Abstract

We respond to the special issue’s call for a multiscalar, historicised approach to state capitalism through an exploration of Sovereign Wealth Fund investment into London real estate. We point to how the UK’s ostensibly market-led recovery since the 2008 financial crisis has relied in part on attracting ‘patient’ state capitalist investments. In this, we contextualise the relational regulation of real estate markets as the outcome of intersecting state projects by considering the investment motivations of the single largest owner of London real estate, the Qatari Investment Authority, and the utilisation of their investment by UK governance actors. Focusing on Qatari Investment Authority’s involvement in London’s Olympic Village, we highlight how this strategic coupling in the real estate market realised domestic and geopolitical aims for the Qataris while facilitating the UK government's strategy to ameliorate London’s housing shortage by fostering a ‘build to rent’ asset class. In doing so, we contribute to readings of state capitalism as an ‘uneven and combined’ process beyond the traditional state/market binary by placing sovereign wealth fund investment into the context of city governance, the geopolitics of real estate and resultant relational forms of regulation.

Global cities are a crucial but thus far neglected scale at which state capitalism is produced and enacted. State-led transnational investors such as sovereign wealth funds (SWFs) have emerged as significant players in global city regional real estate markets since the 2000s while remaining sensitive to political economic priorities and contestations in their countries of origin. As a result, the governance of the built environment in cities, particularly those which are highly integrated into the world economy, is a complex outcome of local government regulation and of the regulations shaping the behaviour of various state-influenced firms. This means that real estate markets are not only shaped by the geopolitical context but in themselves represent key components of geopolitical (re-)alignments (Büdenbender and Golubchikov 2017: 77).

In this paper, we offer a relational reading of the Qatari Investment Authority’s (QIA) investment into London real estate to meet this special issue’s call for readings of state capitalism which are sensitive to the historical and multiscalar constitution of state projects (see Alami and Dixon 2020). In doing so, we explore the ‘geopolitics of real estate’ (Büdenbender and Golubchikov 2017; Rogers 2017) by tracing out the entanglements of state projects as they are refashioned amidst increasing international tensions and shifting state strategies in an unpredictable global political economy. We contribute a relational reading of the geopolitics of real estate through the lens of state capitalism by exploring how the investment priorities of SWF actors have intersected with the UK’s real estate-led recovery following the 2008 financial crisis.

In the first section, we review the literature on ‘state capitalism’, emphasising that its obverse within the wider context of ‘uneven and combined state capitalism’ (Alam and Dixon 2021) is not free market economies but ‘capitalist statist’ configurations whereby state powers are mobilised extensively to support market actors’ aims. In the second section, we overview how various state capitalisms intersect within London’s real estate market amidst the UK’s market-led recovery which targeted ‘patient’ institutional investors who are in practice often state-backed or -influenced (Thatcher and Vlandas 2016). Drawing on the Real Capital Analytics (RCA) commercial property database and interviews with London planners, investors and sovereign wealth industry experts, we then contextualise the investment of London’s biggest real estate owner, the QIA, within Qatar’s wider state project to secure itself through the projection of soft power. Finally, we consider whether and how such large-scale state investment has shaped London’s governance through a case study of the QIA’s investment in the Olympic Village. In doing so, we offer a multiscalar, historically contextualised relational perspective on SWF investment and the geopolitics of London’s real estate market.

State capitalism, capitalist statism

The concept of ‘state capitalism’ has gained currency in recent years as commentators have sought to account both for the importance of state-backed companies in the post-financial crisis global economy (Babic et al., 2020; Gu et al., 2016; Musacchio et al., 2014), and a related geopolitical shift in which developmentalist states are reshaping the global hegemonic order (Apeldoorn et al., 2012; Bremmer, 2010; Kurlantzick, 2016; Nölke et al., 2015; Singh and Chen, 2018). Alami and Dixon (2020) argue that while the term’s recent resurgence reflects this increasing prominence of direct state involvement in the global economy, its conceptual use is limited by a lack of state theory, ahistoricism in which the novelty of the contemporary period is not specified, and methodological nationalism that fails to account for the transnational, multiscalar, nature of contemporary states (Dixon, 2011; Pradella, 2014). We address this by exploring how sovereign wealth fund real estate investment produces geopolitically inflected ‘relational regulation’ (Hall 2017; Raco et al. 2020) at the city governance level as an example of ‘combined and uneven state capitalism’ (Alami and Dixon, 2021).

The primary problem with the term state capitalism, as it has been popularised in press commentary and realist international relations (Bremmer, 2010; Kurlantzick, 2016), is that it functions to draw contrast with imputed liberal free market economies of the Anglo-Saxon countries. This rests on a state/market dichotomy which even critical political economy remains in thrall to (Bruff, 2011). Yet, as economic geographers have often argued, states structure markets and regulate their social embeddedness, mediating the non-market aspects that are the necessary basis of seemingly ‘free’ market relations (Berndt et al., 2020; Block, 2019; Muellerleile, 2013; Peck, 2021, 2013). There is no market without state intervention: the question is one of where and how the capitalist state intervenes.

Recent decades of market-oriented neoliberal deregulation in the Global North represent not the shrinking of the state, but a process of state restructuring in which the state has rescaled and re-regulated around the interests of new sets of market actors (Peck and Theodore, 2019). Neoliberalism is often framed as a repudiation of post-war state-centric Keynesian-managerial economic model and draws its free market ideological credentials from laissez-faire precedents, but even here the ‘neo-’ element entails a recognition that the state plays a crucial minimal role in guaranteeing and structuring markets (Mirowski and Plehwe, 2009). In practice, this has often been a maximal role in prioritised sectors (Peck, 2010), as has become clear over the last decade of strong state intervention propping up financial markets. Uncritical use of the term ‘state capitalism’ to contrast western and developmental states implicitly reinforces the ideological notion of the west representing free market capitalism, obscuring an ‘actually existing neoliberalism’ (Brenner and Theodore, 2002; Peck, 2010) reliant on strong states pursuing selective de/re-regulation (Aalbers et al. 2011).

