Abstract

In this article, we discuss the way offshore financial centres are used by the multi-subsidiary, multi-jurisdictional group structure known as the ‘multinational enterprise’ to arbitrage between social geographies of political jurisdictions. We define arbitrage as the use of corporate legal entities located in diverse jurisdictions to arbitrate a third country's rules and regulations. Using a new method to categorize firm-level data from Van Dijk’s Orbis, we operationalize the notion of arbitrage to systematically detail and compare the structural sequencing choices firms are making, likely in part for reasons of arbitrage. We base our techniques on legal theory of the firm, acknowledging the underpinning of social technologies of law and accounting by which business enterprises are constructed and maintained. We conclude that two specific types of entities, ‘standalones’ versus ‘in-betweeners’, are qualitatively different from others in the activities they perform. We also highlight the existence of liability structures, or ‘fuses’, which typically take the form of a split ownership arrangement. Ultimately, we demonstrate that the position of a firm’s subsidiary within the overall network ecology of that firm is as important as its jurisdictional registration location.

Introduction

Let us consider the following scenario. An American firm interested in setting up a manufacturing facility in Germany has several options. It may opt to set up a German corporation controlled directly through equity ownership by the US parent firm, or it may prefer a controlling structure whereby the parent holds equity in the German subsidiary through an intermediary in the Netherlands. It could have the Dutch subsidiary directly controlled by the US parent or by a Bermudan intermediary controlled, in turn, by the US parent. The firm has a plethora of possibilities. While each permutation ultimately achieves the same aim, an investment in a German subsidiary, each may have different implications on the financial performance of the group, including costs such as taxation.

Why is it that different patterns of investments into the same country may potentially yield different financial returns? After all, the different patterns of ownership are not supposed to affect the financial performance of the German subsidiary in our hypothetical case. Simply stated, the different configurations of corporate subsidiary ownership do not change the economics of the investment, but they change the regulatory treatment of funds flowing out of the investment. Considering that national regulations affect costs such as taxation and the distribution of financial risks and liabilities, the choice of ownership path can have a serious impact on a group’s bottom line. Focusing on a specific genre of corporate subsidiaries located in offshore financial centres (OFCs), this article presents a framework that combines core principles of law, known as entity law (Blumberg, 1993; Ferran, 1999), with an analysis of entity position on corporate chains to differentiate between the diverging tasks performed by subsidiaries located in OFCs.

OFCs typically cater to non-resident clientele (Zoromé, 2007). Why would non-resident clientele seek far-flung financial services, often located in jurisdictions they have little to do with? The literature has tended to assume that the primary attraction of OFCs is low taxation facilitating tax avoidance (Fichtner, 2016; Gumpert et al., 2016; Hines and Rice, 1994; Palan, 2002; Roberts, 1995; TJN, 2019). This might be correct up to a point, but OFCs play other important, albeit neglected, roles in corporate organizations (Boise and Morriss, 2009; Sigler et al., 2020; Zoromé, 2007). In addition, whereas the OFC location is significant, we argue in this paper that an entity’s position within a chain of corporate subsidiaries provides important clues as to its other functions within the corporate group. This paper makes the following arguments. First, both where an entity is incorporated and where it is located on the corporate chain is important in determining the functions it performs for the corporate group. Second, corporate chains consist of certain primary structures. These include ‘standalone’ entities located at the ends of corporate chains (however long or complicated the chain might be), ‘in-betweener’ subsidiaries, located between parent and ‘standalones’, and within the category of in-betweeners, there can be a further structural feature we call ‘splitters’, whereby an entity down a chain is controlled through a split ownership arrangement that consists of at least two separate entities or chains. Third, whereas standalone entities, including those located in OFCs, are more likely to be used for funding and financial activities than as a part of tax avoidance schemes, OFC-registered in-betweeners are best suited for tax arbitrage purposes. Fourth, some forms of splitters, including those located or partly located in OFCs and which are likely to include in-betweeners as well, may be used primarily (but not always exclusively) for limiting legal liabilities through what we call ‘fuses’. Thus, we conclude only a relatively small portion of subsidiaries registered in OFCs are set up primarily for tax arbitrage purposes, but this may not affect the tax avoidance perpetrated through these centres.

The implication is that the inner structure of firms and the different layers and pathways of corporate subsidiary ownership are as important as their external geography and location in countries or regions. Throughout this paper, we use the example of Apple’s alleged tax avoidance scheme to illustrate how the two modes of spatial organization, jurisdictional location and position of corporate entities on corporate chains, were used by Apple to mitigate tax and other costs. We chose Apple specifically because it was the subject of two in-depth investigations, one by the Levin Congressional Committee in the US (Levin et al., 2013), headed by late Congressman Carl Levin, and one by the European Commission (Barrera and Bustamante, 2018; European Commission, 2016a). We complement the study of Apple with additional data on Amazon’s techniques of tax mitigation to show how similar patterns can be used for very different purposes.

We begin with a brief introduction to the literature on offshore subsidiaries, followed by an illustration of the method by which Apple’s inner structure was mapped out and an analysis of Apple’s tax mitigation techniques using a new visualized ‘map’ of Apple. We then illustrate the role of location on corporate chains in Apple’s and Amazon’s tax mitigation and the location of corporate fuses in the structure of these two firms.

OFCs, corporate tax planning and jurisdictional arbitrage

As OFCs tend to levy low taxes on corporations and host relatively minor or inconsequential product markets, they are believed to be primarily performing tax minimization tasks for the corporate sector. Much of the recent research seems to validate this assumption (Alstadsæter et al., 2018; Clark et al., 2015; Clausing, 2016; Cobham and Janský, 2018; Dowd et al., 2017; Garcia-Bernardo et al., 2017; Gordon, 2016; Gumpert et al., 2016; Hines and Rice, 1994; Kaye, 2014; Phillips et al., 2017; Zucman, 2015). OFCs are considered niche players in the global economy, exploiting their size and the right to write laws in their developmental strategies (Roberts, 1995). However, despite how small and insignificant they may appear individually, they have encouraged a phenomenal rise in international tax competition and downward pressure on tax rates (Andersson and Forslid, 2003; Bretschger and Hettich, 2002; Engel, 2000; Keen and Konrad, 2013; Mendoza and Tesar, 2005).

It is increasingly becoming clear, however, that tax is only ‘a part of the story of offshore corporate migration’ (Moon, 2019: 56). As Zucman notes, ‘Multinational corporations routinely use tax havens for treasury operations and group insurance. Some of these activities have legitimate roles’ (Zucman, 2013: 123). International business specialists refer to ‘corporate treasury operations’, including such tasks as cash pooling, investment, financial risk management, hedging, credit, insurance and compliance for the group as a whole (Helliar and Dunne, 2004; Mazzi, 2013; Polak, 2010; Stewart, 2008). Treasury functions have tended to gravitate to OFCs to take advantage, not only of low taxation, but also of other facilitating rules involving liability, governance and the like (Polak and Roslan, 2009). ‘Investors also use offshore jurisdictions for other forms of institutional arbitrage’, note Clark et al., ‘such as ease of raising funds, speed and lower costs of company formation, and access to reliable legal jurisdictions’ (Clark et al., 2015: 238). Small states can leverage ‘the benefits of borrowed size’ by offering global professional services, warehousing, logistics, shipping and finance to wealthy nations or high net individuals (Martinus et al., 2021). Sometimes, offshore jurisdictions are used for hedging against political instability and/or weaknesses of home country court and legal systems (Buckley et al., 2017; Greguras et al., 2008; Sharman, 2012; Vlcek, 2014).

