Abstract

This article asks whether and how local firms in low-income countries can participate, upgrade and capture value in apparel global value chains in the context of increased entry barriers and asymmetric power relations. It focuses on Madagascar, which is the top apparel exporter in Sub-Saharan Africa and one where there is a significant number of local firms. The article examines the capability-building processes of local firms, which are the basis for upgrading paths and broader sector development. We do this by combining conceptual insights from the Technological Capabilities literature with the conjunctural approach to Global Value Chains and Global Production Networks. Based on extensive fieldwork in Madagascar’s apparel export sector, the article explains how the relational, local and regional assets that local firms can leverage in building technological capabilities influence their choices with regards to export strategies and their upgrading paths. In turn, these assets are linked to different types of local ownership, and they emerge through historical legacies and the national socio-economic context, which give rise to specific transnational social relations, as well as through regional economic formations and global value chain dynamics.

Introduction

The apparel export industry is generally perceived as easy to enter, but changes in the global economy have made entry harder for local firms in low-income countries. International competition increased as many low-income countries pursued export-oriented industrialization strategies with the estimated number of apparel manufacturing firms worldwide more than doubling from the 1990s to the early 2010s (Mahutga, 2014). Furthermore, the phase out of the international quota system under the Multi-Fibre Arrangement (MFA), which limited the exports of established supplier countries, intensified asymmetric power relations between buyers and low-income country supplier firms. The upshot has been declining unit values of apparel imports in the key end markets of the United States (US) and the European Union (EU) (Anner, 2019). At the same time, the requirements of US and EU buyers increased and became more stringent, requiring shorter lead times and greater flexibility from suppliers as well as non-manufacturing tasks such as input sourcing, product development and inventory management (Abernathy et al., 2006; Palpacuer et al., 2005; Staritz, 2011).In short, apparel buyers demand more capabilities and shift more risk to supplier firms but generally pay less, which Kaplinsky (2005) described as being caught between a rock and a hard place. This situation creates higher barriers to entry for local firms in low-income countries, which typically start from a position of low capabilities.

In this challenging global context, the share of Sub-Saharan Africa (SSA) in world apparel exports is minimal, accounting for 1.3 percent at the height of the MFA in 2004, which declined to 0.8 percent in 2008, where it remained until 2018. 1 Only a few SSA countries have been successful in creating an apparel export industry of significant size: South Africa, Mauritius, Madagascar, Kenya, Lesotho, Swaziland and more recently Ethiopia. However, South Africa’s apparel exports were minimal in the 2010s due to limited international competitiveness, and the sector also faced high competition in the domestic market from Asian and regional apparel exporters (Morris and Barnes, 2014). In Mauritius, the apparel export sector started in the late 1970s and even though exports declined since the 2000s, the sector remains important (Gibbon, 2000). In Kenya, Lesotho and Swaziland, the sector grew in the early 2000s based on foreign direct investment, largely from Asian transnational producers that were motivated by MFA quotas and preferential market access to the US with the African Growth and Opportunity Act (AGOA). After the MFA phase out, however, many Asian investors left and exports declined. In Lesotho and Swaziland exports stabilized in the 2010s due to the emergence of regional production networks with South African investors exporting to South African retailers (Morris et al., 2011, 2016). In Kenya, exports increased in the 2010s due to the expansion of the remaining foreign firms, which were largely from India and had social networks linking them to the Kenyan Indian community (Phelps et al., 2009; Whitfield and Staritz, 2020).

Only Mauritius and Madagascar have an important apparel export industry in which a significant number of local firms participate (Morris et al., 2016). 2 Madagascar had approximately 31 local apparel export firms in 2019, in addition to 38 foreign-owned firms. While Madagascar experienced difficult country-specific conditions in terms of intense political instability in the early 2000s and again in the late 2000s, the apparel export industry survived and then expanded, becoming the largest SSA apparel exporter in 2017, due to the presence of local firms and regional investment from Mauritius. Despite foreign direct investment driving the emergence of apparel exports in Kenya, Lesotho and Swaziland around the same time as in Madagascar, these countries had less than a handful of local export firms (Morris et al., 2016). In Ethiopia, the sector began in the late 2000s, supported by strategic industrial policy, and grew in the 2010s based on foreign direct investments; it still has to be seen to what extent local firms will succeed in entering and remaining in the apparel export sector (Whitfield et al., 2020b).

The experience of Madagascar raises questions regarding the conditions under which SSA countries can create apparel export industries that endure and grow, despite tendencies towards disarticulation when global economic and political factors change. It also raises questions concerning how local firms can participate as well as upgrade and capture value in the context of asymmetric power relations between buyers and suppliers in apparel global value chains (Bair and Werner, 2011). This article explains why Madagascar has an apparel export industry, despite poor infrastructure, being located far from US and EU end-markets, political instability and general government neglect of the sector, and one in which local firms have been able to enter, remain and upgrade. It builds on previous work on the Madagascar apparel export industry by Morris and Staritz (2014) and Morris et al. (2016) that emphasized the ownership and embeddedness characteristics of supplier firms and their importance for explaining upgrading among supplier firms. This article focuses on local firms and demonstrates how ownership shapes local firms’ upgrading paths, but also how local firms’ relations with specific foreign firms and buyers led them to specialize in particular product types and market segments. It examines firm-level processes of building capabilities, which are the basis for different upgrading paths, and how these processes are linked to the national socio-economic context in which they take place as well as to transnational social relations, regional economic formations and global value chain dynamics. We do this by combining conceptual insights from the Technological Capabilities (TC) literature with the Global Value Chain (GVC) and Global Production Network (GPN) literatures, especially the conjunctural approach advocated by Pickles and Smith (2016).

The article draws on interviews with 30 out of the 31 local apparel export firms that we identified during fieldwork in Madagascar in 2016 and 2017, as one firm could not be reached, as well as on the results from a firm survey that we designed to measure local firms’ technological capabilities and carried out with the 23 local firms that agreed to participate. Based on the survey results, we selected a strategic sample of 7 local firms for in-depth study of their capability building processes and export strategies through repeat interviewing of owners and key managers between 2017 and 2019. The selection aimed to capture variation in ownership type and global value chain function, but was ultimately shaped by which firms agreed to participate in the firm histories. We also interviewed 29 out of the 38 foreign firms in Madagascar, staff of the different industry associations, and government officials in the Export Development Board of Madagascar. Fieldwork was also carried out in Mauritius in 2017 that included interviews with officials in relevant government agencies, staff of the main industry association, and 4 of the 11 large Mauritian firms that accounted for the majority of apparel exports. 3

The article argues that different upgrading paths of local firms are the outcome of firm level export strategies that involve building particular capabilities. In turn, the strategies that firms choose are shaped by the intra-firm resources that they can draw upon, especially relational assets, and can be buttressed by extra-firm factors such as local and regional assets, industrial policy, and the strategies of foreign firms and buyers, as elaborated in the next section.The remaining sections describe the development of the apparel export sector in Madagascar and explain how local firms in Madagascar were able to enter and upgrade in apparel global value chains by leveraging relational, regional and local assets.

