Abstract

The era of dollar-based financial globalisation has seen a steady rise in the use of foreign exchange (FX) swaps. We provide a macrofinancial political economy perspective on the geography of FX swaps, and the spatial effects of central bank policies aimed at taming instabilities associated with the uneven geography of the dollar. First, we analyse the mechanisms and potential sources of instability involved in accessing dollars using FX swaps and repurchase agreement (repo) contracts, respectively, in both private and public (central bank) use. Second, we show that the distribution of currencies and institutions involved in trading swaps is skewed, reflecting both the dominance of the dollar as international financing currency and the uneven international distribution of dollar-denominated assets and liabilities. We document the changing composition of dollar swap users on both the long-dollar and short-dollar side and identify potential sources of macrofinancial vulnerability for dollar lenders and borrowers. The Fed's approach to global liquidity provision via both swaps and repos constitutes a spatially variegated strategy to preserve the hegemony of the US dollar. Despite its partial success in reducing instability due to cross-border financial imbalances, the Fed's uneven and hierarchical lender of last resort approach cannot sufficiently stabilise global finance to underpin a new era of macrofinancial stability.

Introduction

The era of dollar-based financial globalisation has seen a steady rise in the use of foreign exchange (FX) swaps by private financial institutions (Borio et al., 2017; Aldasoro and Ehlers, 2018; Schrimpf and Susko, 2019). Following the global financial crisis (GFC), central banks reintroduced swap lines in response to global dollar liquidity shortages (Aldasoro et al., 2020a; Carré and Le Maux, 2020; Murau et al., 2021; Choi et al., 2021). The growing use of private and official FX swaps reflects the Americanisation of national financial systems – first in rich and then across emerging market economies (EMEs) (Wójcik et al., 2017; Gabor, 2020) – and the increasing interconnectedness of financial networks. These have powered a global financial cycle (Rey, 2015; Gonzalez et al., 2019): changes in financial conditions and policies in the US and other rich countries have a direct, albeit varied, impact on financial conditions across the world, especially in EMEs.

The growing use of FX swaps has substantially altered the structure of global financial networks, reflecting an increasingly uneven geographical distribution of dollar assets and liabilities. This unevenness is closely associated with developments in global financial centres, and the dynamic relations between these. Yet the spread of the FX swap markets across space, the impact on regional macrofinancial vulnerabilities, and the implications of the public use of swaps for the distribution of power in global finance are under-explored from a political economy perspective. This is a significant gap in the literature that has recently studied the spatial aspects of financial markets, actors and instruments – in line with calls for geography-oriented approaches to the analysis of global financial networks (Wójcik, 2011; Coe et al., 2014; Barnes and Christophers, 2018; Hall, 2018; Ioannou and Wójcik, 2019).

Scholarship has investigated, inter alia, the changing pressures on the liabilities of institutional investors such as pension funds and insurance companies (Clark and Monk, 2006, 2007), the growing importance of sovereign wealth funds as instruments to maximise state autonomy (Monk, 2011), the spatio-temporal effects of Special Purpose Vehicles (SPVs) and financial derivatives (Bryan et al., 2016), the demand for EME assets in the context of liability-driven investment by the pension funds and insurance companies of rich countries (Bonizzi and Kaltenbrunner, 2019), and the geography of financial regulation, investment banking and foreign exchange trading (Christophers, 2016; Wójcik et al., 2017; Wójcik et al., 2018). The literature has also explored policy innovations such as Mexico's use of derivatives for increasing FX reserves throughout 2010 and 2011 (Munoz Martinez, 2016), Brazil's tax on foreign exchange derivatives (Alami, 2019) and use of derivatives to limit excessive currency volatility. Yet, the role of FX swaps has only sporadically been discussed in this literature (e.g., Gabor, 2020; Beck, 2021; Murau et al., 2021; Kalaitzake, 2022). A systematic investigation of both private FX swap markets and official swap lines is still missing.

We make three contributions towards filling this gap. First, we clarify the balance sheet mechanisms involved in private and official FX swaps. We challenge the Bank for International Settlements (BIS) view that the FX swap contract is functionally equivalent to the repo contract (Borio et al., 2017): although both are potential sources of financial fragility, the risks generated by swaps are distinct from those generated by repos when used by private financial institutions to access dollar liquidity. When deployed as public tools to stabilise the global dollar financial cycle, the combination of swaps and repos creates a hierarchy of access to official dollar reserves.

Second, we draw on empirical evidence to shed light on the financial geography of FX swaps. Although the relatively persistent structure of global trading centres suggests that ‘the political–economic geography of forex markets is subject to powerful inertia’ (Wójkic et al., 2017, p. 273), we show that the evolving nature of swaps, from public to private, has significantly altered the geopolitical arrangements underpinning the dollar hegemony: the distribution of currencies traded, nationalities of financial institutions (where legally headquartered), and geographic and legal locations of trading are increasingly skewed, reflecting both the dominance of the dollar as international financing and settlement currency and the uneven international distribution of dollar-denominated assets and liabilities. Using a Minskyan lens (see Dymski, 2017; Bonizzi and Kaltenbrunner, 2019; Gabor, 2020), we document the changing composition of FX swaps users on both the long-dollar and short-dollar side and identify sources of macrofinancial vulnerabilities for dollar lender and borrower countries. In doing so, we provide novel insights into the geography of the ‘global financial cycle’ (Rey, 2015), with its large dollar-dominated FX swap footprint, hitherto neglected in the scholarly literature.

Third, we critically assess the spatial and political dimensions of the Federal Reserve dollar lender of last resort mechanisms, which include both swap and repo lines. The Fed's approach to dollar liquidity provision is a spatially variegated strategy aimed at preserving the hegemony of the US dollar while mitigating the financial stress resulting from increasing global demand for dollar liquidity. The Fed's insistence that its swap-based support should provide temporary liquidity relief but not fund exchange rate interventions (Choi et al., 2022) suggests that despite institutional innovation, the dollar hegemon promotes a currency derisking logic in EMEs that insures (global institutional) investors against the depreciation of local currencies (Gabor, 2020; Musthaq, 2021a), while rejecting an EME activist approach both to addressing the vulnerabilities of the global financial cycle via capital controls and to competitive exchange rate management. We argue that despite partial success in containing instability, the Fed's emerging role as global dollar lender of last resort does not constitute a mechanism that can sufficiently stabilise global finance to underpin a new era of macrofinancial stability.

FX swaps vs repos

Although the financial geography literature highlights the importance of global financial centres in FX trading (Wójcik et al., 2017), it pays less attention to the practices through which finance pursues product and process innovation in order to create spaces accommodative to the search for yield. The FX swap/repo nexus is illustrative conceptually and significant empirically. Borio et al. (2017) argue that FX swaps are functionally equivalent to repo contracts but, unlike repos, are not recorded on balance sheets as debt instruments. This accounting contingency implies not only that global financial accounts understate the total volume of debt – by at least $10.7tn in 2017 – but more importantly, that this missing debt, with its distinctive spatial manifestations, can create significant vulnerabilities. We explore (and reject) the claim that FX swaps and repos are functionally equivalent. Nonetheless, we highlight the potential for FX swaps and repos to contribute to macrofinancial instability during periods of market stress, and to create hierarchies of access to dollar liquidity when deployed by central banks.

The FX swap contract

The FX swap is a contract made up of two separate transactions, or ‘legs’: in the first, a cash sum held in one currency, for example, dollars, is exchanged at the prevailing exchange rate for a cash sum held in another currency, for example, yen. In the second leg, a reverse exchange is made, with the original provider of dollars now receiving dollars and handing back yen to the original provider. The sums exchanged in the second leg (in which currencies are ‘swapped’ back) are determined when the contract is initiated, based on the current spot exchange rate and the current ‘forward’ rate: the second leg of an FX swap is equivalent to a ‘forward’ contract, in which two parties agree to exchange cash sums in different currencies at a given future date at a pre-agreed exchange rate. The two legs, spot and forward, are bundled together into a swap to reduce transactions costs and to facilitate the rolling over (renewal) of contracts.

Although FX swaps do not involve interest payments, a related instrument, the currency swap, is equivalent to an FX swap with the addition of interest payment flows for the duration of the contract. FX swaps can therefore be thought of as a money market instrument and currency swaps as a capital market instrument. The duration of both instruments is mostly short term: BIS data show that at the end-2016, three-quarters of positions had a maturity of less than one year, and the modal FX swap has a maturity of less than a week (Borio et al., 2017, p. 41).

FX swaps vs repos: private markets

The economics and finance literature approaches FX swaps from the perspective of arbitrage: the price of swaps is expected to reflect interest parity relationships. This analysis focuses on ‘efficient’ pricing but does not consider the role of liquidity. However, liquidity is crucial, and its macrofinancial role can be illustrated by comparison with an apparently similar repurchase agreement (repo). The repo, a collateralised money market debt instrument, plays an increasingly central role in managing liquidity conditions both within and between major financial centres (Gabor, 2020), despite its systemic role in the run on Lehman Brothers (Gorton and Metrick, 2012; Gabor, 2016; Gabor and Ban, 2016).

