Abstract

The structure of the UK's private rental sector (PRS) is being disrupted by a new series of rental proptech platforms (RPPs). These start-ups are adopting technologies including artificial intelligence and algorithms which draw upon ever broader datasets to automate and mediate the relationships between tenants and landlords. Only recently have researchers turned to examine new RPPs, which are challenging existing processes within the PRS, through their attempts to digitise all aspects of renting, from a tenant's initial search and application, to end-contract management. This paper seeks to provide two contributions: first, to uncover how platform entrepreneur views of ‘ideal’ tenants shape the algorithms and scripts that run within their start-ups, and how they shift to accommodate the demands of external venture capital funding. Second, it seeks to examine how landlords are falling under the gaze of technological surveillance and automated judgements, as well as tenants, to illustrate how fragmented and uneven data topologies create inequalities through automated ordering and judgements.

Introduction

Recent attempts to increase homeownership rates in the UK have largely failed. Rates peaked in 2003 at 70.9%, before falling to 63.9% in 2018 (Hilber and Schoni, 2021). Subsequent interventions by the government to increase homeownership have arguably had unintended effects: inflating property prices and raising barriers to entry for first-time buyers; while rewarding capital intermediaries and buy-to-sell developers with higher returns. Homeownership rates have been undermined by declining wages and increased job precarity, leading to greater demand for rental accommodation (Wijburg et al., 2018). Coupled with the dismantling of local authority housing provision, as part of broader neoliberal reforms, renting has become dominated by the private rental sector (PRS). The UK's PRS is unique amongst highly financialised real-estate markets in that it is fragmented and comparatively unregulated. Many landlords are individuals or families who own a small number of rental properties (Aalbers et al., 2021; Leyshon and French, 2009), in contrast to the larger institutional landlords often found in Europe and the US (Nethercote, 2019). Charities and academics have long decried inequalities within the sector, which privilege private landlords over tenants, but their voices have been joined more recently by a new series of rental proptech platforms (RPPs) who are claiming to restructure power relations of the market for the benefit of tenants.

Proptech refers to the adoption of digital innovations within the real-estate sector, to create new platforms that automate and mediate markets (Shaw, 2020), where platforms are reliant on large volumes of data that can be linked (Sadowski, 2019, 2020). Rental proptech is a subsector of this market, which focuses on the PRS and aims to cover the full tenant lifecycle (Fields and Rogers, 2021). In seeking to move beyond an essentialist conceptualisation, researchers have turned to view platforms as socio-technical arrangements that combine capitalist practices and structure market encounters (Çalişkan and Callon, 2010). These arrangements create multi-sided markets primarily between renters and landlords, but also other actors such as utility suppliers, insurers and concierge services, for example (Fields and Rogers, 2021), with the aim of making renting a smoother, app-mediated process, where digitisation reduces costs for landlords and data enhances transparency for tenants. On the one hand, RPPs can directly challenge high-street letting agents by providing a lower cost, digital alternative for property listings and tenant management. On the other, they can provide technology to high-street operators that displace back-office work with new automated services, such as tenant referencing. As such, RPPs have become more powerful within the PRS by redefining the position of other actors within its structure.

Initially, RPPs joined a public narrative that criticised private landlords as being amateurish, whose low-quality accommodation is expensive and poorly managed (Brill and Durrant, 2021), to justify the disruption and restructuring of the fragmented PRS. However, RPPs are becoming digital obligatory passage points where entry to ‘the market’ is controlled by platforms, which decide who is permitted to participate, before actors are segmented by scripts and algorithms into multi-sided markets (Fields and Rogers, 2021; Fourcade and Healey, 2017). In contrast to homeownership and the stability afforded by spatial fixity that proptech can facilitate, RPPs benefit from instability and circulation. Moving home generates new transactions, data, fees and rents, with apps designed to facilitate and encourage circulation, whether moving city, trading-up or down, or finding new housemates. It can be argued that to meet the demands of venture capital, RPPs seek to attract more potential tenants by smoothing the process of rental circulation. In other words, the physical circulation of tenants and their data through space is central to the circulation of capital for accumulation. While researchers have emphasised the importance of network effects to scale for platform growth (Langley and Leyshon, 2016; Porter at al. 2019), they have arguably overlooked speed. Accelerating rental circulation can increase capital accumulation for RPP investors, as evidenced by the rise of short-term letting platforms.

Proptech in general remains a new and emerging field of research (Fields and Rogers, 2021; Porter et al., 2019; Sadowski, 2019 2020), with rental proptech being particularly under-researched. This paper seeks to advance the field further by addressing the following research question: are RPPs changing the power relations between landlords and tenants? In doing so, I seek to make two further contributions to the literature: first, while researchers have highlighted the role of venture capital in shaping platforms (Fields and Rogers, 2021; Langley and Leyshon, 2021), the role of entrepreneurs has been overlooked. This is important, as the venture team's formative experiences of renting and their imaginaries of what a disrupted PRS sector may look like, determine how their platforms and algorithms function. I argue that insight is needed prior to the funding stage, to answer urgent questions around who proptech is for and to explore how algorithms are not neutral, but social and political actions (Porter et al., 2019). In doing so, I seek to uncover assumptions and notions of the ‘ideal’ renter that underpin algorithms, which in turn, reproduce judgements and PRS power relations. More broadly, the paper also speaks to ongoing debates in financialisation and the PRS, particularly how these new technologies are reshaping relations within rental markets (Aalbers et al., 2021; Fields, 2022) and how this is driven by short-term venture capital and investment in smaller firms (cf. Pollard et al., 2018). Second, I go beyond a focus on tenant judgements (Eubanks, 2018; Sadowski, 2019), to examine how private landlords are subject to an algorithmic gaze as well, where they can be denied access to the PRS. This is achieved by examining the representations of tenants and landlords through data (Iveson and Maalsen, 2019). In doing so, the paper contributes to wider debates concerning platforms and data (Fields, 2022; Langley and Leyshon, 2016; Sadowski, 2019). Specifically, new insight is provided into the uneven and fragmented data topologies that underpin platforms, which creates inequities in ordering and assessment, and is useful in refining the concept of the data dragnet and addressing the patchiness of the data gaze.

The remainder of this paper is as follows: in the Section ‘The rise of RPPs’, I examine recent literature on proptech and the socio-technical calculations used to develop renter profiles. Section ‘Findings: From an analogue to a digitally mediated PRS?’ will investigate the changing power relations between actors in the PRS: prior to, and following, the emergence of RPPs, while examining how entrepreneurs' experiences of renting shape their platforms and algorithms. This section will also turn to explore how renter and landlord profiles are created from uneven data topologies, ordered through RPP algorithms and how they are disciplined. The final section will conclude the paper.

