Abstract

The prevalence of shareholder activism has resulted in the placement of activist-appointed directors onto the boards of firms. Extant research on this phenomenon has taken a rational approach in examining how such directors bring about change but has not accounted for the behavioral implications associated with their placement on boards. Building on theory involving alignment and legitimacy at the team level, this paper adopts a behavioral approach in theorizing how the placement of activist shareholders themselves as directors onto the boards of firms brings about firm change. The study finds that such activists lead to less firm change. Further, it finds support for the effects of demographic similarity between such activists and incumbent directors in causing change.

Keywords

Introduction

Recent years have seen an upsurge in shareholder activism 1 , defined as “the actions taken by shareholders with the explicit intention of influencing corporations’ policies and practices” (Goranova and Ryan, 2014: p. 1232). Driven by a disconnect between firm ownership and management, activist shareholders are increasingly expressing their dissatisfaction (David et al., 2007) and intervening to influence firm strategy and performance (DesJardine and Durand, 2020; Westphal and Bednar, 2008). Dissatisfied shareholders often seek firm change by resolving issues related to cutting costs, selling, or retaining assets, and improving operational efficiency (Activist Insight, 2019; Gow et al., 2023). Because a firm’s board makes important decisions that influence change in firm strategy (Goodstein and Boeker, 1991), activist shareholders 2 advocating for change often push for board representation as the primary mechanism in promoting change (Gow et al., 2023). In support of this view, activist board representation has been found to be the most common request over any other type of activist issue brought up with activist-targeted firms (Activist Insight, 2019; Sawyer et al., 2019). Hence, activist shareholders dissatisfied with certain aspects of a firm often nominate “activist directors” (Gow et al., 2023) to a firm’s board.

Existing literature on this topic has painted a picture of activist directors as successful agents of corporate change who intentionally promote change in underperforming and/or stagnant firms. The study by Coffee et al. (2018), for example, has posited that the presence of hedge fund-appointed activist directors causes leaks of sensitive internal information and is associated with a change in firm stock price prior to the public disclosure of such information. Similarly, the work of Kang et al. (2022) has found that the nomination of activist directors to boards targeted by shareholder activism is associated with an increase in value that persists over time. Besides such empirical work examining how activist directors influence firm change, the remainder of the literature involves theoretical and/or normative arguments, such as the work of Christie (2019), who has proposed that the appointment of activist directors will lead to fundamental changes in firm strategy through a market of activist shareholder quasi-control over the activist-targeted firm.

While the literature has granted us broad ideas regarding how activist directors may influence firm change, our current understanding of the factors that drive activist directors’ effectiveness on boards is limited. As evidenced by the discussion above, the few studies that have thus far examined the involvement of such directors as they play roles in enacting firm change have taken mainly rational approaches in making simplifying assumptions that ignore the behavior of incumbent directors on a firm’s board as they react to an activist board placement (Christie, 2019; Coffee et al., 2018). These studies have typically involved the narrative of activist directors as successful agents of firm change, largely assuming change results from the election of such directors to a board. As a result, much remains unknown about the behavioral implications associated with activist director placement and how it may serve to influence the board decision-making process through an incumbent board’s willingness to work with such directors. Further, it is known that some activist shareholders 3 may nominate themselves or others currently under their employment to a firm’s board. As boards exist to advise and monitor firm management on behalf of shareholders (Jensen and Meckling, 1976), such activists bridge the traditional agency divide between firm ownership and management (Fama and Jensen, 1983) and may impede the board’s decision-making process due to the following reasons; first, boards that include shareholder activists may face inefficiencies in reaching collective decisions. While boards typically function as a cohesive team, relying on each member to share information and expertise (Carpenter and Westphal, 2001; Carter and Lorsch, 2004), their accountability to activist shareholders (Chuah et al., 2024) may lead incumbent board members to experience hesitation and constraint in their board work. Second, activist shareholders themselves are known to often lead activist campaigns designed specifically to oppose incumbent director initiatives. Such campaigns have often involved activist “white papers” designed specifically to discredit incumbent directors, and may cause incumbents to react to a successful shareholder activist board placement with perceptions of uncertainty (Marcel and Cowen, 2024) or even resentment. Third, activist shareholders are expected to pursue issues in their boards more aggressively due to their vested positions as firm shareholders. As incumbents are thoroughly assessed by all shareholders prior to their election, such aggression on the part of activist shareholders may be perceived as a challenge to the dutiful execution of incumbent fiduciary duties, and may serve to worsen working relationships within the board.

Given the above reasons, the research objective of this paper examines the unique position involving shareholder activists on boards, delving into how such a position may set up scenarios that influence their ability to enact change in activist-targeted firms. Drawing on studies that have found alignment (Branson, 2008; Gagnon et al., 2008; Schmit et al., 2011) and legitimacy (Huy et al., 2014; Tost, 2011) to impact change resistance at the team level, I adopt a behavioral approach in theorizing how such scenarios may impact an activist shareholder’s effectiveness in influencing firm change. In developing my hypotheses, I begin by examining how activist shareholder placement on a board may impact firm strategic change through incumbent perceptions relating to alignment and legitimacy. Because homogeneity has been found to influence perceptions of alignment (Tsui & O’Reilly, 1989; Turner and Tajfel, 1986) as well, I then examine how demographic similarity between such activists and the incumbent board may serve to interact with firm change. Ultimately, this paper explores the following important questions related to shareholder activists in firms: How does having activist shareholders or their employees on a board influence strategic change? And how does similarity between such activists and incumbent directors influence such change?

The theory and results associated with the study of shareholder activists and their impacts on firm change contribute broadly to three streams of research. First, it advances research on boards by highlighting the behavioral implications associated with incumbent directors as they work together with activist shareholders to enact strategic change. Second, the paper contributes to research surrounding shareholder activism and its effects on firms by highlighting important board-level factors associated with enacting strategic change. Third, its findings encapsulate a modest advancement towards agency research on boards by examining principals who take on the role of agents as they work together with incumbents to enact strategic change.

Conceptual background

Boards and strategic change

Publicly traded firms are guided by a governing body known as the board of directors. As experienced individuals duly elected by and representing shareholder interests, such directors serve their firms by advising top management on strategy formulation as well as implementation. Operating from an agency perspective, some board responsibilities include establishing strategic goals and monitoring the top management team (TMT) to ensure management action is aligned with maximizing shareholders’ interests. Boards also serve as a medium for firms to understand and manage uncertainty in their environments (Hillman et al., 2000), often playing critical roles in helping govern their firms, especially during difficult times (Goodstein and Boeker, 1991). Such responsibilities often involve directors themselves playing a crucial role in changing the direction of a firm’s strategy through enacting strategic decisions by committing firm resources, setting important precedents, and directing important firm-level actions (Mintzberg et al., 1976).