A repo resembles a swap contract in that it consists of the sale and subsequent repurchase of security at an agreed price. In the first leg of a repo, collateral in the form of securities (e.g., government bonds) is exchanged for cash. In the second leg, the collateral securities are returned, and a cash transfer is made in return. The difference between the cash sums transferred in each leg represents the interest that the repo cash borrowers pay. 1

To make the case for the functional equivalence of repos and FX swaps, Borio et al. (2017) consider the case of an agent, for example, a Japanese bond investor, wishing to hold a dollar-denominated security while hedging exchange rate risk. This can be achieved in two ways: either by swapping yen for dollars in the FX swap market, and using the dollars to purchase a security, or by financing dollar securities through borrowing in dollar repo markets. In each case, the investor is hedged against foreign exchange risk: in the case of the FX swap, the exchange rate at which the swap will be reversed is agreed at the start of the contract. In the case of dollar repo borrowing, the investor faces no currency mismatch. In both cases, the investor will receive a dollar income flow in the form of coupon payments on the bond.

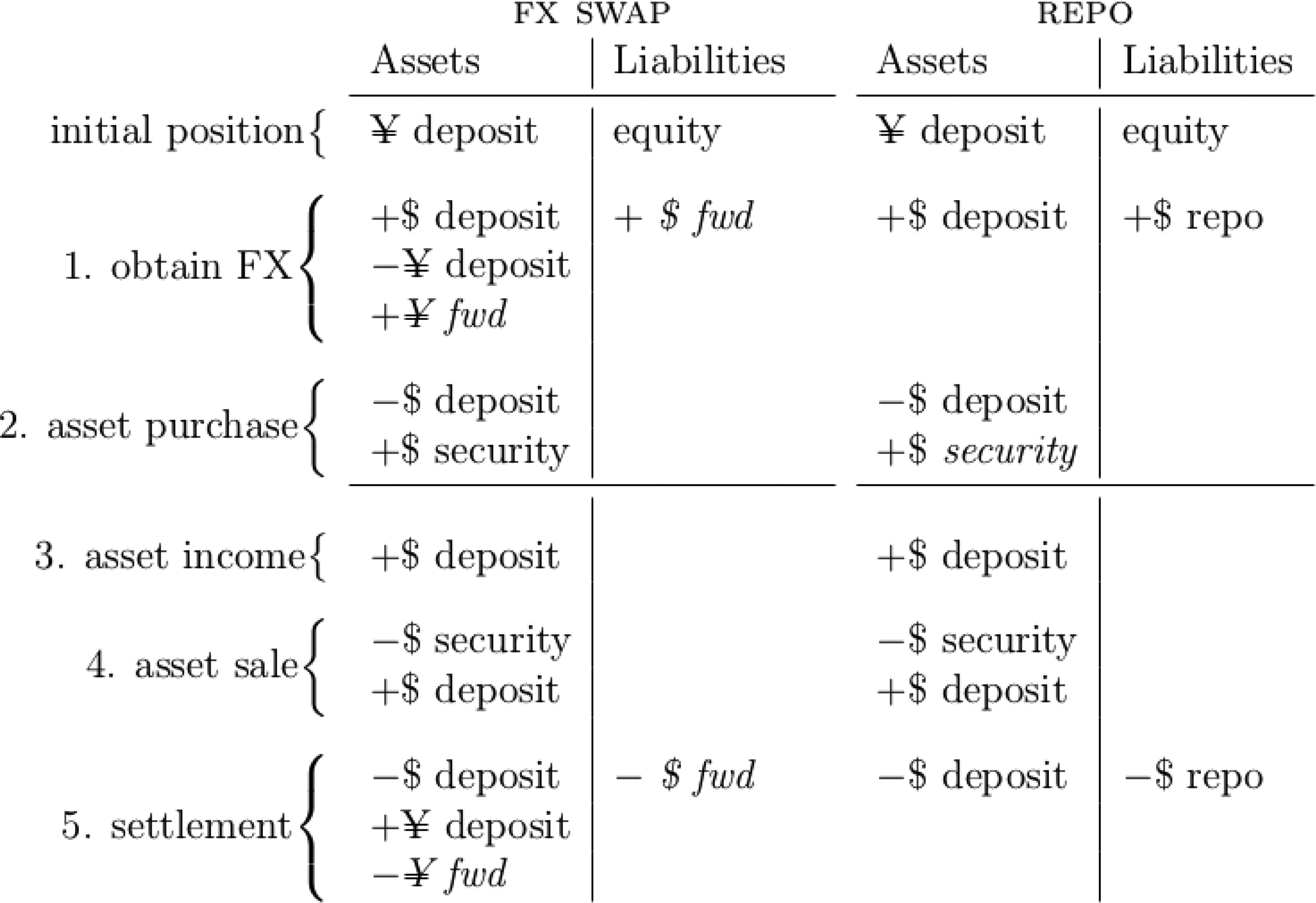

The apparent similarity between the two contracts does not demonstrate functional equivalence, however. Consider the sequence of balance sheet transactions involved in each contract, as shown in Figure 1. These show an initial balance sheet position followed by a sequence of five steps from the initiation of contracts to settlement. For each step, the changes in balance sheet entries are shown.

The sequence of balance sheet transactions involved in the case of repo finance and use of an FX swap.

The initial position of the balance sheet at starting time t is identical in both cases: the investor holds a yen deposit, matched by net worth. In step 1, the investor obtains the dollar deposit that is needed to purchase the security. In the case of the FX swap, this is done by handing over the yen deposit in return for a dollar deposit, while entering into a forward agreement (an off-balance sheet promise to swap back into yen when the FX swap matures). In the case of repo, dollars are obtained by borrowing in the money markets using the security that the investor will purchase as collateral. 2

Note that after step 1, the Japanese investor still holds a yen deposit if it finances dollar securities with a dollar repo. In contrast to the FX swap, which is an exchange of deposits on the asset side (in which the yen deposit is surrendered), repo market borrowing triggers expansion of the balance sheet: a dollar deposit is added to the asset side alongside the yen deposit, while a dollar repo loan is added to the liability side.

Step 2 involves the purchase of the dollar asset: the dollar deposit obtained in step 1 is exchanged for a dollar-denominated security. At time t + 1, in step 3, the investor receives income from the asset (e.g., coupon payments), increasing dollar deposits on the asset side. In step 4, the investor sells the dollar asset, exchanging the security for dollar deposits. Steps 2–4 are thus identical in both cases. Finally, the FX swap or repo contract is settled in step 5: in both cases, this involves handing over a dollar deposit. In the case of the FX swap, a yen deposit is received in return, as the forward claims are honoured and thus removed from the balance sheets. In contrast, the repurchase leg of the repo shrinks on both sides of the balance sheet, as the dollar deposit is surrendered and the repo liability extinguished. Step 5 is thus the reverse of step 1.

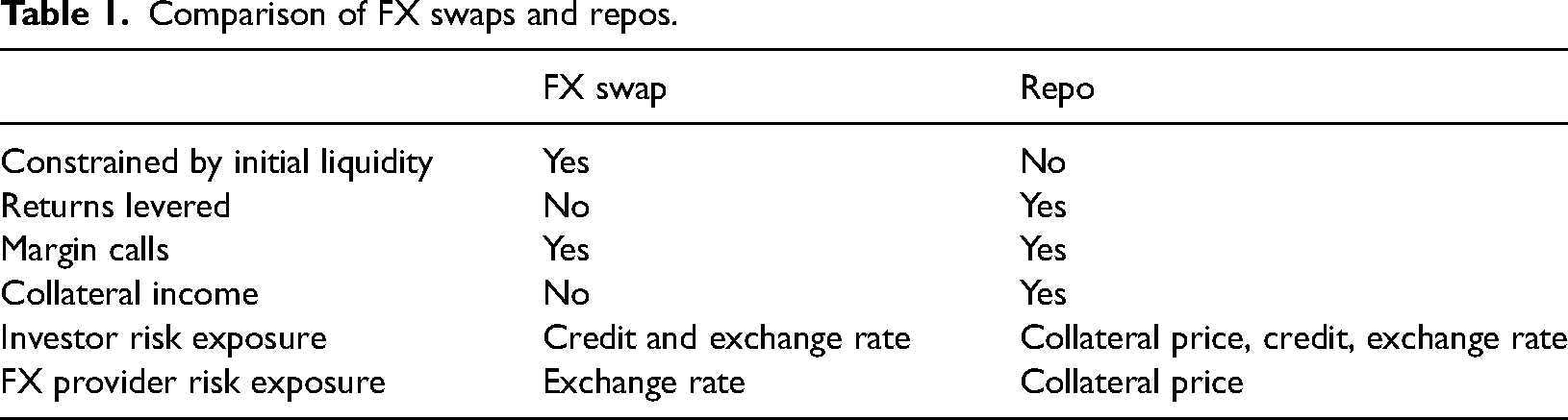

There are several important differences between the two contracts, summarised in Table 1. First, posting collateral in a repo contract, in exchange for cash, is not equivalent to handing over (foreign exchange) cash in an FX swap contract. The repo contract allows the Japanese investor to retain yen cash which can be used to purchase yen-denominated assets, or swapped for dollars to purchase another dollar-denominated security. The use of FX swaps is therefore constrained by the initial liquidity of the balance sheet: in order to take part in a swap contract, an agent must first own domestic currency (yen) deposits. In contrast, a repo loan requires only the security posted as collateral, which itself may be funded by the repo loan.

