Abstract

Taking up the geographer's task of following and defetishizing the commodity, this research taps into the United States (US) federal banking data to locate the commodity “money”. Law is used to specify money's locations. Relative to the size of its economy, Utah's banks report a lopsided share of US money. This paper unmasks important social relations embedded in the money commodities located in Utah's banks by tracing the history of US banking law, which has played a leading role in the processes responsible for Utah's outsized share of the sub-national monetary landscape. Banking law determined the scope and type of business in which banking firms and their corporate affiliates could engage. Throughout the 20th century, investment banks and commercial firms struggled to claim legal rights to engage in business combinations once deemed illegal: combining non-banking business with a commercial bank. The state of Utah, in coordination with financial and commercial firms, has expanded the legal and financial space of Industrial Loan Banks (ILBs), historically idiosyncratic chartered banks exempt from regulations separating banking firms from non-banking business. Utah marketed their banking charters to global, systemically important financial institutions and large commercial conglomerates, which then established or acquired ILB subsidiaries within the state. From Utah, the die had been cast: the largest non-banking firms on the planet were now legally empowered to accumulate capital in ways that had heretofore been forbidden at other locations. American banking had been transformed.

Introduction

The commodity chain analysis has become a staple of the economic geography literature over the years. This analysis is motivated, ultimately, by the simple but all-important insight that the commodity that circulates through capitalist markets “conceals, instead of disclosing” (Marx, 1990: 168) the social relations of production, distribution, and consumption along the commodity chain. Social relations are misidentified or confused with relations between things (Harvey, 1982: 17). Marx, famously, once called money the “god of commodities”, but as Christophers (2011b) has pointed out, money's paths through the world have very rarely been put under the commodity microscope. Instead, geographers have turned to so much else, from papayas to t-shirts. Marx himself suggested the task of defetishizing money should be no different than for other commodities—“the riddle of the money fetish is, therefore, the riddle of the commodity fetish” (Marx, 1990: 187)—but it has not proven so straightforward in practice.

Geographers (Cook, 2004; Cook et al., 2007; Gregson et al., 2010; Harvey, 1990; Hulme, 2017) have generated a rich literature that traces the hidden social and spatial relations in the life of commodities from origin to market shelf. Consumers in London are unaware of their connections to impoverished Jamaican papaya pickers whose labor stocked London's supermarket shelves. Likewise, investors earning interest, dividends and capital gains in a brokerage account are unaware of their connections to an entire world of impoverished fruit pickers that generated the surplus money swept into an insured deposit account, and they are similarly unaware of the location of the bank hosting their deposits.

In the paragraphs that follow, this paper attempts to pick up where Christophers (2011b) left off, to go “behind and beyond”, to connect money in banks to a wider world of social-political relationships. Identifying where and why money travels is essential to the task of revealing how capital extracts and expands value from a world of commodity-producing labor. The challenge, however, as Christophers (2011b) notes, is that it is not easy to follow an intangible commodity like money, which not only simultaneously circulates in many directions and in perpetuity, but is difficult to identify with any specificity in the process of circulation: One money commodity looks a lot like all the others. Indeed, Emily Gilbert argues that the lack of a practicable methodology to follow money is fatal to Christophers' project and goes on to suggest that “to ‘follow the thing’ that is money is not only likely to be impossible but perhaps even inadvisable” (Gilbert, 2011: 1087).

Christophers (2011a, 2011b) acknowledges that “actually following” money from node to node during its life is an unrealistic goal, and to follow it and defetishize it in the same way as, for example, Cook (2004) did so meticulously with papayas, does seem a wild goose chase. But despite the formidable challenges, following money can be approximated and the task of defetishizing money where it is located still applies. Consequently, at least for now, Christophers' appeal to following money is adjusted to locating money, in the form of bank deposits, and thus reveals the social relations associated with money at one place along its long journey through space. That place is Utah.

The rest of this paper is organized as follows. The section Locating Money argues that intangible money has specific locations defined by law and answers the question: “Where, within the US, is money located?” Locating money adapts an approach used by Friedman and Schwartz (1963), who measure and chart the US money stock at the national scale alone. I locate and measure money at the sub-national scale using geo-spatial data from US federal banking regulators. At sub-national scales, Friedman and Schwartz's money stock measurements collect time series snapshots of places money accumulates (or does not accumulate).

Money is of course located everywhere. The question, rather, is where it moves and accumulates relative to other locations within the territorial US. A deep dive into bank deposit money data to answer this question revealed the surprising fact that Utah, relative to the size of its economy, holds a conspicuously lopsided share of US money relative to other states. A US state's share of the nation's money almost always matched that state's share of US Gross Domestic Product (GDP). It was rare to find any exception to this deposit money-to-GDP relationship, but one exception was found in Utah. Twenty years ago, both Utah's share of the nation's deposit money and its GDP share were 1%. By 2018, Utah's deposit money share grew to 4% while, during the same period, its GDP share remained constant at about 1%. Rather than focusing on the quantity of money at a location, the important task is to reveal what money conceals at its locations. The curiously excessive quantity of money located in Utah merits and motivates its defetishization.

The section Lifting the Veil Covering Utah's Bank Deposit Money explains this unusual accumulation of money in Utah and reveals some socio-political relations behind it by looking at the evolution of federal and state banking law. These legal changes are the visible surface of a long history of struggles between capitalist firms seeking unconstrained banking business and policymakers and others demanding limits to the business of banks. Throughout this history, banks have been relentlessly resourceful in their efforts to reach beyond banking. Every legal reform restricting banking firms' attempts to engage in non-banking business (for example, the Bank Holding Company Act (BHCA) of 1956 (12 U.S.C. § 1841)) led banking firms to find an open window through which they could reconnect banking and non-banking investment and commercial enterprises. By the 1990s, global systemically important financial institutions (G-SIFIs) and some of the largest commercial conglomerates were stampeding through this open window into Utah. With Industrial Loan Bank (ILB) charters, Utah provided a “legal” spatial fix (Harvey, 2001) that enabled firms based in Utah to evade the regulatory requirements of the BHCA. This legal exemption is exceptionally useful because the federal government granted the right to charter and host ILBs to only a few states (Utah among them) but denied those rights to almost all other states. Utah used this legal unevenness to offer banks a “get out of jail card” while developing a thriving in-state financial center that made both the banks and Utah richer. From their Utah offices, banking firms can do what is illegal almost everywhere else in the country: gather insured deposits while engaging in non-banking business. The political struggle concerning the scopes of banks' businesses remains central to bank regulation debate to the present day. Recently, the Federal Deposit Insurance Corporation (FDIC), an important bank regulator, has solicited public comment regarding consolidated supervision of ILBs and the firms that own them (Federal Register, March 31, 2020). This special regulatory exception for ILBs remains controversial. Its future status will be hotly contested and will have an important impact on the monetary and financial geographies of the US.

