Abstract

In California, wildfires caused by electrical infrastructure have left the state’s investor-owned power utilities with major and growing liabilities. But even in such an incendiary environment, the financial industry has demonstrated that it can profit from disaster. This paper uses the 2019-2020 bankruptcy of Pacific Gas & Electric to explain how. In it, I show how “risk” in California’s electricity industry is legally constituted, mediated, and allocated. First, I explain how financial perceptions of wildfire risk in California’s electricity industry are shaped by the state’s legal and regulatory environment, and how the law is used to manage this risk. I then turn to PG&E’s bankruptcy to show how litigation functions as a financial strategy. In court, risk is endogenous to legal-financial practice. I develop the concepts of “legal arbitrage” and “leverage” to explain how law mediates the relationship between risk and finance. I adapt the concept of legal arbitrage to show how financial assets (like those in a utility with unprecedented wildfire liabilities) can possess both legal and market value, which can and often do diverge in circumstances of distress. I use the term leverage to refer to a particular kind of legal-financial power which enables actors to transfer risk away from themselves and onto others. In working through these concepts, I argue that that mainstream perceptions of risk in the financial industry are inadequate, especially in an era of increasing climate insecurity.

Keywords

Introduction

In the fall of 2017, 21 major wildfires and over 200 smaller fires tore through Northern California. Sixteen were caused by infrastructure owned and operated by the utility Pacific Gas & Electric (PG&E). A year later, a century-old transmission line in PG&E’s service area ignited the Camp Fire—the deadliest and most destructive wildfire in the state’s history to that point. Facing liabilities potentially exceeding $30 billion associated with these and other wildfires, PG&E filed for Chapter 11 bankruptcy on January 29, 2019. 1

Like California’s other investor-owned utilities (IOUs), PG&E is increasingly beset by catastrophic wildfire risk. Its vast service area spans the northern half of the state, including the fire-prone Sierra Nevada range. Increased aridity, attributable to a warming trend that conforms to models of anthropogenic climate change, has contributed to a fivefold increase in the annual acreage burned by wildfires in California between 1972 and 2018 (Williams et al., 2019). This long-term drying trend combines with decades of total fire suppression to create tinderbox conditions in PG&E’s service area. Centrifugal urban expansion into the so-called “wildland-urban interface” then lights the match, putting property and human life at risk (Simon, 2018). Wildfires caused by a utility’s powerlines are moreover disproportionately large and destructive, because the weather conditions that cause infrastructure failure are also conducive to rapid wildfire spread in places where people live (Office of Planning and Research [OPR], 2019).

Despite PG&E’s unprecedented wildfire liabilities and the seemingly intractable confluence of risks it faces, a parade of hedge funds and other financial firms quickly became involved in the unfolding legal drama surrounding its bankruptcy. In fact, PG&E’s wildfire-induced distress represented a unique opportunity for financiers to profit in court.

PG&E’s was the largest corporate bankruptcy since the 2008 financial crisis, and attracted many so-called “activist” investors experienced in litigation as a financial strategy. At least twelve of the fifty largest hedge funds ranked by assets under management at the time became involved in the company’s protracted restructuring process, entering the courtroom as shareholders (owners of PG&E stock), bondholders (owners of PG&E debt), or subrogation claims holders (owners of insurance claims against PG&E).

There they were joined by the firm’s other creditors, including the thousands of wildfire victims who at the time of PG&E’s bankruptcy had already filed approximately 750 individual and class action complaints against the utility in civil court. PG&E’s declaration of bankruptcy not only froze these wildfire liabilities, but also unlocked billions of dollars in interim financing, and enabled it to roll the numerous tort claims against it into a single restructuring process. “Chapter 11 reorganization,” its board wrote, would allow PG&E to work with each of its constituencies, from bondholders to wildfire victims, “in one court-supervised forum to comprehensively address its potential liabilities” amidst a “challenging liquidity situation.” 2 Addressing its potentially unprecedented wildfire liabilities in bankruptcy court, rather than through a series of civil suits, brought a host of financial actors with extensive professional and technical experience into the process. Their claims and the tort claims of PG&E’s wildfire victims became a single set of outstanding liabilities, stratified by the rules of creditor priority set forth in the U.S. bankruptcy code and to be addressed with a single corporate “Plan of Reorganization.”

For the financial firms seeking value amidst the rubble, the utility’s exposure to catastrophic wildfire liability created a unique arbitrage opportunity which could be leveraged for profit in the courtroom. The case therefore presents us with a novel example of the entanglement of both financial and socionatural risk, and the function of law in mediating both of these forms of risk within a broader context of increasing climate insecurity and widespread infrastructural breakdown (on which see Anand et al., 2018; Cutter, 2021).

Within Environment and Planning, scholars have begun to explore “electricity capital” as the “nexus of state, regulatory, and financial relationships that shape private accumulation through electricity provision” (Luke and Huber, 2022: 1700). This paper contributes by bringing legal specificity to this “nexus of relationships” to demonstrate how law functions to distribute risk and value in the electricity industry amidst persistent ecological crisis. Though it represents a specific confluence of legal, financial and socionatural risks as they emerged in California in the aftermath of two of the state’s worst fire seasons on record, the case described here has broad relevance for research into the ways climate costs will be mediated and contested through existing legal, regulatory, and financial systems. This is especially true within the United States’ electricity industry, where public utility law determines what costs IOUs can recover from their ratepayers—and for whom “accumulation by regulation” thus remains a foundational profit-making activity (Harrison, 2020). I am also here responding to Christophers’ (2015, 2018) calls for further research into the concrete forms of risk that finance produces, mediates, and profits from, and hope to illustrate the often-crucial role of law in these processes. Financial actors tend to treat risk as something quantifiable and external, and profit as the reward for accepting this risk. At the intersection of finance and the law, however, this form of financial self-understanding is inaccurate. Instead, legal and regulatory systems function as arenas in which risk is actively produced, allocated and contested. The specific power of finance in these situations is to take advantage of the tools of law to proactively transfer or minimize the risk to which it is exposed.

In what follows, I make several interrelated empirical and theoretical arguments. First, financial perceptions of wildfire risk in California’s electricity industry are shaped by the state’s legal and regulatory environment. Second, the law has likewise offered avenues for the state to appease market actors that assess and price this risk by introducing mechanisms meant to broadly socialize it. Third, bankruptcy court is a legal space in which concrete strategies of financial accumulation play out. These strategies exploit the divergence between what I describe as the “legal” and the “market” value of financial assets associated with a restructuring entity. I therefore develop the concept of “legal arbitrage” to describe how investors in distressed securities take advantage of the law to maximize returns from the assets they acquire on the market. Fourth, exposure to risk is determined by legal and financial power. One name for this power is “leverage” (cf. Konings 2018). I argue that both PG&E, the largest IOU in the United States, and the financial firms that invested in it possessed this kind of leverage, which enabled them to actively direct and distribute financial and risk-related outcomes within and beyond the firm’s bankruptcy.

