Abstract

This paper examines Sino-UK financial relations in the fintech sector. Through an empirical focus on fintech payments systems, the analysis locates fintech within broader research on the internationalisation of Chinese finance. Conceptually, the paper responds to calls for more attention to be paid to state actors in fintech development. By examining the relationship between the UK and China in fintech, as part of the UK's wider role in Chinese financial internationalisation, I argue that such a focus on the state needs to be expanded beyond the current focus on domestic policy to include wider questions regarding how fintech sits alongside overseas and international policy concerns. I suggest that one productive way of doing this is to understand fintech as a monetary infrastructure. In so doing, the paper argues that fintech needs to be understood as much as a monetary geography as it is a financial geography.

Introduction

Since the early 2000s, the place and power of Chinese finance within the international financial system has changed markedly. Prior to 2004, trading denominated in the Chinese currency, the renminbi (RMB), was prohibited outside of mainland China. Over the past 15 years, the growing political appetite within the Chinese Communist Party to use financial markets to stimulate growth within the Chinese domestic economy has provided the onshore preconditions (Lim, 2019) within mainland China for a transformation in China's financial services sector as it has becomes increasingly internationally focused. Multiple policy areas have been involved in this transformation. These include: the gradual opening up of China's capital markets to international finance since 2002 (Töpfer and Hall, 2018); the increasing internationalisation of assets held by Chinese banks as they follow their clients as they ‘go global’ (Wyman, 2020); and the broader internationalisation of financial institutions to support China's wider Belt and Road Initiative. Each of these developments signals the different and varying ways in which the state is entangled with Chinese finance (Chen and Rithmire, 2020; Kennedy and Blanchette, 2021).

In many of these policy domains, China can be understood as developing domestic responses to already well-developed markets in other countries. The case of fintech is different because fintech has grown faster, and in different ways, in China compared with other markets (Chen, 2016). Rather than starting from a position of what has been termed currency subordination in relation to currencies such as the RMB internationally (Kaltenbrunner and Painceira, 2018), in the case of fintech, China is increasingly identified as global superpower in technology (Deutsche Bank, 2020). For example, 46% of fintech investments made globally in 2018 were in China, with more than half of this involving Ant Financial, a mobile payments provider linked to the online marketplace Alipay discussed in more detail in this paper (Accenture, 2019). As these figures suggest, the fintech landscape is also distinctive in China when compared with other financial centres. In China, Fintech is dominated by firms such as Ali and Tencent which are best thought of as part of the wider BigTech sector. In contrast, in Western Europe, fintech is best thought of as a series of smaller firms that intersect with existing financial and monetary networks (see Arslanian and Fischer, 2019; Tanda and Schena, 2019). China's dominance of global fintech, and its distinctive organisational structure, raises important questions regarding the different ways it may be enrolled into the international financial system compared with other types of financial markets (on which see Hall, 2017).

In response, in this paper I examine the ongoing reconfiguration of fin-tech/state relations through a focus on Sino-UK fintech networks as they relate to payment systems in particular. My focus on the role of the UK in Chinese fintech is important for two reasons. First, London's financial district has played an important role in other policy domains associated with Chinese currency internationalisation (Hall, 2017) and hence it has a series of relations with China upon which fintech collaboration might be developed. And second, fintech is politically and economically important for London's financial district as it begins to reposition itself within the international financial system following the UK's departure from the EU. London recorded the largest volume of fintech investment in Europe in 2019 and the second largest amount globally behind the US (Bain, 2020). I focus on payments within the wider fintech ecology (Lai and Samers, 2020) because of China's dominance in this particular element of fintech. I characterise the relations considered in the paper as networks following the work of Dicken et al. (2001) who argue that a network-based approach to studying processes of economic change allows analysis to incorporate multiple scales of analysis into our research whilst also being cognisant of the ways in which the categories and labels we use shape the processes we study. As my analysis shows, such an approach allows a critical engagement with different forms of fintech in two key global locations for its development.

Building on the domestic growth of fintech in both the UK and China, this paper explores the work of both states and fintech firms in deepening Sino-UK fintech networks. At one level these networks are predominately state-led, through initiatives such as the China-UK Economic and Financial Dialogues that have been central to the wider positioning of London within Chinese financial internationalisation (Hall, 2017). However, Sino-UK fintech networks also include a significant degree of private sector activity by financial services firms’. I explore the inter-relationship between these two modalities through a focus on payment services, reflecting the importance of these activities within China's domestic fintech sector.

In particular, I emphasise the ways in which these state-firm-fintech networks are being radically reshuffled but not necessarily in ways that lead to the smooth development of Sino-UK fintech networks which in many ways remain in their infancy and are anticipated in the terms of this paper. By focusing on the role of the state, the paper responds to Lai and Samers (2020: 8) call ‘for greater consideration of state actors and regulators in not only enabling FinTech growth through regulatory adjustments and risk management but also strengthening IFC competitiveness in entrepreneurial ways’. In this respect, my analysis supports research that has demonstrated the importance of close relationships or strategic coupling between banks and the state in understanding fintech (Hendrikse et al., 2019) and the renewed interest in the state more generally in economic geography.

However, I argue that work in this area can be extended in important ways by acknowledging that the strategic coupling between the state and fintech is not only a domestic policy concern but increasingly wrapped up with foreign policy and international relations. In this respect, I suggest that drawing on work on the geographies of money as infrastructure provides a valuable way of developing understanding of cross-national fintech payment networks (Farrell and Newman, 2019; Westermeier, 2020). Such an approach is valuable because it underscores how geo-politics and international relations are entwined with fintech. I argue that one productive way of more fully capturing the role of the state in fintech networks is to understand fintech not only as a financial geography, emphasising the corporate actors and their services, but also as a monetary geography in which attention is paid to the monetary networks and infrastructures increasingly provided by fintech. In so doing, I show the challenges, as well as the opportunities, for extending the strategic coupling of the state with fintech from the domestic to the international scale as Sino-UK fintech networks remain at an early stage of development, despite considerable political interest in the project.