Recognizing this, Alami and Dixon (2021) argue for closer attention to the contemporary reconfiguration of the state-capital nexus represented by the emergence of ‘state capitalism’, calling for greater geographical sophistication focused on the relational dynamics of combined and uneven development (Dunford et al. 2021). Here the concept of state capitalism is particularly useful for highlighting the prevalence of alternative logics to the profit motive in the immediate operations of the economy. This is especially so where the capital relation is ‘state permeated’ in being directly mediated by state bureaucracy (Nölke et al., 2015; Raco et al., 2020), as is apparent in organisational forms such as sovereign wealth funds which operate according to the profit motive but within the confines of wider state strategic objectives (often domestic as much as geopolitical, per Helleiner, 2009). The concept of state capitalism thus highlights the increasing prevalence of market actors who are state-capital hybrids not motivated solely – or even primarily – by imperatives of profitability (Alami and Dixon 2020; 2021).

More recently, Alami and Dixon have sought to widen the rubrics of ‘state capitalism’ beyond the increased prevalence of politically motivated state-capital hybrids to include the more general trends of ‘muscular statism’ being central to the global economy (2020; 2021; see Alami 2021). This takes the analytical purview of state capitalism beyond the binary of state-dominated markets characteristic of developmentalist economies and highlights the relational, interdependent (‘uneven and combined’, per Alami and Dixon 2021) forms of state intervention in the economy. For example, the state plays a central role in the mixed economies of Europe’s dirigiste and coordinated capitalist models, as highlighted by the comparative political economy literature (Carney and Witt, 2014; Schmidt, 2009; Zhang and Whitley, 2013) and more recently in work on the market-based but state-led EU capital market union (Mertens and Thiemann, 2018). Further than this, Anglo-Saxon economies on the opposite extreme are not ‘free market’ but represent what may be better termed capitalist statism in that there, too, there has been an increasingly explicit reliance on state-capital hybrids and muscular forms of statism (per Alami and Dixon 2021) but in which public goals remain subordinated to market actors’ profitability.

In this ‘capitalist statism’, there has not only been a regulatory capture of states by finance (Aalbers et al., 2011; Pijl and Yurchenko, 2015) but also an increasing structural interdependence between state and market as central banks prop up a stagnant capitalism through recurrent bailouts (Streeck 2016). Associated budget deficits have reinforced market power over these states in the implementation of austerity regimes to guarantee credit-worthiness (ibid). This has entailed a continued reliance on market-led mechanisms such as the use of public-private partnerships to channel investment into delivering public policy (Raco 2013; Tasan Kok et al. 2020)

As a sub-category within the wider uneven and combined trend towards statism which Alami and Dixon (2021) identify,‘capitalist statism’ highlights this centrality of government intervention to market-oriented governance configurations. This market-led statism remains typical of OECD economies (see Svitych, 2021) in contrast to the developmentalist regimes that have been the focus of the state capitalism literature. This is uneven and combined in that different state projects and organisational forms interpenetrate in complex hybridities that make up the mutually constitutive nexus of state-capital relations (Alami and Dixon, 2020; Apeldoorn et al., 2012). This mutual constitution is not only one of state and market, but relational systems of regulation across and within different states. States at different scales and locales de facto govern outcomes in others – as Raco et al. (2020) show in the case of Chinese capital controls and London real estate, for instance (see Hall, 2017). Such relational forms of regulation are particularly notable in the ‘strategic coupling’ Haberly (2011) of market-oriented governments seeking to attract capital and capital-exporting state-led/influenced investment bodies such as SWFs.

In this section, we emphasised that a relational reading of the shifting state-capital nexus is predicated on a rejection of the binary view of free market versus state capitalist economies (see Alami and Dixon 2021). OECD economies are no less ‘state permeated’ (Nolke et al. 2015) but remain market-oriented with state aims frequently subordinated to the profit motive, as opposed to the state-dominated markets in developmentalist countries that are the focus of much of the state capitalist literature. We referred to this former as ‘capitalist statism’ to highlight the continued dominance of market logics and actors in OECD countries within the wider context of what Alami and Dixon (2021) identify as ‘uneven and combined state capitalism’. In the rest of the paper, we explore the intersection of state capitalist/capitalist statist projects in SWF investment into London real estate.

The geopolitics of real estate

Viewing economic governance through the lens of state capitalism draws attention to the (re-)configuration of the state-market nexus and the different logics prevalent in particular state-market hybridities. Within this frame, we have counterposed ‘capitalist statist’ to ‘state capitalist’ forms as interpenetrating and mutually constitutive within a wider ‘uneven and combined state capitalism’, in contrast to the free market/state capitalist binary prevalent in much of the extant literature on state capitalism. This binary rests on a methodological nationalism in which the nation-state is taken as the given unit of analysis (Dixon, 2011; Pradella, 2014), reinforcing the ‘territorial trap’ of taking sovereign territory to be a fixed, discrete container of society (Agnew, 1994; Raco et al., 2020). In this section, we draw on Büdenbender and Golubchikov, 2017 interpretation of the ‘geopolitics of real estate’ to interpret the relational configurations of capital flows, state projects and strategic couplings in the built environment.

The process of state-space formation is a constant one, not only in places where statehood is perceived to be more fragile and contingent but, for instance, in the rescaling and restructuring of post-Fordist states whereby regions have become central scales of governance navigating a globalised world in ways not always congruent with national-scale polities. Globalisation has been a city-regional process (Harrison and Hoyler 205; Scott, 2001; Swyngedouw, 2004) in which international investors, state-backed organisations and local stakeholders transgress national boundaries in forging relational networks to anchor investments in place (Pryke and Allen, 2019; Torrance, 2009). This has been bound up with a shift to urban entrepreneurialism which has at points taken on the form of urban diplomacy (Phelps and Miao, 2020) in which cities actively court foreign investors and governments (see Massey, 2007) while being an important basis of national foreign policy such as in the city regional infrastructure agglomerations making up China’s One Belt One Road initiative (Chen, 2020). The combination of glocalising state restructuring, urban entrepreneurialism and geopolitical considerations has produced fragmentary ‘hybrid contractual landscapes’ (Taşan-Kok et al., 2020) whereby urban governance is relationally constituted across projections of political and economic power both geographically and between state, market and civil society actors (Raco, 2013; Raco et al., 2020; Swyngedouw, 2016).