Conceptualizing local firm capability building in global value chains: Relational, local and regional assets

The GVC and GPN theoretical approaches focus on lead firm strategies and governance, and the implications for supplier firms, particularly in terms of upgrading and value capture (Coe and Yeung, 2015; Gereffi et al., 2005; Henderson et al., 2002). A growing body of literature points to the difficulties for supplier firms to capture value in highly asymmetric global value chains (e.g. Baglioni et al., 2019; Mahutga, 2014; Quentin and Campling, 2018). This literature demonstrates how lead firms’ governance practices allow them to put immense price pressure on suppliers along with demanding higher requirements, which limits the benefits for local firms from participating and upgrading in global value chains. A related literature has developed the notion of disarticulation to focus on the significance of the reproduction of low-value positions and uneven development patterns in global value chains as well as the constitutive exclusion of some firms, regions and workers (e.g. Bair and Werner, 2011; McGrath, 2018; Werner, 2019). However, we still observe diverse supplier firm-level outcomes and sectoral and regional development. The literature critical to the notion of upgrading shows that supplier firms do not necessarily pursue linear and unidirectional trajectories of upgrading or downgrading, especially as their search to capture greater value and reduce risks may also lead to combinations of upgrading and downgrading, and shifting to entirely different chains or new markets (e.g. Pickles et al., 2006; Schrank, 2004; Tokatli, 2013).

Thus, we need to go beyond the inclusion/exclusion focus and upgrading/downgrading dichotomy to examine the diversity of firm-level and industrial trajectories. To do so, Pickles and Smith (2016) propose a conjunctural approach (see also Werner, 2019). Building on insights from conjunctural analysis in economic geography, they argue that global value chains are embedded in systems and networks of social relations, specific cultural histories, and regional economic formations. Pickles and Smith (2016: 48) note that this approach specifies the claim by Gereffi et al. (1994) that global value chains were ‘situationally specific, socially constructed and locally integrated’, and elaborates the point by Henderson et al. (2002) that global production networks absorb and are to some extent constrained by the social dynamics and economic activities that already exist in local places. Hence, the strategies and actions of local supplier firms, as well as those of lead firms and foreign supplier firms, are shaped by specific national and regional contexts and their systems of social relations and geographical legacies.

In order to understand firm-level upgrading paths and value capture trajectories as well as industry-level development in supplier countries, it is necessary to look more closely at firms’ capability building processes and factors driving these processes. We build on the conjunctural approach to analyzing GVCs and GPNs and connect it to the TC approach, which focuses on firm-specific learning efforts and their extra-firm context, the importance of tacit knowledge and the difficulties entailed in learning. It underscores the complexities, costs, risks and uncertainties of capability building and provides a way to operationalize and thus observe where firms are in building capabilities and what factors influence their choices about building capabilities.

The term technological capabilities refers to the technical, organizational and managerial skills that firms need in addition to formal education and scientific knowledge in order to achieve the level of productivity that sets the international market standard (Amsden, 2001; Helfat, 2018; Lall, 1996). It underscores that the barriers to entry in particular industries, even in low-value functions and segments of global value chains, consist of the tacit knowledge required to make use of hard technology and codified knowledge in a profitable way. Firms can only acquire technological capabilities through purposeful and conscious investments in learning and the accumulation of experience in particular contexts, which involves learning by individuals as well as establishing collective routines specific to an organization. This learning process is costly and risky (Khan, 2019). It is uncertain if and when local firms will be successful and hence recoup the costs, especially if firms are far away from the minimum capabilities required to achieve the productivity level, quality standards and delivery speed of existing suppliers in global value chains, resulting in a large capability gap. While local firms are putting in the effort to bridge the capability gap, they are generally not making any profit, and thus the learning has a high cost, especially if tacit knowledge has to be brought from outside the country.

However, local firms differ in the initial resources they can draw upon to invest in learning, which shapes their likely success in building capabilities and thus their profit/risk calculations. Combining the conjunctural and TC approaches, we argue that the resources that matter most for capability building and upgrading are the ability to access finance and (foreign) tacit knowledge as well as the personal relations and social networks of firm owners and managers. Social networks matter because they can be leveraged to access finance and tacit knowledge as well as to create linkages with foreign investors, buyers and input suppliers. Network resources achieved from prior alliances provide differential access and benefits as well as lead to possibilities for firms to form further alliances. Differences in local firms’ initial resources are related to local firm ownership characteristics because firm owners differ in their social, cultural, political and economic traits. Furthermore, as Morris et al. (2016) show, ownership characteristics of foreign supplier firms and buyers also matter for local firm capability building. When local firms share social networks with foreign suppliers and buyers, it is easier for local firms to build personal relations, connect and create linkages. As a result, foreign firms are more likely to allow local firms to access knowledge and contacts through their networks. Thus, social relations and networks are relational assets for local supplier firms (Pickles and Smith, 2016: 183). These relational assets can be leveraged and are products of past processes such as imperial histories, migration, and colonial practices.

In addition to relational assets, local supplier firms can increase their resources through leveraging local assets and benefiting from industrial policies aimed at strategic coupling as well as from the regional context. The GPN literature on strategic coupling argues that even for highly labor intensive manufacturing located in ‘assembly platforms’ where supplier firms are highly dependent on foreign lead firms, strategic state policies are required (Coe and Yeung, 2015). National or sub-national governments need to attract investment through proactive policies that create local assets, as it takes more than low labor costs to create an internationally competitive apparel supplier country. Thus, the state plays a role through industrial policy in resolving constraints external to local firms that result in high production and transport costs but also in increasing the resources that local supplier firms can access in order to build their capabilities, especially access to finance and knowledge (Khan, 2019). These industrial policies reduce the risks and costs of firm-level capability building and create the local assets required for strategic coupling with globalized industries.

However, supplier countries increasingly have the same policy-created local assets focused on lead firm and foreign direct investment attraction and often infrastructure and service provision in the context of some type of special economic zones (Morris and Staritz, 2019). Thus, local supplier firms need unique assets that can make them less easily substitutable, or even irreplaceable, and that lead to longer term buyer-supplier relationships and thus greater opportunities for upgrading and value capture. Sako and Zylberberg (2019) refer to this as specialized complimentary assets, analyzing supplier firms that have been able to create such assets at the firm level. It could also be the case that particular firms leverage country-specific attributes, skills or services available to all or most firms, turning them into firm-level specialized complimentary assets, as we see in the case of Madagascar in terms of artisanal handicraft skills in the country. Resources created through industrial policies might be offered only to particular local firms as a result of political dynamics of country-specific political settlements, excluding other firms or potential investors from benefiting from policy-created local assets (Khan, 2013).

Finally, the specific regional context in which local supplier firms operate offer differential opportunities as the result of regional economic formations, political dynamics and institutions. For example, Pickles and Smith (2016) show how socialist legacies and being next door to Western Europe shaped the ways in which apparel supplier firms in Central and Eastern Europe were restructured in the post-socialist period. Geographic and cultural proximity to core markets shaped opportunities and constraints for local apparel firms and led Western buyers and their suppliers to enter joint ventures with local investors in order to develop regional production networks that could respond rapidly to market requirements. Morris et al. (2016) show that geographic proximity in regional production networks in apparel sectors in SSA has led to more interaction of foreign investors with actors in supplier countries and a more fluid division of labor and functions between head offices and supplier firms. Hence, lead firms as well as foreign suppliers also come from specific regional contexts and are part of systems of social relations and geographical legacies that influence their strategies and relations with supplier firms.

