Abstract

Monetary policies are not usually considered as part of the repertoire of ‘state capitalism’. However, unconventional monetary operations performed by central banks in recent years make this exclusion increasingly problematic. This paper thus explores whether recent central bank interventions should be considered manifestations of ‘new’ state capitalism. Analysis focuses on the actions of three central banks from the advanced capitalist core in the West – the US Federal Reserve, the European Central Bank and the Bank of England. By mobilising the ‘financial chains’ perspective, this paper highlights the fact that, under financialisation, contemporary central banks have assumed a pivotal role in shaping Western capitalism and its uneven geographies. Through these recent unconventional interventions, central banks have in effect become ‘creators’ or ‘generators’ of (financial) capital. As such, their role in shaping uneven economic geographies across space (well beyond their official territorial boundaries) has expanded. Spatial ramifications of central banks’ capital-generating operations could thus fit easily within the framework of ‘uneven and combined state capitalism’. The possibility of considering the unconventional operations of central banks as state capitalist could also go hand in hand with a modified definition of state capitalism. Indeed, the rubric of state capitalism could potentially be enlarged to include configurations of capitalism where the state plays a particularly strong role not only as promoter, supervisor and owner of capital but also as a ‘generator’ of capital. This capital-generating role appears to be essential for the survival of contemporary capitalism.

Introduction

This paper engages with the burgeoning debate on ‘state capitalism’ (e.g. Alami and Dixon, 2020a; Kurlantzick, 2016; Musacchio and Lazzarini, 2014; Sperber, 2019; Wright et al., 2021) while focusing on central banks and their monetary policies. Monetary policies, with few exceptions (e.g. see Alami and Dixon, 2021: 19–20; Alami et al., 2022: 3), are not usually considered as part of the repertoire of ‘state capitalism’. However, unconventional monetary operations performed by central banks around the world in recent years make this exclusion increasingly problematic. Indeed, the augmented monetary activism (including, but not limited to, quantitative easing) – especially in the aftermath of the Global Financial crisis (GFC) and during the Covid-19 pandemic – could be seen as part of a massive state intervention to prevent the collapse of the entire economic system (Tooze, 2018, 2021). The scale and nature of these interventions is in many ways unprecedented. This paper thus explores the question of whether these central bank interventions should be considered as being part of manifestations of (new) state capitalism. It does so by utilising the cases of three central banks from the advanced capitalist core in the West, namely the US Federal Reserve (the Fed), the European Central Bank (ECB) and the Bank of England (BoE).

By mobilising the ‘financial chains’ perspective (Sokol, 2017), the paper highlights the fact that, under financialisation, contemporary central banks have assumed a pivotal role in shaping Western capitalism (see also Braun and Gabor, 2020; Lapavitsas and Mendieta-Muñoz, 2016; Tooze, 2020a; Walter and Wansleben, 2020; Wullweber, 2020) and its uneven geographies. Crucially, through their unconventional interventions (such as quantitative easing) central banks have in effect become ‘creators’ or ‘generators’ of (financial) capital. As such, their role in shaping uneven economic geographies across space (from local to global scales) has been further enhanced. The ‘financial chains’ perspective helps us to highlight not only the centrality of central banks in financialised capitalism, but also their role in shaping these economic geographies. Importantly, the spatial ramifications of central banks’ capital-generating operations could fit easily within the framework of ‘uneven and combined state capitalism’ outlined by Alami and Dixon (2021).

In short, the paper argues that, in financialised capitalism, central banks have assumed a key role in managing financial chains that in turn shape uneven and combined state capitalist development at various spatial scales. The paper thus suggests that central banks and their interventions cannot be omitted from state capitalism conceptualisations. In order to do this, the paper proceeds in the following steps: the section State capitalism debate discusses in more detail the state capitalist debate. It adopts the lens of the problématique of state capitalism developed by Alami et al. (2022) and that of ‘uneven and combined state capitalism’ (Alami and Dixon, 2021). The section Financialisation, state capitalism and central banking: The financial chains perspective mobilises the ‘financial chains’ perspective to highlight the fact that contemporary central banks have assumed a new pivotal role in shaping financialised Western capitalism and its financial chains. The section The Fed, the ECB and the Bank of England: Towards a big (monetary) state? illustrates this using the cases of three leading central banks (the Fed, the ECB and the BoE), highlighting their capital-generating function. The section Central banking, financial chains and uneven and combined state capitalism will explore how the central banks’ management of financial chains is shaping economic geographies and thus contributing to ‘uneven and combined state capitalism’ (Alami and Dixon, 2021). The final section will summarise the findings and discuss their implications for the (new) state capitalism debate.

State capitalism debate

New state capitalism has emerged recently as a potent, yet deeply problematic, construct. Some observers use it to describe authoritarian state-led capitalism in the ‘East’ (especially China) as opposed to the apparently democratic free-market capitalism of the ‘West’, exemplified by the US (Bremmer, 2009; Kurlantzick, 2016; Chen et al., 2015). In this way, the new state capitalism narratives have been used to highlight new geo-economic and geo-political constellations while echoing the old Cold War rhetoric (Alami and Dixon, 2020a) and reviving old dichotomies (state vs. market; socialism vs. capitalism; East vs. West). However, other scholars have pointed out that extraordinary state interventions are not limited to a group of emerging economies in the East but have also manifested themselves in the most advanced market economies of the West, including the US, UK and the European Union (Babic, 2021; Kim, 2021) and these interventions could also be seen as state capitalist. Indeed, as suggested by Dixon and Alami (2020), ‘[w]e are all state capitalists now’.

The ‘visible hand’ of the state in the Western capitalist core – while always present (e.g. Magnusson, 2013; Mazzucato, 2018) – became even more visible in the aftermath of the Global Financial Crisis (GFC) of 2007/2008 and has become patently obvious during the recent pandemic-induced crisis. The ‘Great Lockdown’ of 2020 (IMF, 2020) has seen an unprecedented mobilisation of the state in the West, through both fiscal and monetary policies (Tooze, 2018, 2021). In turn, the economic response to the Covid-19 pandemic in the US and Europe has been described as ‘pandemic socialism’ (Buiter, 2020). This calls for an urgent critical re-examination of the role of the state in advanced capitalist economies (see also Alami and Dixon, 2020b), while also opening the possibility to further expand the state capitalist debate.

Despite a proliferation of debates about ‘state capitalism’, it appears that the term lacks firm conceptual footing. Indeed, as argued by Alami and Dixon (2021: 3), the label of state capitalism – used to describe a wide variety of political and institutional forms (from the resurgence of sovereign wealth funds, state-owned enterprises and national development banks, to the renewal of industrial and neo-mercantilist policies) – is ‘far from perfect’ and the debates surrounding it display ‘significant theoretical and methodological difficulties’. Major shortcomings of the state capitalism debate include the fact that the term ‘lacks a unified definition’ (Alami and Dixon, 2020b: 70) and that state capitalism appears to be turning ‘the shorthand-du-jour for anything involving the intervention of the state’ (Alami and Dixon, 2021: 4). Among many other problems is the ‘missing link’ of a theory of the capitalist state, the neglected time horizons and an underappreciation of the territorial (geographical) dimensions of the state capitalist research (Alami and Dixon, 2020b: 72).

