Abstract

This paper analyses intermediary organisations in developing economy agricultural clusters. The paper critically engages with a growing narrative in studies of intermediaries that have stressed the ownership structure of intermediaries as a key driver for enabling knowledge transfer, inter-firm learning and upgrading of small producers in clusters. Two case studies of Latin American clusters are presented and discussed. The study suggests that in addition to ownership structure, cluster governance and the embeddedness of intermediaries in clusters are critical factors that need to be taken into account in understanding the influence of intermediaries in the upgrading of small producers in clusters.

Introduction

In this paper, we discuss the role intermediary organisations can play in the development of emerging agribusiness clusters in developing countries. 1 We engage with a growing narrative in studies of intermediaries that has stressed the ownership structure of intermediary organisations as a key driver for (strategically) enabling knowledge transfer and inter-firm learning at the cluster level (Goldberger, 2008; Klerkx and Leeuwis, 2009; Provan and Kenis, 2008; Intarakumnerd and Chaoroenporn, 2013). In particular, the argument is made that intermediaries with a public–private governance (PPG) can have “multiparty” governance by combining a private sector drive to establish cross-cutting ties with different organisations outside the cluster whilst at the same time the public sector ethos can ensure there is participatory governance in the cluster, facilitating inclusion of small producers in the adoption of new organisational and technological innovations (Zuckerman and Sgourev, 2006). Great emphasis by policy makers is therefore placed on the agency of the intermediary at the cluster level to achieve inclusive economic transformations.

Whilst the above argument is compelling, particularly for policy makers looking for useful levers to intervene in clusters, we urge some caution and suggest that the analysis of the potential impact of intermediaries needs to take into account at least two additional factors. Firstly, that the influence of the intermediary is likely to vary significantly according to the governance of inter-producer relations at the cluster level, including for example the degree of collective organisation or unequal access to markets by some organisations over others. Secondly, it is necessary to consider that whilst the breadth of the economic activities in clusters that can benefit upgrading has opened up new spaces for intermediation, this space can draw in many organisations undertaking intermediary functions that have deep local roots with varied ownership structures, motivations and incentives. Therefore, the relational network position (central, periphery) of different intermediaries with respect to other organisations will affect its influence. Moss (2009) defines the basic function of intermediaries as the collective pursuit of public, common or individual interests and that a defining asset of intermediaries is their ability to reap collective benefits. However, as will be seen, the expansion of both functions and organisations undertaking intermediary activities means that the relationship between intermediaries and other organisations will be complex and multifaceted and can involve a range of organisations that assume intermediary roles (Moss, 2009; Klerkx and Aarts, 2013). Our enquiry is therefore guided by the following questions:

How does the ownership structure of intermediary organisations (public, private, or PPG) influence inter-producer governance relations in terms of the upgrading activities of small producers? How does the position of different intermediaries in the cluster influence inter-producer governance relations in terms of the upgrading activities of small producers?

Two case studies of emerging clusters in developing country settings are presented – the mango cluster in Piura, northern Peru and a cluster of Palm oil producers in central Colombia. We discuss intermediaries with three types of ownership structure: private organisations, producer associations and an organisation with a public–private ownership governance.

We begin the discussion by posing the opportunities for upgrading through new trading arrangements, fragmentation of value chains and the outsourcing of some service functions. We then engage in a critical discussion of the narrative that upgrading can be enhanced by the intervention of an intermediary with a public private ownership structure that encourages both inclusion and entrepreneurship. This claim is discussed with reference to cluster structure and governance of inter-producer relationships. We suggest that intermediary organisations can indeed play a crucial role in upgrading by means of networking, but that this influence will in part dependent on structures of pre-existing relations between producers involved in upgrading of value chains and the degree of embeddedness of the intermediary in the cluster. We conclude with reflections both on agricultural cluster development and on the study of intermediation more generally.

Evolving opportunities for intermediaries in value chains

Debates over how to facilitate the upgrading of agricultural producers in developing country value chains has gone through different stages. By upgrading we refer to the capacity of organisations (or small-sized producers) to increase the value added of processes or products (Giuliani et al., 2005; Humphrey and Schmitz, 2002). During the 1980s and 1990s, a market-led approach was preferred in the belief that the upgrading challenge could be resolved by improving access to international markets and lowering transaction costs to trade. Whilst this introduced macro-economic stability, only a small number of large firms in some sectors were able to respond and most medium and small-sized firms were excluded (McDermott et al., 2009). A second approach emphasised the importance of external linkages in global value chains (Gereffi et al., 2005; Kaplinsky and Morris, 2001). The opportunities for upgrading here will largely depend on the governance of the value chain, some local, but more often global, and cooperation with key suppliers and sub-contractors. In natural resource settings, hierarchical and quasi-hierarchical relations tend to play a key role in assisting in the upgrading of production capabilities, particularly around quality standards and certifications (Gereffi, 1994; Schmitz and Knorringa, 2001).

A third and more recent development emphasises how countries react to and experiment with a growing patchwork of transnational regulatory integration (Bruszt and McDermott, 2014). Some of these regulations have encouraged buyers to reduce the number of suppliers and focus on large partners, excluding small and medium-sized producers. Nevertheless, there is also some evidence of greater use of incremental experiments and adaption to rules (Perez-Aleman, 2010) that reflect a degree of joint problem-solving and building of local capabilities (McDermott and Ruiz, 2014). Thus, value chains with new channels of integration and more heterogeneous arrangements have emerged, with small producers from developing countries operating in both low value and in some cases higher value specialised niche activities (OECD, 2015) through new arrangements based on ethical trading standards (Barrientos et al., 2011).

The incorporation of small producers in some agribusiness value chains and the focus on building local capacity has brought to relief the need create a strong institutional infrastructure at local level (Bebbington et al., 2008) to facilitate upgrading since, although buyer firms set the standards of production, they have not always been prepared to assume the role of transferring knowhow, leaving the task of capability building to local service providers (Gereffi, 1994; Schmitz and Knorringa, 2001). Such a trend is particularly prominent for small-scale agribusiness producers. As Gomes (2007) in her study of the Brazilian fruit sector suggests, a change in buyer behaviour has taken place in areas where product differentiation is less prominent, with greater responsibility for upgrading placed upon local institutions. Consequently, local service providers and intermediaries have had to increasingly assume the task of building both vertical (external) and horizontal (cluster) relationships and helping local actors overcome the hurdles to the achievement of consistent quality, logistics and establishing a scientific base for testing and measurement of quality standards (Schmitz and Nadvi, 1999). Hence, as new market opportunities appear and establish themselves through value chains, new local governance arrangements emerge that attempt to re-embed the local economy through a combination of local and global regulations, both public and private (Barrientos et al., 2011).

