stored in euro denominated accounts without needing an international transfer. For those with accounts in Venezuela and Madeira, this shields their savings from bolívar inflation. Here Petra explains the process (see Figure 3): I do it with two people because they are friends . . . close friends. One used to live here, so she has an account here in euros, and she returned to Venezuela . . . So, she sends bolívars to my family, and I send her euros here in her account. (Interview in Spanish, 20/03/24)

Enrico, 51, also had a friend who did the same thing. This friend would even send her own Venezuelan earned money to her EU bank account whenever she could.

She travelled with me to Portugal and opened an account. Whenever she can, she sends money here. (Interview in Spanish, 07/03/24)

Enabling transnational access to products unavailable in Venezuela could also be a reciprocal benefit to a friend who enabled these remittances. Sandra, 30, in Madeira, explained: She buys items from here in euros [using the money Sandra puts in her account] . . . Because she lived here, she knows the process and makes her purchases online and sends them to Venezuela through a shipping agency in Madeira. She sends them the products, and they send them to her [in Venezuela]. (Interview in Spanish, 21/03/24)

This reveals a novel form of in-kind remittances that blurs the boundaries between the physical and the digital. It demands new theorisations about the nature of remitter and recipient and remitting and receiving. Can one remit to oneself? How can we conceptualise the agential forces at play?

Finally, the opportunity to send reverse remittances can be a motivation for a friend to provide this service. Scholars have portrayed reverse remittances as a ‘system of reciprocal exchange between diaspora and homeland in which social relationships and trust are embedded’ (Galstyan and Ambrosini, 2023: 673). But as section two explained, reverse remittances are always recorded as a separate set of transactions from those flowing in the traditional direction (Ampah, 2016; Mazzucato, 2011; Ran and Liu, 2023; Yeboah et al., 2021). In the cases explored here, the reverse remittance itself becomes a way to settle the original remittance. This is what makes this method novel. Petra, in Madeira, explained how a father living in Venezuela used the need for people like Petra to remit to Venezuela to support his family members in Madeira: Petra: The other friend’s husband regularly travels here because his . . . children live here. So [he remits] to his children in euro accounts here. When he visits them, he has his euro account here, so we do the same. They send the bolívars to my family, and I make the payment in euros to their account here. (Interview in Spanish, 20/03/24)

This shows that transnational mobility between Madeira and Venezuela is often a socio-economic driver enabling this remittance method. Reciprocal remittances involve remitters and recipients using elements of mainstream financial infrastructure, but in a way that subverts their official use case. In this sense they constitute an inventive practice (Rodima-Taylor and Grimes, 2019). Such inventive practices make up a sizeable volume of remittances to Venezuela (Chaves-González et al., 2021). A key feature of reciprocal remittances is that, in terms of executing international monetary transfers, they are disintermediated from professionals and ‘non-profit’. The interviewees made clear that they did not perceive any attempt by their friends to profit from these transactions. As Petra explained: we follow the official exchange rate . . . we leave it at that, without any kind of interest or percentage payments. (Interview in Spanish, 20/03/24)

Samuel, 39, in Madeira, framed his relationship with a friend who also had an active Venezuelan bank account in similar terms: It’s like a favour he does. I send a hundred euros, and he transfers the same amount in the value of Venezuelan currency, he doesn’t deduct any commission. (Interview in Spanish, 06/03/24)

The opportunity for intermediaries to profit from the transfers is removed. This is important since, as we saw, the intermediaries are often invisible to the remitter and recipient. Yet, in the case of reciprocal remittances, multiple remittance transfer intermediaries are unnecessary. Instead, remitters and friends are providing one another with a service in exchange for another in a mutually beneficial arrangement – in one transaction the remitter gets to send the remittance, and the friend gets to send either a reverse remittance or store money in a euro denominated account. This links to Gibson-Graham’s (2006) interest in finding examples of economic activity that constitute alternatives to the status quo. A remittance service is provided, which is itself a social good, but because of this service the father in Petra’s example can also support his daughter. This is underpinned by transnational bonds and enabled by trust. In Madeira, the level of trust was often emphasised. Helena, 51, explained of her friend: I’ve known her all my life . . . she does that because she is my friend . . . those are transactions that are only made with people of respect, of trust, that you truly know that a person you trust can help . . . it was a favour. (Interview in Spanish, 07/03/24)

Conversely, in T&T, the interviewees revealed that the friends were usually closer to acquaintances who the remitter usually trusted only enough not to defraud them.

Discussion

Ultimately, this paper has highlighted the problem that most remittances research ignores how remittances are transferred. But, as Datta (2012) argues, it is vital to pay ‘attention to the “nuts and bolts” of the remittance industry’ (p. 142). For example, Zelizer (2014) once asked whether cryptocurrencies would ‘intervene in relational processes differently than money orders or personal couriers’ (p. 9). This article answers in the affirmative. It also shows the importance of comparative geographical research since in doing so the paper has highlighted the key differences between reciprocal remittances and other methods. By focusing on the mediums by which remittances are sent, this article contributes to a gap in our understanding. We can now explore what distinguishes the reciprocal remittances method. It is disintermediated, informal, trust-based, non-profit, and invisible. But there are also limitations in its dependence on legal status and fintech regulation.

