Abstract

The rise of asset managers as key nodes of financial intermediation has been one of the most fundamental changes in the global economy over recent years. An emerging literature on asset manager capitalism (AMC) discusses these changes and its implications, though largely in the context of corporate governance in advanced capitalist economies. This paper expands the remit of the AMC literature to spaces outside the global capitalist core, and assesses its implications, based on quantitative data on asset manager allocations and flows, and qualitative data from semi-structured interviews. We find that despite the growth of asset managers’ investments into emerging markets, their presence remains limited and that the threat of exit remains present but increasingly tied with global conditions and the composition of benchmark indices. We also find that asset managers’ investments are increasingly focussing on bonds, and are heavily concentrated in a few companies and sectors, revealing a marginal rather than broad-based presence. Finally, we find very limited evidence that asset managers use their voice to influence corporate governance and macroeconomic policy. Overall, asset managers do not seem to fundamentally reshape the characteristics of financial subordination of emerging markets, and the characteristics of AMCs remain, for now, specific to advanced economies.

Keywords

Introduction

The key actors and institutional structures of the global financial system are changing rapidly. In a development that some have called the rise of asset manager capitalism (AMC) (Braun, 2020a), these changes include: the concentration of asset ownership and replacement of banks as key nodes of financial intermediation by a few large asset managers (AM); a greater role of passive strategies and increasing importance of index providers in steering the flows of capital (Petry et al., 2021); and a reinforcement of market-based finance, characterised by a proliferation of financial securities to store wealth and provide liquidity through collateral-based financial relations.

The literature’s main focus so far has been on the implications of AMC for corporate governance in the context of advanced capitalist economies (Braun, 2020b; Fichtner and Heemskerk, 2020). In particular, it shows the implications the rise of AM has for: the reduction in the structural exit power of financial capital, and its potential ability to stabilise financial markets; the general move towards extensive financial accumulation, that is the expansion of financial assets and institutional transformation towards market-based finance (financialisation); and a potential increase in the exercise of power through voice and engagement with macroeconomic policy and corporate governance.

In their quest to maximise assets under management, AM have become increasingly present in the financial markets of emerging markets (EM) too. Moreover, the institutional changes in the global financial system associated with AMC have had crucial implications for EM’ financial integration (e.g. BIS, 2021). So far though, we lack a systematic conceptual and empirical analysis of how AMC both impacts, and potentially manifests differently in various spaces and in particular in countries characterised by a subordinate position in global monetary and financial markets. A long-standing tradition in critical political economy and heterodox economics (for recent summaries see Alami et al., 2023 and Bonizzi et al., 2022) has shown the systemic and structural nature of EM’ international financial subordination, manifest in both a structural constraint on agency, and a persistent value transfer to the core. Though this literature has analysed specific aspects of recent transformations in the global financial system (e.g. Bonizzi and Kaltenbrunner, 2019; Cormier and Naqvi, 2023; Fichtner et al., 2021; Kaltenbrunner and Painceira, 2018; Musthaq, 2021a; Naqvi, 2019; Petry et al., 2021), so far it has not systematically and conceptually engaged with the rise of AMC.

This paper fills this gap. It brings together the literatures on international financial subordination and AMC to investigate (a) to what extent the main propositions of AMC hold in a different spatial and global structural context, in particular one characterised by international monetary and financial subordination, and (b) whether and how AMC reconfigures and changes EM’ international financial subordination. Empirically, we use a range of financial and macroeconomic data, and secondary and grey literature for 23 EM, defined by their presence in key bond and equity index followed by global AM, 1 as well as insights from 12 semi-structured expert interviews with global and EM asset managers and EM policy makers. We argue that EM’ international financial subordination qualifies some of the core implications of AMC. Though the participation of large AM in EM has increased, their participation is still too narrow and shallow to speak of AMC. Moreover, we show that whilst the rise of AM in EM might lead to similar financial and economic transformation as those observed in advanced capitalist economies, these transformations take particular forms and are fundamentally shaped by these countries’ subordinate integration into the global economy.

In particular, concerning the reduced threat of exit and potential implications for financial stability, we show that this is not–yet–given in EM due to the narrow and shallow exposure of global AM. To the contrary, AM’s increased exposure to EM might further increase these countries’ vulnerability to global financial conditions and risk of large and sudden exchange rate and asset price movements because of AM’ benchmark index following, global investment strategies, and specific liability structures. Indeed, the paper questions whether in a global economy characterised by entrenched hierarchies and a clear core-periphery structure, the reduced threat of exit is a ‘privilege’ of the global monetary and financial hegemon which stands at the top of the hierarchy.

With regards to the shift towards extensive financial accumulation (financialisation), our analysis shows that these processes also take place in EM, though in a specific– subordinate– form. For most clients of AM, EM assets remain risky ‘growth’ or ‘satellite’ assets (Bonizzi and Kaltenbrunner, 2019; Lysandrou, 2018), which means their marketability by AM is constrained by efforts to reduce risk and/or enhance returns. In particular, EM assets sought by AM seem to be tilted towards ‘safer’ debt instrument, which commit to regular, and relatively higher yielding income streams, rather than equity participation. Moreover, AM participation is highly concentrated in ‘safe and liquid’ sectors, in particular traditional comparative advantage sectors and financials.

Finally, concerning the exercise of voice and engagement, in line with what seems to be the case for advanced economies, we find that in EM AM also do not seem to exercise their voice actively. Though we observe a homogenisation of macroeconomic policy across most EM towards inflation targeting regimes cum reserve accumulation and exchange rate management, – which ensure the safe integration of EM into global financial markets – AM seem to exercise little direct influence on these macroeconomic configurations. Though this lack of voice might be due to the risk of political backlash as argued by Braun (2022) for advanced economies, we would argue in EM it is also a reflection of the persistent structural power of AM. This structural power is exercised both through the continued threat of exit (Dafe et al., 2022), and the ability to write the rules of the game (Gill and Law, 1989; Petry, 2021; Strange, 1998) through the dissemination of global investment standards. In the context of corporate governance, AM actions are largely limited to the area of ESG investing. Yet, even here, AM achieve compliance with ESG objectives through the implementation of global criteria and standards, rather than the active exercise of voice.

These subordinate forms of AM exposure modify, yet further cement the structural subordination of EM in the global monetary and financial system, and hence the uneven tendencies of global capitalism. External vulnerability and financial instability – as well as the specific institutional and financial market structures of AMC – maintain, if not deepen, the hierarchic structure of the international monetary system. This currency hierarchy requires EM to gear macroeconomic policy making towards ‘de-risking’ global financial investors at the expense of domestic policy objectives (Gabor, 2023). EM’ specific – subordinate – form of financialisation both reflects and cements the dualistic production structure of EM, characterised by a small pocket of competitive (comparative advantage) sectors, which can engage with international financial markets, and a large number of smaller (domestically oriented) companies, which remain severely finance constraint. Moreover, we show some evidence that the rising importance of AM might tilt domestic economic structures towards the ‘low-risk’ financial or real estate sector. More generally, the institutional transformations towards market-based, and globally integrated financial systems are little conducive to financing long-term structural change (never mind the sustainable transformations needed to address the global climate crisis), and might set up new channels of value transfer to the core. With regards to macroeconomic policy making and the autonomy of EM actors in the presence of the structural power of global finance, our findings indicate that even if AMC might create some more room for active monetary policy and potentially reduces the direct interference into EM economic matters (see also Cormier and Naqvi, 2023), the global constraints remain firmly in place through the rules-based system characteristic of AMC.

Following this introduction and a brief literature review in section 2, the remainder of the paper engages with the three propositions of AMC. Section 3 discusses the possibility of reduced exit power and the implications for financial stability and external vulnerability. Section 4 looks at financialisation processes in EM, and Section 5 examines the role of voice and engagement in corporate governance and macroeconomic policy making. Each section first analyses those propositions in the – internationally subordinate – context of EM, and then sketches out some of the implications these configurations of AM investments have for EM’ international financial subordination. Section 5 concludes.

Conceptualising the interaction between IFS and AMC

The negative implications of EM’ integration into global financial markets have long been an area of concern, ranging from the devastating implications of the external debt crises in the 1980s (e.g. Sachs and Williamson, 1985), the crises of the late 1990s (e.g. Arestis and Glickman, 2002), and more recently the rise of a ‘global financial cycle’ which exposes EM’s to international financial flows largely independent of domestic economic conditions (Rey, 2015). Together with structurally higher interest rates, excessive exchange rate movements, the inability to issue local currency debt, the need to accumulate low-yielding foreign exchange reserves etc., these empirical phenomena have recently been systematically conceptualised under the heading of international financial subordination (Alami et al., 2023). Alami et al. (2023) define IFS as ‘. . .a relation of domination, inferiority, and subjugation between different spaces across the world market, expressed in and through money and finance, which penalizes actors in DEEs disproportionally’ (p. 1363). Though manifest through different empirical phenomena, as exemplified above, the key dimensions of IFS are (a) that it’s both structural and systemic to the global economy (rather than due to domestic policy failures or institutional weaknesses), and (b) that it creates both constraints on agency, and a persistent value transfer from the periphery to the core. Theoretically, the concept of international financial subordination draws on different traditions, including dependency theory, Marxist political economy and imperialism, and the Post-Keynesian currency hierarchy framework (Alami, 2019; Bonizzi and Kaltenbrunner, 2021; Kvangraven, 2021).

More recently, authors in these traditions have started to analyse how international financial subordination is changing in conjunction with recent transformations of the global financial system. For example, Kaltenbrunner and Painceira (2018) show how the increased exposure of foreign investors to short-term, domestic currency assets, creates new forms of external vulnerability manifest in sudden and potentially large exchange rate and asset price movements independent of domestic economic conditions. Bonizzi and Kaltenbrunner (2019) analyse the rise of foreign pension fund investments in EM. Contrary to conventional wisdom, the authors argue that these investments might not act stabilising given pension funds’ embeddedness in the spatially uneven international monetary and financial system. Musthaq (2021a) argues that the rising importance of shadow banking in EM local currency sovereign bond markets represents a shift from a regime of accumulation based on credit intermediation (finance as a service), to one dominated by the maximisation of risk-adjusted returns by global institutional investors. EM are subordinate in this system as ‘providers of not only financial assets in the form of high-yielding government bonds, but also of the necessary liquidity and insurance with which to generate high risk-adjusted returns’ (pp. 559–560).

