Abstract

This paper analyses how different entrepreneurial actors respond to political uncertainty and changing institutional settings. Moreover, it discusses the impact of those actor-level responses on the resilience of entrepreneurial ecosystems (EEs), focusing on how they affect the diversity of and the connectivity among its actors. To address these questions, the paper examines how the decision of the United Kingdom to leave the European Union has influenced the financial technology (FinTech) industry in London, applying data collected from in-depth interviews, covering different groups of stakeholders in London’s FinTech industry, such as angel investors, banks, legal advisers, lobby organizations and private companies. Our results show that political uncertainty and the prospect of institutional change can trigger actor-level responses, which have the potential to modify the diversity as well as the local and non-local connectivity of an EE. Moreover, we demonstrate that the nature of strategic responses of entrepreneurial actors varies significantly, depending on their firms’ characteristics, such as age, size, product specialization and the structure of their egocentric networks. With regard to the latter, our results show that anchor firms play an important role in other firms’ egocentric networks and have the power to shape their strategic responses.

Introduction

The Fourth Industrial Revolution has profoundly changed the way of doing business during the last decade. In the process, new technologies, such as mobile internet, big data, artificial intelligence, and machine learning have become increasingly important for today’s economy. Existing research has shown that in times of deep technological change regional economic prosperity depends strongly on the dynamic development of entrepreneurial activities, with the entrepreneur as the driving agent (Florida, 2003; Malecki, 1997). Consequently, attracting potential entrepreneurs and supporting growth-oriented entrepreneurship have become key concerns of regional economic policy.

London is one of the world’s most dynamic entrepreneurial cities. Its success has been driven by highly educated entrepreneurial individuals from all over the world who choose London to start and expand high value-added, technologically dynamic businesses. London has been able to attract domestic and foreign talent due to numerous characteristics, including a relatively liberal and diverse population, a dynamic job market and an advantageous regulatory framework (Nathan and Vandore, 2014). One of the biggest, if not the biggest, success stories of London’s entrepreneurial ecosystem (EE) in the last decade is the development of London into one of the world’s leading financial technology (FinTech) hubs, hosting 25 of Europe’s 50 most successful FinTech companies (FinTechCity, 2018). However, London’s leading position cannot be taken for granted, as FinTech is a relatively young industry and London competes in this area with other FinTech hubs, including New York, Silicon Valley and Singapore (Ernst and Young, 2016).

The result of the EU referendum held on 23 June 2016 unleashed a series of developments, referred to as ‘Brexit’ for short, including the UK’s formal withdrawal from the European Union (EU) on 31 January 2020 and the end of the transition period currently agreed for 31 December 2020. This process is redefining the UK’s relationship with the rest of Europe and the world at large. It is a process characterized by a high level of uncertainty regarding its outcomes, which can impede the strategic decisions of economic actors and, as a consequence, influence the development of the EE in the UK, including London.

Although the EE concept has attracted increasing attention in policy circles (Mason and Brown, 2014), it has also raised concerns due to a lack of conceptual rigour and a clear analytical framework (Stam, 2015). In this regard, Alvedalen and Boschma (2017) identify several shortcomings of the EE concept, such as a lack of focus on the importance of and connections between different entrepreneurial actors; the evolution of these connections in times of institutional change; and references to the network literature concerning the relative importance of non-local versus local linkages, egocentric networks, diversity and connectivity. So far, empirical studies have mainly highlighted the key components of numerous successful EEs (e.g. Isenberg, 2011; Klingler-Vidra et al., 2016; Spigel, 2016). In order to understand the dynamics of EEs, however, it is essential to go beyond success stories (Auerswald, 2015). In order to address these gaps in the literature, we regard EEs as complex adaptive systems in which micro-level activities are shaped by macro-level patterns (Martin and Sunley, 2007), while macro-level structures evolve as a consequence of the behaviours of the actors involved and the interactions among them (Pavard and Dugdale, 2006). Therefore, we do not only focus on the key components (actors) of London’s EE, but also on the interdependencies between them (Eisenhard and Piezunka, 2011). In this regard, we consider studying the impact of Brexit on London’s FinTech industry an important case investigating how entrepreneurial actors with different firm characteristics and egocentric network structures (Stuart and Sorenson, 2005) react to uncertainty and disruption caused by institutional and political change. Discussing the potential effects of such actor-level responses on the diversity of and the connectivity among actors of London’s EE allows us to draw inferences about its resilience (Boschma, 2015; Martin and Sunley, 2007; Pike et al., 2010).

The remainder of the paper is organized as follows. The second section introduces the conceptual framework, while the third section explains the case study design and methodology. The fourth section presents and discusses empirical results, with the final section drawing conclusions and implications.

Theoretical background

Entrepreneurship is a complex concept that can be studied using different approaches. In the creation-based approach, entrepreneurship is simply defined as the start-up of a new venture (Gartner and Carter, 2003), while in the innovation-based approach, entrepreneurship is understood as the innovative creation of new products or new ways of doing business (Schumpeter, 1934). Entrepreneurship is practised by entrepreneurs who are individuals exhibiting innovative capabilities that allow them to explore ‘opportunities to discover and evaluate new goods and services and exploit them’ (Stam and Spigel, 2017: 1). Here, three different types of entrepreneurs can be distinguished: potential entrepreneurs, early-stage entrepreneurs and owner-managers of established businesses, typically defined as those older than 3.5 years (Singer et al., 2015). Potential entrepreneurs are defined as individuals who have personal characteristics that allow them to start a new venture, such as risk-taking propensity and proactivity (Krueger and Brazeal, 1994). Early-stage entrepreneurs include nascent entrepreneurs, who are actively engaged in creating a new business (Wagner, 2004), as well as owner-managers who run a start-up younger than 3.5 years (Singer et al., 2015). While during its early stage the entrepreneurial process is a sequence of actions associated with identifying and evaluating perceived opportunities and accumulating resources necessary for the successful formation of a new venture (Cooney, 2005), the process of entrepreneurship becomes a cyclical progression of opportunity-targeting and strategic decision-making concerning the allocation of scarce resources once the business is established (Glancey, 1998). In this regard, the entrepreneurial process is not only based on the innovation capacity of the founder and/or manager but is also linked to entrepreneurial employees who develop new activities, such as new goods or services, or set up new business units within their company (Cooney, 2005).

