Abstract

An enduring legacy of the 2007–2009 financial crisis is the growth of “social” and “impact” investing, markets dedicated to the use of financial capital to achieve social good. This paper examines one key manifestation of these markets: the social impact bond, a financial device which uses private capital to fund social programs. While social impact bond (SIBs) have been viewed as a testament to the power of finance and the “financialization” of the social sector, the paper instead highlights the struggles and limits of the SIB enterprise. Informed by a multi-year study of SIBs in Canada, the USA, and UK, and the theoretical lens of the social studies of assetization combined with an ecological approach, these struggles are conceived in terms of the challenge of operationalizing SIBs’ financial imaginary and managing the gaps between finance and the social sector as distinct ecologies. Particular emphasis is placed on three valuation devices—liquidity, risk, and rigor—which are central to this effort. Rather than “hinges” connecting these worlds, these devices have emerged as points of conflict, revealing a distinctly spatial politics which helps to explain the limits not only of SIBs but also other forms of financialization at the frontiers of (social) finance.

Introduction

At 2:45 p.m., the session was called to order. Audience members slowly took their seats, directing their attention to the three individuals seated at the front of the packed conference room. Organized as part of the 2015 MaRS Social Finance Forum, a conference for acolytes of the emerging field of “impact investing,” the session featured representatives of three Canadian charities, one specializing in children's mental health and violence prevention, another mentoring programs for immigrants, and a third care for preterm infants in the developing South. The moderator opened the session by explaining that the providers were each seeking investments in their programs and were offering the prospect of both a financial and a social return. The occasion for this strange collision of finance and the charitable sector was a new model for funding social programs, the social impact bond (SIB). 1 First introduced in the UK in 2010, a SIB uses private capital to fund social programs, with the government providing a return depending on the degree of success and the cost savings from reduced future demand on public services. Ostensibly providing benefits to all three parties—savings for government, steady funding for providers, and new “impact investing” opportunities for investors—the SIB model quickly gained traction, expanding beyond the UK to Australia, the USA, Canada, and Europe.

The global diffusion of SIBs raises fascinating questions about the relationship between finance and the social sector and the role of financial actors in the world of charitable work. A key theme running through the critical literature is that SIBs reflect the “financialization” of social and public services (Dowling, 2017; Sinclair et al., 2021; Warner, 2013). And yet, the SIB enterprise has not been nearly as successful as implied in these accounts. While advocates have established a global roster of projects, they have struggled to build a sustainable market for these investments. In view of these challenges, the question is not simply why SIBs have emerged or what they signify, but why they have struggled to take hold and what these struggles reveal about the limits of finance—that is, the ability to deploy financial models in nonfinancial spaces.

This paper takes up this very question focusing on the practical work of developing projects and the challenges encountered along the way. These efforts are conceived through the theoretical lens of the social studies of marketization and assetization (Birch and Muniesa, 2020; Langley, 2021) combined with an ecological approach (Abbott, 2005). While the former helps to tease out the specific work involved in turning social programs into financial assets, the latter highlights the spatial dimensions of this enterprise and how the process of assetization unfolds within, and is shaped by, the spaces between finance and the social sector as distinct ecologies. Informed by these theoretical touchpoints, and the results of a 3-year study of SIBs and the funding of social programs in Canada, the USA, and the UK, the paper reveals how the course of the SIB enterprise has been impacted by three financial constructs, or valuation devices, central to SIBs’ financial imaginary: “liquidity,” “risk,” and “rigor.” Whereas these kinds of devices have been essential to forms of marketization and assetization in other contexts, helping to link economic and noneconomic domains (Doganova and Eyquem-Renault, 2009; Doganova and Muniesa, 2015), in the case of SIBs, they have not only failed to translate but have emerged as points of conflict. Conceiving of these devices as a type of “hinge” (Abbott, 2005), the paper argues that these tensions reflect a distinctly spatial politics, and that it is these politics which help to account for the limits of the SIB enterprise not simply as an expression of competing values, logics, or interests, but the practical difficulties of operationalizing the SIB imaginary and navigating the spaces and boundaries between the worlds of finance and the social sector.

The analysis presented in this paper not only advances the SIB literature but also contributes to debates around financialization more generally. The case of SIBs affirms the value of more nuanced and empirically robust accounts of financialization and its limits (Christophers, 2015; Mader et al., 2020), while also highlighting the critical role of space conceived not in terms of the expansion of markets or the blurring of erstwhile well-established boundaries but enduring distinctions which shape and frustrate the work of financialization. Considerations of space are especially significant in exploring markets in “social” and “impact” investing which, like SIBs, involve the extension of finance into nonfinancial spaces (e.g., agriculture and the environment). While there is a growing literature on these markets, including work on the “geographies of marketization” which recognizes the contingencies and unevenness of market making and clashes between economic and noneconomic logics (Berndt and Boeckler, 2012; Berndt et al., 2020; Muellerleile and Akers, 2015), the notion of space and spatial politics developed in this paper offers a different lens for exploring these shifting frontiers of (social) finance.

The balance of the paper is organized as follows. The first section introduces the SIB model, juxtaposing SIBs as a form of financialization with the reality of a market that has fallen short of expectations. The next section outlines the paper's theoretical framework and methodology. This is followed by an extended discussion of liquidity, risk, and rigor as valuation devices and hinges, reflections of the spatial politics which have frustrated the SIB enterprise. The paper concludes by noting the implications of the analysis for future research on SIBs and financialization within and beyond the social sector.

