Abstract

The past decade has seen a resurgence of interdisciplinary interest in fiscal studies, from the new fiscal sociology to fiscal geographies and beyond, with roots in the 20th century theories of Schumpeter (liberal) and O’Connor (Marxian). The notion of a ‘tax state’ remains particularly germane, and indeed fiscal studies have all but narrowed to assessments of the relations and implications of taxation. This paper calls for a meaningful engagement with the ‘fiscal’ in fiscal studies where taxation is better understood as being but one component of public sector revenue and expenditure (alongside other important features like asset ownership, debt/credit, and intergovernmental transfers). More than an academic quibble over terminology or unit of analysis, narrowing ‘fiscal’ to ‘tax’ obscures many budget items and misses out on important temporal trends in the political economy of state revenue and expenditure. These issues are explored in two parts: the roots of fiscal studies (politicizing theoretical underpinnings), and the various conjunctural features of the fiscal state (tracing the temporal through Canadian examples).

Beyond death and taxes: Fiscal studies and the fiscal state

Fiscal studies have experienced an interdisciplinary resurgence over the past decade. Under the banner of the new fiscal sociology, a term derived from Schumpeter and chosen “to suggest a science that would transcend increasingly narrow disciplines and unite the study of economics with the study of history, politics, and society,” Martin et al. (2009: 1–2) argue that “… a new wave of multidisciplinary scholarship on taxation is poised for a significant intellectual breakthrough … recogniz[ing] the central importance of taxation to modernity and produc[ing] innovative comparative historical scholarship on the sources and consequences of taxation” (Martin et al., 2009: 1–2). Likewise, Mumford (2019) tags fiscal sociology as “the theoretical, sociological study of tax policy formation” (Mumford, 2019: 11). Areas of study in fiscal sociology include: comparative tax policy, taxpayer consent, and the social consequences of taxation (Martin et al., 2009), along with the social processes informing public sector budgeting (Mumford, 2019), and taxation as cause and consequence of poverty and inequality (Martin and Prasad, 2014; see also Campbell, 1993; Musgrave, 1992).

In geography, Tapp and Kay are also interested in ‘placing’ taxation by illuminating the ways in which “[t]he tax system … plays an outsized, but often overlooked, role in the urban process” (2019: 1). Termed, ‘fiscal geographies,’ this is said to be distinct from financial geographies, even if ‘co-produced’ (on financial geographies, see Aalbers, 2018; Hall, 2011). The thematic trends in fiscal geographies identified by Tapp and Kay (2019) are: governance and politics, urban development and infrastructure, housing and gentrification, and policy mobilities and expertise. By shifting the focus “toward the specific ways that states – at all scales – are actively shaping these [urban] processes through tax and other budgetary systems, a new picture of the city comes into view” (Tapp and Kay, 2019: 1).

Calls for greater attention paid to fiscal dynamics in geography echo across the decades as Cameron’s (2006: 236) earlier assessment similarly held that “the geographies of taxation offer … important but neglected insight[s]” and that “despite the significance of taxation to the economic, social and political geographies of the state … geographers have been notably absent from debates about fiscal space” (239). Like Tapp and Kay, Cameron argued that fiscal studies are important in economic geography but tend to be subsumed within other more dominant themes like welfare, poverty, cities, economies, regionalism, and so on (Cameron, 2006).

The study of the fiscal state is often narrowed to taxation: “A founding principle of fiscal sociology is that there are few, more important, scientific indicators than how taxes are designed, collected and spent” (Mumford, 2019: 11). Indeed one of the longstanding contributions of a fiscal sociology approach is its insistence on the ‘tax state’ as a core actor in capitalism. Tapp and Kay too identify the importance of the tax state in their review of budding fiscal geographies (2019: 7). A limitation of this focus (whether sociological, geographical, or otherwise) is that the fiscal activities of the state extend well beyond taxation to include a broad range of credit and debt services, procurement and universal program spending, intergovernmental transfers, the remittances of state owned assets, and myriad other fiscal activities. As we shall see, founding fiscal studies theorists Joseph Schumpeter and James O’Connor offer a variety of insights on the fiscal state writ large. Schumpeter informs a tradition of fiscal sociology that looks for pluralistic drivers of taxation policy (the tax state) but more generally provides political economy with theory emphasizing the state’s need for autonomous sources of revenue in light of distinct public and private spheres in capitalism. O’Connor fits within the Marxian tradition of class conflict-oriented analyses of public policy and thus his work attends to the state’s role in providing support for capital accumulation and legitimation through fiscal levers (the capitalist state).