In order to overcome some of these shortcomings, Alami and Dixon (2021) have proposed a ‘rigorous definition’ of state capitalism – both as a research object (as a set of real-world processes and phenomena) and as an analytical construct, (‘to grasp these capitalist realities and render them amenable to analysis and critique’ (Alami and Dixon, 2021:8)). In terms of object(s) of inquiry, Alami and Dixon have offered ‘a simple heuristic’ to define state capitalism as ‘configurations of capitalism where the state plays a particularly strong role as promoter, supervisor and owner of capital’ (Alami and Dixon, 2021: 5). What they call ‘the aggregate expansion of the state's role as promoter, supervisor and owner of capital’ is in turn characterised by: (a) multiplication of state-capital hybrids (sovereign wealth funds; state enterprises; policy and development banks); and (b) development of muscular forms of statism (industrial policy; spatial development strategies; economic nationalism) (ibid:10).

Defining state capitalism as an analytical construct, they contend that ‘state capitalism, rather than a fully formed concept, can most productively be construed as means of problematising and critically interrogating the current aggregate expansion of the state's role as promoter, supervisor, and owner of capital across the spaces of the world capitalist economy, and particularly the expansion of state-controlled capital and the concomitant development of muscular forms of statism’ (Alami and Dixon, 2021: 4; emphasis added). By defining state capitalism as a ‘flexible means of problematising the object of inquiry’, rather than as ‘a static categorical construct or rigidly defined model’ (ibid: 9), Alami and Dixon (2021) refer to it as a problématique of the new state capitalism. The construction of state capitalism as a problématique, or a ‘set of critical interrogations’ (Alami and Dixon, 2021: 9) rather than ‘a fully formed concept or model’ (ibid) builds on Peck's (2019a) notion of ‘plastic categories of analysis’.

Alami et al. (2022) further expand on what this problématique of state capitalism might entail. They propose an open set of questions that characterise dimensions of the problématique of state capitalism as a guide for empirical research and they highlight five such dimensions. The first one concerns a ‘critical reflection on the (geo)political reorganisation of global capitalism’ (ibid: 5) or more specifically the interrogation of the relations between state and capital and the accompanying relations between political and economic power. The second dimension is based on the proposition that ‘no state institution, form of intervention, or pattern of development should be assumed to be state capitalist by default’ (ibid: 7), in turn raising the question of why a particular case should be considered as an instance of state capitalism. The related third dimension invites a comparative perspective between a particular (state capitalist) case and other cases that would typically not be considered state capitalist (ibid: 7). The fourth dimension of the problématique interrogates the assumptions of what is considered the ‘normal’ separation between politics and the economy (or between the public and private spheres of economic activity; ibid: 6–7). Finally, the fifth dimension invites the reflection on the implications of a particular case for ‘theorising the historically specific role that the state plays in the reproduction of global capitalism’ (ibid: 8). In other words, the question is what the particular case studied ‘tells us about the changing role of the state in capitalism’ (ibid: 6).

This paper adopts the above approach by Alami, Dixon and their colleagues (this being the most sophisticated theoretical account of new state capitalism to date), while also suggesting that it should be extended further. In particular, this paper suggests that the rubric of (new) state capitalism is ‘plastic’ enough to include central banks and their interventions. Thus, following the above problématique, the case studies of three leading central banks in the West (the Fed, the ECB and the BoE) are used to (a) interrogate their role in shaping relations between state and capital; (b) explore the extent to which this role can be seen as an instance of state capitalism; (c) compare these three cases in order to highlight similarities and differences between them; (d) reflect on the extent to which recent monetary interventions of these central banks could be seen as transgressing the ‘normal’ separation of the public and private spheres of economic activity; and finally, (e) consider the theoretical implications of these interventions for the state's changing role in capitalism. Points (a) to (d) will be explored in the section The Fed, the ECB and the Bank of England: Towards a big (monetary) state?, while point (e) will be tentatively addressed in the concluding section.

The above interrogations will be undertaken while also adopting the lens of ‘uneven and combined state capitalist development’ (Alami and Dixon, 2021). The critical importance of this perspective – rooted in the theory of uneven and combined development 1 – is that it places geography ‘front and centre’ of state capitalism conceptualisation (ibid: 23). In other words, it frames the problématique of the (new) state capitalism in ‘explicitly geographical terms’ (ibid: 9). This addresses one of the major shortcomings of much of the state capitalism debate (as highlighted earlier), i.e. the lack of territorial considerations – or what Alami and Dixon (2021) call the ‘metageographical unconscious’ that permeates state capitalist literature. Spatialising state capitalist development means, inter alia, overcoming methodological nationalism and ‘underdeveloped sense of space’ (ibid: 11). This is associated with several approaches (e.g. Nölke et al., 2021) that draw clear boundaries between state capitalist and non-state capitalist economies or that see state capitalist development as ‘primarily a national creature and a product of domestic forces’ (Alami and Dixon, 2021: 10). Instead, Alami and Dixon offer ‘a geographic reconstruction’ of the (new) state capitalist development. This starts with the recognition that ‘the determinants of the expansion of present-day state capitalism must be sought in the historical-geographical transformations in the material forms of production of (relative) surplus-value on a world scale’ (Alami and Dixon, 2021: 16; emphasis added). Importantly, these transformations include the emergence of the ‘new’ international division of labour, unfolding in the context of ‘secular stagnation’ or ‘long downturn’ and the global financial crisis of 2008 (ibid: 17–18). From this point of view, the aggregate expansion of the role of state as promoter, supervisor and owner of capital (global in scope as well as nature) could be seen as ‘the political mediation of … capitalist transformations and their crisis tendencies’ (ibid: 18). Seeing the expansion of state interventions as being part of global capitalist restructuring also allows us to see state capitalist trajectories ‘together and in relation to each other in a co-constitutive movement’ (ibid: 3; emph. orig.).

These insights are of major significance for the interrogation of the role of central banks in present-day capitalism. Indeed, central banks form part of a global financial architecture and their interventions have implications for economic processes well beyond their formal territorial boundaries (i.e. jurisdictions they are supposed to serve). It therefore makes sense to study central banks ‘together and in relation to each other’ (the section The Fed, the ECB and the Bank of England: Towards a big (monetary) state?) and to pay attention to the ways in which they shape uneven geographical development at various scales (the section Central banking, financial chains and uneven and combined state capitalism). However, before exploring these aspects, it is important to establish (in the next section on Financialisation, state capitalism and central banking: The financial chains perspective) the importance of the role of central banks in the sphere of finance and the importance of the financial sphere in contemporary financialised capitalism. This will be done and by mobilising the ‘financial chains’ perspective, while highlighting the significance of financialisation as a key capitalist transformation.