The social impact bond (r)evolution

On March 1, 2010, officials from the UK Ministry of Justice announced the pilot of a new model for funding social programs. Termed a SIB, the idea was that private investors would fund a consortium of social sector providers to work with offenders released from Peterborough prison. If the program lowered rates of reoffending, the government would use the savings from reduced criminal justice demand to repay investors and provide a return. The result, according to advocates, was a win-win-win scenario (Bolton and Savell, 2010). By only paying for successful outcomes, governments could shift the initial cost of programs and the risk of failure to investors. Social service providers, many of them charities, would receive longer-term and more flexible funding. And investors could achieve both a financial and a social return, the ideal embodiment of “shared value” investing (Porter and Kramer, 2011). Buoyed by these benefits, SIBs quickly gained traction with projects popping up in the USA, Australia, and Europe in areas such as criminal justice, homelessness, and children's services. By July, 2020, 194 projects had been developed globally (Gustafsson-Wright, 2021) with SIBs seemingly poised to become a permanent fixture of the nonprofit funding landscape.

Financializing social services

While celebrated by advocates, SIBs have been scrutinized by critics concerned not only with whether the model works but also with what it signifies and how it might impact the social sector. A key current running through the critical literature is that SIBs are indicative of the “financialization” of social and public services (Bryan et al., 2020; Dowling, 2017; Sinclair et al., 2021; Warner, 2013). In some accounts, this is viewed through a political economy lens, with SIBs conceived as a new “asset class” and response to the crisis tendencies of neoliberalism (Dowling, 2017; Harvie and Ogman, 2019; Sinclair et al., 2021), while in others the focus is on the spread of financial and “derivative” logics (Bryan et al., 2020) and the role of financial interests in reshaping the mandates of charitable organizations (Berndt and Wirth, 2018; Cooper et al., 2016; Tse and Warner, 2020). Regardless, reflecting a common definition of financialization as the growing influence of finance over everyday life (Martin, 2002), the central notion is that SIBs are further evidence of the expanding frontiers of finance, a case of “the penetration of financial criteria and issues into what were previously non-economic areas” (Sinclair et al., 2021: 18).

Struggles, challenges, and barriers

These accounts certainly have merit. SIBs are indeed animated by a financial logic and signal the potential for the greater influence of finance over the social sector. And yet, SIB practitioners have struggled to translate this vision into reality. The global spread of the model is impressive, but the rate of growth has been slower than anticipated (Arena et al., 2016; Maier and Meyer, 2017) with many prospective SIBs failing to come to fruition (Fraser et al., 2018; Heinrich and Kabourek, 2019). The market also remains shallow, limited to one-off projects representing a tiny fraction of public sector spending and the social investment market (Floyd, 2017). Most critically for the financialization narrative, more return-motivated investors have largely steered clear of SIBs with the market supported by public and philanthropic capital. Thus, the reality of SIBs has not matched the hype (Chiapello, 2020).

These struggles point to a different question, not why SIBs have emerged or what they signify, but rather why the SIB enterprise has struggled and what these struggles reveal about the relationship between finance and the social sector. Those familiar with the SIB literature may object that the limits of SIBs have been well-documented. Case studies have revealed the failure of projects to live up to the model's promises (Cooper et al., 2016; Neyland, 2018; Warner, 2013), and researchers have identified various impediments to project development including technical barriers and provider capacity limits. However, while acknowledging the model's shortcomings and “broken promises” (Harvie and Ogman, 2019), the presumption is that the SIB market will continue to grow despite these limitations. These accounts thus do not fully explain, nor explicitly theorize, why a market in these investments has failed to materialize.

Exploring the SIB enterprise

To answer these questions, it is necessary to adopt a more up close view of the actual work of SIB design which, in turn, requires a different conceptual starting point. While useful as a critical trope and orienting narrative, “financialization” is somewhat vague and imprecise as a theoretical framework. Indeed, the larger financialization literature is increasingly circumspect about the value of the concept calling for greater recognition of the nuances, details, and messiness of financialization (Christophers, 2015; Mader et al., 2020). In the case of SIBs, there are two frameworks which are helpful in this regard and provide a valuable foundation for exploring the SIB enterprise.

Marketization and assetization

The first framework emerges from work on how new markets are created and how economic value is assigned to noneconomic goods. Informed by insights from STS, a central premise of this literature is that markets are not pre-given but are actively performed through the enactment of socio-technical networks or assemblages and the mobilization of calculative tools and devices (Caliskan and Callon, 2010; Muniesa, 2014). The focus is thus on the practical work of market making. More recently, these insights have been applied to the distinctly financial forms of marketization underlying financial assets as the dominant form of “technoscientific” capitalism (Birch and Muniesa, 2020; Muniesa et al., 2017). Assets are rooted in the perspective of an investor weighing the risks and opportunity costs of different investment options, and they require an ability to think in terms of the future and to value that future from the perspective of the present. The practical work of assetization, of turning things into assets (Birch and Muniesa, 2020), depends on tools such as discounting and net present value (NPV) which provide exactly this capacity (Doganova, 2018; Muniesa et al., 2017).