In this vein, Naqvi (2019) provides qualitative evidence that institutional investors’ business models and investment mandates exacerbated procyclicality in financial flows to EM after the global financial crisis. Importantly, this is the case both for short-term (e.g. hedge funds), and generally more long-term (pension and insurance funds) investors, as the low-interest rate environment forced traditional long-term investors to seek higher yielding assets (for a similar argument in the context of Sub-Saharan Africa see also Bonizzi et al., 2019). Fichtner et al. (2021) show how the use of indices can further cement the global financial hierarchy, as index providers – largely located in core economies – determine the rules that steer financial flows and with which EM actors have to comply. Though these contributions have analysed elements of the recent transformations in global financial markets, and their implications for EM’ financial and monetary subordination, so far there is no systematic conceptual and empirical engagement with the implications the rise of AMC has for international financial subordination. However, whilst structural in nature, the specific forms and empirical manifestations of international financial subordination change with the nature of global financial markets. At the same time, AMC is both enabled by and takes specific manifestations in a context of subordination and hierarchy.

The conceptualisation of AMC is chiefly due to the studies of Braun (2016, 2020a, 2021, 2022). AMC is seen as a new corporate governance regime, which is characterised by the rise of financial institutions managing wealth through mutual and exchange-traded funds (ETFs), as well as the less regulated and more leveraged institutions, namely hedge, private equity, and venture capital funds as the key shareholders in the economy. Asset ownership becomes heavily concentrated in a small number of very large institutions, which hold diversified portfolios across the entire investible world making them true universal owners (Fichtner et al., 2021). The historical emergence of AMC is marked by a period of ‘capital abundance’, where financial intermediation is driven by savers and their agents in search of (scarce) investment opportunities. Thus, in AMC, the search for investable assets and wealth preservation, as opposed to allocating finance to real investment projects (as is the case for financial systems dominated by banks), become the key financial imperatives.

In our reading of the emerging AMC literature, the rise of AM has three important implications for the way capitalism operates. First, with regards to the behaviour of financial institutions and the way finance exerts power, the rise of large, diversified asset managers might reduce the threat of exit and thus bring some stability to financial markets (Braun, 2022). This is so for two reasons. Firstly, while legal owners, AM do not have economic interest in the performance of any particular company, since their profits derive from fees on assets under management and they frequently hold a diversified and broad investment portfolio (Fichtner et al., 2017). Secondly, due to their large stake in a broad range of companies, the structural ‘exit’ power of AM is considerably curtailed as there is literally nowhere else to go. As a result, according to Braun (2016), ‘an economy dominated by AM seeking low-cost exposure to the market portfolio may, in principle, open up the possibility for the internalisation of externalities, the formation of long-term orientations, and the provision of “patient” capital’ (p. 268). This could lead to the interpretation that AMC might spell a period of decreased financial instability. On the other hand, there are indications that AM enhance the sensitivity of the financial system to liquidity conditions (Carney, 2019). Moreover, specific AM behaviour, such as herding around benchmarks, securities lending, margin trading and less stable sources of funding, could further increase the procyclicality of financial markets and impair market liquidity during times of stress (e.g. Fichtner et al., 2017; Haldane, 2014). The greater reliance on passive strategies, in particular, can generate vulnerabilities associated with the changing composition of benchmark indices that AM follow (Arslanalp et al., 2020).

Secondly, whereas ‘bank-based’ capitalism, and indeed the shareholder revolution of the 1980s and 1990s, was characterised by intensive financial accumulation, that is the maximisation of financial returns and ‘rentier share’ of corporate profits, AM care fundamentally about extensive financial accumulation, that is the growth of investable assets to maximise financial assets under management (Arjaliès et al., 2017; Braun, 2016, 2021; Lysandrou, 2018). Thus, more generally, AMC goes hand in hand with an expansion of financial markets and the rise of market-based finance (financialisation), characterised by a proliferation of financial securities to store wealth and provide liquidity through collateral-based financial relations and the institutional transformations necessary to enable them (e.g. the rise of index funds and passive investment strategies, the increased importance of exchanges, and the key role played by central counterparty clearing (Aramonte et al., 2021).

Finally, according to Braun (2022), AMC also potentially implies greater importance of the exercise of power through voice and engagement, and therefore a more direct influence on corporate governance and policy decisions. Concerning corporate governance, rather than the performance of individual stocks, AM care for aggregate asset prices and general liquidity. In the context of macroeconomic policy, rather than lobbying for restrictive monetary policies delivered by independent central banks, in advanced economies AM are seen to support policies that increase private household savings and sustain high asset prices. As a result, they might create room for more active policy interventions. Empirical evidence so far though shows that this potential of increased power through voice is largely unfulfilled. According to Braun (2022), this might be due AM’s concern about a political backlash – and increased regulation – if their power is expressed too overtly.

The literature on AMC has a clear focus on advanced Western economies, and more specifically the US. While undoubtedly the evolution of the US financial system has implications for global capitalism, it remains important to interrogate to what extent its key arguments carry across and/or impact different spaces, in particular those characterised by a subordinate integration into the global monetary and financial system. These interrogations are important theoretically, as they give some indication as to whether the concept of AMC means more than a new form of US corporate governance. They are also important empirically, as they have implications for EM’ management of financial integration, the design of their domestic financial systems, and macroeconomic policy.

Empirically we draw on a mixed-method design which combines quantitative data on institutional investor fund flows to EM, 2 equity ownership of EM companies by the Big Three (Blackrock, Vanguard and State Street) 3 and macro-financial data, with in-depth semi-structured interviews with 12 global and EM asset managers and macroeconomic policy makers, in particular central bankers (for details see Appendix Table 1). Interview partners were sampled purposively based on their respective expertise and geographical location. Interviewee access was based on networks and snowballing, as well as the collection of publicly available contact details. Though we aimed for an even geographical distribution, our sample is biased towards Latin America reflecting our networks, but also interviewees’ willingness to speak to us. Interviews were conducted between February and November 2023 and followed University ethical guidelines. Interviews were semi-structured, that means a general interview structure was followed, but deviations to explore interviewees’ specific expertise were possible. Questions were formulated open ended to explore interviewees’ knowledge and avoid interviewer bias. All interviews were conducted virtually, recorded, transcribed, and coded by all researchers using thematic analysis. Initial categories of interest were informed by the AMC literature, and then refined into themes and sub-themes using the interview material in an iterative and sequential process (Clark et al., 2021). Theme identification was mainly based on repetition. To further explore the role of voice in AMC, we applied progressive theoretical sampling and a more specific interview questionnaire (Interviews 8–12). Thematic saturation was achieved for our three main arguments (financial instability, the nature of financialisation and the role of voice) (Brinkmann and Kvale, 2018). The interviews also allowed uncovering important technical details and mechanisms underpinning our financial and macroeconomic data and relations.

Reduced threat of exit and financial stability

The first key argument of the AMC literature is that the breadth and depth of AM exposure reduces their possibility of exit. As a result, AMC is seen to potentially increase financial stability as investors lack financial assets they can substitute into. This is unlikely to be the case for EM, which remain a small, and peripheral part of AM portfolios. Indeed, as this section shows, the increased exposure of AM might further increase the sensitivity of EM to conditions on international financial markets through processes such as index trading, global investment strategies, and AM’ specific liability structures.