Financialisation, state capitalism and central banking: The financial chains perspective

The argument pursued in this section is that if the instances of state capitalism are seen as ‘the political mediation of … capitalist transformations and their crisis tendencies’ (Alami and Dixon, 2021: 18) then we need to pay closer attention to one important transformation taking place since the 1970s. The transformation in question is commonly referred to as financialisation (e.g. Mader et al., 2020; Lapavitsas, 2013; Stockhammer, 2008), a shorthand for the increasing power of finance over the economy and society. This transformation is rather fundamental because, as Lin and Neely (2020: 10) have pointed out, it represents ‘the wide-ranging reversal of the role of finance from a secondary, supportive activity to a principal driver of the economy’ (see also Boyer, 2000). What this means for the state capitalism debate is that if we are to understand (new) state capitalism, we first need to have a sound understanding of (new) financialised capitalism. More specifically, we need a clearer understanding of the importance of finance (and financial flows) in contemporary capitalist economies and the ways in which the state (e.g. through central banks) interacts with it. The main point emphasised here is that, under financialised capitalism, central banks play a central role in shaping ‘financial chains’ that in turn have significant effects on shaping economic geographies (and thus uneven and combined state capitalist development). In order to highlight the centrality of central banks in the web of financial chains and their role in shaping economic geographies, a stylised model of financial flows will be presented.

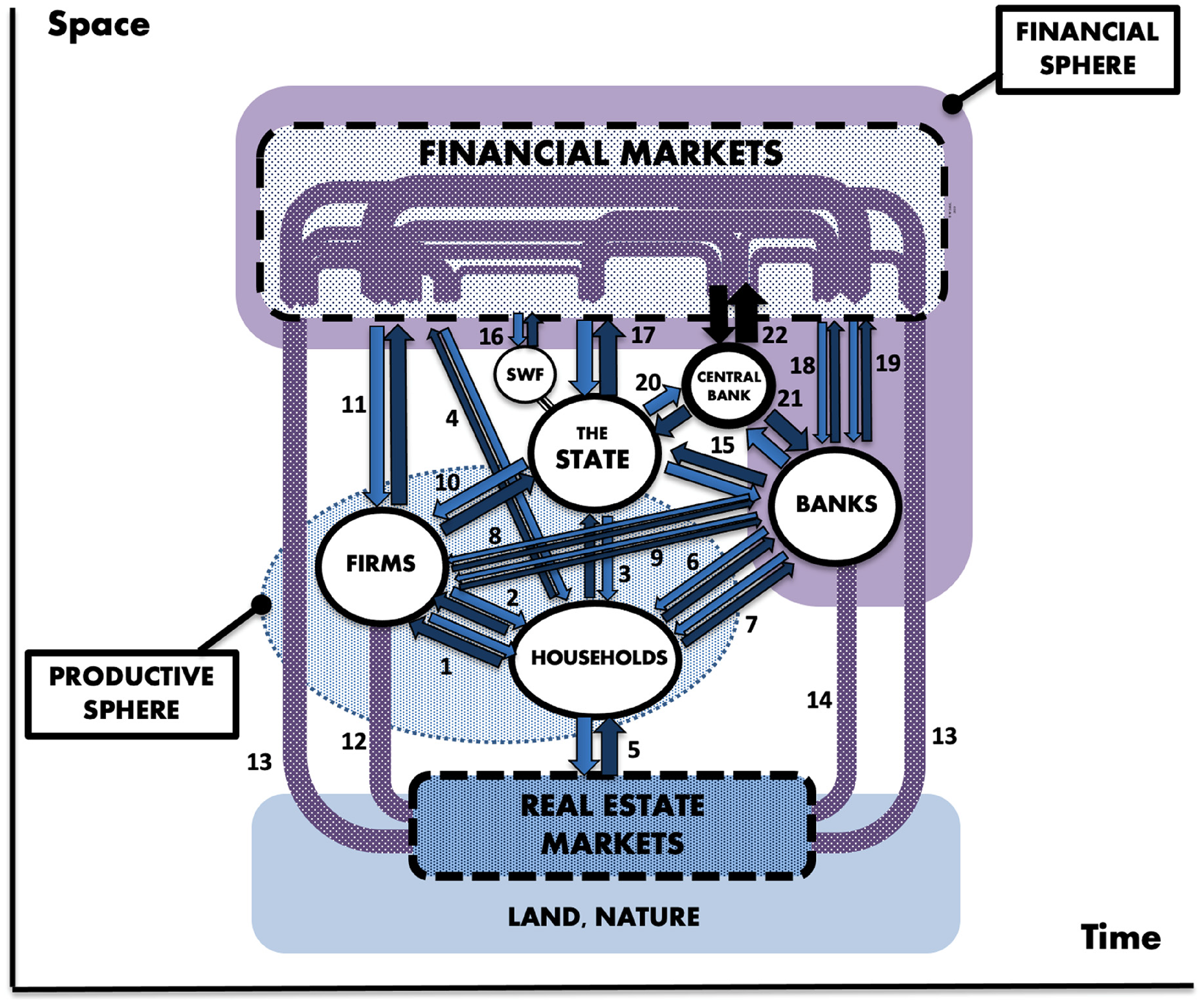

This model views the economy as a network of interlocking ‘financial chains’ (Figure 1), defined as both ‘channels of value transfer (between people and places) and as social relations that shape socio-economic processes and attendant economic geographies’ (Sokol, 2017: 683). The ‘chain’ metaphor has a double meaning – it implies both the linkages through which value can flow and also the way in which economic players are ‘chained’ to each other through these linkages, affecting each other's actions (Sokol, 2017). To put it differently, financial chains are not only about money, but also about power. This also makes the ‘financial chain’ perspective relevant for the problématique of state capitalism and its concern over the relations between economic and political power.

Flows of value in the financialised economy (financial chains perspective). Source: The author, building on Sokol (2013, 508); Sokol and Pataccini (2020, 405).

A simple example of a financial chain is the relationship between a debtor and a creditor where the value exchange is happening through a monetary exchange: a loan flows from a creditor-lender (e.g. a bank) to a debtor-borrower (e.g. a household) and loan repayments (with interest) flow, over time, in the opposite direction (financial chain 7 in Figure 1). The ‘financial chains’ perspective thus recognises that value flows in both directions. Furthermore, rather than being a simple supply-meets-demand market transaction, the balance of value transferred between the economic players is shaping, and is shaped by, power relations involved. This applies to a wide range of economic transactions occurring over time and space, all of which involve the exchange of value (and respective relations of power). In this way, the entire economy can be seen as a network made up of multiple financial chains 2 that in turn shape economic geographies.

