Abstract

This paper investigates how blockchain technology may alter the defining mechanisms of residential real estate transactions in Sweden. It departs from the assumption that blockchain applications do not merely change complex socio-economic, organisational and governance arrangements of mature housing and mortgage markets. Rather, they may trigger resistance among incumbents in the current organisational model, which will drive incremental change. This analysis shows that housing transactions in Sweden are long and complex endeavours, underpinned by exclusivity, uncertainty and information inequalities. A public-private consortium led by Lantmäteriet – a Swedish government agency – has pioneered the use of blockchain technology for the conveyance of a house to address these deficiencies. This project has not moved beyond the proof-of-concept phase, while the socio-technical organisation of transactions has evolved. Insights from institutional and evolutionary approaches help conceptualise how technologically induced and qualitatively different structures and functional effects may change the way housing and mortgage markets will work, thereby highlighting both disruptive potentialities and limitations of blockchain applications for the legacy design underpinning the current Swedish housing transaction system. Following a forensic empirical approach, this paper dissects the organisational architecture, key practices and the linked network of actor groups running Sweden's property and mortgage markets. Results illustrate that understanding concrete blockchain-induced changes and their unintended consequences requires closer scholarly attention at the scale of actor networks, the types of knowledge and technologies, and the micro-geographies in which they are embedded. Such in-depth understanding enables better-informed assessments of the blockchain challenge for complex housing and mortgage markets.

Introduction

Real estate often constitutes the largest component of household wealth, and mortgage finance is the cornerstone of many financial systems in advanced economies (Christophers, 2021; Fernandez et al., 2016). Technological changes in the legacy infrastructure for housing markets could therefore have far-reaching consequences. Selling and buying property is often linked with high transaction costs, and much blockchain-related work – like that in Sweden – focusses on inefficiencies and high costs inherited from legacy routines and infrastructures. Indeed, transaction cost approaches are often employed to analyse and compare the efficiency of real property transactions across countries (Zevenbergen et al., 2008) and property registration procedures (World Bank Group, 2020), but also to explain the diversity of property rights in specific jurisdictions (Ekbäck, 2011). Blockchain enthusiasts, however, tend to underplay the fact that both cryptographic trust and interactive digital spaces of exchange enabled by them are socially embedded, spatially materialised and driven by conflicting interest and agency (Zook and Blankenship, 2018). As a result, the conclusions based on generalisations tend to omit that technology and social practices – steered by aligned forms of governance – may be intertwined in different ways in the contingent housing markets across different national jurisdictions. More specifically, the practices that define how rights are created and linked to land and buildings vary across jurisdictions and reflect the different legal families on which these lineages build (Proskurovska and Dörry, 2018). Two practices can be discerned, namely a recording and a registration procedure (Arruñada and Garoupa, 2005), which vary in how they deal with uncertainty in the transfer of property rights. Unlike the recording procedure, which merely informs the public about the transaction, a registration procedure as in Sweden follows the logic of prevention and strengthens the performance of a contract that results in establishing a valid property title (Bouckaert, 2010). Registration thus produces a constitutive effect and is a process exposed to tech disruption as discussed in this article.

With growing markets, however, both the recording system's inherent risks and conveyancing costs have increased (Limmer, 2013). Likewise, practices of creating and trading secured claims held by noteholders against borrowers, i.e. mortgages, differ across space and time (Ashton and Christophers, 2018; Blackwell and Kohl, 2018). It justifies the importance of empirically investigating how a state-led blockchain development may alter the established organisational architecture, i.e. shape, drivers and power configurations. This paper contributes to the debate about the direction and scope of the blockchain-induced transformation of housing markets by critically engaging with the case of Sweden, where a public-private consortium led by Lantmäteriet – Sweden's mapping, cadastral and land registration state authority – has pioneered the use of blockchain technology for conducting house sales (Bennett et al., 2019). Work on the blockchain application started in 2016 with a task force to develop and better understand the potential of blockchain to eliminate paper contracts, and to bring residential property transactions close to a fully digitalised workflow. Yet, despite a successful proof-of-concept, the project has not yet advanced further. In the literature, the scope of operational blockchain solutions for housing transactions has remained limited as it barely goes beyond securing real property registries and records, e.g. in countries with less mature home financing markets like Georgia or Ghana (Miscione et al., 2020). Blockchain has hence often been considered too complex and not suitable for transactions in mature markets in the near future (Baum, 2020; Higginson et al., 2019), while blockchain enthusiasts continue to grapple with the complex task of reconciling hidden and often opposing groups of actors (Proskurovska, 2021).

Empirical data informing the analysis were obtained from both desktop research and 19 semi-structured interviews conducted with representatives of Sweden's housing and mortgage market ecosystems. This included participants of the land registry in the blockchain project team as well as representatives of Lantmäteriet, a Stockholm brokerage firm, the Riksbank (central bank), SBA (Swedish Bankers Association), the UC (largest credit rating agency), Mäklarstatistik (Swedish Broker Statistics) and others. Importantly, interviewees were asked to (i) assess a flowchart depicting the housing transaction process that had been prepared based on a combination of desktop research and first explorative interviews prior to this research project, and (ii) identify particular situations in the organisation of the processes where they would anticipate change regarding the planned blockchain project. Results from this ‘forensic analysis’ (Ashton, 2009; Dörry, 2022) into the concrete organisational structures and routines enabled us to detect not only processes targeted by the blockchain application itself, but also to understand the logic of current business models along the (largely) opaque value chains crucial in the structuring and execution of the housing trade in Sweden. The overall empirical material is rich; here, we focus chiefly on depicting the processes that allow us to identify what routines and practices the blockchain technology could potentially alter, and – based on this assessment – to venture propositions about the implications on the current sociotechnical regime (e.g. Geels, 2002) that underpins the housing market.

