Abstract

In the introduction to the first-ever special issue on the spatial dimensions of FinTech, we show that despite a FinTech fever in business and media, research on FinTech is still niche, particularly in social sciences. We describe FinTech as a research area full of controversies, ripe and in need of geographical research. As we outline, papers in this issue contribute to the debate primarily by examining the role of the state, financial centres and uneven development in FinTech.

FinTech fever

Finance has always relied on and co-evolved with technology. Finance, after all, is a social technology, based on a system of recording assets and liabilities (credits and debits), which has developed through a series of innovations from coins, through to bills of exchange, double-entry book-keeping, insurance and central banking, all the way to financial derivatives and high-frequency algorithmic trading (see e.g. Ingham, 2004). In the process, the financial sector has been a most savvy user of information and communication technology. However, something special happened to the relationship between finance and technology a little over a decade ago. In March 2007, Vodafone Group and Safaricom in Kenya launched M-Pesa, a service allowing users to deposit, withdraw, transfer money, pay for goods and services and access credit and savings with a mobile phone, without a bank account (Ndung’u, 2018). In January 2009, Japanese inventor Satoshi Nakamoto launched Bitcoin, a cryptocurrency based on blockchain technology, a system that keeps track of transactions without relying on any central authority (Zook and Blankenship, 2018). What was special about both of these financial innovations was their major, large-scale implications, and that they did not come from the financial sector.

M-Pesa, Bitcoin and blockchain were accompanied and followed by many other financial innovations in a wide range of areas, from payments and peer-to-peer lending, through crypto-assets and robo-advisors, to regulatory technology. Thousands of start-ups, funded by tens of billions of US dollars, focused on such innovations and have sprung up around the world in developed, emerging and developing economies. To be sure, financial firms and big technology companies have played a big part too. What helped ignite the development of FinTech around 2008 was the global financial crisis, which damaged the reputation of banks and unleashed a lot of human and financial capital looking for new opportunities. In June 2007, Apple launched the iPhone, ushering in a new era of smartphones, with unprecedented computing power and connectivity. Meanwhile, Apple and other tech giants from the USA and China have been championing the platform business model, gaining billions of consumers, with millennials in the lead (Kenney and Zysman, 2020). In sum, just over a decade ago, technology, business models, talent, capital and consumers were all ready to start a FinTech fever. Governments have contributed to it as well, encouraged by the prospect of improving financial inclusion and competition in financial services. As the Economist (2015) pronounced, ‘a wave of startups is changing finance—for the better’. Findexable, a company charting FinTech development, has referred to it as “the electricity of the global digital economy – making connections, and finding the path of least resistance to make it easier, cheaper, (dare-we-say it fairer?), to transact (…)” (Findexable, 2020: 8).

The guest editors of this special issue became interested in FinTech through their interactions with finance practitioners. In December 2014, for example, we discussed the impact of FinTech developments on financial centres with a group of financiers, consultants and corporate lawyers in Sydney. The idea of a special issue was conceived in 2017. According to the Web of Science, the first peer-reviewed articles on FinTech (defined as those featuring the term in the title, abstract or keywords), appeared only in 2015 (e.g. Zhou et al., 2015). At the end of 2017, there were 64 published articles on FinTech, including one in Environment and Planning A (Langley and Leyshon, 2017). By the end of June 2020, as this editorial was being written, the number had risen to 397, including literature review papers (e.g. Gomber et al., 2018). Over 90% of the papers were published in three research areas: business economics (61%), computer science (16%) and government and law (15%). Half of the authors are affiliated with institutions in the USA (22%), China (including Hong Kong) (16%) and the UK (12%), followed by Australia (9%), Germany (7%), South Korea (7%) and Italy (6%). Mainstream economics has been remarkably slow at engaging with FinTech. In the top three journals in economics (Econometrica, American Economic Review and Quarterly Journal of Economics) there is not a single mention of FinTech, while in the leading three journals in finance (Journal of Financial Economics, Journal of Finance and Review of Financial Studies) there are only three traces: a special issue in the Review of Financial Studies (Goldstein et al., 2019) and two articles in the Journal of Financial Economics. In keeping with the feverish character of FinTech, and the style of publishing championed by business schools, much research on the topic appears first in the form of working papers, with leading articles attracting tens of thousands of downloads on the Social Science Research Network (see, e.g. Arner et al., 2015). Think tanks and consulting firms are busy publishing reports on FinTech, sometimes in collaboration with universities (e.g. CCAF and EY, 2019).

