Abstract

In this paper, we explore how commercialised microfinance institutions and banks leverage remittance-related information to assess and provide microfinance loans to households in Cambodia. We argue that (microfinance) debt regimes profitably sustain precarity in the Cambodian translocal context. Building from five studies undertaken between 2014 and 2022, we illustrate our argument through a two-pronged approach. First, we critically unpack the empirical realities of the relationship between migration, remittances, and debt repayment. We show that the lending strategies of microfinance institutions and banks take into account the remittances received by rural households from adult children who have moved to cities or overseas. It is the social obligations within the family to remit money home – or ‘filial debts’ – that are being collateralised. As the monetary expression of these social obligations, remittances serve as a form of what we call ‘translocal collateral’ which (re)constitutes connections among family members across space to mitigate repayment risks for the microfinance industry, often at the expense of the well-being of its borrowers. Second, we contend that these financial institutions’ lending practices – and the development programmes and policies that promote them – rely on translocal strategies of social reproduction that are unstable and fragile. Sudden interruptions in remittance flows can have significant ramifications for rural households, forcing them to deal not only with decreases in income but also looming debts to repay. This should serve as a call for caution among development practitioners and policymakers promoting the leveraging of remittances for financial inclusion.

Introduction

Remittances have long been conceived in the international development community as a strategic tool to expand and promote financial inclusion. Integrating remittances into commercialised financial circuits would, so the argument goes, harness their developmental potential and enhance ‘the financial resilience and economic empowerment of remittances families’ (IFAD, 2022). In more recent years, the digitalisation of remittances has been recognised as a potential accelerator for incorporating the ‘unbanked’, the ‘underbanked’, women, and even the unemployed into ‘formal’ finance. From this perspective, remittances serve as a mechanism to assist migrants and their recipients in not only accessing but also demanding formal financial services and products such as saving, credit and insurance. Recently, there has been a focus on using remittances to evaluate the creditworthiness of potential borrowing individuals and households. By consistently receiving remittances via ‘formal’ channels, banks would supposedly be able to better understand their customers, allowing them to offer additional financial products and services.

In this paper, we explore how commercialised microfinance institutions and banks leverage remittance-related information to assess and provide microfinance loans to households in Cambodia. We argue that (microfinance) debt regimes not only ignore but also profitably sustain precarity in the Cambodian translocal context. We illustrate our argument through a two-pronged approach, which focuses on the parallel rise of rural-urban migration and commercialised microfinance in the country in the past few decades. First, we critically unpack the empirical realities of the relationship between migration, remittances, and debt repayment. Cambodian households in rural areas have long depended on remittances from migrant labourers, using these funds in part to repay microfinance loans, which are prevalent throughout the country (Bylander, 2014; Green and Estes, 2019; Natarajan et al., 2021). We show that the lending strategies of microfinance institutions and banks account for the remittances received by rural households from their adult children who have moved to cities or overseas. Credit officers factor in remittances when evaluating loan applications and often advise applicants to add their remitting adult children to the loan agreement to help with loan repayments. We posit that it is the moral obligations within the family to remit money home – or ‘filial debts’ – that are being collateralised – similar to, yet distinct from, the explicit social collateral of group lending (Schuster, 2015). As the monetary expression of these social obligations, remittances serve as a form of what we call ‘translocal collateral’, (re)constituting connections among family members across space to mitigate repayment risks for the microfinance industry, often at the expense of the well-being of its borrowers.

Second, we contend that these financial institutions’ lending practices – and the development programmes and policies that promote them – rely on translocal strategies of social reproduction that are unstable and fragile. Green and Estes (2022: 1727) call this ‘translocal precarity’, defined as ‘the looming threat that family members’ efforts to support one another might fall apart due to the instability of urban labour markets in tandem with a lack of sustaining infrastructures in rural areas’. Translocal precarity does not only emerge in sites of work in urban settings before travelling home; it also results from social reproduction challenges faced by migrants’ kin and kith in rural communities, including household debt. Sudden income losses can interrupt the flow of remittances that rural families rely on to cover essential social reproduction needs. These often include microfinance debt repayments in the (almost total) absence of any significant social safety nets in rural Cambodia. As such, we critically analyse and call into question the covert, and sometimes overt, promotion and construction of remittances as collateral on the back of translocal householding in the microfinance industry.

The contributions of the paper are threefold. First, it advances a critical literature on remittances and financial inclusion by proposing the concept of remittances as translocal collateral (see for instance the Special Issue by Kunz et al., 2022 in this very journal on the everyday manifestations of the financialisation of remittances). By doing so, it offers a grounded, critical, and translocal perspective on how microfinance institutions apply international development policies and programmes aimed at expanding the financial inclusion agenda, especially the provision of microcredit, on the back of remittances. Second, the paper explicitly focuses on remittances as a new type of collateral that financial institutions, especially microfinance institutions, use to extend their lending. As such, it provides a novel perspective to a critical literature on microfinance, collateral and the creation of ‘collateral substitutes’ (Bond and Rai, 2002: 1), which mostly focuses on group lending (Elyachar, 2002; Roy, 2010; Schuster, 2015), cash transfers (Torkelson, 2021) and, to a lesser extent, Pay-as-you-go (PAYGo) lockout technology (Baker, 2022). Third, the paper draws on the concept of ‘translocal precarity’ (Green and Estes, 2022) to zoom in on the ways in which the re/spatialisation of households’ social reproduction shapes, and is shaped by, the re/spatialisation of finance and collateral in countries heavily dependent on remittances like Cambodia.

This paper is organised as follows. First, we locate the construction and use of remittances as translocal collateral by microfinance institutions and banks in Cambodia within the critical literature on remittances and micro- and global finance. Second, we introduce the five research projects that the six authors were involved in between 2014 and 2022, which this paper draws on. We subsequently provide a critical account of the re/spatialisation of finance and collateral in Cambodia by, first, evidencing the connection between migration, remittances, and debt repayment and, second, grounding empirically our concept of remittances as translocal collateral. Finally, we discuss how the fragility of remittances as translocal collateral is exposed in times of crisis, before offering some concluding remarks.

Translocal livelihoods on credit

Microfinance – and subsequently financial inclusion – has long been framed as a key development project with the potential to make poverty history. However, after almost five decades of expansion, universalisation, and commercialisation, the capacity for microfinance to help its clients increase their revenues and spending, build assets, and improve health status and other social outcomes, has been seriously called into question (Duvendack and Mader, 2019; Mader, 2018). Instead, there is now strong evidence from critical scholars in geography (Brickell et al., 2020, 2023; Green and Estes, 2019; Harker, 2020; Rankin, 2013), anthropology (Kar, 2018; Schuster, 2015), development studies (Taylor, 2012), international political economy (Bernards, 2022; Soederberg, 2014), and other cognate disciplines that microfinance works at ‘financialising poverty’ (Mader, 2015: 80). Specifically, microfinance renders marginalised and low-income workers, as well as unemployed or underemployed people, dependent on credit for their social reproduction (Soederberg, 2014). This shift towards relying on debt for social reproduction is not a natural market evolution or a voluntary choice. Instead, it is a deliberate strategy by neoliberal states and capitalists to establish monetised debt relationships and their associated disciplinary and exploitative aspects on the working poor (Green, 2023a; Soederberg, 2014). By dismantling welfare systems and tailoring legal and regulatory frameworks to benefit lenders, ‘debtfare states’ have replaced social welfare with mechanisms that enforce the survival of the surplus population through debt. The expansion of this market, where profits are derived from the further exploitation of the unemployed and underemployed, highlights the emergence of what Soederberg (2014) terms the ‘poverty industry’.

