Abstract

This paper provides a monetary perspective on capital flows and their effects on geographically uneven economic dynamics. Contributing to debates on global imbalances and the international dimension of financialisation, the paper applies heterodox theories of endogenous money creation, asset pricing, and balance sheet fragility to capital flows across regions. Three theoretical claims are made and illustrated through coherent balance-sheet accounting and empirical examples. First, trade imbalances usually are financed endogenously by net inflows that need not originate from surplus regions. Second, bank inflows are not a precondition for local credit creation, but certain types of gross financial flows can contribute to destabilising financial booms through exchange rate appreciation and asset price inflation. Third, sudden stops in capital flows can be entirely unrelated to current account deficits but may trigger financial instability, resulting in negative gross flows rather than increased outflows. For debates in economic geography and heterodox economics, the arguments imply that the focus on surplus countries as originators of destabilising flows can be misleading and that global financial centres are likely to be more important. More attention is needed to gross portfolio and FDI flows into asset markets rather than bank flows and net flows.

Keywords

Introduction

The 2008 Global Financial Crisis (GFC) has led to a renewed interest in finance and financial instability. Especially financialisation, broadly conceived as the increasing role of financial institutions and financial markets for socio-economic processes, has become an interdisciplinary research agenda that has brought together economic geographers, heterodox economists, and other social scientists (e.g. Christophers 2012; Christopherson et al. 2013; French et al. 2011; Ioannou and Wójcik 2018; Pike and Pollard 2009; Sokol 2013). However, economic geographers have partly been critical of the concept. French et al. (2011) and Christophers (2012) acknowledge the relevance of financialisation but argue that the literature has failed to fully account for its spatial dimension. By restricting the analytical focus to the national-, firm- or household-level, other spaces like regions or the international financial system had received less attention. More concretely, Christophers (2012: p.279) argues that ‘any identification of fundamental structural shifts in capitalism, such as its “financialisation”, […] must critically interrogate the full array of international capital flows in which individual “national economies” […] are embedded’.

Indeed, capital flows, i.e. financial transactions between residents of different geographical units, and their potentially destabilising effects have received some attention by scholars with a critical perspective on finance. In particular heterodox economists have highlighted the role of capital flows in uneven development in the form of boom-bust cycles in the Global South during the 1990s and early 2000s (Agosin and Huaita, 2011; Frenkel and Rapetti, 2009; van Hulten and Webber, 2009; Ocampo, 2016). Such cycles were characterised by large capital inflows, soaring economic activity, and widening current account deficits during booms; and external deleveraging and oftentimes currency crashes during busts. A more recent literature puts forward the notion of ‘international financial subordination’ (Alami et al., 2022). In this view, financialisation takes a ‘subordinate’ form in the Global South due to its relatively low position in the international currency hierarchy. As a result, countries in the Global South are subject to volatile capital flows as their currencies are the first to be ditched by international investors during global financial distress (Alami, 2018; Bonizzi and Kaltenbrunner, 2018; Bortz and Kaltenbrunner, 2017; Fernandez and Aalbers, 2019; de Paula et al., 2020).

Destabilising effects of capital flows were also highlighted in economic geographers’ analyses of the 2008 GFC and the 2010-12 Eurozone crisis, which stressed their spatial patterns. French et al. (2009), Lee et al. (2009), and O’Brien and Keith (2009) identified a build-up of geographical imbalances across countries and regions before the GFC. Large capital flows were associated with current account imbalances. It was argued that regions with export surpluses such as East Asia and the Middle East had excess savings that were invested through capital flows in deficit countries, where they contributed to over-leveraging and asset price bubbles. A very similar perspective was applied to explain the Eurozone crisis, where it was argued that capital flows from surplus countries fuelled credit booms and current account deficits in the Eurozone’s periphery (Rossi, 2013; Sokol, 2013).

Thus, while some analyses of financialisation are certainly guilty of being ‘geographically anaemic’ (Christophers, 2012: p.276), heterodox approaches to capital flows and subordinate financialisation constitute a fruitful point of departure given the inherently spatial character of capital flows. However, the precise workings of capital flows have not always been spelled out explicitly. It is often left unspecified which types of capital flows (e.g. bank, portfolio, or FDI flows) impact trade, credit creation, asset prices, and financial instability, and through what causal mechanisms. In particular, there has been a tendency to simply refer to aggregate capital flows without distinguishing between net flows, which are linked to trade imbalances, and mutually offsetting gross flows that arise in the context of purely financial transactions (e.g. Alami 2018; Clark 2005; Dunford et al. 2013; French et al. 2009; Frenkel and Rapetti 2009; van Hulten and Webber 2009; O’Brien and Keith 2009; Sokol 2013). This runs the risk of overlooking destabilising effects of certain types of capital flows as well as their spatial origins. A large proportion of gross financial flows are hidden in the aggregate despite being a potential source of destabilising financial dynamics. Likewise, the focus on trade-related net capital flows draws attention to regions with trade surpluses such as China and Germany, but misses financial centres in deficit regions such London and New York as potential originators of flows.

This article aims to provide theoretical insights into the nature and role of gross financial flows in geographically uneven economic dynamics. By building on heterodox monetary theory, the paper follows Dunford et al. (2013)’s call for more consideration of monetary factors in economic geography. It draws on the theories of endogenous money creation, asset pricing through portfolio choice, as well as Hyman Minsky’s theory of financially fragile balance sheets (Minsky, 2008). According to the theory of endogenous money, money is created by banks when borrowers demand credit to finance expenditures (Lavoie 2014: chap. 4, McLeay et al. 2014). While only rarely applied in economic geography (see Dunford et al. 2013 and Haberly and Wójcik 2017 for exceptions), it will be shown that this theory has profound ramifications for the geographic origin and economic effects of capital flows, as it implies that banks can readily create purchasing power without having to collect savings from surplus economies. The monetary theory of asset pricing through portfolio choice (Godley and Lavoie 2007, Taylor 2004: chap.8) further provides a framework to understand which and how capital inflows influence financial conditions in the receiving regions, and how this can contribute to diverging dynamics of the kind described above. Finally, deepening recent efforts to link a Minskyan theory of financial fragility to economic geography (Dymski, 2018; Haberly and Wójcik, 2017; van Hulten and Webber, 2009), the paper offers a spatialised Minskyan perspective on how balance- sheet fragility can play out across geographically remote units, thereby illuminating the role of capital flows in economic instability.

Applying this monetary perspective, the paper makes three theoretical arguments. First, when applied to an international context, the theory of endogenous money implies that trade deficits in a specific region are normally financed endogenously by net flows that do not have to originate from surplus regions. Second, bank inflows are not a precondition for local credit booms. By contrast, the Keynesian theory of asset pricing implies that gross flows (deposit, portfolio, and FDI) impact exchange rates as well as bond, share, and real estate prices, thereby rendering asset markets a key channel through which capital flows translate into local financial instability. Third, the paper distinguishes between net and gross sudden stops in capital flows and argues that the latter can be entirely unrelated to current account deficits, but may trigger Minskyan financial instability resulting in negative gross flows rather than increased outflows.

Our arguments have important implications for economic geography and debates on the international dimension of financialisation. First, for the debate on current account imbalances and the Global Financial and Eurozone crisis (French et al., 2009; O’Brien and Keith, 2009; Lee et al., 2009; Rossi, 2013; Sokol, 2013), they imply that trade surpluses are not a useful indicator for the spatial origins of destabilising flows. Those flows more often than not stem from risk-hungry investors in global financial centres rather than from surplus countries. Second, for the debate on the international sources of financialisation (Alami, 2018; Bortz and Kaltenbrunner, 2017; Fernandez and Aalbers, 2019; van Hulten and Webber, 2009; Sokol, 2013), our argument implies that capital flows can indeed drive local financialisation dynamics such as real estate bubbles, but that speculative gross flows into asset markets and the resulting exchange rates dynamics are key causal drivers that require more attention than bank flows and net flows.

