Abstract

This paper examines vulnerability in the context of affluence and privilege. It focuses on the 1991 Oakland Hills Firestorm in California, USA to examine long-term lived experiences of the disaster. Vulnerability is typically understood as a condition besetting poor and marginalized communities. Frequently ignored in these discussions are the experiences of those who live in more affluent areas. This paper seeks to more closely explain vulnerability at its interface with affluence. The aim is to challenge uncritical explanations of vulnerability. We also offer alternative ways of conceptualizing vulnerability as a material condition and social construct that acknowledges broader cultural, ecological, and economic conditions, which may offset, maintain or deepen true risk exposure. Drawing on in-depth interviews with residents and emergency service managers, the paper presents a suite of vulnerability categories that intersect to create two concomitant and competing conditions. First, vulnerability is variegated between households within communities, including those in more affluent areas. Second, household vulnerability is collectively altered, and oftentimes reduced, by the broader affluent community within which individual households reside. By paying closer attention to the Affluence–Vulnerability Interface the paper reveals a recursive process, which is significant in the context of building more disaster resilient communities.

Introduction

This paper examines vulnerability in the context of affluence and privilege. It focuses on the 1991 Oakland Hills Firestorm in California, USA to examine the long-term lived experience of the disaster, which led to the loss of 25 people and more than 3000 homes over a 24-hour period on 19 October 1991. The aim is to challenge uncritical applications of vulnerability. We also offer alternative ways of conceptualizing vulnerability as a material condition and social construct that acknowledges broader cultural, ecological, and economic conditions, which may limit, offset or perpetuate true risk exposure. A corollary and more general objective is to better understand the complex, yet mutually constitutive relationship between vulnerability and wealth.

For the purpose of this paper, “vulnerability” is understood as being constituted by “components that include exposure and sensitivity to perturbations or external stresses, and the capacity to adapt” (Adger, 2006: 270). Vulnerability is a condition that is held by, and internal to, individuals or communities: it is embodied, experienced and lived (Sword-Daniels et al., 2016). In this sense, vulnerability is contextual (Cutter et al., 2003; O’Brien et al., 2007). Exposure measures the likelihood that, for example, a wildfire will affect a household, while vulnerability refers to the internal susceptibility of that household and illuminates the level of harm and trauma that family will likely experience. Thus, vulnerability at the household or individual scale is commonly understood as being a function of: (1) threat exposure, (2) sensitivity (e.g. disadvantages, disabilities or pre-existing impairments that might influence how an external stress is experienced) and (3) adaptive capacity (e.g. the presence of financial and social capital that may ease or challenge the recovery process) (Adger, 2006; Wisner et al., 2004). This stands in contrast to “risks,” which may be understood as the processes, conditions, events, and activities that comprise threats, destabilizations, and negative exposure to households and social groups. In other words, as risks increase (to fire, for example), those with elevated levels of vulnerability will likely experience risks and their long-term effects more directly and acutely. We argue here that amidst affluence and privilege, vulnerabilities to fire-related risks are substantial, diverse between households, yet significantly mediated by underlying economic and political resources at the community level.

The 1991 Oakland Hills Firestorm (also known as the Tunnel Fire)—located in the East Bay Area of San Francisco, California—is an important case study of urban growth, loss, and regrowth in a densely populated area of the USA (Figure 1). While known even in 1991 as an affluent area, local residents at the time were soon to witness extraordinary post-fire real estate value increases. This increase in wealth accumulation is linked to the ways in which the area and neighborhoods recovered and rebuilt, despite the 1991 firestorm to this day being the largest and most expensive wildfire (ca. $1.5 billion) in California’s history in terms of dwellings destroyed (Figure 2).

Location of the 1991 Oakland Hills Firestorm (also known as the Tunnel Fire), California, USA (map credit: Peter Anthamatten). Looking east late October 1991: an aerial panorama captures a portion of the fire area. The blaze began near the upper left hand corner of the image and stretched out of view in all directions (photo credit: Cal OES).

The process of growth, loss, and regrowth has been labeled “upward social succession” (Davis, 1998: 108). It begs the question, what it actually means to be vulnerable to wildfires in urban peripheries comprised by communities holding a level of overall affluence and privilege higher than the average urban neighborhood (particularly in the context of post-fire reconstruction)? These are living standards that lead many to take a less than sympathetic view of residents living in fire-prone areas—a perspective, for example, that influenced Davis (1995) to posit “the case for letting Malibu burn”. For these critics, many suburban residents appear to take on a level of assumed risk. This means that homeowners know fire hazards are a distinct possibility when moving into areas such as the Oakland Hills. Over the previous century, 12 wildfires occurred within close proximity to the footprint of the 1991 firestorm (Simon, 2014). This stands in contrast to imposed risks, which involves the imposition of unexpected threats that emerge without prior knowledge by local residents—risks that may derive from sudden planning decisions that drastically alter the rate or severity of hazard exposure for community members.

Paying closer attention to the different ways vulnerability and affluence interact reveals a recursive process that is significant in the context of building more disaster resilient communities. To better accommodate this recursive process in debates on how to coexist with wildfire at the interface between cities and beyond, we suggest a shift away from a place-based designated framework—the wildland–urban interface (WUI), which tends to focus on human–environment conflicts (Radeloff et al., 2005). Instead, we propose a process-based designated framework—the Affluence–Vulnerability Interface (AVI), which we use as a construct to contextualize risk and vulnerability within intersecting social characteristics and engrained norms. This broadens understandings of resident and community activities, needs and experiences in the context of complex disaster (or other destabilizing) events.

The paper is divided into five sections. First, we contextualize the study using theoretical frameworks on vulnerability and risk to illustrate how vulnerability is variegated between households and communities exposed to hazards. Second, we provide an outline of the study area and the qualitative research methods applied. We then turn to an examination of the diverse manifestations of risk and vulnerability revealed during in-depth interviews. This is followed by an analysis of collectivized risk and vulnerability reduction—a prominent theme in participants’ narratives. Finally, we conclude by considering if perceptions of risk and vulnerability help explain the willingness of many individuals and groups to transform and occupy high-risk landscapes, such as the Oakland Hills.