The approach taken here to locate money provides a realistic way to match Christophers' objectives for following money. In doing so, it also builds on a wider set of literatures concerning the relation between law and finance. It shows how law (a) redirects capital to new places (Barkan, 2011; Poon et al., 2018); (b) shifts regulatory authority between local, state, and national scales (Kear, 2014; Leitner, 1990); (c) transforms financial firms' legal status and standing via spatial/location choices (Haberly and Wójcik, 2015); and (d) influences the governing locations' firms choose to regulate their trade (Christophers, 2013; Potts, 2016). In the case of ILBs, federal banking law shifted regulatory authority to sub-national state institutions, which then enabled “local” actors to disproportionately shape the global and national distribution of deposit money.

The section Circumventing Legal Limits to Capital's Expansion draws some broader lessons from the development of ILBs in Utah, describing the process as the exceptionally powerful interplay between regulatory arbitrage and entrepreneurial governance, which attract each other like opposite magnetic poles. The state uses its law-making powers to reset regulatory regimes to favor certain industries, often in order to develop their local economies; meanwhile, firms use regulatory arbitrage to select locations with regulatory regimes amenable to their business strategies. The section Going Behind and Beyond: The Hidden Character of Law concludes with a discussion of what the law itself conceals and the roles money and law play in cultivating and sustaining the partnership between capitalist firms and the state.

Locating money

The principal adjustment that makes this attempt to “locate the money” workable is to specify the commodity as money in the bank deposit form. In other words, this study excludes other forms the money stock takes: currency and coin in circulation; banks' required reserves, deposited with the Federal Reserve; travelers' checks; and deposits held by credit unions. Nonetheless, it does include the vast majority of all domestic money, since bank deposits make up the vast proportion of the US money supply. Of the M3 monetary aggregate, a standard measure of money supply, bank deposits make up roughly 87% of domestic money in the US (Federal Financial Institutions Examination Council (FFIEC), 2019; Organization for Economic Co-operation and Development, 2019).

Does deposit money have a location?

In a modern banking system, the deposit money is immaterial. There are no piles of bills or gold bars in a vault labeled “Deposits”. New deposits are created when banks issue debt. Bank deposits are destroyed when a borrower repays the loan principal. Existing deposits are transferred from one account to another, like a paycheck that transfers deposits from an employer's payroll account to a household account. Deposits are represented as accounting entries, mere electronic pulses in computer storage. Most trade involves moving money from a buyer's bank account to a seller's bank account, neither of whom ever touch something we call “money”. Clearly, in a digital age, money exchanged for goods or services need not be located where trade takes place, since debits and credits are cleared electronically between buyers' and sellers' bank accounts. How do we determine where on earth deposits are located?

There are of course multiple methods to assign a location to a bank deposit: where the account holder lives, at the bank office collecting a deposit transaction, etc. For this study, deposits' locations are the result of laws. Locating starts with legal title to the deposits. Once deposited, legal title to the money belongs to the bank rather than the depositor: The money in your bank account “is not your money” (Persson, 2015; Singh, 2012: 83). The account holder of the bank deposit has a claim, not legal title, to the money in their deposit account. Banks enjoy virtually complete discretion to determine where, when and to whom deposit money in the banker's possession is deployed as loan capital, and, to the extent that a bank may move its deposits across jurisdictions (always subject to some restrictions), it can choose where to locate its deposits as it sees fit. Exchanges of title to deposits, which result in exchanges of deposits' locations, are mostly inter-bank transfers. The Uniform Commercial Code provides details on legal title transfers of deposits during exchange (Sommer, 1998). In the US, federal and state laws assign locations to deposit money. The locations accepting deposits are banking firms' offices. All domestic bank deposits in the US are assigned to the branch office locations banks select. Consequently, we can use banks' office locations and the quantity of deposits at each location to map the geographic distribution of deposit money at sub-national scales.

Individual bank corporations typically have many branch offices. The FDIC requires all federally insured banks to report deposits held at each bank office, and this data is collected in the FDIC's annual Summary of Deposits Survey (SODS). The FDIC sets regulatory guidelines for branch banks to assign deposit accounts within their branch office networks. Those regulations allow branch banks limited discretion to assign deposit accounts to branch offices within their networks. For instance, banks may assign deposits to the branch office where the account holder does the most business or to the office where the deposit account was opened. Banks are to be consistent in the methods used to assign deposits to their branches. Overall, the SODS responses appropriately characterize the deposit-gathering activities of each domestic bank office. SODS regulations for banks assigning deposits to a branch office reasonably attach deposits at the geographic coordinates of the bank offices that hold them and where the related economic activity took place that brought the deposits to each bank office as of the time of each annual survey.

There is further evidence that deposits have locations at particular banks in keeping with laws. The quantities of bank deposits that banks hold at various locations are used to enforce banking regulations and to apportion state and local taxes. For instance, the Riegle-Neal Interstate Bank Branching and Efficiency Act of 1994 uses locations of banks' branch deposits to regulate branching across state boundaries. Interstate bank merger applications are denied if a merged banking organization will exceed 30% of a state's total deposits. Interstate banks must also meet loan-to-deposit thresholds in the host states in which they have branches. The Department of Justice enforces antitrust legislation by measuring the concentration of banks' deposits at market locations (Christophers, 2014). Mergers and acquisitions may be denied if they result in a surviving bank obtaining excessive concentrations of deposits in market locations. In recent years, for example, Missouri, New York, and Virginia used the proportion of a bank's deposits located in-state relative to deposits held at all locations to determine the proportion of a multi-jurisdictional bank's franchise tax (Commonwealth of Virginia, 2018; Missouri Department of Revenue, 2014; New York State Department of Taxation and Finance, 2014; Hall and Lusch, 2017). Laws determine the spatial distribution of money—where it is held and/or taxed, for example—which locate intangible bank deposits in very tangible specific locations.

Measuring deposit money at sub-national locations

The SODS data offers geographers an opportunity to locate, measure and (with limitations) track the movement of deposit money. For each bank office authorized to accept deposits, the SODS data provides, among other data, the total quantity of deposit dollars and the street address marking a location. Instructions for completing the survey specify that deposit accounts are to be assigned to offices in branch networks in a manner in keeping with each bank's internal record-keeping. Bankers must not use methods which misstate or distort offices' deposit-gathering activity (FDIC, 2016). The SODS datasets contain roughly 90,000 bank office observations annually from 1998 through 2018, providing a yearly snapshot of deposit money held at all domestic US bank locations as of 30 June. Comparing deposit money values between consecutive surveys allows us roughly to track the aggregate movement of money into and out of bank locations.

The SODS data and ancillary data were imported into statistical software in order to facilitate exploratory data analysis (EDA). With rare exceptions, all states usually experience year-over-year increases in deposit money. Using a state's percent share of national deposits, as opposed to absolute dollar amounts, negates the effects of an expanding money supply, and provides a metric to measure and compare shifting proportions of money between states over time.

