Abstract

This article refocuses attention on issues of mid-20th century state-led development and the role of development banks in shaping capitalist expansion. More specifically, a general recasting of attention back to the era of Import Substitution Industrialisation (ISI) is underway in light of contemporary debates about ‘mixed economies’ in constituting state-led developmentalism. Mixed economies are held to conjoin public and private interests and thus state and market practices as the hallmark of mid-century statecraft in Latin America. Rather than accepting the mixed economy approach, this article focuses instead on the role of nodal planning agencies in Latin America in hothousing capitalist development. As a result, an alternative account is revealed in the making of mid-century state capitalism that does not shy away from assessing its class-relevance. Focussing on Nacional Financiera (Nafin) in Mexico, founded in 1934, and Corporación de Fomento de la Producción (Corfo) in Chile, founded in 1939, foreign capital is revealed as playing a pivotal role in shaping ISI ‘national’ state development plans. Exploring the secret histories involved in hothousing for development in mid-century Latin America thus assists us to inform present economic geography and geographical political economy considerations of state capitalism, class power and public-private sector financing of development.

Keywords

In 1999, the then state-owned Servicio Postal Mexicano (Sepomex), an administrative division in Mexico of the Secretaría de Comunicaciones, issued a MXN$3 postage stamp celebrating 65 years of the development bank Nacional Financiera (Nafin). Set against a silver tint background, designed by Romo, the anniversary stamp features a vertiginous architectural edifice that is seemingly zooming to the heavens in hues of cyan and indigo blue. Suspended above the skyscraper is the faint watermark symbol of Nacional Financiera that has unmistakably appeared across various publications since its founding in 1934. In 1989, the state-owned Correos Chile issued a set of four CLP$60 postage stamps to celebrate the 50th anniversary of the development bank Corporación de Fomento de la Producción (Corfo) in Chile, founded in 1939. Designed by Edgardo Contreras, the quartet all display different commodities on the frontier of Chile’s economic development, covering: maritime transportation and fishing; logging and manufacturing; telecommunications and electrification; and carbon mining and energy. In 1999, the Casa de Moneda de Chile would also release a further commemorative CLP$140 stamp to honour the 60th anniversary of Corfo with a painting of Pedro Aguirre Cerda, President of Chile from 1938 to 1941, by the artist, film director and actor Jorge Délano (or ‘Coke’) to signify ‘the country in movement’. Beyond the interests of philatelists, Hobsbawm (1983: 281) has conveyed that postage stamps are the ‘most universal form of public imagery other than money’. Celebrating Nafin and Corfo, these commemorative stamps highlight the significance of development banks within everyday state capitalism. The stamps carry the signs and symbols of exchange value in and beyond its form of existence as money (or that most universal commodity in which all commodities are dissolved) backed by state-mediated power through the Servicio Postal Mexicano and the Casa de Moneda de Chile. As conscious symbols exchanged for the universal equivalent of money, these forms can thus be understood as commodities that literally come to stamp the substance of definite social relations between people as an economic and fantastic form of relation between things (Marx, 1867/1996: 83). The postage stamps thus assist in marking and identifying the significance of development banks in the construction of state capitalism in Mexico and Chile.

This article seeks to refocus attention on Nafin and Corfo as development banks and their role in mid-century state capitalism in Latin America during Import Substitution Industrialisation (ISI) to trace how developmentalism proceeded through the internalisation of class interests within state capitalist forms in ways that contemporary arguments miss. It does so by engaging with the very latest contributions to mid-century developmental statecraft, political economy and state formation in the Americas. In Sorting Out the Mixed Economy, Offner (2019: 17) argues that mid-century developmentalism in the Americas was marked by a ‘mixed economy’ or hybrid developmental state conjoining the role of state and capital to embed public and private organisations in the forging of ‘state-led’ development. Elsewhere Babb (2001: 49) similarly reasoned that ‘the economy that emerged after the Mexican Revolution was mixed: essentially capitalist but with a strong role for the government in economy and society’. Such rethinking and ‘sorting out’ of the mixed economy holds that the developmental state was a contradictory formation constituted by contending visions of public policy-making and private capital investment, marking processes of land reform, housing, university economics education, business management and corporate business. Rather than focus on ‘direct, on-the-nose forms of connection and exchange’ this sorting out of the mixed economy traces ‘forms of indirect connection’ through linked networks of corporate executives, managers, urban planners, intellectuals and economists in creating the developmental state (Offner, 2019: 287–288).

What the focus on ‘sorting out’ the mixed economy of the developmental state glosses over, however, is a straightforward point made by Dobb (1946: 342) on state capitalism that ‘every economic system is in some degree a “mixed system”’. A dash of Dobb is therefore necessitated to make sense of some of the preliminary distinguishing features of state capitalism in our argument. For Dobb (1951: 57), dominant treatments of economic history deliver a focus on the dynamic impetus of capitalism that is reflective of ‘the half-illuminating, half-distorting, mirror of ideology’. The mirror of ideology refers to common accounts that draw attention to autonomous entrepreneurs, or firms, motivated by considerations of individual profit in relation to capital accumulation. Economic development in these hands is treated as a self-perpetuating process as long as state interference is not regarded as an obstacle to curbing the agency of decision-making innovative entrepreneurs. Our argument is that a focus on the mixed economy is caught within this mirror of ideology because it accepts the given impulses of the state and market and relies on ‘the imagined dichotomy between public and private while systematically conjoining the two’ in its own definition of the developmental state (Offner, 2019: 17). In contrast, for Dobb, the geographical expansion of U.S. economic development in the 20th-century is linked to (1) the concentration of capital in forms of property ownership and (2) processes of dispossession linked to the condition of primitive accumulation (Dobb, 1951: 59–69). We link this to the notion of hothousing for development that is defined not only in relation to the historical basis of capitalist production in conditions of primitive accumulation but also how these processes are ongoing through the concentration and centralisation of capitalist production. Following Marx (1867/1996: 616–623), the formative elements of hothousing for development therefore include the concentration on a vast scale of the accelerated conditions of capitalist production and value-composition. Fractions of capital can be in competition, as individual capitalist rivals struggle against each other during initial processes of primitive accumulation and capital concentration. Equally, within the crucible of hothousing for development, fractions of capital experience centralisation as the process of competitive accumulation forms, destroys and transforms rival capitals. This centralisation of capital is the attraction of capital by capital, or ‘expropriation of capitalist by capitalist’, and is an enormous social mechanism or lever for development (Marx, 1867/1996: 621). Although concentration and centralisation can be distinguished, they both result in the intensification, acceleration and quickening of capital accumulation to mature and force the growth of development, as if in a hothouse (Marx, 1857-8/1973: 225; Marx, 1867/1996: 739). Overall, this metamorphosis becomes the material basis for an ‘uninterrupted revolution’ in capitalism as a mode of production whilst, also, ‘the productivity of labour is made to ripen as in a hothouse’, in the drive for extracting surplus-value (Marx, 1867/1990: 778n.*).

This approach demands an account of the capital concentration and centralisation processes that marked state capitalism linked to conditions of primitive accumulation and thus the role of developmental banks that hastened in ‘hothouse fashion’ the process of capitalism (Marx, 1867/1990: 739). Our claim is that returning a focus back to development banks such as Nafin and Corfo, as direct on-the-nose agencies shaping mid-century state capitalism in Latin America, better assists in understanding what is defined here as the hothousing for development. Sorting out the mixed economy truly entails, then, rejecting the artificial separations of public and private, or state and market, that stand as reflections in the mirror of liberal ideology. At best, analysis of the mixed economy can only ever be half-illuminating due to its reliance on the dichotomies of liberal ideology. At worst, such analysis is half-distorting because of a reliance on artificial separations that obscure the role of the state and class forces within the economy. Instead, by refocusing attention on nodal agencies such as Nafin and Corfo and how they promoted in hothouse fashion economic development during the mid-century offers an alternative sorting out of the mixed economy. It leads us to advance a subtle argument about how planning through development banks ensured the concentration and centralisation of capital that entailed the internalisation of class interests by fractions of capital within state capitalist forms, such as Mexico and Chile. Overlooked in this regard is the argument that, ‘U.S. intervention promoted the internationalisation of capital by securing the political and economic conditions for profitable investment in ISI’ (Maxfield and Nolt, 1990: 78). The nuance of our approach to analysing the internalisation of class interests within state capitalist forms also enables us to avoid the sweeping generalisations of monopoly capital arguments. It is an oversimplification to argue that ‘monopoly capitalism is a system made up of giant corporations’ (Baran and Sweezy, 1966: 52) as it leaves little, if any, room for understanding the various forms of state capitalism (Dobb, 1966: 470–475; Dobb, 1946: 383–384).

There are two main sections that follow to advance the focus on the hothousing of development in Mexico and Chile. The first section addresses the role of Nafin in Mexico as the state development bank entrusted with the long-term debt financing of the economy as well as involvement in fixed capital formation in the drive for surplus value in the form of infrastructure investment. Novelty is added here to debates on state capitalism by revealing how the expansion of capitalism through ISI proceeded on the basis of the internalisation of dominant class interests through the state, thereby addressing a blind spot in theorisations of state capitalism by asserting class analysis (Poulantzas, 1975: 73–76; Sperber, 2019: 117–118; Sperber, 2022: 268). Alfredo Navarrete Romero, Deputy-director (1961–1965) and then Director (1966–1968) of Nacional Financiera, draws our attention to this emphasis rather clearly: Foreign capital, both public and private, participated in several of the key industrial promotions of Nacional Financiera in this period, notably in the establishment of enterprises to produce steel, copper, fertilisers, paper, synthetic fibres and electrical equipment – industries oriented primarily to the substitution of imports . . . Thus foreign capital was able to assist in the active process of transforming the productive structure necessary to economic development and growth (Navarrete Romero, 1968: 78).

Similarly, the second main section advances a focus on the agency of Corfo as a fundamental state developmental agent also connected to the internalising of class interests in relation to foreign capital (see also Avilés, 2024: 4–7). Corfo, during the early phases of ISI, developed short investment plans – called ‘Planes de Acción Inmediata’ – for mining, agriculture, industry (manufacturing), energy (electricity, oil and coal) and transport and commerce (Corfo, 1944: 30–31, 101). This section thus reveals the entwining of national and foreign capital in the construction of ISI, challenging the simple diffusionist narrative of the outward spread of monopoly capital from core to periphery. Finally, this section shows how hothousing development in Chile furthered the concentration and centralisation of capital accumulation. The conclusion is an appropriate juncture to reflect on how our argument on the hothousing of development during the mid-20th century period of statecraft in Latin America may contribute to present considerations in economic geography and geographical political economy regarding state capitalism, class formation and public-private sector financing of development.