At the end of June 2020, there were 10 papers with a FinTech topic classified by the Web of Science as published in the broadly defined research area of geography. While the number is small, this puts geography ahead of international relations, development studies, sociology or political sciences. Out of the 10 papers, five were published in the Environment and Planning A, including three papers in this special issue that were already available online at the time of writing this editorial, plus Bernards (2019) and the aforementioned Langley and Leyshon (2017). Three were published in Geoforum (Boamah and Murshid, 2019; Haberly et al., 2019; Zook and Blankenship, 2018), one in European Planning Studies (Cooke, 2019) and one in Tijdschrift voor Sociale en Economische Geografie (Wójcik and Ioannou, 2020). We could add to the ten a paper on crowdfunding published in Economic Geography by Langley (2016), although it does not use the term FinTech in the topic. Of course, geographers have published in other, not necessarily geography-focused, journals (e.g. Grabher and König, 2020; Langley and Leyshon, 2020), and geographical dimensions of FinTech have been illuminated in works by authors whose main affiliation is not geography (e.g. Gabor and Brooks, 2017; Gruin and Knaack, 2020). There is undoubtedly much research in the pipeline, including two articles in Progress in Human Geography (Lai and Samers, 2020; Wójcik, 2020b). Geography and geographers have certainly demonstrated an ability to engage with FinTech as a new topic.

The goal of this guest editorial is to introduce the first ever special issue devoted to FinTech and geography. As we indicated previously, FinTech research is fashionable but still niche. Mainstream literature is only waking up to its challenges and has not yet come to terms with its significance. In this special issue, we hope to demonstrate that the time to wake up is now, and there is potential for geography and geographers to contribute to the debate on the nature and implications of FinTech is immense. In the following section, we show that FinTech is full of controversies, all ripe and begging for geographical research. In the last section, we briefly preview the four papers in this issue, showing how they have dealt with some of these controversies in terms of theory and methodology and with what empirical results.

FinTech controversies

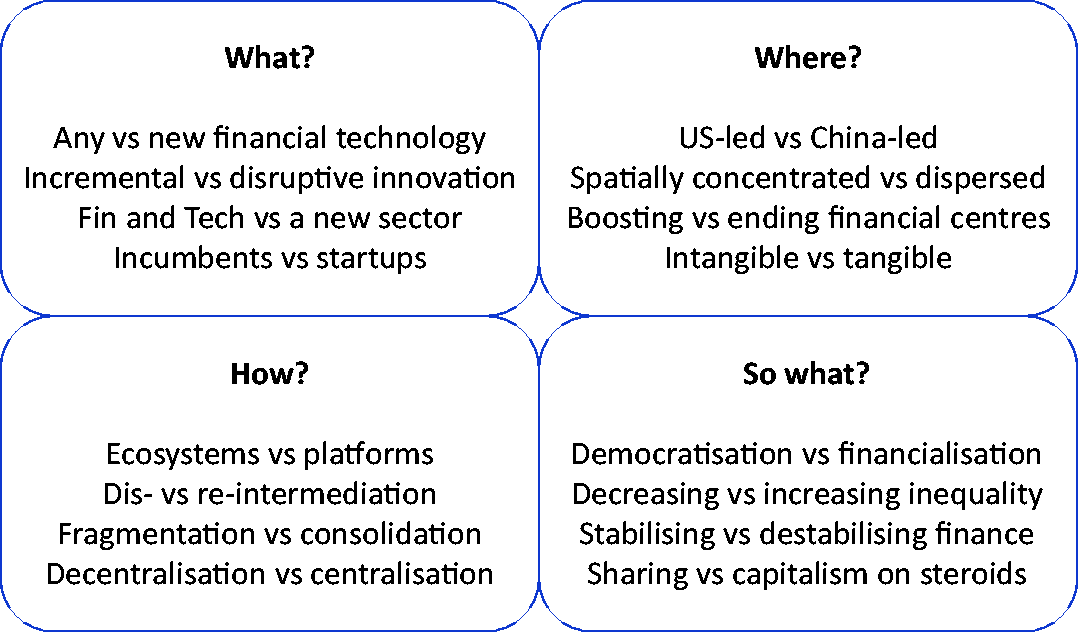

FinTech is nothing if not controversial. To sharpen readers’ interest in this special issue, and research on FinTech in general, we identify 16 important controversies and classify them loosely under four headings: what, where, how and so what (Figure 1). To be clear, while some use the form Fintech or fintech, we prefer FinTech, as to us it better highlights the combination of finance and technology.