As a case study, the PG&E bankruptcy resembles any number of distressed asset plays that blur legal and financial strategies—including other corporate Chapter 11 cases (on which see Ivashina et al., 2016; Jiang et al., 2012) or sovereign debt litigation (Potts, 2017). But it is unique because of the particular risks, and the particular “risk constituencies” (Christophers et al., 2020), it assembles, and the opportunities for leverage that exist for these constituencies within their specific courtroom context.

Though financiers took opposing sides in the PG&E bankruptcy, the goal of this paper is not to evaluate the success or failure of particular legal-financial strategies. While I will explore the differences between PG&E’s various investors, the bankruptcy of California’s largest utility was a coup for “finance” in toto, generating (comparatively risk-free) fee and spread opportunities for all the financial firms that participated. At the same time, thanks to contemporaneous changes made to California’s energy law, PG&E’s wildfire risk exposure has along with the state’s other IOUs migrated outward, to its ratepayers, and the resolution of its bankruptcy process left those victimized by fires the utility caused facing substantial equity risk.

I draw from state legislative material, regulatory public utility rulemaking, relevant litigation and corporate financial disclosures to contextualize the PG&E case. But the empirical backbone of my argument comes from the voluminous docket associated with the bankruptcy itself, which comprises thousands of filings between 2019 and 2023. This methodological choice—to focus intensively on a single litigation process as it unfolds—is useful for two reasons. First, and more narrowly, quite a bit of useful financial data can be found in the numerous filings litigants make in particular cases, which offer a picture of the networks of actors involved in distressed investment and changing extent of their financial exposure over time. Second, and more broadly, this approach gives insight into the ways law is understood and instrumentalized in concrete forms of legal-financial practice—and therefore into the legal terrain of finance itself.

In this paper, I will first briefly sketch the PG&E restructuring process, identifying some of the major actors and outlining the company’s path out of bankruptcy. I then situate this case within the relevant literature on the legal constitution of finance and introduce the relationship between risk, leverage and arbitrage. Next, I will describe the function of California energy law and policy in structuring both the risk and value of the financial assets associated with its electric utilities. I then return to the PG&E bankruptcy to further develop my concept of legal arbitrage. Finally, I use the example of a dispute between the company’s debt and equity investors to show how configurations of leverage shaped the distribution of risk within the courtroom, before concluding with some tentative thoughts about the relationship between law, finance, politics and risk in an era of widespread and increasing climate insecurity.

The bankruptcy of Pacific Gas & Electric

Distressed investment in PG&E notably increased following the 2017 Northern California Wildfires, with approximately 19% of the company’s equity held by hedge funds in Q3 2018, up from only 3.4% the year before (Chung and Friedman, 2019). These financiers were making the calculation that the 2017 wildfire season was a “special situation” that temporarily lowered the value of the assets associated with a firm that was fundamentally solvent—and that the state of California would not let fail.

As I will show below, this calculation was in many ways prescient—anticipating the decisions taken by the state to prop up its electric utilities. But the scope of PG&E’s wildfire liability dramatically expanded when, in November 2018, its infrastructure ignited the Camp Fire, destroying the town of Paradise and leaving 86 dead. At this point, PG&E’s market capitalization further disintegrated and the financial firms that had bought into the utility over the prior year were faced with the choice of either exiting their positions at a loss or seeking out other ways to salvage their investment.

PG&E’s bankruptcy declaration two months later offered just such an opportunity for financial firms willing to follow the company into court. There they were joined by other hedge funds with prior experience in restructuring litigation. After entering bankruptcy, the value of PG&E’s equity fell precipitously from $24 to $6 per share (Wirz, 2019). Its outstanding bonds were likewise discounted by as much as 25% (Chung and Friedman, 2019). Meanwhile, many insurers that had the right to sue the utility for payments that they had made to policyholders in the aftermath of wildfire events elected to sell those rights at a discount to avoid the potentially protracted bankruptcy process.