Apparel export industry development and local supplier firms in Madagascar

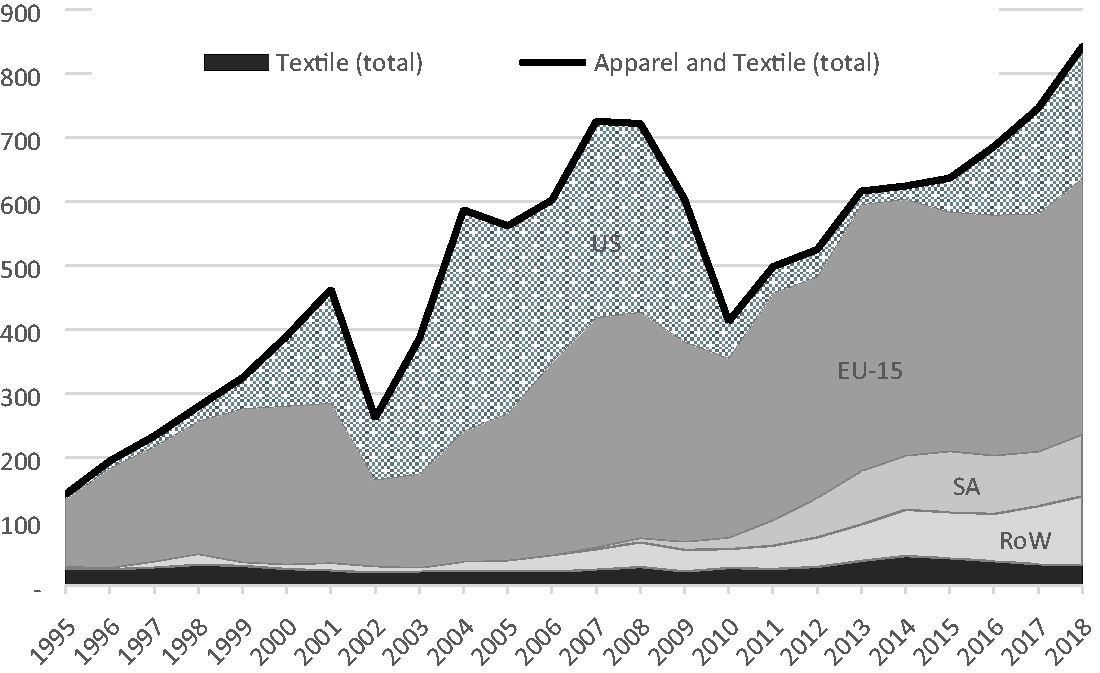

Figure 1 depicts the overall development of apparel exports in Madagascar. The sector began in the mid-1990s after the Export Processing Zone (EPZ) law was passed, with firms benefiting from MFA quotas and preferential market access to the EU under the Lome Convention and the Everything But Arms initiative and later also to the US under AGOA. Overall, as the narrative in this section shows, the key driving forces behind the sector’s growth and resilience were French, Mauritian and Hong Kong investments, which pioneered the sector, along with the emergence of locally owned firms that kept exports going despite the political crises and loss of AGOA, and increased investment by Mauritian firms since the return of AGOA status in 2016.

Total apparel and textile exports from Madagascar (in USD millions).

Madagascar had a small mainly state-owned textile industry as a result of import-substitution industrialization and nationalization policies in the 1960s and 1970s. However, it was decimated during the 1990s, as in many SSA countries, in the context of trade liberalization and the massive importation of new and used clothing combined with state-owned companies’ financial difficulties (Maminirinarivo, 2006). At the same time that local firms lost the domestic market to imports, a new export sector in apparel manufacturing emerged. As part of the structural adjustment economic reforms pushed by the World Bank, the Malagasy government passed the EPZ law in 1989 as a way to attract foreign direct investment and boost exports (Fukunishi and Ramiarison, 2012). Investors were not required to have factories in a specific EPZ location, but rather EPZ status that conferred financial and fiscal benefits was granted to individual firms in return for exporting 95 percent of their production. By 2001, there were 213 firms with EPZ status, of which the majority were apparel firms, and EPZ firms contributed 10 percent of GDP (Maminirinarivo, 2006: 179).

The main foreign investors in the 1990s were French, followed by Mauritian (Cling et al., 2005). French apparel corporations chose Madagascar to offshore their labor-intensive apparel assembly, not only because of the country’s preferential market access to the EU, EPZ incentives, and low labor costs, but also because of colonial legacies: the language and large French immigrant community. According to the owner of one of the first EPZ apparel firms, the French development agency funded an apparel training center, which was the only source of trained labor at the time. Our firm interviews indicate that French EPZ firms consisted of French corporate firms setting up subsidiary factories in Madagascar, as well as individual French immigrants already living in the country who established apparel firms by drawing on social networks in France in order to find buyers, acquire knowledge and raise investment finance. Furthermore, a few French corporate investors became locals, settling in Madagascar permanently, blurring the line between French firm and French immigrant firm.

Mauritian apparel firms were the second largest foreign investors in Madagascar, in response to rising wages and the shrinking pool of labor in Mauritius by the early 1990s (Gibbon, 2000; Neveling, 2018). Mauritian firms saw neighboring Madagascar with its large population as a logical site for its most labor-intensive products, such as hand-knitted sweaters, but also for basic products in other segments. They set up factories in Madagascar with their old machines as they upgraded machinery and moved into higher value apparel products and textile production in their firms in Mauritius. Madagascar shared language and cultural affinities with Mauritius, which facilitated investments by Mauritian owners of apparel firms, who were largely of French-origin but also included Indian-origin and Chinese-origin investors. As Morris and Staritz (2014) note, these regional investors had head offices and pursued higher value functions in Mauritius, but the regional proximity allowed for a more flexible division of labor.

It was not only Mauritian supplier firms that turned to Madagascar but also European buyers that had been sourcing from Mauritius, as they sought a new low-cost apparel assembly location. Our firm interviews indicate that European, especially French, buyers of children’s clothes actively encouraged local entrepreneurs in Madagascar to establish apparel factories. These local firms were established by French immigrants and members of the Karana community. Karana are Indo-Pakistanis (Indian-origin, for short) that emigrated from Gujarat in the late seventeenth century and during French colonial rule (Razafindrakoto et al., 2020). Before Madagascar gained its independence from France in 1960, the exiting colonial rulers granted French citizenship to many Indian-origin Malagasy. There is also significant overlap in the social networks among French- and Indian-origin immigrants, often facilitated through marriage.

The third largest group of foreign investors, after French and Mauritian, were from Hong Kong. Hong Kong apparel firms had driven the start of the Mauritian apparel industry and thus were already present in the region (Lamusse, 1989). Hong Kong firms in Mauritius anticipated the implementation of AGOA and started investing in factories in Madagascar from 1998 (Gibbon, 2000). Our interviews revealed that many of the Hong Kong factories were producing very labor intensive products like hand-knitted sweaters (pullovers), which resulted in many Mauritian-owned firms in this product category as well, which they then moved to Madagascar, also influencing the product category of local firms in Madagascar.

When Madagascar became eligible for AGOA in 2001, other transnational apparel producers from East Asia faced with quota restrictions and rising labor costs in their home countries invested in the country as well. They generally developed triangular manufacturing networks involving buyers largely in the US, head offices in East Asia, and supplier firms in lower-income countries, pursuing highly flexible production and sourcing models with limited autonomy in supplier firms and few linkages to the economy in host countries (Azmeh and Nadvi, 2014; Morris et al., 2016).

However, AGOA eligibility was followed by a decade of political instability in Madagascar, which strongly affected apparel exports. The post-election political crisis in 2002 and ensuing civil unrest led most Asian and Mauritian firms to leave, resulting in a contraction in apparel exports by almost 50 percent. All but a few local firms closed operations and then later had to start again from scratch with new buyers and even new product areas. With the MFA phase out that occurred at the end of 2004, most of the remaining Asian firms left (Cling et al., 2005; Kaplinsky and Wamae, 2010; Morris and Sedowski, 2006). Nevertheless, the industry rebounded through the growth of European, particularly French, firms and local firms, and by 2008 apparel exports overtook primary commodities as the largest source of export earnings (Fukunishi and Ramiarison, 2012). The industry’s rebound was disrupted by the North Atlantic financial crisis and subsequent Eurozone crisis as well as another national electoral crisis and coup in 2009. Apparel exports declined dramatically, and US exports collapsed after 2010 with the loss of the AGOA status due to political conditions attached to AGOA eligibility. Only 60 to 70 apparel export firms were still operating in early 2012 (Morris and Staritz, 2014). Madagascar regained AGOA status in 2015, which became operational in 2016, but only two Asian firms came back and five new Asian firms invested in Madagascar.