Disintermediation

Disintermediated payments are championed by cryptocurrency evangelists and amongst the new wave of app-based payments providers (Nelms et al., 2018). But attempts to disintermediate payments infrastructure from government and mainstream financial institutions invariably create replacement intermediaries (Nelms et al., 2018: 27; Robins, 2025). But although reciprocal remittances still rely on formal banking infrastructure, they do not rely on such infrastructure to execute international transfers. Instead they re-purpose financial infrastructure for migrants’ own use offering a greater degree of disintermediation than other remittance methods. Such disintermediation allows for the agency of all participants in the reciprocal remittance chain.

Informality, trust, and ties

Scholars have criticised a distinction between formal and informal remittance systems (Pieke et al., 2007) and fintech more widely (Preda et al., 2023). Yet reciprocal remittances are truly informal, relying on none of the trappings associated with a typical informal remittance transfer business. Like informal professional remittance systems, they are ‘sustained by close circuits of trust’ (Cirolia et al., 2022: 69). Similarly, as Datta (2017) observes, ‘security and trust. . . [are] crucial factors in shaping remittance practices’ (p. 555). Trust is key in hawala systems (Gräbner et al., 2021; Jegerson et al., 2024). But though the two hawala operators (in the sending and receiving countries) may be linked by trust, they still operate as a business to their customers even if they benefit by their customers trusting them (Cirolia et al., 2022). In this article, trust performs a greater role: it allows the parties involved in the examples from Madeira to be their own hawala operators. Trust enables disintermediation. Trust also helps reciprocal remittances to maintain transnational ties. The power of remittances to strengthen ties is normally understood in terms of strengthening ties between senders and recipients (Yount-André, 2018). But here, ties are strengthened between multiple people, not just remitter and recipient. Friends can function as non-professional remittance agents whose participation can be compensated through embedded reciprocal benefits rather than fees. This allows us to distinguish reciprocal remittances from hawala without occluding both within the category ‘informal’ and to show how friendship itself becomes part of remittance infrastructure.

Non-profit

Following Mullings’ (2022) critique of traditional remittances epistemologies, I suggest that reciprocal remittances instantiate a financial imagination organised around relationality and reciprocity rather than accumulation. We also saw Dacheux and Goujon (2011) argue for an alternative economy that is ‘governed by the principle of reciprocity’ (p. 207), supplying a theoretical backdrop for reciprocal remittances as such an economic practice. As Gibson-Graham (2006) reminded us, profit need not, or at least need not, be the only motivation for economic activity. Reciprocal remittances are distinctly non-profit seeking. Although the process does rely on traditional domestic banking infrastructure because all monetary transfers are domestic, no international intermediary (e.g. an MTO) can charge a fee for these transfers. They also cannot profit by manipulating the spread between the exchange rate offered to remitters against the actual interbank rate. Reciprocal remittances are unique in this respect, and I argue this constitutes their characterisation as an ‘alternative economy’ in Gibson-Graham’s sense of the term.

Invisibility

Hawala usually requires a mechanism to settle transfers if the flow is unidirectional. Eventually, hawala associated transfers must cross international borders. Because reciprocal remittances are settled directly, no such international transfer is needed. It is therefore ‘invisible’ and immune to the pressures that have been recently placed on some hawala operators (Lindley, 2023). Mullings (2022) and Smyth (2022) show how emotional and familial obligations are commodified and securitised by institutions. Here, I have shown how the structural invisibility of reciprocal remittances renders them resistant to commodification and securitisation which is, I argue, a core strength. However, reciprocal remittances’ invisibility is also tied to the issue that the sum total of money in each country does not change; rather it is redistributed (in the horizontal, peer-to-peer sense of the term). Whether this is a net positive or negative is complicated. It avoids the issue of currency appreciation associated with large inflows of remittances from abroad (Hassan and Holmes, 2013). For countries suffering from inflation such as Venezuela, this is arguably a negative but for export and tourism dependent countries, currency appreciation can adversely affect these sectors. Since the wealth is only redistributed amongst peers rather than transferred, this also prevents the issue of remittances causing wealth to leave the economy of the remittance sending country. Yet this also means that the total amount of wealth does not increase in the recipient country.

