Abstract

Amidst climatic and economic volatility, agricultural development and climate adaptation policies have increasingly turned to weather microinsurance to manage uncertainties, particularly in dryland pastoral and agricultural settings. While the political embrace of insurance has been cause for concern amongst those who fear insurance will undermine embedded coping mechanisms and moral economies, economists have puzzled over low insurance adoption rates amongst target populations. This article argues for an approach that scrutinizes insurance in relation to dynamic social practices and norms for responding to uncertainty. We employ this approach to investigate pastoralists’ encounters with index-based livestock insurance in Northern Kenya and Southern Ethiopia. Drawing on interview, ethnographic, and survey data, we demonstrate how insurance is understood within larger moral economies and collective imaginaries for living with and managing uncertainty in the drylands. Relational understandings shape pastoralists’ participation in risk-sharing arrangements, collective and individual decisions about livestock insurance purchase, and eventual uses of insurance payouts. Payouts also support a broad array of social reproductive purposes and investments in social and political life. As we conclude, these findings upset the binary between formal and informal insurance, revealing how “formal” index insurance must be negotiated with embedded social affiliations, rights, obligations, and understandings of uncertainty.

Introduction

Amidst the diverse uncertainties proliferated by economic crisis, political conflict, climate change, and pandemics, market-based insurance products are frequently proposed as “solutions” to be achieved through actuarial transformation of uncertainty into quantifiable risk in relation to agriculture, health, life, and livelihoods (Aguiton, 2020; Bernards, 2018, 2020; Peterson, 2012). Increasingly, both development and social safety net programs in Global South countries have turned to insurance to provide coverage for specific weather risks. But uncertainties can never be reduced to singular risks, as they intersect, overlap, and are embedded in—and magnified by—social and political relations (Scoones and Stirling, 2020). This makes the implementation and negotiation of insurance programs perennially fraught processes (Johnson, 2020).

In the drylands of East Africa, programs offering index-based insurance for pastoralists – whose livelihoods depend on herding cattle, camels, goats, and sheep over extensive rangelands – have become common over the past decade. Because the organization of pastoralist production systems on unenclosed, unirrigated rangelands appears so particularly exposed to weather variability, and especially drought, the drylands have become prime targets for experimentation with insurance interventions using weather indices. These index-based approaches use environmental measurements made over specified geographical areas as proxies for losses experienced by policyholders. They have become mainstays of global climate and disaster risk finance policy (Jarzabkowski et al., 2019) and also serve as the basis for safety-net schemes backed by governments or humanitarian agencies, including in Kenya and Ethiopia (Johnson, 2021a). Because contractual payouts do not depend on the insured's actual loss or behavior, but only on specified measured variable(s), these designs promise to make insurance more easily administered and less expensive, with fairer, quicker, and more transparent payouts. The vision is to vastly increase the scale and scope of “formal” insurance available to remote and poor populations.

For some critical political economists and development studies scholars, index insurance epitomizes the “financialization of everything,” cynically accomplished through the devaluation and displacement of deeply adapted coping strategies and mutual aid networks by neoliberal market logics (Isakson, 2014; Johnson, 2013; Keucheyan, 2018; Peterson, 2012; Taylor, 2016). The fear is that insurance will monetize and individualize redistributive social networks (Müller et al., 2017) and affective relations of solidarity (Isakson, 2015). Meanwhile, development economists have sought to determine the relationship between “formal” and “informal” insurance arrangements, asking whether market provision of insurance “crowds out” (i.e., supplants) existing informal networks or provides them additional support (Mobarak and Rosenzweig, 2013; Takahashi et al., 2019). However, to date there is virtually no ethnographic evidence about the practical encounter between rural producers, mutual aid networks, and index insurance interventions, a gap first noted by Peterson (2012) a decade ago.

We argue that both economic and critical social studies of index insurance have overestimated its potential reach and impact because they have failed to grasp its social, cultural, and political contexts and so its limits. This is a result of scholars’ strict demarcation between “formal” and “informal” insurance arrangements for responding to uncertainty on the one hand, and a preoccupation with the logic of singular insurance technologies on the other. The important critical move this article makes, then, is to illuminate the gap between the idealized, immaculate design of financial practices, and the lived relational experiences that complicate, adapt, and attach other meanings to financial designs in practice. Instead of focusing on the logic of index insurance designs in theory, as represented by development and insurance discourse, we investigate its reception and reformulation in practice: that is, how target subjects and beneficiaries have made everyday sense and use of insurance programs in ways that may or may not be consistent with the imaginaries of their designers. We show how pastoralists have engaged with a particular individualized, single-peril insurance—index-based livestock insurance (IBLI)—within the broader coordinates of pastoral moral economies and socially embedded practices for managing uncertainty.

This in-depth empirical account of relational uncertainties challenges some central individuating assumptions of index insurance design and policy. There are never singular “perils,” and only rarely singular assets or decision-making subjects. Participation in collective risk-sharing arrangements, collective and individual decisions about livestock insurance purchase, and even eventual uses of insurance payouts are all shaped by pastoralists’ relational understandings and experiences of uncertainty. By grounding this study in the negotiation between formal insurance and diverse, local practices, we identify the emergence of hybrid forms that match neither the plans and promises of insurance's promoters, nor the dire predictions of its critics.

In turn, these findings suggest a crucial reformulation of the objectives and methodological approaches that animate many critical financialization studies. Though it is certainly necessary to identify the reductive simplifications introduced by financial imaginaries, it is insufficient to conclude by speculating about the negative effects that are presumed to follow. Critical examinations must investigate how financial products entwine with, transform, and are transformed by social affiliations, obligations, rights, and understandings of uncertainty in practice. In our case, reconceptualizing insurance as part of layered and networked practices—rather than singular and individualized ones—suggests new pathways for reimagining insurance as a relational tool of solidarity, mutual care, and affinity amidst growing uncertainties in the drylands and beyond.

Our argument proceeds as follows. In Section 2, we introduce moral economies as socially-embedded systems for managing uncertainty, showing how formal economic accounts of risk and insurance minimize the significance of moral economies and entrench a misleading binary between “formal” and “informal” insurance. Section 3 situates our research design in pastoralist areas of Southern Ethiopia and Northern Kenya where an international research-development institute, governments, and private insurers have introduced various models of formal index-based livestock insurance for drought. Section 4 identifies the operational simplifications that allow for the creation of index-based contracts, while Section 5 illustrates the array of actually-existing practices pastoralists mobilize to manage livelihood uncertainties and shocks. Section 6 considers the encounter between individualized single-peril insurance with the networked, layered approaches to uncertainty in pastoralist production systems, demonstrating how these incongruities help explain the tepid reception of formal insurance, yet also allow insurance payouts to be used fungibly to support social reproduction and social relations. Section 7 concludes, abstracting principles for a relational approach to studying insurance as a technology of affinity embedded within moral economies, both in and beyond the drylands.

