Abstract

This paper examines profit-seeking investments that US financial industry actors have made in the name of racial justice since the summer of 2020. This trend, which builds on the proposition of “sustainable” finance that private profits and social benefits can coexist, is known in the industry as racial justice investing. To understand how the industry frames racial justice as an object of financial intervention, I draw from theories of social reproduction, racial capitalism, and social finance to analyze the historical and contemporary processes through which racial injustice is conceived in economic terms as a “gap” between the wealth of white and racialized households. Then, I analyze the political economy of these investments, focusing on how solutions to the wealth gap are oriented around extending credit and economic inclusion to racialized households and business owners. Ultimately I illustrate how the financial industry’s investments in closing the racial wealth gap largely sidestep questions of power and, paradoxically, justice that animate many contemporary racial justice movements.

Introduction

On June 5, 2020, days after the murder of George Floyd by the Minneapolis, Minnesota police, Jamie Dimon, the CEO of JPMorgan Chase, made an impromptu visit to the local Chase bank branch near his home in Mt. Kisco, New York. Earlier that week, Dimon had publicly supported the protests erupting across the US in reaction to Floyd’s death. During his visit to Mt. Kisco, Dimon and the bank staff posed kneeling on one knee for a photograph in front of the branch’s open vault (McEnery, 2020), a symbolic gesture used to protest racism in the United States (see Figure 1). A reporter tweeted out the image with the hashtag #TakeAKnee, 1 and the image went viral.2,3 Several months later, Dimon announced a $30 billion Chase “commitment” to invest in promoting racial justice in the United States, 4 noting that “we can do more and do better to break down systems that have propagated racism and widespread economic inequality” (JP Morgan Chase, 2020). This pledge was among $50 billion in pledges by some of the biggest US corporations to combat racial inequality in the months following Floyd’s murder (Jan et al., 2021), with press releases acknowledging the ties between racial and economic injustice and promoting private financial investments as a tool to alleviate racialized disparities (e.g. Bank of America, 2020). More than 90% of the $50 billion was earmarked as future investments or loans, which would profit the companies making the pledges (Jan et al., 2021).

Jamie Dimon and Chase employees take a knee on June 5, 2020.

The aim of this paper is to conceptualize the political economy of such investment pledges, which are emblematic of a growing consensus between government, civil society, and the private sector that corporate actors can increase racial equity in society through targeted investment activities—often the extension of credit to racialized households and business owners. In this process, personal and business debt becomes tied to the promise of increasing racialized peoples’ social equity in the future. In the context of public debates in the US about the impacts of racism, particularly anti-Black racism following the summer of 2020, I critically assess claims that racism can be conceptualized as an economic measure and resolved through private investments. While there is a lengthy history to this type of investing, it is my contention that scrutiny of its post-2020 guise is necessary for several reasons: these investments’ growing popularity as an alternative to public policies to address racism and economic injustice, the ways the financial industry discursively and materially narrows racial justice to an economic indicator, and the fact that private capital is touted by powerful economic and political actors as the only way to solve many other global crises, from pandemics to climate change to biodiversity loss (Hughes-McLure and Mawdsley, 2022; Kim, 2015; United Nations Development Programme [UNDP], 2018). As corporate financial actors move to make racial justice actions fit with their profitable missions, I explore how these financial instruments work, the logics and spatialities through which they operate, and how this trend fits into processes of 21st century racial capitalism.

The companies making the investment pledges I consider in this paper couple their financial actions with acknowledgements of the racial disparities that characterize the US economy. These disparities are often described in terms of a symbolic economic indicator of inequality: the racial wealth gap. The racial wealth gap is calculated from statistics on how US household wealth varies by racial identity group. In 2020, the average white household held nearly ten times the wealth of the average Black or Latino/a household, a disparity that widened substantially after the 2008 financial crisis (McIntosh et al., 2020). Measured this way, the gap conceptualizes justice as something that will be achieved when racialized people’s average wealth reaches the average wealth of white people (e.g. Sullivan et al., 2016). Following trends of increased corporate interest in addressing the gap through return-seeking investments—namely through extending credit to racialized borrowers (Jan et al., 2021)—the theoretical framework of this paper draws from theories of racial capitalism and social reproduction to critically analyze the expansion of debt relations that underlies corporate investments claiming to promote racial justice.

I use theories of racial capitalism to understand how the racial wealth gap, and proposals to solve it, are imbricated with historical processes of racialized dispossession in the global financial system. Anti-colonial scholarship on the dispossessive logics of “inclusion” in imperial economies (Byrd et al., 2018) and the financial industry’s extension of control over the sustenance of precarious households and communities (e.g. Mullings, 2022) highlights how these processes tend to reproduce, rather than abolish, the racial logics of the 21st century financial system. In studying the relationship between race and capitalism from this perspective, Pulido (2017: 527) cautions against examining racial outcomes without considering racial production, arguing that “racial production. . .informs how a problem is conceptualized, and thus shapes political strategy.” Applying this lens to racial justice investing, I analyze the historical relationships between racialization and capital accumulation that produced the racial wealth gap in the first place before examining contemporary logics that place debt at the center of eliminating it. I use social reproduction theory to understand the particularly generational and identity-based characteristics of racialized wealth disparities in the US, as well as to highlight the role of wealth in contemporary society. Here, I conceptualize the racial wealth gap as a cumulative historical measure of how racialized people’s lives and communities—particularly Black people and Black communities—have been sustained at levels below the standards demanded by (and deemed appropriate for) white communities.

