Abstract

This article combines a fiscal sociology framing with value theory in the classical tradition to yield a composite lens through which to examine the relation between Global Value Chains, Global Wealth Chains and the tax state. It has specific regard to the ongoing crisis of tax states globally, as corporate profits go undertaxed. In summary, the argument is as follows. Although capital and the state are both primarily in the business of capturing value from Global Value Chains indirectly (i.e. otherwise than through ownership of means of material production), labour in Global Wealth Chains has a dual role of (i) suppressing the profitability associated with material production in favour of returns from intangibles and (ii) suppressing the corporate tax take. It therefore simultaneously constitutes capital's instrument of value capture, and its instrument of supremacy in its contestation with the state over the proportion in which value capture is shared between the two. Better-paid labour associated with value capture on the part of capital (i.e. better paid Global Wealth Chain labour) is predominantly located in wealthier states, giving those states an alternative source of revenue and consequently giving them a reason for maintaining a global order in which capital has supremacy over them in the contestation over value capture from Global Value Chains. Further, these dynamics are in a feedback loop which serves as a countervailing tendency staving off a structural crisis of capitalism, and that feedback loop is a core driver for today's crisis of tax states.

Introduction

Untaxed corporate profitability is a defining phenomenon of our times. We live in a world of widespread austerity onshore (Ortiz and Cummins, 2019) while vast profits accumulate untaxed offshore (Tørsløv et al., 2021; Garcia-Bernardo and Janský, 2021). This problem has been high on the agendas of G7 and G20 meetings for a decade, and relatedly a major programme of international corporate tax reforms has been conducted by the OECD, in an initial phase known as ‘BEPS’ (Base Erosion and Profit Shifting) which concluded in 2015, and a second phase known informally as ‘BEPS 2.0’, which is ongoing.

From the beginning, the problem has brought to the fore difficult questions to do with immateriality in production. The BEPS process evolved out of an existing project to review transfer pricing rules as they apply to intangible assets, and BEPS 2.0 is fundamentally about the failure of the international corporate tax system to capture profitability within the digital economy. Accordingly, throughout the process, there has been an implication that the problem lies outside the sphere of material production; that there exists a problem of allocating between states (and away from offshore) the disproportionate profits that today accrue otherwise than by reference to production as classically understood (Quentin, 2021).

It is deeply unfashionable in disciplines which consider questions of tax to view relations between material production and the rest of the economy as being structural, in the way that a political economist in the classical tradition might. And so, while there is a vast and growing literature on today's problem of untaxed corporate profits, scholars have not looked directly and with an established set of tools at perhaps that problem's most obvious feature: that it seems to exist in blissful isolation from the savage inequalities, environmental degradation, tendency to conflict, and other messy features of the global network of material production that lies behind the contents of the shopping baskets of the Global North.

This is not to say that scholars are unaware of international tax phenomena connecting inequality with materiality. It is well known, for example, that wealthy countries can rely to a substantial extent on taxing the salaries of armies of well-paid individuals predominantly working outside the sphere of material production, while lower-income countries will be placing greater reliance on the taxation of physical commodities, e.g. in the form of consumption taxes, trade taxes or resource royalties (Bird, 2013; Belsey and Persson, 2013; Barma et al., 2012). Indeed these sorts of readily observable asymmetries, where a position on an axis of materiality seems to correlate with a position on an axis of inequality, form the background to a wealth of academic and institutional literature on the fiscal problems faced by lower-income countries (see e.g. Tanzi and Zee, 2000; International Monetary Fund, 2011; Mascagni et al., 2014; Moore, 2015; Mills, 2017; Moore et al., 2018).

What is missing from the literature on global tax issues, however, is express recognition that those asymmetries spring from a fundamental analytical distinction to be drawn between production as a material process and the rest of the sphere of market relations. More specifically, what is missing is an approach that takes as its starting point that the proliferating structural contradictions of actually existing capitalism, including the problem of untaxed corporate profits in the immaterial economy, all themselves unfold from the central conjunction of materiality and inequality that is to be found where value in the form of means of production valorizes itself through the exploitation of human labour. A Marxist approach, in other words. And it is the aim of this article to sketch out what the elements of such an approach might look like.

The article proceeds as follows. Sections 2 and 3 set out (respectively) the value theory and the international fiscal sociology which provide this article with its composite conceptual framework. Section 4 deploys that composite framework to develop an argument regarding the global contestation over revenues between capital and the state which has three elements, viz.: (i) while capital and the state are both in the business of capturing value from production indirectly, intangible assets have a dual role of suppressing the profitability associated with material production and suppressing the corporate tax take, simultaneously constituting capital's instrument of value capture, and its instrument of supremacy in its contestation with the state over the proceeds of value capture; (ii) better-paid labour associated with value capture on the part of capital is predominantly located in wealthier states, giving those states an alternative source of revenue (i.e. the taxation of that labour) and consequently a reason for maintaining a global order in which capital has supremacy over them in the contestation over revenues; and (iii) these dynamics are in a feedback loop which serves as a countervailing tendency staving off a structural crisis of capitalism, and that feedback loop is a core driver for today's crisis of tax states. Section 5 concludes with some (necessarily utopian) policy recommendations.

The analytical building blocks for this argument are Global Value Chains and Global Wealth Chains which (if disentangled along lines that classical value theory would suggest) constitute an emerging framework for addressing materiality in the global production network. It is to the initial step of disentangling them that we therefore turn in the subsection that follows.

Value creation and value capture in the global production network

The Global Value Chain (GVC) analytic follows production processes from raw materials extraction to the consumption of goods and services, taking in the entire spectrum of possible relations between chain nodes from being under common control within an MNE, through various alternative governance mechanisms, to contracting in an open market (Gereffi et al., 2005). The Global Wealth Chain (GWC) analytic follows profits from business processes to the ultimate beneficial owners of assets, often along paths that minimise exposure to tax, regulation and accountability (Seabrooke and Wigan, 2014).