Financial inclusion has contributed to rendering poverty favourable to the logic of finance-led capital accumulation in various ways. Mader (2014, 2015) shows that it has done so by (1) mobilising narratives that portray finance as empowering and liberating (see also Green, 2023b; Schwittay, 2014); (2) creating financialised material relations between wealthy lenders (owners of capital) primarily in the Global North and poor borrowers (sellers of labour power) primarily in the Global South (see also Aitken, 2015; Schuster, 2019); and (3) constructing layers of financialised governmentality which have a disciplining effect on not only investors and microfinance institutions but also loan officers and borrowers (see also Young, 2010). This behavioural (re)orientation of every single actor involved in microfinance has been facilitated by a wide range of technical means, from monitoring and rating devices at the level of institutional investors and capital providers, and financial metrics at the level of MFIs, to intense reporting and constant visits at the level of loan officers, and public shaming and social capital devices at the level of borrowers (Mader, 2014).

Building on this latter insight, we are particularly interested in the contested construction of collateral as a technology of control that makes people repay their loans (Green, 2019; Natarajan and Brickell, 2022). Around the world, collateral security has long underpinned the private governance of global financial markets, functioning as ‘an additional or cumulative means for securing the payment of the debt’ alongside the principle promise (Riles, 2011: 2). Perhaps the most innovative aspect of the microfinance industry has been its active development and use of ‘collateral substitutes’ (Bond and Rai, 2002: 1). Microfinance famously eliminated physical collateral requirements by turning social ties of dependency and obligation into ‘social collateral’ through the technology of the joint-liability group loan (Schuster, 2015). Group lending with joint liability allowed microfinance institutions to circumvent income and asset requirements for borrowing by pushing group members to draw on their social ties to monitor and enforce loan repayment.

Proponents of microfinance originally celebrated the use of mutual aid among women and communities to collateralise loans. As Schuster (2014: 564) argues, ‘microcredit’s purchase in development circles has in large part been due to its promise to correct a gender injustice, namely, that men had physical collateral and women did not’. However, more critical development scholars have called microfinance’s use of social collateral into question. They have argued that it has contributed to the commodification of borrowers’ – and especially women’s – social relationships of reciprocity, obligation, and care within families and communities (Elyachar, 2002; Kar, 2017; Karim, 2011; Roy, 2010). By creating social collateral through technologies like the joint-liability group loan, the microfinance industry has actively transformed, regulated, and exploited borrowers’ interdependency to secure the credit-debt relation (see also Green and Estes, 2019; Maclean, 2010). This exploitation has in turn facilitated the expansion of the financial frontier across the global south (Bernards, 2022; Roy, 2010).

The concept of social collateral is helpful for our present argument because it shifts the analytical focus of ‘the social unit of debt’ away from the individual and onto the relations of interdependency and obligation in which debtors are embedded (Schuster, 2015: 8). With group-based lending, for instance, borrowers are not individually creditworthy; rather, it is their group membership that marks them as creditworthy. Even in contexts where the microfinance industry has moved away from joint-liability group loans as the norm, instead relying on more traditional forms of collateral like land titles, relations of dependency and obligation within families continue to underpin debt repayment (Green and Estes, 2019; Kar, 2017). In this sense, the concept of social collateral helps to highlight how relations of dependency and obligation can both substitute, but also complement, other forms of collateral security.

In this paper, our goal is to expand the concept of social collateral to include the social ties that connect together members of translocal households. The translocal household is based on relations of dependency, obligation, and care that sustain family members who work and reside in different places. While scholars of transnational migration have highlighted how these connections often extend across national borders, the concept of translocality also includes relationships between places within the same country, such as in rural to urban migration (Brickell and Datta, 2011; Lawreniuk and Parsons, 2020). In many contexts today, translocal connections underpin credit-debt relations, as migrant family members remit money home to repay household debts (Green and Estes, 2019; Harker, 2020).

We contend that it is the obligation to remit money home which is being used as a collateral substitute by the microfinance industry in Cambodia. Around the world, remittances serve as a vital element in the social fabric of translocal households and their communities (Carling, 2020). Zharkevich (2019) argues that remittances constitute the very ‘substance’ of relatedness for spatially-stretched households, fostering bonds of intimacy. This perspective illuminates ‘money’s role in delineating the boundaries of contemporary families that often depart from conventional norms of physical copresence’ (Zharkevich, 2019: 886). Such approaches challenge purely economic perspectives that view remittances as simple one-way transfers, instead recognising that money transfers are deeply embedded in, and dynamically shaped by, the relationships between migrants and kin left behind (Åkesson, 2011). Moreover, ethnographic research has demonstrated that remittances are embedded in culturally specific ‘scripts’ of gifting, reciprocity, and mutual aid (Carling, 2020). These are shaped by kinship structures, as well as gender norms, ideologies of care, religious orientations, and moral frameworks. Migrants are often expected to fulfil moral roles and obligations – as dutiful sons or daughters, caring parents, or ‘responsible persons’ – through the act of sending money (Åkesson, 2011; Simoni and Voirol, 2021; Zharkevich, 2019). The ways that family members receive and use remittance money is also morally evaluated, with expectations around gratitude, appropriate spending, and reciprocal support. Fulfilling moral obligations to kin through remittances can enhance migrants’ sense of personal dignity, particularly in cases when migrants face undignified working conditions and discrimination in their daily lives (Thai, 2014). However, remittances can also strain relationships within translocal households, particularly when flows are interrupted or when moral expectations around reciprocity go unmet. Migrant family members who do not send remittances can be framed as ‘ingrates’ or otherwise derided (Åkesson, 2011: 334). Remittances can also reinforce inequitable gendered divisions of labour, as it is often women who shoulder the burden of caregiving and emotional labour within dispersed family networks (Hall and Posel, 2019). These tensions surrounding remittances reflect broader dynamics of intra-household negotiation, where entitlement, duty, and affection are continually contested (Neves and Du Toit, 2013).