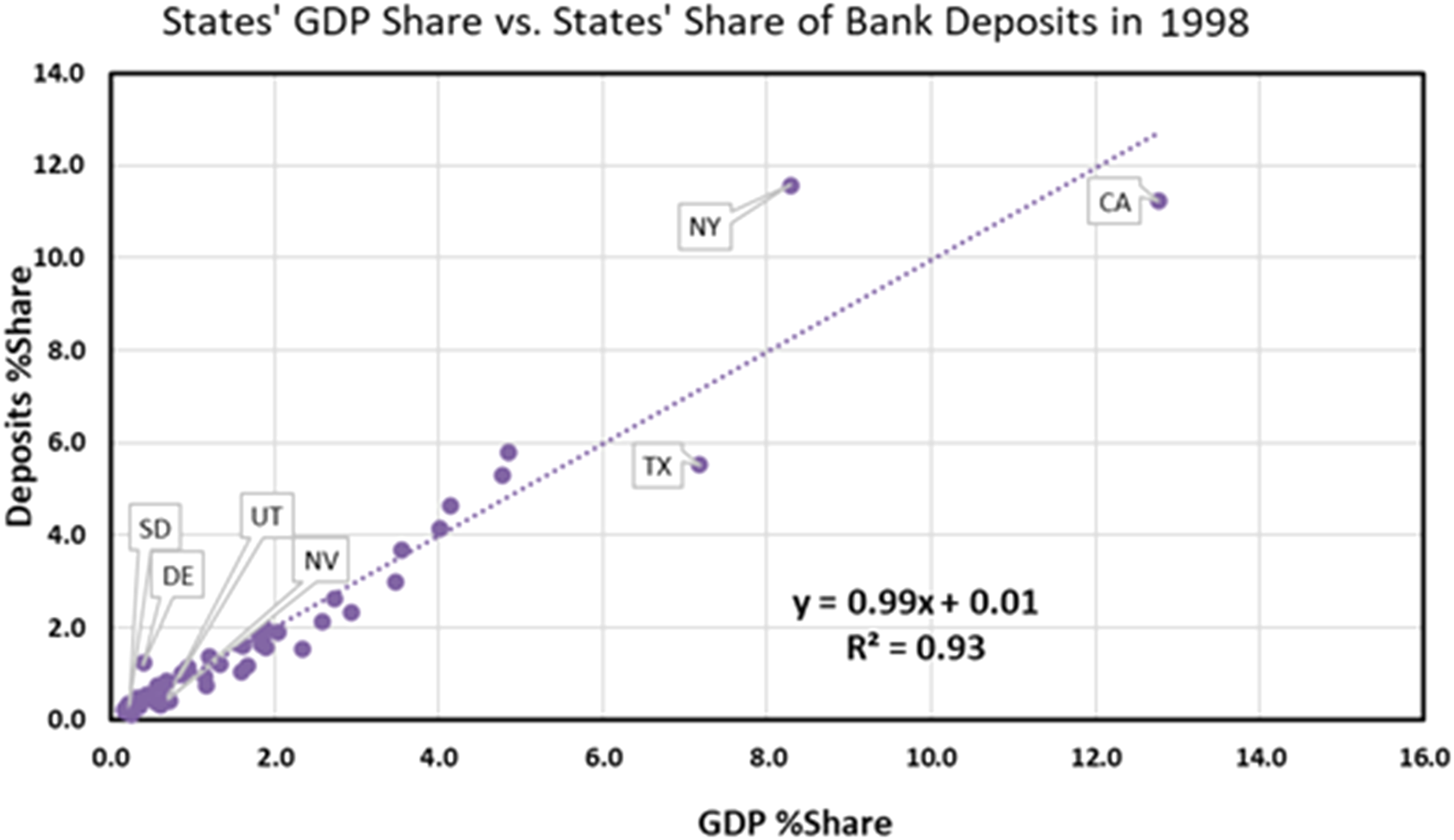

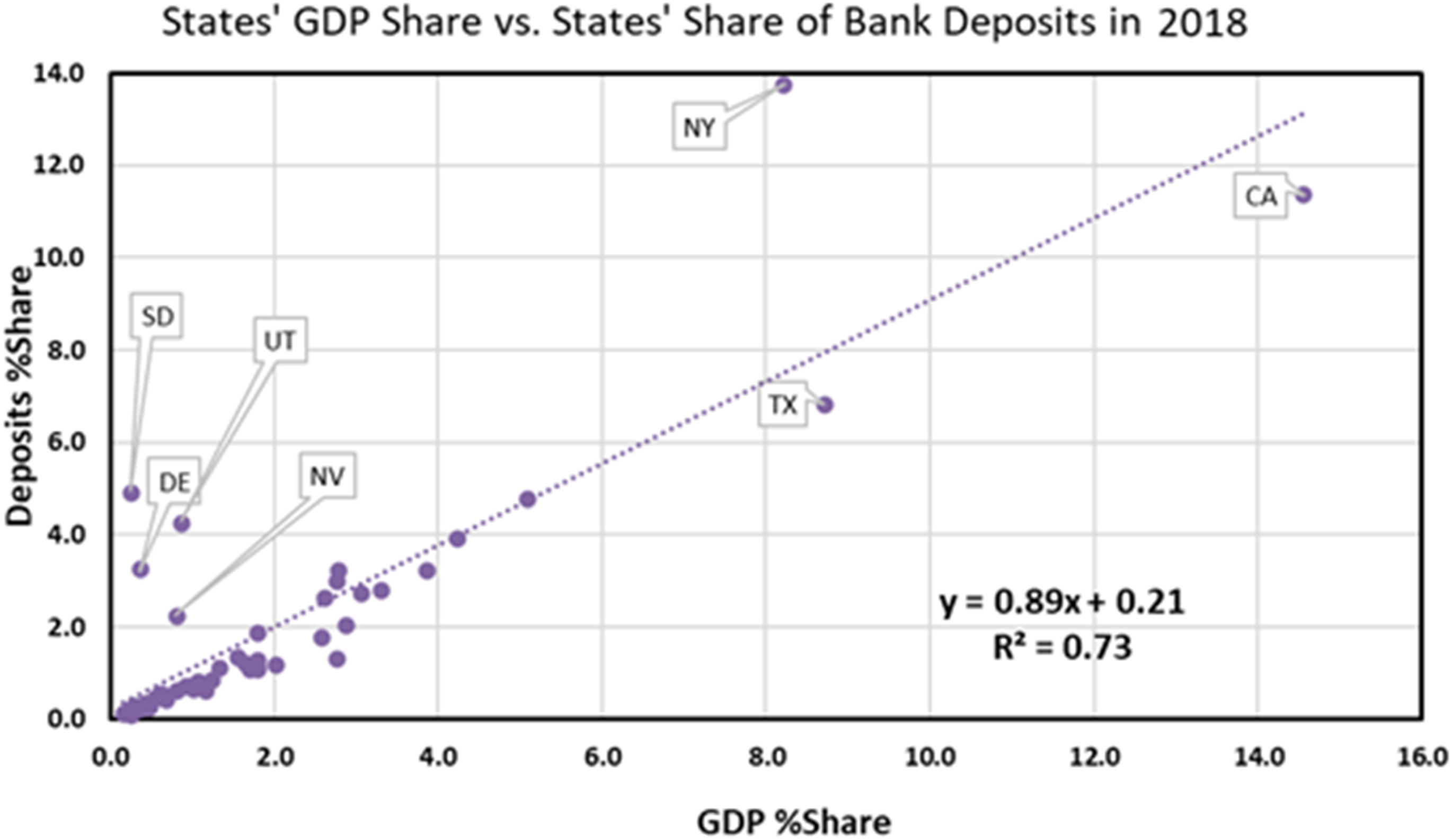

EDA confirmed the expectation that deposit money concentrates where people are concentrated, or where economic activity is abundant. There is a strong co-linear relationship between a state's total bank deposits, population, and GDP. The strongest co-linear relationship exists between a state's deposits and GDP. Figure 1 shows the relationship between states' deposits and GDP in 1998 after converting the values to proportions. Almost all states lie near the regression line. Figure 2 pairs the same variables for 2018, when the relationship between deposits and GDP was slightly weaker than 1998. Nonetheless, the two figures reveal that the relationship between a state's share of the US's bank deposits and a state's share of the US's GDP remained strong for almost all states for two decades.