Analysing the entanglements of GVCs and GWCs requires a position to be taken on the role of intangible assets. If one were to adopt what might loosely be classed as a ‘subjective’ approach to value, for instance in accordance with the dominant marginalist school of economics (or, arguably, the ‘value-form’ school within Marxist political economy), one would be likely to treat business functions which give rise to intangible assets as value-producing, in which case those business functions are best characterised as GVC nodes. By contrast, if one were to adopt what might be labelled an ‘objective’ approach to value, for instance in accordance with the ‘classical’ value theory of Smith and Ricardo (and also Marx insofar as he may be interpreted as working within the classical tradition), one would be likely to establish a ‘production boundary’ (Boss, 1990; Mazzucato, 2018) around material production, and place intangible assets in the GWC alongside such phenomena as debt and real property regimes. Between these two poles, within the Marxist tradition at least, is a (highly contested) compromise stance that characterises some forms of labour in immaterial production as productive of value but not others (Mohun, 1996).

In the classical tradition, the purpose of the concept of value is to account for capitalist surplus, which confronts us simultaneously as a cash surplus in the form of profit and as a physical surplus in the form of more commodities being produced than are used up. A distinct concept of value is required in this tradition because the commodities constituting the physical surplus are heterogeneous, and so (in order to make the specifically physical surplus as amenable to quantitative analysis as the cash surplus) a property must be attributed to them which makes them commensurable notwithstanding their heterogeneity. The rootedness of the classical perspective in this central phenomenon of physical surplus means that in the classical value-theoretical framework all labour in immaterial production is ‘unproductive’ (in the sense of being unproductive of value), however useful or profitable its output. This is because it is not meaningful for immaterial products to say of them that more is produced than is used up.

That strictly classical approach is adopted here in order to brings analytical clarity to the entangled relation between GVCs and GWCs. The consequence of adopting it is to distil the GVC axis down to the sequence of material production processes leading to the consumption of goods and services, and place all of the remainder of today's financialised, intangibles-oriented business processes in the spaces described by the GWC. To do so appears to be consistent with an emerging consensus, at least among some GWC scholars. ‘Value’, as the leading scholars in the GWC field put it, ‘requires […] the transformation of physical states’ (from the introduction to Seabrooke and Wigan, 2022, foregrounding in this context analysis developed in Quentin and Campling, 2018; via Coe and Yeung, 2019; cf Marx, 1976, 133 on the ‘reordering of physical matter’). This approach is also (while highly controversial within the Marxist tradition) consistent with at least some contemporary Marxist thinking with regard to the commodification of knowledge and information (see e.g. Rotta and Teixeira, 2019; see also Marx, 1969, 268 & 353).

It should be emphasised that the analytical step of placing business functions which produce intangible assets in the GWC as opposed to the GVC yields a huge transfer of the labour element of the global production network into the GWC (as compared to a narrower conception of GWCs as being primarily to do with, say, certain elite finance and advisory sector functions). We are talking here about the workforces of the most ‘value adding’ business functions of many of the world's most profitable businesses. In this analysis, those business functions do not create value; they serve to effect the capture of value, whether by enhancing the market footprint of goods and services physically produced by the firm (e.g. branding, marketing), capturing value by interposing the firm between producers and consumers (e.g. ‘platform economy’ and social media firms), or bringing about the preconditions for the exploitation of formal intellectual property monopolies in the context of physically produced goods and services (e.g. R&D, design).

Accordingly, understood by reference to the famous ‘smile curve’ schematic of value added in GVCs (OECD, 2013a; Meng et al., 2020), the standpoint adopted here is one whereby the value in GVCs is entirely created at the bottom of the curve, where the classically recognised factors of production are situated and physical surplus arises. By the same token, the functions up the sides of the curve (R&D, branding, design, marketing &c) serve to determine which firms get to enjoy the proceeds of that value-creation in the form of profitability. That low point at the centre of the smile curve, where comparatively low levels of value added are associated with activities within the classical production boundary, may be thought of as being suppressed to its position by mechanisms of value capture, while the value added associated with those mechanisms of value capture rises up the sides of the curve accordingly.

How does it make sense to say that the incredible creativity and skill that go into producing intangible assets serve merely to capture value created by workers doing cheap drudgery elsewhere? Marx pre-empted this objection to the classical approach to value by deploying a vivid analogy – that of a match lighting a fire. The fire's heat is caused by the match but the amount of heat generated by the fire comes from the amount of fuel thereby caused to burn (Marx, 1978: 207–8). In the same way, the fact that a thing fetches a price in markets is caused by the desirability or utility of a thing, but the value it possesses is exclusively a function of the extent to which it predicates the material resources (i.e. living labour, and means of production which is dead labour) deployed in the circuits of production from which it comes. The key points for present purposes (deploying this analogy) are that in today's global economy there is a lot of investment in matches, and a firm can capture the heat without having to supply the fuel. And even where it does supply the fuel, it is the investment in matches that is nonetheless commercially significant.

It may easily be recognised that returns attributable to material production are suppressed by the revenues of proprietors in other asset regimes such as debt and real property. The analytical step being taken here is to extend that logic to intangible assets. In the case of debt and real property, profitability is suppressed by actual payments to the proprietor in the other asset regime in the form of interest or rent, and of course this also sometimes happens in the case of intangible assets in the form of royalties, fees, commissions and so on. Often in the case of intangible assets, however, the suppression takes place indirectly through market power, one way or another. If material commodities struggle to reach their consumers except via spheres of market activity where intangibles reign, actors in that sphere (whether or not they are the same actor that physically produces the goods) are going to be taking a large cut (Baglioni et al., 2021). The phenomenon is one whereby the value is created at one node in the network but it accrues as profit in another (Starosta, 2010). And this happens worldwide across the entire network of global production (Hadjimichalis, 1984; Suwandi, 2019; Hickel et al., 2022).