Building on, and going beyond, the work of Sokol (2013, 2017) and Sokol and Pataccini (2020), the model presented here (Figure 1) integrates both the productive and financial sides of a financialised economy and illustrates the financial links (‘financial chains’) between them. Moreover, it features the three key players in the ‘productive sphere’ made up of firms, households and the state, alongside the ‘financial sphere’, made up of financial intermediaries (banks) and financial markets (themselves composed of a myriad of financial players, including the so-called ‘shadow banks’). The (ever-increasing) power of financial markets (and shadow banks) over the rest of the economy is considered as one of the key aspects of financialisation (e.g. Stockhammer, 2012; Braun and Gabor, 2020). This level of power is reflected by placing financial markets at the top of the model. In the financialised economic system, the productive (‘real’) economy is effectively sandwiched between financial markets and real estate markets (which are themselves increasingly financialised; e.g. see Aalbers, 2016) and the whole edifice rests on land and nature. Moreover, it is important to point out that financial chains linking the above actors and markets are unfolding in space and time. The spatial dimension of financial chains will be further explored in the section Central banking, financial chains and uneven and combined state capitalism.

Regarding the debate on state capitalism, it is worth emphasising that financialisation does not make the state disappear. Indeed, in addition to performing its function as a spender via its fiscal policy, the state now performs a number of other critical roles in the financialised economy. First and foremost, the state continues to be a major borrower (debtor), in what Streeck (2013) called the ‘debtor state’ – exposed to the disciplining forces of financial markets (see also Rommerskirchen, 2015). State borrowing represents an important financial chain (financial chain 17 in Figure 1) with implications for the rest of the economy. Indeed, the sovereign debt issued in the form of government bonds underpins the entire financial system by acting as safe collateral necessary for financial market transactions (e.g. Gabor and Ban, 2016; Gabor and Vestergaard, 2018; Gabor, 2021). Thus, as Gabor (2021: 18) notes, government bonds ‘have become the cornerstone of modern financial systems’. As a consequence, there is a strong mutual interdependence between the state and the financial markets: the state depends on financial markets and financial markets also depend on the state (see also Braun, 2020a; Gabor, 2016).

Furthermore, there are two important institutional developments that extend the influence of the state in the financialised economy even further 3 . Firstly, the state increasingly acts as a financial investor. Indeed, sovereign wealth funds (SWF) have become state vehicles for investing in financial markets (e.g. Dixon and Monk, 2012; see also Alami et al., 2021: 5–7) and they are gradually becoming important economic players in their own right. This is represented in Figure 1, which shows SWF as a stand-alone actor interacting with financial markets via financial chain 16. As noted by Alami and Dixon (2021: 6), SWF have mushroomed in the last two decades and their assets have ballooned to $8.6 trillion as of 2020, making them a prime example of state-capital hybrids of state capitalism.

The second institutional development concerns the state's monetary authorities (i.e. central banks) and their policies which, as noted from the outset, are not usually considered part of the repertoire of state capitalism. However, central banks in advanced capitalist economies have assumed extraordinary power and have performed operations of unprecedented scale and nature. In fact, it could be argued that central banks have become essential to the operation of financialised capitalism (Bowman et al., 2013; Braun, 2020a; Braun and Gabor, 2020; Gabor, 2016; Lapavitsas, 2013: 192–193; Lapavitsas and Mendieta-Muñoz, 2016; Tooze, 2020a; Walter and Wansleben, 2020; Wullweber, 2020). Furthermore, thanks to a significant degree of independence gained since the 1980s and 1990s, the present-day central bank has in effect become ‘a state within a state’ (Gabor, 2021: 17).

Building on these insights, the financial chains perspective considers a central bank as a player in managing financial flows through its interaction with the state (via financial chain 20), with other banks (financial chain 21) and with financial markets (financial chain 22) as captured in Figure 1. The figure highlights the fact that central banks effectively act as key hinges between the ‘financial’ sphere and the ‘productive’ sphere (aka the ‘real economy’) as well as between the ‘public’ finances and ‘private’ financial sphere. Consequently, they could be perceived as state-capital hybrids (see also August et al., 2021; Wullweber, 2020), a notion which was highlighted by Alami and Dixon (2021) as indicative of state capitalism. Through their central position in the economic system, actions of central banks have far-reaching consequences for financial institutions, productive firms, households and governments. Moreover, their influence goes well beyond their official territorial boundaries (see the section Central banking, financial chains and uneven and combined state capitalism). As highlighted in the next section, central bank power has been significantly increased by the recent economic crises.

The Fed, the ECB and the Bank of England: Towards a big (monetary) state?

The central banks examined in this section are the three most prominent central banks of the Western capitalist core: the US Federal Reserve (the Fed), arguably the most powerful central bank in the world; the European Central Bank (ECB) presiding over the Eurozone members of the European Union (EU) and widely accepted as ‘the second-most important central bank in the world’ (Tooze, 2020a); and the Bank of England (BoE), UK's central bank, which is ‘one of the oldest central banks in the world’ (Mishkin et al., 2013: 281) and remains one of the most important. While institutional histories of these three banks differ greatly, they also share many common features. Arguably, the key one is that all three have achieved a relatively high (albeit varying) degree of independence from the elected government. Furthermore, all three have engaged in unconventional interventions during recent crises and, in doing so, have shaped state-capital relations.

The Bank of England is, by quite a margin, the oldest of the three – founded in 1694 to ‘provide and arrange loans to the government’ and to ‘mobilise the country's resources in order to provide finance for trade’ (Mishkin et al., 2013: 281). Vernengo (2016: 453) notes that the Bank of England's role as ‘fiscal agent of the government’ throughout the 18th century (marked by frequent wars with France and the expanding role of the state) affirmed the institution's position as ‘the banker of the state’. One crucial innovation ‘was the possibility to borrow almost unlimited amounts of money with very low risk, since the state could not default in its own currency’ (Vernengo, 2016: 454, emphasis orig.). The growing market for government bonds was, in turn, ‘central in the development of British financial markets’ (ibid).

Progressively (through the 18th and 19th centuries), the Bank of England took on additional roles, including becoming ‘the bankers’ bank’ (Mishkin et al., 2013: 281) or the ‘bank for bankers’ (Bordo, 2007: 1, emphasis orig.). Eventually, BoE assumed its role as the focal point of the British financial system, a role ‘forced on it by various financial crises’ (Leyshon and Thrift, 1997: 19). The British central bank thus emerged as the ‘lender of last resort’ (LOLR), acting as a backstop for banks during crises – an idea which then ‘spread to the rest of the world’ (Leyshon and Thrift, 1997: 19). In summary, BoE firmly anchored itself in the centre of British financial system through the three main financial chains (Figure 1) which link it with the state (financial chain 20), with banks (financial chain 21) and with financial markets (financial chain 22). In the late 1990s, however, the direct link with the state has been considerably weakened as part of the ‘central bank independence’ shift. Indeed, in 1997, the BoE was granted ‘operational independence’ (Ashworth, 2020: 6) and is no longer ‘statutorily subordinate’ to the Treasury (Casu et al., 2015: 155). That said, the inflation target is still set by the Chancellor of the Exchequer, making the Bank of England ‘less goal-independent than the Fed and the ECB’ (Mishkin et al., 2013: 282).

