Abstract

The wealth chain is a conceptualisation of extended flows of capital operating across multiple tax jurisdictions in order to extract maximum value from investment locations. To date, such chains have largely been considered in relation to either international tax-avoiding flows of capital to offshore havens or in relation to prime property markets in major metropoles. In this article, we use new data to explain the geographical variations in asset strategies and investment types associated with different types of wealth chain in a historically deprived city region. The data relate to the purchase of real estate in the Liverpool and Merseyside Area (LMA) of the UK by companies from offshore jurisdictions. We use data to empirically model the wealth-chain concept. We compare the results from our empirically derived model with the key theoretical propositions regarding such chains. Our results confirm the actions of identifiable types of wealth chain. By geographical distribution, the specific asset strategy that dominates suggests that wealth-chain offshore investors in Liverpool’s real estate are primarily motivated by their desire to protect their identities and their assets. In the literature on the subject, these are much sought after attributes of money launderers and others involved in illicit wealth accumulation. In money terms, the dominant asset strategy is situated in a much smaller geographical space in and around the city centre. In the literature, this type of wealth chain is associated with the multinational corporations who are, theoretically, the main source of innovation in wealth-chain operations.

Keywords

Introduction

Existing theories of finance generally focus on deposit-taking institutions, equities trading and price formation, and underline the market-completing and welfare-enhancing functions provided by financial innovations (Allen and Santomero, 1997). We seek to go further and get behind the veils that mask the play of capital across nations, regions and urban areas, much of it orchestrated from offshore locations. In this regard, we wish to improve public understanding of how financial and legal innovations are articulated through wealth chains that run from offshore to onshore locales. Historically, the key product of financial innovation has been the asset. In the contemporary setting, the key product is no longer the asset, it is a capacity to reproduce assets and exposures synthetically. Synthetic assets are financial asset products created by financial modellers to sell to corporate, private and public investors in the financial markets (McKenzie, 2011). In the contemporary context, finance has been revolutionised in ways that are advantageous to asset holders and the wealthy, while being increasingly destructive to those who lack such resources – urban communities in particular (Goulding et al., 2022; Stein, 2019).

Today, the boundaries between institutions and assets are far less clear than they used to be, making for a setting in which finance is far more mobile than at any time in history and the capabilities of ownership have become more fluid (Bryan and Rafferty, 2006) and enhanced in ways that allow for instantaneous and relatively, frictionless switching, so that ‘an exposure to an asset or an ownership position can be transformed in terms of character, term and “geopolitical locations” (Merton 1995: 463–464).

The area of theory with which we engage in this article comes from Seabrooke and Wigan’s (2017), theorisation of the global wealth chain typology. The study of wealth chains is essentially a study of information asymmetries within investment strategies. In finance, informational asymmetry (whereby certain actors possess greater knowledge of market conditions and tax rules than others) generates innovation, such as looking for ways to work around rules, including seeking to avoid regulation or prosecution. Obviously, there are varying levels of such innovation from company to company and protection from regulation will vary among institutions – we are concerned with explaining these variations in strategy and we focus on three key problematics. First, the literature on financialisation is important because it explains how global wealth chains are articulated and governed. Much of this research focuses on the ways in which financialisation has changed organisational forms and reconstituted social relationships. This body of work helps to improve our understanding of the changed organisational forms we are studying.

What has been the called the social studies of finance literature also conveys crucial insights that aid our understanding of wealth chains: ‘These studies focus on the plumbing and wiring of financial markets, as well as the social environments that propel them, with research often situated in the trading room or “nerve centres” in financial institutions’ (Seabrooke and Wigan, 2017: 6). 1 Finally, the economic sociology literature helps us to understand and explain the market structure, the role of client perception and client and supplier status.

Finance is now embedded 2 in our economic lives in ways that have displaced locales of productive activity and replaced them with novel forms of purely financial activity. In both poor and more active city regions, finance plays an extended role, with new and uneven sets of winners and losers. We can now see how capital nested in offshore zones is a significant component of this financialised economy, with massive amounts of this capital flowing into assets wherever and whenever it is most profitable to do so (Bullough, 2018; Shaxson, 2011).

The proliferation of financial innovations since the 1980s has produced a disjuncture between what is mobile and what is fixed (Bryan et al., 2017), so that financial assets are increasingly separated from the fiscal apparatus of the state. This is the space that provides the institutional basis for the concept of global wealth chains – it provides an avenue through which wealth-chain investors can avoid or evade tax obligations and hide their assets from regulators.

Our work has much in common with Revington and August (2020), who, as part of their analysis, examine the business strategies and geographical patterns of investment. In their research on Canadian purpose-built student accommodation (PBSA), they demonstrate the ways in which finance has managed to insert itself into what they term ‘niche real estate sectors’ (Revington and August, 2020: 856). In assessing the local impact in Waterloo (Ontario), they find that the PBSA’s ‘finance-driven new-build studentification has contributed to higher housing costs and age segregation’ (Revington and August, 2020: 856). In their analysis of Canadian conditions, they reveal that the financialisation process was different from that in other housing sectors because it depended on the creation of new student housing to provide a channel for new investment. Thus, according to these authors, ‘finance-driven new-build studentification functions as a spatial fix 3 by directing investment to secondary cities’ (Revington and August, 2020: 856). In a related study to that of Revington and August, Mulhearn and Franco examine the substantial and ‘rapid development’ of PBSA in Liverpool, UK, and raise ‘questions not just about its impacts but about its sustainability’ (Mulhearn and Franco, 2018: 477). The authors anticipate a disorderly end to Liverpool’s PBSA boom and conclude by considering the likely social implications of such a sudden stop.

Horton (2022) discusses the increasing financialisation of everyday life through an analysis of the ownership of care homes by investment funds. She finds that this type of financialised ownership is determined by debt financing and the value realised through the sales of property assets. Importantly, she finds that ‘financialization has also been shaped by labour’ (Horton, 2022: 144). Her argument is in two parts: first, the low status of a largely female workforce supports investor buyouts and, second, the financial burden associated with neoliberalism is ‘partly absorbed’ in the interactive labour of care. In Horton’s view, ‘this reflects a neoliberal model of investment and regulation, which treats workers as disposable – unskilled and replaceable’ (Horton, 2022: 144). She posits that in continuing to care under deteriorating conditions, workers provide a source of value to investors and, by the very act of continuing to care, workers are rejecting the notion that they are disposable. This rejection, she argues, opens avenues for resistance to financial discipline and is also an example of caring labour limiting financialisation. The main thrust of her argument is that financialisation should be understood ‘as constituted not only by financial practices, property assets and regulation but also by specific forms of labour’ (Horton, 2022: 144).