The housing market is closely entwined with the state's monetary and fiscal policies, which is why we hypothesise that blockchain technology – in light of its institutional restructuring potential – has the capacity to redefine the long-established socio-economic land, property and consequently financial markets. Every year around 50,000 houses and 100,000 apartments are sold in Sweden, of which only a fraction consists of newly constructed properties sold off-plan. We therefore focus on the organisation of the trade of already built residential real estate, i.e. one- and two family detached dwellings and apartments owned directly. Homes owned indirectly, i.e. tenant-owner apartments, are beyond the scope of this investigation, given that Lantmäteriet does not have a mandate over the registration of this type of ownership, an important topic that will be addressed elsewhere.

The remainder of this paper develops as follows. The section Contextualising Sweden's housing and mortgage markets contextualises Sweden's housing and mortgage markets, engages with its specifics and the challenges Lantmäteriet's blockchain application aimed to solve. Sweden is the world's first and, so far, only country where a government agency has gone so far as to explore the use of the blockchain technology to power the entire lifecycle of a residential property transaction, outlined in the section The current socio-economic system. The section Conceptualising the technology-induced redesign of complex socio-economic systems employs institutional and evolutionary perspectives to help analytically guide and order the potential change processes of a socio-economic legacy system. The section Empirical insights into potential change processes dissects empirically the current processes to demonstrate where and how blockchain technology offers opportunities to address the various caveats within a publically governed system, which is juxtaposed with the implementation of a competing private initiative, the Tambur platform. Discussion and conclusion discusses and interprets the main empirical findings and concludes with a discussion of fruitful avenues of future enquiry.

Contextualising Sweden's housing and mortgage markets

As is the case nearly everywhere, the Swedish housing market has been growing almost uninterruptedly since the mid-1990s. Today, 64% of Sweden's population are owner-occupiers, with more than 80% having mortgage loans secured on their homes (Eurostat, 2019). In Sweden, the stable demand for homes is due not least to one of the highest rates of population growth coupled with low construction activity, which particularly affects the amount of available housing on the highly regulated rental market. Given this tense situation, an owner-occupier tenancy remains a sensible – and often the only – available option for many Swedish households.

As a result, house prices did not substantially fall in the wake of the financial crisis, picking up their steady growth with only a brief correction at the end of 2017 (SBA, 2020). The rapid increase in house prices and much slower growth of household income has created opportunities for households to reallocate parts of their additional equity (Li et al., 2020). While this concerns many national housing markets, up until 2016 no legislation required the amortisation of mortgage loans in Sweden. In effect, private borrowers rent their homes from their lenders paying only the (admittedly low) interest as opposed to the principal loan. Between 1995 and 2015, household debt rose from 90% to 179% of households’ disposable income (Hull, 2017). At the end of June 2020, the total residential mortgage lending amounted to 4,569bn SEK (SBA, 2020), or US$450bn, and banks primarily finance these loans by issuing mortgage bonds held by foreign (almost 40%) and domestic investors (20% by Swedish insurance companies). To ensure their compliance with existing regulations, their issuers must continuously monitor the value of the assets in the cover pool over its full lifetime (Elliot and Lindblom, 2017).

Further, mortgage lending is based on the market value of a property at the time of acquisition (FI, 2016). Between 2010 and 2017, one-third of mortgage borrowers in Sweden (866,075 households) pledged the same home as collateral to obtain additional credit by increasing the existing mortgage amount against an updated valuation (Li et al., 2020). Therefore, transaction data informs subsequent policies that directly affect the functioning of both the housing markets and home financing (Bjellerup and Majtorp, 2019; Hull, 2017). Since 2016, Swedish authorities have tightened borrower- and capital-based measures; and an improved monitoring of vulnerabilities and structural changes related to mortgage lending and residential real estate remains a priority (European Systemic Risk Board, 2019). This implies that timely access to this data describing housing market dynamics, and especially to the property purchase prices stated in the sales contracts, is vital for the sound functioning of Sweden's mortgage markets connecting borrowers to lenders and lenders to investors. The need to modernise the information infrastructure was a first motivation for the blockchain application led by Lantmäteriet.

Currently, there are several types of organisations engaged with the handling and/or circulation of the property sales contracts. One of them is Lantmäteriet, a public authority that collects and registers the evidence about real estate dealings such as sales deeds, which are recorded in the Real Property Register. Sales deeds have legal value and are enforced by the state (Jensen, 2004). Historically, this information infrastructure has developed alongside the bond-based mortgage type of home financing, which relies on public registries that ensure that lenders rank as higher-tiered creditors in the case of foreclosure (Blackwell and Kohl, 2018). The modern state of these records is a result of simplification and objectification processes through measures of standardising data collection practices, data categorisation, aggregation and, eventually, digitalisation originating in the 1970s (Husz, 2018; Papakostas, 2018). By 1995, paper-based real estate and population-related data was fully digitised. Today, Sweden's level of digitalisation is among the most advanced in the OECD countries. The governance of this infrastructure is consolidated at the national level and spread between public agencies that ‘favour silo-based approaches rather than inter-institutional co-ordination, alignment and rationalisation’ (OECD, 2019). It is based on a restrictive legal model to share fee-based data between public agencies: Public datasets could be made available to other organisations only if authority-specific procedural rules were fixed in a register statute (DIGG, 2018). As a result, Sweden is one of the few OECD states without a formal open data policy, another point that would have been addressed by the planned blockchain application.