The Fed's institutional history is somewhat shorter but not less interesting. In the US, Britain's former colony, the development of an effective central bank was hampered by the Americans’ ‘fear of centralised power’ (Mishkin et al., 2013: 282) and a ‘deep-seated distrust of any concentration of financial power in general, and of central banks in particular’ (Bordo, 2007: 2). Two earlier attempts to establish a central bank were short-lived (1791–1811 and 1816–1836), until eventually, and amid fierce political battles (Jäger and Maggor, 2020), the banking panic of 1907 forced the creation of the Federal Reserve in 1913 (Bordo, 2007: 2; Mishkin et al., 2013: 282). The role of the Fed has been subsequently shaped by further economic crises.

The first major change in the Fed's role within the American financial system came in the wake of the 1930s crisis. As the focus of capitalist development progressively shifted away from Europe towards the US, the American economy became the epicentre of a financial crisis of major proportions. In the banking panics of the early 1930s, the Fed failed to act as a lender of last resort (Bordo, 2007: 2) and thus failed to contain the financial crisis. What followed was a devastating deflation and economic depression, accompanied by a catastrophic loss of employment. The Great Depression of the 1930s, in turn, led to the reshaped role of the country's central bank – the Fed was made ‘subservient to the Treasury’ (Bordo, 2007: 2). In other words, financial chain 20 was further strengthened, with the Treasury having the upper hand.

After WWII, the Fed's role expanded to include full employment as its second key objective. Since then, the US central bank formally maintains its dual mandate (price stability and maximum employment; Ashworth, 2020: 6), although its commitment to the latter was tested when the Keynesian post-war consensus unravelled in the crisis-ridden 1970s. Indeed, as Jackson (2019) notes, when the Fed was forced to choose between the two mandates amid stagflation in the late 1970s, it clearly prioritised fighting inflation. The neoliberal and monetarist turn of the late 1970s and 1980s thus marked a dramatic shift of the role of the central bank in the US (and elsewhere). For some, combatting inflation now forms part of the very definition of a central bank (Casu et al., 2015: 122). This anti-inflation zeal went hand-in-hand with a drive towards ‘central bank independence’ of which the ECB is the starkest example.

The ECB is the youngest and perhaps the most unusual of the three central banks as it came into existence through a culmination of efforts towards a European economic integration after WWII. This eventually led to the establishment of the Economic and Monetary Union (EMU) and the launch of the single currency, the euro, on the back of the Maastricht Treaty signed in 1992 (Heine and Herr, 2021). The ECB itself was established in 1998 (Casu et al., 2015: 168), ahead of the introduction of the euro – which was first an ‘invisible’ currency (between 1999 and 2001) and subsequently a physical one (since 2002). Unlike its US counterpart though, the ECB maintains only one primary objective, which is price stability (i.e. low and stable inflation) in the eurozone.

Another crucial difference between the ECB and the Fed (as well as any other central bank in the world for that matter) is that there is no ‘European state’ to speak of – and so the ECB does not have a corresponding national Treasury to interact with, the way the Fed or BoE do. Indeed, the eurozone, over which the ECB presides, is a collection of 19 European Union (EU) member states (out of EU's total of 27) that fulfilled the so-called Maastricht criteria (Heine and Herr, 2021: 18–19) and agreed to adopt the euro as their currency. The absence of a European state makes the ECB an extremely interesting case in the state capitalism debate – at the EU level the ECB is the state 4 . This also led some observers to conclude that the ECB is ‘the most independent central bank in the world’ (Mishkin et al., 2013).

The issue of ‘central bank independence’ is critical for examining the links between the state and capital. In essence, ‘central bank independence’ involves removing the influence of (supposedly profligate, inflation-inducing) Treasuries over central banks (Fontan and Larue, 2021). Thus, while still considered ‘the government authorities in charge of monetary policy’ (Mishkin et al., 2013: 275), central banks are largely free from direct control of democratically elected governments (Fontan and Larue, 2021; Tooze, 2020a).

The ECB appears to have the highest degree of independence between the central banks examined. Indeed, from the outset the ECB ‘was strictly forbidden to finance public budgets of member states or support the EU central budget’ (Heine and Herr, 2021: 17) and this principle was anchored in Article 123 of the Maastricht Treaty (Bateman, 2021: 941). This contrasts with cases where it is ‘legally possible for central banks to create money on behalf of governments … by lending to them’ (Ryan-Collins et al., 2012: 117). In the UK for instance, BoE is able to provide a sizeable ‘overdraft’ for the government through its ‘Way and Means’ facility (Bateman, 2021: 943) – thanks to the fact that direct loans to the government (financial chain 20 in Figure 1) are ‘expressly permitted’ under UK law (Bateman, 2021: 946).) Interestingly, the Fed appears to be the least independent of the three central banks. Indeed, its policies are subject to oversight by the US Congress and so the Fed could be best described as ‘independent within the government’ (Casu et al., 2015: 179). Nevertheless, the Fed is also considered an independent central bank because its decisions are not subject to approval by either ‘the president or anyone else in the government’ (ibid: 178). And while direct loans to government are not ‘expressly permitted’ under the US legal framework, they are not prohibited and the Fed (unlike the ECB) is also permitted to purchase government debt on primary markets (Bateman, 2021: 946).

Regardless of these differences, it could be argued that in all three cases, the principle of the ‘central bank independence’ normalised a separation between politics and the management of the economy via monetary policy. At the same time though, central banks have become more deeply entangled with, and dependent on, financial markets (Braun, 2020a; Braun and Gabor, 2020; Fontan and Larue, 2021). In other words, the ‘central bank independence’ weakened the financial chain 20 and strengthened the financial chain 22 (see Figure 1) as part of a wider neo-liberal turn.

Towards a big (monetary) state?