Beyond formal economic approaches to insurance

Both economists’ expectations of widespread formal insurance uptake and critics’ fears of the accompanying evisceration of traditional coping mechanisms neglect how people's use of all insurance strategies—market or non-market, formal or informal—are relational. That is, responses are positioned in reference to larger moral economies and available strategies for managing uncertainty. Sociologists of insurance have documented the social negotiation of insurance practices and the “economization” of uncertainty in Global Northern and mass consumer contexts (e.g., Elliott, 2021; Lehtonen and Van Hoyweghen, 2014; McFall et al., 2020; Ossandón, 2015). In examining a rural Global South context where formal insurance is rare, we attempt to articulate an understanding of uncertainty from the drylands, rather than from metropolitan centers of calculation that have defined the terms by which uncertainty has come to be understood (cf. Pollard et al., 2009).

Development economics of the early 1990s provided foundational problematizations of informal insurance and covariate shocks upon which later proposals for formal index insurance were based. Policy working papers published by the World Bank pointed to the simultaneous impact of “covariate shocks”—particularly droughts—on assets, savings, and wages of most or all members of mutual support networks (Alderman and Paxson, 1992), ostensibly rendering inadequate those risk management strategies based on kin, clan, or caste. The Bank then proposed formal market-based weather index insurance to solve the covariate problem by mobilizing outside pools of capital (Gautam et al., 1994; Morduch, 1999).

Market formality is often reified as an end in itself, and industry narratives commonly portray formal insurance as the self-evident culmination of an historical evolution toward market arrangements for risk transfer. For instance, the multilateral Access to Insurance Initiative narrates the apparently inevitable substitution of formal insurance as a response to covariate risk: “Historically, when risks are too large for individuals to manage in their own right, they have looked to pool these risks. This pooling may start through relatively intuitive, informal risk pooling and later develops into more formalized products… and eventually, insurance products provided by formal insurers” (IAIS, 2010 page 13, in Bernards, 2022). Insurance historians have celebrated insurers’ dissemination of formal insurance as the leading edge of European market reason: [T]he insurance industry increasingly succeeded in … pushing back other forms of risk protection …Quite a few cultures … offered financial, legal, moral, and ethical resistance because insurance … altered traditional forms of living together just as much as it did morality and ethics. Europeans, on the other hand…conceived [of insurance] for people who acted rationally, who wanted to change and could do so, who were decent, hard-working and productive and proposed to take risks (Borscheid, 2013).

While economists’ demarcation frequently assumes the inadequacy of informal arrangements, critical social scientists conversely assume that formal market insurance decimates functional informal arrangements. Accordingly, critical social scientists have often interpreted the growth of weather index insurance markets as disruptive, extractive, and parasitical upon longstanding methods of traditional risk-sharing (Da Costa, 2013; Isakson, 2015; Johnson, 2013; Keucheyan, 2018; Taylor, 2016). We are highly sympathetic to these critiques; yet in reifying a clear distinction between the “formal” and “informal,” they entrench this dichotomy (Berndt et al., 2020). This neglects ethnographic evidence on how people deliberately “juggle” between formal and informal systems and negotiate informal financial arrangements within formal market and state systems (e.g., Bouman and Hospes, 1994; Guérin et al., 2014; Rankin, 2008). The enduring “enmeshed relationship between formal and informal financial practices” (Guérin et al., 2011, page 103) belies the evolutionary presumption that formal microfinance can or will completely “substitute” for or replace informal financial relations. For critical studies of finance, the contingency and complexity of these enmeshed relationships must become a subject of methodological and analytical attention.

Building on a long tradition of research across the social sciences, we understand market relations—including commercial insurance—as embedded in historically-constituted social and political relations (following Polanyi, 1957; e.g., Berndt and Boeckler, 2009; Çalışkan and Callon, 2009; Parry and Bloch, 1989; Peck, 2013; Ewald, 2020). Contra the abstracted assumptions of mainstream economics in its neoclassical rational choice, behaviorist, and institutionalist forms, this approach insists that it is hybrid combinations of diverse modes of economic integration that “govern the ways in which real economies work, as… sites of multiple rationalities, interests, and values, rather than as spaces governed by singular and invariant economic laws” (Peck, 2013, page 1555).

It is in these spaces that forms of “moral economy” operate. We define moral economy as a set of social conventions and cultural norms governing exchange—socially embedded practices that redistribute risk and resources in the face of uncertainties and transformation. In Scott's (1976) account of peasantries in Southeast Asia, moral economies function as a sort of “subsistence insurance,” evening out “the inevitable troughs in a family's resources which might otherwise have thrown them below subsistence” (Scott, 1976, pages 2–3). Moral economies may be structured through, inter alia, expectations between elites and other classes of surplus redistribution, reciprocity, forced generosity, work and resource sharing, ritual sanction against untoward gains, patron-client relationships, and obligations to recapitalize kin or clan members following shocks (see also Edelman, 2012; Palomera and Vetta, 2016; Scott, 1976, page 9; Siméant, 2015; Watts, 1983). Moral economies inevitably take many forms. They are not just the preserve of local, “pre-capitalist” indigenous systems, and very often intersect with market institutions and wider state practices (e.g., Edelman, 2005; Walsh-Dilley, 2013; Wolford, 2005). Likewise, more formalized markets are never independent of social rights and obligations, but rather entwined and co-constituted with changing social and moral orders (Zelizer, 1979). Although we see value in distinguishing formal market-based arrangements for insurance from more socially-embedded redistributive practices for support in the face of uncertainty, it is the relations and continuum between the two that are especially important for understanding outcomes and implications.

Much scholarship on moral economy also uses the concept to explain the emergence of revolt and popular indignation against the growth of market forces, following Thompson's account of revolts of “the crowd” against the depredations of exploitative, capitalist market relations (see also Edelman, 2012; Palomera and Vetta, 2016; Scott, 1976, page 9; Siméant, 2015). In cases like ours, there is no outright revolt against the introduction of insurance or insurers. Nonetheless, the concept of moral economy remains pivotal to understanding the transformations formal insurance seeks to engender, given the negotiation of tradition and the shifting expectations of redistribution that accompany it (cf. Siméant, 2015).

As many have demonstrated, neither state social insurance nor market-based insurance have essential, fixed forms, but rather construct and reflect broader moral norms and social priorities (Baker and Simon, 2002; Ericson and Doyle, 2003; Ewald, 2020; O’Malley, 2002). They indicate a given society's norms of responsibility, fairness, and solidarity (Baker, 2002; Lehtonen and Liukko, 2015; McFall, 2019), indicating “the contours and limitations of mutual aid, compassion, and membership” (Elliott, 2021, page 25). After the neoliberal turn, particularly in the Anglo-American context, state-authorized imaginaries of insurance as a tool of collective solidarity were dismantled and supplanted by imaginaries of private insurance that would encourage responsibility, individual risk-bearing, and entrepreneurial self-fashioning (Hacker, 2006; O’Malley, 2002; Rose, 1999). It is largely these imaginaries that have informed the growth of index-based insurance in development programs in East Africa and elsewhere.

Yet appearances can be deceiving. Despite their market-oriented appearance, index-based agricultural insurance programs have proven far less commercially successful than backers hoped and critics feared, and frequently remain heavily dependent on government subsidies and donor support (Aguiton, 2020; Bernards, 2022; Da Costa, 2013). The IBLI program itself is a prime example. From 2010 to 2014, pastoralists received 9% more in insurance payouts than they paid in insurance premiums, a financial transfer enabled by heavy donor subsidies (Johnson, 2022, page 13).