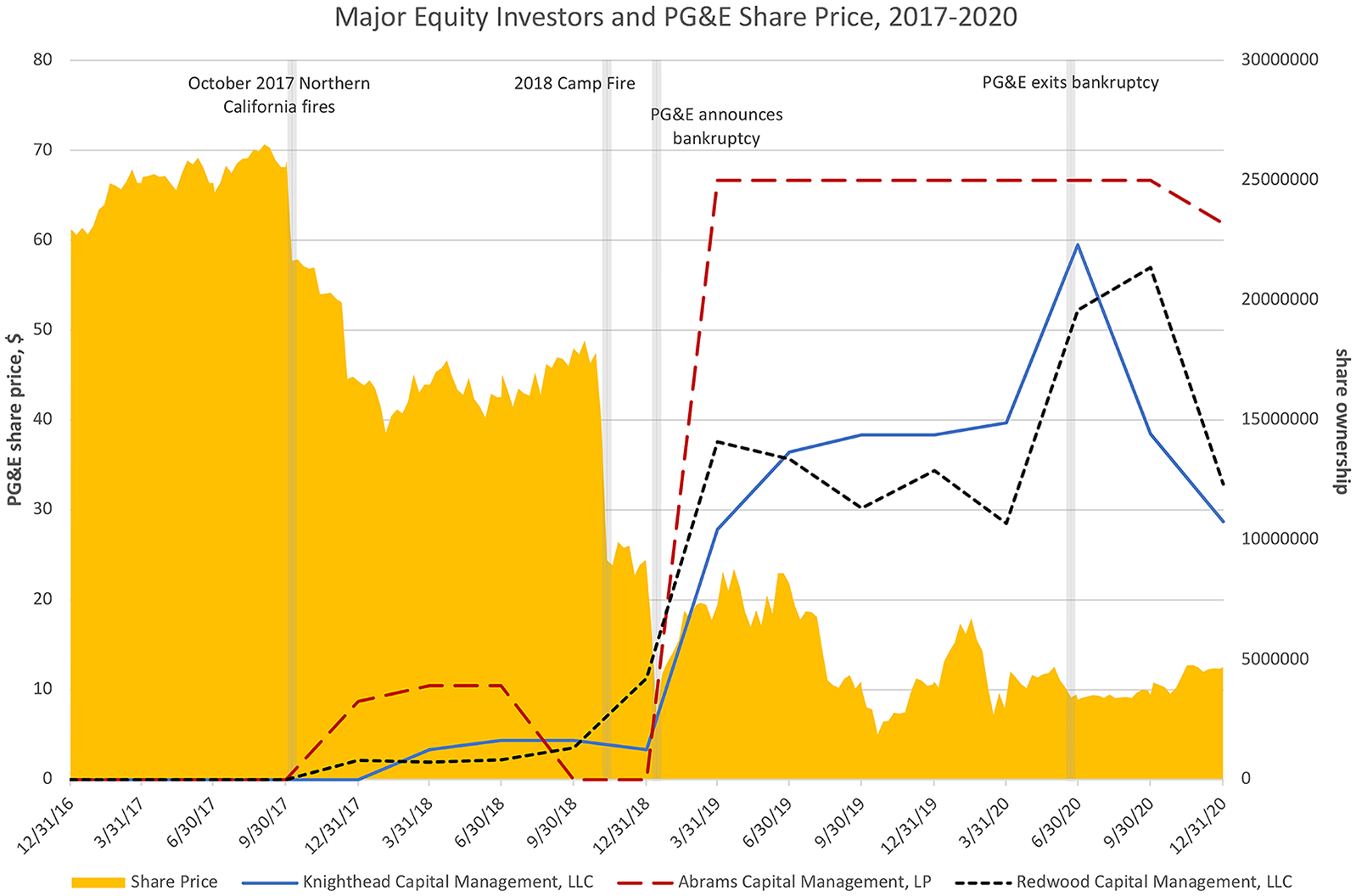

As prices fell, these assets became concentrated in the hands of financial firms enticed by what I describe here as the arbitrage opportunities offered by bankruptcy litigation. On the equity side, SEC filings show a triumvirate of hedge funds—Knighthead Capital Management, Abrams Capital Management, and Redwood Capital Management—collectively acquiring nearly 10% of the company’s outstanding shares in Q1 2019 (Figure 1). On the debt side, the “Ad Hoc Committee of Senior Unsecured Noteholders,” a constituency of investors led by Elliott Management Corporation and PIMCO, purchased $11.2 billion of the firm’s outstanding bonds over the course of its bankruptcy. 3 Meanwhile, The Baupost Group, a Boston-based financial firm, hedged the 4.6% of PG&E’s outstanding common stock it had acquired in the lead-up to the firm’s bankruptcy with 23% of the outstanding insurance claims against the utility, 4 purchased from insurers at rates as low as 35 cents on the dollar (McDonald and Chediak, 2020).

Major equity investors and PG&E share price before, during, and after its bankruptcy.

Early on, the interests of PG&E’s debt and equity investors began to diverge around two competing plans to reorganize the firm. Major shareholders like Knighthead, Abrams and Redwood developed a plan that would restructure PG&E’s debts while preventing the stock they possessed from becoming valueless. Bondholders like Elliott and PIMCO, meanwhile, put forth their own plan, which would have maximized their return on investment by transforming them into majority shareholders upon the company’s emergence from bankruptcy. The bondholders enrolled wildfire victims to their cause by promising them a larger settlement than the company itself had initially put forth. To dispel this competing bondholder proposal, PG&E and its shareholders matched the amount it offered to wildfire victims—though, importantly, this matching offer was funded through a combination of cash and company shares, passing along a new form of equity risk to those who had been victimized by fires it caused.

Nevertheless, the offer was enough to secure the support of the wildfire victims’ legal counsel, who withdrew their support for the bondholders’ competing plan in December 2019. PG&E, having already reached an agreement with those who held insurance claims against it, then settled with the bondholders themselves in January 2020, who had lost the original momentum behind their competing plan and agreed to let the company refinance its debts. In March, the governor of California announced his support of PG&E and its shareholder’s plan. The firm exited bankruptcy on June 20, 2020.

The legal constitution of finance

This brief account fits neatly into a growing body of work within and beyond economic geography that has come to recognize that “there is no ‘outside’ the legal in contemporary capitalism” (Knuth and Potts 2016: 458). This is especially apparent in the world of finance, which deals in contracts whose “value. . .depends in large part on their legal vindication” (Pistor, 2013: 2). So too is the very existence of specific markets often a function of legal design. Law generates assets by, for example, “unbundling” and rendering saleable property rights for conservation purposes (Kay, 2016) or by creating fiscal and tax incentives that induce private investment in arenas as disparate as historic building preservation, conservation easements, and renewable energy infrastructure (Kay and Tapp, 2022; Knuth, 2021). Markets in distressed securities are likewise produced by law. It is the specter of bankruptcy and nonpayment that drive up yields as distressed assets are discounted. And while some “passive” distressed investors are making the bet that the entity in which they invest will avoid bankruptcy, the most sophisticated and potentially profitable strategies involve intervening directly in the bankruptcy process to realize returns. This is possible because bankruptcy court, while formally rule-bound (cf. Pistor, 2013), is a site of contestation between litigants (e.g. a firm and its various creditors). The outcome of a bankruptcy is not predetermined by doctrine but actively negotiated between (and fought over by) those party to it. It is the possibility of manufacturing an advantageous legal outcome that makes the “activist” vulture fund strategy tenable.

In bankruptcy, judges adjudicate between “competing claims to the same assets” (Pistor, 2019: 3). When a firm enters bankruptcy, it no longer considers itself capable of honoring all of the claims others hold against it. “Restructuring” means determining who gets what and whose claims get written down or written off. The bankruptcy code establishes priority, situating creditors over shareholders; creditors secured by collateral over unsecured creditors; and “senior” unsecured creditors over “junior” unsecured creditors. In PG&E’s bankruptcy, the firm’s tax, employee compensation, and lien-secured creditor obligations were situated at the top of this hierarchy, while its tort claimants (i.e. wildfire victims) occupied an intermediate position alongside the firm’s new bondholders, who had mostly acquired senior notes unsecured by collateral. The shareholder funds that bought low on PG&E’s stock had least priority, but their successful ability to guide the company through the bankruptcy process meant that the value of their equity was nonetheless preserved.

In this way, bankruptcy establishes an elaborate hierarchy in relation to an unfolding legal event. But the specific actors who occupy positions within this hierarchy can and often do change over the course of a bankruptcy. Secondary trading in distressed asset markets enables financial actors to secure exposure to and the ability to actively participate in a restructuring process. The law is thus a resource for concrete strategies of financial accumulation (Potts, 2020). For some financial economists, distressed securities have “matured into a genuine asset class” (Altman and Benhenni, 2019: 22)—blossoming countercyclically in the aftermath of economic crisis as credit dries up and firms and sovereigns begin to face default. Hedge funds, which justify their high-fee structures with the promise of “absolute return” uncorrelated with broader market swings, are thus prolifically involved in both public and private debt litigation—perhaps as much as 90% of the time in corporate Chapter 11 cases (Jiang et al., 2012)—in what is estimated to be a $300 billion a year industry (Velchik and Zhang, 2019).

Risk, leverage and arbitrage

The hedge funds that participate in bankruptcy litigation often present themselves as sophisticated legal operators whose above-average returns flow from an appetite for taking on credit and default risk. Indeed, finance more broadly is often represented as a professionalized and technically complex arena of calculable risk-taking (de Goede, 2004). Yet concrete financial practice belies this self-image. Financiers are, in fact, adept at minimizing the risk to which they are exposed by “systematically transferring it to counterparties” (Christophers, 2015: 6). Moreover, as Christophers and Niedt (2016) have suggested, “The law figures. . .as a crucial field where value and risk outcomes are rendered negotiable and are, accordingly, contested and (re)produced” (487).