Comparison of FX swaps and repos.

In consequence, the extent to which balance sheets, and thus returns, can be levered differs. In the case of the FX swap, at step 2 in Figure 1, the investor has reached the limit of their exposure to dollar assets using FX swaps: without yen deposits, the investor has nothing to swap for dollars, and thus cannot extend their holdings of dollar assets. In contrast, there is no such constraint to repo borrowing: the volume of dollar assets that that investor can hold is limited by the willingness of lenders to extend dollar credit, and potentially by regulatory requirements, but not by the borrower's initial liquidity.

The risks faced by the (Japanese) investor and the supplier of dollars likewise differ across each funding strategy. In both, the investor faces credit risk associated with holding the dollar-denominated security. Margin calls are a potential source of risk in each contract type, but for different reasons. Repo contracts require collateral to be ‘marked to market’ as protection against collateral price volatility: if the price of the security posted as collateral falls (potentially as a result of illiquidity in collateral markets), the dollar lender will demand either additional collateral or cash, potentially leading to funding stress (illiquidity) for the Japanese investor. This risk may be exacerbated by exchange rate movements if there is a currency mismatch arising from the need to post margin in dollars. Repo lenders also face risks associated with liquidity in collateral markets: if the price of the collateral falls due to illiquid markets, it may not be possible to liquidate it should the borrower default. In some jurisdictions, and for some types of institutions, FX swaps also involve margin calls (known as ‘variation margin’) if the exchange rate moves relative to the agreed rate (Smith, 2017; ESA, 2019). In the case of the FX swap, both parties therefore face the potential risk of margin calls as a result of exchange rate movements while the contract is open. For both repo and FX swaps, liquidity-related market moves can therefore cause problems for either party while the contract is in effect. These risks are not identical, however. In particular, exposure to illiquidity in collateral markets is a feature of repo contracts but not FX swaps.

Potential liquidity issues arising from swap and repo positions are not limited to the balance sheets of the parties to the contract. Liquidity management practices and collateral illiquidity can generate spillovers that affect other market participants and market segments. Liquidity issues in repo markets can affect the FX swap market and vice versa. Some suppliers of US dollars in the FX swap market will borrow USD in the repo market and place the deposits obtained in the FX swap market, if it is profitable to do so given relative returns and collateral availability. Likewise, those holding dollar deposits – corporate cash pools for example – will compare the available returns on repo market loans to those available in the FX swap market. Repo rates and FX swap rates thus face pressure to remain aligned, at least outside periods of market stress: the repo market is both a source of dollar deposits that can be supplied in the FX swap markets, and an alternative to the FX swap market for those looking to park cash balances on a short-term basis. At times of market stress, liquidity concerns will trump potential arbitrage opportunities, and contracts will be unwound where possible.

The repo/FX swap nexus thus constitutes a significant innovation that enables leveraged positions to be taken across borders. These positions originate in traditional bank lending activities but are amplified by shadow banking. Systemic expansion of leverage involves both the traditional banking system – depository financial institutions and central banks – and shadow banks (Dafermos et al., 2020; Michell, 2017). The growing accumulations of leveraged cross-border positions have triggered significant changes in the relational and spatial arrangements of finance, and with it, new systemic vulnerabilities in the globalised, networked and hierarchical system of forex markets (Wójcik and Ioannou, 2020).

Official use of swaps and repos

The balance sheet mechanics of swaps and repos involving central banks differ substantially from those between private market participants (see also Aldasoro et al., 2020a; Murau et al., 2021). Consider swaps between central banks. In the first leg, central banks each ‘lend’ their own currency; these currencies can be issued directly by central banks, in contrast with the liquidity constraints involved in private swaps. Take, for example, the ECB and the Federal Reserve. They each hold a deposit account with the other. When they agree to enter a swap, the ECB's dollar deposit account with the Fed gets credited with the agreed sum, at an agreed exchange rate and for an agreed period. The ECB pays interest and also increases the euros in the Fed's account at the ECB. In the second leg, these operations are reversed, and the balance sheets of both parties are reduced. 3 Thus, the ECB, or any other central bank, can access dollar funding from the Fed to the extent that the Fed agrees to enter swaps. In contrast to private swaps, the money creation power of the central banks enables official dollar lending constrained only by the willingness of the US Federal Reserve to provide lender of last resort support to other central banks.

In contrast, official dollar borrowing via repos with the Fed is constrained by central banks’ official holdings of dollar securities to post as collateral. In the example above, the ECB can tap the Fed's dollar funding via repo lines to the extent that it holds US government bonds or other dollar securities that the Fed accepts as collateral. Where the Fed chooses to extend last resort dollar liquidity via official repo lines, it forces the counterparty central banks to first hold, or source, dollar securities. The Fed can also impose haircuts on securities to protect itself from credit risk, as is the case in private repo transactions, thus restricting the liquidity that can be obtained via repo lines. The dollar liquidity of non-US central banks can also be affected by revaluations of the securities that might lead to margin calls. Thus, there are limits to the amount of USD liquidity that central banks can access through repo facilities.

By determining which countries can access dollars via swap lines and which via repo lines, the Fed's repo/swap dollar lender of last resort mechanism creates a two-tier system of central banks: the first tier of central banks of rich countries enjoying (theoretically) unlimited access to dollar liquidity via swap lines, whereas the second tier of central banks of EMEs can only borrow via repo lines to the extent that they already hold dollar assets on their balance sheets. The first tier of central banks can, thus, more easily address local dollar vulnerabilities arising amongst others from the growing use of private FX swap markets, while the second tier of central banks faces constraints on their ability to do so. This reinforces the hierarchical nature of dollar-based financial globalisation. 4

The rise and vulnerabilities of private FX swap markets

Since the end of World War II, the dollar has retained its hegemonic position at the top of the currency hierarchy, despite major changes in settlement and exchange rate regimes and the international financial architecture. Although financial geography has traced the role that the demise of Bretton Woods played in the rapid increase in FX trading (Agnew, 2010), the role of swaps is less understood. The nature of swaps shifted, as the official swap arrangements used to defend exchange rates during the Bretton Woods system made way for private FX swap markets in the period up to the GFC. Following the crisis, alongside continued private expansion, official swap lines were revived and then formally institutionalised in an attempt to ensure that shortages of dollar liquidity would not destabilise globalised finance.

The Bretton Woods system, which lasted until 1971, was characterised by convertibility of dollars to gold, ‘fixed but adjustable’ exchange rates, liberalised currency exchange and restricted capital flows. This configuration meant that the US balance of payments substantially determined the availability of dollars as means of settlement. The 10-year period starting in 1958 saw continuous dollar outflows, driven by US current account deficits. Official swap lines among central banks were used to counter exchange rate pressures: when central banks were forced to buy dollars to prevent appreciation of their own currencies, the US Federal Reserve would guarantee a future exchange rate through the extension of swaps, reducing pressure on counterparty central banks to exercise their right to convert dollar holdings into gold (Tew, 1977; Bordo et al., 2015).

In addition to exchange rate management, official swap lines were also historically used for managing cross-border dollar liquidity. Alongside the flood of offshore dollars resulting from the US current account deficit, the late 1950s and 1960s also saw the rise of the Eurodollar markets: unregulated dollar lending by banks outside the US, predominantly in Europe. Central banks also used Eurodollar markets as a repository for official dollar reserves (Braun et al., 2020). During the 1960s, acting in concert with the Fed and other central banks, the BIS drew on Fed swap lines to manage liquidity in the Eurodollar markets. The BIS intermediated between central banks and Eurodollar commercial banks, making unsecured deposits with the latter to support their dollar liquidity during periods of speculative pressure on the dollar or war (McCauley and Schenk, 2020). The BIS thus acted as the first global dollar lender-of-last-resort throughout the late 1960s, albeit in close coordination with the US Federal Reserve.

This complex official swap architecture could not withstand the imbalances that ultimately overpowered the Bretton Woods system. In 1971, Nixon announced ‘temporary’ suspension of convertibility, with the intention of forcing countries with current account surpluses to abandon their pegs to the dollar. By 1973, most rich countries had moved reluctantly to floating exchange rates. Throughout the 1970s, the Fed drew on official swap lines, primarily for German marks, in attempts to defend the dollar from devaluation. 5 In turn, Germany attempted to limit the Fed's recourse to official swaps by attaching conditionality. From 1980, official swap lines between G10 central banks lay almost entirely dormant: only the Fed's swap line with Mexico saw continued use. US political discomfort with the expansion of this line during the peso crisis of 1993–94 led to the termination of all official swap arrangements in 1998.