This is not to endorse or excuse the individualized, market-based forms IBLI has taken, but to consider what these encounters with IBLI make available for critical thought. Here we follow Deborah Stone's (2010, page 54) suggestion that insurance contains “moral opportunity” for cooperation and collective repair that can provide a focus for mobilization and collective action. If we reject that homo economicus exists as such and insist that individual risk-bearing financial subjectivities and behaviors are not easily inscribed on development's target subjects (Berndt, 2015), new questions emerge. How do diverse individuals, households, and collectives gain access to, construe, and share insurance as a technology of affinity? Locating these opportunities becomes all the more necessary in conditions where uncertainty predominates, making technocratic, managerial control impossible via either state or market (Scoones and Stirling, 2020). These conditions require a greater reliance on mutual care, shared responsibilities, and horizontal accountabilities—relational approaches to uncertainty that are already evident in the drylands.

Context and research design

Our field sites are from the drylands of Northern Kenya and Southern Ethiopia, where Boraan pastoralists dominate (although in some areas of Northern Kenya, Gabra, Turkana, Rendille, and Samburu are also present). Cattle, camels, and small stock (sheep and goats) are core to the local economy, although livelihoods are also sustained from small-scale agriculture, local off-farm employment, trading and migration to towns and cities. Arid lowland areas predominate, averaging between 200 and 400 mm of rainfall annually, while highlands receive 650–900 mm rainfall, usually spread across two wet seasons. However, patterns of rainfall are changing due to climate change, resulting in increased variability in rainfall and heightened uncertainties around access to pasture for animals. Such uncertainties due to rainfall variability intersect with uncertainties due to conflict, market dynamics, external investments in infrastructure and energy development, and changing relationships with the state. With the growth of small towns in pastoral areas—such as Yabello in Ethiopia and Isiolo and Marsabit in Kenya—pastoralists are increasingly integrated in market economies and have access to financial and social services provided by the state and private sector, enhanced by widespread access to mobile phone networks and money transfer systems (Lind et al., 2020; Mohamed, 2022; Taye, 2022).

Our evidence is drawn from our long-term involvement with index-based livestock insurance programs and pastoral systems in these areas, as well as intensive fieldwork investigating pastoralists’ wider responses to uncertainty and engagements with insurance. While the research we report here was not designed as a collaboration at the outset, this article has emerged from our connected experiences over the previous decade, including research projects, PhD fieldwork, employment, and consultancy engagements.

One of us worked for the International Livestock Research Institute as coordinator of IBLI's Ethiopia program for five years. From 2019–2021, this author's intensive fieldwork in Borana, Ethiopia, focused on pastoralists’ perceptions and responses to risk and uncertainty in the context of financialization, using household surveys, case studies, ethnography and photovoice from more than 400 pastoralists in two sites, including both agro-pastoral and extensive pastoral rangeland areas. Participants included current insurance policyholders, others who had discontinued purchasing insurance, and others who had never held policies (Taye, 2022). Over the same time period, about 200 km further south, another author conducted intensive ethnographic fieldwork with the Waso Borana in Isiolo, Kenya. 1 This work employed participant observation, in-depth narrative interviews, focus discussions, and historical event mapping to trace changes in social support institutions over time, involving over 190 research participants. While not explicitly focused on formal insurance, the research explored the interaction of different forms of moral economy and their intersection with formal support systems in two contrasting sites, one more urban (around Kinna) and the other more remote (around Merti) (Mohamed, 2022). Meanwhile, one of us conducted an institutional ethnography of the IBLI project's work in Northern Kenya's Marsabit and Isiolo counties over repeated visits from 2013 to 2017. This included embedded participant observation of IBLI sales and educational extension with pastoralists, IBLI training sessions for sales agents and NGO and government partners, focus groups and interviews with insured and uninsured members of savings and loan groups, and key informant interviews with the International Livestock Research Institute team and private insurance sector partners (Johnson et al., 2019). And finally, one of us has worked on the intersections of pastoralism and uncertainty in both sites over many years and has supported the recent fieldwork (Scoones, 1995).