States may be understood as relational assemblages through which territorial power must be enacted and performed (Paasi, 2012, 2002; Painter, 2010). Especially important to such processes of state formation are large-scale space shaping practices such as infrastructure projects (Lawhon et al., 2018; Lemanski, 2020; Swyngedouw, 2015), supply chain management (Cowen, 2014) and housing market composition (Büdenbender and Golubchikov, 2017; De Decker et al., 2005; García-Lamarca and Kaika, 2016; Rogers and Koh, 2017)

In particular, Büdenbender and Golubchikov call for more attention to the internationalisation of real estate markets not only as conditioned by, but an ingredient in, contemporary geopolitics as part of the assemblage of ‘soft’ power within a competitive state world order. They point to how both direct state-backed investment and flows of bodies and capitals from Russian citizens into foreign real estate markets has acted as a source of leverage in international negotiations, while other work has pointed to China’s soft power in its regulatory control over its citizens’ investments (Raco et al., 2020; Rogers and Koh, 2017). It is within this context that we must understand large-scale SWF investments into global real estate markets such as London’s.

Recent work has highlighted the role of sovereign wealth funds after the financial crisis in processes of ‘strategic coupling’, in what Haberly (2011) termed a ‘state-led global alliance capitalism’. Within this, Haberly interprets state-backed organisations such as strategically oriented sovereign wealth funds to be an ‘institutional manifestation of the synthesis of the twin political dynamics of defensive state adaptation and changing state territoriality under conditions of globalisation and financialisation’ (ibid: 1834). Understanding various state projects and their strategic coupling through multiscalar investments is a central component to the relational constitution of contemporary uneven and combined state capitalism. We explore this through a case study of relational regulation and the geopolitics of real estate in an analysis of the motivations of the single largest holder of London real estate, the QIA, and how market-oriented governance actors in London sought to utilise this investment to achieve their urban policy goals.

The role of the state(s) in London’s real estate market

London real estate is a key node for global investment flows (Fernandez et al., 2016; Sassen, 2001). This in itself is geopolitical, in part reflecting the British state’s post-imperial project of maintaining infrastructural power over the world economy as the territorial networks of its former empire remain central to the circulation of global capital (Haberly and Wojcik 2015). Within this wider state project the UK government has fostered a domestic growth model dependent on rising house values powered by international capital entering the London region (Hofman and Aalbers, 2019; Massey, 2007), with multiple scales of the state taking an active role in courting such investment as critical to the country’s post-2008 economic recovery. Despite the government’s free market rhetoric justifying this approach, however, the institutional capital it seeks to enrol are frequently state-led or -influenced actors such as sovereign wealth or pension funds, entailing strategic coupling (Haberly, 2011) between Britain and investing countries’ state projects. London’s internationalised real estate market thus offers a fertile ground in which to explore uneven and combined state capitalism as it unfolds beyond developmentalist states.

We investigate this through QIA’s investment into London real estate by drawing on three sources of data: an extensive commercial database of transactions since 2004 provided by Real Capital Analytics, interviews with 102 key real estate professionals and public officials across London as part of a 3-year project analysing the city’s real estate market; 12 of which were with investors and developers specifically focused on sovereign wealth funds, and discourse analysis of policy and political discussions on a national, city and local level. Additionally, the Olympic Village case draws on multiple site visits led by the developer team conducted over the course of 2019.

Capitalist statism: The UK’s state-led real estate recovery

An example of a capitalist statist configuration, the UK has undertaken extensive state intervention to support market with a particular focus on pumping up financial and real estate assets in hand with active efforts to deliver public policy priorities by channelling private investment. To this end, planning was flexibilized within a context of state austerity in which local governments were prompted to actively compete for capital to compensate for funding shortfalls (Brill and Durrant 2021; Ferm and Raco 2020; Peck and Theodore 2019). As a result, meeting London’s development and urban governance aims is reliant on funding from external capital, as one investor with a major international bank emphasised the need for foreign direct investment to realise London’s strategic development projects: We don’t have the capital in the UK. The UK institutions, pension funds and savings entities don’t have the capital to put the £10 billion into Canary Wharf on their own. We need external investors. If you look at the co-owners of buildings around here and over there [indicating landmark buildings in London’s financial district] that’s Qatar, Brookfield and CIC…

1

we wouldn’t be building this stuff [without them].

Within this context, the British government have sought to shape the investment environment around ‘patient’ capital institutional investors who are perceived to have the longer investment horizons and higher risk profiles necessary to deliver strategic development goals and social benefits. This goes beyond enabling specific developments. For example, as we explore in the London case study, the UK government explicitly sought to craft a ‘build to rent’ housing sector as an attractive asset to such patient institutional capital capable of aligning private profitability with public policy aims (Brill and Durrant 2021; Brill et al. 2022).

One of the paradoxes of London’s post-crisis market-led governance is that such patient institutional capital are themselves typically state-backed or influenced (Thatcher and Vlandas 2016). Thus, the focus on attracting patient capital has entailed greater reliance on foreign states either through citizenship investment subject to regulatory controls (Rogers 2017; Rogers and Koh 2017; Raco et al. 2020) or more directly through state-backed/influenced investors in sovereign wealth or pension funds. London’s position as a liquid global market perceived to be a safe haven in which to park capital has meant even private investment fluctuates markedly with geopolitical events and changes in foreign regulatory regimes, underpinning the relational regulation of its built environment as the product of intersecting state projects (Raco et al. 2020). As one developer in the city related: If there is a regulatory change [in a big overseas market] you get a big influx of money, and sometimes they discreetly turn the tap off and you don’t. Similarly, huge amounts of money flowed into the UK, almost overnight, when Colonel Gaddafi was shot… the impact of the Arab Spring on the London property market cannot be underestimated in terms of the amount of money that came into London so, so quickly.