Two financial concepts, arbitrage and leverage, can help us better understand the distribution of risk within the courtroom. Both words have technical definitions. Leverage refers to the act of borrowing money to multiply exposure to and by extension the potential returns from a particular financial position. Arbitrage is the process of exploiting price discrepancies across markets. In financial practice, both leverage and arbitrage are central conceptual and practical categories. But their limited academic definitions do not fully capture the financial attitude toward risk implied by each. I mobilize them here to illustrate how the law enables the exercise of a specific form of legal-financial power (leverage)—and how access to this form of power in turn enables financiers to systematically avoid risk (arbitrage).

Arbitrage is the opposite of risk-taking in finance. Unlike traditional investments, which are putatively governed by calculable future risks, the logic of arbitrage is fundamentally about synchronism (Langenohl, 2018). Arbitrage opportunities allow financial actors to buy low in one market and immediately sell high in another. This combination of simultaneity and difference enables profits that are (virtually) “risk-free.” Economists emphasize the rare and ephemeral nature of arbitrage—not only is it difficult to locate identical assets circulating at two distinct prices in (increasingly globalized) markets, but, over time, executing arbitrage trades should eliminate the arbitrage opportunity itself as efficient markets equilibrate in response.

In practice, however, “arbitrage” does not refer exclusively to price spreads on identical assets; rather, the concept relates to “products that are construed as comparable in their market risk exposures” (Langenohl, 2018: 29, emphasis added). Thus the meaning of arbitrage in financial practice is more capacious than its textbook definition would suggest (Miyazaki, 2013), and it is “not a fleeting, marginal aspect to financial trading, but the central form of financial profit making that firms pay dearly to engage in” (Hardin and Rottinghaus, 2020: 120). The ubiquity of what many financial actors informally describe as arbitrage indicates in this way a risk-minimizing behavior that orients many discrete kinds of financial activity.

The underlying logic of arbitrage as a riskless (or risk-minimal) profit operation that exploits simultaneous difference expands further still when financiers (and their critics) refer to things like “labor arbitrage,” “merger arbitrage,” and “legal” or “regulatory” arbitrage. “The economic genius of arbitrage,” Riles (2014) writes, “is that the similarity and the difference [it seeks out] can be of virtually any kind” (p. 72). As I will explain using the example of the PG&E case below, the value of financial assets can vary depending on social context. An asset may deteriorate in value on the market while still retaining value in a courtroom. I characterize the attempt to take advantage of this spread—between “legal” and “market” value—as a strategy of “legal arbitrage.”

This kind of legal arbitrage is not just about reacting to a special situation in the market—for example, identifying a spread between the price of an asset during a crisis versus in normal circumstances. Rather, it involves using the law to manufacture a particular financial outcome. The success of this strategy depends upon the arbitrageur’s power in the courtroom. I call this power “leverage.”

As mentioned above, in technical terms leverage describes borrowing to amplify returns. Hedge funds are masters of leverage in this sense, with “leverage ratios [that] are on average 4 to 5 times the value of their AUM [assets under management]” (Sgambati, 2022: 11). But Konings (2018) usefully approaches the concept of leverage in a less restrictive way. Writing about the power of highly leveraged financial actors to enroll the state into ensuring their continued survival in moments of economic crisis, he argues that “leverage is not just about increasing my exposure to the world, but about increasing the world’s exposure to and investment in the risk that I am taking” (Konings, 2018: 16). In other words—as colloquial use of the word suggests—leverage is about establishing a position of social centrality to gain an advantage. Thus once a bank has positioned itself as a key part of the infrastructure of social life at large, its failure or merely the threat of it will activate forces that seek to secure it. . .To say that leverage allows financial institutions to expose society to the risk they take on means that they are in a position to shift risk away from themselves and onto others. (Konings, 2018: 18)

Even beyond the “too big to fail” operators that Konings describes, this concept of leverage is useful for understanding configurations of financial, corporate, and legal power in general, and in the PG&E bankruptcy in particular.

First, it complicates simple creditor/debtor dichotomies and the tendency to treat financialization as the mere expansion of creditor power. This may be true in particular contexts—for example, in sovereign debt restructurings (Potts, 2017), or mortgage markets (Ashton, 2014). But debt and leverage, too, can confer power. Like much in the world of corporate finance, the dynamics of PG&E’s bankruptcy are not captured by notions of creditor supremacy and debtor subordination. PG&E’s creditors included not only activist hedge funds leveraging their investors’ money, but also individuals who held claims against the utility for wildfire damages and who constituted a class of “involuntary creditors.” PG&E’s path out of bankruptcy, as we will see, required leverage as well—both in the restricted sense of taking on additional debt, and in the more expansive sense of leveraging its position within the “infrastructure of social life” as the sole provider of electricity to much of California.

The concept of leverage also illustrates the relational quality of legal-financial power. Power in a legal context cannot be understood apart from “the way in which law positions us relative to others” (Blomley, 2020: 38). Understood more specifically as leverage, power is an effect of the density of connections a particular entity has formed within a given sociolegal context. Established legal hierarchies matter here, but so do claims to social centrality and the investment you are able to induce others to make in your financial position. This logic is captured in financial rhetoric, which often describes the best places to exert leverage over a distressed firm in bankruptcy court as “fulcrum” positions (Lichtenstein and Carney, 2007). Typically, such positions will be located in unsecured (i.e. noncollateralized) debt, discounted in secondary markets and assumed to be unlikely to be paid in full, giving debt investors considerable influence over restructurings.

Finally, leverage suggests that contrary to mainstream accounts risk is not (or not always) simply exogeneous to finance. Rather, finance produces or “crystallizes” risk through the “issue and circulation of various forms of credit” (Christophers, 2015: 5)—and then actively manages, rather than passively accepting, this risk. Leverage, which “does something to shape the configuration of reality itself” by attempting to create certain (beneficial) outcomes (Konings, 2018: 15), is a form of risk management. In court, exposure (or not) to risk becomes a function of legal-financial power—of the leverage you have. Thus, while losing your home in a powerline-caused wildfire is a (socionatural) risk that can be explained through some combination of climate-induced drought, forest mismanagement, historical patterns of (sub)urbanization, and corporate malfeasance, the risk of being properly remunerated or not for that loss during bankruptcy litigation depends wholly on where you are situated in the complex social universe of leveraging and counterleveraging that emerges in the courtroom.

Structuring risk and value

In what remains of this paper, I show how law determines both the risk and value of electric utilities as vehicles for investment—both in the lead-up to PG&E’s bankruptcy and during the company’s Chapter 11 process.