Given the board’s responsibilities in influencing the strategic decision-making process, there are a few compelling reasons why they may influence strategic decisions related to a firm’s change. First, Mizruchi (1983) noted that a firm’s board is positioned within the hierarchy of an organization to establish the parameters from which strategic decision-making occurs. Because boards provide monitoring and advice to firm management while representing firm shareholders, they thus also influence the strategic decision-making process in such a way that ensures alignment of any organizational change with shareholder interests (Goodstein and Boeker, 1991). Second, there exist critical periods in organizations where boards of directors may assume a more direct role in strategic issues affecting the allocation of resources. When an organization encounters crisis in its evolution (Mizruchi, 1983), its board of directors may play a vital and direct role in influencing strategic change. Boards may also be directly involved in significant shifts in corporate strategy, such as those associated with strategic reorientations (Tushman and Romanelli, 1985) often demanded by shareholder activists. Important to note here is that in these periods of organizational evolution, changes in ownership, the composition of the board of directors, or both may have a critical impact on the strategic change of a firm (Goodstein and Boeker, 1991). Finally, beyond acquiring resources or representing shareholder interests, the board’s role also involves confronting important decisions on strategic change that help the organization adapt to significant environmental changes (Mintzberg, 1983). This strategic function of the board is particularly important during critical periods involving a decline in organizational performance (Mintzberg, 1983), a common reason for activist engagement (Bebchuk et al., 2020), as such an event provides significant opportunities for the maximum mobilization of board power and the initiation of strategic change.

Strategic change represents a firm’s response to the recognized need for change and to adapt to its environment (Carpenter, 2000). Chandler (1962, p. 58)’s work examining firm strategy and structure has defined strategic change as “entailing the discretion of strategic leaders (such as boards) to adjust and renew resources to attain or sustain competitive advantage.” As firms navigate increasingly complex environments, scholars have thus far also examined how internal factors associated with the strategic decision-making process involving its leaders may serve as antecedents of strategic change. The work of Wiersema and Bantel (1992) involving TMT demography and strategic change, for example, has demonstrated that TMTs sharing demographic homogeneity invoke perceptions of similarity and attraction to each other, leading to change via congruence in beliefs and perceptions of how a firm operates, as well as through the promoting of high consensus and continuity in team decision-making. Similarly, Westphal & Fredrickson (2001)’s work has highlighted the importance of board composition and dynamics as they work together to influence a firm’s strategic change.

Resistance to change

Motivated by prior studies on team resistance to change, this paper highlights two theoretical concepts associated with how incumbent boards may resist change. First, efficient boards operate fundamentally as teams (Payne et al., 2009), and existing research on team alignment has suggested that aligning behaviors, values, and goals within the board can help reduce resistance to change. Gagnon et al. (2008)’s study, for example, has highlighted how the inability to commit to change on employees’ part may lead to them failing to engage in behavior that supports and aligns with the organization’s strategic goals. In the context of boards that include both activist and incumbent directors, incumbents who refuse to commit to activist-driven change may also avoid behaviors that align with or support addressing the issues raised by activist shareholders. Similarly, Branson’s (2008) research emphasizes the significance of value alignment—specifically, the alignment between organizational and individual values—as a driver of change by fostering positive employee attitudes, such as organizational commitment and job satisfaction. Put into perspective, activist directors who share similar values with incumbent directors in an organization are more likely to foster positive attitudes in their implementation of activist-related changes. In a similar vein, Schmit et al. (2011) highlighted that goal alignment within an organization leads to more effective communication, facilitating the successful implementation of a strategic initiative. Although activist campaigns often feature differing goals between activist shareholders and a firm’s management, activist directors who can bridge these differences may enhance communication and more effectively advocate for activist change.

The second concept relates to legitimacy as a crucial social phenomenon that involved scholars across the social sciences in discerning its nature, origins, and consequences. Synthesizing the large and fragmented literature on legitimacy content, Tost (2011) argues that there are three main dimensions of content underlying legitimacy judgments: instrumental, relational, and moral. First, instrumental legitimacy is present when the entity is perceived as effective in facilitating a team’s attempts to reach self-defined or internalized goals or outcomes. Second, relational legitimacy exists when the entity is perceived to exhibit fairness, benevolence, or commonality in affirming the social identity and self-worth of individuals or social groups. Finally, moral legitimacy happens when an entity is perceived as being legitimate on moral grounds as it relates to the evaluator’s moral and ethical values. Further linking the phenomenon of legitimacy judgments to change resistance is the work of Huy et al. (2014), who, in their paper examining an organization’s implementation of radical organizational change, have found that managers’ judgments of the instrumental, relational, and moral legitimacy of change agents impacted their level of resistance towards the change efforts initiated by those agents. As becomes evident from the articulation above, these theories facilitate the understanding of behavioral perceptions, particularly when regarding incumbent directors, as they work within a board mired by the involvement of an activist director placement.

Shareholder activism and boards

“I’ve done that in the past, once or twice asked for board seats, and most often I got one.” – Nelson Peltz, Trian Fund Management Activist Shareholder (CNBC, 2017a)

Shareholders who disagree with their firms possess divergent goals, becoming known as “activist shareholders” (Goranova and Ryan, 2014). Defined as “the use of ownership positions to actively influence company policy and practice,” shareholder activism can be exerted through letter writing, dialogue with firm management or the board, and through filing formal shareholder proposals. Extant literature has portrayed shareholder activism as stemming from two distinct motivations: socially and financially motivated activism (Judge et al., 2010). Shareholder activism that is social in nature is defined as “instances in which individuals or groups of individuals who lack full access to institutionalized channels of influence engage in collective action to remedy a perceived social problem, or to promote or counter changes to the existing social order” (Briscoe and Gupta, 2016: p. 4). On the other hand, shareholder activism that is financial in nature involves “shareholders disappointed by what they perceive to be mismanagement by the firm, who then pressure managers and/or directors to do things such as spinoff a losing portion of the business, compensate executives less generously, or pay out more dividends to firm owners” (Judge et al., 2010: p. 259). It is important to note that social activism in the context of a firm stems largely from motivations that are social in nature (Ahn and Wiersema, 2021), which rarely involve the need for an activist representative on a firm’s board.

Activist board representation involves activist shareholders (and their proponents) nominating director candidates for a firm during its annual general meeting (AGM). Nominated by activist shareholders who are often vocal about their dissatisfaction with certain aspects of the firm, activist directors champion for activist-related causes and often attempt to garner support from their incumbent peers on a firm’s board in seeking redress for issues they deem as critical firm weaknesses affecting the return of shareholder value (Monks, 1998; Walker, 2016). Working with the incumbent board, such directors influence a firm’s strategic direction by addressing and highlighting activist concerns. Crucial to note is that activist and incumbent directors differ in their perspectives on how a firm should be run. Activist directors fundamentally represent an activist shareholder’s view on addressing critical firm issues. In contrast, incumbent directors are responsible for the prior decisions that led to these issues in the first place.

Despite this difference in perspectives, direct interaction between activist shareholders and a firm’s board during an activist campaign (Sawyer et al., 2019) can sometimes also afford an activist shareholder placement onto a firm’s board. Here, activist shareholders may nominate themselves or others currently under their employment to a firm’s board to directly influence activist change (DesJardine et al., 2021). One example of such an activist shareholder involves Peter A. Feld, a portfolio manager employed by the activist hedge fund Starboard Value, who also held board seats in the activist-targeted boards of Darden Restaurants, Brinks Co., and Aecom. Similarly, prominent activist shareholders such as Nelson Peltz, Eric Singer, and Jeffrey Ubben have held board seats in the firms they target in recent years.

