Abstract

During the 2010s, collateralized loan obligations rapidly became a trillion-dollar industry, mirroring the growth profile and peak value of its cousin—collateralized debt obligations—in the 2000s. Yet, despite similarities in product form and growth trajectory, surprisingly little is known about how these markets evolved spatially and relationally. This paper fills that knowledge gap by asking two questions: how did each network adapt to achieve scale at speed across different jurisdictions; and to what extent does the spatial and relational organization of today's collateralized loan obligation structuration network, mirror that of collateralized debt obligations pre-crisis? To answer those questions, we draw on the global financial networks approach, developing our own concept of the networked product to explore the agentic qualities of collateralized debt obligations and collateralized loan obligations—specifically how their technical and regulatory “needs” shape the roles and jurisdictions enrolled in a global financial network. We use social network analysis to map and analyze the evolving spatial and relational organization that nurtured this growth, drawing on data harvested from offering circulars. We find that collateralized debt obligations spread from the US to Europe through a process of transduplication—that similar role-based network relations were reproduced from one regulatory regime to another. We also find a strong correlation between pre-crisis collateralized debt obligation- and post-crisis collateralized loan obligation-global financial networks in both US$- and €-denominations, with often the same network participants involved in each. We conclude by reflecting on the prosaic way financial markets for ostensibly complex products reproduce and the capacity for network stabilities to produce market instabilities.

Introduction

When the collapse of the collateralized debt obligation (CDO) market in 2007 brought about one of the deepest financial crises in modern times, it was assumed by some commentators that it would sound the death knell for the structured finance revolution which had transformed loan markets during the early 2000s 1 . Yet although the CDO market never recovered, by the end of 2018 amounts outstanding for collateralized loan obligations (CLOs)—a close relation to the CDO—were at or around the same value as the CDO market at its peak, raising important questions about the regenerative capacity of finance after major crises. Recent research has highlighted the political dimension of the post-crisis renaissance in securitization (Aalbers and Engelen, 2015; Braun, 2020). However, there is very little work on how these markets themselves adapt and reorganize across space and time in order to regenerate and re-scale at speed, or indeed whether these two securities are organized entirely differently from each other.

Authors working within the global financial network (GFN) framework have typically understood questions of financial security production and market development by examining the networked relations between large banks operating in global financial centers and a range of advanced business service providers operating in on- and off-shore jurisdictions (Coe et al., 2014; Lai, 2018; Wójcik, 2018). This work has provided an integrated way of understanding financial and territorial network evolution as financial products of different kinds are brought to market. Other studies have flipped this analysis, examining how the agentic properties of products themselves organize financial and spatial networks, facilitating market expansion (Faulconbridge et al., 2007; Haberly et al., 2019). This paper develops our own concept of the “networked product” to understand and integrate these dialectical processes, whereby networked actors shape products as they bring their spatially embedded expertise to bear upon them; and products shape networks as their technical and regulatory “needs” influence which roles and jurisdictions are enrolled in their structuration. We explore whether relations of this kind can become mutually reinforcing or isomorphic, producing the architectural stability that allows markets to scale or regenerate at speed, which would provide one explanation for the rapid regeneration of structured finance markets after the 2008 crisis.

To explore this idea, we ask two basic research questions. First, how do securities markets like CDOs and CLOs organize across multi-jurisdictional spaces to achieve scale at speed? Second, to what degree do today's CLO structuration networks, in terms of their actor relations and spatial networks, resemble those of CDOs pre-crisis? By answering those two questions we aim to form a better understanding of how financial networks reproduce in space and time and how financial products play a role in organizing those networks.

We answer these questions through an empirical study which examines the structuration of US$- and €-denominated CDOs and CLOs using data extracted from 706 offering circulars (OCs) between the years of 2000 and 2018. We analyze those relations using social network analytic techniques and measure network similarity within and across those markets. We find that CDOs were able to scale at speed by organizing through a process of transduplication—that product needs led to a mirroring of activity-based networks as the market moved from one regulatory regime to another in search of new collateral to securitize. This organizational form allowed markets for CDOs—and later CLOs—to scale at speed. We also find a strong correlation between pre-crisis CDO and post-crisis CLO networks, with often the same network participants involved in each. However, we do find some evidence of “adaptive resilience” (Wójcik and Cojoianu, 2018) when regulatory change leads to minor reorganizations in advanced business services. We conclude that whilst financial securities may embody some degree of calculative and technical complexity, the spatial and organizational relations which bring those products to market are often simple, regular, and characterized by recurring patterns of exchange (Christophers, 2009). We consider the implications of these network regularities for financial market resilience and the possibility that these network stabilities may create financial market instabilities.

Our work contributes to the literature on the spatial architecture of financial products (Clark and O’Connor, 1997), the post-crisis renaissance of securitization markets (Aalbers and Engelen, 2015; Wójcik and Cojoianu, 2018), and the GFN literature generally (Coe et al., 2014; Lai, 2009, 2018). Specifically, we provide new empirical work on patterns of continuity and change in the relations between on-shore and “off-shore” centers (see Clark et al., 2015; Wójcik, 2013a) and add to the ongoing work on the sensitivity of advance business services’ organization to regulatory change (Haberly et al., 2019; Wójcik, 2013b).

Our paper proceeds as follows: the next section briefly revisits the work on relational global financial centers and the contributions made by the GFN framework, before outlining our concept of the networked product to explore the agentic qualities of products in shaping spatial and organizational relations. In “Data and Method” we describe our self-built database and the social network analytic methods used to investigate that data. The “Findings” section presents our empirical results, applying the networked product concept to CDOs and CLOs, establishing how those securities organize to achieve scale and identifying similarities and differences between CDO and CLO GFNs. The discussion sets out the implications of our approach, method and findings for existing and future work; and reflects on the relation between network regularities and market disruption. The final section concludes the paper.

Framing financial networks: From relational global financial centers to GFNs and networked products

From the early 1990s to the mid-2010s, economic geography understandings of financial product and market development advanced through the theorization of global financial centers as relational sites (Amin and Thrift, 1992; Christophers, 2013; Clark, 2002; Cook et al., 2007; Faulconbridge, 2004; Martin and Pollard, 2017; Wójcik, 2013a). It was argued that global financial centers generated relational agglomeration economies and competitive advantage (Clark et al., 2015; Wójcik, 2013b) and that these were best understood through four main processes. First, as sites for directing flows of capital, labor and information in a network of relations that included advanced business service organizations and institutions (Beaverstock et al., 2005; Clark, 2002; Faulconbridge, 2004; Lai, 2009; Sassen, 1999; Taylor et al., 2014; Wójcik, 2013a). Second, as sites which navigated regulatory difference bridging on- and off-shore jurisdictions (Aalbers, 2018; Clark et al., 2015; Haberly and Wójcik, 2015), which could be either global financial centers or smaller specialized off-shore financial centers acting as conduits or sinks for flows of assets (Garcia-Bernardo et al., 2017). Third, as sites to initiate, evaluate, and close business transactions, in a labor process fostered by trust, reputation, and reciprocity (Beaverstock and Hall, 2012; Dorry, 2016; Hall, 2011, 2019). Fourth, as sites that generated demand for adjunct advisory and administrative expertise through the intermediation of advanced business services, sustaining the work of particular epistemic communities within and between on- and off-shore jurisdictions (Clark et al., 2015; Cook et al., 2007; Hall, 2009; Wójcik, 2013b).

These individual studies contributed greatly to our understanding of the spatial contours of financial market development. However, much of this knowledge was generated in a fragmentary way through global financial center focused case studies (e.g. Thrift, 1994) or isolated studies of “inter-city” relations (Beaverstock et al., 2005). From the mid-2010s, Coe et al. (2014) developed a more unified and holistic approach drawing on the insights of Global Production Network scholarship (Henderson et al., 2002). The resulting GFN framework produced an integrative analysis of the key advance business service firms (building on Wójcik, 2013b), and the geography of world cities and off-shore jurisdictions to conceptualize agency and power relations in financial and territorial networks (Coe et al., 2014: 763; Lai, 2018; Wójcik, 2018). The GFN framework has since been used to frame a multitude of empirical studies from financial networks and regional development in China (Pan et al., 2020) to the establishment of fintech ecosystems in Europe (Hendrikse et al., 2020).

Importantly for the purposes of this paper, the GFN framework acknowledges an enlarged role for advanced business services which connect and coordinate relations between on- and off-shore financial centers to produce the networked architectures that allow markets to grow or regenerate more easily (Coe et al., 2014: 764). There is also some recognition that these networks operate across different fields and may change over time as regulation or technology evolves. Haberly et al.’s (2019) analysis of asset management platforms, for example, unpacks the four-pronged interactions between, “the ‘relational’, ‘virtual’, ‘technical’, and ‘paper’ geography of finance” where each sphere has its own centripetal and centrifugal processes which combine “to condition the role and formation of particular financial centres” (p. 169). They argue that technological change and disruptive innovation could lead to global financial center “de-clustering” or “centrifugal unbundling” as capital and labor seek low-cost solutions and locations, whilst the “paper geography of finance” may flow disproportionately to off-shore financial centers as havens for tax efficiency (Haberly et al., 2019: 170).

GFNs through a product-centered lens: The networked product

In Haberly et al.’s (2019) example, the effects of technological and regulatory change have the potential to transform products and the spatial and relation organization of their GFN. This implies a more complex, interactive relation between territories, actors, and products. This multi-directional causality is the concern of Faulconbridge et al. (2007) who considers the implications of changes in the stock exchange landscape for financial center development, focusing on the trade of different financial products in Amsterdam. They conclude that the type of financial product developed and traded in each center shapes the spatial (re)configuration of Europe's financial centers, with implications for the clustering of local epistemic communities. Financial centers, in other words, may structure financial products, but the characteristics of those products also reproduce and reconfigure clusters of expertise within different financial centers.

To apply this product-centered approach within a relational GFN frame, we offer our concept of the “networked product.” Networked products represent a spatio-temporal mode of organization based on two orders of interaction: emergence and transformation. In terms of emergence, the concept describes a dialectical relation whereby a network of actors shape the product as they bring their situated expertise to bear upon it; but the product also shapes the network as its characteristics create “needs” that influence which roles and jurisdictions are enrolled in its structuration. Those “needs” are determined by the product's techno-scientific, risk-mitigating, economic, and legal characteristics. Consequently, the spatial networks formed depend not only on the location of skill clusters but also the regulatory environment and the opportunities to lower costs or arbitrage rules which are central to what Haberly et al. (2019) term the “paper geographies” of finance. Whilst the need to lower costs, for example, provides sourcing advantages for actors based in low-tax jurisdictions over others (Christophers, 2014; Fleischer, 2010), the wider legal regime—whether contracts are written in English law for example—may also create strong incentives to locate other activities in a jurisdiction with a similar history of English law systems. These legal complementarities between territories can emerge from historic colonial dependencies (de Goede, 2020), or may be engineered actively by states to provide local corporate interests with access to new markets (Rixen, 2013). A center like Luxembourg, for example, achieved a specialist nodal position in “investment fund global production networks” by tweaking regulatory structures to reduce costs for specific tasks, whilst benefitting from wider complementarities between its regulatory regime and others (Dorry, 2015).

Networked products can therefore explain relational stability, for example if they produce strong financial incentives for national jurisdictions to preserve or reform rules to protect their domestic service providers from competition in particularly lucrative structuration networks. Yet networked products also have the capacity to be transformational (the second order of interaction): the ensemble of actors and products are adaptive, capable of changing form and structure to circumvent legislative impasses or open-up new market opportunities for the product. Understanding the regrowth of securitization markets from a networked product perspective therefore allows us to consider the regularities and adjustments in network form that occur when GFNs expand into new territories to achieve scale, as CDOs did pre-2008; or when whole markets regenerate after a crisis, as was the case with CLOs after 2008. To understand these processes, we first need to engage with the technical and organizational features of those products, before mapping the GFNs that arise as a consequence of those product features and the requirements they demand. Our subsequent sections will do just that, and we describe our data and methods below.