I develop this argument over four subsequent sections. Next, I examine how extant work on the international dimensions of state intervention in fintech networks can be developed by bringing it into closer dialogue with work on fintech as a form of monetary infrastructure. In the third section, I examine the onshore preconditions (Lim, 2019) in both China and the UK that have shaped the development of Sino-UK fintech networks. In the fourth section, I examine how focusing on Sino-UK fintech networks as monetary infrastructures reveals both the political and economic logics that have been central to their formation, but also the risks and limitations associated with their future development. I conclude by reflecting on the implications of this argument for work on the changing place of China within global finance, and fintech in particular, as well documenting the value of approaching fintech as a monetary as well as financial geography.

Theorising Sino-UK fintech networks within the geographies of money

Fintech is a broad set of activities that in many ways escapes clear definition. It is generally taken to refer to the ways in which finance and technology intersect both now and historically, with some researchers warning that it has the potential to become something of a ‘chaotic concept’ (Sayer, 1992). However, within this breadth, it is possible to identify a series of innovations within financial services which are using data and IT in novel ways. This includes insurance, retail banking, financial infrastructure such as payments and investment. Collectively, these activities are commonly understood as operating ‘at the intersections of the finance and technology sectors where technology-focused start-ups and new market entrants are creating new platforms, products, and services beyond those currently provided by the traditional finance industry [that are] changing how businesses and consumers make payments, lend, borrow, and invest’ (Lai and Samers, 2020: 1).

Reflecting the breadth of fintech activity, a range of different theoretical approaches have been developed by economic geographers and cognate social scientists. This includes work on fintech firms and their growth and investment strategies (Hendrikse et al., 2019, 2018); work on platforms and their potentially disruptive capacities within financial ecologies (Langley and Leyshon, 2017); research into blockchain technology and bit coin in particular (Zook and Grote, 2020) and work on the regulation to fintech (Shim and Shin 2016). In this paper, I take work on the corporate strategies of fintech firms as my starting point.

Much of the literature in this area examines how small fintech start-ups have challenged larger incumbent firms through strategic coupling with both lead firms and with state actors. For example, in a detailed examination of the development of fintech firms in Belgium, Hendrikse et al. (2019) emphasise the role of both tech firms and the state in supporting the fintech sector's development. By adopting a framework that they term the Fin-tech-state triangle, they draw attention to both the opportunities but also the challenges made available as leading firms need to innovate and adopt tech in order to remain competitive in the face of fintech challengers. In so doing, their research reveals how the institutional thickness of already existing financial centres is important in providing the conditions upon which fintech can develop.

Of particular importance for my research on Sino-UK fintech networks is their emphasis on the role of the state in shaping fin tech and particularly work on the entrepreneurial state (Mazzucato, 2011) through which the state ‘uses public funds to underwrite the risks of innovation and stimulates the anchoring of Fintech innovation in the confines of a particular platform’. Hendrikse et al. (2019) understand this relationship between the state and fintech as an instance of strategic coupling. I follow this approach because it provides an analytical approach to understand how fintech firms are tied into the international financial system. In so doing, I follow Yeung (2016: 54) who defines strategic coupling as a ‘mutually dependent and constitutive process involving particular ties, shared interests and cooperation between two or more groups of economic actors who otherwise might not act in tandem to achieve a common strategic objective’. This approach is relevant to the fintech networks examined in this paper because fintech is seen as a developmental strategy for both the UK and China. In the UK, in November 2020, the then Chancellor of the Exchequer, Rishi Sunak, identified what he termed digital finance, alongside green finance as core areas of financial services growth post Brexit (Sunak, 2020). Meanwhile in 2019, the Chinese Ambassador to the UK identified the potential for fintech, alongside other financial market activities such as RMB internationalisation to be developed through Sino-UK cooperation.

However, much of the focus of extant work on the strategic coupling of fintech and the state is in the field of domestic, as opposed to foreign, policy with much of the work focused on case studies of different elements of fintech in the West. There are important limitations when translating this literature to the Chinese context, that stem from the different organisational form and role of the state in fintech in China and this is reflected in the literature that has developed analysing the distinctive nature of the growth of fintech in China (Buchanan and Cao, 2018; Huang, 2021; Zhang, 2020). The growth of China's fintech sector dates back to December 2004 when Alipay launched online. However, growth in the sector did not really start to accelerate until June 2013 when Ant Financial launched its ‘online money market fund’. Over the course of this growth, China's fintech sector has emerged with different foci compared to its counterparts in Europe and North America. Whilst in the latter, the focus of attention has been on crypto currencies and cross-border payments, within China, more focus has been to mobile payment systems, online consumer lending and online investment. The corporate geography of fintech in China is also distinctive. Whilst in North America and Europe, the sector is characterised by a larger number of small firms, China's sector is dominated by a ‘small number of unicorn players such as Ant Financial Tencent, Baidu and JD Digits’ (Hua and Huang, 2020: 1) with fintech in many ways being part of the wider BigTech landscape in China (Fernandez et al., 2020).

The relationship between the Chinese state and its financial system, including fintech, is also distinctive. The financial system has always been dominated by the party state but within this, there have been periods of marketization, internationalization and privatization as China has adopted a targeted approach to policy experimentation across a range of financial activities (Hall, 2021; Töpfer and Hall, 2018; Wojcik and Cammilleri, 2013). In the case of fintech, large firms, notably Ali and Tencent have sought to challenge the incumbent state-owned banks and wider monetary authority (Tanda and Schena, 2019). The state has responded by seeking to manage the power of BigTech and Fintech firms. For example, Ali and Tencent have now become financial holding companies which means that they are regulated by the Chinese central bank in the same way as more longstanding state-owned banks. This suggests that the nature of strategic coupling between incumbent banks, fintech firms and the state may operate differently in China as compared with the UK raising important questions about the extent to which fintech firms such as Ali and Tencent are part of the mainstream Chinese banking system as opposed to outside challenger firms. 1

International fintech networks and the geographies of money

In order to understand the ways in which fintech development becomes coupled with international policy concerns, I turn to work to writing on the geographies of money, a body of literature that has been somewhat eclipsed by work on the geographies of finance when it comes to the case of fintech For example, whilst the first set of Progress in Human Geography reports written on the geographies of money and finance by Andrew Leyshon (Leyshon, 1998, 1997, 1995) included the geographies of money, by the 2000s, the focus had turned to the geographies of finance (see Aalbers, 2017; Hall, 2011). This literature focussed on understanding money through the functions it performs: a store of value; a unit of account; and a medium of exchange (Leyshon and Thrift, 1997). Particular emphasis is placed on how each of these functions rely on trust in money to be developed and sustained through social, cultural and political dimensions.