While activist shareholder placement on a firm’s board may at first glance seem innocuous, it must be mentioned that such placements afford an activist increased interaction with a firm’s board. In advocating for their vision of change, activists holding board positions are provided unique opportunities to engage directly with their boards during board meetings instead of during a company’s yearly AGM. Further, such board placements also serve to fundamentally violate the traditional agency divide guiding most corporate boards. As boards exist to advise and monitor firm management on behalf of shareholders (Jensen and Meckling, 1976), the presence of activists within boards may also complicate the agency role of boards. Here, boards working with shareholder activists may experience issues with their decision-making due to the uninvited presence of an activist shareholder within their ranks. As shareholders themselves holding board positions, activist shareholders may serve to impact firm change by influencing the board decision-making process in distinct ways; first, boards possessing shareholder activists may experience inefficiency as it relates to making collective decisions. As boards are directly accountable to their shareholders (Chuah et al., 2024), incumbent board members may experience constraint 4 in their board work, as making any recommendations unaligned or against those of the activist may put into question their fiduciary duty towards a shareholder. As a result, incumbent directors may feel obligated to agree with activist demands and experience dissatisfaction and misaligned goals through working with activists. Hence, such experiences are expected to cause incumbents to become more resistant towards change due to the attributing of low-value alignment (O’Reilly et al., 1991) and low-goal alignment (Schmit et al., 2011) towards working with activists.

Second, activist shareholders have often spearheaded activist campaigns opposing incumbent director initiatives (DesJardine et al., 2021). Such activism campaigns have involved both firm management and activist shareholders contesting for shareholder attention and votes through media campaigns that champion their respective visions of firm strategy. It is worth mentioning that such activist campaigns have often revolved around activist “white papers,” which are operational and strategic analyses designed by activist shareholders to discredit incumbent directors specifically (Monks, 1998; Sullivan & Cromwell LLP, 2018). As such, incumbent directors are expected to react relationally to a successful activist shareholder board placement with perceptions of uncertainty (Marcel and Cowen, 2024) or even resentment. It is worth noting that because incumbent directors are directly accountable to shareholders (Chuah et al., 2024), activist shareholders who bridge the agency divide (Jensen and Meckling, 1976) on boards may be perceived by incumbents as an ethical problem as well. Thus, such negative relational perceptions from incumbent directors, along with the belief that having an activist shareholder on the board is ethically questionable, may then lead incumbents to resist change due to an attribution of low relational legitimacy and low moral legitimacy (Tost, 2011) in formally working with shareholder activists on their boards.

Further compounding the issue of shareholder activists having previously discredited incumbent directors during activist campaigns involves what such activists may do with their board seats. It is known that activist shareholders who obtain board seats often view themselves as “first among equals” in the boardroom, causing incumbent directors to feel intimidated in acquiescing to their demands on boards (Kirman, 2017: p. 77). As vested shareholders of a firm taking an activist stance, shareholder activists may thus also aggressively pursue issues in the firm that may include removing certain underperforming management or board members, addressing excessive management pay, and amending existing but inefficient corporate bylaws (Activist Insight, 2019; Gow et al., 2023). Here, the incumbent board may interpret such action on the activist’s part as opposition to properly executing their fiduciary duties. This may be so as most incumbent directors are put up for nomination by a nominating committee for shareholder election during a company’s Annual General Meeting. Because activist directors circumvent this process and only enter boards through private settlement or proxy contests (Ahn and Wiersema, 2021: p. 109; Chuah et al., 2024), incumbents may thus perceive such shareholders in their boards as instrumentally illegitimate. Hence, given that the incumbent board has been thoroughly assessed by all shareholders for their experience and leadership capabilities prior to their election (Charan et al., 2014), such highlighting of firm weaknesses by shareholder activists may be perceived instead as an aggressive challenge made by instrumentally illegitimate directors towards decisions made by incumbent board members. Besides reflecting a fundamental difference in goals between the two parties, such highlighting of firm weaknesses by a shareholder activist may worsen working relationships within the board, serving subsequently to impede strategic change through the exacerbating of issues with alignment (Schmit et al., 2011) and legitimacy (Tost, 2011). Taken together:

Activist shareholders on a board are negatively associated with firm strategic change.

Demographic similarity

Existing studies have highlighted the importance of similarity in influencing alignment within the context of teams. For example, Tsui & O’Reilly (1989)’s work examined performance evaluation and hiring practices and found bias in evaluation decisions from raters who favored rates based off various demographic dimensions. Relatedly, Latham et al. (1980)’s work on hiring decisions have demonstrated a relationship between applicant-rater demographic similarity and the perceived quality of an applicant. Such studies suggest that similarity provides mutual reinforcement or “consensual validation” of each individual’s characteristics while enhancing interpersonal attraction and producing bias in evaluation decisions (Byrne et al., 1966). It is worth noting here that the effects of similarity on bridging issues relating to alignment may also extend to perceptions involving legitimacy. Extant studies examining individual similarity have suggested that demographic similarity provides a salient basis for psychological group membership (Useem and Karabel, 1986) by encouraging individual self-esteem and self-identity (Turner and Tajfel, 1986). From such a perspective, individuals seek to legitimize demographically similar individuals in constructing or maintaining homogeneous “in-groups” to maintain or enhance their self-esteem, identity, or both (Zajac and Westphal, 1996).

With resistance to change positioned as a theoretical mechanism explaining how shareholder activist appointments may lead to change in a firm’s strategy, I next examine how age similarity involving shareholder activists and incumbent board members may serve to interact with shareholder activist-led firm change. Prior work in the literature has found that employees of similar age, regardless of their expertise, status, or tenure in a firm, tend to have similar non-work-related experience (Lawrence, 1986). The work of Ryder (1985, p. 845), for example, has highlighted that a group of individuals possessing similar age takes on “a distinctive composition and character reflecting the circumstances of its unique origin and history.” According to Ryder (1985), employees who were working in different companies during a recession may share memories of similar experiences during such a difficult time. Similarly, employees who grew up during the Great Depression, for example, may share memories of that economic disaster which serves to distinguish them from younger employees. In addition, employees of similar age may also share common non-work-related experiences, as such employees often tend to be at similar points in their family lives as well (Lawrence, 1986).

Viewed in the context of shareholder activists possessing similar age with incumbent directors, such similarity is expected to influence firm change in two ways. From a relational legitimacy perspective, non-work-related experience may first allow for the cultivation of a common group identity between activists and the incumbent board (Mortensen and Hinds, 2001). Such identity cultivating experiences may involve historically generated similarities that may relate to time spent in similar schools, or similar experiences gained growing up or working. Second, non-work-related experiences may encourage for familiarity between shareholder activists and incumbents. In such a scenario, both the activist and incumbent directors may be at similar points in their lives (Lawrence, 1986), and as a result may share experiences relating to their personal lives. Because the mere exposure to others powerfully affects peoples’ feelings about one another (Zajonc, 1968), such experiences that facilitate familiarity may in turn lead to a reduction in relational tension between the two parties. Further, similarity in age is expected to also alleviate goal alignment issues between shareholder activists and the incumbent board as well. When an activist with drastically different goals also has a similar age as the incumbent board, the sense here is that commonality in terms of non-work-related experience may cause the activist and the board to be more receptive to compromising on the alignment of their goals (Lawrence, 1986). This then serves to improve goal alignment, and in doing so allow for both activists and incumbents to address issues 5 identified during an activist campaign (Huy et al., 2014). Hence:

Age similarity lessens the negative main effect between activist shareholders on a board and firm strategic change.

Methods

Research design

In researching how alignment and legitimacy perceptions impact shareholder activists as they worked with incumbent directors on boards, it was necessary to design a study that tracked individual activist shareholders who gained board representation, as well as the incumbent directors they worked with in firms targeted by activist campaigns.