Data and method

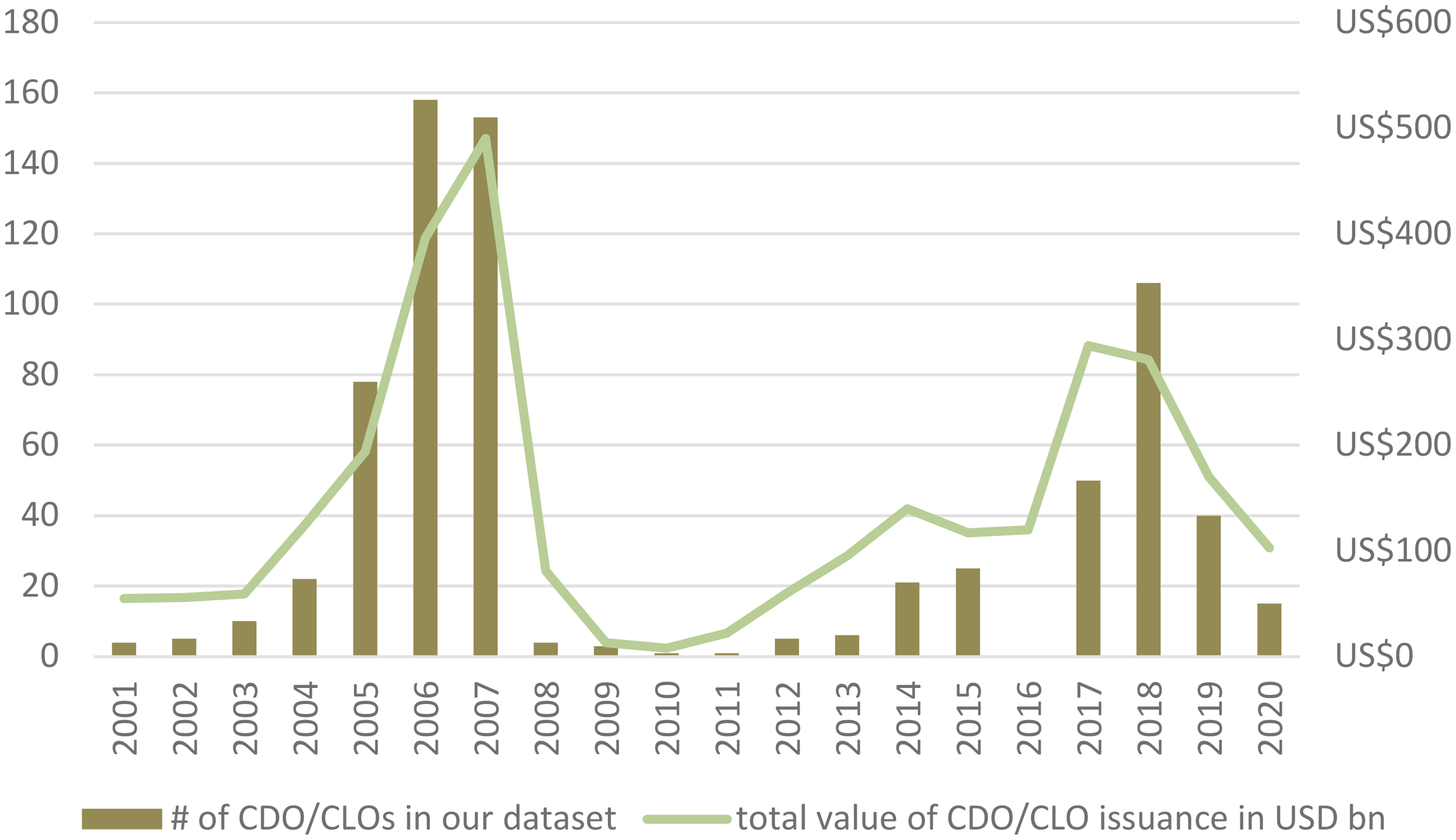

To understand the needs generated by CDOs and CLOs, and to then map and analyze the GFNs that emerge from those needs, we draw on data collected from OCs for both US$- and €-denominated CDOs and CLOs. OCs detail the participants involved in the structuration process, their location and their role within the structuration process. We extracted this data, producing our own dataset on organizational actors and their jurisdictional base, as well as their role played in the structuration network. Our dataset only comprises CDOs and CLOs for which OCs are publicly available and as such represents a subset of all CDOs proportionate to the overall volume issued each year according to SIFMA (2021) (see Figure 1).

Number of products in our dataset mapped against overall value of all CDO/CLOs issued.

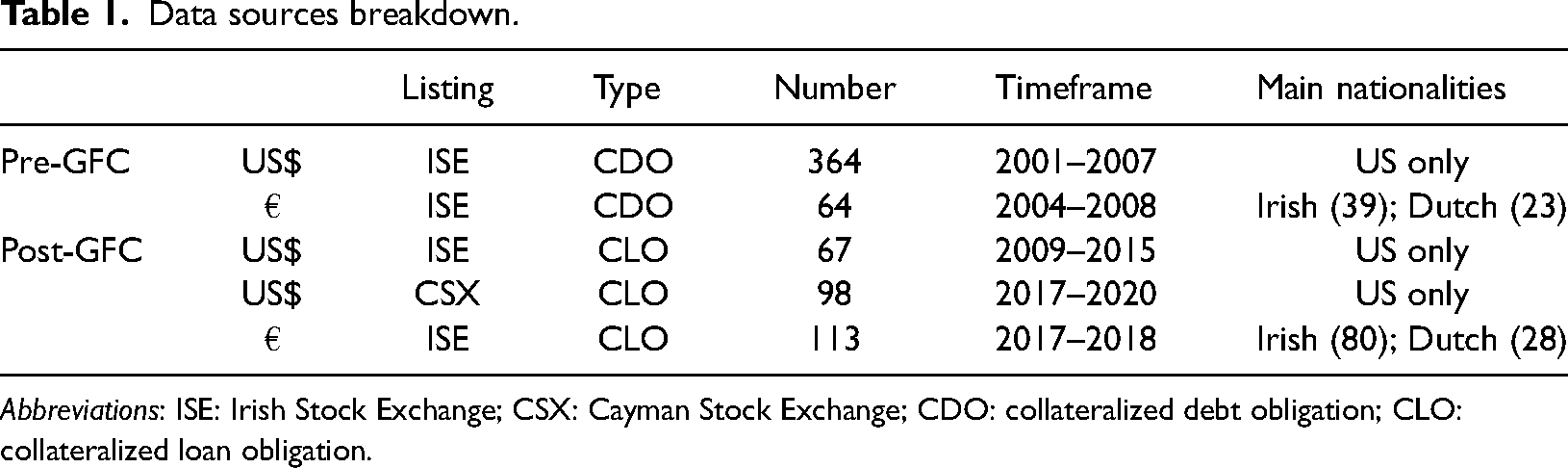

We collected data on 428 CDOs and 278 CLOs from OCs made available via the Irish Stock Exchange (ISE), with a breakdown of numbers by denomination and year in Table 1. In addition, we located a further source of OCs listed on the Cayman Stock Exchange (CSX), which became more important in US$-CLO networks after 2016, which we discuss below. Unlike ISE-listed products, OCs are not available online from the CSX website and can only be viewed in person for a period of 14 days at the CSX offices (Walkers, 2020). We therefore harvested data on firms participating in the structuration for 98 CSX $US-CLOS from the CSX website and supplemented that data with information provided by Moody's, Standard & Poors, and the Securities and Exchange Commission.

Data sources breakdown.

Abbreviations: ISE: Irish Stock Exchange; CSX: Cayman Stock Exchange; CDO: collateralized debt obligation; CLO: collateralized loan obligation.

Once built, we conducted a social network analysis of the data in our database. Data was organized as two-mode networks where each CDO/CLO is connected to a set of actors that fill particular roles within these GFNs. Each role was filled by one actor only; some administrator functions were combined because they were performed by the same actor, generally large banks. The base dataset was coded as binary data, that is—each actor could only be connected to a CDO/CLO once.

Our prime objective was to explore the underlying structural features of the resulting networks of relations between parties involved in the issuance of CDOs at a global level. For this purpose, the two-mode “affiliation” networks were then transformed into a one-mode “co-membership” matrix. This matrix contained value data which told us how many times an actor jointly engaged with other actors in the structuration process.

To render these networks visible, we analyzed the co-membership data through blockmodeling to reveal key structural features (see Borgatti et al., 2013; Glueckler and Doreian, 2016). A traditional blockmodel approach would group actors with similar positions in blocks using partitions, such as structural equivalence of actors (see Borgatti et al., 2013); however, as we are interested in the connections or flow between locations we partitioned the network by the location attribute collected for each actor. This forced actors with the same geographic attribute—for example, New York City—into the same block and relations between blocks presented the geographic flow of information between the various on- and off-shore financial centers for each of the product networks.

To improve the visualization and to account for differences in membership numbers for each block, we normalized the block models by dividing all relations by their square root using the SQRT-normalization approach in UCINet (Borgatti et al., 2013). The resulting relations were then overlaid on a map to illustrate the networked nature of the product across on- and off-shore financial centers. On the map, the thickness of the tie signifies the number of connections or “ties” between two sites. In addition, a breakdown of firms by type/role is provided in an accompanying table to capture the distribution of different functions for each location to illuminate the general versus specialist nature of financial centers within this networked product. The degree of firm concentration within individual structuration activities can be observed by relating the tie-strength results in the map to the firm frequency data in the table.

Finally, we compared the structural similarity of the blocked networks using a quadratic assignment procedure (QAP) to test the association between these simplified networks. To do this, we matched the co-membership network matrices to contain the same rows and columns and conducted the QAP correlation procedure in UCINet (Borgatti et al., 2013). The results of this routine provided us with both effect and p-values.

Findings

CDOs as networked products

Our data reveals a remarkable consistency in the roles required to bring both CDOs and CLOs to market. To understand why that is, we need to explain their comparable “techno-scientific” (Birch and Muniesa, 2020) features, and hence why our “networked product” concept helps understand other commonalities in their relational and spatial networks.

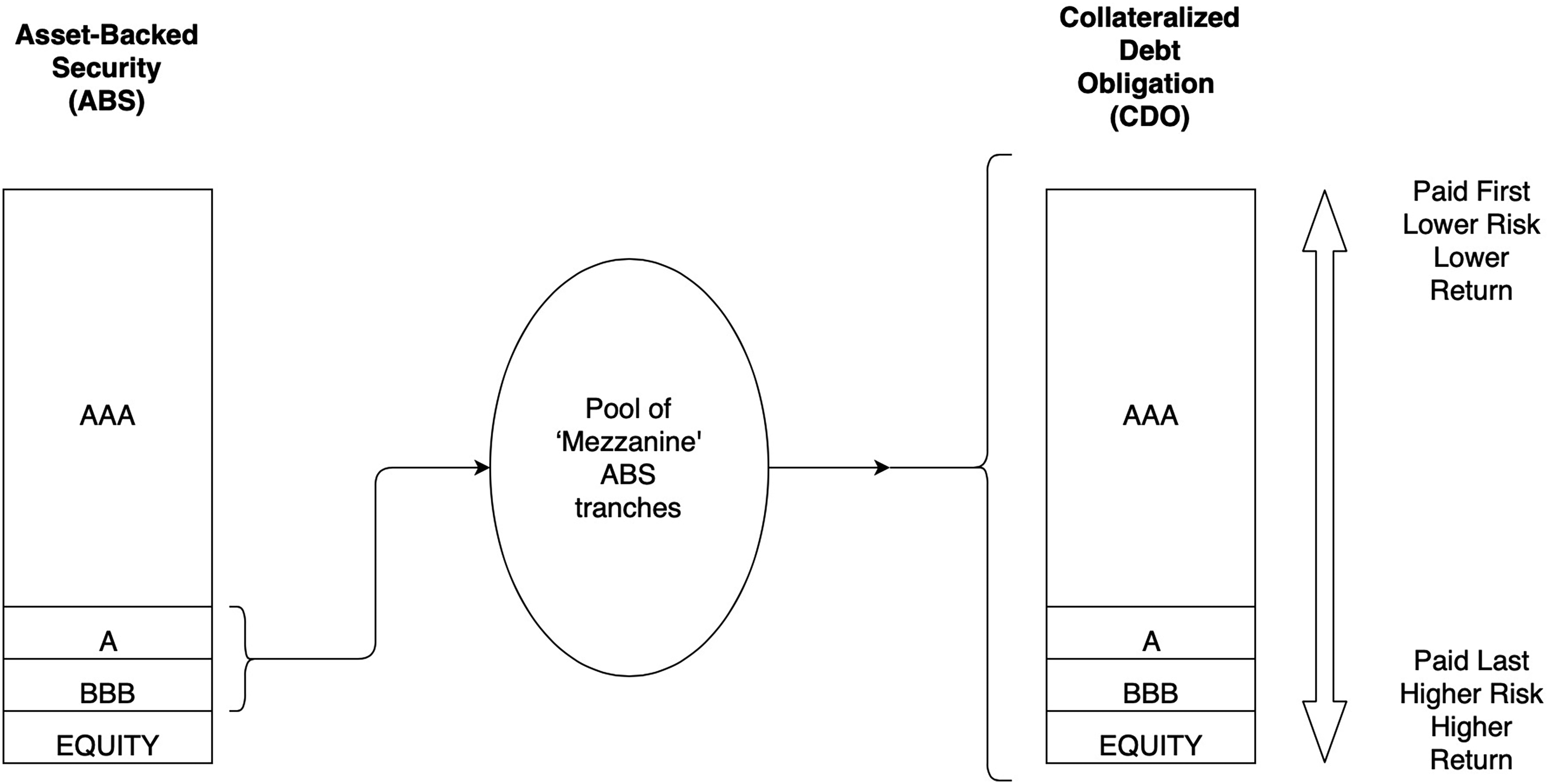

CDOs emerged out of the structured finance revolution of the late 1980s and early 1990s (Engelen et al., 2010; Erturk et al., 2013) and the growth of algorithmic credit scoring technologies (Poon, 2009) which made residential mortgage loans amenable to probabilistic default risk assessment and securitization (Langley, 2008). CDOs allowed banks to transform underlying portfolios of risky mortgage-backed securities into safe “AAA-rated” securities. They did this by first diversifying the underlying portfolio of securities to minimize default correlation and second, using a “Gaussian copula” model to structure and price tranches of securities into hierarchically organized, differently prioritized legal claims on the income streams of the underlying asset pool (Engelen et al., 2011). A stylized figure of this process is outlined in Figure 2.

A basic collateralized debt obligation (CDO) structure.