The rise of RPPs

Finance in the PRS

Studies of real-estate markets have scrutinised how the politics and tools of finance reshape residential markets (Aalbers et al., 2021; French et al., 2011). Until recently, the potential for financialised narratives of the PRS has largely escaped the attention of researchers (Byrne and Norris, 2022), which is surprising given that earlier work by Leyshon and French (2009) on the growth of the buy-to-let (BTL) industry in the UK, and Aalbers et al.'s (2021) later work on the Dutch PRS sector, recognising the renewal of finance-led BTL markets. BTL is driven by small-scale landlords in local housing markets, whereby affluent families seek to accumulate properties to fund asset-based welfare (Hulse et al., 2019). This makes the PRS fragmented, in contrast to the more concentrated institutional landlord markets found in the US and Germany, but does resonate with Christophers' (2020) observation of the re-emergence of rentier capitalism, with a focus on generating rents through controlling asset access, where an absent capitalist retains ownership. As such, the power of financial capital in the UK PRS has often been driven by small-scale investors acting as asset owners and landlords, often funded by BTL mortgages.

Through RPPs, speculative venture capital from the boutique and institutional funds has begun to enter the PRS. This is notable as much less attention has been directed to entrepreneurial businesses and the practices of financialisation (Pollard et al., 2018), where measures, tools and politics for growth strongly shape the operation of start-up businesses. Particularly in the PRS, studies have often examined the role of institutional landlords (Brill and Durrant, 2021; Fields, 2018). However, the recent turn to examine platform capitalism has drawn greater attention to the role of alternative investors, including venture capitalists, who are often behind some of the largest tech platforms listed on the US S&P 500 index (Langley and Leyshon, 2016). Pollard et al. (2018) argue that these investors have the ability to shape start-up behaviour, through contractual power and control. In turn, the aims of these investment funds, seeking speculative high growth, align the behaviour of start-ups such as RPPs to govern tenants and landlords in a way which organises them to enhance returns on capital. As RPPs have begun to attract venture capital funding, they are pushed to modify and ‘pivot’ their business models (Langley and Leyshon, 2021), to ensure that the businesses scale and grow to maximise returns. As will be examined later, venture capital is moving into the PRS in search of rents, captured from tenant and landlord fees, which is seeing the reorganisation of relationships between the sector's actors.

Platforms, rental proptech and calculative practices

Langley and Leyshon (2016) have argued that platform capitalism focuses on the use of rights and the coordination of ideas, knowledge and labour, whereas online markets facilitate collaborative arrangements and intermediation, creating spaces for brokerage (Wood and Phelps, 2018). Research into platforms has grown considerably, focusing on FinTech, crypto, peer-to-peer lending and robo advisors, for example (Hendrikse et al., 2021; Langley and Leyshon, 2016; Sohns and Wojcik, 2020). Platforms seek to replicate particular business models, which seek to extract value from data circulation, data trails, and monopoly rents, with a focus on scalability to meet the aims of venture capital investors. Grabher and van Tuijl (2020) argued that platforms are not neutral, but act as market makers, existing as socio-technical arrangements that create multi-sided markets (Caliskan and Callon, 2010). Platform operators seek to scale for growth through network effects (Grabher and van Tuijl, 2020), while aiming to reduce distance and overcome coordination problems in market exchange and price regime enactment.

Digital marketplaces are able to de- and re-territorialise (Kear 2021), particularly for property markets where locally embedded assets can be introduced to a much wider geographical market of potential renters or investors, helping to liquefy fixed capital (Aalbers, 2019) and affording new technology-facilitated opportunities for data capitalism (West, 2019). Doganoa and Muniesa (2015) argued that platform values are derived from perceived future processes of valorisation and capitalisation, based on the potential for scaling and market growth. Central to scaling and efficacy is the creation of connectivity and the sharing of data through application programming interfaces (APIs) and interconnected systems which provides access to further data and revenue streams. Beer (2018) views this increased interconnectivity as being part of the data gaze, where the melding together of data into new structures enables analytics to become more powerful and performative, where access to greater volumes of data enables lives to be viewed more forensically by technocratic elites. These technologies become more predictive and performative as people's lives are viewed and shaped differently through new modes of ordering and governance infrastructures, which in itself is problematic as these systems are open to error, manipulation and misuse (Greenfield, 2013).

Of particular relevance here, for later in the paper, is the functioning of platforms and their socio-technical devices, such as algorithms which act as obligatory passage points (cf. Hendrikse et al., 2021), where data is used to determine access to markets. Konberger et al. (2017) refer to these socio-technical devices as evaluative infrastructure, while Zuboff (2019) uses the term surveillance capitalism, however, it is Fourcade and Healy (2017) who identify what they term a data dragnet. Under the data dragnet, organisations follow an imperative to harvest as much data on an individual as possible, before automated scoring, ranking and stratification of individuals into groups, where moral judgements and classifications determine their access to particular products and services in a market. Proptech has arguably ‘borrowed’ and extended the moral technologies and calculative practices used in retail financial services where behavioural scoring is mobilised to govern populations, order and segment consumers based on their lifestyles (Knights and Sturdy, 1997; Poon, 2007; Wainwright, 2011). Later in the paper, I mobilise the dragnet concept to show how RPPs seek to classify tenants and landlords, but how the underlying calculative technologies are also performative, in changing and governing user behaviour (Langley and Leyshon, 2016).

More recent research has turned to examine the real-estate sector's adoption of platforms to create short- and long-term rental markets and to automate facilities and portfolio management (Shaw, 2020). Often referred to as ‘proptech’ or ‘real tech’ emerging from industry coined neologisms (Baum, 2017), Sadowski (2019) argues that RPPs are becoming a ubiquitous and dominant feature of rentiership in capitalism. There has been an intensification of digital innovation in residential real-estate over the past decade, embedding technology in everyday life, with the potential to exacerbate inequalities through power dynamics, having moved beyond property listings, to cover the full rental lifecycle (Fields and Rogers, 2021). This extends the reach of such platforms into different areas of tenant life, and in doing so, reshapes the capitalist relations of real-estate (Shaw, 2020), including the volume of real-estate data that can be traded and linked (Sadowski, 2019). This leads Fields and Rogers (2021) to call for more research that moves beyond technological determinism to look at changes to the interrelations within proptech and the wider industry. For example, these may include, associated services, such as flat sharing, bill splitting, digital concierge services, cleaning and facilities management, tenant referencing and data analytics, end of tenancy and deposit management too, covering the rental lifecycle from looking for a rental property, through to completing the tenancy. What is notably absent from the literature, which I shall turn to examine later, is the emergence of platforms that seek to scrutinise landlords, through tenant reviews and landlord data.