Despite a discourse of this being a market-led recovery, then, a focus on channelling patient institutional capital has in practice meant heavy reliance on state-influenced capital flows and state-led investors such as SWFs, further compounding the cities’ sensitivity to geopolitical events. As such, London’s property market presents a key site in which different forms of state-capital hybrids intersect and strategically couple. In the next section, we consider the nature of SWFs and their involvement in the relational regulation of London’s real estate market.

Sovereign wealth funds

State-influenced investors’ counter-cyclical spending and appetite for risk made them important sources of capital in the UK’s post-2008 real estate/finance-led recovery. This was especially so for sovereign wealth funds, whose money the UK government explicitly aims to channel into strategic projects as a means of subsidising social commitments under conditions of state austerity, as demonstrated in a 2016 Parliamentary debate ‘UK Sovereign Wealth Fund’ in which members of parliament across the political spectrum frequently framed international SWF inward investment as a necessity. Sovereign Wealth Funds are defined by the UK government as state-owned investment funds typically seeking to invest national wealth (earned through various commercial channels) in assets to sustain long-term socio-economic goals (House of Commons Debate Pack, 2016).

While not new, SWFs gained greater prominence and professionalisation during the financial boom of the 2000s in which recently industrialised East Asian nations – notably China – became major players in the Sovereign Wealth Fund landscape (Huat 2016; Shih 2009). This growing importance of state-owned investment funds in the global economy reached a crescendo after the global financial crisis of 2008 with state-backed companies taking advantage of the market downturn to strategically acquire distressed assets and companies. The counter-cyclical spending of state-backed entities was actively welcomed by the UK government as it sought to reinvigorate its real estate-finance led growth regime (Baccaro and Pontusson, 2016; Hofman and Aalbers, 2019).

A key commitment which facilitated this rise of SWFs is their promise to adhere to the ‘Santiago Principles’, a behavioural code agreed on by sovereign wealth funds in 2008 in response to receiver country anxieties regarding their investment. In this code they commit to being transparent in their actions and not investing with political motive. One interviewee involved in the standards setting organisation argued that the codes worked in practice but was being threatened by the challenges to free trade emanating from the US and UK becoming more protectionist and engaging in trade wars. However, another interviewee, an asset manager specialising in sovereign clients, argued that these principles lack specificity and have acted as an ‘invisibility cloak’ legitimising SWFs as separate from the states backing them: … by the time they’d done [the Santiago Principles] the world was open because we’d gone from ‘we don’t want your money’ to ‘I’m not sure about you’ to ‘please, can we have your money because we’re in a global financial crisis.’ So we had this curious combination in terms of timing, and they’ve enjoyed much more open access to western markets as a consequence of the Santiago Principles. But the principles are not a guarantee, it’s a ‘we will try and do this’