Fiscal studies theory equally urges an historical lens. For Schumpeter, taxes bring in revenue for the state; taxation is not an end in itself. His assessment emphasized taxation because it was the central mechanism of funding European state power at the time of writing. With the forms and roles of the state having changed dramatically over the few decades that separated Schumpeter from O’Connor, the latter’s late Keynesian era assessment highlighted other dimensions of the fiscal state like intergovernmental transfers and social services. Through different routes, the roots of fiscal studies theory support its broadening beyond the here-and-now of taxation. This is not to suggest that taxes are in any way unimportant, only that tax alone cannot sufficiently uncover the capitalist dynamics at play (whether involving liberal interests or Marxian conflicts). Accounting for the conjunctural, or historical context of the fiscal state, likewise clarifies the multitude of state revenue and expenditure forms over time.

This paper contributes to interdisciplinary fiscal studies, and fiscal geographies more specifically, by clarifying the theoretical-analytical dimensions of fiscal studies and temporalizing the fiscal activities of the state. The paper argues for a meaningful engagement with the ‘fiscal’ in fiscal studies, finding tax obligations alone to be an insufficient measure of the fiscal. More than an academic quibble over unit of analysis or terminology, slippage from ‘fiscal’ to ‘tax’ unduly narrows the political economy of public revenue and expenditure in capitalism, omitting roles and obligations relating to public ownership, debt/credit relations, transfers, and epochal trends in state support for accumulation. Expanding the remit of fiscal studies to include a fuller range of revenue and expenditures beyond taxes more accurately captures how states govern, implement changes over time, and thwart or enable social struggle. It equally allows for more multi-faceted analyses of how/where/when fiscal and financial interests intersect, and the geographical implications of the fiscal state. In short, an expanded definition of ‘the fiscal’ does more than merely add areas of study – it enables a better understanding of the state and state-society relations in capitalism.

There are two main sections to the paper: one on fiscal studies (theory) and another on the fiscal state (empirics). First, the theoretical roots of fiscal studies are assessed to politicize the ideological dimensions of tax/capitalist state analysis and its contours. Second, several conjunctural roles or historical eras for the state as a fiscal actor are identified. Traced through the Canadian case, this history indicates wide variation in the political economy of state revenue and expenditure dynamics, with the nature of taxation, ownership, debt/credit, and transfers oscillating across (overlapping) governance epochs: settler-colonial, developmental-nationalist, Keynesian-liberal, neoliberal, and the crosscutting theme of the state as crisis manager.

Fiscal studies

Schumpeter’s tax state and O’Connor’s capitalist state are important foundational concepts in interdisciplinary fiscal studies, with Schumpeter tending to inform liberal variants, and O’Connor Marxian analysis. They may also be usefully combined to indicate a sequence of expanding state purview and interests over time, as capitalism develops and within distinct national contexts. 1 Whether contemplated separately or apart, both theorists urge a broader view of ‘the fiscal’ given that the end goal is revenue and power (to fulfill capitalist state roles and particular sectional desires). Thus today’s ‘tax state’ is a misnomer given that taxes make up on only one aspect of state revenue and expenditure. Other relevant budget items include dividends and interest earned off assets, transfers from other levels of government, and debt/credit obligations.

Using Canada’s federal 2019 budget as an example (Department of Finance, 2019), we see multiple sources of revenue and expenditure, ripe with intersectional consequence. For the operating budget, revenue is drawn from: income tax (personal, corporate, non-resident), excise taxes/duties (e.g., Goods and Services Tax, customs import duties), fuel charge proceeds, Employment Insurance premium revenues, enterprise Crown corporation revenues, and net foreign exchange. Operating account expenses include: transfers to persons (elderly, Employment Insurance, Canada Child Benefit, etc.), major transfers to other levels of government (Canada Health Transfer, Canada Social Transfer, Equalization, Territorial Formula Financing, Gas Tax Fund, etc.), direct program expenses (e.g., fuel charge proceeds returned, other transfer payments, and operating expenses including capital amortization and depreciation). Beyond that there is the capital budget with transactions relating to pensions, non-financial assets, loans, investments, advances, enterprise Crown corporations (state owned enterprises), accounts payable, receivable, accruals, allowances, and real property assets.

Taxation is far from the limit of state revenues and expenditures and yet some descriptions of fiscal sociology slip from tax to revenue without acknowledgment. “Indeed, tax revenues are the ‘life-blood’ of the modern state,” writes Campbell (2009: 256) “… Without them it is hard to imagine how states could sustain welfare or defense programs; maintain infrastructures like roads, airports, schools, and public transportation systems; regulate business and markets; enforce property rights and the law; or support commerce. To be blunt, without revenues it is inconceivable how states could provide the support necessary for capitalism itself.” Descriptions such as these conjure insights from Schumpeter (tax state) and O?Connor (capitalist state), and themselves demand an expanded purview for fiscal studies. The theoretical roots of fiscal studies ought not be overlooked; ideological lenses are integral to politicizing what is at stake with changes in state revenue and expenditure in capitalism.

Schumpeter’s tax state

“The spirit of a people, its cultural level, its social structure, the deeds its policy may prepare… all this and more is written in fiscal history. He who knows how to listen to its message here discerns the thunder of world history more clearly than anywhere else” (Schumpeter quoted in Musgrave, 1992: 90).