The article is related to recent empirical research in mainstream economics and international finance that has highlighted an independent role of gross capital flows for financial stability (Blanchard et al., 2017; Borio and Disyatat, 2011, 2015; Broner et al., 2013; Forbes and Warnock, 2012; Obstfeld, 2012; Shin, 2012; Rey, 2015). While building on this research, it goes beyond it in the following ways. First, this article specifically engages with the treatment of capital flows in economic geography and heterodox economics. Second, while much of the mainstream literature’s theoretical foundations remain unaddressed, this paper provides an explicit theoretical underpinning using heterodox monetary theory. Third, this paper employs a balance-sheet perspective that analyses capital flows through the lens of a ‘set of interrelated balance sheets’ as proposed by Hyman Minsky (2008: p.116). The balance-sheet perspective utilises coherent accounting to track ‘the flows of value between different social and geographical spaces’ as postulated in Sokol (2013: p.510). Stylized but instructive examples will be used to work through the relevant accounting relationships, including the balance-of-payments, making sense of some of the empirical findings (e.g. in Broner et al., 2013). Fourth, the paper highlights the causal relevance of capital flows into asset markets as opposed to the much-discussed bank flows (e.g. Shin, 2012). Overall, rather than adding to the wealth of empirical work, this paper’s main contribution is to enhance conceptual and theoretical clarity on capital flows. 1

The remainder of the paper is organised as follows. The next section lays out a balance-sheet perspective on gross capital flows by explaining how they are represented in the balance-of-payments and on domestic balance sheets, clarifying some accounting issues that are often overlooked. Section 3 discusses the role of net capital flows in balance-of-payments adjustment. Section 4 examines the effects of gross capital flows on uneven financial dynamics, specifically trade imbalances and finance-driven booms. Section 5 turns towards the role of capital flows in sudden stop crises from a Minskyan financial fragility perspective. The last section summarises and discusses the implications for economic geography and heterodox economics.

A balance-sheet perspective on capital flows

The key criterion for a financial transaction to qualify as a capital flow is that the transacting parties are residents of different geographical units. Thus, the concept of a capital flow is an inherently spatial one. Although official balance-of-payments data that empirically record capital flows are only available at the national level, the logic of balance-of-payment accounting presented in this section can be applied to any geographical scale. This makes balance-of-payments accounting a natural tool for tracking the role of capital flows in geographically uneven dynamics. We first review the more familiar balance-of-payments concepts and then introduce a balance-sheet perspective that makes more explicit the bilateral nature of financial transactions between residents of different regions.

The four main types of capital flows recorded in the balance-of-payments are portfolio investment, foreign direct investment (FDI), other investment, and derivatives and employee stock options. Portfolio investment mostly contains short-term investment in bonds and equity that does not come with a controlling stake. Importantly, it includes international trade in those securities on secondary markets. By contrast, FDI consists of equity flows that involve a controlling claim in a company (a stake of at least 10%), debt flows (e.g. between a parent company and its subsidiaries), and investment in real estate. Other investment contains cross-border bank flows (loans, deposits) as a key component, but also currency flows, trade and IMF credit, and some residual items. Lastly, derivatives and stock options constitute a separate (and difficult to measure) category. 2 We will mostly focus on other investment, portfolio, and FDI flows, which are at the centre of the theoretical channels that will be discussed in this paper.

Turning to the balance-of-payments, this is usually written as:

where the current account (

A useful way of re-writing the balance-of-payment is the following:

Another, less familiar, way of looking at gross flows is to conceive of them as changes in external assets and liabilities on the balance sheets of residents of different geographical units. Indeed, the precise definition of a gross inflow is a net incurrence of a liability vis-à-vis a resident of a different geographical unit. A gross outflow is the net acquisition of a foreign asset by a domestic resident. Equations (3) and (4) imply that such gross capital flows can be independent from trade flows. In fact, a large proportion of gross flows is entirely unrelated to trade. All incurrences of foreign liabilities that are matched by an acquisition of foreign assets constitute what we will call offsetting financial flows that do not involve trade. Correspondingly, they also do not involve net flows, which are only a subset of total gross flows. To see this clearly, consider the following example, 4 which shows what happens on domestic balance sheets and in the balance-of-payments.

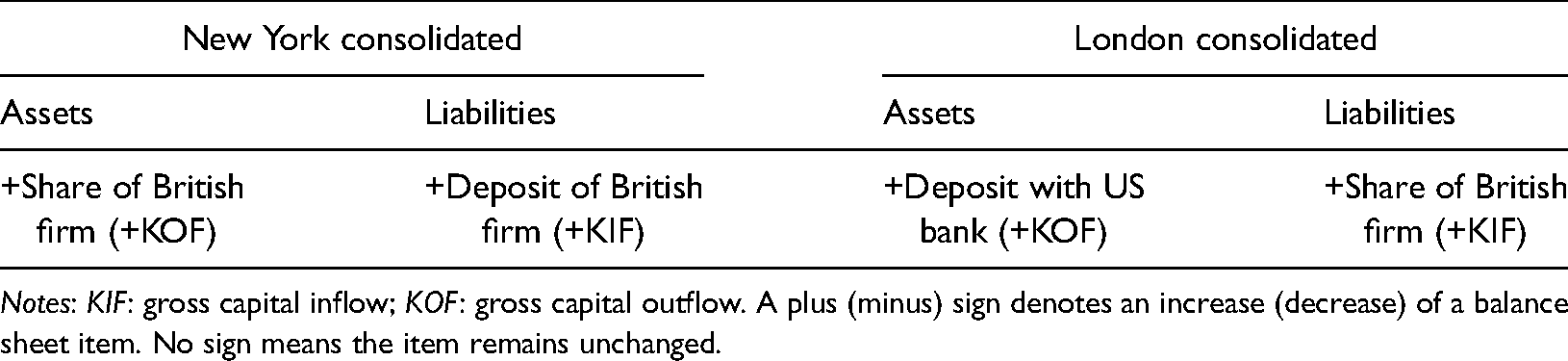

Suppose an institutional investor from New York buys a share from a London-based firm. To keep the presentation simple, we use consolidated external balance sheets of the two traders and their respective commercial banks at the city level (Table 1).

A New York resident purchases a share issued in London.

Notes:

In this case, there is a gross portfolio outflow from New York (investment in a foreign share) that is matched by a gross other investment inflow (increase in deposits held by a London bank). From London’s perspective, this is a gross portfolio inflow (sale of a domestic liability to a foreigner) that is directly matched by a gross other investment outflow (acquisition of a deposit with a US bank). Thus, gross flows take place, but no net flows: New York’s (and London’s) financial account and trade balance remain unchanged:

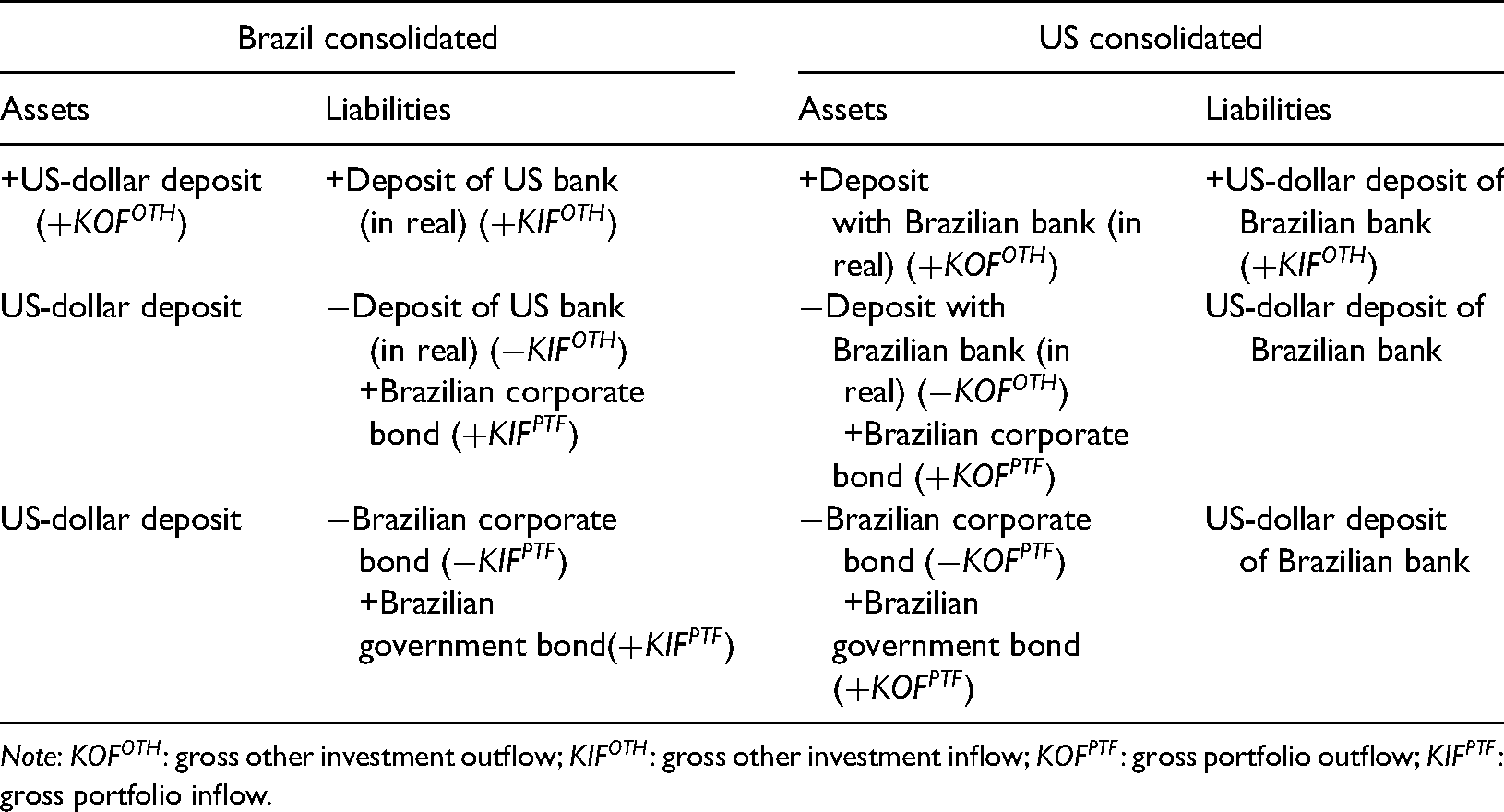

A further often overlooked feature of capital flows relates to the fact that despite being called gross flows, these are defined as net acquisitions/incurrences of external assets/liabilities. In fact, many gross capital flows net out in the balance-of-payments when examined on an aggregate basis. Consider the example of a US investor who wants to invest in Brazilian financial assets. In the first instance, the investor will go on the foreign exchange market to convert US dollar deposits into deposits in Brazilian real. In return, a Brazilian bank obtains US dollar deposits. This transaction leads to offsetting gross (other investment) inflows and outflows for both countries (first row of Table 2).

US investor purchases Brazilian financial assets.

Note:

In the next step, the investor decides to invest these deposits in a corporate bond from the Brazilian petroleum company Petrobras (second row). Importantly, although this clearly is an international financial transaction, no gross flows take place on an aggregate basis. The reason for this is that while Brazil has increased its foreign liabilities by selling a bond to a foreigner (a positive portfolio inflow), it has also reduced its foreign liabilities by losing the deposit held by the US investor (a negative other investment inflow). Everything else constant, a reduction in a foreign liability (asset) is recorded as a negative gross inflow (outflow). At a more disaggregated level, these flows are thus recorded in Brazil’s balance-of-payments as a positive portfolio inflow and a negative other investment inflow:

5

The preceding discussion has illustrated the importance of clearly differentiating between offsetting gross flows and net flows. While it is common to simply speak of ‘capital flows’, this usage is imprecise as it does not discriminate between flows that have no net impact on the financial account and the trade balance (i.e. offsetting financial flows) and those that do (i.e. non-offsetting, trade-related net flows). Similarly, to fully understand how gross flows impact and behave during geographically uneven booms and busts, it is necessary to distinguish between different types of in- and outflows that can become positive or negative during certain periods. In the following sections, we will illustrate the importance of these distinctions for debates in economic geography and heterodox economics.

Capital flows and balance-of-payments adjustment

A fundamental theoretical debate addresses the question of balance-of-payments adjustment (Dunford et al., 2013; Harvey, 2019; Thirlwall, 2011). If region and countries with different specialisations and cost advantages trade with each other, are there mechanisms that will ensure balanced trade? If not, how can imbalances persist? This seemingly abstract question has important implications for the role of capital flows in geographically uneven economic dynamics discussed below. We will argue that extending the theory of endogenous money to open economies can clarify the issue of balance-of-payments adjustment.

The theory of endogenous money is a long-standing element of the post-Keynesian branch of heterodox economics (see Lavoie 2014: chap. 4, Taylor 2004: chap.8) and has more recently also been endorsed by economists at central banks (Carpenter and Demiralp, 2012; McLeay et al., 2014). According to this approach, money creation by commercial banks is driven by the demand for credit. Commercial banks endogenously create the desired deposit money and, in turn, may borrow reserves from the central bank to stay liquid without first having to collect the deposits of savers. The central bank sets the short-term interest rate on the interbank market. The lending rate offered by commercial banks is then determined by the interbank rate plus a mark-up that commercial banks charge to compensate for risks. Conditional on their creditworthiness, borrowers obtain as much credit as they wish at the given interest rate. Thus, in monetary economies, the ability of private financial institutions to generate purchasing power is not restricted by resource constraints such as the supply of saving.

With respect to the issue of balance-of-payments adjustment, the logic of balance-of-payments accounting discussed in the previous section dictates that for constant foreign reserves a change in the trade balance must be accompanied by a change in the financial account, and thus be matched by net capital flows. In this sense, it is trivial to assert that a region that runs a trade deficit receives capital inflows. But what is the direction of causality between trade flows and net capital flows? Some geographical narratives suggest that trade imbalances stem from surplus economies that ‘recycle’ their surpluses in the form of capital flows abroad (e.g. French et al., 2009; Lee et al., 2009; O’Brien and Keith, 2009). In this view, the causality seems to run from net capital flows to the trade balance. While a different interpretation of this narrative will be explored below, let us first evaluate this view.

The argument that net flows determine trade flows could be justified by the fact that a desired (net) import can only be realised if it can be financed. Indeed, the creditor has the ultimate power to decide whether a net import can go ahead. However, is this constraint normally binding? Can a creditor force a potential importer to import? From the perspective of the theory of endogenous money, the answer is no. Insofar credit creation is demand-driven, it is implausible that a creditor can force a debtor to borrow. In a monetary economy with an elastic supply of credit, trade flows should usually lead to accommodating net capital flows (Taylor 2004: chap.10, Harvey 2019, Lavoie 2014: chap.7).

One of the clearest expositions of this view can be found in Lavoie (2014: chap.7), who argues that changes in the current account are normally accommodated by changes in bank loans and deposits through endogenous money creation by commercial banks. Insofar foreign banks deem domestic borrowers creditworthy, they accommodate the demand for credit. In an international context, this means that trade flows are normally financed endogenously by bank flows (which are a component of the other investment category of capital flows).

Trade deficits are normally financed endogenously by net capital inflows, provided domestic borrowers are creditworthy. Surpluses in one region are thus an outcome of trade deficits in another region, not the other way around.

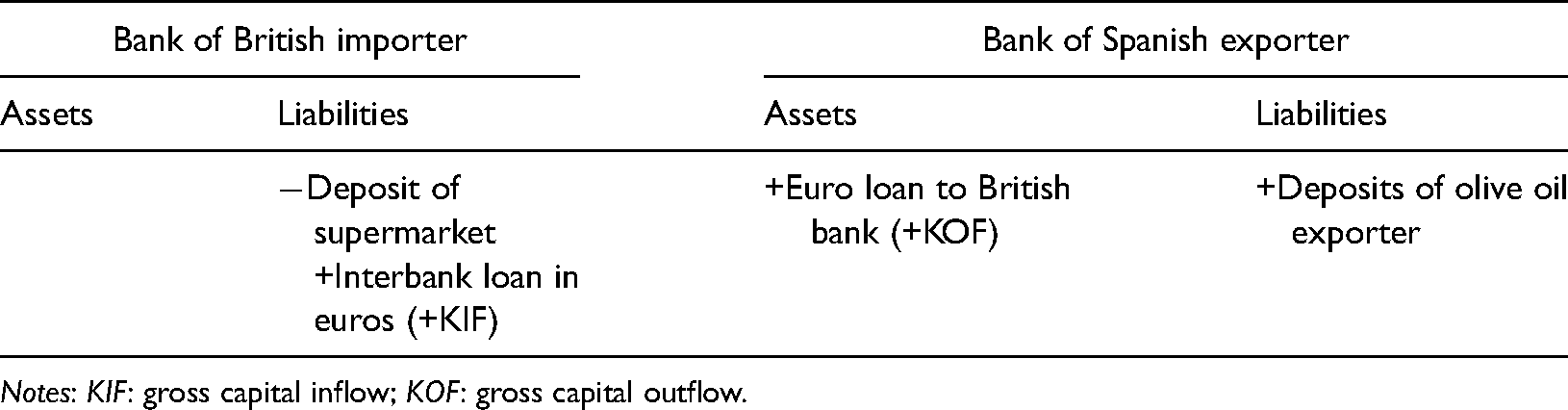

Consider an example that illustrates the endogenous financing of trade flows. Suppose a British supermarket imports Spanish olive oil (Table 3). This is an import that reduces the UK’s trade balance. The importer’s bank may obtain euros through an interbank loan from the Spanish bank, which expands its balance sheet accordingly. The British bank can then use these funds to supply the supermarket with the necessary euros for the import.