Notably, there were no industrial policies in the apparel export sector during the 2000s and 2010s. The government lacked interest in the apparel export industry despite its employment and revenue generation importance (Morris and Sedowski, 2006). Political elites were embroiled in conflict that could not be contained within the political institutions, and the country was on the brink of civil war twice (Razafindrakoto et al., 2020). There is one major industry association for EPZ firms, which focused on lobbying the government and offering some training programs, but our fieldwork indicates that it had little effect in initiating industry-wide activities. Furthermore, the infrastructural situation in Madagascar was not particularly competitive, as firms faced problems with customs, inland and sea transport, electricity costs and reliability, telecommunications, and rents (Kaplinsky and Wamae, 2010; Morris and Sedowski, 2006). There were some improvements in infrastructure by 2016, but the lead time from Madagascar was still very high, estimated at 4 to 5 months. As a result, local firms tended to specialize in product categories with repeat orders (where firms rely on large inventories), in niche products with less competition, and in luxury clothes produced in small volumes and shipped by air.

Madagascar still became the largest apparel exporter among SSA countries in 2017, driven primarily by Mauritian investment, which expanded at a greater pace than other foreign and local firms. Mauritian firms that had left after the 2002 crisis returned to Madagascar starting around 2012, and other Mauritian firms shifted their production to Madagascar for the first time. Based on our interviews with Mauritian firms, by the mid-2010s, the Mauritian apparel industry was characterized by 12 large firms that accounted for 70 percent of apparel exports. 4 Six of these firms had major investments in Madagascar, retaining their headquarters in Mauritius to carry out design and marketing and factories focusing on fast fashion products, and developing regional production networks using their factories in Madagascar to sew long run, basic products using fabric produced in Mauritius, though a few Mauritian firms also established vertically integrated factories in Madagascar. Mauritian firms produced largely for European buyers, but the Eurozone crisis and duty free access under the Southern African Development Community led Mauritian firms to shift a significant proportion of their production to the South African market. 5 Local firms in Madagascar also experimented with supplying the South African market, but local firms that specialized in high value products found the prices of South African buyers too low. Mauritian firms and some larger local firms in Madagascar were better able to align their business strategies with the basic high-volume products demanded by South African retailers. Figure 1 above shows this growth in exports to South Africa. Regional production also involved input sourcing, with Mauritian firms sourcing most of their cotton from SSA countries and Mauritius accounting for 13 percent of fabric imports in Madagascar in 2018, after China and India. 6

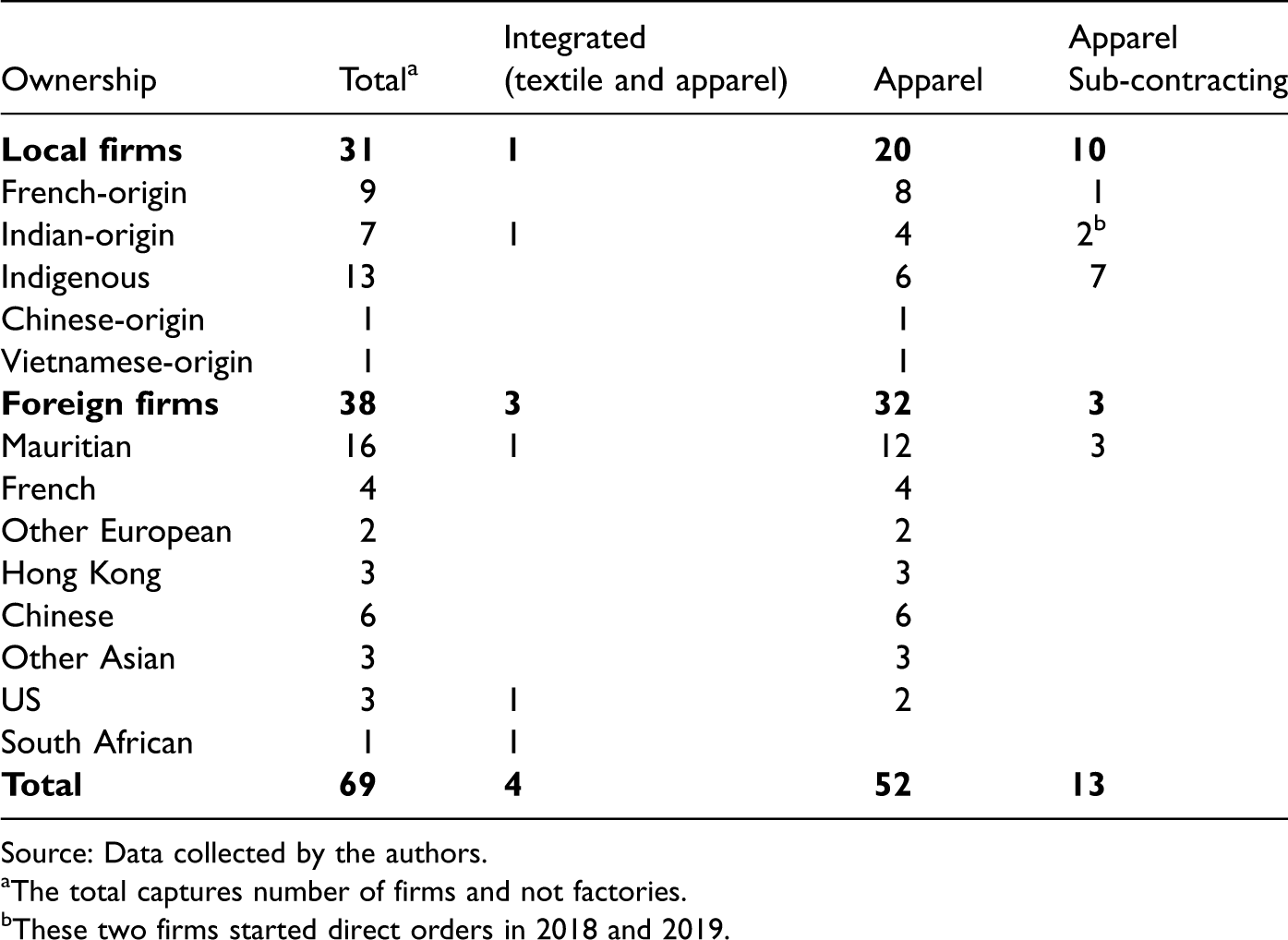

When we conducted our research between 2016 and 2019, there were approximately 69 apparel firms in Madagascar producing for export directly or indirectly through sub-contracting, including 31 local firms and 38 foreign firms, as shown in Table 1. 7 Our definition of a local firm emphasizes local embeddedness in terms of decision-making and residency and thus includes firm owners who may not have Malagasy citizenship. Our ownership classification builds on Morris and Staritz (2014), but also differs in two ways. First, we differentiated between French corporate firms that have headquarters abroad and only an assembly factory in Madagascar, which we classify as foreign firms, and French firms that have most or all business functions within Madagascar and whose owners consider themselves local Malagasy, which we treat as local firms. Second, we identified several categories of local firms, which include French immigrants and indigenous Malagasy but also other immigrants, most importantly Indian-origin firms. Taking these two differences into account, a comparison of firm numbers in Morris and Staritz (2014) from 2012 with our data from 2019 confirms trends highlighted in the sector’s development narrative. Among the foreign firms, Hong Kong and European corporate firms decreased, while Mauritian firms increased as a result of their intensified delocalization strategy after the return of political stability, and Asian firms increased slightly after the return of AGOA. The number of local firms increased as well, with new indigenous and Indian-origin firms starting through sub-contracting.