Financial specialists argue that tightening regulations and anti-avoidance rules are making it harder for the single corporate entity located in an OFC to be used for tax avoidance purposes (see, in particular, Forstater, 2018, but also Debono et al., 2016; Lewellen and Robinson, 2013.) Experts seem to agree this has not resulted in an overall decline in tax avoidance. Rather, they point to the emergence of what Judith Freedman calls ‘exotic tax planning devices’, such as ‘double-non-taxation’, ‘dual resident entities’, ‘hybrid entities’, ‘hybrid financial instruments’ and ‘single-dip-no-pick-up’, all of which are replacing simple transfer techniques (Freedman, 2008: 16).

Corporate tax lawyers coined the term ‘jurisdictional arbitrage’ to describe such complex schemes (Fleischer, 2010; Jan and Matthias, 2021; Marian, 2013; Panayi, 2013). Jurisdictional arbitrage tends to operate through structures designed to take advantage of ‘a gap between the economics of a deal and its regulatory treatment, restructuring the deal to reduce or avoid regulatory costs without unduly altering the underlying economics of the deal’ (Fleischer, 2010: 227). Such schemes typically consist of a number of corporate subsidiaries and affiliates linked to each other through equity ownership, traversing several jurisdictions in way that allows them to exploit gaps, loopholes, or omissions in nations’ laws and regulations (HM Treasury, 2014; Hodaszy, 2017; Lambooy et al., 2013; Stewart, 2008). Some tax arbitrage schemes have achieved notoriety, labelled with pub crawl terminology, such as Double Irish or Dutch Sandwich, and more recently, Double Irish and Single Malt (Coyle, 2017; Kelly, 2015; Loomis, 2011). Several additional tax mitigation structures and/or structures driven by other regulatory considerations may still be unknown (Zucman, 2014). 1

Geographers add important spatial dimensions to the study of offshore corporate structures. Whereas investment in firms’ productive and administrative capacities results in organizations that, in the words of Peter Dicken, ‘pursue a strategy of transnational integration, geographical fragmentation, in which individual units in a specific country form only a part of the firm’s overall operations’ (Dicken, 2007: 237), these strategies are supplemented ‘by financial and fiscal cartographies with their own hierarchies, interface of global and local relationship, affecting, in addition, the inner structure of firms as well’ (Clark et al., 2015: 238). The offshore world comprises ‘several parallel and overlapping networks’ (Aalbers, 2018: 920) traversing diverse jurisdictions and performing a variety of territorial functions (Haberly and Wójcik, 2015; Martinus et al., 2021; Sigler et al., 2020). Several triangulation techniques using global FDI, portfolio data, and tax data have been developed to map out these overlapping networks. Van ‘t Riet and Lejour (2018), for instance, employ a network approach to calculate the potential ‘shortest’ tax minimization paths in such jurisdictions. Tax treaty shopping, they conclude, is one of the leading drivers of the rise in conduit jurisdictions (see also Borrego, 2006; Nakamoto et al., 2019). Garcia-Bernardo et al. (2017: 2) use network analysis to differentiate between ‘sink’ jurisdictions, attracting and retaining foreign capital, and conduits, by which they mean ‘countries that are widely perceived as attractive intermediate destinations in the routing of investments’. 2 These intermediating jurisdictions, known as ‘conduit entities’, have contributed to a phenomenal rise in financial turnover worldwide, leaving only a small residue of funds in the OFCs themselves (Cobham and Janský, 2018; Garcia-Bernardo et al., 2017; Mintz, 2004). 3 Haberly and Wójcik (2017: 236) map out financial flows, reaching the conclusion that smaller ‘sink’ jurisdictions are more likely to attract ‘structured investment vehicles (SIVs), collateralized debt obligations (CDOs), and credit arbitrage conduits issuing the most problematic forms of ABCP’ (i.e. asset-backed commercial paper).

The interplay of corporate fiscal and financial strategies, combined with diverging national rules and regulations, encourages the phenomenon of jurisdictional arbitrage to handle tax and other regulatory frictions (Lewellen and Robinson, 2013; Orts, 2013; Robé, 2011). Countless managerial decisions relating to costs and regulatory frictions affect the location of investment and contribute to the layering of corporate controls. Katharina Lewellen and Lucie Robinson suggest ‘firms design the internal structures to circumvent the tax and (other) legal constraints imposed by their host countries’ (Lewellen and Robinson, 2013: 7). As they do so, they generate diverse lines of control that result in ‘lengthy ownership chains with multiple cross-border links’ (UNCTAD, 2016). The study of such structures, they argue, can identify the way ‘firms minimize US repatriation taxes, foreign withholding taxes or foreign income taxes’ (Lewellen and Robinson, 2013: 7). Admittedly, however, ‘tax motives are only one of several distinct forces that drive internal structures’ (Lewellen and Robinson, 2013: 8).

Firms set up subsidiaries in OFCs for a variety of reasons. How can we differentiate between OFC subsidiaries engaged in tax avoidance and those engaged in other functions? This aspect of corporate organization and its effects, argue Haberly and Wójcik, has been neglected so far because of the ‘compartmentalized approaches to the study of corporate control’ (Haberly and Wójcik, 2017; see also Clark et al., 2015; Haberly and Wójcik, 2015a, 2015b; Hall, 2017). There is a great deal of discussion of corporate ‘structures’ employed in tax avoidance, and far less of structures used for other regulatory frictions (Eicke, 2009; Gordon, 2016; Hodaszy, 2017; Lee and Gordon, 2005). Zucman suggests about 80% of OFC subsidiaries are used for avoidance purposes, while a recent IMF estimates that about 30% are ‘phantom’ investments (Damgaard et al., 2019). Others believe these estimates are arbitrary (Forstater, 2018). Clark et al. (2015: 235) hint at a possible way of differentiating subsidiaries by pointing to ‘the way financial, regulatory and taxation decisions impact the inner structure of firms’. The concept of ‘inner structure’ is not elaborated upon or even defined by Clark et al., but it seems to refer to ‘the way a firm’s subsidiaries are connected through ownership links’ (Lewellen and Robinson, 2013).

Studies of the inner structure of firms present, at best, generic examples of structures used for avoidance, such as the Double Irish or Double Dutch arrangement (Jones et al., 2016; Lewellen and Robinson, 2013; Loretz et al., 2017; UNCTAD, 2016). The problem is that the ‘bespoke’ nature of arbitrage schemes, which typically involve specific corporate structures and highly choreographed financial transfers among subsidiaries, makes it difficult to identify generic forms within organizations. Moreover, little is known about the differences between schemes targeting tax minimization and those targeting other regulatory frictions. As a result, the approach to this dimension of the geography of offshore remains largely descriptive.

The rest of this article presents a framework combining legal theory with a structural analysis of location to map out generic forms of arbitraging corporate structures.