6

This is a gross other investment inflow (

British supermarket imports Spanish olive oil.

Notes:

In the UK’s balance-of-payments, the transaction leads to a fall in the trade balance and an increase in the financial account:

Are there any equilibrating mechanisms that ensure a balanced current account (and thus zero net flows) over longer periods? In their discussion of trade and regional development, Dunford et al. (2013) hold that (regional) trade deficits can be financed by international credit, but suggest that there are constraints over longer periods. Similarly, according to the post-Keynesian theory of balance-of-payments constrained growth (Thirlwall, 2011), trade must be balanced over the long run, and economic growth must be consistent with this requirement. The (implicit) assumption is that fast-growing deficit countries may eventually lose their creditworthiness with foreign banks. Foreign creditors may then refuse to finance further deficits, the country undergoes a stop in capital inflows, and the central bank runs out of foreign reserves. In this case, the deficit country is forced to rebalance its current account, which will typically require a slowdown in economic growth. Historical examples of balance-of-payments crises indeed suggest that most countries cannot run ever rising external debt ratios, especially in the Global South. However, these are temporary episodes that typically occur in specific historical and economic contexts. While the existence of such crises points to limits to an endogenous financing of trade deficits, they are not inconsistent with such financing under normal conditions.

The bottom line is that provided domestic borrowers are deemed creditworthy, trade flows are financed endogenously by what can be called accommodating net flows. Those net flows do not cause the trade flows but are merely their flip side. The exporting party’s capacity to provide the necessary financing for the transaction is completely independent from any prior export surpluses. Export surpluses are the outcome of trade transactions that are financed by the creation of purchasing power through banks. Sudden stops in capital flows, which will be discussed in more detail in section 5, can temporarily disrupt the endogenous financing of trade flows, but are the exception rather than the norm.

Capital flows, trade imbalances, and geographically uneven financial booms

Economic geographers have assigned a key role to capital flows from surplus countries in the build-up of financial instability in deficit countries (French et al., 2009; O’Brien and Keith, 2009; Rossi, 2013; Sokol, 2013). However, if net capital flows normally accommodate, as argued in the previous section, do capital flows have such causal effects? We will argue that gross capital flows do influence uneven economic dynamics, but that these flows need not stem from surplus countries. We propose distinguishing between different types of flows to understand the potential theoretical channels. More specifically, capital flows are not a precondition for domestic credit creation but may impact financial booms through asset markets and exchange rates.

Capital flows, regional imbalances, and credit creation

According to a common view expressed succinctly in French et al. (2009: p.295), ‘[t]he geographical recycling of surpluses and deficits has always been critical to the production of financial booms and their eventual collapse’. This idea has been applied both to the 2008 GFC and the 2010-12 Eurozone crisis. With respect to the GFC, Lee et al. (2009: p.741) argue that the recycling of surpluses from exporting economies in Asia and the Middle East ‘provided the energy and material for the build up of bubble in asset prices in the west’. Similarly, O’Brien and Keith (2009: p.248) claim that ‘[t]he free flow of capital eventually led to the current account imbalances that led to a global savings glut being recycled into the USA and UK financial sectors; a necessary condition for households and the banking sector to become highly leveraged’. Similar narratives were proposed to describe the run-up to the Eurozone crisis. According to Sokol (2013: p.510), ‘Germany’s current account surplus has been recycled as bank lending in the European periphery […] creating housing bubbles and debt-driven consumption booms’. Rossi (2013: p.382) claims that core countries with current account surpluses were ‘providing to “peripheral” countries in the euro area an increasing volume of savings in order to pay for their […] domestic expenditure’.

From the perspective of the theory of endogenous money, there are two issues with this narrative. First, it is misleading to suggest that the net inflows into deficit countries must have stemmed from surplus countries’ savings. As shown in the previous section, surpluses from net exports arise at the end of an endogenous financing process. They are not a precondition for net flows to take place. In this sense, the metaphor of a ‘recycling of surpluses’ is not helpful as it suggests that money was a scarce resource. This distracts from the fact that, in monetary economies, banks can endogenously generate purchasing power and do not need to recycle existing funds. More importantly for the geographical dimension of capital flows, the claim that net inflows into deficit countries (regions) must come from surplus countries (regions) is not necessarily correct in a multi-spatial environment. While in a world with only two regions, a trade deficit of region A must be matched by a net capital inflow from region B, this no longer hold in a world with more than two regions.

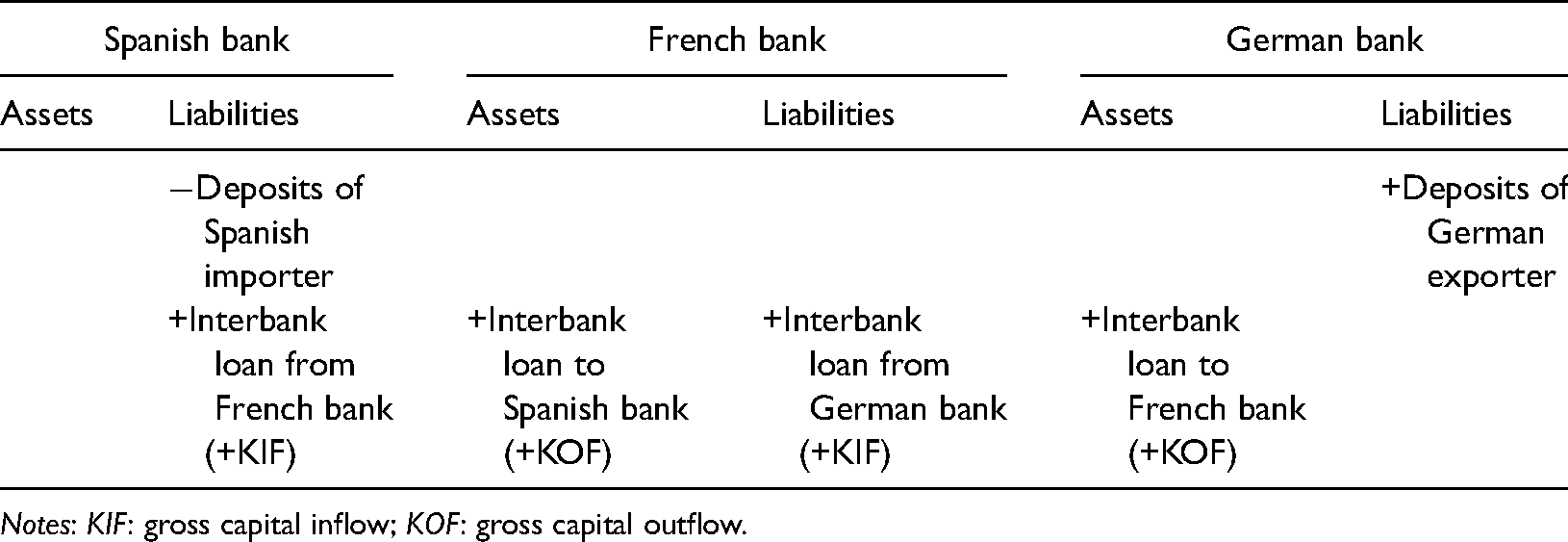

A trade deficit vis-à-vis region B does not imply net capital inflows from region B.