Sample selection and data collection methods

Because firms are targeted by shareholder activism more often in the United States (U.S.) than anywhere else in the world (Activist Insight, 2020), a sample of archival data from publicly traded firms affected by shareholder activism in the United States was used. Building upon past literature, I began by obtaining a list of U.S. firms affected by shareholder activism events through the Activist Insight database (DesJardine and Durand, 2020). As a result, the Activist Insight database constrained the sample of firms affected by shareholder activism from January 2010 to November 2020. Because the focus of this study involves activist directors appointed onto boards through financial activism, individual shareholders, firms such as activist hedge funds, and large institutional investors (Activist Insight, 2019) were considered in creating the list of firms affected by shareholder activism that also had board representation as the outcome of the activist campaign. The final dataset 6 involved 813 distinct activist-targeted firms in the United States, which amounted to 2251 total firm-year observations in the dataset.

Dependent variable

Because shareholder activists and their targeted firms often involve diverse industries, a measure of strategic change as proxied by resource allocation was used. As the focus of this paper involved shareholder activists and how they shape firm change, such an approach is thus consistent with definitions of strategy that “entail the discretion of strategic leaders (such as boards) to adjust and renew resources to attain or sustain competitive advantage” (Chandler, 1962: p. 58). Following prior research, six strategic resource dimensions of a firm were examined: Advertising Intensity, Research and Development (R&D) intensity, Plant and Equipment (P&E) newness, Nonproduction Overhead, Inventory Levels, and Financial Leverage (Finkelstein and Hambrick, 1990). Aside from tracking how boards make important changes in their strategic decision-making, this method of measuring for change aligns with the context of shareholder activism as well; it is known that activist campaigns rarely involve just one demand from a shareholder activist. Many such campaigns involve multiple shareholder demands, often from multiple activist shareholders as well (Ahn and Wiersema, 2021).

Below, I articulate how each resource dimension aligns within the context of shareholder activism. First, Advertising Intensity is defined as a firm’s advertising expense divided by its net sales. The importance of advertising in financial markets and its potential to shape investor perceptions is examined in studies that suggest investor attention can be significantly swayed by a firm’s advertising efforts (Madsen and Niessner, 2019). Activist shareholders targeting firms may perceive excessive advertising expenditures—especially when they do not correlate with improved financial performance—as indicative of broader mismanagement.

Second, R&D intensity is measured as a firm’s R&D expenditures divided by its net sales. Shareholder activism has seen firms reduce their expenditures on R&D as a direct result of activist involvement. For instance, DuPont has laid off research scientists to lower its R&D spending, influenced by activist pressure from hedge fund Trian Fund Management (Semuels, 2016). Similarly, GlaxoSmithKline has shifted funds away from R&D, in response to the activist demands made by hedge fund Elliot Management (Elliott Advisors (UK) Limited, 2021). A statement that best epitomizes this inclination of shareholder activists influencing firm R&D spending is a statement by former P&G CEO David Taylor, who expressed this sentiment when his firm came under scrutiny from activist hedge fund Trian Fund Management, “… and he’s proposed something very dangerous for the long-term future of this company, and that is eliminating our corporate R&D” (CNBC, 2017b).

Third, P&E newness is defined as net P&E expenditure divided by gross P&E expenditure. Expenditures related to the plant and equipment of a firm may be impacted by merger and acquisition (M&A) related activism, which has seen steady increase in recent years (Sawyer et al., 2022). Notable examples of M&A activism of late have mainly involved activist hedge funds, such as Icahn Enterprise’s vocal opposition towards the acquisition of Anadarko Petroleum by Occidental Petroleum, Third Point’s opposition towards the merger between United Technologies Corporation and Raytheon, and Mantle Ridge’s push for the sale of Aramark (ICLG, 2020).

Fourth, Inventory Levels are measured as the cost of inventory divided by a firm’s net sales. High inventory levels can indicate potential issues such as overproduction or poor sales, which may prompt activist intervention (DesJardine et al., 2021). Further, firms targeted by activists tend to exhibit significant operational changes in response to activism, which may include strategies to streamline inventory management as part of broader performance improvement initiatives (Goranova and Ryan, 2014).

Fifth, Nonproduction Overhead is defined as a firm’s selling, general and administrative (SGA) expenses divided by its net sales. SGA expenses pertain to the operational costs of a business that are not directly related to the manufacturing of its goods and services. Shareholder activists very commonly demand for firms to reduce operational costs and optimize business processes, as seen in examples involving hedge fund Starboard Value and Darden Restaurants (Gara, 2016), as well as Trian Fund Management and DuPont (Semuels, 2016).

Last, Financial Leverage measures a firm’s total debt divided by its total assets. Shareholder activists may advocate for companies to reduce their debt, as demonstrated by the campaign led by hedge fund Engine Capital Management surrounding Parkland Corp. (The Canadian Press, 2023). Relatedly, such activists may also insist that their target firms divest assets associated with underperforming businesses within their portfolio. This was exemplified in the situation between Icahn Enterprises and eBay, where eBay spun off its PayPal business following pressure from the activist investor (Mitchell and Chang, 2014). Therefore, measuring for firm strategic change through the six dimensions of firm resources articulated aids in comprehensively tracking the diverse demands that activists often impose onto firms (Ahn and Wiersema, 2021).

A one-year 7 time lag was induced into these resource dimensions and is consistent with Park (2007) and Westphal and Fredrickson (2001), who have suggested that lagging the dependent variable captures the time needed for strategic decision-makers to implement appropriate changes. Borrowing from the work of Triana et al. (2014), I then utilized data related to firms targeted by activists to create change scores for each of the six resource dimensions. This was done by subtracting the 2011 resource level from the 2010 resource level of each dimension, for example, for all firm years up to 2020. Because change is indifferent to the direction of the change, the absolute values of each of the change scores relating to the six resource indicators were utilized to create a single measurement of strategic change (Triana et al., 2014). Due to each resource indicator having a different unit of measurement than the other, z-scores were also created for each change score relating to the six resource indicators so that no single indicator would have a greater weight than any other (Triana et al., 2014). Finally, to coalesce at a single measurement of strategic change, the standardized absolute value differences in each of the six resource indicators from 2010 to 2020 for each 3-year period were averaged to create a final composite measure of strategic change (Haynes and Hillman, 2010).

Independent variables

The independent variable of this study concerns activist shareholders or employees of such shareholders who themselves hold board positions as activist directors. In obtaining data on such shareholder activists, data from Activist Insight was paired with hand-collected data obtained via director biographies in the Mergent Online database and through the SEC’s DEF14a filings. If an activist director was the activist shareholder or was also currently employed with the activist shareholder targeting a firm, this was operationalized through a count variable for the number of shareholder activists holding board positions associated with each firm year in the dataset. The moderating variable of age similarity involved the age of activist shareholders and incumbent board members (Zajac and Westphal, 1996) in an activist-targeted firm. Accordingly, age similarity was measured via a ratio of the average age of activist(s) over the average age of the board.