Visualizing the inner structure of firms: The case of apple

To advance our understanding of how the inner structure of firms can convey information about function, we developed a method of visualizing the inner structure using the Orbis database. We call this ‘equity mapping’ (EM). The EM approach takes advantage of the rules used to map out corporate inner organization (for a detailed discussion, see Phillips et al., 2020.) Contrary to common perception, the vast majority of modern multinational enterprises (MNEs) are not set up as a single unified legal entity; rather, they consist of a network of corporate entities held together through equity holdings (Ferran, 1999; Hadari, 1972; Robé, 2020). 4 This facility or ‘fiction’ as some call it (Blumberg, 1993; Greenfield, 2008) can be used by ‘business planners’ (Manesh, 2011: 20) to minimize regulatory frictions, including taxation (Biondi, 2017; Phillips, et al., 2020).

That difference between perceptions of MNEs and their legal status is clear from Apple’s filings. In its response to the case brought against it by the European Commission, Apple describes itself as the following: [The Apple Group] designs, manufactures and markets mobile communication and media devices, personal computers and portable digital music players. It sells a variety of related software, services, peripherals, networking solutions and third-party digital content and applications. Apple sells its products worldwide through its retail stores, online stores and direct sales force, as well as through third-party cellular network carriers, wholesalers, retailers and value-added resellers. In addition, Apple sells a variety of third-party products compatible with Apple products, including application software and various accessories and peripherals, through its online and retail stores. (European Commission, 2016b: 7) The Apple Group is composed of Apple Inc. and all companies controlled by Apple Inc. (hereafter collectively referred to as ‘Apple’). Apple is headquartered in the United States of America. (European Commission, 2016a: 2.11, 40)

The model adopted by Apple is otherwise known as the parent-subsidiary model. This model evolved historically as a pragmatic solution to an intractable problem that emerged in the late 19th century. 5 As businesses sought to expand their manufacturing base across borders, they had to find ways of legitimizing their contractual rights in other jurisdictions. The fledgling multinationals experimented with several organizational solutions. During the first phase of internationalization, several multinationals developed a system of foreign agents and foreign branches. 6 New options emerged following an amendment to the laws of incorporation introduced in 1899 by the ‘mother of trusts’, the State of New Jersey. Soon emulated elsewhere in the US and beyond (Arsht, 1976; Cheffins, 2015; Yablon, 2006), this legal innovation allowed a corporation to own stocks in other corporations (Grandy, 1989). Businesses could set up a subsidiary or affiliate abroad controlled through equity ownership. In their country of registration, these subsidiaries were considered independent legal persons. As such, the subsidiaries could raise funds in local markets while simultaneously restricting the potential liability of the parent company against claims (Blumberg, 1993; Ferran, 1999).

Due to these and other advantages, MNEs began to replace their system of foreign branches with the parent-subsidiary model. As separate legal persons, each subsidiary and affiliate has its own set of directors and enters into contractual relationships with other members of the group or with entities outside the group. Each subsidiary is subject to the ‘internal affairs doctrine (IAD), that is, subject to the rules and regulations of the country of registration’ (Blumberg, 1993; Ferran, 1999; Lambooy et al., 2013; O’Hara and Ribstein, 2009; Robé, 2011). As most countries in the world require corporations to file annual accounts, corporate subsidiaries file annual accounts in their respective jurisdictions as well. The unintended result of this system is that in addition to presenting consolidated accounts, MNEs provide data on their activities in a dispersed and decentralized manner through subsidiary filings. These individual filings are collated by data providers, such as in the Orbis database. The Orbis database is estimated to contain information on about 400 million private and public companies worldwide. 7

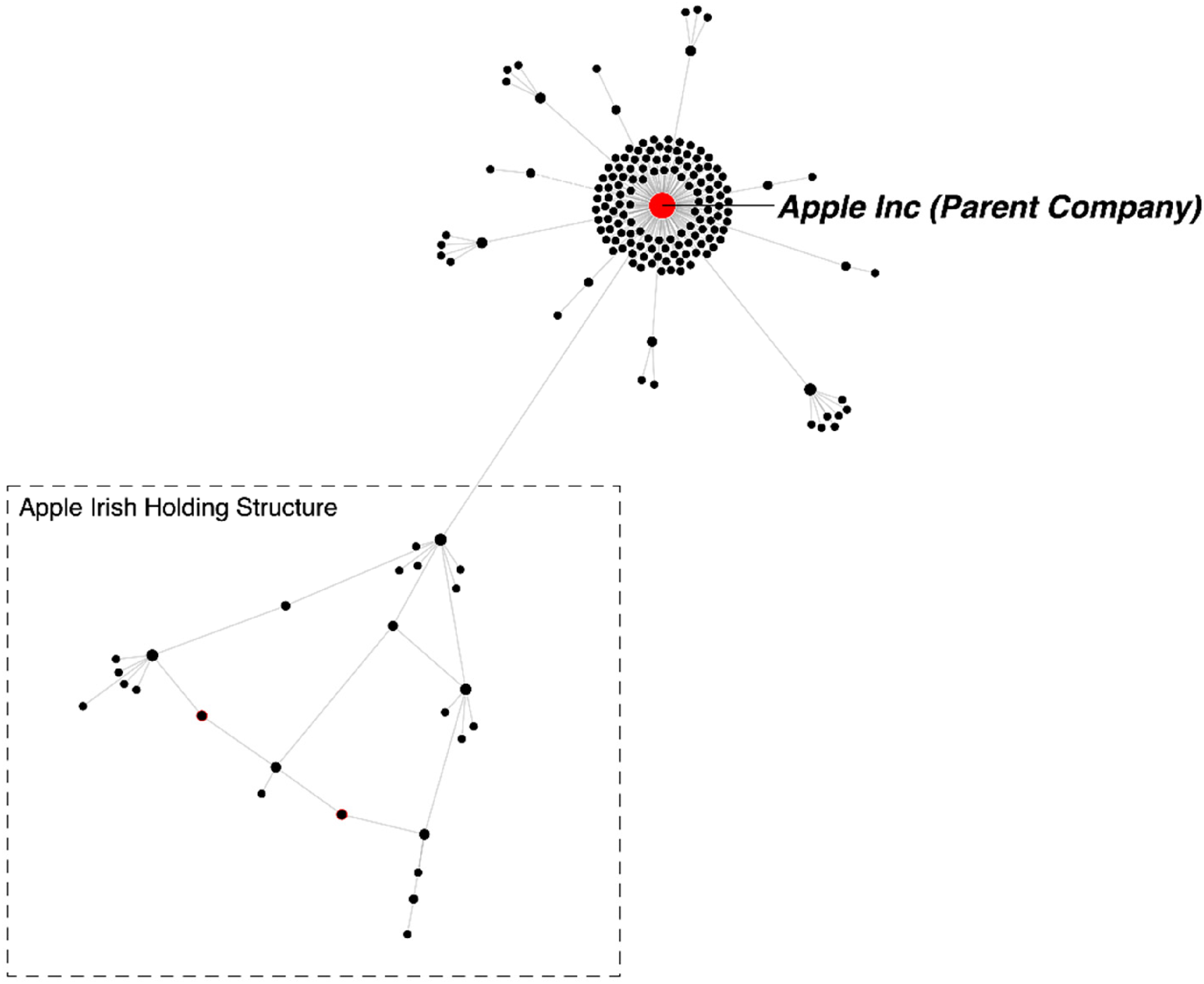

We developed an algorithm that captures the information on corporate holdings registered in the Orbis database which we then display using force-directed layout algorithms (Kobourov, 2012) to produce a visual diagram of a firm’s equity map. Figure 1 is an EM of the Apple group’s subsidiary structure, that is, all entities held directly or indirectly at 50.01% by Apple Inc., as reported by the Orbis data and identified by our algorithm. The subject of dispute regarding Apple’s tax planning is highlighted in the box in Figure 1.