Entrepreneurial ecosystems and evolutionary economic geography

Initially promoted by Isenberg (2011) in the business management literature, the EE concept incorporates several themes from earlier literature on entrepreneurship, clusters and innovation systems. While entrepreneurship research focuses on the characteristics and functions of entrepreneurs, cluster research focuses on the general geographic concentration of interconnected companies and institutions in a specific place (e.g. Gordon and McCann, 2000; Martin and Sunley, 2003; Porter, 1998), whereas research on innovation systems analyses the contribution of different agents in the generation and diffusion of knowledge and innovation at different spatial levels (e.g. Asheim and Isaksen, 2002; Cooke, 2002; Cooke et al., 1997; Freeman, 2004; Fritsch, 2001). Although some aspects discussed in the literature on clusters and innovation systems help to understand why some places are persistently more entrepreneurial than others, the links in the entrepreneurship literature remain implicit (Acs et al., 2014). The EE concept combines these different strands of literature by explicitly focusing on the unique needs of start-ups and innovative high-growth companies, as well as the place-specific components and interactions required (Mason and Brown, 2014). EEs can be defined as ‘a set of interconnected entrepreneurial actors (both potential and existing), entrepreneurial organizations (e.g. firms, venture capitalists (VCs), business angels, banks), institutions (universities, public sector agencies, financial bodies), and entrepreneurial processes (e.g. the business birth rate, number of high growth firms, number of social entrepreneurs (…)) which formally and informally coalesce’ (Mason and Brown, 2014: 5) in a way that creates and maintains a dynamic, cumulative local process of entrepreneurship.

From a theoretical perspective, the EE concept is also strongly linked to evolutionary economic geography (e.g. Martin and Sunley, 2007; Pavard and Dugdale, 2006; Pendal et al., 2009), which regards economic ecosystems as complex adaptive systems, in which macro-level structures evolve as a consequence of the behaviour of the actors involved and the interactions among them (Pavard and Dugdale, 2006). At the same time, micro-level activities are shaped by macro-level patterns (Martin and Sunley, 2007). Consequently, disturbances arising from shifting external and internal conditions can impact the evolution of an economic ecosystem (Cadenasso et al., 2006). Typically, economic ecosystems evolve slowly over time (Stam, 2010). However, they can also change abruptly due to fundamental events (Pendal et al., 2009). As economic ecosystems are non-linear self-organizing systems, fundamental events can change the characteristics of an economic system in an unpredictable and irreversible way (Martin and Sunley, 2007; Pavard and Dugdale, 2006). Due to path-dependency, there is the risk that such changes become embedded in the economic system and hamper its future evolution (Levin, 1998). In contrast, the capacity of an economic ecosystem to resist, recover from, reorganize and renew in the face of fundamental events is defined as resilience (e.g. Boschma, 2015; Hassink, 2010; Simmie and Martin, 2010).

The resilience of an economic ecosystem is strongly linked to certain network features, such as diversity and connectivity (Martin and Sunley, 2007; Pike et al., 2010). According to Metcalfe (2005), the entrepreneurial diversity of an economic ecosystem, which is defined as the degree to which an economic ecosystem contains a broad variety of entrepreneurial agents (entrepreneurs, mentors, talents, investors) and venture types (size, age, business model), is seen as a critical factor. Moreover, the connectivity of an economic ecosystem, which concerns the connections between elements in an EE, is seen as another critical factor. Following Spigel and Harrison (2017), resilient EEs are characterized by high entrepreneurial diversity. Therefore, their ability to attract external actors, while preventing their loss through outmigration or failure, is crucial for the resilience of the EE. In addition, resilient EEs are also characterized by actors’ ability to create and maintain internal and external ties, which increases actor connectivity and, consequently, fosters knowledge exchange and the recycling of resources (Boschma, 2015). In contrast, weakened EEs are characterized by the loss of actor connectivity, a decline in the inflow of entrepreneurial actors, increasing outmigration of entrepreneurial actors and business failure (Spigel and Harrison, 2017).

While entrepreneurs are regarded as the core actors in building and sustaining the EE (Acs et al., 2014), they are complemented by other actors with whom they are connected directly and indirectly through customer–supplier relationships and strategic alliances, forming their egocentric networks (Stuart and Sorenson, 2005). Egocentric networks concern the functions and compositions of network ties around a specific actor and thereby help to explain how firms’ patterns of interaction provide access to different types of resources and shape actor-level outcomes, such as strategic responses (Provan et al., 2007). According to Isenberg (2011), the actors of an EE can be divided into six domains: policy, finance, culture, support, human capital, and markets. The domain of markets covers the availability of sophisticated customers, who are willing to experiment and adapt to new products and services, as well as access to international markets (Isenberg, 2011). A systematic decrease in their demand can lead to a shrinking market size and weaken the EE (Martin et al., 2019). Finance involves access to funding, such as bank loans, angel investors and venture capital, as well as related financial services (Isenberg, 2011). While access to loans is seen as being more important in the start-up phase, venture capital is considered more important for scaling up (Motoyama et al., 2013). Without sufficient access to loans and venture capital, the EE is likely to stagnate or decline (Feldman et al., 2005). The domain of policy involves the availability of public sector advocates who are willing to promote entrepreneurship, as well as the government’s provision of legal and regulatory frameworks for entrepreneurial activity (Isenberg, 2011). The domain of support covers the availability of non-governmental institutions, such as entrepreneurship associations; support professionals, such as legal, accounting and technical experts; and infrastructure, such as internet and transport (Isenberg, 2011). Human capital concerns the availability of experienced entrepreneurs who can act as mentors and serial entrepreneurs (Feldman, 2001), skilled labour and higher education institutions, such as universities (Isenberg, 2011). Following Menefee et al. (2006), it can be assumed that access to human capital positively affects business performance. Moreover, a culturally heterogeneous labour force is seen as beneficial, as it expands the local variety of ideas, knowledge and skills (Rodríguez-Pose and Hardy, 2015). Finally, the domain of culture concerns the attitude towards entrepreneurship and involves the visibility of success stories, international reputation and societal norms, such as tolerance of risk, mistakes and failures; creativity and experimentation; and the social status of entrepreneurs in society (Isenberg, 2011). A positive attitude towards entrepreneurship is assumed to increase the willingness of potential entrepreneurs to take the risk associated with innovative entrepreneurship (Fritsch and Storey, 2014).