Consider an example from the Eurozone (an analogous scenario could apply across currency areas and different regions). A Spanish firm imports goods from a German firm (Table 4). The Spanish firm’s bank decides to borrow from a French instead of a German bank to compensate for its loss in deposits. In this case, Spain receives a net inflow from France, not Germany. In turn, the German bank may lend money to the French bank and thus records a net outflow to France, not Spain. Net flows do not change for France, but France increases its financial integration vis-à-vis Spain and Germany without being involved in the trade at all.

Spain imports from Germany but receives net inflows from France.

Notes:

The example calls for caution with the assumption that a region with a trade deficit vis-à-vis another region is also indebted to that region. Likewise, it illustrates that a region or country can have a relatively balanced trade account but exhibit substantial financial exposure to other countries (France in this example). Hobza and Zeugner (2014) present empirical evidence on gross flows in the Eurozone and conclude that current account deficits were mostly financed by surplus countries, but also by countries with large financial centres like Paris and London. Similarly, Borio and Disyatat (2011) and Tooze (2018) show that in the run-up to the GFC, gross capital inflows to the USA from Europe, especially from the deficit country UK, outstripped the flows from East Asian surplus countries. This suggests that large financial centres are often more important originators of risky financial flows than surplus countries.

A second issue with the narrative outlined above is that it suggests capital inflows are a precondition for domestic credit booms. However, from a monetary perspective, it is not clear why countries would need capital inflows to finance credit creation. As demonstrated in the previous section, net capital flows accommodate trade deficits but do not have any direct implications for domestic lending. Domestic banks can create loans and deposits without first having to collect funds abroad.

Capital inflows are not a precondition for local credit creation since banks do not need to borrow abroad to make loans.

Why do domestic credit booms then typically come with (net) capital inflows? Credit booms are often driven by bubbles in local asset markets, such as real estate in Spain and the US before the GFC (Martin, 2010). We will explain below how certain types of capital flows can play a role in stimulating such bubbles. Empirical research shows that rising asset prices in turn boost economic activity through (residential) investment and wealth effects (Stockhammer and Wildauer, 2015). A boom in economic activity then also increases imports, leading to a worsening current account position that must be matched by net capital inflows. 8 In addition, domestic residents may increasingly invest in foreign assets, leading to an outflow of deposits that is compensated by international interbank lending. Indeed, as shown in Febrero et al. (2019) for the case of Spain during the run-up to the GFC, while domestic banks did borrow abroad in European money markets, these funds were used to finance net imports and acquire foreign assets (especially FDI). Inflows were not a precondition to finance the Spanish real estate bubble.

In summary, this suggests that narratives of global imbalances and financial instability would benefit from a more careful consideration of the nature of capital flows in monetary economies (French et al., 2009; O’Brien and Keith, 2009; Lee et al., 2009; Rossi, 2013; Sokol, 2013). First, while large bank inflows into the US and the European periphery were a striking feature of the period before the GFC, their causal relevance for rising trade imbalances and credit booms is much less obvious than often suggested. Second, the geographic focus on surplus economies as the origin of destabilising flows is not always helpful in a global economic system in which banks do not need to collect savings to generate financial resources. Instead, the presence of large financial centres is often a better indicator for the capacity of a region to generate large capital flows into other regions. Indeed, the relevance of the two major financial centres London and New York for the GFC, which has been emphasised by economic geographers (Wó jcik, 2013), can only be properly understood against the background that their location in deficit countries did not prevent them from sending huge capital flows to each other as well as to surplus countries like Germany.

Capital flows and asset price booms

If capital flows are not a precondition for local credit creation, how do they affect geographically uneven dynamics? One branch of the heterodox literature discusses the ‘international financial subordination’ of countries in the Global South and highlights the speculative and volatile nature of short-term capital flows (Alami et al., 2022; Alami, 2018; Bonizzi and Kaltenbrunner, 2018; Bortz and Kaltenbrunner, 2017; Fernandez and Aalbers, 2019; de Paula et al., 2020). Due to their lower position in the international currency hierarchy, currencies of economies in the Global South carry lower liquidity premia than currencies that fulfil international money functions like the US dollar. As a result, they are the first that investors will abandon in periods of international financial distress. These episodes may lead to abrupt currency depreciations and hikes in domestic interest rates, imposing constraints on national policy-making. Likewise, periods of increased risk appetite come with higher demand for riskier assets issued in the Global South, leading to currency appreciation and lower interest rates. Importantly, this literature implicitly shifts the focus from surplus countries as the originators of destabilising capital flows to international financial investors.

The literature on subordinated financialisation thus focusses on gross financial flows that are unrelated to trade, and typically distinguishes short-term flows, which are speculative and volatile, from more stable long-term investment-oriented flows. However, it rarely distinguishes between different types of financial assets. For example, is it the rate of interest on loans or on bonds that adjusts to changes in international risk appetite? A more fine-grained differentiation of different types of flows would help clarify the theoretically expected effects of offsetting financial flows. Importantly, although some of these transactions may not appear in (aggregate) measures of gross flows as shown in section 2, they can still impact financial dynamics.

The monetary theory of asset-price determination through portfolio choice is helpful to disentangle the effects of different types of flows. Initially developed by James Tobin, it has been integrated into the post-Keynesian branch of heterodox economics (Godley and Lavoie 2007, Taylor 2004: chap.8), and has recently been revived by researchers at the International Monetary Fund (Blanchard et al., 2017). In this approach, the prices of different financial securities such as government bonds and corporate shares are determined on secondary financial markets by the demand of wealth holders seeking profitable portfolios. A typical result is that exogenous changes in the preferences or expectations of wealth holders, e.g. their preference for internationally liquid assets like the US dollar, translate into changes in either the quantity or the rate of return on assets. Whether there is quantity or price adjustment will depend on the nature of the financial asset.

Consider first cross-border bank loans and deposit inflows as a key component of other investment. They provide domestic borrowers with foreign currency liquidity that can be used to finance net imports or to acquire foreign assets. From the perspective of endogenous money theory, these inflows are driven by the demand for foreign currency. Importantly, they are unlikely to affect the rate of return on loans, as the domestic interbank rate is fixed by the central bank. Lending rates are determined by commercial banks that add a mark-up on the interbank rate to compensate for risk (Lavoie 2014: chap.4). While the price of loans is thus fixed, their supply is elastic. It is thus unlikely that loan inflows will directly stimulate domestic lending. Instead, if interest rates on foreign loans are lower than the domestic interbank rate, banks may borrow more cheaply abroad to obtain liquidity and then pass some of these lower cost on to domestic borrowers, thereby stimulating credit demand. As a result, risk premia on domestic lending rates may be influenced by international factors that impact external borrowing cost such as global risk perceptions or foreign monetary policy. It is then these international factors that are an exogenous causal driver of the domestic credit boom rather than the resulting bank flows, although the latter can contribute to a build-up of financial fragility as will be discussed below.

A different channel through which bank flows matter is related to the exchange rate. Gross deposit flows (as well as derivative flows, see for example Alami 2019) arise in the context of foreign exchange trading. For example, the transaction examined in section 2 where the US investor sells dollar deposits to acquire Brazilian assets is likely to put upward pressure on the Brazilian real, since – everything else constant – the Brazilian bank has no excess demand for US dollars. The US bank may thus have to offer its dollars for a better price (i.e. a more depreciated dollar-real exchange rate) to convince the Brazilian bank to buy, so that the Brazilian real appreciates. If there are currency mismatches on local balance sheets, appreciation can lead to wealth effects that stimulate investment and borrowing (Kohler, 2019; Ocampo, 2016). Importantly, this mechanism operates through the exchange rate as an asset price rather than foreign liquidity being lent out to domestic borrowers.