Although exchange rate flexibility did little to tame the growth of international imbalances, it greatly increased the need for hedging mechanisms, in the form of FX swaps and forwards. Alongside cross-border positions arising from current account imbalances, the rolling back of capital controls and financial regulation enabled the rapid growth of cross-border financial positions that were increasingly disconnected from current account dynamics: dollars could be lent both by banks and, increasingly, by non-bank financial institutions around the world, while non-US institutions could take positions in dollar assets (Shin, 2009).

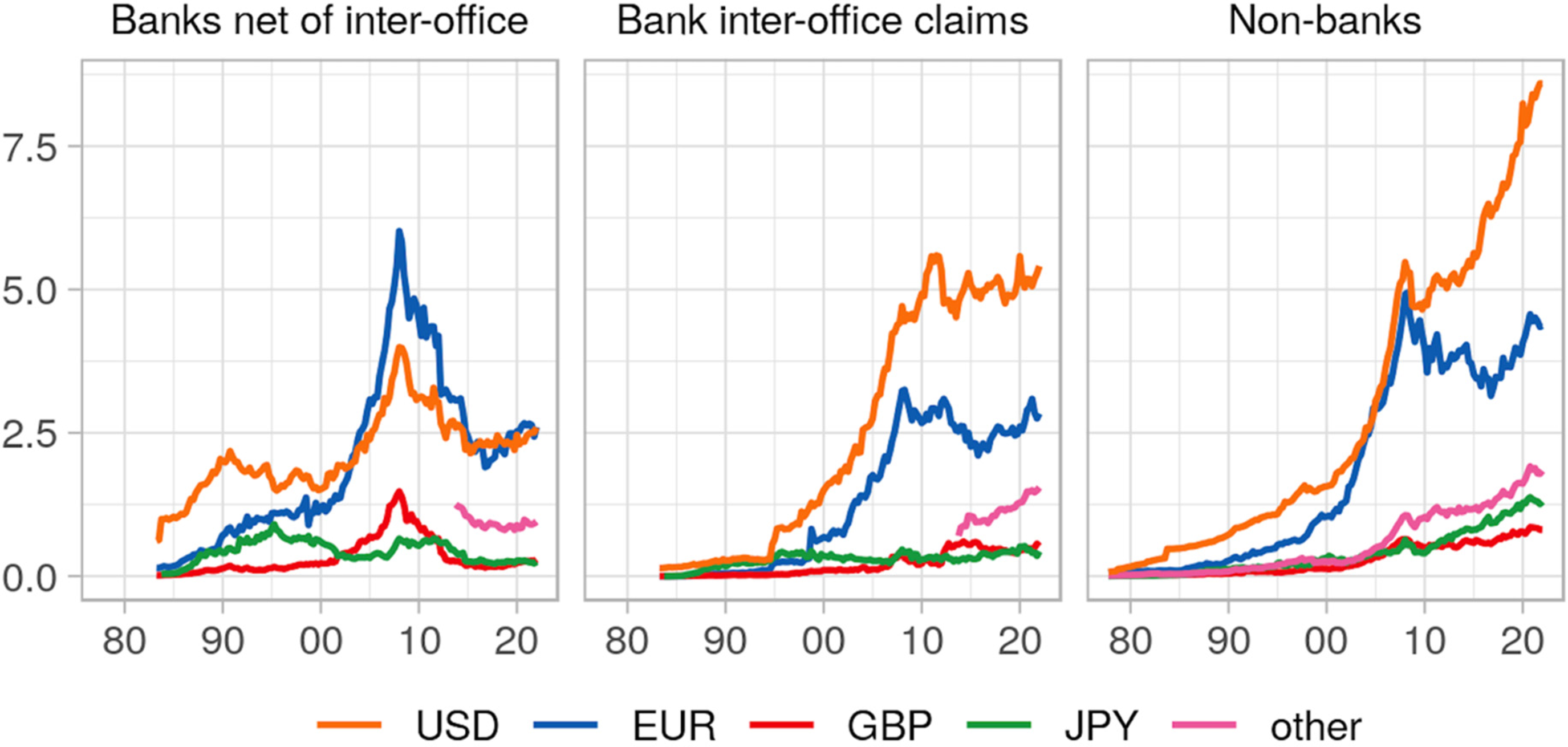

The growth in cross-border financial positions accelerated during the ‘great moderation’ of the late 90s and 2000s, as shown in Figure 2 (note that the use of nominal figures somewhat overstates this acceleration). The introduction of the euro saw rapid growth in euro-denominated cross-border positions, apparently challenging the dollar for the role of international settlement currency. 6 The aggressive expansion strategy of European banks saw a rapid increase in euro-denominated bank lending during the 2000s: euro-denominated cross-border bank assets (claims) grew rapidly (see also Christophers, 2013), reaching levels almost equal to dollar-denominated claims by 2008. In contrast, dollar-denominated interoffice claims – global banks circulating liquidity through internal capital markets – grew faster than euro-denominated interoffice claims. 7 The architectural flaws of the Eurozone and the mishandling of the Eurozone crisis tempered the viability of the euro as an international currency: since 2008, cross-border interbank positions shrank substantially, but euro positions shrank even more dramatically than dollar positions. 8

Total cross-border claims of BIS reporting banks, disaggregated by counterparty and currency, $tn, 1977 Q4 to 2022 Q1. Series for ‘inter-office’ and ‘banks net’ start 1983 Q2.

As global banks came under regulatory pressure to shrink investment banking activities, shadow banks (institutional investors, asset managers and others) became the engine of cross-border financial activity, driving a structural shift towards securities-based lending: bank claims on non-banks have driven the rise in cross-border dollar lending, with dollar-denominated claims rapidly recovering from the 2008 crisis, while euro-denominated claims declined. 9 The rise in cross-border holdings of dollar-denominated debt securities is not only more pronounced in rich countries but also visible in EMEs, starting from a lower level. At the same time, banks have reduced their holdings of cross-border securities, which are increasingly held by non-banks.