Compared to financialization, thinking in terms of assetization offers greater precision and nuance, shifting the focus from the more generic process of making things “financial” to the distinct work of turning objects, ideas, and people into assets (Birch and Muniesa, 2020; Langley, 2021; Wirth, 2020). As noted by Birch and Muniesa (2020), “Talking of “turning things into finance” would grant too wide a scope, as finance—and financialization—is a process of more abstract proportions” (5). Langley (2020) echoes this sentiment in direct reference to SIBs suggesting that the financialization critique in the SIB literature overlooks the specific form of “financial marketization” (131) underlying the model. Thus, rather than financialization, the SIB enterprise is better viewed as a form of assetization with SIBs conceived as a type of asset, an investment in the present yielding value in the future in the form of cost savings and investor returns. Like other assets, SIB design is informed by an investor perspective and the mobilization of financial tools and devices.

And yet, while useful in exploring the work of SIB development, the lens of assetization is less helpful in accounting for the limits of the SIB enterprise. To be fair, struggle and failure are acknowledged as inherent features of marketization and assetization, a reflection of the difficult work and inevitable contingencies of market design as well as the limits of market frames which are continually threatened by omissions or “overflows” (Callon, 2009) thus requiring a constant work of adjustment and accommodation. These dynamics are particularly evident in markets in public goods, “civilizing markets” (Callon, 2009) or “markets for collective concerns” (Frankel et al., 2019), where the work of marketization is challenged by the clashes between market and nonmarket logics, values, and interests (Callon, 2009; Cooper, 2015; MacKenzie, 2009). Similar insights emerge from the “geographies of marketization” which foregrounds the incomplete, fragile, and contested nature of market making (Berndt, 2015; Berndt and Boeckler, 2012; Berndt et al., 2020; Muellerleile and Akers, 2015). However, while alive to the challenges and politics of market design, these accounts are primarily focused on expanding “market frontiers” (Berndt et al., 2020), and how market specialists are able to overcome struggles and repair markets (Frankel et al., 2019). Less attention is devoted to cases of failure, instances where designers have struggled to establish markets in the first instance and where the very process of market design is uncertain and contested. In particular, this scholarship has not fully appreciated the extent to which marketization (or assetization) is shaped not only by clashes between competing logics but also by the relationships between economic and non-economic domains as distinct fields. This points to a critical question of space.

Spaces of marketization and assetization

In one respect, notions of space are central to the social studies of marketization and assetization, reflected in the very framing of marketization in terms of the enactment of socio-technical assemblages which extend across space enrolling different groups of actors and linking economic and noneconomic domains. Indeed, a key feature of market devices such as business models is their mobility and ability to “circulate and enrol allies” (Doganova and Eyquem-Renault, 2009; Doganova and Muniesa, 2015: 4). These boundary-spanning devices have been conceptualized in various ways, as “mediating instruments,” common frames and visions of the future which “link formally separate actors and arenas” (Miller and O’Leary, 2007: 729), and “boundary objects” which provide mutual benefits across fields (Star and Griesemer, 1989). Thus, Doganova and Eyquem-Renault (2009) frame business models as both “mediating instruments” and “boundary devices,” while Helgesson and Lee (2017) view randomized controlled trials (RCTs) in the pharmaceutical industry as “mediating instruments” bridging science and the market.

However, while appreciating the spatial dimensions of marketization, and the specific work involved in linking different fields, these accounts have largely focused on cases where devices have successfully performed this role as bridges with less attention to the possibility of failure and devices not only falling short but themselves becoming points of conflict. This oversight reflects the particular understanding of space within these literatures, and STS-inspired accounts of “networks” and “assemblages” more generally, a topological view that is appreciative of the manifold connections and proximities that are constitutive of networks but is less attuned to the variegated topographies that characterize many market environments. Moving beyond the “flat ontology” (Müller, 2015) which defines networks and notions of topological space, more careful consideration is needed of the spatial boundaries informing processes of marketization and the tensions between financial and nonfinancial spaces.

One perspective that is helpful in thinking about these kinds of dynamics is Abbott's (2005) ecological approach and his concept of the “hinge.” An ecological approach recognizes the spatial, contextual, and contingent features of social worlds and conceives of the social in terms of particular domains or spheres of practice, such as professions, defined by distinct logics, identities, and competitive relations. Informed by his interest in the relationships between ecologies, Abbott (2005) developed the concept of the “hinge” to capture how ecologies become linked through devices which provide mutual benefits or “dual rewards” (255). de Souza Leão and Eyal (2019) invoke this concept in their account of international development policy, describing how a connection was forged between the fields of development aid and academic economics through the hinge of the RCT which helped to “overcome resistance created by the tension between the incommensurable logics of the fields” (387). du Gay et al. (2012) likewise invoke Abbott (2005) in exploring the financialization of public governance in the UK. Drawing from examples such as the Public Finance Initiative (PFI), they describe how these efforts relied on “governing devices” (e.g., “value for money”) which functioned as hinges, allowing for an “interecology process of translation” (1087) and thus connecting the economic and public realms.

This ecological perspective, and the view of market devices as hinges, helps to draw out the distinctly spatial features of marketization and assetization. It does so by highlighting the extent to which these practices hinge on the ability to negotiate and bridge the gaps between market and non-market (or financial and non-financial) ecologies with these efforts depending on a distinctly spatial form of labor: acts of translation and the construction of hinges. This perspective complements the central insight of the geographies of marketization that market making is inherently spatial, while focusing less on space as a shifting boundary or expanding frontier and more on the spaces between fields. 2 It also resonates with work on “financial ecologies,” which has similarly sought to nuance the network analytic (Lai, 2016; Langley and Leyshon, 2017), while emphasizing the discontinuities between financial and nonfinancial networks rather than within financial networks themselves. 3 Thus, thinking in terms of ecologies and hinges further sharpens the lens of assetization, accentuating the spatial dynamics involved in turning things into assets, especially in domains far removed from the world of finance. As these concepts have once again largely been applied to cases where hinges have successfully linked different ecologies (e.g., du Gay et al., 2012), the question is whether they can also account for failure, a question that is directly relevant to the case of SIBs.