Brokers and banks are further parties involved with the circulation of the sales contracts. Indeed, even though formally the sale of a house in Sweden is considered a ‘simple matter’ (Högberg, 2006) – legally, sellers and buyers can transfer a residential property on the basis of a single contract without involving a notary or a lawyer –, more than 90% of all property sales are mediated through a broker. Brokers must safeguard buyers’ interests. They help draft sales contracts and insure the validity of the transfer. Other brokers’ responsibilities include collection and verification of information, running ascending bidding auctions, which are the preferred way of selling existing residential properties but are not legally required, matching transacting parties and communicating with the seller's and the buyer's banks on their clients’ behalf. The latter usually happens when the buyer needs either to finance the house purchase, or the house has already been mortgaged by its current owner. The bank also needs the sales contract to originate a mortgage loan, which is essential evidence to help ensure a creditor's priority over the collateral in the case of foreclosure.

The complexity of the sketched transaction patterns is amplified by the fact that to be valid, the final sales deed still must come in paper form. It must identify the property, contain a statement from the seller that the property is conveyed to the buyer, the sale price and the wet signatures of both parties. Thus, a major goal of the new blockchain application was to eliminate the use of paper contracts to improve the process of property ownership transfer, which is, at times, as we will show below, non-transparent and inefficient.

The composition of the state-led consortium, introduced to better understand the potential of blockchain for real estate transactions, involved, when it was established in 2016, Lantmäteriet, Chroma Way (IT developer), two large banks SBAB Bank and Landshypotek Bank, and the telecom company Telia. Eventually, more parties joined, including Sweden's tax authority (Kairos Future, 2017). Together, they have designed, developed and tested a blockchain application for the sale of a home with a focus on learning about concomitant technical issues (interview with [5], 27/09/2019). The capability of the application relied on the existing, fully digitised public information infrastructure governed by Lantmäteriet (Bennett et al., 2021). Its functionality allowed digitising the entire house sales and mortgaging processes into one workflow, secured by a permissioned blockchain. Using smart contracts to orchestrate property transactions and generate claims to Lantmäteriet, however, allowed the buyer and the seller to interact directly, therefore reshuffling other established ecosystems, which threatened, for example, the privileged business position of brokers in the housing sales markets. To identify processes in the envisaged changes, we offer an empirical deep dive into the existing mechanisms and processes underlying the sales contracting.