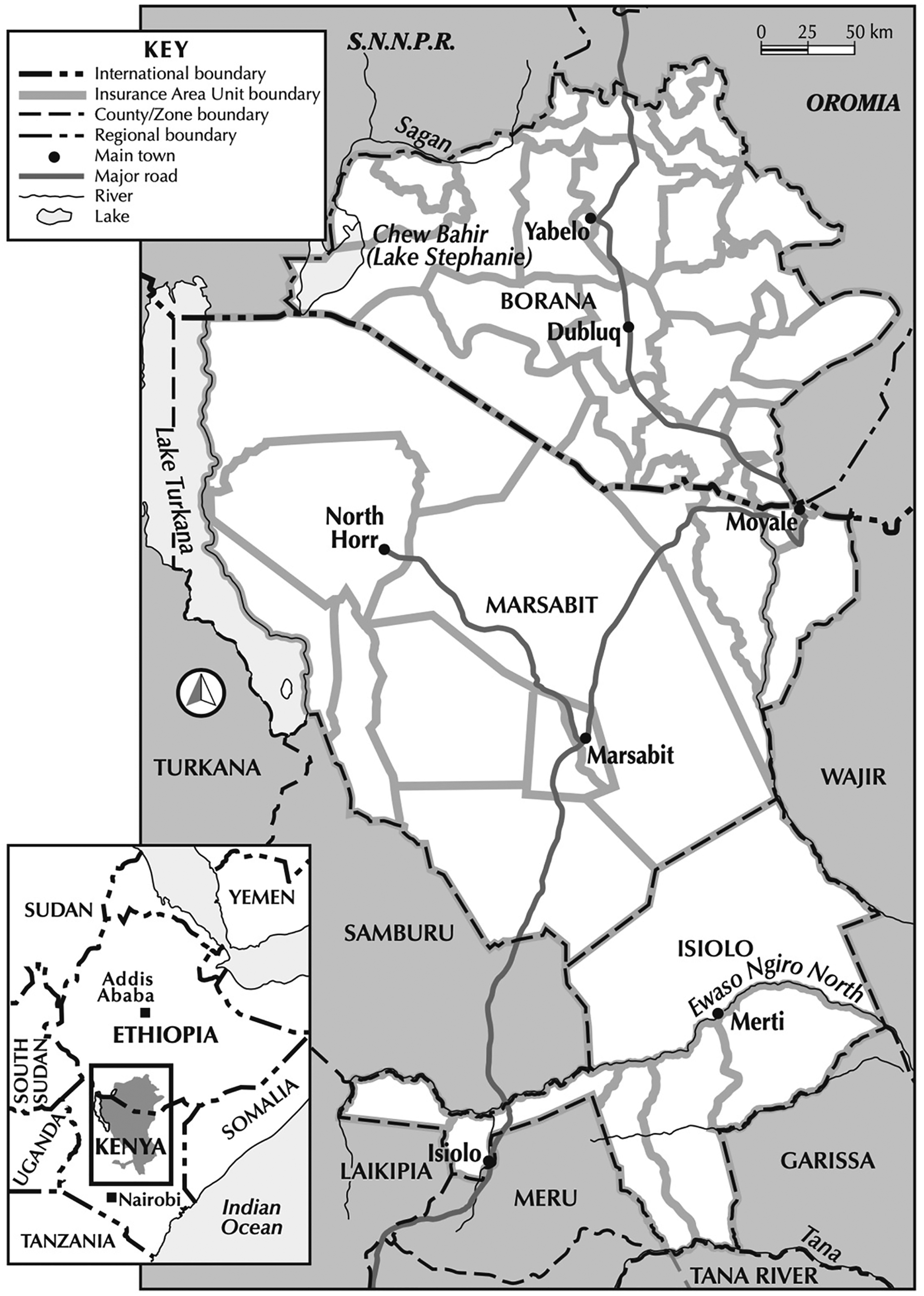

Our interest in exploring these insights further coalesced during conversations at a symposium that we all attended in 2019, and this article has emerged as a result. 2 Although the article draws on two cases (from Ethiopia and Kenya; see Figure 1), we do not develop a formal case comparison; instead we draw on detailed ethnographic insights and survey material from two locations where index-based livestock insurance has been implemented. The two sites have comparable agro-ecologies and both are considered “remote” in terms of market connections and infrastructural development. They are subject to similar climate, livestock disease, market, and other uncertainties. Despite being situated on either side of an international border, there are important social, cultural, and ethnic connections between the two sites, and the wider Boraan area is often understood as a broader, connected space, bound together by culture, language, and shared practices centered on pastoral livestock production. Indeed, the movement of people, animals, and goods across the border is frequent, although affected by conflicts and changing border controls.

Northern Kenya and Southern Ethiopia with index insurance area units.

Nation states of course have their own imprint on what were once much more fluid and connected landscapes. In particular, there are important contrasts between Ethiopia and Kenya due to the institutional contexts for formal insurance, drought management, and wider development policy, themselves the result of long histories of colonialism, state formation and international aid interventions. In both sites, livestock insurance was introduced through an aid-funded program supported by an international research-development organization. However, each insurance program has evolved differently. In Ethiopia, the program has adopted a more individual, commercialized arrangement, while in Kenya it has transitioned away from an original model based on individual purchase, ultimately developing into a public-private model in which beneficiaries’ premiums are financed by the state as part of a social welfare program. Thus, while there is broad similarity between the socio-cultural underpinnings of “informal” moral economies and the type of uncertainties pastoralists face across the two areas, their engagements with “formal” insurance have been multiple and sometimes contrasting. The two cases together therefore offer diverse examples of how these “formal” and “informal” practices intersect, illustrating the manifold ways in which pastoralists reimagine and reconstruct insurance in disparate institutional contexts.

Formal attempts at insurance in the drylands

The index-based livestock insurance (IBLI) program was designed in a collaboration between academic economists and the International Livestock Research Institute (ILRI), an international research-development organization with headquarters in Nairobi, Kenya. IBLI was first piloted in 2010 in Marsabit, Kenya, extended to Ethiopia in 2012, and later scaled up as part of government and/or humanitarian agency operations in both countries (Chantarat et al., 2013; Johnson et al., 2019). Most recently, ILRI is working with national governments to advance a regional index-based program across the Eastern Sahel and Horn of Africa, and the World Bank is channeling hundreds of millions of dollars to Kenya, Ethiopia, Djibouti, and Somalia for a program using index insurance to “de-risk” investment in pastoral value chains (World Bank, 2022).

The Kenyan and Ethiopian programs we discuss below all have their origins with ILRI's index design (Chantarat et al., 2013). The commonality across all of these initiatives is the use of a standardized, remotely-sensed drought measure. The cumulative Normalized Difference Vegetation Index (NDVI) is fed into an algorithm that triggers payouts over an entire geographic area unit, standing in for assessment of individual livestock losses. In essence, the product is a derivative contract settled on a measure of forage availability.

There are at least three variations of insurance form. The first is heavily subsidized, NGO-facilitated commercial microinsurance. In the Marsabit pilot, later expanded to several other Northern Kenyan counties, ILRI conducted the majority of insurance education and marketing to pastoralists. Although IBLI policies were underwritten by Kenyan insurance companies, pastoralists’ premium payments were heavily subsidized by donor funds (Johnson, 2022). The second variation is more commercially-oriented microinsurance, exemplified in Ethiopia, where the Oromia Insurance Company took on field operations and pastoralists’ premiums were minimally subsidized for a short period. The third variation is a public-private safety net model, illustrated by the Kenya Livestock Insurance Programme (KLIP) launched in 2015. The national government uses funds from the National Treasury to pay premiums to a commercial insurer, insuring up to five tropical livestock units (5 cattle, 50 goats or sheep, or 3.5 camels) per named beneficiary. Beginning in 2022, government subsidies were to be reduced from 100% to only 50% of the premium. Although this program bears a resemblance to the initial heavily-subsidized commercial microinsurance model, here the government—not donors—identifies eligible beneficiaries and funds premium subsidies.

All index insurance products are assembled and implemented through a series of technical, social, and political assumptions and simplifications (see also Aguiton, 2020). Most foundationally, IBLI is premised on the assumption that a co-variate drought peril is the predominant risk pastoralists face, and that any remaining idiosyncratic risks can be managed through individual informal local coping mechanisms (Chantarat et al., 2013). If drought is a generalized phenomenon that affects everyone within a defined area, then particular interacting factors—e.g., pastoralists’ ability to move animals, provide labor, treat diseases, or offer supplementary feed—become less significant influences on livestock mortality and livelihood outcomes. IBLI thus encodes a particular set of simplifications about the relationship between drought, vegetation cover, and pastoralist livelihood outcomes.

The product also requires a number of spatial and temporal assumptions. Index values are calculated and spatially averaged across specified geographic areas (see Figure 1). Contracts are issued for a named insured area unit, and the index represents aggregated vegetation readings in that unit over a particular time period. If a unit's index value falls below a threshold percentile of normal historical seasonal vegetation, this “triggers” a payout to policyholders. The index's ability to flag correctly an extreme condition depends on both satellite-based sensors’ technical ability to detect the current forage available for livestock, as well as analysis of past seasons in the historical record to calculate deviations from the “normal.” This poses a number of challenges. First, as sensors on earth-observing satellites have changed and been replaced over time, the spatial resolution, spectral wavelengths, and algorithms used to generate products like NDVI have changed. 3 This means current and past data are incommensurate, requiring extensive calibration and interpolation to generate historical records adequate for insurance pricing (Vrieling et al., 2014). The non-equilibrium dynamics of pastoral rangelands (Behnke et al., 1993) pose a further problem for products based on assumptions of statistically “normal” or “average” conditions.

The spatial aggregation of NDVI readings across insurance area units mobilizes social and ecological simplifications as well. Any vegetation sensed within the unit is treated as equally available to all livestock grazing there. This assumes, first, that all pastoralists in the unit have similar abilities to move their animals and access all the grazing areas within it and, second, that all vegetation is equally edible by all insured species (cattle, camels, goats, and sheep). Both simplifications are inaccurate. Insured area units were originally based on administrative-political boundaries, which roughly correlated with traditional grazing territories. Such territories can be overlapping and contested, and some units aggregated dramatically different agroecologies into a single reading. In response to complaints from pastoralists about these simplifications, index designers at ILRI subdivided several of the original insurance area units in later years (Johnson, 2021c). Nonetheless, not all insured pastoralists are equally able to move their animals within a unit, and forage needs vary dramatically across species. Small stock in particular are able to survive off of browse, including shrubs, while cattle require the most intensive grazing on grasslands.