Of particular importance for my focus on fintech payment practices is work on money as a medium of exchange. This work charts the development of different types of money as a medium of exchange from coins and notes through to credit money, all of which require trust to be placed in money. As payments have become more distanciated, across time and space through forms of credit money as well as the forms of digital payments, attention has increasingly turned not only to the mode of payment (such as a bank note or a credit card) but also to the development of payment infrastructures that are needed to enable such payments (Westermeier, 2020).

In terms of fintech payment infrastructures, much of this work has been conducted in an anthropological tradition. For example, Maurer (2012) uses an actor network theory approach to understand how individuals engage with emerging networks of what he terms mobile money – monetary systems based around mobile phone technology of which M-PESA in Kenya is the most well-known. Gabor and Brooks (2017) expand this work to consider the implications of such technologies and practices for questions of financial inclusion. Crucially, work on payment and financial infrastructures more broadly has emphasised the ways in which control of such networks and decisions about access need to be understood as part of the shaping of geopolitical power relations, in a similar way to which other infrastructure networks are, such as those associated with energy (Farrell and Newman, 2019). For example, since 2015, the Society for Worldwide interbank Financial Telecommunications (SWIFT) based in Belgium has become increasingly bound into question of geopolitical security in terms of which banks based where have access to its payments messaging system which is central to facilitating global interbank transfers. This culminated in 2018 with SWIFT disconnecting a number of Iranian banks from its systems, including the Central Bank of Iran (Goede, 2020).

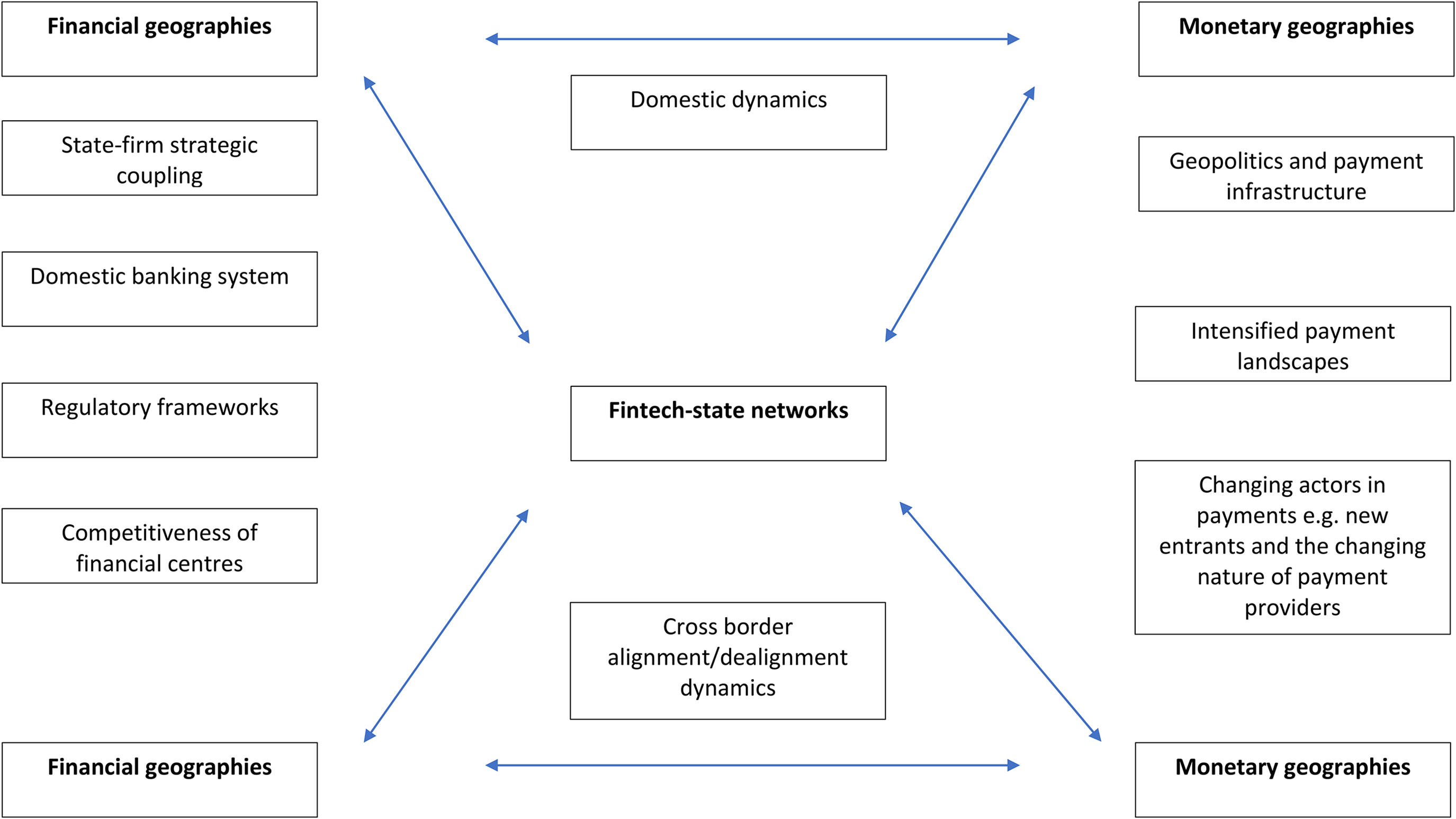

In this paper, I bring this work on the geopolitics of monetary infrastructures, particularly those associated with payments, into dialogue with the broader literature on the financial geographies of strategic coupling in fintech to explore the development of Sino-UK fintech networks. The resulting theoretical framework is shown in Figure 1. This shows that rather than seeing financial and monetary geographies as separate entities, through the reworking of fintech-state networks they are co-constitutive of each other and operate at both the domestic and international scale. Indeed, there are other geographies in play, not least the urban and the local as fintech networks develop but these are beyond the scope of this paper. Crucially, both monetary and financial geographies are being reconfigured within both China and the UK with respect to fintech. It is the extent to which these state-fintech reconfigurations align, or not, that will be crucial in determining the extent to which Sino-UK fintech networks develop in the future, and the form that they take. Clearly network development will also be shaped by wider changes in the place and power of China within the world economy, not least its geo-political and geo-economic relationship with the US. Indeed, in the case of finance, this has already become readily apparent with the US being notable by its absence from the early stages of RMB internationalisation due to the challenges of aligning US and Chinese domestic politics with closer bilateral financial relations between the two countries following the 2007–2008 financial crisis. This crisis in many ways served to prompt China to reduce its reliance on US finance and hence was a significant driver of RMB internationalisation (Hall, 2021).