In the EE literature, there is an ongoing debate on the role of anchor firms (e.g. Feldman et al., 2005; Johns, 2016), which are large established firms with significant capital endowment, as well as technological and organizational skills. They are considered key players in all domains of EEs due to their ability to attract international talent, produce spin-offs, provide business infrastructure and act as customers and investors (Feldman et al., 2005). In addition, anchor firms act as brokers (Morrison, 2008), linking local EEs with international markets and global knowledge networks (Johns, 2016). Due to direct and indirect connections, start-ups and innovative high-growth firms develop in co-evolution with anchor firms (Johns, 2016). Hence, it can be assumed that changes in the operations and strategies of anchor firms have a potential impact on entrepreneurial actors interlinked with them.

Conceptual framework

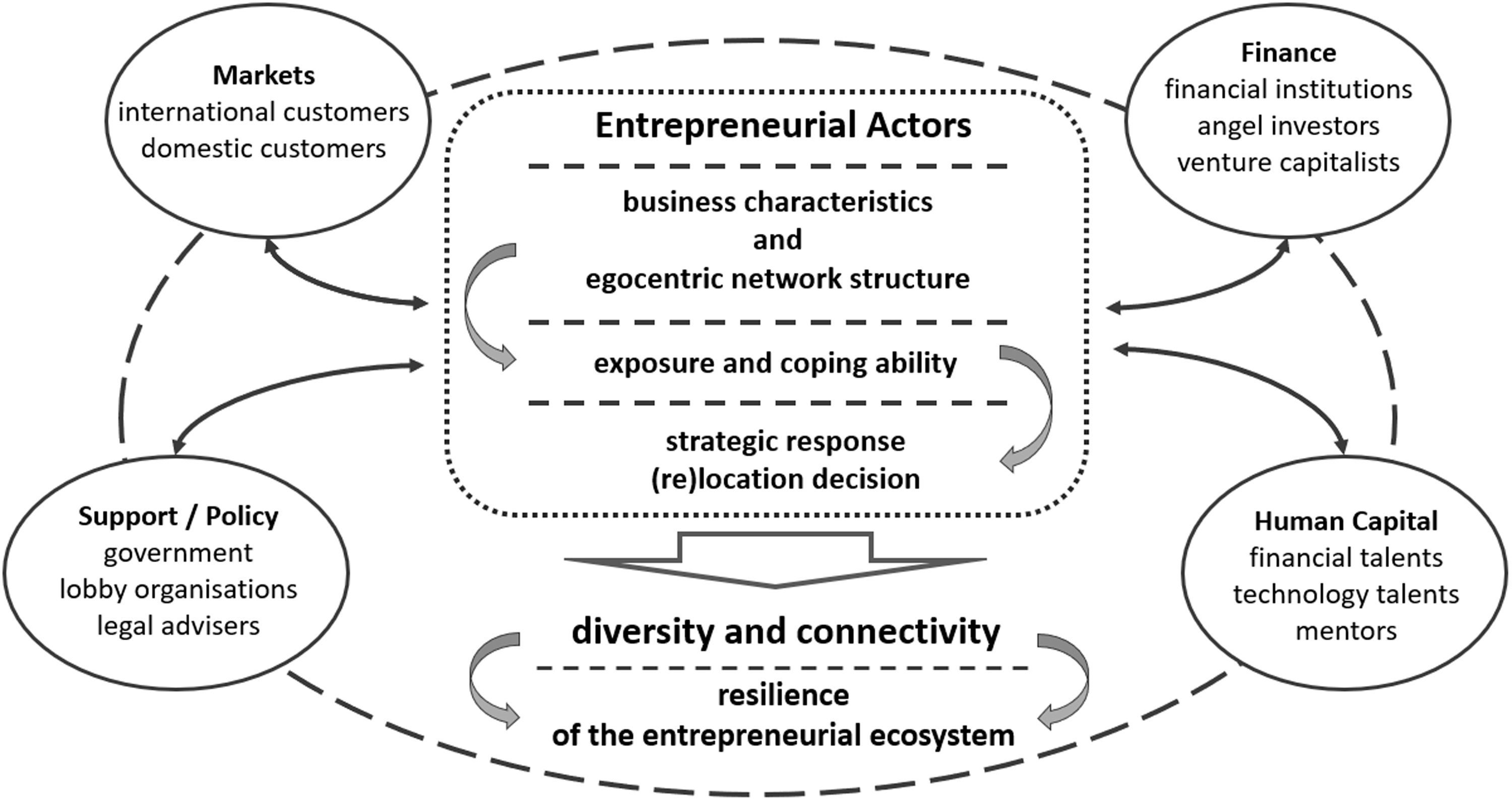

The concepts presented above form the foundations for the conceptual framework used to analyse the effects of Brexit on the EE of London’s FinTech industry (Figure 1). We see the time since the EU referendum as a period of high political uncertainty and Brexit as a process of institutional change. We are particularly interested in analysing how different entrepreneurial actors respond to political uncertainty and changing institutional settings, and how these actor-level responses might affect the resilience of London’s FinTech EE.

We follow Isenberg (2011) by grouping the key actors under consideration into the domains of markets, finance, human capital, policy and support, and consider how each domain has been affected by the decision of the UK to leave the EU. Compared to Isenberg (2011), we regard the domain of culture as a more general feature of the EE rather than a group of actors. As Brexit is likely to modify the flow of labour, goods, capital and services between the UK and the EU, we expect the domains of human capital, finance and markets to be affected (e.g. Dörry, 2017; Hall and Wójcik, 2018; Pollard, 2018; Ringe, 2018). However, the UK government has the potential to influence the domains of policy and support, such as by changing the country’s regulatory, legal and tax frameworks, and by offering support infrastructure to the industry to counteract the negative effects of leaving the EU. Overall, the domain of culture may be affected by a perceived decrease in the acceptance of foreigners and the contribution of their entrepreneurship to British society (Fritsch and Storey, 2014).

Following the operational definitions of Singer et al. (2015), we are interested in the responses of actors at different stages of the entrepreneurial process to the political uncertainty and the prospect of changing institutional settings related to Brexit. From an EE perspective, the capacity of political uncertainty and institutional changes to trigger actor-level responses of nascent entrepreneurs and start-ups are of particular interest (Stam, 2007), as entrepreneurial actors that are new to the EE play a specific role in its evolution (Metcalfe, 2005). Strategic decisions of owner-managers of established high-growth businesses are also considered significant, as their relocation would negatively affect the evolution of the EE, particularly in times when start-up activities tend to be postponed and cancelled (Stam, 2007).