Pastoralists’ recent experiences have painfully highlighted the failures of formal insurance in the face of intersecting uncertainties. Following a severe drought in 2017, good rains in 2018 had begun to revive pastures. Nonetheless, most areas of southern Ethiopia and northern Kenya fell into another drought in mid-2019, followed by heavy rains and flooding during the last quarter of 2019. Grazing was plentiful in some areas, but waterlogged in others. Around this time, massive swarms of locusts across the Horn of Africa removed available grass in huge quantities. Then, in 2020, governments implemented lockdowns in response to the Covid-19 pandemic. Although Covid-19 rates remained low in pastoral areas during this time, restrictions closed markets and dramatically limited the movement of people and animals, making it extremely difficult to transport animals, fodder, and water in response to diminished grazing (Simula et al., 2021). Yet there were no IBLI payouts in 2020 because the period of satellite assessment coincided with higher—indeed, excessive—rainfall, and thus higher aggregate vegetation cover. In Ethiopia in 2021, there were again no payouts, although in this case the index failed to reflect the reality of cumulative intense drought on the ground. Pastoralists’ preparations to sue the insurer prompted the company to issue discretionary ex gratia payouts to quell client grievances. By early 2022, forage conditions across the region were extremely poor, reflecting the ongoing drought across the Horn of Africa; during this period the IBLI index triggered major payouts across almost all insured area units in Borana, Isiolo, and Marsabit, although many clients still perceived these as too little, too late.

With the exception of 2021, the lack of payouts we describe was not the result of a technical error or miscalculation. It was a logical corollary of the simplifications necessary to make an index “work” as a calculative device to adjudicate losses remotely. Although well-designed insurance that pays out when it is supposed to can have valuable benefits, the nature of contracts based on environmental indices dictates that, by definition, there will be numerous times when contracts do not pay out, even though policyholders have experienced a welfare-depleting loss—a mismatch known as “basis risk” (Jensen et al., 2016). This arises from index insurance design, which follows from an ontology of singular events and individual subjects: an individual insurance contract is designed to secure against discrete defined shocks, affecting a specific asset, purchased by an individual person, who will use any payout on expenditures related to the asset. If these covariate shocks alone are less significant than contract designers expect, the insurance tool may have limited value or relevance to the target population, and an expenditure on insurance may actually leave them worse off (Carter and Chiu, 2018; Clarke, 2011).

While the sequence of events between 2019 and 2022 was particularly dramatic, each year sees a set of uncertainties unfold, with different sequences and spatial imprints. Longitudinal household surveys have suggested that IBLI's vegetation index correlated with only 30 percent of the herd losses that households experienced, while the remaining 70 percent of livestock mortality resulted from idiosyncratic variation, uncorrelated with observed household characteristics or herding practices (Jensen et al., 2016). These causes of death could include livestock disease, predation by wildlife, flooding of pasture, or lack of access to veterinary care. Basis risk was therefore considerably higher than estimated in economists’ original design (Chantarat et al., 2013). Yet, despite this dramatic limitation, cushioning this 30 percent of losses with insurance payouts seems to have meaningful welfare impacts for those who are covered: insured households were less likely to resort to skipping meals or selling animals during a drought, spent more on veterinary care, produced more milk, and had higher incomes and fewer livestock losses (Janzen and Carter, 2013; Jensen et al., 2017). While index insurance fails to account for all or even most sources of uncertainty that pastoralists face, it appears to provide material benefits for certain events. Studies suggest that IBLI is more effective and efficient at securing these outcomes than a parallel unconditional cash transfer program, the Hunger Safety Net Programme (Jensen et al. 2017), yet there continue to be important questions about the relative costs and benefits of subsidizing private insurers to provide social protection (Johnson, 2022). This recognition of insurance's limitations and possibilities therefore motivates our call to rethink insurance as a relational tool within layered and networked practices of solidarity and mutual support.

Practicing social relations in pastoral drylands

Hoorriin kaa Boraan Balla

(“Livestock wealth belong to the larger Boraan”)

-Boraan phrase

Living with and from uncertainty is fundamentally reliant on a complex of social practices and negotiations embedded in relations and networks stretching between the individual and household to wider society. These social relations have typically been the foundation of pastoralists’ response to diverse, intersecting uncertainties—whether via routine strategies like organizing herding labor for transhumant movements to distant pastures, or novel ones such as getting young men to ride their motorbikes to disperse locusts. What economics stylizes as “informal insurance” encompasses a diversity of syncretic practices based on various identities and associations. These practices range from everyday informal reciprocity to more formalized arrangements mediated through clan or religious institutions. We review these here to provide a sense of the existing social coordinates into which formal insurance is introduced.

The dominant principle structuring pastoralists’ relations of care, mutual support, and redistribution in much of East Africa is the exchange of animals in order to maintain social networks. Although norms differ based on ethnic group and clan, such networks, created by investment of surplus stock in “marriage alliances, bond friendships, patronage, hospitality and the like…spread risk and foster reciprocity” (Waller, 1999, page 42). Herd pooling, herd labor sharing, and livestock gifts and loans are all routes to recovery after major losses (Broch-Due, 1999; Dahl, 1979).

Intra-household and intra-generational relations are a cornerstone of many strategies. Herds are typically split between home and satellite camps, with women and younger children looking after pregnant, lactating, and young animals at home, while men and older boys herd animals across vast rangelands and at satellite camps. Parents and grown children may jointly hold livestock so as to pool labor and remittances to manage the wider herd. For instance, in Korbesa, Kenya, brothers Kiyya and Jillo own a large number of animals that remain under the custody of their mother Tume, who manages the herd with Kiyya, while Jillo works in town and sends remittances to pay other herders. 4

Herding arrangements often extend beyond individual households to join forces with other kin or clan members. Reallocating animals through stock sharing, loaning, and entrustment is a common risk reduction strategy, orchestrated through strong social relationships. Trust is pivotal, as valuable animals are passed on without close management supervision. Many of these arrangements are developed through informal relations, but are embedded in long-established cultural practices and family, kin, and clan networks, which act to enforce agreements if things go wrong. Families who pool animals also commonly hire herders to assist with large, shared herds and flocks. Although hired laborers augment herding capacity, they also introduce another element of uncertainty, since they are entrusted with huge responsibilities to care for animals across vast distances. In Lakole, Kenya, Boru explained his family's combined strategy for reducing both environmental and labor uncertainties: We have camels, cattle, and small stock and due to the diverse needs of the animals, we disperse them in different places. We often combine our stock with Galgallo's family and supervise in shifts. We have also hired herders for each species. Joining our herds and sharing labor costs provides us with extra time to spend on other business activities in town and also provide proper care to the animals, rather than entirely entrusting them with hired herders.