States' share of deposits vs. domestic product for 1998 (Bureau of Economic Affairs (BEA), 2019; FFIEC, 2019).

States' share of deposits vs. domestic product for 2018 (BEA, 2019; FFIEC, 2019).

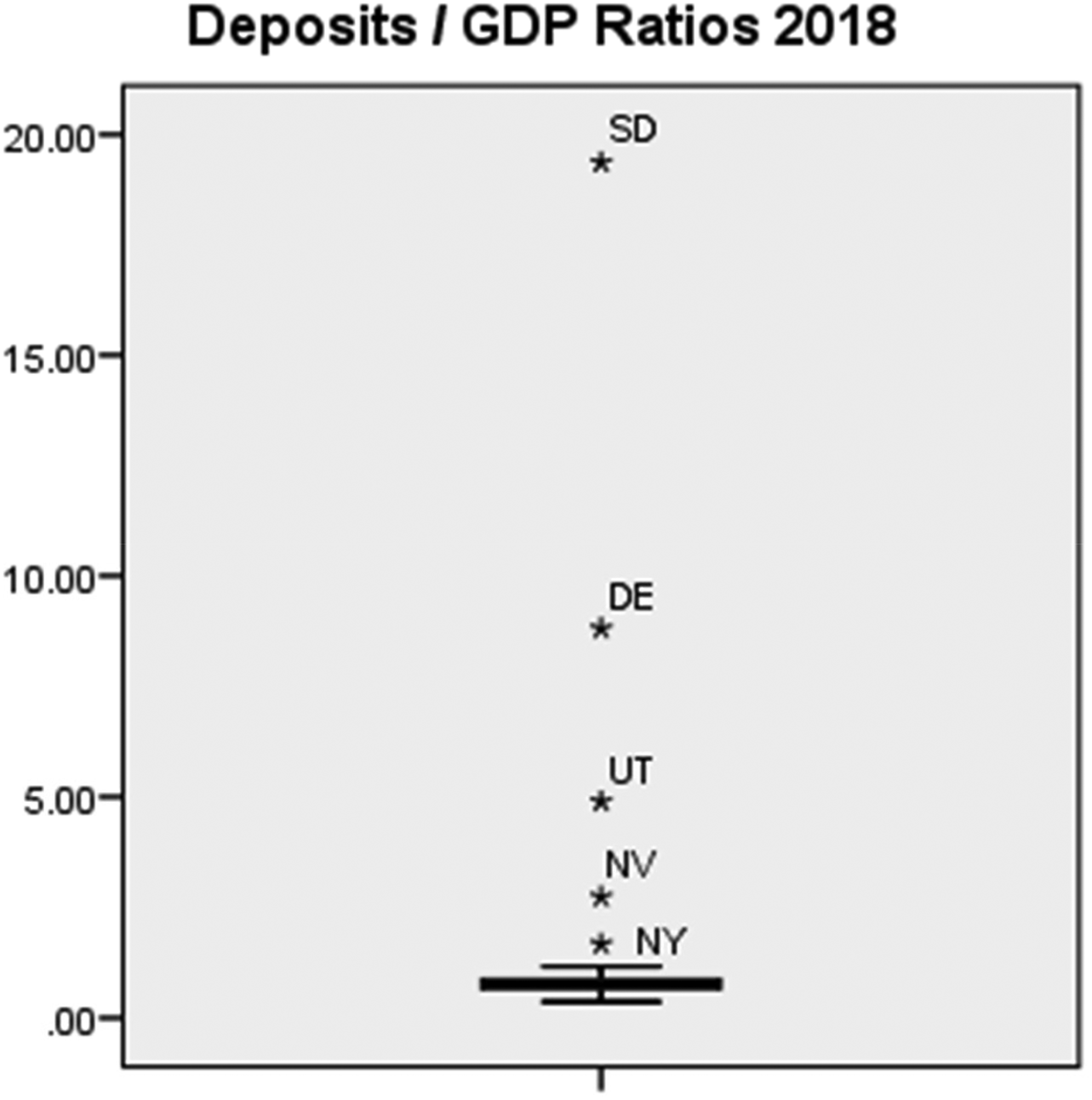

By 2018, however, a remarkable departure between deposits and GDP is observed in four small states: Delaware, South Dakota, Utah, and Nevada. New York, a large state in terms of GDP, also experienced a growth in deposit share. This change is visible by observing that the values of these five states shifted further above the regression line in Figure 2. The distribution of the ratio of 2018 deposits to GDP fails the Shapiro-Wilk test for normality, (W(51) = .293, p < 0.001), suggesting that box and whisker charts are more appropriate than z-scores to identify outlier values. The box and whisker chart (Figure 3) marks values of deposits to GDP ratio outliers belonging to these same five states. The values of their deposits to GDP ratios exceed three times the inter-quartile range for all states.

Box whisker chart: deposits/GDP ratios 2018.