Selected FinTech controversies.

The debate on FinTech starts with the very definition of the phenomenon. Arner et al. (2016: 22) refer to FinTech as ‘the use of technology to deliver financial solutions’, while Schueffel (2016: 45) defines it as ‘a new financial industry that applies technology to improve financial activities’. So what is FinTech? Is it about any financial technology, with the developments of the last dozen years or so representing the latest stage of FinTech, or is it just about new technologies? Do technologies have to be disruptive rather than just incremental to belong to FinTech? How does FinTech differ from online, digital or internet finance? If it is a new economic sector, does it go beyond startups focusing on FinTech and cover parts of financial and technology industries? Definitional issues surrounding FinTech are so acute that Dorfleitner and Hornuf (2016: i) state bluntly that ‘a general definition of FinTech is not possible’. However, avoiding this issue is not an option, and definitional choices have to be made (and debated) for research on FinTech to progress both theoretically and empirically. It is notable that, to the best of our knowledge, FinTech is not yet recognised as an industry by any international industrial classification (Wójcik, 2020a).

With definitional issues far from settled it is difficult to measure and map FinTech. While research focusing on startups and venture capital investments highlights the US leadership in FinTech, studies focusing on funds raised through broadly defined peer-to-peer lending, and including FinTech activities of big technology firms, show the dominance of China. CCAF (2018), for example, ranks Beijing, Shanghai, Hangzhou and Shenzhen among the seven leading global FinTech hubs (next to San Francisco, New York and London). In contrast, in their ranking, Findexable (2020) does not show a single PRC city in the top 20 and paints FinTech as a spatially dispersed industry, creating new hubs away from established financial centres. Interviewing professionals related to FinTech we often hear that FinTech will not so much re-write the history of financial centres, as write financial centres into history, enabling the provision of financial services from anywhere to anywhere. This brings back the ‘end of geography’ thesis, calling for research on the geography of both intangible and tangible components of FinTech. After all, code, artificial intelligence and blockchain all require hardware, energy, infrastructure and people (e.g. Zook and Blankenship, 2018).

Another group of questions fraught with controversy is how FinTech works and how it can be conceptualised. Platforms and ecosystems seem to be the most common conceptual descriptions of FinTech, in both academic and grey literature, but how they relate to each other is not very clear (Grabher and König, 2020). For some, FinTech is underpinned by the logic of disintermediation, seemingly exemplified in peer-to-peer lending, but others stress the reality of powerful platform companies as evidence of re-intermediation (Langley and Leyshon, 2020). Related to that, while myriads of FinTech startups may imply unbundling and fragmentation in financial services provision, economies of scale and scope inherent to platforms may result in consolidation and re-bundling of services (ibid.). Witness, for example, the spectacular growth of Blackrock taking advantage of platform economies in asset management (Haberly et al., 2019). As such, FinTech epitomises the clash of the cyberlibertarian vision of power decentralisation, as exemplified by Bitcoin, with the centralisation of power, as illustrated with the social credit system, being developed by Chinese tech giants in collaboration with the government (Gruin and Knaack, 2020).

Governance issues take us to questions on the broader developmental impacts of FinTech. Particularly in developing countries, FinTech is promoted under the banner of financial inclusion and democratizing finance (Blakstad and Allen, 2018). However, others see it as digital financialisation (Gabor and Brooks, 2017), with finance (and capitalist social relations) penetrating society and life ever more widely and deeply, with potential negative consequences for inequality. Financial stability may suffer as well as a result of FinTech enlarging debt markets and accelerating financial flows. On the other hand, its innovations may improve the pricing of risk and technology used for regulation and supervision of financial markets (Carney, 2017). The significance of these debates cannot be underestimated. It is about the constructive potential of FinTech to contribute to a more sharing and inclusive economy versus its destructive power to create a capitalism on steroids (Grabher and König, 2020).