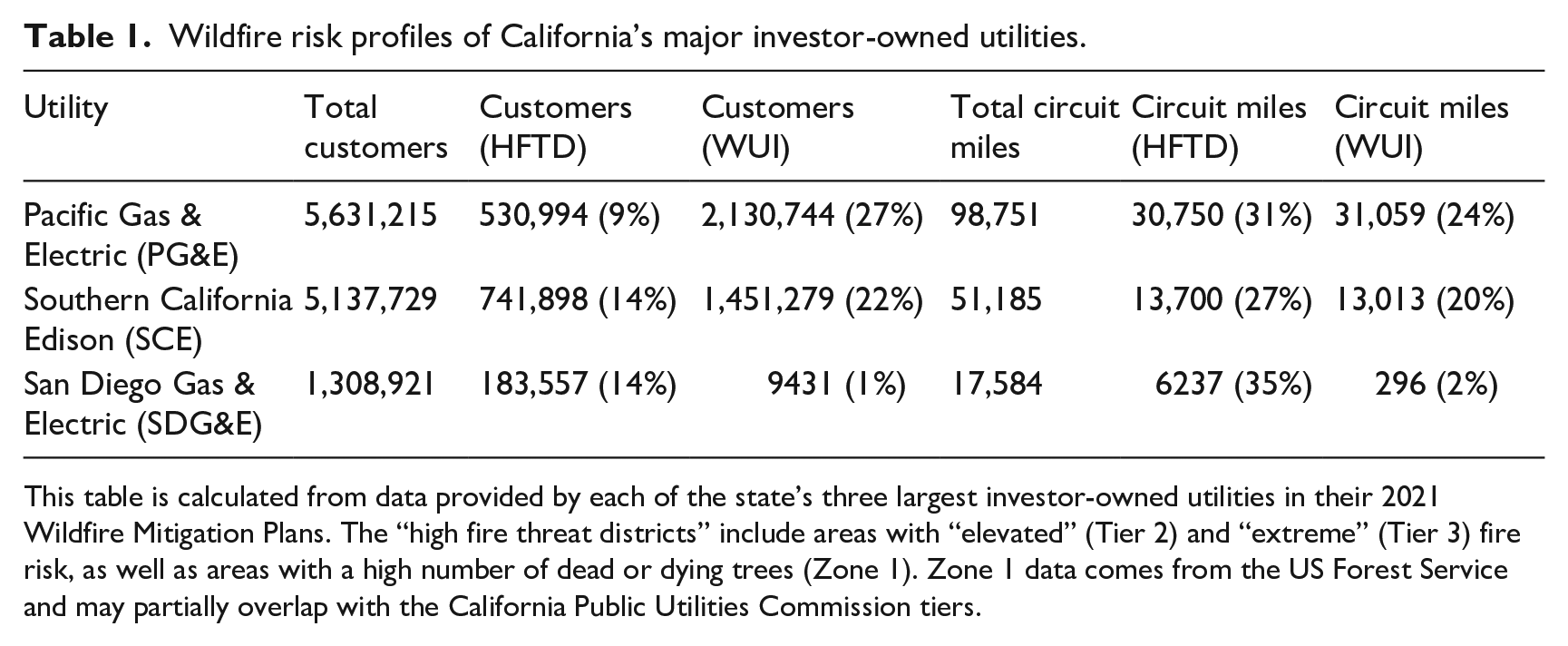

Financial perceptions of risk in California’s electricity sector are influenced by both legal and biophysical factors. Many of the customers and electrical assets of each of the state’s major investor-owned utilities are located in either the combustible wildland-urban interface or what the California Public Utilities Commission (CPUC) deems “high fire threat districts.” Among others, IOU powerlines have been responsible for major fires in 2007 (the Rice, Guejito and Witch Fires), 2015 (the Butte Fire), 2017 (the Northern California Wildfires and Thomas Fire), 2018 (the Camp Fire and Woolsey Fire), and 2021 (the Dixie Fire) (Table 1).

Wildfire risk profiles of California’s major investor-owned utilities.

This table is calculated from data provided by each of the state’s three largest investor-owned utilities in their 2021 Wildfire Mitigation Plans. The “high fire threat districts” include areas with “elevated” (Tier 2) and “extreme” (Tier 3) fire risk, as well as areas with a high number of dead or dying trees (Zone 1). Zone 1 data comes from the US Forest Service and may partially overlap with the California Public Utilities Commission tiers.

This wildfire risk exposure is compounded by the state’s uniquely exacting set of regulatory standards and legal precedent governing utility wildfire liabilities (see, e.g., Kousky et al., 2018; Nagano, 2020; Obeid, 2021). In general, the Takings Clause of the Fifth Amendment requires “just compensation” be paid for any public taking (condemnation) of private property. When a taking occurs without compensation, property owners can sue the public entity responsible for it for recovery under the doctrine of “inverse condemnation.” In California, state courts have given this doctrine particularly broad scope. §19 of California’s state constitution expands the Takings Clause by mandating just compensation not only in the event of a public taking, but also if property is damaged by public use. California courts have interpreted this as implying strict liability for damages caused by public use, even when that damage is caused “neither intentionally nor negligently” and “whether foreseeable or not.” 5 They have furthermore twice extended this strict liability standard to IOUs, reasoning that their status as regulated monopolies providing a public good makes their private ownership structure irrelevant when considering their potential liability. 6 Thus when an electric utility’s infrastructure ignites wildfires that destroy private property, they are subject to the state’s interpretation of inverse condemnation and the strict form of liability it confers.

In short, California’s utilities face high levels of wildfire risk in a strict and expansive liability environment. These risks were already by 2018 being priced in to financial and insurance markets. Massive wildfires have begun to confound the conventional methods available to utilities for mitigating their liability costs through insurance. Since fires in 2007 caused by San Diego Gas & Electric (SDG&E) first exceeded a California utility’s insurance coverage (OPR, 2019: 32), wildfire liabilities have begun to routinely outstrip insurance, while premiums have risen to as high as 40 cents for every dollar of available coverage (Graves et al., 2018: 25). The $4.7 billion incurred by Southern California Edison (SCE) from fires in 2017-18 was nearly five times its insurance policy, while the $30 billion in liabilities estimated by PG&E at the outset of its bankruptcy proceedings exceeded its insurance coverage by a factor of twenty. 7

As I briefly explained above, insurers themselves also have the legal right to “subrogate” against utilities for payments made to policyholders when those utilities are liable for insured damages. The right of subrogation is a standard clause in insurance contracts that allows insurance firms to recover some of their costs when a third party is liable for damages that they have covered. Like bonds and shares, this right is an alienable claim, capable of being sold to financial firms and enforceable in court. Holders of subrogation claims—including both property insurers and, most prominently, the hedge fund The Baupost Group—thus became an important constituency in PG&E’s bankruptcy process. PG&E settled with this group of insurance claims holders prior to reaching an agreement with bondholders and wildfire victims.