Sharman (2017a, 2017b), Chiodelli (2019) and Ward (2022) focus on the issue of corruption in the process of illicit wealth accumulation, which is integral in the study of wealth chains. Sharman (2017a) examines the varying impact of supra-national regulatory initiatives to target banking and corporate secrecy on the various types of wealth chain that run through two stereotypical havens, Liechtenstein and the Seychelles, and Australia (a country rarely associated with illicit financial flows). He shows how regulatory shifts can change the flow and form of wealth chains by unintentionally creating new avenues for offshore finance. In a related contribution, Sharman (2017b) describes the ways in which kleptocrats use offshore jurisdictions to loot their countries. As in the previous case, he depicts Australia as a country in denial because of its failure to acknowledge that it is a significant host for looted money. Both Chiodelli (2019) and Ward (2022) place the planning process centre stage in their research. From our point of view, the main insight emerging from these studies is that there are institutional incentives to corruption that play an important role in the governance of global wealth chains.

In addition to the aforementioned literature, our work here is also informed by a number of empirical writers who attribute sector-specific specialisations to the various offshore jurisdictions around the world. These include Palan et al. (2010), Harrington (2016), Muasya (2018) and Garcia-Bernardo et al. (2017). We use this literature to contextualise our work and to connect with the business-sector dynamics that influence what is taking place on the ground in Merseyside.

The focus of our study is Liverpool. The city region, the Liverpool Metropolitan area (LMA), consists of 249 square miles of urban, semi-rural and rural locations divided into five metropolitan boroughs: Knowsley, Sefton, St Helens, the Wirral and the city of Liverpool. With a population of 1.4 million people, it is the fifth most populous region in England (ONS UK, 2018). Historically, levels of inequality and deprivation in the region have been among the highest in England 4 and, at first glance, it is not obvious why offshore money should flow to the area. A large part of the explanation derives from a key event in the mid-1990s, when the European Union designated Liverpool as a deprived EU ‘Objective 1’ area (Mulhearn and Franco, 2018).

The funding from the Objective 1 designation greatly improved the economic possibilities of the region: ‘Objective 1 directly supported several flagship projects including transformational improvements to the waterfront, airport and rail infrastructure, but more importantly – alongside Liverpool’s successful bid to be the European Capital of Culture in 2008 – it helped to positively condition private sector perceptions of Merseyside’ (Garcia et al., 2010, cited in Mulhearn and Franco, 2018). Today, Merseyside’s economic progress is such that ‘Objective 1 status is no longer justified given that local GDP levels have closed on the EU average’ (Garcia et al., 2010). The net effect of this state-sponsored rejuvenation has been to create conditions in which capital can be invested to take advantage of future growth in rental yields or greater asset-value appreciation following this investment (Eldred, 2012). According to the real-estate investment press, on both these counts, the city region offers investors very competitive returns compared with the rest of England and Wales. These conditions are highly suggestive of a state-sponsored form of rent gap.

The paper is structured as follows: in part 1, we discuss the concept of global wealth chains; in part 2, we describe our methodology and analyse the data; in part 3, we operationalise the wealth chain, apply it to the LMA region and report our results; and, in part 4, we compare the results of our empirical modelling with the propositions from the global wealth chain theorisation.

Understanding the forms of global wealth chains

Extending an earlier framework Gereffi et al. (2005) and Seabrooke and Wigan (2017: 2) define wealth chains as ‘transacted forms of capital operating multijurisdictionally for the purposes of wealth creation and protection’. Expressed in a slightly less abstruse way, we may define such chains as the elongated and connected pathways of monies flowing around the global economy that are designed to limit tax responsibilities and maximise personal or corporate returns. The utility of this concept is that it helps us to visualise, and then measure, the kinds of vehicles and arrangements through which value is extracted, and ownership is achieved, by investors and wealth managers across national jurisdictions (McKenzie and Atkinson, 2020), by focusing attention on the institutions, actors and flows of capital around the global financial system. We use the concept of wealth chains here to focus on the types of strategy used by offshore property owners in relation to the Liverpool city region. Our overall reading of the data is that the concealment of wealth from national tax agencies has become a key mechanism through which property resources are exploited by offshore investors using offshore shell companies and opaque ownership structures.

Seabrooke and Wigan (2017) show that the main idea behind the conceptualisation of the wealth chain is its focus on the asymmetry of information between three principal links in the chain: the client (the beneficial owner or investor), the supplier and the regulator. The aim of the wealth chain is to exploit these varying asymmetries in order to limit information flows to regulators that would otherwise lead to the identification of the beneficial owners of these assets. The dark space in which wealth chains operate thus forms the basis of the advantage of offshore ownership, which works to conceal the identity of the beneficial owners and offers the possibility of limiting tax obligations as a result. The wealth chain can be seen as a kind of pooling device, or mechanism, which may help to merge, protect and expand the wealth and assets of the client. It brings together a multitude of professional suppliers – real-estate professionals, wealth managers, lawyers, bankers, multinational corporations and international networks – to design and execute transactions that minimise tax and obscure identities (Christensen, 2021; Wainwright, 2011).