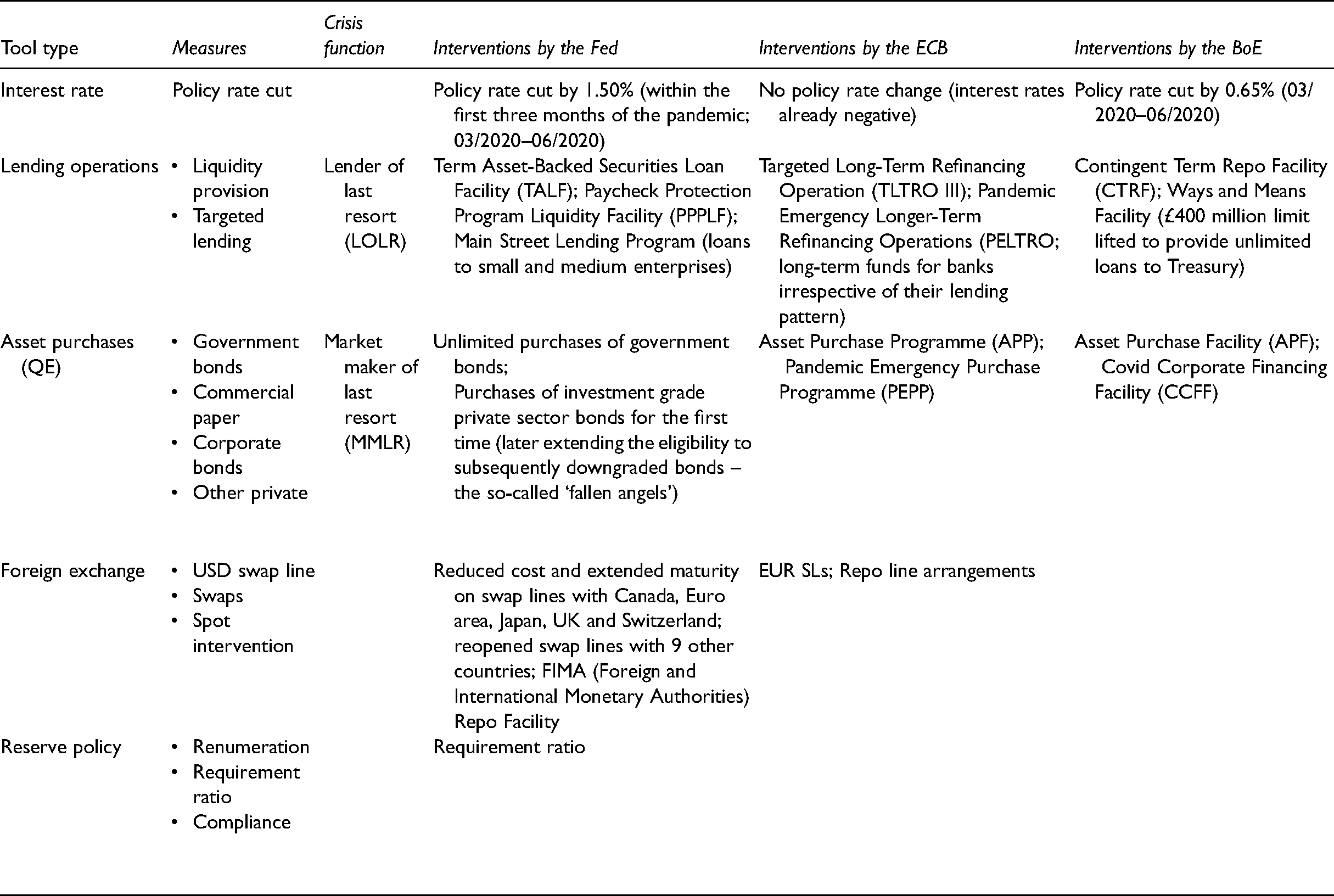

The limits of neo-liberal, financialising capitalism were starkly exposed in 2007–2008 when the Global Financial Crisis hit. At the time, all three central banks in question were forced to intervene to prevent a major collapse (see also Tooze, 2018). In order to contain the potential economic damage, a range of unconventional tools were deployed with quantitative easing (QE) 5 being the most prominent and most contentious one (Ashworth, 2020). Similarly, the Covid-19 pandemic that hit the global economy in 2020 and caused the Great Lockdown (IMF, 2020) forced a fresh round of extraordinary interventions to prevent the system's collapse (Table 1).

Central banks’ pandemic toolkit: The Fed, the ECB and the Bank of England. Source: Building on Cavallino and De Fiore (2020) and Cantú et al. (2021).

Monetary authorities’ power has been greatly amplified by these economic crises. Central banks nowadays, act simultaneously – through the financial chains described above – as bankers of the state, bankers for the banks and bankers for the financial markets. In addition, and as part of its financial intervention due to the Covid-19 pandemic, the Fed also established lending facilities for the non-financial sector (Cantú et al., 2021: 12). Thus, in a crisis situation, central banks can act as ‘lenders of last resort’ (LOLR) for banks, governments, and even non-financial firms, as well as being the ‘market makers of last resort’ (MMLR) for financial markets (Hauser, 2021: 6; Gabor, 2021) while performing ‘buyers of last resort’ (Hauser, 2021: 9) or ‘dealers of last resort’ functions (Mehrling, 2011; Tooze, 2020a; Wullweber, 2020). Crucially, it is important to stress that the above functions are underpinned by the extraordinary capacity of central banks to ‘create’ or ‘generate’ (financial) capital 6 .

It is generally accepted that without these monetary interventions, advanced market economies would have probably already collapsed (see also Tooze, 2020b). Central banks themselves are aware of the power they hold over the economic and financial system. For instance, the ECB president Christine Lagarde made it clear that the Bank's pandemic response prevented a ‘full-blown financial meltdown with devastating consequences for the people of Europe’ (Lagarde, 2021). Clearly, it is no exaggeration to say that contemporary central banks have assumed a pivotal role in Western capitalism (see also Braun and Gabor, 2020; Lapavitsas and Mendieta-Muñoz, 2016; Walter and Wansleben, 2020).

In fact, from all the actors depicted in Figure 1, central banks are perhaps the only players that can act independently of prevailing economic circumstances during crises and thus alter crisis dynamics (Sokol and Pataccini, 2020: 409–410). As rightly noted by Tooze (2020b), a central bank's budget ‘is unlimited’ and so the institution ‘is the only crisis-fighter with truly unlimited firepower’. The extraordinary power of a central bank stems from the fact that it can create money (capital) at will, so to speak. It can expand its balance sheets to undertake unlimited asset purchases (QE) or provide unlimited lending (see Table 1) – thanks to its function as a ‘creator’ or ‘generator’ of (financial) capital. Much of the money created ‘out of thin air’ is passed onto the financial markets (financial chain 22) and commercial banks (financial chain 21). Furthermore, as suggested by the proponents of Modern Monetary Theory (e.g. Kelton, 2020; Wray, 2020), central banks could also transfer funds directly to the government (financial chain 20 but with no strings or repayments attached) – a form of a pure, direct monetary financing that the government can use to invest in the economy. One way or another, these capital-generating operations raise important questions about the state-capital relationship, as highlighted by the problématique of state capitalism.

As trillions of dollars have been pumped into the financial system in the aftermath of the GFC and during the Covid-19 pandemic (Boesler and Takeo, 2020; Cavallino and De Fiore, 2020), we are reminded that ‘at the heart of the profit-driven, private financial economy is a public institution, the central bank’ (Tooze, 2020b). For Gabor (2021), the extraordinary interventions by central banks represent a ‘shadow monetary financing’ – central banks purchasing large quantities of government bonds. In effect, one branch of the state (the central bank) has been buying up, via the financial markets, debt of another branch of the state (the government) to keep the system functioning. However, as Gabor argues, these operations of central banks signal their commitment ‘to maintain cheap financing conditions for private finance, not for fiscal authorities’ (Gabor, 2021: 22). That said, some authors have noted that, during the Covid-19 crisis, some central banks (such as the ECB) pursued policies whose ‘explicit purpose [was] to facilitate government borrowing’ (van ‘t Klooster, 2021: 6). Meanwhile, with regard to their support of financial markets, some scholars have argued that public authorities (including central banks) simply ‘stepped in to prevent the worst from happening’ (Murau, 2017: 814; see also Mehrling, 2011). Nevertheless, it is hard to escape the impression that, by doing so, central banks in effect provided a massive public ‘subsidy’ for private financial markets. This begs the following question: if subsidies provided by the state for the productive economy are seen as indicative of state capitalism, would subsidies for the financial markets and banks also qualify? Several recent contributions to the state capitalism debate (e.g. see Alami and Dixon, 2021: 19–20; Alami et al., 2022: 3) appear to contemplate this possibility.