Limitations: Dependence on legal status and regulatory environment

As Datta (2017) writes, ‘migrants’ diverse behaviours in relation to . . . how [remittances] are transmitted are critically shaped by the social relations in which they are embedded’ (p. 545). Reciprocal remittances are dependent on complex social relations. There are agential and structural requirements to enable this remittance method. It clearly relies on the social capital needed to form sufficiently developed trust-based relationships that elevate the meaning of ‘friend’ in this context. The role of the friend can only be elevated in the context of a wide variety of market options to send remittances. In T&T, where, for many, using friends is the only option, the meaning and value of a ‘friend’ becomes deteriorated to signify anyone within the remitter’s wider social circle who they can trust enough to help them remit. In T&T, migrants are consequently taken advantage of by the ‘monopoly’ of informal actors. Remittances through friends in T&T could still be described as an alternative economy but they fail to fulfil Gibson-Graham’s vision. It is driven by profit not reciprocity. Such alternative remittance practices mirror wider patterns of fintech diffusion (Bernards, 2022; Joassart-Marcelli and Stephens, 2010) since they are embedded within structural and spatial inequalities. Structurally, reciprocal remittances rely on migrants’ legal status and the institutional social capital necessary for at least one spouse to own a Portuguese passport. It also often relies on transnational mobility. Many times, these transfers were only possible because of those who had returned to Venezuela retaining bank accounts in Madeira or through still having close family in Madeira. Further, it is also predicated on the comparative economic stability of the migration destination itself, which makes storing money in its banking system preferable to Venezuela. These practices are difficult to scale to destinations where the domestic currency is more inflationary than euros. Still, we saw the quantitative data indicate that elsewhere, in Peru and Ecuador for example, remitting through ‘family and friends’ is widespread (Chaves-González et al., 2021). Further qualitative investigation is needed to uncover the roles of friends and families in these contexts and whether the methods used there constitute reciprocal remittances. It is likely that at least some part of these transfers would do. Reciprocal remittances seem to flourish in the context of a regulatory system that allows for diverse formal and semi-formal methods of transferring remittances. Yet, in Madeira, these options were almost always compared negatively to the use of friends and family.

Policy recommendations

This article challenges assertions from the World Bank that enhancing access to formal banking and identification documents needs to be linked to an increase in use of formal remittance channels and that encouraging remittances to flow through such channels should be treated as a necessary goal (Ratha, 2005; Ratha et al., 2023, 2024). It challenges these policy assumptions by showing that the most informal, non-profit, and disintermediated remittance practices emerge precisely when migrants have legal status and full access to banking. This not only destabilises the formal–informal binary but demonstrates that informality can be an elective and relational practice rather than simply a response to exclusion. The World Bank has also called for improved data collection of informal remittance flows (Ratha et al., 2024: 10). The data from this paper indicates two important improvements here. First, regarding the World Bank’s Remittances Prices Worldwide (RPW) project, which tracks the cost of remittances, they must establish links with leading cryptocurrency exchanges to help understand the volume of remittances that travel through these platforms. Analysts have estimated these flows to be significant (Torres, 2024). Some claim cryptocurrencies are the main channel for remittances into Venezuela (Hernandez, 2024). RPW’s data is limited in this respect. Second, future quantitative surveys need to distinguish the differences in sending through a family member, sending ‘informally’, through an acquaintance, and so on. Demarcating these categories to understand the methods behind them will provide better data.

Advocating for improved methods of formally recording remittances flows is not a call to formalise remittances transfers themselves. As Lindley (2023) argues, ‘there is limited evidence that financial inclusion has transformative effects on poor people’s living standards or clearly drives economic growth’ (p. 368). While the goal of the formalisation of remittances is nominally about financial inclusion framed as development aid, there is too often ‘mission drift from poverty alleviation to profit maximization’ (Roy, 2010: 386). Critics even suggest that ‘financial inclusion’ can be predatory (Akolgo, 2023; Lindley, 2023; Mader, 2018). Therefore, we need to make informal remittances more visible so their advantages over formal methods become clearer. As this article reveals, migrants are capable of creating their own inventive practices which meet the UN’s SDG goal of reducing remittances transfer costs. Policymakers should consider financial regulations that acknowledge and accommodate alternative remittances, including informal and fintech-based transfers. In fact, the minimum requirements to access cheap remittances are an official identity document and a mobile money wallet. With these two items a migrant in T&T could directly access a cryptocurrency exchange and use it to send remittances with fees that are fractions of a percent of the total amount sent (Robins, 2025). Rather than being treated as ‘obstacles’, such alternative methods should be researched further in terms of how they can be scaled to other contexts where there is a weaker culture of alternative remittances and/or higher transfer fees.

Conclusion

This article argued for closer attention to the financial mechanisms and practices which enable remittances to occur and the social relations that sustain them. The paper introduced reciprocal remittances as a widely used but analytically distinct remittance method. Through comparative analysis of Venezuelan migrants in Madeira and T&T, the article demonstrated that similar surface practices, such as ‘sending money via friends’, can signify fundamentally different social and material contexts. The article showed that remittance systems are not only embedded in social relations but actively constitute them. The article challenges the policy assumption that greater integration into formal financial infrastructures will improve efficiency and inclusion. It calls for greater qualitative attention to approaches to quantifying remittances to understand the size, quality, and significance of different informal remittance systems.

Footnotes

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article is funded by the Leverhulme Trust. Grant no. ECF-2022-542.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.