There is hardly any other aspect of history … so decisive for the fate of the masses as that of public finances. Here one hears the pulse beat of nations at its clearest, here one stands at the source of all social misery” (Goldscheid, 1917, 2; quoted in Musgrave, 1992: 99).

Rudolf Goldscheid (1870–1931), a Viennese Marxist, novelist, and philosopher, coined the term the ‘tax state’ in 1917, one year before the better-known iconoclastic political economist Joseph Schumpeter (1883–1950), arguing that tax struggle epitomized class struggle (Campbell, 1993: 194). 2 Schumpeter did pay homage to this forerunner by, for example, quoting Goldscheid with through his famous line ‘the budget is the skeleton of the state stripped of all misleading ideologies’ (Swedberg, 1989: 516). However, Schumpeter’s extended analysis in The Crisis of the Tax State (1918) traded Goldscheid’s Marxian approach for Max Weber’s pluralism in viewing social, economic, political, cultural, and ideological dynamics as interrelated drivers of public policy.

Turning points, or crises, when older arrangements are replaced with newer ones, are “times which always involve a crisis in the old fiscal methods” (Musgrave, 1992: 90). Such is the purview of ‘fiscal sociology’ and the ‘tax state’ for Schumpeter. “Behind the superficial facts of budgetary data, the nexus between fiscal affairs and social structure must be understood, and their historical interaction must be examined” (Musgrave, 1992: 90). Schumpeter traced a deep history for the tax state, with origins located in feudal Austria and Germany of the fourteenth and fifteenth centuries when the tax state was born of a crisis in the fiscal system and relations of princes to feudal lords. He offered a detailed and complex lineage but for our purposes here it is enough to summarize that through this history the modern state becomes the “representative of a common purpose” (Schumpeter quoted in Musgrave, 1992: 92). Distinct public and private social realms were created out of an historical fiscal crisis and yet the state with its ‘common purpose’ was left without autonomous fiscal means. Fulfilling the common purpose therefore required some mechanism of wealth transfer – the invention of a tax state.

Schumpeterian fiscal sociology is, in other words, a theory of the state; and the tax state both then and now rests on particular social (as opposed to ontological) divisions between public and private spheres. The tax state was an economic parasite given that private market actors generated most revenue in capitalist society (contrast this with Schumpeter’s vision of socialist society whereby neither wages nor taxes are required given that all income returns to government and individuals receive compensation untethered from the marginal product or returns to production 3 ). This parasite had limits, however. Motivations driving capitalist profit making, industriousness, personal savings, and entrepreneurialism (the spirit of enterprise), ought not be unduly limited through heavy taxation (Smart, 2012: 536).

For Schumpeter, fiscal policy was “the central piece of economic policy” for government (Musgrave, 1992: 94). Given that the capitalist market economy requires limited taxation, what or who is taxed matters; therefore the distribution and burden of taxes is at issue. Opposed to progressive taxation and taxes on capital formation, especially entrepreneurial endeavours, Schumpeter favoured consumption taxes (sales, value added, and turnover taxes) rather than income and capital gains taxes (Musgrave, 1992: 94–6), policies promoted both through his academic writing and while Finance Minister in Austria. Schumpeter argued for independent local finance derived through property and consumption taxes because this would, in his view, incentivize taxpayer responsibility and generate fiscal-disciplining competition (Musgrave, 1992: 96). These devices and arguments would seen to be implicated in contemporary financialized urban governance (Peck and Whiteside, 2016), however, he was also insistent on a robust pipeline of grants (fiscal-federal transfers) from central to local governments as a key element in the mix, grants which have been increasingly cut or shunted through neoliberal austerity over the past four decades, prompting local governments to seek out global finance capital as of late.

Despite contributing important work to the ‘tax state’ literature, and his own personal role in directing the Austrian Ministry of Finance in 1919, Schumpeter’s fiscal sociology was limited by its macro scale and approach. Schumpeter’s theory largely ignored internal public sector economics and fiscal policy decision-making, and downplayed the expenditure side of the equation – tax policy simply adjusts to exogenous circumstances (Musgrave, 1992: 103). Schumpeter equally omitted revenue from state owned enterprises, a loose thread picked up in O’Connor’s (1973, Chapter 7) work, as we shall see.