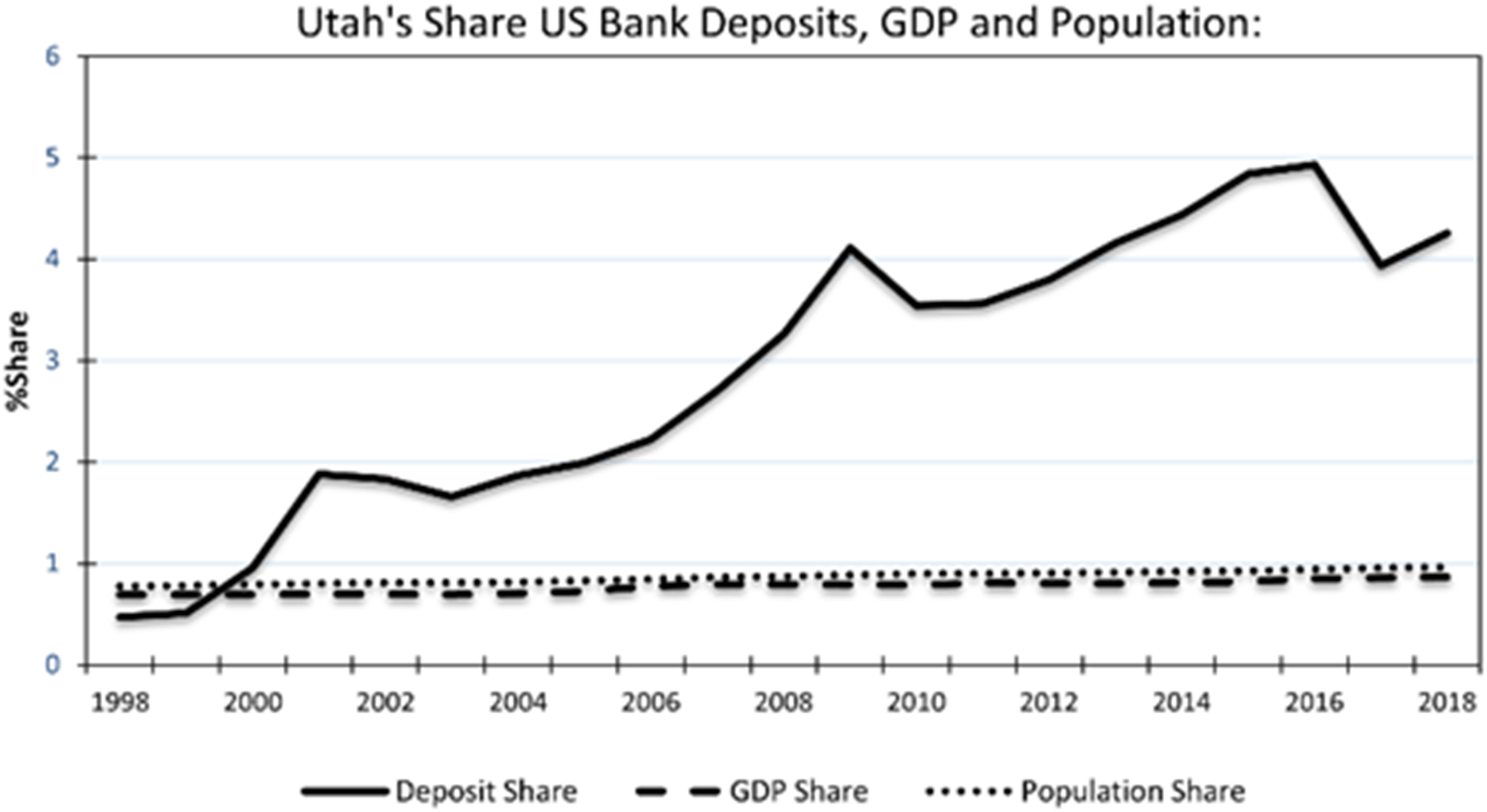

An increasing share of national deposits over time indicates the capacity of the state's banks to attract deposits, relative to banks in other states. The growth of Utah's deposit share is extraordinary. Figure 4 graphs the state's deposit share, along with ancillary economic data. Utah's deposit share increased from less than 1% in the late 1990s to more than 4% after 2013, while its share of national GDP and population remained roughly 1%.

Time series of Utah's share of the US's deposits, GDP and population.

Lifting the veil covering Utah's bank deposit money

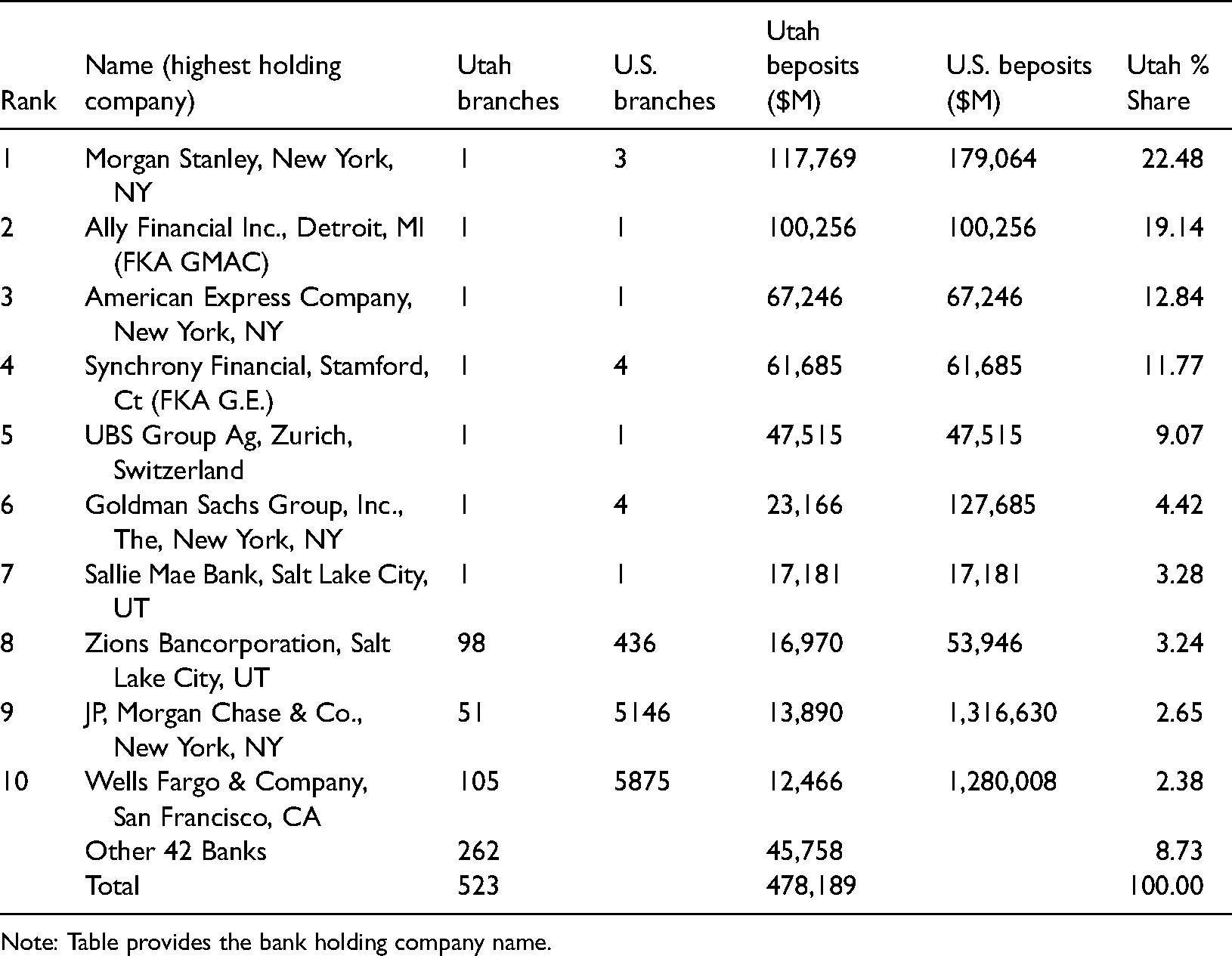

Understanding Utah's money accumulation machinery requires tedious but necessary data forensics. Examining the dominant banking corporations taking deposits in the state along with their numbers of offices reveals irregular characteristics as compared with leading banking firms outside Utah. Table 1, derived from SODS data, lists the top 10 of 52 bank-owning corporations in Utah, based on 2018 in-state deposit market shares. The table includes the number of bank offices for each institution, both inside and outside Utah. Remarkably, Table 1 shows that each of the seven leading banking corporations operating in Utah gather billions of dollar deposits at a single office in Utah. These offices typically occupy commercial space in less busy or accessible locations than typical storefront offices used by most retail banks. Google Street View also shows a lack of signage indicating office locations, while other retail banks' signage is prominent. Four of these top seven banks have their office in Utah serving as their only deposit-gathering location in the US. Even though Morgan Stanley and Ally have offices outside Utah, they chose to book the preponderance of the deposits they collected at their single office in Utah. The same type of market report for any other state reveals a mixture of large- and medium-size banks having a substantial retail branch office footprint spread across the state to accept local depositors' money. Zion, JP Morgan and Wells illustrate the typical office attributes of retail banking: A lot of offices in a lot of places.