To understand the rise of racial justice investing industry, I analyzed press releases from the financial industry, media analyses of post-2020 corporate racial justice commitments, and secondary data on the types of investments being made and by whom. Throughout the paper, I use JP Morgan Chase and Citi, two of the biggest investors and most vocal promulgators of racial justice investments after 2020, as examples to analyze the discourse and financial arrangements undergirding these type of investments. Aside from after outlining the structure of racial justice investments by the US financial industry, the argument of this paper is conceptual: analyzing this emerging industry in its political economic context and answering the question of how the racial wealth gap has been constituted as an investible object, where “increasing racial justice” is done through the existing debt-credit relationships of the financial industry.

The rest of this paper is organized into five sections. First, I introduce this emerging industry—who made racial justice investing pledges after 2020 and what did these pledges look like? Second, I theorize this niche form of impact investing at the intersections of racial capitalism and social reproduction theory to consider the kinds of debt relations and institutional geographies that characterize this claimed intervention in structural inequality. Third, I provide a brief genealogy of how the racial wealth gap has been framed as a problem that becomes an object of intervention. This is followed by an analysis of the investment structures that use the racial wealth gap as a proxy for racial inequality, with credit proposed as a solution. Finally, I consider the ethico-politics of the financial industry treating the racial wealth gap as an investable object seeking “returns on inclusion,” and the implications of looking to the financial industry for solutions to racism and racial inequality.

Racial justice investing in response to the Black Lives Matter protests of 2020

Racial justice investing is a type of impact investing, a style of private investing with the professed goal of creating social or environmental impacts that benefit publics beyond the investors or shareholders (Rosenman, 2019). Impact investing, also known as social finance or sustainable investing, has grown exponentially since the 2008 global financial crisis, with ¼ of all US professionally managed assets under some sort of social or environmental “screen” by the end of 2018 (Global Sustainable Investment Alliance, 2018). Investments branded as fighting the socioeconomic impacts of racism are one of the latest trends in this industry, finding an especially eager audience in the US in the summer of 2020 amidst Black Lives Matter protests. Corporate America, in particular, responded to 2020’s public debates on racism with financial pledges unmatched by any previous social justice cause in US history (Jan et al., 2021): corporate actors pledged donations, investments, and operational shifts (such as diversifying their boards) in the name of combatting racism in US society. Reflecting a growing consensus around the problem of racism in US society and the ubiquity of financial investments with social goals, hundreds of corporations spent the summer and autumn of 2020 making public announcements of their commitments of resources to fighting racism.

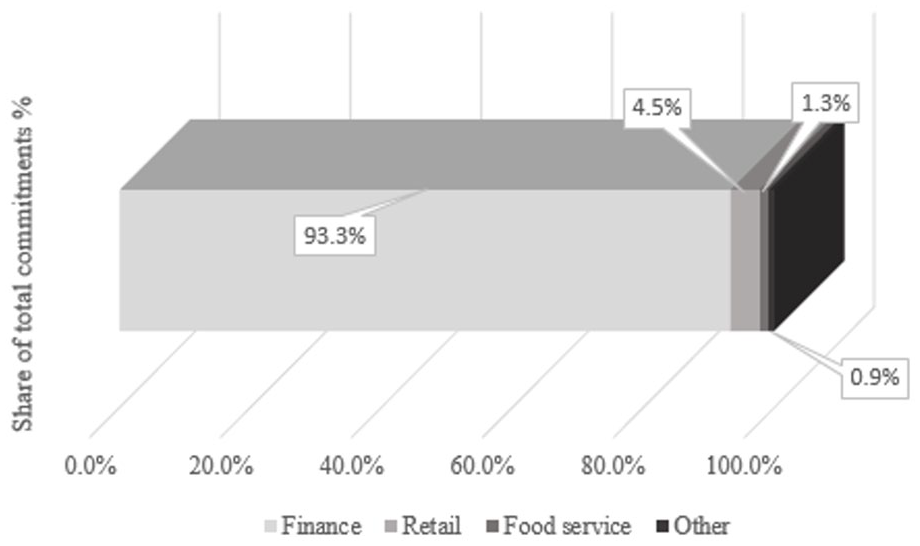

According to analysis by the McKinsey Institute for Black Economic Mobility (Fitzhugh et al., 2021), Fortune 1000 companies 5 promised $200 billion to fight racism in the US from May 2020 to 2021, with 90% of these commitments coming from the financial industry. As corporate commitments continued even a year after the Black Lives Matter protests, financial institutions continued to be the source of 90% of pledges, dwarfing other sectors (see Figure 2). McKinsey’s research also noted that, of all commercial sectors making financial commitments in the name of racial justice, the financial industry is by far the whitest in terms of its labor force (Armstrong et al., 2023). While non-financial corporations tended to make donations to antiracist organizations or groups providing social services to racialized neighborhoods—and many made commitments to diversifying their own labor forces—the financial industry focused on deploying return-seeking capital to racialized households, businesses, and communities. Major banks and asset/investment managers making pledges included Bank of America, Wells Fargo, Citi, Goldman Sachs, Morgan Stanley, JP Morgan Chase, State Street, and Blackrock (SOC Investment Group, 2021).