Contextualizing variegated vulnerability

Three theoretical frameworks—vulnerability-in-production, intersectionality, and unequal risk—inform our analysis of the interface between affluence and vulnerability. First, a historical-structural perspective illuminates how vulnerability and affluence are co-produced (Simon, 2016). Vulnerability is shown to be a recursive and relational process—embedded within disaster recovery as well as regional environmental and development histories. These are always in-production, at play, and inscribed unevenly over time and space. Vulnerability is thus much more than simply a planning ending, produced outcome or material inscription (Mustafa, 2005; Pelling, 2003; Wisner et al., 2004). While conventionally viewed as a negative condition experienced by discontented communities, a historical-structural perspective illuminates how vulnerability is generated within landscapes that are intentionally altered, developed, and maintained in a manner that retains their productivity or desired purpose for homeowners, developers, landholders, and city agencies alike (Collins, 2008, 2010; Simon and Dooling, 2013). Vulnerability thus both facilitates and results from market opportunism and private wealth accumulation.

Second, the study follows postcolonial intersectional analyses, prominent within feminist political ecology (Elmhirst, 2011; Rocheleau et al., 1996), to demonstrate how “relationships are shaped by particular regimes of cultural meaning that in turn shape social relations” (Mollett and Faria, 2013: 117). By explicitly integrating and examining the role of, for example, affluence and privilege, risk and vulnerability, age and disability within a single study, instead of just highlighting differences and disparities, it is possible to interrogate class and wealth not as a critique of upper-middle-class or asset-rich people. Instead, it recognizes class and affluence as a financial status that intersects with other cultural practices, identities and politics, which are based on ideological norms and are lived but often generalized and/or unacknowledged (Eriksen, 2014; Pease, 2010). Intersectional analysis allows insights into concomitant yet competing conditions. On the one hand it shows the way certain heterogeneities are hidden, for example, by the presence of individuals with the personal energy, means and ability to access crucial resources, which enable these individuals to improve the conditions of other community members. Some inter-household vulnerability disparities in the Oakland Hills were thus ironed out, creating an impression of wholesale affluence and privilege. On the other hand, it shows how certain combinations of attributes (e.g. age and disability) alongside affluence can activate and deepen levels of vulnerability. For example, during the 1991 firestorm, many elderly and/or disabled individuals were unable to reach the phone, open the door when emergency personnel door-knocked or leave their house to seek help.

Third, by “weaving chains of explanation into webs of relations” (Rocheleau, 2008: 716) our study heeds the call for a reevaluation of the concept of “risk as hazard exposure”, which Collins’ (2010: 285) presents as “a dialectical conception of risk that incorporates hazard exposure, social vulnerability, and relational processes of marginalization/facilitation”. By providing in-depth and first-person narrative insights, our study reconciles common shortcomings often found in comparative vulnerability analyses of lower socioeconomic versus affluent populations—a line of argumentation that oftentimes presents vulnerability as a condition that rests uneasily within, and in contradiction to, areas and communities of affluence and privilege. For example, analysis of the production of unequal risk before and after the 2006 Paso del Norte floods in the bordering El Paso County (USA) and Ciudad Juárez (Mexico), concluded that: “Many residents of the [affluent] Westside [of El Paso] may choose to live in hazardous locations. They do so only under the condition that state and market investments (in fixed capital, the consumption fund, and social infrastructures) are provided to maximize positive environmental externalities and minimize negative ones. While such households may be exposed to flood hazards, they are not socially vulnerable. Accumulated assets and privileged access to the social surplus facilitate their pursuit of lifestyle rewards in the face of danger.” (Collins, 2010: 282, italics added)

This paper, by using the frameworks of vulnerability-in-production, intersectionality and unequal risk, leverages the field of political ecology (and its intellectual roots in cultural ecology and feminist studies) to argue that vulnerability exists (and is therefore a valuable analytic subject) amidst conditions of more general, community-level affluence. We have given many presentations on this topic in university lectures, colloquia and public lectures, and in several instances audience members have raised questions about the validity of the claim that households in the fire-ravaged Oakland Hills can, in fact, be “vulnerable” (see also Wisner et al., 2004). This perspective tends to revolve around three assertions. First, these are households with considerable resources (such as home indemnification) to help overcome and recover from such trials. While it is true that such households will likely lose irreplaceable items to the fire, most will also hold full cost recovery insurance plans enabling the reconstruction of new, bigger and perhaps more valuable homes. Second, these residents knew there were fire risks when purchasing their property. So did they not assume this risk? This stands in contrast to imposed risks that afflict communities in unpredictable and unforeseen ways. Third, claims of hillside precariousness raise skepticism for some when contextualized within a world full of acute water and food insecurities, race and gender based violence, religious persecutions and pernicious economic injustices. Using the term “vulnerable” to describe residents in the Oakland Hills has the effect of watering down the term and rendering vulnerability as an analytically blunt social descriptor.

Political ecology presents a useful framework to challenge these broad criticisms because the field is premised on precisely the opposite set of a priori analytic approaches: the pursuit of fine-grained analysis of specific communities, households, and individuals for the purpose of assessing household differentiation, social interactions with changing environmental and economic systems (Robbins, 2004). This scaling down to local levels is meant to substantiate, challenge and/or overturn other explanations premised on more synoptic, “distant” and simplified analysis.

To be sure, we do not suggest that political ecology scholars generally support the notion that affluent communities cannot contain vulnerability. Most political ecologists are indeed clear that vulnerability is experienced differently across space. Broad social categories such as class, race, and gender cannot themselves explain levels of vulnerability. In fact, one of the hallmarks of political ecology-informed vulnerability analysis is its attention to the unevenness of vulnerability as it is manifest differentially at community, household and even individual scales (Watts, 1983). We agree with Wisner et al. (2004: 12) who argue that although class-based analysis is “too simplistic to explain all disasters … in general the poor suffer more from hazards than do the rich” and thus “vulnerability is closely correlated with socio-economic position”. This is why it is important to differentiate between the concepts of exposure and vulnerability, as acute sensitivities afflict poor and disenfranchised groups most directly.