Drawing on these insights, we argue that the microfinance industry leverages migrants’ moral obligations to remit as a form of social collateral, a process which we aim to capture with the concept of translocal collateral. This concept helps to explain what has become an increasingly common practice within the global financial inclusion agenda. Across the world, remittances are now deemed an important entry point to integrate the unbanked and underbanked into the formal banking system (see for instance Anzoategui et al., 2014; Global Migration Group, 2017; IFAD and World Bank, 2015; Isaacs, 2017; UNCTAD, 2015). They serve as a means to assist migrants and their families in not only accessing but also demanding formal financial services like bank accounts, loans, insurance, mortgages, and credit cards (Ardic et al., 2022; IFAD and World Bank, 2015). Efforts have also been made to incorporate remittances into the evaluation of the creditworthiness of recipients and migrants (Isaacs and Watson, 2021; UNCDF, 2018). By consistently receiving remittances, banks can better understand their customers, allowing them to offer additional financial products and services. The development of such ‘remittance-linked’ and ‘remittance-backed’ financial products is considered crucial to leverage remittances for financial inclusion (Guermond, 2023). Remittance-linked products include savings accounts, insurance, and loans available to recipients, while remittance-backed products, such as mortgages and loans, use remittance receipts to assess and provide credit.

Such policy efforts to use remittances as translocal collateral are shaped by broader processes of financialisation and marketisation (Datta, 2012; Guermond, 2020a, 2020b; Kunz et al., 2020, 2022; Mullings, 2022; Paudel, 2022; Smyth, 2021). For example, Bakker (2016) contends that initiatives aimed at leveraging remittances to democratise finance and transform migrant resources into financial flows are part of broader efforts to extend the reach of the market under the guise of development (see also Cross, 2015). This subordination of remittances to the interests of financial markets (re)produces a gendered hierarchy between remitters and remittance recipients as well as between remittance-receiving and non-transnational families (Kunz and Ramírez, 2022). It also reflects ‘longer histories of extraction and racial dispossession within the global financial system’ (Mullings, 2022: 746; see also Paudel, 2022). At its core, the attempt to marketise remittances is based on fostering financial discipline and control over remittance subjects, ensuring that they help with debt repayments to sustain the accumulation of finance capital (Kunz and Ramírez, 2022; Mullings, 2022).

However, using remittances as translocal collateral also involves contradictions and failures, and faces repertoires of covert and overt resistance (e.g. Guermond, 2020a; Kunz et al., 2022; Zapata, 2013). For instance, drawing on field research with remittance recipients in Ghana and Senegal, Guermond (2020a) shows that any attempts to channel remittances away from so-called ‘informal’ financial circuits face differentiated forms of contestation, namely reluctance, refusal, and dissent. Moreover, in Cambodia, as we will show in the next sections, such development initiatives and programmes to produce links between migration, remittances, and debt repayment often exacerbate translocal precarity. As Cambodian households have become dependent on migrant remittances partly to service (microfinance) loans in the absence of sustaining infrastructures in the countryside, they have also become exposed to structural uncertainties, insecurities, and fluctuations within wage-labour markets (Bylander, 2014; Green and Estes, 2019, 2022, Natarajan et al., 2021). In this regard, mobilising remittances as translocal collateral often has the perverse effect of sustaining precarity rather than fostering economic development.

Researching the re/spatialisation of finance and collateral in Cambodia

This paper draws on five different research projects that the six authors have been involved in between 2014 and 2022. By bringing these studies together, we aim to provide a detailed picture of the lived realities of everyday finance, migration, and livelihood-making in Cambodia. While the critical literature on remittances is still prone to examining both ends of the remittance process separately (Guermond, 2021), we underscore the critical analytical significance of focusing on both remittance sending and receiving in the context of ‘translocal precarity’. Guermond, Brickell, and Parsons draw on original research conducted between October 2020 and December 2022 in three villages in the provinces of Prey Veng, Battambang, and Kampong Cham. While this project, entitled Depleted by Debt?, used a wide range of methods, in this paper, we draw mostly on a quantitative household survey of 621 respondent complemented by 1161 individual questionnaires, as well as semi-structured interviews with local and national stakeholders, including credit officers, microfinance institutions executives, and ministry representatives.

Brickell and Lawreniuk draw on a research project tracing the impacts of Covid-19 on female garment workers in Cambodia. The project, entitled ‘ReFashion’, employed longitudinal methods (Brickell et al., 2024) to repeatedly engage with a cohort of 203 female garment workers between October 2020 and January 2022. In this paper, we draw from a complementary set of three rounds of quantitative survey data and three rounds of qualitative interview data collected during different phases of the pandemic. Our quantitative survey captured monthly data on work and income, as well as financial and wellbeing impacts on worker’s immediate household and rural-based families, whilst our semi-structured interviews permitted scope to discuss women’s experiences in fuller detail. We also draw on our semi-structured interviews with industry representatives, including trade union leaders.

Green draws on two research projects in Cambodia to help inform the arguments in this paper. Between 2014 and 2017, in a project titled ‘Landscapes of Debt: A Political Ecology of Microfinance and Land Titling Programs in Cambodia’, he carried out 20 months of ethnographic research in a rural community, conducting participant observation and interviews with microfinance institutions and banks, farmers, and other community members. From 2021 to 2022, in a follow-up project titled ‘The Financialization of Agrarian Landscapes in Cambodia’, Green conducted research in collaboration with a Cambodian research organisation about the microfinance industry. This project involved interviews with national banking regulators, microfinance industry leaders, and foreign investors in Phnom Penh, as well as farmers, credit officers, bank branch managers, and informal lenders in two rural communities. Estes draws on 20 months of research conducted between 2014 and 2017 in southern Cambodia. As part of a broader ethnographic project, she conducted participant observation of everyday life in a rural community and conducted interviews with over 40 youth in order to examine intergenerational relations and young people’s changing livelihood strategies.

The re/spatialisation of finance and collateral

Migration, remittance sending, and debt repayment in Cambodia

Before, people, especially rural people, relied heavily on farming production and there wasn’t any alternative work . . . That was in the past . . . Now most people have at least one or two [household members] who work in the city or the town. And in the community, they no longer rely only on cropping. (Interview with Ministry of Rural Development representative, February 2022, DBD project)

Following an explosive expansion since the early 2000s, microfinance has become an integral dimension of the household economy in Cambodia. The Cambodian microfinance sector is diverse, encompassing both formal and semi-formal institutions of varying sizes. These institutions offer different loan terms and requirements for borrowers. Between 2000 and 2019, the number of borrowers increased significantly, from approximately 175,000 to 2.6 million people. In 2019, Cambodian borrowers held over 10 billion USD in microloans, which made Cambodia one of the world’s largest microfinance industries in terms of borrowers per capita. Additionally, the average loan size in Cambodia – 3804 USD – far exceeded the global average and even surpassed the country’s GNI per capita (CATU, 2020: 1).

The rise of microfinance has occurred in close relation to increases in both migration and remittances. From a base of very low mobility in the early 1990s, labour migration has rapidly accelerated, driven by Cambodia’s structural transformation from a rural and agricultural-based economy to an increasingly urban, industrial, and service-based one (see Lawreniuk and Parsons, 2020). The garment sector, based mainly in and around Phnom Penh, has represented the most significant pull factor in the past 20 years, employing around a million workers, mainly women, from rural areas (ILO, 2018). Nearly one quarter of the Cambodian population (approximately 4.1 million individuals) is now a domestic migrant (UNESCO, 2018), in addition to an estimated 1 to 2 million further international migrants, who work primarily in Thailand (IOM, 2020).