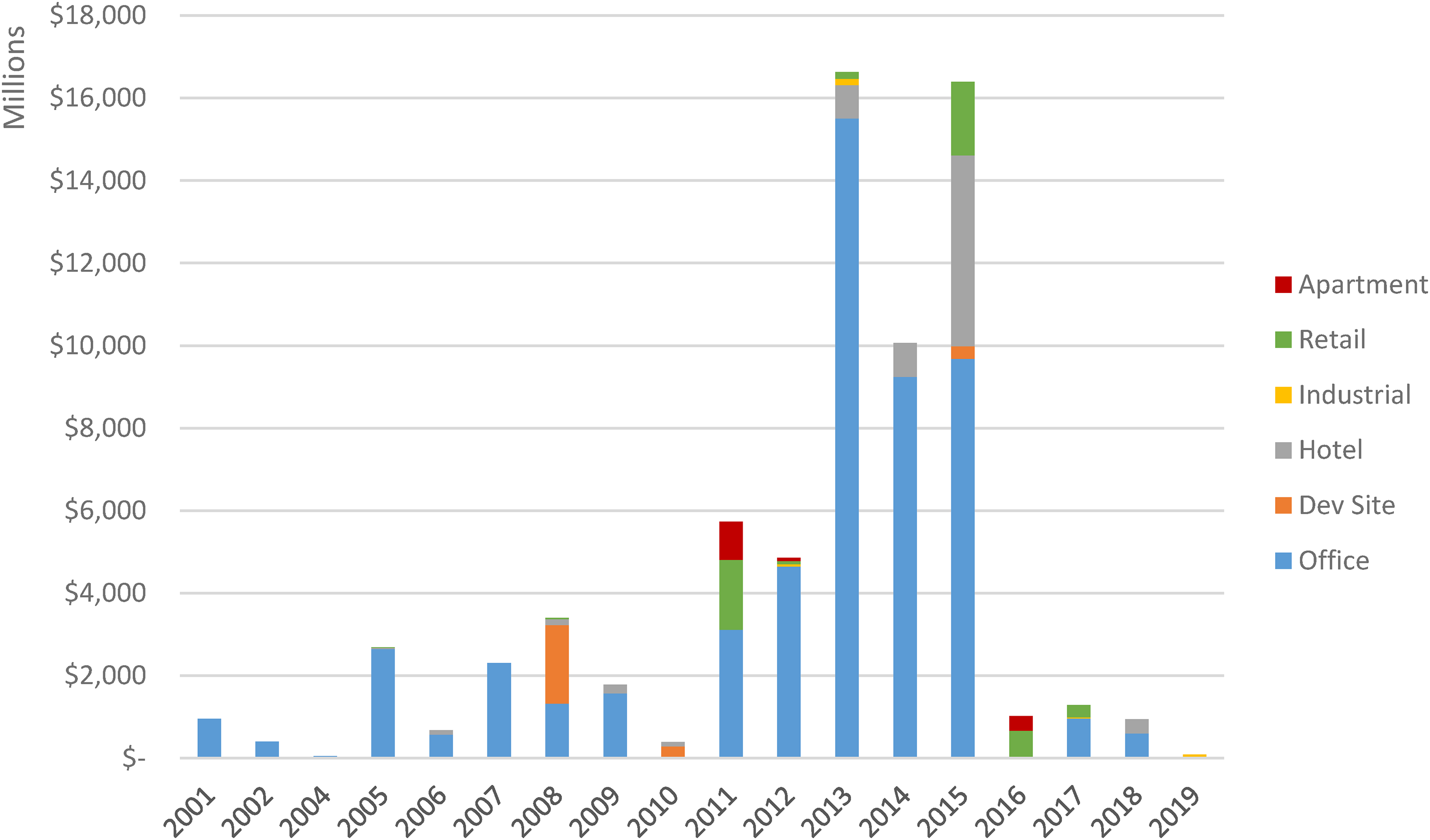

Nevertheless, the outward commitment to acting in accordance with market rather than political principles combined with the post-2008 appetite for counter-cyclical international investment saw an influx of SWF capital into real estate markets across the globe. Today this is a very significant portion of the global market, with SWF investment accounting for 30% of Assets Under Management tracked by the alternative assets database Preqin in 2021. While their initial rounds of post-crisis investment focused on distressed firms and banks, SWF investment flowed into London real estate during the post-2010 recovery, as is observable in Figure 1.

Transactions involving sovereign wealth funds by type, London metropolitan area, all time RCA history, downloaded March 2021.

The majority of this investment is in commercial office space, an asset class which is well-established and typically considered to be of institutional grade quality. This reflects tactics of many SWFs who seek out long-term investments and trophy assets with low levels of risk exposure. Notably, the intensification of SWF investment into real estate coincided with the election of the 2010–2015 Conservative-led coalition government. However, interviewees were sceptical of this being a direct causal factor. Instead, they pointed to market conditions of a general boom in London real estate in the period, with the drop off after 2015 attributed primarily to a crash in oil prices around that time and end of this boom as opposed to any specific domestic causes.

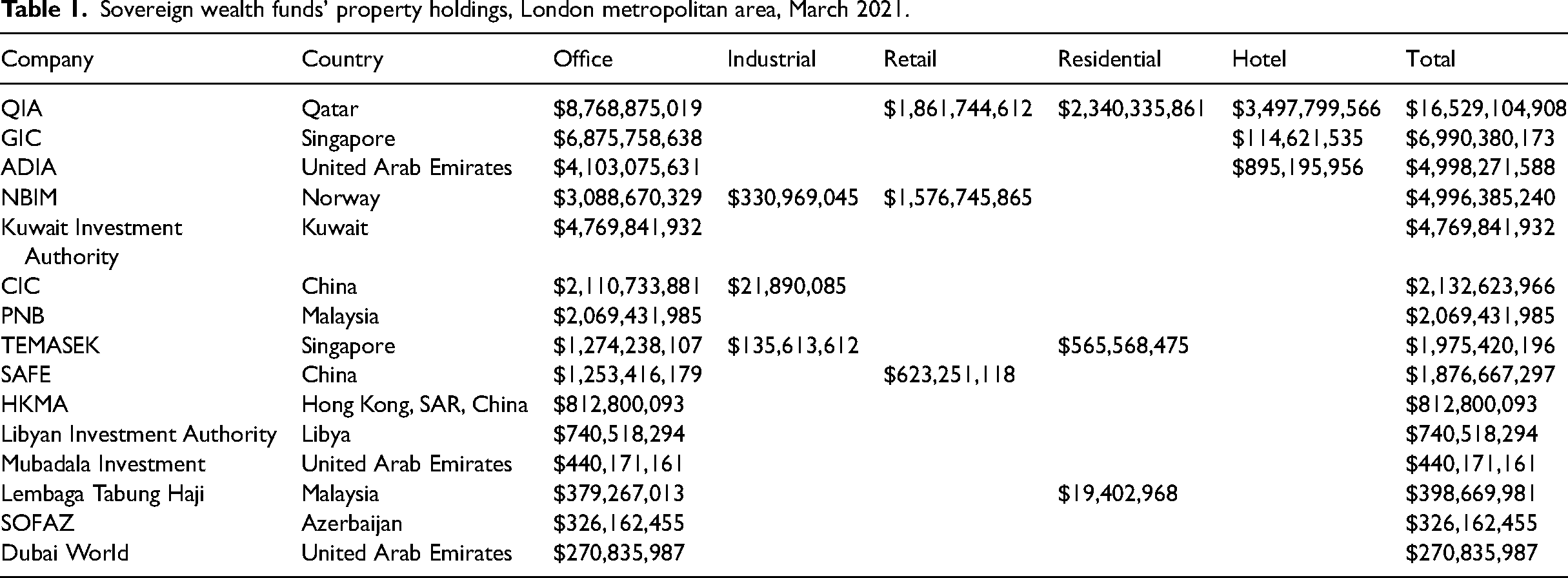

In this post-crisis period, the Qatari Investment Authority (QIA) became the largest player on London’s real estate market. Its property holdings have an estimated value of $18.6bn according the Real Capital Analytics database, 2 by some margin ahead of the next largest, the listed REITS British Land ($12.3bn) and Landsec ($7.7bn). Of the top 20 largest property holdings in the London metropolitan region, 5 were SWFS (not including the 20th largest, the UK monarchy’s own ‘Crown Estate’, which is not a SWF but ‘the sovereign’s public estate’ and is described in the RCA database as an ‘endowment’). SWFs have become an integral part of London’s real estate landscape. Table 1 shows the quantity and type of SWF property holdings in the city, demonstrating the scale of QIA and a strong preference for office investments.

Sovereign wealth funds’ property holdings, London metropolitan area, March 2021.