Control variables

Slack resources was operationalized as the log transformation of a firm’s financial cash reserves due to variances involving the amounts of cash involved in a firm’s financial holdings (Flammer et al., 2021; George, 2005). The firm size of the activist-targeted firm consisted of the firm’s market capitalization in a given market. It was mean-centered and operationalized as a log transformation of the value obtained from a firm’s market capitalization on a per year basis (Lungeanu and Zajac, 2019). Firm growth reflects change as it relates to the yearly sales of a firm and was operationalized as the log transformation of a firm’s yearly sales (Wiersema et al., 2020). Due to fluctuations over different industries, volatility was measured as the log transformation of the dispersion of sales in relation to the means of a firm’s dominant industry, on a per year basis (Qi et al., 2020). It is known that each day in an activist campaign constitutes an expensive event for both shareholder activists and firm management (Gantchev, 2013). An activist having spent large amounts of money and time in an activist campaign is likely to be more motivated to push for change than one who has not. Hence, I control for the commitment of activist shareholders through the variable activist days, which tracks the total number of days that an activist had invested into a firm and which was logged transformed due to variances in the data (Wiersema et al., 2020). Activist holding relates to the number of shares held by the activist shareholder in a firm during a given year and was log-transformed due to large variances over industries and firms (Wiersema et al., 2020). Firm performance was included as a control variable in all analyses and was operationalized based on a firm’s return on assets (Emilia, 2014; Youndt and Snell, 1995). Firm underperformance was operationalized as a binary variable, with “1” indicating that a firm that has a return on assets (ROAs) in a year exceeding its industry’s average and “0” indicating a firm has not (Wei et al., 2019). Increased share measures the difference in activist share ownership between the first and last (or current) years of activist involvement in a firm. This variable controls for an activist’s commitment; if the difference between the first and last (or current) year was positive, the categorical variable was coded as “1.” If the difference was negative, it was coded as “2.” If no changes occurred between the 2 years, it was coded as “0” (Miller et al., 2011). Mode of entry measures for how activist directors are nominated onto boards of firms. Unlike most incumbent directors nominated onto a board by shareholders during a firm’s Annual General Meeting, activist directors are distinct in how they enter the boards of firms. Resultantly, this paper tracks their mode of board entry through a binary variable, which codes for “1” if the activist director enters a board through a proxy contest and “0” if board entry was gained through private settlement (Ahn and Wiersema, 2021: p. 109). Board size measures the number of directors per year on a firm’s board (Chen et al., 2016). Because activist shareholders holding board positions gain board seats by first involving themselves in a firm’s activist campaign (Activist Insight, 2019; Monks, 1998), I track activist shareholders in a firm through the log transformed variable of more activists, which measures the number of activist shareholders involved in a firm’s activist campaign (Gupta et al., 2018). It is also known that board decision-making often occurs during board meetings, where board members may interact with each other to evaluate ideas and suggestions that may influence their firms’ strategy (Carpenter and Westphal, 2001). Resultantly, board meetings were measured as the number of times a firm’s board meets per year. In the United States, activist directors may be appointed by individual shareholders, firms such as activist hedge funds, or large institutional investors (DesJardine et al., 2021). To account for how this may influence activist change, shareholder category was operationalized as a binary variable, with “1” indicating individual shareholders and “0” indicating grouped shareholder (hedge funds and institutional investors) involvement in firms. To address outliers, all continuous variables were winsorized at the 1% level in both tails (DesJardine et al., 2022). All control variables were collected from Compustat except activist days, activist holdings, increased share, mode of entry, more activist, and shareholder category, which were collected from the Activist Insight database.

Analysis and results

Two-stage least-squares (2SLS) regression for endogeneity analyses

The longitudinal nature of the panel dataset used subjected this study to endogeneity concerns. In this study’s context, endogeneity may involve omitted variables that may influence the relationship between activist shareholder board placement, their similarity with incumbent directors, and a firm’s strategic change, which may lead to biased results (Semadeni et al., 2014). Because board members are not randomly appointed to boards (Fahlenbrach et al., 2010), 2SLS regression utilizing instrumental variables was used for this study. Accordingly, steps were taken to uncover valid instruments through instrumental variables that met the exclusion and relevance criteria (Greene, 2000).

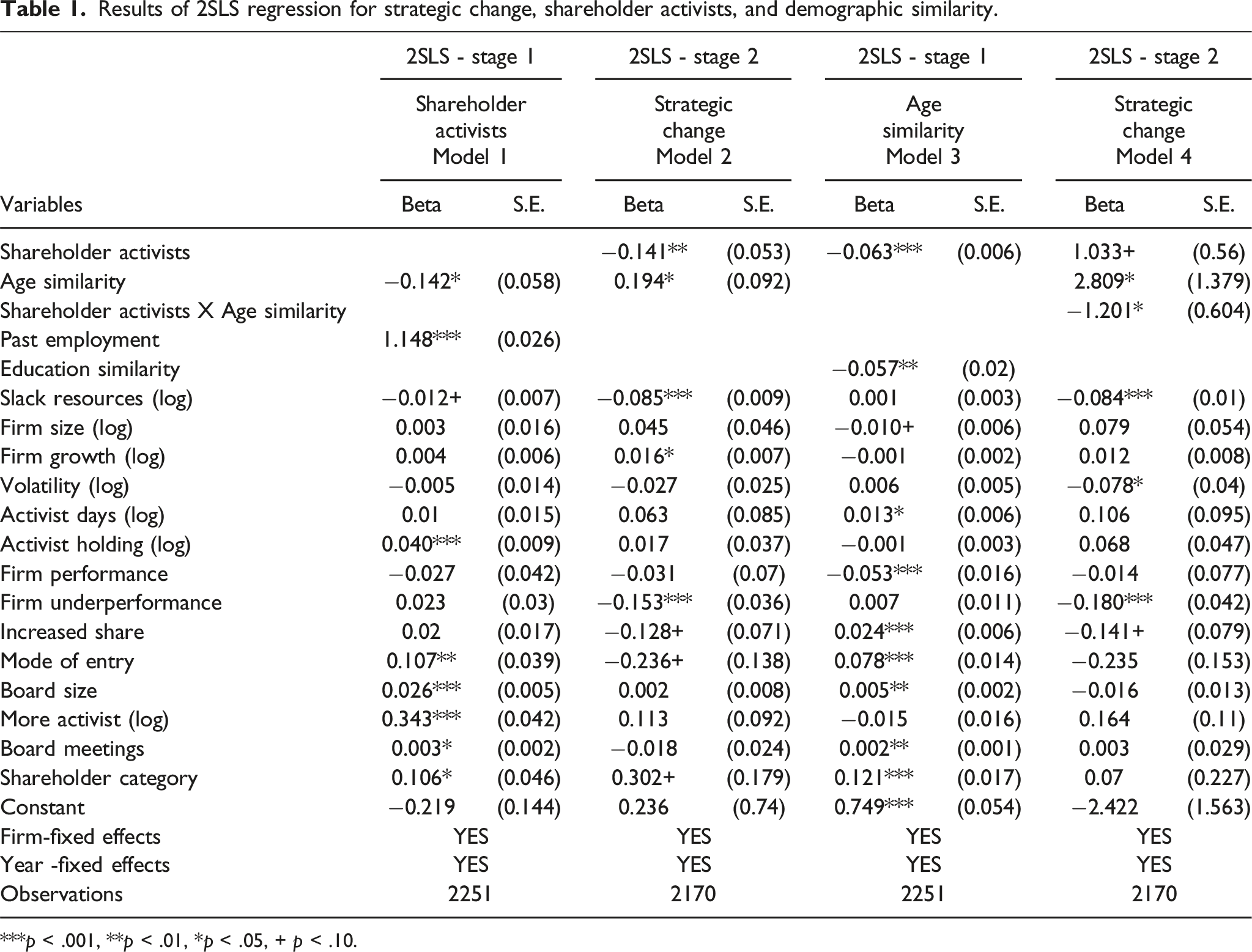

Results of 2SLS regression for strategic change, shareholder activists, and demographic similarity.