Group structure of Apple Inc. (circa Jan 2019) highlighting Irish holding structure.

Legend:

Red Dot = Apple Inc. (parent company)

Black Dot = Direct and indirect holding of 50.01% and above by Apple Inc. (subsidiary)

Standalone = Subsidiary at end of chain (generic)

Intermediary = Subsidiary controlled and in turn controlling other subsidiaries

Cluster = Bunch of subsidiaries held by parent or regional parent who do not control other subsidiaries in a group.

Each corporate entity is represented on the EM by a dot. The algorithm ‘pulls’ entities that are directly controlled by their parent or regional parents but distances entities that control other entities in a group. Quite often, a substantial number of subsidiaries are held by a central or regional holding company with no other relationship to the group. These subsidiaries are huddled together in the EM and are displayed as a cluster of subsidiaries located near the central holding company. The figure shows that most of Apple’s subsidiaries are controlled directly by Apple Inc., creating a visual image of a cluster around Apple Inc. (red dot).

The EM in Figure 1 presents the inner structure of the Apple group. Our hypothesis is that this inner structure contains smaller elements, specific structures designed to fulfil various tax and regulatory optimization tasks. In the next section, we develop our theory by examining the rationale for specific types of structural features embedded in the ecology of the corporate group.

Framework section: Entity law and paradoxes of a global marketplace

Intermediate entities

Recent work by Lewellen and Robinson (2013) is one of the first scholarly attempts to theorize structural features of the internal ownership structure of firms. These authors contrast two hypothetical scenarios, a ‘pure historical accident scenario’, the default position of mainstream approaches to FDI, and a non-random organizational structure. In a pure historical accident scenario, the choice of ownership structures is irrelevant for the firm (as in the Modigliani–Miller model), and the structures may evolve randomly over time. Firms set up a separate subsidiary in each country in which they operate, and over time, subsidiaries are added to (or eliminated from) the structure. The ownership links of new affiliates are random: any new affiliate can be owned directly by the parent or by any other affiliate in the group with equal probability. The pure historical accident scenario can be rejected, Lewellen and Robinson argue, when ownership structures are demonstrably not completely random but follow some systematic pattern. 8

The parent-subsidiary model described above evolved originally to solve practical problems and was likely used, at least initially, in what Lewellen and Robinson brand the ‘pure historical accident scenario’. Managers soon discovered, however, that the device of the independent corporation could be used creatively to mitigate against certain types of regulatory frictions. At that point, non-random structures began to take shape. The history of those non-random structures is yet to be told, but it seems the dynamism and size of the American economy, with its unique federal structure, was an important breeding ground for innovatory arbitraging techniques (O’Hara and Ribstein, 2009). As far as we can tell, the earliest regulatory arbitrage in the US developed not because of taxation, but as the result of a competition between New Jersey and Delaware over the location of corporate headquarters (Arsht, 1976; Dyreng et al., 2013). Delaware stole a march over New Jersey early in the 20th century by allowing the separation of holding companies from headquarters, raising issues of ‘control’, discussed at length by Adolf Berle (Berle, 1950, 1947). Over time, Delaware corporate statutes granted business planners and investors broad latitude to privately order the rules of the internal firm, but also crucially allowed firms to limit or even eliminate the fiduciary duties of managers (Manesh, 2011). Delaware could also be used on occasion as an internal tax haven in the US (Dyreng et al., 2013). The perverse results, as Greefield notes, is that a state with a population of less than one-third of 1% of the overall US population was allowed ‘to set the rules of corporate governance’ for the rest of the country (Greenfield, 2008: 2).

