Abstract

Studies of job loss and deindustrialisation have tended to reproduce findings of long-term disadvantage for people and places. Far from purely reflecting matters of historical interest, recent studies have found that deindustrialisation exhibits a ‘half-life’ in which effects linger for generations after major closures. But these literatures are yet to fully consider job loss in contemporary societies where workers’ lives have been transformed by assetisation. Historical studies of deindustrialisation have tended to focus on times and places where assets were marginal to working-class peoples’ lives. Combining insights from parallel literatures on deindustrialisation, job loss and assetisation, this article addresses the questions: How important is asset ownership for workers during mass closure events? And to what extent does asset ownership generate new fault-lines of inequality between workers when confronted with job loss and its aftermath? These questions are addressed by quantifying financial outcomes, home ownership, and retirement arrangements for a group of nearly 900 older workers whose long careers were extinguished by major plant closures in 2017. While findings demonstrate that workers with greater asset ownership were relatively protected from the negative impacts of unemployment and precarious work, they also contribute to recent debate about the role of labour in the asset economy by pointing to the dynamic interaction of assets and employment over the working life course; that outcomes from job loss are shaped by the interaction of assets and employment, not assets or employment.

Introduction

The idea that the high-income countries and regions have been reshaped by deindustrialisation is well-known. Numerous studies argue that major closures have had devastating effects on people and places (Bluestone and Harrison, 1982; High, 2003; Irving et al., 2022; Massey and Meegan, 1982; Sugrue, 2005; Webber and Weller, 2001). Common effects include lower incomes, long-term unemployment, and exposure to labour markets typified by precarious or insecure work (Bailey and de Ruyter, 2015; Barnes, 2021), as well as negative consequences for workers’ mental and physical well-being (Beer et al., 2006; Dudley, 1994). While such effects have been documented since the early 1980s, these are far from matters of purely historical concern. More recent interventions have established that deindustrialisation possesses a ‘half-life’ in which impacts are transferred cumulatively and intergenerationally (Linkon, 2018).

While deindustrialisation and job loss thus raise matters of ongoing importance, the context in which mass layoff events occur is very different to the earlier wave of studies in the 1980s and 1990s. Some important features of change have been acknowledged, including the preponderance of multi-income households and higher employment insecurity for younger workers (Damaske, 2021; Morris, 1995). However, the increasing social dominance of the asset economy has not received the attention needed to fully understand job loss in the contemporary era. While assets were assumed to be marginal to working-class households affected by closures in previous eras, the treatment of housing and retirement savings as assets has reshaped the context for job loss.

In this article, it is argued that the asset economy has become sufficiently central to household financial arrangements that it now plays an important role in workers’ life trajectories after job loss. Nowadays, workers’ material conditions are differentiated by assets possessed at the time of job loss, as well as by employment conditions and occupational status. This argument is demonstrated through the study of a group of workers whose long careers were extinguished after the closure of an entire industry – the Australian automotive manufacturing industry – in 2017. Although following a familiar trajectory into employment insecurity, workers’ capacity to insulate themselves from the negative effects of precariousness in workplaces and labour markets was shaped by asset ownership in housing and retirement savings.

While the article’s findings are consistent with claims that the asset economy has become a dominant influence over workers’ lives (Adkins et al., 2021), they also demonstrate the dynamic and interactive combination of causal mechanisms rooted in assets and employment. Methodologically, this is demonstrated in two senses covering the periods before and after redundancy: In the lead-up to closure, the benefits of participation in the asset economy were tied strongly to occupations and job tenure. In the aftermath of closure, workers’ subjective financial security and wellbeing was tied to the benefits of asset ownership and secure employment. Conversely, those without assets reported much poorer financial security and wellbeing. The mixed fortunes of this cohort offer a glimpse into the future for younger workers blighted by falling housing affordability, alongside rising insecurity and uncertainty in labour markets.

Section two of this article offers a review of literature on deindustrialisation and job loss, demonstrating that, despite advances in the study of household financial arrangements, considerations of asset wealth among workers are largely absent from the field. This section thereby demonstrates the relevance of recent debates on the relationship between assets, work and social class. Section three outlines the article’s approach, based on a three-step methodology that combines ordinal regression modelling and data comparison between the study cohort and national-scale trends. Section four outlines results from each of these steps, before concluding with the implications of article findings for contemporary research on deindustrialisation and job loss.

Deindustrialisation and job loss in the age of assetisation

International research on deindustrialisation and job loss has accumulated over decades into a vast interdisciplinary field (Cowie and Heathcott, 2003; Strangleman and Rhodes, 2014; Weller, 2012). The most common conclusion within this field is that closures and mass layoffs have been devastating for workers, households, communities and places in, for example, North America (Bluestone and Harrison, 1982; Cowie and Heathcott, 2003; High, 2003; Linkon and Russo, 2002; Sugrue, 2005), Britain (Harris et al., 1987; Hudson, 2005; Massey and Meegan, 1982; Westergaard et al., 1989) and Australia (Beer et al., 2006; Irving et al., 2022; Webber and Weller, 2001). Studies of deindustrialisation have tended to reproduce findings that mass redundancies lead to unemployment and precarious employment (Bailey and de Ruyter, 2015; Barnes, 2021; Standing, 2011), 1 as well as negative consequences for workers’ physical and mental health. Studies have repeatedly found that outcomes are worse for women and racial minorities (Sugrue, 2005; Weller and Webber, 2004). While such findings are well known, the impacts of deindustrialisation are far from matters of purely historical concern. Deindustrialisation possesses a ‘half-life’ that continues well into the 21st Century through reverberating and intergenerational effects (Linkon, 2018).

However, major socio-economic changes have occurred since the heyday of deindustrialisation studies in the 1980s to transform the context for job loss. These include the feminisation of paid employment and concurrent changes to the provisioning of paid and unpaid work within households (Damaske, 2021; Morris, 1995), as well as rapid industrial development across the Global South led by China (Barnes, 2017), the crisis of climate change (Weller, 2019), and the emergence of Industry 4.0 technologies (De Propris and Bailey, 2020). This article focuses on another major qualitative transformation – the rise of the asset economy. This concept suggests that capitalism has become gradually attuned to logics of asset price inflation (Adkins et al., 2020) and to an institutional process – one of ‘assetisation’ – in which things, possessions and attributes are treated increasingly as assets (Birch and Muniesa, 2020; Christophers, 2021b). In particular, the assetisation of housing and personal savings has been encouraged by a range of policy changes since the 1980s, including the conversion of public housing into mortgaged property in Britain and the favourable tax treatment of capital gains in Australia and the US. While these trends have incorporated working-class people into the asset economy in much greater numbers, they have also generated new and much wider socio-economic inequalities (Adkins et al., 2021; Piketty, 2014).