Reshuffling fin-tech state relations.

The research examined below forms part of a wider research programme that has examined the growing influence of China in the international financial system which began in 2015. The research was conducted in London and Beijing and involved two stages pertinent to the internationalisation of fintech in particular. First, desk-based reviews were conducted to establish the changing policy context for Sino-UK fintech networks in London (including the City of London and Hm Treasury as well as relevant media reporting) and China (including statements from the Chinese ambassador to the UK and the work of the China UK fintech bridge). Second, 35 semi-structured interviews were conducted in a range of financial services markets from September 2014 to December 2019. This marked a period of significant changes in the depth of interaction between the UK and China in financial services. At the start of the period, under Prime Minister David Cameron and Chancellor George Osborne, the UK actively pursued closer collaboration with China and China identified advantages in partnership with the UK in order to meet its strategic ambitions for RMB internationalisation (Hall, 2017). However, as the period progressed and the UK began to rethink its international economic relates as part of its wider Brexit project and geo-political tensions grew between the US and China, the strategic focus between the UK and China decreased. Methodologically, this trend became apparent as it became more difficult to secure interviews as time went on but also in the ways in which the later interviewees were generally more speculative about the future prospects for Sino-UK fintech networks.

Interviews included financiers, lawyers working in Chinese financial market development, regulation and market commentators. Interviews were conducted in English and took between thirty and two and a half hours. Interviews were recorded and transcribed before being coded following grounded theory with key themes emerging from the first stage being used to design the coding framework. The content of the interviews underpins the analysis in this paper.

Geopolitics and payment infrastructure in Sino-UK fintech network development

Fintech has become a strategically important element of the financial services ecosystem in both China and the UK although the development trajectories in the two countries differ in terms of their rationale, governance and actors. This is particularly true in the case of payments because of the different regulations and normalised practices surrounding payment, online retail and credit that have shaped how payments are typically made in the UK and China within but also beyond fintech. Figure 1 provides my analytical frame for placing payments within the wider Sino-UK fintech network development. As this figure shows, in terms of financial geographies, the growth of fintech in China needs to be situated within China's strongly state controlled banking system (Shim and Shin, 2016) and the wider role of the Chinese state within the economy. Under the central bank, the People's Bank of China (PBOC), the banking system is dominated by four state owned banks (The Bank of China, China Construction Bank, Agricultural Bank of China and the Industrial and Commercial Bank of China) (Hall, 2021). Government control has been maintained through the creation in 2003 of the China Banking Regulatory Commission (CBRC) which was established to undertake banking supervision in place of the PBOC.

This banking system then operates alongside third-party payment (TPP) – payment services providers that have been largely separate from merchants and from banks (this is changing through the fintech sector as discussed below). Here again there are important differences in monetary and payment infrastructures between China and the UK. Most notably, the use of credit cards has historically been much lower in China than in other countries with its significant e-commerce market being dominated by mobile payment. It is estimated that close to 75% of online consumer transactions are completed on a mobile device, worth $873 in sales in 2019 (JP Morgan, 2019). As a result, the TPPs have developed an important role in facilitating third party online payment and cash on delivery, reflecting the Chinese preference for cash as opposed to credit card payments. This is reflected in the fact that TPPs are often labelled as payment service providers. Two of China's biggest fintech companies are TPPs: Alibaba and Tencent. The latest card payment company is UnionPay. Moreover, other online media companies notably the social network WeChat have also expanded into online retail and payments.