CLOs also date back to at least the early 1990s, yet are backed by risky corporate loans, often leveraged loans, rather than mortgages (see Carlson and Fabozzi, 1992). CLOs experienced major growth in the post-2008 period, with some estimates putting the current CLO market value above the peak CDO market of 2007 (Aramonte and Avalos, 2019). CLOs share many of the same structural similarities of CDOs: loan repayments from borrowers collateralize tranched securities, and the Gaussian copula model is still the dominant calculative device used to structure, rate, and price CLO tranches (ESMA, 2020). And like CDOs, the financial goal of a CLO is to achieve arbitrage gains from the spread between the higher return risky collateral and the lower return lower risk securities they issue.

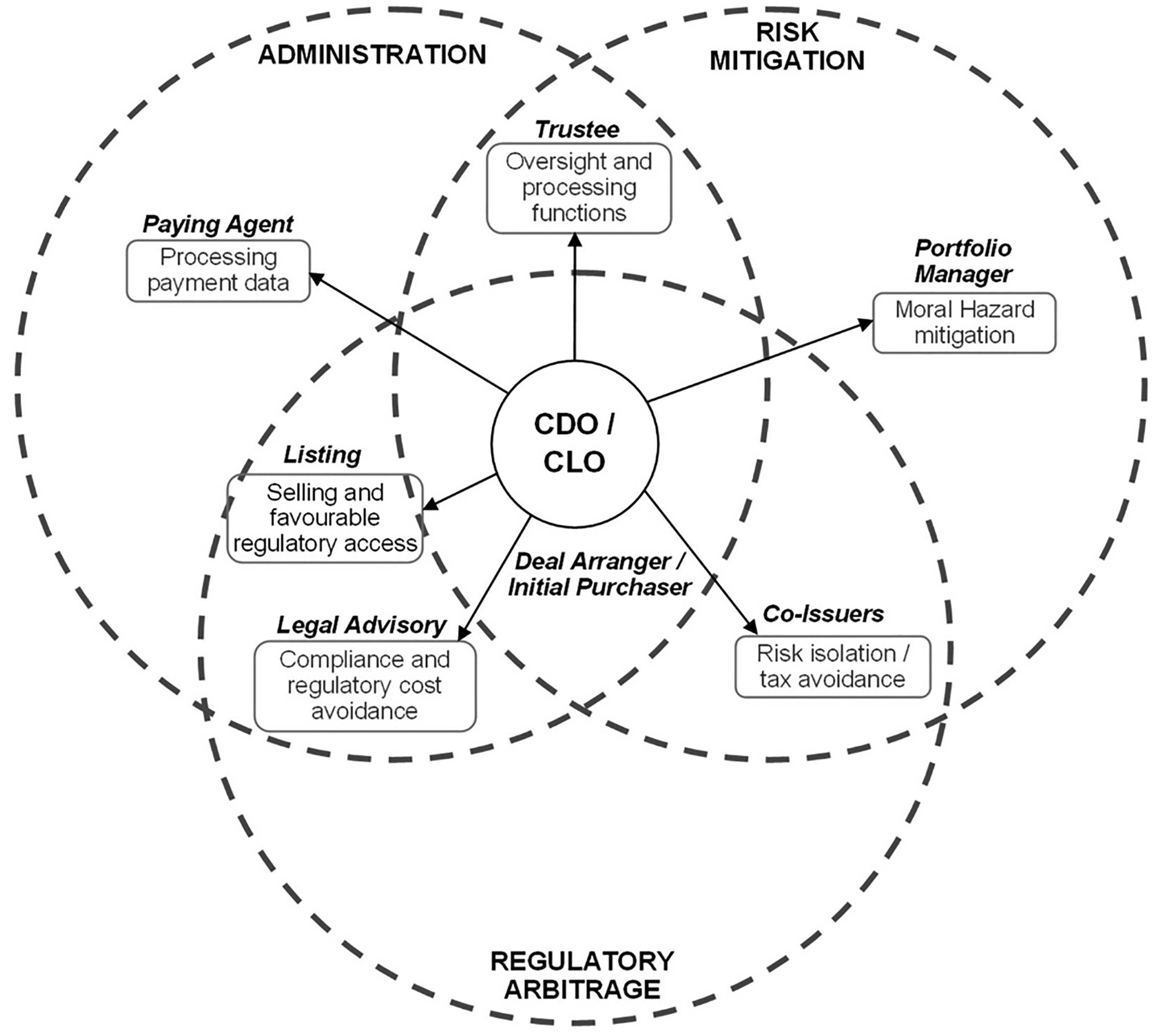

CDOs and CLOs are similar “networked products” insofar as their technical, economic, and legal features create demands for similar skillsets and regulatory benefits within their GFNs. First, the techno-scientific features of the product reinforce the central position of investment banks as deal arrangers—the locus of CDO/CLO development. Their derivatives teams comprise employees with refined quantitative skills (MacKenzie, 2011). CDOs and CLOs are, however, also legal technologies operating in the paper geographies of finance (Haberly et al., 2019) which define commitments and obligations between buyers and sellers through forms of contracting (de Goede, 2015). This generates a need for advanced business service suppliers—notably legal advisory services. Additionally, in order to convert default risk into a commodity, it must be isolated from other risks in order to be quantified and priced (see Knorr Cetina and Preda, 2006). Extraneous risks—such as the credit risk of the arranging bank—were isolated through the creation of off-balance-sheet special purpose vehicles (SPVs) which acted as bankruptcy remote issuers and co-issuers of the structured securities (Gorton and Metrick, 2010). To mitigate the risk of adverse selection and moral hazard—that is, that banks would cherry-pick good assets and offload bad assets to CDO investors—collateral managers working on behalf of investors would be used to select assets from the market (Duffie and Garleanu, 2001), an activity overseen by another organizational actor—trustees (Tavakoli, 2008). These risk-isolating and risk-mitigating organizational features also generated a need for supportive administrative services, including those provided by trustees, but also listing agents and other back-office administration (Cook et al., 2007). Product needs thus fundamentally shaped the key roles involved in a CDO or CLO structuration network—they are networked products—and a summary of those roles and functions can be seen in Figure 3.

An outline of the roles within a CDO and CLO structuration network.

Although product needs shape the roles involved in a GFN, role location was shaped by the economics of those securities. CDOs generated very low margins for their arrangers—as little as half a cent in the dollar (FCIC, 2011) 2 . Scale was therefore important because small margins on a large volume of assets generate meaningful amounts of profit for the banks who arrange the deals (Thiemann, 2012). However with such slim margins, reducing or even eliminating regulatory costs became paramount (Hardie and MacKenzie, 2012), and because financial regulation was and is nationally-based primarily, there are opportunities to lower costs through regulatory arbitrage and forum shopping (Pistor, 2013). Yet accessing the optimal mix of low costs and regulatory benefits must be done without creating what is known as a “taxable event” (Tavakoli, 2008). And there must be complementarities between the legal systems of those different jurisdictions accessed to reduce regulatory frictions and other costs (Dorry, 2015). These factors combine to construct GFNs with strong network regularities.

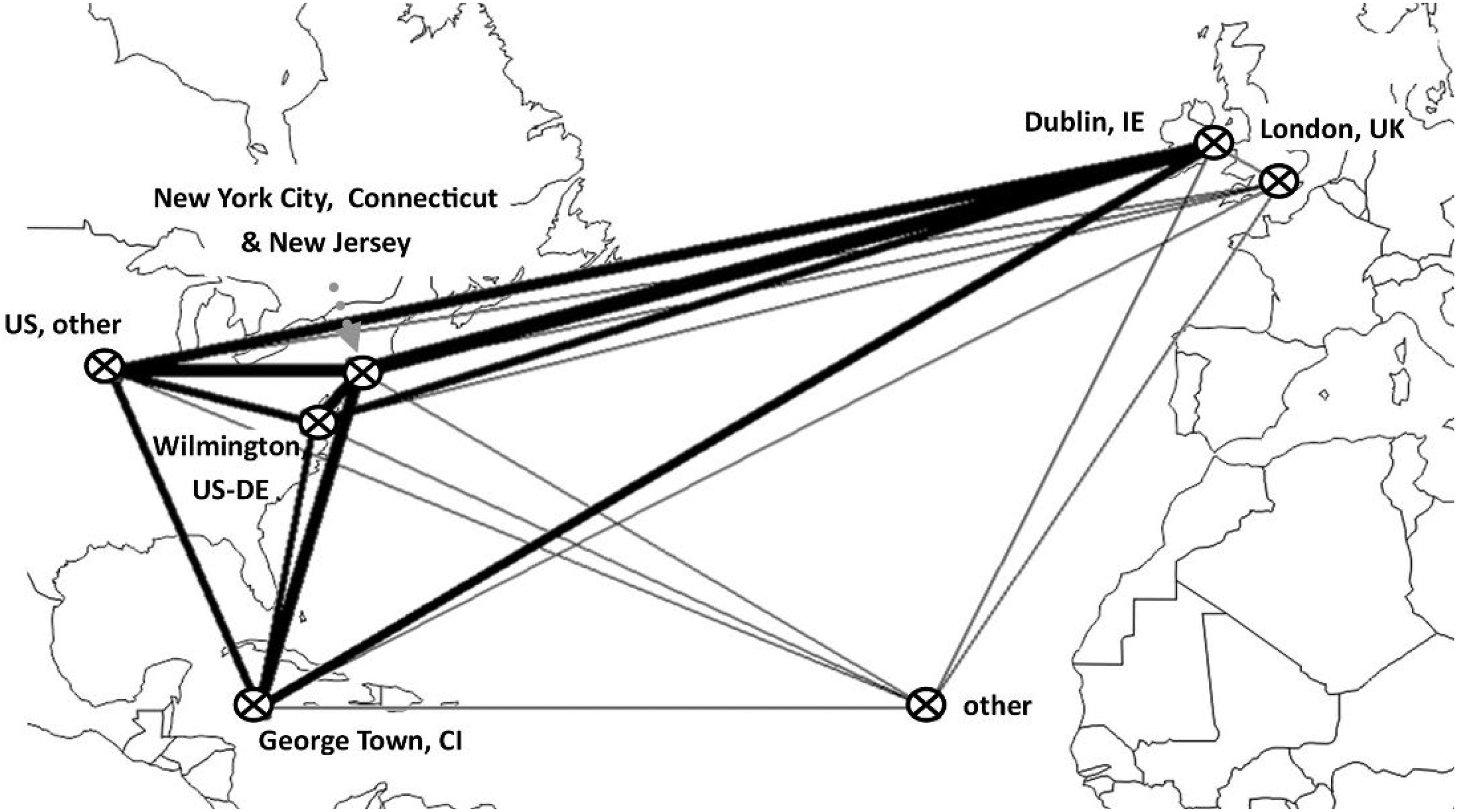

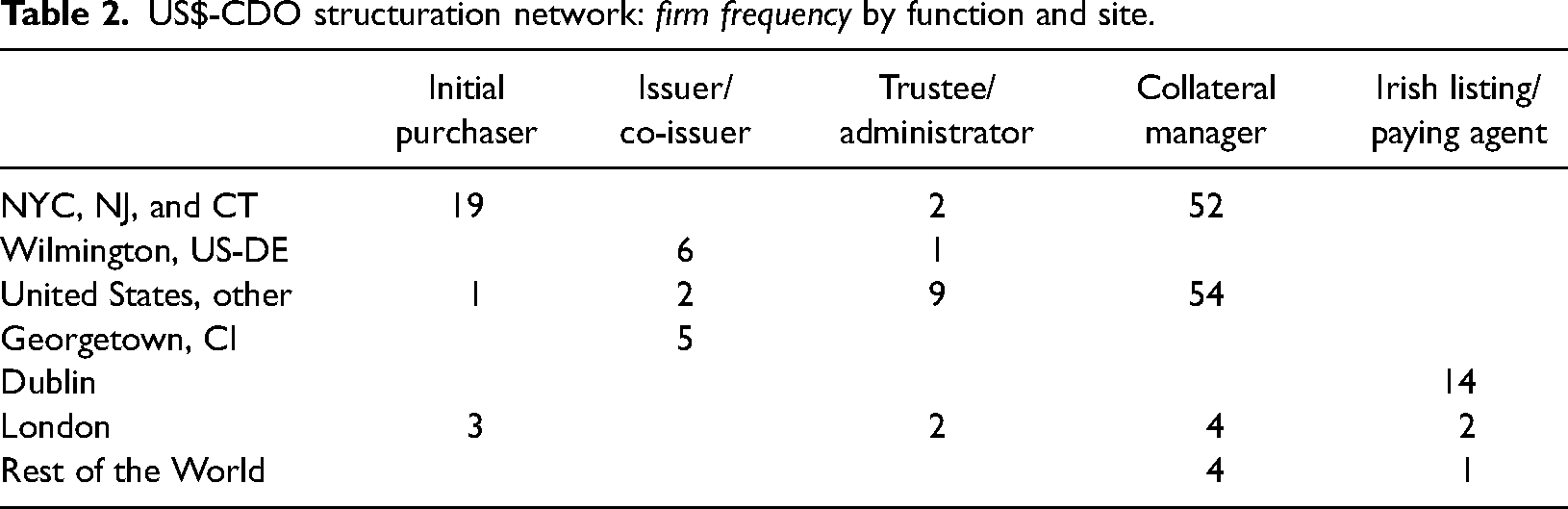

Our network analysis for US$-CDOs is described in Figure 4 and Table 2 and shows the importance of these techno-scientific and cost-based drivers of network structures. New York features, unsurprisingly, as the key financial center for deal arrangement and trading: most arrangers (normally investment banks) are based in NYC, whilst many collateral managers are based in the tristate area of NYC, NJ, and CT (71), although some are otherwise dispersed across the US (54). The administrative and oversight roles of trusteeship are also predominantly performed by large banks based in the US, but operate primarily out of non-NYC cities (e.g. LaSalle—Chicago, IL; Wells Fargo—Columbia, MD; Deutsche Bank—Santa Ana, CA; JPMorgan and Bank of New York—Houston, TX), confirming other studies which observe a spatial hierarchy between trading-based or deal-making activities in core global financial centers and administrative functions in secondary financial centers within the US (see discussion by Coe et al., 2014).