Share of Fortune 1000 commitments earmarked for racial justice, May 2021–October 22.

In line with non-financial corporations, financial industry actors frequently invoked the racial wealth gap in their 2020 pledges. In announcing a $1 billion investment toward racial justice in 2020, for example, Citi CEO Michael Corbat stated that: “Addressing racism and closing the racial wealth gap is the most critical challenge we face in creating a fair and inclusive society and we know that more of the same won’t do. We are bringing together all the capabilities of our institution. . .like never before to combat the impact of racism in our economy. This is a moment to stand up and be counted, and Citi is committed to leading the way and investing in communities of color to build wealth and strong financial futures” (Citi, 2020).

Corbat’s statement invoked finance and investments as the key ingredients to produce equitable futures for racialized communities and Citi’s commitments reflected this view. These included mortgages for people of color and loans to Black entrepreneurs ($600 million); interest-seeking capital deposited into federally-designated minority banks ($100 million); moving procurement to Black-owned businesses ($350 million); and making grants to “community change agents” that address racial inequality ($100 million; Citi, 2020). With only these latter funds—10% of Citi’s total pledge—earmarked for control by communities affected by racism, credit and financial inclusion were the primary mechanisms through which Citi planned to fight racism with its investments, a trend mirrored by other financial industry actors (Fitzhugh et al., 2021; Jan et al., 2021). Similar commitments were made by JP Morgan Chase, Wells Fargo, Bank of America, Goldman Sachs, and others (Bank of American, 2020; Rabouin and Witherspoon, 2020). Like those of Citi, these initiatives focus on expanding credit for Black- and minority-owned businesses and Black-focused community development financial institutions, expanding mortgage credit for racialized borrowers, and providing impact investing capital for Black entrepreneurs.

Conceptualizing for-profit racial justice

Beneath invocations of the racial wealth gap as a social problem is the function that wealth holds in a capitalist economy: wealth (often in the form of assets) is crucial for sustainable livelihoods and for the generational reproduction of households and communities. Here, the backdrop of corporate actors’ ability to “invest” in closing the US racial wealth gap are specific arrangements of social reproduction—whose responsibility social reproduction is made to be, and how it is paid for. Meanwhile, the specific debt-credit relations of racial justice investing—involving racialized debtors and, overwhelmingly, white-led institutions as creditors—speak to how this form of investing operates within 21st century racial capitalism, reproducing race-based financial relationships even while claiming to solve the problems these relationships create. Thus, this section draws from theories of social reproduction, racial capitalism, and social finance to outline a theoretical framework for understanding corporate racial justice investments.

In this paper I take a broad view of social reproduction that is attentive to how it exceeds the scale of the household and is increasingly a market relation (Strauss and Meehan, 2015; Winders and Smith, 2019). In the contemporary US economy, household wealth and/or access to financing is a primary driver of social mobility, ability to obtain healthcare and education, and ability to provide for one’s family and wider community (Adkins et al., 2020; Karaagac, 2020), despite the fact that bringing these activities into financial markets negatively impacts the people whose socially reproductive activities produce private profits (Ebner and Johnson, 2020; Henry and Loomis, 2023; Karaagac, 2023). Specifically relevant to racial justice investing, including racialized participants in the dominant financial system has a poor track record for increasing racial equity (Ponder, 2021; Taylor, 2019; Wyly and Ponder, 2011; Aalbers, 2016) and often sidesteps the demands of people most affected by racism. The present paper thus seeks to understand the tools that the financial industry proposes to support the social reproduction of racialized communities and the mechanisms by which these tools are made acceptable to (read: profitable for) the financial industry, with the aim of analyzing who or what entities are taking on the bulk of risk in the extension of racial justice-branded debt relations.

Recent scholarship has identified transitions in the logics, mechanisms, and temporalities of social reproduction in the 21st century economy, with authors such as Adkins et al. (2020) arguing that access to assets, not employment, is the primary way that households and communities now reproduce themselves in the Global North. Life course events such as education and procuring a home have been conceptually and financially reoriented into investment opportunities “whose logic is dominated not by one of the extraction of surplus value from labor power but by a logic of the extraction and creation of surplus from money” (Adkins, 2019: 20). Without access to generational wealth, credit (i.e. taking on debt) is the means through which life is maintained in the asset economy. With waged labor no longer being sufficient to fund households’ daily existence, let alone to pay for education and housing that might lead to social mobility and asset accumulation, debt has become crucial to the survival of working- and middle-class households (Montgomerie and Tepe-Belfrage, 2017). In effect, for a great many households, particularly but not exclusively in financialized, (post)industrial societies (cf. Torkelson, 2021), social reproduction is no longer about supporting labor power but about providing payments to finance capital. As growth in the value of assets like property has outpaced the growth of wages in the past four decades, social stratification according to one’s access to assets is a new vector of inequality—one that is deeply racialized. This, in turn, has racialized effects on social reproduction, as indebtedness may stifle and/or delay what were previously seen as normal milestones of middle-class life, such as marriage and homebuying.