The current socio-economic system

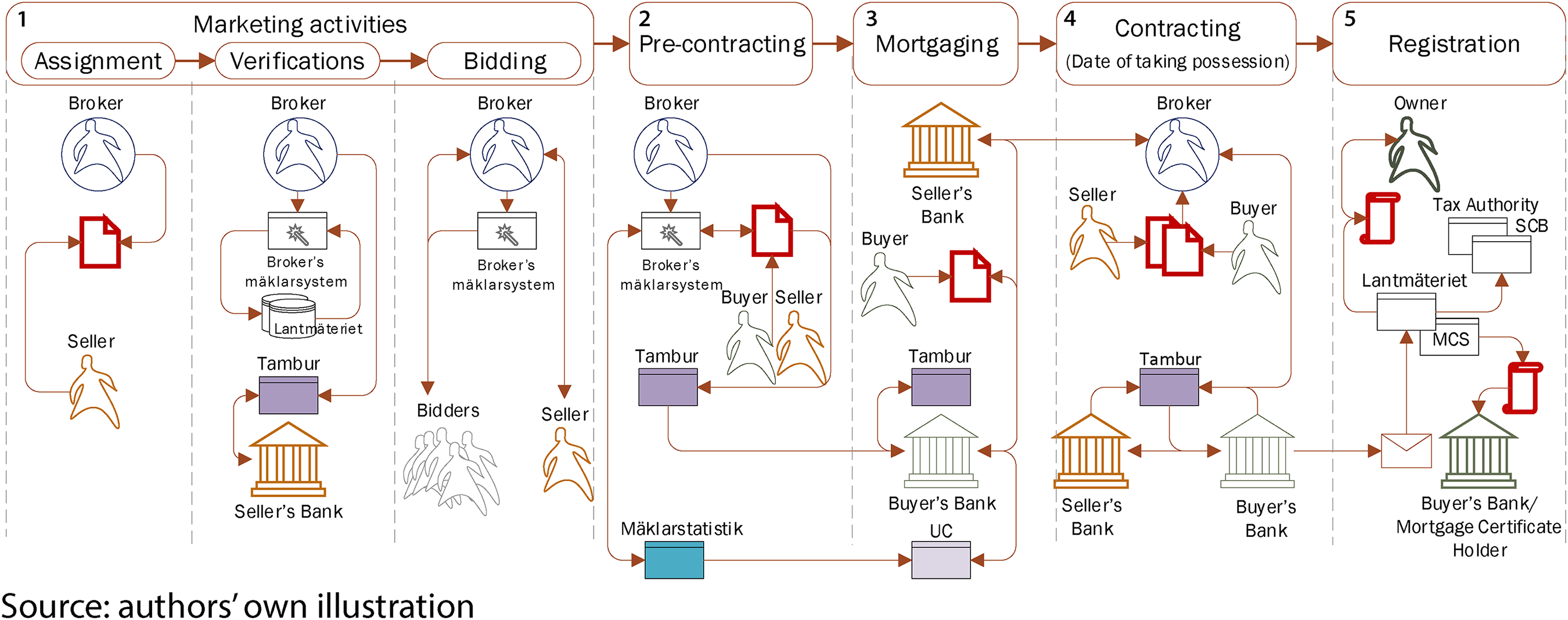

Under the current sociotechnical arrangements, to complete the sale, the new owner of a house must apply for the registration of the sale with Lantmäteriet, proving the latter with the deed of sale (DS) [Köpebrev] (ch.§ 1, Land Code), and paying the fee of SEK 825 and 1.5% of the purchase price, respectively. The workflow of a transaction can generally be divided into five phases (Figure 1): marketing activities (1), pre-contracting (2), mortgaging (3), contracting (4) and registration (5). While we discuss each phase in more detail in section 5, it is important for the argument here to mention that – during the registration phase (5) – Lantmäteriet verifies the application's validity and, if correct, grants the ownership title to the applicant within seven days. Lantmäteriet collects, processes and distributes the transactional data contained in the DS, which it then re-uses for statistical purposes and valuation processes. For example, every three years, Lantmäteriet conducts a mass valuation of real estate by using purchase prices from the DS needed to identify the taxation value for each real estate property on behalf of the Tax Agency, while Statistics Sweden (SCB) – the Swedish government agency – uses this data to compile the Real Estate Price Index or Consumer Price Index. Indeed, transaction data informs subsequent policies that directly affect the functioning of both the housing and home financing markets (Bjellerup and Majtorp, 2019; Hull, 2017). It makes timely access to this data vital for the sound functioning of these markets. Critically, a DS is usually signed only 3–4 months after the signature of the first, conditional sales agreement (CSA) [Köpekontrakt]. The CSA also specifies the selling price but is conditional on future events, e.g. on granting the mortgage and the transfer of funds. This not only creates a lucrative arbitrage opportunity for actors able to receive the data ahead of Lantmäteriet, including banks and brokers; the delay in the registration process has further implications.

The design of housing sales workflow (own illustration).

Lantmäteriet also registers mortgages via its Mortgage Certificate System (MCS) (Högberg, 2006). The MCS is both a register and a processing system for affiliated customers, i.e. banks and credit institutions, which help, for example, to reliably identify a creditor's priority over real estate securities. Security over real estate is created by pledging (a) mortgage certificate(s) (MC) [Pantbrev] for a specific amount in relation to the real estate property. Lantmäteriet issues MC upon request by the registered homeowner who can choose its face value freely but has to pay a stamp duty of 2% of that value. Issued MC can be passed on to the financing bank via the MCS. The registration of the pledge in the MCS turns a credit grantor (bank, credit institution) into an MC holder, whose priority over the certificate is determined by the registration date (Högberg, 2006). Upon repayment of the debt, the house owner can re-use the MC an infinite number of times to secure a new loan or to extract new equity, without additional stamp duty. The system is therefore instrumental in supporting the non-accessory 1 style of Swedish mortgages. Changes in fully digitised registries would still depend on the signature of the paper DS, on which the house owner's registration is based, and which, as Figure 1 shows, only happens at the very end of the transactional cycle. The Swedish blockchain application sought to address this problem, with implications detailed below.

Crucially, only the most recent applicant for ownership registration is permitted to apply to Lantmäteriet for the issuance of MC or the registration of a pledge (Högberg, 2006). In practice, however, the DS – needed to register the ownership – is signed only after the final payment is settled. It leaves the bank promising a mortgage loan and transferring the money before its priority over the collateral security is perfected with the MCS registration. Risk, then, becomes a function of time, but Lantmäteriet can protect the bank and the buyer by creating a pending registration of both the ownership title and mortgage, based on the CSA. Providing these pending registrations, Lantmäteriet also recognises the validity of the application. It assures both parties that there will be no legal obstacles to the change of ownership or the registration of the creditor's priority once the DS perfecting the sales is submitted to Lantmäteriet. In addition, it protects both the creditor and the buyer from unlawful sellers who may try to double-sell or re-mortgage their property.

In reality, only a small percentage of CSA is actually submitted to Lantmäteriet for the pending registration of an ownership. This poses a problem. In 2019, 90% of the 179,004 total applications for ownership registration were granted by Lantmäteriet. Yet a mere 2.37% of these were pending (email exchange with Lantmäteriet, Legal Division, 1/25/2021). Interview data suggest that this somewhat irrational behaviour can be explained by a range of (overlapping) factors, e.g. individuals’ deep trust in the state and the overall system, additional fees that pose an obstacle, or reluctance to publicly disclose details of a CSA. Indeed, the information contained in the Lantmäteriet registry is publicly available. Regardless of the cause, this implies that as long as the content of the contract remains private, the property owner is better protected than both the buyer and creditor (Arruñada, 2014). The blockchain technology with its smart contracts and novel ways of distributing transactional information offered a way to address these caveats in the system.

Conceptualising the technology-induced redesign of complex socio-economic systems

Blockchain, a type of distributed ledger technologies (DLTs), offers a novel way of recording and sharing timestamped and cryptographically secured data across multiple databases (Natarajan et al., 2017). The spectrum of DLT models and their designs is broad. They vary in their degree of centralisation, types of access, control and procedures for agreement consolidation, but are all designed to work as mediums of interaction between transacting strangers and help create verification records, i.e. cryptographic hashes, for digital documents. A cryptographic hash is a string of numbers generated from the content of digital documents that validates a document by matching its hash with a hash stored on the blockchain. As a result, a ‘truth’ produced by the document could be reliably established without revealing its content. In a similar vein, digital signatures are a means of verifying identity cryptographically. They prevent changes to the existing record without prior consensus through validation by authorised nodes. The validation of one agreement automatically triggers further action, which is a key point in relation to the case study at hand and known as a smart, or embedded, contract (Kairos Future, 2017). This functionality is believed to reduce information asymmetries and improve efficiency not only in real estate (Baum, 2017; 2020) but also in banking (Gozman et al., 2020) and land administration (Bennett et al., 2019). Indeed, information and information asymmetries constitute the very core of real estate markets (Garmaise and Moskowitz, 2004), and a multitude of business models (Spielman, 2016) exists relying on the ability of leveraging and mobilising information at the system's margins, which a blockchain can help reduce.