Migrants, who are predominately adolescent and adult children, play a significant role in supporting the economic viability of their rural households through their remittances (Zimmer and Van Natta, 2018). At the time the DBD project’s quantitative survey was conducted – between September and November 2020 – a substantial 76% of migrants (n = 457) from the three villages were actively sending remittances. Remittances to all household types were substantial, averaging over 2269 USD per annum. These incoming funds were crucial to rural livelihoods of all types – that is, farming-only households, mixed livelihoods households, and non-farming households – especially given their scale in comparison to rural incomes, with GDP per capita averaging only 1735 USD annually as of 2022 (Ly and Rastogi, 2022). In the ReFashion study, 65% of the female garment workers in the sample regularly sent remittances to at least one other household in the first round of the survey (Oct/Nov 2020). Before the pandemic, the average amount of money remitted by workers comprised 38% of their basic wage, or 30% of their average income with overtime and other bonus payments added. Corroborating the data from the DBD study, the most common reported uses of these remittance payments by recipient households included daily living (85%), health or medical expenses (41%), childcare (31%), and loan repayments (27%).

As these data illustrate, while remittances are often used to directly cover the costs of basic needs, they also play a further indirect role of crucial importance to rural households: facilitating and servicing household debts related to these same expenditures. The role of debt – and remittances to service that debt – is increasingly unavoidable when it comes to farming, as rural prices have risen, mechanisation has increased, and the use of chemical fertilisers and pesticides has proliferated (Brickell et al., 2018; Green, 2022; Guermond et al., 2025). However, as the DBD study and other work has shown, microfinance/bank debts are taken on to pay not only for ‘entrepreneurial activity’, including asset purchases for agriculture. Households also borrow from banks and MFIs to cover everyday social reproductive costs, including for food, health, education, and lifecycle events, reflecting the significant social protection deficit in Cambodia (Brickell et al., 2023; Green, 2023a; Green and Estes, 2019).

Taken together, the above analysis demonstrates how the nexus of migration, debt, and remittances plays a vital role in supporting the translocal livelihoods of rural communities in Cambodia. Debt is an essential part of life among rural households, whilst migration and remittances are crucial tools in meeting debt repayments.

Migrants’ obligations to remit are often underpinned by Theravadan Buddhist conceptions of filial piety. Buddhism is the state religion of Cambodia and is practised by around 95% of the population (NIS, 2025). Although the idea of filial piety is not discussed extensively in canonical Theravadan Buddhist texts, in practice it is a significant tenet of Buddhist ethics across the Theravadan world (Kourilsky, 2022). Cambodian monks – who play an important role in shaping popular moral discourses – frequently emphasise the importance of filial piety through sermons, songs performed during life cycle rituals, written texts, and more recently, social media posts (Walker, 2022). In these teachings, children are framed as indebted to their parents, particularly their mothers, for their existence and for the work of raising them. The Pali term koun, which more widely refers to ‘virtue’ or ‘merit’, is used to describe this ‘debt’ (Kourilsky, 2022). While it is considered impossible to ever fully repay this debt, pious children acknowledge it (doeng koun; literally ‘know [one’s] debt’) and attempt to address it through both general forms of respect and obedience as well as specific means. Historically, the most significant way for sons to repay their filial debt was through monastic ordinance. Daughters, who were barred from ordaining, were expected to address their debt through caretaking activities, particularly looking after their parents in their old age.

Due in part to these notions of filial piety, children have always played a significant role in sustaining their natal households. However, as both ideas about filial piety and households’ needs shift, so too have children’s contributions. Recently, influential monks have broadened notions of filial piety, framing the ideal child as ‘a model student and productive citizen, industrious to a fault and obedient to parents, teachers, and the state’ (Walker, 2022: 7). This newfound emphasis on filial children’s productivity – and its implicit economic output – squares with monetary demands on households as historical agricultural livelihoods have become increasingly untenable, state services remain scarce, and debt levels have risen. It is becoming more imperative for children to realise their filial debts by securing incomes and sending remittances to their parents than by engaging in non-monetised activities like performing labour at home or entering the monkhood.

Based on ethnographic research in a rural community, Estes found that older adults frequently stressed the importance of this monetised obligation. For instance, a farmer in her late 50s explained that: In my day, people didn’t need much money. Good children stayed near their parents. They helped them farm and took care of them. But now everything is expensive, everyone needs money to pay for things, and everyone is in debt. So, children have to leave so they can find money to send to their parents. In the past, children helped with their energy, and now they help with money. (Interview, October 2017)

As a retired teacher put it, ‘It is good to have many children. They are like having a bank account. Children will be there to help provide money for you when you are old’. As this quote indicates, financial logics have come to shape the very framework through which filial piety is conceived.

The youth that Estes worked with recognised this obligation and consistently planned to remit money once they were employed. They often explicitly referred to the notion of filial debt when discussing their intentions. For instance, a secondary school student commented that ‘In the future, I’ll send money to my parents. It’s really important to care for them. Khmer people know our debts’. Others evoked their emotional connection to their parents. ‘In the future, I’ll send money to my parents and help them forever when I have a job. I don’t want life to be difficult for them. I love them and they’ve helped me’, another student shared. While some young people worried about the pressure that their obligations to their parents put them under, the majority felt that addressing their filial debt was a meaningful part of living a good, moral life.

Kin and community members reinforced the need for young people to remit through moralising discourses that compared ‘good’ children with ‘bad’ ones. For instance, a retired civil servant in his 60s told Estes that, ‘Good children always think of their parents and care for them by giving them money . . . Bad children don’t give their parents money. It’s very important for people to have good children, otherwise being old is hard’. Parsons and Lawreniuk similarly found in their research that ‘a failure to fully comply with remittance duties is discouraged to the point of disdain, with migrants who remit nothing or who remit less than similarly aged siblings liable to be branded by family members as “lazy” or “selfish”’ (Parsons et al., 2014: 1376).

Crucially, microfinance credit officers are themselves embedded in these cultural discourses and thus recognise how filial piety can be mobilised to secure repayment. As one officer told Green, children help their parents repay loans because ‘if they don’t, neighbours will call them an ungrateful child who has violated a filial debt’. Such pressures translate directly into financial reliability: the moral economy of filial piety becomes a mechanism of credit discipline. In this sense, filial debt is effectively collateralised – not through assets or land, but through children’s remittances and the moral sanction attached to their failure to pay. We further unpack this dynamic of remittances as translocal collateral next.