The new space for intermediation has led to an extensive range of, what sections of the literature have identified as intermediary activities. In particular, Howells’ (2006) typology of intermediaries in innovation activities drew attention to the varied and holistic role played by intermediaries than was previously recognised. In the area of both industrial clusters and agribusiness clusters, a range of studies (for example, Bell and Giuliani, 2007; Batterink et al., 2010; Caniels and Romijn, 2003; Clarke and Ramirez, 2014; Kilelu et al., 2013, 2017a; Mmari, 2015; Poulton et al., 2010; Shou and Intarakumnerd, 2013; Szogs, 2008; Szogs et al., 2011; Visser and Atzema, 2008; Watkins et al., 2015) have increasingly underlined the roles of intermediation, particularly in knowledge transfer. Intermediation also includes activities supporting local producers by improving vertical and horizontal coordination roles (Bolwig et al., 2011; Kilelu et al., 2017b; Poulton et al., 2010) and enabling the collective action of producers (Kilelu et al., 2017a; Poulton et al., 2010). Intermediaries are also argued to help in the upgrading of producers in terms of process and product upgrading, introducing better production methods to boost cluster performance and in enhancing compliance with quality standards (Iizuka, 2009; Kilelu et al., 2017b; Klerkx et al., 2012; Perez-Aleman, 2010). Lastly, intermediaries may help in enhancing the institutional environment, for example helping producer organisations lobby for favourable legislation (Poulton et al., 2010).

This array of activities makes analysis of intermediation a challenging task. Additionally, an important narrative has emerged that focusses on the importance of the ownership structure of the intermediary as a decisive factor to achieve accelerated and broader upgrading (Sabel, 1994; Schneider, 2004). Poulton et al. (2010) pick up on this when they suggest that during the 1980s and 1990s private sector organisations were preferred as the primary providers of business services as they were deemed more efficient. However, whilst this tended to improve outputs to markets in high productivity areas, as intervention of state bodies was rolled back, it weakened market access in more remote areas. The argument now more commonly made is that intermediary organisations based on public–private ownership structure have advantages for the delivery of collective goods and services. Within an agricultural development context, an example of this argument is illustrated by McDermott et al.’s (2009) study of two clusters in the wine industry in Argentina, where great stress as an explanation for the success of cluster transformations is placed upon the intervention by organisations described as “Government Support Institutions” (GSIs) or using Sabel’s (1994) term, “Developmental Associations”. On the one hand, these are able to respond to commercial realities that encourage them to establish lines of communication and cross cutting ties between different social and geographical producer communities. On the other hand, the mandated requirement of these intermediaries to have “participatory governance”, whereby resources and membership of boards is made up of representatives of the state, the regulator, the private sector, phytosanitary organisations and producer associations on the governing and advisory boards ensures that the process of upgrading is inclusive of smaller producers. Further examples include McEvily and Zaheer (1999) and Owen-Smith and Powell (2004) who describe the establishment of public institutes and training centres that help firms access new knowledge due to their mandates to provide collective resources and collaborate with firms from distinct localities. The contrast is drawn with, for example, producer associations which, whilst playing important intermediary roles of coordination, their ownership structure leads them to prioritise their members and preside over insular and vertical networks that benefit their members rather than all the actors within a cluster. Hence, re-ordering relationships is likely to keep the basic network closed.

Structures and governance of value chains and cluster

The basic premise upon which the above argument is built is that intermediaries can reshape the existing structure and composition of organisational fields by instigating the creation of new institutions with relevant stakeholder groups at the level of the cluster. Traditional views of value chains involving small and medium-sized agricultural producers selling to exporters emphasise the endemic power relations in quasi-hierarchical relationships (Giuliani et al., 2005). Significant roles are conferred to lead firms in determining upgrading opportunities to local producers (Gereffi, 1999), such as through processing and packaging in fruit and vegetables chains (Dolan and Humphrey, 2000).

As discussed, the development of value chains with different governance rules highlights new opportunities for institutionally and socially embedded organisations such as government agencies, consultants, associations, NGOs and other intermediaries to support process and product upgrading. However, heterogeneous arrangements require added insights into local production networks and the power relations inherent within them. One approach that is particularly relevant to developing economy agribusiness is to focus on the structural characteristics of local geographical clusters tied into value chains. Humphrey and Schmitz suggest that upgrading happens in both value chains and clusters although these represent a quite different scope of analysis. Unlike value chains, cluster analysis focusses on local inter-actor linkages (Humphrey and Schmitz, 2002) and therefore on specific production ensembles and the structure and composition of the networks (McDermott et al., 2009). The structure of agribusiness clusters with a preponderance of small producers is likely to be dominated by a small number of exporters, large producers or service organisations. One can draw some parallels with Markusen’s (1996) region-centred identification of hub-and-spoke districts, where regional structure revolves around one or several major corporations in one related specialised sector. As well as cluster structure, analysis of knowledge transfer in clusters also needs to consider cluster governance, by which is meant the coordination of economic activities between producers and organisations through non-market relationships. This approach places greater importance on issues of intermediary embeddedness. According to Granovetter and Swedberg (2001), embeddedness refers to a detailed understanding of the mechanisms and processes of the social construction of institutions and local business and non-business networks. Embeddedness is closely tied to our account of how inter-organisational governance evolves and how intermediaries (including individuals acting on behalf of intermediary organisations) are able to coordinate production strategies and link knowledge of local producers inside and outside the cluster. This includes questions such as the history of associationalism and the density of relations between economic and social organisations that underpin coherent public policy and collaboration between organisations. Intermediaries can indeed play a crucial role in opening up links. However, defining which intermediary organisations assume this role and the extent of this influence will be in part dependent on structures of pre-existing relations between producers involved in value chains and productive clusters. A cluster with weak traditions of social capital and low bilateral cooperation between producers will be more likely to depend on the organisation with prime access to exporters or processors of raw materials. This dependence may leave little space for a separate intermediary organisation, especially if many of the functions of intermediation are performed by the large buyers or its producer association, albeit within a structure based on tight bonds of dependency. By contrast, Tsai (2007) provides a view of cluster governance where there exist high levels of civic participation and where service organisations, including government bodies, share obligations and interests of the local community, which she contrasts with sectors characterised by fragmentation and corruption. With more socially cohesive clusters, a demand is created for broader services to facilitate economic development and social inclusion that creates spaces for specialised services and intermediaries. Therefore, an analysis of the opportunities, boundaries and limits of intermediary influence needs to incorporate both structures and governance of agribusiness clusters in value chains and cluster governance.