Yet, despite sparking much scholarly interest, especially regarding the technology's disintermediation promise and potentially reduced transaction costs (Wouda and Opdenakker, 2019), including less optimistic views on the application of the technology in real estate due to legal, technological and institutional constraints (Arruñada, 2019; Garcia-Teruel, 2020), scholars provide little evidence on the implications of the re-organisation of established socio-economic order with its specific legacies, routines and power structures. Blockchain solutions, currently being tested, for example, by central banks and newly created public cryptocurrency regimes, can follow opposing logics that guide their implementation: (i) to change an established system entirely and/or create a new system, or (ii) to leave the system intact and improve its efficiency. Sweden is largely following the latter. Given the sparse literature on organisational change through blockchain technology, we apply a guiding evolutionary-cum-institutional lens to order and analyse the processes visible in the proof-of-concept-stage.

Inevitably, simplifying transactions in the current paper-based contract system would eliminate a number of intermediaries who hold key positions as trusted third parties. This is why blockchain enthusiasts frequently compare embedded contracts to an institution, or a ‘trust machine’ (The Economist, 2015), that would enable information exchange to become faster, cheaper and more transparent. These economics-informed narratives usually depart from the assumption that low interpersonal trust and weak institutions result in high monitoring and control costs, which in turn reduce the efficiency of markets and prevent specialisation, and consequently the emergence and trade of more complex products and services (North, 1990). Further, however, North (1990) links difference in economic outcome to cultural and political contingencies, and therefore to the difference of institutions and their evolution in specific socio-spatial contexts. The crux of the matter lies in their legacies.

A blockchain potentially dis-intermediates and re-designs the established long transactional workflows embedded in the housing conveyance system, thereby inevitably challenging specific roles and privileged positions of actor groups and, unsurprisingly, creating resistance. Important actor groups in the example at hand are brokers and banks. They have benefitted from arbitraging, which relies on the creation and exploitation of difference, here access time to the transactional data that aids the manipulation of the micro-geographies of profits (see Dörry, forthcoming) through controlling the sharing of information critical for Sweden's housing and financial system in general. Put differently, difference creation is actively designed via legacy routines and social structures that have stabilised – and institutionalised – the system to a high degree (Aoki, 2007; Buitelaar et al., 2007), while institutions themselves are an outcome ‘of intentional action and unintended consequences of human behaviour’ (Essletzbichler, 2009: 161). The technology-based change processes introduced by the consortium were designed to re-organise these routines and structures to address the long-standing and increasingly harmful issues of inefficiency and non-transparency, and in doing so, to institutionalise a re-design of the system in a top-down process and a public-private environment. Co-evolving new technology and new institutional structures will therefore design also new routines, i.e. social practices and organisational capabilities, which determine what actors do and how productively they do it (Nelson, 1995). A variety of institutional arrangements is thus necessary to secure and alter social relations (Allen, 2013) as performed by private and public actors in Sweden's housing sales and financing markets. Arguing from an evolutionary and institutionalist perspective, Lantmäteriet is not only a public organisation that has set rules to facilitate the system in its functions. It is also an enabling information infrastructure, on which a range of interlocked socio-economic systems (housing sales, home financing, taxing, etc.) with constraining and aiding, but overall stabilising institutions have developed (cf. Amin, 2001).

In this sense, institutions are ‘carriers of history and keep information stable long enough for selective forces to operate’ and ‘together with quasi-fixed elements, such as firm and organizational routines pass on information over time’ (Essletzbichler, 2009: 161). Therefore, institutions and the formation of routines change usually only slowly and incrementally. Sudden systemic change as that of Sweden's housing sales markets – even though change concerns just parts of the system's routines – thus requires an in-depth understanding of its micro-geographies (cf. evolutionary theorists, e.g. Nelson and Winter, 1982), including newly evolving governance regimes that are subject to change. At the same time, these micro-geographies provide the organisational space in which the processes of institutionalisation occur (Buitelaar et al., 2007), yet, as Furubotn and Richter (1991) aptly pointed out, the emergence of particular institutions is itself subject to transaction costs.

The fact that the process of (re-)institutionalisation is guided by institutions (Hodgson, 1993), and that institutional change has a cost itself, may steer institutional evolution in a specific direction (North, 1990). Consequently, institutions may well ‘persist if they serve the actors or coalitions in power’, regardless of their efficiency (Buitelaar et al., 2007: 894). Below, we add empirical life to this conceptual framework, thereby highlighting how resistance, (high) costs and unintended consequences may have influenced the decision not to proceed with the blockchain application.

Empirical insights into potential change processes

Proof-of-concept

Two major parts constitute the application, (1) a private blockchain run by a group of public and private units, and (2) a software application that manages contracts controlled by and recorded on the blockchain. The contract was running on the client [participating] side, while the verification records were recorded on the blockchain, as one interviewee astutely explains: [T]he blockchain is a message base. (…) We store [digitally] signed messages [exchanged] between different parties, [e.g.] ‘I want to sell this house’, (…) ‘here are the mortgage deeds’, ‘I hereby commit [to transfer] the money’. (…) So you are vouching for legally binding [things]. (…) And what you can get with signed statements, whether it is run by a company or on the blockchain, you can see what everybody has signed and, more importantly, what they have not signed. (Interview with [1] 24/09/2019)

Thus, the actors’ power to act, the scope of available actions, and actors’ access to data were constrained by their roles in this first phase. Each role was strictly defined and delimited by the blockchain application and its architecture. Vitally, and as outlined above regarding the function of smart contracts, a fulfilled pre-set condition triggered the automatic execution of consecutive steps. Hence, the registration of a pending ownership title and pending mortgages was executed upon the signature of the CSA, free of charge.