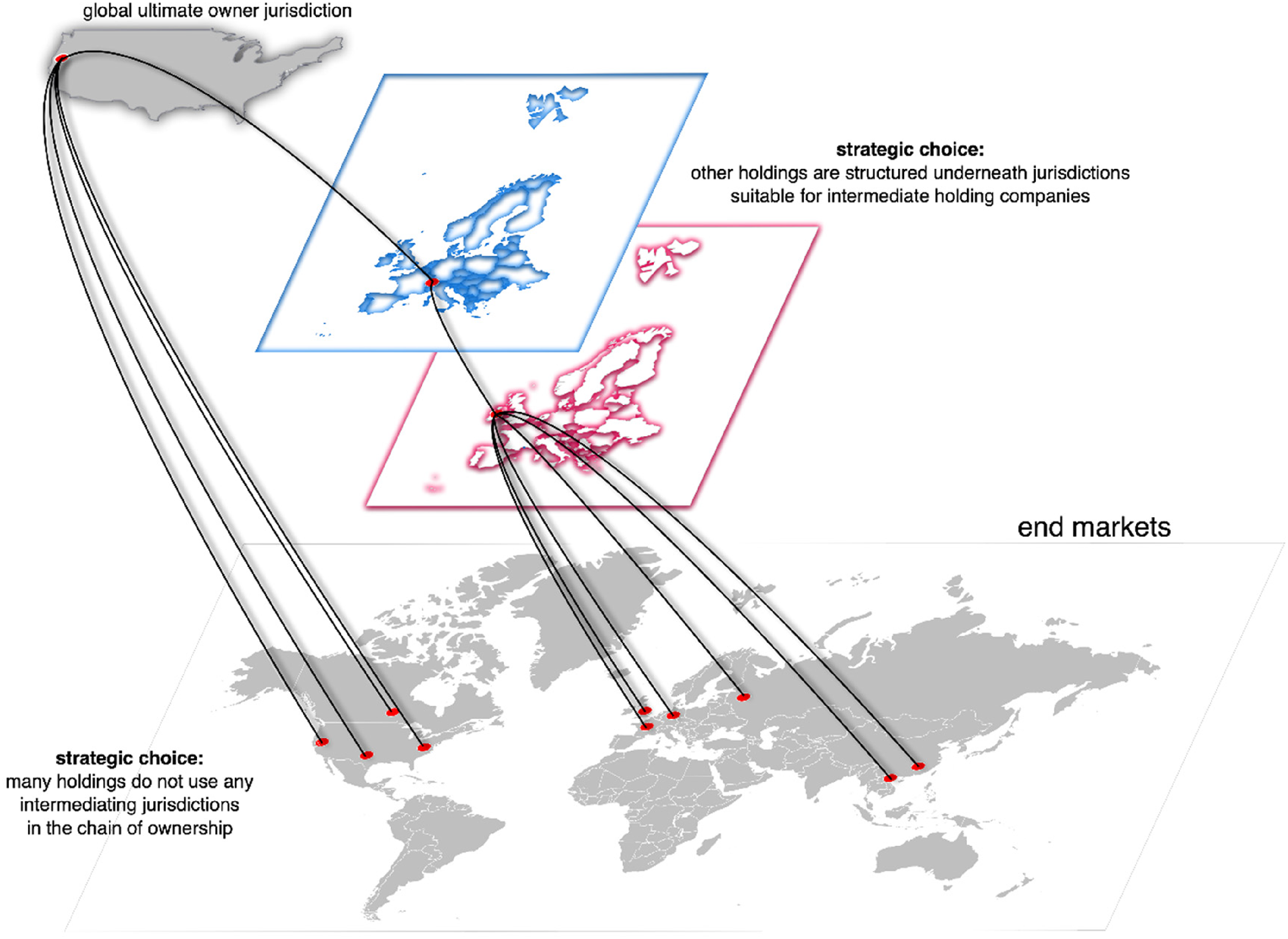

While Delaware’s main attraction may be its ‘enabling’ governance laws, the state has proved less valuable for subsidiary incorporation (Dyreng et al., 2013). Internationally, things work differently. A subsidiary located in a different jurisdiction can serve an American company as a ‘regional Delaware’, taking advantage of the enabling governance laws and rules of that jurisdiction. Learning from experience at home, there is evidence that American companies began to set up subsidiaries in ‘enabling jurisdictions’ (otherwise known as OFCs) that could serve as ‘regional Delawares’ abroad. Such ‘regional Delawares’ were controlled by the parent in the US, and they, in turn, controlled downstream subsidiaries. In other words, they were placed structurally as in-betweener subsidiaries. To counteract this trend, many countries, beginning with the US in the early 1960s, enacted rules called Controlled Foreign Companies (CFCs) rules, whereby the first layer subsidiary abroad could be treated by the parent’s jurisdiction for tax purposes as part of the parent (Sandler, 1998). To sidestep CFC rules, business planners may set up a second layer subsidiary, either in the same country or another country. 9 A stylized image of this type of structure is shown in Figure 2.

Layered ownership structure of a stylized multinational enterprise (MNE) consisting of several intermediary subsidiaries.

In this type of layered structure, profits are typically repatriated upwards through a chain of subsidiaries by means of dividend distributions to the parent company. Unless the chain is organized carefully, the group could easily end up being taxed in both home and local jurisdictions (Eicke, 2009). 10

The intermediary entity (the ‘regional Delaware’) is subject to the rules of governance, taxation and relevant regulations of the country of registration. Dividends’ repatriation would be subject to the rules and regulations of the home country, the intermediary’s location country, and rules of double taxation and the like signed between the two countries. The rules and regulations of the intermediary’s location are therefore crucial, as the combination of entity law and IAD ensures the location of a subsidiary as an intermediary on a corporate chain changes the regulatory calculus of an investment and thus can create opportunities for arbitrage (Brunson, 2012; Eicke, 2009; Gajewski, 2013; Gomtsian, 2015).

Intermediary corporate subsidiaries can simultaneously play another function, drawing on a technique described in the parlance of US tax advisors as ‘blockers’ or ‘stoppers’. The original blockers exploited US exemption rules granted to certain charitable entities (Silber and Wei, 2015; Taylor, 2010). Firms would set up charitable entities as their ultimate owner (top of chain) or more often insert a charitable entity on the corporate chain to serve as an intermediary. From the perspective of American companies, international zero-tax jurisdictions could be seen as variants of the domestic tax-exempt company. It was not a big step for American companies, therefore, to use intermediary foreign subsidiaries in OFCs as blockers. The international blocker had to be placed on a corporate chain and in a jurisdiction in such way that it could arbitrage the rules of taxation or governance of the parent and the rules, regulations and taxes of the country of registration of that entity. This is precisely the technique used, as we will see in the next section, by Apple.

The group would then accumulate funds from lower layer subsidiaries of the ‘charitable’ blocker. The practice was expanded to change ‘the character of the underlying income or assets, or both, to address entity qualification issues, to change the method of reporting, or otherwise to get a result that would not be available without the use of more than one entity’ (Taylor, 2010: 1).

Apple’s use of Irish blockers

Apple’s tax planning illustrates how modified blockers could be used in Ireland for tax purposes. Apple’s submission to the European Commission refers to certain anomalous subsidiaries it had in Ireland: The Apple Group includes companies incorporated in Ireland. Among the companies of the Apple Group incorporated in Ireland, a distinction can be made between companies headquartered in Ireland and are also tax resident in Ireland… and companies that are incorporated in Ireland but are not tax resident in Ireland. (European Commission, 2016b: 2.1.2, 45)