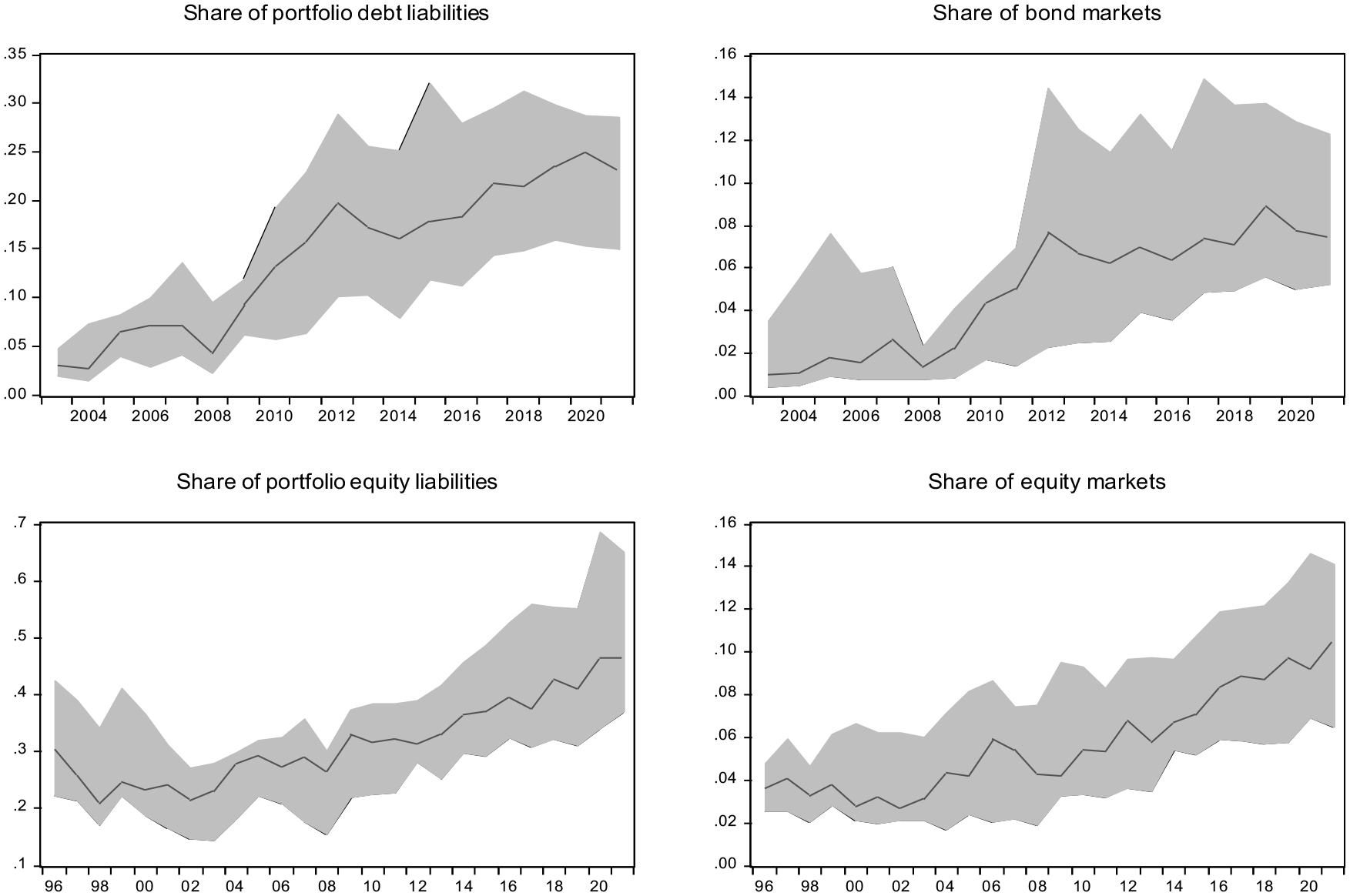

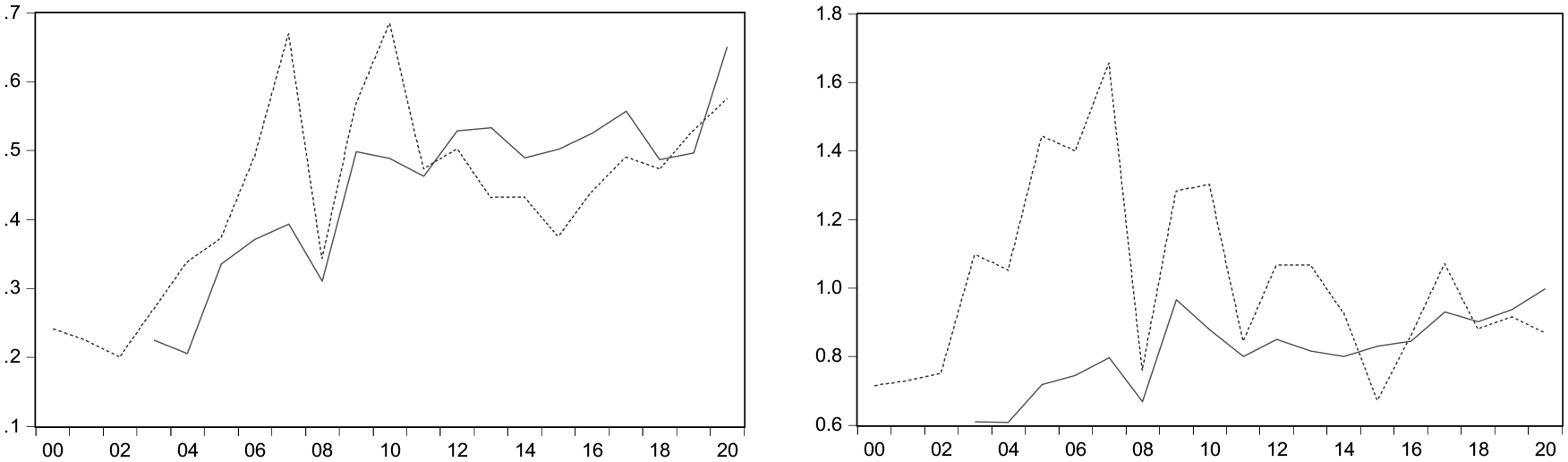

Although AM participation in EM assets has increased considerably since the global financial crisis (in particular in bond markets), their importance for domestic financial markets still remains considerably lower than what has been observed in the US. As Figure 1 shows, across our sample, AM channel an increasing share of portfolio investments to EM, respectively about half of equities and a quarter of bonds in the median EM. They have also become a more sizeable, but still limited force in capital markets, 4 with an ownership of about 10% of equities, and 7.5% of bonds in the median EM.

Asset managers’ growing presence in EM.

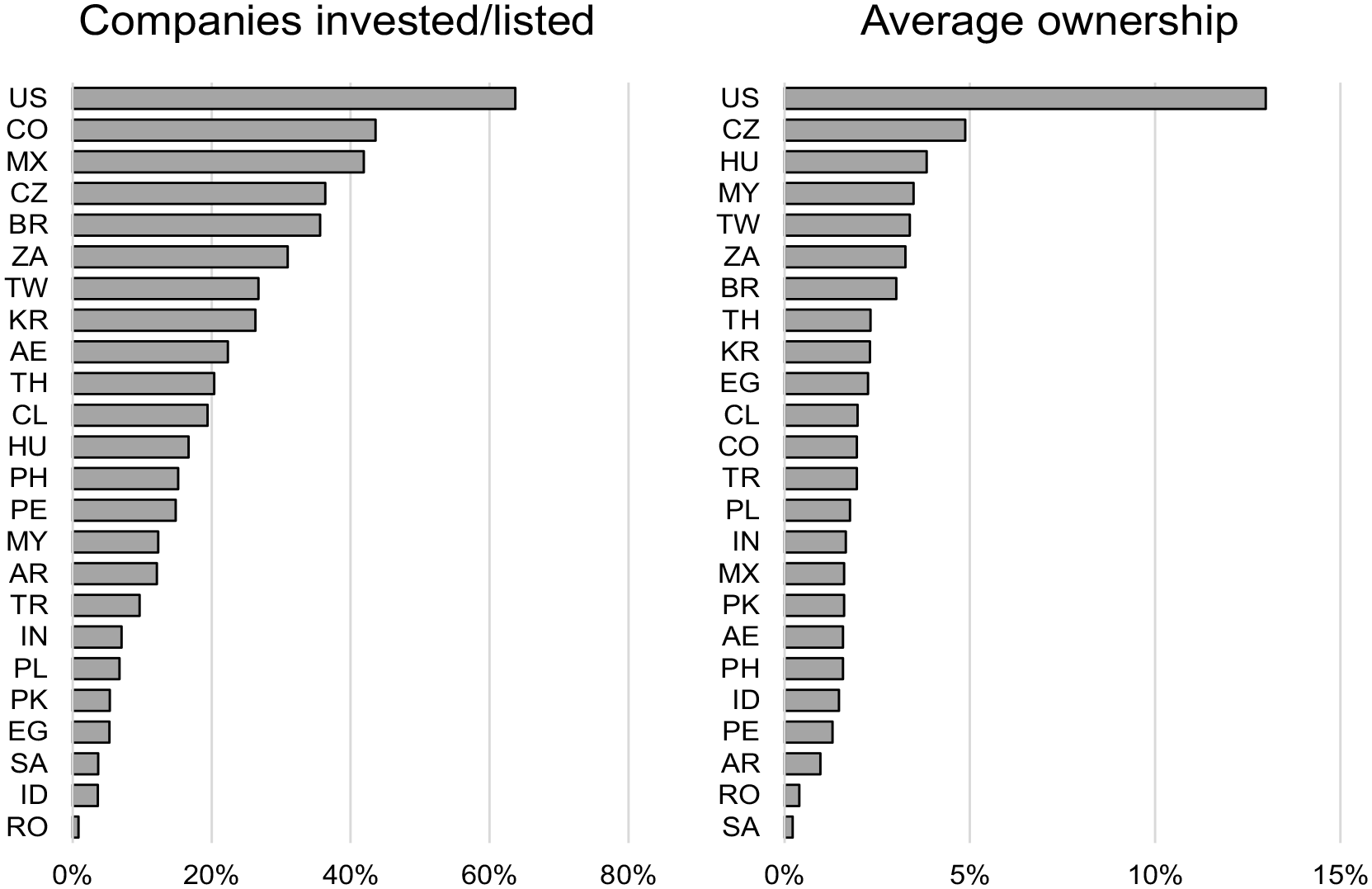

Importantly, with regards to the AMC literature, and in contrast to what has been observed in US financial markets, the exposure of AM to EM assets still remains very limited in terms of breadth (number of companies invested relative to all listed companies) and depth (average company ownership). Looking at the equities owned by the ‘Big Three’ in Figure 2, we can see that on average their ownership in locally listed companies is around 2.1%, with a maximum of 5% in the Czech Republic. This compares to 13% in the United States. In terms of breadth, AM invest in about 18.7% of the listed companies on average. Although the spread across countries is large, with a minimum of 0.84% in Romania and a maximum of 43.6% in Colombia, it still remains significantly smaller than 63% in the US.

The limited breadth of ‘Big Three’s investment.