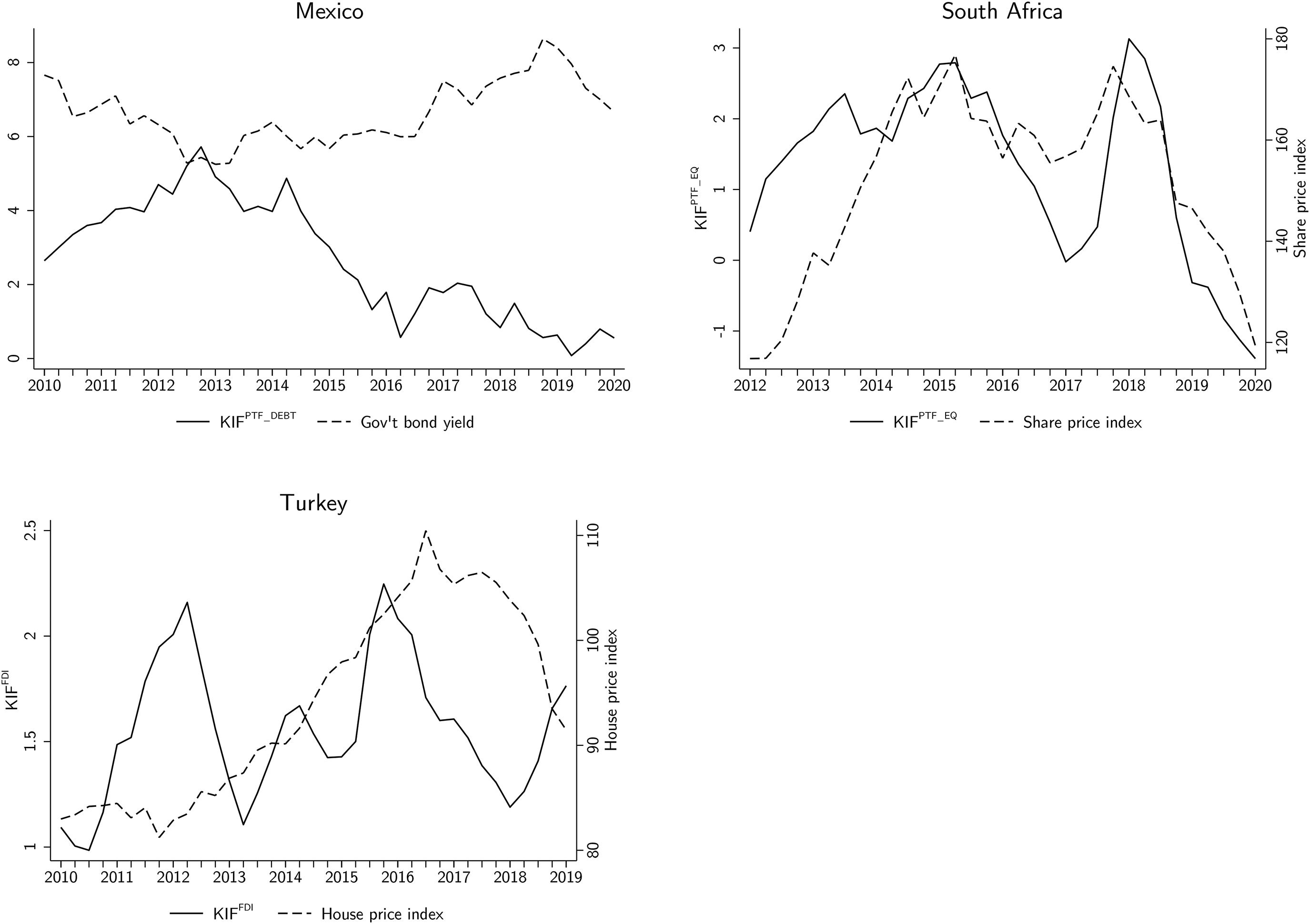

Next, consider portfolio investment. In contrast to loans, securities like bonds and shares are traded on secondary markets and have flexible prices that determine their rates of return. An exogenous change in the risk appetite in global financial centres can thus lead to portfolio inflows that push up local asset prices. In the case of portfolio bond inflows, this may drive down long-term interest rates (see Warnock and Warnock 2009 for empirical evidence). Likewise, sales of domestic bonds by foreigners may raise long-term rates, as highlighted in the literature on subordinated financialisation (Bortz and Kaltenbrunner, 2017; de Paula et al., 2020). A recent example displayed in Figure 1 is from Mexico, where portfolio bond inflows increased substantially during the second Quantitative Easing programme of the US Federal Reserve, leading to a decline in government bond rates. Flows began to gradually revert with the 2013 Taper Tantrum and before the 2016 US presidential election, driving up yields again.

Gross capital inflows and asset prices.

Data sources: IMF International Financial Statistics, IMF Balance-of-Payments Statistics, OECD Analytical House Price Data. Author’s calculations.

Notes:

Similarly, portfolio equity inflows can inflate stock prices. For example, South Africa underwent a boom-bust cycle in stock prices during the 2010s that was arguably partly driven by portfolio flows (see Figure 1). Thus, unlike bank loan flows, surges in portfolio inflows are a potential exogenous source of local financial booms.

Finally, FDI flows often arise in the context of mergers and acquisitions or the reallocation of funds within multinational corporations. Insofar offshore subsidiaries of those corporations domestically engage in speculation, FDI flows can become a vehicle for those activities. An important aspect that is often overlooked is speculative investment in real estate. This may be driven by multinational real estate companies but also by real estate acquisitions by foreigners that can directly contribute to domestic house price inflation (see Badarinza and Ramadorai 2018 and Li et al. 2020 for empirical evidence on London and the US, respectively). This channel has received less attention but is highly relevant for the claim that capital inflows can fuel housing bubbles (Lee et al., 2009; Fernandez and Aalbers, 2019). For example, Turkey underwent a housing bubble between 2012 and 2017 that was in parts driven by real estate purchases by foreigners (Ergven, 2020), reflected in increased FDI inflows (see Figure 1). 9

Locally destabilising effects of gross capital inflows mainly operate through exchange rates and asset markets. Portfolio inflows can reduce bond yields and push up share prices, inward FDI can contribute to property price bubbles, whereas bank flows mostly influence exchange rates.