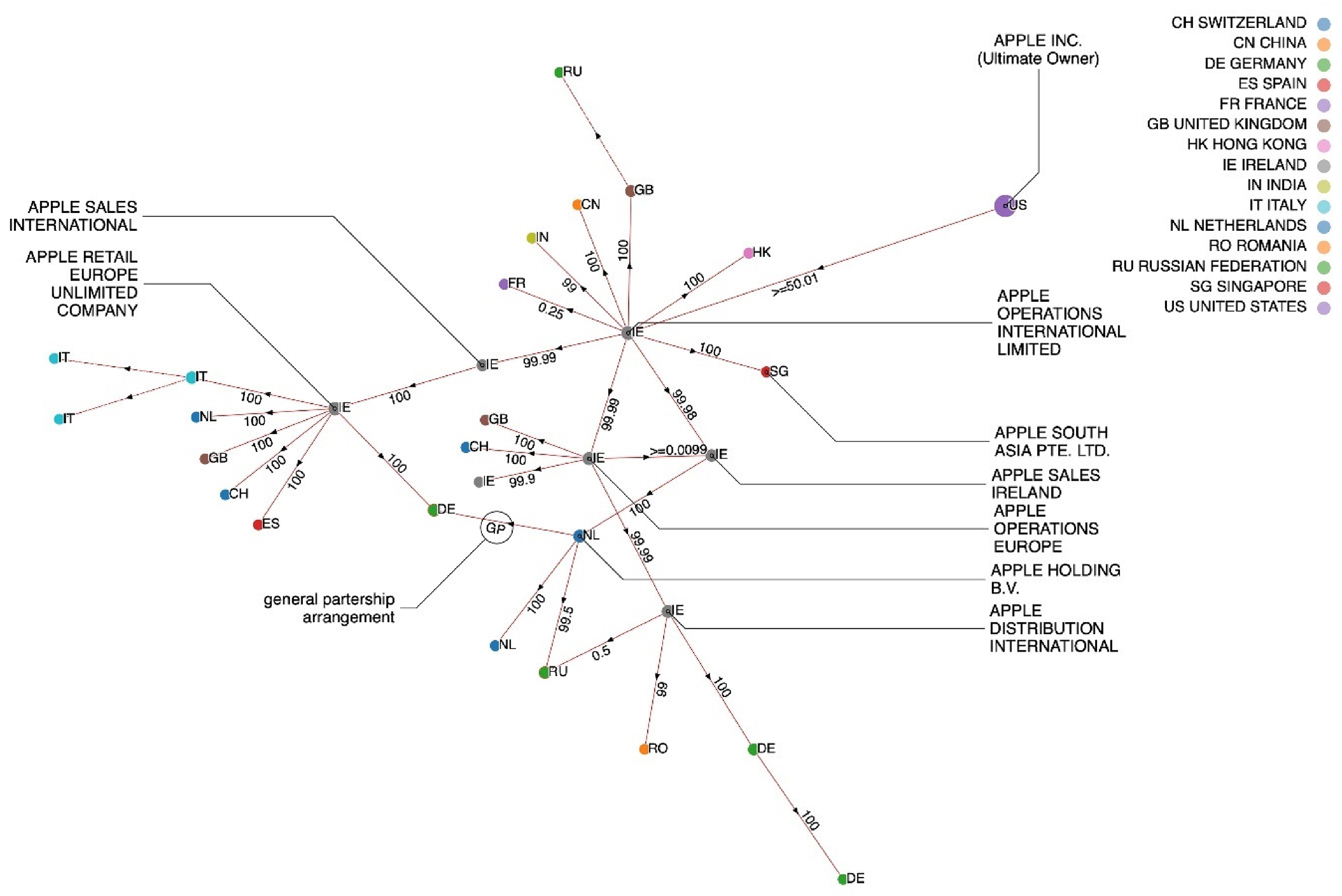

Figure 3 shows an EM of the branch of Apple with the two entities in question, Apple Operations International (AOI) and Apple Sales International (ASI). As Figures 1 and 3 show, one of these entities, AOI, served as the ‘gateway’ or ‘regional parent’ for a group of more than 30 corporate entities located in 12 countries. AOI, however, had no employees and insufficient physical presence in Ireland to meet Ireland’s nexus requirements. Therefore, it did not meet Ireland’s tax residency requirements. AOI was not a tax resident in the US either. It was essentially a tax resident nowhere. Despite being a shell, AOI’s location at the top of the chain ensured that as purported equity owner of the entities in that branch, it was entitled (as per the principles of entity law) to the profits generated by subsidiaries located on that chain. AOI reported a net income of $29.9 billion between 2009 and 2012, constituting nearly 30% of Apple’s total profit during those years. With 97% equity in AOI, Apple Inc. ‘chose’ not to repatriate those funds, thus avoiding potential US residency taxation.

Apple’s operations through its Irish SPVs.

The second subsidiary, ASI, played a more ‘active’ role in Apple’s affairs, serving in 2012 as a repository for Apple’s non-US intellectual property rights. According to the Levin Commission, in 2012, ASI was a subsidiary of Apple Operation Europe (AOE), another intermediary Irish SPV, which, in turn, was a subsidiary controlled by AOI. Our own EM analysis suggests the structure was changed sometime between 2012 and 2020 (for reasons unknown), and ASI is now directly controlled by AOI. We discuss the potential implications of the old structure below. Taking advantage of the ‘fiction’ that ASI was a separate legal entity, ASI entered into a cost-sharing agreement with Apple Inc., the parent company, over the development of the iOS software. On that basis, ASI had rights over a considerable portion of income generated from Apple’s sales of software outside the US market, whereas under the cost-sharing agreement, Apple Inc. had rights over the remaining portion. 11 In addition, ASI bought many of Apple’s finished products from manufacturers in China and resold them at substantial markup to other Apple affiliates. As a result, ASI accumulated substantial income. Overall, ASI had net revenues of about $74 billion between 2009 and 2012. As subsidiaries controlled by AOI in Ireland, AOE and ASI were not subject to the US’s CFC rules, and as subsidiaries located in the same country (Ireland), they were not subject to Irish CFC rules either. 12 But like AOI, ASI did not meet the requirement for tax residency in Ireland. Indeed, it did not claim tax residency anywhere, though this changed in 2012. 13 In our estimation, had ASI been a first-layer gateway entity instead of AOI, those profits would have been attributed to Apple Inc. under US CFC rules and might have been subject to taxation in the US. The internal structuring of the equity relationship between ASI and AOI and the location of each on corporate chain was thus critical to this scheme.

The Apple case is a vivid demonstration of the way the internal organization of subsidiary chains can be used by planners to arbitrage tax or other regulatory rules. It also shows the mere location of subsidiaries in an OFC, in this case Ireland, would not have worked in and of itself as a tax mitigation scheme. Indeed, Ireland’s nominal corporate tax of 12.5% – considered low when compared to other OECD countries but not particularly low when compared to many non-OECD jurisdictions – played a negligible role in the scheme. To all intents and purposes, Ireland could have had a nominal rate of corporate taxation closer to the OECD’s average or perhaps higher. It would not have mattered, because the key to Apple’s scheme was the arbitration of tax residency rules, not Ireland’s rate of taxation. Ireland’s willingness to accept the scheme at face value, rather than asking tough questions about the purpose of such non-tax resident entities located in its territory, combined with the location of those subsidiaries on corporate chains as ‘intermediaries’ and, equally, the sequence of control established between them, is what mattered in this case.

In the case of Apple, the entities without tax residency were used for the purpose of hoarding cash. Amazon, in contrast, took advantage of precisely the same set of rules and principles, entity law, IAD and US CFC rules, not to hoard cash abroad, but to transfer losses from its international operations in order to benefit from generous US tax deferral rules, using three intermediary subsidiaries in Luxembourg (Phillips et al., 2021; The Fairtax Mark, 2019).

The European Commission’s investigations of Apple and Amazon highlight the role played by certain OFC-based intermediary subsidiaries in tax planning, but the precise way these subsidiaries are used can differ considerably from one scheme to another. Despite important differences, these two cases illustrate a point repeated by corporate tax lawyers: intermediating ‘holding companies are a great opportunity in a suitable vehicle for implementing controlling and adjusting tax reduction strategies’ (Eicke, 2009: 5). As Eicke notes, it is the location of subsidiaries on chains and the principles of entity law that have rendered intermediating so salient for tax planning purposes: ‘the law itself, it is the main driver, since it creates planning opportunities with its wordings, its systematic inconsistencies and in particular with its omissions’ (Eicke, 2009: 11).

End of chain subsidiaries

Following the same logic, entity law would suggest subsidiaries located at the end of a chain, standalones, are far less suitable for tax arbitrage purposes. As Maya Forstater notes, ‘several jurisdictions that make up a high proportion of the ‘rest’ (such as the British Virgin Islands, Bermuda, and the Cayman Islands) do not have double tax treaties, so payments from non-tax havens would be subject to withholding taxes’ (Forstater, 2018: 1261). What is the role of standalone OFC subsidiaries, then? To the best of our knowledge, the concept of the standalone entity or end of chain subsidiary has not been discussed so far in an academic paper. Nevertheless, there are some useful hints in the literature about their possible role and function. Haberly and Wójcik (2017: 236) find certain types of OFCs are disproportionally active in the provision of financial instruments and are used in corporate investment, hedging and the like. Phillips et al. (2020) say subsidiaries in those OFCs are often located as ‘standalones’.

A report commissioned by the Jersey Authority provides detailed assessment of the role of Jersey as an ‘active secondary market’, a concept that refers to alternative regional financial centres supplementing the large global centres of New York, London, and the like. The report argues: ‘Jersey is not a material centre for corporate profit shifting. Multinational companies that use their transfer pricing arrangements to shift profits into the bailiwick will likely not be sheltered from taxes due elsewhere’. The report says this is in sharp contrast to arrangements in places like Luxembourg and Ireland (our own work shows both are often located as intermediaries; see Phillips et al., 2020, 2021). In such places, ‘profits brought there through transfer pricing from elsewhere in the union would be out of reach of other member states’ tax authorities’ (Debono et al., 2016: 7).