Rental proptech has grown since the 2008 Global Financial Crisis (Srnieck, 2017), driven by rentiership and the appropriation of value through control rights (Birch, 2020), where RPPs, in particular, undertake three mechanisms: tenant data extraction, digital enclosure and capital convergence capturing value and controlling property in new ways with the relations mediated through new technology infrastructures (Sadowski, 2019). Porter et al. (2019) have argued that the deepening abstraction and extraction of data has created issues around data privacy, ethics and surveillance, with important questions concerning how data is used and for whose benefit remaining unanswered, yet deserving of urgent research. Eubanks (2018) argues that digital sorting can create social and racial biases with algorithms deliberately or inadvertently targeting particular groups, as part of the process of inclusion and exclusion, leading Porter et al. (2019) to argue that proptech algorithms are not neutral, but rather social and political actions, which require further research. Given that data collection is often a condition of the use of platforms in order to access housing (Porter et al., 2019), and the biological need for housing (Dorling, 2014), it is increasingly difficult to opt-out of platforms and their classification systems. This issue is compounded by the increasingly personalised data available, moving beyond job and education, to previous roommates, social media profiles, credit reports, and feedback from previous landlords to generate data (Fields and Rogers, 2021), which provide an ever more granular profile of tenants.

The nascent field of rental proptech research has begun to grow. For example, cross-border investments by high-net-worth individual Chinese investors in US housing markets, using criteria on rents, yields, valuation and bid optimisation tools (Dal Maso et al., 2019), while Fields (2022) reveals how new rental proptech was instrumental in enabling private equity to create a new asset class, by enabling automation of many core functions from geographically dispersed portfolios, including rent collection, maintenance and property acquisition. Property firms are increasingly identifying as data businesses, using algorithms to process neighbourhood desirability, proximity to employment, transport and amenities, to calculate potential investor yields, while benefitting from the ability to displace previously paid labour such as with property viewings and maintenance, while seeking to optimise the work of contractors (Fields, 2022).

Studies of platforms and proptech have frequently drawn upon the socio-technical perspective from Science and Technology Studies (STS), previously used to examine the social construction of markets (Callon et al., 2007) and how they consist of socio-technological arrangements of materials, technical devices, texts, algorithms, rules and (non)humans (Caliskan and Callon, 2010). Markets are not abstract, but are real, and messy (Mackenzie, 2009), where data does more than simply mirror the world, but where the resulting knowledge changes the real-estate market (Shaw, 2020). Platform-mediated markets and property technology consist of performative devices that intervene in the social construction of new markets (Shaw, 2020; Kear, 2021), in either disrupting incumbent markets or creating new ones. Despite functioning technology applications being viewed as socio-technical achievements in assembling various elements (Fields, 2018), behind the marketing slogans, technology does not work perfectly. Devices are contested and under continuous management (Birch, 2020), leading Shaw (2020) to argue that this instability has not yet received sufficient attention, especially as business models pivot to extract rents from new markets, as a start-up grows or is acquired.

Shaw further notes that many proptech studies remain technologically essentialist and that digital real-estate technology could be better viewed through an analytical lens that views it as a platform which connects users (Srnicek, 2017) and creates new aggregations to develop value (Bratton, 2015). In seeking to move beyond essentialist conceptions of proptech, Shaw (2020) posits four main types of proptech clusters: finance and capital investment, residential markets, commercial markets and the management of buildings as material assets. Proptech platforms are a site of data collection, flows, circulation and accumulation through datafication, but this raises questions over how the data is collected and used, as beneath the abstract algorithms are structural imbalances, where not all market participants will be able to negotiate the power shift, as platforms centralise activities that were previously undertaken in distributed, local letting markets (Shaw, 2020). This will be particularly problematic as calculative frames and measurements strip tenants of their narratives (cf. Espeland, 1997), but are in themselves opaque systems making them difficult to unpack the power relations, something I seek to do later in the paper.

In being stripped of their narratives, tenants become represented by data captured from the dragnet (Fourcade and Healey, 2017), where platforms are beginning to draw-in data from a variety of sources through APIs (Langley and Leyshon, 2016) to create data representations used assess tenants and landlords. Iveson and Maalsen (2019) refer to this as the development of ‘datafied dividuals’, where fragments of data from various sources are assembled to create a partial representation or profile of an individual, which I argue is increasingly the case for tenants and landlords. This is problematic and creates uneven power dynamics as platforms make decisions on incomplete tenant subjectivities, but also due to opacity on what data is available through APIs, tenants are unable to provide selective disclosure. Kear (2021) highlights how platforms also do more than bring together heterogeneous elements. They create the conditions for the performance of model markets, using an app and interface design to nudge actors into alignment with particular market models, arguably in an attempt to create homo-economicus or the ‘ideal’ tenant who is frequently mobile and performs a lifestyle that enables maximisation of rent extraction.