Yet, despite evidence of transformative impacts on workers, the asset economy has received almost no attention in ongoing research on deindustrialisation and job loss. In early studies, terms such as ‘asset’ and ‘wealth’, or even ‘mortgage’ or ‘debt’, were rarely mentioned (see, e.g. Bluestone and Harrison, 1982; Massey and Meegan, 1982). Of course, historical and geographical context explains part of this absence. In Britain and Australia, for instance, asset ownership was less important, simpler, and more marginal to working class people in the 1980s and 1990s (Morris, 1995; Weller, 2012). Nevertheless, deindustrialisation studies have not caught up to new realities of assetisation among workers. Important British studies of household financial arrangements did not extend into the worlds of asset wealth (Harris et al., 1987; Morris, 1995; Pahl, 1984; Walkerdine and Jimenez, 2012), while American and Australian studies on the entanglement of workers’ benefits in company assets did not generalise beyond the specifics of bankruptcy cases (Dudley, 1994; Weller, 2012).

In rare cases, studies foreshadowed concerns raised in contemporary studies on the asset economy. Webber and Weller’s (2001) comprehensive study of job loss among textile, clothing and footwear workers in Australia found that migrants often purchased additional houses as investment properties for their adult children. Weller’s (2012) later study of unemployed airline workers found that workers often borrowed additional money by using the value of housing equity as collateral, a practice known as equity borrowing. This analysis drew on Parkinson et al.’s (2009) study of equity borrowing in Britain and Australia which argued that equity borrowing and mortgage equity withdrawals had become ‘reasonably routine’ by the early 2000s, especially in times of need such as job loss (see also Lowe et al., 2012; Wood et al., 2013).

Notwithstanding these insights, the effects of assets on the socio-economic differentiation of workers have not been addressed in any systematic way in studies of deindustrialisation and job loss. The key to assetisation among workers is the tendency to treat increasing fractions of workers’ income as assets. For example, housing is not a financial asset from the vantage point of renters, nor necessarily framed thus by mortgaged residents if their intention is solely to occupy a property. But housing becomes an asset when it becomes an investment property for private rental income, if equity in the property is used as collateral to borrow additional funds, if acquisition presupposes expectations of future capital gains, or if it is treated by policymakers as an asset in terms of favourable tax concessions. Australia and Britain provide important examples of societies where the treatment of residential housing as an asset has become dominant (Adkins et al., 2020, 2021; Christophers, 2019, 2021b; Doling and Ronald, 2010; Forrest and Hirayama, 2015).

Like housing, retirement savings can become assets from the vantage-point of workers; in this case, when they are invested into financial securities. Australia provides a useful context for the treatment of retirement savings as assets because its system of compulsory private pension fund contributions applies to all employees and employers. While this system, known locally as superannuation (herein ‘super’), was widely practiced among managerial and professional salary earners after World War Two, all employers in Australia have been required to pay a fraction of employees’ wages into a pension fund since 1992. At the time of writing, the minimum compulsory super rate was 10.5% of wages. Super was intended as a means of supplementing and, ultimately, displacing the public aged pension as the primary means of subsistence in retirement and old age. While super has enriched many retirees, it has also deepened inequality between those who use high-value ‘self-managed super funds’ as investment vehicles into property and financial assets (Stebbing and Spies-Butcher, 2016) and low-paid, disproportionately female workers whose super is too meagre to provide meaningful protection in retirement (Masterman-Smith and Pocock, 2008).

The dominant treatment of super and housing as assets in Australia has influenced claims that asset ownership has supplanted employment as the primary determinant of life chances and class inequalities (Adkins et al., 2020, 2021). Others have retained emphasis on the importance of employment as the main causal mechanism in the reproduction of such inequalities (Christophers, 2021a; Wigger, 2021). This article seeks to address the interaction between assets and employment in the context of mass layoffs, thereby contributing to the ongoing advancement of deindustrialisation scholarship by correcting the absence of asset ownership in studies of workers who lose jobs. Its case study on the closure of auto manufacturing in Australia is relevant because asset ownership among these workers was widespread. Furthermore, a common outcome following job loss was a combination of precarious work and unemployment. Prior to the closure, over 85% of workers were in permanent fulltime jobs; 3 years after the final closures, 14.4% of workers were still unemployed, although many of these workers had been through more than one job post-closure. Of those in paid employment, 66.4% had a permanent contract and 33.6% were in casual, agency, fixed-term or other insecure employment arrangements (Irving et al., 2022). While such findings are not new, the article demonstrates what happens when asset ownership is considered alongside these labour market effects.

Methodology

This article uses a three-step methodology to address the role of assets in the differentiation of worker outcomes following job loss. The first step quantifies and compares the magnitude of asset- and employment-based variables with a significant impact on workers’ life chances. The second step quantifies and compares variables with a significant impact on asset ownership during workers’ career histories. The third step assesses the relative social importance of these findings by comparing impactful predictor variables with Australia’s working-age population.

For each step, primary data was drawn from a longitudinal study of workers who lost their jobs after the closure of auto manufacturing in Australia. Between late 2016 and late 2017, Australia’s last three carmakers – Toyota, General Motors Holden and Ford – closed down their domestic car manufacturing facilities. Approximately 14,000 job losses had occurred among the three carmakers and their manufacturing suppliers 12 months after the final closures (Australian Government, 2019). The first wave of survey data, conducted in mid-2020, drew 1277 responses from retrenched workers across Victoria and South Australia (SA) where manufacturing facilities were located (Irving et al., 2022). This article draws data from Wave 2 of the longitudinal survey in mid-2021 (n = 886) which included questions about workers’ financial security, asset wealth and housing status, as well as their labour market status and employment conditions.

Step 1. Ordinal regression modelling for subjective financial security & wellbeing

The first step uses ordinal regression analysis to test work-based and asset-based predictor variables against two proxies for material life chances: Subjective Financial Security (SFS) and Subjective Wellbeing (SWB):

• SFS is based on workers’ answer to the question: ‘How secure do you feel about your overall financial situation?’ Participants chose from an ordinal scale of answers: ‘Not secure at all’, ‘Not very secure’, ‘Slightly secure’, ‘Very secure’, and ‘Extremely secure’. This 5-scale response was simplified to a 3-scale ordinal variable based on ‘low’, ‘medium’ and ‘high’ SFS.

• SWB is based on the answer to the question: ‘How much better or worse off has your life as a whole changed since you finished in the automotive industry?’ Participants chose from the following ordinal scale: ‘A lot worse’, ‘A bit worse’, ‘About the same’, ‘A bit better’ and ‘A lot better’. Like SFS, this was simplified to a 3-scale variable based on the descriptors, ‘worse’, ‘same’ and ‘better’.

The basic proposition is that workers in a more materially prosperous position were more likely to report higher SFS. Furthermore, workers in a stronger material position at the point of job loss were expected to be likelier to report a positive change in SWB since, that is, more likely to report that SWB was the same or better than those in a relatively weaker position materially.