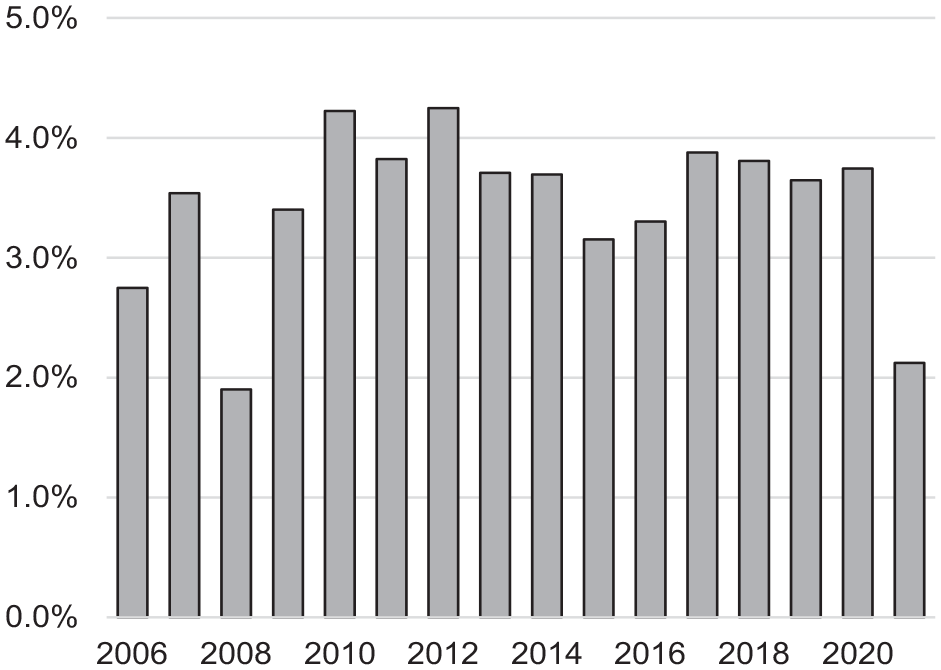

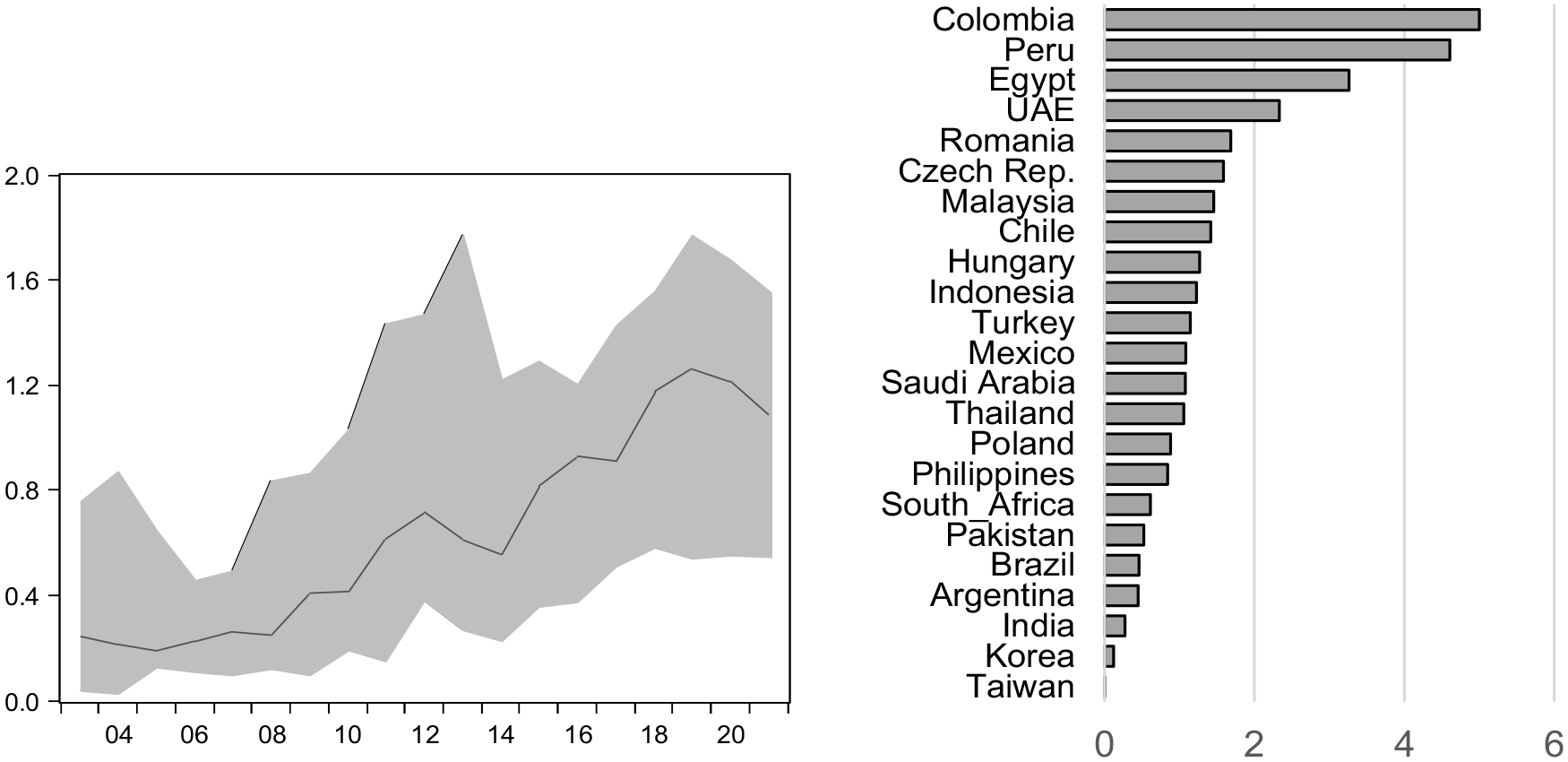

Furthermore, EM investments remain a very small share of AM portfolios. Figure 3 shows that AM investments in our 23 sample countries have been consistently between 3% and 4% of total global investment fund assets. 5 Moreover, there are clear signs of cyclicality. The share of EM assets in total global fund assets declines markedly in years of crises such as 2008 and 2021. These declines are driven both by a decrease in allocations and prices. Thus, as of now, AM remain much less committed to EM assets compared to that in the US, which facilitates their potential withdrawal and maintains the threat of exit.

Asset managers’ exposure to emerging markets.

More than that, rather than alleviating financial instability and external vulnerability, AM might further contribute to it. One reason for that is the importance of index trading and passive investment strategies for these financial actors. As highlighted in the literature (e.g. Arslanalp et al., 2020; Converse et al., 2023; Cormier and Naqvi, 2023; Lau et al., 2020; Petry et al., 2021; Raddatz et al., 2017), AM, more than other financial investors, use indices to inform their investment decisions. The predominance of index trading, however, makes financial flows more sensitive to changes in the index that AM follow as benchmarks (Raddatz et al., 2017). Thus, rather than active buying and selling decisions, investment behaviour becomes characterised by quasi-mechanical benchmark trading, frequently independent of the complex realities of underlying asset markets (Arslanalp et al., 2020; Lau et al., 2020). These quasi-mechanical changes in asset allocation are likely to be particularly significant and synchronised across EM, as investors concentrate around the same indices (Miyajima and Shim, 2014).

As Figure 4 shows, the share of passive investment – which tightly follows benchmark indices – in total holdings has increased significantly over time. In our dataset, cumulative flows from passive funds have been consistently positive since 2014. The increased importance of passive investment strategies in EM financial markets was also confirmed by several interviewees. Interviewees 2 and 4 raised the issue of herding among AM, whereas Interviewee 6 stressed the significant volatility and dependence on global conditions such passive strategies brought to EM (also relative to active strategies which predominated previously).

Share of passive investment.

Sensitivity to changes in the key benchmark indices can be shown by the example of flows to and holdings of Brazilian equities. From January 2011 to January 2014, AM cumulative outflows from Brazil totalled $13 billions, and the value of their Brazilian holdings reduced by over 40, despite average GDP growth rates of 3%, and positive overall capital inflows. 6 This adjustment in AM investments – despite Brazil’ good economic performance – can be explained by the reduced weight of Brazilian stocks in the MSCI-EM index, which declined from 15% to 10% over this period. This decline, in turn, was mostly driven by the underperformance of the Brazilian stock market, which lead to automatic portfolio readjustments by AM.

The ultimate impact of indices becomes evident when countries are added or removed. For example, our EPFR data show that the inclusion of Saudi Arabia in the MSCI-EM index in May 2019 resulted in a very large increase in AM equity inflows, increasing total holdings six-fold in the first 6 months of the year. Another example is Argentina, which had three peso-denominated bonds included in the local currency bond GBI-EM index in February 2017, and then dropped in 2019. On 7th of January, as the inclusion in the index was announced, the price of the three bonds increased by 7%, and AM flows to Argentine bonds increased significantly and remained positive throughout 2017, totalling $3.85 billion or 23% of the holdings at the end of 2016 in our EPFR dataset. Political and economic volatility partly reversed these flows in 2018, but the price of the three bonds contracted further by over 40% in November 2019, as they were delisted from the GBI-EM index (primarily owing to the imposition of capital controls by the new Argentine administration (Campos, 2019)).

Another reason why the heightened exposure of AM to EM assets might increase financial instability and external vulnerability is these financial actors’ sensitivity to global factors. This sensitivity is due, one the one hand, to the global approach AM take to their investments and, on the other hand, their specific liability structures, which are fundamentally embedded in dollar-dominated, market-based international funding markets.

With regards to the first point, our interviews indicated the growing importance of global investment strategies for investors. For example, as an EM asset manager noted: ‘. . .as you manage, you get it more global and less local. . . there’s more money flow into global products compared to regional or selected products’ (Interviewee 4). This was also echoed by a global asset manager: It’s definitely more global because you don’t have too many regional funds there (Interviewee, 5). In this context it is also interesting to note that Interviewee 1 mentioned an increased aspiration of EM to be included in global indices, such as the JP Morgan and Citibank World and International bond indices, rather than specific emerging market indices, ‘which are generally trivial in macro terms’. Interviewee 5 also explained that this global approach becomes particularly important during moments of global portfolio adjustment. According to this interviewee, rather than discriminating among countries depending on their respective fundamentals, AM withdraw their assets from the entire asset class to avoid a product that becomes too skewed towards less liquid, and riskier holdings.

With regards to AM’ liability structure, it is important to note that – in contrast to banks that can create their own liabilities through providing credit – large global AM are reliant on external funding to increase their portfolio. Moreover, in contrast to banks that have at least a share of stable retail deposits, AM raise their liabilities in competitive, international funding markets. These funding markets are dominated by the US dollar, and largely located in advanced economies’ financial centres, which makes AM very vulnerable to changes in global dollar liquidity conditions and ultimate investor demand. For example, most mutual funds allow for daily redemptions, which can lead to sudden selling needs if clients withdraw their investments (Aramonte et al., 2021; Howell, 2020; Schrimpf et al., 2021).

Indeed, as Interviewee 1 pointed out the apparent benefits of EM investment for AM are misconceived partly because in contrast to local actors, which have their liabilities denominated in local currencies, AM face significant dollar liabilities: ‘. . .. . .the key source of volatility. . .is currency. . .and domestics aren’t exposed to currency risk, you know. If you’re a Polish asset manager is doesn’t matter. . .your liabilities are in zloty. . .’ In a similar vein, Interviewee 5 stressed that EM selling pressures in 2022 were largely related to issues in the US Treasury market which forced global AM to adjust their portfolios. The vulnerability to global dollar funding conditions is exacerbated by the fact that, in contrast to banks, AM dont have direct access to the FED as the global lender/dealer of last resort. This is likely to make them – and indeed their clients – more sensitive to expected exchange rate changes (in particular in the case of local currency investments that shift the currency mismatch of cross-border investments to the investor (Bertaut et al., 2021; Kaltenbrunner and Painceira, 2018).