We are therefore not arguing against a vocal faction within the political ecology community. Rather, our study is simply motivated by the relative silence given to forms of vulnerability operating in affluent areas. In this way, we are responding to what the expansive vulnerability literature is not addressing. The vast majority of research within political ecology that examines vulnerability—as a condition emerging from both exogenous economic and environmental forces as well internal structures of inequity—has been conducted in more marginal and impoverished areas. In light of this genealogy, and despite being sympathetic to these past and contemporary trajectories of vulnerability research, we seek to open further dialogue at the intersection of vulnerability and affluence in order to problematize how each exists and operates within and alongside the other.

In the following sections, we use a suite of categories to illuminate the topography of risks and vulnerabilities that characterize and delineate the experiences of individuals: from psychological to financial impacts both during and after the firestorm. With this understanding we see that broad-brush stroke descriptions of risk, which tend to characterize entire neighborhoods as vulnerable or not vulnerable, are both inaccurate and misleading. This paper provides a nuanced examination of the social fabric, as well as risk and vulnerability disparities, within this largely affluent Oakland Hills community. Teasing out such differences in the context of affluence, privilege, and risk offsetting resources (or the lack thereof) is important in California (and elsewhere) where decades of suburbanization and climatic change are increasingly exposing communities to frequent and intense wildfires (Dennison et al., 2014; Theobald and Romme, 2007).

Study area

Each year around the American West, news reports fill the airwaves with stories of devastating wildfires, shattered communities, lost lives, and costly reconstruction efforts. The state of California witnessed 8745 separate wildfire incidents in 2015 (NICC, 2016). These fires—many of which occur at the WUI—fan debates among scholars, governments and the public over why communities are constructed in such vulnerable landscapes (Jensen and McPherson, 2008; Moritz et al., 2014).

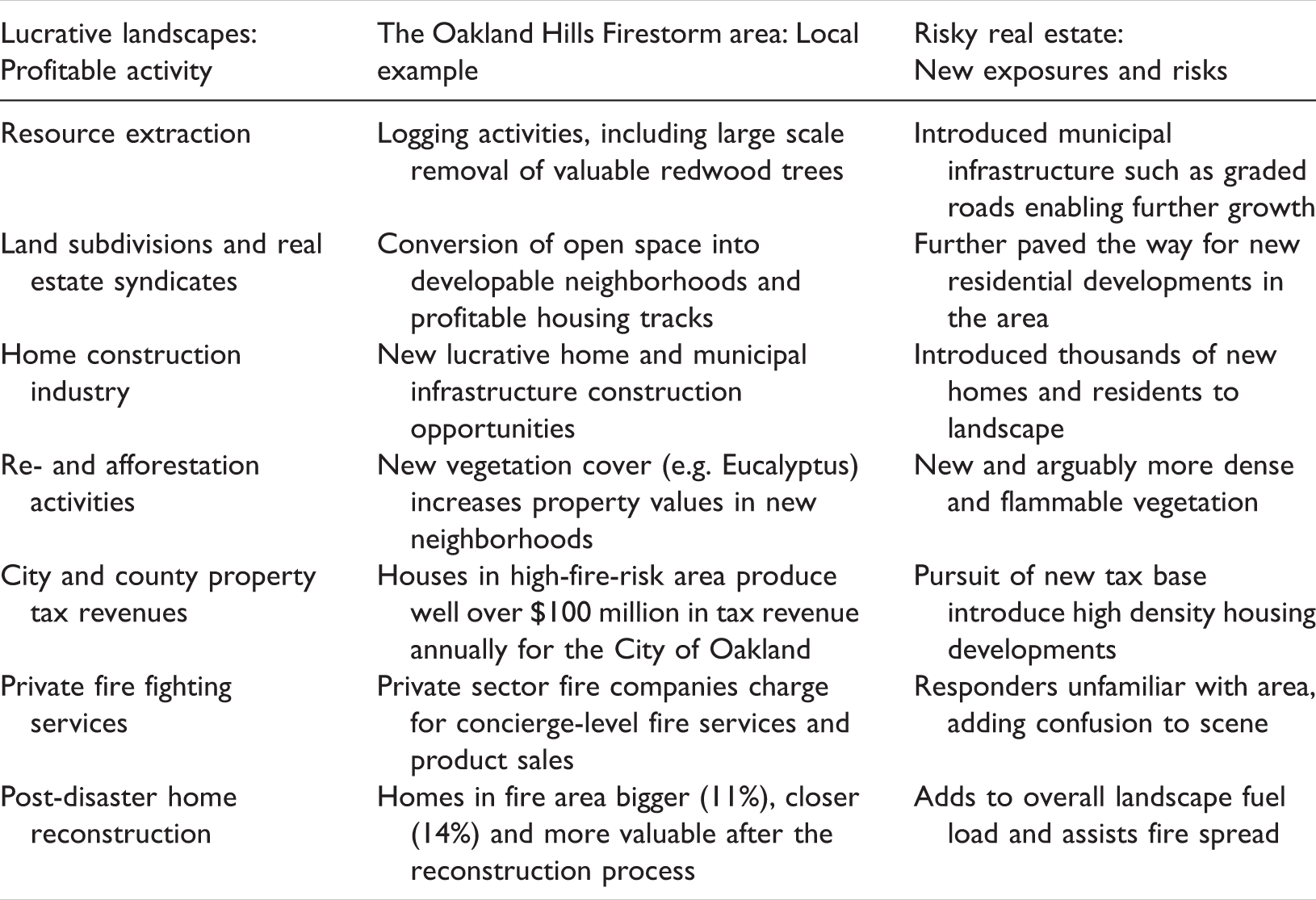

Examples of the profitable activities and associated risks that since the 1800s have turned the Oakland Hills into a lucrative, amenity-rich and highly fire-prone landscape.