5

Yet Boru and the Galgallo family cannot simply disperse their combined herds wherever they please. East African pastoralism has a long tradition of collective institutions for pasture management (in Boraan, dheedha), which governed decisions regarding where and when animals may be grazed and watered (Dahl, 1979; Oba, 1996). Although such institutions no longer function in the ways they once did, new institutions governing movement and access to grazing have emerged, still often associated with the use of well sites (Swift, 1991; Tari et al., 2015). In the Merti area of Isiolo, Kenya, a Resources Users Association that governs seasonal grazing stipulates that livestock should only be grazed and browsed near boreholes in severe dry periods, while pasture on the Waso plains, rain pools, and water pans should be used in the wet season. In Borana, Ethiopia, water and pasture are managed under the umbrella of the customary Gada administration. Local members select councilors for the management of water and pasture who assess both the area's available resources and seasonal demand to set use regulations accordingly.

Pastoralists frequently make and receive calls for assistance through loans or gifts, guided by social and moral norms of reciprocity – reciprocal exchange between parties enacted over time. Dabarre (long-term loaning of animals), amesa (loaning animals for milking), and livestock gifting are deeply ingrained cultural practices to help clan members in need. In Kinna, Kenya, Mohamed explained: “I can never let anyone who comes to my enclosure leave empty-handed because they will definitely help me when I am in need. When I lost many small stock to hyenas in 2017, I received several phone calls from different people asking me to come and collect animals. In the end, I received more than I lost!” 6 Repeated over time and between different households, such exchanges deliberately create webs of relational expectations, obligations, and interdependent support networks.

In the Boraan worldview, animals belong not to individuals, but to the “larger Boraan.” An individual who loses animals may request to be restocked by the community, but if they have not previously “invested” in others’ livestock by giving in times of need, elders declare “loon ka uufi d'abee hin hirbinaafi” (they lost their own livestock, do not restock them). Such a person is said not to know that livestock belongs to all Boraan and is consequently dismissed as selfish and excluded from hirba (restocking). Thus ironically, the assumption in insurance design that livestock are an individually-owned asset only easily maps on to those whose decision to withdraw from community moral economies have led them to be excluded from collective risk-sharing networks.

Other more structured relationships are based on obligatory ties. In Kenya, organized collective Harambee (“all pull together” in KiSwahili) practices are prevalent in response to various life events and uncertainties. Leaders mobilize the wider clan to contribute to events including weddings, orphan support, medical needs, and restocking of vulnerable families. With the growth of Islam in northern Kenya, Zakaat—the religious obligation to donate and support others—has also gained prominence. For instance, a mosque in Merti, Kenya organized a Zakaat collection following a series of local disasters in 2018. The collection gathered four cattle, two camels, and 18 small stock, which were redistributed among needy and poor pastoralists, amongst them Kaduubo, who had lost some of his small stock to wildlife attacks. Because performing Zakaat is a form of religious adherence, those who do not contribute are admonished, and their wealth is considered unlawful (haram) until they pay the Zakaat due.

Such forms of organized sharing and redistribution are confirmed through membership—of a mosque or a clan for example—and may involve ritualized association to bind people together within age-groups or the wider society. The ritual induction of members into a Busa gonofa society involves publicly pledging to uphold ones’ obligations to share animals and support others. In our Ethiopian case, regular clan contributions consisted of monetary and material contributions, including livestock, guns, and bullets. Clearly, members are bound together to provide security for far more than drought risk.

Yet such pastoralist practices are not inherently egalitarian or universally inclusive, nor do they necessarily provide minimal subsistence for all. For example, Hawo and Guyo from Isiolo's Kinna area lost around 100 small stock to hyena attacks, but were unable to seek out clan elders for help, as Hawo had just given birth to their son and Guyo was away managing cattle. As a result, they received nothing. Access to support also depends on one's ongoing generosity in clan contributions, and the extent to which clan leaders advocate on behalf of their poorest members to secure support from wider Boraan networks.

The mechanisms of reciprocity and redistribution that were credited with ensuring a relatively even spread of livestock resources in the past no longer accomplish the same “levelling effect,” if they ever truly did so (Waller, 1999, page 41), and poorer pastoralists may be excluded, forced to migrate or take up non-pastoral livelihoods (Broch-Due and Anderson, 1999; Santos and Barrett, 2011). Increasing social stratification and class formation have emerged from a process of commoditization and growing market orientation, leading to the breakdown of redistributive practices and growing individualization of economic relations (McPeak et al., 2012; Scoones, 2021). In East Africa, these trends have been exacerbated by inter-ethnic conflict, political instability, famine relief interventions, and sedentarization (Fratkin and Roth, 2005; McCabe, 1990).

The encounter between insurance and uncertainty in the drylands

These complex moral economic dynamics clearly influence how pastoralists have encountered and engaged with formal insurance in our case study sites, leading to more limited and uneven purchase than product designers expected. In this section, we trace the encounter between the logic of insurance policies and pastoral systems. Although early studies in Kenya estimated substantial “willingness to pay” for insurance—with surveys and field experiments suggesting 36 percent of pastoralist households would pay a commercial price and insure 71 percent of their herds (Chantarat et al., 2009)—actual results were far different. When the product was marketed in Marsabit, the most successful sales season saw only three and a half percent of the county's total households purchase coverage. 7 Most insured only a handful of animals, and sales declined quickly in later seasons, with few renewals. Equally, in spite of aspirations to offer an accessible pro-poor product, long-term sales data from Ethiopia suggest that it is primarily richer male pastoralists who renew their contracts. 8

Pastoralists encounter formal insurance in ways quite unlike those supposed by program designers and implementers thanks to the radically different ontological and epistemological frameworks through which they understand uncertainty. In contrast to methodologically individualist assumptions about property in animals and purchase choices, pastoralists’ decisions about insurance purchase and use of payouts are influenced by matrices of affinity, collective expectations, social ties, and obligations. And rather than seeing risks as singular “perils” associated with particular “events,” they often adopt a more expansive, cumulative framework in which plural uncertainties become most significant when they are overlapping. In Borana, Ethiopia, Glicha Galgalo reflected on the interwoven uncertainties that contributed to his shifting welfare over time: Over the years I have met many challenges. Sometimes I have been rich with many livestock, sometimes poor with few. Challenges have been drought, human disease, government policy, conflict, livestock disease, livestock trade, prices, and issues around the border controls. The unfortunate part is none of these happen alone.

9

The covariate shocks of economic theory are not neatly separable from the idiosyncratic risks pastoralists face as they manage herds. While a drought is defined in climatological terms as a significant shortfall of precipitation, and in IBLI index terms as a lack of vegetation, pastoralists experience the climate event only in relation to other factors that impact forage availability, grazing, and livestock management. A proverb from Isiolo, recounted by pastoralist Edin Boru, illustrates these relational terms: “Although we are concerned about drought, it does not defeat us. As our elders put it, ‘drought does not kill the animal that has someone to manage it’. Livestock die of drought due to lack of proper management.” 10 In one year, reduced rainfall may be disastrous—as when locusts wipe out the available grazing—while in another, animals can be moved to refuge grazing without difficulty. In still other years, conflicts with neighboring groups may mean refuge areas cannot be reached, or it may be impossible to herd animals to lowland key resource areas due to a shortage of herding labor. Such uncertainties clearly interact and may change year on year in unpredictable ways. This means that in practice, there is no easily administered formula to distinguish between a bad drought and a tolerable one.