These risks are inherent to (cross-border) investments by AM. However, they are likely to be exacerbated in the case of EM given their subordinate position in international money and financial markets. As discussed in the literatures on currency hierarchy, dollar dominance, and the global financial cycle (Bertaut et al., 2021b; de Paula et al., 2017; Kaltenbrunner, 2015; Miranda-Agrippino and Rey, 2020), the hierarchical structure of the international monetary system, and the dominant role of the US dollar as the global funding currency, make currencies lower down the hierarchy particularly sensitive to changes in global liquidity conditions. In addition, relative to financial markets in advanced capitalist economies, capital and foreign exchange markets in EM remain thinner and less liquid, which increases their vulnerability to fire sales. Indeed, there is evidence that investment funds targeting less liquid asset classes are particularly sensitive to shocks in aggregate liquidity and risk aversion (Aramonte et al., 2021; Falato et al., 2021).

Moreover, EM assets are also more vulnerable to changes in demand by the ultimate assets owners, that is the clients of AMs. This is so, because just as for AM themselves, EM asset continue to occupy a peripheral – ‘return-seeking’ – position in the portfolios of AM clients (Lysandrou, 2018). For example, as Bonizzi and Kaltenbrunner (2019) show in the case of pension funds from advanced economies, although these large institutional investors have increased allocations to EM assets and operate frequently through AM, these assets are not used to hedge their liabilities, which remain firmly embedded within the monetary, financial, regulatory and macroeconomic remit of advanced economies. Instead, EM assets are generally allocated to the ‘growth’ portfolio, whose primary purpose is to generate extra returns (Bonizzi and Kaltenbrunner, 2019). For this role they compete with several other ‘return-seeking’ assets, such as high-yield debt, hedge funds and private equity, the allocation to which increased in a context of a global search for yield. While allocations to EM can bring international diversification benefits, their position in the ‘growth portfolio’ means they are in general not part of stable core investments, and they compete with other asset classes that can similarly bring high returns and diversification benefits.

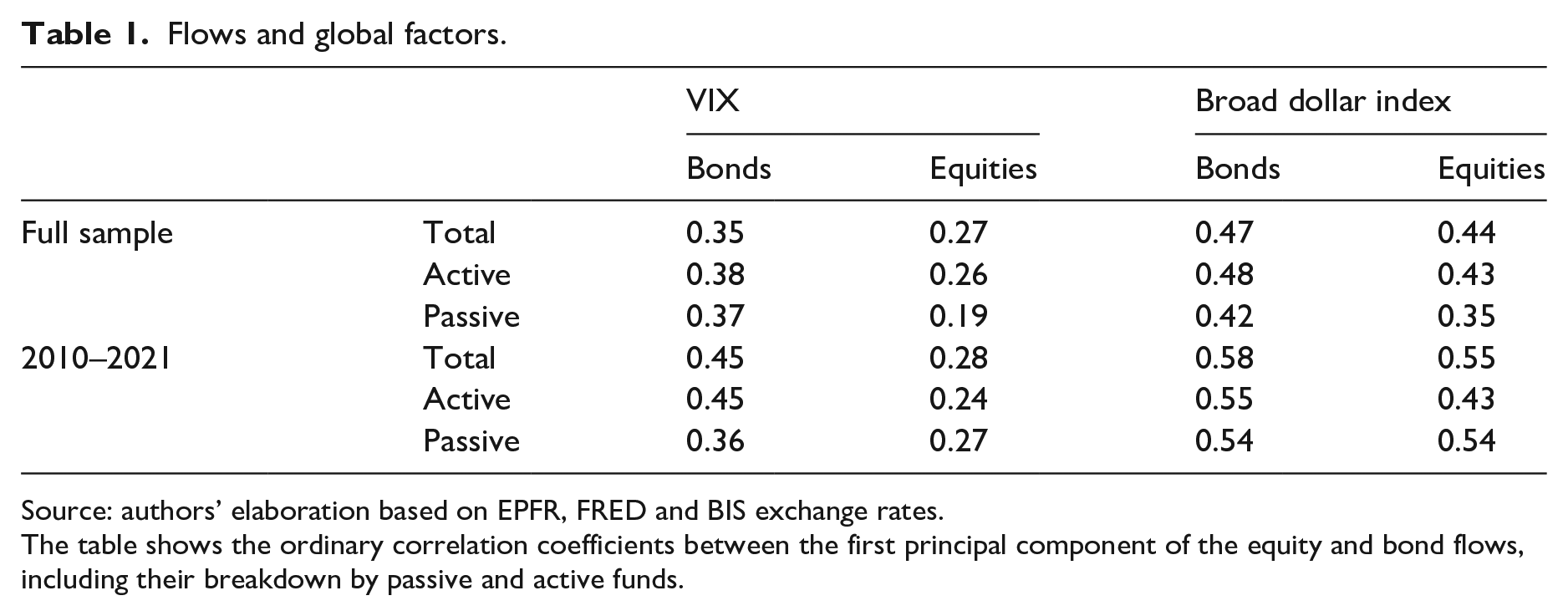

The importance of global factors for AM investments can be seen in the very significant co-movements of the EPFR flows to different countries. To show that, we use the first principal component 7 of the monthly investor flows across the countries in our sample. 8 These explain roughly 56% and 77% of the total variation of equity and bond flows respectively, thus indicating a strong common component in investor flows across EM. Furthermore, as shown in Table 1, these common movements are highly correlated with the VIX and the Broad Dollar Index, which are commonly used as indicators of global risk aversion (Shin, 2016). These correlations have been higher since 2010s, especially for bonds, indicating a stronger pro-cyclicality of bond flows compared to equity flows. With regards to global factors, the correlation with the broad dollar index seems to be stronger than with the VIX, reflecting the dominant role of the dollar for EM.

Flows and global factors.

Source: authors’ elaboration based on EPFR, FRED and BIS exchange rates.

The table shows the ordinary correlation coefficients between the first principal component of the equity and bond flows, including their breakdown by passive and active funds.

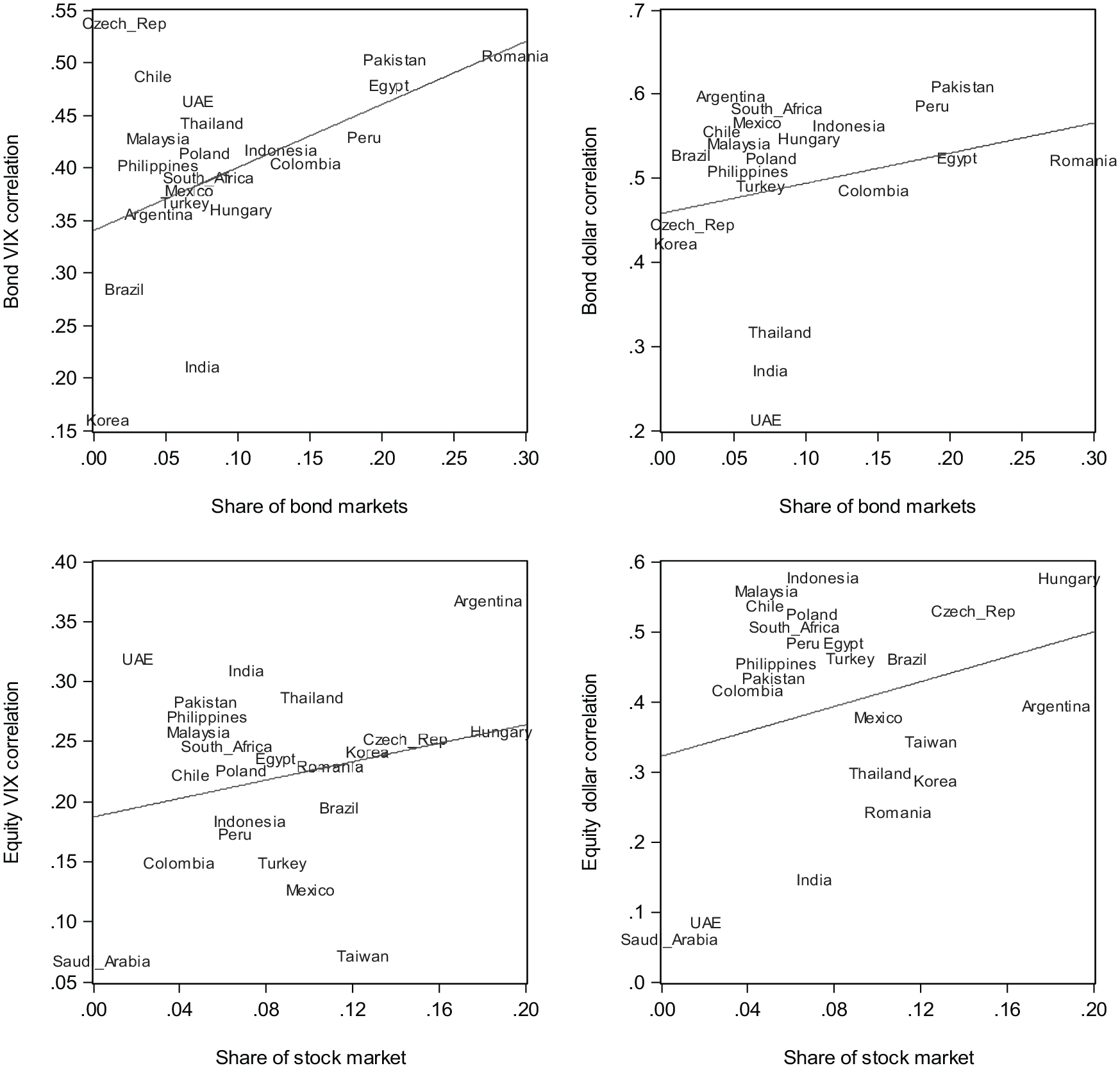

AM sensitivity to global factors appears to be somewhat larger for countries where the presence of AM in stock and bond markets is higher. This seems to indicate that a more significant presence of global AM in a country does not stabilise these flows. This positive relationship between sensitivity to global factors and AM exposure to stock and bond markets, shown in Figure 5, appears to be stronger for bonds than for equities.