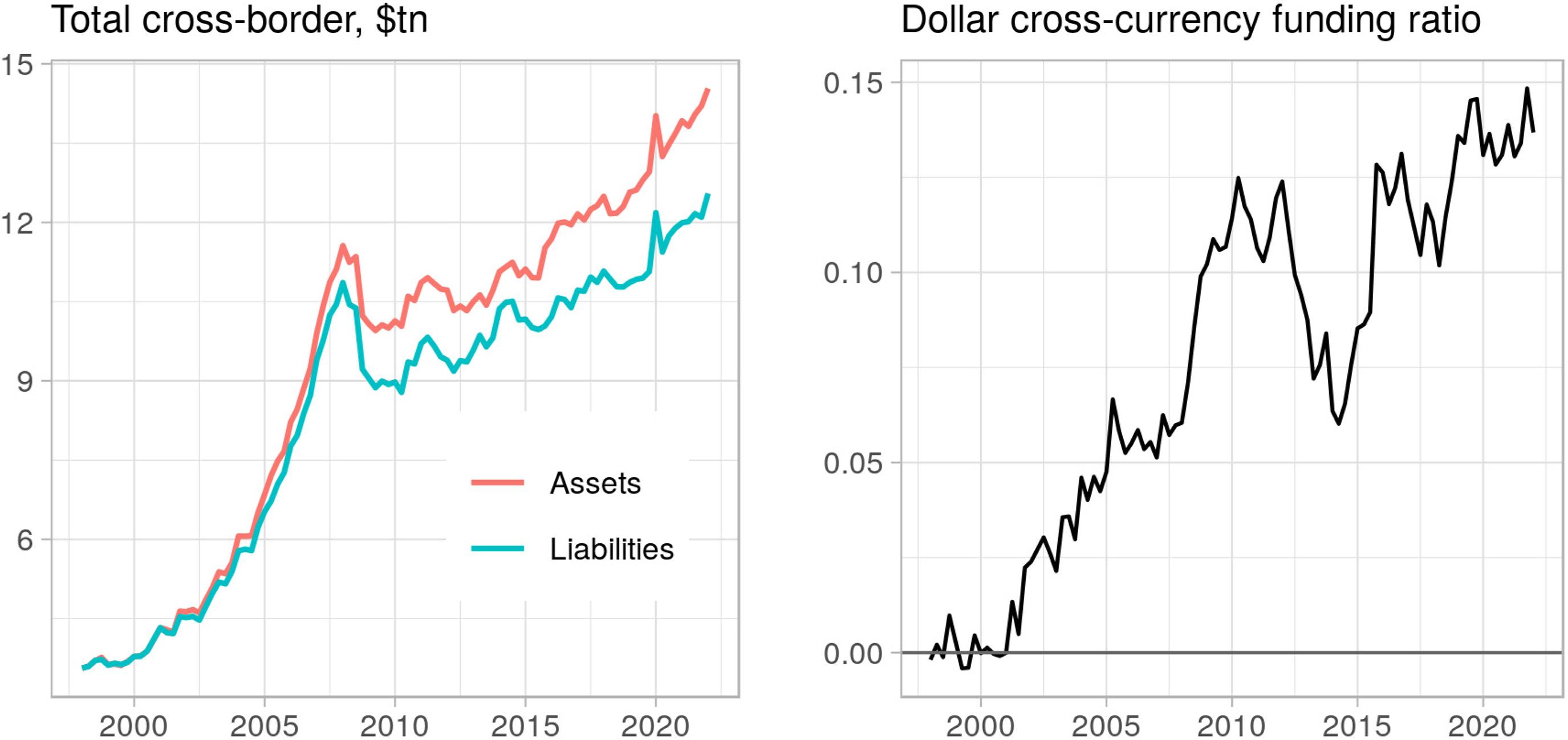

In a world of liquid and deregulated FX markets, (shadow) banks do not need to match the currency denomination of their assets and liabilities. From around 2000 onwards, a gap opened up between total dollar assets and dollar liabilities on bank balance sheets (see Figure 3). It is typically assumed that this gap is covered off balance sheet via the FX swap market (e.g., Borio et al., 2017; Nakaso, 2017). The overall funding gap declined substantially in the wake of the global financial crisis from around 12.5% of dollar-denominated assets to around 6%. From around the middle of the 2010s, however, the gap widened, reaching almost 15% by the final quarter of 2019.

Global dollar funding gap of banks reporting to BIS, 1998 Q1 to 2022 Q1.

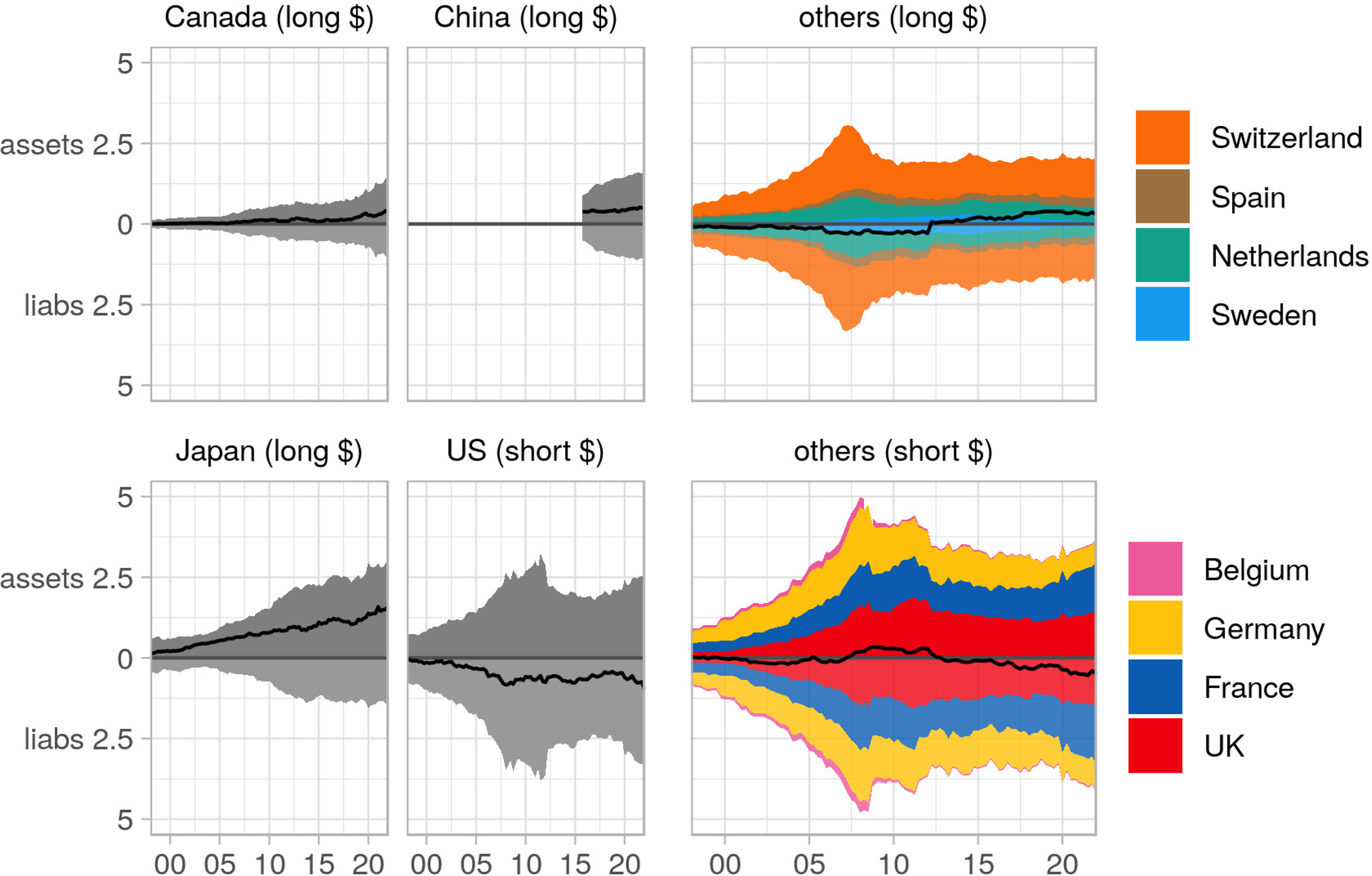

Although the structure of forex trading by currency has changed little (Wójcik et al., 2017), the aggregate dollar funding gap is distributed unevenly across banks of different nationalities (Figure 4). Japan is an outlier – the gross dollar-denominated positions of most other banking systems contracted in the wake of the 2008 crisis, while the dollar funding gap of Japanese banks has grown steadily since the mid-1990s. The banking systems of China, Canada, Switzerland and the Netherlands also have an excess of dollar-denominated assets over liabilities (long-dollar countries), while UK banks switched to short dollars overall. The US banking system has significantly greater dollar liabilities than assets, as, to a much lesser extent, do those of France and Germany. 10

Dollar assets, liabilities and net positions of banking systems by country, $tn (1998 Q1 to 2022 Q1).

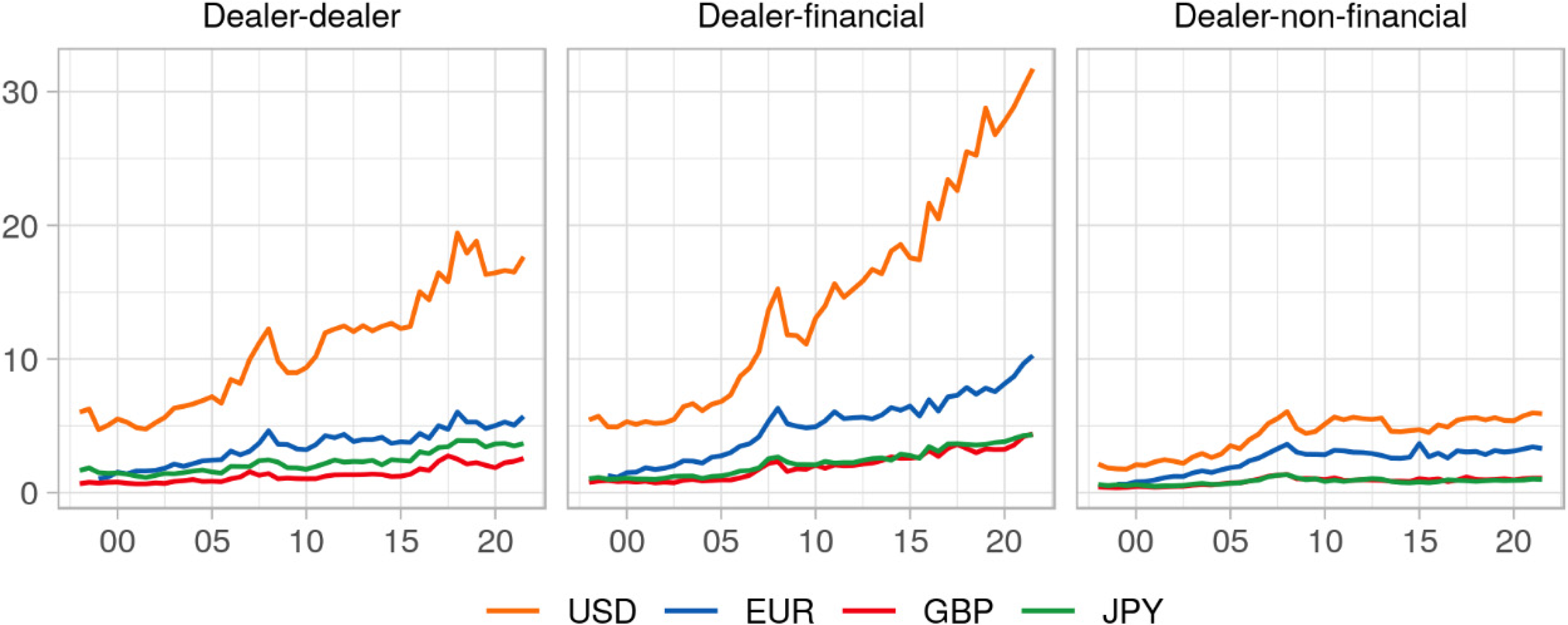

The trends in FX swap contracts reported to the BIS by dealer banks, disaggregated by currency and by counterparty sector, confirm the picture of USD dominance (Figure 5). After recovering rapidly from the dip during the crisis of 2008, total outstanding volumes remained relatively stable until a rapid rise from 2015 onwards, driven by inter-dealer contracts and swaps with other financial institutions. While it is likely that, in the period preceding the GFC, growth in swaps was partly driven by cross-border holdings of dollar-denominated mortgage-backed securities, the rapid recovery and growth of swaps since the crisis – which exceeds the growth of the dollar funding gap – suggests that such positions are not the fundamental driver of FX swap growth.