The hothousing of capital accumulation and state formation in Mexico

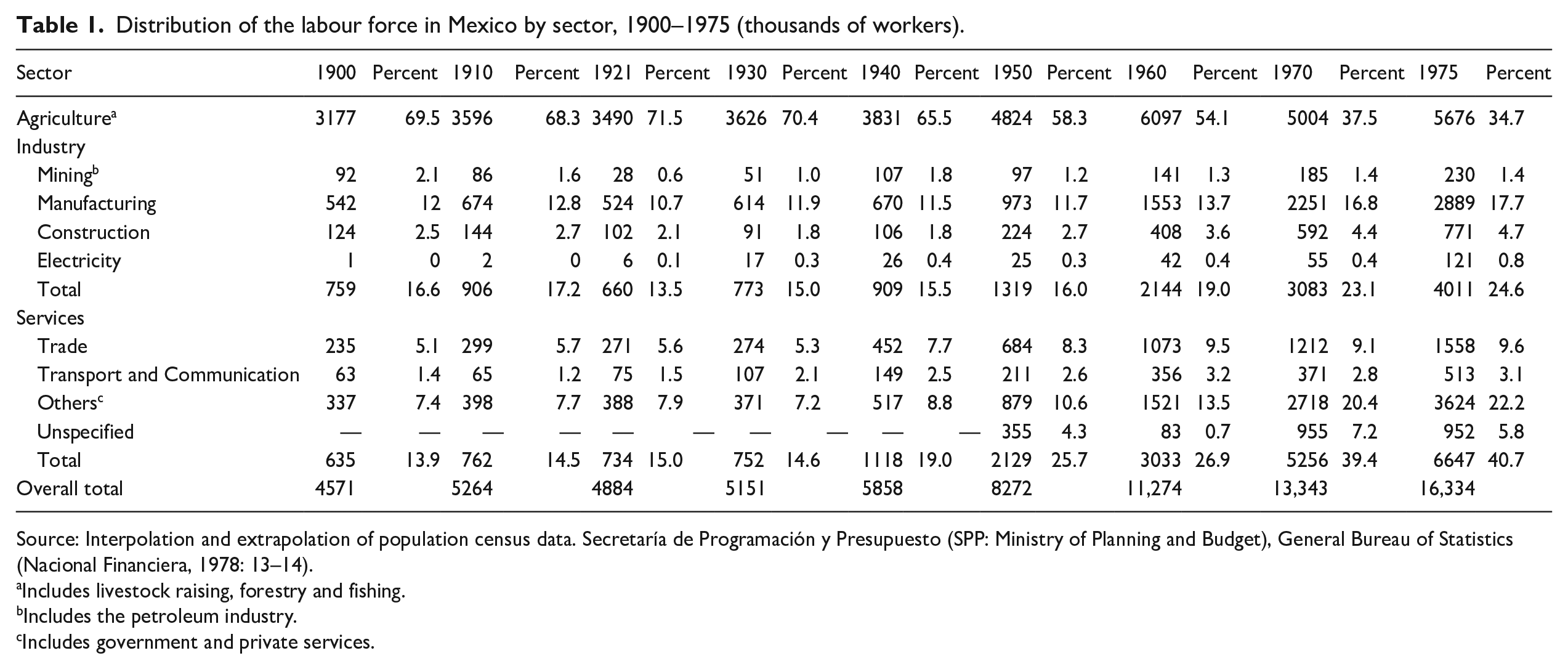

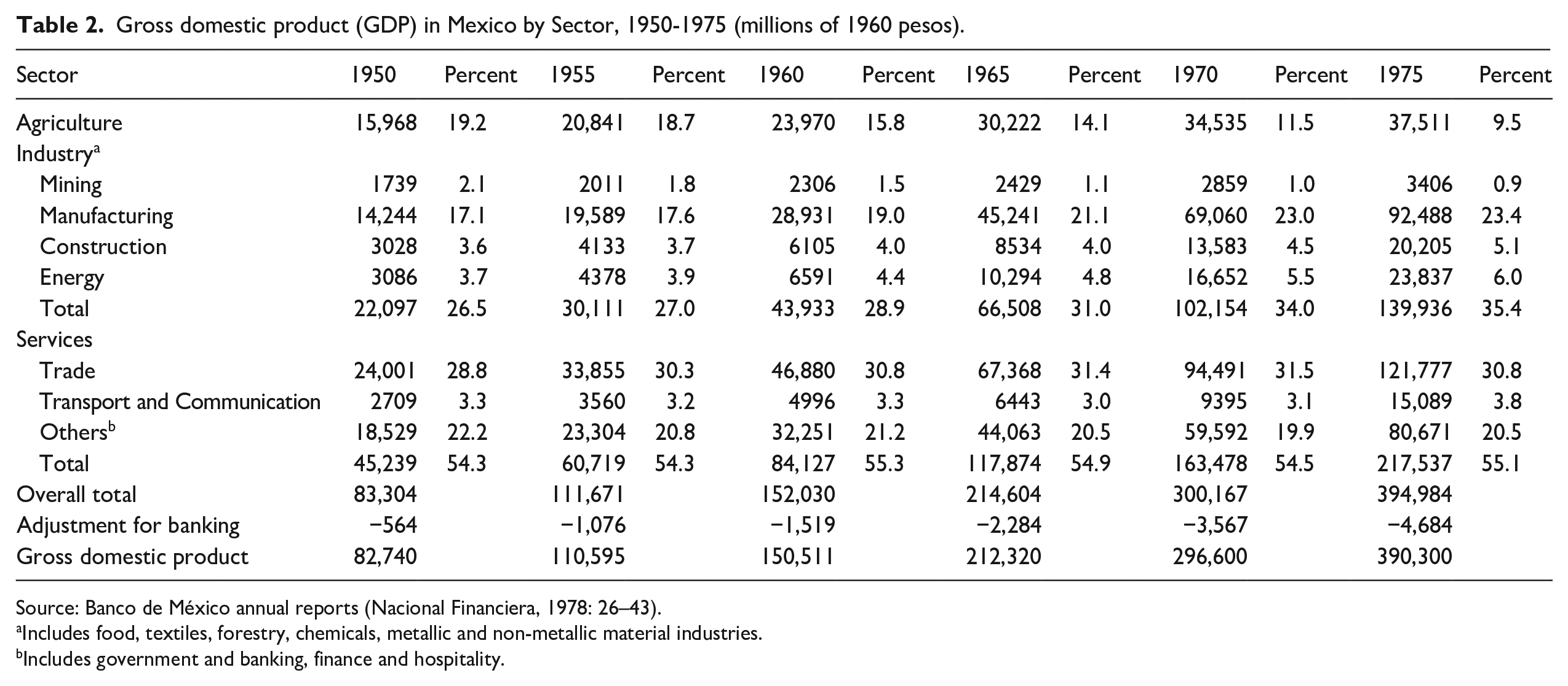

The task of this section is to focus on the class-relevance of the reorganisation and consolidation of the mid-20th century state in Mexico during the initial phase of Import Substitution Industrialisation (ISI; 1940–1954) and the subsequent period known as desarrollo estabilizador, or stabilised development (1955–1972). Between 1950 and 1972, Mexico’s growth in Gross Domestic Product (GDP) averaged 6.3% (Ramírez, 1986b: 41). Average GDP per capita (at 1960 prices) rose from 3,230 pesos in 1950 to 6,718 pesos in 1975; despite population growth more than doubling across the same time period from 26 million (1950) to just under 60 million (1975) (Nacional Financiera, 1978: 4, 19). Taking macroeconomic real rates of growth from 1940 to 1975, Mexico experienced GDP growth of more than 8% per year between 1960 and 1970. On a per capita basis the rate exceeded over 3% over the same period. Furthermore, industrial production rose at a rate of at least 8% per year between 1940 and 1975, although agricultural production plunged from a significant growth rate of 8% in the 1940s, to roughly 4% during the 1950s and 1960s, to less than 1% per year in the 1970s (Morton, 2011/2013: 67; Morton, 2017). In 1950 the agriculture sector constituted just over 58% of the labour force and approximately 19% of GDP, whilst in 1975 the distribution of labour within this sector of the economy had dropped to about 34% and its share of GDP output had fallen to less than 10%. Across the same period, industry accounted for just 16% of the labour force in 1950 and about 27% of GDP, shifting to nearly 25% of the labour force and a more significant proportion of nearly 36% of GDP in 1975 (see Tables 1 and 2). As a whole, the financing of capital formation by the state through public investment reached over 50% of total capital formation in the 1935–1945 period and declined to 33% between the 1955 and 1965 period (Fitzgerald, 1977: 83). These transformations were wrought by the state serving as the locus of accumulation and the construction of the political order of capital based on ‘violence, struggle and expropriation characteristic of the process of permanent primitive accumulation’ (Bartra, 1975: 141). The state as fulcrum of capital concentration and centralisation unfolded through ownership of surplus-generating sectors, furthering the expansion of the public sector through the support of financial groups (financieras), sustaining the management of credit and domestic manufacturing by the channelling of foreign exchange through state banks thus ensuring a mediatory role between domestic and foreign capital.

Distribution of the labour force in Mexico by sector, 1900–1975 (thousands of workers).

Source: Interpolation and extrapolation of population census data. Secretaría de Programación y Presupuesto (SPP: Ministry of Planning and Budget), General Bureau of Statistics (Nacional Financiera, 1978: 13–14).

Includes livestock raising, forestry and fishing.

Includes the petroleum industry.

Includes government and private services.

Gross domestic product (GDP) in Mexico by Sector, 1950-1975 (millions of 1960 pesos).

Source: Banco de México annual reports (Nacional Financiera, 1978: 26–43).

Includes food, textiles, forestry, chemicals, metallic and non-metallic material industries.

Includes government and banking, finance and hospitality.