A relational view of intermediary functions

Having discussed the structural and governance factors affecting upgrading we can more directly address the main question posed of intermediaries, ownership structures and impacts in emerging clusters. As discussed earlier, ownership acts as an indicator of the likely motivation of an organisation. However, in a number of empirical studies there appears to be little consensus about what sort of intermediaries should undertake the role of providing information, technical assistance and building capacity (Markelova et al., 2009). This is partly because intermediaries can undertake different roles, assume contrasting objectives and have dissimilar motivations. For example, some intermediaries position themselves as “neutral” and “honest” and claim to provide facilitating roles by bringing together stakeholders and promoting collective action (Hellin, 2012; Klerkx and Leeuwis, 2009). Others have a key normative interest in achieving policy or business goals and actively lobby for and translate interests of those they represent (Goldberger, 2008; Hargreaves et al., 2013; Yang et al., 2014), or may aim to gain control over the relationships they mediate (Dhanaraj and Parkhe, 2006; Obstfeld, 2005) or exploit these (Barrientos, 2013). Ownership structure will provide a less than clear-cut indication of an intermediary’s actions where it performs multi-roles and the same intermediary may serve different audiences that have different needs. For example, private buyers will be primarily profitmaking organisations when acting as single buyers of local produce. Nevertheless, because of its cluster position as a seller to an exporter, there may be also incentives for it to act as an intermediary and provide collective services to small producer that supply its raw material, thereby facilitating small farmers to “upgrade” in value chains (Raju and Singh, 2014). Other examples include private organisations but based on collective governance such as commodity boards and producer and industry organisations (Klerkx and Leeuwis, 2008; Ton et al., 2007; Watkins et al., 2015; Bijman, 2016; Luo et al., 2017). Organisations may also adopt multi-functions where the clusters are being orchestrated by a shared leadership and different intermediaries are active (Kilelu et al., 2013; Parag and Janda, 2014; Stewart and Hyysalo, 2008) meaning there is not a single lead organisation/hub firm. In these cases, the activities of intermediaries may need to serve the same audiences but for different purposes and therefore new functions are assumed.

An analysis of intermediation should therefore incorporate ownership structures of relevant organisations, but a holistic account would view intermediary agency power as a relational capability, emanating from its deliberate function to coordinate and/or support the activities of communities of actors and to mediate between different interests (Medd and Marvin, 2004; Klerkx and Leeuwis, 2009). The relational feature of this activity means that how the intermediary relates to the structures and governance of local knowledge transfer in value chains and local clusters critical. Moreover, as we have argued, it is not completely clear that ownership structure provides a clear, singular or even dominant indication of behaviour. Organisations playing intermediary roles can be influenced by negotiated arrangements between firms and associations, civil society, corporate social responsibility initiatives in value chains, as well as activist and consumer pressure (Barrientos et al., 2011). Indeed, a more useful approach may be to see that organisational practices are likely to evolve from complex synergies (Rhodes, 1997) between actors that vie for similar spaces.

The case studies

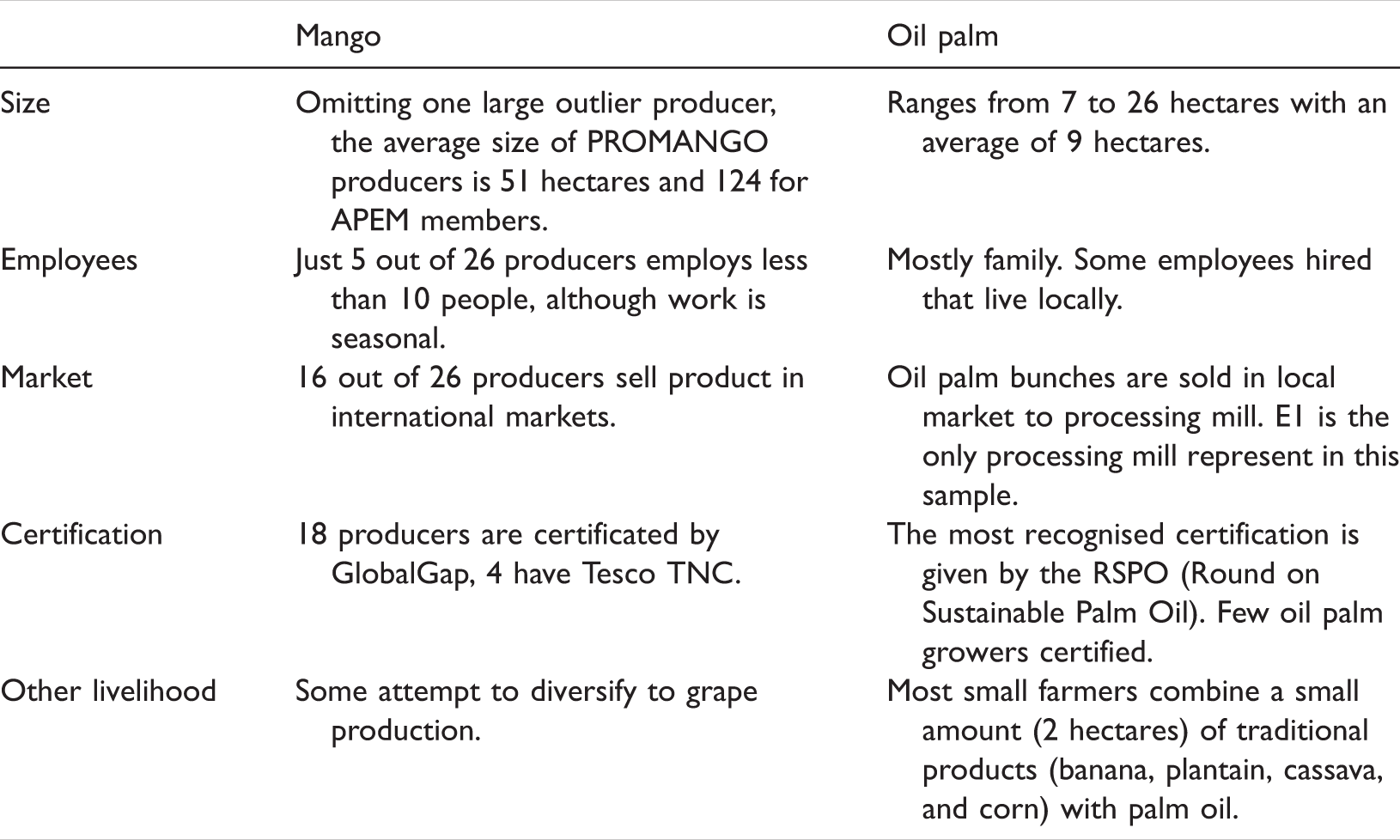

Detail of mango and palm oil cluster characteristics.

These clusters share a number of features. In both cases, there exist opportunities for penetrating large markets and a numerical dominance of small sized producers. The average size of the land for mango producer members of both producer associations is 51 ha and 9 ha for palm oil producers. Nevertheless, we agree with Fernandez-Stark et al. (2012) that what defines a small, medium and large producer in different products is heterogeneous and producers have different levels of development that require support. In our case, we distinguish small producers through their reliance on larger producers for access to markets. A key competence in the mango is reaching certification standards necessary for exports, combating fruit plagues such as fruit fly, incorporating a greater control and improvement in the detail of production processes and technologies and establishing networks with a range of buyers from different export markets. In both clusters, the main responsibility for upgrading and development of capabilities is the responsibility of local institutions (including intermediaries). However, as a key cash crop productive sector, the mango cluster in Peru has benefitted from direct government intervention. This is through PROMPERU, a public private intermediary agency that helps producers of mango. The short window of production means that so far in Piura there are no large dominant firms, although there is a division between medium-sized firms that produce and export and smaller producers that only produce and sell their products to the medium sized firms (Clarke and Ramirez, 2014). The strong tradition of mango production in the area is represented by two producer associations. These are APEM, the association of exporters who are also producers, and PROMANGO that organises small producers without direct access to exporters. Members of both associations make up around 30% of growers and 60% of production and form the centrepiece of the study, although key organisations at local level include SENASA, the phytosanitary government body and other service organisations play important roles. The producer organisations rapidly assumed an important space for intermediation, including small producers that achieved a degree of self-organisation through PROMANGO. The primarily focus in the mango is reaching international certification and accessing global markets. Eighteen of the producers included in this study are certified by Global Gap and four firms have Tesco certification.