Indeed, it may be possible to argue that one of the features that is new about the ‘new’ state capitalism in advanced market economies is the greatly enhanced role of central banks as capital ‘generators’ with new state-capital constellations created in the process. In this context, it is important to note that calls have already been made that we may be witnessing the rise of the ‘central bank-led capitalism’ (Bowman et al., 2013; Wullweber, 2020: 12). It appears that central banks are now central to financialised capitalism – without massive monetary interventions, the system could collapse. After decades of the neo-liberal mantra of the ‘small state’, we have thus ended up with what could be described as a ‘Big (monetary) State’. This to some extent echoes the earlier state capitalist arrangements under a post-war ‘Big (fiscal) State’ (see Gabor, 2021: 5), but without the automatic benefits of fiscal largess and in a radically altered political economy environment, with the central bank firmly in the driver's seat. Others described this as a ‘paradigm shift’ towards ‘technocratic Keynesianism’ (van ‘t Klooster, 2021).

At this point, it is important to underline the sheer scale of these monetary interventions. It has been estimated that in the case of the US, the Fed's balance sheet expanded from 5% of US GDP in 2007 (before the Global Financial Crisis hit) to over 20% of the country's GDP in 2014. The pandemic-related interventions of the Fed in 2020 then doubled its balance sheet to over 40% of GDP in a space of few months, and may increase even further (Heine and Herr, 2021: 154). In the case of the ECB, its balance sheet has more than tripled between 2007 and 2019 (in the aftermath of the GFC) and at the end 2019 (just before the pandemic hit) stood at 26.6% of eurozone GDP. The pandemic interventions in 2020 are likely to increase that figure to over 35% of eurozone GDP (Heine and Herr, 2021: 153). The size of this ‘subsidy’ for the financial system (and the economy more generally) is therefore far from negligeable.

It is worth noting that the growing power of central banks has met fierce criticism from both sides of the political spectrum. In the US, progressives point out that the Fed's policies benefit (financial) capital and wealthy elites, while lacking effective democratic scrutiny. Jackson goes as far as to suggest that the US is ‘not a country with a central bank’ but rather ‘a central bank with a country’ (Jackson, 2020a), pre-occupied with saving financial markets at the expense of workers (Jackson, 2020b). Meanwhile, conservatives complain that the Fed is ‘wielding undemocratic, Soviet-style powers over markets’ (see Politi, 2019).

In Europe, the ECB's interventions are also subject to political debates, further complicated by the fact that the eurozone membership involves 19 sovereign nation-states. ECB's independence in handling crises has frequently been called into question and some argue that ECB actions are favouring certain member states over others (e.g. see Tuori, 2016; Tooze, 2020a; Vermeiren, 2017; see also Bateman, 2021: 961–963; Varoufakis, 2017). Meanwhile in the UK, the Bank of England perhaps went farthest towards a direct monetary financing of the government by using, in crisis times, its ‘Ways and Means’ facility (Bateman, 2021). Offering the UK government unlimited borrowing from the central bank may have raised some eyebrows, although the BoE is at pains to stress that this is only a temporary measure, and that the money will eventually be repaid by the UK government. 7

To sum up, unconventional, and in many ways unprecedented, interventions performed by the three central banks – especially those involving new ways of creating capital – have important implications for the problématique of state capitalism debate. With regard to the questions raised in the section State capitalism debate, one could make the following preliminary observations. First, in terms of central banks shaping relations between the state and capital, it could be argued that the role of the state has increased in relation to capital in a sense that the state (via its central bank) acts as a ‘creator’ or ‘generator’ of capital to support the financial markets and the (new) financialised economy more generally. Second, it is hard not to see this as not being an instance of state capitalism. Indeed, if augmented interventions in the ‘real’ economy (e.g. subsidies to the productive enterprises) are included in the definition of state capitalism, it is difficult to exclude these sizeable ‘subsidies’ for the financial markets (and financial institutions more generally) from such a definition. Third, while a comparison of the three central banks reveals important differences in their links with the (rest of the) state, there are also significant similarities. Importantly, all three banks have acted as creators of (financial) capital. Moreover, their combined interventions could be seen as part of an aggregate expansion of the state's role in the Western capitalist core and in the global economy more generally.

Fourth, the extent to which monetary interventions of these central banks could be seen as transgressing the ‘normal’ separation of public and private spheres of economic activity is subject to intense debates. Certainly, by comparing the current post-crisis reality with the ‘ideal’ of central bank independence, their recent unconventional operations may have crossed the line in the eyes of many. However, seeing things from a longer-term perspective (e.g. see Gabor, 2021), the current level of central bank involvement (measured by their balance sheet size) is matching pre-central bank independence era levels. The difference is that previously (during the post-WWII Keynesian consensus) central banks were subject to direct government control, while nowadays (courtesy of their independence) they are acting without any real democratic control (see also van ‘t Klooster, 2021). Moreover, interventions of central banks also have implications for the ‘uneven and combined’ nature of state capitalism discussed in turn.

Central banking, financial chains and uneven and combined state capitalism

This section addresses the question of how contemporary central banks fit within the framework of ‘uneven and combined state capitalism’ (Alami and Dixon, 2021). Here there are two dimensions that need to be emphasised. First, it is clear that, by managing financial chains, central banks are (willingly or not) shaping economic geographies within their respective jurisdictions. The main traditional policy tool of central banks is the power to set interest rates (and in doing so, to control inflation). But it is well documented that changes in interest rates are not spatially neutral (e.g. Mann, 2010). For example, the dramatic rise of rates in the US in 1980 (the so-called ‘Volcker shock’) had devastating implications for jobs in manufacturing heartlands (Jackson, 2020b; Tooze, 2020a; see also Lapavitsas and Mendieta-Muñoz, 2016). In the UK, the infamous statement from the Bank of England governor that increased unemployment in the country's north was ‘a price worth paying’ for keeping national inflation low (quoted in Martin, 2001: 56, note 4) highlights the problematic nature of central bank policies for less favoured regions. However, as described in previous sections, central banks are now deploying a much larger range of policy tools. It is to be expected that the massive monetary interventions undertaken in recent years will have significant uneven consequences amongst different regions within their jurisdictions through spatial impacts of the affected financial chains (see Sokol and Pataccini, 2021 for more details).