Exploring the SIB enterprise

Positioned between the worlds of finance and the social sector, SIBs embody the challenge of forging connections between distinct ecologies. Much of the work of SIB design (conceived as a process of assetization) depends on the efforts of SIB practitioners to translate the financial imaginary underlying the SIB model into the world of social programs—that is, to render it mobile, to engage prospective partners, and to forge connections between finance and charitable work. Several accounts of SIBs have touched on these dynamics (Chiapello, 2015, 2020; Langley, 2020; Neyland, 2018; Wirth, 2020), highlighting the role of accounting tools (Cooper et al., 2016) and metrics and measurement devices (Berndt and Wirth, 2018) in SIB design. However, as with the SIB literature more generally, these analyses have tended to focus on projects successfully brought to fruition, thus capturing the details but not necessarily the messiness of SIB design. Drawing from the framework of assetization, and the concepts of ecologies and hinges, the question is exactly how SIB practitioners have sought to operationalize SIBs’ financial imaginary, the specific devices underlying this effort, and the extent to which this particular work of assetization—unfolding across the spaces between finance and the social sector—helps to account for the limits of the SIB enterprise.

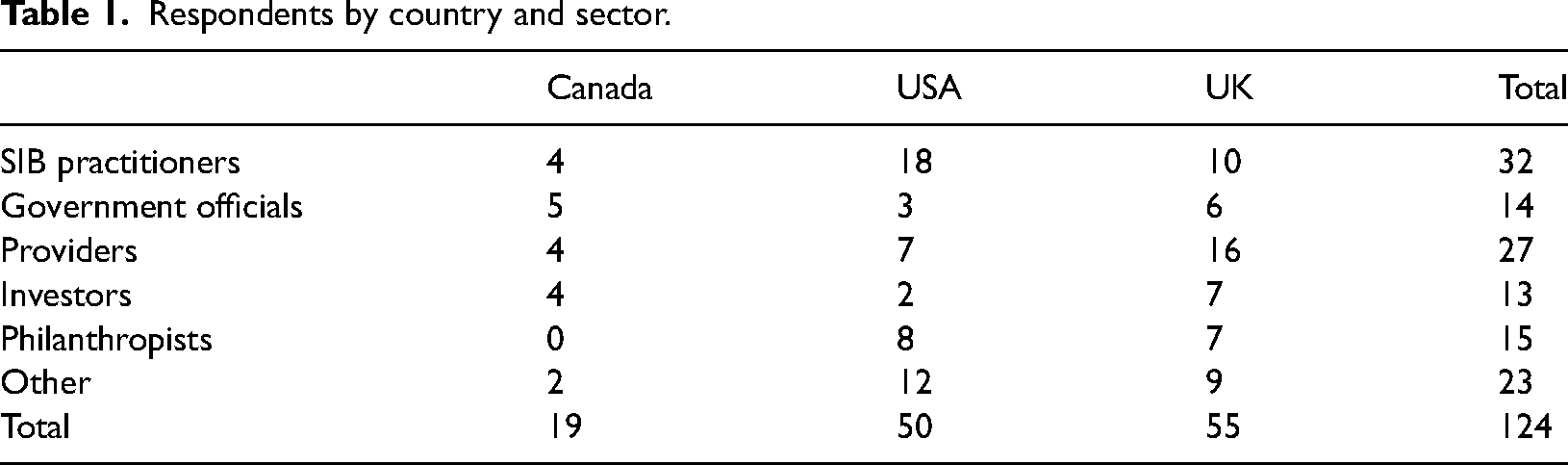

These questions are explored based on the results of a larger, 3-year study of SIBs and the funding of social programs in Canada, the USA, and UK. Rather than individual projects, the primary reference point was the SIB market and the activities of the specialized advisory firms responsible for project development. 4 The study started with these firms and then moved outward to include other actors in the SIB ecosystem and the larger nonprofit funding regime (e.g., government officials; providers; investors; and philanthropists). The project was also comparative, exploring the SIB enterprise in two of the largest (UK by number of projects; USA by total value) and one of the smallest (Canada) SIB markets. The research itself consisted of documentary research and semi-structured, confidential interviews. In total, 196 interviews were conducted mainly in the cities of Toronto, Boston, and London, homes to the major SIB advisory firms and the gravitational centers of these respective SIB markets. The interviews took place between 2016 and 2019, a pivotal period for the SIB enterprise which followed the initial wave of interest and enthusiasm and involved efforts to transition into a more sustainable market.

While informed by this larger study, the following discussion draws primarily from a smaller subset of interviews with those most directly involved in SIB projects in each country including: SIB practitioners; public officials; social sector providers; investors; philanthropists; and other contributors and stakeholders (see Table 1). These respondents were asked about the process of developing projects and the challenges encountered in the course of this work. They were also asked about the state of the SIB market and its future prospects. The interviews were digitally recorded, transcribed, and analyzed using a thematic coding system. 5 Although the larger study was comparative in nature, many of the core challenges noted by respondents were similar across Canada, the USA, and UK. Thus, what follows focuses on these common struggles, combining insights and interview data from each country.