In the case of the Colombian palm oil, the main feature is the growing importance of small producers as a proportion of cultivated land. The industry was traditionally dominated by 50 large oil refinery firms, however in 2012 18.7% of the palm oil land was cultivated by small producers (through “alliances” of producers in local clusters – predominantly small farmers – and in farms of less than 20 hectares in size), up from 3.7% in 1999 (Gomez, 2012). The result is that the relationship between firms has changed, with large firms increasingly dependent on purchasing from small producers. Secondly, as with the mango, the sector has experienced excess demand as a consequence of the rise in domestic demand for bio-fuel and the spread of the Pudricion del Cogollo (PC), (translated but root disease) an airborne disease that has wiped out large numbers of palm trees. In the palm oil sector, few growers are certified, this being less important as the product is processed before sold on the market. As will be discussed, the need to deliver the fruit quickly to the refinery after it has been cut means small producers will be located close to refineries that are in relatively close proximity. Hence, the intermediary is often a private refinery organisation that, apart from being a buyer, has had to assume the provision of some collective services with the guidance of the technology arm of the palm oil federation, CENIPALMA, through a scheme termed UATTA, whereby large firms provide extension services. This represents a significant formalisation of the role of the private firm as an intermediary. These two cases were therefore chosen because they allow an examination of the influence that the different ownership structures of intermediaries can have on cluster practices and upgrading, and the role that local governance within the cluster plays in mediating intermediary influence.

Methodology

Our principle research question is how the process of upgrading of small producers in agricultural clusters is influenced by intermediary organisations and how this influence is conditioned by existing local governance relations. We discuss the proposition that the ownership structure of intermediaries plays an important explanatory role in how intermediaries intervene, but insist that the evolution of network structure of the cluster will influence both the types of intermediaries that exist and which of these assume key positions as measured though their centrality. Therefore, the engagement, impact and even existence of the intermediary will emerge from a complex and contingent mix of entities and structures. The data collection occurs in two agribusiness clusters in Colombia and Peru that share some characteristics but contrast in terms of inter-producer structures especially in regard to the levels of producer organisation (detailed below).

The basis of our comparison is through patterns of inter-producer governance as demonstrated in the network structure. Social network analysis (SNA) is used to provide a structural analysis of the position of actors in the cluster and their relationships (Wassermann and Faust, 1994). This allows us to observe which intermediaries are more central and which are marginal and infer through the links they establish the influence they may have on other actors. The analysis also provides information on the influence and position of other organisations in the cluster (further details of SNA analysis below). The second stage of the analysis involved interviews with key organisations, i.e. those that network maps showed as important “brokers” (bring knowledge into the cluster by establishing links outside the cluster) and “bridgers” (consolidate links between actors in the network) (see below of details of actors interviewed).

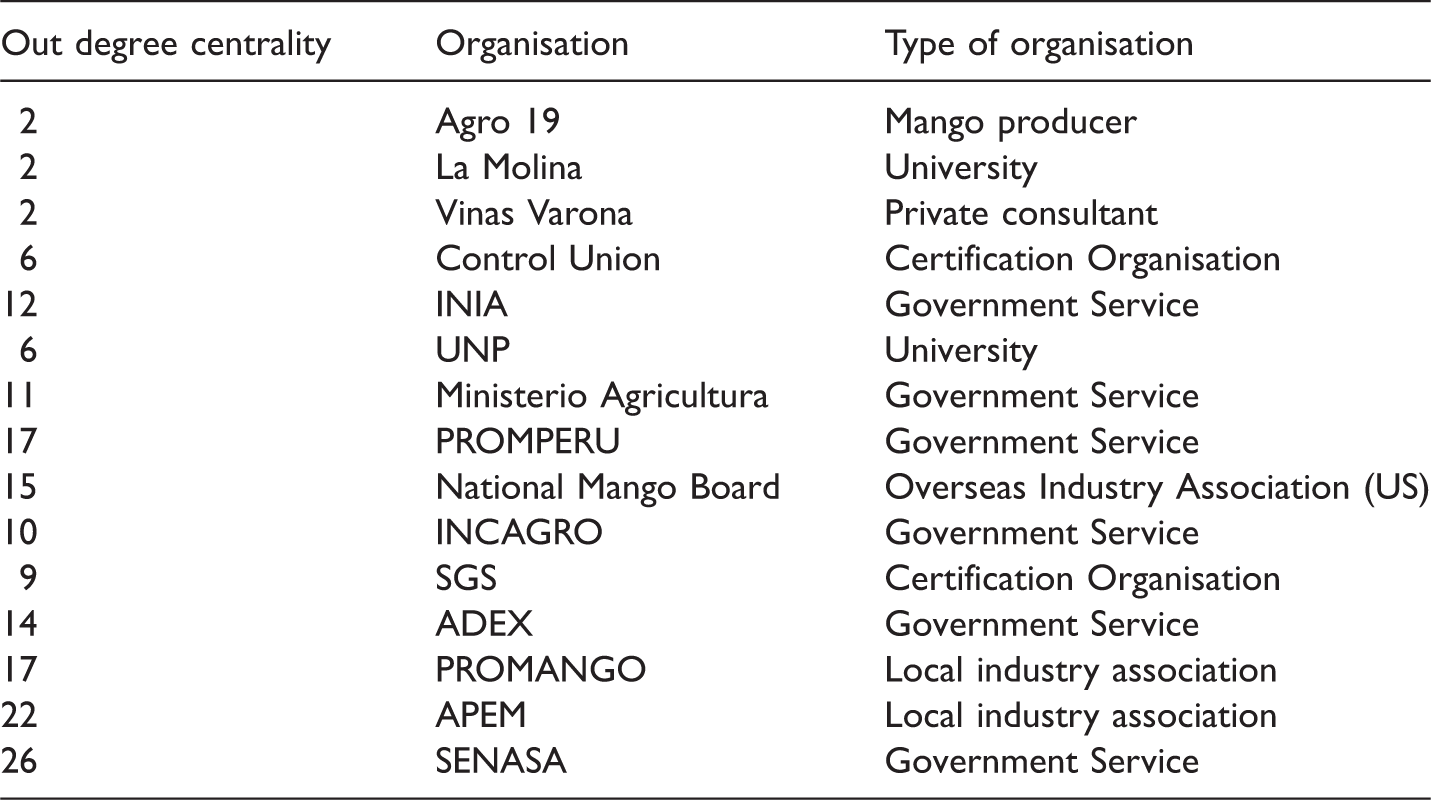

The information for the SNA was gathered through two identical surveys, one for producers (17 in the palm oil, 26 in the mango cluster), and one for service organisations (9 in the mango cluster, 5 in the palm oil). Analysis of survey data was undertaken through SNA techniques that permit visualisation and measurement of the structures of relationships and the strategic of positioning of actors in these relationships. The question asked to firms was: “from whom did your organisation (or business) receive technical assistance and how important was this to your organisation”? Respondents were provided a list of organisations (producers, services, universities, consultancies) and an open section to name other 15 organisations from whom assistance had been received and to then identify and rank organisations from whom assistance was received from 1 to 5 in ascending order of importance. From this information, it was possible to produce a network map using open source software, Pajek, for SNA.