The concept of SWB deployed in this article has similarities with developments in psychology (Diener et al., 1999) and sociology (Inanc, 2018), although its focuses on a subset of SWB – life satisfaction, rather than feelings or affect – during a specific time-period (time since job loss). The concept of SFS has similarities with that of subjective financial wellbeing (Arber et al., 2014), although it is measured here as a general subjective reflection on an individual’s financial status in life rather than a conventional focus on the adequacy of income to maintain a subjective standard of living or to avoid financial stress. As with extant studies, there is a relationship between material wellbeing (such as SFS) and SWB, but they are also distinct and mutually irreducible. For the study sample, SFS and SWB were moderately correlated (r = 0.37, p < 0.001, n = 886) and, as demonstrated below, predictors for each variable were different.

To select predictors for ordinal regression modelling, two approaches were taken. First, model predictors were constructed for 13 variables aggregated into three groups:

• social variables: age; gender; birthplace: whether respondents were born overseas and primarily speaking a language other than English at home (0) or born in Australia or primarily English-speaking at home (1); highest level of education; presence of at least one additional contributor to household income

• labour-based variables: labour market status, whether unemployed (0), withdrawn from the labour force (1) or in paid work (2); duration of previous employment in auto industry (years); size of redundancy payment; weekly wage in previous job in auto industry; occupational group in auto industry, measured as: manual process workers, operator or labourer (0), manual craft worker (1), services or clerical worker (2), professional (3), manager (4) 2

• asset-based variables: housing status, whether renting (0), paying mortgage (1) or outright homeowner (2); investment property ownership (0, 1, 2, 3 or more); confidence about super, whether low (0), medium (1) or high (2) 3

Second, in order to measure effects from the quality of new jobs, separate models were constructed for the subset of Wave 2 respondents in paid employment. This model used the same predictor variables as above but removed the first labour-based variable – labour market status – replacing it with the following three variables: employment contract in current job, whether insecure (0), permanent part-time (1) or permanent fulltime (2) 4 ; occupational group in current job, measured on the same occupational scale as above; and, weekly wage in current job.

Step 2. Regression modelling for asset wealth

Step 2 deploys the same broad approach – regression analysis – to predictors of the asset-based variables listed in Step 1, with the addition of a fourth variable, housing equity, that provides respondents’ estimated net wealth on their primary residence. This is calculated by subtracting self-estimated residual mortgage debt (i.e. how much mortgage debt remains on a respondent’s primary residence) from self-estimated current market value, or what a respondent believes their primary residence is worth on the open market.

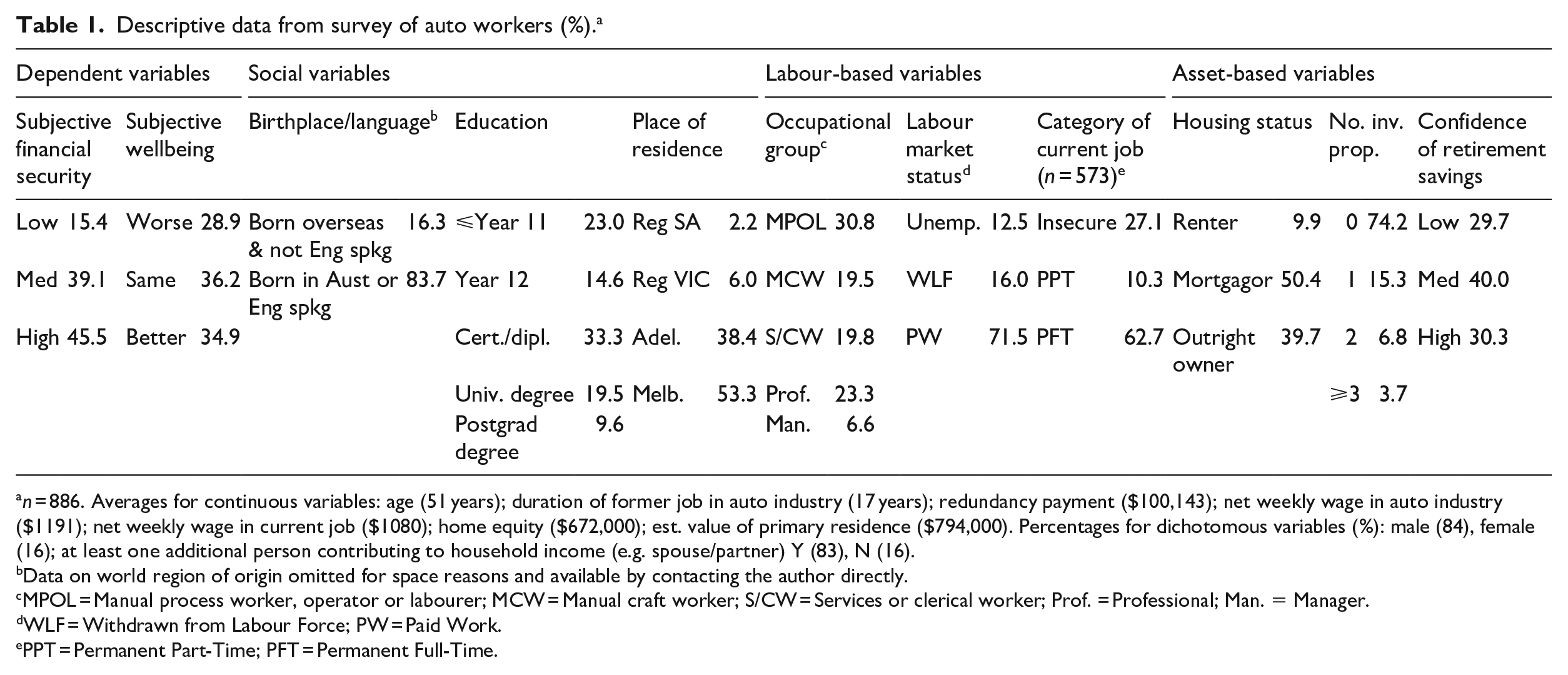

Predictor variables were two of the labour-based variables listed in Step 1 – duration of previous employment and occupational group – as well as each of the social variables, with the additional of a further two: world region of birth, whether a worker was born in Africa and the Middle East (0), South and Central Asia (1), East Asia and Oceania (excluding Australia and New Zealand) (2), non-English speaking countries in Europe and the Americas (3), Australia and other mainly English-speaking countries (4); and, place of residence, whether in Regional SA (0), Regional Victoria (1), Adelaide (2) or Melbourne (3). This latter variable was derived from respondents’ post/zip codes. Step 2 modelled predictors against the first three dependent variables using ordinal regression as per Step 1. The fourth dependent value (housing equity) was modelled using stepwise multiple regression due to its continuous, rather than ordinal character. Descriptive data for variables used in Steps 1 and 2 are provided in Table 1.