Second, it is becoming clear that unconventional monetary policies of leading central banks have profound effects well beyond their formal territorial boundaries. Indeed, it appears that monetary interventions are shaping, and are shaped by, the global uneven development. In this context, it is worth noting that Fernandez and Aalbers (2020) have advanced the notion of ‘uneven and combined financialisation’ as a way of capturing uneven trajectories of financialisation across the Global North and Global South. Importantly, they also recognise the role central banks are playing in the process. In particular, they highlight (following Kaltenbrunner and Painceira, 2018; and others) how quantitative easing (QE) by central banks in advanced market economies has had an impact on capitalist peripheries and semi-peripheries. In essence, massive asset purchases completed as part of QE in the wake of the GFC freed up capital in the Global North that subsequently found its way into the Global South, accelerating financialisation and increasing vulnerabilities there (see also Lim et al., 2014). In other words, powerful central banks in the capitalist core can have a significant impact on the development trajectories of economies well beyond their territorial boundaries. As such, they are, in effect, participating in wealth redistribution at a global scale via transnational financial chains.

Transnational impacts of monetary policies and the financial chains they shape also underline the point made by Sokol and Pataccini (2020: 410) that ‘not all central banks are born equal’. Indeed, it serves as a valuable reminder that the global financial architecture is underpinned by a powerful international hierarchy of money (e.g. see Kaltenbrunner and Painceira, 2018) with the US dollar (and the Fed) in a hegemonic position. As such, the US economy enjoys ‘exorbitant privilege’, supported by the Fed's unlimited ‘firing power’. Europe, despite its monetary integration efforts, remains in a subordinate financial position vis-à-vis the globalised US financial system (Grahl, 2011), with the euro (and the ECB) still playing second fiddle to the US dollar. At the same time, central banks in many emerging economies are left ‘fire-fighting’ the effects triggered by the actions of their counterparts in advanced market economies. Finally, the cascading international hierarchy of money (and financial chains) ensures that central banks in the poorest countries of the global periphery are the least powerful. Having access to US dollars from the Fed (via swaps or repo facilities; Table 1) can be a matter of national economic survival. These asymmetries of central bank power support the ways financial chains operate at an international level, facilitating transfers of value at a global scale. Indeed, as Fernandez and Aalbers (2020: 686, emphasis original) argue, ‘net financial movements have been flowing uphill, from the periphery to the core’ (see also Kaltenbrunner and Painceira, 2018; Lapavitsas, 2009; Sokol and Pataccini, 2020). Either way, it would appear that spatial dimensions of central banks’ capital-generating operations could easily fit within the framework of ‘uneven and combined state capitalism’ put forward by Alami and Dixon (2021), while also contributing to inherently geographical nature of financialised capitalism (e.g. see Christophers, 2012).

Conclusions

This paper has explored the question whether unconventional interventions of central banks could be seen as manifestations of (new) state capitalism. The paper has mobilised the ‘financial chains’ perspective to illustrate the pivotal role contemporary central banks play in the Western financialised capitalism and its uneven geographies. By examining the cases of three central banks from the advanced capitalist core in the West (the US Federal Reserve, the European Central Bank and the Bank of England) the paper has highlighted the fact that through their unconventional interventions such as quantitative easing, these central banks have in effect become ‘creators’ or ‘generators’ of (financial) capital. These interventions could be seen as providing sizeable ‘subsidies’ for the financial markets, financial institutions and the economy more generally, and it is difficult to exclude them from being considered as instances of state capitalism. Furthermore, it could be argued that central banks’ role in shaping uneven economic geographies across space has been further enhanced by these interventions. Spatial dimensions of central banks’ capital-generating operations could thus easily fit within the framework of ‘uneven and combined state capitalism’. Based on this, the exclusion of monetary operations performed by central banks from being understood as part of the repertoire of ‘state capitalism’ is unjustified. Indeed, the state capitalism approach should include central banks in its rubric – recognising their pivotal role in managing (creating and sustaining) of financial chains and in turn shaping uneven economic geographies at various scales.

Theoretical implications of these insights are twofold. First, the possibility of recognising the unconventional operations of central banks as state capitalist could go hand in hand with a modified definition of state capitalism. Indeed, the rubric of state capitalism could potentially be enlarged to include configurations of capitalism where the state plays a particularly strong role not only as promoter, supervisor and owner of capital but also as a ‘generator’ of capital. Second, one could argue that the list of state capitalist tendencies (‘productivist’, ‘absorptive’, ‘stabilising’ and ‘disciplinary’) identified by Alami and Dixon (2021: 18–21) could also be extended. Indeed, a fifth category could potentially be added, tentatively called here a ‘generative’ tendency. This ‘generative’ tendency of the ‘new’ state capitalism, while partly overlapping with the other four tendencies, appears crucial in sustaining financialised capitalist systems and thus requires further attention. In some sense, this capital-generating tendency could be seen as strongly associated with the ‘stabilising’ tendency. But given that the very process of generating capital can potentially have de-stabilising effects further down the line, the ‘generative’ tendency could be treated as distinct from the ‘stabilising’ tendency.

In addition to this, there are some practical (policy) implications that should be highlighted here. The existential question is whether the enormous power of central banks could also be mobilised to meet societal challenges (rather than focusing on propping up financial markets at all costs). Indeed, there is a growing debate on whether central banks should promote more socially just (e.g. Braun, 2020b; Jackson, 2020b) and more environmentally sustainable economies (e.g. Braun et al., 2020; Mazzucato et al., 2020). With regard to the environmental imperative, and as noted earlier, the whole economic edifice rests on land and nature. Thus, unless the climate emergency is addressed, the whole financialised economy, no matter how sophisticated, may collapse. It is becoming clear that monetary authorities can no longer remain passive in climate action (even if they stick to their current, rather narrow mandates). Indeed, they need to act decisively, and in tandem with fiscal authorities, to avert ecological disaster, e.g. by directly supporting transformational climate policies such as Green New Deals (Boyle et al., 2021). In parallel, it is important that central banks, as key state institutions, utilise their potential for positive social impact (including employment and, more widely, social equality). Finally, it is essential that the spatial impacts of monetary actions are thoroughly scrutinised, and that new monetary tools are developed to promote balanced territorial development which cannot be separated from environmental and social sustainability goals.

Footnotes

Acknowledgments

This research has received funding from the European Research Council (ERC) under the European Union's Horizon 2020 research and innovation programme - project GEOFIN “Western Banks in Eastern Europe: New Geographies of Financialisation” https://geofinresearch.eu (Grant Agreement No. 683197). I am grateful to the guest editors of this special issue - especially to Jamie Peck and Adam Dixon - and three anonymous referees for their generous and valuable comments and suggestions, all of which helped to greatly improve the paper. All remaining mistakes or omissions are mine. An earlier version of this paper appeared as GEOFIN Working Paper No.13 and was presented at the Global Conference on Economic Geography (GCEG) in Dublin, Ireland, in June 2022 at a special session ‘Financialisation: Disruptions, Displacements and Discontents', co-organised with Leonardo Pataccini and Jennie Stephens. I would like to thank my co-organisers and all participants of the session for stimulating questions, discussion and feedback. Last but not least, I would like to thank members of my GEOFIN team, in particular to Leonardo Pataccini, Rodrigo Fernandez, Zsuzsanna Pósfai, Sara Benceković, Caroline Bourke, Flo O’Regan, Dimitri Paraskevas and Marek Mikuš, for their feedback, collegial support and creative intellectual environment.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work was supported by the H2020 European Research Council (grant number 683197).