Following the founding of the Banco de México as the central bank (1925), a plethora of institutions were created that, taken as a whole, ‘formed the basis of a new system of state finance which, in combination with the Banco de México, could provide finance for public sector investment and exert some leverage on private accumulation’ (Fitzgerald, 1984: 225). Between 1940 and 1950 the Banco de México accounted for 80% of the total claims of the banking system on the government sector, with the state running a steady public sector deficit (Ramírez, 1986b: 46). Nafin was formed within this context as the government development bank focussing on long-term debt financing of sectors of the economy as well as involvement in infrastructure investment, such as electric power and railroads (1934). During the first period of ISI (1940–1954) in Mexico, based on the substitution of consumer goods, two major overall policies were noteworthy: (1) tariff protection to entice domestic capital into import-substitution industries and encourage private sector investment, whilst low import duties were granted towards raw materials and rates in excess of 100% were allocated to finished manufactures; and (2) an elaborate system of import licencing constituting the major control over imports with up to 80% of overall Mexican imports at the end of the 1950s subject to such licencing requirements (Hansen, 1974: 48–49). The administration of Manuel Ávila Camacho (1940–1946) – hailed as signifying the ‘end’ of the Mexican Revolution (Aguilar et al., 1993: 159–161) – was particularly marked by these more ‘inward’ strategies of developing industry through direct state intervention whilst supplying U.S. demand for mineral exports (zinc, copper, lead, mercury, cadmium) and, during World War II, petroleum and rubber to the Allied Forces. 1 Notably at this time, as early as 1941, the U.S. Department of the Treasury and the Banco de México also agreed a monetary stabilisation package of $50 million to strengthen the peso-dollar parity (Cárdenas, 2000: 185–186). Under the Miguel Alemán Valdés (1946–1952) administration, funds were then channelled to the building of irrigation projects, electric power, and more extensive communications and transportation networks.

Movements in the exchange rate were also a principal mechanism used to adjust the balance of payments deficit, with devaluations resorted to twice, in 1948–1949 and 1954. Especially under the administration of Adolfo Ruíz Cortinez (1952–1958), a policy of devaluation and inflationary financing of public sector expenditures (rather than direct taxation) was pursued, supported by the Banco de México compelling capital through private financieras to supply the deficit financing required by the state (Ramírez, 1986b: 48). This led to a ‘fiscal crisis’ referring to the imbalance between the acceleration of state accumulation and its inadequacy in financing public sector borrowing requirements (Fitzgerald, 1978: 280). Allied with the central bank controlling the aggregate supply of money and credit there was, then, an increased dependence on external financing of the public sector deficit. Due to this structural dependence on foreign capital (external loans and/or investment) the main mechanism of adjustment was therefore through devaluation, which resulted in the dollar rising in price by more than 200%. Devaluation – from 4.05 pesos/dollar in 1945, to 8.65 pesos/dollar in 1948–19, to 12.50 pesos/dollar in 1954 – resulted in the balance of payments shifting from a deficit of $49.6 million to a surplus of $72.5 million, in 1948–1949, and then a deficit of $32.6 million to a surplus of $34.9 million, in 1955–1956 (Nacional Financiera, 1978: 377–378; Villareal, 1977: 71).

After 1955 and the second period of ISI known as desarrollo estabilizador, or stabilised development, the central bank shifted the burden of financing both government and public enterprises to credit institutions and financieras within the private sector. At the same time, the Banco de México also issued peso-denominated securities with high real rates of interest, convertible in dollars at any time at a guaranteed rate, which attracted foreign finance capital. This would subsequently present an increased reliance on foreign borrowing to cover public sector deficits. Up to the 1950s, cycles of devaluation and inflation were thus evident with the latter regarded as an expression of class conflict, meaning that inflation is as much a manifestation of the class character of the state in terms of its unequal impact on social conditions as it is a monetary feature (Barkin and Esteva, 1982). Throughout the era of ISI, it is illustrative that the increase in wholesale prices in Mexico City averaged 76%, while across the period of stabilised development the increase was 39% (Nacional Financiera, 1978: 231–233). Hence, ‘during the initial phase of ISI (1940–1954), the Mexican economy adjusted primarily via price increases, while later, during the stabilising adjustment period (1955–1972), increases in the real rate of interest became the mechanism of adjustment’ (Ramírez, 1986b: 49). In the second period of stabilised development to contain inflation and defuse class conflict, the substitution of intermediate and capital goods was promoted through dependence on foreign capital, hence an increase in the current account balance of payments deficit due to the continued reliance on foreign investment and external loans. Illustrative here would be the plummeting of the balance of payments from a $34.9 million surplus in 1955 to a $761.5 million deficit in 1972 and then to a $3,692.9 million deficit in 1975 on the eve of the next major devaluation of the peso in 1976 (Nacional Financiera, 1978: 379–383). Between 1960 and 1975 Mexico’s external public debt, as a percentage of GDP, rose from 9.7% to 24.4% (Ramírez, 1986b: 44).

Across this mid-century period of state capitalism, shaping the specific social relations that enabled conditions of capital accumulation was the pivotal role played by Nacional Financiera in hothousing development. ‘History in Mexico’, President Adolfo López Mateos (1959: 12) once commented, ‘has determined that the State many times assumes the role of a pioneer. Nacional Financiera has been the prime instrument in the execution of this policy, with the object of accelerating economic development’. Given that Nafin directed nearly 90% of total financing to expand Mexico’s economic infrastructure, to invigorate basic industries and to favour the development of manufacturing throughout the 1940s and 1950s – as well as becoming the origin of 56% of all the fixed capital formation from 1950 to 1970 – it is regarded as intrinsic to the concentration and centralisation of capital accumulation and the hothousing of development in Mexico (Cypher and Wise, 2010: 39–40; López Mateos, 1959: 11). Various fractions of the capitalist class coalesced in the post-revolutionary period in Mexico alongside the state taking on the role of co-ordinating capital accumulation. These fractions of capital are significant in that they reveal the concentration and centralisation of capital in the drive for surplus value allowing for a more rapid hothouse expansion of production. While concentration can proceed through the process of primitive accumulation, centralisation involves the clustering of capitals and, simultaneously, the destruction of one capital and the surge in valorisation of another (Marx, 1867/1996: 620–621; Smith, 1984/2008: 163). For example, in Mexico, under Manuel Ávila Camacho’s 6-year (1940–1946) presidential term (or sexenio), business associations were restructured, leading to the rise of the Confederación de Cámaras Nacionales de Comercio (CONCANACO), mainly associated with large commercial capital, and the Confederación de Cámaras Industriales (CONCAMIN), mainly associated with large industrial capital, in 1941. Importantly, within CONCAMIN, the Confederación Nacional de la Industria de Transformación (CANACINTRA) was also created, which was a semi-autonomous ‘chamber’ that elevated Mexico City-based industrialists to a more central position closer to the ruling Partido Revolucionario Instituciónal (PRI) and the president. CANACINTRA became a locus of industrial fractions of capital in the 1940s, involved in state-led development that ensured the control of capital over labour while also acting as a bulwark against the larger confederations of CONCAMIN and CONCANACO. At the same time, ‘the development of a national bourgeoisie capable of carrying forward the project of economic growth was made possible by the successful reconstruction of the banking system’ (Bennett and Sharpe, 1982: 180). This included the nurturing and co-ordination of both the national bourgeoisie and finance capital through the Secretaría de Hacienda y Crédito Público (Ministry of Finance), the Banco de México as the central bank and the development bank Nafin. Advancing Hamilton’s (1982: 207, 284) work, figures such as Luis Montes de Oca – Director of the Banco de México (1936–1940) – epitomised what can be identified as a Treasury-Banco de México-Nafin complex that connected the internalisation of capitalist class interests within the state. It would also be true of architects of ISI and the stabilised development model, such as Antonio Espinosa de los Monteros, Director of Nafin (1936–1945), or Antonio Ortiz Mena, minister of finance for a 12 year period across the sexenios of Adolfo López Mateos (1958–1964) and Gustavo Díaz Ordaz (1964–1970). 2 As a result, a trend of capital accumulation was concentrated and centralised amongst fractions of the capitalist class, located across state-civil society relations. As Felipe Leal (1974: 185) states: ‘all the governments that “emanated from the revolution” have followed a political tendency favouring capital, particularly national, and within it established the hallmarks of state ownership’. Consequently, a ‘process of private accumulation strengthened a small group of capitalists in relation to the dominant class as a whole and ultimately in relation to the state’ (Hamilton, 1982: 215). Taken together, the class fractions linked to the bourgeois sector through the various confederations and allied with the state could ‘contain and channel the development of capitalism in Mexico in a global way’ (Bartra, 1993: 131). Hence, ‘Nafin’s intervention in foreign capital markets on behalf of credit-seeking private firms was perhaps as important as its own investments were in promoting industrial development’, although at the same time one can reserve some circumspection about the development bank’s statements on its own self-importance (Blair, 1962: 211; Aubey, 1966: 146–147).

During the 1940s the bulk of Nafin’s loans and investments went to public sector infrastructure projects in manufacturing industries, transport and communication, electric power and construction. Its financing of transport and communication sectors increased by over 500% between 1945 and 1952, at an average rate of 62.6% with the main destination of external finance between 1942 and 1961 covering electric power (26%), transport and communication (22%), industrial manufacturing (20%) and construction (16%) (Nacional Financiera, 1963: 152; Ramírez, 1986a: 71). Indicative of capital concentration and centralisation, there was no major highway, railway, electrical company (including the Comisión Federal de Electricidad), irrigation work or dam, university, agricultural credit programme, public works programme, or land use ‘improvement’ scheme that was not a recipient of foreign credits obtained by Nacional Financiera (see Nacional Financiera, 1964: 32–34; Nacional Financiera, 1985: 82–89). From 1950 onwards, Nafin would come to account for between one-third and one-half of the banking system’s total financing of industry (Bennett and Sharpe, 1982: 183). Major instances of Nafin’s role in hastening hothouse fashion processes of capitalist transformation would include the cases of Diesel Nacional, one of the first major companies involved in the automobile industry, using Fiat technology to produce diesel trucks, and Sociedad Mexicana de Crédito Industrial, one of the most important financieras (private banks) funding industrial projects in automobile assembly, household appliances and the canning and fishing industries under the acquisition of the state. Practically all the external credits received by public enterprises in Mexico were obtained with the intervention of Nacional Financiera. From 1958 to 1964, the sectoral distribution of such funds went, respectively, to transport ($190.5 million or 27%), electrification ($153.6 million or 22%), industry ($82.8 million or 12%) and irrigation, education and public health ($145.7 million or 28%) (Ramírez, 1986a: 102). Prominent among parastatal firms was the first integrated steel mill, Altos Hornos de México, at Monclova in the state of Coahuila, using Mexican coal and iron ore and expanding into investments in paper, sugar and cement as well as railroad construction. To help finance its founding, Nafin was instrumental in negotiating credits from the U.S. Export-Import Bank (EXIM Bank), in 1942, whilst loan transactions followed with the International Bank for Reconstruction and Development (World Bank), in 1949, the Inter-American Development Bank (IDB) and the United States Agency for International Development (USAID) in the early-1960s. Although figures vary, José Hernández Delgado as the Director of Nacional Financiera (1952–1970), has indicated that between 1942 and 1959, Nafin obtained overseas credits of US$992 million from the Export-Import Bank of the United States, the World Bank, Bank of America and the Chase Manhattan Bank for public works and industrial or public service enterprises (Hernández Delgado, 1959: 19). A little after, Nacional Financiera’s own report 50 Años de Revolución Mexicana en Cifras documented that between 1942 and 1961 Nafin obtained credits of over US$1.6 billion with 53% alone deriving from the quartet of the EXIM Bank, the IBRD, Bank of America and Chase Manhattan Bank (Nacional Financiera, 1963: 151).