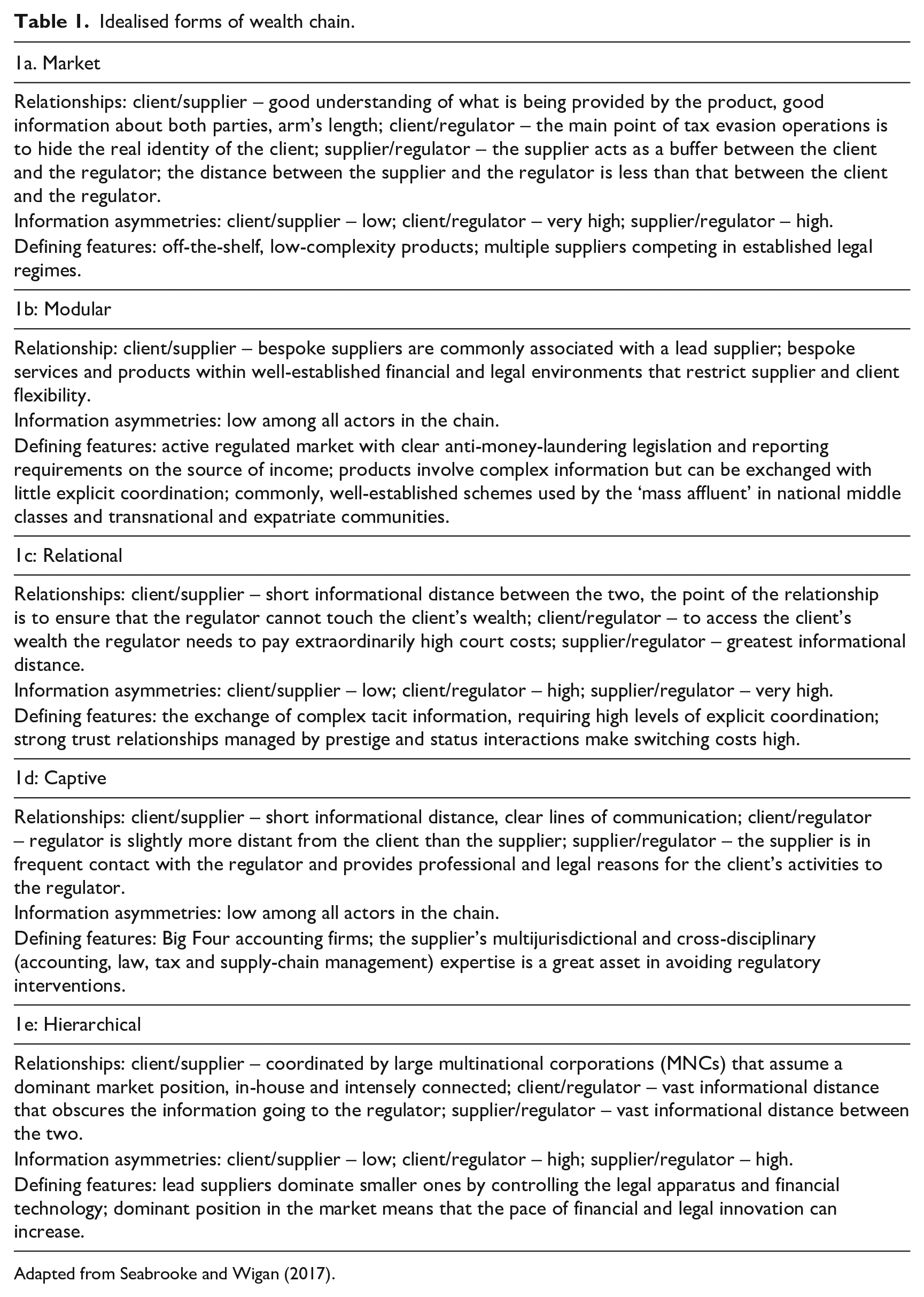

Table 1 summarises the key relationships, information asymmetries and the defining features associated with each of Seabrook and Wigan’s five ideal types of wealth chain. In our model, four of the five ideal types are identified. We find no captive wealth chains and, thus, we do not discuss them. As we move down the table (from 1a to 1e), the degree of explicit coordination associated with each type of wealth-chain operation progressively increases.

Idealised forms of wealth chain.

Adapted from Seabrooke and Wigan (2017).

Garcia-Bernardo et al. (2017) map asset strategies to reveal a network of ‘sink’ and ‘conduit’ 5 jurisdictions with an associated range of jurisdiction-specific, sector-based specialisations. Other writers have used network analysis to map multiple corporate units through intra-firm ownership stakes (Heemskerk et al., 2016; Buch-Hansen and Henriksen, 2019, cited in Seabrooke and Wigan, 2022: 8). Haberly and Wójcik (2015) complement this work in their study of regional agglomerations of foreign direct investment (FDI) flows that allow for the characterisation of ‘global financial networks’. This work finds that offshores in Northwest Europe and the Caribbean play the most important role in the world system of FDI flows. This research was able to identify four principal FDI subnetworks, which the authors associate with geopolitical hegemonic formations that were moulded by historical processes.

We turn now to our own approach to the mapping of asset strategies, which we present in the next section.

Methodology

There are three steps in our methodological approach. First, we use data from HM Land Registry’s Overseas Companies Ownership Data (OCOD) (HM Land Registry, n.d.) to delineate the scale and scope of the purchases. The data run from January 1999 to January 2020 as HM Land Registry did not routinely record the country of incorporation in the register before January 1999. The dataset is a list of freehold or leasehold title registrations in England and Wales where the registered legal owner is an overseas company. Private individuals, UK companies with an overseas address and charities are excluded from this dataset for dataprotection purposes. We use a subset of the OCOD dataset that contains 2312 titles obtained from a CSV file of all Merseyside addresses and postcodes. This data analysis provides a basis for the geographical mapping of asset strategies that we aim for.