Yet while the asset economy has been discussed by scholars of social reproduction as a novel form of class inequality, attention to the racialized implications of finance-driven social reproduction is more recent. Foundational work in this area explored how remittance payments and transnational care labor subsidize social reproduction in the Global North at the expense of racialized workers from the Global South (Ebner and Johnson, 2020; Mullings, 2009; Pratt, 2012). Yet assets—who can accumulate them, who can pass them down to their children, and who is locked out of this possibility—are also extremely racialized within the United States (Dantzler, 2021; Woods, 2009). As Gilmore (1999: 180) explains, the social reproduction of white workers has been subsidized directly by the state, and the “surplussing” of racialized populations has gone “hand in hand with the accumulation of other [white wealth] surpluses.” In short, racialized hierarchies of social reproduction in the US have allowed white people to engage in overaccumulation, via lower standards, both de facto and de jure, for the life outcomes of racialized people—accompanied by high levels of indebtedness in racialized communities (Mustaffa and Dawson, 2021). The racial nature of this debt deserves more scrutiny as scholars attempt to understand social reproduction as a variegated process (Bakker and Gill, 2019) in contemporary capitalism.

Consumer, healthcare, and student debt drag disproportionately on the economic futures of racialized households in the US, while “good” forms of debt (such as mortgages) benefit white households (Mishory et al., 2019; Seamster, 2019). In an economy organized around debt-financing most major lifetime purchases, this means that racialized households on a whole have fewer assets but also that these households shuttle a disproportionate amount of their income to debts. This is not simply a household level phenomenon, or even a trend that disproportionately burdens racialized households in aggregate, but an economic and financial structure that disproportionately burdens racialized populations through higher interest rates and utility bills, lower home appraisal values, and other key financial metrics connected to the material components of social reproduction (Ashton, 2012; Ponder, 2021; Taylor, 2019) through a financial system structured around racialized practices of pricing and offloading risk (Fields and Raymond, 2021; Harris, 1993; Robinson, 2000). It is here that how the financial system operates under contemporary racial capitalism becomes integral for understanding racial justice investing.

This relationship has manifested in multiple ways throughout US history, from slavery, labor market exclusion, and unequal wages (Gilmore, 1999; Melamed, 2015) to predatory inclusion (Wyly et al., 2007). These are the historical and ongoing foundations of lower standards of social reproduction for racialized populations (Dawson, 2016). While, as noted above, the US state has historically subsidized the social reproduction of white households, racialized populations have largely had to rely on private markets to satisfy their social reproductive needs, illustrated for example in the contrast between massive federal support of white middle-class homeownership and welfare in the 20th century and the exclusion of racialized households (Brown, 1999; Gilmore, 1999; Katznelson, 2006; Taylor, 2019). Meanwhile, in the uneven burden of cuts and other austerity measures taken in response to economic crises, states have reinscribed racialized inequalities.

Yet as Dawson and Francis (2016) have noted, this process evolves as the primary mode of accumulation shifts. Their observation of the dynamism of racial capitalism is particularly instructive for examining racial justice investing: the latter can be understood as a shift from accumulation based on exploiting racial difference (i.e. labor that does not pay enough to sustain racialized life and/or finance that preys on racial marginalization) to one based on inclusion (i.e. finance as a practice of investing in the systems and forms of debt that now sustain racialized life). In an economy in which social reproduction is being further financialized and atomized to a household-level responsibility, the persistent racialization of social reproduction has deepened but also been opened up for financial profits through predatory financial inclusion. In many cases racialized predation via the means of social reproduction, such as housing and transportation, has been a constituent component of capital’s profit strategies (e.g. Fields and Raymond, 2021; Pollard et al., 2020; Wyly et al., 2009).

To understand the specific branding of racial justice investing as anti-racist, despite the extremely racist history of financial exploitation in the financial industry, I look to literature on impact investing and social finance. This literature illustrates how these investments often respond to crises of social reproduction (Harvie and Ogman, 2019; Rosenman, 2019), supplementing or replacing defunded state social programs while transferring risk to the private sector (Dowling, 2017). Here, the “burden” of providing for racialized groups is transferred from the state to private and NGO sectors; this process of marketization converts the racial wealth gap into a business opportunity for private capital by framing the gap as a simple lack of financing. Investment structures and strategies often focus on recasting populations previously viewed as economically value-less or value-sapping (e.g. incarcerated or impoverished people relying on state aid) as people from whom financial value can be derived once their behavior is adjusted to adhere to predominant social norms (e.g. reduced recidivism or unemployed people finding work; Lake, 2015). Kish and Leroy (2015: 631–632) highlight this characteristic of social finance investments made in racialized communities, observing a “capitalization of human potential” through “generating profits by revaluing racialized life.”