Following Liesch et al., (2014), we assume the strategic responses of entrepreneurial actors to be triggered by their exposure to and ability to cope with political uncertainty. Therefore, we consider EEs as consisting of a variety of actors who respond to uncertainty and institutional change in different ways. Hence, we focus on how actor-level responses differ based on companies’ characteristics, such as size, age, degree of internationalization, integration in complex value chains and accumulated sunk costs (Clark and Wrigley, 1997; Hill et al., 2019; Stam, 2007), as well as on the structure of their egocentric networks (Stuart and Sorenson, 2005). In this regard, we consider anchor firms to play an important role in firms’ egocentric networks and in the EE as a whole (Dörry, 2017; Johns, 2016; Svensson et al., 2019).

Following Spigel and Harrison (2017), we assume that the resilience of an economic ecosystem is strongly linked to the diversity of and the connectivity among its agents. Therefore, we focus our analysis on the ability of London’s FinTech industry to attract entrepreneurial actors from outside the EE, while preventing the loss of entrepreneurial actors through relocation. Moreover, we focus on the ability of London’s FinTech industry to maintain high connectivity among its actors.

Conceptual framework for studying the impacts of Brexit on London’s entrepreneurial ecosystem.

Case study design and methodology

FinTech is recognized as one of the most important and dynamically evolving innovations, promising to reshape the financial industries profoundly. This process does not only lead to the creation of new products, services and business models, but also to profound changes in the financial services value chain (Lee and Shin, 2018). Following Hendrikse et al. (2018), we define FinTechs as organizations expediting the digital transformation of financial services by combining innovative business models and new technologies. As a hybrid industry, FinTech encompasses a variety of different business models, combining financial services with modern technologies (Dorfleitner et al., 2017). In this regard, some FinTech companies focus on offering new financial products and services, such as new payment solutions, automated wealth management, peer-to-peer lending, crowdfunding, real-time capital market engagement and customized insurances (Lee and Shin, 2018), while others focus on the technological building blocks that facilitate the delivery of new financial products and services, such as big data, artificial intelligence, blockchain, cybersecurity and cloud banking (Gozman et al., 2018). Both sides of the industry are strongly interlinked through business-to-business (B2B) supplier–customer relationships. Over the last years, traditional financial institutions have reacted to the rise of FinTech by investing in the development of in-house FinTech solutions as well as by cooperating with FinTech companies in order to get access to new technology (Gozman et al., 2018). As a result, part of the FinTech industry has evolved in close collaboration with financial incumbents, upon which it relies for access to payment infrastructure, banking licences and know-how (Svensson et al., 2019).

With 61,000 employees, annual revenues of £6.6b and £524m of investment in 2016, the UK is one of the world’s leaders in FinTech, alongside the USA and China, and an undisputed leader in Europe (Ernst and Young, 2016). InnovateFinance (2017) identified 1600 FinTech companies in the UK, most of which are concentrated in London. With an average business age of 5.3 years and a median headcount of fewer than 50 employees, the UK’s FinTech industry can be described as relatively young and dominated by small and medium-sized companies. The majority of the UK’s FinTech businesses concentrate on payments and remittances (13.5%), lending (13.1%), financial software (10.2%), online investment (8.2%), big data analytics (6.9%) and RegTech (regulatory technology; 6.9%), with small and medium-sized enterprises, as well as financial institutions, as their main customers. Nearly half of the UK’s FinTech businesses are governed by the Financial Conduct Authority (FCA) and/or the Prudential Regulation Authority (PRA).

The peak years in the short history of the UK’s FinTech industry fell between 2014 and 2016. Overall, 54% of FinTech start-ups were created in this three-year period (InnovateFinance, 2017). Existing reports highlight several features of the UK’s EE conducive to FinTech development, including access to highly qualified labour, availability of early-stage capital, a supportive regulatory regime, robust demand driven by a large consumer market open to innovation, and a financial services industry of global importance (Ernst and Young, 2016). However, at the same time reports stress that global competition in FinTech, particularly from the USA and China, has the potential to threaten the UK’s position (Ernst and Young, 2016).

To study the effects of Brexit on the UK’s FinTech industry, we focus on London as it hosts the majority of the UK’s FinTech businesses – 80% of the UK-headquartered FinTech firms and 98% of the internationally headquartered FinTech firms operating in the UK (InnovateFinance, 2017). In addition, London is well known for being Europe’s capital of innovation-based entrepreneurship (Nathan and Vandore, 2014) and remains one of the world’s leading financial centres (Cassis and Wójcik, 2018).

Methodology

Our secondary data analysis is based on online articles published by the news webpage FNLondon.com (FNL) from January 2016 to May 2018. FNL is updated daily and supplements the weekly newspaper Financial News. The Financial News, established in 1996 and focusing exclusively on finance, is recognized as the voice of the City of London. To narrow down the analysis, we downloaded 750 articles that cover the FinTech industry. These articles were analysed using the text-analysis software NVivo. In a first step, we selected 113 articles that mention the term Brexit, representing 15% of all articles published about FinTech. In a second step, we coded the Brexit articles based on the themes derived from our conceptual framework to calculate their relative coverage.