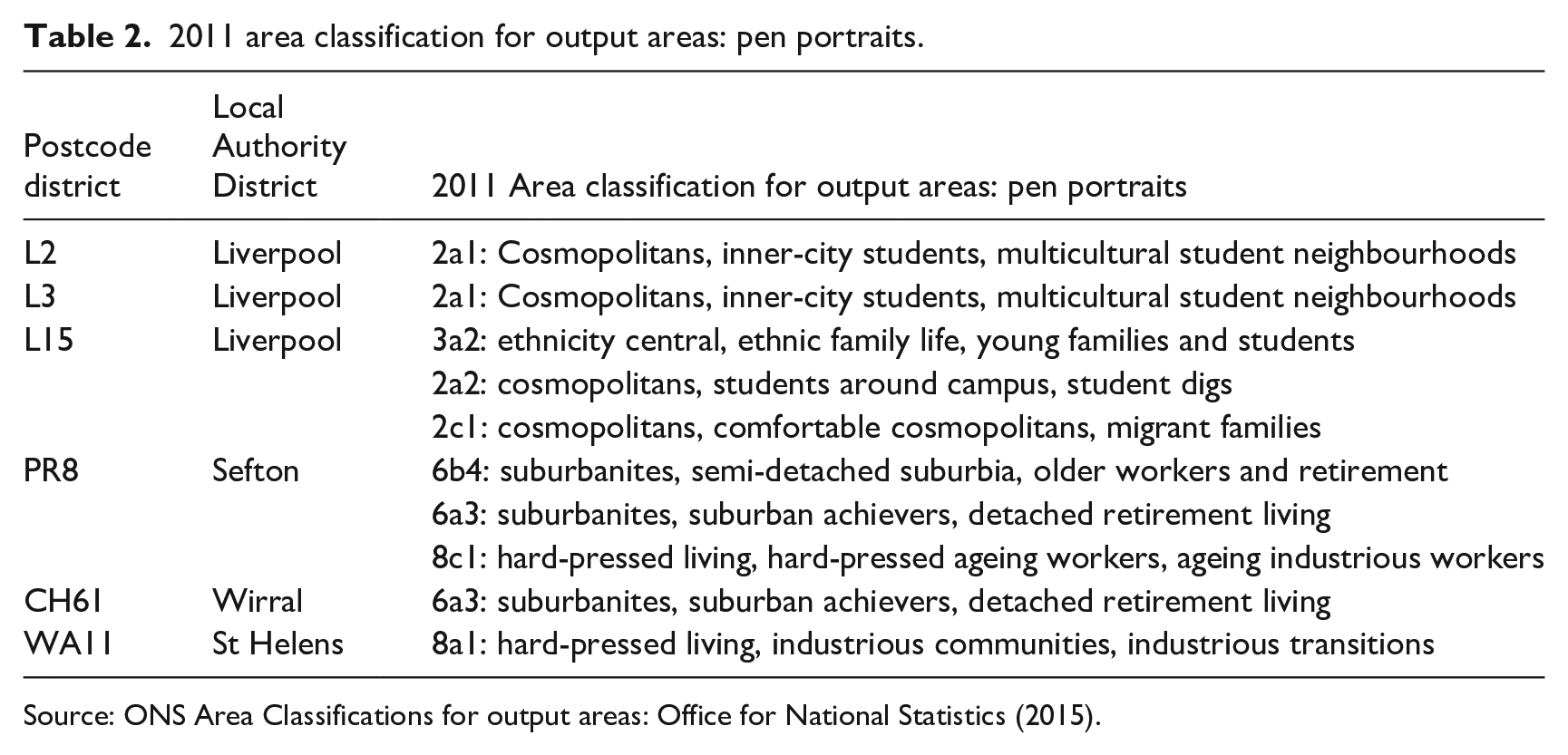

Second, we combine the statistical analysis with the 2011 Area Classification for Output Areas: Pen Portraits (Office for National Statistics, 2015; Table 2) in order to map the flow of offshore money to Merseyside to specific postcodes and neighbourhoods. We use the empirical insights obtained as the basis for important assumptions in the construction of the algorithm that we undertake later in this section. Table 2 shows the six postcode areas in the Merseyside area that have significant concentrations of offshore real-estate investment: in the city of Liverpool, the L2, L3 and L15 postcodes and, across Merseyside in general, the PR8 postcode in Sefton, the CH61 postcode in Wirral and the WA11 postcode in St Helens.

2011 area classification for output areas: pen portraits.

Source: ONS Area Classifications for output areas: Office for National Statistics (2015).

The Office for National Statistics postcode classifications are shown in column 1. The three Liverpool city postcode areas are classified as student areas (column 3) and the postcode areas outside the city are classified as retirement-living or hard-pressed and older-worker areas (column 3). In short, in common with Revington and August (2020), we find that property-investment areas are differentiated by age: the city (close to Liverpool’s several universities) for student homes and the rest of Merseyside for retirement homes.

The third and final step is the construction of a Partitioning Around Medoids (PAM) k-medoids algorithm (Kaufmann, 1987). This is based on a methodology that we borrow from machine learning in order to conduct a cluster analysis of offshore global wealth chain property investment in the LMA. The algorithm organises the property titles into groups, or clusters, based on how similar they are to one another. The aim is to find similar clusters, where ‘similarity’ between each pair of titles means some global measure over the whole set of characteristics. Cluster analysis has successful applications in urban studies (Czamanski et al., 1979; Feser, 2003; Hoesli et al., 1997), in business and in social sciences generally (Fonseca, 2013). The number (k) of clusters is assumed to be known a priori. Thus, the programmer assigns this number. The goodness of fit of the given value of k can be assessed through techniques, such as the silhouette method, that tell us how well each title has been classified (Rousseeuw, 1987). The medoid of a cluster is defined as the title in the cluster whose dissimilarity to all other titles in the cluster is minimal, that is, it is the most centrally located point in the cluster. The strengths of this approach are that k-medoids can be used with arbitrary dissimilarity measures and, as k-medoids minimises a sum of pairwise dissimilarities instead of a sum of squared Euclidean distances, it is more robust in dealing with noise and outliers in the data. 6

We partition (i.e. we break up the datasets into groups) offshore real-estate investments defined by property titles based on three criteria of governance proposed by Seabrooke and Wigan (2017):

i. Regulatory liability

ii. Capabilities in mitigating uncertainty

iii. Complexity

In order to transform these theoretical criteria into measurable empirical features we make three key assumptions, to which we now turn. 7

The keys to the global wealth chain typology are three variables that determine the form of information asymmetry among five types of wealth chain. In our model, secrecy replaces regulatory liability, the number and type of special purpose vehicles (SPVs) replaces capabilities in mitigating uncertainty and specialisation replaces complexity. We use these measures to empirically capture the real-world forms of the variables posited by Seabrook and Wigan. In our work, these three measures transform the theoretical propositions into empirical features that we are able to measure and quantify. We operationalise these variables to apply the global wealth chain analytical lens to the Merseyside area.