Although this requires further research, we suggest, provisionally, that the standalone subsidiaries located in OFCs are more likely to play a variety of treasury function roles for their corporate group, such as financial investment vehicles, foreign exchange functions, hedging and the like (Stewart, 2008). Those investment and hedging vehicles tend to be in what the professional literature often refers to as ‘tax neutral’ jurisdictions (Debono et al., 2016), or tax havens for the rest of us, so if and when they are profitable, they would not pay tax in their countries of registration (such as the Cayman Islands, Bermuda or Jersey). However, avoiding taxation on repatriation of these profits would necessitate an intermediating entity or entities controlling those end of chain subsidiaries.

Are all in-betweeners and intermediaries in OFCs? The role of the corporate fuse

Should we conclude from the above that all intermediary in-betweeners in OFCs are designed for profit shifting? Not necessarily. Blockers may target other financial, governance or regulatory frictions. The Irish branch of Apple discussed above contained a possible additional risk liability mitigation structure that we dub corporate ‘fuses’. 14 We use the metaphor of an electric circuit breaker or electric fuse that trips to prevent current surges from damaging electronics to describe these types of corporate structures. Like electric fuses, the corporate fuse is inserted to protect the parent from damage.

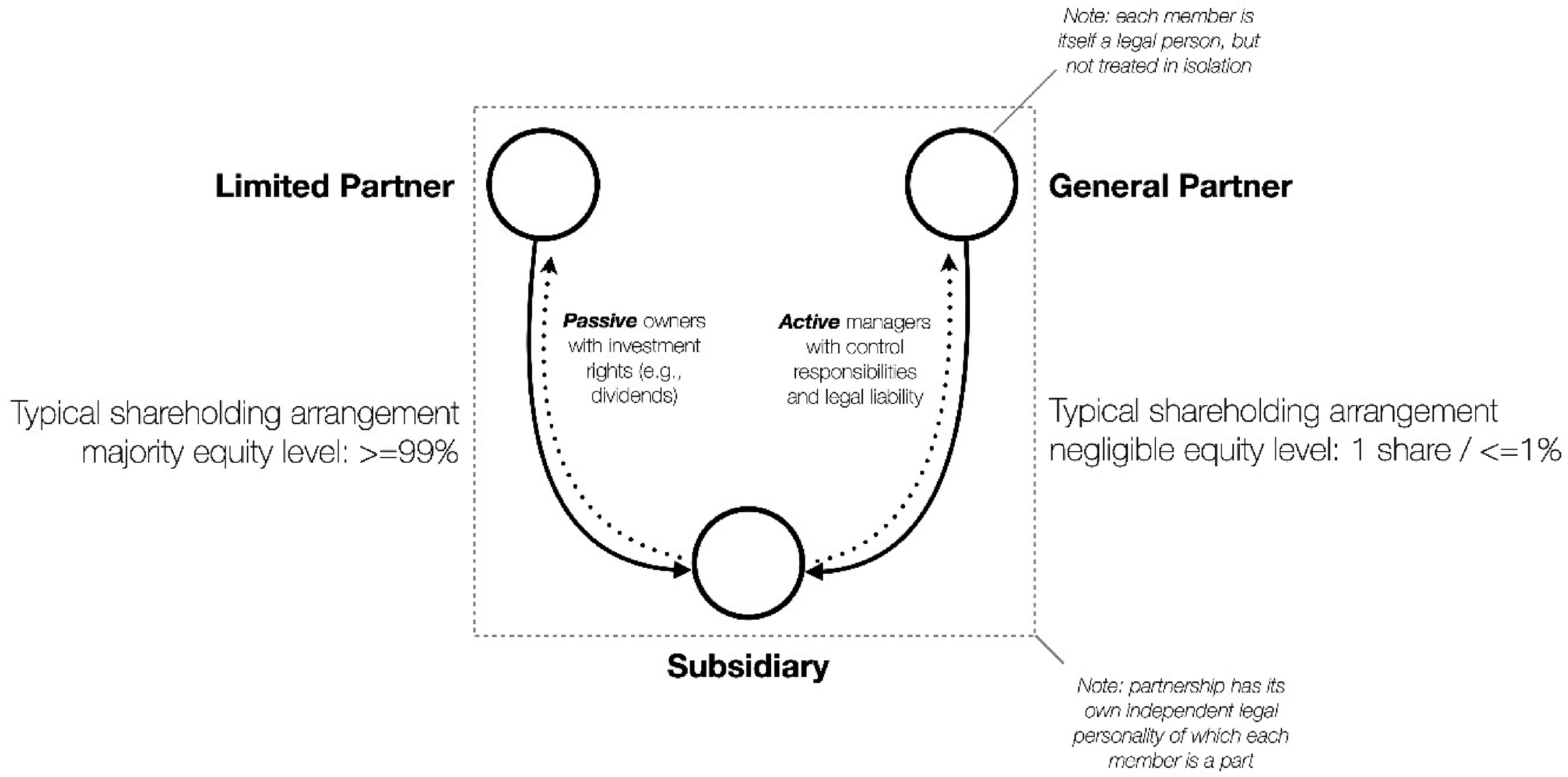

It appears the technique of risk mitigation embedded in corporate structure was innovated in the US. In 1822, both New York and Connecticut legislatures created the facility to form a limited partnership entity. This consisted of two types of partners: general partners, who ran the company and hence were subject to legal proceedings, and special partners, who had no managerial authority, and whose liabilities, therefore, were limited to their investment (Lamoreaux, 2004). The structure allowed the special partner to be considered, in other words, as a passive investor and, as such, shielded from potential liabilities and court cases (Hayes, 1997). Such structures are pervasive today in financial investment vehicles, such as hedge funds (Gross, 2004).

It seems similar structures have migrated to the corporate world as well. In such a configuration (see Figure 4), the partnership creates a two-tiered structure consisting of at least two separate legal persons: general partners and limited (or special) partners. Taking advantage of the fiction of the separate and independent corporation, management sets up a split ownership structure. A controlling subsidiary or a branch owns a small stake in a low-layered subsidiary (typically holding 1% or even less in the subsidiary company), emulating the general partner role in the scheme above. At the same time, the group sets up another controller or a chain of subsidiaries, typically holding 99% majority of the low-layered subsidiary. This controlling subsidiary (or chain subsidiaries) emulates the role of the special partner and remains, at least formally, a ‘passive’ investor in the low-layered subsidiary. The organization can thus ensure that the general partner maintains control of low-level subsidiaries. The simulated general partner is subject to legal proceedings in case of misdemeanor. However, with little financial stake in the entity, the liability attached to the simulated general partner is limited. The simulated limited partner is formally a ‘passive’ investor and cannot be made liable. The simulated general partner and the limited partner are both controlled by the same parent. However, rarely, if ever, are courts prepared to challenge such schemes (Blumberg, 1993).

Schematic of a corporate fuse.