Descriptive data from survey of auto workers (%). a

n = 886. Averages for continuous variables: age (51 years); duration of former job in auto industry (17 years); redundancy payment ($100,143); net weekly wage in auto industry ($1191); net weekly wage in current job ($1080); home equity ($672,000); est. value of primary residence ($794,000). Percentages for dichotomous variables (%): male (84), female (16); at least one additional person contributing to household income (e.g. spouse/partner) Y (83), N (16).

Data on world region of origin omitted for space reasons and available by contacting the author directly.

MPOL = Manual process worker, operator or labourer; MCW = Manual craft worker; S/CW = Services or clerical worker; Prof. = Professional; Man. = Manager.

WLF = Withdrawn from Labour Force; PW = Paid Work.

PPT = Permanent Part-Time; PFT = Permanent Full-Time.

Step 3. Comparing cohort results with Australia’s working-age population

Step 3 compared findings from Steps 1 and 2 with equivalent historical measures for Australia’s working-age population using Australian Bureau of Statistics (ABS) data. Descriptive analysis of trends in key social, labour-based and asset-based variables aimed to discern the most important lessons from the study’s findings; for example, which findings were most relevant or instructive in understanding wider social trajectories in terms of work, the diffusion of asset ownership among workers, and interactional effects. Results from Steps 1-3 are outlined below.

Study results

Step 1. Results from ordinal regression of subjective financial security & wellbeing

As described above, Step 1 was based on four ordinal regression models. These models aimed to predict:

• SFS, based on predictors from the:

○ whole study cohort (

○ sub-cohort in paid employment (

• SWB, based on predictors from the:

○ whole study cohort (

○ sub-cohort in paid employment (

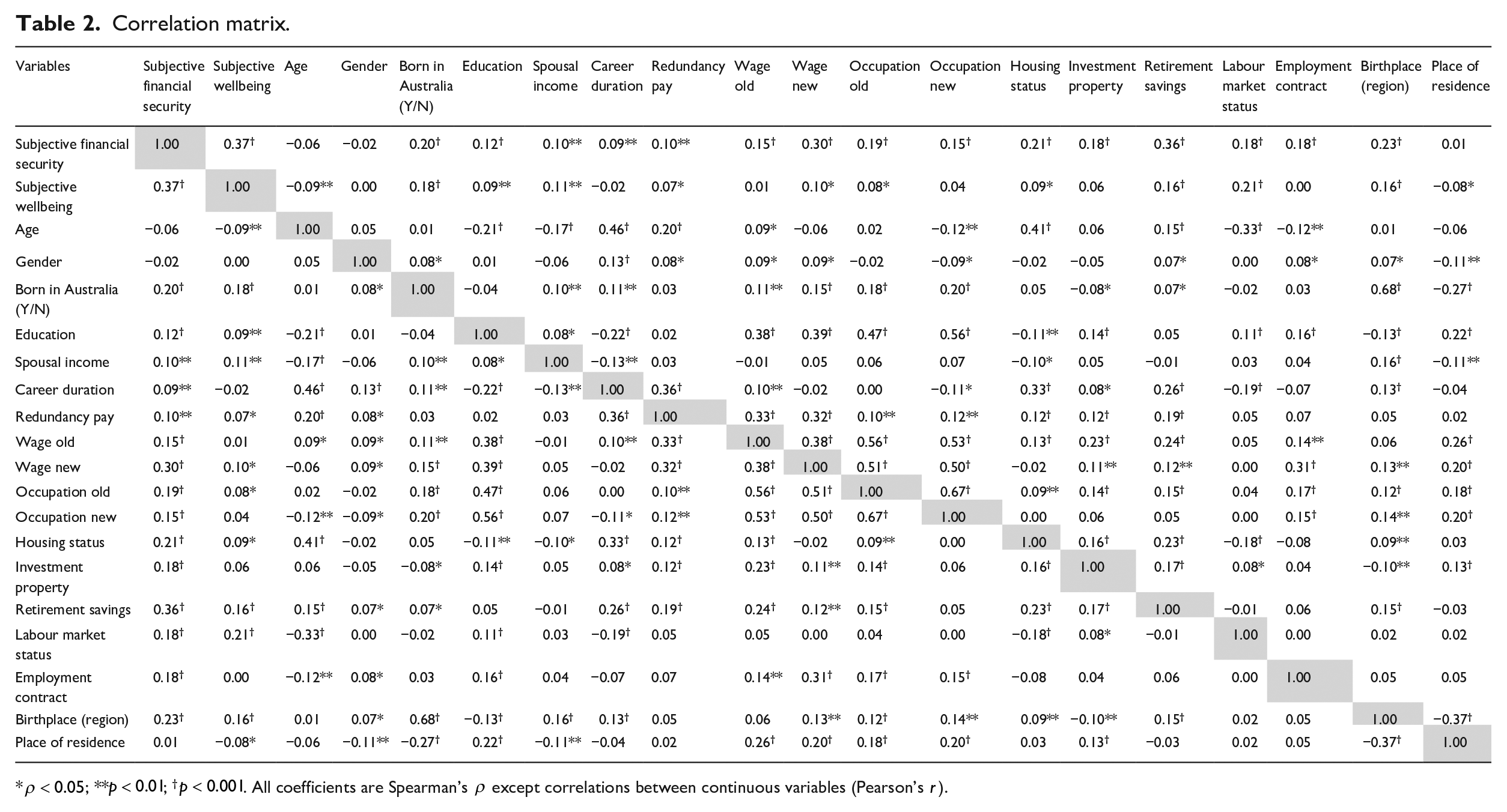

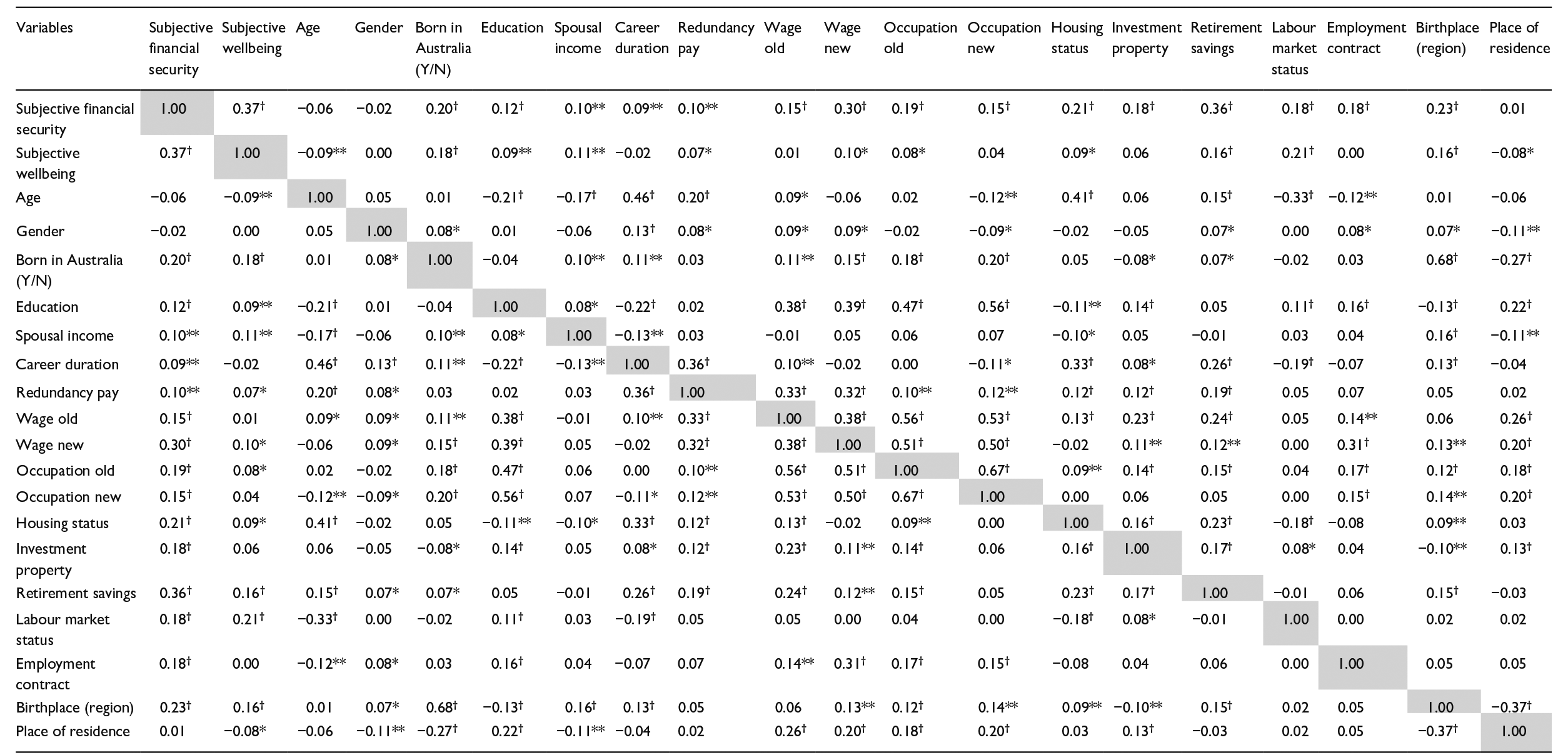

A correlation matrix was generated for use in all models (Table 2).

Correlation matrix.

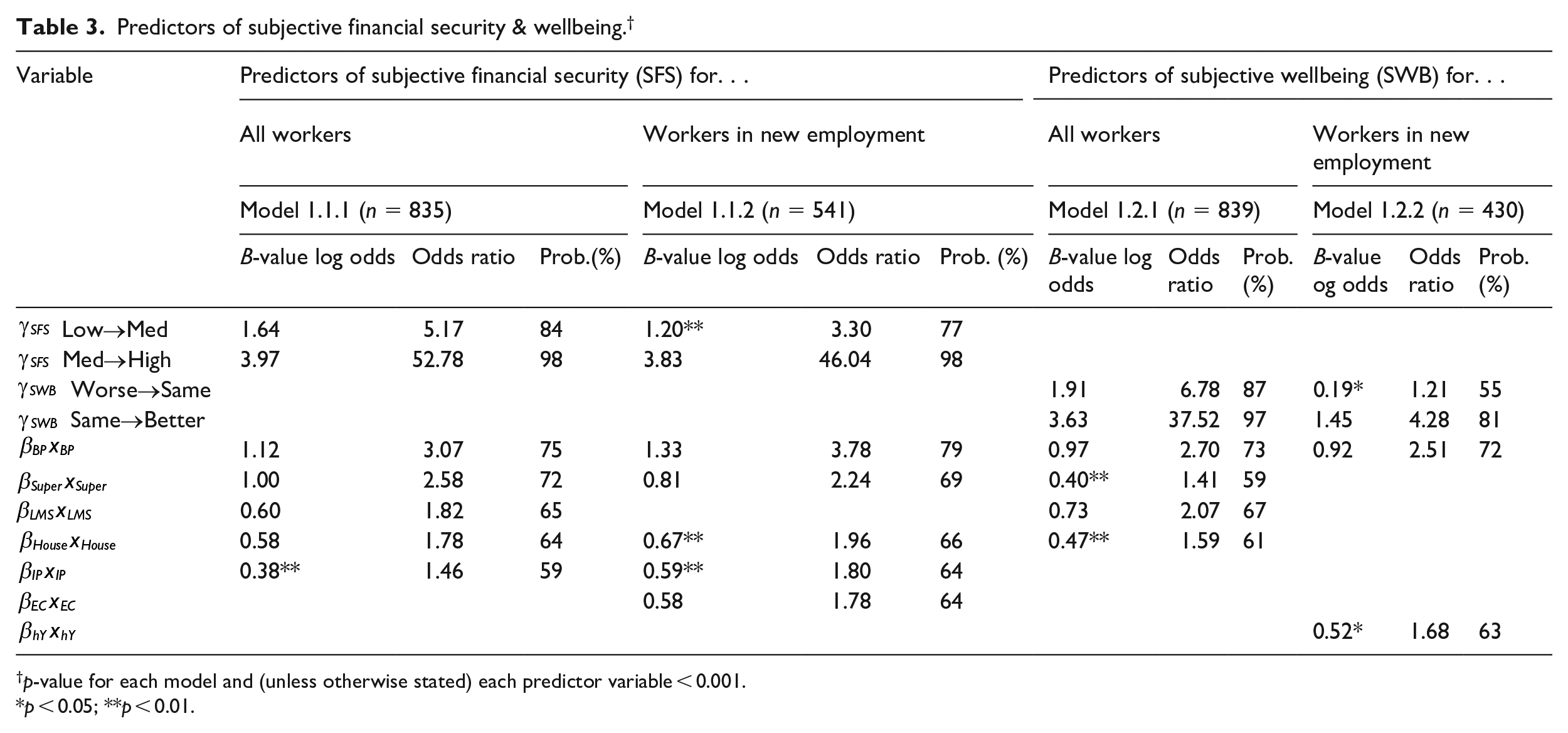

A standard iterative procedure was followed to select model predictors from Table 2. First, predictors without a significant relationship with the dependent variable (SFS or SWB) were eliminated, followed by predictors with multicollinearity (r ⩾ 0.7), predictors without a significant result in initial tests of model effects (p > 0.05) and, finally, predictors that lacked a meaningful relationship with dependent variables in probabilistic terms (probability of change in SFW or SWB > 0.5). For each of the four models, results are reported in Table 3.