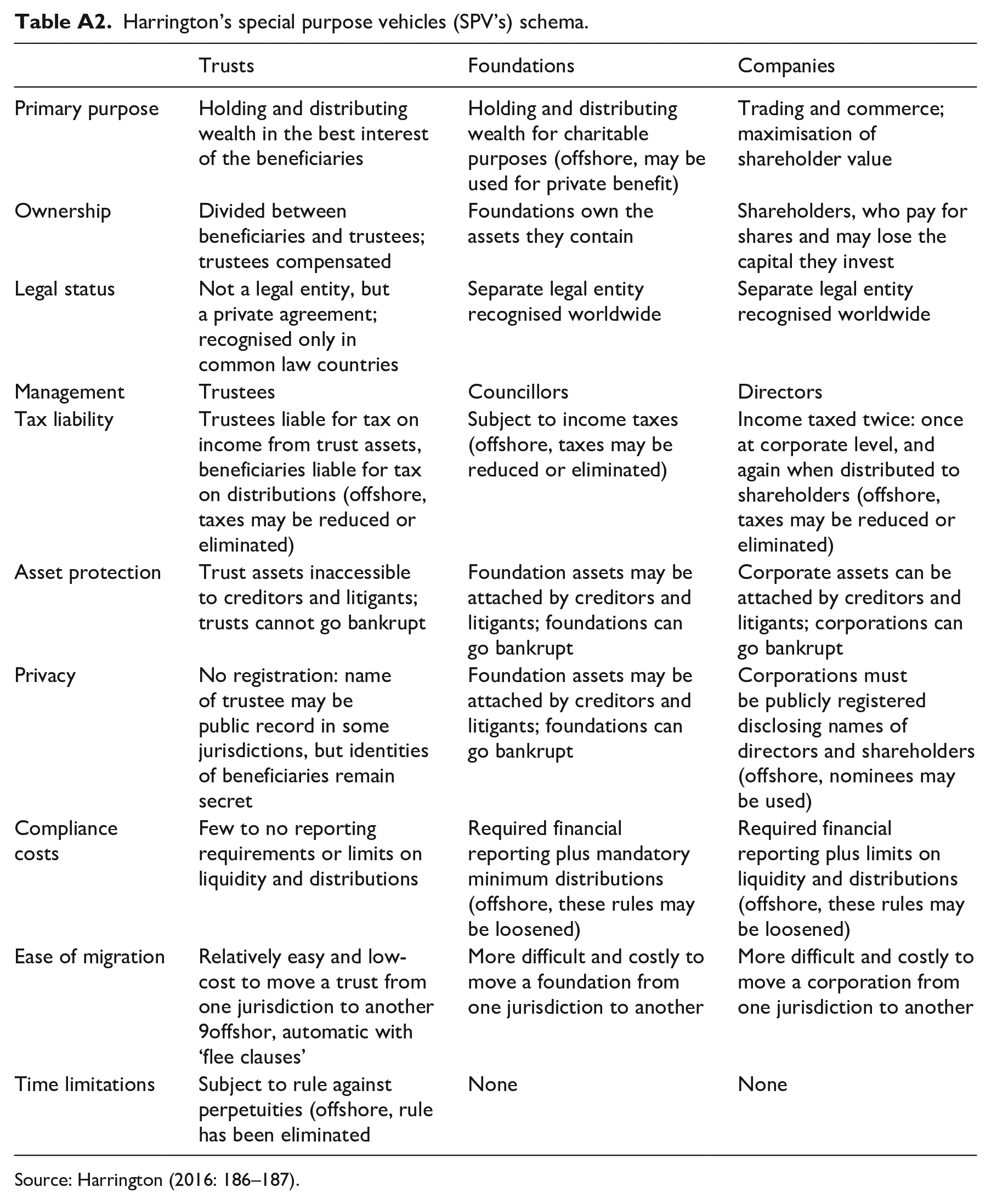

Our selection of empirical measures is guided by our own empirical work and understanding of the case study work of Palan et al. (2010), Harrington (2016), Revington and August (2020) and Horton (2022), discussed earlier. In short, we use this literature to inform our assumptions.

i. Regulatory liability: we use Tax Justice Network (TJN) (2018) secrecy scores by offshore jurisdiction, under f1 – the assumption that secret jurisdictions are those with low regulatory liability.

We use the TJN financial secrecy index (FSI) scores to estimate the levels of regulatory liability associated with each of the secrecy jurisdictions in our sample. A TJN score over 60 is assumed to be extremely secret and below 60 only moderately secret. Thus, a high secrecy score means low regulatory liability (the principle being that as little is known about the actions of investors, there is little to regulate) and vice versa. We measure regulatory liability in the TJN FSI secrecy scores, but we acknowledge that if regulatory liability were measured by some proxy for the mobility of capital, where market wealth chains may have a competitive advantage, this changed assumption may well yield different results.

ii. Capabilities in mitigating uncertainty: we construct a count measure based on three key legal f2 vehicles.

Here, we lean on our understanding of Harrington’s (2016) work. Based on her 10-year research-project experience, she concludes that, among the various legal forms of business entity, the private trust affords the greatest asset and identity protection. We take this legal feature and examine the data, looking for the terms 'trustees’, holdings’ and 'limited liability companies’. 8 The attribution of these criteria is based on a textual analysis of company names given as regular expressions (regex). In addition, we assume that, in general, the greater the number of SPVs, the greater the ability to mitigate uncertainty. We therefore assume that the higher the number of these features, the greater the capacity to mitigate uncertainty. We simply count the number of times these labels appear in the data and attribute asset protection capabilities accordingly.

iii. Complexity: we assume investors operate f3 in one of two segments in the real-estate market.

From the Office for National Statistics classifications, we can see that offshore property investment is highly concentrated on one of two market segments: student accommodation or care-home accommodation. It involves specialist investors from the PBSA (Mulhearn and Franco, 2018; Revington and August, 2020) and care-home (Horton, 2022) sectors. Here, we assume that the greater the degree of specialisation, the greater the ability to offer (more) complex services and products, and the greater the capacity for innovation.

Once clusters of offshore-owned titles are formed, median values of their features are used to label clusters qualitatively in accordance with our key determinants of global wealth chain governance. Thus, using machine-learning computer techniques the data is grouped (by an iterative process) around three information asymmetry criteria. The closer the data points are to one central point (the medoid), the purer the form of the wealth chain in terms of the five types (market, modular, hierarchical, captive and relational). Hybrids occur when the points, while being closer to the X medoid, have some relation or proximity to the Y medoid in one of the other clusters.