Remittances as translocal collateral

The majority of MFI loans in Cambodia are nominally individual, and require a land title as formal collateral. Yet, based on interviews with dozens of credit officers and CEOs in the industry for his studies, Green found that a consistent and widespread practice of the industry is to assess a household’s entire income as part of the loan application. For example, the chief marketing officer of one of the largest MFIs in the country, who had previously worked as a credit officer, said that ‘When people borrow from an MFI, they borrow as a household. When they borrow, it is based on household income. Not the individual income’ (May 2022, Financialization of Agrarian Landscapes project). In particular, microfinance institutions and banks take into consideration rural households’ remittances from adult children who have migrated to urban areas or abroad in order to mitigate their lending risks. Minimising risk is an institutional priority for MFIs and banks, who must ensure a stable return on investment for their shareholders and investors (Green, 2023a; Green et al., 2023). Remittances thus serve as a form of translocal collateral, connecting family members across space while protecting the interests of MFIs. 1

Remittances are important for MFIs when calculating lending risks due to the instability of agricultural livelihoods. A former credit officer who had worked in the industry for 10 years explained that: Few people can repay their loans through farming. Animal husbandry like pig farming is difficult because of the cost of buying the piglets, the feed, medicine, and then the cheap price when people go to sell. (September 2017, Financialization of Agrarian Landscapes project)

Given that farmers present such a high risk to lenders, MFIs and banks prefer to lend to farming households that have access to more stable forms of income. In most cases, this means that they prefer households where at least one member of the family holds a wage labour job. A credit officer in a rural area of southern Cambodia explained: Families with steady incomes are the best to lend to. For this reason, my institution really likes to lend to families that have children working in factories. If they have factory jobs, then the family is likely to repay the loan on time and consistently. It is because factory workers have steady incomes, not like small traders. (July 2017, Landscapes of Debt project)

Credit officers not only take remittances into consideration when making loan assessments. They go further by actively encouraging loan applicants to include their adult children on the loan contract as co-signers, both due to their steady incomes and because credit officers are aware that children are obligated to help their parents due to filial debt. When migrant children sign onto the loan formally as a co-signer, it provides an extra layer of risk mitigation, as the children are then legally responsible for repaying the loan in the event of the main borrowers’ default. For example, on one occasion in his Landscapes of Debt project, Green observed a credit officer tell a loan applicant, who was a rice farmer with only seasonal income, that his son needed to be on the loan, because his son worked construction in Phnom Penh and earned a regular income.

However, it is often impractical for migrants to return home to sign a loan contract. In such situations, MFIs and banks will request a pay slip, or in some cases, just a verbal confirmation that the adult child will help support their parents’ loan repayment via remittances. For example, in response to a question about whether remittances are assessed as income in a loan application, the branch managers of the bank in Battambang replied that: Yes, we can consider the income earned by other family members away from home. We just need, for example, a salary slip. The least we should do is to talk to that family member to check their repayment ability. This is not 100% correct, but we try to collect as much information as possible. Sometimes, the family does not have the ability to repay, but they have migrant children who can repay for them, so we need to check with those children to confirm. We also check their passport, work permit, etc. (May 2022, Financialization of Agrarian Landscapes project)

The problem for lenders is that is difficult for credit officers to verify incomes of migrants working in the city or abroad in countries like Thailand. One foreign consultant, who has worked consistently to raise awareness about over-indebtedness in Cambodia, commented that: So, what’s happening is the MFI is lending effectively to people they don’t know, no one did a financial analysis of the son. They look at the woman, her remittances, but they don’t look at the end borrower. The only reason they do this is because the son doesn’t have land [for formal collateral], it’s his mother who does. (April 2022, Financialization of Agrarian Landscapes project)

For this reason, some institutions will restrict the proportion of household income that can come from remittances when making their loan assessments. They do this to mitigate the risks inherent in lending based on remittances that they cannot verify. For example, the same bank branch managers in Battambang clarified how they assessed income earned in Thailand:

We cannot include these incomes because we cannot manage their income-generating activities away from the village. For our technical assessment, we look at their economic activities in the village they intend to use the loan for. Incomes from outside are considered ‘other incomes’ and they cannot be over 20% of the family’s income.

I heard some families depend on family members working away from home to send money home to repay loans.

If they migrate legally, we can look at their account statement and their migration document. However, this type of loan is high-risk one, so we don’t prioritise that.

Why is it high risk?

We cannot see with our own eyes, so we don’t know if they lie. If they say they earn $2000 a month, we cannot tell if they lie. If they are in the community, we can get to see their employment contract and salary slip (May 2022, Financialization of Agrarian Landscapes project).

There are thus trade-offs to using remittances as a form of translocal collateral. On the one hand, remittances potentially provide a more stable source of income that allows MFIs and banks to lend to farm households. On the other hand, it is difficult to verify remittance income, and this type of income, especially when it is linked to foreign migration, can be risky if migrants lose their jobs. Credit officers are acutely aware of these trade-offs, captured by the phrase ‘dare to assume an income and lend people money’ (ហ៊ានឆ្នៃមុករបរនិងឱ្យគេខ្ចីលុយ). They nonetheless practise a form of what Bylander (2023) after McGoey (2019) refers to as ‘strategic ignorance’ with regards to the risks of exploitation and unfreedom that migrants may face in migrant destination countries. 2 As we explain in the remainder of this paper, MFIs and banks regularly dare to provide loans backed by remittance incomes, because these risks are ultimately borne by indebted families, whose livelihoods are rendered more precarious as a result.

‘The tap turned off’: The fragility of remittances as translocal collateral in times of crisis

How the use of remittances as translocal collateral profitably sustains precarity was cruelly exposed during the Covid-19 pandemic. In previous years, rising employment in the garment sector provided a steady cash flow of income directed to the repayment of loan instalments. By May 2020, as global brands and retailers cancelled contracts with their factory suppliers due to the pandemic, up to half of the factories in Cambodia had suspended production for some period, putting hundreds of thousands of women out of work on a temporary or permanent basis (Lawreniuk et al., 2022). The potential for the crisis in employment to spill over into a crisis of insolvency, foreclosures, and confiscation of collateral was immediately raised as a pressing concern by workers and union groups (CATU, 2020; Lawreniuk, 2020). Garment suppliers in Cambodia have long been reluctant to provide their employees with long-term or permanent employment contracts – ‘unlimited duration contracts’ [UDCs] in Cambodia labour law parlance – preferring instead the more precarious offer of rolling 3- and 6-month fixed-term contracts. Under these contracts, employers have no responsibility to provide severance pay or benefits in the event of job forfeiture.

Notoriously a ‘footloose’ and flighty form of capital (House of Commons, 2019), the global garment industry generally exemplifies ‘routine volatility . . . accepted as an essential feature of contemporary capitalism’ (Bair, 2019: 71). Indeed, fashion retailers and sourcing agents are renowned for optimising profit by ‘chasing the cheap needle around the planet’ (House of Commons, 2019), searching for lowered pay, protections, and regulation across production territories. As scholars of production networks have argued, dis- and re-articulations of supply chain nodes are part of the ongoing reproduction of capitalist relations as buyers, suppliers, and intermediaries fine-tune margins (Bair and Werner, 2011).