It would of course require a separate article in and of itself to elaborate on prevailing business models in a variety of sectors to set out how this works in practice across the global production network. And the nexus of intangible assets and market power (or, alternatively conceived, rent extraction) is in any event variously explored in the wider critical value chain literature without intangibles being wholly ruled out as factors of production (e.g. Davis et al., 2018; Durand and Milberg, 2020). The purpose here operates on a more theoretical level, however, than to illustrate how value creation may be understood as being exclusively the preserve of material production in the context of specific business models. It is to elaborate on certain structural implications that emerge as between capital and the state, if one treats that axiomatic stance not as an arbitrary choice, but as consistent with principled value-theoretical foundations.

The tax state on a global scale

Fiscal sociology: The tax state in isolation

The analytical step of disentangling GVCs and GWCs along the lines of the classical production boundary has important implications for how we conceptualise the state. In the classical tradition, the labour of servants of the state is another form of unproductive labour (Marx, 1969, 160). In the popular orthodoxies of today's neoclassical era, too, it is believed that state expenditure is unproductive, albeit in the general, pejorative sense rather than a technical value-theoretical sense: state expenditure is popularly contrasted with the activities of the private sector which is believed to be inherently productive (Mazzucato, 2018: xvi-xvii). There exists a school of thought that counters this popular contemporary orthodoxy by arguing that through its causal (or ‘interdependent’) relation with the activities of the private sector the state, too, should be considered to be productive of value (Boss, 1990). The analysis adopted in section 2 above, by contrast, has the consequence that, rather than including the state in the sphere of production, we are excluding vast swathes of private sector activity from it.

This has two major implications. First (in common with the aforementioned theories of interdependence), it assists in resisting the otherwise dominant (albeit theoretically questionable) presumption that a contestation over revenues between capital and the state is simply a matter of the productive private sector resisting having its output siphoned off by the parasitical institution of the state. Secondly, as we shall see, the distinction between corporate sector processes inside and outside the classical production boundary has implications for the structural relation between capital and the tax state; implications which are not discernible if that distinction is not drawn. We turn in this section (by way of background) to the study of that structural relation, which is sometimes pursued under the specific disciplinary label of ‘fiscal sociology’ (Mumford, 2019).

At its inception, fiscal sociology had a core set of questions, which are to do with the nature of the ‘tax state’ and its tendency towards crisis. Schumpeter's 1918 essay ‘The Crisis of the Tax State’ (Schumpeter, 1991), generally said to have founded the discipline, was a response to Rudolf Goldscheid’s, 1917 book prompted by the dire state of Austria's public finances towards the end of World War I, Staatssozialismus oder Staatskapitalismus. Goldscheid had argued that, in the modern era, as the productive forces under the prevailing mode of production shifted from being the property of princes to being the property of capitalists, and as over the same period states became increasingly democratic, what the people inherited was an impoverished state saddled with war debt, incapable of meeting public needs and reliant for revenue on the mechanism of taxation – a mechanism to which capital is hostile, and which ultimately only channels revenue back to capital in any event. The solution, argued Goldscheid, if the tax state is to escape from a condition of permanent crisis, is a capital levy leading to public ownership of the means of production. Schumpeter's response to this was to prescribe instead the unleashing of private enterprise so that the abundance that it can create will free us all from both capitalism and the state.

It is noticeable in this debate that its content, framing and teleology is Marxian. The institution of the tax state is understood historically as contingent upon the mode of production underpinning its continued existence, and the inquiry is fundamentally about how structural contradictions – in circumstances where the mode of production in question is capitalism – lead to a complete overturning of existing conditions. This is an unmistakeably Marxian preoccupation. Goldscheid, certainly, was working within the Marxian tradition. For his part, Schumpeter was careful to meet Goldscheid on this ground, even going so far as to claim in his conclusion that Marx himself would agree with it.

We shall return to these Marxian preoccupations with crisis in section 4.3. But it is crucial to note at this stage that the ‘tax state’, while it is perhaps the most fundamental institution in actually existing capitalism, is considered at both ends of the fiscal sociological spectrum (i.e. by Goldscheid the Marxist and Schumpeter the devotee of capitalism) to be unsustainable in the long term. A forgotten but (it is here urged) necessary component of fiscal sociology is the requirement to consider what could replace that institution, and it is to that utopian end that the analysis in this article tends.

From today's perspective, another feature of the debate between Goldscheid and Schumpeter that is particularly noticeable is that the tax state is viewed largely in isolation from the global economy. Indeed Schumpeter makes express reference to international tax competition only in order to flag that he was (no doubt understandably given that he was writing long before many of the key features of today's global economy were even invented) ignoring the phenomenon. And while fiscal sociology now has a considerably broader scope than the debate as framed by Goldscheid and Schumpeter, its focus continues to be on the domestic fiscal sociology of tax states (for an overview see Martin and Prasad, 2014; updating Campbell, 1993).

Constituting the actors in international structural antagonism between capital and the state

And so when scholars do address fiscal crisis on an international scale they do not generally characterise themselves as doing fiscal sociology, albeit sometimes the language of fiscal sociology is deployed (Avi-Yonah, 2000; Genschel, 2005). Indeed the extensive and ever-growing literature on the problem of corporate tax avoidance by MNEs is notable for its lack of disciplinary coherence. Needless to say, scholars working in the mainstreams of economics, law and accounting lack a shared framework for addressing the specifically structural phenomenon that the international antagonism between capital and the state so obviously is. But this appears to be true even of the more heterodox and interdisciplinary approaches that one might group under the broad label of ‘international political economy’.