FX swaps outstanding reported by dealer banks, disaggregated by currency and counterparty sector, $tn (1998 H1 to 2021 H2, euro data starts 1999 H1).

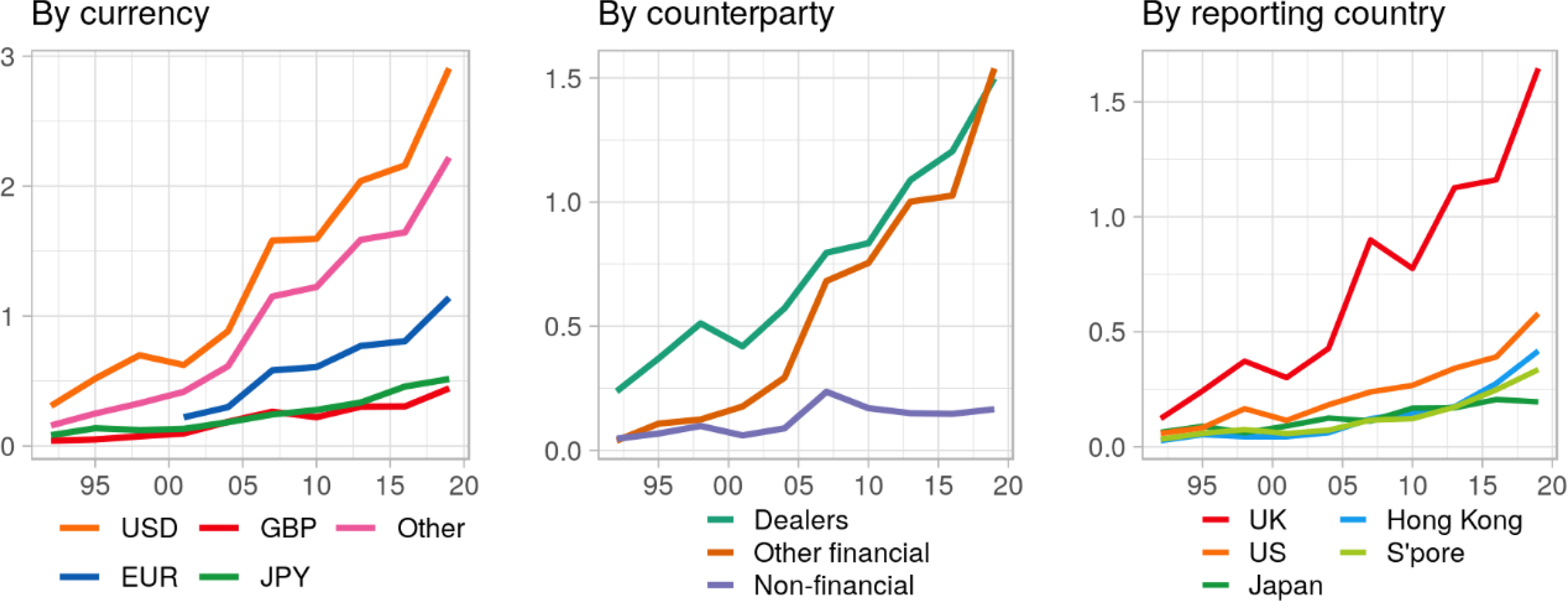

Turnover volumes reported in the BIS triennial survey of reporting dealer banks confirm that the dollar is the most used currency by a substantial margin and recent growth has been driven by inter-dealer and dealer–financial institution swaps (Figure 6). The UK dominates the trading of FX swaps, with a daily turnover in 2019 almost three times that of the US. Hong Kong and Singapore are rapidly growing as FX swap trading centres, while non-UK Europe sees relatively little activity.

FX swaps turnover reported by dealer banks, by currency, counterparty and reporting country, $tn (annual data, 1992–2019).

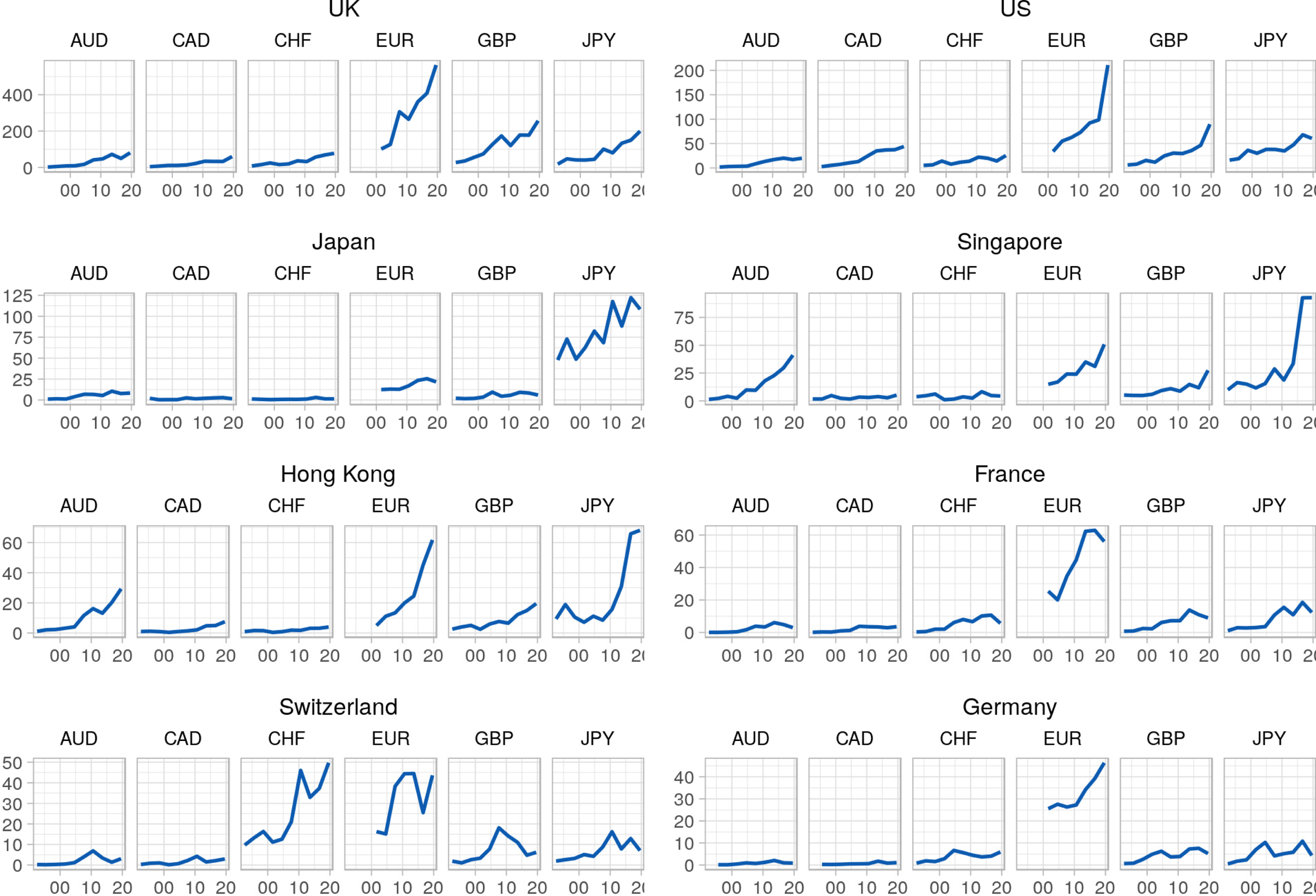

The geographical structure of FX swap trading locations (reporting countries), disaggregated by currency pairs, shows that in the UK and the US, which dominate total trading, the dollar-euro pair is by far the most traded swap, followed by dollar-sterling and dollar-yen (see Figure 7). US–Canadian dollar swaps are also substantially traded in the US. Trading in Japan is predominantly dollar-yen, while the emerging centres in Singapore and particularly Hong Kong see significant volumes of dollar-yen, dollar-sterling and US–Australian dollar trading. Switzerland, France and Germany see much lower volumes than the US and UK and are likewise concentrated in dollar-euro trading alongside Swiss Franc-dollar pairs which are traded in Switzerland.