Asset manager penetration and global sensitivity.

In sum, above section showed that in contrast to what has been observed for advanced economies, the threat of exit by global AM remains an acute possibility in EM due to the still rather limited depth and breadth of their exposure to EM assets. Indeed, external vulnerability might even be heightened due to the peripheral position of EM in AM portfolios, the relative importance of index trading, the global approach, and the specific liability structure of AM which might exacerbate the transmission of global shocks in the context of a hierarchic international monetary and financial system. During ‘normal’ times, AM follow global financial conditions and keep investment flowing into EM, but during liquidity contractions, the risky and illiquid EM assets are likely to be sold and drop in value, as investors ‘fly to safety’ and/or face significant (dollar) funding pressures. While these represent small portfolio adjustments by major AM, they can result in very large changes in asset prices and exchange rates in EM. Indeed, one could argue that given this hierarchic nature of the global economy, the argument that AMC reduces the threat of exit is limited to the prevalent hegemon which stands at the top of the hierarchy and whose assets are not substitutable. Subordinate, ‘risky’ asset classes – including EM – will always remain in competition to each other, and hence subject to the threat of exit.

These sudden – and potentially very large – exchange rate and asset price movements, however, are likely to further cement EM’ subordinate position in the international monetary and financial system. For one, investors will be reluctant to hold EM assets, unless they are compensated by high returns and/or macroeconomic ‘de-risking’ as put by Gabor (2023: 1), ‘to steer price signals, correcting market failures that generate “uninvestable” risk/returns profiles.’ This involves pursuing policies that enhance market liquidity and external financial stability such as reserve accumulation and exchange rate interventions. However, while these policies may safeguard financial integration, they constrain the space to use macroeconomic policies for domestic objectives, let alone creating the macroeconomic conditions required for long-term structural change or tackling the climate crisis. Moreover, despite gains in competitiveness, large exchange rate devaluations can have a contractionary effect on the economy due to the dollar’s role in determining global borrowing conditions, and the increased uncertainty perceived by EM firms and households (BIS, 2021).

At the same time, whilst continuing to undermine the value stability of EM assets and their currencies, arguably AMC – and the market-based infrastructures underpinning it – work to further reinforce the role of the US dollar as the dominant global vehicle and funding currency. Our EPFR data show that investment funds are largely denominated in US dollars, independent of their location and headquarter. In our sample, the proportion of total holdings held in US-dollar denominated funds as of November 2021 was 65%, compared to 31% of the funds domiciled in the US. It is also higher than other commonly used measures of dollar dominance, such as the proportion of foreign exchange reserves, cross-border banking liabilities, and foreign currency debt, all around 60% (Bertaut et al., 2021b). Moreover, the financial infrastructures and practices underpinning AMC lead to a global segmentation of asset markets, which privileges the dollar as the safe assets (as it does with treasury bonds in the closed economy, e.g. Sissoko, 2019). For example, collateral and margin requirements of clearinghouses, which are skewed towards dollar-denominated assets, create a segmentation in asset markets and can exacerbate dollar demand, in particular during periods of market stress (Shin, 2021). Similarly, Aramonte et al. (2021) show that mutual funds engage in cash hoarding in order to protect against redemptions. On a global level, this hoarding is likely to be in US dollars given the currencies’ dominant role as global means of settlement.

Extensive financial accumulation and financialisation

The second key characteristic of AMC is investment managers’ imperative to expand assets under management to maximise fees and investment income. Thus, in addition to ensuring sufficient financial returns, AMC is also fundamentally about the production of new financial assets. In addition to providing sufficient yields, these assets need to be ‘de-risked’ by putting in place institutions and policies to ensure the liquidity and stability of currency and capital markets so that investors are able to withdraw their assets at no to little loss of value, and meet their outstanding (dollar) liabilities with them (Bonizzi and Kaltenbrunner, 2019; Gabor, 2021; Musthaq, 2021a).

These de-risking pressures should lead to a global homogenisation of institutional, regulatory, and governance structures in line with those prevalent in core financial centres (a process which Gabor, 2020; Konings, 2007 characterised as the ‘Americanisation’ of global finance). In AMC, these pressures can become explicit requirements, as securities need to fulfil certain criteria to be included in key benchmark indices (Fichtner et al., 2021; Petry, 2021). As a result, arguably more so than financial flows dominated by global banks, the rise of AM potentially contributes to the financialisation of the domestic economy, reflected in both: the growth and development of the ‘emerging market’ asset class, and the regulatory and institutional changes (to market-based finance) necessary to make them suitable and ‘safe’ for global investors.

The development of the ‘EM asset class’ is reflected by the substantial growth in capital markets shown in Figure 6 for the 23 EM.

Absolute and relative (to bank-lending) growth in EM capital markets.

One can observe that relative to economic output both stock and bond markets have increased substantially over the last 30 years, reaching nearly 70% of GDP in 2020 (compared to around 150% of GDP in the US). The dynamics are a bit less clear-cut when one looks at the developments of financial markets relative to bank lending. Here, after a surge before the global financial crisis, stock markets seem to have circulated around 80% of bank credit. Bond markets, on the other hand, have increased from near 60% in the early 2000s to equal size in 2020. The EM asset class has therefore significantly grown, more so for bonds than for equities, increasing the availability of assets that AM can market to their clients. Such growth is also important for inclusion in key benchmark indices, which have minimum size requirements (MSCI, 2021).

In addition to contributing to the increase in existing market-based financial assets, AM can also act as catalysts for domestic financial innovations that enable them to expand their assets under management. This is particularly the case for instruments used for passive investment strategies. For example, ETFs are now locally traded in all countries except Argentina and the Czech Republic. 9 Our interviews give some indication that AM play a significant and active role in creating those assets. For example, in Brazil, BlackRock worked closely with the local exchange (B3) and the Brazilian securities and exchange commission (CVM) to enable the cross-listing of its ETFs through the creation of Brazilian Depositary Receipts (BDRs) linked to overseas listed ETFs. Whilst previously limited to accredited investors (financial institutions, investment funds, and/or investments above US$ 200,000), these BDRs were also made available to retail investors ‘in a push to popularise index-based strategies in the South American country’ (Financial Times, 2020; Funds Society, 2014, Interviewee 6). Another key area where AM have contributed to the creation of ‘new’ assets, is in the area of ESG investing. Indeed, as confirmed by all our interviewees, ESGs funds are being actively promoted by AM to broaden their global investment portfolio. As noted by Interviewee 6, labelled bonds might at times allow issuers to price inside their curve and access cheaper financing.

Alongside the increase in financial assets, most EM have been undergoing institutional and regulatory transformations to accommodate market-based forms of financing and assimilate their financial systems to global standards. For example, all EM in our sample have started the process to comply with the Principles of Financial Markets Infrastructure (PFMI), a key aspect of the post-2008 G20 financial regulation reform agenda. As mentioned above, and discussed in more detail by Petry et al. (2021), adherence to such standards is important for AM as the inclusion in key global indices requires EM to conform to these market and infrastructure configurations (Petry et al., 2021, 154). For example, MSCI requires markets to have minimum size and liquidity requirements, as well as market organisation and infrastructure – clearing, custodian and depository institutions, rules on stock shorting/lending – to be included in the index (MSCI, 2021). As passive investors and ETFs become more important, these rules become crucial to guarantee foreign investments. As Interviewee 2 noted: ‘for the ETFs. . . the micro-details are important, for example, the liquidity of the asset that is key. It is a key characteristic that you have to promote if you want to be part of this kind of ETFs, I don’t know iShares from Blackrock. So the liquidity is very important.’ In this vein, Interviewee 6 explained for the case of Brazil that the lack of homogenized regulations, and limited availability of ETFs, was one the reasons why the country remained under-exposed to large AM.

In sum, above discussion showed that en gros EM have experienced a rise in marketable financial assets, and the institutional configurations akin to the processes observed in the US to increase their liquidity and ‘safety.’ The nature of this financialisation process, however, – and with it the implications for the financing of economic development – differ.

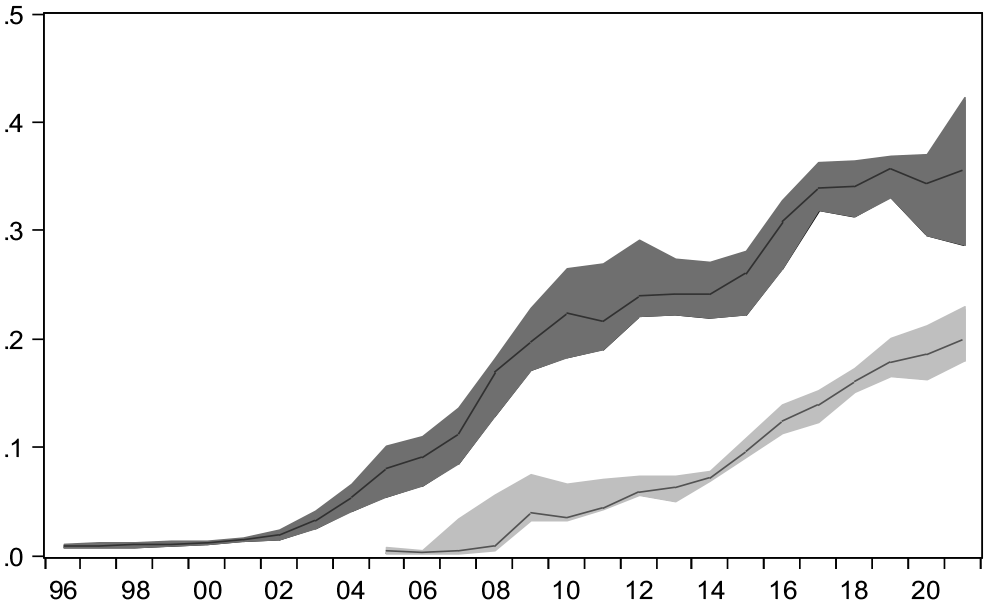

In contrast to the AMC literature on advanced economies, which focuses largely on corporate equity markets, recent capital market expansion in EM has been rather through the bond than the stock market. Figure 7 illustrates that the median country share of bonds versus equity investments by AM in EM increased from 20% in the early 2000s to nearly 120% in 2019.