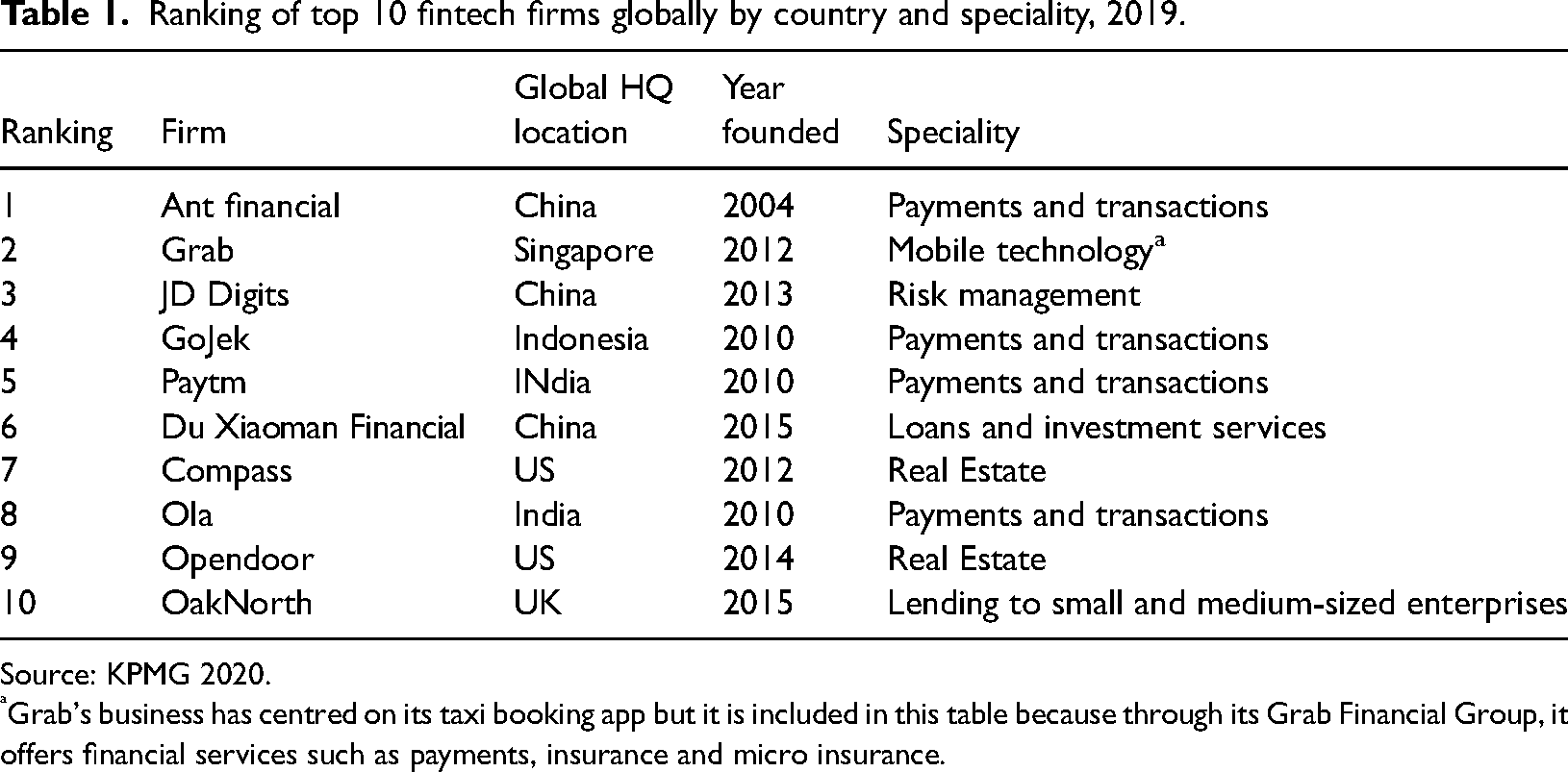

Given the domestic market for online digital payments in particular, it is not surprising that Chinese fintech firms are some of the largest fintech start-ups in the world. For example, the consultancy firm KPMG produces an annual ranking of what it classes as the most innovative fintech companies globally. This is based on the average annual capital raised, the rate of capital growth, the firm's geographic and sectoral diversity and a measure of business model innovation. The rankings for 2019, the latest year for which data is available, are shown in Table 1. Clearly such rankings need to be treated with caution, but two trends emerge that are pertinent to my arguments in this paper. First, Asia Pacific dominates the rankings in contrast to much of the existing work in financial geography in other sectors which emphasises the importance of Europe and North America, and the NYLON connection in particular (Wójcik et al., 2017). Second, the report shows that fintech companies working in payments and transactions dominate the rankings with 27 of the 100 companies included operating in this area. This is particularly true of China where its largest fintech firm is Alibaba which was started in 1999 by Jack Ma as an e-commerce company. It is now expanding its operations internationally through a focus on the introduction of technology in payment networks.

Ranking of top 10 fintech firms globally by country and speciality, 2019.

Source: KPMG 2020.

Grab's business has centred on its taxi booking app but it is included in this table because through its Grab Financial Group, it offers financial services such as payments, insurance and micro insurance.

In China, fintech can be understood to emerge from the need to facilitate the rapid growth of e-commerce, particularly for small- and medium-sized enterprises that began to grow from the late 1990s, or what I term in Figure 1, an intensified payment landscape. However, facilitating payment in an economy when the use of credit cards was limited posed a major limit on growth and it is here that Alibaba contributed through the development of TrustPass. A key moment emerged in 2005 when Alibaba launched the payment system Alipay which allowed buyers to send money from their bank to Alibaba, allowing Alibaba to outgrow eBay in China. Alongside fellow payments company Tencent, Alipay became one of the most significant fintech companies globally and its growth is central to the ways in which payments have been at the core of Chinese fintech growth. Indeed, in response the state-owned banks have been increasingly eager to compete with these payment systems.

China's fintech development has therefore been largely domestically (see Figure 1) focussed with a prioritisation of using payments services in particularly to address challenges in the growth of other parts of e-commerce. The slight change to this was the announcement in 2014 that the China State Council ‘would open up the country's bank card clearing market as part of a greater liberalization of the financial sector’. Such a move would put UnionPay at risk of losing its dominant position to foreign firms when domestic TPP platforms have also eroded its revenue. As a result, foreign players, such as Visa and Mastercard now have direct access to the domestic Chinese market.

On the financial geography side of Figure 1, the regulatory framework for fintech (a key element of financial geographies as shown in figure one) in China was set to a large extent through the publication in July 2015 of the Guiding Opinion on Promoting the Healthy Development of Internet Finance jointly written by the People's Bank of China, the CBRC, the China Securities Regulatory Commission, the China Insurance Regulatory Commission and the Ministry of Finance. This guidance seeks to promote innovation whilst also ensuring market stability. This includes regulation on issues such as Peer to peer lending, information disclosure and insurance. More recently, in 2020, the chairman of the China Banking and Insurance Regulatory Commission raised the prospect of greater regulation for large fintech firms arguing that they were going to investigate the possibility for enhanced risk control. There is also growing interest in data and how this is used to share information with consumers. The State Administration for Market regulation released draft rules that for the first time set out what constitutes anti-competitive behaviour. These are broadly understood to be aimed at China's tech giants including Alibaba, Tencent and Baidu. This growing regulatory focus on Chinese fintech became most notable in November 2020 when regulatory action was taken against Ant Group which saw its initial public offering in Shanghai and Hong Kong (anticipated to be the world's largest) suspended days before following a meeting between regulators and the management of Ant Group. At the time, the Shanghai Stock Exchange noted that Ant was dealing with issues in response to financial technology regulation changes. This appears to be linked to the Chinese central bank regulatory changes in relation to new rules of online micro-lending which would include the Ant Group. In this sense, whilst strategic coupling between the state and lead firms in particular can lead to the development of fintech (Hendrikse et al., 2019), it is important to remember that the state can shape the form that this development takes in terms of the firms involved for example, as well as potentially limiting the sector's development more widely.