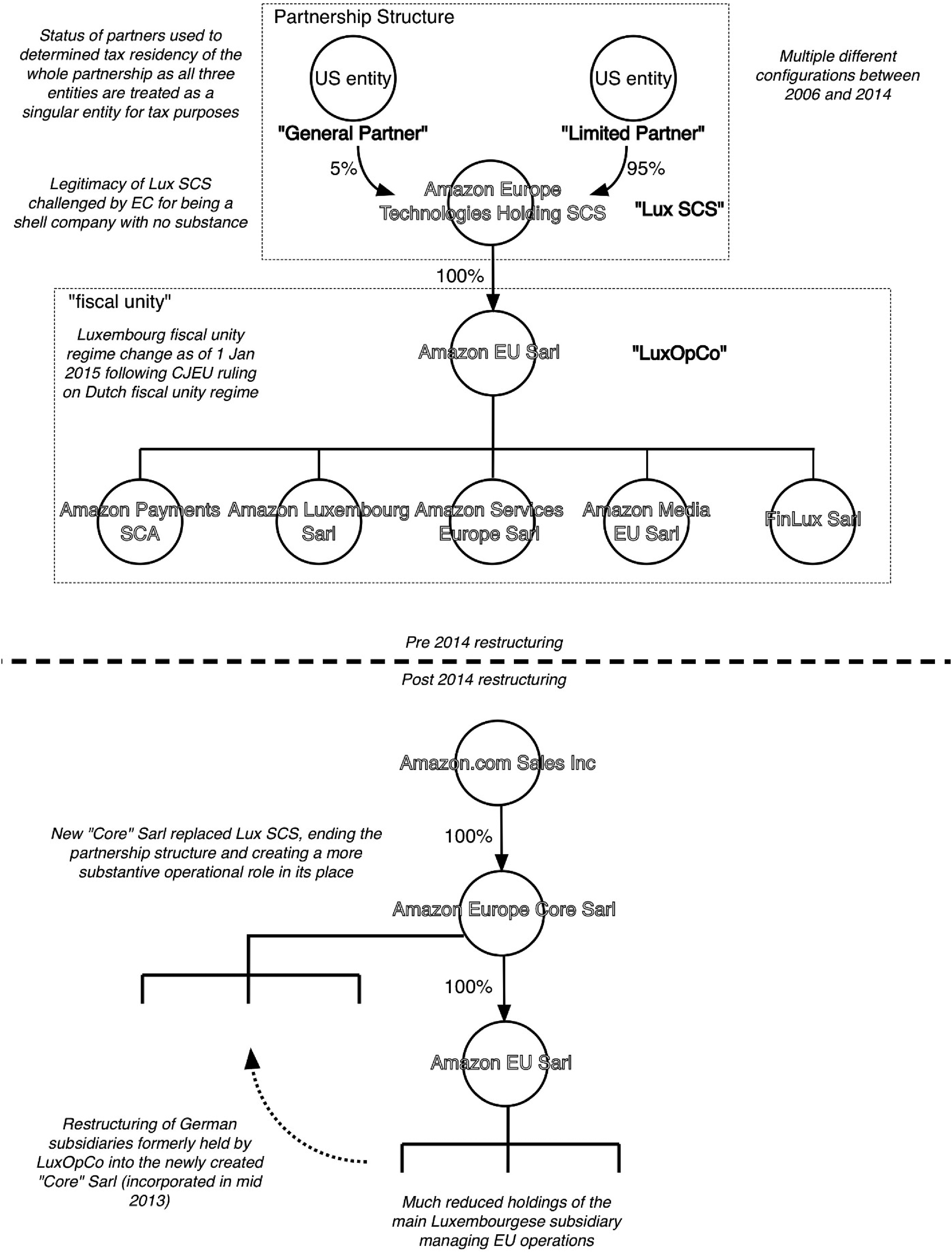

Amazon’s Luxembourgish arrangement pre- and post-EC case.

The structural features of this setup include a splitting of authority, isolating those involved in funding activities from management. Management often introduces doubled fuses, just to insure against risk that courts in one country will find against such an arrangement. The double fuse involves additional jurisdictions; potentially, then, litigants could face more courts located in different countries, raising the costs while reducing the chance of success. Some jurisdictions, including Germany and Scotland, as well as OFCs like the Netherlands, or Luxembourg, have legal regimes that are particularly amenable for the creation of such fuses. The implication of such a structure is that a number of important legal distinctions (such as who bears the liability risk, the level of risk and even the location of tax residency for the transactions involved) are not ‘givens’ dictated by law, but decisions based on the contracts set up between the parties involved in the hybrid entity.

A fuse often takes the format of a split ownership, typically 1/99% (but not always) equity holding of the downward subsidiary. The Apple branch described contains several such holding structures, which can be inferred from the prevalence of 99.9% holding arrangement among several entities. In Figure 3, we also highlight one such structure involving a German entity, Apple Retail Germany BV and Co KG, wholly owned by Apple Retail Europe Unlimited Company, was controlled by an emulated ‘general partner’ (denote as GP in Figure 3), a Dutch entity Apple Holding BV. We have no way of verifying independently whether this structure was set up intentionally as a fuse.

Interestingly, an analysis of the European Commission case against Amazon, combined with an EM of Amazon, reveals a somewhat different split ownership arrangement located at the gateway of Amazon’s international investment through Luxembourg that could potentially be a fuse. This fuse-like arrangement is not discussed in the EC case. Equally, for reasons that were not made public, the fuse-like arrangement was removed following the EC investigation (Phillips et al., 2021).

EM analyses can identify the location of a corporate fuse. We know that such structures are generally used for liability mitigation, but the precise reasons for mitigation are not entirely clear from the structure.

Conclusions

MNEs supplement their investment in productive and administrative capabilities with commensurate structures designed to mitigate a range of risks, including political and regulatory liabilities and costs, such as taxation. Whereas the choices of location of strategically relevant productive activities by MNEs have been studied at great length, decisions on the spatial configuration and layering of control of corporate groups remain less understood. This article discusses the spatial dimension of the use of diverging investment pathways through intermediating corporate subsidiaries and jurisdictions. We focus specifically on the way MNEs employ one subset of subsidiaries, those located in OFCs. We suggest that the fragmentation of the global markets amid diverging legal systems is forcing multinationals to consider their investment options carefully. MNEs are taking advantage of laws of incorporation and corporate governance, specifically laws relating to entity and IAD, to minimize tax and other regulatory frictions. Topographically speaking, MNEs comprise three generic types: global ultimate owners, intermediaries, and end of chain subsidiaries. As the article shows, due to principles of entity law and IAD, the location of subsidiaries along those generic positions determines the range of options for regulatory roles and arbitrage they perform in the context of group holding. By retracing the logic of laws of incorporation and IAD and classifying entities based on their geographical and corporate position, we can identify different tasks performed by subsidiaries located in OFCs. We can identify with a certain degree of probability which subsidiary is more likely to play an arbitrage role and which one is less likely to do so.

By superimposing the different geographies of corporate organization, the location of a subsidiary along these three topographical features, and the location of subsidiaries in a political/legal jurisdiction, we can advance our understanding of the complex cartographies of the offshore world. Various US Congressional and EU investigations into the fiscal affairs of Apple and Amazon, combined with an EM analysis, are illustrative of the importance of the types of geographies involved in corporate planning. As these two cases show, there is great scope for new types of EM geographical investigation and potentially a new line of research into the geography of the modern corporation.

Footnotes

Acknowledgements

The authors benefitted greatly from the advice and support of many colleagues, including Daniel Haberly, Sandy Hager, Adam Leaver, Omri Marian, Yuval Millo, Anastasia Nesvetailova, Jean Phillip Robé, Sarah Rennoldson, Amin Samman, Leonard Seabrooke, Jason Sharman, Daniel Tischer, as well as two anonymous referees. All usual disclaimers apply.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work was supported by the H2020 European Research Council (Grant No. 694943), Corporate Arbitrage and CPL Maps: Hidden Structures of Controls in the Global Economy (CORPLINK).