The test bed was ready in 2018; a demo transaction was conducted in real time. The property transaction was governed by pre-programmed procedures enacted and approved by a ‘group of nodes’, comprising public and private actors. With the majority of interactions occurring in Lantmäteriet's digital space created by the application, node participants can interact directly. Once the Telia ID system issues a digital certificate and records it on the blockchain, node participants are able to choose their role, e.g. being the buyer or the broker. Telia ID allows controlling and tracking ‘who did what’ in a shared ledger that connects action-with-actor. As soon as the system receives a required signed message, it records its verification and moves the workflow forward. Sellers would have the choice of either initiating the sales contract on their own, or inviting a broker to help via the certificate server. Moreover, since sellers can transact on their own, and buyers can access the application, nothing seems to prevent the seller from receiving offers from potential buyers directly. The signature of a CSA, as well as the mortgage contract, would automatically trigger the pending registration with Lantmäteriet. The possibility to encrypt [parts of] CSA preserves individuals’ privacy while making evidence contained in the Lantmäteriet registry public: The actual content of the CSA would be accessible only to those who have the right key to decrypt it.

This functionality gave the project a serious spin. First, it would unite all the transacting parties in one single digital space and strictly order the sequence of interaction. The resulting transparency would allow the existing ‘complex process for agreement’ to be simplified – devised by sellers, buyers, brokers and banks in order to deal with the uncertainty that results from the current registration time lag (Kairos Future, 2017). Second, it would speed up the availability of the transaction data for Lantmäteriet and therefore its ability ‘to know if there is an agreement and (…) the price because they levy taxes on it’ (Interview with [1]).

Under this new organisation, Lantmäteriet would not only be present in the transaction from the very beginning, it would also become a member of the housing market ecosystem as ‘the sole key provider [with] (…) the master key. [Lantmäteriet] would have pretty much all the power (…) [to decide] who would be in (…) [the system], who the nodes would be, who can read the information, who can use the information, who can sign everything’ (Interview with [2], 19/09/2019).

However, and notwithstanding the fundamental change and the resulting possibility of obtaining timely insight into housing markets dynamics, it would be difficult to create leeway in policy-making such as taxation. One obstacle is the current lack of a legal framework that would enable the seamless sharing of public data between public actors, as well as their reliance on automated processes. Indeed, as explained above, the sharing of data with other public organisations is usually subject to complex public governance arrangements, which, in addition to other matters, affects their revenues as profit centre-structured organisations (OECD, 2019). Interviewees suggested that Lantmäteriet – currently the sole authority of Sweden's land registries – would need to cede control, but ‘then the banks would also become a part of [the system] (…) And to do that we have to change the way we work together’ (Interview [2]). While under the current arrangements the scale-up of the application is nearly impossible, solutions are being worked on (DIGG, 2019).

Despite successful testing of the application, which attracted international attention and resulted in further collaboration (IDB, 2019), Sweden has not yet implemented it. A popular explanation is the missing legislation that would make digitally signed DS equivalent to hand-signed paper DS (Kairos Future, 2017; McMurren et al., 2018). However, it remains unclear how the current economic organisation of Sweden's housing market would change and how this alteration would affect the entangled value chains once the system had been transferred to a blockchain that commands the entire workflow of a property sale in reality. Other, less anticipated and unintended consequences in related social systems may thus occur.

Challenging brokers’ privileged roles and functions in the system

Brokers often use dedicated information management systems, generally dubbed Mäklarsystems, to facilitate and manage transactions. Mäklarsystem providers like Mspec and Vitec usually deliver them as subscription-based services that help brokers to organise and coordinate the sales workflow, run auctions and generate and store contractual agreements, bidding histories, etc. (see Real Estate Brokerage Law, effective since 2011). Mäklarsystems can receive and respond to requests via Application Programming Interfaces (APIs), which enables them to communicate with other transaction parties’ digital applications that leverage each other's data. This includes Lantmäteriet registries, which a Mäklarsystem can access when a broker wishes to verify the property information, as well as the Swedish Broker Statistics, an organisation that collects contractual data from the Mäklarsystem once brokers have marked a CSA as signed.

A current project seeks to integrate Mäklarsystems with a new (private) platform, Tambur, to help facilitate the broker-bank transactions. Tambur was launched only a few months before the Lantmäteriet blockchain application was tested live in 2018. Having been developed by the largest Swedish credit rating agency, UC (since 2018 part of Asiakastieto Group, currently Enento Group), in cooperation with SBA and eight other banks, it is now open to other lenders. Any licensed broker can register for free with its BankID, a widely applied private identification solution in Sweden (Husz, 2018). The platform defines the order of exchange in broker-bank interactions during a property sale, hence prudently structuring how and when information is exchanged. By August 2020, almost 80% of all Swedish brokers had registered with Tambur; about 120,000 transactions were handled on the platform during the previous 12 months (Tambur Insights, August 2020; email exchange on 08/09/2020). Importantly, both UC Property Valuation and Tambur are private firms belonging to the Enento Group. By wedding their services under one roof, the group has gained substantial competitive advantage.