In light of the Covid-19 crisis, the coupling of microfinance repayment to remittance transfers from an inherently unstable sector has deepened translocal households’ precarity. Over the first 10 months of the pandemic to October 2020, the ReFashion study found that the average garment worker’s income fell by 25% due to the ongoing impacts of rolling suspensions of production lines. The compulsion to make debt repayments, however, remained (Res, 2021). With the vast majority of existing commercialised loans collateralised against land holdings, debt repayment emerged as one of the most immediate financial worries of workers. As Ratana, a worker in the ReFashion study attested, At first [when I heard about the outbreak of Covid-19], I was worried that there would be no work since it affected countries that we imported raw materials from. I was worried. Most of us are indebted to microfinance institutions. It would be really hard if we had no income. Around 80% of workers like me are indebted. (Ratana, garment worker, December 2020, ReFashion project)

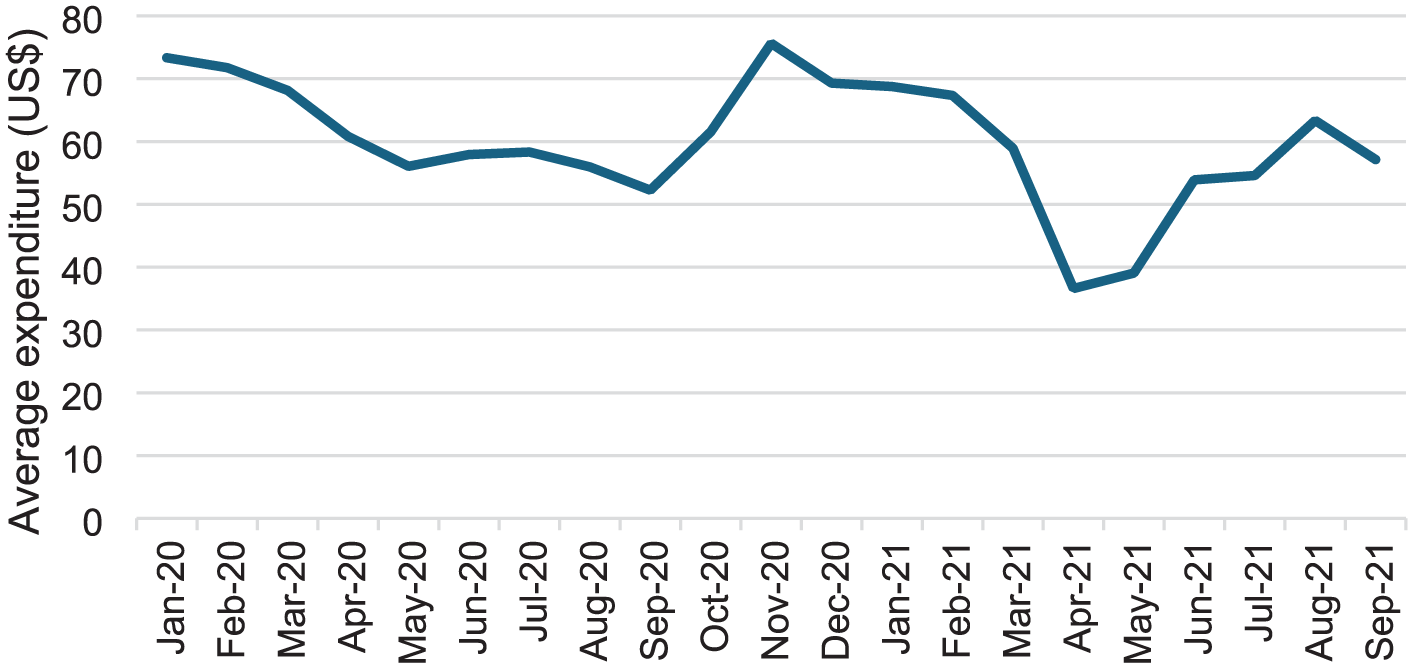

As their income collapsed, many were under immense pressure to finance repayments that they could no longer afford. In fact, during this period of acute crisis, garment workers faced a unique double debt burden: as direct borrowers of microloans, and indirect financers of family-held debt elsewhere. Yet as working hours and consequent income shrank, the ability of workers to continue to send remittance payments was also sorely challenged. As such, a hidden impact of the pandemic’s immediate ripple through global supply chains was the consequent multiplier effects of this significant loss of employment and earning upon these remittance recipients. Before the pandemic, for example, 70% of the female garment workers in the ReFashion sample regularly sent remittances to at least one other household. By Mar/Apr ’21 the number of workers regularly sending money had declined to 51%, and by Nov ’21/Dec ’22, it had declined still further to just 48% of women. The average amount of remittances also dropped sharply among those who continued to send, from a pre-pandemic peak of $73 each month on average in January 2020, to lows of $52 in September 2020 and $37 by April 2021 (see Figure 1).

Average remittance expenditure among remittance-sending workers, Jan ’20–Sept ’21.

In response to the credit crisis slowly gathering momentum for households across the rural-urban divide, the National Bank of Cambodia [NBC] issued guidance in March 2020 to encourage lenders to assist clients ‘facing actual impacts’ from the pandemic, particularly by pausing repayments of principal. However, its recommendations to lenders were voluntary rather than binding, and had to be agreed on a case-by-case basis (for a fuller discussion of the shortcomings of the loan restructuring programme, see Res, 2021). As such, many lenders refused to comply with the directive and few workers reported receiving any benefit, despite requests to lenders and agents. As Sina described: I asked [the microfinance lender for help] but they did not agree and demanded me to pay the full price. If we are late just one day, we will be punished of around US$20. If we choose not to pay, they will confiscate our property as stated in the contract. Therefore, I was trying so hard to ask help from my sister and relatives in order to pay them . . . No matter what we said, they just did not agree. All they know is paying them the full price and on the due date. (Sina, June 2021, ReFashion project)

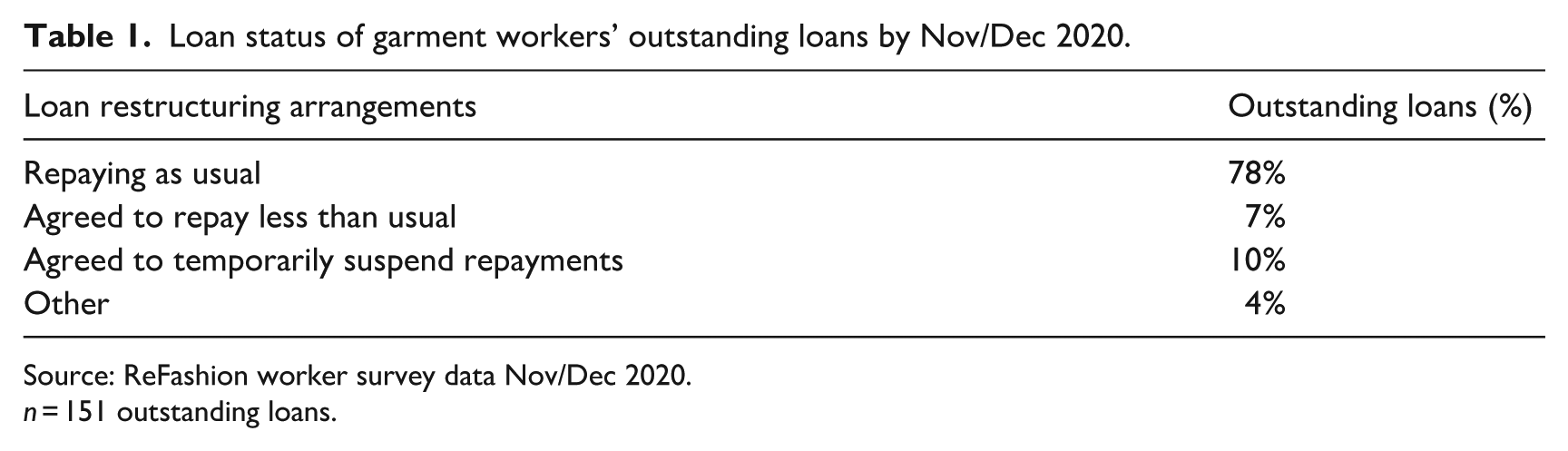

Indeed, by December 2020, 78% of workers reported that they were compelled to repay loans as usual despite the significant shortfall in expected income experienced (see Table 1).