Given its size in the London market, we focus on the Qatari Investment Authority to explore the geopolitics of SWF investment into London real estate. We overview Qatari investment into London real estate from the perspective of both receiver and originator country’s political economic strategies. First, we contextualise the priorities of Qatar’s SWF within the wider state project in which it is embedded, pointing to how crucial geopolitical and domestic considerations shape their investment strategy. Second, we consider this from the perspective of London’s governance, focusing on QIA’s investment in the Olympic Village and how this furthered political economic aims in both originating and receiving countries.

Sovereign investor motivations: Qatar’s quest for security

Mindful of the need to engage with the relational nature of governance to go beyond the territorial trap (see Raco et al., 2020), in this section we consider the context of Qatar’s investments from the perspective of the originator country. Here, investment is geared towards strategic coupling and diversification of the originators’ economy in what Haberly (2011) termed the ‘new state-led alliance capitalism’. However, such state-led investments are motivated by domestic politics as much as any geopolitical concerns (Braunstein, 2019; Helleiner, 2009; Huat 2016; Shih 2009). In this section, we consider the motivations of QIA within the context of Qatar’s wider project to use soft power to secure the state.

The heterogenous motivations of state-led actors such as SWFs have shaped their investment priorities in contrast to market actors who work to clear metrics centred on defined risks and profitability. For instance, the particular focus on super-prime trophy assets amongst SWF is attributable to their low risk, prestige, and fit with the scale of investment (scalability being one key reason they have tended to prefer the commercial market over residential). However, an investor specialised in working with sovereign bodies emphasised that this risk was not in line with each SWFs’ liability profiles as would be expected in traditional asset allocation theory (a common approach for institutional investors in property), but instead was more closely related to domestic political concerns: … it is noteworthy how many of them have adopted this style of investing: trophy first and then more mainstream investments after … I don’t want to say that this is not sophisticated investing, but it reflects some of the pressures that they are under… I think the way to think about it is they are not liability driven because they don’t know what their liabilities are and that’s not their fault, the government or sheikh or whoever, doesn’t give them a liability framework. It is a] don’t mess up, b] do a good job.

The relevant metric of success for SWFs, this investor argued, is perceived success in comparison with neighbouring countries funds’, creating emulation pressures driven by a fear of being left behind rather than selecting investments according to a particular portfolio strategy as private investors would. SWFs combine investment with political logic rather than the two being mutually exclusive (Haberly, 2011; Lenihan, 2014), as achieving returns and economic diversification is itself a key political aim. However, fostering a perception of SWF success amongst domestic stakeholders is more critical than market indicators of success or shareholder value, creating a marked difference with traditional private sector investors (see Huat 2016; Shih 2009). As a result, trophy real estate is a particularly attractive investment for SWFs in terms of constructing domestic political legitimacy because it is prestigious and its value is untransparent compared to investing in a listed company whose value is constantly and publicly tracked.

Further, in Qatar’s case, geopolitical motivations of securing the state through capital diplomacy are at the core of its SWF’s overarching strategies. Qatar is a small state with a population of circa 2.8 million, about 300,00 of which are Qatari citizens and the rest expatriates (primarily migrant workers). Having few resources until the lucrative mid-20th century discoveries of oil and (more recently) gas, Qatar was historically reliant on navigating alliances with more powerful regional and global powers. Its foreign policy was effectively under the auspices of the British from the colonial period until independence in 1971 after which, choosing not to join the United Arab Emirates, it relied on Saudi Arabia. Qatar’s contemporary strategy has its origins in Saudi Arabia’s weakened position as a regional power after the 1990s Gulf War and a souring of Qatari-Saudi relations following the bloodless coup from Khalifa bin Hamad Al Thani to his son Hamad Bin Khalifah Al Thani at that time (Roberts, 2012). This precipitated a new answer to the question of how the small state would navigate its defence. As an expert on UK-Qatari relations we interviewed explained: The question is, how do you secure Qatar, how do you secure the state? [Khalifa bin Hamad’s] answer was, ‘you don’t do anything and you hide under Saudi Arabia’s auspices. You hide yourself from view’… [but Hamad Bin Khalifah’s regime] had these sentiments that Qatar must and should be a deeply internationalised state in order to secure itself and so that is the core of their thrust… If you multiply all your friends, then there’s a security in numbers.

As Qatar’s natural gas discoveries made it extremely cash rich throughout the 2000s, they continued pursuing this strategy through the establishment of QIA in 2005. This was controlled by a key Hamad Bin Khalifah Al Thani ally and force behind Qatar’s foreign policy shift, Hamad bin Jassim Al Thani, who one expert interviewee argued ‘used it as a personally driven kind of fund he used to augment Qatar’s foreign policy’, reflecting the long-standing close intertwinement of the Qatari state, capital accumulation and its royal family (Hanieh, 2018). The SWF was therefore heavily influenced by domestic politics and a geopolitical strategy of soft power projection as Qatar sought to become an internationalised foreign policy player to ensure its own survival independent of Saudi Arabia.

Thus, the Qatari Investment Authority is part of a two pronged strategy to promote Qatar in diversifying its revenues and internationalising the state, blurring the lines between foreign policy and economic objectives. Since Hamad bin Jassim Al Thani was removed from his posts when Hamad bin Khalifa’s son (Tamim bin Hamad Al Thani) came to power in 2013, the fund is perceived to have made an effort to professionalise. However, the foreign minister of Qatar, Mohammed bin Abdulrahman bin Jassim Al Thani, remains the chairman of the SWF at the time of writing.