Table 1 shows how the post-1991 disaster rebuilding process presented yet another opening for market opportunities and private wealth accumulation. Yet, the rebuilding process also increased the susceptibility of the area to future fires, despite improved building standards, by increasing the overall landscape fuel load and creating more proximate structures (Syphard et al., 2012). Valuable estate-based assets are protected from these risks, in part, by a multi-tiered structure of risk subsidization that includes personal indemnification plans and government subsidies. These resources help people justify living in this landscape, which is not just prone to wildfire but also susceptible to earthquakes and landslides. Collectively, these benefits, exposures and risk-reduction programs raise questions about levels of net household vulnerability in the area. This raises an important question, how does vulnerability exist in landscapes where residents have so clearly benefited financially from land use planning decisions and are buffered from many of the acute negative impacts of wildfire?

Methods

This paper reports findings from 11 in-depth interviews with 16 research participants (eight men and eight women) conducted by the authors during December 2014. Four of these interviews were with current emergency service managers (Fire Chief, Fire Marshal, Battalion Chief, Executive Director), all of whom were also involved in the 1991 fire fighting or recovery efforts. Seven interviews were with 12 residents that constitute six households, all with homes within or bordering the footprint of the 1991 firestorm. Three of these homes were burnt to the ground and two were located in the fire zone and suffered exterior damage. Recruitment materials inviting participation in an interview were extended via e-mail to the Hills Emergency Forum (HEF). 1 In turn, this e-mail was forwarded to HEF committee members who were asked to distribute the invitation to firefighters and residents still working and residing in the area. Interested parties were instructed to contact the authors directly to ensure confidentiality. All who volunteered to participate were interviewed during the period of fieldwork, which was defined by budgetary constraints. Our findings are also informed by informal conversations with other residents that experienced the firestorm. Finally, first-hand accounts of the fire and its effects are gathered from secondary sources such as newspapers and government reports.

The interview questions were designed to guide the conversation along five themes: (a) what attracted people to the area, (b) wildfire awareness and preparedness pre-1991, (c) personal experiences of the firestorm, (d) the rebuilding and recovery process, and (e) perceptions of social vulnerability today compared with 1991. The interviews were conducted as a team effort that openly acknowledged the “outsider” status of the lead-author (a female academic with international wildfire research experience) and the “insider” status of the co-author (a male academic and survivor of the firestorm with national wildfire research experience). As the interviewers’ gender, positionality, and conduct may influence the answering of questions depending on shared knowledge, cultural differences and trust, a semi-structured ethnographic style interviewing approach discussed by Riley and Harvey (2007), Desmond (2007), and Eriksen (2014) was employed to create possibilities for sharing alternative, humanized narratives.

Interviews occurred at a location of the participants’ choosing to ease any potential discomfort or concern relating to discussing emotionally charged stories. They lasted between 75 and 150 minutes and were audio-recorded and transcribed verbatim before being analyzed in the Computer Assisted Qualitative Data Analysis Software (CAQDAS) program NVivo v.10 (Bazeley, 2007). The data was coded using: (a) a priori themes, such as type of loss, rebuilding/recovery processes, risk rationalization and vulnerability categories and (b) emerging themes, such as emotional responses, insurance battles, opportunities arising from loss, and mental and physical health impacts (Riessman, 2008).

The following section demonstrates how several defining categories emerged from the interview data, which link affect and effect in terms of how people coped with and were variously impacted by the firestorm.