Bank deposit market share for Utah in 2018 (FFIEC, 2019).

Note: Table provides the bank holding company name.

Morgan Stanley, UBS, and Goldman Sachs each own a bank subsidiary in Utah. These firms engage in the security broker-dealership business, i.e., “investment banks”. Each is a globally significant Wall Street firm considered “too big to fail” (Financial Stability Board, 2011). JP Morgan and Wells Fargo, who rank 9th and 10th in Utah based on deposits, also have investment bank affiliates, but their presence in Utah is less surprising, since both have a substantial retail branch office footprint in Utah. American Express is a credit card business which also specializes in travel services. Sallie Mae, originally a government-sponsored enterprise, makes student loans (and then packages those loans as securities for sale to investors). Ally is the successor to a bank owned by General Motors, an automotive manufacturer. Synchrony is a successor bank owned by General Electric, a company known for, among other things, manufacturing power generation equipment, durable goods, and light bulbs. Utah's seven leading banking firms engage in many businesses beyond banking.

The business of banking debate

In the US, the practice of separating the business of banking from other sectors of the economy is longstanding. Of course, capitalist firms always oppose any state regulations limiting the activities in which they desire to engage. Citizen groups, labor unions, small businesses, and community banker associations argue that the business of banking must be separated from commerce in order to provide customers credit on an unbiased basis, unencumbered by commercial self-interest Current debate regarding the scope of banking business came to a head before the Senate Banking Committee in 2007, when retail giant Walmart tried to enter the banking business in Utah (the application was ultimately withdrawn in the face of public resistance). At the Senate committee hearings, however, the American Enterprise Institute defended Walmart's application: Not only are there no sound policy reasons for applying the separation in banking and commerce … but doing so would cause harm to consumers and working families. Companies that sell goods and services to the public, retailers, auto companies, others, can save significant cost by gaining access to the payment system through an affiliated depository institution (United States Senate Committee on Banking, 2007, Peter Wallison's testimony).

Other arguments for combining banks and commercial firms include increased profitability; delivery of new products; equity financing to augment lending; and enhancing internal financial oversight and discipline of commercial activity, since banks could encourage appropriate decision making from within a firm rather than from outside it (Krainer, 2000).

Proponents of maintaining the separation of banking and commerce are concerned about the concentration of economic power that combination might enable. Before the same Senate Committee hearings in 2007, for example, the United Food and Commercial Workers Union argued that “Working people are concerned about their money”: I mean, even though some of our members make minimum wage, they are concerned about where their money goes. But if you have a company that comes into a town, specifically a small town, and takes over the hardware store and the florist and the bakery and the grocery store, and then they have to be your bank, too, that is a problem for us, whether it is Walmart or another large retailer (United States Senate Committee on Banking, 2007, Briged Kelly's testimony).

An affiliation exists when two separate firms are related through common ownership. There are potential conflicts of interest between a bank and any affiliated non-banking firms. When making loans, banks collect proprietary information from borrowers. Banks also set prices and terms on loans. A company owning a bank may influence the business decisions of their affiliated firms based upon the proprietary information collected from an affiliate's competitor. A bank may be pressured to offer their affiliates favorable loan prices and terms and deny the same prices and terms to an unaffiliated competitor. If a bank feels an obligation to bail out a financially troubled affiliate, the safety and soundness of that banking firm is at risk. Furthermore, ownership affiliations between banks and commercial firms extend the federal safety net of deposit insurance to the commercial sector of the economy.

The tradition of separating banking from commerce in the US presumably mirrors the practice established in the Bank of England Act of 1694, which prohibits the bank from “buying or selling of any Goods Wares or Merchandizes whatsoever” (Bank of England, 2015). Similar restrictions were included in the 1791 charter of the First Bank of the United States (Federal Reserve Bank of Philadelphia, 2009). These early “best practices” led federal and state policy makers to strictly limit banking businesses' powers. The National Bank Acts of the 1860s used New York's legislative standards for chartering banking corporations, which included the business powers to receive deposits and issue debt, and excluded powers to “directly or indirectly, deal or trade in buying or selling any goods, wares, merchandise or commodities” (Shull, 1999; see also Wilmarth, 2007). These laws demonstrate the longstanding US view that the business of banking is understood to be financial activities closely related to accepting deposits and issuing loans—and separate from other commercial activities.

In the US dual banking system, the federal government charters national banks and Congress determines their business powers, while each of the 50 states is empowered to charter, regulate and define the powers of state banks. Over time, both the federal and state governments have used charters to expand and contract banks' business powers. For example, states such as Delaware and South Dakota permitted their banks to sell and underwrite insurance, while federal banking regulators denied those powers to bank holding companies owning banks in those states. For the most part, however, banking and commerce remain separate businesses. Yet, one type of institutional charter, the ILB, was exempt from federal regulation prohibiting non-banking activities. Utah's seven leading banks (Table 1) were chartered as ILBs. At the peak of the financial crisis, most of these leading banks urgently required eligibility for federal bailouts and access to the Federal Reserve discount window. That eligibility was conditioned on converting their ILB charters to national or state banking charters. But it is the legacy of the ILB charter that is the special feature that unites the seven banks listed in Table 1.

A series of laws granting ILBs special powers

The ILB charter is a financial innovation developed a century ago by Arthur J. Morris, an attorney serving banking clients in Norfolk, Virginia, who observed the difficulty working people experienced when seeking bank loans. Industrial workers, having no loan collateral, could not qualify for bank credit from commercial banks or savings banks. In Morris's business model, credit was extended to wage earners on the basis that the borrowers obtain loan guarantees from two reputable members of the community. In 1910, Morris obtained a special purpose state bank charter in Virginia to implement his model. Morris and other opportunistic copycats replicated this business model, creating state-chartered ILBs and licensed industrial loan companies (ILCs) across 40 states (Barth et al., 2012). Later, commercial banks began providing credit to wage earners, soon dominating the market. The size and scale of their operations, and their ability to gather low-cost deposits through FDIC insurance, allowed commercial banks to enjoy competitive advantages over ILBs and ILCs. These competitive advantages led to ILBs' obsolescence, stunted growth, and later contraction (Baradaran, 2013). However, a handful of ILBs persisted in a few states.

During the Great Depression, many suffered financial ruin with the destruction of deposits they entrusted to failed banks. The Banking Act of 1933 (Pub. L. 73–66), commonly known as the Glass-Steagall Act, established the FDIC as an independent agency of the US government to administer deposit insurance. FDIC insurance renewed depositors' trust in banks. For bankers, FDIC insurance allowed them to attract money capital at low cost. To minimize risks to the deposit insurance fund, Glass-Steagall required banking firms to operate as either a commercial banking firm or an investment banking firm. The former, engaged in business limited to accepting deposits and making loans, were eligible for FDIC insurance. The latter, engaged in riskier business like underwriting stock or trading securities, were ineligible for this federal safety net.