The interviews in the palm oil cluster involved two ground visits in Colombia and eight semi-structured interviews. Because of the reduced numbers of actors present in the palm oil cluster from which SNA information was gathered, these interviews included representatives of large refinery firms and small producers of two palm oil clusters adjoining the cluster that is the focus of the study. Although SNA was not conducted in these, the interview suggested a similar network structure, i.e. a dominant refinery firm surrounded by a number of small level producer suppliers. Interviews were also conducted with high-level officials of two key intermediaries, CENIPALMA and FEDEPALMA. FEDEPALMA is the Colombian palm oil’s official producer association, whilst CENIPALMA is the technology arm of FEDEPALMA. Two interviews were conducted with CENIPALMA employees working in the field, one of whom was also shadowed over two days in the same palm oil cluster that was surveyed. Two interviews were also held with small farmer representatives and two interviews also took place with executives of large palm oil companies. In the case of the mango cluster, twenty semi-structured interviews were held with owners of small and medium-sized mango firms and directors of the main intermediaries including APEM, PROMANGO, the producer associations and with PROMPERU. The producer association congresses of APEM and PROMANGO were attended in Piura and detailed notes made as observers. We are therefore able to study three types of intermediaries: public–private, producer associations and private organisations. The purpose of the interviews is three-fold. They provide background information on the challenges and strategies of each cluster and technologies used. Secondly, by looking at the network maps produced in the first stage of the analysis and the resulting structure of networks, we can infer certain patterns concerning the governance of inter-cluster relations (e.g. hub and spoke) which can then be validated and explored in more detail through interviews. Finally, the interviews can focus in detail on the intermediary as a provider or services and on users as consumers (i.e. producer firms) of these services and their impacts. Open questions were used to guide the background to the clusters, semi-structured questions were used to define questions on cluster relations and the intermediaries.

Findings from social network analysis

Centrality of knowledge providers in the mango cluster.

Centrality of knowledge provides in the palm oil cluster.

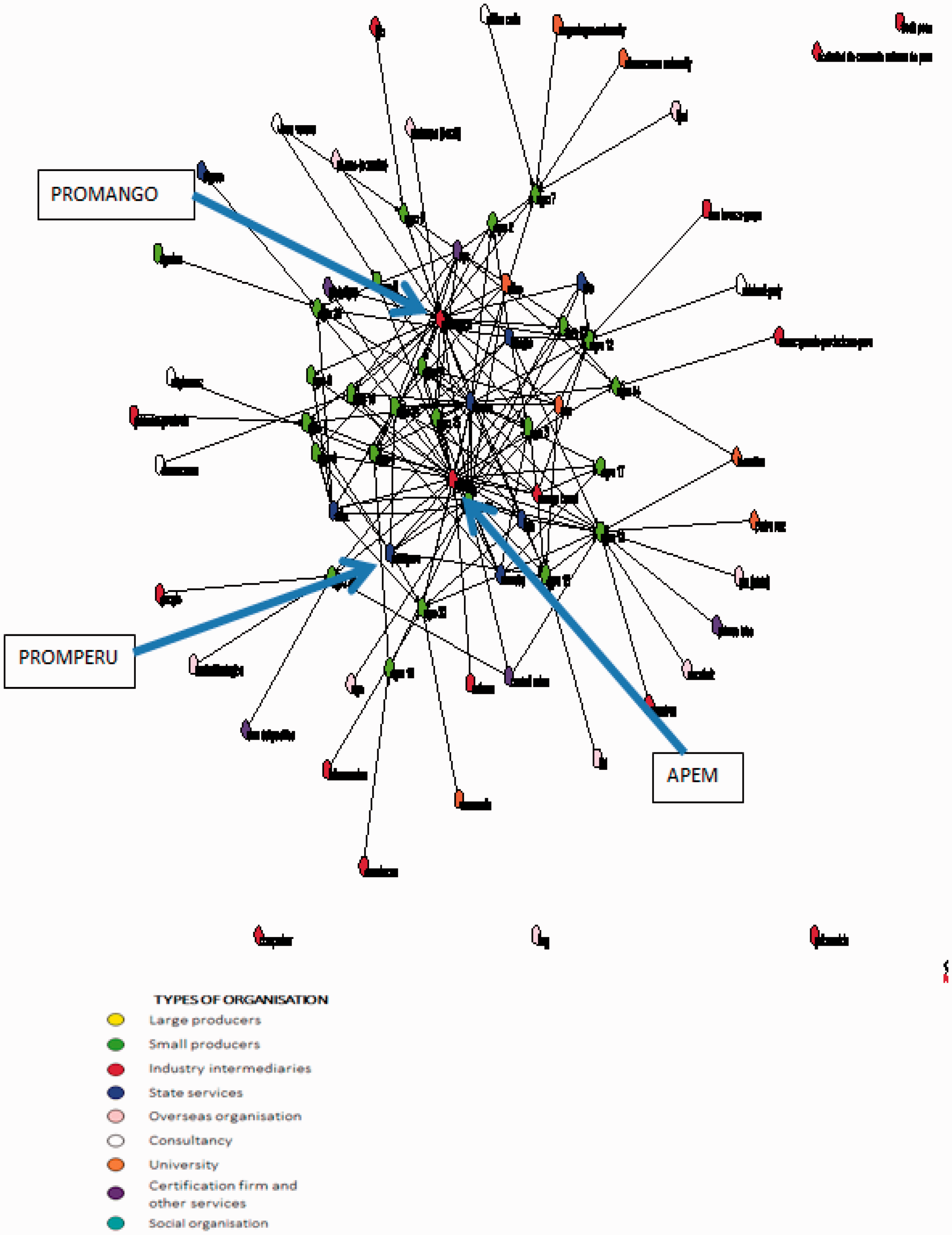

Figure 1 provides a network map of the entire cluster. APEM and PROMANGO are clearly shown at the centre of this network, receiving knowledge from a wide range of organisations and linking together small producers. PROMPERU by comparison is in a more marginal position. We focus the discussion on the cases of the two dominant producer associations, APEM and PROMANGO, and PROMPERU as a PPG organisation.

Social network analysis map of the mango cluster.