Diverse manifestations of risk and vulnerability

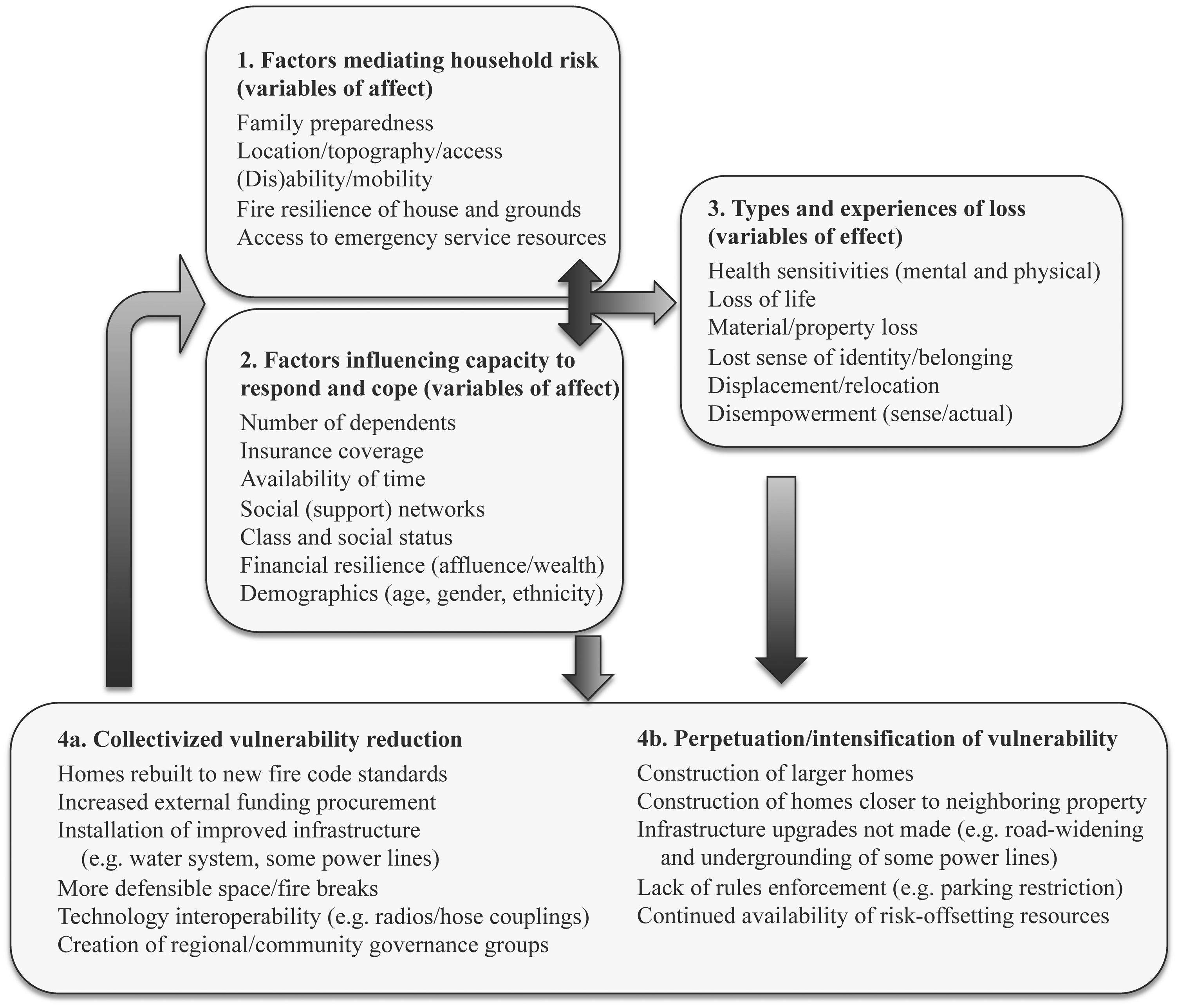

To better understand the complexity of how people in this affluent area were impacted by the firestorm, we divided our findings into four categories (Figure 3). The first category describes factors (pre-conditions) that affected exposure and the likelihood of loss. The second category describes social characteristics that conditioned capacity to respond. These conditions carry through temporally to the third category, as they affected the degree and magnitude of impact on individuals. The third category outlines the effects of categories one and two—i.e. the lived experiences of loss, and associated short- and long-term consequences. Vulnerability factors in categories one and two may be understood as pre-conditions for the eventual physical, mental, and material losses described in category three. The fourth category in Figure 3 refers to post-disaster conditions in the aftermath of the Oakland Hills firestorm. These conditions are shaped by both collectivized vulnerability reduction (4a) and other activities that maintain vulnerability to wildfire (4b).

Variables of affect and effect contributing to variegated vulnerability as exposed by the 1991 Oakland Hills Firestorm.

The summation of interview themes/examples in Figure 3, as well as the detailed examples and quotes in the following sections, highlight the complexity of what it means to be vulnerable. However, they also illuminate how interview participants’ experiences of risk and vulnerability fit within two broad headings: vulnerabilities of affect and effect. All interview participants described conditions that contributed to increased exposure and hardship as well as factors that exacerbated already difficult circumstances (Figure 3: Categories 1–2). These can be understood as variables of affect in so far as they shaped and conditioned potential/future experiences of risk. These include attributes such as geographical location, level of mobility, number of dependents and/or race and gender association (all known to influence risk management). Many also described actual experiences of loss as a result of the fire (Figure 3: Category 3). Here, interview participants focused on the consequences of being vulnerable. These variables of effect were diverse in nature and included issues such as property loss, physical ailments and emotional stress from displacement. One of the most interesting yet tragic aspects of vulnerability in the aftermath of the firestorm was the way many attributes of risk, injury, and trauma became linked up with future manifestations of suffering and distress. Several descriptions below highlight the ripple effect of interconnected fire-related stresses and losses, as vulnerabilities extended outward from the event itself, shifting forms and re-emerging in new, complex and sometimes unpredictable ways.

Variables of affect: Factors mediating risk and influencing coping capacity

Risk and vulnerability—oftentimes understood in composite and totalizing fashion—are in fact comprised by a suite of experiences, conditions, sensitivities, and activities that vary from one household to the next. Each individual and household experienced the firestorm, and the effects of fire, differently. This may seem an obvious point, but it is one worth repeating, particularly in affluent communities where all residents are assumed by some to contain a level of privilege that insulates them from any substantive, meaningful or acute form of vulnerability. In fact, all interview participants were quite aware of the very unique ways in which loss and tragedy are manifest and experienced from one household to the next. Perhaps more crucially, they questioned the way vulnerability is uncritically assessed, as if the whole firestorm and its aftermath hold a common tragic denominator. The husband of a married couple whose home burned in the fire commented on the challenge of applying the term “tragedy” to the firestorm:

I do not view [the firestorm] as a tragedy. … There is loss. My children’s childhood artwork is lost forever. But tragedy is the professor I met who has pain walking because he was burned so badly and whose wife and dear friend died in the fire. That’s tragedy, ok. Losing your children’s artwork is painful, but it’s not tragic. It interests me how there is so much hyperbole around the fire. The number of people I heard say after the fire, “It looks like Hiroshima up there”. Which is ridiculous. We have a friend who walked through Hiroshima two weeks after the bomb … and they lost their house in the fire too. I said, “Some people are saying, who are walking through the neighborhood, who don’t live up there, that it looks like Hiroshima”. And he said, “Oh no, its more like the Battle of Manila. Chimneys remained”. [Laughing] I loved it. That’s a man with experience talking. Oh goodness.

(Interview 2: Male, resides in home rebuilt after family home burnt to the ground)

The need to fend for oneself was also a prominent theme with regards to insurance settlements and indemnity plans, which were the cause of extensive worry and heartache for many homeowners. The sense of vulnerability linked to insurance claims ranged from the difficulty of collating lists of all items lost in the fire, to settlement disputes and lack of insurance providers in the aftermath of the firestorm. A married couple that lost their home near the fire perimeter described the psychological distress of dealing with insurance companies:

It’s easy [for us] to get out of here, it was easy that day … so I don’t worry about that. Risk has to do with the psychological and emotional maze that you go through on the way to a settlement with an insurance company. So risk has to do with what kind of insurance you have. Do you have to go through a drawn out settlement process, which will probably happen because consciously or unconsciously, the insurance companies have as a tactic to draw out settlements where a settlement is contested.

(Interview 2: Male, resides in home rebuilt after house burnt to the ground)

Demographics count. If you’re a single woman, if you’re a person of color, they’ll treat you differently. And we were low income. So they accused us of fraud. How could we live here? Even though we had all the proof in the world.