O’Connor’s capitalist state

“The capitalistic state must try to fulfill two basic and often mutually contradictory functions – accumulation and legitimization. … Nearly every state expenditure has this twofold character.” (O’Connor, 1973: 6–7)

Half a century after Schumpeter, James O’Connor (1930–2017) contributed to the sociology of economic difficulties with his The Fiscal Crisis of the State (1973). O’Connor located the American state budget crises of the 1970s in large postwar infrastructure commitments dedicated to supporting monopoly capital (accumulation), social program commitments responding to popular pressures (legitimation), and military programs (coercion). His is a fiscal sociology because the social context of fiscal crisis matters; it is not merely a revenues vs. expenditures narrative of budget crises (Block, 1981: 2). But O’Connor was not simply updating Schumpeter’s vision for fiscal sociology either, instead he flipped the cause-consequence relationship on its head: for Schumpeter high taxes cause problems for capital accumulation/national economic growth, whereas for O’Connor problems with growth create crises in fiscal policy (Musgrave, 1992: 111). 4

O’Connor (1973: 3) defined fiscal sociology as being focused on “the principles governing the volume and allocation of state finances and expenditures and the distribution of the tax burden among various economic classes”. His three categories of public finance are social investment, social consumption, and social expenses; in turn these categories relate to particular social groups and pressures placed on the state, pressures that capitalist states often respond to through increased state spending in order to maintain the legitimacy of an inherently exploitative system. Aside from O’Connor’s work, sociological analyses of public finance were relatively sparse after Schumpeter, Bell (1976) being a notable exception. 5 Schumpeter’s work was limited for its ignorance of private sector reliance on the state (Smart, 2012: 536), an error that O’Connor attended to, as did Goldscheid earlier in noting “how strongly tax exploitation and capitalistic exploitation, the turn of the tax screw and the turn of the profit screw, reinforce each other” (quoted in Smart, 2012: 537). In short, O’Connor’s analysis highlighted social groups (classes) as cost pressures, and connected this with Marxian state theory.

O’Connor described three ways of state moneymaking: tax collection, revenue from state owned enterprises, and government borrowing. With taxes widely covered in the new fiscal sociology literature (Martin and Prasad, 2014; Martin et al., 2009; Mumford, 2019), let us address the other two items. On state owned enterprises, O’Connor states, “surpluses typically are not available to the state treasury because the enterprises normally are not managed by government representatives, but rather by autonomous administrations” (1,973,185). However, the current and historical operation of many commercialized state owned enterprises challenges these views, to be discussed shortly via the Canadian case; similarly, this list omits intergovernmental transfers despite these being of consequence for national economies and subnational states (Peck and Whiteside, 2016). User fees are equally ignored, despite their bearing on state revenue (and their negative impact on access and income). Insofar as government borrowing is concerned, O’Connor highlighted the constraints imposed by credit ratings on local governments. 6 While similar concerns certainly persist today, his writing did not encounter the myriad new forms of debt financing, public-private partnerships, and special purpose agencies innovated over the past few decades to generate off-book funds. 7

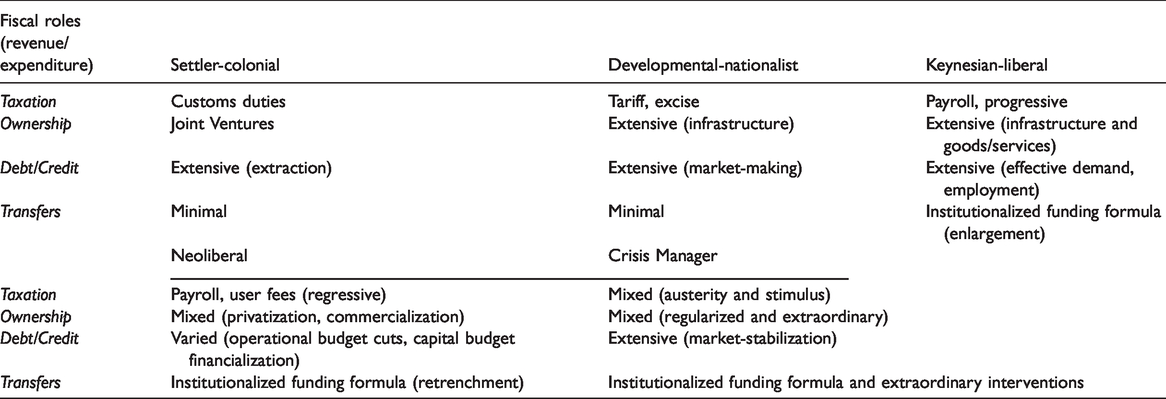

Schumpeter and O’Connor provide contemporary fiscal studies with a solid foundation for both liberal (tax state) and Marxian (capitalist state) investigations. A full application of their theories is, however, limited by their time and place, contextualization being the subject to which we now turn. Temporal changes in revenue/expenditure for the Canadian fiscal state indicate the significance of four fiscal roles (taxation, ownership, debt/credit, and transfers) expressed in different degrees through four historical conjunctures (settler-colonial, developmental-nationalist, Keynesian-liberal, and neoliberal), albeit with some degree of overlap throughout, and a crosscutting role for the state as crisis manager. 8

The fiscal state

“Public finances are one of the best starting points for an investigation of society, especially though not exclusively of its political life. The full fruitfulness of this approach [fiscal sociology] is seen particularly at those turning points, or better epochs, during which existing forms begin to die off and to change into something new” (Schumpeter, 1918: 101).