Predictors of subjective financial security & wellbeing. †

p-value for each model and (unless otherwise stated) each predictor variable < 0.001.

p < 0.05; **p < 0.01.

Based on this procedure, Model 1.1.1 is expressed as:

Where

As reported in Table 3, Model 1.1.1 is highly significant statistically and provides a powerful explanation for covariables leading to rising SFS. An increase in any single predictor means that a worker with ‘low’ SFS was over five times more likely to increase their SFS (OR = 5.17). The model is especially strong in explaining those who became the most secure financially. An increase in any single predictor means that a worker with ‘medium’ SFS was nearly 53 times more likely to increase to ‘high’ SFS (OR = 52.78), or over 98% more probable. The model, therefore, shows that a worker with medium SFS would almost certainly achieve higher SFS if exhibiting any one of the following features: if they were born in Australia or from an English-speaking background or they reported increased confidence about super; improved labour market status; improved housing market status, or acquired at least one investment property.

But, in terms of the article’s theoretical concerns, the most important issue is the comparative magnitude of predictor effects. The largest effect on rising SFS was workers’ country of birth and linguistic background. A worker born in Australia or who primarily spoke English at home was over three times more likely to achieve rising SFS (OR = 3.07). Asset-based predictors also had strong effects, although labour market status, as well as confidence about super, had greater effects than housing status or investment property ownership.

The next model focused on interactional effects for the sub-cohort in paid employment. Model 1.1.2 is expressed identically to Model 1.1.1 with one exception:

As reported in Table 3, results also suggest a combination of asset-based and work-based predictors influenced SFS for this sub-cohort. Like the previous model, confidence about super has a stronger effect than housing status. Additionally, while job quality is the weakest in odds ratio terms, it is comparable to asset-based predictors in probabilistic terms. On this measure, there is no difference between employment conditions and investment property acquisition – both yield probabilities of 64% – and little difference with housing status, which is slightly higher (66%).

Next, predictors were tested against

Model 1.2.1 predictors are identical to Model 1.1.1 except

Model 1.2.2, which included job quality, also yielded a highly significant result, although model effects were weaker.

Results from four models in Step 1 demonstrate that a combination of social, asset-based and labour-based variables influenced SFS and SWB among workers. Modelling shows that the most consistent predictor was workers’ country of birth and linguistic background, supporting well-established findings that ‘local’ workers do better in local labour markets (Sugrue, 2005; Irving et al., 2022; Weller and Webber, 2004 ).

In terms of this article’s main theoretical concerns, three findings stand out. First, results show that asset ownership tended to be highly influential across the board. Asset ownership in housing and retirement savings had a significant impact in all but one of the models, while investment property acquisition was impactful in two. Asset ownership in super (retirement savings) and housing generally had a major impact on workers’ SFS and SWB. Second, ownership of non-housing assets was often more important than housing-based assets. For example, the biggest material impact on workers’ financial security was a sense of confidence about the value of retirement savings (Model 1.1.1). Finally, labour-based variables were at least as important as asset-based variables, and sometimes more so. For example, labour market status had a slightly larger impact on SFS than housing status (Model 1.1.1) and more so for SWB (Model 1.2.1). For the sub-cohort in paid employment, job quality was slightly less impactful than housing status but equally so with investment property acquisition (Model 1.1.2). These results point to the interactional effects of labour and assets in shaping workers’ material conditions and life chances. However, given the evident importance of assets in this interaction, the article now turns to the variables that influenced which workers acquired assets and why.

Step 2. Results from regression modelling of asset wealth

Step 2 is comprised of a further four regression models that calculate impacts on each of the following dependent variables:

• housing status (

• investment property ownership (

• confidence about super (

• value of housing equity (

As demonstrated in Step 1, the first three variables were important predictors of SFS and SWB, alongside social and labour-based variables. Following the same iterative steps to select predictors, model results are reported in Table 4.

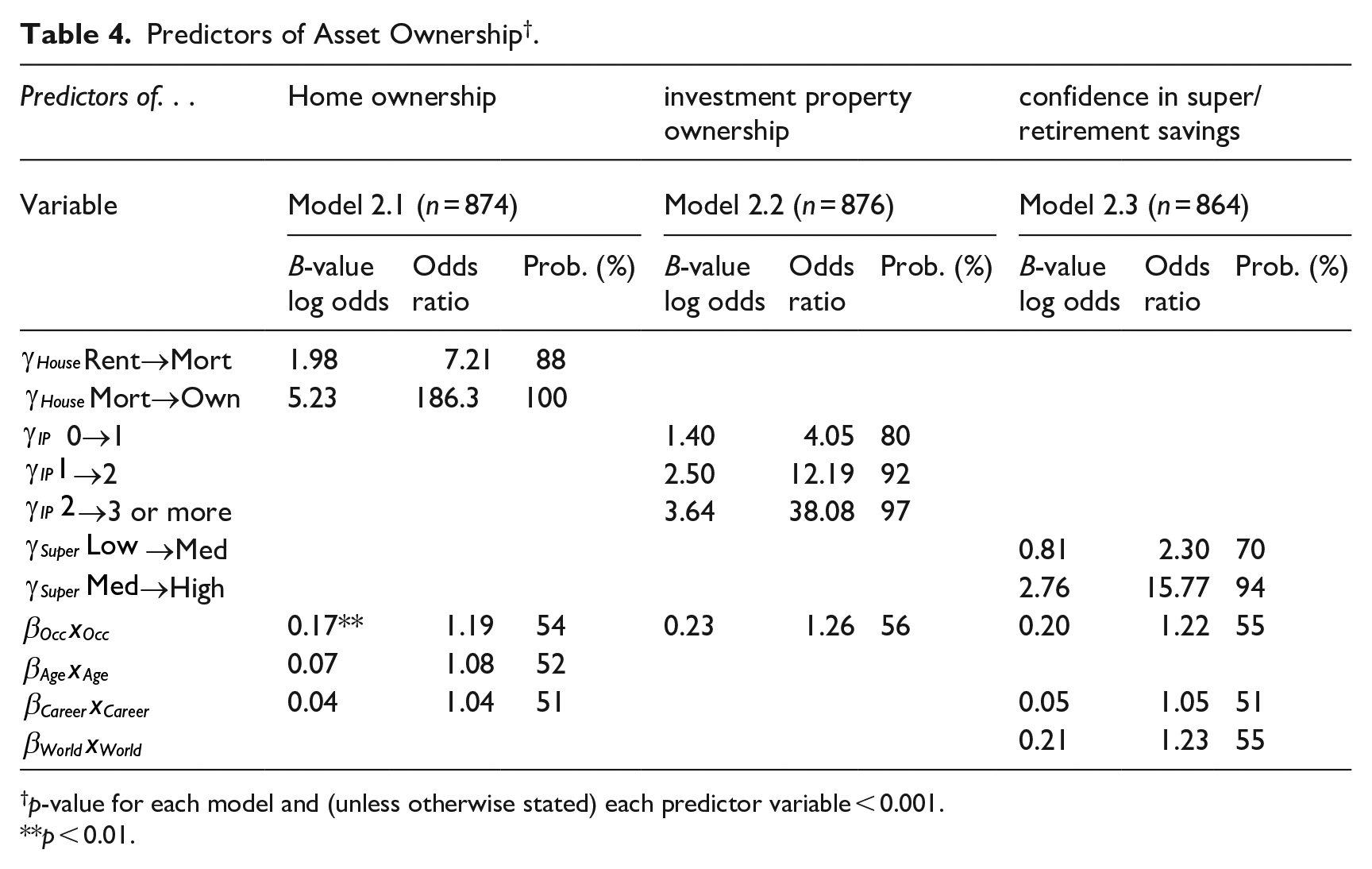

Predictors of Asset Ownership † .

p-value for each model and (unless otherwise stated) each predictor variable < 0.001.

p < 0.01.