(Interview 2: Female, resides in home rebuilt after house burnt to the ground)

Initially we just, we lived, like just crashed in other people’s houses … and we sort of went between two different families' homes in the area … I’d been going to Oakland Tech, and so I went to Berkeley High for my senior year of high school, which was kind of a strange thing to do, because it’s like being a freshman in your senior year, which … made for kind of a very disjointed [experience].

(Interview 3: Male, child of family who rebuilt after house burnt to the ground)

Variables of effect: Types and experiences of loss

For some, the loss of their house also meant the loss of their livelihood as valuable tools and/or home offices went up in smoke and as physical resources and work-related items required to fulfill career responsibilities were lost. Tradesmen and women in particular mentioned the challenges they experienced working (and earning a salary) in the weeks and months after the firestorm. A self-employed house painter in the area lost nearly all of his painting equipment. According to his son, his father and mother were “forced to go out and spend a lot of money that initially they didn’t actually have. Just to get back some of the basic equipment he had to have to keep working” (Interview 3). Drawn out negotiations with insurance companies delayed property replacement efforts so that many homes wound up paying out of pocket just to put money back in their pockets. This pressure also caused tension between family members. For example, a married couple described the pressure of compiling lists and reconstructing architectural drawings for their house, all of which had burnt in the fire:

[Husband] The settlement just took an enormous amount of time. The insurance company would not process anything until you had submitted your list of contents and to do that, you had to picture every room in your house, every closet, every drawer, every bookshelf, and figure out what was there … Because of my skills [as an architect], I was able to reconstruct the plans of the house. Well, there was another thing too; I had the plans about 75% complete for a client. The plans were burned in the fire and luckily there was a copy some place but in order to proceed I had to hire somebody to reconstruct the plans and then proceed from there. [Wife] Yeah, so there was still a lot to do and I wanted him to do it fast, you know, so there was a lot of tension.

(Interview 5: Married couple, resides in home rebuilt after house burnt to the ground)

Furthermore, mental and physical health sensitivities to the firestorm presented significant short- and long-term challenges. The types of trauma experienced by interview participants ranged from anxiety during the firestorm, insurance battles, feelings of survivor’s guilt when the extent of loss and devastation became evident, the subconscious trauma of living in a visually scarred landscape, to the ongoing exposure to smells, particles, and fumes as well as the pervasive noise from trucks and building work. Some of the most persistent illnesses induced by the firestorm thus occurred after the event and affected both those who lost their homes and those who did not. One interview participant described life in the fire zone in the years after the firestorm: Every time it would rain it would activate all of the carbon and all the other stuff that had melted and burned was re-emitted back into the air. There were a lot of toxins that people have in their homes. … You have paint supplies, you have kinds of toxins that you have in your garage and in your car that just got into the air, and we just sat here, lived here and breathed all that stuff. I got chronic fatigue syndrome about six months later, and was sick for years, and went on disability from work … I think it definitely affected me, and a lot of people.2 … You know, a lot of us defer to people that lost everything. I mean, people were writing poetry and telling stories, and it just felt like for me with survivor guilt I felt like “Well, who am I to complain about anything? I still have my house, I still have my family pictures”. It didn’t feel appropriate to be telling our story too much, to me. … [But] you couldn’t get away from it [the illness]. It’s not like you could sell your house. (Interview 9: Female, resides in house that sustained exterior damage from spot fires)

There were no fire trucks here because this was designated a perimeter, a no regress perimeter, while the fire was raging. … But the really sad part was that the families would sneak through, or maybe they got an escort with a car and they would come through, and they would see their houses, lack of houses. It was hard ‘cause I was the only person on the street. Then [a neighbor] came by and I was there watering [the ruins of] his house down, and I felt like a real shmuck. Here I am, watering his house, so that other houses can’t burn. Didn’t feel good. Felt selfish.

(Interview 11: Male, residing in home built on burnt-out plot purchased after previous home sustained exterior damage)

Temporal and spatial dynamics of vulnerability

All of the above narratives illuminate how lived experiences of vulnerability run the course of time. Conditions before and during the firestorm are frequently linked to expressions of vulnerability after the event (sometimes a decade or two later). This chronological dynamic connotes the temporality of experiencing and being vulnerable; a set of longitudinal connections that are unique and variegated across diverse individual and household exposures. A spatial dynamic also emerged from the interviews in the form of the difference between primary and secondary vulnerability. During the 1991 firestorm, first responders, such as firefighters and police officers, represented another distinct, vulnerable population group. In this case, it became manifest as a secondary vulnerability, as first responders were placed at risk in order to assist households who were themselves deemed vulnerable to the fire (see below quote). The firestorm thus set in train a positive feedback where vulnerability produced still further vulnerabilities (which was intensified by the topography of steep hills and densely vegetated canyons intersected by narrow roads and exposed power lines). [Were you fearful of the fire and smoke?] No. I wanted to get my cats out of there. I wanted to see what was going on, see how the house was, and I couldn’t get information. So I just started to walk, they weren’t letting cars through. A cop stopped me of course and said, “No, you can’t go up there”, and I said, “I want to get my cats”, “No ma’am, sorry, they’ll have to deal with it. Get in your car and drive back”. I said, “I don’t have a car, that’s up there too” and as soon as he heard that, he goes “Okay, jump in”. He was Mutual Aid,

3

so he didn’t know the hills that well, so I directed him, and we came up here and the flames were across the street. You could see them, they weren’t towering over us, but you could see them … Everything here was still standing around me. So he let me out for a minute. … I had to break into the garage to get my car out, because the electricity was off. Got my car, and he didn’t know how to get out. He was scared. … “Come on lady, we’ve got to get out, don’t you see, the flames are right there!” … I just didn’t get the magnitude. I mean, I did and I didn’t. I was still too shocked to be afraid. I just had a mission. So he asked me to lead him back down, so we went careening back down the hills. (Interview 9: Female, resides in house that sustained exterior damage from spot fires)

Collectivized risk and vulnerability reduction

Collectivization in numbers and resources

Along with diverse expressions of vulnerability, our household scale analysis also reveals community attributes and behaviors that reduce other modalities of risk and even produce financial gains for residents. For example, the ability of particular individuals with linkages to financial resources and political capital helped many residents forestall various forms of risk and, in some instances, procure benefits from the disaster (see also, Klein, 2008). When viewed as a collective, the fire-affected community of the Oakland Hills was able to combine their resources to increase community adaptive capacity and secure a better future. Perhaps the most important community characteristic contributing to this favorable post-fire response was the fact that over 3000 homes burned at once. Several interview participants expressed this condition:

If your house is going to burn, be sure that it does it with 3,000 of your neighbors’ in a major media market! Because people who have fires that are solitary fires and that are up against the insurance company do not do very well. That’s really what drove a good settlement on this house – being part of a large middle and upper middle class group in a major media market.