In response, large commercial and financial firms sought legal methods to work around laws prohibiting combining banking and non-banking business. The primary instrument of these efforts was the bank holding company, which is structured to skirt regulations limiting the business activities of banks. A bank holding company, which is not itself a bank, could control both a bank and non-banking firms engaged in activities not directly permitted by banks.

In an attempt to reassert the separation between banking and non-banking business, the 1956 federal BHCA (12 U.S.C. § 1841) barred the affiliation of banking and non-banking business and empowered the Federal Reserve to regulate the business activities of bank holding companies and their subsidiaries. But the BHCA only applied to holding companies owning two or more banks—leaving single-bank holding companies free to engage in non-banking activities. Perhaps because of their relative insignificance, ILBs were explicitly exempted from the BHCA (Johnson and Kaufman, 2007).

Unsurprisingly, commercial and financial firms rushed to form single-bank holding companies, which either acquired or formed a new bank and also owned other firms involved in non-banking businesses. The Bank Holding Company Act of 1970 (Public Law 91-607), Sect. 2(c)) amended the earlier BHCA to equally apply to both multi- and single-bank holding companies. Nevertheless, this renewed effort to separate banking and non-banking business was quickly outmaneuvered. The amended BHCA changed the definition of a bank, which it deemed an institution that performed two functions: accepting demand deposits and making commercial loans. This revised definition gave rise to a new business creature not subject to the regulatory constraints of the BHCA: the “non-bank bank”. Banks of the non-bank bank type either accepted deposits or made commercial loans, but not both. Free from BHCA regulation, corporations like General Electric, Sears, and General Motors established non-bank banks to compete for bank deposits and originate non-commercial loans. The non-bank banks captured market share from banks of the traditional “bank” type. The unconstrained non-bank banks enjoyed the benefits of FDIC insurance while their traditional bank competitors were constrained in their business to accepting deposits and issuing loans. Even Chase Manhattan, a large money center bank that lends to governments, large corporations, and smaller banks, considered “debanking” to a non-bank charter (Proxmire, 1987). In a new attempt to readjust the business powers for non-bank banks and banks resulting from the BHCA amendments of 1970, the Competitive Equality Banking Act (CEBA) of 1987 (Pub. L 100-86) redefined a bank once again. This time a bank was defined as any institution receiving FDIC insurance (Huber, 1988). Existing non-bank banks were grandfathered. However, CEBA limited existing non-bank banks' growth, ultimately leading to their obsolescence, thus reinscribing the separation of banking and non-banking business.

US Senator Jake Garn of Utah used his power on the Senate Committee on Banking to shape banking law to strengthen his home state's ILB constituents. The 1982 Depository Institutions Act (Pub. L. 97-320), also known as the Garn-St Germain Depository Institutions Act, made ILBs eligible for FDIC insurance. In addition, Garn, as the ranking member of the Senate Committee on Banking, introduced an explicit exemption of ILBs from the definition of a bank during the final draft of the CEBA legislation (Johnson and Kaufman, 2007). The exemption enabled non-banking commercial firms and investment banks to own an FDIC-insured non-bank bank in the form of an ILB. Furthermore, CEBA prohibited new ILB charters in states that did not already have a statute requiring ILBs to have FDIC insurance, thus protecting Utah from interjurisdictional competition, since only Utah and six other states had such a statute in place.

Within a year of CEBA's passage, General Motors became the first commercial owner of an ILB, acquired in Utah. Merrill Lynch, which owned a non-bank bank, rushed to Utah to obtain an ILB charter. Utah's members of congress also thwarted future efforts to limit ILBs' special regulatory privileges. The 1999 Gramm-Leach Bliley Act (Pub. L. 106–102, 133 Stat. 1338) (GLBA) repealed parts of Glass-Steagall, enabling financial and banking firms to affiliate as subsidiaries of a financial holding company, which was granted business powers to simultaneously engage in commercial banking, investment banking and insurance, subject to the regulatory oversight of the Federal Reserve. GLBA retained the longstanding prohibitions barring banks from owning commercial firms and commercial firms from owning banks, and closed the loophole allowing commercial firms to own a single savings bank.

But once again ILBs' special exemptions were included. The ILB became the only option for a commercial firm to own a bank, or for an investment bank to own a bank free from Federal Reserve oversight. The safety net of federal deposit insurance now extended beyond the banking sector into the wider financial and commercial sectors of the economy. Utah actively promoted its special privilege to charter ILBs with eligibility for FDIC insurance, and some of the largest commercial conglomerates and many of the largest investment banks in the US stampeded into Utah to establish ILB subsidiaries. Utah became the banking regulator of the largest banks offering financial services nationally and internationally.

Goldman Sachs, Morgan Stanley, UBS, Lehman, and other large Wall Street investment banks followed Merrill Lynch with ILBs in Utah. Together, the ILBs owned by the holding companies that also owned investment banks, and several ILBs owned by commercial firms, contributed the lion's share of Utah's deposit growth during the 2000s. Since the investment banks' holding companies chose ILB charters for banking subsidiaries rather than reorganizing as a financial holding company, it is fair to assume the choice was motivated in part to avoid Federal Reserve supervision. Utah's FDIC-insured ILBs provided a warm resting place for deposits gathered worldwide to serve as interest-earning brokerage cash accounts linked to Wall Street firms' brokerage customers (Ergungor and Thomson, 2006; Spong and Robbins, 2007). These developments transformed Arthur Morris's small limited-purpose ILBs serving wage earners into deposit-gathering instruments for G-SIFIs serving a wealthy global clientele. UBS, for instance, used their Utah deposits to fund loans to high-net-worth individuals located around the world (Johnson and Kaufman, 2007). With the special privilege of avoiding BHCA regulations while licensed to accept federally insured deposits, ILBs in Utah quadrupled the state's share of US national bank deposits from 1% to more than 4%.

Utah's BHCA circumvention strategy fell apart abruptly with the financial crisis of 2008. Many institutions, particularly those with ILB subsidiaries in Utah, were on the brink of financial collapse. The Troubled Asset Relief Program and access to the Federal Reserve discount window provided a lifeline but required G-SIFIs like Morgan Stanley and Goldman Sachs to expeditiously relinquish their ILB charters and reorganize as financial holding companies regulated by the Federal Reserve. Other firms with Utah-based ILBs such as Merrill Lynch elected to merge with existing bank holding companies (Luhby, 2008).

Wall Street firms' abandonment of the ILB charter may have redirected deposit flows away from Utah. Without an ILB charter, G-SIFIs surrendered the regulatory advantages associated with locating in Utah. Looking at the bank deposits market share report (Table 1), UBS and Sallie Mae Bank are the only top seven Utah banks holding an ILB charter today. SODS data confirm, however, that disproportionate deposit accumulation persists in Utah. This may be partly the result of state taxes. High tax locations like New York City—a typical command and control location for G-SIFIs—provide some incentive to maintain bank subsidiaries in low tax states like Utah even without an ILB charter. In a proactive maneuver to maintain the status quo, Utah exploited its own law-making powers through tax abatements to nudge G-SIFI firms to remain in state and increase capital investment. Goldman Sachs and Morgan Stanley inked special tax abatement deals with the state in 2012 (LaCapra and Wachtel, 2012) and Goldman Sachs obtained additional tax rebates in 2014 in exchange for adding new in-state jobs (Utah Governor’s Office of Economic Development, 2014). Even though Utah's leading banking firms eventually found it expedient to switch banking charters, the ILB charter was the critical force that stimulated institutions to establish deposit gathering in Utah.