In ‘The new politics of global tax governance: taking stock a decade after the financial crisis’ international political economy scholars Rasmus Corlin Christensen and Martin Hearson offer a summary of the state of play in the international political economy of corporate tax, surveying and critiquing some of the most significant literature on the topic (Christensen and Hearson, 2019). Despite the different disciplinary label, it is clear that Christensen and Hearson – and the scholars they survey – are to a degree working in the same vein as Goldscheid and Schumpeter. At the very least there can be no doubt that the upheavals Christensen and Hearson are concerned with – i.e. the upheavals to which the introduction of this article draws attention – constitute something in the nature of a fiscal crisis of the state, albeit that there is no single state in crisis. What is in crisis, rather, is an unnamed composite formation comprising the world's tax states. ‘Tax states generally’ or ‘tax states in general’, perhaps, although they do not articulate it this way.

As regards the antagonist of tax states generally, the structural antagonism identified by Christensen and Hearson is initially said to exist between ‘globalisation and the state’, but since globalisation is referred to as having ‘structural power’ it could be understood as synonymous with global capital. The habit in the literatures they survey, however, is to treat the ‘structural power of capital’ as being coextensive with (and indeed nothing other than) the phenomenon of tax competition between states. What is absent from these literatures is a sense of capital as an ontologically distinct actor, deriving ultimately from the generation of surplus value, but capable of exerting structural power and also capable of exhibiting other features and behaviours which unfold from that core dynamic. Dietsch, 2015, for example, defines ‘capital’ as nothing other than (i) portfolio investment, (ii) foreign direct investment, and (iii) the paper profits of multinational enterprises. These are not a force powerful enough to wrestle over revenues with the combined might of all the states on the planet – they are mere accounting artefacts.

It is as if these literatures remedy Schumpeter's omission of the phenomenon of international tax competition from the original fiscal sociology, but at the same time drop the Marxian underpinning of his debate with Goldscheid and, in doing so, deploy that phenomenon of international tax competition as (by default if not expressly) a replacement for one of the core antagonists of the piece, rather than seeking to understand how the core antagonist in question, capital, appears to act through that phenomenon.

This echoes the contrast between competition as understood in modern mainstream economics and competition as understood by political economists in the Marxian tradition. Mainstream economics treats competition as a universal dynamic, whereas political economists working in the Marxian tradition view competition between actors under capitalism as a historically contingent phenomenon, coeval with (and indeed unfolding from) the commodity form. What this means is that economic actors as viewed within the Marxian tradition conduct themselves under compulsions emanating from the core dynamic that Marx identifies. These compulsions may be thought of as the ‘laws’ of capital, and competition, rather than going hand-in-hand with autonomous economic actors on a walk through a realm of infinite economic possibility, is the enforcer of those laws (Palermo, 2017). It is by virtue of compliance with those laws on the part of individual economic actors that one is able to treat capital as a system-wide whole to which it is possible to ascribe behaviours and even a kind of agency, notwithstanding that the interests of the individual firms comprised within it are in conflict with each other (Chattopadhyay, 2012).

In this analysis, it is a structural actor arising from competition between firms (i.e. global capital), rather than the phenomenon of competition between states, that is the counterpart antagonist to ‘tax states in general’. This is of course not to say that tax competition between states does not play a role – indeed the dynamic between firms that has the consequence that one can regard capital as a whole as an actor also applies to states, hence the existence of the ‘tax states in general’ that a specifically international fiscal sociology must on some level be about. These, then, are the macro-scale antagonists of the piece: global capital versus tax states in general, with competition within each playing a role in constituting the whole rather than constituting the antagonist of the whole.

As regards the antagonism between the two specifically over revenues, it will be recalled from section 2 that the approach taken here is to locate business functions associated with the production of intangible assets in the GWC rather than the GVC, with the consequence that profitability associated with those functions represents value capture, rather than value creation. Accordingly, on this view, both capital and tax states are effecting the capture of revenues from the sphere of production. In the case of tax states, it is (paradigmatically, at least) through tax, and in the case of capital, it is (as elaborated in section 2) through the deployment of intangible assets in addition to (or, in the case of many highly profitable individual firms, wholly instead of) the deployment of classically value-creating factors of production.

Fiscal sociology on a global scale

The fiscal not-smiling-so-much curve

It is a truism of the international political economy of corporate taxation today and in recent times more generally that intangible assets are deeply implicated in tax-enhanced sequestration of profits (Christensen and Hearson, 2019; OECD, 2013b, 49). Although the structures in question are usually very complicated, speaking in the most general possible terms the mechanism whereby this occurs is the placing of intangible assets in low-tax jurisdictions, so that the profitability associated with them is allocated to those jurisdictions pursuant to the operation of global corporate tax norms (Collier and Andrus, 2017: 3.45–47).

It follows then that intangibles are playing a dual role in the global contestation over revenues between capital and the state. In contrast to the world analysed by Goldscheid and Schumpeter, where ownership of means of production formed the basis for primary entitlement to revenues (subject of course to interest, rent and taxation), the world today is one where (as observed in the foregoing section) capital and the state are both in the business of capturing value from material output indirectly. And it is the dual role of intangible assets that they provide capital (a) with its instrument of value capture (as contrasted with the state's value-capture instrument of taxation), and (b) with the source of its supremacy in its contestation with the state over how that value capture is to be shared between them.