3

From 1941 to 1966, it is claimed that foreign loans obtained by Nacional Financiera amounted to US$3.4 billion (Nacional Financiera, 1969: 44). In the words again of José Hernández Delgado (1985: 87), ‘the greater variety of the origin and the instruments of credit reflected – it is fair to recognise – the increased competition between industrial countries to place their products in the Mexican market, which was in clear expansion’. As Cockcroft (1983: 184–185) summarises: Nafin co-operated with both the Mexican government, whose top financial officials were usually drawn from Nafin’s board of directors, and private capital, including foreign investors, to whom it often made loans. U.S. bankers, through their status as Nafin’s creditors and their purchases of state bonds issued by Nafin, were thus able to assert considerable influence over state economic decision making.

Indeed, as early as 1951, Nacional Financiera proposed that a combined working party be established with the IBRD (World Bank), ‘to assess the major long-term trends in the Mexican economy with particular reference to absorb additional foreign investments’ (The Combined Mexican Working Party, 1953: ix). Based on a review of investments by Raul Ortiz Mena (Nacional Financiera), Victor L. Urquidi (Banco de México) and Albert Waterston and Jonas H. Haralz (both from the IBRD), the emphasis was on Mexico’s capacity to absorb foreign investments by supplying ‘the essential foundations needed by the Mexican government to formulate a development programme’ (The Combined Mexican Working Party, 1953: vii). One outcome of the combined working party between Nacional Financiera and the IBRD was the reinvention of an earlier agency, the Comité de Inversiones (Investment Commission), in 1954, under the sexenio of Adolfo Ruiz Cortines, that combined representatives of the Treasury-Banco de México-Nafin complex. As Thompson (1979: 115) has stated, Nafin and the IBRD established ‘a great identity of interest’, after the 1954 devaluation. At this time, the Investment Commission received criticism ‘for having satisfied itself with the job of sorting out the investment projects prepared by the numerous state agencies and enterprises’ (Wionczek, 1963: 161, emphasis added), rather than directly coordinating economic planning. Hence the Investment Commission drew up its first 2-year investment plan in 1956 (for 1957 and 1958) that served as the basis for negotiations with the IBRD and other foreign financial agencies with respect to external credits. The activities of the Investment Commission then became absorbed by the creation of a centralising Plan de Acción Inmediata (1962–1964) to coordinate coherent state economic planning in the context of low yields on long-term investment, dependence on foreign public credits, and the predominance of international lending agencies. Although the Plan de Acción Inmediata was the first national investment programme, it still struggled to coordinate economic planning for development because, according to its architects in 1962, ‘the combination of elements necessary to increase the efficiency of planning within the framework of a mixed economy does not exist as yet’ (as cited Wionczek, 1963: 176, emphasis added). Capturing the ideology of the mixed economy so effectively, President López Mateos (1959: 10) would state, ‘in practice, there is no possible conflict between private initiative and the State, for the latter is not prepared to assume the task of business promotion, and the former is not interested in sectors where profits are low or absent’ (López Mateos, 1959: 10). Or, in following the ideology of the ‘mixed economy’, as Nafin Director Hernández Delgado (1961: 20) would reiterate: ‘The assertion that the industrial promoter moves only for profit is as unjustifiable as the assertion that the action of the State is exorbitant and inefficient’. As a result, between 1942 and 1967, Nacional Financiera received US$4.2 billion in foreign capital channelled to infrastructure projects and basic industries (electric power, railroad transportation, highways, agricultural investments and irrigation, petroleum and petrochemicals, steel and vehicle production). From 1942 to 1954, 79% of the amounts drawn by Nafin came from the United States, 19% from international institutions and the remaining 3% from European and Canadian sources (Navarrete Romero, 1968: 82). Capturing the goal of creating ‘national’ capitalists, Alfredo Navarrete has stated that ‘the action of the Revolutionary governments has not been at the expense of private Mexican investment . . . In fact, public investment has filled the vacancy left by the massive foreign investment of the regime of Porfirio Díaz’. Hence, national integration and productive expansion were at the core of this strategy of financing social development, ‘yesterday in violent and forceful stages, today in a more subdued and quiet manner’ (Navarrete Romero, 1960: 533, 535). More critically, whereas Nacional Financiera would itself assert that it was important to canalising finance to important sectors of the national economy, we would rather shift the stress to its role in hothousing economic development by providing the necessary conditions for the concentration and centralisation of capital accumulation within state capitalism (Hesketh, 2017: 84–88; Nacional Financiera, 1963: 148).