Circumventing legal limits to capital's expansion

Why are G-SIFIs and large commercial conglomerates able to find ways to engage in the business of banking, regardless of any regulatory obstacle? Large capitalist firms deploy their immense market power to disrupt regulation obstructing their accumulation strategies (Mann, 2013: 50–51). Since banking capital is particularly mobile, the principal strategy, known as regulatory arbitrage, is to shop the regulatory marketplace for new spaces offering firms the legal powers (Potts, 2016) to engage in the businesses they desire. Banking firms adapt their spaces of operation and restructure their businesses to take advantage of gaps between the regulatory demands of their current locations and those of their new spaces (Aalbers, 2018; Fleischer, 2010; Leyshon, 1992). In many ways, this process is a clear variation on the “spatial fix”, Harvey's famous term for the spatial solution to a crisis of accumulation: “geographical expansion depended crucially upon…the search for markets, fresh labor powers, resources (raw materials), or fresh opportunity to invest in new production facilities” (Harvey, 2001: 26). We can add to this the search for accommodative law. Firms seeking bank ownership found their legal fix through an ILB chartered in Utah and when they moved in, they brought their highly mobile deposit-gathering machinery with them.

Capitalist firms' demands for accommodating laws are supplied by competitive entrepreneurial states (Harvey, 1989) which create regulatory gaps between themselves and other states. These gaps benefit the industries and firms for whom they are designed, while the state benefits from tax revenues, charter fees, jobs, and other capital investment the firms bring to the states. In other words, law has a value that can be monetized (Pistor, 2020), and the uneven playing field offered by Utah is of special added value for themselves and for non-banking firms engaging in banking.

Banking law suppliers in the US include a combination of regulations produced at the federal level and individual state governments who have powers to regulate state-chartered banks. In the case of state-chartered banks, the opportunities of accommodative law from Utah are particularly attractive, because the benefits provided extend far beyond the state's territory. State-chartered banks' business powers have national and global reach. For instance, if a firm obtains a banking charter for a subsidiary in Utah, that bank can accept insured deposits from—and issue loans to—depositors and borrowers worldwide.

It is no accident that ILBs flourished in Utah while not emerging elsewhere. When CEBA closed the non-bank bank loophole, Utah's Senator Garn seized the opportunity to attract the non-bank banks from other locations to his state by not only exempting ILBs from the definition of a bank: He also inserted barriers in the law to other states' entry by denying them the same rights to charter their own ILBs unless they happened to have statutes already in place requiring their ILBs to obtain FDIC insurance. The state-chartering banking powers of Utah allowing non-banking firms to own banks, combined with exemptions from the BHCA and the federal safety net of deposit insurance, make regulatory benefit differences between Utah and all other states exceptional. Utah’s Department of Financial Institutions (2020) gleefully markets ILB charters and their BHCA exemptions to attract banking firms into the state.

Going behind and beyond: The hidden character of law

For decades firms' efforts to expand the business scope of banking despite any regulatory barrier fit directly into Harvey’s (2010: 47) reasoning that capital's expansion cannot abide to any limits. Why are legal decrees bounding the business scope of banking capital ultimately remodeled into new laws expanding their business powers?

Recent Marxist scholars of jurisprudence (Balbus, 1977; Miéville, 2004; Webb, 1985) suggest that law parallels the logic of the fetishized commodity. Just as the commodity obscures the human conditions behind its production, law hides the social and political interests upon which it is constructed. Like the commodity, the apparent “objective character” of the law hides the social reality of the law, why law holds in specific places, and whom the law serves. As legal subjects, we come to fetishize law. In a “democracy”, law is conceived as that social framework that preserves formal equality, liberty, and justice for all. On this conception of law, we relate to each other as social and political equals. But the “objective character” of “justice” disguises class domination. There is a class character to legal relations. The interests of the ruling class are installed as law. Labor does not have the financial means to match capital's ability to shop the regulatory marketplace at the same scale as the G-SIFIs. Labor cannot easily relocate to more favorable jurisdictions like highly mobile capital. States are not using law to import new labor like they do for capital investments. Defetishizing the money commodity or defetishizing law leads to similar conclusions: Behind the veil of objective neutrality is a systematic domination via money capital and state-sponsored legal capital to extract greater surpluses. The riddle of the money fetish is therefore the riddle of the legal fetish.

Money, Marx (1990: 256) famously said, “preserves and multiplies itself within its circuit, comes back out of it with expanded bulk, and begins the same round ever afresh.” Essentially Marx argues that money is deployed by capitalists for the purposes of self-expansion. Like money, law is deployed by capitalists, in coordination with the state, to abet this process. The largest U.S. securities firms, among the most powerful firms on the planet, own a Utah-chartered ILB. These firms found that insured deposits provided superior returns over uninsured money market mutual funds (Wilmarth, 2007). With banking deposits covered by federal insurance, the costs to bank-owning firms for new money capital declines, enabling the combined business firm to retain more surplus for themselves. In return for the law, Utah also makes more money. The new money paid to the state by bank subsidiaries includes franchise taxes, charter fees, bank examination fees, jobs and office rents. The law serves capitalists as a surplus capital-generating commodity.

Unmasking the lopsided share of Utah's money reveals important relations between bank-owning firms, governments, a worldwide set of investors, and a hidden underclass of worldwide labor. Investors' bank accounts located in Utah are credited by interest on debts, rents, and surplus values extracted from worldwide labor. Those same investors are also related to Wall Street firms, commercial conglomerates, and governments who traded for the laws that produced the advantageous environment for banking businesses, benefitting ILBs and their holding companies. Investors do not see their connection to the class of laborers they are related to, the government laws that gave their banks their powers and, in the cases of their sweep accounts held at brokerage firms, they may not know the bank that holds those deposits, the type of charter the bank holds or where that bank is located. They only see their money in their deposit accounts. Likewise, those investors do not see the lawmakers who made ILBs' exemptions possible.

The modified approach to follow and defetishize money used in this paper can be replicated by going behind and beyond the many locations where money accumulates. Like Utah, Delaware, Nevada, and South Dakota also report a lopsided share US's money. Each of these locations' concentrations of money merits defetishization. The defetishization will likely reveal many targeted legal spatial fixes these states provide their capitalist firms to circumvent regulatory barriers to their capital expansions. Given the many locations where money accumulates, there is so much more work for geographers to do.

Footnotes

Acknowledgements

I am grateful to Geoff Mann, Suzana Dragicevic, and Elvin Wyly for the encouragement, support, and insightful comments they gave me to develop and complete this paper. I also extend my thanks to the anonymous reviewers for their useful comments and suggestions.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.