Loan status of garment workers’ outstanding loans by Nov/Dec 2020.

Source: ReFashion worker survey data Nov/Dec 2020.

n = 151 outstanding loans.

With income severely reduced on several fronts of migrant work, debt repayments were already under significant strain when the pandemic proper finally reached Cambodia in March 2021. In response to a spike in cases, initially slow but subsequently surpassing 1000 cases a day by June, the Cambodian government enacted a series of strict policies restricting movement of the general populace, and then at times in designated zones (e.g. Phnom Penh and Poipet by the Thai border) from April 2021. In these ‘Red Zones’, 300,000 people at one point were unable to leave their homes except for medical emergencies, COVID-19 tests, or vaccinations (Tatum, 2021). Across the country as a whole, travel bans and curfews saw labour migration in a usually hyper-mobile country come almost to a standstill and the flow of remittances with it. As a representative of a major microfinance organisation explained: We had a very challenging year . . . basically the tap of cash just stopped. So, tourism, garments, and trade with borders closing, just like the tap turned off. You have a poor farmer who is a rice farmer who depends a lot for his income on his daughter working in the garment sector in Phnom Penh. He wasn’t getting his monthly remittances from his daughter anymore. Migrant workers [sending home money] from Thailand - all of that turned off. The trickle down was widespread and significant. We did some research with borrowers, and it was bad. They had lost 30%, 40% of their income. (Chamroeun Microfinance Ltd senior representative, February 2022, Depleted by Debt project)

Despite microlenders targeting rural households with migrant family members for loan provision, thus acutely aware of the centrality of translocal remittances in household financial capacity, few were as quick to take this into consideration when the tap directing this steady cash flow from urban income turned off. At the height of the crisis, for example, Sokny, a female worker in the ReFashion study cohort, found herself confined to her room in one of Cambodia’s strictest lockdown areas (a ‘Red Zone’), unable to leave her home to attend work in her factory. Her own internment and its implications for the household’s income and economic security were not considered when her father, who relied on her remitted income to repay a loan, tried to restructure his repayment obligations in line with the NBC’s directive, as she described: For the bank, I am responsible for paying the debt but the debtor is my father who lives in my hometown. We asked the bank for exceptions to pay since I live in the Red Zone but the bank did not accept it because the debtor is my dad, they did not care about who works to pay off the debt. So, we have to pay the debt. (Sokny, June 2021, ReFashion project)

The perils for workers and rural families were rendered more acute by the simultaneous drying up of additional lending itself. In the absence of reliable social protection coverage to help them cope through periods of crisis, households in Cambodia are accustomed to relying on microcredit loans to smooth consumption in times of crisis, under what Green (2020) argues represents a ‘debtfare’ model of social security (see also Soederberg, 2014). Many are also habituated to the practice of ‘credit circulation’ or ‘bongvil luy’ (Res, 2021: 62), relying on new lending to effectively refinance existing repayments when circumstances make current obligations untenable. Yet with lenders attentive to a potential contraction in defaults and an increase in the historically low rate of loan non-performance, the previously insistent provision of credit to migrant workers and their families rapidly dried up. Data from the National Bank of Cambodia evidence further how formal lending sharply contracted during the pandemic, with the rate of credit growth to households falling from ‘12.6 per cent in 2019 to a negative contribution in 2020 for MFIs’ (NBC, 2021: 23). Otherwise put, the volume of lending decreased. As Malis described, during the height of the pandemic: Firstly, some banks don’t approve the loan to workers because they are afraid whether or not our factories will be closed and the workers will lose their jobs from the factory. Also, we are not sure whether or not our factory can continue. Before, they gave a loan to workers without too much consideration, but now they take it seriously. They ask for more information from the workers because the factory can close any time without alerting the workers in advance, so getting a loan from the bank for our daily expenses or do anything else is harder and they concern more. (Malis, November 2020, ReFashion project)

Thus, many households found that the previously reliable supply of microfinance itself turned off, at precisely the moment it was most needed.