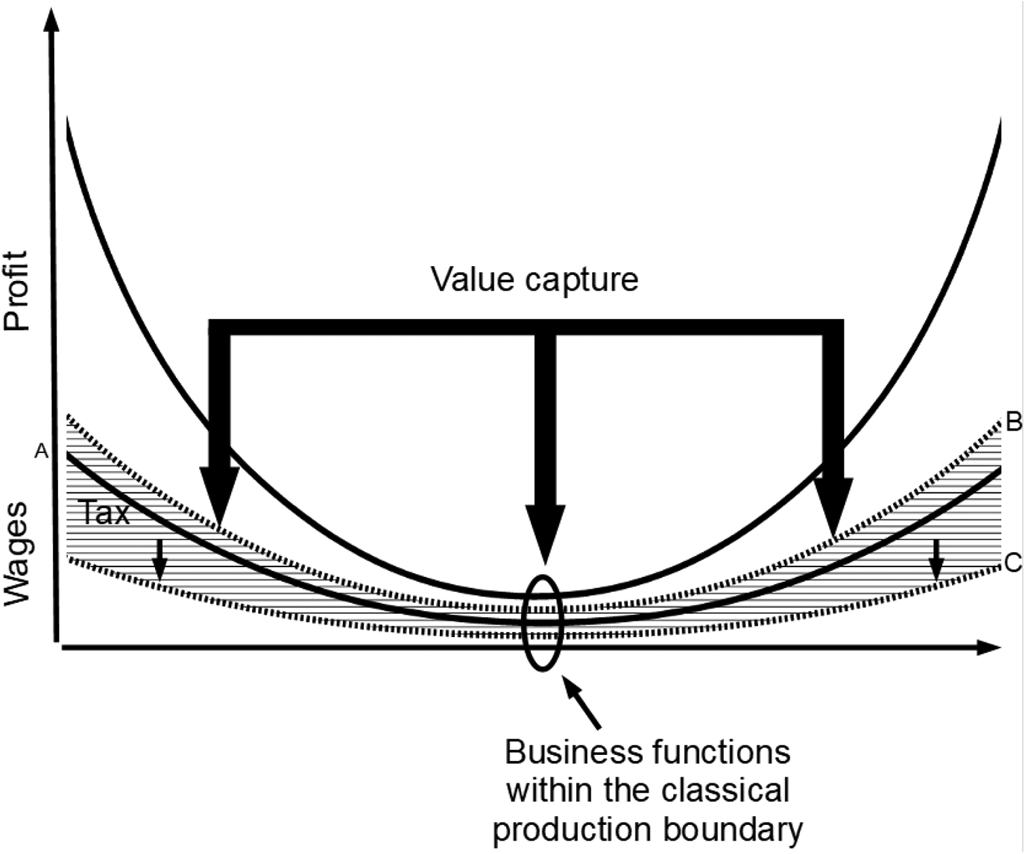

This dual role may be visualised by adapting and elaborating upon the aforementioned ‘smile curve’ schematic (see section 2 above). It will be recalled that the smile curve plots value added schematically along an axis of business functions. That axis of business functions has R&D, design, product development and so on on the left, and it has marketing, advertising and so on on the right. All of these are business functions tending to give rise to intangible assets and are therefore GWC elements rather than GVC elements. In between, yielding the central dip in the curve is material production, bulk transportation and the other business functions within the classical production boundary. The elaborations on the curve which illustrate the point made in this subsection are shown in the figure which follows.

The first step in that elaboration is to disaggregate value added into its constituent elements, i.e. wages and profit. It should be borne in mind that (as recalled above) developing and maintaining the intangible assets that effect value capture from GVCs requires labour. It is labour which (in common with the labour of servants of the state) is outside the classical production boundary, but it is labour nonetheless, and that labour requires to be remunerated (often much more generously than labour in mines, on farms, in factories, at logistics hubs &c). Recognising that wage component of value added yields the secondary smile curve at A in the figure below.

The second step in the elaboration is to divide both the wage region and the profit region into what is retained by (respectively) labour and capital, and what is collected in tax in the form of taxes upon (respectively) wages and profit. This yields the tertiary smile curves at B and C in the figure below. For the purposes of clarity, the taxed regions are placed contiguously, at either side of the boundary between wages and profits, so as to yield three bands under the smile curve of (i) after-tax profits, (ii) tax (the shaded band) and (iii) after-tax wages.

The third step in the elaboration is to integrate into the picture the role of corporate tax avoidance. We have already observed that intangible assets depress by means of value capture the main curve at its central point i.e. where the business functions within the production boundary are located. The significance in this context of the corporate tax avoidance associated with intangibles is that that same downwards pressure is also exerted outside that central point but, crucially, it is not exerted on the main curve. It is exerted, rather, on the tertiary curve at B, suppressing the extent to which profitability outside the classical production boundary is exposed to tax. The pressure exerted by value capture across the smile curve is shown with the heavy arrows. As will be seen, the downwards pressure at the centre of the main curve and on the sides of the tertiary curve at B causes the region of untaxed profits to (in effect) bulge.

A final elaboration, which is crucial to the point made in the subsection which follows, is that there exists an alternative route to recouping at least some of the lost tax i.e. reliance instead on taxes on the wages and consumption of GWC workers. The same downward pressure as is exerted at the centre of the main curve and onto the sides of the tertiary curve at B is therefore transmitted further on down to the tertiary curve at C (illustrated in the figure below by the lighter downwards arrows against that curve).