US$-CDO structuration network: relationship strength between sites. Note on maps: For each location, relations between nodes were aggregated using a block modelling approach. Here line thickness corresponds to all inter-firm relations and node location for each jurisdiction has been manipulated to match the map geography.

US$-CDO structuration network: firm frequency by function and site.

There are also a very strong relations between the core financial center of New York and the specialist off-shore centers of Delaware, the Cayman Islands and Ireland: all four jurisdictions feature in every one of the 314 US$-CDOs for which we have complete data. These repeat relations are consistent with both Haberly and Wójcik’s (2017: 250) and Christophers’ (2009) findings that the production of securities of this nature is highly standardized, with strong, enduring network relationships between key actors and jurisdictions. Skill specialization explains some of this relational consistency, but much is determined by the regulatory needs of the CDO product. As Wainwright (2017) notes, financial networks are often structured by arbitrage logics which can require the linking together of multiple entities located in different jurisdictions to maximize regulatory benefits and minimize costs. Hence, in our CDO network, there is a dual issuer/co-issuer SPV system to maximize regulatory benefits. A first SPV would ordinarily be a wholly owned subsidiary of the initial purchaser (investment bank), located in Delaware to which the assets would be transferred 3 from New York. The New York-to-Delaware exchange constituted a “true sale” in accounting rules and so served to isolate the default risk of the securities from the credit risk of the bank (Tavakoli, 2008). However, the Delawarean SPV's status as a wholly owned subsidiary meant the transaction was classified as a form of intra-company debt financing for the purposes of US Federal taxation law, and so did not qualify as a taxable event (Tavakoli, 2008: 8). The exploitation of this “categorical arbitrage”—that is, profiting from legal discrepancies in the treatment of two forms of conduct that are functionally the same (Riles, 2014)—served to reinforce long-standing relations between New York and Delaware evident in other studies (Palan et al., 2009).

From Delaware, the assets were sold or transferred synthetically to a second SPV independent of the initial purchaser, located usually in the Cayman Islands to achieve jurisdictional arbitrage. The independent and non-resident status of the Cayman Islands SPV meant it avoided Section 882(a)(1) of the US Internal Revenue Code, which taxes the net income of foreign corporations if they are connected to a US trade or business (Carden and Nasser, 2007: 121). The absence of tax treaties between the Caymans and the US also meant there was no mechanism for reclaiming tax withheld (Tavakoli, 2008: 17). These specific regulatory features allowed CDOs to incorporate as tax “exempted companies” (Gorton and Souleles, 2007) and allowed collateral managers who were US based to select and trade in the underlying asset pool (of mainly US$-denominated assets), as independent agents of the foreign issuer rather than as a principal; thus exploiting the safe harbor rules of US tax law (Carden and Nasser, 2007: 121–122). Finally, Ireland became the jurisdiction of choice as a listing agent because it triggered the Quoted Eurobond Exemption rules which reduced tax payable on interest (Arthur Cox, 2013: 3).

The spatial relations constructed by CDOs were therefore in large part a legal contrivance—part of the paper geography of finance where the virtual “flow” of the product through the four sites of New York, Delaware, Cayman Islands, and Ireland sequentially were directed by the product's need for regulatory cost savings (Morgan, 2008). In networked product terms, the spatial and relational organizations of the CDO GFN were shaped by the idiosyncratic features of the product, which deepened skills concentration in particular jurisdictions, facilitating increased CDO volumes and throughput in a self-reinforcing way.

Achieving scale in €-denominated CDOs through transduplication

Those spatial and relational regularities provided the architecture for the rapid expansion of US$-denominated CDO in the late 1990s and 2000s. However, as international demand for AAA-rated fixed income investments increased against a backdrop of low interest rates and regulatory incentives for banks to hold low risk assets, demand also grew for €-denominated CDOs (Tett, 2009). The burgeoning market for €-denominated CDOs grew rapidly from 1999 onward 4 (Barclays Capital, 2002). Many European banks had already participated in US$-CDOs either as buyers from the Irish exchange, or as arrangers through their US subsidiaries (McCauley, 2018). But to facilitate this growth in €-CDOs, GFNs had to be built within a European space with quite different regulatory systems and jurisdictional complementarities. Market expansion, therefore, meant reproducing the activity network structure with similar regulatory benefits in an altogether different juridico-political context. Or in Haberly et al.’s (2019) terminology, it meant constructing new technical and paper geographies to facilitate the extension of CDOs into Europe.

This was achieved through a process of what we term transduplication. Transduplication, in its biological usage, explains genetic duplication and adaptation as elements with open reading frames (i.e. the capacity to translate) are transposed and replicated elsewhere, adapting to the environments they encounter (Joly-Lopez and Bureau, 2018). In our application of the concept this implies certain network-based processes: it captures the process whereby an architecture of nodes and nodal relations determined by the techno-scientific, risk-mitigating, economic, and legal needs of the product integrates with and shapes the inter-jurisdictional relations and spatial environments they encounter as the market grows.

Transduplication in the €-CDO structuration network was facilitated by at least three developments, which complement existing research on the dissemination of US securitization knowledge within Europe (Wainwright, 2015). First, was the liminal position of London as a global financial center which sat between US and European networks, acting as a site of knowledge and practice exchange. There was, as Wójcik (2013a) notes, a NY-LON axis upon which this market was built, with London acting as a coordinating hub for much of the early European CDO GFN formation 5 . Second, US banks with knowledge of the securitization process acted as arrangers for continental European dealmakers 6 , facilitated by the formation of associations, such as the European High Yield Association, which brought together the most prolific US-based securitizers such as Merrill Lynch, Credit Suisse First Boston, and Goldman Sachs with aspirant European structurers, asset managers, and investors (High Yield Report, 2001). Third, it required the conducive legal environment and jurisdictional complementarities equivalent to that in US$CDOs to minimize tax and regulatory costs. The role of specific national rules, such as those around the tax-neutral treatment of SPVs in Ireland and Amsterdam (Arthur Cox, 2013: 1–3) played a significant role in encouraging the translation of US-like structuration networks into a European context (see also Thiemann, 2012).