Model 2.1 is expressed as:

Where

As reported in Table 4, Model 2.1 is highly significant and provides a strong explanation for causes of rising home ownership. While age and career duration had a predictably positive effect, the most impactful variable was occupation. Workers from higher status occupational groups such as managers and professionals were more likely to experience home ownership than service/clerical workers and manual workers. Model 2.1 is an especially strong predictor of mortgage debt elimination: an increase on any single predictor meant that outright home ownership was virtually certain, with a probability score rounding up to 100%.

For Model 2.2, occupation was the sole predictor of rising investment property ownership. A worker from a higher status occupation was over four times more likely (OR = 4.05) to own an investment property. For multiple property owners, a worker with a higher status occupation was over 12 times more likely to acquire a second property (12.19) and over 38 times more likely to own three or more properties (38.08). For Model 3.3, occupation again played a central role in predicting confidence about super, generating a similar impact as workers’ country background.

Model 2.4 used stepwise multiple regression to predict the estimated value of workers’ home equity. 5 The model is expressed as:

Where

The combination of these variables provides a model with high significance such that

For each

To summarise results from Step 2, the most notable finding is that workers’ occupational status was the most common causal mechanism explaining workers’ positioning vis-à-vis assets. Occupation had the largest impact on workers’ housing status and on investment property acquisition; it was the equal largest predictor of super and, after place of residence, had the largest impact on housing equity. In the context of median housing equity of $550,000 and a median house value of $650,000 (n = 657), a difference of more than $100,000 in housing equity per occupational increment is especially notable.

These results show that occupational status was the key driver of asset wealth for these workers. Workers with strong assets tended to have experienced careers in higher-status occupations. This suggests that, while asset-based variables were influential in shaping workers’ SFS and SWB alongside labour-based variables (cf. Step 1), labour (especially in terms of occupations) was the key driver of asset wealth via working life histories. But this finding relates to workers in this study’s cohort – a shrinking group of older, predominantly male manual workers. The socially significant question is how this group, as a notable, if still unequal beneficiary of historical labour market security, occupational citizenship, home ownership and asset wealth, compares to trends in the wider working-age population.

Step 3. Comparing study findings with population trends

Step 3 compares the study cohort with the working-age population. In terms of key differences, gender is the most obvious starting point given the male-dominated character of study cohort: 83.7% of the sample were men compared to 49.3% of the working population (ABS, 2022a). Female disadvantage in asset ownership, asset wealth and retirement savings is well understood (Masterman-Smith and Pocock, 2008), meaning that gender is likely to be a predictor of SFS/SWB in industries with higher female employment. A second notable difference concerns age: the proportion of the study cohort aged 40–64 (79.8%) was nearly twice as high as general population (42.9%). 6 Since study findings confirm that age is a driver of home ownership and asset wealth, and that assets play a causal role in SFS and SWB, it follows that studies of more youthful sectors will be likely to reproduce the relative financial disadvantages experienced by younger workers in this study.

In terms of labour-based factors, the study cohort exhibited worse labour market outcomes than the working population. Although 71.5% of the cohort were in paid work—slightly higher than the equivalent population figure of 70.1% – a much lower percentage had withdrawn from the labour market (16.0% against 26.1%) and a much higher percentage were unemployed (12.5% against 3.8%) (ABS, 2022a). This represents an effective unemployment rate of 14.9%, or more than three times higher than the national unemployment rate at the time (4.7%). This relatively poor outcome is likely to be influenced by age discrimination and social disadvantage, including the high proportion of overseas-born workers from culturally and linguistically diverse backgrounds: 45.3% were born overseas, against 29.1% for the working-age population (ABS, 2022a). As the findings reported above indicate, place of birth and linguistic background had the strongest effect on both SFS and SWB.

Further labour market disadvantages arise for older workers who have been employed by a single firm for a long period of time and sheltered, therefore, from external labour markets. On average, auto workers had been with their previous employer for over four times longer than job tenure in the working-age population. Nearly three quarters (74.3%) of auto workers had been with their previous employer for 10 years or longer, compared to a population equivalent of 27.5%. 7

Job tenure was, however, a Janus-faced issue. Although contributing to disadvantage in labour markets – an established finding in the deindustrialisation literature (Beer, 2008; Beer et al., 2006; High, 2018; Strangleman, 2001; Weller, 2009) – job tenure contributed to greater asset wealth as a driver of home ownership and retirement savings (cf. Models 2.1 and 2.3). It follows that, although shorter job tenure may familiarise younger workers with the experience of external labour markets, it is highly disadvantageous in terms of asset-based financial security.