Apparel export firms in Madagascar by ownership type, 2019.

Source: Data collected by the authors.

aThe total captures number of firms and not factories.

bThese two firms started direct orders in 2018 and 2019.

Of the 31 local export firms, 9 have owners of French-origin, 7 of Indian-origin and 13 are owned by indigenous Malagasy, while the remaining two have owners of Chinese- and Vietnamese-origin. There is a minority Chinese community in Madagascar that dates to the colonial period, similar to the Karana (Razafindrakoto et al., 2020). The owner of the Vietnamese-origin Malagasy firm is a more recent immigrant, but she is married to a French immigrant and thus there is a strong French connection.

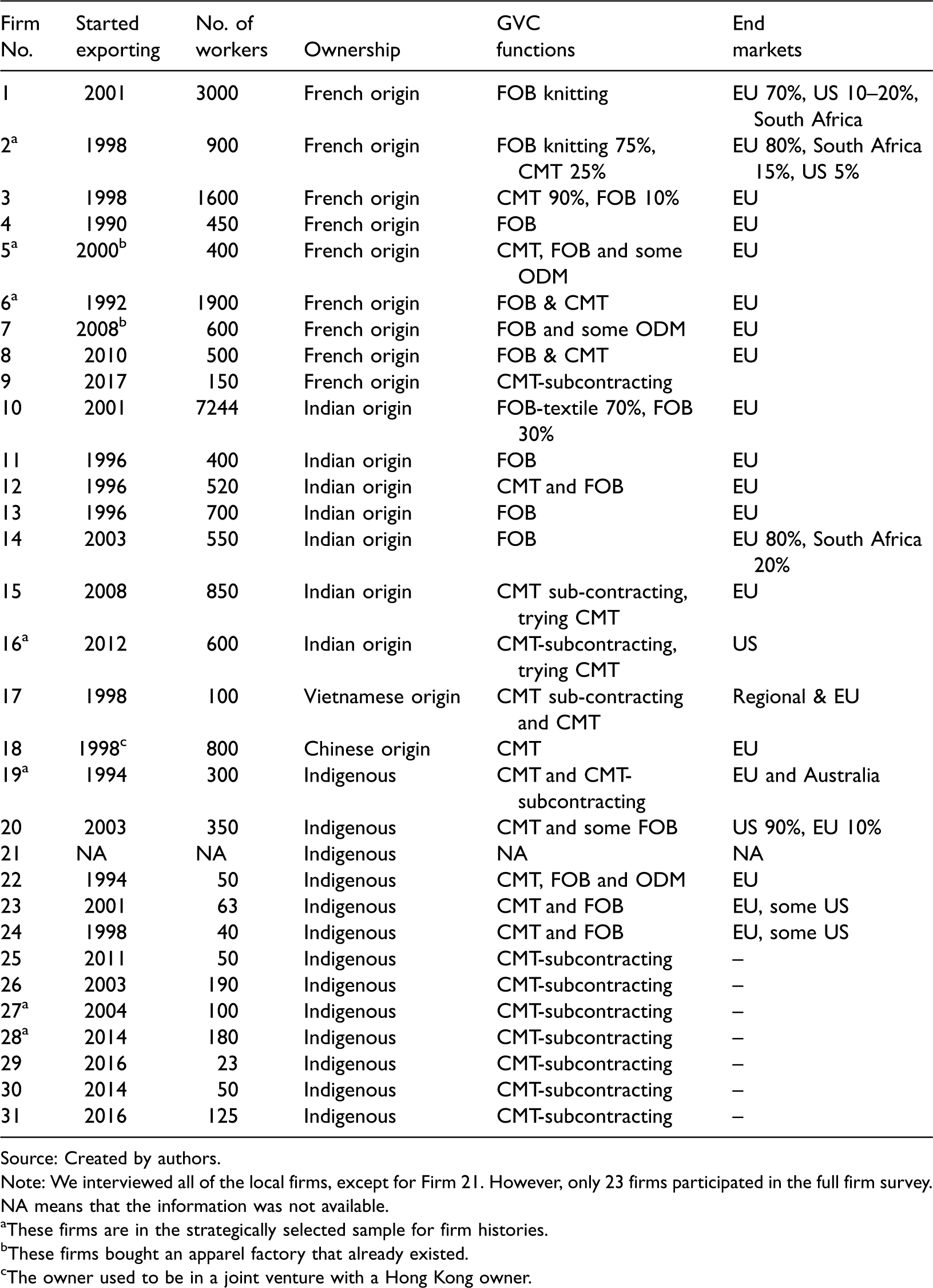

Table 2 provides an overview of the characteristics of these local firms. Most of the local firms that directly exported have been doing so since the 1990s or early 2000s, as explained in the sector’s development narrative. Local firms that were established in the 2010s were all owned by indigenous Malagasy and were engaged in cut-make-trim (CMT) sub-contracting. In terms of size, indigenous Malagasy firms are smaller, employing on average about 100 workers compared to about 850 workers for the French-origin firms and 600 for the Indian-origin firms. 8 Local firms generally produced niche and high value products, which fall into four product categories: children’s clothes with a large degree of labor intensive smock and embroidery (S&E) handiwork; specialized work wear; knitted pullovers; and high end and niche fashion clothes. Only three local firms produced basic apparel products. Local firms exported primarily to the European market except for two firms that exported predominantly to the US. Local firms varied in terms of the functions they performed within apparel global value chains, but there was limited vertical integration towards textile production among local firms, with the exception of the two knitting (pullover) firms and one vertically integrated textile mill. 9

Overview of local apparel exporting firms in Madagascar, 2019.

Source: Created by authors.

Note: We interviewed all of the local firms, except for Firm 21. However, only 23 firms participated in the full firm survey. NA means that the information was not available.

aThese firms are in the strategically selected sample for firm histories.

bThese firms bought an apparel factory that already existed.

cThe owner used to be in a joint venture with a Hong Kong owner.

Measuring technological capabilities of local apparel supplier firms

We assessed the technological capabilities of local firms by building on the standard methodology in the TC approach. The methodology involves dividing capabilities into categories, specifying the capabilities required in each category, choosing indicators for these capabilities, and developing a method for scoring firms based on these indicators. 10 We adapted this methodology to the context of exporting through global value chains.

Lall (1992) produced the classic conceptualization of technological capabilities in a matrix generated by two classificatory principles: the categories of capabilities that firms need, and their degree of complexity. His capability categories included investment, production and linkage capabilities. We elaborated this matrix by incorporating the upgrading concept, where the classic upgrading dimensions include process, product, and functional upgrading (Humphrey and Schmitz, 2002). Process upgrading refers to improving technology and/or production systems in order to increase efficiency, and product upgrading refers to moving into higher quality products. Functional upgrading refers to increasing the range or moving into higher value added activities, including non-manufacturing activities such as design, branding, logistics, and distribution (Kaplinsky and Morris, 2001). Firms may also attempt to capture more value or reduce risk by diversifying or moving to new buyers and markets, referred to as end market upgrading, or by strengthening backward and forward linkages through supply chain upgrading (Frederick and Staritz, 2011). Thus, our elaborated technological capabilities matrix has five categories of capabilities on the horizontal axis, which include investment, product, production, end-market, and linkages. Functional upgrading puts the focus on different positions in terms of value-added activities in global value chains, which to a large extent determines the capabilities required in the above categories (Giuliani et al., 2005). Therefore, the vertical axis specifies the different functions in particular global value chains. Moving into higher functions generally involves deepening existing capabilities but also developing new and more complex capabilities. 11