Moving beyond death and taxes, 9 cataloguing the state’s role in managing the 2020 economic and health crisis suggests several ‘pillars of action’ (ILO, 2020) relevant to fiscal studies today: stimulating the economy and jobs (through active fiscal policy, accommodative monetary policy, lending and financial support to specific sectors), and supporting enterprises, employment, and incomes (extending social protection for all, implementing employment retention measures, and providing financial/tax and other relief for enterprises). While this is a surely an unprecedented time, and the pandemic has dramatically heightened the magnitude of state economic activities, these ‘pillars of action’ retain correspondence with certain general fiscal activities – taxation, asset ownership, debt/credit, and fiscal transfers.

Schumpeter “called for students of public finance to take a comparative and historical approach to their subject and to treat tax policy as both a ‘symptom’ and a ‘cause’ of larger-scale changes in the economy and society” (Martin et al., 2009: 2). Several identifiable phases and forms of fiscal governance are evident with the Canadian state: settler-colonial, developmental-nationalist, Keynesian-liberal, neoliberal, and crisis manager. The Canadian state has always played a particularly active (settler-liberal) role in capitalist market development, with fiscal policy dimensions as evidently both cause and consequence of epochal shifts. Taxation makes no monopoly claim on the political economy of fiscal relations when we look at comparative conjunctures, and how fiscal roles are reflections and drivers of these contexts.

The settler-colonial state pre-dated income and sales tax and drew instead upon revenue at the border through customs duties, featured asset ownership largely tethered to joint ventures with private financiers, accommodated substantial debt-to-revenue levels through credit markets geared toward colonial extraction, and frequently managed bailouts for debt-stricken governments. The developmental-nationalist period saw far greater public ownership and debt, with credit and assets geared toward market-making endeavours (largely through state-funded physical infrastructure), taxation remained limited to tariffs and excise duties, and transfers between governments were miniscule given the lack of social services and safety net. The Keynesian-liberal period saw a dramatic increase in the relevance of taxation and intergovernmental transfers through the institutionalization of funding formulae and progressive taxation (personal and corporate) to support a welfare state, public ownership expanded beyond infrastructure to include social and commercial enterprises, and debt was leveraged to support demand management. More familiar neoliberal fiscal relations brought regressive user fees by emphasizing sales and value added taxes, mixed forms of ownership favouring either outright privatization or partnerships with corporate entities, varied and financialized credit/debt relations, and the dwindling of robust intergovernmental transfers. As crisis manager, across decades the Canadian state appears ready and able to use any fiscal levers necessary to support the renewal of capital accumulation, including stimulus and austerity, regularized and extraordinary bailouts and nationalizations, the ratcheting up of extensive debt to stabilize markets and income, and the use of fiscal transfers to support vulnerable subnational governments. Despite all such conjunctural variations, taxation plays but one part in an intricate web of fiscal-financial relations (Table 1).

Conjunctures of the Extended Fiscal State (Canada).

Settler-colonial

English Canada?s early colonial heritage (from the seventeenth century) largely featured land claimed, regulated, and exploited by the Crown via corporations holding a royal charter. In contrast to the tax state or capitalist state, joint-stock royal charter companies like the Virginia Company and Hudson’s Bay Company were the leading fiscal-legal vehicles of early colonialism and settlement in the British North American ‘new world’. These groups of merchant investors were often known as ‘adventurers’ for their development of transcontinental trade between England and its colonies around the world (see Brenner, 1993), and were responsible for the exploration, extraction, and dispossession that set the tone for settler-capitalism, legal relations, and early colonial state forms.

Colonial British North American governments were scarcely analogous to Schumpeter’s European state as ‘representative of a common purpose’ where taxation was the main fiscal mechanism of wealth transfer. It is worth quoting at length from the Report of the Royal Commission on Dominion-Provincial Relations. Book 1. Canada: 1867–1939 to get the full flavour of the colonial fiscal state – its limits, its responsibilities, and its focused capacities (Rowell-Sirois Royal Commission, 1940: 37): “British North American governments did not […] assume any significant responsibility for social welfare. They took seriously their responsibilities for maintaining defence and internal order but they carried them out with frugal care. … But the application of the [laissez-faire] doctrine was modified by certain conditions peculiar to the colonies. The United States and all European countries at the time had incurred huge burdens for defence. European governments were spending as much as half of their current revenues on military purposes, and the United States had just emerged from a costly civil war. The colonies, relying on Great Britain, escaped most of the costs of military and naval defence. Had they been able to stop at that point, their burden of public expenditures would have been extremely low. However, release from expenditures on defence gave them resources for other tasks and all the colonies took on heavy commitments in aiding economic development. Pioneer communities in North America were always hampered in realizing their dreams of progress by the tremendous difficulties of transport and communications. The scarcity of capital and the scattered nature of settlement added to the difficulties. As a result, the task of securing the provision of community equipment such as canals, harbours, roads, bridges and railways was saddled on government. … The colonial interpretation of laissez faire did not forbid strenuous government activity for developmental purposes. The state was required, by general consensus, to help people to help themselves.”