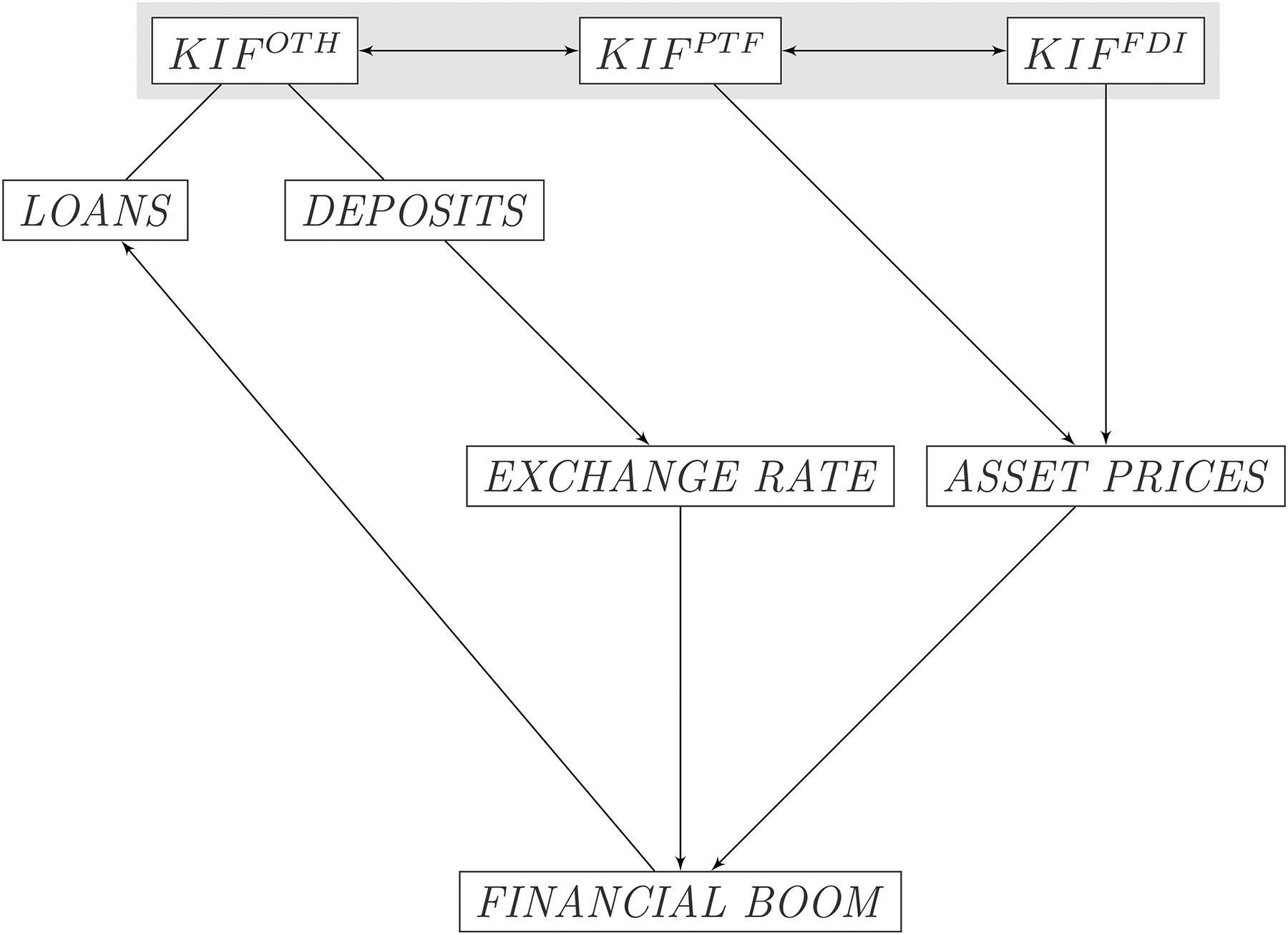

Figure 2 illustrates the argument. To understand how offsetting financial flows impact local financial booms, it is important to distinguish different types of flows. The mere reference to capital flows in the aggregate is not helpful, first, because a lot of gross flows cancel out in the aggregate and, second, because different gross flows are likely to have different effects.

Types of gross capital inflows and their effects on local financial booms.

Notes:

Gross flows and sudden stop crises

After the boom comes the bust. But again, the exact role of capital flows for the bust phase is not always spelled out clearly. In the narrative of capital-flow driven imbalances outlined at the beginning of the previous section, there is the assumption that current account deficits are ultimately unsustainable and lead to crises. Concerning the trigger of the bust, the literature often refers to the notion of a ‘sudden stop’, i.e. an abrupt drying-up of capital inflows (Agosin and Huaita, 2011; Dymski, 2018; Frenkel and Rapetti, 2009; van Hulten and Webber, 2009). The common perception of a sudden stop refers to net capital flows: a country runs a trade deficit; at some point foreign creditors refuse to supply further credit, i.e. there is a stop in net inflows, and the country is forced to reduce its deficit as soon as it runs out of foreign reserves.

An issue that has received less attention is that sudden stops can also arise with offsetting gross financial flows, in which case they may play out differently for the affected economy. To understand how, it is useful to build on the work of the post-Keynesian economist Hyman Minsky (2008). In the Minskyan approach, the composition of gross assets and liabilities is crucial. Financial fragility arises from risky balance sheet structures that compromise debtors’ ability to generate the necessary liquid funds to meet their financial payment commitments. Dymski (2018), Haberly and Wó jcik (2017), and van Hulten and Webber (2009) have integrated Minskyan perspectives into economic geography, and Bonizzi and Kaltenbrunner (2018) and de Paula et al. (2020) into the literature on subordinate financialisation. We will apply this approach to international financial commitments across spatially remote actors to understand how sudden stops in gross capital flows play out.

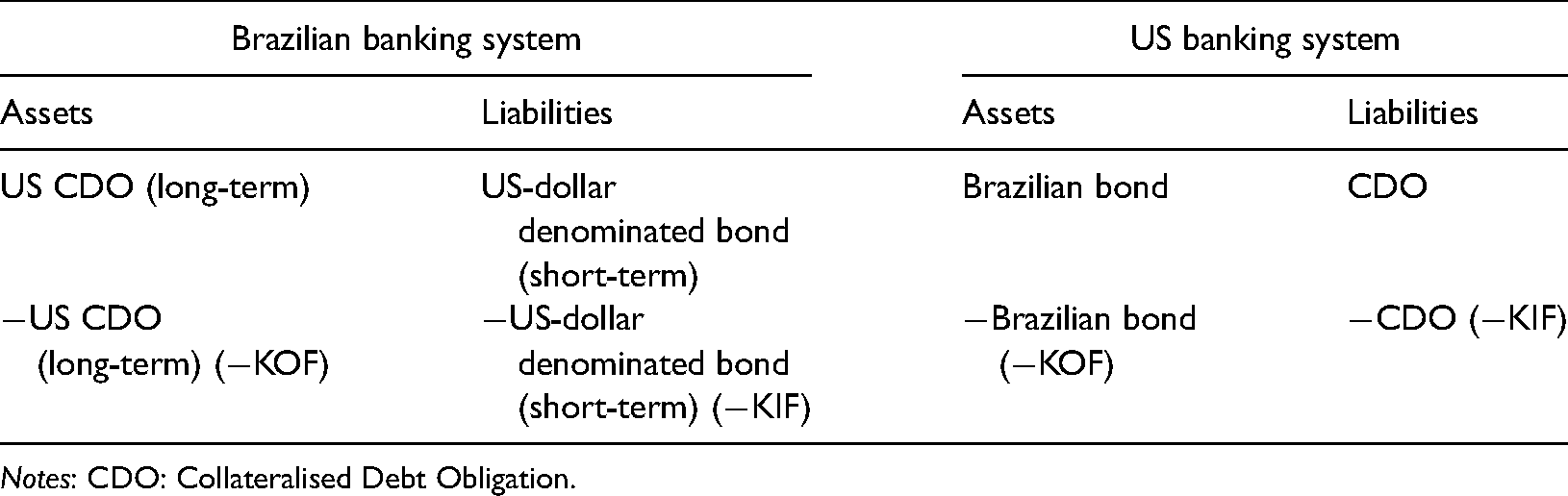

Consider first the classic version of a sudden stop which we will refer to as a net sudden stop. Suppose a Brazilian firm wishes to import goods from a US exporter of machinery. However, due to Brazil’s sizeable trade deficit, the Brazilian banking system is no longer deemed creditworthy and therefore not able to borrow the necessary US dollars from abroad. At the same time, the Brazilian central bank has run out of foreign reserves that could be used to finance those imports. In this case, the importers’ bank would have to decline the transaction and the import cannot go ahead. This is the classic case discussed in section 3, where a country hits its balance-of-payments constraint and is forced to reduce its trade deficit:

Gross sudden stop: US bank refuses to refinance Brazil's short-term external liabilities.

Notes: CDO: Collateralised Debt Obligation.

Importantly, the gross sudden stop is entirely unrelated to Brazil’s current account position. It may occur although Brazil has balanced trade, as assumed in this example. Likewise, the gross sudden stop has no instantaneous implications for Brazil’s trade balance:

A sudden stop in capital flows plays out differently for net and gross flows. Gross sudden stops are related to fragile external balance sheets and can occur even if current accounts are balanced.