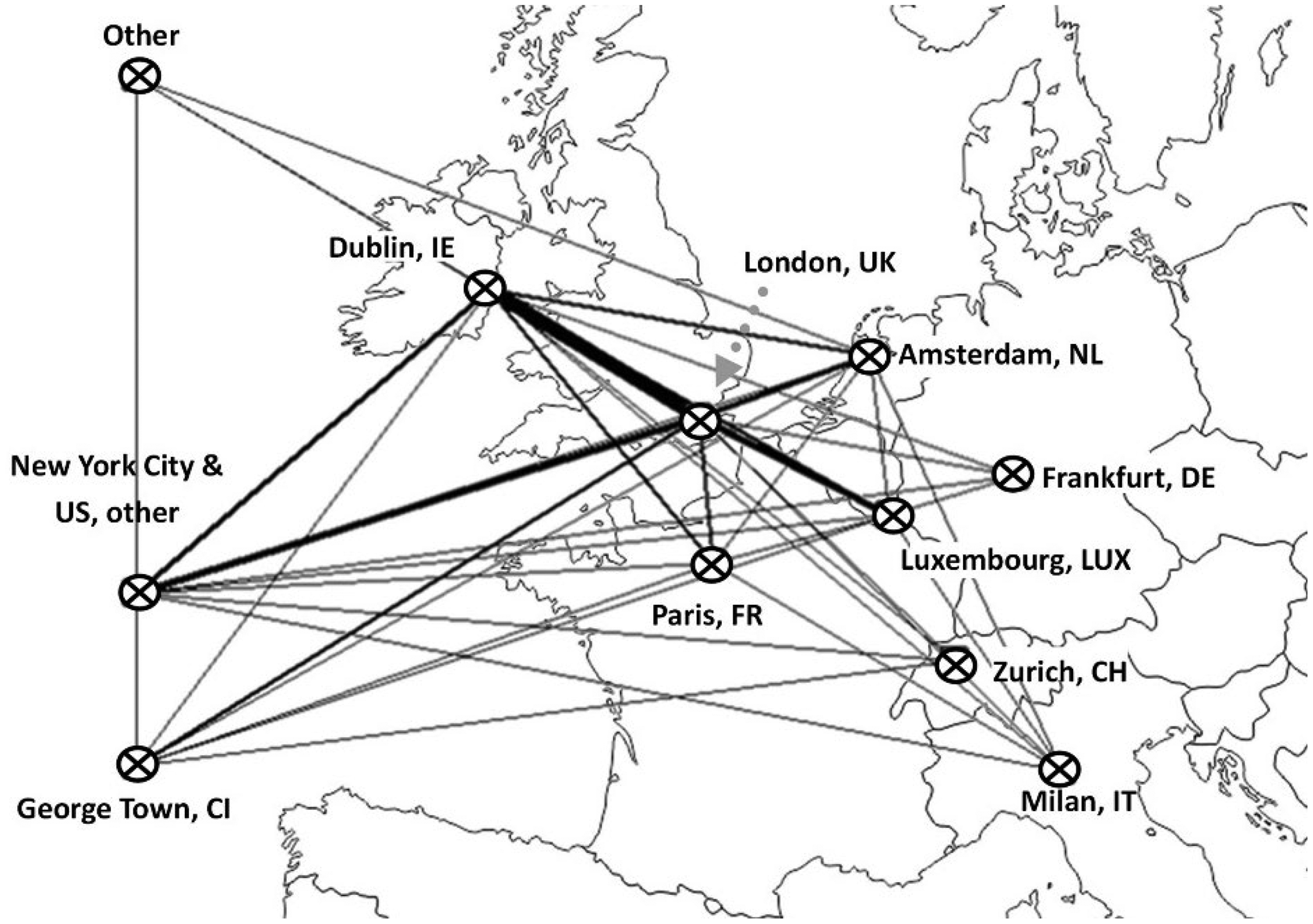

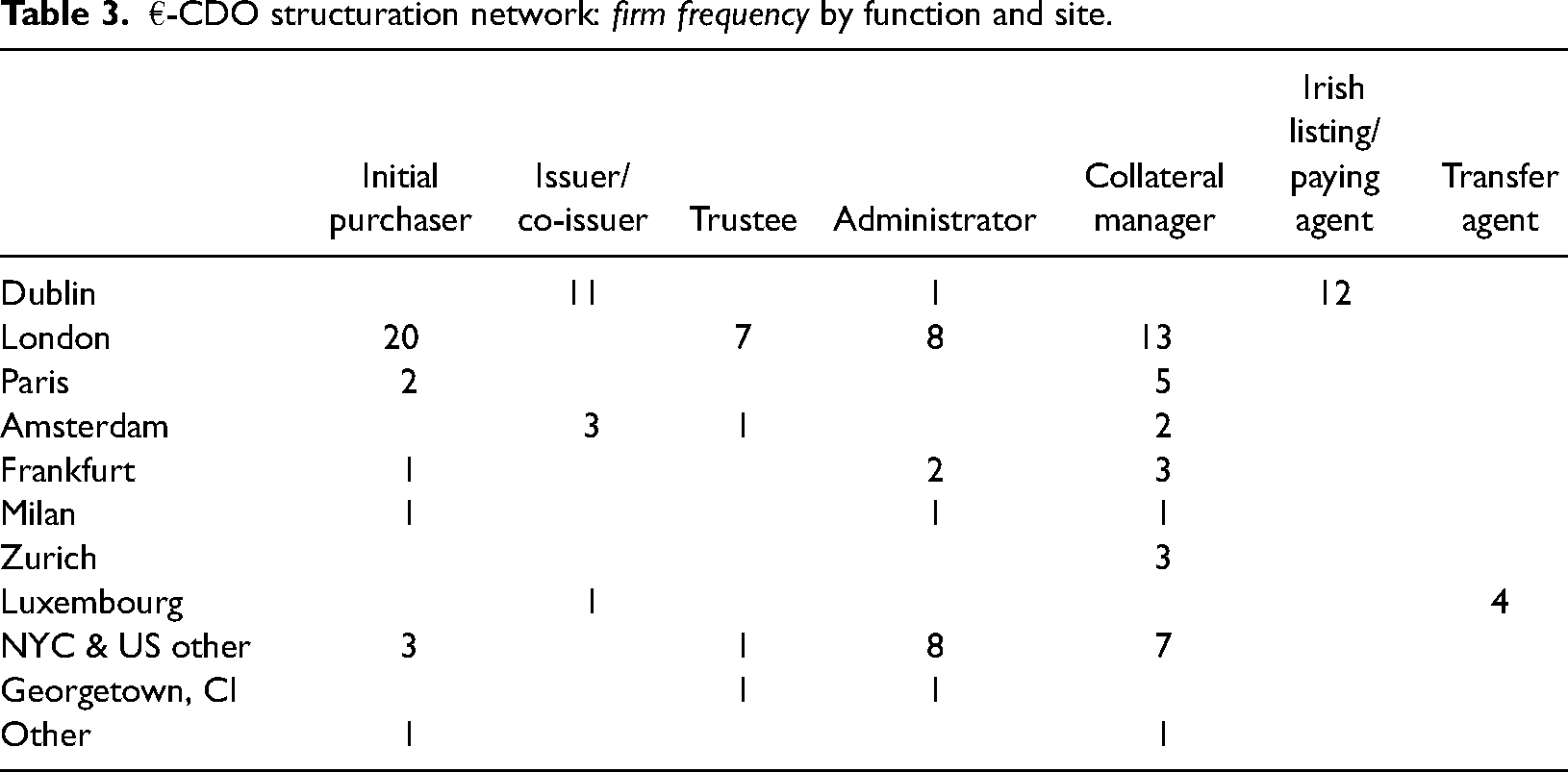

As our network shows (Figure 5), the most important sites in the €-CDO market were London and Dublin. London played the equivalent role of NYC as a key organizing node in the network as home to the initial purchasers (banks) and collateral managers (Table 3). Trustees and administrators were also clustered in London—unlike the US, they were not distributed across non-metropolitan cities, emphasizing London's pre-eminent role in the UK political economy as a core financial services hub and as a key location for European and US banks’ global activities. Dublin acted as Irish Listing and Paying Agent, as it did in US$-CDOs, suggesting skills specialization or regulatory advantage. In addition, Ireland acted as issuer for many of the €-CDOs in the network (39) combining the issuer/co-issuer roles played by the Cayman Islands and Delaware in US$-CDOs into a single European issuer function. Again, regulatory complementarities mattered: London-based deal arrangers used mainly Irish issuers because of its English law-based system (Tavakoli, 2008: 47), again reinforcing Dorry’s (2015) observations about the importance of legal and regulatory harmony in shaping spatial relations. However, there were also issuers—approximately one-third—based in Amsterdam, which was also attractive because of its tax benefits (Engelen, 2007), and the absence of restrictions on the type and origin of assets purchased by SPVs (Butt et al., 2005; Graaf and Steffens, 2005). US firms retained a position in the €-denominated CDO network, with collateral managers, and some administrative functions (registrar and paying agent) appearing as part of larger intra-bank subsidiary arrangements.

€-CDO structuration network: relationship strength between sites.

€-CDO structuration network: firm frequency by function and site.

Overall, there was greater room for organizational choice within the European CDO structuration network, and thus a less regular structure than in US$-denominated CDOs. While London and Dublin were dominant, other major financial centers—Frankfurt, Milan, Zurich, and Paris—also featured as peripheral actors performing multiple functions. There is some evidence of embeddedness and home bias—French initial purchasers worked with mainly French collateral managers for example; but this was not a general trend. Other spatial relations appear to have been organized on the basis of organizational preference: Citigroup, for example, tended to favor sourcing administrative functions from Frankfurt. There is no single European equivalent of a Delaware or Cayman in administrative and advisory functions, which were shared by a number of jurisdictions. The result is a more diffuse spatial distribution of activities, even though activity roles remain virtually identical across US and European CDOs.

The structural similarity of CLO and CDO GFNs

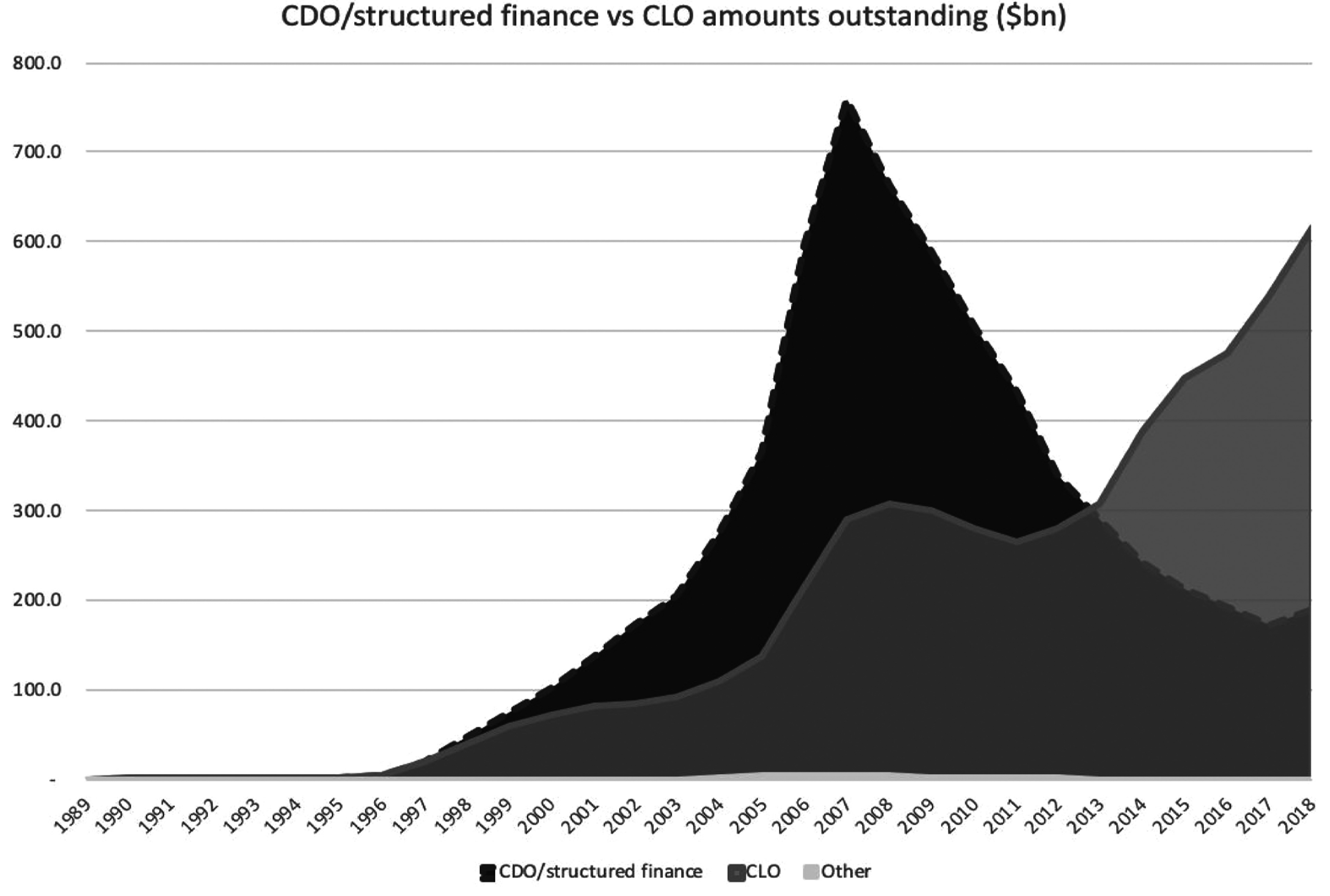

The market for both US$-CDOs and €-CDOs collapsed completely in 2008, pushing the international finance sector into the deepest crisis since the Great Depression. Yet from around 2011 onwards, the market for CLOs grew at a similar rate and in similar volume to that of the early/mid-2000s CDO market. By Q1 of 2019 CLO amounts outstanding were roughly the equivalent of the CDO market in 2006, 1 year before the peak (Figure 6); with some estimates putting CLO market value above the 2007 CDO peak (Aramonte and Avalos, 2019). The context of this revival was a regulatory easing which followed a concerted lobbying effort on the part of the financial services industry 7 (Aalbers and Engelen, 2015) and the infrastructural power of finance more generally to shape political agendas in policy circles (Braun, 2020). It also reflected the growth of the leveraged loan market and the associated conjunctural yield climate of low interest rates, liquid credit markets, and tight credit spreads which made the comparatively higher returns on CLOs more attractive to would-be investors (Moldovan and Palligkinis, 2018).

Collateralized debt obligation (CDO)/structured finance amounts outstanding versus collateralized loan obligation (CLO) amounts outstanding ($bn). Source: SIFMA 2021.

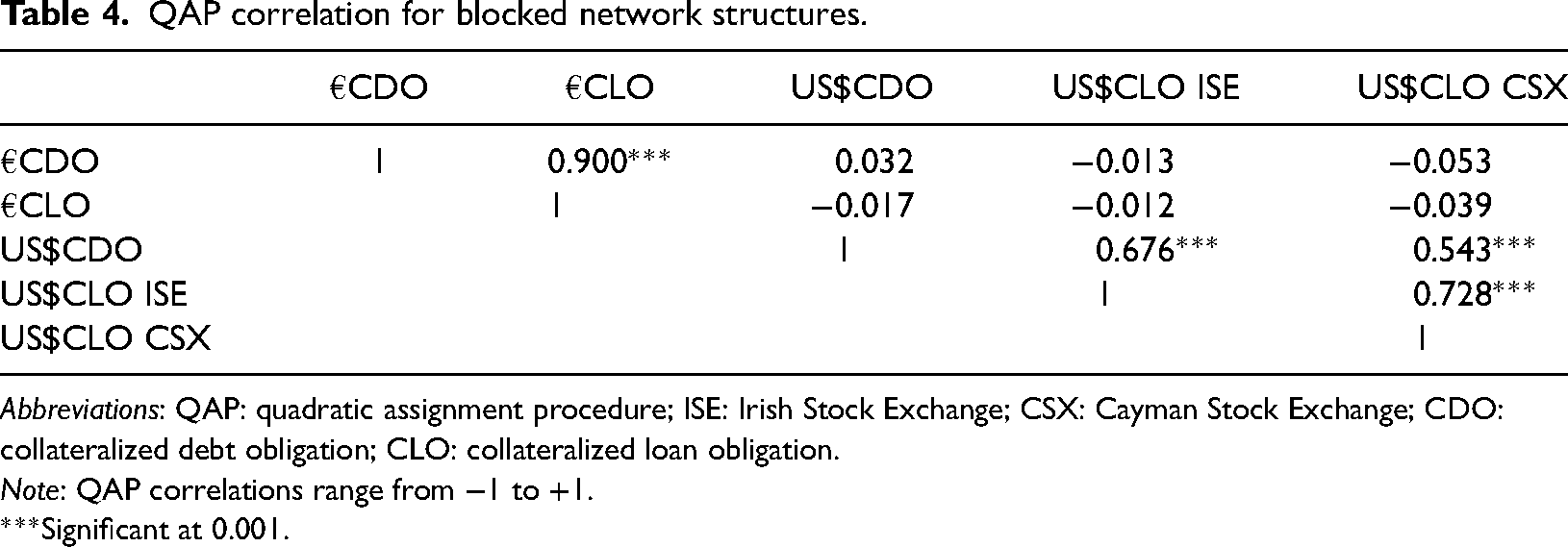

The CLO structuration networks that developed after the 2008 crisis were almost identical to the networks that helped propel the growth of the CDO market in the 2000s. Our QAP network correlation modelling (Table 4), which examines structural similarities across different networks, shows that €-denominated CDO and CLO networks are significantly correlated at 0.900***. QAP correlations range from −1 to +1, and so US$-CDO and ISE-listed CLO structuration networks are also strongly correlated at 0.676***, falling to 0.543*** when we account for US$-CLOs with a CSX listing. The similarity between CDO and CLO structuration networks along denominated currency lines is therefore striking.

QAP correlation for blocked network structures.

Abbreviations: QAP: quadratic assignment procedure; ISE: Irish Stock Exchange; CSX: Cayman Stock Exchange; CDO: collateralized debt obligation; CLO: collateralized loan obligation.

Note: QAP correlations range from −1 to +1.