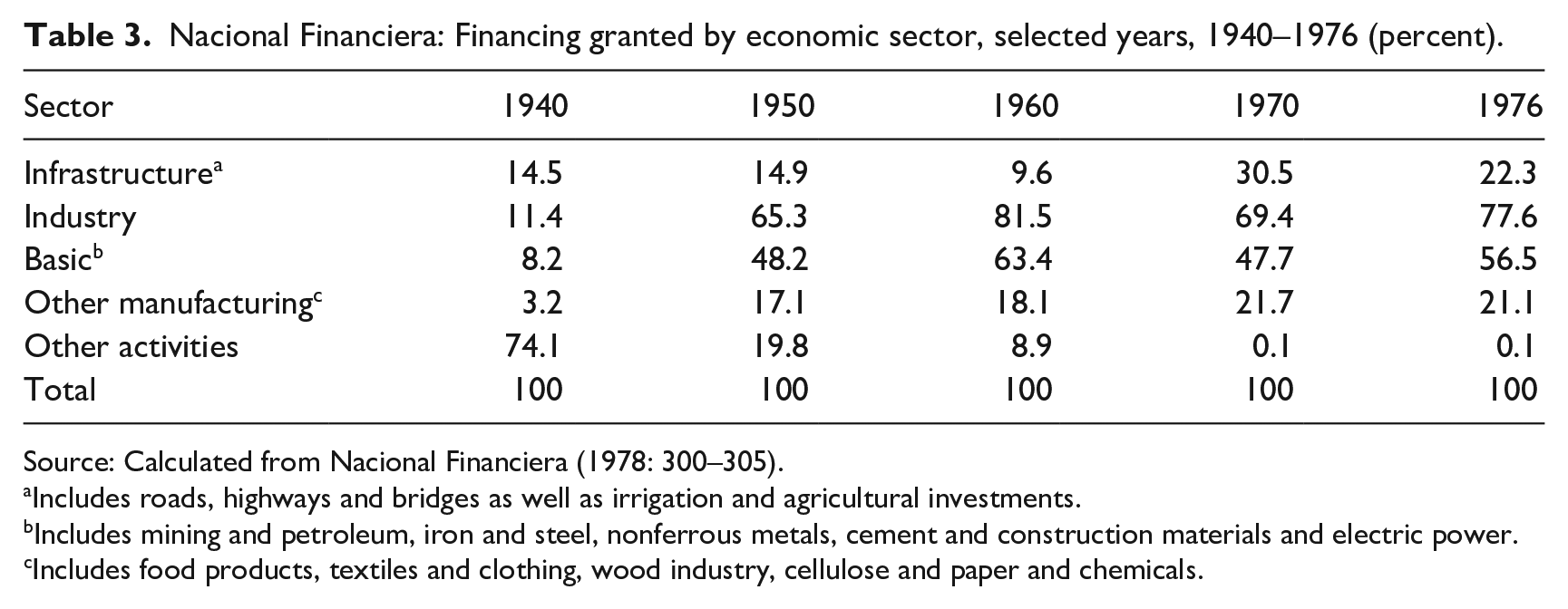

The dominance and significance of state financing of agriculture was also crucial to the hothousing of development during ISI and was an early priority sector for Nafin. In 1940, financing granted by Nafin to the agricultural sector was 14.5% compared to 11.4% to industry (see Table 3). By 1950 the level of Nafin’s financing granted to agriculture remained roughly constant just below 15%, while the industrial sector had jumped to over 65%. More dramatically still, in 1960, the shake out from agriculture to industry was signified by the industrial sector receiving over 81% of Nafin’s state-led developmental financing compared to the drop to below 10% granted to agriculture. By the 1960s the economy shifted to more intensive forms of labour processes within industry (and increased proletarianisation) and agro-industrialisation came to further the modernisation of the food industry and transform the organisation of production. While agriculture in Mexico grew at an annual rate of 5.7% from 1940 to 1955, by the end of the 1960s the overall rate of agricultural growth had fallen to 1.5% (Arizpe, 1985: 206). At this time, food self-sufficiency had been maintained and the agricultural sector was directly financing the industrial and service sectors with the net transfer from agriculture to the rest of the economy estimated at some $250 million at 1960 prices (Hansen, 1974: 59). There was, then, widespread ‘squeezing’ of agriculture under ISI in order to finance new manufacturing industries, undertaken through price controls on basic foods, forms of taxation and the control of wages in urban centres (Bruton, 1998: 914). The hothousing of agriculture thus refers here to how ‘the surplus labour of the peasants, who work under the least favourable conditions, is bestowed gratis upon society’ (Marx, 1894/1998: 792), because of the increase in the portion of ground-rent and thus surplus value transferred by state-mediated mechanisms to capital. Or, as Bartra (1993: 64) clarifies, it was the bourgeoisie as a whole in Mexico that benefitted from peasant surplus labour, a portion of which was ‘bestowed gratis upon society’ through state agencies. One result was the transformation of basic grain production by ganaderización (livestock-oriented commercial production) involving the displacement of sorghum for corn and the industrial production of poultry and pork meat so that the agricultural productive process became increasingly controlled by industrial capital. As Barkin (1990: 31) has detailed, ‘the distorted pattern of development of Mexican agriculture has resulted in a generalised move towards a demand-driven model of agricultural production’ and a productive structure oriented towards animal feed (sorghum), luxury foods and agro-exports. This drive came to dominate the agrarian landscape in the 1970s albeit, at the time, with enhanced state support to halt the demise of food self-sufficiency, such as the Compañia Nacional de Subsistencias Populares (CONASUPO). The latter, set up in 1965, ensured that labour’s urban consumption needs of basic foodstuffs could be met by maintaining cheap foodcrop supplies appropriated from peasant producers. CONASUPO ensured, then, the commoditisation of the peasant economy by bringing ejidal production to the market (Bartra and Otero, 1987: 343). Attempts to offset the crisis in the peasant economy also included expanded agrarian reform during the Díaz Ordaz administration, with the total surface of distributed lands amounting to 25,568,204 hectares, which was more than the 21,654,920 hectares distributed under Cárdenas (Nacional Financiera, 1978: 53–54). 4 This partly explains the spike in Nafin financing granted to agricultural investments throughout the 1970s, shooting to just over 30% in 1970 and holding at 22% in 1975 (Table 3). Linked to this was also the prominence of new initiatives such as the Programa Integral para el Desarrollo Rural (PIDER), launched in 1973 with financing from the World Bank channelled through Nafin aimed at promoting a self-sustained development process within ‘micro-regions’ by targeting livestock production and small-scale irrigation through the provision of agricultural credit, infrastructure support and education facilities. As a result of PIDER, the World Bank claimed that ‘the Mexican Government has organised itself through both spatial (river basin and micro-region) and functional (credit, extension, irrigation, feeder road) programmes for a major effort to address rural poverty’ (World Bank, 1975: 3). The three phases of World Bank funding covered a 12-year period amounting to loans of $110 million (1975–1980), $120 million (1977–1983) and $175 million (1982–1987). In summarising, the World Bank stated that PIDER was instrumental in two main ways by: (1) assisting the Secretaría de Programación y Presupuesto (SPP) in building a decentralised institutional framework that formed the basis for subsequent major rural and regional development programmes (World Bank, 1986: 17) and (2) shifting the focus solely from infrastructure support ‘to an emphasis on productive investments to promote self-sufficiency and improve income distribution’ and to tap into ‘unrealised productive potential’ (World Bank, 1990: vi).

Nacional Financiera: Financing granted by economic sector, selected years, 1940–1976 (percent).

Source: Calculated from Nacional Financiera (1978: 300–305).

Includes roads, highways and bridges as well as irrigation and agricultural investments.

Includes mining and petroleum, iron and steel, nonferrous metals, cement and construction materials and electric power.

Includes food products, textiles and clothing, wood industry, cellulose and paper and chemicals.

These are some of the main paradoxes of mid-century developmentalism in Mexico whereby state agencies came to internalise the class interests and orientations of capital, inextricably tying together the state capitalist Treasury-Banco de México-Nafin complex within a world context linked to foreign capital. In Mexico, state capitalism through myriad institutions, including Nafin, engendered and extended hothouse processes of primitive accumulation that was necessary to ensuring national capitalist development albeit ‘articulated within the global rationality of specific core capitals’ (Hamilton, 1982: 21, 186). Nafin, then, was especially significant in concentrating and centralising the accumulation of capital and hastening in hothouse fashion processes of state capitalism in Mexico. The participation of foreign capital was an important feature of ISI in the 1950s and 1960s and was instrumental in establishing key manufacturing industries, investment infrastructures, state-owned heavy industry and agrarian transformation. ‘It seems’, notes Baer (1972: 109–110), ‘that many forget that a large number of the key manufacturing industries of Latin America were constructed by or with the aid of foreign capital’. Rather than focussing on a ‘mixed economy’ – a term that featured across mainstream economic planning analysis of the era – our discussion so far has stressed the concentration and centralisation of capital that became integrated through the Treasury-Banco de México-Nafin complex linked to the presence of capitalist interests on a global scale. The focus now turns attention to Corfo and the role of specific fractions of the capitalist class in also abetting the capital concentration and centralisation in mid-20th century state capitalism in Chile, which is at the heart of the next section.

The hothouse fashion of capital accumulation and state formation in Chile

If the ideology of the ‘mixed economy’ approach is accepted, then the Chilean case potentially expresses a plethora of state/market dichotomies. From the neoliberal origin story of the Chicago Boys to the economic policies and technocratic continuity of the Cieplan Monks (Silva, 1991: 388), Chile is rife with binary economic approaches that supposedly enhance ‘social innovation for public policy’, provide ‘private solutions to public problems’ and promote ‘public-private partnerships’ through the ‘state’s narrow interventions into the economy’ (see, for instance, CIEPLAN, 2016; Larroulet, 1991/2003; Villalobos and Escobar, 2016). Such approaches resonate with the stress on ‘elements of the mixed economy that have survived’, over time, to become reconstituted in the present as a set of aggregated practices derived from mid-century state developmentalism (Offner, 2019: 289). Yet, our argument is that the mixed economy approach provides analysis that is trapped in the mirror of ideology, as a result of a ‘retrospective projection’ of the current structures of capitalist development rather than providing clarifying insights on state capitalism (Balibar, 1965: 445–446). This section advances, instead, the analysis of mid-century developmentalism in Latin America through a focus on the concentration and centralisation of capital and the role of fractions of capital in internalising the construction of state capitalism in Chile. Additionally, this approach reveals the intermingling of foreign and national capital in the construction of ISI, which also challenges the simple diffusionist monopoly capital narrative of the outward spread of capitalism from core to periphery. Finally, this section shows how hothousing development in Chile also required extending primitive accumulation through the nodal role of the state.

In unpacking the internalisation of class interests, it is important to go beyond false dichotomies because, not least, the result can lead to the notion that dependent relations were simply imposed. Advancing the work of Zeitlin and Ratcliff (1988: 221), the endeavour here is to shed light on ‘an actually existing capitalist class’ to understand how mid-century state capitalism in Chile was formed through fractions of capital linked to Corfo. In the first three decades of the 20th-century, the Chilean dominant class contingently came to understand foreign capital as an ally to expand their own interests. At this time, the Chilean dominant class became, ‘a definite and coherent, if internally differentiated, social form’ (Zeitlin and Ratcliff, 1988: xx). By the time Corfo was created there were three main fractions of capital, with short and long-term economic interests contending and cooperating. First, there was the hegemonic fraction, derived from the aristocracy with a Basque-Castilian (Spain) background that started to rule Chile during the post-colonial period (Nunn, 1970: 20). These ‘landlords’ were linked to the agricultural sector via the latifundio system in the Central Valley. Their hegemony is identified as derivative from a central core of families in which, by the 1960s, ‘the ownership of land and capital was indissoluble; and the more concentrated the close family’s ownership of capital, the more concentrated is its ownership of land’ (Zeitlin and Ratcliff, 1988: 176). In this sense, landownership and ‘lordship’ in mid-20th century development in Chile was still a symbol of prestige. In the mid-1930s, therefore, ‘a large estate [fundo] was a token of aristocracy and dominion . . . In short, it was the senator’s seat or, in other words, the dominance of the central government’ (Melfi, 1932: 76). During the first three decades of the 20th-century, this hegemonic fraction articulated different accumulation challenges, as agricultural production was mainly export-oriented and exposed to world-market shocks. These changing conditions in the world-market moved landlords to look for new economic sectors to diversify their investments, such as banking, mining and an emergent industrial sector (Burbach, 1975: 51). The latter emergent sector was especially crucial in the process of concentrating and centralising capital by becoming ‘lords of capital’ (Marx, 1864/1974: 80) through the state capitalist agency Corfo from 1939 onwards.

Second, the mining fraction of the dominant class was linked to the boom and bust of nitrate and copper exploitation in the northern region of Chile. This fraction of capital is crucial to understanding the structural internal relations between foreign and national capital, especially embedded within the rising role of U.S. foreign investments in Chile. In 1904, William C. Braden bought the ‘El Teniente’ copper mine, which in 1908 was bought by the Guggenheim Exploration Company, and in 1910, the Guggenheim brothers bought Chuquicamata copper reserves. In 1913, Anaconda Copper founded the Chilean Andes Copper Mining company to exploit copper at the Potrerillos mine. By 1916, the U.S. became the major destination for Chilean exportations by controlling copper mining production. Between 1919 and 1929, the U.S. controlled 33% of Chile’s total foreign commerce, displacing other European powers. In 1927, 90% of U.S. investments in Chile were directed to the copper mining industry. In the same year, U.S. capital accounted for more than 44% of the total foreign capital investments in Chile. By 1929, U.S. mining corporations owned 96% of the Chilean copper production (Rinke, 2013: 49–53). These developments created an expansive effect on the wider economy by means of infrastructure projects, the arrival of new technological products, the establishment of air mail between Chile and the U.S., and industrial investments related to the mining industry, especially linked to fuel (Rinke, 2013: 58).