These efforts to recuperate the value-generating potential of people and places previously seen as value-less are also characterized by the neoliberal notion that market efficiency will produce better outcomes than direct state interventions. Some of these market-based claims actually replicate the calls of contemporary racial justice movements, such as rooting capital in place and providing financial “freedom” to people with insufficient income and wealth (e.g. Movement for Black Lives, 2020). Thus, as I outline in the conclusion of this paper, the relations of debt and credit that underlie racial justice investing are not simply good or bad. Rather, I inquire about distributions of financial risk, terms of investment, and the power of the financial industry to dictate what racial justice looks like. The next section provides a brief history of these relationships.

Historicizing the wealth gap as an object of policy

The US federal government began the post-civil war period (1862–1868) with polices based on the idea that formerly-enslaved people would need a means to accumulate wealth in order to participate in society—and the workforce. In 1865, at the end of the war, the government planned to set aside 400,000 acres in the US south for this purpose, with land redistribution proposed as a catalyst for economic self-sufficiency. But amidst white backlash (Du Bois, 1998[1935]; Robinson, 2019), the administration of President Andrew Johnson rolled back these land promises, leaving formerly-enslaved people to the private land market. This was justified in part with the reasoning that “freedmen should have land, but they. . .must pay for their land” through working for wages (quoted in Baradaran, 2019). As historian Mehrsa Baradaran (2019: 18) writes, “[Johnson] claimed that the laws of capitalism and free trade would allow the freedmen to accumulate land without any special help from the state.” Even when formerly-enslaved people were able to afford to buy land, white landowners would rarely sell it. Meanwhile, the federal government subsidized white settlers’ wealth accumulation with the Homestead Act, giving out millions of acres of state-appropriated Indigenous lands to settlers if recipients farmed it for 5 years (Dawson & Francis, 2016; Gilmore, 1999). “Capitalism without capital” for Black Americans was the policy from the beginning—and “pay[ing] for their land” usually meant taking on debt (Baradaran, 2019: 40).

During the Civil Rights era in the mid-20th century, federal policy continued to reject the idea that economic reparations were necessary for racial equity. The federal government countered calls for reparations, autonomy, and anti-capitalist politics (e.g. Carmichael, 1966) with so-called “Black capitalism” programs from the federal government—programs in Black neighborhoods that supported Black-owned businesses with financing and technical assistance and were intended to have “multiplier effects” for wider communities (Ferguson, 2013). Previewing racial justice investing today, the federal government looked to the private sector and civil society to execute this vision. In the 1960s and 1970s, philanthropic initiatives from the Ford and Rockefeller Foundations, among others, made targeted investments in Black neighborhoods with the goal of expanding access to credit and revenue generation. Meanwhile, dwindling Keynesian-era public support for labor and social reproduction accompanied the narrative that the state now lacked the resources to provide for everybody, exacerbating racism and precipitating under-employment and incarceration of racialized people, particularly in Black communities (Gilmore, 1999).

Descriptions of racialized wealth inequality as a gap picked up during the Johnson Administration’s (1963–1969) “war on poverty,” during which divergences in outcomes for poor (and often) racialized communities became the object of federal interventions in the form of investment in healthcare and education. Sociological research during this time period inquired about the causes of widespread poverty; Oscar Lewis’s (1966) theory that poor communities displayed a specific “culture of poverty” that explained their economic circumstances, and Robert Moynihan’s (1956) ascription of this culture to the conditions of deprivation in racialized US communities, cemented an idea that a cultural deficit explained wealth divergences between Black and white communities—leading federal policy to focus on changing this culture (Greenbaum, 2015). Civil rights era-inspired analyses of education inequality (Lauter, 1966) and other divergences in social outcomes framed these divergences as stemming from unequal access to resources, but the idea that “dysfunctional” economic behaviors such as financial irresponsibility and sociological/cultural factors (e.g. higher numbers of single-parent households, lower marriage rates, and different values; Darity et al., 2018) dominated academic and policy attention to the existence of a gap. This framing continued in the 1970s with Nixonian era national economic analyses and theories of race relations (for a critical outline see Blauner, 1972). Much research was devoted to understanding the gap as a division between Black and white households, with less attention to other racialized groups. In sum, early understandings of the racial wealth gap focused on culture as the basis of economic achievement “deficiencies.”

From the 1970s, federal policy (e.g. the 1977 Community Reinvestment Act) focused on the wealth gap as derived from unequal access to financing for wealth-generating assets (Taylor, 2019). Subsequent state and private sector efforts to include racialized people in the benefits of economic growth and institutions have continued to center the idea that racial uplift should be achieved through the market: “inclusion” in employment and private financial markets, financial literacy, strategic public policies and spending to incentivize private investments in racialized neighborhoods, and charitable initiatives with the same goals (e.g. Loomis, 2018). Legal decisions such as 1978’s Regents of the University of California v Bakke (1978) constrained state options for directly addressing past discrimination, replacing specific numerical inclusion targets based on race with “goals” or “timetables” for increasing diversity in higher education; the effects of Regents rippled into other sectors and reinforced the private markets as the venue for addressing racialized economic disparities.