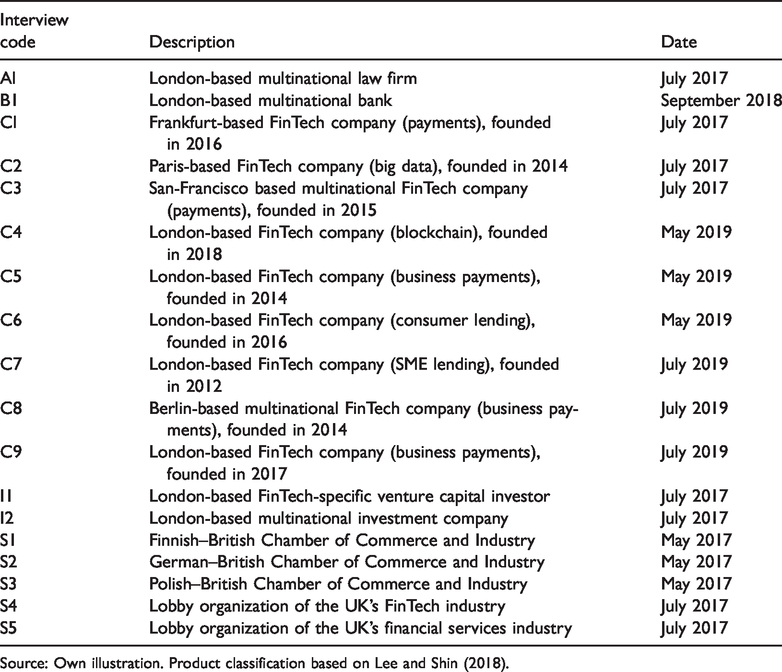

Our primary data analysis is based on the recording of two panel discussions and 13 in-depth semi-structured face-to-face interviews conducted in 2017–2019 in London. The interview partners were chosen in a manner that ensures the interviews cover actors from different domains of the EE, such as angel investors (I), banks (B), legal advisers (A), support organizations (S) and private FinTech companies (C) (Table 1). The interview partners were approached by email and during industry events, such as London FinTech Week. In total, we interviewed 9 FinTech companies, of which 56% were start-ups at the time of the EU referendum (younger than 3.5 years), and additional 44% founded after June 2016. We are confident that these companies were able to assess the effects Brexit has had on FinTech start-ups, based on their own experiences. Due to their young age, we also assume that these companies could assess the effects Brexit has had on nascent entrepreneurs. Moreover, we believe that other interview partners – such as the support/lobby organizations, banks and angel investors – were able to provide valuable insights into the start-up scene, as they work closely with nascent entrepreneurs and start-ups. In addition, we are confident that the diverse structure of our interview samples allowed us to capture some of the developments in the broader ecosystem. All interviews were recorded and manually transcribed. The transcripts were coded according to the analytical framework and analysed using NVivo.

List of interviews.

Source: Own illustration. Product classification based on Lee and Shin (2018).

Though limited in scope, this qualitative approach allowed us to develop an understanding of the multifaceted, temporally unfolding motivations, opinions and perspectives of different actors of London’s FinTech industry in the context of Brexit, as well as of the evolving industry narratives. We consider these personal opinions and industry narratives to be important, as in times of high uncertainty entrepreneurial actors are constrained in making informed decisions and rely on their personal opinions when making strategic choices (Cyert and March, 1992; Machado-da-Silva and Fonseca, 1999). Hence, although personal opinions and industry narratives per se are not sufficient to accurately predict the impact of Brexit, they can be seen as influencing the strategic decision-making process and behaviour of entrepreneurial actors and, consequently, as impacting the development of the EE as a whole.

Empirical results

The following sections present our empirical results, closely following the conceptual framework presented in the theoretical background section. The first subsection here highlights the impact of Brexit on different domains of the EE, while the second focuses on actual and planned (re)location decisions of different actors along the entrepreneurial process. All direct quotations used in this section refer to the individual interview transcripts (see Table 1).

The impact of Brexit on different domains of London’s entrepreneurial ecosystem

In the

Consequently, problems with attracting, recruiting and retaining tech talent are a major concern in light of Brexit, and are mentioned in 26.6% of the FNL articles under consideration. One concern is that the complicated and cumbersome visa system currently used for prospective non-EU employees might be used for potential European employees in the future: ‘If any of you ever had to fill out a visa form to bring in someone from America or Australia into a business, you realize … it’s not exactly the most flexible arrangement’ (S5, page 2, rows 6–10). In addition, it has been observed by the interview partners that ‘foreign talents are less ready to come to London due to the uncertainties’ (C9, page 7, rows 2–3). As a consequence, competition has increased noticeably: ‘Everybody is fighting for the same employees’ (C8, page 2, row 33). This problem is more acute for early-stage than for established FinTech companies, as the former often lack financial resources to go through extensive visa applications and pay high salaries. These findings suggest that political uncertainty and institutional change can potentially weaken companies’ ability to establish and maintain links with talented employees. In this regard, a company’s size/age increases its ability to establish and maintain links with talented employees. As access to talent affects business success (Menefee et al., 2006), this finding suggests a positive relationship between a company’s size and its ability to cope with political uncertainty and institutional change. The ability to attract international entrepreneurs and international talent is also strongly related to the domain of culture. For many years, London had been seen as a top location for global talent to work and start businesses due to its reputation as a liberal, tolerant, and diverse city. Since the EU referendum, the UK has been seen as losing some of this good reputation: ‘It makes it less attractive, if you have the feeling not to be welcome’ (C1, page 1, rows 1–4). This finding illustrates the sensitivity of international talents to uncertainty and cultural change, which has the potential to reduce the variety of ideas, knowledge and skills in the EE (Rodríguez-Pose and Hardy, 2015) and, consequently, can negatively affect its diversity.

Considering the

These results suggest that uncertainty associated with political change can weaken some companies’ ability to establish and maintain links to international venture capital markets. In addition, they highlight that the greater risk-aversion of global investors in times of political uncertainty disadvantages early-stage more than established companies. As access to venture capital is crucial for business success (Motoyama et al., 2013), this finding suggests a negative relationship between a company’s size/age and its exposure to political uncertainty and institutional change. While venture capital is more important for high-growth start-ups in order to scale up, access to loans is more important for nascent entrepreneurs. In this regard, the founder of a recently launched FinTech start-up reported having difficulties accessing banking infrastructure and funding: ‘the banks … were very sceptical’ (C5, page 2, rows 36–37). In such situations, nascent entrepreneurs and young start-ups might decide to use alternative funding sources provided by peer-to-peer lending FinTech companies: ‘Small businesses come to us and we route them to a wide range of lenders. We solve a recognized problem of the market, which is that when small businesses cannot get a loan from the bank, they really struggle to find the right alternative’ (C7, page 1, rows 25–32). However, as a response to the current Brexit uncertainties, these FinTech companies develop tighter lending criteria: ‘We have to be more careful who we lend money to and how we originated our loans’ (C8, page 3, rows 1–4). This is seen as having a negative impact on access to funding for start-ups. This finding illustrates the interconnected nature of London’s FinTech industry and highlights the importance of ties among companies of different ages and venture types (Metcalfe, 2005). Interestingly, it suggests that uncertainty associated with political change has the potential to weaken such ties and/or prevent them from evolving, potentially reducing the connectivity of the ecosystem.