Research design

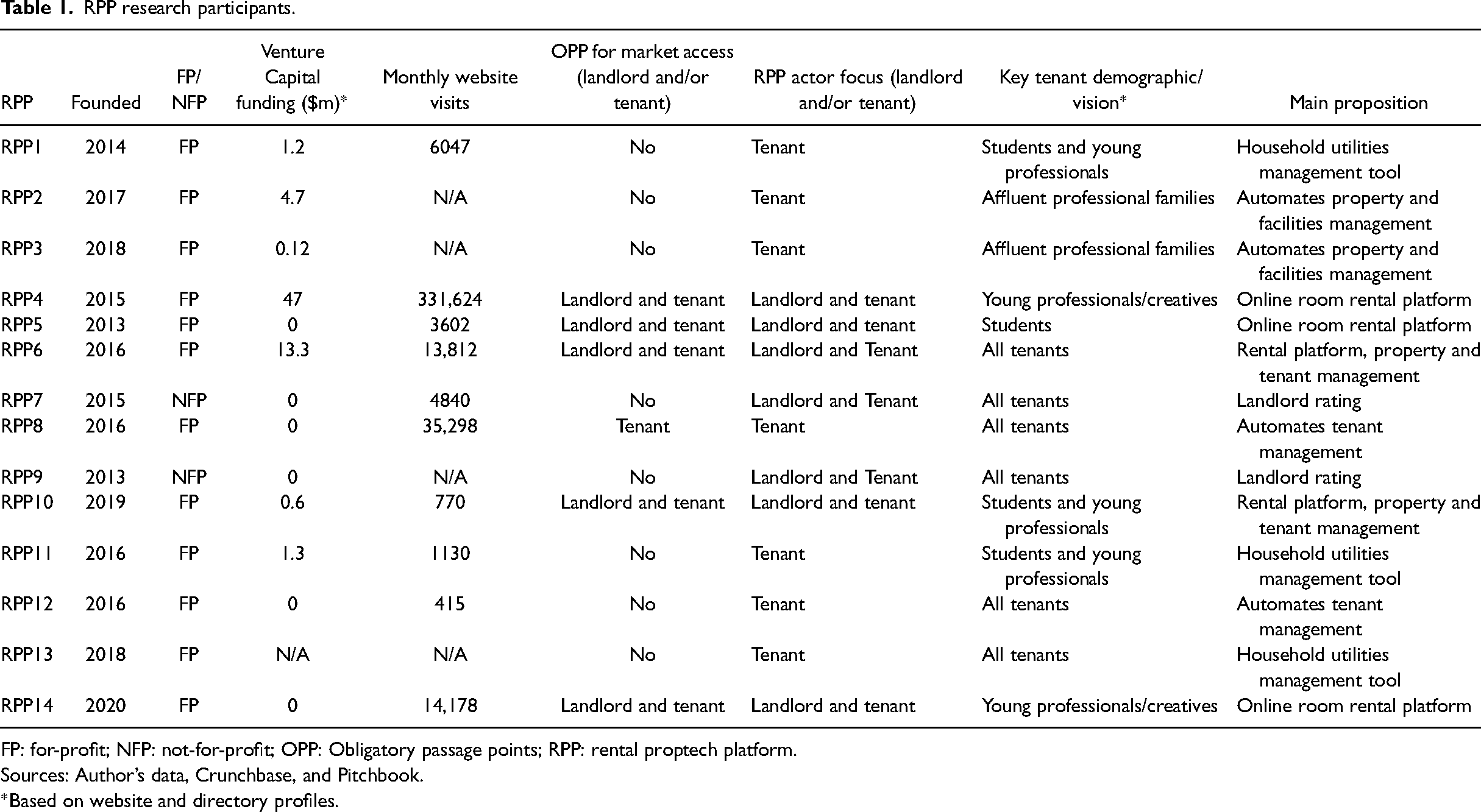

The platforms were identified through searching online proptech directories such as Unissu, in addition to scanning the participants of accelerators and incubators and through following specific threads and tags on LinkedIn and Twitter to identify RPPs. In total, 28 semi-structured interviews were undertaken in the UK, between 2019 and 2021 with a range of actors within the rental proptech ecosystem. These included industry representatives of proptech and landlords, institutional investors, venture capital and incubators. The participants were directors or analysts within these businesses. For the RPPs, I interviewed a diverse range of entrepreneurs which included rental listing firms, bill sharing apps, tenancy management, digital concierge, flat sharing and landlord review sites – see Table 1 for an overview. Some of these functions overlapped, depending on the business model and products offered. The participants were either founding entrepreneurs or members of the venture teams.

RPP research participants.

FP: for-profit; NFP: not-for-profit; OPP: Obligatory passage points; RPP: rental proptech platform.

Sources: Author’s data, Crunchbase, and Pitchbook.

*Based on website and directory profiles.

The websites of these businesses and associated reports were examined to determine their main products and business models. To complement this, I undertook further reviews of industry reports of the rental proptech sector to develop an understanding of the main UK participants. These resources also provided an additional check on some of the claims made by the interview participants. While most of their products seemed to work broadly as described, a caveat here, is that some interviewees may have overstated the performance and accuracy of their technologies, to highlight the ‘novelty’ as often pitched to investors, or the technical devices underpinning the platforms may in some cases not perform as well as designed, or even be fully understood, in the context of machine learning.

The interviews were semi-structured to enable the participants to discuss issues not raised by the researcher. The themes examined focused on the platform business models, digital devices, data generation and sharing, algorithms, data ethics and tenant impact. The interviews lasted between 45 minutes and 2 hours and each conversation was recorded prior to transcription. Transcripts were later thematically coded, to capture similarities and differences across the themes and different types of RPPs.

Findings: From an analogue to a digitally mediated PRS?

In contrast to the US and Europe, where some cities benefit from rent controls, the UK PRS is lightly regulated. Historically, the sector is loosely coordinated and represented by industry bodies, serving landlords, or other supporting actors, such as local letting agents. However, power relations are asymmetrical, benefitting the landlord. Short-term rental contracts promote instability and enable landlords to regularly re-market properties, often with an increase in rent. Tenants who are unable to afford these increases, due to static/declining wages or precarious work, must find new accommodation, which can be problematic in local areas with constrained supply. Requests for improvement work or complaints can result in ‘revenge’ evictions by landlords, making tenants hesitant to assert their rights. Local government underfunding makes it difficult to detect and enforce regulatory violations.

RPPs are beginning to change the relationship between landlords and tenants by taking over as mediators of these relationships (cf. Wood and Phelps, 2018), claiming transparency, ‘objectivity’ and efficiency. As will be demonstrated later, the power relations have not become symmetrical under this relationship, but rather platforms have positioned themselves with power over both landlords and tenants – see Table 1 for the RPPs studied. 1 While RPPs use new data and technologies to assess and order tenants, they are increasingly seeking to order and rank landlords. RPPs are spatially different to locally embedded letting agents as they seek to de-territorialise (Kear, 2021) and operate on a national, or multi-city scale. To protect their brand reputation, some directly rate the quality of landlords, or even assist in their prosecution, using data collected on their platforms (RPP7 & 9).

The sector has its antecedents in early property portals, which interviewees did not recognise as ‘true’ proptech. Sites such as Rightmove launched in 2000, and Zoopla in 2008, operated as simple online property listings with limited integration, prohibiting co-innovation with other platforms. Instead, RPPs are characterised by their use of new types of shared and open data, and novel tools such as artificial intelligence (AI), algorithms and apps. The emergence of the RPP sector did not follow a smooth trajectory, but rather responded to a series of events and triggers for growth, arguably culminating in three phases. Srnieck (2017) observed a first, post-2008 phase that can be characterised by its entrepreneurial disruption, which at first glance broadly follows a narrative of technological essentialism (Shaw, 2020), where tech entrepreneurs sought to change the market to provide a better experience for renters, by challenging some of the power imbalances within the market. For example, biases of individual landlords and letting agents against tenants are replaced with ‘objective’ data and scripts, which entrepreneurs thought could remove discrimination and seek to empower tenants. 2