We filled out this generic matrix for apparel global value chains using the broad GVC/GPN literature on the apparel sector and insights from interviews with global buyers and suppliers in different supplier countries. The functions include first subcontracting for other firms based in the country, and then assembly (cut-make-trim, CMT) where the firm has direct contact to buyers and carries out production according to the requirements of and with the inputs provided by buyers. In original equipment manufacturing (OEM, or FOB) the firm is responsible for financing and sourcing the inputs, all production steps, finishing, and packaging. Firms may then progress to original design manufacturing (ODM) where the firm also provides design functions to buyers, and even original brand manufacturing (OBM) where the firm also owns the brand (Gereffi, 1999). Supplier firms may also functionally upgrade to key input sectors, the most important of which is fabric production (textile). Thus, our apparel GVC-specific matrix describes the technological capabilities needed for entering each function in terms of the five capability categories. For example, CMT subcontracting already needs substantial production related capabilities but limited end market and supply chain linkages capabilities. Moving to direct relationships with buyers requires substantial end market capabilities but only the move to FOB requires linking to suppliers and managing and financing the input sourcing process, i.e. supply chain linkages capabilities. The matrix is presented in the Supplementary Material.

We used this matrix to design a survey questionnaire for local firms, selecting quantitative and qualitative indicators that could capture the capabilities described in the matrix cells. The survey also included questions on the background of the owner as well as the history of the firm’s development and its specific integration into global value chains. The survey was carried out through face-to-face interviews with firm owners and/or top managers. For the scoring exercise, where we directly measure firms’ capabilities, we selected only a few of the indicators included in the survey in order to facilitate comparison across firms. The Supplementary Material elaborates which indicators we selected and why, and how they were scored.

Building capabilities and upgrading paths using relational, local and regional assets

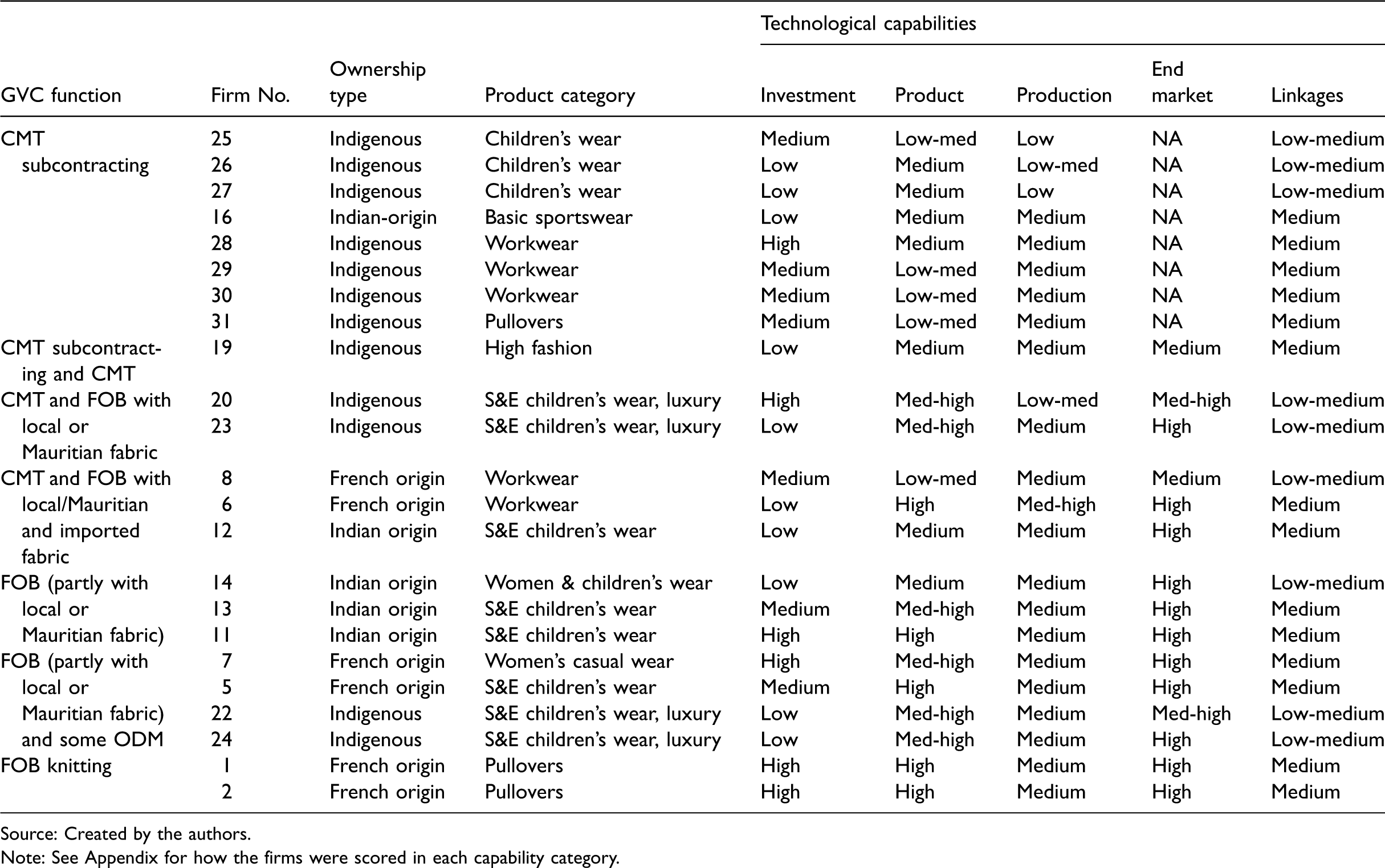

Table 3 summarizes the results from the TC scoring exercise for the 23 local apparel export firms that participated in the survey, grouping firms according to their global value chain function and indicating their ownership type, product category and how high they built their capabilities within each function. Local firms pursued different export strategies that were linked to the product categories in which they specialized: knitted pullovers, children’s clothes with S&E, intermediate and complex workwear, high end and niche fashion. There is a clear correlation between local ownership type on the one hand and export strategy and capability scores on the other hand, which is visually presented in Figure 2. Using the firm survey data and detailed firm histories, this section explains why local firms selected specific export strategies, and how they built capabilities drawing on relational assets from transnational social relations, local assets from artisanal traditions and colonial legacies, and regional assets from proximity to Mauritius.

GVC function, product category and capability scores of local export firms.

Source: Created by the authors.

Note: See Appendix for how the firms were scored in each capability category.

Local firms’ technological capability scores by ownership type.

The first export strategy was specialization in knitted pullovers, and related products such as knitted gloves, hats and scarves. The two directly exporting local pullover firms (Firm 1 and 2) had a large number of stable buyers, and by 2016 had invested in fully automated knitting machines, but outsourced some parts of their production to smaller firms or groups of indigenous Malagasy working with manual machines. Firm 31 is an indigenous Malagasy investor that is trying to take advantage of sub-contracting opportunities for these pullover firms, as well as for Mauritian pullover firms in Madagascar. The owners of Firm 31 invested in a small building, and they acquired secondhand manual machines from the owner of a now closed Hong Kong firm in which they used to be employed. However, the sub-contracting work is seasonal, and Firm 31 produced for the domestic market during the off-season periods, which included infrequent and volatile orders for different products.