As suggested, the workflow of a transaction among the involved parties can generally be divided into five phases (Figure 1). Since we seek to understand a blockchain's benefit and challenge to the technical workflow in an established socio-economic system and the potential re-organisation of established actors and actor-relationships therein, the following explanations must necessarily be of a technical nature. Each phase (Figure 1) involves a signature of different contractual agreements to enable the sale to move forward. Brokers structure almost every such encounter, a provision for sustaining their value chain, position and income sources. Further, value chains are hinged on the indispensability of a broker's involvement, centred on two circumstances: (1) the diminished ability of the registrar – Lantmäteriet – to strengthen the performance of the ownership transfer contract earlier in the process, and to protect the transacting parties by issuing pending registrations, and (2) since the appearance of Tambur, the complete exclusion of buyers and sellers from broker-bank interactions.

The first marketing activities phase consists of three parts (Figure 1). During the assignment part, the seller grants the broker the power of attorney, so that the broker can collect and verify related information on the seller's behalf, e.g. ownership rights and outstanding mortgage(s). The broker can thus interact with the seller's bank via Tambur by ‘using his or her BankID [that] is traceable. So we always know exactly who did what’ [interview with [4], 18/09/2020].

The broker then clears the property for sale, advertises it and, after the public viewing of a house, the bidding kicks off. Bids are non-binding; anyone can participate, sometimes anonymously. The broker collects the bids and informs both the seller and bidders throughout the process. 2 An auction stops when the seller accepts an offer. Auctions are usually fast, competitive and stressful endeavours; the average time of a single-family house being on the market is 3.7 days. ‘Bidding wars’, i.e. where the winning bid ends far above the listing price, have become increasingly common in large Swedish cities (Hungria-Gunnelin, 2018). The broker, like the seller, is a direct beneficiary of the high prices as fees depend on the purchase price of the property (2–5%). Often, the broker influences the seller by giving advice as to which bid to pick. While this is a common mechanism in all forms of brokerage, it nonetheless creates information asymmetries between the broker, the seller and the buyer – with the aforementioned price arbitrage advantage for the broker based on time differences. By exploiting this difference, brokers can influence the distribution of the sale prices and control the time a property is on the market, therefore further aligning the auction outcome with their commission structure (Hungria-Gunnelin, 2018). The Mäklarsystem facilitates the operation of this chain of events, along which the broker communicates with the bidders or even broadcasts the state of the auction on property advertising websites. The more bidders a property attracts, the higher the expected selling price. This fierce competition also legitimises the broker's pressure exerted on the bidding winner to commit to the purchase on the very same day their bid has been accepted (Hungria-Gunnelin, 2019). It gives buyers little time to contact their bank and ensure that the property is accepted as collateral to be granted a mortgage, but makes brokers, who reduce uncertainty by adequately formulating contractual clauses, indispensable in the process.

As soon as the broker signs a CSA in the Mäklarsystem (pre-contracting phase 2, Figure 1), its transactional data becomes available to Swedish Broker Statistics, querying it ‘every four hours throughout the day' via API (Interview with [3], 15/09/2020). Although the purchase price in the CSA may differ from the eventual amount paid and later registered with Lantmäteriet, ‘it shows the temperature of the market when the contract is signed because that is when the money is supposed to be paid’ (Interview with [3], 15/09/2020). Swedish Broker Statistics thus allows insight into the residential real estate market dynamics far in advance of the public authorities (Mäklarstatistik, 2021), e.g. Lantmäteriet. This preview enables private service providers such as the UC Property Valuation service to leverage data to conduct almost real-time market assessments of properties’ market value and produce various statistics and indices ahead of the public statistics by SCB (Bjellerup and Majtorp, 2019).

During the mortgaging phase (phase 3, Figure 1), the buyer's bank relies on UC or other credit agencies services to devise the mortgage contract in compliance with the existing requirements (see Hull, 2017). This involves, for example, the valuation of the property and the identification of the buyer's credit ratings.

Although the majority of applications to register ownership and almost all applications to register mortgages are submitted by proxies, e.g. brokers and banks, they have less leeway when it comes to the pending registration. To reiterate, CSA are hardly ever registered with Lantmäteriet (despite being recognised by it). Therefore, despite having one of the most efficient registration procedures in the world (World Bank Group, 2020), Lantmäteriet updates its records only months after a sale. This delay creates lucrative arbitraging for those who have access to the CSA and the transactional data earlier in the process for purposes of timely analysis. By being obligatory passage points, brokers and their Mäklarsystems define the core elements of these processes in the current organisational design. The large-scale failure to register a pending mortgage with Lantmäteriet and the resulting uncertainty, more acute even when a tenant-owner apartment secures a mortgage loan, further explains the central role of Tambur in (re-)organising the broker-bank transactions. We stressed already the Mäklarsystems’ importance as information management systems for brokers through which they share contractual data with the Swedish Broker Statistics. In the future, Mäklarsystems can be integrated in the Tambur platform (Figure 1, phases 1–4).

Although the access phase (the buyer takes possession of the property) starts roughly three months after signing the CSA, Tambur can unmask unlawful activities, including double sales from creditors or brokers, reduce information asymmetries, pre-set a workflow order to accelerate the assessment of individuals and properties for loans and collaterals, and coordinate the drafting of all documents required for the final transfer with the bank. Lantmäteriet is unable to perform these activities. As a result, once the day of taking possession of the property arrives (Figure 1, phase 4), signatures on the cash settlement, the DS, the money transfer and the mortgage certificate will proceed seamlessly and immediately.