Developmental-nationalist

Nation-building ambitions (roughly mid-1800s to early-1900s) were largely orchestrated through the creation of a federal-provincial confederation and national development policies stretching from east to west. Confederation itself was intended to create an economy where the whole would be greater than the sum of its parts through domestic trade and industrialization encouraged by a protective tariff, the Hudson Bay land purchase intended to stimulate Dominion development and link Atlantic to Pacific, and a transcontinental railway project financed by private bonds but underwritten by Treasury funds. Mackintosh (1934: 7) summarizes: “The settlement of the prairies, the provision of an all-Canadian transportation system, and finally, the adoption of a protective tariff policy are all… major and related elements of policy in the structure of the Canadian economy.” Conceivable as a proto-capitalist state in O’Connor’s vein of analysis, or when the Canadian state began to assume responsibility for ensuring generalized accumulation, Confederation in 1867 required the integration of distinct colonial economies into a single national market, an ambition equally supported by state owned enterprises. In the early period of industrialization at the beginning of the 20th century, Crown corporations in energy, transportation, and infrastructure were called upon to assist capitalist ambitions (accumulation and dispossession) in Canada.

The significance of the fiscal state and its relationship to political and economic development only intensified when the newly created federal government took on “the pre-Confederation debts of the provinces and was expected to finance the new program of development, to provide for better defence and to assume the major burden of general government and legislation. The budgets of this period show that these expectations were being substantially realized. Virtually all of the Dominion debt accumulated between 1867 and 1896 was incurred for development” (Rowell-Sirois Royal Commission, 1940: 61). Thus intergovernmental debt transfers were an important part of the fiscal mix at the time.

Even within this era of nationalist development, the Canadian economy remained exaction-oriented and connected to international markets and finance, “the financial fortunes of the Federal Government were directly and completely linked to the ups and downs of international trade and investment. As revenues rose with rising imports, the Dominion embarked on large developmental expenditures. This involved the investment of foreign capital, which entered the country in the form of goods. The increase in imports at once swelled the customs revenue. Meanwhile, investment stimulated internal activity, increasing employment, raising wages and consequently improving domestic trade. This increase in domestic trade boosted excise taxes” (Rowell-Sirois Royal Commission, 1940: 61). Needless to say, World I and the Great Depression were a desperate time for many on several fronts, not the least of which were government finances, “The budget was a more prosaic instrument before Lord Keynes revolutionized our understanding of its use as an instrument of economic policy” (Macdonald Commission, 1985: 27).

Keynesian-liberal

Whereas national scale trade-related tariffs (excise and customs duties) were especially important in the 19th century, the tax state in its contemporary sense began in 1942 with the introduction of payroll deductions, a development that “not only employs private business as unofficial state tax collectors, but greatly increases the ability of governments to extract resources from society” (Macdonald Commission, 1985: 27). Modern tax collection in Canada thus enabled the fiscal state as conceived of by Schumpeter and O’Connor. Greater revenue through national payroll tax enabled greater transfers from government to individuals, rising from 7 to 13 percent as a percentage of total personal income from 1950 to 1980 (Macdonald Commission, 1985: 25). A sophisticated system of intergovernmental transfers was ushered in through the creation of a welfare state. As summarized by the Report of the Royal Commission on the Economic Union and Development Prospects for Canada (Macdonald Commission, 1985: 26), “The welfare state, of which we had only episodic evidence prior to the Second World War, has become a complex and comprehensive set of programs which offers collective provision against the normal hazards of life, such as sickness and old age, as well as against particular risks, such as unemployment, which attend economic fluctuations. Private economic actors are linked to the state in a maze of incentives and disincentives, opportunities and obligations. Countless subsidies, guaranteed loans, quotas, tax provisions, technical and research assistance, environmental regulations, and other instruments and policies too numerous to mention affect decision making in the economy.”

The Canadian case stands in contrast here to O’Connor’s American analysis that dismissed the role of state owned enterprises given their unique development (or lack thereof) in America. To quote O’Connor (1973: 182): “In the United States no significant political force has advocated state enterprise (except when private businesses such as urban transit companies cease to be profitable). As early as the third quarter of the nineteenth century the business-dominated courts introduced new criteria making it unconstitutional to use tax moneys for other than ‘public purposes,’ which did not include state enterprises. … During crisis periods (e.g., World War II), monopoly capital has used the state to directly develop and manage directly productive activities in the interests of economic expansion and technical development. However, with the return to ‘normalcy’ the state is rapidly stripped of its capital assets. From 1946 to 1949, for example, the cumulative percentage decline of state-owned producer durable assets exceeded 40 percent.”