US dollar FX swaps turnover reported by dealer banks, by currency pair and reporting country, $bn, (annual data, 1992–2019).

Overall, the picture that emerges is complex: the dollar is the dominant currency for both international financial positions and FX swap trading. Japanese banks are the largest cross-border dollar investor, financed via FX swaps. The most traded FX swap pairs are dollar-euro and dollar-yen, the majority of FX swap trading takes place in the UK and dealer banks are increasingly entering into swap agreements with non-dealer counterparties.

To what extent do these trends constitute a risk for financial stability at the global level? And what is the impact of FX swaps on spatial financial and macroeconomic vulnerabilities? Vulnerabilities differ across long-dollar and short-dollar countries. In long-dollar countries, macrofinancial distress can arise from a decline in the availability of dollars. First, such a decline can increase hedging costs, leading financial institutions to use other instruments, such as repos which increase leverage and potential fragility. If the cost of dollar liquidity increases across all instrument types, financial institutions may replace dollar-denominated assets with domestically issued assets, such as corporate and government bonds (Hong et al., 2021), lowering costs for domestic borrowers. Thus, the overall financial implications depend on how financial institutions react to increased hedging costs. Second, and most crucially, if the reduction in the US dollar supply is sudden – making it difficult for banks to find dollars at a reasonable cost – investors might not be able to roll over their FX swap contracts (Borio et al., 2017; González, 2017). 11 In that case, a liquidity crisis can emerge that might require central bank intervention. If the decline in the US dollar supply is accompanied by dollar appreciation, margin calls on FX swaps might induce investors to sell domestic safe assets to meet these calls (Czech et al., 2021), leading to an increase in domestic bond yields.

Since the GFC, the growing excess demand for dollars has increased the potential for shortages in dollar liquidity to generate stress via FX swap positions. On the demand side, institutional investors (life insurance companies and pension funds) as well as global banks have increased their investment in USD-denominated assets. Ageing populations and private pensions and welfare provisions have inflated the balance sheets of these institutions, while USD-denominated assets have provided relatively higher yields during periods in which monetary policy in the US has been less expansionary than in other rich countries. 12 Between 2015 and 2019, the Fed reduced its asset purchases and tightened its monetary policy. The resulting increase in yields increased the demand for dollar-denominated assets from non-US institutional investors and banks (Nakaso, 2017; Schrimpf and Susko, 2019), and thus increased demand for dollar swaps.

However, the post-GFC increase in the demand for hedged dollar positions (as proxied by the dollar funding gap mentioned above) has not been accompanied by an equivalent increase in dollar supply. In the pre-GFC period, increased demand for US dollars could be satisfied by US banks and institutional investors. Post-GFC regulation has, however, restricted the ability of US banks to rely on leverage in order to engage in arbitrage activities and supply dollars (González, 2017; Nakaso, 2017; Du et al., 2018): previously, divergence between money market rates and FX swap rates would induce banks to borrow in the money markets and supply dollars in the FX swap market. Basel III increased capital requirements on derivatives, introduced a capital charge for mark-to-market losses of over-the-counter (OTC) derivatives and raised liquidity requirements. Moreover, the Volcker rule has prohibited US banks from engaging in proprietary trading in FX forwards and swaps (González, 2017; Nakaso, 2017). Although the US Fed added large amounts of dollar liquidity to the US onshore banking system, this more stringent regulation has increased the hoarding of these additional reserve balances by US banks.

Money market investors, such as SWFs of oil-producing countries and reserve managers, have instead taken an increasing role as suppliers of dollars in FX swap markets. 13 These institutions can hold their dollar reserves in safe bonds (US Treasuries or highly rated private bonds), lend them via the private US repo market, or exchange them in the FX swap market, accommodating demand for dollars from investors in dollar-denominated assets. The last option has been increasingly attractive from a ‘returns’ perspective. Consider the example of SWFs supplying Japanese investors with dollars in FX swap markets: supplying dollars against yen allows SWFs to purchase Japanese government bonds during periods in which the combined return of the swap and the Japanese bond exceeds the return on US government securities. Importantly, they can do so without facing currency risk. As a former Deputy Governor of the Bank of Japan puts it, ‘FX-hedged investments in JGSs may be viewed by investors as safe assets substitutable for U.S. government securities’ (Nakaso, 2017, p. 10).

The fact that the demand for dollars has outstripped the supply of dollars is reflected in the cross-currency basis – a measure of the cost of obtaining dollars via FX swaps – which has been consistently negative since 2007 in several countries (see Borio et al., 2016; González, 2017; Avdjiev et al., 2019). 14 Financial institutions in long-dollar countries are, therefore, vulnerable to small changes in the supply of dollars in FX swap markets. This vulnerability is enhanced by the fact that the provision of dollars in FX swap markets is pro-cyclical: during periods of tranquillity, dollar suppliers are willing to surrender dollars and invest in local and non-US government securities, bringing down yields on both non-US government bonds and FX swap premia. However, during periods of financial distress or declining oil prices, money investors and banks are less willing to act as suppliers of US dollars (see Barkbu and Ong, 2010; Iida et al., 2016; Nakaso, 2017), leading to dollar liquidity shortages, as during the onset of the COVID-19 crisis (Avdjiev et al., 2020; Park et al., 2020).

In short-dollar countries, financial institutions fund high-yielding local currency assets by relying on low-interest rate dollar-denominated liabilities, hedging the exchange rate risk of their dollar funding via FX swaps. Macrofinancial distress can thus arise from a potential decline in the local currency supply. Such a decline can increase the cost of hedging, leading financial institutions to stop relying on USD liabilities to finance local currency assets. The implications might differ across rich countries and EMEs. In rich countries (e.g., Australia) financial institutions can replace dollar liabilities with local currency liabilities without experiencing a significant increase in their cost of borrowing. Thus, the provision of local currency credit might not be distorted significantly by developments in FX swap markets. In contrast, in many short-dollar EMEs, the replacement of dollar liabilities with domestic currency liabilities is likely to be more costly. Thus, when local liquidity conditions in the FX swap markets tighten, domestic financial institutions may shrink their balance sheets instead of issuing local currency liabilities, potentially creating a credit crunch.

The Fed as the dollar lender of last resort: swap vs repo lines

Since the GFC, the Federal Reserve has introduced new mechanisms to mitigate the instabilities arising from the increasingly uneven geographical distribution of US-denominated assets and liabilities. When the GFC started, the Federal Reserve reintroduced official swap lines with other central banks. This marked a ‘quantum leap in central bank cooperation’ (Papadia, 2013, p. 5), enabling the Fed to become a dollar lender of last resort (LOLR) and directly manage the cross-border instability of dollar liquidity (Helleiner, 2014; Bordo et al., 2015). Although the management of global dollar liquidity through Fed swap lines has a long history, by the time of the GFC the international financial system had evolved significantly from the institutional architecture of the 1960s when official swap lines were last used extensively. The Fed's role of dollar LOLR thus had to adjust to the collateral-based nature of the global financial system, anchored in the FX swap/repo nexus.