In more recent decades, the recognition of structural racial barriers to economic mobility has become more mainstream in policy and economic discourse. Today, analyses of inequitable capital flows to racialized neighborhoods and so-called minority owned businesses, underinvestment in schooling for racialized children and young adults, divergence in intergenerational wealth transfers, and disproportionate impacts of the 2008 economic crisis (McKernan et al., 2012; Mishory et al., 2019; Shapiro et al., 2013; Weller and Hanks, 2018) all frame racism as an explicit factor. Yet explanations focused around cultural differences in economic activities remain influential: understood as different “choices” in savings, investment, and consumption priorities (Choudhury, 2002) to financial illiteracy (Boshara et al., 2015).

Such perspectives on the causes of the wealth gap, by neglecting to account for the economic benefits that capital has accrued by either excluding or predatorily including racialized households and businesses, produce the wealth gap as an abstract space (Inwood, 2013) where wealth divergences are acknowledged but not historicized. As an ahistorical measure, wealth is depoliticized from its roots in the unequal provisioning of everyday life over generations. Rather, these framings of the gap focus on the future as the place a more level playing field will emerge. Gap analysis is the comparison of actual performance with potential or desired performance—a comparison between the “current state” and a “desired future state” of being. It rests on the premise that there is an ideal, optimized allocation of resources. As noted in the corporate commitments to invest in racial justice outlined above, the “desired future state” is for racialized households to catch up with the wealth levels, consumption practices, and business successes of white communities.

The wealth gap as economic inefficiency and credit as proposed solution

21st century policy justifications for addressing the contemporary racial wealth gap are also driven by economic arguments. A foundational analysis used in the racial justice investing industry, the Kellogg Foundation’s “Business Case for Racial Equity,” argues that racial inequality is economically inefficient (Turner, 2018); analyses by the financial industry frame racialized wealth inequality as an overall economic detriment. Citi Global Perspectives and Solutions, for example, calculated the wealth gap as costing the US economy $16 trillion in the past 20 years (Peterson and Mann, 2020). Beyond closing the Black wage gap, Citi’s analysis highlights the socially reproductive sectors of housing and education: Citi claims that access to higher education for Black students could have increased their lifetime incomes from $90 to $113 billion, while improving access to housing credit could have added over 700,000 Black homeowners and $218 billion in sales and expenditures. Here, racialized communities are framed as investible by portraying their exclusion as economically inefficient for the economy as a whole and by painting racialized divergences in wealth-generating potential as a problem of lack of investment.

Framing the gap as an economic inefficiency—and solving the gap as an economic boon—allows racial injustice to be homogenized into an investment object. While many stakeholders clearly see political, marketing, and ethical value in engaging in racial justice investing, thought leaders like Kellogg and investors like Citi and Bank of America argue that framing the racial wealth gap as a great market opportunity invites a larger range of investors to the table (e.g. Bank of America, 2020). Claims that racial justice investing is good for everyone abound: “racism impoverishes the whole economy” wrote economics professor Lisa D. Cook (2020), a member of the Biden-Harris presidential transition team, in an November 2020 op-ed. Meanwhile, in the months after George Floyd was killed, credit ratings agencies like S&P Global started to report that a failure to attend to racial injustice was now a business risk for corporations. According to S&P, shareholders “are increasingly holding companies to a higher social standard, demanding that they demonstrate a real commitment to advancing racial equality, beyond donations and promises” (Longdon et al., 2020, np). This reputational risk, S&P noted, “could have an impact on. . .performance and, ultimately, on credit quality if loss of customers reduces profitability” (Longdon et al., 2020, np). This characterization of risk appears to be novel to the period after the Black Lives Matter protests of 2020; proponents of racial justice investing quickly reframed it into a strategic opportunity. As noted by the editors of impact investing publication Impact Alpha in reaction to Black Lives Matter protests in 2020, ““If racism is a systemic risk, overcoming its legacy and investing in justice and equality are systemic opportunities” (Price and Cortese, 2021, np). These “systemic opportunities” are accompanied by specific relationships between creditors and debtors—as well as types of investments and risk distributions—which I outline in the rest of this section.