Firm 2 also invested in computer design linked to its automated knitting machines in order to produce unique designs for buyers. The owner’s strategy was to achieve a diversified product portfolio that included large orders of basic to intermediate products and smaller orders of more complex products, including very small orders for European luxury brands that included products with labor intensive handiwork such as crochet and embroidery. Firm 1 and 2 had French-origin owners, whose capital investments in automated machines were higher than most of the Mauritian pullover firms working in Madagascar, but parts of the assembly process still required labor-intensive work in sewing the knitted panels together, which slowed down productivity. They had strong linkages with other firms and with the EPZ industry association, but they had low linkages with public sector institutions—which was common across all the local firms.

These French-origin owners had experience working in foreign pullover firms in Madagascar prior to setting up their own firm. The specialization in pullovers is a legacy of Hong Kong investment. Manual knitting of pullovers was the most labor-intensive apparel product, and thus pullover firms were the first to relocate from Hong Kong to Mauritius in the 1970s. The largest Mauritian pullover firm was started in 1972 by a local investor buying a Hong Kong firm that was operating in Mauritius and keeping the Hong Kong staff. Some Mauritian managers at this firm later left to start their own apparel firms in Mauritius. Hong Kong and Mauritian pullover firms began relocating to Madagascar in the 1990s. The owner of Firm 1 was already living in Madagascar with a Malagasy wife and started to work in a Hong Kong factory in 1998 as an accountant. A few years later he and one of the Chinese production managers set up their own firm. The Chinese partner left, and a Dutch investor was brought in, setting up a sales office in Europe. Similarly, the owner of Firm 2 was living in Madagascar with a Mauritian wife, and established a pullover firm in 1995 as a joint venture with a Mauritian firm. He sold his share in that firm and set up his own firm in 1998 with shareholders from Switzerland. The biggest buyer of Firm 2 is a French retailer in children’s clothes that was sourcing in Mauritius, with a buying office there, and then turned to Madagascar and is also an important buyer for several other local firms; the owner of Firm 2 commented that his firm ‘grew up with this client’. In 2000, there were 16 local and foreign knitting factories in Madagascar; by 2018, there were just 6, with these two local firms being among the top in terms of production volume.

The second export strategy, and the one that the most local firms pursued, was specialization in children’s clothes, with two sub-strategies based on the degree of handiwork involved. One group of firms (Firm 5, 11, 12, 13) produced large volumes of intermediate products with S&E, and another group (Firm 20, 22, 23, 24) produced products with more extensive S&E, and often with their own designs, but in small volumes exported by air. The first group was entirely composed of French-origin and Indian-origin owners, and the second group entirely of indigenous Malagasy owners.

The firms producing intermediate S&E children’s products exported to the same group of French buyers with whom they had long-term relations. Madagascar is among the few former French colonies that have artisanal skills in the handiwork that French buyers demand (the only other being Vietnam), and manual S&E cannot be replicated exactly with machines. The high degree of handiwork reduced labor productivity but fetches higher unit prices due to the low number of suppliers globally. However, these buyers tried to create competition in Madagascar in order to reduce unit prices, with one firm owner noting that ‘buyers shop to different firms in Madagascar doing smock and embroidery: they are using us’.

Local firms entered these products with different amounts of prior experience. The owner of Firm 5 had been in Madagascar for several generations. He used to work for the local textile mill as a commercial manager, and in 1999 decided to buy an existing French firm that was producing S&E children’s wear. Notably, the indigenous Malagasy owner of Firm 20 also worked at this French firm and left to start her own firm, bringing one US buyer with her. The owner of Firm 13 was producing plastic products and went into apparel exports in response to demand from a French buyer, but notably he had shares in his brother’s branded apparel retail firm in France (which had an apparel factory in Mauritius) and thus also contacts in the industry. He had the same French buyers for more than twenty years. In general, this group of firms relied heavily on Mauritian production managers, who circulated among them, while the owners managed buyer relations using their social linkages to France.

The second group of firms specializing in luxury children’s clothes with S&E had very small factories that were more like artisanal workshops; the owners started production using parts of their houses. These indigenous Malagasy firms were able to enter apparel exports because they could leverage Malagasy handiwork skills as well as contacts to France to start producing small volumes of French-style children’s wear, selling their own collections to buyers. They operated on a CMT and on a FOB basis: sourcing light woven fabric from Madagascar and Mauritius for summer collections, while clients sent heavier fabrics for winter collections. The owners, all of whom were women, generally had limited experience in manufacturing prior to starting their firms, except for Firm 20, who had experience working in a French firm and later as a buying agent.

The buyers for this product were small boutiques, which limited the order size and the ability of local firms to expand using this export strategy, and thus most of these firms stagnated at a certain level of production. Firm 24 tried to scale up, but in a different product segment (workwear), investing in a large factory, but could not achieve the necessary quality and efficiency, and went back to the old export strategy. Firm 22 succeeded in scaling up in luxury children’s clothes, but then lost her buyers after the 2002 political crisis and again in 2009, and was still trying to rebuild in 2018. Firm 20 was trying to transition from luxury children’s clothes to larger volumes of children’s clothes with less or no handiwork. She invested in a proper factory space, hired a French production manager (that she knew from social networks) to change the production system, and invested in higher efficiency sewing machines, all in order to achieve the efficiency required to be profitable on the lower unit prices of the intermediate products. Thus, the production processes required by the two groups of firms within children’s clothes were very different, and transitioning from one to the other required significant investments and related risks in building production capabilities as well as end-market capabilities to find new buyers.

Both groups of firms producing children’s clothes sourced fabric from the only local fabric mill (Firm 10) when possible. Firm 10 is a vertically integrated woven textile mill and apparel factory, which is part of one of the largest Indian-origin family owned diversified business groups in Madagascar. This family had a woven textile mill in Madagascar, but when the independent government nationalized the mill in the 1970s, the family moved to Mauritius. It slowly took back its factory in Madagascar in the 1990s and then modernized and expanded it. By 2020, it remained the only locally owned mill and the only mill that sold fabric to other firms. The ability to access light weight woven fabric within Madagascar, as well as from fabric mills in Mauritius, led local firms to specialize in summer clothes, mostly for children’s wear but also for women’s wear. Given its mill with the capacity to produce a large number of different fabrics with prints, Firm 10 is the only firm in Madagascar that is able to produce fast fashion products for large European buyers, with Zara as its largest client. While the diversified business group had experience in textile production, Firm 10 entered apparel assembly in the early 2000s through a joint venture with Sri Lankan investors and the sourcing branch of a fast fashion US retailer. These partners left after the MFA phase out and the Indian-origin family assumed full control.

The third export strategy pursued by local firms was specialization in intermediate and complex workwear products on a CMT and FOB basis (Firm 6, 8, 28, 29, 30). Firm 6 specialized in workwear for a particular French buyer after it lost its fast fashion clients due to the 2002 political crisis. While it gained other workwear buyers and also produced a particular type of children’s wear for a French buyer, it forged a long-term relationship with the original French workwear buyer. This eventually led the buyer to buy shares in the firm when the other French shareholder exited, resulting in 50 percent ownership. Firm 6 produced on a CMT basis for this buyer, but on a FOB basis for the other buyers, holding a large inventory of fabric for repeat orders. This firm was one of the first apparel export firms established in the early 1990s. The current French immigrant owner had worked for Firm 10 as a mechanic and started the firm together with another French immigrant that had been producing clothes for the domestic market and who provided financing and two partners in France who were in charge of finding buyers.