(Interview 2: Male, resides in home rebuilt after house burnt to the ground)

I’ve always felt that it was very fortunate this fire happened to so many people in an affluent area. That the response wouldn’t have been nearly as overwhelming as it was if not, and we wouldn’t have come out as well otherwise. … A few people, including the Governor, made their mark by helping us.

(Interview 7: Male, resides in home rebuilt after family home burnt to the ground)

Throughout the post-disaster recovery process, numerous examples can be found that illustrate how general neighborhood improvements were secured, and community adaptive capacity was increased, through individual and collectivized vulnerability reduction. Two examples of the integrated process of collectivized vulnerability reduction are public participation with the United Policyholders (UP) program 4 and the placement of power lines.

United Policyholders: A butterfly effect

As members of the fire community—faced with a myriad of personal, legal, and financial decisions—struggled to regain footing in the weeks and months after the fire, many residents worked with UP, which was at the time a fledgling insurance holder advocacy program that subsequently grew in prominence both during and after the immediate aftermath of the firestorm. UP helped uninformed residents engage with complicated and oftentimes adversarial insurance settlement complications. Not only did UP provide advice to households during insurance company negotiations, they also worked alongside residents to generate data on socioeconomic settlement trends. A community member who worked with UP described their collaborative research, which revealed, among other things, “that single women did worse than married women and minority single women … did the worse of all” (Interview 2). As a result of these efforts, many individual residents credit UP with helping them navigate the complicated settlement process and emerge from the ordeal with a just and fair outcome.

The relationship between UP and residents was mutually beneficial. While the staff at UP were viewed as crucial allies by community residents, UP itself owes much of its success to the gritty determination of this group of tenacious community members—many of whom spent months collecting and analyzing local data, which proved crucial to UP’s success and ascendance into a leading national insurance holder advocacy organization. In collective risk-reduction fashion, the diligent commitments of these residents fed right back into the community. As UP grew in size, publicity, knowledge, and financial capacity, they were able to deliver valuable assistance to more and more residents in the fire-affected Oakland Hills. By helping themselves, residents provided data, insights and settlement precedents that would eventually benefit hundreds of others and increase the availability of recovery benefits to the entire community.

Power lines: Conduits of electrical and political power

The case of fire-zone power line placements further illustrates collectivized risk and vulnerability reduction. Above ground power lines downed during the firestorm presented a serious challenge for both residents and fire response efforts. Exposure to electrical currents resulted in injuries, fatalities, blocked evacuation routes and impeded firefighting capabilities. Moreover, as power lines were destroyed, many water pumps and hydrants in the Oakland Hills failed (Simon and Dooling, 2013). Replacing this utility infrastructure would prove to be neither cheap nor straightforward. Upon receiving replacement value for electricity lines, power companies initially planned to install poles, transformers and lines similar to pre-fire conditions. According to one community member active in the negotiation process, neighborhood members collectively rallied, “No you won’t”:

You cannot just replace what burned. You’ve got to do it better. Because [pre-fire conditions] created all kinds of problems for us. Among other things, PCBs [printed circuit boards] … I had a PCB laying there along those transformers, right down on the corner of the street... And this is very unsafe. And not only do power poles burn down … They were exposing chemicals that were very toxic. So there’s no way you’re going to replace the current infrastructure.

(Interview 11: Male, resides in home built on burnt-out plot purchased after previous home sustained exterior damage)

“I don’t tell you how much money you don’t have, but if you don’t do something about it, a lot of people are going to hear about it. You just can’t replace what you got.” … [The city] knew that that was the right thing to do, so they were having their own meeting, which I was not attending, saying “Look, these guys are pissed [sic, angry], we need to do it better.” So then we would talk amongst ourselves and say, “It’s really important that we get this underground. I’ll give you reports or whatever you want and … a lot of leaders were saying the same thing.” So we decided that we were going to share on a tax levy on our property, a third, a third and a third, we would pay a third, the city would pay a third, and then PG&E [Pacific Gas & Electric Company] would pay a third.

(Interview 11: Male, resides in home built on burnt-out plot purchased after previous home sustained exterior damage)

“Power lines” within the post-disaster landscape therefore served as conduits of both electrical and political power. They reflect both the physical infrastructure that connects homes, generators, pumps, and substations, and also the lines of political influence that connect affluent communities to key decision makers around the city; decisions that ultimately resulted in the replacement of damaged power lines underneath neighborhood roadways. In both a material and political sense, post-disaster “power lines” have reduced future risk levels. This includes a form of secondary risk reduction for first responders who now have better resources to fight fires with (e.g. more reliable sources of water and power). Meanwhile, from the perspective of homeowners, improvements to power lines as well as aesthetic streetlamps, upgraded water conveyance systems and other municipal advancements made possible by active community members, have contributed to increases in property values that have further concentrated affluence and privilege in the Oakland Hills. It is clear that the active participation of a few individuals raised all neighborhood estate values and reduced future levels of fire risk for both residents and first responders alike. Yet, individual and sometimes individualistic actions still mattered in the recovery process.