Bond versus equity holdings by Asset Managers.

The growing importance of bonds is partly the result of the lacklustre performance of EM equity markets in the 2010s, and in some countries the still relatively small size of those markets. However, it also reflects the specific - subordinate - form of EM financial integration. Bond investments are in general safer, offering regular interest payments, which are higher in EM, in contrast to dividends which are performance dependent and up to the discretion of managers. In addition, bonds are less exposed to currency risk than equities, whose returns are related pro-cyclically to local currencies in EM (Bruno et al., 2022. Currency risk can even be entirely removed with foreign currency bonds which predominate in EM, at least in the private sector. Moreover, local bond markets in EM are still dominated by sovereign bonds, which significantly lowers credit risks. Thus, EM bonds represent a safer yet high-yielding 10 option for global investors.

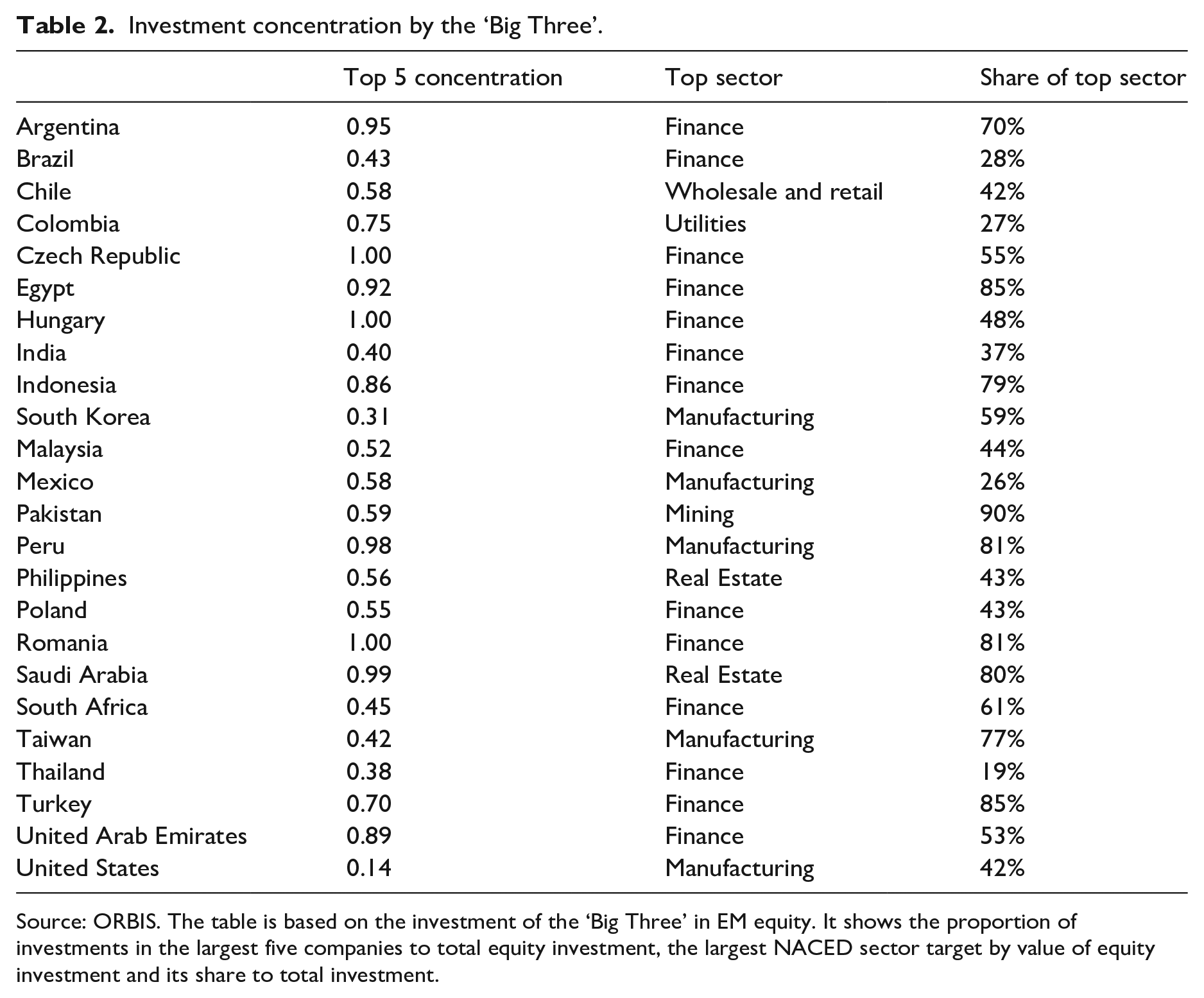

The other important observation about AM exposure in EM, is its highly concentrated nature, both with regards to size of the firms they invest in, and the sectors. Table 2 shows the investment into the largest five companies (as a share of total investments) by the Big Three, as well as the sectors which received the largest share of AM investments (by value).

Investment concentration by the ‘Big Three’.

Source: ORBIS. The table is based on the investment of the ‘Big Three’ in EM equity. It shows the proportion of investments in the largest five companies to total equity investment, the largest NACED sector target by value of equity investment and its share to total investment.

The share of the largest five companies in the total value of AM investments ranges from 31% (South Korea) to 100% (Argentina, Czech Republic and Romania), compared to 14% in the United States. In line with the discussion above, and also stressed by interviewee 6, minimum size and liquidity requirements are a key aspect for index inclusion and hence AM investments. Only a few companies in EM meet these requirements contributing to the strong concentration of AM exposure. Additionally, these investments are heavily skewed by sector. The financial and real estate sector are the largest recipient sectors in 16 out of the 23 EM, often with extremely high shares of total investments. The only genuine exceptions seem to be Korea, Peru and Taiwan, where a high share of investments are in manufacturing companies, similarly to the US (61%). This high concentration of AM investments into ‘safe’ and liquid sectors, in particular financials, was also noted by our interviewees (particularly Interviewees 2 and 6). For example, Interviewee 6 noted that, in Brazil, the financial sector is transparent and ‘the only sector that meets all of the elements an international investors could consider. . .a developed market, using very well the capital market, good liquidity for the asset, ESG triggered. . .’

In sum, above section showed that the rise of AM in EM financial markets has been accompanied by an increase in capital markets, and changes in the structure of domestic financial systems towards more market-based forms, which provide liquid and ‘safe’ financial assets for foreign investors. Though at a much lower rate than in advanced capitalist economies, we also observe the creation of new asset classes which speak particularly to AM portfolio demand, such as ETFs and most prominently ESG assets. However, given the specific – subordinate – role EM assets play for AM, these assets are skewed towards debt rather than equity instruments, bear structurally higher returns than those in advanced capitalist economies, and have been concentrated in a few ‘safe’ sectors, such as real estate and financials.

This specific nature of financial market development arguably does little to provide the long-term, risky financing for the broad-based, structural transformations needed in these economies. Instead, the increased participation of AM in local financial markets seems to cement existing dualistic production structures, where small (largely non-tradable sectors) remain dependent on restricted bank finance, whereas a few selected national champions – and FIRE sectors – take advantage of additional financing opportunities. The imposition of ESG guidelines, on the other hand, is largely driven by AM needs to increase their assets under management, rather than paying attention to the specific developmental needs of recipient economies (the claims of greenwashing aside). For example, Loscher and Kaltenbrunner (2023) show in the context of Nigeria that the significant data requirements to meet ESG standards – conceived in the Global North – will exclude exactly those economies which most need that financing from international capital markets. Moreover, market-based institutional structures might make it more difficult for traditional financing institutions, for example development banks, to provide patient capital (Quist, 2022). As historical evidence shows, the financing of ‘late-comer’ industrial change has been largely due to patient bank financing, rather than capital markets (Gerschenkron, 1962).

Finally, as has also been highlighted in the interviews (in particular Interviewees 7 and 10), EM’ institutional transformations and integration into the global networks of AM might also contribute to facilitating the financial transfer of value from EM to the capital markets in the global North. In line with their business model, AM seek to continuously expand their asset under management, targeting EM clients. In this way, wealth can be channelled through the same circuits used by other investors globally resulting in significant investment flows, as well as fees from EM to the Global North. For example, AM have been very active across Latin America in promoting investment funds that can work as vehicles for international investments of local pension funds (Bonizzi et al., 2021). Several ETFs tracking foreign indices such as the S&P500 are listed by foreign AM in Mexico, Brazil, Colombia and Peru (Johnson, 2020). ETFs are particularly important channels of foreign investments, as they often allow local pension funds to by-pass stringent regulations on asset allocation. In South Africa for example, a regulation was proposed and promoted by AM which would have allowed locally listed ETFs tracking foreign indices as domestic investments (Brown, 2021). Similarly, according to the World Federation of Exchanges, the ability to cross-list Brazilian ETFs provides Brazilians more cost-effective access to global financial markets and the ability to build diversified portfolios (Cohen and Shongwe, 2020).

Voice and engagement: Corporate governance and macroeconomic policy

The final point of the AMC literature this paper engages with is the argument that – due to their broad and deep corporate ownership – AM exercise their power through voice, rather than exit. According to Braun, this voice is not only exercised on the corporate, but also the regulatory, and indeed macro-policy level as concerns about individual firm performance are superseded by an interest in general asset price inflation. However, existing evidence shows that large AM don’t seem to exercise their voice either. For example, recent work by Baines and Hager (2023) demonstrates that AM do not act as stewards for better environmental standards, but generally vote in line with incumbent managers and seldom promote resolutions for green transitions. According to Braun (2022), this failure to exercise voice is related to the increasingly political role of AM and their need to strike a balance between achieving their financial return goals, and generating a (regulatory) backlash against their growing structural power.