Respondents by country and sector.

Lost in translation: SIBs and their limits

The results of the study affirmed the more skeptical view of SIBs as a market that has fallen short of expectations. The interviews revealed a prevailing sense of frustration around the slow growth of the SIB market with respondents juxtaposing the outward enthusiasm for the model with the more troublesome reality unfolding behind the scenes. In the words of a UK provider turned SIB practitioner, “The external view is it's swans on water. But there's some desperate paddling going on” (UK Respondent #54). A U.S. respondent echoed this sentiment, “It's not been a smooth sailing, not at all … I think that the public conversation about it may be more positive than the private conversation” (US Respondent #58). Even those involved in “successful” projects came away somewhat soured on the model and skeptical of its future.

Various explanations were provided for these struggles, many of which echo those cited in the SIB literature (Fraser et al., 2018; Tan et al., 2021). These ranged from cost and complexity, to technical barriers, to opposition to the very idea of investing in social programs. However, while these factors have certainly slowed SIB development, the more fundamental challenge revealed by the interviews involved difficulties in turning social programs into viable investments. As with other forms of assetization, SIB design involves considerable work and effort (Chiapello, 2020). Part of this work stems from the need to convert the outcomes of social programs into financial returns, an endeavor which relies on devices such as financial models, data analytics, and cost–benefit analyses. However, beyond simply valuing social programs, practitioners must also demonstrate the value of these projects as investments with the SIB value proposition hinging on three key promises: cashable savings; risk transfer; and social impact. These promises reflect the financial features of SIBs as bets on the future performance of providers with investors compensated for delivering clear returns (in the form of “impact” and “savings”) and for assuming the financial risk associated with these bets. And yet, these promises were repeatedly cited by respondents in discussing the challenges of SIB development. In particular, interviewees spoke to the difficulties of operationalizing SIBs’ financial imaginary with tensions emerging around three financial constructs, or valuation devices, which are central to these promises and represent key “hinges” between financial and social sector ecologies but are not easily translated into the world of social programs: (1) liquidity; (2) risk; and (3) rigor.

“Liquidity”

A first promise of the SIB model is that investments in social programs will yield not only cost savings but savings that are cashable—that is, which can be realized as gains in specific budget lines and then reallocated to other spending priorities. The ability to generate and redeploy savings in this way is a key attraction of SIBs for government, especially in the context of austerity-based cuts, and is essential to investor returns which (in theory) are tied to government savings. This promise of “cashability” (Bolton and Savell, 2010: 39) presumes that public capital, like private capital, possesses a degree of liquidity 6 allowing governments to cash out and realize the gains of these investments. As noted by one SIB practitioner, “Our definition of cashability is funds that are actually available in a liquid form that you can reallocate from a budgetary standpoint” (CDN Respondent #7).

However, as SIB practitioners quickly realized, there are significant barriers to the liquidity thesis. Government costs tend to be fixed (e.g., buildings and staff) and are resistant to the kinds of incremental, marginal savings generated by SIBs. For example, many reoffending programs have sought to reduce the number of “bed days” in prison, which result in marginal savings (e.g., uniforms and food) and will only impact fixed costs if they are large enough in scale and duration to allow a reduction in capacity such as closing the wing of a prison (McKay, 2013). Determining the point where these marginal gains convert to savings in fixed costs is challenging and mostly speculative. Even if these kinds of reductions could be achieved, other challenges loom in realizing imagined savings. One such challenge, noted by a UK SIB practitioner, is the possibility that any freed-up capacity will simply be backfilled with latent demand, “How often are the cashable savings realized? We try not to talk about them. Because you can guarantee that within public services there is latent demand” (UK Respondent #55). Service cuts may also be politically unpopular. All of this suggests that public capital possesses a viscous quality that makes it difficult to liquidate in the way imagined by SIB proponents.

Recognizing these challenges, SIB practitioners have sought to reframe the benefits of SIBs advocating for broader notions of “public value” (Kohli et al., 2015). A senior US SIB practitioner admitted that cashable savings were a rhetorical ploy, “If you dig deep, cost savings is the rhetoric. Even if you reduce recidivism, you don’t really save much money. It's just a way to talk about it” (US Respondent #52). However, it is not entirely clear what a shift from a “cost savings play to more of a value play” (US Respondent #31) actually entails. It is sometimes framed in terms of future cost avoidance, what one local commissioner described as “taking the heat out of potential future demand” (UK Respondent #9), or an efficiency argument of better outcomes for the same investment, “… shifting that discussion to is the money being spent more effectively and more efficiently rather than are we able to spend less money” (US Respondent #20). At other times, the focus is on broader societal benefits determined using willingness-to-pay and contingent valuation frameworks. However, as the savings case is broadened in this way, it becomes more speculative (Fourcade, 2011), making it difficult for governments to define the value of these investments. Liquidity, as an essential attribute of financial capital and defining feature of SIBs’ financial imaginary, thus fails to translate into the public sector.