When it comes to the

London’s FinTech ecosystem has benefited from its access to the European Single Market, providing a gateway to a wider customer base. This market access is based on the harmonization of financial services laws, which are the foundation of the so-called ‘passporting rights’, allowing financial service companies regulated in one EU member state to offer their products and services in other EU member states with no need for further authorization (Ringe, 2018). Consequently, losing access to the European Single Market has been another concern of London’s FinTech industry in light of Brexit, mentioned in 11.5% of the FN articles under consideration. Brexit is seen as leading to higher transaction costs, predominantly in the form of non-tariff barriers, such as changing standards, certifications and regulations: ‘You have to start from the premise that … we are out of the single market … that means that many businesses in the UK that trade into the EU are using passporting that’s not going to exist’ (S5, page 1, rows 31–37). However, the effect of the loss of passporting depends on the market focus, the organizational structure and the specific products and services a company provides. In this regard, FinTech companies that focus solely on the UK market or feature a multi-domestic organizational structure seem to be less affected: ‘We are a global company that is acting very locally … we see this as a benefit’ (C8, page 2, rows 15–16). The same applies to FinTech companies with a strong focus on technology: ‘For the services I’m going to provide in the future, I don’t really feel that it’s going to have an impact’ (C4, page 3, rows 20–21).

The extent to which most FinTech services are passported is seen as overstated by some of the interviewees: ‘If you are a B2C FinTech or a B2microB FinTech, there’s not that much that is passportable. Our key regulator authorisation is consumer credit, which is not passportable … The only regulatory position that we rely on and is passported, is the PSP2 open banking license’ (C7, page 5, rows 25–39). In contrast, FinTech companies that offer passportable financial services and want to continue offering them in the European Single Market are indeed affected by the potential loss of the passporting rights: ‘If you were talking to capital markets FinTechs … you may get a different answer’ (C7, page 5, rows 30–31); ‘With the passport it meant you could really start to play in a big market. Losing it is a massive downside’ (C5, page 4, rows 3–4). These results highlight the significance of access to the European Single Market, and the associated low transaction costs. Links facilitated by this access are likely to be weakened by institutional changes associated with Brexit. Our findings also indicate that a company’s exposure to these changes depends on their market focus, organizational structure and the level of integration in highly regulated value chains.

When it comes to the

In addition, the UK government is seen as being very responsive when being approached by high-growth FinTechs: ‘If a certain bit of regulation or policy doesn’t work for FinTechs … they actually listen and are open to potentially change’ (C9, page 2, rows 30–31); ‘They are very responsive and an invitation is usually immediately granted’ (C8, page 6, rows 13–14). Some high-growth FinTechs are consulted by the government concerning possible impacts of Brexit: ‘We were invited to a round table at the London Stock Exchange … this one was specifically about Brexit … there was one person from the Trade Department, one from the Treasury, and other ministers’ (C7, page 5, rows 11–14). Start-ups, in contrast, face higher barriers: ‘If you’re a really small player in the market, there is no optimal way’ (C7, page 8, row 10).

These findings illustrate the importance of direct ties with government representatives in times of political uncertainty and institutional change. A company’s size/age may not only determine its ability to establish and capitalize on direct ties with government representatives, but it may also enable larger/established companies to further strengthen such ties in times of political uncertainty and institutional change. As having strong ties with government representatives increases access to information and a company’s political influence (Mason and Brown, 2014), this suggests a positive relationship between a company’s size/age and its ability to cope with political uncertainty and institutional change. While smaller companies are less likely to establish and utilize direct ties with government representatives, they can benefit from joining support organizations, such as Innovate Finance, which provides ‘information flow, keeping you abreast of what is happening, and does certain amount of lobbying’ (C9, page 2, rows 2–3) and is seen as ‘a really great organisation to be part of to get introduced on different levers’ (C8, page 4, rows 32–33), as well as an authority with impact, particularly when addressing generic topics such as Brexit. In addition, London’s FinTech industry increasingly engages in collective lobbying together with the financial services industry: ‘We are in the same sector, and we must speak with one voice’ (S4, page 3, rows 14–16). In this regard, industry events and All Party Parliamentary Groups (APPG) are commonly used for exchanging views and forwarding collective opinions: ‘The key one is the APPG of Fair Business Banking, we have already regular contact with them’ (C9, page 2, rows 13–14);’We are one of the initial members of an APPG for business support and engagement’ (C8, page 4, row 12). These results illustrate that industry representatives can act as brokers, closing structural holes between otherwise disconnected actors in the ecosystem (Mason and Brown, 2014). This process does not only connect start-ups with government representatives through indirect ties, but also creates direct ties among start-ups that attend the same lobbying events, potentially fostering the exchange of new ideas and knowledge. As such, political uncertainty may foster the creation of new direct ties among start-ups, potentially increasing the connectivity of the ecosystem.

Location decisions of entrepreneurial actors

Despite uncertainties regarding Brexit, no significant decline in the UK’s tech start-up rate has been observed since the EU referendum: ‘It seems as busy. I haven’t noticed any change, positive or negative’ (C6, page 4, row 11). The persistent ability of London’s FinTech ecosystem to attract nascent entrepreneurs is seen as being strongly linked to the benefits of agglomeration effect: ‘You have really good infrastructure, you have a big network of support’(C6, page 1, rows 39–40), as well as to London’s strong global reputation: ‘When it comes to London, it’s a brand name. If you’re successful in London, you can be successful everywhere. That’s why you start here’ (C4, page 2, rows 21–23). In fact, three of our interview partners founded their companies after the EU referendum: ‘We were building this company from the beginning in the heart of Brexit’ (C6, page 3, rows 31–32). In addition, some fast-growing European FinTech start-ups still plan to open offices in London to expand their businesses: ‘If you are a serious FinTech somewhere else in Europe, you would be moving to London at some point’ (C7, page 4, rows 15–16); ‘We decided to launch the UK office after the referendum’ (C8, page 2, rows 17–18); ‘We are pretty sure that we are coming. We started thinking about it even after Brexit’ (C2, page 2, rows 1–2). In contrast, when focusing on the ability to attract fast-growing US and Asian FinTechs that seek to expand into the European Single Market, London’s leading role might be challenged to a certain degree. The Chinese FinTech company Ping Pong, as well as the Japanese FinTech company Rakuten, which set up their European branches in Luxembourg instead of London, can be seen as first examples of this trend.