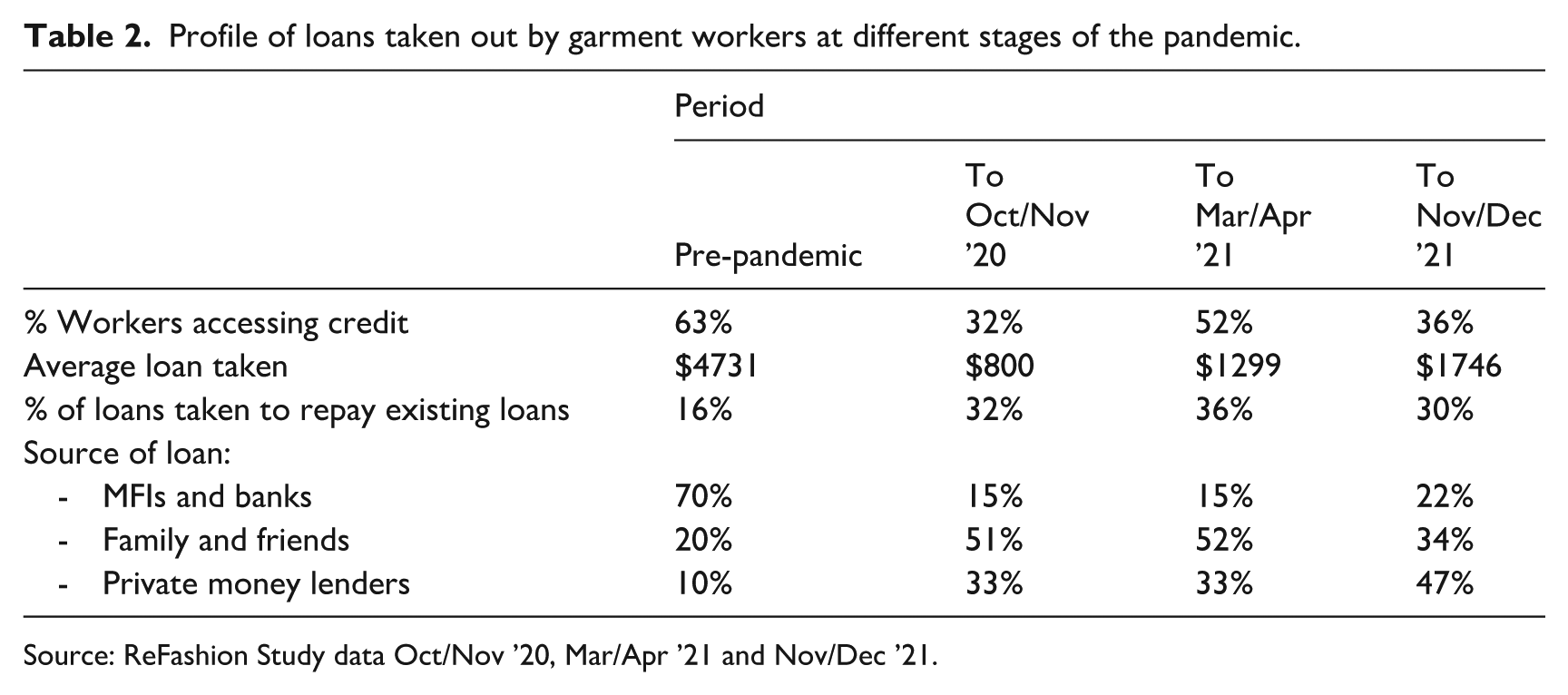

Instead, therefore, households were compelled to adopt a number of more adverse strategies to help manage the compulsion of debt repayment during this period of fiscal distress. For example, within our ReFashion Study, respondents explained that while the practice of bongvil luy remained important, the profile of new lending changed significantly, as Table 2 demonstrates. This shows that access to credit remained a critical coping mechanism for large numbers of workers through the pandemic, particularly around the period of the harshest lockdowns in April 2021, by which time more than 52% of workers had taken on new loans averaging more than 1000 USD each. Notably, the number of loans taken out to repay existing loans steadily increased through the pandemic, from 16% to 36% by April 2021. With formal lenders unwilling to gamble on the increasingly unstable salaries of migrant workers, however, informal sources of lending became the most important source of credit for garment workers. Indeed, by December 2021, private moneylenders – often unscrupulous loan sharks charging excessive interest – accounted for 70% of all new borrowing, far up from the 10% pre-pandemic baseline. Where microfinance lenders in Cambodia often claim to be saving customers from the usurious practices of private lenders (Green et al., 2023), during the pandemic they delivered households unto them in droves. These findings are corroborated by a larger-scale survey of waged workers (n = 671) that concurs that the Covid-19 ‘period has seen a tendency for new loans to shift towards informal sources’ (Angkor Research and Future Forum, 2020: 4; see also Res, 2021).

Profile of loans taken out by garment workers at different stages of the pandemic.

Source: ReFashion Study data Oct/Nov ’20, Mar/Apr ’21 and Nov/Dec ’21.

Where access to alternative sources of credit proved difficult, other households responded by selling assets, including land and gold, often at deflated rates due to market conditions. Whilst selling assets is a coping mechanism that enables households to manage crises in the short term, it adds to their economic precarity and vulnerability over the longer term, severely reducing their capacity to withstand future crises and risk events (Green and Estes, 2019). Indeed, as the data show, for those with ‘nothing left to sell’ (Chanthou, June 2021, ReFashion project) – having lost any household land and major assets already, whether during the pandemic or previously – the only coping strategies left were most severe. Typically, as we have detailed more extensively elsewhere (Brickell et al., 2023; Lawreniuk et al., 2022), this took the form of making sacrifices within the already fine margins of daily household expenditure, reducing outlay on basic necessities, especially food, to be able to meet repayment demands.

Conclusion

This paper has explored how microfinance institutions in Cambodia leverage migration and remittance information from rural households to assess their creditworthiness. It has shown how microfinance institutions and banks consider remittances when evaluating loan applications, often advising borrowers to include their remitting relatives in the loan agreements. This prevalent lending practice by financial institutions turns remittances into a form of what we called ‘translocal collateral’, re/constituting connections among family members across distances to reduce repayment risks for lenders. Yet, we argue that this often comes at the expense of the borrowers’ well-being. Such practices – and the related development policies that promote them – remain inherently precarious due to their reliance on unstable urban labour markets on the one hand, and the lack of rural social infrastructure that threaten the support systems of migrant families on the other. As a result, sudden interruptions in both translocal and transnational remittance flows can have significant ramifications for rural households, forcing them to deal not only with decreases in income but also looming debts to repay.

The contributions of the paper are manifold. First, it extends the concept of social collateral by introducing translocal collateral – a form of security rooted not in physical assets or group liability, but in the moral and affective ties that bind translocal households. This reframing foregrounds how financial institutions exploit kinship-based obligations across place and space to mitigate risk and ensure repayment, even in the absence of formal guarantees. Second, by drawing on the concept of translocal precarity, we highlight how the spatial reorganisation of livelihoods – through migration, remitting, and borrowing – is not merely a coping strategy but a structural condition produced and sustained by financial institutions and development agenda that aim to re/spatialise finance and collateral in countries like Cambodia. Finally, by bringing together multiple research projects, this paper has offered a holistic and in-depth understanding of the lived realities of debt and indebtedness, understood as translocal phenomena. It is precisely this translocal methodological approach that has allowed us to understand how filial debts have been both monetised and subsequently collateralised in the form of remittances. Furthermore, a translocal approach has helped expose the inherent fragility of such projects when remittance flows – the monetary form of often unavoidable social obligations – suddenly stop. Overall, the paper has highlighted the critical analytical significance of focusing on the numerous actors and localities involved in this translocal web of collateralised debt relations in Cambodia and beyond.

While the paper focuses on the Covid-19 crisis, we also want to emphasise that the abandonment of garment workers by international firms during the pandemic is reminiscent of the 2008 financial crisis, experienced more than a decade before. In the age of polycrisis (Tooze, 2022), global development and private interventions that aim to create collateral substitutes based on unstable remittance flows remain a precarious, if not dangerous, endeavour, which financial institutions have profited from at the expense of workers and their families. Ultimately, the paper offers a critical take on the ways in which international development interventions aiming at harnessing remittances for financial inclusion can contribute to the expansion of (microfinance) debt regimes that exploit translocal precarity. This is particularly important at a time when the digitalisation of remittances is now increasingly promoted as ‘an enabler of financial inclusion’ (Guermond, 2022; IFAD, 2024: 5) worldwide, including Cambodia.

Footnotes

Acknowledgements

We would like to thank the anonymous reviewers at this journal for their comments, which have greatly improved the finished article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The ‘Depleted by Debt’ project was funded by the UK Research and Innovation’s Global Challenges Research Fund (ES/T003191/1). The ‘Refashion’ study was supported by the UKRI (EP/V026054/1). The ‘Landscapes of Debt’ project was funded by the Center for Khmer Studies and the Fulbright Institute of International Education. The study entitled ‘The Financialization of Agrarian Landcapes’ was funded by a faculty start-up grant at the National University of Singapore (A-0003620-00-00). Estes’ study was funded by the Fulbright Institute of International Education and the Center for Khmer Studies.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.