“Risk”

A second aspect of SIBs and their financial vision involves the question of risk. Following the well-established script for public-private partnerships, SIBs are built on the premise that because governments only pay for successful outcomes, the financial risk of paying for a program that does produce expected results is transferred to investors. Thus, what is being monetized in a SIB is not simply a set of “outcomes” and their putative savings but also the value of the risk transfer. A government official articulated this value proposition through an analogy with public infrastructure projects, “What's the value of the risk transfer? I lovingly refer to this as P3 for people. Part of the costing that we do for bridges, and buildings, and highways is what's the value of transferring risk … What would you pay to have a guaranteed outcome? There's value in that” (CDN Respondent #37). Like other types of investments, it is the commodification of risk (LiPuma and Lee, 2005) that is critical to SIBs.

As with liquidity, the thesis of risk transfer has been difficult to operationalize. A common refrain of critics is that the risks of SIBs are minimal given the focus on proven programs (Cooper et al., 2016; Neyland, 2018; Warner, 2013). Yet, from the perspective of investors, these projects are inherently risky. As noted by a Wall Street veteran turned SIB practitioner, “They are enormously high risk. There's not one project in the United States or around the world that is not extremely high risk” (US respondent #19). This same individual went on to explain that this risk stems from the distinct properties of SIBs and their departure from more conventional, asset-based investments (e.g., housing), “They don’t have an asset class called PFS. It's too new. So I’ve been spending more time educating [investors] on why would you create an asset class … But then we get, ‘That's too risky, I didn’t realize that. We’re used to have a building on the ground’” (US Respondent #19). The head of a UK charity pointed to a similar challenge in selling investors on a SIB for children in care whose value was based on improved life chances in adulthood, “And that, although it is completely valid as a way of proving financial worth, is less attractive than being able to sell a house if you are trying to get your money back” (UK Respondent #30).

A further difficulty stems from the roots of these investments in the vagaries and vicissitudes of human behavior which render SIBs unpredictable and challenging from a due diligence perspective. A U.S. SIB practitioner presented this as a key barrier, “What does it mean for [investors] to diligence a social service outcome? … What does it mean that your payment is contingent on human behaviour?” (US Respondent #35). Moreover, with limited experience with the world of social programs, investors are ill prepared to undertake these assessments, “For the most part they don’t know how to diligence these projects. If you’re a [Community Development Financial Institution] and you know how to diligence public housing or mixed income housing, now you’re being asked to diligence a recidivism program? I think there's straight up risk” (US Respondent #30). Social programs also entail distinct forms of risk. Providers may struggle to secure sufficient referrals into programs, a form of “execution risk” (US Respondent #60). There is “policy risk,” the risk that a change in government policy or social conditions will impact outcomes (Government Accountability Office, 2015). Time itself is a source of risk, a reflection of financial calculations (i.e., NPV) which attach a financial cost to time making investments that take longer to generate cash flows both risker and worth less (Chiapello, 2015; Doganova, 2018).

To make projects more palatable to investors, SIB practitioners have developed various risk mitigation strategies. One strategy is to shorten the timescale of projects and thus the length of time capital is at risk by using shorter-term indicators that are (in theory) correlated with, or proxies for, longer-term “outcomes.” A UK respondent described how this strategy was used in projects where the initial outcomes were deemed too risky, Some of those we’ve tried to walk back to kind of interim outcomes and to soften the return/risk profile so that you get paid for something that might happen six months down the line rather than waiting seven years for an outcome to come about where you’ve got no idea whether it is or not. So it's trying to walk back some of the ones that are really high risk for investors. (UK Respondent #34)

A related strategy is the use of “output-based” payment metrics such as program enrolments which provide an early, steady, and essentially guaranteed source of cashflow.

While reducing investor risk, these risk mitigation strategies make projects less attractive for governments which are expected to pay a risk premium for metrics that are low risk and far removed from outcomes of interest. This point was made by a UK respondent who described how shorter-term outcomes “can also de-risk the investor unintentionally because it gives them an additional cash subsidy early on in the process which means that the investment funding isn’t needed” (UK Respondent #45). Not surprisingly, these measures have emerged as points of tension in SIB negotiations. A participant in one US project described how the SIB advisory firm pushed for early payments based on enrolments to make the deal more attractive to investors: Because their goal is to sell the deal to investors, [firm x] wanted there to be an enrolment payment so that the investors got paid per enrollment so that there would be payment outcomes starting in quarter three instead of the first payment starting in quarter eleven. (US Respondent #49)

The government pushed back, “holding hard and fast to ‘this is called PFS. Success is showing somebody that they did something and so I’m not going to pay you for an enrolment payment’” (US Respondent #49), but ultimately capitulated, consummating the deal but no doubt coming away somewhat soured on the merits of the SIB model.

Even if longer-term “outcomes” are used and investors assume greater financial risk, “risk” is never fully transferred as governments bear the political and reputational costs of failed projects, a point made by a UK respondent, Initially it was kind of positioned as you just transfer all the risk over … But risk is never fully transferred. It's risk sharing. If a children's services SIB goes really badly wrong, it's still the head of social care that gets in trouble for that. You never have proper risk transfer. So I think if you don’t have risk transfer, risk sharing, what's the right return for that? (UK Respondent #34)

Governments also retain responsibility for the underlying problem with much of the “risk” in these projects rooted not in the financial risk of spending public money on a failed project, but the political risk of leaving social challenges unresolved. As explained by a UK SIB practitioner, a “successful” SIB that spares government the cost of a failed program may have limited value, I don’t think the public sector really value the transfer of risk. They have the problem. They feel responsible for the problem. They want to solve the problem. Simply telling them you don’t pay unless it's successful means “so you mean when it fails I don’t pay.” Well that's not a great outcome. So if you think about the agendas and the motivations of the various partners the concept of transferring risk is not a very compelling one. (UK Respondent #31)

The promise of risk transfer is thus another conceit of the SIB model, a further reflection of the gaps between SIBs’ financial imaginary and the realities of the social sector.