***Significant at 0.001.

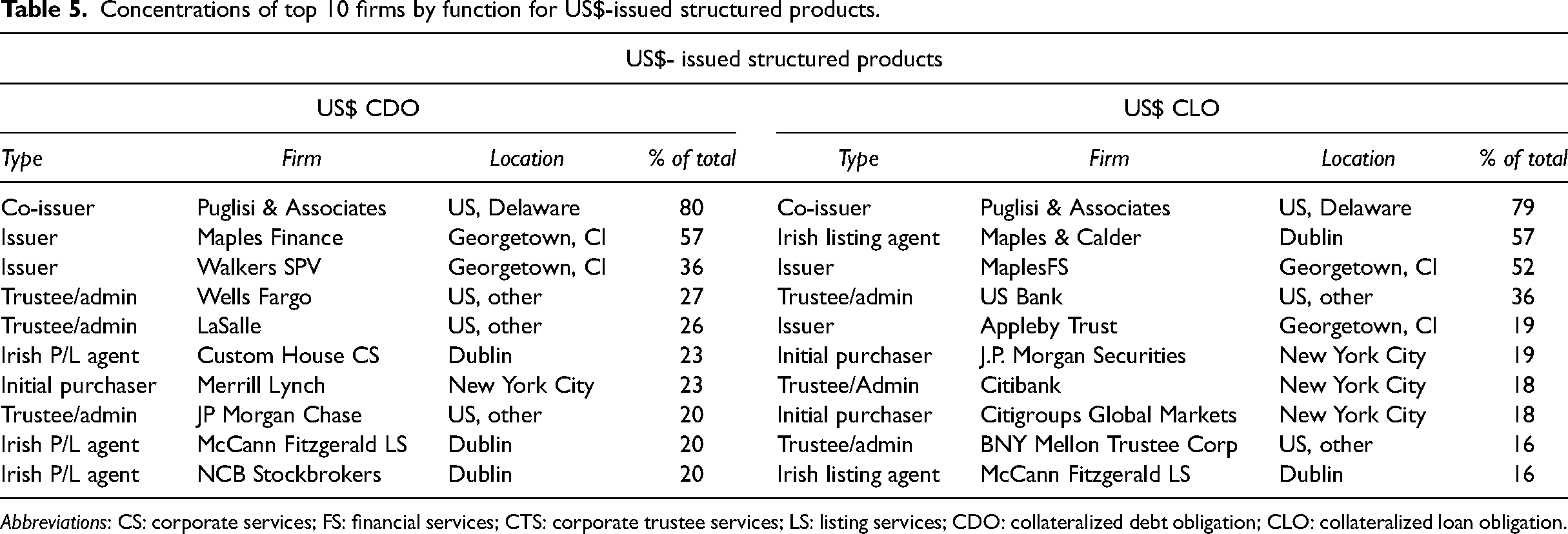

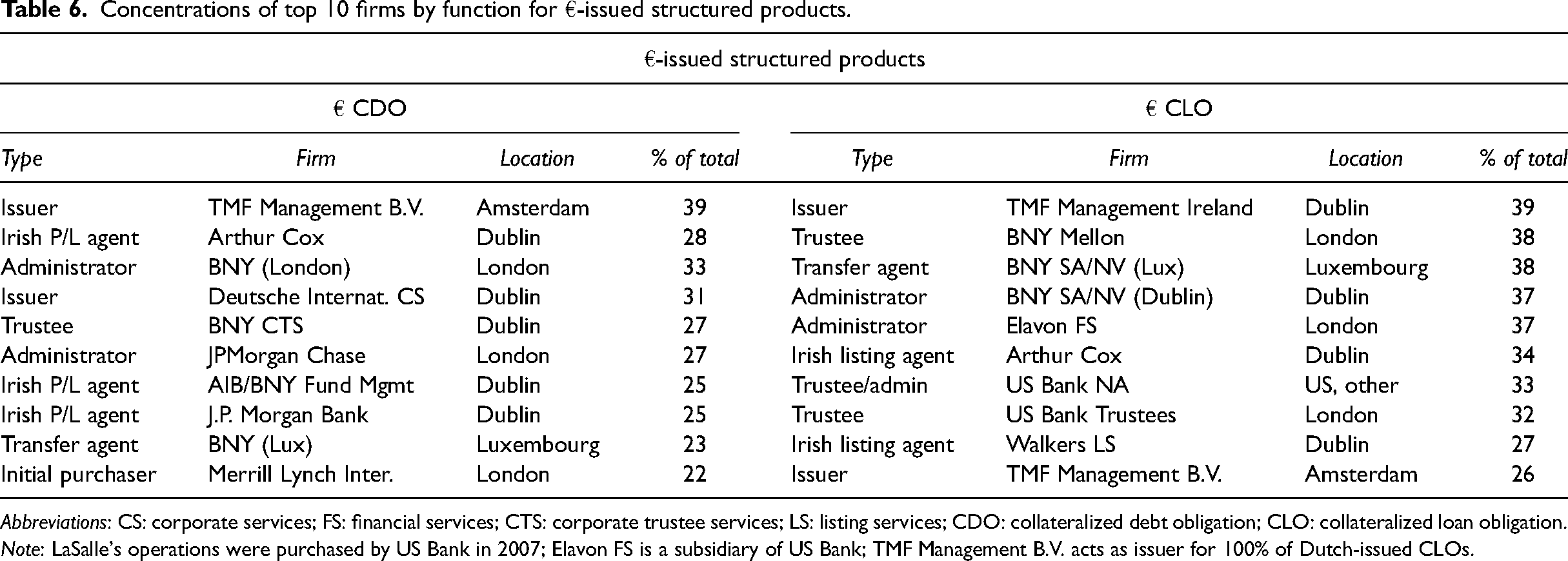

These similarities are brought out further through a comparison of concentration levels, whether by function or spatial position within the activity of structuration in US$- and €-networks; and by the involvement of the same actors in core positions across CDO and CLO structuration. Tables 5 and 6 show that in the US$-networks, the Delawarian co-issuer, Puglisi & Associates was the most involved actor in both CDO and CLO structuration networks—active in 80% of CDOs and 79% of CLOs in our dataset. Following that, Cayman Island based Maples were a key issuer and became a key Irish Listing Agent. We also find various US banks acted as trustees, administrators, and initial purchasers. Even then, many of the changes in firm presence within the network are explained by acquisitions, such as, for example, US Bank purchase of LaSalle's and Deutsche Bank's trustee operations in 2006 and 2012, respectively, cementing its position in that market; similarly J.P. Morgan sold its trustee operations to BNY Mellon in 2006 (Businesswire, 2006a, 2006b). Hence, despite a significant passage of time, and a large financial crisis, many of the core positions of the US$-CDO network were held by the same organizations in the US$-CLO network, with similar concentrations in the market. In the European networks we found similar trends. TMF Management expanded its role as issuer to cover a combined 65% of the activity in Europe through its Dutch and Irish operations 8 . US Bank and BNY dominated the Trustee and Admin functions through multiple subsidiaries (BNY SA/NV and Elavon FS) and Arthur Cox retained its position as lead Irish Listing Agent.

Concentrations of top 10 firms by function for US$-issued structured products.

Abbreviations: CS: corporate services; FS: financial services; CTS: corporate trustee services; LS: listing services; CDO: collateralized debt obligation; CLO: collateralized loan obligation.

Concentrations of top 10 firms by function for €-issued structured products.

Abbreviations: CS: corporate services; FS: financial services; CTS: corporate trustee services; LS: listing services; CDO: collateralized debt obligation; CLO: collateralized loan obligation.

Note: LaSalle's operations were purchased by US Bank in 2007; Elavon FS is a subsidiary of US Bank; TMF Management B.V. acts as issuer for 100% of Dutch-issued CLOs.

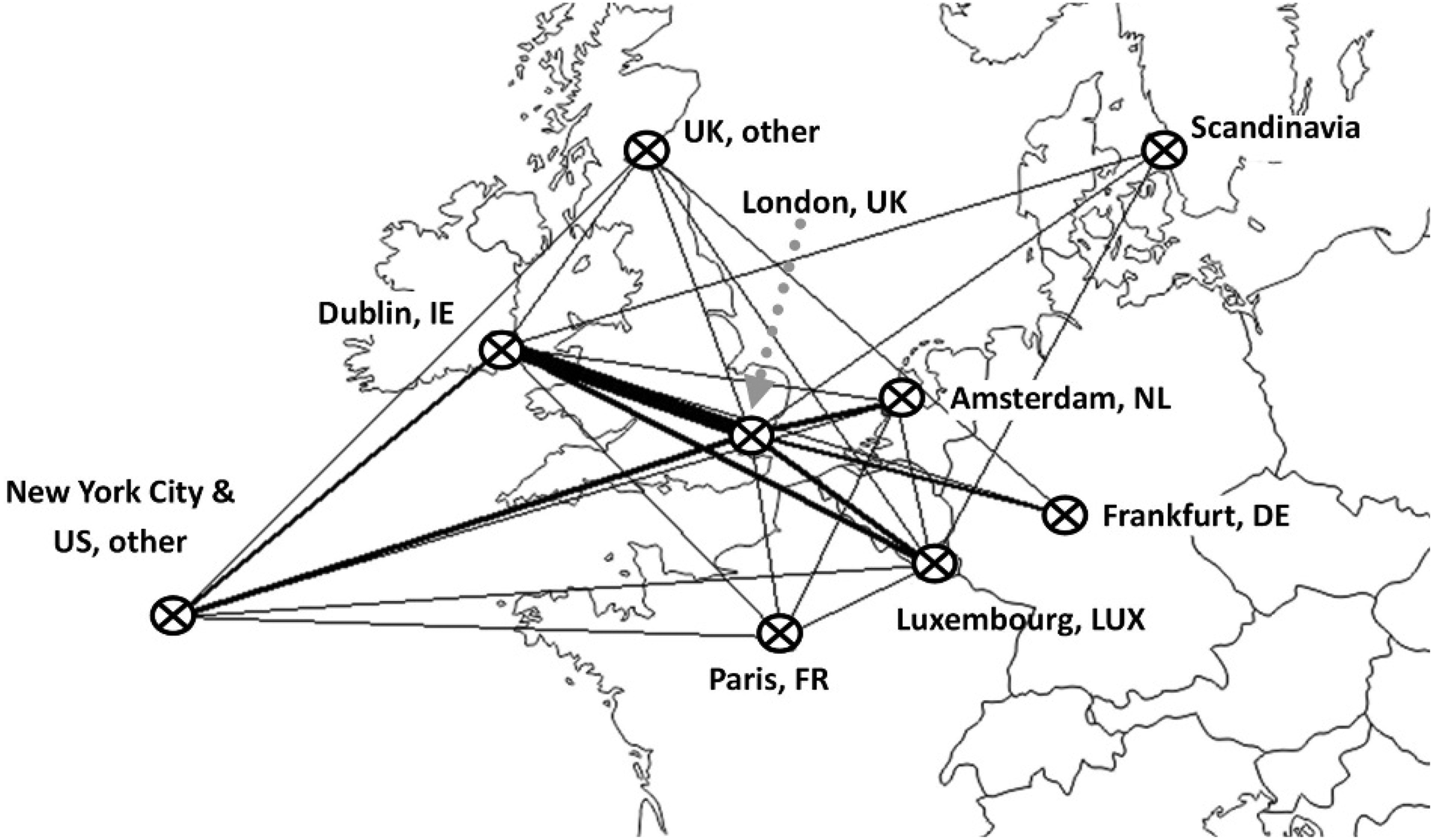

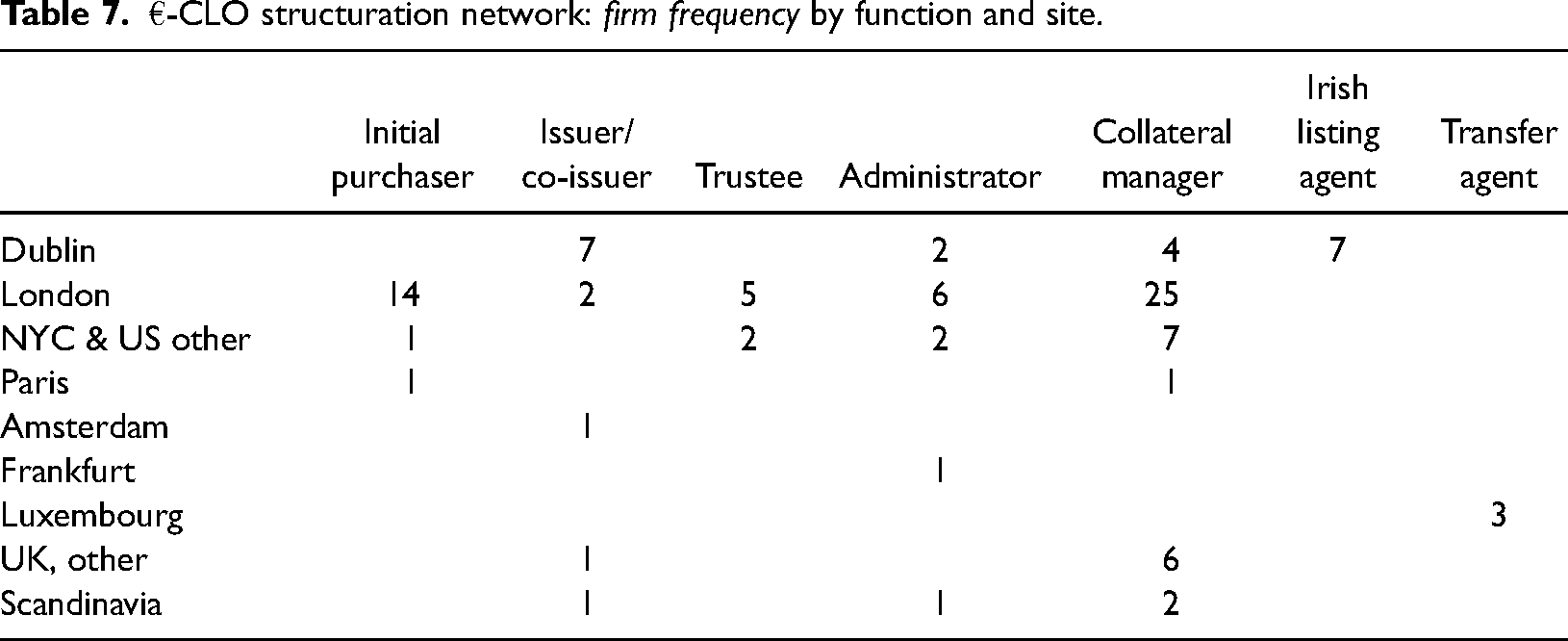

The GFNs for CDOs and CLOs are thus strikingly similar, reflecting networked product logics: the parallel needs of each product produced demands for similar roles and regulatory features, giving rise to symmetric relational and territorial networks. Where network differences are evident, they are small and consonant with Wójcik and Cojoianu’s (2018) concept of “adaptive resilience”—that is, the ability of a system to maintain its integrity by adapting to “external disturbances” (Boschma, 2015). €-CLO networks are slightly more European than equivalent CDOs, with changes mainly in administrative and support services. As the map of €-CLOs issued in 2017/2018 shows (Figure 7), activity remained concentrated across the English Law jurisdictions of London and Dublin, which acted as core financial centers. In the UK, London continued to dominate the collateral management function, despite the emergence of a few collateral managers outside of London (Table 7). Luxembourg and Amsterdam retained their specialist functions as locations for transfer agents 9 and issuers. Other financial centers named in €-CLOs remained peripheral in the sense that they are linked to few products. These included Paris, Frankfurt, and a selection of Scandinavian cities tied to one CLO only.