Our interviews seem to point in a similar direction. None of the interviewees thought that large AM actively try to steer corporate governance and/or macroeconomic policy. Concerning macroeconomic policy, there was a general perception among interviewees that securing market access, that is, open capital accounts, and a macroeconomic framework of inflation targeting cum managed exchange rates and reserve accumulation was the most suitable macroeconomic policy regime. While managed exchange rates and reserve accumulation reduce the exchange rate risk for foreign investors and secure access to foreign exchange (dollar) liquidity (Kaltenbrunner and Painceira, 2017; Musthaq, 2021a, 2021b), inflation targeting regimes provide macroeconomic homogenisation and transparency (Best, 2018; Painceira, 2023).

However, none of our interviewees thought AM actively exercised voice and engagement to influence this regime choice. Though regular investor meetings took place, none of the interviewees reported that AM expressed a view in these meetings, or indeed attempted to influence them directly. As Interviewee 8 noted: That kind of interaction is almost non existent, really. I’ve never heard a colleague of mine say in an MPC Meeting, for instance ‘Oh, well. the chief Economist of Vanguard was in a meeting. and they said this and this, you know, and this is my view’. I mean that kind of direct communication from those kinds of institutions into our policy-making environment is extremely rare and basically non-existent. Similarly, Interviewee 11 noted ‘. . .the influence of international investors towards the monetary policy stance is very limited unless there is some international turbulence. . ..then the central bank may be providing liquidity to the banks, or doing foreign exchange interventions. . .but in a normal framework of the policy it is very limited what international investor can affect.’

This apparent lack of active exercise of voice reflects the fact that – as discussed in section 3 – structural power through exit remains an acute reality for EM (see also Dafe et al., 2022). Indeed, asked what he thought would happen if the central bank started to deviate from their inflation targeting regime, Interviewee 12 responded: ‘. . .they would probably rush out of their positions in bonds. They have actually done that in some occasions.’ Similarly Interviewee 3 noted: ‘If some government likes to put some capital controls when things are not good, for sure the asset manager is going to think twice about the option to invest in that emerging market.’

Moreover, we would argue, AM lack of active engagement acts as an indication of a second aspect of structural power highlighted in the literature, that is the ability of powerful actors to write the rules of the game (Strange, 1998;; Gill and Law, 1989; Petry, 2021). That is, rather than having to influence EM actors directly, AM set the global parameters within which they have to operate and which determine the ultimate inclusion of countries in the investable spectrum. As discussed above, in AMC, these parameters are increasingly set through the criteria that need to be fulfilled for the inclusion into global indices. These criteria range from indicators of market size and depth, to sovereign debt ratings and macroeconomic policies such as the absence of capital controls. This gives AM and index providers significant power, but an indirect one which differs from the traditional active ‘bond vigilante’ role: As Interviewee 3 noted: The policies are important, but the impact is not direct. . . they are just following rules. The rules are super clear, since the beginning . . . and if you don’t fulfil your requirements, you are going to be out of the ETFs, that’s it, it’s super simple. So it’s actually not the ETF trying to change your behaviour or your policies.

Even in the context of ESG investing, and the implementation of corresponding standards, the influence AM took was rather through setting the criteria, than through active interventions in corporate governance. As interviewee 4 noted: ‘They basically do a little bit of negative screening by taking out all the companies that don’t comply, and they create an index for the reminders which is good. But they are actually not doing any engagement, because if the company is not in the index they are not talking to the company.’

The structural power of the providers of new financial infrastructures has been highlighted by Petry (2021) and Petry et al. (2021) using the example of index providers. Our research would agree with this general finding. However, we also find that even those infrastructures are fundamentally shaped by the actions of AM themselves. Interviewee 1 recounted some examples: ‘China ticked all the boxes, none of the investors wanted China in there, so [a large global bank] created a separate index which includes China, and produced some criteria otherwise to do so.’ He continued: ‘The one, I think slightly interesting thing . . .was the inclusion of the Gulf States. So the UAE and Saudi, and you know, Qatar and a couple of others. Now strictly these did not belong in emerging market bond indices because they are high income countries according to the World Bank. But [a large global bank] just came in one day and said, actually, they’re going in. My understanding is that that was at the request of the managers. . … the large money managers . . …, and then the day after, because they held large amounts of Quatar and Saudi, and whatever they got a big one off boost. . .But that’s a bilateral thing that’s between the clients and the index people. . .and the people who have the influence on index inclusion are the clients. ’

11

The only time, AM exercise active and forceful voice is when the rules get fundamentally broken, in the case of default and/or a serious restriction on market access. For example, interviewee 1 pointed to the involvement of a few big asset managers with significant exposures in the restructuring of Ukraine and Argentinean debt. According to the Interviewee, in the case of the Ukraine, [a large asset manager], which had built a very large position in the country, ‘exercised a huge amount of influence on the shape of final restructuring.’ He explained: ‘. . .what they [the large AM]) are really worried about is a repayment capacity and default. That’s in a way the different parameters we’re looking at’ (in contrast to hedge funds or short-term macro funds’. ‘So it’s really distressed state of debt situations are the one time when you would get a Black Rock or a Franklin Templeton effectively calling the shots.’

Above sections described the spread of globally accepted institutional structures, governance rules, and macroeconomic policy frameworks to EM. This section provided some evidence that, in the EM context, rather than the active execution of voice, this diffusion is taking place through the sustained structural power of global finance (AM). This structural power includes both, the sustained threat of exit, and the ability to ‘write the rules of the game,’ for example through the global dissemination of passive investment strategies and index trading. With regards to macroeconomic policy, it seems that AMC does open some more space for active central bank interventions to safeguard financial and macroeconomic stability (for a similar argument that AMC might open some – temporary – increase in policy space see also Cormier and Naqvi, 2023). In the case of EM, this is particularly manifest in the foreign exchange market, where central banks are key to de-risk AM local currency investments. Yet, these interventions are largely aimed at securing EM’ continued and smooth integration into global financial markets, rather than fundamentally re-orienting macroeconomic policy in support of domestic development. Significant policy measures, which fundamentally try to create some more domestic policy space (e.g. capital controls) are ‘institutionalised’ away, whereas any attempt to seriously break the rules through default is severely sanctioned.

Conclusions

This paper has made a first step in expanding the remit of the AMC literature to spaces outside the global capitalist core. Bringing together the literature on AMC with that on the structural and systemic international financial subordination of EM, it has shown that despite their growing presence in intermediating investments into EM, one cannot speak of AMC in the context of EM. More than that, the paper raised the question whether – from an angle of international financial subordination – AMC remains a ‘privilege’ of the monetary and financial hegemon that stands at the top of a hierarchic global economy.

The paper showed that AM investments in EM remain peripheral, and highly sensitive to global factors, as well as changes in key international benchmark indices. Thus, ‘exit’ remains a distinct possibility, and during periods of financial turbulence, AM do pull out of EM. The characteristics of AM investments are also reflective of the peripheral role of EM in global portfolios: in most EM they are increasingly tilted towards bonds, and heavily concentrated across sectors and companies. There is therefore limited evidence of the sort of breadth of presence seen in US markets. Finally, AM do not seem to exert much significant active influence on corporate governance and macroeconomic policy in EM. Their influence is largely indirect, through the design of international rules, especially concerning those governing the inclusion into indices and ETFs, reflecting AM growing structural power.

Yet, despite their limited and concentrated presence, AMC – as an advanced country phenomenon – has major implications for EM and ultimately cements their international financial subordination. Heightened external vulnerability and financial instability maintain constraints on policy making and set up new channels of value transfer. Concentrated and skewed capital provision does little to finance productive structural change and provide stable and broad-based liquidity to domestic financial markets. Market-based financial systems are historically ill-suited to provide long-term, stable, and indeed risky finance to industrial development. AM act less as bond vigilantes, pressuring governments into specific policies, which could be seen as opening up additional space for policies. At the same time, there is limited scope for deviating further from conventional policies (e.g. capital controls), as this would likely lead to countries’ and companies’ exclusion from the AM investable spectrum.

An important limitation of our article is that it focuses on global trends and subordination of EM as a group and asset class. By so doing so, it inevitably underappreciates the importance of cross-national variation. While a move to global index investment generates more synchronous cross-country investment patterns, domestic political and institutional factors continue to matter for global finance and financialisation (see e.g. Bonizzi and Karwowski, 2023). While not an explicit focus of our paper, our analysis shows significant differences in the nature of integration across EM, in terms of depth and breadth of AM investment as well as domestic market structures. Understanding these cross-country differences and their interaction with domestic political and institutional factors is crucial to fully appreciate the extension of AMC in EM.

On a more general level, our analysis shows that as long as the global financial and monetary asymmetries exist, so will international financial subordination. Though different types of investors, in particular those with a longer investment horizon, might mitigate some of the worst implications, their embeddedness in those asymmetric structures – and with it international financial subordination – remains. The logical conclusion seems to be that developing EM financial systems, for example through promoting domestic institutional investors and regional financial centres, and making their currencies more accepted internationally, will be key to reducing their monetary and financial subordination. Whether this is really the case remains to be seen and requires substantially more research.

Footnotes

Appendix

List of interviewees.

| Interviewee | Position | Region | Date | Modality |

|---|---|---|---|---|

| Interviewee 1 | Global Asset Manager | Europe | 8th of February 2023 | Virtual |

| Interviewee 2 | Risk Manager – ECE Asset Manager | Latin America | 28th of February 2023 | Virtual |

| Interviewee 3 | EM financial regulator | Latin America | 2nd of March 2023 | Virtual |

| Interviewee 4 | EM/Global Asset Manager | Latin America | 2nd of March 2023 | Virtual |

| Interviewee 5 | Global Asset Manager | Europe | 3rd of March 2023 | Virtual |

| Interviewee 6 | EM Financial Regulator | Latin America | 13th of March 2023 | Virtual |

| Interviewee 7 | EM Central Banker | Latin America | 15th of March 2023 | Virtual |

| Interviewee 8 | EM Central Banker | Africa | 14th of November 2023 | Virtual |

| Interviewee 9 | EM Central Banker | Europe | 29th of November 2023 | Virtual |

| Interviewee 10 | EM Central Banker | Latin America | 5th of December 2023 | Virtual |

| Interviewee 11 | EM Central Banker | Latin America |

5th of December 2023 | Virtual |

| Interviewee 12 | EM Central Banker | Latin America |

7th of December 2023 | Virtual |

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.