“Rigor”

A final feature of the SIB imaginary involves the nature and definition of the change produced by social programs—i.e., their “social impact.” Social impact is critical to the value of SIBs as this is what is ultimately being monetized as public savings and investor returns. Here, impact is defined not only by the outcomes produced by programs but also by the extent to which these results exceed what would have been produced in their absence, what is referred to as “additionality.” Valuing SIBs in this way requires the construction of a counterfactual in which “two future states of the world—one with the project and one without it—are played against each other” (Ehrenstein and Muniesa, 2013: 162). The value of projects is derived from the difference between these futures. A critical question, then, centers on the nature and terms of this counterfactual display and the kinds of methods to be used in determining program results.

Early reports on SIBs advocated for the most rigorous methods possible on the grounds that this would provide the most precise measure of the impact of SIB-funded programs. Rigor and precision are highly valued in finance, particularly when calculating risks and returns, and it was believed that this same degree of rigor should be brought to bear in determining the impact of SIB projects. Thus, emphasis was placed on experimental or quasi-experimental methods (Bolton and Savell, 2010) which were seen to offer a more robust indicator of additionality given their use of a contemporaneous comparison group allowing for closer comparisons between program and nonprogram groups and a clearer demonstration of the relative impact of programs. 7 In the USA, there was a concerted push toward RCTs on the grounds that experimental designs (by virtue of the element of randomization) yield the most rigorous measure possible of program effects, revealing genuinely causal connections between programs and outcomes (Milner and Walsh, 2016). Reflecting this presumed relationship between epistemic rigor and financial value, numerous US projects have been built around RCTs.

However, these more rigorous evaluations, especially RCTs, conflicted with the financial attributes of these projects. They not only increased their costs but also created an additional, unanticipated, risk for investors, what one investor described as “evaluation risk,” “[The RCT] adds a … risk that in the early days we didn’t think of, which is evaluation risk which basically is the risk the structure and process of the evaluation will actually impact the results that are observed” (US Respondent #55). As discussed in Williams (2021), this form of risk stems from the technical features of RCTs, particularly conventions around statistical significance, which create additional logistical demands on projects (e.g., minimum size thresholds for program and control groups which exacerbate pressures on referrals and, given limited provider capacity, necessitate that programs be run through multiple cohorts extending the timeline of projects and thus their costs and risks), and expose investors to the risk of false negatives and not being compensated for real results. As these risks became better understood, evaluation emerged as a point of tension, particularly in the USA where respondents provided examples of battles being fought over RCTs. One provider described how neither they nor the advisory firm wanted an RCT, but the government and its advisors insisted, “In order to get the whole deal, we had to do an RCT” (US Respondent #49). Another provider reported a similar experience describing a “battle over randomized control” that was “almost a deal breaker” (US Respondent #22).

RCT-based tensions provide further evidence of the distinct challenges of SIB development. While RCTs were initially viewed by all parties as a suitable valuation device, a way to gauge the precise “impact” of projects, their technical features (i.e., randomization, statistical significance) conflicted with the financialized form of valuation underlying SIBs—with investors’ preference for early, steady, and predictable cashflows, and with financial tools (NPV) which treat time itself as a cost and source of risk thus making RCT-based projects inherently more risky. Realizing these tradeoffs, investors have pushed for less rigorous methods and thus valuation devices (Helgesson and Lee, 2017) 8 , privileging market pragmatism over epistemic rigor. As a Canadian SIB practitioner surmised, “you don’t actually need these vehicles to be as statistically rigorous for them to still be valuable” (CDN Respondent #7). And yet, less rigorous measures devalue projects for government which are left unsure as to whether they are paying for real results. The battles over RCTs are thus a further testament to the gaps and tensions between finance and the social sector.

The spatial politics of assetization

These conflicts around liquidity, risk, and rigor clearly speak to the difficulty of operationalizing SIBs’ financial imaginary. This challenge is not simply the result of the competing values or interests which the parties bring to these deals (Maier and Meyer, 2017), nor are they mere manifestations of clashing logics or the incommensurability of social programs with financial frames as work on markets in public goods is wont to suggest. Rather, they are emergent within the small details and technicalities of SIB design, in the use of valuation devices (themselves financial constructs) which have engendered tradeoffs impacting the distribution of risk and rewards and leading to alternative operationalizations—notions of “public value,” forms of risk mitigation, and less rigorous methodologies—and thus articulations of value. All of this points to a distinct form of politics, a “micropolitics of valuation” (Williams, 2021), with the course of SIB experiment having been shaped by these battles.

These politics of valuation, in turn, reflect the spatial dimensions of the SIB enterprise. As with many other forms of assetization, SIBs rest on the translation of financial ideas into nonfinancial spaces and rely on valuation devices to perform this work. However, unlike other contexts where devices have served as “hinges,” creating mutual benefits and interstitial assemblages linking different ecologies, the promises of SIBs have been difficult to operationalize, and the devices employed as part of this effort have not only fallen short—limited in their mobility and ability to bridge these gaps—but also have themselves become points of conflict. These trials and tribulations speak to the differences between finance and the social sector as distinct ecologies: a presumption of liquidity that fails to align with the nature of public capital; limits to risk transfer given the myriad, unfamiliar risks associated with social programs and the political risks retained by government; and the use of social science methods which deliver rigor but at the cost of greater uncertainty. This is not to suggest that finance and the social sector are fundamentally distinct, nor is it to deny the increasingly complex entanglements between financial logics and social programs (McGoey, 2015; Phillips and Smith, 2014). Rather, it is to acknowledge the enduring gaps between these worlds, the specific work of translation (and devices) required to bridge these gaps, and the politics which define these efforts. Ultimately, it is these considerations of space, and the distinctly spatial politics of assetization, which account for the limits of the SIB enterprise.