But all of this exposure is potentially offset by IOUs’ ability to redistribute their liabilities through rate increases—which effectively transfer risk from the company and its shareholders to its customer base. Under the regulatory model devised by Progressive reformers at the beginning of the twentieth century, regulators determine rates in consultation with IOUs to guarantee a particular rate of profit based on the latter’s fixed capital investments. In exchange for regulation of profits, IOUs were granted exclusive franchises to deliver electricity to predefined service areas. This “utility consensus” (Hirsh, 1999) was envisioned by regulators as a way of protecting consumers from monopoly pricing, but such an arrangement also insulated utility companies from both state takeover and market competition. The spatial barriers it erected in the market and the profits it guaranteed kept interest rates low for electricity firms by reducing the risks of doing business, while providing “utilities with a captive customer base. . .as well as a requirement that utilities earn fair returns” (Harrison, 2020: 4).

Though California was among the first states to deregulate its electricity industry in the 1990s, the now-infamous 2000-01 electricity crisis—which led to skyrocketing costs and the first bankruptcy of PG&E—left retail electricity service largely the responsibility of the state’s three regulated IOUs. Public utility law gives these IOUs purview to recoup costs from ratepayers provided regulators deem rate increases “just and reasonable.” 8 Recouping costs is precisely what SDG&E attempted to do in 2015, filing an application with the CPUC to recover from ratepayers $379 million in uninsured costs associated with the 2007 fires it caused. In November 2017 the CPUC denied this application, determining that the utility had “imprudently” managed its infrastructure in the lead-up to the fires. 9 It was this regulatory decision, combined with the destructive 2017-2018 wildfire seasons, that prompted a series of credit rating downgrades for all of California’s IOUs, beginning in March 2018 and culminating in PG&E’s drop below “investment grade” following its declaration of bankruptcy in early 2019 (Office of the Governor, 2019: 33).

So it was the law—California’s interpretation of inverse condemnation and regulatory decisions made by the CPUC—as much as it was the increasing vulnerability to catastrophic wildfire that structured insurance and financial sector perceptions of risk and value in California’s electricity industry. And it was likewise the law where the state’s utilities and their shareholders sought remedy. After being denied rate recovery, SDG&E petitioned the Supreme Court to review California’s interpretation of inverse condemnation in April of 2019. Though the Court declined to review the case, concerns over the financial wellbeing of California’s IOUs was enough to trigger other roughly contemporaneous transformations of California energy law.

State legislators, recognizing the precarious credit ratings of its major electric utilities, passed two pieces of legislation meant to address the markets’ risk assessments. This legislation should be interpreted as a function of PG&E’s social leverage in the state of California. The first, SB 901 (September 2018), stipulated that the CPUC must among other things consider an electric utility’s “financial status” when determining whether it can pass along wildfire costs to ratepayers. 10 But this failed to stem the utilities’ credit rating tailspin, and it was quickly followed by the more expansive AB 1054 (July 2019). In addition to easing the prudency standard that the CPUC had used to deny SDG&E’s request for rate recovery, the centerpiece of the bill was the establishment of a statewide insurance program known as the California Wildfire Fund. Proposed by SDG&E as early as 2009, 11 and with the explicit purpose of stabilizing California IOUs’ credit ratings (California Earthquake Authority, 2020: 3), the Wildfire Fund is a specialized insurance mechanism that aims to remake California’s utilities into attractive investments by broadly socializing the financial risk of infrastructure-caused wildfires across the state, its utilities, and their customers. The fund pools $21 billion to cover future IOU wildfire liabilities. It was initially capitalized by a loan from the state and individual contributions from the state’s three large IOUs. This base of money is supplemented by “nonbypassable charges” levied on the utilities’ collective 11.5 million ratepayers, which can be securitized by the fund to issue additional debt as needed.

Though this scheme resembles other state-devised insurance mechanisms to address climate risk to critical infrastructure, such as the “Storm Reserve Accounts” established in Florida after Hurricane Andrew (Kousky et al., 2018), the fund is unique in its scope and the specific nature of the damages it covers—not climate damages to infrastructure, as in the Florida case, but wildfire damages caused by infrastructure. The establishment of the fund can be understood as a mobilization of political forces meant to ensure the survival of California’s highly socially-leveraged electricity industry, specifically enabled by public utility law (on which see Boyd, 2014; Harrison, 2020)—which centrally situates investor-owned companies within the “infrastructure of social life” by delegating to them the responsibility of provisioning a public good in exchange for monopoly privileges and a regulated (i.e. guaranteed) rate of profit. The Wildfire Fund is in effect a legal technology for transferring risk and thereby lowering the cost of capital for these firms.

California’s unique legal and regulatory regime was widely perceived as an impediment to the ability of its IOUs to attract investment in an era of increasingly catastrophic wildfire. The changes made by the state in the form of SB 901 and AB 1054 represent an attempt at solving this problem through the socialization of wildfire risk, articulated through the existing structures of public utility law. These mechanisms are the sociolegal context in which PG&E’s bankruptcy unfolded. Participation in the Wildfire Fund, for example, was an essential component in the firm’s pathway out of bankruptcy, as the state emphasized throughout the process, including in a December 2019 statement insisting on the right of the firm’s wildfire claimants to pursue an alternative settlement with its bondholders. 12 The fund—coupled with, on occasion, the threat of public takeover 13 —provided a tool for the state to attempt to impose a timely and politically palatable exit from bankruptcy for PG&E. But it was also meant to assure financial markets that California utilities would remain an attractive investment proposition at the very same time that many financial actors were betting on their own ability to leverage their position within the firm’s bankruptcy to profit from the acquisition of its distressed assets. It is to these actors that I now turn.

Arbitraging the law

Savvy investors understand that utilities like PG&E possess the kind of leverage that tends to activate forces (like the state of California) committed to their ongoing survival in moments of crisis. In this and the following section, I return to PG&E’s bankruptcy to demonstrate how these investors used the law to manage their own risk exposure. Earlier, I suggested that arbitrage is a powerful internal logic and peculiar orientation towards risk that guides many forms of concrete financial practice. Here, I interpret the strategies of the financial firms that participated in PG&E’s bankruptcy through the concept of “legal arbitrage.”

My conception of legal arbitrage is related but not identical to the familiar notion of “regulatory” arbitrage. Riles (2014) argues that regulatory arbitrage has the same effect on legal differences that economists suggest other forms of arbitrage have on price differences: it eliminates (or “harmonizes”) discrepancies across legal or regulatory space by selecting the financially advantageous (e.g. low-tax, low-regulation or business-friendly) regime in which to operate. This may be true when an arbitrage operation seeks out “jurisdictional” spreads—for example, differences in fiscal or regulatory regimes across national boundaries that make financial innovation possible (Bryan et al., 2016)—or selects global financial centers as sites of dispute resolution with governing law clauses embedded in contracts (Potts, 2016). But what if difference is not functionally eliminated but rather persists in the face of an arbitrage action?