Figure one also shows that the financial centre development is a key element of the financial geographies of fintech. This process has been particularly important in the UK, most notably in terms of (re)producing the competitiveness of London as an international financial centre following the 2007–2008 financial crisis. This reflects the dominance of London within financial services in ways that are not seen to the same extent in China (Pan et al., 2018). Following the banking crisis that was at the heart of the crisis, the government and City of London specific authorities, notably the City of London Corporation (which works to promote London as an international financial centres) actively sought new areas of specialism to support the competitiveness of London. This included green finance, Islamic finance as well as fintech (Hall, 2017). In so doing, frequent reference was made to the historic ways in which London had innovated through period periods of crisis and in so doing had fostered regenerative capabilities. The sector was initiated through the development of what was called initially called ‘Silicon Roundabout’ in 2000s and became ‘Tech City’ following government support in 2011. This is found in Shoreditch in East London. In contrast to the central role played by large fintech firms in China, the UK sector originated through small start-up firms. This location was important because it allowed the coming together of financial expertise which has historically been concentrated in the City, to the South of Tech City with legal expertise found to the west whilst attracting technology experts. Led by the then Prime Minister David Cameron, the aspiration was to create a technology hub capable of competing with Silicon Valley. The City could also supply the finance needed to establish tech firms.

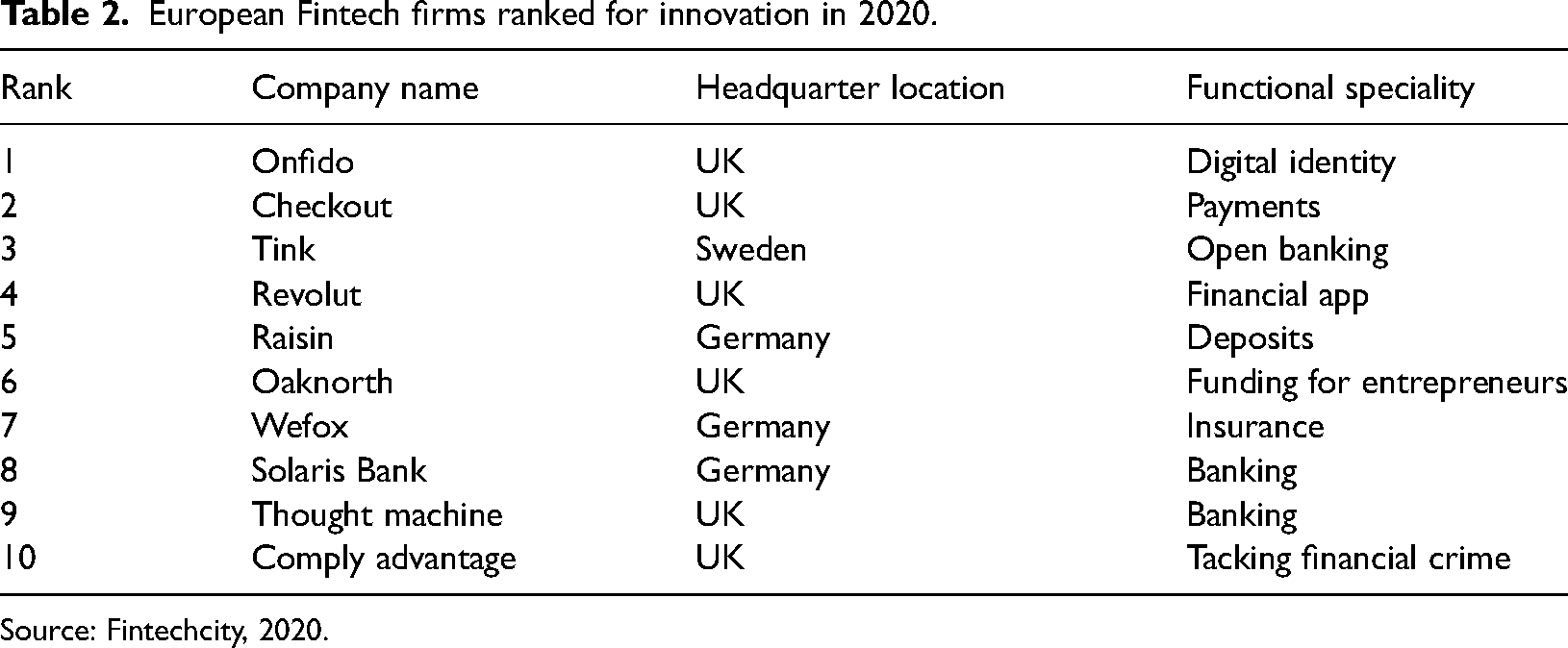

Beyond financial centre dynamics, regulatory frameworks (as shown in Figure 1) have also been critical to the development of Tech City and the UK's wider fintech sector has been its regulatory landscape. In this respect, the Financial Conduct Authority set out to include regulatory and other standards globally notably through the use of regulatory sandboxes that allowed new ideas to be test with consumers in a ‘safe environment’. A further contrast with China is the sectoral focus of fintech in the UK. Rather than focussing on one element such as payments, the UK's fintech development is characterised by the range of sectors it houses. This includes challenger banks, personal and wealth management, alternative lending and finance, blockchain and digital and Insuretech as well as payments. Indeed, in terms of rates of investment payments is the smallest part of the UK's fintech landscape. This diversity is reflected when looking at the Fintech50 rankings for Europe, six of which are based in the UK that operate in areas including addressing financial crime, funding for entrepreneurs, payments and digital identity verification (Table 2).

European Fintech firms ranked for innovation in 2020.

Source: Fintechcity, 2020.

Developing Sino-UK fintech networks: from limited strategic coupling to the geo-politics of money as infrastructure

In this section, I examine how the domestic development of fintech in China and UK has been crucial to the creation of nascent Sino-UK fintech networks, paying particular attention to the role of the state in developing fintech networks. I begin by drawing on the corporate approach developed predominately in economic geography to understand fintech that focuses on the domestic dynamics identified in Figure 1. In particular, I follow work on the role of strategic coupling between fintech firms and the state in the development of such networks. I then turn to work that has focused on fintech as a monetary infrastructure as shown in Figure 1, to reveal how geopolitical concerns about Chinese state involvement in UK infrastructures poses challenges to the ongoing development of Sino-UK fintech networks that remain in their infancy.

Much of the impetus for the development of Sino-UK fintech networks comes from London, possibly reflecting the global dominance of Chinese fintech in payments in particular as noted above and London's desire to access this to support its own fintech sector, or what I term in Figure 1, the financial geographies of competition between financial centres. Consequently, my analysis starts with the rationale and activities in London that initiated Sino-UK fintech networks. In common with other elements of Chinese financial services in London (Hall, 2021), the impetus for this comes primarily from the City of London Corporation, an organisation that focuses on promoting the interests of the City internationally, the Treasury and the Foreign Office rather than being led organically by fintech firms themselves.