Conclusion

In the months following the 2015 MaRS SIB session, all three charities worked tirelessly to transform their nascent proposals into fully fledged projects, but not a single SIB resulted from these efforts. This session is thus the perfect embodiment of the SIB enterprise. On the one hand, it reflects the increasingly close encounters between finance, government, and charity propelled by the power of the SIB imaginary. On the other, it speaks to how this vision has fallen short in practice. Informed by an in-depth account of the SIB enterprise, this paper has explored this tension between the promise and more complicated reality of SIBs. While the promise of SIBs has provided the perfect hinge at the level of discourse, enrolling actors across the spaces of finance, public policy, and the social sector, the elements of this financial imaginary have been difficult to translate into practice. The paper has argued that these challenges stem not only from the practical work of turning things into assets, and the contingencies and struggles which define this process, but also the differences between finance and the social sector as distinct ecologies. This reveals the value of thinking about SIBs as an inherently spatial endeavor with the work of SIB design defined by forms of translation and the deployment of devices across the spaces of finance and the social sector. Instead of hinges connecting the worlds of finance and charitable work, the valuation devices underlying SIBs—liquidity, risk, and rigor—have emerged as points of tension, reflections of a distinctly spatial politics of assetization that has frustrated SIB development in similar ways across Canada, the USA, and the UK. 9

Several implications follow from this account. First, in view of the limits of the SIB enterprise, future research must move beyond the SIB model. On this point, some might object that the imputed demise of the model is premature as SIBs continue to be developed. 10 However, recent projects look very different from the original model. Rather than a financial instrument tied to private capital and a financial imaginary (i.e., cashable savings; risk transfer; epistemic rigor), the focus is on SIBs as a policy tool and means of promoting new services. This proves the paper's point about the limits of SIBs as a financial model, while suggesting that more research is needed on these policy-based variants. The need to move beyond SIBs also follows from the shifting focus of SIB practitioners. Faced with limited market prospects, key advisory firms have moved away from the SIB model, developing new service lines including consultancy practices where practitioners work directly with governments applying the lessons learned from their SIB work in an effort to transform how governments invest in social programs. More research is needed on this evolution of the “SIB space” and how the financial logics and devices underlying SIBs are being applied in the context of non-SIB work. Of particular interest is the extent to which these efforts signal a more subtle form of financialization with governments increasingly thinking like investors (Mennicken and Muniesa, 2017) and using financial tools to allocate public capital. The question is exactly what these dynamics look like and the impact of these modes of valuation as both a “political technology” (Muniesa and Doganova, 2020) and the object of, and context for, the kinds of politics examined in this paper. Absent outside investors, these politics are bound to be more subtle, but battles will continue to be fought around liquidity, risk, and rigor as aspects of these investments and determinants of their value, reflections of the enduring boundaries between finance and society.

The paper also contributes to debates around financialization, affirming the value of more nuanced and empirically rich accounts of financialization and its limits (Christophers, 2015; Mader et al., 2020; O’Brien et al., 2019). Most notably, the SIB enterprise highlights the need to consider the spatial dimensions of financialization not simply as an extension of finance through space (Hall, 2013; Pike and Pollard, 2010), or space as a source of contingency and unevenness (French et al., 2011; Lee et al., 2009), but the differences and boundaries between financial and nonfinancial worlds. This is to think, along with the geographies of marketization, in terms of the expanding frontiers of markets and finance (Berndt and Boeckler, 2012; Ouma et al., 2013), while focusing more on the limits to these efforts and how the need to bridge the spaces between financial and nonfinancial ecologies and to construct functioning hinges renders the work of market making more difficult and subject to challenge. Ultimately, future work must consider both the topologies and topographies of financialization. Following Langley (2020), there is certainly merit to viewing the relationship between finance and society through a topological lens and in terms of the Deleuzian “fold,” a view which “expressly dissolves the imagined boundary between social and market domains” (132). At the same time, we must acknowledge the continued relevance of a topographical view, reflected in the enduring boundaries and spaces between finance and other social worlds.

This more nuanced view of the spatial features of financialization is especially critical in exploring markets in social and impact investing which raise similar questions around the extensions of market logics and the links between financial and nonfinancial ecologies. While there is a growing literature on these markets, and their politics and failures (Dempsey and Suarez, 2016; Ouma, 2020), more attention must be devoted to their distinctly spatial features and the challenges underlying the specific work of operationalizing these financial imaginaries and negotiating the boundaries between these different worlds. As per this account of the SIB enterprise, future work should engage more fully with the emerging entanglements and enduring distinctions, the topologies and topographies, which define the frontiers of (social) finance.

Footnotes

Acknowledgements

I would like to thank the editor and anonymous reviewers for their valuable feedback on earlier versions of this paper.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article. This work was supported by the Social Sciences and Humanities Research Council (SSHRC) (grant number #435-2016-1039).