Here we may think of a form of arbitrage that takes advantage not of price differences across spatially discrete markets or legal differences across national or subnational jurisdictional space, but rather conceptual differences between the “law” and the “economy” as distinct but imbricated social systems. One of the functions of law is to create and manage “conceptual boundaries between. . .law, economy, and politics” (Potts, 2020: 114). The phenomenon of “legal closure” (Barkan, 2011) created by these boundary-making practices makes it possible for the “legal” and “market” value of particular financial assets to begin to diverge in circumstances of distress.

For example, a bond is a financial instrument: a promise to pay, with interest. It is also a contract with certain legal affordances—including the right to participate in a legal process as an affected creditor, vote on a debtors’ plan for restructuring its obligations, and gain access to whatever refinancing, restructuring or fee-generating opportunities such a process may produce. In bankruptcy, the market value of the financial assets associated with a debtor declines, while what I am calling the “legal” value of those same assets can in fact grow. Legal arbitrageurs transgress the boundary between law and economy to exploit this simultaneous difference.

PG&E’s bankruptcy transformed those who had invested in the firm from passive observers of an unforeseen socionatural risk into active managers of financial risk within an unfolding litigation process. The market value of the financial assets associated with PG&E may have been evaporating as the company prepared its bankruptcy; but as vehicles for crossing over into the domain of the law—where active pressure to direct an unfolding, hierarchical situation could be exerted—these assets retained legal value. It was this spread between legal and market value that activist investors sought to exploit.

Depending on which of the firm’s distressed assets they acquired, the particular interests of the financiers involved in PG&E’s bankruptcy litigation diverged at various points; as I will show below, the success of individual actors in these moments of divergence depended on the leverage they possessed to advance their courtroom agenda. But all distressed investors in PG&E were able to extract legal value from the assets in their possession during the bankruptcy.

Shareholders like Knighthead and Abrams could use their investments to dictate the composition of the firm’s board of directors and craft a “Plan of Reorganization”—the company’s formal path out of bankruptcy—that preserved the value of the firm’s existing equity despite the legal position of common stock at the bottom of the priority hierarchy. This was achieved in part by dramatically expanding the firm’s leverage (in the restricted sense), which is how PG&E exited bankruptcy with approximately 60% more outstanding debt than it entered with. Bondholders like Elliott Management Corporation and PIMCO, meanwhile, successfully swapped the discounted, unsecured debt they had purchased in the market for new senior bonds secured by collateral. 14 And both the equity and debt camps were offered access to the firm’s new equity fundraising round, which promised underwriting fees and gratis shares in exchange for a “backstop” commitment to purchase newly issued stock if buyers could not be found on the open market. 15 PG&E’s bankruptcy, then, unlocked many layers of legal value for all of the financial actors willing to follow the company into the courtroom.

Leverage as power

The affordances of PG&E’s distressed assets in bankruptcy court created a spread that legal arbitrageurs could exploit. At this point, the risks associated with investing in PG&E became fully endogenous to its unfolding legal situation. Though all financial parties to the bankruptcy benefited from the legal value of the assets in their possession, the outcome of the firm’s restructuring process—whether it would be more profitable to PG&E’s shareholders or bondholders—was not predetermined but contested. Though the bankruptcy code hierarchizes creditor claims in a general sense, there is nothing in it that preordains a specific resolution over who will be paid and how, and creditors deemed “impaired” (i.e. asked to accept a writedown) are eligible to vote on the debtor’s restructuring plan. It is precisely this ambiguity, and the possibility of leveraging your position to affect a legal process, that attracts financial actors into bankruptcy court.

The goals of a distressed firm’s equity and debt investors are often at cross-purposes. In the early stages of PG&E’s bankruptcy, several competing blocs began to emerge along these lines. On one side, PG&E’s equity investors wanted to restructure the company’s debts and settle its legal liabilities (to subrogation claimants and wildfire victims) in a way that would preserve the value of the company’s existing stock. On the other, the company’s bondholders pursued a so-called “loan-to-own” strategy of converting their distressed debt position into a controlling equity stake. Caught between these competing financial positions were those who held tort claims against the utility for its role in igniting destructive wildfires.

Represented by the “Torts Claimant Committee” (TCC), the company’s wildfire victims were a class of “involuntary creditors” whose claims against PG&E were at the center of the proceedings and continuously leveraged by all parties in the bankruptcy. By the estimation of the presiding judge, these wildfire victims were “the parties most deserving of consideration.” 16 Or, as the bondholders later averred, “All major constituents. . .agree that the full, prompt, and fair payment of wildfire victims’ claims is paramount.” 17 But it would be a mistake to view the wildfire tort claimants in this role as mere pawns whose position of social centrality provided useful leverage for other constituencies in the case. In fact, their early alliance with the bondholders constituted a kind of double leveraging.

How so? Typically in a bankruptcy the debtor is granted an “exclusivity period” during which it is the sole party legally able to advance a reorganization plan in court. But others with a financial interest in a case may develop their own plans for how a debtor should emerge from bankruptcy. This is what happened in the early months of PG&E’s restructuring process. The TCC wanted a larger settlement from PG&E than it was initially willing to offer, while the bondholders wanted to reorganize the firm’s capital structure to maximize return on investment. The alternative Plan of Reorganization developed between these two parties was a vehicle for achieving each of these ends.

Attempting to abrogate PG&E’s exclusivity period in September 2019, the TCC and bondholders announced that they had “locked arms on an alternative,” crafted jointly in a separate set of direct negotiations. 18 For bondholders, the wildfire victims’ claims against PG&E provided rhetorical and legal justification for judicial acceptance of this alternative plan, which would have provided greater remuneration than the company itself had proposed. For the TCC, the bondholders likewise offered an opportunity for leverage, amplifying their power to extract concessions from PG&E.

Together, the bondholders and TCC identified themselves as “the two largest stakeholders in [the] case.” 19 Their plan immediately increased the amount of money set aside for wildfire victim claims by $4.1 billion—while by PG&E and its shareholders’ objections also guaranteeing an “unjustifiable economic windfall” of $5.57 billion to the bondholders through a combination of discounted equity, reinstatement of corporate debt without the ability to refinance, and backstop fees. 20

At first, the doubly leveraged gambit of the TCC and bondholders seemed to succeed. Over the objections of PG&E and its shareholders, the presiding judge issued an order on October 9, 2019 allowing the alternative plan to go forward in court. He did so while also acknowledging that PG&E’s own shareholder-driven plan was progressing apace, and with a note of skepticism: While the court has expressed concerns about avoiding any type of litigation that deals with corporate control and sophisticated and rarified bankruptcy issues at the expense of paying the wildfire victims, it will not second-guess the informed decision of two well-counselled groups [i.e. the bondholders and TCC] who are willing to take the attendant risks that go with competing plan disputes.