€-CLO structuration network: relationship strength between sites and the ego-nets for banks and subsidiaries.

€-CLO structuration network: firm frequency by function and site.

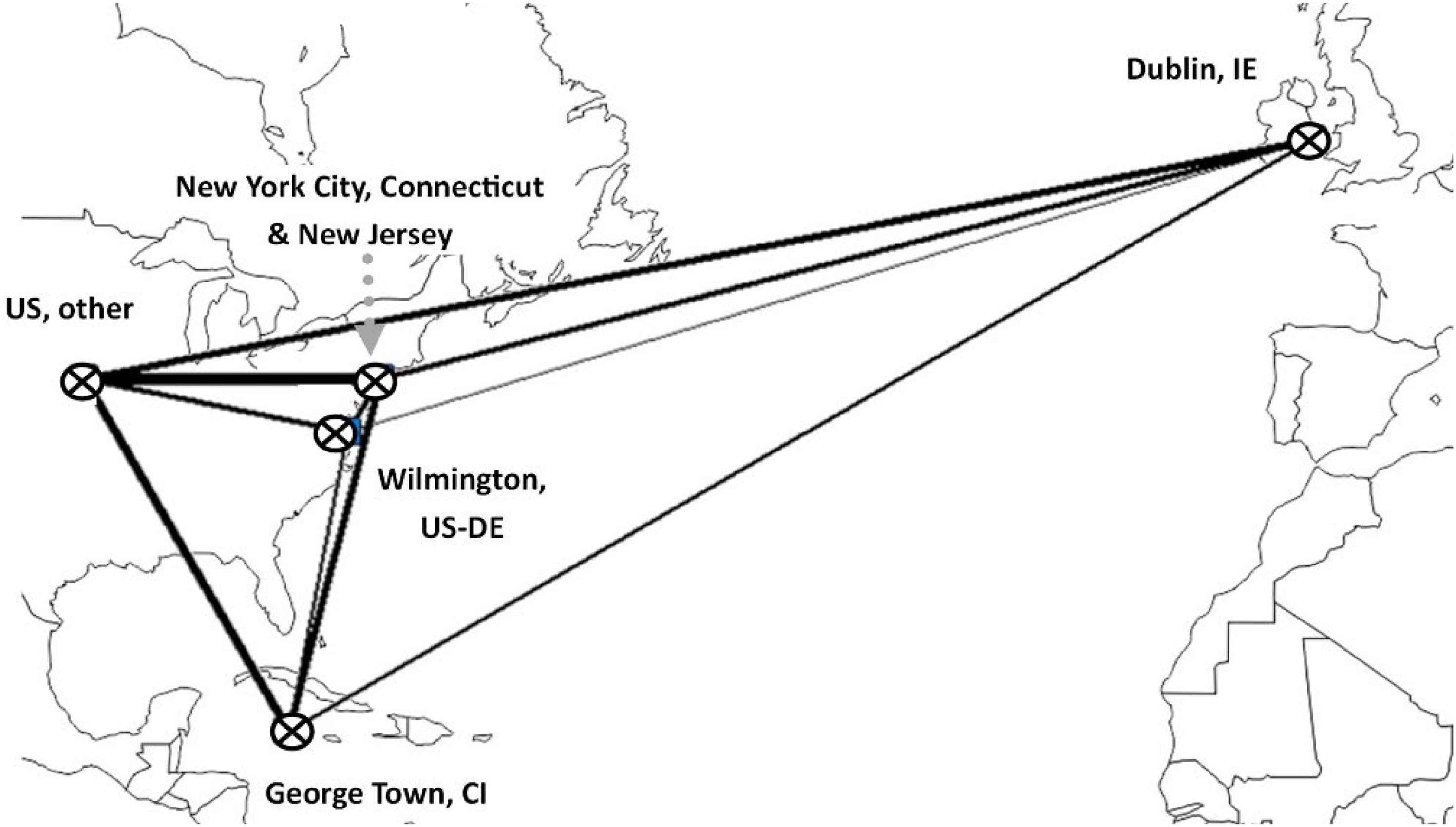

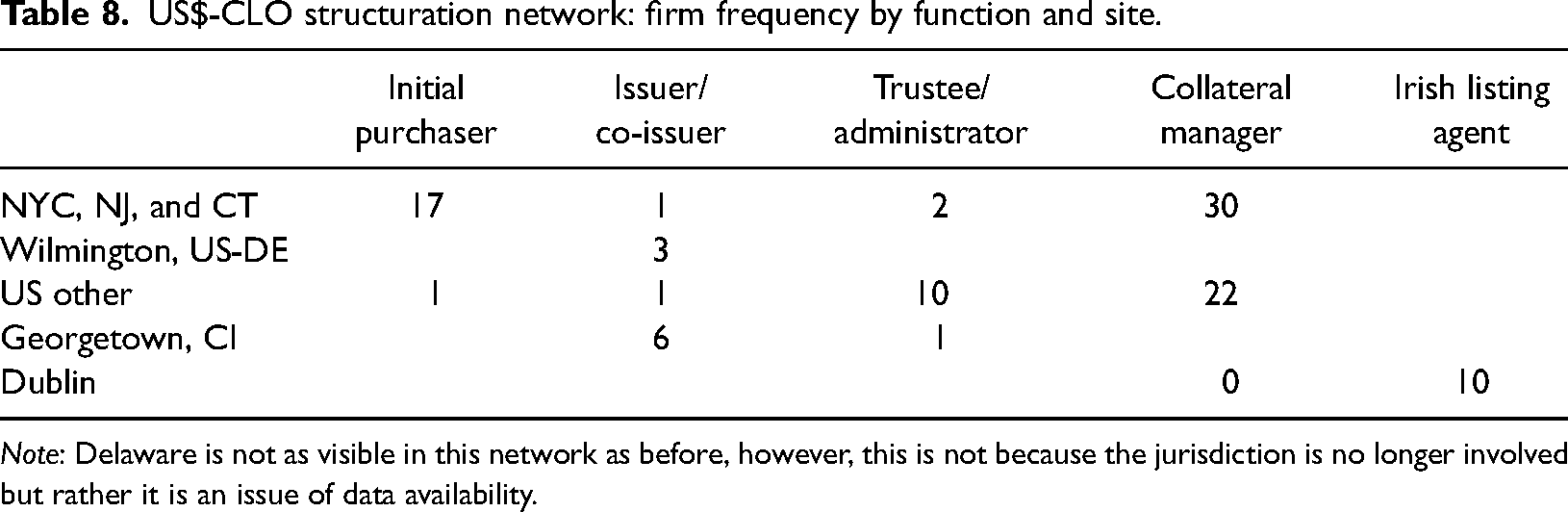

There were also small changes in US$-CLOs advanced business services, which became less European and more North American. This partly resulted from the consolidation of certain activities in response to the updated “Transparency (Directive 2004/109/EC) Regulation 2007” which made it no longer a statutory requirement for the issuer to appoint an Irish Paying Agent alongside the Principal Paying Agent (Figure 8). This did not remove Dublin-based entities from the network altogether because Irish Listing Agents were unaffected by this legislation and so remained key nodes until 2016 (Table 8). London also largely disappeared from the network, further reinforcing the more North American and less European character of US$-CLOs after 2008.

US$-CLO structuration network: relationship strength between sites and the ego-nets for banks and subsidiaries.

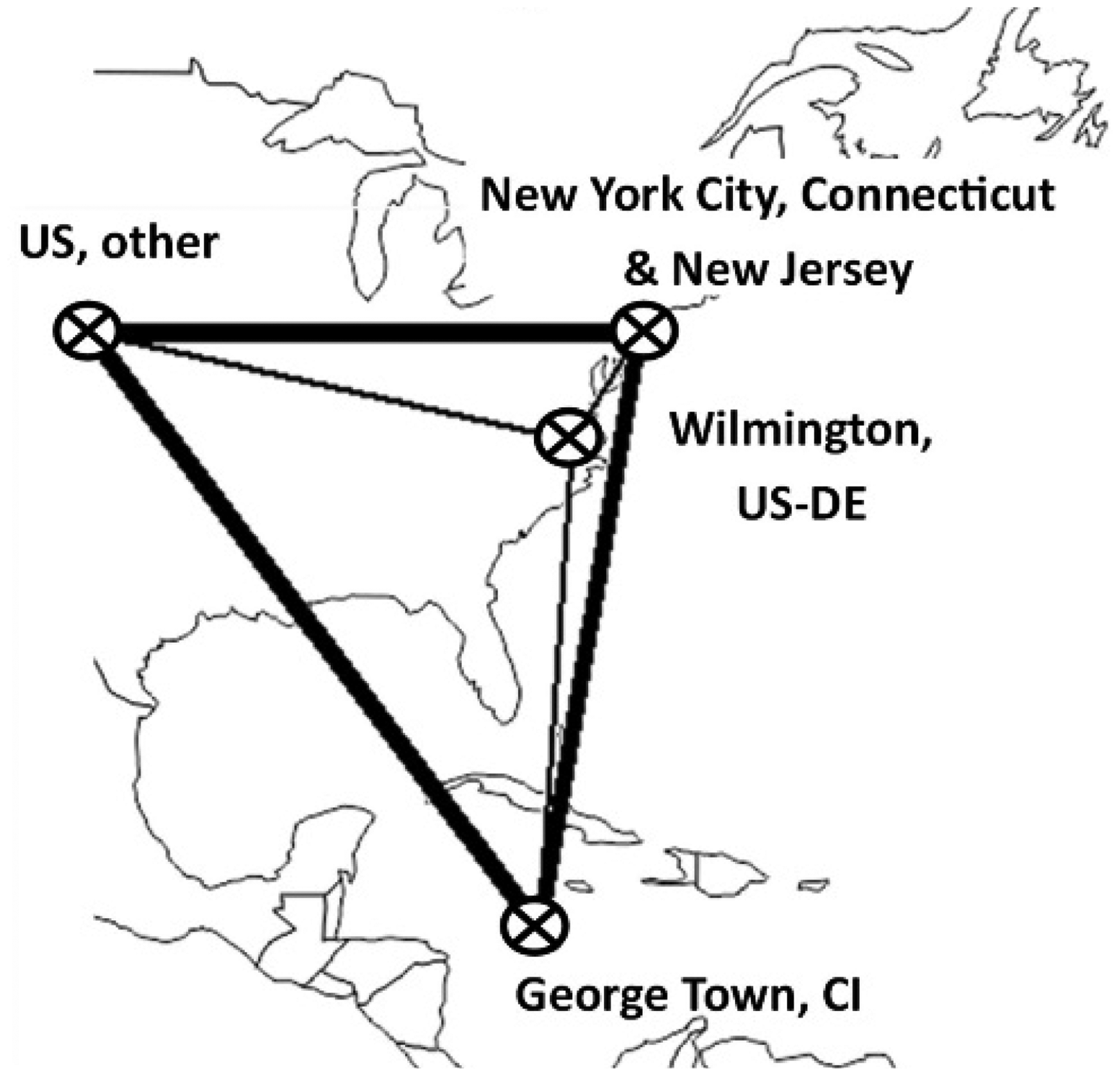

US$-CLO structuration network: relationship strength between sites for CSX-US$ CLOs 11 .

US$-CLO structuration network: firm frequency by function and site.

Note: Delaware is not as visible in this network as before, however, this is not because the jurisdiction is no longer involved but rather it is an issue of data availability.

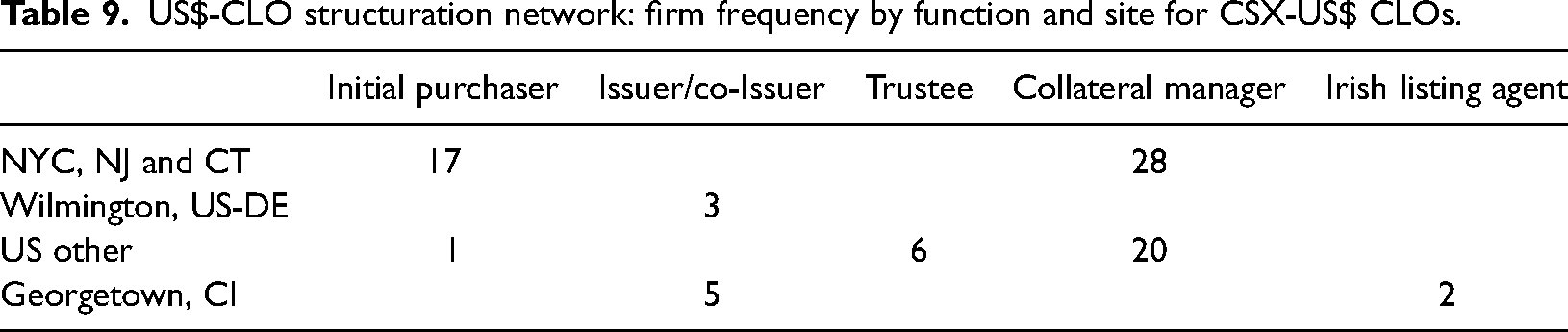

The impact of Regulation (EU) No. 596/2014—Market Abuse Regulation (MAR) in July 2016, also made listing US$-CLOs on EU exchanges, including the ISE, more costly (Harneys, 2019). After MAR, some (but not all) market participants began delisting US$-CLOs from ISE's Global Exchange Market. To capitalize, the CSX—wholly owned by the Cayman Island Government—changed their regulation to attract US$-CLOs seeking to avoid MAR in order to capture some of Ireland's listings market (MacDonald, 2018), illustrating the imbrication of state action in inter-jurisdictional off-shore competition (Rixen, 2013). In networked product terms, this is an example of transformation to circumvent a legislative impasse: the margin profile of CLOs generated a need for lower costs and thus an incentive for the Cayman Islands to (re)configure regulations to capture markets, entrench local expertise, and build strength in local epistemic communities. The expansion of the CSX, in this example, reinforced the skills base of the Cayman Islands as a financial center—Maples group, for example, acted as both an Irish listing agent as well as a Cayman Island issuer, but pulled personnel from Dublin to the Caymans post-MAR, enhancing the expertise and connectivity of the Cayman Islands financial center. Since year-end 2016, the aggregated market value of all securities listings on the CSX more than doubled from US$198bn to US$428bn year-end 2019, of which US$262.8bn was specialist debt securities (Lazier and Cornett, 2020).