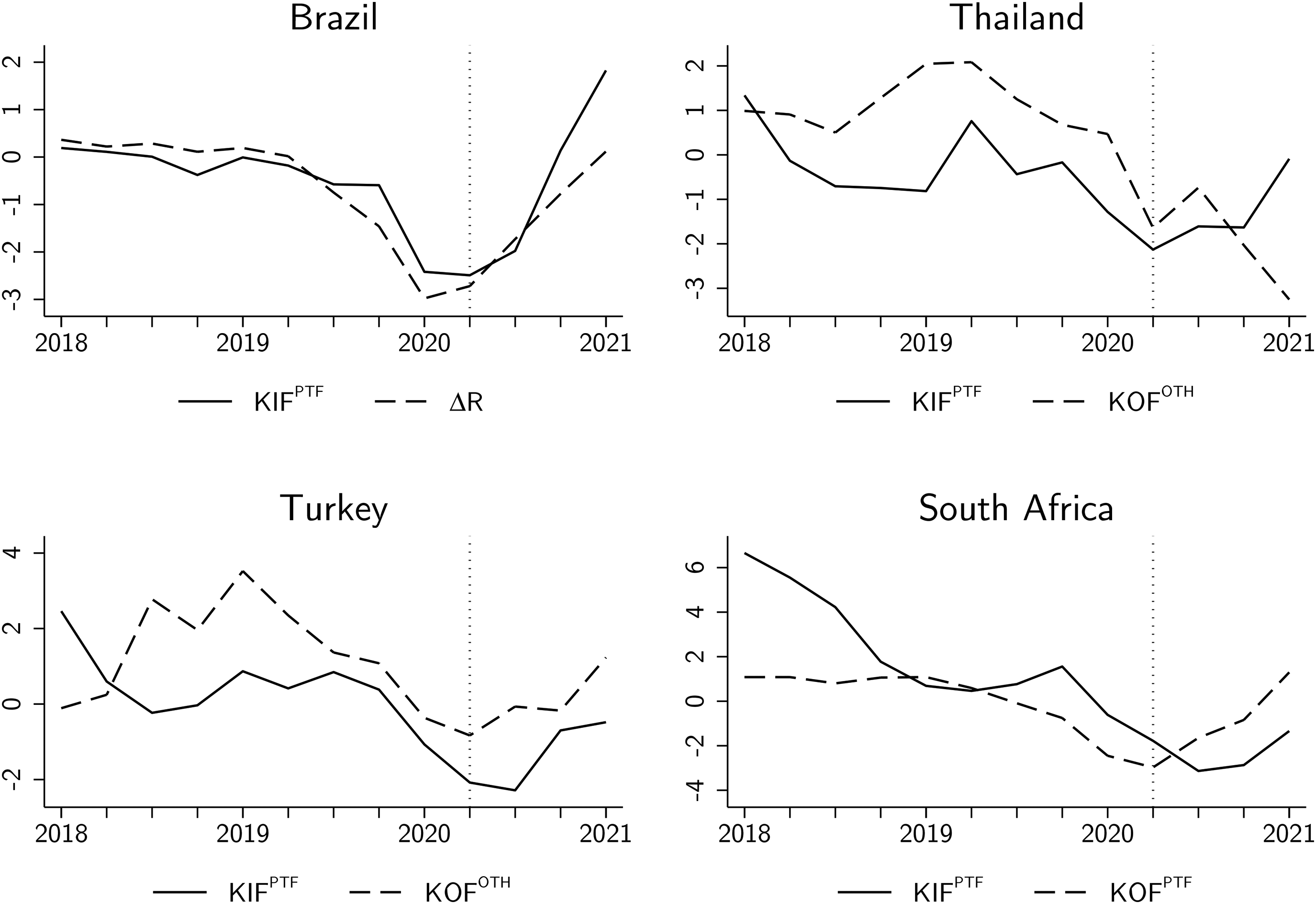

A final remark relates to the frequent association of external financial crises with rising capital outflows (e.g. Frenkel and Rapetti 2009; van Hulten and Webber 2009; de Paula et al. 2020). From the Minskyan perspective adopted here, domestic residents’ external assets are likely to decrease during crises as they are sold to meet external payment commitments, leading to a reduction in outflows. This issue may be compounded by foreign investors reallocating funds into high-quality currencies by selling domestic securities back to domestic residents. These dynamics result in negative out- and inflows as shown in Table 5. A recent example are the large reversals of gross portfolio flows to many emerging markets at the beginning of the COVID-19 pandemic (Figure 3). For Turkey and Thailand, these negative inflows were matched by negative other investment outflows, whereas Brazil compensated them by a loss in foreign reserves and South Africa by a net reduction in its foreign portfolio assets.

Negative gross flows to emerging markets during the COVID-19 pandemic.

Data sources: IMF International Financial Statistics, IMF Balance-of-Payments Statistics. Author’s calculations.

Notes:

Gross capital flows can become negative, especially during financial crises when local residents deleverage and foreign investors rush into high-quality assets.

To conclude, offsetting gross flows can play a distinct role from trade-related net flows, not only during economic booms but also in busts. A Minskyan analysis of the balance sheets of geographically distinct actors and their interrelations through different types of external assets can help identify financial stability risks beyond the frequently cited unsustainable current account deficits.

Conclusion

This article has argued that heterodox monetary theory provides tools for a more precise understanding of the role of capital flows in geographically uneven dynamics. Applying the theory of endogenous money creation to an international setting, it was argued that trade deficits are normally financed endogenously through the creation of purchasing power by banks, which is reflected in net capital flows. Although net flows are thus endogenous, gross flows can still drive destabilising financial dynamics, but a key channel for this works through asset markets and exchange rates rather than the direct provision of bank liquidity. Drawing on the theory of asset pricing through portfolio choice, we posited that offsetting financial flows can influence exchange rate- and local asset-price dynamics. Specifically, portfolio inflows can drive down long-term interest rates and push up share prices, whereas FDI flows can inflate property prices. By contrast, cross-border bank flows do not directly affect local interest rates and asset prices as short-term rates are determined by monetary policy, but they may influence exchange rate dynamics. Finally, we argued that sudden stops in gross flows can be a major source of instability even if current accounts are balanced, and often come with external deleveraging reflected in negative gross flows.

Our analysis has two main implications for debates in economic geography and heterodox economics. First, the theory of endogenous money implies that a large proportion of gross capital flows across geographic units is independent of these units’ surplus or deficit position. For the debate on current account imbalances and the Global Financial and Eurozone crisis (French et al., 2009; O’Brien and Keith, 2009; Lee et al., 2009; Rossi, 2013; Sokol, 2013), this means that the exclusive focus on surplus countries like China and Germany as the spatial origin of destabilising flows has been somewhat misleading. The presence of large financial centres like New York, London and Paris is a better indicator for a country’s or region’s capacity to originate speculative capital flows, vindicating geographical research on financial centres (e.g. Wó jcik 2013; Wójcik et al. 2018). Similarly, the debate would benefit from greater consideration of gross financial flows as opposed to (trade-related) net flows. This includes allowing for the possibility of sudden stops in gross capital flows that are related to risky external balance sheets, independently of current account deficits. Such a perspective would underpin existing efforts to integrate Minskyan concepts of financial fragility into economic geography (Dymski, 2018; Haberly and Wó jcik, 2017; van Hulten and Webber, 2009).

Second, the monetary theory of asset pricing implies that cross-border bank flows are more likely to be an outcome of geographically uneven dynamics than a cause. By contrast, gross portfolio and FDI flows can be an exogenous force of instability. For the debate on the international sources of local financialisation dynamics (Alami, 2018; Bortz and Kaltenbrunner, 2017; Fernandez and Aalbers, 2019; Frenkel and Rapetti, 2009; van Hulten and Webber, 2009; Ocampo, 2016; Sokol, 2013), this implies that it is important to differentiate not just between short- and long-term financial flows, but also between different types of financial assets. It is vital to appreciate the special nature of securities and real estate assets that are traded on secondary markets, making them prone to speculative dynamics. Flows into local asset markets therefore deserve as much attention as potential drivers of unsustainable booms as the much highlighted bank flows. This also implies that speculative portfolio and FDI flows may require stricter regulation beyond already existing capital controls on bank flows.

Finally, there are also important insights that economic geography can bring to heterodox monetary theory. A major weakness of the macroeconomic focus in post-Keynesian and Minskyan approaches is its methodological nationalism and the correspondingly high level of spatial aggregation. However, processes of financial instability are typically geographically uneven not just across countries. For example, house price bubbles are often geographically varied within countries and driven by major cities (Martin, 2010). Similarly, a large part of international financial transactions are conducted between major global financial centres and tax havens. Recently, financial geographers have started unpacking the spatial nature of capital flows using bilateral and micro-level data, revealing the network-character of those centres (Haberly and Wójcik, 2015; Wójcik et al., 2022). This approach could be used to analyse how financial centres transmit financial shocks emanating from the Global North to economies in the Global South. Knowledge of a local financial centre’s relative position in the ‘Global Financial Network’ (Wójcik et al., 2022) might shed light on exposure to the country-level gross sudden stops discussed in this paper. Such a spatialised Minskyan perspective would indeed help make the financialisation debate less geographically anaemic.

Footnotes

Acknowledgments

I’m grateful to three anonymous referees, the editor Brett Christophers, Sergio Cesaratto, Yannis Dafermos, Sabine Dörry, Alexander Guschanski, Hannah Hasenberger, Annina Kaltenbrunner, Achilleas Mantes, Tom Purcell, Engelbert Stockhammer, Zsofi Zador and participants at the 47th Annual Conference of the Eastern Economic Association for helpful comments. All errors are mine.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.