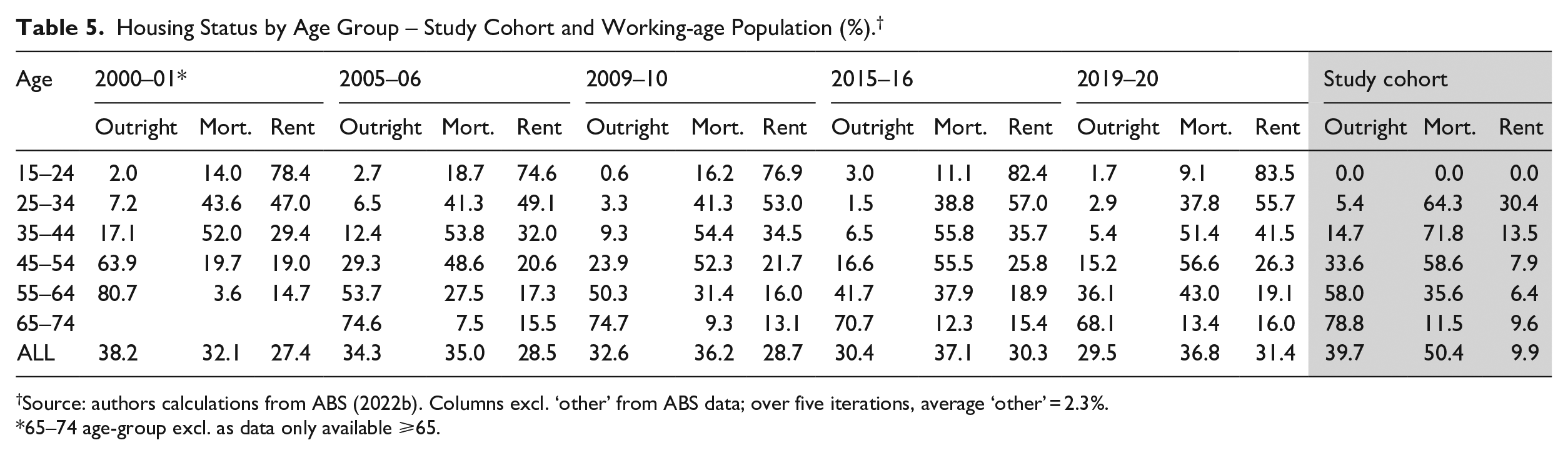

In housing terms, the study cohort was dominated by mortgagors and outright homeowners. Over half were mortgagors (50.4%) and nearly two in five (39.7%) were outright homeowners, leaving fewer than one in ten as renters (9.9%). In contrast, outright home ownership in Australia declined from 38.2% in 2000–01 to 29.5% in 2019–20. The decline in outright home ownership was met by an increase in mortgagors and renters to 36.8 and 31.4% respectively (Table 5).

Housing Status by Age Group – Study Cohort and Working-age Population (%). †

Source: authors calculations from ABS (2022b). Columns excl. ‘other’ from ABS data; over five iterations, average ‘other’ = 2.3%.

65–74 age-group excl. as data only available ⩾65.

This problem is illustrated further by comparing housing status by age group. For workers aged 35–44, there was a large rise in the proportion of renters from 29.4% to 41.5% from 2000–1 to 2019–20. The proportion of outright homeowners in this group dropped by over two-thirds, from 17.1% to 5.4%. For the 45–54 age group, there was a dramatic decline in outright homeownership from 63.9% to 15.2% and a large rise in mortgagors (19.7%–56.6%). For those closest to the retirement age (55–64), there was also a major fall in outright homeownership (Table 5). When combined with findings from Step 1, which models that housing status is a predictor of SFS and SWB (cf. Models 1.1.1-1.2.1 in Table 3), this suggests that financial security will continue to deteriorate as workers age – a period in which security is conventionally assumed to improve with the gradual elimination of housing costs.

Undoubtedly, house price inflation is the main cause for extended mortgage debt later in life as well as extending the age of first-home purchase. This view is consistent with study findings (cf. Model 2.4) that show place of residence has the biggest impact on workers’ net wealth in home equity. But this problem is not driven by house prices alone; model results demonstrate that improved housing status was also driven by age, career duration and occupation (cf. Table 4). The benefits of atypically long job tenure among workers in the study cohort were reflected in superior housing status relative to the working-age population. As Table 5 shows, younger auto workers were much more likely to be mortgagors than other workers in the same age group (71.8% against 51.4% for the 35–44 age group) and far less likely to be renters (13.5% against 41.5%); for older workers, 33.6% of those in the 45–54 age group were outright homeowners against 15.2% for the population; for 55–64 year olds, the equivalent figures were 58.0% and 36.1%. Logically, it follows that the disappearance of such long careers and resulting lower job tenure, as well as housing price inflation, is likely to impact upon declining financial security and wellbeing later in life.

Discussion and conclusions

This article’s findings point towards three main conclusions. First, they show that asset wealth played a central role in differentiating worker outcomes after job loss. As demonstrated in this article, the idea of workers acquiring and accumulating asset wealth is almost entirely absent from the vast literatures on deindustrialisation and job loss. In addressing this lacuna, this article’s empirical results demonstrate how asset ownership in housing, investment properties and retirement savings can play an important role in the differentiation of life chances after job loss. It shows that workers’ housing status relative to mortgage indebtedness, investment property ownership and confidence about retirement savings each influenced workers’ subjective financial security and wellbeing. Conversely, lack of asset ownership put workers in a comparatively disadvantageous position.

Second, while such asset-based causative factors are important, findings show that labour-related factors or social factors such as ethno-cultural background are at least as important, and sometimes more so, in shaping workers’ security and wellbeing after job loss. For the study cohort, the impact of improved labour market status led to 82% better odds (OR = 1.82; see Table 3) that a worker would have higher SFS—a stronger impact than housing status or investment property ownership. For workers in new jobs, a more secure employment contract had an equally strong impact on SFS as investment property ownership.

Moreover, the most consistent impact on workers’ positioning in the asset economy was occupational status via their career histories. Occupation, age and job tenure drove changes in workers’ housing status. In the study, an increase in any one of these measures meant that workers were virtually certain of improving their housing status and eliminating mortgage debt. Occupation was the sole driver of investment property acquisition, the largest driver of confidence in retirement savings and, after workers’ place of residence, the largest driver of home equity wealth. Contra recent assertions that assets now trump labour in the shaping of class-related outcomes (Adkins et al., 2021), this suggests that the relationship between assets and labour is a combinatory process; not a matter of preferencing assets or labour in the determination of life chances but an insistence that assets and labour work in dynamic interaction over the life course; that what matters are the cumulative reciprocities, or the circular and cumulative causalities, of assets and labour. The effects of historical job security and occupational pathways enable workers to benefit from asset ownership through housing and retirement funds during relatively long careers, while asset-based gains work in tandem with labour-based variables such as new jobs with permanent contracts to maximise workers’ life chances after job loss.

Finally, comparison between the study cohort and the wider working-age population suggests that the benefits of asset ownership among wage-earning workers will decline over time or become the domain of a privileged elite of high-status occupations. The extent to which material benefits were accumulated by auto workers in Australia was driven by job tenure and stable career paths generated within highly developed internal labour markets. This provides a compelling explanation for why nearly half of these workers (45.5%) could still claim ‘high’ SFS after losing their jobs while nearly three-quarters (71.1%) reported their SWB was either the same or better despite recording poor labour market outcomes compared to the working-age population. It follows that the disappearance of this cohort from the employment landscape, alongside a wider decline in job tenure and internal labour market opportunities for manual labourers, means that other workers will have much weaker social protection when confronted with job loss in the future.

Footnotes

Acknowledgements

For indispensable help with graphic design, the author would like to thank Ms Sophie Cotton. For their comments and advice on earlier drafts, he also thanks Prof Jack Barbalet, Dr Gareth Bryant, participants in a session at The Australian Sociological Association (TASA) conference in Melbourne, and at a workshop at Australian Catholic University Rome Campus, both in November 2022.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The article was researched and written in collaboration with the Australian Research Council (ARC) ‘Future Work, Future Communities’ Linkage Project Team LP170100940.