As shown in Table 1, this was a long phase, with this project's interviewee platforms not becoming established until the mid-2010s. The second phase of regulatory disruption began in 2019 when the government introduced a ban on tenant application fees, which cut income for incumbent letting agents. For some, this led to substantial revenue shortfalls, leading them to unbundle their services and outsource parts of their rental operations to RPPs to cut costs, as summarised below: Proptech exploded after the announcement of the Tenant Fees ban. [Letting agents] just couldn't make ends meet, so they were culling the expensive work…cutting out staff time…the cost of the referencing…now, you couple a massive loss of income and the Tenant Fees ban together with what we have seen with Coronavirus, they are desperately looking at cutting costs at the moment. And if you’ve got a good proptech business, it's winning out. (Representative group 2)

The regulation had an unintended and positive effect on RPPs, who were not planned beneficiaries of the new law. The government had been interested in supporting proptech to make it cheaper and easier to buy property, by reducing transaction costs and numbers of failed sales in an attempt to increase property ownership. While seeking to reduce costs for tenants through the fees ban to support renters, the effect was to disrupt many letting agents’ business models, leading to the acceleration of the adoption of RPP in the sector. Rather than view market incumbents as actors to be solely disrupted, RPPs began to view them as potential clients. For example, an online agent with automated tenant management, identity authentication and referencing systems, could sell the service to local high-street letting agents. As such, RPPs began to not only directly challenge incumbent non-digital firms, they began to work with high-street agents, diffusing the new technology more widely within the PRS.

Evidence of a third phase has begun to emerge, signalling consolidation within the sector, and attracting additional venture capital to fund acquisitions and expansion (Langley and Leyshon, 2016; Pollard et al., 2018). This is illustrated by Goodlord, 3 which acquired Vouch in 2020, a tenant referencing platform and Acasa in 2021, a utility management platform, in an attempt to cover more parts of the tenant's lifecycle’ bringing convenience for its letting agent clients, while diversifying the platform.

The ‘ideal’ renter: Holding a mirror?

As start-ups, RPPs concentrate on smaller segments of a market to focus their limited resources. When platform entrepreneurs discussed their target market of renters, they were consistent in the profiles that they provided. For example, they often described renters who would use their platform as being young, urban, internationally mobile, professionals who moved cities frequently, and who were also affluent, as highlighted in the following quote: I think it makes sense to look at those cities which are quite dynamic in terms of people, especially young professionals moving to this place for their job…so they come for an internship, and they would come half a year later for a permanent role at JP Morgan, for example. (RPP14)

These descriptions were consistent with those of a creative class of entrepreneurs, often found in entrepreneurial ecosystems (Sohns and Wojick, 2020). Based on the participants’ background narratives on both their careers and those of their co-workers, their ‘ideal’ profile descriptions reflected the venture teams themselves, where the RPP interviewees were mostly aged between their mid-20s to late 30s. These views are also gendered, as 12 out of 14 of the RPP interviewees were men, with experience working in ‘big tech’, or start-ups. As will be examined in the next section, the platforms were designed to solve problems from their rental experiences in the PRS. The platforms have then co-evolved around the broader perceived needs of renters, through the lens of the platform venture teams. This is a unique finding as recent research on platform capitalism has often highlighted how venture capital shapes start-ups (Langley and Leyshon, 2016), which while important, obscures the agency of entrepreneurs.

This also reveals an interesting contradiction. On the one hand, the market of ideal renters sought by the platform entrepreneurs is in a particular niche, for example, in flat sharing, or short-term lets. On the other hand, venture capital funders pressure RPPs to widen their market to broader groups of renters, to expand the number of tenants using their platform and enable rapid scaling-up and greater investment returns. Despite this pressure from venture capital, the interview probes revealed limited insight into platform research commissioned on broader or alternative groups of renters. As such, the diversity of renters, such as those who are not urban, with limited geographical mobility, lower incomes and perhaps family caring responsibilities, were absent from the narratives. While this does not particularly preclude the use of the platforms by renters outside of the creative class, nonetheless, it does raise questions over how the needs of other renters are met. This is particularly problematic, when platforms are beginning to act as controlled entry points to the PRS. Design assumptions that feed into algorithms may not be inclusive for all renters, and as will be seen shortly, the patchwork of available data can also be problematic.

RPP entrepreneur narratives often focused on the development of the business as being connected to personal, negative experiences of the rental market and a desire to fix it for other renters, as part of a collective identity. For example, being a victim of fraud by a rogue landlord, poor property management by landlords, or ineffective and expensive letting agents, appeared in the interviews. Despite the altruistic aims of disrupting the market to improve the renter experience, and as highlighted in the following quote, as platforms grow, their design and development evolve, so despite initially seeking to solve a common problem for renters, as experienced by the venture teams themselves, these platforms and their aims can change over time as they move from solving the problem to growing the business: I think a lot of companies will start out with absolutely the right intention of understanding a problem, very often because they’ve gone through it themselves personally. And trying to use technology to solve that problem…I think sometimes you can lose the context of the real world and what's happening… I think property companies and technology companies focus very heavily on what is legal and what is technologically possible. And I think whilst ethics overlaps both of those, it isn't the same thing. (Industry consultant)

Platforms would often turn to venture capital funds to support their growth and to raise funds. Following Pollard et al. (2018), even though the platforms are not publicly traded, financialised pressures and support from these groups would often see recommendations or requirements made to change the business model of a platform, to enhance their scale and future profitability (cf. Doganoa and Muniesa, 2015). For example, RPP4, was advised to ‘loosen’ its flat share matching service, to grow its market by placing more tenants in accommodation. As highlighted by one entrepreneur, the privileged background of venture capital managers meant they failed to understand the rental sector, which could distance the platforms further from the diverse needs of renters: VCs don't have a clue about the realities of renting a property, and it would be completely beyond their comprehension that you might not be doing it as a lifestyle choice, that you have to rent because you’re not able to buy. (RPP9)

Fourcade and Healey’s (2017) information dragnet concept can be refined in the context of the UK's RPP sector, as the net apertures are of different sizes and consist of multiple nets – user data is not evenly and consistently captured or used. For RPPs, data landscapes are geographically uneven, with profiles created from a fragile patchwork of inconsistent data sources collected at different scales and by various institutions. To critically consider the data gaze concept amongst RPPs, the gaze is patchy and discontinuous. A multiplicity of datasets are used by different RPPs, each using the data for varying purposes and calculations, underpinned by diverse assumptions, meaning a prospective renter could be assessed quite differently from platform to platform. Of particular interest was the variation between which types of data are used by platforms, and the granularity and sensitivity of the data, as will be seen in the next section.