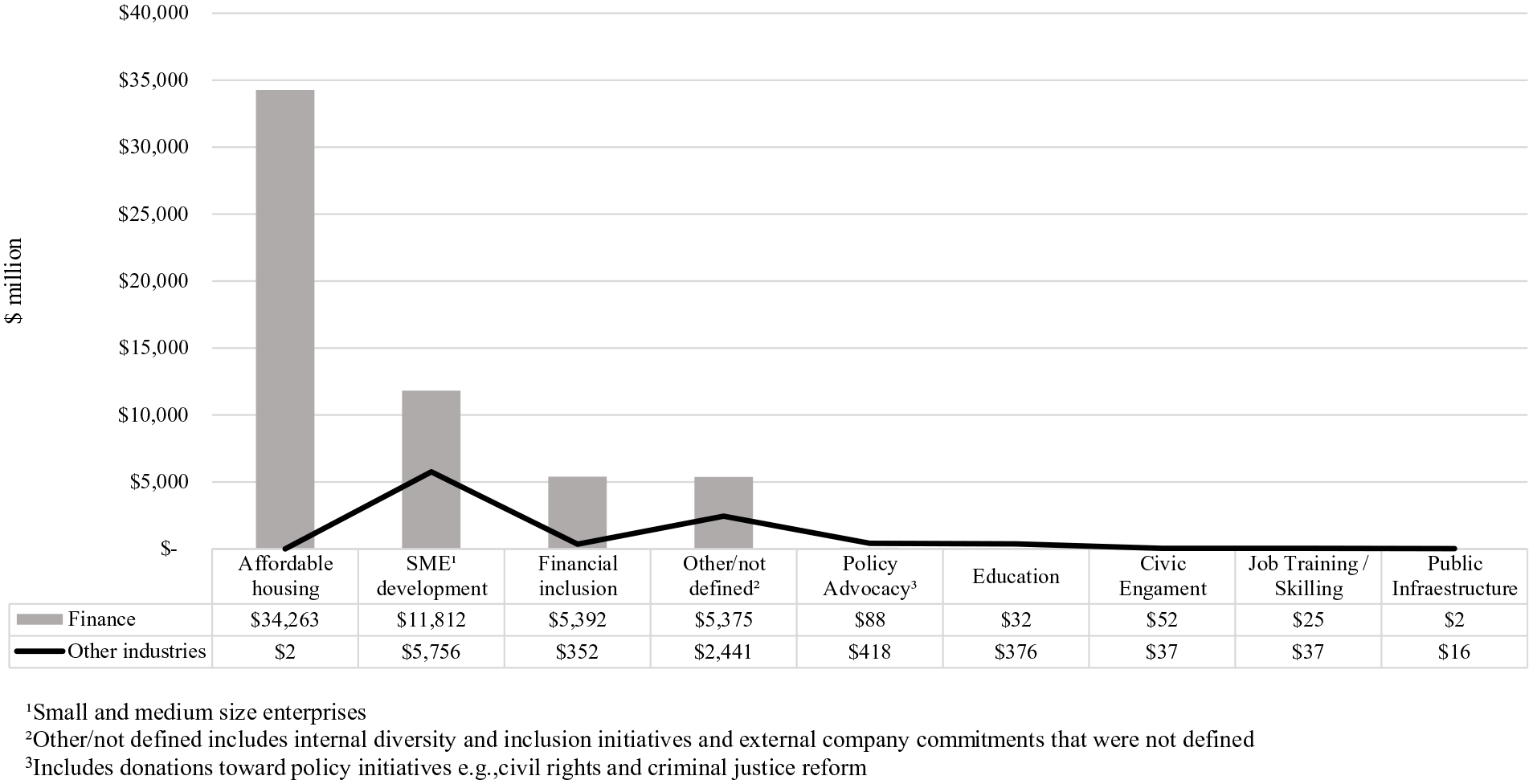

According to analyses of the financial industry’s post-2020 investment pledges (Jan et al., 2021), the dominant tools of racial justice investing involve expanding access to credit: for homeownership, construction of affordable rental units, and minority-owned business ventures (see Figure 3). In the first 18 months after the 2020 protests, affordable housing and business development were by far the top investments made (Armstrong et al., 2023; Fitzhugh et al, 2021). This is the structure of racial justice investing—rather than a donation, access to credit (on which the borrower will pay interest) is the tool intended to produce benefits for racially- and economically-marginalized people. Yet while homeownership and business ownership are primary means of generating generational wealth in the long term, mortgages and business loans involve racialized households or business owners taking on debt in the short term, while rental housing ultimately means wealth flowing out of racialized communities. While credit access as social provisioning is widespread in anti-poverty policy (Atkinson, 2019), the use of this tool as a way of fighting racism perpetuates and reinforces racial capitalist debt relations. Rather than acknowledging capital as being indebted to racialized communities for ill-gotten profits, racialized households remain in debt to capital, under the guise of increasing justice.

Areas of investment commitments to advancing racial equity by Fortune 1000 companies, May–October 2020.

Yet this relationship, which lies at the root of racial justice investing, remains mostly invisible in the contemporary racial capitalist asset economy: framings of the wealth gap as economically inefficient here collide with how households acquire assets, through credit. Thus, when companies like JP Morgan Chase label their normal business (mortgages and small business loans) as racial justice investing, they fail to acknowledge how such “necessary” debts affect racialized people differently (Seamster, 2019) due to systemically higher interest rates, worse terms, and reduced chances of being able to convert debts into assets, let alone successfully pay them off (Charron-Chénier, 2020). Credit is based on the idea that debts can be repaid by borrowers who are progressively better off, essentially requiring future prosperity of households and business owners (Atkinson, 2019). But in an environment of educational disparities, structural racism, and now inflation, this future prosperity is far from guaranteed. The temporalities of credit proposed to end the wealth gap are much shorter than the production of the processes that created the wealth gap to begin with.