This intertwinement of foreign policy and economic motivations in securing Qatar was demonstrated when the 2017–2021 economic blockade of Qatar by neighbouring countries (led by Saudi Arabia and the United Arab Emirates) disrupted supply chains and closed land access to the country. With Qatar reliant on imports via land for 80% of its food, the division of QIA tasked with achieving food security, the Hassad Food Company, arranged food imports by air from allied countries in the initial months of the crisis and invested into infrastructure to create a domestic dairy industry which claimed to have achieved self-sufficiency by 2019. More intangibly, the relationships Qatar had fostered through the country’s internationalisation were crucial in diplomatic efforts to counterbalance the influence of its Gulf rivals during this geopolitical crisis, as the military expert we interviewed reflected: It’s about forging personal relationships up and down London, from the City and through Whitehall and I imagine that the Qataris can command an audience with whomever they want, whenever they want. They’re not alone, in the Gulf, in being able to do that, but… I think it’s very clear that the Qataris are an ally of such proportions that the UK would be loath to really go against their interests… Almost certainly, they felt they had such an investment, a metaphorical and very literal investment, that there’s no way that Britain could have sided with the UAE [in the blockade].

Attending to Qatar’s fraught regional histories, we have argued that the QIA combines economic and foreign policy motivations as part of the overarching project of securing the Qatari state. This blurring of the strict distinction between economic and policy objectives promised by the Santiago Principles is not unique to Qatar or the Gulf states, but reflects analysis on the literature on East Asian SWFs as to their role in shoring up domestic legitimacy while securing the state (Helleiner 2009; Huat 2016; see especially Shih, 2009, on Singapore). In the next section, we consider how these state-driven investment priorities embedded into the London real estate market were furthered the governance projects of the receiving country.

‘Dubai on Thames’: SWF investment in London

The flood of Qatari money into post-2008 crisis London caused consternation in public discourse as to what the BBC referred to as ‘buying Britain by the pound’ (Robertson 2017). Or, as the UK Secretary of State for International Trade summarised these investments in 2016: ‘It is no exaggeration to say that, through these ventures, Qatar has become part of the fabric of our nation’ (Fox 2017). Numerous deals for skyscraper commercial office space with various SWF actors were reached with the active solicitation of mayor Ken Livingstone as part of his strategy to attract investment and create London landmarks, leading Boris Johnson to complain of a developing ‘Dubai-on-Thames’ during his successful 2008 mayoral campaign (Moore 2016). Despite this, once Johnson was in power London saw its most intense period of SWF investment into real estate, including several high-profile mayoral projects that required investors with generous funding and an appetite for risk. Throughout this paper, we have highlighted that such state investments produce geopolitically inflected ‘relational regulation’, as a key component of uneven and combined state capitalism. In this section, we thus consider how QIA’s state capital investment impacted the regulation of London’s built environment.

Infamously, Johnson’s courting of SWF investment to achieve his flagship projects included investment by the United Arab Emirates to fund a cable car project in a sponsorship deal which initially included stipulations that London’s transport authority could not deal with Israeli businesses and the mayor would not criticise the UEA government. These restrictions were subsequently removed after public outcry, but illustrate the combination of political and economic factors in state capitalist investments as well as the urban diplomacy required of receiver governments as they seek capital to fuel their own domestic political agendas through market means. Beyond funding Johnson’s predilection for eye-catching vanity projects, however, SWF’s political orientation and associated willingness to risk large investments on flagship or strategic projects made them key partners in the UK’s efforts to deliver social aims through market means.

We expected this such SWF involvement to impact the regulation and outcomes of specific developments, but was judged by our interviewees to have little impact at the project level. While acknowledging their geopolitical motivations, London planners and local politicians we interviewed argued SWFs to be no different than any other forms of overseas and domestic capital flowing through the city. Interviewees attributed this lack of impact on the form of the development to SWFs’ utilisation of joint ventures with UK-based partners largely responsible for operational management, an investment structure which allowed them to embed within the local context while avoiding direct reputational risk. However, London planners we interviewed did note that the different motivations of SWF investment enabled different types of development, as a private sector London planning consultant reflected: I think it’s just capital, if I’m honest Perhaps a different way of looking at it would be not does it affect the development, but does it affect whether development happens. It’s certainly the case that [major projects in London’s docklands area] wouldn’t have happened without an international investor, without the Chinese Government putting in a billion pounds through their vehicle. Now, the nature of the scheme itself is going to be identical if it was British money or Chinese money… but you probably wouldn’t have found a British investor who was going to put that amount of money into that site, in that location.

In this sense, the presence of SWFs was not perceived to impact development outcomes or day-to-day regulation, but did impact wider London strategic planning in providing capital for large projects that otherwise would not find funding. In addition to the £1.7bn flagship regeneration of east London’s Royal Albert Dock by Chinese developers the interviewee referred to, the £9bn redevelopment of Battersea and Nine Elms (see Hofman and Aalbers 2019) was delivered by a consortium of Malaysian state-owned companies: whole neighbourhoods of London have been transformed by state-led or -influenced ‘patient’ capital investment over the past decade. Similarly, QIA investment was critical in the redevelopment of the East London Olympic Village area.

The Athletes Village in East London was a low-income area dramatically transformed during the lead up to the 2012 Olympics (Watt, 2013). QIA invested in this project through a wholly owned subsidiary, Qatari Diar, in partnership with real estate advisory firm Delancey. This joint venture, QDD, purchased 6 plots of developable land, ‘The East Village’, on the former Olympic site in partnership with Triathlon Homes (in turn a joint venture between two UK housing associations and an investment company). At the same time, QDD directly invested in Get Living, a new company formed in 2013 by experts from the hotel industry and private rental sector, specifically to develop and run institutional-quality rental property for investment. QDD’s investment enabled Get Living to purchase 2 of the East Village plots for conversion into Build-to-Rent (BTR) housing. This approach made QIA the sole investor in the redevelopment of 1439 homes from the former Olympic Village, resulting in homes aimed at middle class professionals with almost half meeting the government’s criteria of ‘affordable’. That QIA were willing to take the risk of being the first mover in a nascent market was argued by interviewees to be, in part, demonstrative of QIA’s ‘soft power’ investment approach. Specifically, the East Village allowed QIA to place themselves as central the perceived success of the 2012 Olympics in providing ‘the first leading legacy neighbourhood for London’ (www.qataridiar.com/English/OurProjects).