Data topologies and renter profiles

The data sources used to build individual renter profiles and to feed algorithms are diverse, but could be spatially patchy, raising issues over equity between renters. Data collected across the platforms could include information on age, previous addresses, time in occupation and employer, income, outgoings, dependants, and credit score, as commonly used in tenancy applications at high-street letting agents. However, RPPs were able to draw on a variety of previously untapped data, for example, local authority databases, including data on previous neighbour complaints as well as official judgements. The interviews revealed spatial disparities and digital inequities whereby some local authorities provide access to more detailed data, while others do not, making data visible for renters in some spaces, but not others: Some are even able to log directly into local authority systems as well that can check council tax records and antisocial behaviour complaints, and things like that…not just the county court judgements, but the bits that don't get to the county court judgements …it's all about the integration…it's sensitive personal data. (Representative group 2)

Another recent addition is the use of the open banking API, which enables a platform to access and analyse bank account data, as part of the rental application process. Open banking data is the information source closest to a dragnet as it captures transaction level data from everyone with a bank account, providing a wide data gaze over renters. As the API was funded by the UK's largest retail banks, they effectively subsidised RPP start-up development costs by providing access to substantial volumes of data, enabling rapid scaling through API integration. While it is possible for a tenant to deny an RPP permission to access this data, renters have to increasingly give opt-in consent to gain access to the PRS market mediated by the platforms (cf. Hendrikse et al., 2021).

4

The data gaze extends far beyond credit referencing information used in the behavioural scoring of retail financial services on payment records and includes richer data on amounts of money spent, locations, times and type of retailer, data which could be sensitive and as highlighted below, is much more granular than is needed to decide on rental affordability, and could be used to make moral judgements on a tenant's profile: I mean, you couldn't see what you’re buying at Tesco's [supermarket], but you could see an off-licence, and you could see betting companies, or you could see porn…you could see all this. And we did have one agent once…a relatively big name. And they were wanting to actually, can we do some of this? And we were pretty much like a flat no, we would never do that. So maybe they’re working with someone else now… (RPP4)

The platforms interviewed had decided on ethical grounds to guard sensitive data from landlords, but as highlighted above, the data could be provided by other RPPs. This could also extend to religious or political donations. However, for tenants who are reliant on unbanked cash transactions, ‘absent’ data through open banking could be problematic, reducing access to properties in the market. While APIs from global social media platforms such as Facebook and Google are often cited as potential data sources in the literature, they were not used as frequently as perhaps would be expected under a data dragnet backdrop (Fourcade and Healey, 2017). The data was seen as unreliable and outdated, with better sources available for verification available through open banking, or from potential tenants themselves, where bespoke data can be captured at no cost. As such, global databases were not seen as useful, highlighting further the patchy data landscapes. Instead, substantial volumes of data gleaned were digitally self-submitted by renters themselves, to negotiate the obligatory passage points, but without knowing how exactly the data will be used. Interviewees recounted how well-designed interfaces could encourage renters to share much more data than they would on a paper form, which could later be tracked and also shared, raising questions over data sharing protocols: …the vast majority of data we had was input by customers…So in terms of raw consumer spending we have an absolute shitload of data. Which is really valuable, really interesting to draw a lot of insights for us. When it comes to other forms of data sharing, we share data with all of our partners. (RPP1)

Resonating with Fields (2018), submitting data on facilities maintenance and other updates to profiles can create substantial volumes of data. Arguably, much of the data held on tenants previously existed, whether more rudimentary details such as names and telephone numbers. The new power behind data and RPPs is garnered through being able to share and connect other data sources to leverage its value by providing increasingly powerful tools, that attract more fee-paying letting agents or landlords, or through selling that data to other organisations. More granular and invasive data, and its varying availability, create inequalities in how tenants are assessed, based on if the data is available or not, which a tenant may not have control over. This contrasts with credit agency data which often provides more homogeneous coverage of UK consumers, where lenders will access very similar data from across the main three agencies (Wainwright, 2011).

Algorithms and sorting renter profiles

The interviewees revealed two main mechanisms at work when using data to sort potential tenants: binary sorting and ranking. Binary sorting included more basic affordability checks, which would seek to verify an applicant's identity, income and regular outgoings to establish if they could afford the monthly rent payments. Renters either meet the criteria, or they do not. The ranking and matching of applicants would often use more complex algorithms and AI, which could draw on a wider set of data. This could range from data on hobbies and other personal attributes for flat sharing sites, for example, or to act as a broader filter. In constrained local PRS markets with high demand, algorithms can use the data to filter and rank applicants for a landlord, to manage demand as part of the platform's service: …they don't have to go to a classifieds website where maybe they get 100 applications per room and they have to sift through and say, okay, this one's not good, this one's not good… the demand that gets funnelled is very targeted to what they want, so for them it's good…They know that maybe they get ten applications and maybe five of them are qualified and can work, while with [listing site] they’ll get 100 and they have to go through 95 to get the five. (RPP8)

While the algorithms will sort the applicants, the ultimate application decision is often left to landlords of small portfolios who seek personal involvement, but for larger landlords, this can also be automated. The overlapping topologies of data could potentially assist some tenants in rising-up the rankings or could have a negative impact, although, in contrast to ‘traditional’ sources of information used by some letting agents and landlords, the fixed scripts underpinning the algorithms can be more ‘objective’ and exclude some prejudices. However, structured biases within algorithms have the potential to discriminate against some tenants, for example, those with incomes that fluctuate on zero-hour contracts, or those who operate predominantly in the cash economy.

An interesting finding here concerns the impact of AI and algorithms, and how personal data is used to develop these sorting devices. Entrepreneurs would often note how an individual would have their data anonymised and could have it removed from the system under The General Data Protection Regulation (GDPR), but that the AI and algorithms would continue to function and apply sorting criteria based on their previous learning, which as highlighted earlier, may be based on incomplete data topologies. As the following quotes highlight, this creates a digital stereotype against which applicants can be judged, but it may not be clear to them individually why they were rejected, or deprioritised in an application, which could be clearer under a manual process with a local letting agent. Of particular interest is how once data is removed, even if flawed, the model will not necessarily unlearn or adapt from that removal: …everyone I spoke to, and also the lawyers, is that the way we do it is all the data is anonymised anyway for the machine learning model. So, we take the data and what we then do is it then builds up models…and this is how it learns over time. So, that stuff is all on the system, if you ask to say, I want to take all my data off, we can remove all the conversations, everything that you’ve ever done on the platform, but what you’ve taught the model doesn't change. It's like a human being, you can't remove what the learning is from that situation, but you can tell them never, ever to share that conversation again. (RPP2)

It is notable how few RPP websites had clear information on how long data would be retained, why particular data was required, and how it would ultimately be used. For example, self-entered data may be provided, but it may not be clear how it could be linked to other data sets, to create a leveraged tenant profile, and how data may have a positive or negative effect on an application. While an RPP may make a decision based on incomplete disclosure through a partial datafied dividual (Iveson and Maalsen, 2019), the applicant cannot provide additional data where it is missing from platform sources to provide a more favourable rating, nor do they have the power to offer incomplete disclosure and to ‘hide’ data that may portray them negatively.