Our discussion centres on the influence and position of the three intermediary organisations: APEM, PROMANGO and PROMPERU. PROMPERU (The Commission for the Promotion of Peru) was established in 1993 and although it is dependent on the Ministry of Commerce, it acts as a public–private organisation through its provision of both financial and organisational support to exporting organisations. Its directorate is made up of a mix of public and private sector representatives. The organisational structure of PROMPERU reflects two important principles in the Peruvian political discourse as put forward by a succession of Peruvian governments. The first is to promote export-led growth in the Peruvian economy and secondly to make this growth inclusive of poorer groups of society.

PROMPERU has worked in several agricultural sectors encouraging knowledge transfer and industry organisation needed for export success. In addition to accessing commercial intelligence, it works with industry actors on market penetration strategies. It also has a special emphasis on supporting SMEs as this is recognised as an important sector within the Peruvian economy. PROMPERU’s most influential period in the mango cluster was at the end of the 1990s when it used its links to open up the international markets for mango producers. Initially, it attempted to establish one local association for all mango producers as a single point of contact for the industry to lower costs through economies of scale and a route to encourage cooperation and joint learning. However, this failed and seed money was provided firstly for APEM and shortly afterwards PROMANGO. According to a PROMPERU representative, the separation of producer organisations had little to do with commercial needs. As a PROMPERU manager commented: if you are seeking to export then you are working with huge companies, they are asking for volume and they are asking for quality…if you are not well organised then you do not have any chance at all of entering international markets. They (APEM and PROMANGO) do not have a different strategy, and they do not have a different way of proceeding.

The experience of PROMPERU highlights the importance that a PPG intermediary can have by supporting collective action among different groups of producers, including those reliant on small-scale production. Its mission is defined by the need to open up the cluster to new markets, combining business acumen with commitment to support niches as well as commodity production and markets. PROMPERU therefore created the formal outward facing network links that has transformed this region into an export hub. Nevertheless, as our network map suggests, the internal architecture of this network has reproduced rather than replaced the historical structural cleavage between medium-sized direct exporters and small producers. Once the export supply chains became established, PROMPERU’s role became more peripheral and the producer associations APEM and PROMANGO assumed the main coordinating roles.

A defining feature of APEM (Peruvian Association of Mango Exporters) is its strong commercial and business focus, which is a reflection of the pioneering export firms that first set it up. Its core competency is helping grower firms serve international export markets, primarily the USA and Europe. In its early days it worked on improving the infrastructure, including the port of Paita which serves the Piuran cluster. Since the mid-2000s, APEM has, with support from PROMPERU, developed markets in East Asia including Japan, China and, since 2014, South Korea. This has involved moving into better packaging and more general product aesthetics through the selection of the Kent mango variety for export to South Korea. A major step forward has been the establishment of a Standards Committee in the early 2000s, made up of exporters, producer representatives and a local university researcher that meet regularly and evaluate international quality norms for mangos. It produces a “technical norms” document for producers, providing guidance on sweetness level, fibrosity and colour in addition to specifying maximum limits for pesticide contamination. APEM has been particularly effective at preventing the flooding of the US market and subsequent fall in prices by coordinating with other mango exporters in South America to monitor volumes being released for export. The market intelligence it obtains is closely guarded and treated as secret, accessible only to APEM members.

As a representative for medium-sized larger exporters, its governance reflects its member’s commercial interests. There has been some fundraising to facilitate certification of small producers (that sell to APEM members), but engagement with PROMANGO for example is minimal and quality development centres on consolidation and vertical integration, rather than through an inclusive-based network. Indeed, a number of APEM firms have acquired land from small producers.

Like APEM, PROMANGO is a producer association that was formed in 2002 with seed money from PROMPERU. Unlike APEM, it represents smaller producers that have little direct access to international markets. PROMANGO members have had difficult relationships with larger exporting firms over a number of years and this was crucial in shaping how PROMANGO was constituted. Its members are primarily concerned with the challenges of producing (rather that selling) for the export market under difficult soil conditions and an erratic local climate. Much knowledge is tacit. The annual congress of PROMANGO is dominated by discussion of treatment of diseases, management of fruit and diversification into other products. These practices have spawned a strong sense of community and as a result, the actions of PROMANGO are primarily based on strengthening the network of producers and enhancing collective actions. For example, the first hot water treatment machine was purchased between all members and its use is shared by all members of the association. PROMANGO therefore has played a critical role as a bridge builder for previously fragmented producers. As the director of PROMANGO stated: the situation before was that all of the producers felt that they had the secret for producing good mangos, and they didn’t wish to share it with anyone…. Through forming PROMANGO, we started to share all types of information, group together what each firm was doing, and in this way we created a network between the organizations members.

The discussion of the mango cluster highlights cluster evolution as the outcome of new opportunities, ongoing tensions between groups and negotiations between intermediary organisations. Rather than imposing a set of top-down solutions as might have been the case in the past, the state has intervened to “steer” a set of cluster actors towards the international market. The resulting cluster structure mirrors entrenched structures of power and is reflected in the creation of two networks around APEM and PROMANGO. APEM’s business orientation is outward looking and emphasises cross-cluster cooperation but does not represent the cluster as whole. Indeed, the asymmetry of information between large and small-sized producers has actually been magnified, as small producers remain vulnerable to climate and price fluctuations in a way that large and medium firms have been able to insulate themselves against. Hence, the historical fragmentation has become more entrenched through the development of APEM. The influence of PROMPERU has been constrained by resource limitations, geographical distance and the difficulties of working in a cluster with a complex power structure. Nevertheless, it has used its position to make the small producer networks visible and to carve out an independent route for access to international markets. 2 Without PROMPERU’S aid, small producers may well have remained on the margins of the network.

The Colombia palm oil cluster

Colombia is the world’s 4th largest producer of palm oil. However, unlike production in Malaysia and Indonesia that is dominated by large firms, the mutual dependence (and tensions) between small producers and refinery organisations is critical to understand the palm oil industry in Colombia. As discussed above, at the time of the interviews, knowledge transfer around new technologies and new organisational practices has been dominated by the spread of the PC (translated but root disease), an airborne disease affecting tropical climate areas that has wiped out large numbers of palm trees. Large resources, including R&D spending by CENIPALMA, have been devoted to developing alternative disease resistant trees and prevention measures to stop the spread of the PC. Upgrading therefore is dominated by the processes of preventative management of this phytosanitary disease control that can strongly impact quality and efficiency of the palm oil fruit.