Significantly in terms of London’s public policy aims, East Village became the first BTR site to open in the city and preceded several more investments into the sector. QDD is understood in policy-making circles as integral to the emergence of a new asset class which UK governance bodies have fostered in order to leverage in addressing the housing crisis (Brill and Durrant, 2021). BTR is a rapidly developing market with almost 200,000 homes in the pipeline across the UK with QIA’s investment giving them the first mover advantage. Their partners see themselves as ‘proud pioneers’ (Get Living, n.d.) and have used this market position to align themselves as an indispensable cornerstone of the BTR development market in policy-making circles. In this regard, the involvement of SWF as a form of institutional investment is a successful example of what the British government explicitly set out to achieve in fostering this sub-market (see Department for Communities and Local Government 2012): institutional investment into the UK’s housing market to address the failures of existing stock.

The Olympic Village BTR development is thus an example of the intersection of state capitalist (as state-led market actors) and capitalist statist (as market-oriented state intervention) projects’ strategic coupling as both seek to exercise forms of soft power. While entering the residential market is somewhat unusual for SWFs, the specific features of East Village advance the priorities of the Qatari state. Through this investment the Qataris furthered their informal networks across the British establishment in working closely with prominent London and UK politicians (including the then-mayor and future Prime Minister Boris Johnson). Their association with both the perceived success of the Olympics and promise of regenerating a deprived area of London met goals to enhance their profile internationally and offered a prestigious investment to satisfy domestic stakeholders. To this end, the regeneration of the Olympic Village afforded a risky but promising asset whose day-to-day value is untransparent, satisfying a political corporate governance structure which lacks performance metrics beyond the prime directive of ‘don’t mess up’ (per the interviewee quoted in the previous section).

From the perspective of London and UK governance actors, meanwhile, a strategic planning aim of attracting institutional investment into east London’s post-Olympic regeneration projects was met expediently. The Olympic Village investment provided a launch pad for the new BTR asset class designed to address London’s housing crisis through the attraction of patient capital. This project of a state-fostered asset class designed to channel private investment into profitably ameliorating public policy problems thus intersects with QIA’s geopolitically inflected investment strategies in an example of relational regulation within contemporary combined and uneven state capitalism.

Concluding discussion

In this paper, we responded to this special issues’ calls for a multiscalar, historicised approach to state capitalism (see also Alami and Dixon 2020) through an exploration of the geopolitics of SWF investment in London’s real estate market. First, we rejected the dichotomy implied by the use of ‘state capitalism’ in mainstream discourse and international relations literature, as a term offering implicit contrast to a presumed Anglo-Saxon free market liberalism. Rather, we argued, that strong state intervention is integral to contemporary capitalist political economies (Block 2019; Svitych 2021) in which the question is how and to what end state power is constructed and wielded. We thus proposed the term capitalist statism to contrast the ‘state permeated market’ (Nolke et al. 2015) of the state capitalist literature with the UK’s subordination of public policy to private profitability while staying within the framework of a combined and uneven ‘muscular statism’ (per Alami and Dixon, 2021). Exploring the strategic coupling of a London government seeking to ameliorate public policy problems by creating investment vehicles for ‘patient’ capital and the state-led institutional investors which often constitutes this patient capital, we contextualised the motivations of the QIA and how their investment in London’s Olympic Village has contributed to state projects in both countries.

While sovereign investment appeared to have little impact on the day-to-day operation or regulation of developments, its presence shaped what could be built and so significantly changed London’s strategic planning overall. There is a tension here that despite its free market rhetoric, the UK’s market-led economic recovery through pumping up real estate assets and channelling international patient capital entails the multiplication of fundamentally geopolitical entanglements. While the Santiago Principles’ commitment to transparency and following market rather than political incentives promise to guard against this, the case study of Qatar underlined that such funds are dependent on domestic political sentiment and geopolitical aims in their seeking of economic returns. It is precisely this blurring of the line between public and private priorities embodied in SWF investment (Raphaeli and Gersten, 2008) that have made them an attractive partner in UK public projects dependent on private sector investment such as QIA’s entry into the East Village, kickstarting the UK’s strategy to channel patient capital into an emerging ‘build to rent’ asset class in order to address the city’s housing crisis (Brill and Durrant 2021).

In this, the strategic coupling (Haberly 2011) identified in supply chains is also identifiable in the geopolitics of real estate, as public policy aims and local elite projects find favour from state-led or influenced investment such as SWFs. However, while the political logics of state capitalist patient capital actors have made them useful partners. Post-2015 SWF investment into London has slowed down to a trickle (see Figure 1) with the end of its office boom, shocks to oil prices and Brexit; raising the question of whether sovereign investment will remain a viable source of international investment to sustain London’s market-mediated state projects. Moreover, geopolitical considerations such as conflict amongst the UK’s largest Gulf investors during the blockade of Qatar and trade tensions with China are coming to the fore in an increasingly fractious geopolitical environment, driving regulatory and public awareness that SWFs are ultimately sovereign actors closely bound up with their originating state projects. Further research on the role of SWFs in the geopolitics of real estate is required to explore the impacts of growing political tensions on the relational regulation of regional property markets, and whether and to what extent we are seeing ‘strategic decoupling’ as SWFs appear to be turning their attention away from Europe amidst geopolitical and geoeconomic realignment. The associated politicisation of transnational real estate investment and institutionalised landlordism has been thrown into sharp relief by Russia’s recent invasion of Ukraine and a UK government response which in part centred on sanctioning prominent Russian citizens’ extensive London real estate assets. Amidst increasing geopolitical tensions, the relational regulation of economic activities will be a crucial sphere of contestation.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The researchers gratefully acknowledge the funding and support of the Economic and Social Research Council UK [Grant Number: ES/S015078] under the Open Research Area project ‘WHIG What is Governed in Cities: Residential investment landscapes and the governance and regulation of housing production’.