To buy or not to buy

We can thus begin to understand why expectations of wide and sustained uptake proved so unrealistic. Decisions to purchase insurance are complex outcomes of capacity, affinity, expectations, and trust, mediated by one's access to other coping strategies. Some simply lacked the necessary cash at the time premium payments were due; some women may also have been unable to access cash typically held by husbands. Cultural, religious, and ethnic values were deeply significant, too. Many Muslims initially avoided the product out of concerns that it violated prohibitions against gambling. Despite the arrival of a Somali Kenyan company providing Islamic Takaful insurance in 2013, some village religious leaders took a more conservative interpretation of Shariah (Islamic law), advocating for the long-standing Zakaat system of charity governed through the mosque rather than insurance through an unknown company. Finally, drought events that did not trigger payouts stoked discontent with the product, resulting in community organizing and backlash (Johnson, 2021b). Illustrating these affective, layered uncertainties, Yaya from Borana, Ethiopia explained why he did not renew his contract: Following my first insurance purchase, I received information about a huge payout from the local mobilizer. But I do not know why the insurance company did not transfer the payout to my bank account. I just lost trust and decided to drop out of the scheme. How could someone I don’t know give me so much money? Investing such amounts will be gambling, which is prohibited.

11

Insurance providers attempt to counter such doubt, working with local institutions and influential individuals—churches, mosques, savings groups, burial societies, chiefs, NGO projects, and local government officials—to link insurance sales with sources of authority and garner trust. Many sales agents are pastoralists who buy insurance themselves, offsetting fears and suspicions. In some places, the agent is well-respected and highly persuasive, while in others the agent is dismissed amidst circulating rumors about exaggerated benefits, misuse of funds, and untrustworthy payment methods.

Crucially, decisions to buy insurance are not purely individual, but rather the unpredictable results of collective processes and wider social relations. Purchasing insurance is often an intensely social, deliberative, and uncertain process in which individual “adoptions” may actually represent experiments by wider social networks. Participants in the IBLI Marsabit pilot often entered into insurance contracts as an experimental social endeavor. In some women's village savings and loan self-help groups observed in 2013 (Mburu et al., 2015), women coordinated trial purchases of IBLI strategically; a few group members insured a handful of sheep and goats to act as a test for the rest in the group. Pastoralists also attempted to transfer experimental discount coupons from ILRI's pilot study to non-study households. Such examples upend the models of discrete individual decision-making on which willingness-to-pay studies are based.

Finally, livestock insurance rests on a presumption that animals are alienable property, owned by individuals or households who make autonomous choices to purchase insurance for their assets. Yet in pastoral settings, animal “property” is often mutable and collective, with rights over animals varying over time and across different people (Khazanov and Schlee, 2012). The idea of an individual animal as singular property of one person is alien to Boraan practice. Property in animals is more about relations, and so multiple and overlapping, than things (Schlee, 2012). Loaned or shared animals, women's stock, and those inherited by children before fathers die may have multiple claims and no neat property definition. Thus, deliberations about livestock management across families, between kin, and more widely within the clan are the norm, rather than the exception.

Given that traditional Boraan forms of moral economy are intensely collective, individualized private arrangements are often frowned upon, and the interplay of formal and informal insurance imposes a new set of negotiations. For instance, in Ethiopia, 46 year old Bokayo, a female head of household, intended to renew her livestock insurance policy, believing that the upcoming rainy season would be poor. Women-headed households like hers accounted for 31 percent of IBLI clientele in Ethiopia up to 2017. 12 Yet Bokayo struggled with how to negotiate informal and formal demands. Because she is not wealthy, and is a widow, she had typically been exempted from contributing labor or resources to community well-digging projects. But community members, aware of her insured status and her intention to pay an insurance premium, pressured her to use her funds to pay for the labor of well digging and repair, and to support community migration to remote pastures. Meeting the community's moral economic expectations with these outlays would prevent Bokayo from purchasing IBLI, and at the time of the research, she was at an impasse, unable to decide how to negotiate these demands. In this case, the continuing need to sustain social ties and informal community support networks—on which Bokayo still heavily depends—complicates and constrains the advance of formal insurance.

Obligations to the collective also generate strain and tension for those with significant numbers of animals, who face enormous pressures from kin and clan members to give loans, support families with food, and generally provide assistance to those in distress. Some pastoralists in southern Ethiopia admitted they sought to escape these redistributive expectations through private insurance purchase and deliberately hid their decision from others (whether to avoid social censure for their individual strategy or to evade pressure to redistribute payouts). Some felt freed by the escape from collective responsibilities and social arrangements, echoing Bähre's (2020) findings in South Africa.

For some wealthy pastoralists—adult men in particular—livestock insurance has become part of an individualized investment strategy. They combine insurance payouts with private resources (accumulating feed and crop residues) to sustain large herds in place, instead of leading communal transhumant movements to distant pastures as wealthy adult men would traditionally do. Private resources allow them to evade collective norms and communal drought-response responsibilities. Agents and extension messages play into these sensibilities, advocating insurance as an abstract market product that promises a route to emancipation, individual gain, and self-improvement.

As these examples demonstrate, it is critical to avoid artificially delineating “formal” insurance products from the broader social relations into which they are introduced. Formal insurance necessarily encounters systems that are already partially integrated into other market relations. Insurance is rarely a strategy pursued in isolation, nor does it appear to be the first commercial exchange that sets off a “domino effect.” Even without insurance, in both our Ethiopian and Kenyan sites, wealthy herders already commonly resort to commercial arrangements such as purchasing fodder and hiring herding labor to avoid moral economic norms. Yet there are still powerful reasons to remain embedded in obligations to kin and clan. Holding individual insurance coverage does not necessarily or even usually signal an exit from these wider moral economies. Not surprisingly, we find that pastoralists partially integrated insurance benefits and payouts into their existing strategies for managing uncertainties.

Insurance payouts

When index insurance payouts are triggered, highly publicized and orchestrated ceremonies often follow. Insurance company personnel distribute giant symbolic cheques printed on placards in front of local dignitaries and selected pastoralist beneficiaries 13 , and media reports enthusiastically construct an image of progressive pastoralists released from backward practices taking on new, market-oriented personae. In this trope, insurance allows pastoralists to intensify and manage livestock herds more effectively.

Yet when payout monies are disbursed, they are not usually used to invest in “productive” livestock related-investments such as fodder, water, or veterinary services. Money is used strategically and fungibly for a range of social reproductive needs that shift depending on the season, a household's health and wealth, pre-existing obligations, and the availability of other aid. Some use payouts for immediate household needs, while other invest in social ties and reinforcing existing collective arrangements. This fungible use of payout money stands in contrast with anthropological findings on compartmentalization of money and credit from different sources (Guérin et al., 2014; Zelizer, 1994). Not surprisingly, payout uses appear to differ depending on the insured's wealth. Surveys in Ethiopia in 2019–2020 suggest richer livestock keepers 14 did indeed use payouts to support their herds, while non-wealthy pastoralists used the money to purchase food for their households, expand agricultural activities, or finance trading activities (Taye, 2022).