These changes of financial geography occur when evolving local institutional contexts meet the cost-minimizing, profit-seeking imperatives of global capital markets (see Lai et al., 2020 for discussion). The paradoxical effect of MAR, which was designed to increase transparency, was to push US$-CLO listing functions back into the Cayman Islands (see Figure 9 and Table 9), where disclosure is weaker (Lazier and Cornett, 2020; cf. Black, 2012).

US$-CLO structuration network: firm frequency by function and site for CSX-US$ CLOs.

Discussion: The networked product's enrichment of the GFN framework

Our network product approach shows how the techno-scientific, risk-mitigating, legal and economic characteristics of a financial product shape the relationships between, and thus the development trajectories of, different types of financial center. It therefore has the capacity to enrich existing GFN research on the way product features give form to the advanced business services within, and territorial relations between, on- and off-shore worlds (Coe et al., 2014; Haberly and Wójcik, 2015, 2017; Lai, 2009, 2012, 2018; Wójcik, 2018; Wójcik et al., 2018). A networked product approach helps to change the way we think about agency in GFNs. It allows us to move beyond the idea that core decision-making centers freely choose partners, and so determine the spatial organization of finance and money. Our approach suggests product features constrain the free associative choices of any one organization located in any one financial center. Networked products tend to produce isomorphic and thus durable relations between products and the network of sites involved in their structuration; they may also shape the processes of change and adaptation when product needs encounter legislative impasses. “Adaptive resilience” (Wójcik and Cojoianu, 2018) may result from the isomorphic logics that constrain radical GFN change, rather than any inherent conservatism in the relational choices of individual companies.

The networked product approach we employ also has methodological implications for GFN research. Mapping the relational histories of particular financial products through the legal artefacts they leave behind can also reveal different developmental trajectories and territorial connections formed as markets emerge. Patterns of network conformity, as we see in our example of CLOs, can be identified and differentiated from those of transduplication as with European CDOs; or even patterns of divergence as we might expect to see, for example, in the structuration networks of mortgage-backed securities and CDOs over time, as different valuation cultures and different organizations took hold in each (MacKenzie, 2011). As Riles (2006) notes, documents, such as the OCs we use to construct our social and spatial networks, are “artefacts of modern knowledge” which contain rich empirical detail about the contractual relations between on- and off-shore actors that can be difficult to capture through ethnographic or observational research (see also Tischer et al., 2019), and which remain elusive in studies of world city networks (Taylor et al., 2014).

Networked product mapping could enable the development of typologies of financial network formation according to the spatial footprints left by the structuration process. This could shed new light on skills clustering and financial center formation, but it could also illuminate the strengthening and weakening of relations between centers over time. This, in turn, would complement the nascent work on the geography of financial innovation (Wainwright, 2015)—explaining, through the dialectical relation between network and product, how product innovation in a core hub like New York may create the need to enroll different technical skills located in other financial centers. It may highlight the different vulnerability of particular nodes within a network: multi-functional global financial centers may exhibit a stickiness which anchors activity, which may be less evident in off-shore jurisdictions where regulatory competition plays a more significant role (Cook et al., 2007; Thrift, 1994). It could thus also augment the corpus of work on financial center decline (Cassis, 2010; Engelen and Grote, 2009) mapping the growing peripherality of certain centers as their skill clusters become obsolete when products change or are replaced.

Our findings highlight, as a consequence, the importance of national regulation and legal actors in supporting financial market development (Töpfer and Hall, 2018). Our study reinforces Riles (2014) observation that regulatory arbitrage is at the heart of many financial products. Accordingly, it may be appropriate to adjust our notion that financial products are built in one core financial center and that relations to other centers are ancillary. The economics of many financial products means they are constructed to take advantage of a distributed international architecture of regulatory loopholes which link on- and off-shore worlds allowing products and their arrangers to obtain the maximum benefits from each site. That may have implications for what is understood by a “flow” between these jurisdictions, when there is rarely any tangible movement of goods, labor, or capital between them; the flow is a legal imaginary or contrivance in the paper geographies of finance (Haberly et al., 2019).

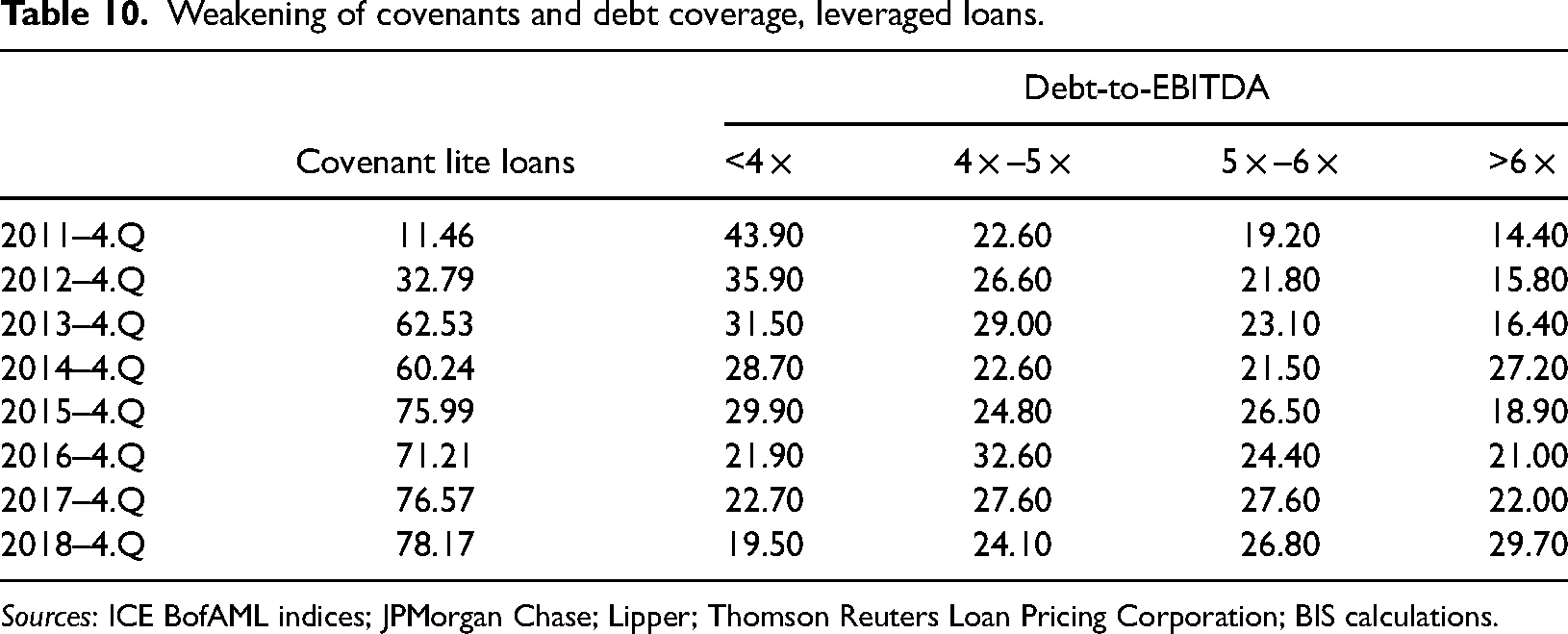

Moving from the general to the specific, our findings show strong organizational and spatial regularities in the structuration networks between CDOs and CLOs despite a gap of over 12 years peak to peak and a fundamental discrediting of the CDO market. The language of “complexity” which accompany descriptions of structured credit products can obscure the duplication embedded in processes of financial innovation and the often prosaic and symmetric relational structures that emerge when markets form or regenerate (Christophers, 2009). Whether this suggests a similar fate will befall CLOs to that of CDOs is as yet unclear. It is important to recognize important differences between CDOs and CLOs—the latter are first-order rather than second-order securitizations for example—although both may be levered on roughly the same ratio of tangible assets because CLOs are secured on corporate assets which can be primarily intangible, whilst CDOs are (ultimately) secured on the properties mortgaged 10 . The more salient point is that, given how many market failures there have been, it would be naive to view all of these failures as primarily the result of idiosyncratic problems in product design. A networked product approach would ask whether the quotidian sociology of exchange within relatively unchanging structuration networks produces Minskian tendencies—the tendency for the cushion of safety to decline. Uzzi (1999) suggests repeat exchanges within social networks improve the terms of trade. But if the underlying product is default risk, improved terms might mean a growing tolerance for lower quality, higher yielding loans, or strategies to encourage rating agencies to rate a greater proportion of the product structure as AAA. There is some evidence that leveraged loan quality is deteriorating (Table 10). Covenant-lite or “cov-lite” loans—that is, those with fewer restrictions for the borrower and fewer protections for the lender—have increased from 11.46% of the market to 78.17% of the market since 2011. Similarly, the proportion of those loans given to firms that are 6 times levered or more has grown from 14.4% to 29.7% over the same period. That deterioration in quality has been driven by demand from CLOs who now buy ∼65% of all US leveraged loans (Bank of England, 2019; International Monetary Fund, 2019) mirroring the erosion of quality seen in the CDO market before the 2007/2008 crash.

Weakening of covenants and debt coverage, leveraged loans.

Sources: ICE BofAML indices; JPMorgan Chase; Lipper; Thomson Reuters Loan Pricing Corporation; BIS calculations.

From a networked product perspective financial centers may therefore provide the relational infrastructures that produce mundane, repeat interactions which build shared understanding, tolerances, and concessions which lower costs for incumbents. That can have a dark side if it produces systems of reciprocity, obligation, favor exchange, and dependence which reduce sensitivity to risk and drive standards down (Skinner et al., 2014). These network regularities which lead forms of exchange that increase market risk are little acknowledged, but are illuminated by the networked product approach. It may well be that the network stabilities observed here create market instabilities if the quotidian sociology of exchange within those networks build tolerances, risk-blindness, and a slow erosion of standards.

Concluding remarks

Our research has shown the utility of the networked product concept and method for enriching the GFN approach through an understanding of the growth of debt securities markets across jurisdictions and their capacity to replicate and regenerate over time. We show how the risk-mitigating, arbitrage-led and administrative features of CDOs produced a demand for specialist, spatially situated skilled inputs and low regulatory regimes, reinforcing existing on- and off-shore strengths and relations isomorphically. We show that the CDO market grew in the US through strong repeat relations between New York, Delaware, the Cayman Islands, and Ireland. We also show that those activity and arbitrage relations were transposed into Europe through a process of “transduplication.” Once established, those network relations became remarkably durable—the relations formed during the CDO boom recur in the CLO market 10 years later. We also find similar levels of activity concentration with many of the same organizations core to both CDO and CLO networks. Change, where it is observed, is limited and takes the form of what Wójcik and Cojoianu (2018) call “adaptive resilience” in more peripheral advanced business services.

Our findings show how products create and sustain the relationality of GFNs across space and time. Consequently, we call for a more central positioning of the product in future studies of GFNs in financial geography. As our study has shown, financial products are not simply the output of interactivity between world cities, advanced business services and off-shore territories. Products, like other non-human entities, have agentic qualities (Zook and Grote, 2017), connecting and reconfiguring those financial and spatial networks isomorphically. We thus provide a different and novel view of the evolution of structured finance GFNs, one rooted in the technical and paper geographies of finance (Haberly et al., 2019). A similar approach could be applied elsewhere to study how, why, and where the processes of structuration take place within a global economy.

Finally, by looking through the prism of the product, and showing the remarkable consistency between CDO and CLO structuration networks, we echo the skepticism of other authors who have argued that the emphasis on the complex technical features of financial products obscures many relatively mundane, routinized relations, and processes (Christophers, 2009). Our findings suggest that more work needs to be done to explore whether the enduring relational infrastructures that we observe in our case study foster patterns of risk tolerance and concession giving more generally in finance which lead to a decline in standards or even collusive practice, as we saw in the Libor-fixing scandal. The role of networked products in fostering the network stabilities that produce market instabilities could provide a potentially fruitful area for future investigation.

Footnotes

Acknowledgements

We would like to thank Anna Krystalli for help compiling some of our CLO database.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Independent Social Research Foundation (grant number 160839).