While the Tambur platform solves a range of information asymmetries, it solidifies the key role of the broker in the transaction and manifests the transactional order through the design of this structure. This order, however, is vital not only to organisations hinging their services on the existence of Swedish Broker Statistics but also to the UC's own services, i.e. Property Valuation: Valuations are based on the sale prices and other key data widely applied by the banks to establish property market values to originate mortgages. Tambur not only provides the UC with early information, e.g. the volume and time of ongoing transactions, it also insures that the users of the Property Valuation services comply with regulations (EBA, 2020). Brokers visit properties and value them prior to advertising. Visits to the property precondition collateral valuations considered by the EBA, which statistical models alone are unable to provide. Therefore, by obliging the broker to supply valuations when requested to do so by the bank, the Tambur workflow also helps UC to secure its market share.

Discussion and conclusion

We have empirically investigated how the well-established socio-economic organisation of the mature Swedish housing and mortgage market may potentially be affected by a blockchain-based redesign. For this reason, we carefully dissected its organisational architecture, its actors and agency, and key practices and routines that link Sweden's housing to financial mortgage markets; in short, its micro-geographies. Empirical findings have illustrated that – contrary to what is often claimed (see Högberg, 2006) – real estate transactions in Sweden are long and complex endeavours underpinned by exclusivity, uncertainty and information asymmetries. The use of paper contracts along with digital technologies plays a key role in their structuring. Against this background, the forensic empirical drilling conducted here has helped evaluate not only the government's effort to improve the situation but also clarified how such improvements would affect key actor groups and their agency in the established system.

Overall, empirical evidence suggests that the adoption of the Swedish blockchain application for real estate transactions could, first, eliminate systemic inefficiencies by including both the buyer and the seller into transactional process, which would potentially challenge the central role of brokers and the organisation of the ascending bid auctions they conduct. Second, by automating pending registrations, it would already at an early stage of the transaction create a reliable link between the creditor and the real estate collateral, therefore reducing uncertainty and enabling state actors to access real-time market data and information vital to managing risks. Third, by offering an alternative digital identification solution to BankID, the application would challenge the banks’ dominant role in official digital identification. Fourth, the reinforcement of Lantmäteriet's role would – by giving it a strategic central role in the housing and mortgage market ecosystem itself – alter the governance of real estate transactions and the existing housing and mortgage market order, which would require further shifts in current governance arrangements. At the same time, Tambur – the new private platform developed in parallel to the government's blockchain application – has indeed successfully established a tech-driven organisational re-design, thereby not only ensuring the future significance of brokerage and related services in the value chain, but also shifting the direction of the system's potential change.

From an institutional perspective, the described power struggle between vested private interests to resist, defend and admittedly arbitrage the current system on the one hand, and a more transparent – public – governance information system crucial to improving the shortcomings of the current housing sales system linked to fiscal and monetary spaces and risks, may point to strong resistance against change. Not surprisingly, a new blockchain-based system would have altered the balance of power between actor groups and their agency and would have transformed Lantmäteriet from merely a registrar into the governor of a more inclusive, new digital space. The popularity of Tambur suggests such resistance from within the system defined by vested private interests; evidence that the micro-geographies are the organisational space in which the processes of (re-)institutionalisation occur and that the emergence of new institutions may come with high transaction costs. Nevertheless, the position of private firms will remain relatively stable. Moreover, as legislation to recognise digital signatures for real estate transactions is on hold, we can conclude that, for the time being, the incumbent institutions will not only remain largely unchallenged. Rather, they will continue to solidify the system's configuration and further serve the actor groups in power, mainly banks and brokers, as Tambur has indeed addressed some of the systemic inefficiencies with which they exercise more control over the modalities of information sharing, among other things.

We expounded how risk is a function of time when explaining the long-time lags for Lantmäteriet to receive much-needed housing market data on which national economic forecasts and tax calculations by other public institutions rely. Indeed, the new blockchain system would rather replicate established institutions and keep information stable enough for established private actor groups, now including Tambur, brokers and their Mäklarsystem to operate. Thus, the window of opportunity actively opened by a state agency to address systemic inefficiencies with the help of blockchain technology, and specifically across the mainly public levels in the organisation of Sweden's housing trade market, seems to have closed for now. In this regard, our empirical findings align with critical housing studies that engage with the digitalisation of real estate, thereby proving that realising the social restructuring potential of blockchain is not a given but subject to intense struggle (Fields and Rogers, 2021). Actively changing the micro-geographies of such crucial social systems like that of Sweden's housing trade and financing is inevitably interlinked with alterations at the meso- and macro-levels.

Finally, we would argue that blockchain could alter the defining mechanisms and processes of residential real estate transactions. Indeed, even if not adopted, its capacity to simultaneously connect and disrupt connections between both public and private parties across sectors and domains creates dynamics that challenge complex socio-economic organisation of mature housing and mortgage markets. As empirically demonstrated, attempts to infer the impact of blockchain solely from technological capabilities or conventional business analysis that require delineation of operational, often siloed, domains focused on the imaginaries of its developers or users (Shaw, 2020) may not only obscure the true extent of the networks of actors, types of knowledge and technologies that they are designed to disrupt ( Proskurovska, 2021). Rather, such attempts may hinder a more in-depth understanding of the struggles, unintended consequences and new uncertainties for the system associated with this change.

Fundamentally, this research suggests that to better understand the shape and the direction of evolving processes driven by blockchain, attention must be paid to the context and contingencies of markets and, in particular, the embedded micro-geographies where actual change occurs. It underlines the importance of the ongoing digital transformation and invites scholars to take this opportunity to further unpack the actual organisation and practices through which, ultimately, labour, land and urban fabric are transformed into a multiplicity of commensurable financial assets.

Footnotes

Acknowledgements

The authors would like to thank Mr David Magård for opening up the Swedish blockchain ecosystem to them.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Research Fund (FNR), Luxembourg under Grant “Applications of Blockchain Technology in Land Administration Systems” (ABTLAS), 13275702.