Household surveys in both Kenya and Ethiopia suggest the significance of payouts in sustaining basic household expenditures and social reproduction. Analyzing longitudinal surveys from Marsabit, we find that households reported using the majority of their insurance payouts from 2011 to 2015 on social reproductive expenditures (see Appendix Table 1), spending 53 percent of total payouts on food and 20 percent on school fees and associated costs; distantly trailed by livestock purchase (eight percent) and livestock production (five percent). Even in 2015, after the contract's design changed to make earlier payouts to enable clients to purchase fodder, water, and veterinary inputs for animals, 93 percent of expenditures went to socially reproductive purposes. Cross-sectional surveys collected in both Kenya and Ethiopia during the 2016–2017 droughts suggest households continued to use payouts for food and educational expenses, as well as ceremonies (weddings, rituals, and social events); repaying debts; livestock sharing and loaning; and cash transfers to others, especially poorer kin (Taye et al., 2019). In these examples, for some IBLI supports part of a de facto social reproductive safety net, partially integrated into government programming via Kenya's Livestock Insurance Program (KLIP).

Although pastoralist encounters with insurance are highly differentiated by wealth, age, gender, location, and so forth, there are clear contrasts with the individualist and event-based assumptions of insurance design. Insurance enters into a wider set of support relationships, becoming at least partially integrated into the social moral economy, rather than distinct from it (Rodima-Taylor and Bähre, 2014; Shipton, 2014). It is not surprising that the socio-technical practices of market-based insurance become embedded in local social and political relations, yet these outcomes are contingent and complex. They are predictable neither through economic analyses of individuals’ willingness to pay, nor by models that assume “informal” local moral economies will be eliminated by market risk-bearing mechanisms. Diverse, hybrid relations are the norm.

Conclusion

The arrival of technical forms of drought insurance for pastoralists in Kenya and Ethiopia has generated ambiguous, hybrid outcomes. While some pastoralists have welcomed index insurance products for livestock as an escape from the strictures of community and kin obligations, others have ignored them altogether. Yet many have understood individualized insurance through matrices of embedded social relations for risk sharing and coping, into which they have selectively incorporated “formal” insurance tools.

This was not the reception anticipated by IBLI's designers, who imagined the straightforward uptake of individual policies for a single drought peril. Nor does it reflect a simple tussle between the assumed opposites of “modern” markets on the one hand, and “traditional” reciprocities and redistributive moral economies on the other (Bähre, 2020; Parry and Bloch, 1989; Strathern, 1988). Rather, our evidence demonstrates a complex comingling of multiple modes of economic integration and accompanying social negotiation of meanings and obligations between different modes of insurance, both formal and informal.

IBLI was launched with the hope that it would dramatically expand the scale and scope of formal insurance, and so increase social protection and human welfare within the drylands. In practice, this vision has proven far more difficult to achieve—in part because of the limitations of index-based design, but in part because formal, market-based insurance must always intersect with more informal, local arrangements. Many critical studies might overlook these limits and nuances, pursuing only the impulse to scrutinize the disciplining, rationalizing logics of formal insurance. Yet this impulse does only half of the work.

Following a relational approach, the fact that “uptake” of the insurance product was selective and limited is unsurprising. Formal insurance holds no particular pride of place in the drylands. Insurance is always understood from within local moral economies and repertoires of exchange, in which it figures as just one amongst a diverse set of relational tools for confronting uncertainty. These include networked household relations, friendship, kin and clan relations, obligations via social and faith-based organizations, and reliance on the spirit world (eg. Shipton, 2014). Pastoralists’ hybrid strategies combine livestock insurance with a variety of livelihood responses for sharing and redistributing risk, including herd mobility, animal entrustment and adoption, and sharing and gifting relations. The resulting negotiation leads inevitably to hybrid and diverse outcomes, and limits the supposed inexorable advance of financialization.

We conclude with a set of three principles and questions to motivate critical geographical and development studies research on the practice of insurance in spaces far beyond East Africa's drylands. While these principles reflect analytical moves familiar to economic sociology and anthropology, they have been largely neglected by much economic geography and development studies, and noticeably absent in scholarly conversations about index insurance. We propose these principles with the belief that the pooling technology of insurance can in some circumstances become a valuable technology of affinity, mutual care, and solidarity amidst uncertainties—but only if it is one amongst diverse practices of responding to uncertainty.

Our first principle is methodologically socializing insurance. This stance rejects the narrow methodological individualism of many economic assessments, exploring socially-situated understandings, norms and practices of insurance from the perspective of social participants. This requires recognizing the spectrum of participants’ relations to uncertainty, rather than strictly demarcating between in/formal arrangements and un/insured risks. It also calls for tracing the post-payout travels of transfers, refusing tendencies toward individualization that assume payouts end with the individual, or that recipients treat them as compensation for particular losses.

Our second principle is querying insurance solidarities. By what logic does a particular insurance operation bind individuals or collectives together to assemble a larger “community of fate” (Elliott, 2021)? How are socio-spatial relationships effaced or embraced in different models of insurance risk pooling (e.g. Christophers et al., 2020) and index unit construction? By what criteria do members join the pool, and to what degree is this geographically constructed solidarity understood as socially legitimate? To what extent does, or can, insurance support rather than replace relational networks rooted in interpersonal ties?

Our third principle is attending to exclusions. How do power, inequity, and conflict manifest in inclusion and exclusion from socialized practices for responding to uncertainty? How are these evident in moral economies both with and without insurance? How does formal index insurance amplify or mitigate the dynamics of exclusions?

This research agenda is especially pressing given recent trends in international policy and funding for “climate risk insurance,” which is usually index-based (Johnson, 2021a). Of recent note, the landmark agreement to finance Loss and Damage at the 2022 UN Framework Convention on Climate Change (COP 27) was brokered in concert with German-led G7 proposal for a “Global Shield,” in which significant financing will be channeled to scale up insurance arrangements. Meanwhile in the Kenyan and Ethiopian drylands, multi-million-dollar programs aimed at “derisking” through index insurance are in development (World Bank, 2022). Understanding both the effects of these efforts and their limitations requires going beyond the narrow framing of index insurance as an individual response to a singular peril operating in a separate market sphere. Instead, research must illuminate embedded responses to uncertainty and diverse forms of both “formal” and “informal” insurance. These principles are all the more crucial as insurance products become increasingly frequent techno-managerial interventions in an uncertain world.

Supplemental Material

sj-docx-1-epn-10.1177_0308518X231168396 - Supplemental material for Uncertainty in the drylands: Rethinking in/formal insurance from pastoral East Africa

Supplemental material, sj-docx-1-epn-10.1177_0308518X231168396 for Uncertainty in the drylands: Rethinking in/formal insurance from pastoral East Africa by Leigh Johnson, Tahira Shariff Mohamed, Ian Scoones and Masresha Taye in Environment and Planning A: Economy and Space

Footnotes

Acknowledgments

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

Mohamed, Scoones and Taye were partially supported through a European Research Council Advanced Grant to PASTRES (Pastoralism, Uncertainty and Resilience: Global Lessons from the Margins, pastres.org), Grant number 740342. Johnson's work was partially supported by a Swedish Research Council grant for the project “Climate Change and Transformations of Financial Risk” (2015-01694). IBLI survey research was funded by the Australian and UK governments, and the EU through a UKAID Accountable Grant Arrangement for Index-Based Livestock Insurance, Arid Lands Support Programme, project code 202619-101, and the CGIAR Research Program on Dryland Agricultural Production Systems.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.