The limitations of our approach are two-fold. First, they relate to the restricted nature of our modelling: we only include three explanatory variables with one simple count measure (asset protection/capacity to mitigate uncertainty). Second, in terms of our assumptions, we rely solely on one body of casework – financialisation literature – and our understanding of that literature to inform the algorithm.

Results

We find that the offshore centres of Jersey, Guernsey, the Isle of Man and the British Virgin Islands accounted for almost all the purchases. These jurisdictions are well-known for their ‘flexibility, pragmatism, and the ability to manage and control a property investment vehicle without incurring any local income tax or deductions for withholding’ (Lombardi and Kershaw, 2003: 27). Internationally, as offshores, their credibility is enhanced by their status as British Overseas Territories or British Crown Dependencies. From the viewpoint of prospective clients, this denotes a stable capitalist country, known for good governance. Jersey company registrations accounted for more than 930 titles, Guernsey and the Isle of Man accounted for 232 and 358, respectively, and the British Virgin Islands for a further 249 titles, all since January 1999. Furthermore, the investors from these jurisdictions almost exclusively utilised the limited company as the legal vehicle for acquiring property titles in the region. Private trusts were used to a far lesser extent than limited companies.

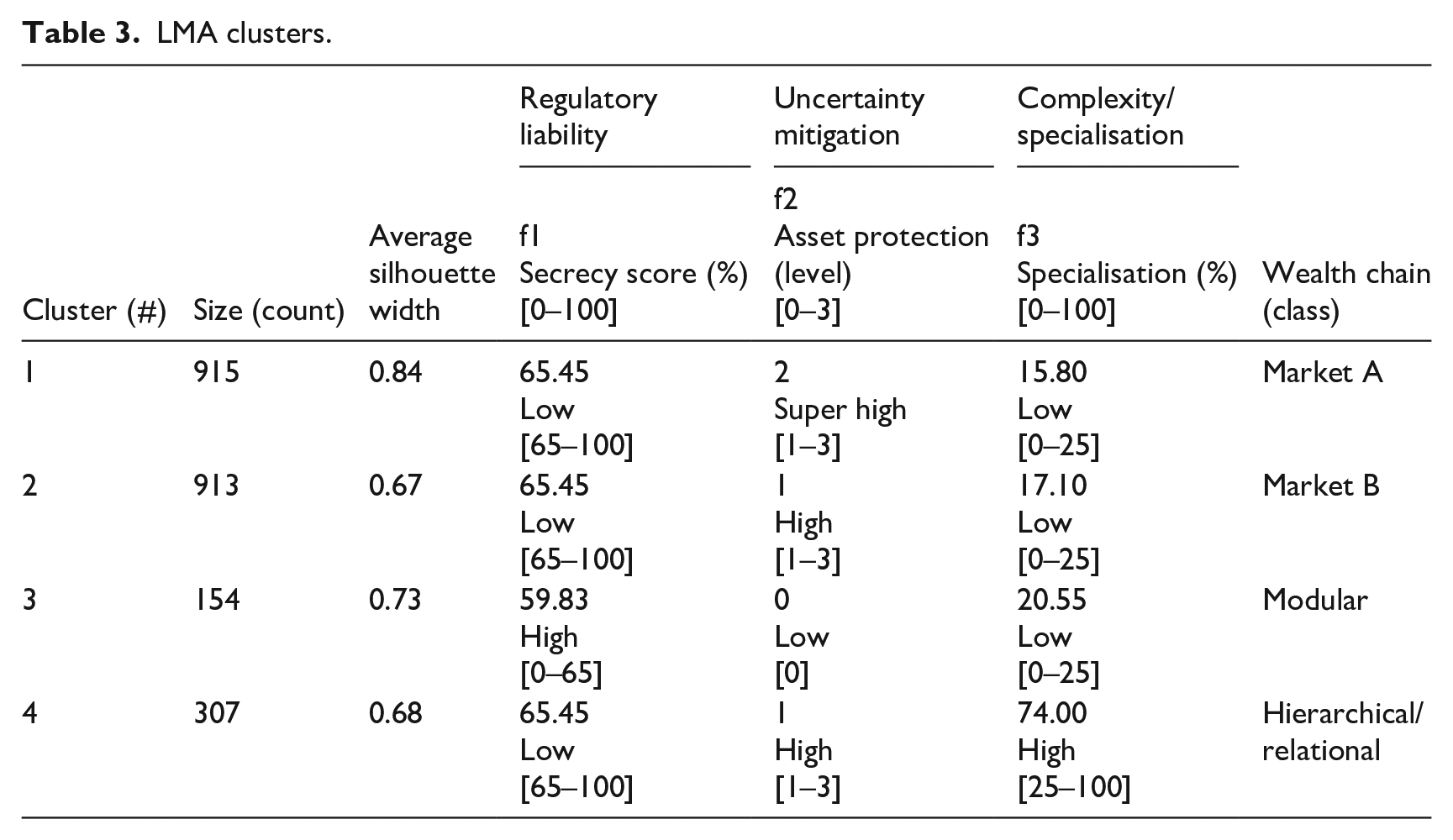

Having operationalised the global wealth chain typology by building the aforementioned three key theoretical assumptions into the workings of our PAM k-medoids algorithm, the algorithm selects a dissimilarity metric (with k = 4), forming compact and separated clusters. Median values of features f1, f2 and f3 for each cluster are reported in Table 3, where we use combinations of these features to label each of the four clusters identified by the PAM algorithm. In our construction, jurisdictions with high secrecy scores, ranging from 65 to 100 on the secrecy index scale, are assumed to have low regulatory liability risk. The ability to reduce uncertainty is associated with high levels of asset protection [1–3] and low product and service complexity is associated with low levels of specialised investments with a maximum share of either student or retirement-age population in the range [0–25].

LMA clusters.

Clusters 1, 2 and 4 have low regulatory liability because their secrecy scores of 65.45 are high (>60). Cluster 3 alone has high regulatory liability risk with a low secrecy score of 59.83 (<60). Also, as shown in Table 3, clusters 1, 2 and 4 have the capability to achieve a high degree of uncertainty mitigation because they have high asset-protection scores. Only cluster 3 has a low capacity to ensure uncertainty mitigation.