Papers in this issue

Papers collected in this special issue all contribute to the controversy-ridden debates on FinTech, but with important differences and similarities. The thematic and geographical focus ranges from a broadly defined FinTech sector in Brussels (Hendrikse et al.) and London (Sohns and Wójcik), through initial coin offerings (ICOs) in Germany (Zook and Grote), to FinTech lending and payments in refugee camps in Kenya (Bhagat and Roderick). All papers use qualitative methods, including case studies, interviews, participant observation, and a critical analysis of media and policy documents.

Theoretical approaches utilised in the issue differ. Bhagat and Roderick (2020) apply a racial political economy approach, which helps to investigate exploitation, expropriation and exclusion of refugees facilitated by FinTech. In doing so, the authors show the importance of race to the concept of financial-philanthropy-development complex coined by Gabor and Brooks (2017). Zook and Grote (2020) analyse ICOs as a process of financialisation to be understood through the notions of catalysts, cracks and voids. The cyber-libertarian ideology, blockchain technology and capital availability serve as catalysts used by managers and entrepreneurs to crack open the relationships between clients and services. In the process, they also take advantage of voids, created by missing regulation. The remaining two studies are grounded in evolutionary economic geography and focus on FinTech ecosystems. Sohns and Wójcik (2020) explain the challenge of Brexit to London’s FinTech industry conceptualised as an entrepreneurial ecosystem, emphasizing the role of human capital, finance, markets and government and non-government support and policy. Hendrikse et al. (2020: 17) propose a new analytical concept of the Fin-Tech-State triangle to explore tensions in strategic coupling among the three groups of actors.

All four papers offer important empirical findings. While acknowledging the positive impacts of FinTech on development in Kenya, Bhagat and Roderick (2020: 1) show that “processes of financial inclusion carried out by and through fintech are still distinguished largely by exclusion”. More specifically, Somali refugees and their camps are excluded, and those included have to show ability to be entrepreneurial, which is determined by ability to repay debt. Fintech firms profit in the process. Hendrikse et al. (2020) show how banks dominate FinTech in Brussels, and how law and consultancy firms participate in the ecosystem as well. This leads them to conclude that “For despite the ongoing surge in digitisation, and notwithstanding the threat of Big Tech to established finance, the emerging geography of Fintech is likely to remain anchored in a global network of financial centres in which new specialisations and niches specific to Fintech will be integrated” (2020: 19). Sohns and Wójcik (2020) suggest that although London’s FinTech showed resilience and continued to attract talent and new firm formation, the uncertainty facing the sector ahead of Brexit was significant. This was because of the role of anchor firms in the ecosystem, including financial services incumbents, and the potential domino effect that their relocations could have on FinTech firms. Zook and Grote (2020) demonstrate the significance of financial centres for FinTech in yet another way, by discussing how ICOs shifted from countries like the USA and Switzerland to offshore jurisdictions with the Cayman Islands and the British Virgin Islands in the lead.

Put together, papers in this special issue showcase the potential to explore the spatiality of FinTech and its implications. They do so by highlighting the role of location, place, space, scale, heterogeneity and uneven development. Scales examined in these papers range from racialised bodies, through firms and their collections to the state and international organisations. Readers of this issue will hopefully find motivation to build on these contributions and advance research on FinTech. While papers collated here rely on qualitative data, quantitative data is becoming available, offering potential for quantitative and mixed-methods approaches (CCAF, 2018; Findexable, 2020). The timing of this issue should serve as further encouragement. On the one hand, COVID-19 and the resulting recession mean that FinTech start-ups may struggle with access to funding. On the other hand, the pandemic has weakened incumbent financial institutions and accelerated the uptake of digital financial services among consumers. Less in-person and more online finance may also be seen by governments as a way to make their economies and societies more resilient to future pandemics (Wójcik and Ioannou, 2020). It is clear that we are living in an important moment for FinTech.

Footnotes

Acknowledgments

Early versions of the special issue papers were presented at the Fifth Global Conference on Economic Geography in Cologne in July 2018, where we benefited from comments by Paul Langley, Andrew Leyshon, Christopher Murphy and Fenghua Pan among others.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Dariusz Wójcik would like to acknowledge funding from the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation programme (grant agreement number 681337). The article reflects only the authors’ views and the ERC is not responsible for any use that may be made of the information it contains.