The tax-farming of poor countries by global capital on behalf of rich countries

The phenomenon identified in the foregoing subsection has certain important structural implications once inequality between states is brought into focus. The vast majority of the world's population lives in states with a GDP per capita very substantially below the GDP per capita enjoyed in the rich countries of the Global North (this uncontroversial claim may be readily substantiated by data from e.g. the World Bank). Further, those lower-income states are almost exclusively states that have a proportion of the workforce employed in raw materials extraction, agriculture and manufacture which is substantially higher than the kinds of proportion generally to be found in the higher income states (similarly, this uncontroversial claim may be readily substantiated by data from the International Labour Organisation). As the World Bank recently explained to the OECD, ‘while some of the jurisdictions we work with represent significant markets in their own right […] activity at the other end of the value chain, production of raw materials and manufacture, is a proportionately more significant part of their economies’ (World Bank, 2019).

Or, to express the point by reference to the ‘smile curve’ schematic, from the point of view of headcount, the business functions at the low point at the centre of the smile curve are disproportionately located in poorer countries, and the activities up the sides of the smile curve are disproportionately located in wealthier countries. From the point of view of payroll, of course, that effect will be hugely magnified, because of the higher cost of labour in wealthier countries, or (alternatively put) because of the hyper-exploitation of labour in low-income countries (Smith, 2016; see also Suwandi, 2019 and Hickel et al., 2022).

The phenomenon of sustained inequality between states under the capitalist mode of production is susceptible to formal analysis in Marxist economics, and as such, it is sometimes referred to as ‘unequal exchange’. On a technical level, this is an exceptionally complex topic. Even before spatial unevenness is taken into account, Marxist economics suffers from the complexity that, in order to yield quantities that behave analogously to market prices, value must be adjusted in accordance with how capital-intensive the sector is (this is the notorious ‘transformation problem’ of which there are a number of vigorously contested and mutually incompatible solutions [Potts and Kliman, 2015; Moseley, 2015; Shaikh, 2016; Hahnel, 2017]). In addition, the value-theoretical step of treating labour as fungible means that the wide heterogeneity of labour actually taking place in the real world is reduced to a notional system-wide average labour (Heinrich, 2012: 51–2). Once the possibility for geographical variation in these core parameters becomes a focus of analysis (i.e. dealing with circumstances where equivalent sectors have lower capital intensity and lower wages in poorer countries), the modelling complexities are hugely compounded (Ricci, 2021). Those complexities are not engaged, however, in the context of the strictly classical axioms of the investigation here. We are not concerned with spatial unevenness within the global network of value-creating processes. We are, rather, concerned with spatial unevenness between the global distribution of those processes and the global distribution of business processes which are not to be treated as value-creating at all.

In any event, it follows from the analysis adopted here that multinational enterprises capturing value from material production by deploying labour outside the classical production boundary to dominate GVCs disproportionately suppresses the corporate tax take in low-income countries, because it is disproportionately in low-income states that the profitability arising from material production would otherwise accrue. (It will be recalled that the GVC is agnostic as to the governance relation between nodes and similarly this phenomenon takes place whether the material production takes place in-group or through market relations, because the suppressed market prices are replicated in-group for corporate tax purposes by virtue of transfer pricing norms.)

Meanwhile, the labour deployed to capture value, when it comes in the form of higher-waged labour in wealthy countries, gives rise to a substantial alternative tax base in those countries. And while this is clearly the case if one compares the incomes of Global South workers in functions at the bottom of the smile curve with the incomes of, say, workers in the Global North in IT or creative roles, it is all the more pronounced in view of the vast incomes of certain other GWC workers such as bankers and MNE senior management. And so the adverse fiscal impact for tax states of their contestation over revenues with capital is disproportionately visited on low-income countries. The corporate tax base is suppressed everywhere, but wealthier countries have vastly greater recourse to, in particular, social security contributions as an element in their tax compositions (Modica et al., 2018).

At this point in the analysis, we have not gone past (although it is differently articulated) the already-noted and well-understood point that wealthy countries can rely on the taxation of the employment and consumption of large numbers of well-paid individuals working in office jobs, while lower-income countries are more likely to have to rely on the taxation of material commodities in various forms (see the introduction to this article). Expressing the point as a structural one within the global production network, however (i.e. by reference to the distinction between GVCs and GWCs elaborated at the outset of the article, where only the material production is value-creating, and the rest is value capture) yields a startling additional implication.

It was observed at the end of section 3 that both capital and tax states are effecting capture of revenues from the sphere of production, and in the case of capital, it is through the exercise of value capture in the global production network. It follows from the dynamics described in this subsection that, in the case of states, it is not primarily through the direct power to tax the sphere of production that revenue is raised, but indirectly through the power to tax the salaries and consumption of the GWC workers performing the labour required to effect the capture of value from GVCs.

Accordingly, owing to the uneven economic geography of GVC and GWC functions noted above, the fiscal antagonism between capital and tax states has the consequence that wealthy states are in large part obtaining their tax revenues indirectly from less wealthy states. The creation of value takes place predominantly in less wealthy states, the capture of value takes place overwhelmingly in the corporate and financial sectors of wealthier states, and the tax revenues of wealthier states are in large part derived from the taxation of labour in those sectors. The dynamics described here are, in other words, a major form of contemporary imperialism. The value is created in what is sometimes referred to as the global economic periphery, and it ends up (via the route of GWC labour) yielding tax revenue in the global economic core. And the maintaining by wealthy states of a global legal and economic order in which intangibles have such commercial power, despite the adverse impact of that power in the fiscal arena, is accordingly a form of tax farming: outsourcing to capital the job of capturing revenues for wealthy countries from material production in less wealthy countries.

It is no secret that wealthy states act to skew the system of international corporate tax norms so as to disadvantage less wealthy states (Christians, 2009; Oguttu, 2018; Quentin, 2020; Hearson, 2021). Further, there is even a corner of the international tax literature that seeks to recognise the apparent exploitation underpinning the market outcomes plotted schematically in the ‘smile curve’ (Quentin, 2017; Apeldoorn, 2019; Christians and Apeldoorn, 2019). This subsection, while serving to further the argument in this article, is also offered as a contribution to (and bridge between) those literatures.