Under complexity/specialisation, clusters 1, 2 and 3 record low scores (between 0 and 25) and cluster 4 alone records a high score of 74.00. Table 3 also records average silhouette width (goodness of fit) and the wealth-chain classifications of clusters 1 to 4. Our classifications involve clusters 1 and 2 (market A and its variant market B), cluster 3 (modular) and cluster 4, a hybrid form (hierarchical and relational).

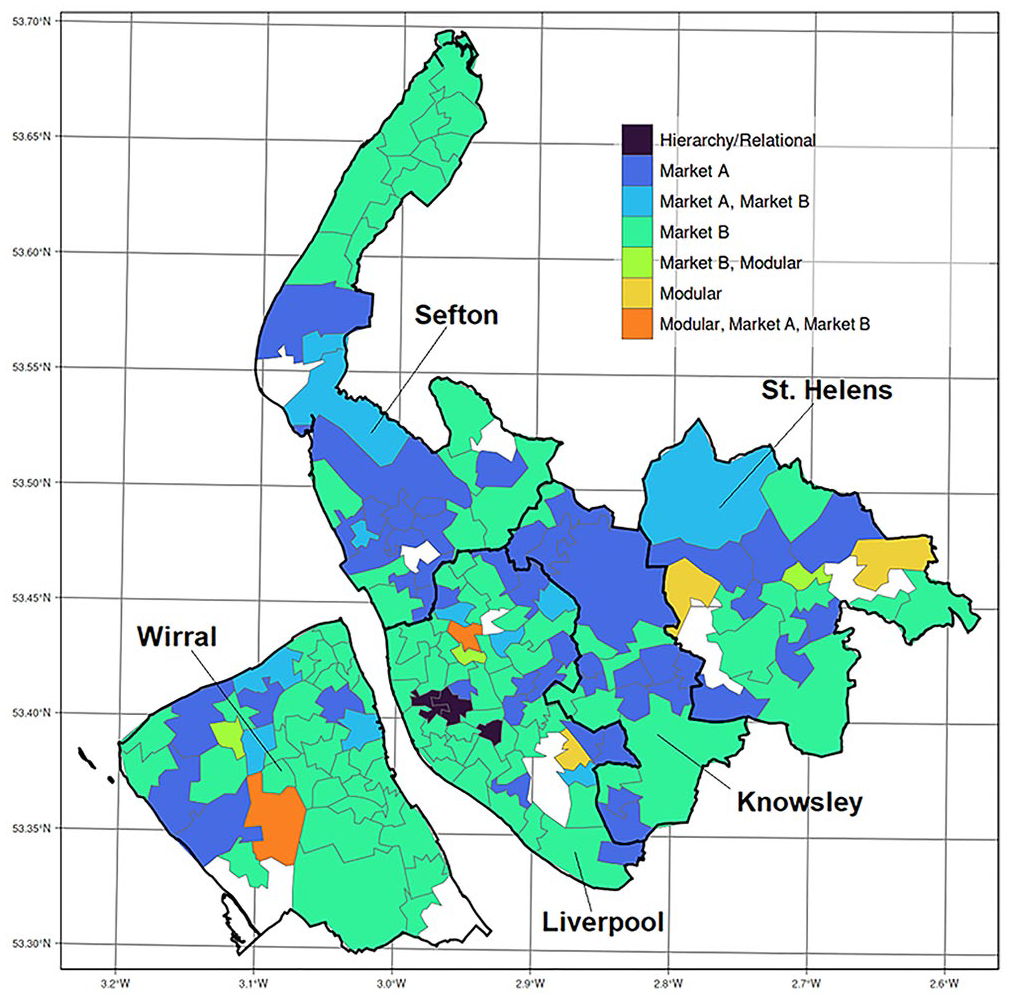

The clustering process revealed no captive wealth chains in the LMA but it did reveal modular wealth chains in the Wirral, St Helens and Haydock (coloured brown in Figure 1). We know that ‘modular forms of global wealth chains are commonly well-established schemes used by the “mass affluent” in national middle classes and transnational and expatriate communities’ (Seabrooke and Wigan, 2017: 13).

Asset strategies across the Liverpool and Merseyside area.

Typically, modular wealth chains are subject to reporting requirements with a ‘clear antimoney-laundering agenda’ (Seabrooke and Wigan, 2017: 13). Here, as Seabrooke and Wigan (2017) observe, the governance of these wealth chains stems from a lack of political will rather than capacity.

Geographical distribution of asset strategies

Figure 1 shows the geographical distribution of wealth-chain asset strategies in operation across Liverpool and Merseyside. By volume, the market wealth chain and its variants dominate in the region. In Seabrooke and Wigan (2017), assets in market chains relative to other types of wealth chain are simple, undifferentiated and readily available, with a great deal of price competition among suppliers. Here, the informational distance is a result of the supplier’s ability to act as a buffer between the client and the regulator. Should the buffer prove ineffective, the main strength/advantage of the market wealth chain is its ability to relocate titles and assets to other offshore jurisdictions. Figure 1 shows that the market wealth chain dominates across the LMA. Markets A and B are subcategories/variants of the market wealth chain defined by Seabrooke and Wigan (2017). In theory, both would operate in market segments characterised by low regulatory liability and low complexity. Theoretically, these wealth chains (along with the hierarchical–relational form) have a greater capacity than other wealth chains to mitigate uncertainty.

The most important attribute of the market A variant is that it offers super-high mitigation of uncertainty capabilities. In other words, the level of asset protection is formidable, with the market A variant’s extensive use of trusts and other SPVs. This raises questions relating to the determination of what Seabrooke and Wigan (2017) call the continuum (ranging from left to right) of explicit coordination. The market wealth chain stands at one end of a continuum of explicit coordination. At the other end of the continuum lies the hierarchical wealth chain where highly complex products are often tailormade for clients or developed in-house. Hierarchical wealth chains are associated with the multinational corporations that use complexity to shroud their transactions, while taking advantage of their geographical and juridical mobility. By contrast, market wealth chains centre on simple products and suppliers and clients have a clear idea of the goods offered for exchange. Our results raise the spectre of uncoordinated, simple, atomistic chains offering greater asset protection than the tightly run, intensely coordinated and highly complex tax-planning operations of contemporary corporations. In order to explain this slightly curious result, we suggest that, when considering asset protection, the competitive advantage derived from the ability to transfer titles between jurisdictions appears to be on a significant scale. Here, the key asymmetry seems to be the informational distance between the supplier and the regulator, which is much greater in both the hierarchical–relational hybrid and market wealth chains than in the other chains. This possibility prompts a re-examination of the idea that innovation is driven by the complex end of the explicit coordination continuum. The existing theory posits that innovation is associated with the capacity to dominate the market that is derived from greater know-how found in hierarchical wealth chains of the MNC. This result suggests that significant innovation may also originate at the simple, uncoordinated end of the continuum.