21

The judge acknowledges here that allowing the alternative plan to proceed awards the kind of “rarified” legal maneuvering that the bondholders have (obviously) entered the case to pursue. But the social leverage of the TCC and the wildfire victims it represents, which has promoted the alternative plan, is enough to override this concern.

Securing the support of the wildfire victims was thus essential to the shareholder exit strategy. After first settling with its subrogation claimants in September 2019, PG&E and its equity investors severed the combined leverage of the TCC and noteholders by reaching an agreement in December to match the $13.5 billion the latter were offering to wildfire victims in their alternative plan through a combination of cash and company shares. Contemporary reporting suggested that the architect and chief proponent of the settlement was Mikal Watts, an attorney representing 16,000 wildfire victims favored by PG&E and its equity investors and possessing a “special rapport” with Knighthead’s vice chairman (Blunt, 2020). Once the wildfire victims were convinced to accept PG&E’s revised settlement, the bondholders had a less plausible claim to social centrality in the case. That is: they lost much of their leverage, and assented to withdraw their alternative plan in a separate settlement with PG&E in January of 2020.

Though the leverage of the wildfire victims may have been consequential in determining the outcome of an internecine conflict among the financial factions arranged around PG&E during its bankruptcy, what the resolution of the competing plan dispute reveals in a broader sense is how the law functions to allocate risk and the unmatched power of financial actors to minimize the risk to which they are exposed. The result has been to unevenly distribute risk among the constituencies assembled during PG&E’s bankruptcy. The successful shareholder plan created a trust to pay wildfire victims’ claims; the $13.5 billion it set aside was funded by $6.75 billion in cash and 478 million shares of newly issued PG&E common stock (Trotter, 2022). The wildfire victims were the only class of creditors that PG&E paid in stock. Not only did this have the perverse effect of inducing an (affective and literal) investment among wildfire victims in the firm directly responsible for the destruction of their livelihoods, but so too did it leave these victims with substantial equity risk.

At the conclusion of the bankruptcy process, the Fire Victim Trust held a 24.6% stake in a highly indebted company with ongoing wildfire exposure only partially mitigated by the risk socialization measures written into legislation like AB 1054. Though the Trust has been steadily liquidating stock, it remains one of PG&E’s five largest shareholders as of summer 2023, with over $3 billion still owed to wildfire victims per the terms of PG&E’s settlement. The financial actors involved in PG&E’s bankruptcy, meanwhile, evaded much of this risk. The firm’s distressed debt investors may have lost out on their ability to restructure the company to their liking with an alternative Plan of Reorganization, but they nevertheless succeeded in converting the unsecured debt they had purchased at a discount into senior secured notes that will sit atop the priority hierarchy in any future litigation. And PG&E’s distressed equity investors began closing their positions in the company rapidly following the conclusion of the bankruptcy, collectively selling off more than 250 million shares in the company by October of 2021—many of which had been acquired at zero cost through participation in the company’s equity fundraising round (Jamali, 2021).

Conclusion

In this paper, I have shown how risk in California’s electricity industry in an era of increasingly catastrophic fire is legally constituted, mediated, and allocated—both during a particular litigation event and beyond it, through the passage of laws that aim to remake the state’s utilities into attractive investments by broadly socializing the wildfire risks associated with them.

Financial assets can retain legal value even (and perhaps especially) when their market value deteriorates. When the entity that issues these assets enters a courtroom, they grant investors the right to participate in and actively determine the outcome of an unfolding legal event. Buying into such an event is possible through markets. During bankruptcy, the legal-financial strategies of activist investors therefore depend upon both the putative independence of legal and economic space, and the actual ability of those same financial firms to navigate between these spheres. I describe the strategy of transgressing this (ultimately fictitious) boundary between the “law” and the “economy” as a form of arbitrage: an attempt to exploit the simultaneous difference between the legal and market value of a particular set of financial assets. This concept indicates the risk-averse nature of many discrete strategies of financial accumulation and the ways different social systems like law and finance create not just spatial spreads but conceptual spreads as well.

During bankruptcy litigation, risk is not somehow external to or ontologically independent of legal-financial practice. Exposure to this risk depends fundamentally on the power you have to manufacture an advantageous legal outcome for yourself. Following Konings (2018), I have identified this power as a kind of leverage—here meaning not just borrowed money, but the density of the connections you have formed in a given sociolegal context and the way you are able to utilize these connections to induce others to back up your investments. Both PG&E and the hedge funds that invested in it during its bankruptcy were leveraged in this sense. The risks such leverage enabled them to avoid have, to date, migrated elsewhere—to the company’s ratepayers and those who have been victimized by the wildfires its infrastructure has caused.

In this paper, I have also hoped to make a theoretical contribution about the relationship between economy, politics, and law. We should not treat legal and political domains as purely subordinate to capitalism and the market. But neither should we, like the legal formalists of old, treat law as somehow purified of politics (Unger, 1983), or accept the boundaries legal practitioners themselves have historically erected between the “economic” and the “political” (Britton-Purdy et al., 2020). Instead, the analytical task is trace how law offers avenues for fundamentally political and economic processes of contestation and accumulation, and how legal systems interact with or impinge on these processes.

This is no less true in regard to risk. As the bankruptcy of PG&E shows, the failure of a powerline or transmission tower has cascading social effects. When it is determined to be the cause of a destructive wildfire event, such a failure sets in motion legal and financial processes that determine who will bear responsibility for such risk—long after the last embers have been put out. As climate risks continue to grow, the costs associated with the mitigation and adaptation of infrastructure—whether decarbonizing the grid or simply hardening existing systems—will be negotiated through existing legal and regulatory systems. A crucial theme for further research along the lines proposed in this paper will be to follow how public utility law, and transformations of it, enables or constrains the socialization of these costs. And as insurers begin to vacate markets in areas facing the increasingly common possibility of wildfire and flood, “climate risk” itself is becoming a more openly contested category. The task is not only to understand how the law is used to cajole insurers and other actors to accept this risk, but the opportunities the law offers financiers to mediate, manage, and ultimately profit from its existence.

Footnotes

Acknowledgements

Thank you to three anonymous referees for their generous and incisive comments. A portion of this paper was presented in a panel on “Global Debtscapes” at the 2022 AAG Annual Meeting. Thank you to Drew Kaufman for organizing this session and to all its participants, especially Mark Kear for his thoughtful engagement. Zachary Frial, Bryan Ziadie, Sammy Feldblum, Kelly Kay, William Boyd, and Eric Sheppard each provided invaluable feedback on the work on which this paper is based. Above all, I am indebted to Shaina Potts for her enduring support, insight, and patience.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.