The French partners left early on, and Firm 6 expanded gradually and built high capabilities in product, production and end-markets capabilities over time, initially drawing on foreign experts from Hong Kong and Mauritius. When asked about how he learned apparel production, the owner said ‘production is 5 percent technique and 95 percent organization’, and that he personally sought solutions to the organization of production, ‘but there are now people in my factory able to find solutions, other than me’. Deciding not to expand further due to diseconomies of scale, the owner supported some of his indigenous Malagasy managers (all women) to start their own firms by providing financial assistance to buy machines and providing orders through sub-contracting (Firm 28, 29, 30). The owner of Firm 30 worked in Firm 6 for twenty years, moving from a sewing machine operator up to production manager, and since 2014 worked at Firm 6 while also establishing her own firm. She bought land in 2019 and began building a larger factory in order to export directly to buyers accessed with the help of Firm 6.

The fourth export strategy of local firms was specialization in high end and niche fashion products (Firm 7, 19). The owner of Firm 7 is part of a large French-origin family company with another apparel firm in children’s wear (Firm 4); the French family settled in Madagascar in the 1990s. Firm 7 was set up in order to produce women’s wear for the main buyer of Firm 4, and bought an existing factory owned by an Indian-origin family. Firm 7 and 4 have a sales office in France, and Firm 7 produces women’s summer clothes with its own design collections, at the demand of its buyers, using fabric sourced from Madagascar and Mauritius. Firm 19, with an indigenous Malagasy owner, started in high-end fashion products driven by its early buyers. The owner of Firm 19 was supported at the beginning by the owner of Firm 6, who encouraged him to enter the sector and put him in touch with French firms operating in Madagascar that provided sub-contracting opportunities that later led Firm 19 to produce designer jackets for Moncler. Firm 19 exported small orders of high end products and supplemented this with sub-contracting for local and foreign firms. The firm aimed to expand order size, but struggled to shift its export strategy into different product areas.

Several other indigenous Malagasy investors remained in sub-contracting positions producing children’s clothes for foreign and local firms (Firm 25, 26, 27). Most of them had experience and some tacit knowledge because they had worked in foreign firms or high capability local firms, but they had limited financial capital and social networks with which to find and maintain direct buyers. This point becomes clear in the recent experience of Firm 16, whose Indian-origin owner bought a factory in 2012 from a Hong Kong firm. The owner had been importing secondhand clothes and had several other businesses, which were part of a family diversified business group. The owner failed in the first years of trying to run an apparel export firm and eventually hired a Mauritian manager, who had worked at a foreign firm in Madagascar, to reorganize the production systems and brought in a South African partner who had worked in apparel retail to take over buyer relations and open a sales office in the US. Making such moves required finance and social contacts and networks that indigenous Malagasy investors do not have. Firm 16 was the only local firm trying to export sportwear for the US market, the product category that the Mauritian manager had been producing in the foreign firm. Exporting this product category is more difficult for local firms, as they cannot leverage local and regional assets to carve out a niche and thus reduce competition from other apparel supplier countries, but rather benefit from preferential market access under AGOA. Firm 14 tried to produce basic products in ladies’ casual and sleepwear for European buyers, but could not compete with Bangladesh and China and had to switch to children’s clothes.

Conclusion

Local investors in Madagascar were able to leverage relational, local and regional assets to enter and upgrade in apparel global value chains, building technological capabilities linked to specific export strategies. The presence of foreign apparel firms offered possibilities to learn, but transnational social relations explain why specific local firms could leverage foreign firms’ presence (and others not). Immigrant French-origin and Indian-origin local investors formed connections with specific types of foreign supplier firms - French, Mauritian and Hong Kong investors – and European buyers that could be leveraged to start local export firms and build capabilities. As the local firm cases show, these social relations were leveraged in a variety of ways, including joint ventures with Mauritian investors, buying out existing French firms, and partnering with Hong Kong investors and with a range of French shareholders that straddled France and Madagascar. In addition to relational assets, local firms were able to leverage a local asset in the form of artisanal handicraft skills and capitalize on (largely French) buyers’ demand for children’s clothes with labor-intensive S&E handiwork that are characterized by less competition and higher unit values. This also allowed indigenous Malagasy firms to enter apparel global value chains by producing small volumes of high value products. However, given the small volumes in this niche product, local firms that wanted to expand needed to ‘downgrade’ to intermediate children’s wear products and upgrade their production processes. In contrast to Indian- and French-origin firms, indigenous Malagasy firms lacked the finances to pay Mauritian managers that had the requisite production knowledge. Proximity to Mauritius provided important regional assets that local firms could draw upon, including a pool of experienced production managers, access to textile and other inputs, and the regional relocation of Mauritian and Hong Kong firms as well as European buyers that had been sourcing from Mauritius. Finally, sub-contracting for foreign firms and high capability local firms was an important way for indigenous Malagasy and also some Indian-origin firms to enter apparel global value chains, but only a few of these firms progressed to direct exports.

Despite the important number of local firms that have built capabilities and upgraded compared to other SSA low-income apparel export countries, the apparel export industry in Madagascar faces critical limitations in terms of industry expansion and the broader benefits from apparel global value chain participation for industrialization. In addition to the limits to expanding production of niche products based on unique local assets, local firm participation based largely on relational assets keeps many local investors from entering, as they do not have these assets. Furthermore, the supply chain within Madagascar had stagnated, particularly in terms of textile production. The Madagascar government announced a plan in 2017 to create a Textile City industrial zone—a plan put forward by Mauritian firms operating in Madagascar. After several years without action, the Mauritian government took over the initiative in 2019, announcing that it would finance and build the Textile City. 12 This could allow more local firms to enter by increasing local textile production and thus making access to inputs easier, reducing lead times and expanding the range of profitable export strategies. However, the extent to which the Mauritian government can drive this kind of industrial policy in place of the Madagascar government remains to be seen.

The case of Madagascar’s apparel export sector demonstrates the complexities and unevenness with which local export firms have built technological capabilities linked to specific export strategies and related upgrading paths. By drawing on the TC literature and making the capabilities behind upgrading (and downgrading) the focus of the analysis, the article shows that export strategies linked to specific product categories require building particular types of capabilities and are related to specific functions in global value chains. The article not only assessed which capabilities were built by local firms, but also how and why firms chose specific export strategies and were successful in them or not. Reinforcing the call by Morris et al. (2016) that ownership matters, the article explains how different types of local ownership influenced the intra-firm resources that firms were able to access in building capabilities as well as their ability to leverage relational, local and regional assets. Relational assets were particularly important for accessing tacit knowledge by building linkages to specific types of foreign supplier firms and buyers. Such social relations between firms take place within global value chains and their dynamics, but are also shaped by the history of social relations, economic activities and geographical legacies that exist in local places. Thus, the specificities of local places and their regional context are equally crucial in explaining the strategies, actions, opportunities and constraints of local supplier firms, as well as those of foreign supplier firms and buyers. This highlights the importance of the conjunctural approach by Pickles and Smith (2016), arguing that global value chains are embedded in systems and networks of social relations, specific cultural histories, and regional economic formations.

Supplemental Material

sj-pdf-1-epn-10.1177_0308518X20961105 - Supplemental material for Local supplier firms in Madagascar’s apparel export industry: Upgrading paths, transnational social relations and regional production networks

Supplemental material, sj-pdf-1-epn-10.1177_0308518X20961105 for Local supplier firms in Madagascar’s apparel export industry: Upgrading paths, transnational social relations and regional production networks by Lindsay Whitfield and Cornelia Staritz in EPA: Economy and Space

Footnotes

Acknowledgements

We wish to thank Gerald Jaonary for providing research assistance in Madagascar and Bernhard Tröster for support with trade data. Further, we thank all interview partners in Madagascar and Mauritius for the time they took to discuss with us the dynamics of the apparel sector in their country and the firms’ history and experiences. Lastly, we also thank the journal editors and the three anonymous reviewers for their very useful comments.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was financed by the Danish Council for Independent Research in the Social Sciences, grant number DFF 4182-00099.

Notes

Supplemental material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.