Another key outcome is the identification of a hybrid hierarchical–relational wealth chain located in and around the city centre (coloured dark blue in Figure 1). The hierarchical– relational wealth chain that we see most clearly in Liverpool city centre is a hybrid form that, according to Seabrooke and Wigan, is vertically integrated and involves explicit coordination among clients and suppliers who are also well integrated. As this type of wealth chain involves exchanges of complex information (Seabrooke and Wigan, 2017: 11), we connect the empirical wealth chain to real-world corporate entities involved in the regeneration projects and the substantial increase in PBSA (Mulhearn and Franco, 2018) in or near the city centre. We know from other researchers (notably, Palan et al., 2010) that the Isle of Man provides specialist services for the alternative investment industry which serves investment funds in the PBSA sector. We suggest that this money has played an important role in the construction of the built environment in and around the city centre.

The clustering process revealed no captive wealth chains in the city region, but it did identify modular wealth chains in the Wirral and Haydock in St Helens (coloured orange in Figure 1). The suggestion here is that there are modular areas where ‘well-established schemes [are] used by the “mass affluent” in national middle classes and transnational and expatriate communities’ (Seabrooke and Wigan, 2017).

Overall, we observe the dominance of the market asset strategy with the identification of a hierarchical–relational hybrid strategy that lends empirical support to the theoretical claim that ‘the five global wealth chain types are not silos but [are] often mixed in the articulation of wealth chains’ (Seabrooke and Wigan, 2017: 17).

Conclusion

The benefit of using the concept of wealth chains is its ability to help discern the geographical distribution of asset strategies deployed by investors from offshore. We are able to isolate key aspects of these processes to help us see the different approaches to offshore investment in the region and the city. The key message of our work is that the asset strategies deployed across the city region are associated with large companies that use tax haven registrations to minimise costs (and expand net worth) by engaging in taxation arbitrage (Muasya, 2018, McKenzie and Atkinson, 2020; Palan et al, 2010, Shaxson 2011) between jurisdictions (hierarchical–relational wealth chain), alongside other actors who aim (above all else) to conceal and hide the real identities of the beneficial owners (market wealth chain).

While the strategies employed to avoid or evade tax obligations may or may not be formally illegal, they all generate social harm and are therefore significant in social and political terms. In our modelling, tax-evasion and tax-avoidance practices expand wealth inequalities, particularly by enabling weakened consumer purchasing power.

We suggest that there is a need for further studies aimed at fleshing out the empirical manifestation of the concept of global wealth chains, so that we may better discern asset strategies on the ground in specific locations. Analytically, the motivating force for the proliferation of wealth-chain types in the Liverpool City Region appears to be asset protection and it is here that we believe the research work might be concentrated. In particular, the influence of the capacity to mitigate uncertainty, asset protection and secrecy in the determination of the distribution of levels of coordination among the types of wealth chain offers a useful direction for future work aimed at developing the theory of wealth chains.

The significance of our analysis can be identified in three particular contributions. First, our work highlights how the use of official data can enable important insights into the types of strategy being deployed by offshore investment centres. This is a major advance in our understanding of the dynamics of such investment. Second, the evaluation of such strategies alerts us to the potential impacts of such investment and the range of possible risks in deprived city-region contexts. Given that the market form of wealth chains predominates in offshore investment in Liverpool, we can begin to consider the types of public policy setting required to dampen or disincentivise such approaches. Finally, our work shows that innovative approaches may be found to help close the empirical gap facing urban and regional property-based research involving the offshore world, and that asymmetries between communities and investors benefiting from anonymity may begin to be addressed in critical research.

Footnotes

Appendix

Harrington’s special purpose vehicles (SPV’s) schema.

| Trusts | Foundations | Companies | |

|---|---|---|---|

| Primary purpose | Holding and distributing wealth in the best interest of the beneficiaries | Holding and distributing wealth for charitable purposes (offshore, may be used for private benefit) | Trading and commerce; maximisation of shareholder value |

| Ownership | Divided between beneficiaries and trustees; trustees compensated | Foundations own the assets they contain | Shareholders, who pay for shares and may lose the capital they invest |

| Legal status | Not a legal entity, but a private agreement; recognised only in common law countries | Separate legal entity recognised worldwide | Separate legal entity recognised worldwide |

| Management | Trustees | Councillors | Directors |

| Tax liability | Trustees liable for tax on income from trust assets, beneficiaries liable for tax on distributions (offshore, taxes may be reduced or eliminated) | Subject to income taxes (offshore, taxes may be reduced or eliminated) | Income taxed twice: once at corporate level, and again when distributed to shareholders (offshore, taxes may be reduced or eliminated) |

| Asset protection | Trust assets inaccessible to creditors and litigants; trusts cannot go bankrupt | Foundation assets may be attached by creditors and litigants; foundations can go bankrupt | Corporate assets can be attached by creditors and litigants; corporations can go bankrupt |

| Privacy | No registration: name of trustee may be public record in some jurisdictions, but identities of beneficiaries remain secret | Foundation assets may be attached by creditors and litigants; foundations can go bankrupt | Corporations must be publicly registered disclosing names of directors and shareholders (offshore, nominees may be used) |

| Compliance costs | Few to no reporting requirements or limits on liquidity and distributions | Required financial reporting plus mandatory minimum distributions (offshore, these rules may be loosened) | Required financial reporting plus limits on liquidity and distributions (offshore, these rules may be loosened) |

| Ease of migration | Relatively easy and low-cost to move a trust from one jurisdiction to another 9offshor, automatic with ‘flee clauses’ | More difficult and costly to move a foundation from one jurisdiction to another | More difficult and costly to move a corporation from one jurisdiction to another |

| Time limitations | Subject to rule against perpetuities (offshore, rule has been eliminated | None | None |

Source: Harrington (2016: 186–187).

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.