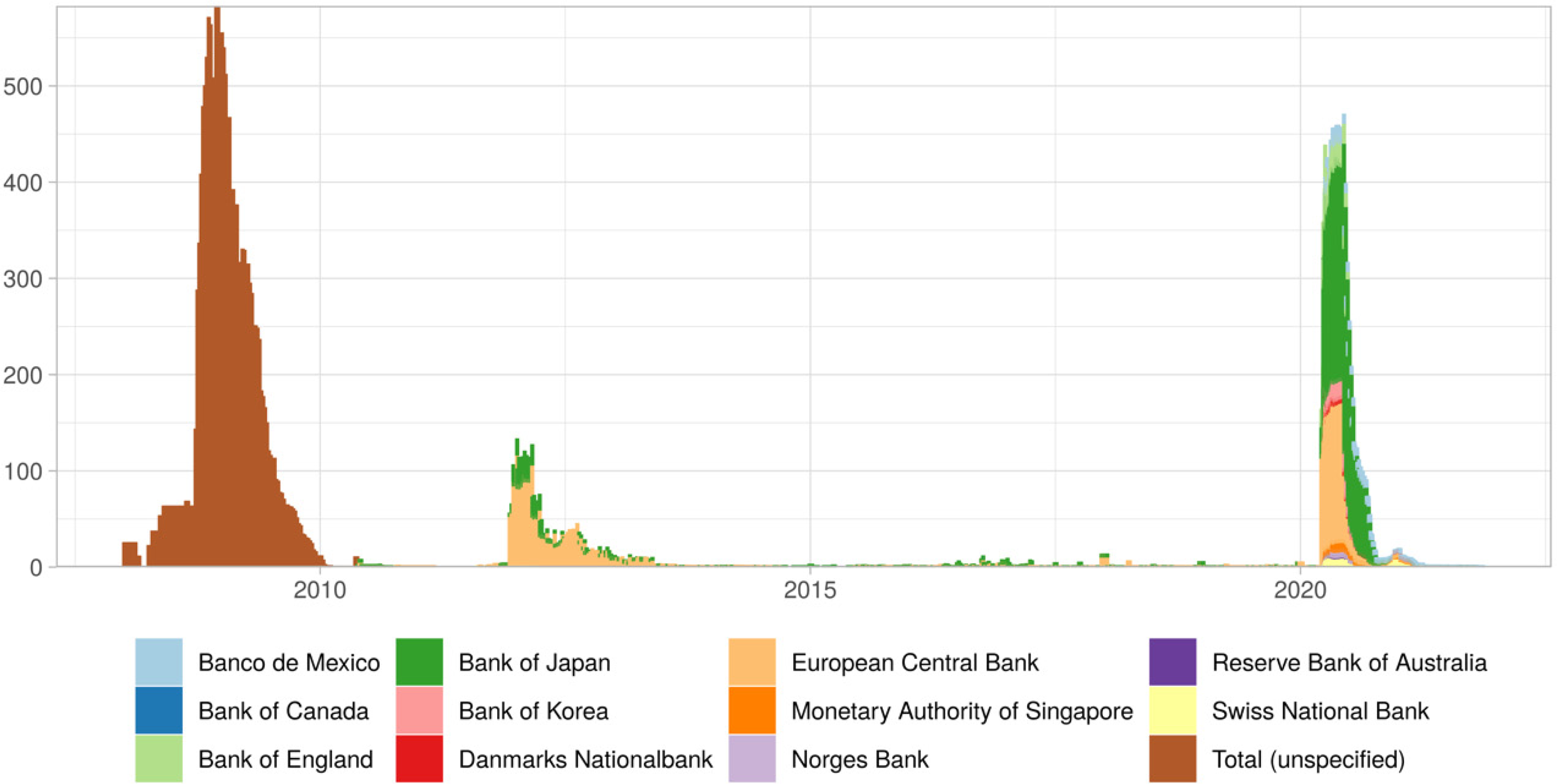

The swap lines that the Fed opened in 2007 provided access to USD liquidity for the central banks of many rich countries (Australia, Canada, Denmark, New Zealand, Norway, Sweden, Singapore, Switzerland, Japan, UK and euro area countries) as well as to the central banks of a small number of EMEs (Brazil, Mexico and South Korea) that supported US-led financial globalisation in global policy circles (Sahasrabuddhe, 2019). The lines were terminated in 2010 but were reactivated in the same year for the Bank of Canada, the Bank of England, the European Central Bank, the Bank of Japan and the Swiss National Bank – and were converted to standing arrangements in 2013. 15 As Figure 8 shows, the usage of FX swaps peaked at about $600 bn during the GFC.

Outstanding amounts of official swaps with the Federal Reserve, $bn 2010–2021.

The outbreak of the pandemic in March 2020 led to the reactivation of the temporary swap lines with nine central banks, through December 2021. The Fed capped swap liquidity provision to USD 60bn for Australia, Brazil, Korea, Mexico, Singapore and Sweden, and to USD 30bn for Denmark, Norway and New Zeeland. 16 The volumes outstanding and length of time in use were both lower than during the GFC (see Figure 7). Notably, the Bank of Japan drew on its permanent swap line with the Fed more extensively than all other central banks combined. Given that Japan is the most significant dollar borrower in the FX swap market (see previous section), its financial system has significant dollar liquidity needs during periods of distress (see also Aldasoro et al., 2020b).

The limited use of the temporary swap lines should be understood in the context of structural changes in currency markets. Currency dynamics no longer primarily reflect trade in goods and services, but capital flows arising from both local entities borrowing in foreign currency, and from non-resident investments in local assets (e.g., portfolio flows into local currency sovereign bond markets). This structural shift increases pressures on central banks to shift from currency interventions that protect exporters to providing insurance against depreciation for investors (Domanski et al., 2016), a derisking logic that accompanies the increasing Americanisation of local financial systems (Gabor, 2020; Musthaq, 2021a, 2021b). The US Federal Reserve reinforces such derisking pressures by explicitly warning that its swap lines should only be used for temporary dollar liquidity relief but not fund mercantilist exchange rate interventions (Choi et al., 2022). Put differently, the Fed is willing to act as a dollar LOLR as long as its emergency dollar liquidity is deployed for market-based management of countries’ exposure to the global dollar financial cycle.

The Foreign and International Monetary Authorities (FIMA) repo facility, announced in March 2020, is another policy innovation designed to preserve the Fed's hegemonic position at the top of the global financial cycle without altering its fundamental dynamics. 17 FIMA account holders, that is central banks and other international monetary authorities with accounts at the Federal Reserve Bank of New York, can borrow up to USD 60bn via repo arrangements with the Fed by using US Treasuries collateral. 18

The structure of Fed repo and swap lines reflects the hierarchical nature of the global dollar system. Central banks with access to Fed swap lines can issue their own currencies in return for dollars and deploy dollars for derisking purposes. Those with access limited to the FIMA repo facility need to hold US Treasuries to access dollars. The FIMA repo facility thus incentivises non-US central banks to borrow against US Treasuries rather than selling them during periods of dollar illiquidity. This ensures a sustained demand for US Treasuries during periods of turmoil: indeed, the Federal Reserve cited the smooth functioning of the US Treasury market as one critical reason for introducing the FIMA facility. 19 Furthermore, in contrast to the longer-term swaps (up to 5 months), the overnight duration of the FIMA loans gives the Federal Reserve daily discretion over renewing the loans, and the terms on which it renews (including the interest rates and collateral eligibility).

The rapid action taken by the Fed during the COVID-19 pandemic does appear to have provided an effective counter to the rush for dollar liquidity. Goldberg and Ravazzolo (2021) show that access to the Fed facilities was associated with a lower cost of obtaining dollars in the FX swap market. Aizenman et al. (2021) show that economies with access to the Fed liquidity facilities stopped selling US Treasuries to raise dollar liquidity at the beginning of the pandemic. They also find that auctions related to the Fed facilities reduced sovereign bond yields and the cross-currency basis. However, vulnerabilities remain. The uneven and hierarchical nature of dollar liquidity provision raises the possibility of gaps where dollars do not flow. This is exemplified by the fact that in countries with FIMA repo facility accounts, stabilisation in FX swap rates after the COVID-19 outbreak took longer than in countries with access to swap lines (Goldberg and Ravazzolo, 2021). But at a deeper level, Fed liquidity provision via swaps and repos treats the symptom, not the disease. Like central banks delivering ever more domestic liquidity through asset purchases to counter the underlying structural imbalances of financial capitalism, Fed liquidity facilities may hold the global dollar crisis at bay – but they do little to address the root causes of recurring crises and vulnerabilities.

Conclusion

Our analysis of the role played by FX swaps highlights the continuing global dominance of the dollar alongside the shifting geographical structure of dollar financing networks. Although we argue that FX swaps do not constitute disguised leverage, we identify several mechanisms by which FX swaps can create financial vulnerabilities for both lenders and borrowers of dollars.

We identify important characteristics that distinguish private from official swap transactions: for private market participants, expansion of dollar swap positions requires prior holdings of non-dollar liquidity, yet repo expansion is not similarly constrained because assets purchased using borrowed funds can be used as collateral for further borrowing. This pattern is reversed in the case of official lending: the money-issuing capacity of central banks means that bilateral swaps between central banks can expand to any level the counterparties choose. In the case of official repo lending, however, prior ownership of dollar treasuries is required to obtain access to dollar liquidity. The Fed's repo/swap dollar lender of last resort mechanism has thus created a tiered system of central banks, which serves to reinforce the hierarchical nature of the dollar-based financial system.

Future research should address unresolved questions about the political economy and geography of FX swaps. What are the implications of swap market developments for the global hierarchy of safe asset provision, and how can EMEs and low-income countries protect their local sovereign bond markets from disruptive shifts in the portfolio decisions of dollar suppliers? Would capital controls provide an effective policy response to the geographies of the FX swap/USD repo market?

An important open question is whether the current status quo, with the Fed as unofficial dollar lender of last resort, is sustainable. At the time of writing, the international dollar stabilisation architecture that emerged since the GFC has yet to be tested during a sustained period of monetary tightening. Can the current institutional arrangement form the basis for a new global institutional architecture, or are deeper structural reforms required to set the system of continued dollar hegemony on sounder foundations? (see Dafermos et al., 2020; Dafermos et al., 2021).

Footnotes

Acknowledgements

The authors thank the editors of the SI ‘Financial Networks And The New Normal' and two anonymous referees for useful comments and suggestions. This paper is part of the project ‘Managing supercycles: globalisation and institutional change’ funded by Rebuilding Macroeconomics, Economic and Social Research Council (Grant reference: ES/R00787X/1).

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Rebuilding Macroeconomics Network.