Conclusion

For most residents living in amenity-rich but high fire-exposure landscapes, such as the Oakland Hills, life is, on a day-to-day basis, not about negotiating disaster vulnerability. Rather, it is about lifestyle and personal choice. Residents’ justification and preference for living in these landscapes minimize perceived risk, as lifestyle attainment overrides the fear of potential natural hazards. The facilitation of vulnerability in the Oakland Hills has arguably been compounded further in the years after the 1991 firestorm, as fire survivors have aged and turnover in property ownership has resulted in both a collective memory-loss and a reduced sense of urgency towards the inherent threat of wildfire (Eriksen, 2014). As one local Fire Marshal mentioned, many people living in the area “… didn't go through the fire. They don’t even know what it is all about” (Interview 4). The enormous risk subsidization apparatus at play further explains the ease with which people justify living with the inherent threat of wildfire. This is despite the continual topography-related infrastructure limitations, such as inadequate water pressure and routes of access/egress, as well as the many long-term and prolonged experiences associated with fire recovery.

The root-causes of vulnerability in places like the Oakland Hills where homeowners are active agents in the production and consumption of vulnerability are linked to social, cultural, economic, and political norms. The results of our intersectional analysis illuminate key adaptive capacity mechanisms through which affluent areas collectively leverage existing privilege to garner further advantages and, furthermore, how this accumulation of wealth proceeds through long-standing, locally-rooted, channels of material accumulation. It also demonstrates how these advantages and resources do not erase individuals’ acute levels of vulnerability and loss. This was evidenced in the interview narratives, which revealed short- and long-term lived experiences of psychological, physical, material, and financial trauma and loss. There is a continuous interplay between the rise of diverse household-scale vulnerabilities and their simultaneous decline across neighborhood scales due to collective community action.

These concomitant yet competing conditions demonstrate how affluence does not negate disaster vulnerability. Instead, affluence and vulnerability are useful subjects to examine in tandem, as vulnerability typically is understood as an unfortunate, and oftentimes spatially removed, byproduct of affluence. Understanding how the two reside within the same community and set of households can be more challenging. For many, the Oakland Hills is an affluent region that has benefited from pre- and post-fire development activities. It is thus easy to label the entire community as simply not socially vulnerable, or to simply ignore such areas within vulnerability research, given all of the associated financial and lifestyle benefits that come with living in the area. As the previous sections have demonstrated, however, there are real risks associated with living in this high-exposure, fire-prone landscape that cannot be written off with a broad-brush label of neighborhood affluence. Characterizing the Oakland Hills as not socially vulnerable to natural hazards simply due to overall wealth and privilege is both misleading and inaccurate. To be sure, levels of vulnerability within the Oakland Hills are certainly not, on a day-to-day level, equivalent to the types of risk experienced by many residents in the relatively poorer flatlands of Oakland, let alone other more impoverished, marginalized and precarious regions of the world. But to dismiss an entire population as if it were bereft of vulnerability (or, similarly, to label an entire population as equally afflicted by tragedy) is to rebuff good political ecological analysis and reject nuanced, data driven and non-discriminatory inquiry.

Dedicated spatial inquiry of vulnerability, focused on the interplay between household and neighborhood scales, is thus central to this form of political ecological analysis. On the one hand, we have linked specific vulnerabilities to unique places (e.g. from one home to the next, with each containing unique family histories, demographic attributes and composite risk sensitivities). On the other hand, we have up-scaled and linked household-specific experiences to the broader neighborhood scale (e.g. by highlighting how levels of household vulnerabilities are mediated by collective community action, adaptive capacities and the behavior of a few well-connected people). Moving across scales enables us to see how individual homes influence community level action, and also how overall community scale governance impacts household vulnerabilities.

We argue that vulnerability is (a) very much present in largely affluent areas, (b) variegated across all community households, and (c) collectively reduced by the broader affluent community within which individual households reside. As the earlier contextualizing variegated vulnerability section suggests, paying closer attention to the different ways vulnerability and affluence interact reveals a significant recursive process, which highlights the need to think temporally as well as spatially about risk and vulnerability to understand how different community members embody different combinations of social attributes, which in turn influence levels of vulnerability in threatening situations. Presenting the historical production of vulnerability reinforces the notion of vulnerability as a complex and dynamic process that is produced over time and space in connection with affluence (Collins, 2010; Simon, 2014). Yet, even with these insights, the diverse range of lived vulnerabilities (as experienced from one household to another), and the way these experiences are mediated by community level wealth and privilege, remains somewhat opaque. Leveraging more nuanced intersectional and relational analysis reveals how vulnerability is comprised by a set of complex and contingent factors that are both heterogeneous and shared across all households and social groups. It also highlights the important role trauma plays in understanding how vulnerability is framed individually and collectively. Careful consideration of sensitivities, such as short- and long-term manifestations of psychological distress and physical suffering in disaster recovery, can leverage the field of political ecology.

Thus, there are real analytic benefits of integrating the study of vulnerability and affluence in the context of disaster recovery. By bringing the vulnerability-in-production, intersectionality, and unequal risk frameworks of inquiry into productive dialogue, the AVI emerges as a rich conceptual container. Beneath a landscape of variegated vulnerabilities lies a level of affluence and privilege that, although not directly held by all residents, is collectively leveraged to reduce vulnerability throughout the broader community. Interestingly, this recovery process can simultaneously reduce, perpetuate and in some instances intensify, levels of vulnerability. For example, while the construction standard of post-1991 rebuilt homes is an improvement on the homes lost in the firestorm, houses were rebuilt at greater density in the same exposed locations. Similarly, much of the vegetation consumed by the firestorm has regrown in the succeeding 25 years; gardens planted as homes were rebuilt have matured; and the relentless built-up of duff continues, as eucalyptus trees shed their stringy bark. Such concomitant conditions point to some fundamental questions about how we develop and live at the WUI, as well as how we manage disaster policies given the complex and influential nature of the AVI.

Footnotes

Acknowledgements

We are grateful to the research participants who generously shared their time and firestorm experiences. We also thank the journal’s editors and anonymous reviewers for constructive feedback.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: A 2014 Small Research Grant from the Australian Centre for Cultural Environmental Research supported this research. The lead-author is funded by the Australian Research Council (DE150100242).