The initial drive for global relations to support the development of UK fintech builds on the sector's growth domestically. Given the breadth of activity encompassed within the term fintech, it is hard to be precise and quantify this growth because different indicators include different elements of fintech activity. However, fintech is widely understood to have grown to contribute over £6bn to the UK economy per annum (Innovate Finance, 2019). Despite this growth, narratives of the sector's growth are typically accompanied by the identification of risks to future growth. Some of these are conjunctural such as the possible changes in demand triggered by the Covid-19 pandemic and the potential challenges of attracting labour to work in UK fintech from the EU in particular following Brexit. However, other challenges are more structural. For example, it is estimated that only 6% of UK-based fintech firms were making a project in 2019, before the Covid-19 pandemic, and 84% of firms reported in 2019 that their losses were increasing (KPMG, 2020). Given the fact that the UK's fintech sector is dominated by a large number of small firms where access to finance for growth is critical, these figures point to potential challenges for the continued growth of the sector.

A number of policy strategies have been identified by fintech trade bodies, the City of London Corporation and national policymakers, notably HM Treasury, to respond to these challenges. This includes financing the scaling up of small fintech firms (KPMG, 2020) and better understanding customer demand in order to continue the innovative nature of products developed and sold. Forging international connections with leading fintech markets globally such as China needs to be located within this policy landscape as it can be understood as a further example of a policy agenda aimed at facilitating the continued development of the UK's fintech sector (although alongside this economic imperative it is also important to note that it sits alongside a much wider set of UK foreign policy concerns, particularly with respect to China).

The launch in 2018 of the UK's first Fintech Sector Strategy was central to using national policy to work with private sector firms to support the development of fintech in ways which resonate with the literature on strategic coupling (HM Treasury, 2018). The strategy was closely linked to the Industrial Strategy launched by the Department for Business, Energy and Industrial Strategy in 2017 (BEIS, 2017). Reflecting the concern of the government of the time with industry, and particularly manufacturing, much of the focus of these two documents was about stimulating industrial economic recovery across the UK and using fintech as a way of achieving this. For example, the strategy explicitly states the government's aim of using fintech to support wider economic growth through targeting markets that are underserved by the big banks […] fintech firms have been particularly effective at generating new lending for small businesses, supplying the vitally important capital that fuels economic growth across the UK […] The Fintech Sector Strategy sets out how, in support of the Industrial Strategy, and responding to the Fintech Census, the government plans to maintain and extend the UK's leading edge in Fintech (HM Treasury, 2018: 4).

In a sign of the dominance of China within fintech, unlike the other bi-lateral bridges, the UK-China fintech bridge was launched in November 2016 in advance of the Fintech Strategy. Rather than being embedded within fintech strategy from the start, it was actually launched within the UK-China Economic and Financial Dialogue which has underpinned the UK's wider role in RMB internationalisation (Hall, 2017). The Bridge is underpinned by a Regulatory Cooperation Agreement between the Financial Conduct Authority in the UK and The People's Bank of China (FCA, 2016). This agreement allows the respective regulators to share information in relation to new fintech innovations and any associated regulatory issues. However, beyond this, activities under the auspices of the fintech bridge have been very limited. UK-China fintech bridge held its first conference in December 2018 although the subsequent meeting has been delayed due to the Covid-19 pandemic. This inaugural conference was followed by a visit from the Lord Mayor of the City of London to Shenzhen, Shanghai and Beijing in March 2019 focused on promoting Sino-UK links in fintech as well as green finance and the Belt and Road Initiative (City of London, 2019). As one report summarised with the exception of the Singaporean fintech bridge ‘They [Fintech bridges] are not delivery value for British fintech firms and they aren’t encouraging sufficient levels of collaboration’ (Horton, 2019). Further evidence on the lack of activity through the UK-China fintech bridge can be found in policy documentation relating to the wider involvement of the UK within Chinese monetary and financial strategy. For example, in the latest UK-China Financial Economic and Financial Dialogues, the key meetings through which Sino-UK financial networks are developed, in 2019, the reports on the fintech bridge were all forward looking with the outcomes noting that Both sides expect to strengthen cooperation under the framework of China-UK Fintech Bridge. Both sides agree to provide a facilitating policy environment for Fintech enterprises’ development in both countries’ markets, and for them to serve the real economy in joint efforts with incumbent financial institutions … Both sides agree to provide sustained guidance to Fintech enterprises in terms of compliance, data security and privacy.

Sino-UK fintech networks as infrastructures

Despite the limited entry of UK fintech firms into China, China has also identified fintech as a key area of potential collaboration. For example, in March 2019 the Chinese Ambassador to China, Liu Xiaoming, identified fintech as an important area of future bilateral cooperation, also emphasising the importance of the fintech bridge saying ‘Fintech has been a new area for China-UK financial cooperation … The goal is to make FinTech a bridge for deepening China-UK business cooperation’. However, rather than discussing higher level bilateral cooperation as encouraged by the fintech bridge, he then went on to focus on Alipay's, acquisition of the payments provider Worldfirst. This focus reflects the importance of fintech mediated payments in China's approach to fintech, suggesting that in order to understand Sino-UK networks from the perspective of Chinese financial policy, more attention needs to be paid to fintech as a series of monetary infrastructures, and particularly in the case of Sino-UK fintech relations, the importance of fintech payment infrastructures. As Figure 1 shows, the advantage of such an approach is that it moves beyond firm state relations as emphasised in strategic coupling approached to instead draw attention to the ways in which foreign as well as domestic policy is entwined with state support for fintech. This is particularly the case for fintech payment infrastructures and Sino-UK relations given the questions of infrastructure security that have been raised more frequently with reference to China by several Western countries, including the UK in recent years (see e.g. Sabbagh and Henley (2019) on the case of the Chinese communication company Huawei's involvement in the UK's 5G mobile phone network).