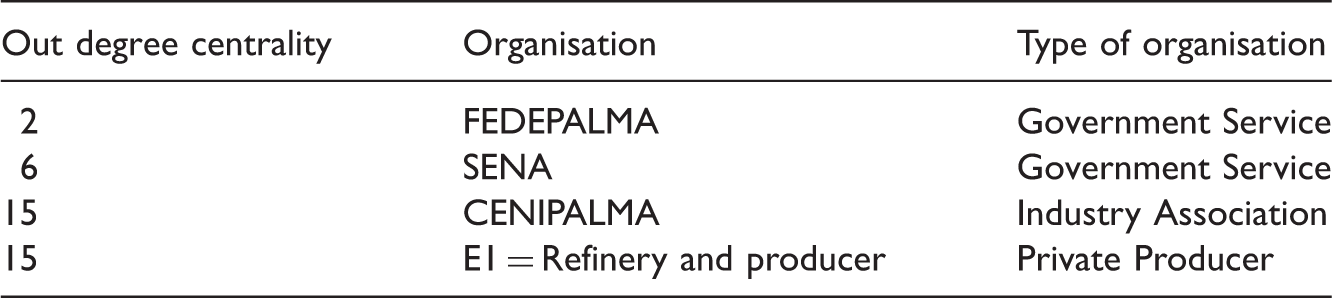

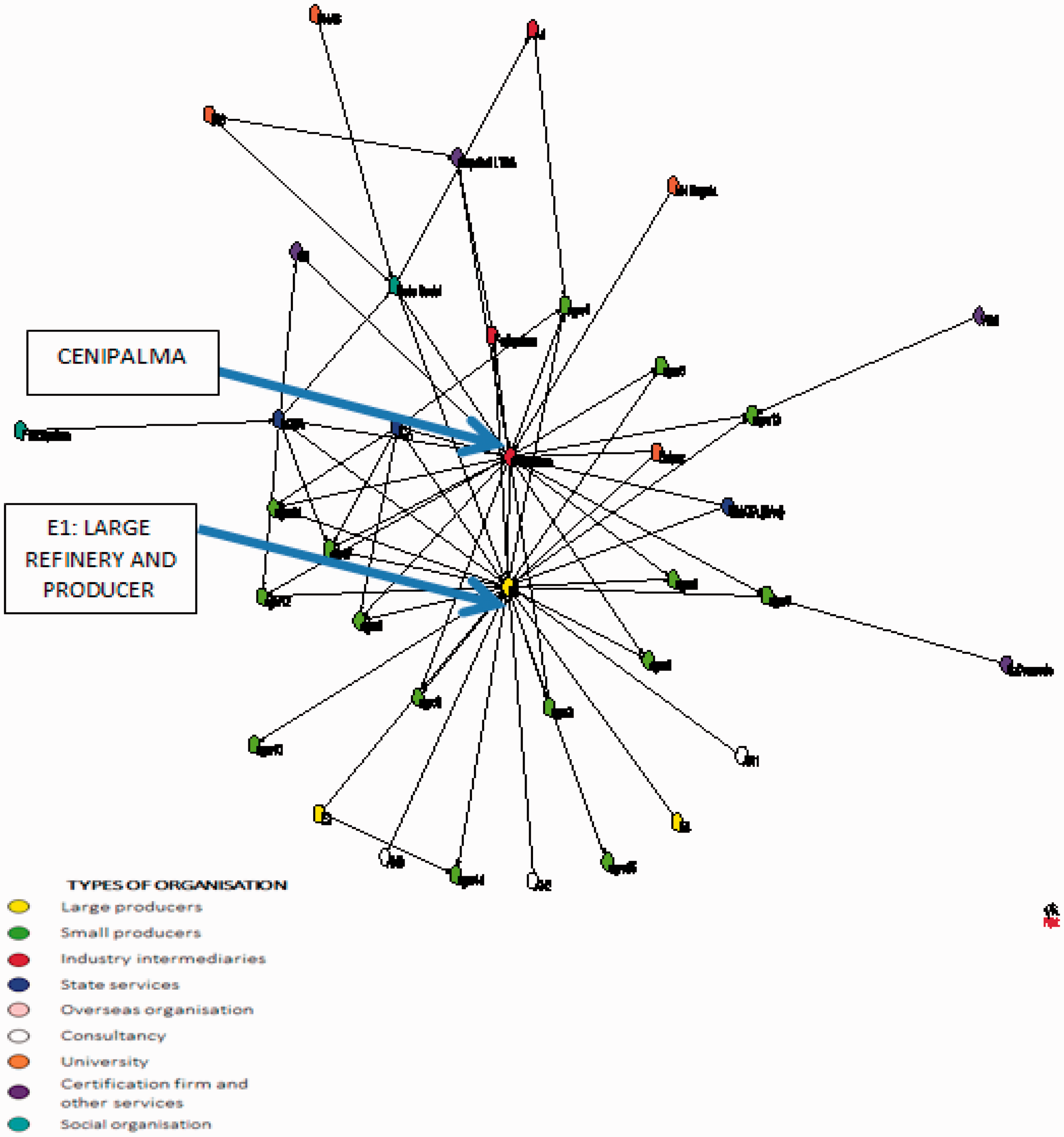

Critical to the adoption of this protocol is the “UATTAS”, the national institutional architecture drawn up by CENIPALMA for technology transfer. This involves creating an alliance between small producers and a neighbouring refinery firm for preventative treatment of trees and vigilance. Each UATTA is supported by one agronomer per 3000–5000 ha and one technical assistant per 1000–1500 ha and involves provision of technical services, including adoption of ISO 9000 certification. The refinery firm acts as the intermediary for the small producer, transferring practices from CENIPALMA. Technology transfer therefore is designed in a top-down manner. The network architecture of the palm oil cluster in Figure 2 shows this clearly. There is a refinery organisation that we call E1 in the middle of a network of small producers. CENIPALMA, the industry association, brings knowledge in from outside the cluster and provides knowledge to E1 and has a direct link to some of the small producers. In contrast to the mango case study, the palm oil cluster shown in Table 3 and Figure 2 therefore shows a simple hub and spoke structure with information largely centralised around two nodes. The small producers are almost totally dependent on E1 for access to new knowledge. Moreover, there are very few bilateral links between the organisations themselves.

Social network analysis map of the palm oil cluster.

We focus the discussion on the role of the industry association CENIPALMA and the refinery firm E1 as intermediaries in the knowledge transfer process with small producers. As indicated earlier, the programme of technology transfer has been designed by CENIPALMA. Its national coverage allows it to transcend narrow local interests and it has advanced international cooperation agreements with palm oil related centres of excellence around the world. The 2015 international palm oil congress held in Cartagena in Colombia brought together 1700 practitioners, 100 company representatives and expert speakers from 30 countries. Ninety percent of the speakers were from overseas. CENIPLAMA has a specialised R&D laboratory in Barrancabermeja staffed with postgraduate technicians and is recognised as one of the top science centres in the country. It also has agricultural extension staff with specialised knowledge in Palm oil and the technicians are therefore strongly embedded in the sector. There is little representation of small producers in CENIPALMA or FEDEPLAMA, its sister organisation, as most of the subscriptions are made by large refinery firms.

The UATTA framework for technology transfer reflects an effort to rationalise the fragmented nature of technology transfer in Colombia with many small-sized producers. This means there is high reliance not only on agricultural extension workers in the different areas of the country, but also on technical specialists employed by the refinery firms. Although these are employees of the refinery firm, this is a potential win-win situation for large and small producers. Refinery firms receive a steady supply of raw material from small producers, who in turn receive technical assistance to improve productivity and disease prevention. CENIPALMA states that there are currently 100 “strategic alliances”, in so-called “inclusive business” partnerships (Córdoba, 2011). However, a major problem is that “the technical teams in the plantations do not work as a strategic unit, but rather as individuals” (Córdoba, 2011). This reflects the difficulties of establishing uniform norms in highly contrasting climate and soil conditions, but also the diverse local relations between small producers and refinery firms.