***p < .001, **p < .01, *p < .05, + p < .10.

Regarding the first instrumental variable, past employment, studies of the past have found that a commitment to one activist campaign often develops continued participation in activists toward activism for years on end (Van Dyke and Dixon, 2013). Put in the context of this study; it is thus plausible that activist shareholders employed previously with activists outside of a firm’s current activist campaign may choose to seek out board seats in a bid to continually participate in changing firms themselves. Conceptually and as an instrument, past employment fulfills the relevance condition as activist directors currently employed with an activist shareholder are likely to have some sort of past employment relationship with the activist as well. An activist hedge fund, for example, having spent considerable resources in challenging a firm (DesJardine et al., 2023), is unlikely to appoint representatives who have recently joined their ranks onto a firm’s board. Indeed, seasoned veterans of activist hedge funds such as Nelson Peltz and Carl Icahn have all but in recent years taken activist board positions in their targeted firms. Further, past employment also fulfills the exclusion condition as having only previous employment with the activist shareholder outside of the years of activism and without placement onto a firm’s board is unlikely to impact a firm’s strategic change significantly.

Concerning the second instrumental variable, education similarity, extant studies have found that the effect of education strengthens across age (Lynch, 2003) and that age influences the attainment of education (Cobley et al., 2008). Conceptually, education similarity fulfills the relevant condition for age similarity as activist shareholders sharing a similar age as incumbent board members are likely to possess similar education as well (Sanderson and Scherbov, 2016). Further, education similarity also fulfills the exclusion condition for age similarity as having similar education as incumbents without placement onto a firm’s board is unlikely to lead to any firm change on the part of the activist director.

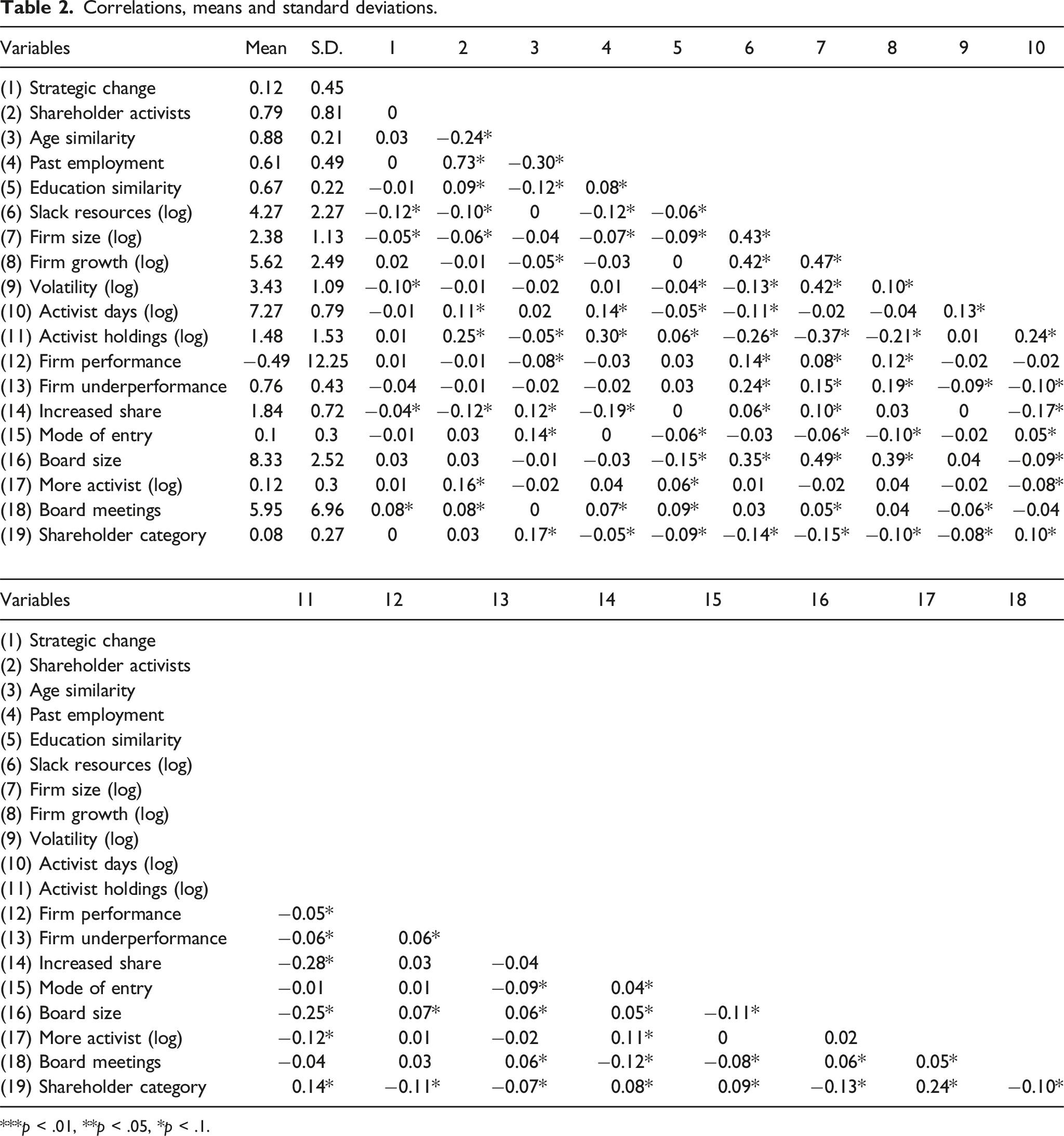

Correlations, means and standard deviations.

***p < .01, **p < .05, *p < .1.

Model 1 shows the first stage of the 2SLS fixed effect regression involving activist shareholders, whereby I estimate activist shareholders using past employment as an instrument. Following guidance involving single instruments (Semadeni et al., 2014), I highlight results that empirically illustrate how past employment is a valid instrument for activist shareholders. First, the coefficient estimate of past employment is positive and statistically significant (b = 1.148; p < 0.001) in the regression involving activist shareholders. Second, the p-value of past employment is 0.338 when regressed against strategic change. Third, the Cragg-Donald Wald F statistic (weak identification) of 821.875 shows that past employment as an instrument is well above the Stock and Yogo (2005) weak instrument threshold of 16.38 at 10% of maximal IV size. Thus, we can reject the null hypothesis that the model is weakly identified. Fourth, the Sargan statistic (overidentification) of 0.000 shows that the equation is exactly identified and does not suffer from overidentification. And last, the Kleibergen-Paap rk LM statistic (under-identification) of 552.125 shows that the model is not under-identified.

Model 2 shows the second stage of the 2SLS fixed effect regression involving activist shareholders, whereby the instrumented activist shareholder variable was estimated against strategic change. Hypothesis 1 predicts that activist shareholders are negatively associated with firm strategic change. The results from Model 2 are consistent with this prediction, as the relationship between activist shareholders and strategic change is negative and significant (b = −0.141; p < 0.01). Thus, Model 2 supports Hypothesis 1.