Third, the industrialists’ fraction towards the end of the 1930s was formed by a diverse yet united group constituted by members of the old Chilean aristocracy that diversified their investments with the involvement of immigrants and their descendants who made their capital through merchant and financial activities (Burbach, 1975: 37–38). In parallel, up to the 1930s, U.S. capital was also diversifying its investments in the industrial sector, creating some friction with the Chilean industrialists. However, perceptions of foreign capital soon changed in Chile as opportunities to concentrate and centralise capital investments emerged. So, besides the role of U.S. capital in the mining industry, two wider strategies unfolded at this time for U.S. foreign investment to enter the Chilean market and offset high import duties for industrial products: (1) either directly build factories on Chilean territory; or (2) buy shares in established Chilean industrial companies. By 1930, 17 U.S. corporations held factory branches in the country and during the same decade sixteen U.S. companies expanded into Chilean firms by means of buying shares (Burbach, 1975: 56; Rinke, 2013: 54–55). Notably, in 1925, Ford built an assembly factory in Chile, and in 1931, Camilo Carrasco Bascuñán, president of the Sociedad de Fomento Fabril (Industrial Manufacturing Association: Sofofa), founded in 1882, declared that the Ford Motor Company was ‘fundamentally nationalistic’ because it was ‘Chilean in Chile, Brazilian in Brazil, Mexican in Mexico’, in providing relevant benefits for the countries by ‘using its natural resources’ (Sofofa, 1931: 486). As Antonio Gramsci (1971: 241, Q14§68) might recognise in Sofofa, ‘a class that is international in character has . . . to “nationalise” itself in a certain sense’ (see also Morton, 2007). If in 1925, total foreign investments were thus US$723 million, by 1930 they accounted for more than US$1 billion, which exceeded domestic investments in the mining and industrial sectors combined (Loveman, 1979/2001: 183). In 1935, the industrial fraction of capital made clear their change in attitude towards foreign capital. Sofofa’s president (Sofofa, 1935: 320) thus declared that, in a poor country like Chile, it is an enormous error to place difficulties in front of foreign capital. It has produced many benefits in copper, iron, and nitrate mines, as well as in railroads, ports, and public works projects. Essentially, all capital-poor countries should make an effort to stimulate foreign capital investments in domestic companies.

Indeed, if foreign capital contributed to new productive industry with innovative technological capabilities, the investments themselves entered the country with no opposition from and in alliance with the Chilean industrial fraction of capital (Burbach, 1975: 62–64). State policies slowly showed the influence of this particular group. Between 1914 and 1938, three main strategies unfolded that were independent of whoever controlled the state executive branch: (1) the increase in importation tariffs; (2) currency devaluation; and (3) the creation of state agencies to centralise specific economic sectors aimed at enhancing the national market and containing the effects of world-market economic shocks, which included a complex of the Banco Central (Central Bank, 1925), the Servicio de Minas del Estado (State Mining Office, 1925), the Caja de Crédito Agrícola (Credit Bank for Agriculture, 1926), the Caja de Crédito Minero (Credit Bank for Mining, 1927), the Caja de Crédito Carbonífero (Credit Bank for Coal, 1928) and the Instituto de Crédito Industrial (Credit Bank for Industry, 1928) (see Palma, 1984: 56–68). These initiatives were temporarily successful in decoupling industrial production from world-market shocks and producing an emergent process of industrialisation (Palma, 1984: 73). Hence, this budding industrialisation process slowly changed the distribution of employment, specifically by increasing the number of blue-collar workers and decreasing agricultural-based employment so that, by 1938, the industrial sector was responsible for 47% of employment (Loveman, 1979/2001: 198). As a result, despite the hegemonic fraction of the dominant class being ideologically opposed to direct state intervention, this period nonetheless witnessed the consolidation of an incipient industrialisation strategy that expanded capital concentration and centralisation through state activity (Meller, 1998: 49–50).

This ‘actually existing dominant class’ was embedded in the state’s delineation of economic policies, and Corfo came to be the inflexion point for dominant class differences to organise a coherent accumulation strategy. Indeed, as Zeitlin and Ratcliff (1988: 213) point out, ‘state policies have attempted to reconcile the common, yet contradictory, interests of landlords and capitalists’. In other words, it is not that the industrial fraction emerged – as an alien group of society – attached to protective state policies and that they had a strong dependency on the state’s support, as argued by Cavarozzi (1975: 9). Or, put differently, it was not the case that the industrialists and the state were externally related in building a ‘mixed economy’. It is, rather, that the industrial fraction was building its way into the core of the dominant class, which by the mid-1960s would consolidate landlords and capitalists as a structural ally of foreign capital (Zeitlin and Ratcliff, 1988: 143–185). For instance, Sofofa itself was summoned and funded by state initiatives, receiving more funds than the older business associations, such as the Sociedad Nacional de Agricultura (Agricultural Business Association: SNA), the core association for landlords (Kirsch, 1973: 42). Furthermore, Sofofa’s first president, Agustín Edwards Ross, was a member of a traditional banking family (Zeitlin, 1984: 136). Another illustrative case would be the presidency of Pedro Aguirre Cerda (1938–1941), instrumental in creating Corfo in 1939. In 1934, Roberto Wachholtz (Minister of Finance under Aguirre Cerda’s government and the leader of Corfo’s credit negotiations with the EXIM Bank), would found the major Chilean oil distribution company, Compañía de Petróleos de Chile (Copec), which largely benefitted from state policies and Corfo investment (Bucheli, 2019: 178–179). Allied in this endeavour with Walter Müller – himself Sofofa’s president between 1934 and 1955 – business associations thus had a clear influence on many of the state capitalist agencies that were created during the 1920s and 1930s aimed at enhancing capital concentration and centralisation (Kirsch, 1973: 130, 33). Hence, a close reading of the class character of the state’s leveraging in Chile shows that Corfo would become crucial to hothousing development and consolidating mid-century state capitalism as a crucial locus for the concentration and centralisation of capital accumulation.

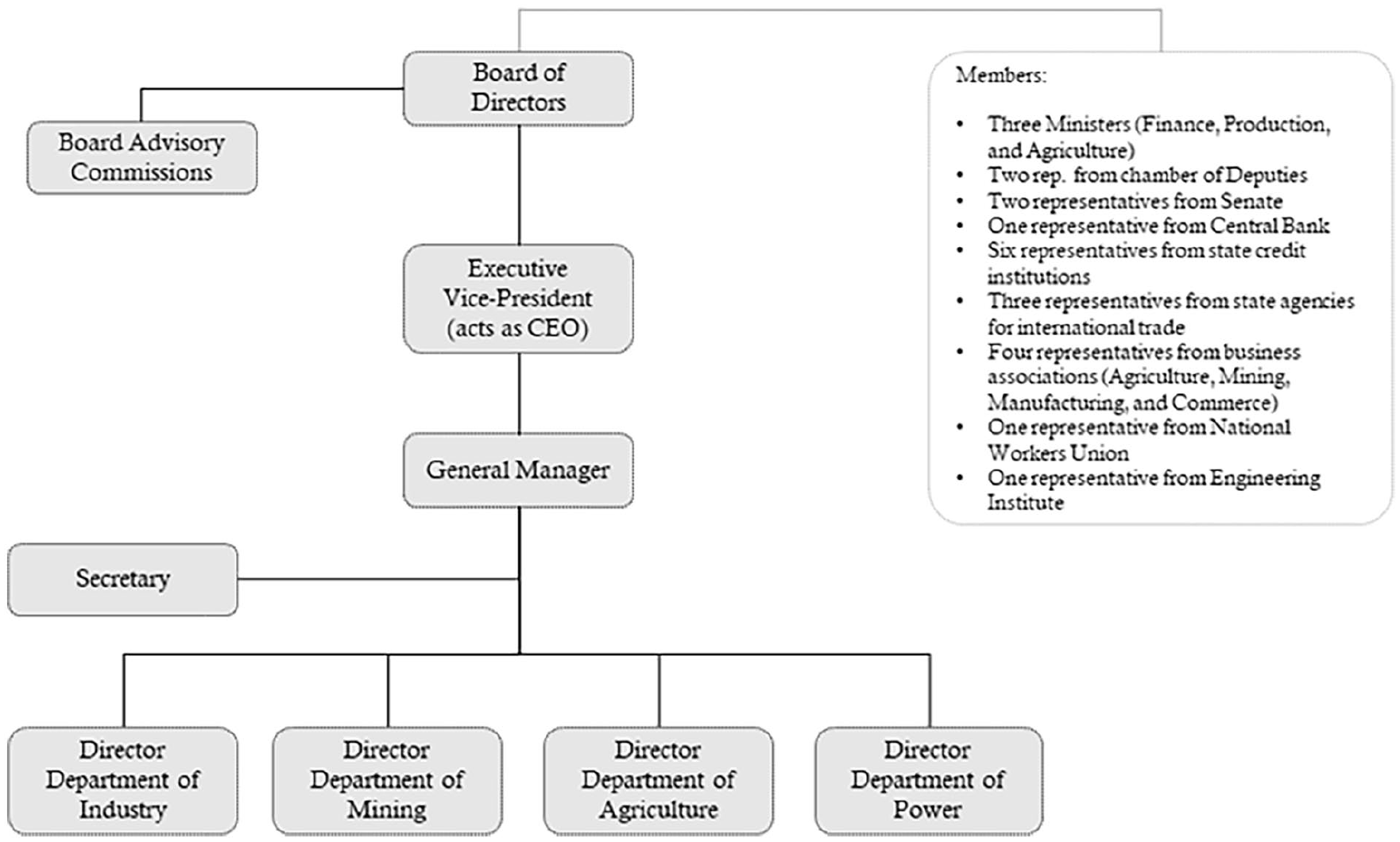

The industrialists publicly supported the creation of Corfo, as Sofofa’s president declared in January 1939, ‘state intervention is convenient in the planning of the political economy when it favours the growth of Chile’s industrialisation . . . This action could be organised in a National Economic Council’ (Sofofa, 1939: 43–44, emphasis added). Following, in June 1939, leading industrialists, among them Sofofa’s president, published through the Engineers Association’s main journal an article called ‘The Concept of National Industry and State Protection’ to highlight the state’s prominent role in protecting, assisting and enhancing the Chilean industrial sector (Simon et al., 1939: 293). Corfo was thus created by law in April 1939 with the governing body organised as shown in Image 1.

Corfo’s first administrative body (1939).