The case of Alipay's acquisition of Worldfirst is emblematic of such an approach in many ways. Alipay, or more specifically its financial arm Ant Financial's acquisition of Worldpay demonstrates these issues clearly. Ant Financial, known as Ant, traces its roots back to its time as the payment processing division of Alibaba since 2004 when it was called Alipay. By 2013 it became the world's largest mobile payment platform, overtaking PayPal as a result of it becoming China's most commonly used mobile payment service. It was rebranded as Ant Financial Services Group in 2015. From 2018 onwards its international ambitions became clearer because it raised USD14 billion from local and international investors which was explicitly aimed at funding international expansion. One of the earliest indications of this international expansion came in early 2019 when Ant financial acquired WorldFirst for USD700m, the UK-based international payments company.

However, there is evidence that WorldFirst was not the first-choice international acquisition for Ant. In 2018, it had sought to acquire the US payment company MoneyGram. The US Committee on Foreign Investment prevented this deal largely because of data security concerns. Reflecting the ways in which money within payment services can increasingly be viewed as data (Westermeier, 2020), this was driven by concerns that if the deal was concluded, the Chinese government could have access to US citizens and companies personal and private information, because the Chinese government remains a part owner of Ant financial. It appears that these data privacy concerns extended to the WorldFirst deal. In February 2019, Amazon sellers in the US received a notification from World First that its US business was closing with immediate effect. These operations did cease on 20 February 2019. This is significant because US law would allow the US government the opportunity to stop the Ant and WorldFirst acquisition, despite the fact that WorldFirst is headquartered in the UK. A fintech executive summarised the reasons behind this decision by saying that it was ‘the only way to avoid the US regulatory blocking the [Ant Financial] deal’ (Megaw and Lucas 2019). Subsequently, the US operations of WorldFirst operated independently of the wider World First Group under the Omega brand.

The Worldfirst acquisition can be located with the wider development of London's position as a leading Chinese financial hub in the mid-2010s (Töpfer and Hall, 2018). However, in many ways, the relationship has become more distant in recent years. Whilst Prime Minister David Cameron and his Chancellor George Osborne had pursued China as a key trading partner for the UK, Prime Minister Boris Johnson became increasingly keen to align the post-Brexit UK more closely with the US. As a result, he adopted a much more cautious approach to Chinese foreign direct investment, particularly in UK infrastructure which has continued under subsequent prime ministers.

Focusing on fintech as a monetary infrastructure through the case of payments reveals the importance of geopolitics and international relations in shaping Sino-UK fintech networks in ways which resonate with work that emphasises the questions of control that surround infrastructure networks and payment networks in particular (Farrell and Newman. 2019; de Goede, 2020). In particular, the case of Sino-UK fintech networks reminds us that monetary infrastructure networks are fragile, both economically in terms of the depth of activity involved and politically. They also need to be situated in both domestic and wider cross-border dynamics as shown in Figure 1. As a result, Sino-UK fintech networks have an uncertain future as the place of China within the world economy continues to develop in a post Brexit, post Trump environment.

Whilst this shows how the geopolitics of Sino-UK fintech networks are uncertain and anticipatory at an international level, my emphasis on bringing financial and monetary geographies into closer dialogue across scales also points to the ways in which domestic changes to fintech are also likely to be the source of uncertainty in the future. Most notably, and more recently since the conclusion of the research reported on in this paper, through its digital RMB program, China is seeking to develop a new digital payments system that could challenge the dominance of Alipay and WeChat Pay (Kynge and Yu, 2021). 2 The driver for this for the state is that the digital RMB is distributed through state-owned banks as opposed to the role of large finance companies, notably Ant Group (behind Alipay) and Tencent (behind WeChat Pay). As summarised in Figure 1, This reminds us that strategic coupling in the case of financial institutions is a cross-scalar set of processes with domestic development shaping the international and vice versa.

Conclusion

This paper has used the development of Sino-UK fintech networks to contribute to empirical understandings of China's changing position within the international financial system and conceptual understandings of the geographies of fintech. With regards to the former, the paper has shown how the domestic development of fintech in China and the UK has been very different. China's fintech sector is dominated by a small number of large tech firms and is focused in particularly on payments. In contrast, the UK's fintech sector has grown predominately through a larger number of smaller firms with a more diverse range of services included ranging from payments to insurance and lending, for example. From these diverse backgrounds, the shared interests upon which Sino-UK fintech networks could develop may appear relatively limited. However, in the mid-2010s in particular, both countries were seeking to enhance the international power of their financial services sector, albeit for different reasons and with complementary areas of fintech expertise, sought to exploit these synergies through state led initiatives, notably the China-UK fintech bridge. However, fintech firms, particularly those based in the UK have not widely sought to follow this state led form of financial network formation. More recently, as UK geopolitical relations with China have become more strained, a process that has intensified following the Russian invasion of Ukraine in 2022, the extent of fintech network development between the two countries has become more limited. Given the different developmental logics and political conditions of fintech in the UK and China, the future of UK-Sino fintech networks at the time of writing remains uncertain and are characterised as being anticipatory in nature rather than being under development in this paper.

Conceptually, I have argued that Sino-UK fintech networks reveal the need to understand fintech as both a financial and a monetary geography in which bilateral ties such as those between China and the UK need to be located in the context of both domestic and cross-border dynamics as shown in Figure 1. Responding to calls to understand the role of the state within fintech more fully, I have suggested that work that focuses on the corporate geographies of fintech through strategic coupling with the state is instructive in analysing the initial development of Sino-UK fintech networks. However, it does not pay sufficient attention to the geopolitics of fintech development and the implications of the limited engagement of UK fintech firms in fostering Sino-UK fintech networks. To address this, I have argued that work that understands fintech as a monetary geography and particularly as an infrastructure (Farrell and Newman, 2019) through payments illuminates how international geo-politics, as well as domestic state policy has been important in shaping the development of Sino-UK fintech networks to date. As such, I argue that fintech can be understood as both a financial and a monetary geography that is reconfiguring state-finance-technology relations in important ways. There is considerable scope for this paper's focus on payments to be extended to other aspects of fintech activity such as crypto currencies, blockchains and crowd funding. In so doing, the development of a wider body of work at the intersection of the geographies of money and finance would provide important empirical cases through which geographies of money can and should be reinvigorated within economic geography and cognate social scientific disciplines.

Footnotes

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the British Academy (grant number MD130065).