Model 3 shows the first stage of the 2SLS fixed effect regression involving age similarity, whereby I estimate age similarity using education similarity as an instrument. Key results that empirically illustrate how education similarity is a valid instrument of age similarity follow. First, the coefficient estimate of education similarity is positive and statistically significant (b = −0.057; p < 0.01) in the regression against age similarity. Second, the p-value of education similarity is 0.241 when regressed against strategic change. Third, the Cragg-Donald Wald F statistic (weak identification) of 17.289 shows that the instrument of education similarity is above the Stock and Yogo (2005) weak instrument threshold of 16.38 at 10% of maximal IV size. This means we can reject the null hypothesis that the model is weakly identified. Fourth, the Sargan statistic (overidentification) of 0.000 shows that the equation is exactly identified and does not suffer from overidentification. Lastly, the Kleibergen-Paap rk LM statistic (under-identification) of 17.289 shows that the model is not under-identified.

Model 4 shows the second stage of the 2SLS fixed effect regression involving age similarity. Here, the interaction of shareholder activists with the instrumented age similarity variable was estimated against strategic change. Hypothesis 2 explores how age similarity between activist shareholders and incumbents lessens the negative relationship between shareholder activists and firm strategic change. The results from Model 4 provide empirical support for this hypothesis, as the interaction between shareholder activists, age similarity, and strategic change is negative and significant (b = −1.201; p < .05). In addition, age similarity remained statistically significant (b = 2.809; p < .05).

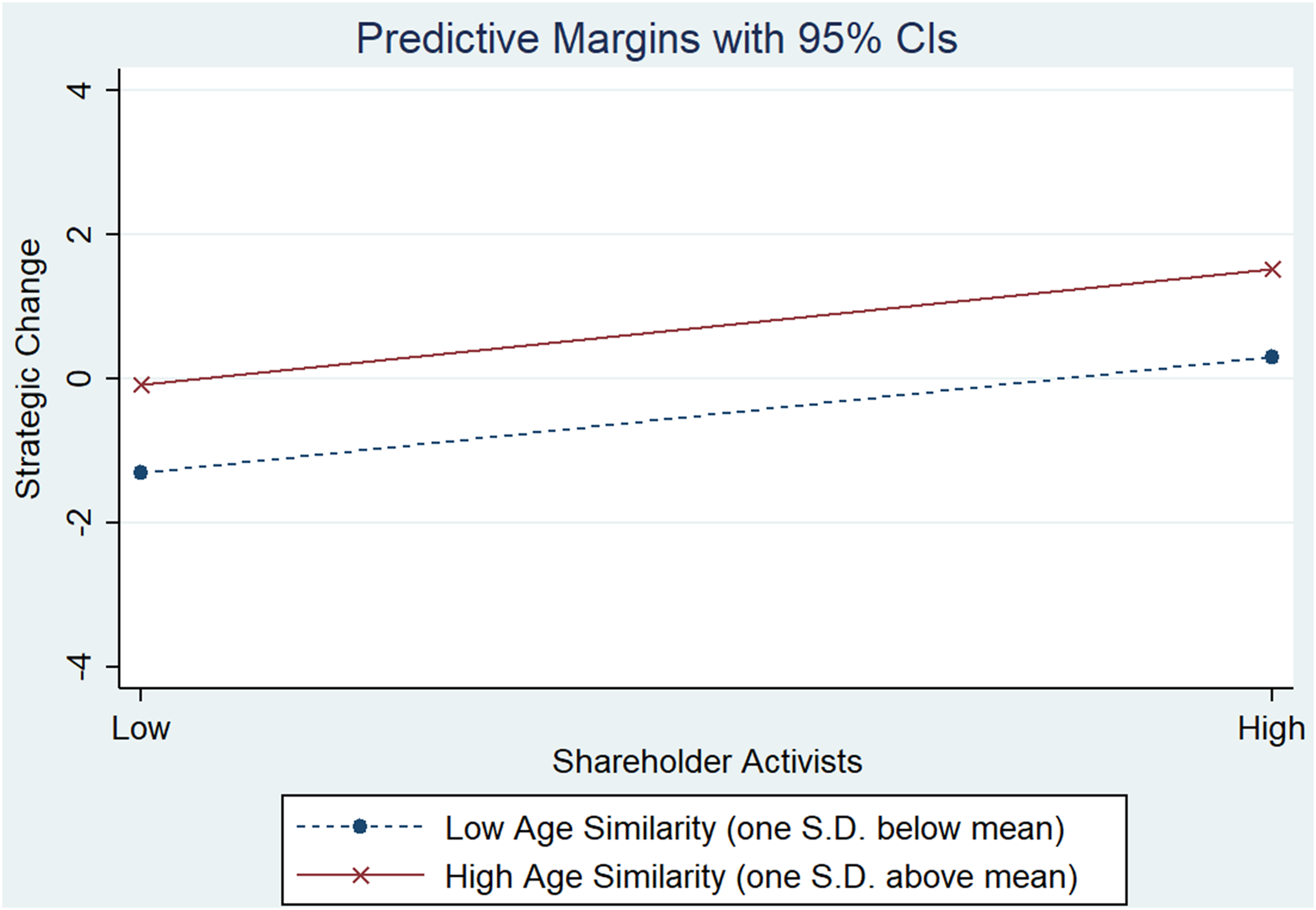

To further illustrate the moderating effect that age similarity has on shareholder activists and strategic change, I conducted a simple slope analysis. To do so, I took ±1 SD (standard deviation) from the mean for both the independent and moderation variables. Thus, 1 SD above the mean for the independent variable shareholder activists represents high numbers of shareholder activists, while 1 SD below the mean represents low numbers of shareholder activists on boards. Similarly, 1 SD above the mean for the moderating variable age similarity reflects high age similarity, with 1 SD below the mean reflecting low age similarity.

Figure 1 depicts the moderation effect outlined in Hypothesis 2, showing that the interaction slopes for both low and high age similarity were significant. Both slopes consistently exhibit positive effects on strategic change as the number of shareholder activists increases from low to high. In summary, Figure 1 demonstrates that the negative effect of activist shareholders on strategic change is lessened as age similarity between activist and incumbent directors increases. Thus, Model 4 and Figure 1 together provide support for Hypothesis 2.

Moderation effect of age similarity on shareholder activists by strategic change. The simple slope analysis shows both low and high age similarity lessening the negative main effect involving shareholder activists and strategic change.

Discussion

The research question considered for this study involved examining how activist shareholders or employees of such shareholders on a board affect strategic change. It is known that boards exist to advise and monitor firm management on behalf of shareholders (Jensen and Meckling, 1976). Yet, the recent prevalence of activist shareholders and their employees holding board positions in activist-targeted firms has served to challenge traditional notions of board agency. This paper’s attempt at explaining such a phenomenon has led to the formation of theories that examine how the placement of such activist shareholders on a firm’s board may impact its strategic change, as well as how demographic similarity between such activists and incumbent directors may serve to further explain such change. Below, I discuss the results, some important implications, limitations, and future research directions.