The key observation made here from the perspective of those literatures is that it is no coincidence that material production lies at the bottom of the smile curve. That location in the smile curve is not merely an arbitrary one where more value happens to be created than market outcomes suggest, with the implication that international tax norms are inadequate to recognise the contribution to overall value made by workers who just happen to be located predominantly in poorer countries. Rather, that location in the smile curve is where all the value in the curve is created – it is the structural epicentre of exploitation as analysed by that pre-eminent political economist of exploitation, Karl Marx. And the legal and economic order that keeps profitability in GWCs rather than at the materially productive GVC nodes at the bottom of the smile curve, while not itself being an obviously fiscal regime (indeed at first blush it appears to run counter to states’ fiscal interests owing to the aforementioned utility of intangibles in corporate tax avoidance), is fundamental to the ongoing fiscal supremacy of wealthier tax states notwithstanding that the exploitation in the system as a whole is predominantly taking place elsewhere. Indeed it is indirectly via the mechanism of value capture in the corporate sector that imperial domination of the world's most exploited populations is being perpetuated into the 21st century.

The tendential dimension

The smile curve is (or at least in recent times has been said to be) deepening (OECD, 2013a; Meng et al., 2020). This accords with the widespread observation that intangibles are of increasing importance in the global economy (Haskel and Westlake, 2018). This means that the structural phenomena identified here are also apparently tendential. Superficially, it is not hard to speculate as to why the phenomena discussed above might be self-expanding. For example, fiscal constraints in low-income countries might contribute to the low cost of labour in those countries, which owing to the phenomena discussed above would contribute in turn to the fiscal constraints suffered by those countries. Similarly, if profitability referable to intangible assets benefits from a favourable tax profile as compared to profitability referable to material production, then investment will flow up the sides of the smile curve, with the consequence that wage spend in those areas will be greater, further pushing up the sides of the smile curve.

But (to return to fiscal sociology's roots i.e. in a Marxian approach) structural tendencies within capitalism such as the deepening of the smile curve may potentially be analysed as deriving ultimately from the fundamental conflict Marx identified between (a) the relations of ownership and control under capitalism and (b) the productive forces it unleashes. It is from the contradictions inherent in the dynamic arising from that conflict that unfolds capitalism's central structural antagonism; the antagonism that subsists between capital and labour. This antagonism further unfolds, in traditional Marxian analysis, into class conflict, and various other contradictions that Marxist scholars are inclined to identify, including (among some Marxist scholars at least) a tendency for capital to invest increasingly in unproductive labour (Olsen, 2017: 123).

These contradictions proliferate because capitalism as understood by Marxists is at the same time compelled towards crisis by its own core internal contradictions, and also constantly revolutionising itself so as to seek to stave off crisis by means of countervailing tendencies. Capitalism is therefore understood as lurching from crisis to crisis, with each new lurch reflecting a reconfigured system and each new crisis different from the last – a crisis not so much of the system as a whole but of whatever countervailing tendency was driving the lurch. A classic illustration might be imperialism of the traditional territorial kind, which reached its crisis with the First World War. Another is the financialisation of the neoliberal era, which reached its crisis in 2008.

Identifiable countervailing tendencies do not necessarily determine the nature of the forthcoming crisis; multiple such tendencies might be in operation and it just depends on which one hits the buffers first. One tendency which was observed in the 1960s and 1970s, but which did not seem to have driven the crisis of the mid 1970s, and so has not been much commented upon since, was the aforementioned tendency for capital to spend greater and greater amounts of money on unproductive labour. A major strand of observation to this effect was the ‘monopoly capitalism’ school, of which the founding text is the 1966 book of that name by Paul Baran and Paul Sweezy.

The picture painted by Baran and Sweezy is of a world in which oligopolies emerge in markets where the largest players preserve their excessive profits by choosing not to compete on price, instead investing increasingly in operations such as marketing, advertising, branding and product design, in order to compete with each other in other ways. Baran and Sweezy focused on the national economy of the United States, and on players which generally owned means of production within the group, selling at monopolistic prices commodities they themselves manufactured. But there is a clear commonality with the deepening smile curve noted here, insofar as in both instances there is a tendency for unproductive elements of corporate sector activity to assume greater and greater economic significance.

Underlying the monopoly capitalism outlook is a perception that is sometimes framed in terms of the idea that capitalism has a tendency towards overproduction and underconsumption, and that tendency is counteracted by a tendency to fund increasing consumption on the part of labour outside the classical production boundary (Foster, 2014; Wolff, 1987; Bleaney, 1976). The reason that such a tendency would help capital stave off crisis is perhaps easiest to conceptualise if one revisits Schumpeter's prediction mentioned in ****section 3.1.

Schumpeter suggests, it will be recalled, that the productive forces unleashed by privately owned capital will create such abundance that capitalist relations as we know them will be rendered obsolete. This long-term prognostication suffers from a fatal defect. Under the capitalist mode of production, money is invested in means of production on the basis of the expectation that the commodities thereby produced will be purchased. That being the case, while the productive forces of capitalism may on a technical level potentially be driving us towards such automated conditions of abundance that commodities are given away for free and no-one need ever work again, the relations of ownership and control under capitalism are driving it in the opposite direction because they require that people work for wages and pay for their consumption. And one way out of the contradiction is for a greater and greater proportion of investment to be spent on unproductive labour, which absorbs surplus rather than cycling it back into yet more production of surplus, thereby suppressing material production without suppressing demand.