The structures of accountability that underlie racial justice investing are also variable between debtors and creditors. Debtors must qualify for financing and repay their debts—standard financial relationships remain the same. Creditors claiming to be enacting racial justice, however, are facing increasing public and political scrutiny and have often responded by attempting to evade forms of accountability that might allow a racial justice mission to disrupt standard financial relationships. JP Morgan Chase (2022), for example, published an “audit” of its racial justice investing activities in 2022, claiming to have invested $18 billion of its promised $30 billion. Yet this audit was authored by JP Morgan Chase itself, did not contain independent recommendations, and failed to disclose how much of the $30 billion pledge would have been lent out anyway as part of the bank’s preexisting business operations. The audit did not include any perspectives from the racialized communities that JP Morgan Chase claimed to be helping (SEIU, 2023), and Chase and other banks have urged shareholders to vote no on actions that would hold the companies to meeting their racial justice goals (Levitt, 2022). As with traditional investing, investments are governed by the creditors, not the communities most affected by racism. These structures of governance and accountability, and the consensus around using credit from private financial actors as a form of social provisioning, make it possible for the financial industry’s business as usual to count as “racial justice investing.”

Conclusion

As scholar and journalist Nikole Hannah-Jones (2020) noted in the wake of 2020 protests, “Wealth is. . .the most consequential index of economic well-being for most Americans. But wealth is not something people create solely by themselves; it is accumulated across generations.” Neoliberal policy organized around corporate sovereignty has outsourced public responsibilities for ensuring equitable social reproduction, framing race-based financial discrimination and inequality as something that can be corrected from within the system. This has recently been buoyed by well-publicized corporate commitments to address racial injustice in US society, translated into narrower focus on racialized economic inequality and a narrower focus still on “inequitable” access to capital systems.

As I have shown above, responding to the racial wealth gap with private credit frames racial injustice as an economic measure that can be addressed by financial companies—often in the form of extending credit to racialized borrowers. This is also a process of homogenizing racialized inequality such that improvement can be measured in terms of an abstracted racialized economic subject. The gap analysis behind these investments does not account for how white wealth was derived, despite robust evidence about how the financial industry’s wealth was made possible by dispossession of racialized people (e.g. Inwood et al., 2021). Alternative mechanisms of supporting social reproduction in the asset economy—public banking, student loan forgiveness, alternative capital structures— thus deserve greater attention, especially given how contemporary racial justice movements like the Movement For Black Lives focus far more on redistribution and reparations than on financial inclusion. Against the racial justice investing industry’s tendency to collapse racialized people into a singular category, greater attention is due to the specific demands of different communities, as well as how they care for each other in the current system of unequal life chances. Alternative financial models look very different when they are derived by and for marginalized communities. The Boston Ujima Project, for example, is an investment opportunity in racialized Boston communities that pegs investor influence not to the size of their investment but to the investor’s connection to the community and overall wealth; those with lower wealth and closer connections get more say. This is just one of numerous examples of economic justice that build on long-standing models of racialized peoples’ economic self-determination.

It is also worth considering the limits of racial justice investing in terms of how it perpetuates the valuing of Black and other racialized lives in terms of their function as a site of accumulation. Mistaking racialized social reproduction for a depoliticized “gap” drives the underlying logic of the solutions put forth, recognizing (but not compensating) historical exclusion while proposing inclusion in (white) capital systems as the road to racial justice. Yet appealing to these interests tends to involve omitting an accounting of how white people and financial institutions have benefited from the devaluation of racialized people’s lives. Valuing the wealth gap only in terms of the net present value of closing it discounts its lingering effects on social reproduction and the life chances of future generations. While a cultural shift can be seen in (white) capital’s newfound desire to understand itself as antiracist, its evolution—and how attaches understandings of racial justice to new paths of accumulation—deserves continued scrutiny.

Banks and finance, which were both the target of racial justice activism during the summer of 2020 (Nguyen et al., 2020), have been pulled in two directions by more recent political and legal debates over racial inequality. On one hand, many investors responded to the 2023 US Supreme Court decision banning affirmative action in universities by doubling down on their racial equity goals (Bank and Price, 2023). On the other hand, conservative activists have accused racial justice investors of “reverse racism,” in one case successfully suing a firm offering start-up capital to Black women entrepreneurs for violating federal law prohibiting racial discrimination in contracting (Mark, 2023). Many investors, however, continue to believe that racism is a systemic risk to profits, and shareholders have filed lawsuits against companies for not abiding by the racial justice goals they set in 2020 (Hood, 2023), claiming that these companies are not executing their fiduciary duties. Fears of the financial and legal consequences have led JP Morgan Chase and the “Big Four” asset managers (BlackRock, Fidelity, State Street, and Vanguard) to block shareholder actions on racial equity issues (SEIU, 2023).

In an asset economy, in conditions of racialized social reproduction, mortgage and business debts are both a tool for wealth accumulation and a possible means of dispossession. Racial justice investments that have led to debt taken on by racialized borrowers are thus a complex social relation. Examining the terms and governance structures of these debts is key to understanding what they are inscribing. The overrepresentation of the financial industry in efforts to “invest” out of racial injustice—and the tools this industry uses in its claims to do so—have much to teach us about market-based understandings of anti-racism.

Footnotes

Acknowledgements

This paper has benefited from conversations with Bob Lake, Rachel Weber, Jessa Loomis, Josh Inwood, Sharlene Mollett, and Tom Baker. Thank you to Alejandra Bonilla Mena for data visualization. My gratitude also goes to the anonymous reviewers and editor Brett Christophers. All errors and omissions are my own.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.