In Hypothesis 1, activist shareholders on a firm’s board were posited to negatively influence firm strategic change. This hypothesis was found to be statistically significant through Model 2 of this study’s analysis. Activist shareholders holding board positions are believed to be instrumental in enacting firm change (Monks, 1998; Walker, 2016). Such a belief may stem from the positions that their dual roles afford them; not only do such activists highlight firm weaknesses as activist shareholders (Sullivan & Cromwell LLP, 2018), they are also privy to board positions that allow them to address such inadequacies in shaping firm strategy (Westphal and Fredrickson, 2001). Yet, such a belief relies upon a rational lens in viewing how activist placement may lead to change. Answering the call for a behavioral approach (Ahn and Wiersema, 2021: p. 110) involving incumbent directors on a board, the first finding supports the notion that board placements involving activist shareholders introduce alignment and legitimacy issues into boards targeted by shareholder activism, which then negatively influences firm change. Adopting a board-level perspective which differs from existing firm-level studies on activist change (DesJardine et al., 2021; DesJardine et al., 2023), this finding underscores the crucial role that activist shareholders can play in driving activist change. While previous research on hedge fund activism has depicted activist-appointed directors as a key mechanism for such change (Bebchuk et al., 2020; DesJardine et al., 2023; Wiersema et al., 2020), the specific behavioral conditions under which this change may be driven have remained largely unexplored. This finding shows that perceptions of alignment and legitimacy associated with activist shareholders can negatively impact activist change, demonstrating that activist shareholders themselves may play a crucial role in shaping such perceptions, particularly in the context of collective decision-making by boards that affect activist change.

One practical implication of this finding relates to shareholders’ selection of activist directors. Based on the findings from Hypothesis 1, activist shareholders advocating for change may do well to avoid selecting and appointing themselves or their employees onto the firm’s boards. Such shareholders may choose instead to appoint activist directors who may be more independent in nature to avoid issues relating to alignment and legitimacy perceptions that may accompany shareholder activist placement on boards. A limitation of the finding from Hypothesis 1 involves how the intensity and complexity of activist change remain unexplored in relation to activist shareholder perception on boards (DesJardine et al., 2021; Triana et al., 2014). It is known that some activist shareholders who gain board seats may see themselves as “first among equals” in the boardroom, often causing incumbent directors to feel intimidated in acquiescing to their demands (Kirman, 2017: p. 77). Yet, it would be unfair to generalize this behavior upon all activist shareholders on boards, as activist hedge funds like Starboard Value and ValueAct Capital, for example, are known to embrace collaborative approaches towards their activism in firms (Wiersema et al., 2020). Given that strategic change as proxied by resource allocation remains as one of the more prominent ways of measuring for changes in firm strategy resulting from strategic decision-making (Oehmichen et al., 2017; Triana et al., 2014; Zhang and Rajagopalan, 2010), it would be interesting for future research to explore how different activism approaches embraced by activist shareholders on boards may result in firm change that is intense (high investment and short timeframe), or complex (low investment and long timeframe). Doing so may then reveal uniquely interesting findings that speak to the intensity and complexity of activist change in firms, as they relate to having activist shareholders on boards.

Hypothesis 2 proposed that age similarity lessens the negative relationship between shareholder activists and firm strategic change. This hypothesis was found to be statistically significant through Model 4 of this study’s analysis, with its moderating effects depicted in Figure 1. As demonstrated by a recent proxy battle involving Disney and Trian Fund Management, activist shareholders like Nelson Peltz frequently appoint themselves to boards to directly influence a firm’s strategy (Weprin, 2024). Despite Trian Fund Management’s extensive efforts to secure board seats for its activist nominees at Disney, shareholders ultimately opted to support the incumbent slate of directors over the activists’ candidates. In retrospect, the outcome of this activist campaign might have differed if the activists had considered the potential benefits of age similarity with incumbent directors when nominating themselves onto the firm’s board. The second finding supports the notion that age similarity between shareholder activists and incumbent directors fosters a shared group identity and promotes familiarity, facilitating the exchange of experiences between the two parties. This then serves to help reduce relational tension and mitigate goal alignment challenges, two potentially common problems experienced in activist campaigns (Lipton, 2024), and ultimately lessens the negative impact of shareholder activists on firm strategic change. Reflecting the behavioral governance perspective advocated by Wiersema et al. (2020), this finding highlights the significant role that demographic factors may play in shaping the behavior of incumbent directors on a board. As noted by Wiersema et al. (2020) and Westphal and Zajac (2013), the behavior of corporate actors occurs within a “socially situated context,” which influences the perceptions and interactions among them. Given that activist campaigns are increasingly becoming ambiguous and uncertain social contexts (Wiersema et al., 2020) to which board members must respond, this finding further emphasizes that certain demographic factors should not be overlooked in their impact on motivating activist change. One practical implication of this finding involves how activist shareholders may do well to embrace boards of similar age, particularly as they consider appointing themselves, or activist directors employed by them onto boards. Given how activist campaigns involving shareholder activists on board have been found to negatively impact firm strategic change in this study, such activists may instead focus their board appointments on boards that have incumbent directors like themselves in age, to lessen the negative effects associated with their board placements on strategic change. A limitation of Hypothesis 2’s finding involve how other factors may interact with similar age, in influencing perceptions relating to activist shareholders on boards. For example, an activist director may be similar both in age and education as compared to incumbent directors. Similarly, incumbents may be similar in tenure and functional experience as activist directors on boards. Hence, future research exploring three-way moderating interactions, as they relate to demographic similarity on boards may yield interesting theory and findings as well. Further, future research in this area may consider as well, how other similarity-related factors influence firm change through alignment (Tsui & O’Reilly, 1989) and legitimacy (Tost, 2011) perceptions in exploring antecedents that influence a firm’s strategic change. For example, it is known that stock ownership by directors serving on boards is commonplace in modern firms (Hillman et al., 2011). Similarly, social ties have also been found to foster collaboration in boards (Westphal J. D., 1999). Further, many directors stem from diverse professional backgrounds (Westphal and Bednar, 2005). Yet, much remains unexplored as to how such board-related factors influencing activist and incumbent directors may serve to align, or misalign interests in firms targeted by shareholder activism. The theory and results associated with the study of activist shareholders and their impacts on firm change contribute broadly to three streams of research. First, it advances research on boards through theory that explains decision-making between activists and incumbent directors. While considerable research has been done on board decision-making in the past, most of it has not focused on boards in the context of shareholder activism. Further, much of the board literature has put forth how boards cohesively gather and share information (Carter and Lorsch, 2004) in creating team-based decision outcomes that affect the long-term change of an organization (Judge and Zeithaml, 1992). Yet, assumptions remain about the passive stance incumbent directors may take as they work together with activist shareholders who themselves may play the role of an activist-appointed director in the enactment of firm change. Through theorizing the alignment and legitimacy perceptions associated with incumbent board members as they work together with activist shareholders on their boards, this paper highlights the behavioral implications related to the roles incumbents play in enacting change. Second, the paper contributes to research surrounding shareholder activism and its effects on firms. The literature on shareholder activism has acknowledged boards as instrumental in the enacting of change (Bebchuk et al., 2020; Coffee et al., 2018; Wiersema et al., 2020). Yet, much of the conversations in this literature have digressed from the specific examination of boards containing activist-appointed and incumbent directors to rational and more event-level explanations for activist-related firm outcomes. In examining vital demographic characteristics between activists and incumbent directors through a behavioral approach, this paper adds to the conversations in shareholder activism by highlighting important board-level factors associated with strategic change. Last, it advances agency research on boards by examining board-level decision-making involving activist shareholders and incumbent directors. While traditional agency research on boards has maintained that a board’s governance role obliges directors to serve shareholders through ratifying and monitoring managerial decisions (Hillman et al., 2000), much has been left assumed regarding shareholders who may act as agents in enacting change in their firms. In this light, the findings from this paper highlight conditions under which principals who themselves are agents may or may not work well with incumbent directors in enacting change on boards.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.