At this point in the analysis fiscal sociology swings right back into the frame, for the simple reason that states are (given adequate fiscal resources) extremely dependable mobilisers of such labour. And so an increasing tax take can in principle serve the same crisis-averting purpose as modern capitalism's vast and seemingly ever-increasing spend on marketers, administrative assistants, advertisers, designers, consultants, call-centre workers, bankers, programmers and managers &c (not to mention the cleaners who clean their offices). But for the reasons that it is the very stuff of fiscal sociology to identify, states are hampered in their ability to perform this crisis-averting role by capital's own aversion to seeing its revenues expropriated. It is (at least in part) for this reason that, alongside the development of the ‘monopoly capitalism’ theory, the final years of post-war growth preceding the crisis of the mid-1970s saw a revival of the fiscal sociology framing, exploring from a number of diverse (but on the whole broadly Marxian) perspectives the fiscal contradictions of the state under the capitalism of the specific oligopoly-oriented variety that prevailed in the wealthy states of the Global North at that time (O’Connor, 1973; Gough, 1975; Foley, 1978; Fine and Harris, 1976; Musgrave, 1980; Foster, 2014: ch 6).

*****It is here suggested that the fiscal not-smiling-so-much curve elaborated in Section 4.1 be understood in a similar vein. Servants of the state, and GWC labour (i.e. corporate sector labour up the sides of the smile curve), are both able to perform the crisis-averting role of absorbing surplus value rather than producing further surplus value. But GWC labour has an additional function in this regard: it also functions as an instrument in the antagonism over revenues between capital and the state having the effect that it is itself, rather than the labour of servants of the state, which performs that role. It is for that underlying reason, it is suggested here, that the sides of the fiscal smile curve are self-raising: they are (for the time being at least) the dominant emergent structural outlet for excess surplus value. The structural phenomenon manifesting itself in (a) downward price pressure on material output in global value chains and (b) corporate tax avoidance, is a crisis-countervailing tendency in a feedback loop. And (neoimperial softening of the adverse impact for wealthy countries as set out in section 4.2 notwithstanding) that feedback loop is a key driver of today's crisis of tax states.

Conclusions

While capital and the state are both in the business of capturing value from GVCs indirectly (i.e. not directly through ownership of means of material production), intangible assets have a dual role of suppressing the profitability associated with material production and suppressing the corporate tax take. They therefore simultaneously constitute capital's instrument of value capture, and its instrument of supremacy in its contestation with the state over the proportion in which value capture is shared between the two. Better-paid labour associated with value capture on the part of capital (i.e. better paid GWC labour) is predominantly located in wealthier states, giving those states an alternative source of revenue (i.e. the taxation of GWC labour) and consequently giving them a reason for maintaining a global order in which capital has supremacy over them in the contestation over value capture from GVCs. Further, these dynamics are in a feedback loop which serves as a countervailing tendency staving off a structural crisis of capitalism, and that feedback loop is a core driver for today's crisis of tax states.

The content of that countervailing tendency, it should be recalled, is that it channels output to surplus-absorbing (i.e. unproductive) forms of labour rather than towards further production. But, crucially, it is in a feedback loop that channels it specifically towards surplus-absorbing labour in the corporate sector and predominantly in richer countries.

It does not have to be this way.

As already noted surplus-absorbing labour may be perfectly well performed in the public sector. Indeed some of these forms of labour – for example, labour in such sectors as healthcare, education, care and the arts – are particularly socially useful and particularly well-suited to being performed in the public sector. Further, given the flatter wage structures that prevail in the public sector, public expenditure on these sectors may actually be better at absorbing surplus than GWC labour (i.e. a greater proportion of the wage expenditure will go into consumption by individuals rather than further investment). In addition, these forms of labour have the benefit of relieving social burdens that would otherwise be disproportionately borne unwaged by women and people of other marginalised genders. Finally, they are forms of labour for which there is a disproportionate need in lower-income countries.

And so clearly there is an argument here for (i) better taxation of corporate profits and (ii) more equitable distribution of the fiscal proceeds between states – so far so unremarkable among tax justice policy asks. The implications of the dynamic identified here being tendential, however, are remarkable and profound. What it suggests is that there is a vast and, as the sides of the smile curve rise, increasing latent capacity within the system for funding state expenditure, without any diminution of corporate sector productivity in the form of goods and services.

That being the case, it is here suggested that we revive the discussion about the tendentially increasing capacity (and indeed need) of the system to absorb excess surplus value, so that a progressive international fiscal sociology may be built around that discussion. This discipline, reinvigorated by a return to its Marxian roots, could develop fiscal technologies whereby a tendentially increasing proportion of capitalist surplus is placed in the hands of states – on a redistributive basis as between states in view of the unequal economic geography discussed in Section 4.2 above – to be absorbed by socially useful but (to adopt the classical terminology) ‘unproductive’ spending targets such as healthcare, education, welfare and the arts.

An embryonic example of a fiscal technology having the necessary globally redistributive effect (albeit not the hypothecation) might be unitary taxation by formulary apportionment of the entire value chain (Quentin, 2017). Such a system, if combined with a rate that increases towards 100%, would have the consequences of (i) equitably redistributing the fiscal power of states upstream in GVCs and therefore towards the Global South, (ii) redistributing the surplus-absorbing function of unproductive labour away from GWCs and towards public sector labour and (iii) restoring to primacy within the demesne of capital its core technology-enhancing function of placing the means of material production in the hands of competing capitals. As it becomes increasingly available for humans around the world to sell their labour to states, while consumer demand remains undiminished, capital will have no choice but to concentrate on increasing automation of material production. And eventually, as the corporate tax rate approaches mere basis points below 100%, and the number of workers in the corporate sector drops to zero, and all our material needs are being met by robots while our only labour is caring for each other, a synthesis of the contradictory utopian visions of Goldscheid and Schumpeter will have been realised.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.