At the time of writing, several established FinTech companies, such as TransferWise, WB21, Azimo, PPRO and WorldRemit, have not only put in place firm Brexit contingency plans, but have already started executing them. Our empirical results confirm this observation, as, in fact, three of the interviewed FinTech companies have already established a licence in the EU in order to open an office: ‘Given that we are expanding across Europe…, we’ll have to find a way to open an office in Amsterdam’ (C7, page 4, rows 33–37); ‘We may have to do some emergency legal arrangements’ (C9, page 5, row 22); ‘We have already established a Belgium licence … And the reason for that has pretty much to do with continuity post-Brexit’ (C5, page 1, rows 15–18). As these FinTech companies want to maintain access to the UK market, their relocation plans do not involve a full relocation to the EU. Rather, they plan to start subsidiaries in the EU for the sake of market access: ‘When we are talking about relocation, it’s not so much that the company is relocating, it’s more that they are setting up satellites’ (B1, page 5, rows 18–20). What these companies have in common is that they provide ‘passportable’ financial services. As such, their behaviour can be explained by their integration in highly regulated value chains. Moreover, their behaviour is linked to their dependency on the infrastructure of established banks, which allow them to deliver their services: ‘At the front … you are engaged with the FinTech company, but what happens behind the scenes is that the company still needs to be engaged with a traditional corporate bank to have the banking infrastructure behind them that allows them to operate’ (B1, page 1, rows 32–38).

Following the order of the Bank of England in 2017, established banks had to develop contingency plans for different Brexit scenarios. During this process, some of them developed concrete plans concerning the relocation of specific business functions (e.g. euro-clearing) to the EU. With the Brexit deadline approaching and uncertainty remaining high, some of the banks in question decided to execute their relocation plans independently of the UK–EU negotiation outcome: ‘We process … euro-clearance … and it’s moving … to a location in Europe … even if Brexit got cancelled … that decision has been made’ (B1, page 1, rows 5–15). This has led to a situation in which FinTech companies that want to continue working with these banks also need to obtain regulatory authorization in the EU: ‘They will also have to change if they want to continue having their euro-clearance with us’ (B1, page 2, row 35). These findings confirm previous work of Svensson et al., (2019) highlighting the relational dependency of parts of the FinTech industry on alliances with financial incumbents who meet their needs for market legitimacy by allowing them to use their banking licences and infrastructure. Therefore, financial incumbents can be seen as brokers (Morrison, 2008), allowing start-ups to access a wider customer base. However, our results also indicate that having strong ties with financial incumbents can reduce the variety of strategic options FinTech start-ups can resort to, as they are forced to comply with strategic changes of incumbents or to dissolve the tie. This corroborates previous work of Johns (2016) that highlights that strongly connected anchor firms play an important role in firms’ egocentric networks and have the power to shape the strategic responses of entrepreneurial actors. Consequently, strongly connected anchor firms have the potential to change the structure of EEs (Dörry, 2017).

Established FinTech companies see establishing a licence in the EU as relatively easy, particularly if they already have authorization in the UK and experience operating in the EU: ‘I think that Brexit will, for incumbent companies that are already operating [in the EU] … just be a pain and they would get over it’ (C5, page 3, rows 38–41); ‘there is actually no hurdle of getting a license, if you have one in the UK’ (C9, page 6, row 13); ‘we could solve it with two or three people working for six months and a few tens of thousands of legal fees … it is not existential’ (C7, page 6, rows 9–12). Although it is seen as unlikely that divestment and relocation of whole companies will occur on a large scale, some companies expect that Brexit will lead to changes in their strategic expansion, favouring locations outside of the UK: ‘The question is about strategic expansion’ (I1, page 4, row 24); ‘Once there is a base in Continental Europe there will be a higher likelihood that Europe will be served from that base. Not just some licensing point of view, but also from sales and customer service and so on’ (C5, page 3, rows 20–22). In contrast, nascent entrepreneurs and young start-ups with limited resources are assumed to face bigger hurdles when seeking a European licence: ‘I think for businesses that are yet to start it will be a barrier, because … this is an extra hurdle to have to get another licence and another set of banking relationships’ (C5, page 3, rows 38–41; page 4, rows 1–3); ‘If you’re very early FinTech, so you have very limited resources, it probably would delay internationalisation’ (C9, page 6, rows 24–25). Many of these smaller companies have to follow a wait-and-see approach: ‘Many haven’t really changed yet. They are waiting to get a clearance on what is going to happen’ (S1, page 4, rows 13–14). However, they have developed contingency plans that can be executed depending on the final negotiation outcome: ‘They do scenario planning and at one point they will execute’ (S2, page 7, rows 28–31).

As start-ups typically start from a small size, they may be relatively easy to relocate to other places in case Brexit leads to shrinking business opportunities: ‘The team is going to be quite small at the beginning … and so it would be easy to go maybe to Paris or to Madrid or Frankfurt or whatever’ (C2, page 2, rows 1–2). These results confirm findings by Stam (2007) highlighting that a company’s size/age affects its relocation decisions. Established companies seem more able to maintain access to the European Single Market while remaining in the UK. In contrast, poorly equipped start-ups will either have to give up on their links to the European Single Market, with potential negative consequences for their growth prospects, or leave the UK altogether. In line with Clark and Wrigley (1997), who discussed the effect of sunk costs on firms’ market-exit decisions, companies that have not yet accumulated high sunk costs may be more able to leave the UK market.

Overall, our results highlight that, at the time of writing, London’s ability to attract entrepreneurial actors from outside the EE has not decreased significantly. Moreover, London has been able to prevent significant loss of entrepreneurial actors through relocation. However, the final negotiation outcome at the end of the transition period is likely to affect this ability.

Conclusions and implications

The goal of this paper was to contribute to the debates regarding the resilience of EEs in times of political uncertainty and institutional change. In doing so, we wanted to address some shortcomings that Alvedalen and Boschma (2017) identified in the EE literature, including a lack of focus on the importance of, and connections between, different entrepreneurial actors and the evolution of these connections in times of institutional change. In addition, we aimed at putting a stronger emphasis on concepts discussed in the social network literature (Stuart and Sorenson, 2005), such as egocentric networks, the relative importance of non-local versus local linkages and certain network features, such as diversity and connectivity.

First, our results confirm that the six dimensions of Isenhard’s Entrepreneurial Ecosystem Model (2011) are useful as a heuristic to identify and engage with strategic responses of entrepreneurial actors and anchor firms embedded in EEs to uncertainty and institutional change.