The values underpinning algorithms are determined by internal discussions within RPPs. In contrast to the decision-making tools developed by banks for mortgage lending, they do not have experienced and extensive credit committees or substantial datasets which cover varying parts of economic cycles. Some entrepreneurs noted that currently, their datasets while useful for developing preliminary correlations are not yet large enough to be fully robust, highlighting device instability. As such, algorithms are encoded with subjective values, some derived from an entrepreneur's personal experience, which meant that different platform algorithms could potentially be underpinned by different assumptions, highlighting the instability of these assemblages. For example, one entrepreneur observed how they would be more likely to penalise a high-earner who spends most of their salary quickly, while favouring a lower-earner who moves a proportion of their money to savings, following open banking data. In the following case, the platform venture team did not particularly see all county court judgements as problematic, so their algorithms were designed to recognise that renters may occasionally struggle financially, although other platforms could flip this favourability around: …we built an algorithm around our tenants…that's why I’m saying is that a job, is it for us, and employment trumps a credit score…if it's CCJs, bankruptcy, I think that is a red flag. But even CCJs. How much was it for? Did they pay it off immediately? There's a big difference between £100 and £10,000. And how many? Is there a repeated pattern? (RPP6)

Providing an applicant had a particular type of job and income, it may not impact their ability to rent, to a degree. However, it may make a tenant less likely to be shortlisted for a particular property in areas of high demand and accommodation shortages. This raises two interesting points in contrast to mortgage credit scoring. First, credit scoring algorithms often use three credit referencing agencies in the UK, which provides more equity in the sense there is more consistency across the data used in decision-making, and a more comprehensive data gaze, whereas this is patchier using the spatially variegated systems in RPP, where each platform may use different data. Second, rather than specialist credit committees making decisions which conform to a series of tacit standards within the sector, adding arguably more consistency, small RPP teams, tend to use their own ideas, introducing more variation in how the data is used in their algorithms. While Burrell and Fourcade (2021) have observed the rise of a new occupational class which they call the coding elite, with power exercised through their technical control of decision-making systems, these elites act as a cohesive profession in credit and finance. However, it appears that in rental proptech, these elites are self-appointed and make moral judgements, based on their understandings and visualisations of how they believe the PRS and its actors should function.

Data topologies and the making of landlord profiles

As highlighted earlier, platforms can cover multiple sides of a market (Langley and Leyshon, 2016) and while RPPs order and sort tenants, some would also undertake rankings of landlords. Two particular platforms rated landlords as their main activity, as the entrepreneurs wanted to bring transparency and disciplinary mechanisms to the PRS (Table 1), and had created products around this, selling data on ‘rogue’ landlords. Multi-sided platforms that sort landlords were ‘for-profit’ and platforms that focused on landlord transparency were ‘not-for-profit’ entities. In contrast to renters, the data used to develop landlord profiles on both types of platforms was much less comprehensive, invasive and personal. For example, data from social media was not used, and open banking data was used sparingly which led to the development of, comparatively speaking, much more partial profiles (Iveson and Maalsen, 2019), used predominantly to screen out ‘fake’ landlords.

As such, there were only two main types of data generated to create landlord profiles. The first was self-reported landlord data, where basic information could be checked through open banking, such as address and account details, or property ownership data through APIs from the Land Registry and other commercial directories. Although this information can be digitally and automatically verified through the platforms, it does not necessarily provide access to ‘new’ types of linked data, as seen in the development of renter profiles. For example, paper copies of bank statements could be used to verify this data, rather than new forms of digital surveillance (Zuboff, 2019): So, we did this landlord checking product. Landlords can create a profile, and they could share it, and you could validate information like bank details, mobile number, property address, ownership, all for free… (RPP4)

In addition to the data being less granular, property ownership structures can make this process more opaque. For example, landlords can purchase property through a legal vehicle for tax advantages, rather than as an individual, making it more difficult to identify the actual owner, and developing further information asymmetries between landlord and tenant. The second type of data relied on by platforms was renter-generated data, which was obtained in two main ways. First, through tenants leaving reviews of landlords and/or their property, with quantitative scores, qualitative feedback and photographic evidence. This mode of data collection only works well in areas with a high turnover of renters, for example, in student-dominated neighbourhoods, or cities with high-numbers of short-term lets. More advanced business models have sought to use the data to create new products by collecting data that identify breaches of safety standards, or to detect properties that should be licensed, but are not, and to directly reveal properties potentially violating building standards to local authority enforcement teams for targeted inspections, keeping the service free for tenants: …the local authority can understand what's going on with landlords, what's going on with the properties, what's people's actual feedback of living in a particular area. We can help them find landlords who aren't licenced, but should be. Because the reviews have the landlord's name, and that's super valuable to them, because they can take them to court. (RPP7)

While RPP apps exist which assist landlords in ensuring that they comply with regulations in their local area, and arrange safety inspections and servicing, not-for-profit landlord review platforms seek to actively use the data to support landlord prosecutions or help tenants in making formal complaints, based on guided complaint forms through apps to collect the required evidence. This approach takes the position that legislation is ineffective and that tenant reviews and support in legal claims will have a more direct effect on changing landlord behaviour.

Algorithms and sorting landlord profiles

As with renter profiles, the mechanisms of landlord sorting could also be separated into binary and ranking functions. First, binary verification of landlord identity and property ownership was used to remove fraudulent listings. Primarily, this was to protect renters, but entrepreneurs were aware that as part of a multi-sided, for-profit RPP, they needed to develop a favourable reputation that is proactive in dismissing ‘rogue’ landlords from the platform, to attract more potential renters, to enable it to scale and grow to meet venture capital demands. Second, for-profit and not-for-profit RPPs operated ranking functions of properties and landlords to assist renters. Not-for-profit RPPs were limited as they would use what was referred to as the ‘Trip Advisor’ model, based on the hotel review site, which is not easily scalable.