This organisational structure led Cavarozzi (2017: 49–51) to argue that Corfo was a successful case of ‘bureaucratic isolation’ as it prevented the Corporation from receiving pressure from clientelist politicians and the board of directors, which was populated with business representatives; hence keeping Corfo’s ‘technical expertise’ as the main driver of decision-making. While it is true that Corfo had a degree of relative autonomy in its decision-making, this emphasis on independence is again caught up in the mixed economy mirror of ideology. We need to step beyond the half-illuminating noisy sphere of surface appearances, guarded by the threshold sign that says ‘No admittance except on business’, to delve into the ‘hidden abode of production’ linked to how capital produces and is produced (Marx, 1867/1996: 186). In this sense, Permanent Commissions and Departments were crucial to achieving industrialists’ aspirations, as we can corroborate from Corfo’s 5-year report in relation to the decision-making process of the corporation’s involvement in industry. Citing Corfo (1944: 61), ‘the first stage is to discuss the issues in the respective Department, then it is presented to the Permanent Commission for the specific industrial sector, which aligns the analysis into Corfo’s main plans, if the Permanent Commission considers it to be a viable project, then it makes the proposition to the Board for approval’. This bottom-up procedure was crucial for the industrialists. To illustrate this point, notably, the president of the Industrial Permanent Commission was Sofofa’s president, Walter Müller, and the director of the Industrial Department was one of the engineers who, along with Müller, wrote the Engineers Association’s article, mentioned before. In other words, these departments – populated with members of the industrialist fraction of capital – created, evaluated and proposed to Corfo’s board of directors the plans and involvement of the corporation in the various economic sectors and its companies. Hence, Corfo’s vice president was clear in mentioning that these emergent initiatives came from interested entrepreneurs. ‘The corporation has never intervened by its own initiative in a private endeavour’, he stated in 1944 about fractions of the capitalist class, rather ‘they have come asking how the corporation could help them . . . and the corporation acts as a capitalist partner and a technical advisor’, showing, ‘a necessary elasticity in Corfo’s operations’ (Corfo, 1944: 41; del Pedregal, 1942: 10). Or, in our framing, Corfo assisted in concentrating and centralising capital to intensify, accelerate, and quicken the hothousing of development to shape state capitalism in Chile.

The solid ties that bound the structural internal relation between national and foreign capital during the decades surrounding Corfo’s creation set the required pace for hothousing development. Focussing on business associations in Chile – as agents or fractions of capital – different industrialisation plans developed throughout the 1920s and 1930s, and these economic plans were incorporated into Corfo’s economic strategy known as Planes de Acción Inmediata (Nazer Ahumada, 2016: 295–296). These Immediate Action Plans represented the initial steps in the state’s hothousing for development by coordinating the efforts to concentrate capital accumulation. As declared by Corfo’s first executive vice president in a 1942 speech to the general assembly of the Confederación de la Producción y del Comercio (The Confederation for Production and Commerce: CPC), a peak business association, ‘before 1939 [in reference to Corfo], the conventions of producers, the gatherings of business organisations, and generally, the entire country, was preoccupied with finding a way to coordinate the confused state’s activities to increase production’ (del Pedregal, 1942). With these plans, the bulk of Corfo’s activities were canalised into the economy for the first 5 years. The Chilean President who created Corfo, Pedro Aguirre Cerda, justified these plans in a message to Congress, ‘these plans aim to achieve an increase in production for different industrial sectors in the short-term . . . It is about, on one hand, substituting to some extent the importation of raw materials and products that could be produced in the country and, on the other hand, to conquer external markets with [Chilean] quality products’ (Corfo, 1944: 101). There is an interesting similitude here to what some industrialists dreamt by 1939, which was that Chilean manufactured goods could ‘conquer’ foreign markets such as Peru and Bolivia (Sofofa, 1939: 21).

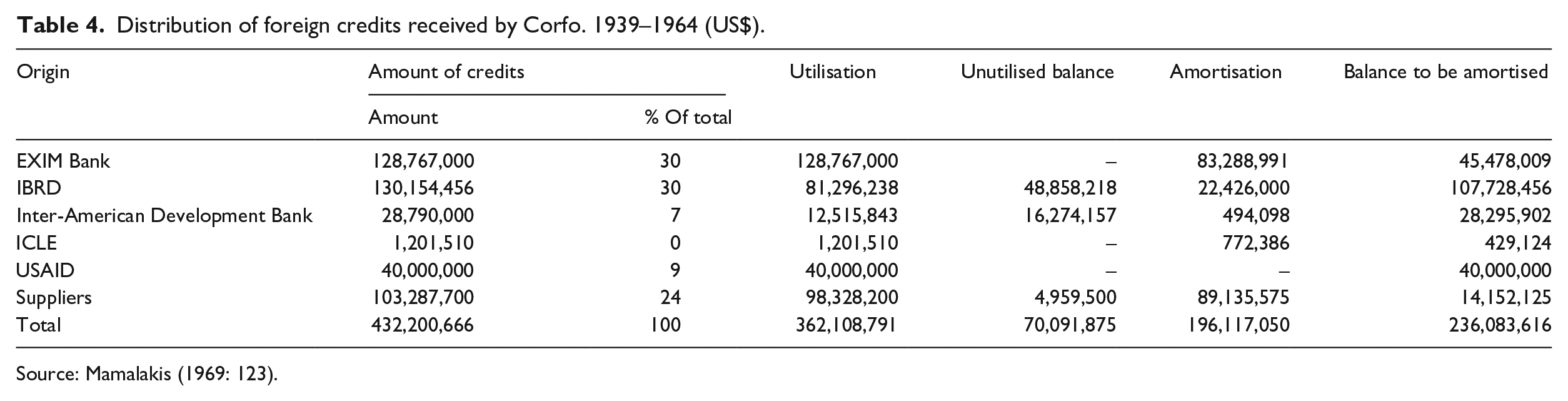

Focussing on foreign capital, we have shown already how the expansion of U.S. capital in Chile increased and how it emerged as an ally for the Chilean dominant class. In 1939, industrialists also advocated for the newly established Corfo to act as a mediator to receive foreign loans: ‘there can be no development plan if a foreign loan of CLP$500 million is not obtained. If this loan is not forthcoming, Corfo will not last for more than six months. Foreign loans are crucial for getting foreign currency, creating new spheres of activities, and renovating or replacing machinery’ (Sofofa, 1939: 83). As soon as Corfo was created, it engaged in negotiations with the EXIM Bank, subscribing to three consecutive credits in 1940, 1942 and 1943 for a total of US$22 million (Corfo, 1944: 85). Additionally, Corfo received direct credits from U.S. manufacturing companies for agricultural machinery and electric materials, accounting for US$4.8 million (Corfo, 1944: 86). By 1964, the EXIM Bank provided credits for more than US$128 million (Mamalakis, 1969: 123), and more from different international agencies (see Table 4).

Distribution of foreign credits received by Corfo. 1939–1964 (US$).

Source: Mamalakis (1969: 123).

The EXIM Bank requested three relevant conditions for the loans in the general agreement. First, Corfo should prepare a detailed plan to show the use of the loan and the potential total amount that would be required. Second, all shipments of goods obtained through this credit should be made via U.S. cargo companies. Third, crucially, the loan must be used to buy equipment, machinery and materials from U.S. companies, and the Bank would source providers for those items (Corfo, 1944: 81). While this agreement was the central scheme for financing Corfo’s activities and Chilean industrialists’ aspirations, it was nevertheless clearly reflected in transnational institutions linked to U.S. forms of intervention. In this sense, then, it is apparent that there was the induced reproduction of capital or the internalisation of class interests through Corfo that was itself linked to transnational processes. Therefore, ISI was a crucial strategy for expanding the U.S. economy, especially benefitting those industries producing capital goods that could have faced structural imbalances after World War II (Maxfield and Nolt, 1990: 57).

In this way, Corfo, as the agency for hothousing development, placed large resources at the disposal of industrialists to achieve their aspirations. As mentioned before, the corporation operated through loans to industrial companies and through direct investments as a capitalist partner. In the case of credits, Corfo acted as the intermediary but the state was the real debtor since it assumed the amortisation payments to the foreign agency, so the beneficiaries (or so-called ‘national’ companies) were not requested to repay the loan in dollars or an equivalent hard currency (Mamalakis, 1969: 123). As Marx (1867/1996: 742) forewarns, ‘the public debt becomes one of the most powerful levers of primitive accumulation’. Hence, as the rate of inflation increased throughout the 1940s, the average interest payments on the loans were less than the actual decrease in the value of the loan, making the companies repay with currency worth less than the original loan, constituting a direct subsidy to the industry (Burbach, 1975: 84). As Mamalakis (1969: 125) summarises, ‘foreign credits permitted Corfo and the recipient enterprises to obtain the country’s scarce dollars through the back door’ by ‘breaking the bottleneck of foreign exchange, bypassing the Central Bank to proceed with their investment plans’. In consequence, Corfo became the agency to extend the concentration and then centralisation of capital accumulation by expanding the financial horizons of industrial fractions of the dominant class and also partnering with them to create new industries and markets. By 1944, Corfo held shares in 27 Chilean companies, and as soon as a company was profitable, Corfo sought to disengage by selling its shares to the capitalists that requested the partnership (Cavarozzi, 1975: 145). However, Corfo did not have a specific mechanism to sell back its shares. Hence, as one former Corfo Secretary General revealed, ‘the final price was the result of an agreement between Corfo and the given private corporation’ (as cited Cavarozzi, 1975: 154). In other words, the flow of money had a clear direction – it was an injection of capital into the roots of the industrialist fraction to hothouse development.