Second, they complement previous research (Clark and Wrigley, 1997; Dörry, 2017; Hill et al., 2019; Johns, 2016; Stam, 2007; Svensson et al., 2019) and address the call of Alvedalen and Boschma (2017) by illustrating that not all types of entrepreneurial actors respond to political uncertainty and institutional change in the same way. Rather, their strategic responses are influenced by their exposure to and capacity to cope with political uncertainties and potential institutional changes, which vary with regards to their business characteristics and egocentric network structures (Stuart and Sorenson, 2005). Our findings suggest that the exposure to Brexit is greater for companies whose egocentric networks show strong dependencies on non-local ties with the European Single Market (consumers, investment and labour). In addition, our results suggest that the exposure to Brexit is greater for companies that are integrated into highly regulated international value chains, such as FinTechs that offer passportable financial products and services. In line with Dörry (2017), our results also suggest that exposure to Brexit is greater for companies that have strong ties with financial incumbents. Therefore, our results confirm that anchor firms play an important role in firms’ egocentric networks (Johns, 2016; Svensson et al., 2019). Companies with high exposure to Brexit are likely to feel the need to strategically respond to the associated uncertainty. Such actor-level responses cover a variety of coping strategies, including putting increased emphasis on attracting and retaining talent, searching for alternative funding sources, intensifying lobbying activities, and relocating business functions. Our results show that the capacity to execute such coping strategies is strongly affected by a company’s age and size (Stam, 2007), disadvantaging start-ups in comparison to high-growth and established companies. In this regard, we show that the advantages of high-growth and established companies can be explained by their better resource endowment, which increases their ability to maintain local and non-local ties with key actors inside and outside the EE, such as other local FinTechs, government representatives, international talent and international VCs, allowing them to continue capitalizing on their egocentric networks.

Third, the evidence gathered in this paper confirms that anchor firms have the power to shape the structure of EEs (Johns, 2016). Hence, our results point in the same direction as Dörry (2017), suggesting that, in an extreme scenario, large-scale relocations of financial incumbents out of London could trigger a domino effect of relocations among FinTech firms.

Fourth, the paper addresses the call of Alvedalen and Boschma (2017) by illustrating that political uncertainty and the prospect of institutional change have the potential to modify the diversity and the local and non-local connectivity of an EE, potentially affecting its resilience (Spigel and Harrison, 2017). Concerning the diversity of London’s EE, our results highlight that, at the time of writing, the start-up rate in the UK remains high and several FinTechs were launched after the EU referendum. Therefore, it seems that London’s ability to attract entrepreneurial actors from outside the EE has not decreased significantly. Likewise, our results illustrate that, so far, London has been able to prevent the loss of entrepreneurial actors through outmigration. This suggests that the diversity of London’s EE has not decreased drastically since the EU referendum. Following Spigel and Harrison (2017), this can be seen as reflecting the resilience of London’s EE. However, our results also show that strategic responses of entrepreneurial actors concerning relocation decisions are conditional on the final Brexit deal. Hence, we would suggest that the final negotiation outcome at the end of the transition period has the potential to further affect the diversity of London’s EE. With regards to the connectivity of London’s EE, our results suggest that the political uncertainty associated with Brexit has weakened non-local ties with VCs, and some vertical local ties between FinTech firms of different ages and venture types, which has the potential to negatively affect the connectivity of London’s EE (Spigel and Harrison, 2017). In contrast, local ties between established FinTechs and government representatives appear to have been strengthened since the EU referendum. In addition, we show that entrepreneurial actors try to reduce uncertainty and strengthen their bargaining power by establishing horizontal ties with their local competitors. Following Spigel and Harrison (2017), these new ties have the potential to positively affect the connectivity and resilience of London’s EE by fostering the exchange of opinions and knowledge between start-ups (Gilsing et al., 2008). Overall, our results confirm the theoretical considerations of Martin and Sunley (2007), highlighting that EEs are complex adaptive systems, in which micro(actor)-level responses shape macro-level patterns of EEs, and vice versa, and, due to complex interdependencies among actors, the very prospect of a fundamental institutional change has the potential to change its structure and resilience.

However, it is important to stress the exploratory nature of our research as offering some of the first and limited insights into the impacts of Brexit on London’s EE. This unique research opportunity comes with significant challenges, particularly the limited availability of data and fundamental uncertainty regarding the ultimate outcome of the UK–EU negotiations. Further, we were only able to interview a limited number of actors relevant to the industry and rely on their personal, subjective opinions. These opinions are not only shaped by the environment of uncertainty, but also by the positionalities of the interviewees, such as their political beliefs, as well as by the political agenda of specific industry associations. Moreover, we must acknowledge that we did not interview potential/nascent entrepreneurs directly. Rather, we rely on the assessment of start-ups and other actors in the EE, such as bank representatives, angel investors and support organizations, when discussing the impact of Brexit on potential/nascent entrepreneurship, assuming that, due to their close contact with potential/nascent entrepreneurs, they could provide some insight.

While qualitative research is helpful to obtain first insights into ongoing processes, quantitative research methods, such as surveys or experiments, could be used to test our findings on a larger scale. Such research could focus in greater detail on how relocation decisions are shaped by different company characteristics. For example, the role of egocentric networks of companies could be further considered (Borgatti and Foster, 2003) to analyse the impact of different ties among actors on their relocation decisions, particularly focusing on the co-location between incumbents and FinTech start-ups. In addition, it would be interesting to quantify whether the decision of the UK to leave the EU will lead to temporary decentralization of the FinTech scene by focusing on the spatial distribution of future start-up rates, particularly comparing the UK, the EU and the USA. Moreover, panel analysis could be used to track companies over time in order to analyse changes in their strategic responses. However, we should bear in mind that it will probably take many years, if not decades, before we are able to fully understand how the decision of the UK to leave the EU has changed London’s EE. And even then, its net effects are likely to be difficult to quantify.

Footnotes

Acknowledgements

We would like to acknowledge all participants of the ‘5th Global Conference on Economic Geography’, which took place 24–28 July 2018 in Cologne, for their constructive comments, which helped to finalize this article. In addition, we thank the anonymous reviewers whose constructive comments helped to improve and clarify the manuscript.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received financial support for the research, authorship and/or publication of this article: Dariusz Wójcik has received funding from the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation programme (grant agreement number 681337). The article reflects only the authors' views and the ERC is not responsible for any use that may be made of the information it contains.