Neoliberal

The neoliberal fiscal state is a variant most familiar to the economic geography literature, with related studies largely centering on urban austerity and how these processes implicate scalar dumping, fiscal federalism, theories of local growth, financialized governance, privatization and public-private partnerships, etc. (e.g., Aldag et al., 2019; Fanelli, 2016; Ji et al., 2016; Kim, 2019; Peck and Whiteside, 2016; Rodriguez-Pose et al., 2009; Siemiatycki, 2005; Theodore, 2020; Theret, 1999; Walks and Simone, 2016; Whiteside, 2019; Xu and Warner, 2016). In fiscal geographies more specifically, there appears to be a latent (perhaps unintentional) shift in the literature from more explicitly capital accumulation-oriented perspectives of state fiscal policy (like O’Connor’s) (e.g., Fainstein, 1992; Friedland, 1981; Hill, 1977; Schwartz, 1983) to implicit concern for the pluralistic drivers or implications of tax policy (like Schumpeter’s) in the context of neoliberalization (e.g., Cameron, 2006, 2008; Cirolia, 2020; Tapp, 2019).

To provide but a few details on the Canadian case, the 1995 federal budget restructured and eliminated programs, and cut expenditures to levels not seen since the 1950s (Good and Lindquist, 2015: 59). In 1996, federal health, welfare, and social program transfers to the provinces were rolled into a single block grant funding scheme that limited federal oversight and permitted neoliberal-inspired initiatives by subnational governments (such as tighter eligibility requirements, lower benefit levels, and the introduction of user fees) (Vogt, 1999: 193). A dramatic decline in federal transfers to support urban infrastructure began in the 1980s (detailed in Whiteside, 2015). Unlike in the US (Botein and Heidkamp, 2013; Logan and Molotch, 2007; Peck and Whiteside, 2016; Weber, 2010), tight provincial regulation of municipal debt has effectively thwarted bond use at the local level (Amborski, 2013; Joffe, 2012; Stewart, 2013), and yet urban financialization has nevertheless crept in via municipal housing markets (August and Walks, 2018) and public-private partnerships to develop urban infrastructure and services (Whiteside, 2015).

The neoliberal privatization of state owned enterprises limits the fiscal capacities of the state, and yet public ownership in Canada over this period was also reconfigured such that new/existing Crown corporations now provide a range of financial services that have proven quite significant for the Canadian fiscal state as sources of revenue, transfers, and credit beyond taxation. The Canada Mortgage and Housing Corporation (CMHC), for example, a key state owned enterprise in the national housing sector, shifted from its postwar role of providing veterans with housing services to a Keynesian involvement in urban and low-income housing renewal, and then to a more neoliberal focus on household mortgage insurance and underwriting services, down payment assistance, information services, and selling Canada Mortgage Bonds. Public enterprise roles have changed over the years, but continue to shape the capacities of the extended fiscal state through their governance services, revenue streams, and financial activities (detailed in Whiteside forthcoming).

Crisis manager

While it is true that, “By moving from one fiscal crisis to another, urban scholars fail to capture the long trough of recovery that keeps the state solvent between crises” (Tapp and Kay, 2019: 3), crises are also moments of transition in fiscal policy with significance for social relations as well as the contours and capacities of the tax/capitalist state. Whereas previous sections summarized the historically contextualized activities of the fiscal state with many governance epochs featuring crises big and small, a few examples of post-2008 crisis management initiatives equally underscore the significance of fiscal geographies beyond taxation. 10

In the wake of the 2008 Global Financial crisis, Canadian state fiscal activities included propping up capital accumulation and providing for tax/spending initiatives such as: stimulus and guarantees (credit underwriting, insurance support, etc.), bailouts (asset taking, nationalization), and write-offs. Supporting banking sector liquidity, government began to provide “temporary loans against illiquid assets of questionable and unknowable value” (Walks, 2014: 269), through the Term Loan Facility and the Term Purchase and Resale Agreement, amounting to over $44 billion. The Extraordinary Financing Framework of nearly $220 billion was setup “to guarantee the principal and interest of all new wholesale debt issued by the financial institutions” (Walks, 2014: 269). The largest source of financial assistance for private accumulation was the Insured Mortgage Purchase Program that allowed state owned enterprise CMHC to purchase mortgage-backed securities from financial institutions across Canada up to $125 billion.