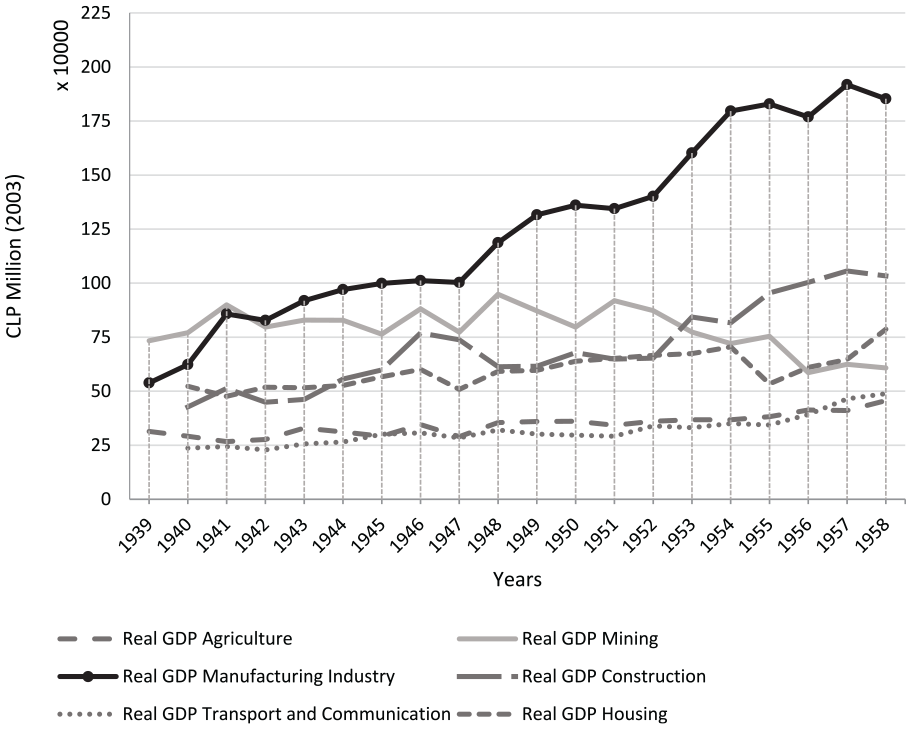

Corfo’s hothousing for development, achieved through the injection of capital into the economy, had long-term effects on the industrialist fraction and the capitalist class in general. Between 1939 and 1954, Corfo investments in machinery accounted for 30% (Bucheli, 2019: 177). Corfo’s investments in the economy were able to increase manufacturing production to surpass mining production from 1942 onwards so that between 1939 and 1958, manufacturing increased by 344%. As shown in Chart 1, the rate of growth in the manufacturing sector had different moments between 1939 and 1940, when it averaged 16.6%, as signalled towards the end of the Immediate Action Plans. Between 1943 and 1947, the manufacturing sector averaged 4% growth, which is the period when Corfo redirected many resources into planning and creating state-owned companies. Between 1948 and 1951, the rate of growth averaged 8%, and between 1951 and 1958, it averaged 5%, which is the period during which state-owned companies became profitable. From 1958 to 1973, the rate of growth for the manufacturing sector as a whole averaged 5%. Clearly, overall, the manufacturing sector shows that Corfo was the state agent for hothousing development and, therefore, the central institution involved in concentrating and centralising capital accumulation.

Gross domestic product (GDP) in Chile by relevant sector, 1939–1958.

Capital itself cannot always carry out primitive accumulation but requires others to act as its agents in and through state-backed violence as well as legislative interventions (Marx, 1867/1996: 723–731). For some, these processes of primitive accumulation therefore operate ‘always anterior to the specific operations of capital’ (Roberts, 2017: 536). Thereafter, both the concentration and centralisation of accumulation are required, and our contribution is that Corfo carried out such work in hothousing development by appropriating nature, borrowing money and organising the national economic system for the expansion of capitalism from which the industrial fraction of capitalists benefitted. As expressed by Germán Picó Cañas (1948: 63–64) – Corfo’s Executive Vice President – in 1948, in his presentation to the board of directors, [Corfo] has demonstrated throughout nine years of activity that its policy is not a threat to capital or private initiatives, as it was feared of this new state institution. On the contrary, it has become the best help to reach where private initiative is afraid to reach.

Consequently, we can now see further how mid-20th century state capitalism in Latin America proceeded through the hothousing of development, the concentration and centralisation of capital accumulation, and the internalisation of class interests within the state form in ways that mixed economy arguments miss. Hence ‘the decisive axes of the inner structure’ of the dominant capitalist class are here revealed as ‘axes of that class’s integration with foreign capital’ in forming mid-century state capitalism in Chile (Zeitlin and Ratcliff, 1988: 251). This stance is different from accepting the mirror-image reflections of 20th-century state policymakers and the visions of capital. In our view, mixed economy arguments tend to leave unexplained precisely what power relations are being projected (Offner, 2019: 285). These issues are now addressed by way of conclusion in relation to present debates on state capitalism, class power and public-private sector financing of development.

Conclusion: Mixed-up in the mixed economy

Alfredo Navarrete Romero – Director of Nacional Financiera (1966–1968) – consistently projected the role of Nafin in Mexico as a ‘government instrument for industrialisation’ to accomplish what we have called the hothousing of development (Navarrete Romero, 1960: 520). He debated this role with fellow economist Juan Noyola (who worked at the IMF and subsequently at CEPAL), as part of a winter course of roundtables in 1957 on ‘Problems of Economic Development in Mexico’ at the National School of Economics at UNAM. They raised two remarks of fundamental interest for our conclusion. First, that in developed countries, savings and investment could be facilitated more easily through capital markets. Yet, in underdeveloped countries, development banks such as Nacional Financiera would take on greater importance by channelling public and private investment. Second, by contrast, ‘in Chile, there is a development corporation that only channels public investment, but does not capture private savings’, leading to the point that, ‘it can only be said that we need capital, whether national or foreign’ to assist in channelling investments (Navarrete Romero, 1957: 155–156). The celebration of Nacional Financiera here is important for two reasons in that (1) it is lauded for more rapidly channelling public and private investment as a development bank, especially when compared to counterparts such as Corfo and (2) as a result, Nafin is endorsed as ‘more’ successfully capitalist in achieving the status of a ‘mixed economy’ sooner. As Blair (1962: 213) reminds us in relation to the entrepreneurship of the ‘mixed economy’, ‘private capital had no special compunctions about seeking public help . . . and practically every promotion was a joint venture in some degree’.

It may seem that the direct evidence of economic crisis and inflation (as much as war and revolution) can come through the changing images on postage stamps. If stamp collecting offers this impression of dramatic change, then another direct line to history can come ‘through the changing coins and banknotes of an era of economic disruption’ (Hobsbawm, 2002: 9). Perhaps, just as money is symbolised externally on the face impression of a postage stamp, appearing as an external thing, then so too do the dualities of the ‘mixed economy’ – as public and private sectors, or state and market – in appearing as autonomous developments of exchange between self-seeking interests. However, these forms of the ‘mixed economy’ – like money and stamps – are merely the perceptible appearances of capitalism, which is best recognised as a determinate totality whose content is grasped by focussing on the relations of production in their specificity (Altun et al., 2023). By relying on the categories of the ‘mixed economy’ any explanatory power in advancing our understanding of mid-century developmentalism in Latin America is constrained in two ways. First, as with the focus on regional development banks (Krasner, 1981), there is the obscuring of the role of class fractions in favour of a focus on transnational policy paradigms and the role of ideas in policymaking so that the transformation of state apparatuses by class agency is downplayed (Babb, 2012: 269). Here, class-relevant power relations behind economic ideas become obscured by more anodyne descriptions of policy, so that developmental catchup is accounted for by ‘normative isomorphism’ (occurring through institutions) or ‘coercive isomorphism’ (projected by external actors) as synonyms for conditions of class agency (Babb, 2001). Second, such arguments offer in similar ways a set of indirect pluralist connections to explain the ‘mixed economy’ through transnational networks of policymakers, planners, economists, or academics (Offner, 2019: 287–288). The upshot is a form of historical institutionalist explanation that offers economic geography a loose heuristic framework and leaves causal explanation off stage, thereby producing stylised descriptions rather than explanations rooted in underlying dynamics (Hameiri, 2020: 643). Studies on the ‘mixed economy’ thus mix-up our understanding of capitalism by taking as given and relying on the very surface processes and economic categories of the ‘mixed economy’ as their subject matter. As a result, ‘mixed economy’ analysis is caught within the mirror of ideology: it is half-illuminating in revealing surface connections across the state/market dichotomy but beneath such appearances it is also half-distorting in obscuring the hidden depths of underlying economic dynamics. As Marx might advise, ‘what all this wisdom comes down to is the attempt to stick fast at the simplest economic relations, which, conceived by themselves, are pure abstractions’. Studies on the ‘mixed economy’ thus recycle the dualism of the state and the market so that ‘sometimes one and sometimes another side is dropped in order to bring out now one, now another side of the identity’ (Marx, 1857-8/1973: 248, 250). All these manifestations also reside in some of the recent economic geography and geographical political economy debates on the role of development banks, with two skeins in the literature pointed out here by way of conclusion. First, there are debates on the ‘entrepreneurial state’ and the future of development banks in traversing the ‘public’ and ‘private’ sector. Development banks have once again been spotlighted as key agents or ‘flexible financiers’ for entrepreneurial states in providing capital and absorbing investment risk, for example in relation to renewable energy projects and the green transition or in supporting infrastructure investment and promoting innovation (see Mazzucato, 2018: 149–150 or Giffith-Jones and Ocampo, 2018: 21–33). Hence, 21st-century development banks are promoted as either at the centre of active, entrepreneurial, risk-taking states, or as crucial second-tier capital lenders (increasingly to micro- as well as small- and medium-sized businesses), aiming to overcome ‘dysfunctional modern capitalism’ (Mazzucato, 2018: 19; Giffith-Jones and Ocampo, 2018: 12–13). Yet, in arguing ‘for a new economics of the common good’ in the interests of ‘blended finance’ (Mazzucato, 2022: 6, 14), a more critical eye on the class pertinency of such advocacy is still needed, as also argued elsewhere in advancing a dynamic theory of development banks (Marois, 2022). Second, there is the recent focus in debates on the ‘new’ state capitalism where development banks are positioned as crucial fixes within mixed economy public-private ownership forms that are called ‘state-capital hybrids’ (Alami and Dixon, 2024: 166, 168). Development banks, it is argued, ‘have returned to fashion’ with more than 900 worldwide, controlling assets worth $49 trillion, used to maintain financial stability, funding infrastructure and providing capital for development projects (Alami and Dixon, 2024: 9). Yet, despite claiming to provide a theory of the emergence of development banks within processes of capital accumulation, such an undertaking is omitted in preference for a focus on developments since the early 2000s that only offers a strictly presentist lens (Alami and Dixon, 2024: 144). This means that the claims about the contemporary rise and mutation of development banks can only ever furnish a partial perspective on their constitution. There remains the challenge of historicising the origins (and mutations) of development banks and to be more precise about the hybridity constituting state capitalism (Alami and Dixon, 2023: 95). Putting into historical context the concentration and centralisation of capital accumulation during ISI and the role of state agents in hothousing for development thus prompts: (1) how contemporary analysis of the class-relational character of state capitalism can be built on (Sperber, 2019, 2022); (2) how a more critical questioning of today’s claims about the aggregate growth of states as promoters, supervisors and owners of capital might be encouraged (Alami and Dixon, 2024: 16); and (3) how points on the different magnitude and unprecedented growth in the centralisation of capital today can be supported (Alami and Dixon, 2024: 157). Returning to our dash of Dobb (1946: 384), under the generic title of state capitalism there are always a number of species – different in social content and significance – shaped by the social relations of production and thus the form of the state, the prevailing class relations, and the class-relevance of state policies, which our argument here has aimed to shape.