The case of E1 is perhaps most significant since this is a privately-owned organisation that has been drawn into acting as an intermediary for surrounding producers through the provision of collective services (e.g. agricultural extension, financial loans). Its role needs to be considered in the light of the changing relationship between large landowners involved in agroindustry (some of whom have historically been based in the palm oil, others that have diversified into the sector from livestock or bananas) and subsistence farming. 3

In our interviews, we were able to discern contrasting attitudes by the large refineries towards their intermediary functions. Figure 2 demonstrates the case where the large refinery firm has stepped in to assist small farmers in the adoption of new techniques and other assistance such as the provision of bridging loans and donations to local community schools. It is this model that CENIPALMA has hoped to institutionalise across the industry based on the close physical proximity between refinery firms and small firms. However, as intimated, a feature of the industry is the uneven geographical pattern of relationships between firms in cluster. As a CENIPALMA official commented: There are some nucleos where the leading company is only really interested in buying the fruit, it is not interested under which conditions this is produced, but there are cases of projects such as Indupalma, where there is a contract between the anchor firm and where the whole sanitary scheme is run by the anchor firm, the ally is just waiting to pay off the credit and they then take charge of their plantation. So in some places it is working in others it hardly exists…this is very new and requires a change in the scheme of things.

However, it is also common for refinery firms to show reluctance to involve themselves in national institutional agreements to provide collective services. This view was underlined by an executive of a neighbouring refinery firm that, when asked to intermediate for small producers commented: We don’t feel responsible for their survival, and small producers don’t see us as having the authority to make them. In sanitary terms, it has to be done via the scheme we developed that unifies criterion. Everybody has to speak the same language. So if there is a user and he says “I have this experience of working on this disease”….no sir, we are not going to do that, we have to follow the norms developed from the agronomic committee. We have to have a unified criteria.

The intermediary actions of the privately owned refineries reflect a combination of pressures and expectations. Expectations exist for refineries to step in and help small producers introduce preventative practices to stop the spread of the PC disease because they are indeed the only organisation at local level with the resources to able to work with small producers. Nevertheless responses vary. Some refineries clearly recoil at the attempt to formalise their role of intermediaries (perhaps following past experiences of less than loyal small producer allies 4 ) and because it gets in the way of their core activities. Other refineries will undertake the provision of collective services in a paternalist fashion to create reciprocal local ties.

The provision of intermediary services therefore reflects the ownership of the intermediary, but also industry expectations and the history of local relationships between refinery and small producers. Ownership structure therefore is an important factor, but so are local traditions. The absence of a tradition of collective organisation means paternalism is often prevalent.

Discussion and conclusion

This paper has provided an account of the agency of intermediary organisations in a social space defined by clusters of agricultural producers related by networks of production and differing degrees of dependency. In terms of the research questions posed at the beginning of the paper concerning intermediation and upgrading, although in both case studies intermediaries are critical actors for the provision of collective services, it is also clear that the extent, nature and scale of upgrading is linked to the type of organisation providing intermediation and how it influences inter-producer governance relations. Ownership structure and the position of the intermediary in the cluster plays a significant role in this process. Taking first the case of the mango cluster, a significant feature is that all intermediaries facilitated in opening up the clusters to opportunities for radical changes in production strategies, which resembles findings elsewhere on the contribution of intermediaries (e.g. Kilelu et al., 2017a). PROMPERU, the public–private intermediary, was indeed a crucial change agent. It advanced the broader government agenda to open the mango cluster, assisted in upgrading and improved inter-cluster coordination. Nevertheless, it was the producer associations, APEM and PROMANGO, that played the main role in helping to build the capabilities to enter the export markets. Their source of legitimacy (and ability to do this) derived partly from their role as the principle agent of the communities of producers, but also from the fact that, unlike PROMPERU, these organisations are deeply embedded in the cluster and the relationships between producers. However, as might be expected, these producer associations also replicated rather than transformed the basic architecture of the network, reproducing the traditional knowledge asymmetries between larger producers with direct access to exporters and smaller producers. Direct exporters will therefore have advantages in terms of upgrading in specific features of this value chain. On the other hand, PROMANGO, because of its strong intermediary agency role is in a strong position to search for and open up alternative upgrading strategies in different value chains such as ethical trading. These would have significant implications for inter-producer governance relations.

The second case of the Colombian palm oil case also highlighted the critical role of the intermediary for knowledge transfer and capability building, but with a privately owned firm and in a context of weak small producer self-organisation. The private palm oil refinery firms sits at the centre of a highly centralised network structure in which sharing experiences and learning-by-doing between the large firm and smaller producers to combat the phytosanitary disease is critical to the survival of all actors in the cluster. The style of intermediation is based on paternalism and reciprocal favours. The firm, E1, moreover is clearly not comfortable with the formalisation of its intermediary position within the palm oil system. In other words, it provides collective services but within a governance framework that reflects its ownership mission. Major changes in governance in this top-down context are unlikely to occur. We conclude the discussion with two points that reflect the broader theoretical implications of our findings. The first is that although intermediaries clearly work across boundaries and between different actor groups and can potentially help to break down insularity, their actions will also be influenced by existing governance relations between incumbent actors. The most significant differences in our study concerned the ownership structure of intermediaries and level of small producer organisation. Consequently, the contribution and ultimately the impact of intermediaries emerged from the negotiation between the interests and pressures that these factors exercise. This is a point supported by other studies such as Yang et al. (2014). Secondly, and following from the previous point, the discussion also highlighted that it may be wise to eschew classifying intermediary organisations into narrow definitions, roles, categories and indeed impacts. Our discussion of intermediaries provided information of the different roles and potential impacts these organisations can have in the clusters. A similar point has been made by Howells (2006) who highlights the varied roles and functions of intermediaries in innovation, but also the range of more traditional service activities they often undertake. Our study is in line with these conclusions, but in addition points to ownership, inter-producer governance relations and embeddedness as factors that influence intermediary functions. The implication is that, rather than forcing fixed labels and narrow functions (and impacts) to an intermediary, more holistic approaches can provide more fruitful avenues to future studies.

In the terms of the advantages and limitations of the methods used in this study, the use of both SNA and qualitative methods in this study is novel and provides a broad canopy to investigate intermediation within a specific context that includes structural relationships between cluster actors, the governance relations that underpin these and the embeddedness of intermediaries within these relations. Nevertheless, it is clear that more research within the context of development and agriculture is necessary before moving to typologies of how agribusiness cluster structures relate to different forms of intermediation.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors acknowledge the support of CENIPALMA, APEM and PROMANGO for the production of this paper and the financial support of the British Academy for the study of the Peruvian mango cluster. We are also indebted to the anonymous reviewers for their valuable comments.