5

However, these reviews were seen as effective by some potential tenants in signalling poor quality accommodation and applying pressure for change on some landlords: I had one landlady contact me. The reviews that had been left about her were so absolutely appalling that I just thought, well, you’re going to have to show me that this is wrong…I’ve been contacted by people saying that I’m stopping them from making a living, and I said, make your place better then…I’ve had feedback on social media from people saying, I was going to rent this place, and I saw a dodgy review, and I’m so glad I didn't. (RPP9)

In contrast, for-profit platforms which mediated multi-sided markets between tenants and landlords that were backed by venture capital, their need to grow and scale up are reliant on attracting potential renters, which required presenting landlords perceived to be of a higher quality. A poor reputation would fail to attract enough tenants, so some algorithms were developed to sort landlords, based on a series of graded criteria, which assessed the accommodation and accuracy through verification and the ongoing conduct of landlords using AI, which could see some landlords and their properties de-listed from the platform: On the [landlord] side what we’re doing, which is very cool, is actually algorithmic sorting…certain things or actions you will go to the top of the list…so, if you’re a landlord with one room, if you’ve booked that room three times over the space of one year, for example, you would be pumped up to the top, or if you’ve entered your bank account details and they’ve been verified…[On sexual harassment by landlords] we had to adapt the way we found these things and tackle them very quickly… we check on key words such as that if chats get reported or we find explicit word usage on our chats we can find it very quickly and send warnings or ban people very quickly. (RPP6)

This was arguably more effective, especially for multi-sided short-let RPPs, as they were able to collect data that was not just renter generated, but also benefitted from more renters, enabling them to draw upon additional data for landlord rating algorithms. In this context, they act as a disciplinary mechanism, encouraging landlords to be more transparent and to discourage poor behaviour, with a direct sanction of having their ranking reduced to tenants, making them less visible in the PRS. However, this can potentially create a subprime market for renters. Profiles that are closer to the ‘ideal’ tenant stereotype are ranked more highly, so they have more choice to select higher-rated landlords. Tenants who are ranked lower by algorithms may find they are limited to landlords and properties with lower scores, and will likely find themselves with fewer choices. While the algorithms can be seen as relational achievements, they can be spatially inconsistent, based on which data sources they are able to obtain and what omissions exist. As such, two similar tenants may be represented by quite different datafied profiles on alternative RPPs. Moreover, de-ranking poorer quality landlords rather than removing them completely enable RPPs to make rents from them, and in constrained rental markets, high demand from tenants, make a low ranking potentially an ineffective mechanism for landlord change.

Conclusion

Research has highlighted how homeownership rates have been undermined by decreasing wages, increasing house prices and job precarity, leading to a rise in demand for rental accommodation (Wijburg et al., 2018). Following the privatisation of housing stock, the UK has seen substantial growth in a fragmented PRS, where landlords are often individuals or families owning a smaller number of properties (Leyshon and French, 2009). Historically, the power balance has favoured landlords rather than tenants, but this is beginning to shift with the rise of RPPs (Fields and Rogers, 2021; Porter et al., 2019).

At the beginning of the paper, I posed the question: are RPPs changing the power relations between landlords and tenants? In short, RPPs are changing power relations within the PRS. RPPs are beginning to provide more transparency over landlord quality, but they comparatively also make use of much more personalised tenant data, which in turn, is used to mediate access to landlord properties. This should not be read as a broader move to reducing the power asymmetries of landlords over tenants. Instead, RPPs have reordered the power structures of all actors in the PRS, where the platforms have newfound influence over both tenants and landlords, while also reshaping the activities of other actors including high-street letting agents. I also sought to provide two further contributions: First, to move beyond the role of capital in moulding new RPPs (Fields and Rogers, 2021; Langley and Leyshon, 2021), to investigate how the formative rental experiences of venture teams, shaped their platforms and the functioning of their underlying technologies. Second, in addition to examining how tenants are becoming increasingly surveyed and judged (Eubanks, 2018; Sadowski, 2019), I extended this analysis to how landlords are increasingly falling under the gaze of RPPs, and in doing so, highlighted how the data underpinning RPPs is fragmented and uneven, leading to inconsistent tenant judgements.

The paper also makes contributions to two wider debates. First, it speaks to research in financialisation and the PRS, particularly how these new technologies are reshaping relations within rental markets and how they are being mobilised by investors to extract rents from real estate (Aalbers et al., 2021; Fields, 2022; Wijburg et al., 2018). In departing from research which often focuses on institutional investors, I build upon work that has recognised the role of venture capital in shaping business models (Langley and Leyshon, 2021), by suggesting how venture capital can have a particular impact on smaller firms in steering their business model and product development and in pivoting the aims and priorities of entrepreneurs (cf. Pollard et al., 2018), potentially undermining attempts to create social value for users in solving their problems.

Second, in examining the digital representations of tenants and landlords (Iveson and Maalsen, 2019), the findings contribute to debates concerning platforms and data (Grabher and van Tuijl, 2020; Hendrikse et al., 2021; Sadowski, 2019). Specifically, new insight is provided into the uneven and fragmented data topologies that underpin platforms, which creates inequities in ordering and assessment, and is useful in refining the concept of the data dragnet and recognising the patchiness of the data gaze, where the gaze is incomplete, leading some datafied dividuals to be partially or entirely hidden. In the context of this paper, it can restrict tenant access to the PRS, but in other platform contexts, can shape access to other goods and services, whether digital or material. This raises broader questions over data transparency and governance, as users may be forced into giving consent to platforms who want to access their data, to enable them to enter digital marketplaces. In addition, questions concern the ownership of data and who has the power to modify it, as it is often unclear to users as to how their data is used, tracked and distributed.

This paper's findings add further weight to Shaw’s (2020) argument that the advance of proptech is not a foregone conclusion due to uncertainties concerning models failing to replicate real life. As highlighted in the paper, data unevenness and questions over the validity of assumptions underpinning algorithms plague these new technologies, although these issues do not seem to have stemmed from the proliferation of RPP technology in the UK, so far. The initial uptake of these platforms has been slow, but the ability to cut costs following the Tenant Fees Act, coupled with propositions of user convenience, has seen the appeal of these platforms and their technologies increase, while venture capital funding and its pressure to scale will potentially see the technology move deeper into the PRS. As RPPs have become recognised as a unique market sector, they have become more visible to potential venture capital investors, which in turn, may be likely to further influence entrepreneurial venture teams to pivot their business models to favour scaling and greater returns, rather than the solving of problems in the PRS, as experienced by renters.

In closing, I join Fields and Rogers (2021), in calling for further research into RPPs given the potential for their business models and technologies to be adopted by new financialised PRS markets. It would be particularly useful to gain further insight into the assumptions underpinning algorithms in different geographical settings, how they vary and which values are embodied within them, if they travel across space, and how they are challenged in new locations. Furthermore, a new understanding is needed of data topologies, their unevenness and the institutions that produce and share them, to comprehend how they could accelerate or impede the expansion of RPPs into variegated political economies, and how the unevenness of these topologies can introduce spatially contextualised tenant data inequalities. Finally, it is challenging to gain access to data on the market scale, share and size of RPPs. As they become more important in the PRS, better data is needed to understand the scale of these changes, using novel data science approaches to capture information on their platform operations.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the British Academy (grant number 158907)