State owned enterprises played a market-coordinating role through fiscal-financial levers and direct crisis management. Rather than strictly taxpayer-funded bailouts, fiscal stabilization in Canada was widely provided via the credit/debt services of Crown corporations. Export Development Canada (EDC) and the Business Development Bank of Canada were called upon to provide liquidity assistance in 2009–2010, offering banking sector guarantees of $200 billion through the temporary Business Credit Availability Program (directed by public-private partnership which included representatives from the Department of Finance, the Bank of Canada, Export Development Canada, Business Development Bank of Canada, and private financial institutions). EDC managed, arranged, and financed the GM and Chrysler bailouts as well. With the Business Credit Availability Program later wound down, EDC and the Business Development Bank of Canada quietly continue their longstanding focus on providing financing credit and support to Canadian exporters and Canadian businesses, respectively, including advisory services, venture capital, insurance, and the like. The Canada Deposit Insurance Corporation (CDIC), another Crown corporation, protects Canadian deposits up to $100,000 in the case of a bank failure. In 2017 CDIC was designated the ‘resolution authority’ for Canada’s largest private banks – quite literally the lender of last resort, making public credit mechanisms essential for the health of private debt markets.

Concluding remarks

It is exciting to see a resurgence and expanded interest in interdisciplinary fiscal studies. Schumpeter is less sanguine, for him interdisciplinarity creates “a no-man’s land or an everyman’s land” where disciplinary “cross-fertilization… might easily result in cross-sterilization” (quoted in Swedberg, 1989: 511–512). His caution notwithstanding, the value of interdisciplinary fiscal analyses is that, to quote Goldscheid, “‘the pattern of public finance’, the struggles over taxation policy and measures to meet common needs, and the ‘immanent contradiction between capitalist economy and socially productive public economy’” are cross-disciplinary in nature, and “the pattern and evolution of society determine the shaping of the interrelations between public expenditure and public revenue” (Smart, 2012: 534).

To the interdisciplinary fiscal studies literature, this paper adds: the political economy of fiscal policy extends well beyond taxation; a broader sense of public revenue and expenditure can better capture the sociological, geographical, and political economy dimensions of the fiscal state. Along with taxation, ownership, debt/credit, and transfers round out the list. Understanding the implications of each category, together with their relative importance and composition, requires contextualization and temporal framing. Evidence from the Canadian context suggests that fiscal studies can be usefully differentiated by epochs (themes, timelines, or conjunctures) in state governance: settler-colonial, developmental-nationalist, Keynesian-liberal, neoliberal, and crisis manager. Other countries and levels of government likely have their own unique timelines to contemplate.

Contextualization equally provides insight into theory development. The early fiscal studies theory of Schumpeter (1917–8) appraised a world where capitalism was not yet ‘ecologically dominant’ (Jessop, 2002), there were plenty of rival economic systems on offer and much associated social conflict (class struggle, war, and revolution) surrounding the still-palpable demise of feudal relations set amid world wars, enthusiastic socialism, incubating fascism, and the decline of empire. Structural change and seemingly-imminent social transformation bred an economics of possibility for reconstruction and alternatives. Taxation was thus debated and analyzed not just for its capitalist relations but also for what, if any, role it held in socialist transition, to fund imperialism, and fuel wars of domination. Global capitalism is now largely consolidated and thus the ‘tax state’ and issues of fiscal-federalism take on different implications. O’Connor was also writing at a time of dissolution and disruption, but the 1970s were not, to use Jessop’s (2002) distinction, a crisis of the system, but rather in the system – the tumult of the 1970s witnessed a paradigmatic shift from Keynesian redistribution and more direct forms of state management in capitalism to neoliberal regressive redistribution and fiscal-financial support for capital formation.

Riven through four fiscal roles (taxation, ownership, debt/credit, and transfers) expressed through four historical conjunctures (settler-colonial, developmental-nationalist, Keynesian-liberal, and neoliberal), is the fiscal state as crisis manager given the inherent instability of the capitalist system. Crisis management is witnessed most clearly today in the context of the 2020 pandemic and its capitalist implications (production, reproduction, circulation, and distribution), to say nothing of the dramatic impact on health, wellbeing, and daily life. One evolving feature of the current crisis is the expansive role played by the fiscal state in commanding the economies of otherwise liberal laissez-faire countries. The parallels with wartime governance are plain, less obvious are connections running throughout capitalist fiscal governance.

Picking up once more on the Canadian case, we see Air Canada, a national carrier with a global footprint (as part of the Star Alliance), in serious financial trouble after the border closures and other travel restrictions initiated in March, 2020. By late 2020, it has become evident that the Canadian government will likely provide a substantial financial bailout (possibly through an equity stake) in the airline to save it from free-fall (Fife et al., 2020). Air Canada, privatized in 1988 through neoliberal logic, was created in 1937 as a state owned enterprise only after several failed attempts by the Government of Canada to entice private for-profit actors into developing a national airline (Whiteside, 2012). Thus if Air Canada is subject to nationalization once more in 2021, it will not be the unprecedented or unimaginable initiative that most commentators will likely suggest. The airline has already been bailed out twice since being privatized (receiving substantial federal bailouts in 2003 and 2009); nationalization would be a full-circle going-to-ground for the fiscal state in the airline industry. Conjunctural patterns and temporal connections such as these most clearly emerge when we adopt an historically contextualized understanding of the extended fiscal state.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.