Abstract

As environmental problems continue to intensify, firms can consider using green innovation as an effective strategy to mitigate these problems. Although the effect of digital transformation on companies has been comprehensively evaluated, whether it is a positive factor for green innovation remains unclear. Thus, this study examined the relationship between digital transformation and green innovation. Panel data on 3021 firms from 75 industries in China’s A-share stock market for the period 2011–2021 were analyzed, and a fixed effects model was employed. Results showed that digital transformation positively influences green innovation; green management disclosure is one of the transmission channels for this influence. Additionally, industry-level institutional pressure negatively moderates the relationship between digital transformation and green innovation. This result is attributable to the duplication of influence paths with digitalization and unquestioning mimetic behavior to peer. The study expands the universality of the research results and further investigates the transmission mechanism between digital transformation and green innovation. Moreover, it suggests that firms should accelerate their digital transformation and utilize it to improve their disclosure of green management information. Firms can also employ other green practices to obtain legitimacy in the industry and reduce the negative impact of institutional pressure.

Keywords

Introduction

With the gradual development and increasing popularity of digital technology, large firms have been steadily accepting and implementing digital transformation as a crucial strategic decision (Bharadwaj et al., 2013). Managers need to understand the new management tool of digital transformation and apply it to address different issues, such as environmental problems.

Environmental problems continue to intensify, attracting global attention. As a result, various countries have reached consensus on the goal of carbon neutrality (Xue et al., 2022). How firms, as social subjects, fulfill their social responsibility is a crucial question. Green innovation involves waste reduction, pollution prevention, and recycling of products, processes, and management. It can achieve the goal of environmental protection as well as improve firms’ competitive advantage and economic performance (Xie et al., 2019). Therefore, green innovation serves as an effective strategy for firms to balance profit and environmental protection, thereby achieving sustainable development (Shahzad et al., 2022). Abundant research has focused on the factors that influence green innovation, such as strategy, culture, top manager characteristics, shareholders, policy, and society (Li et al., 2022). However, research on the emerging concept of digital transformation in the context of green innovation remains limited. Whether an effective mechanism exists between digital transformation and green innovation is worth discussing.

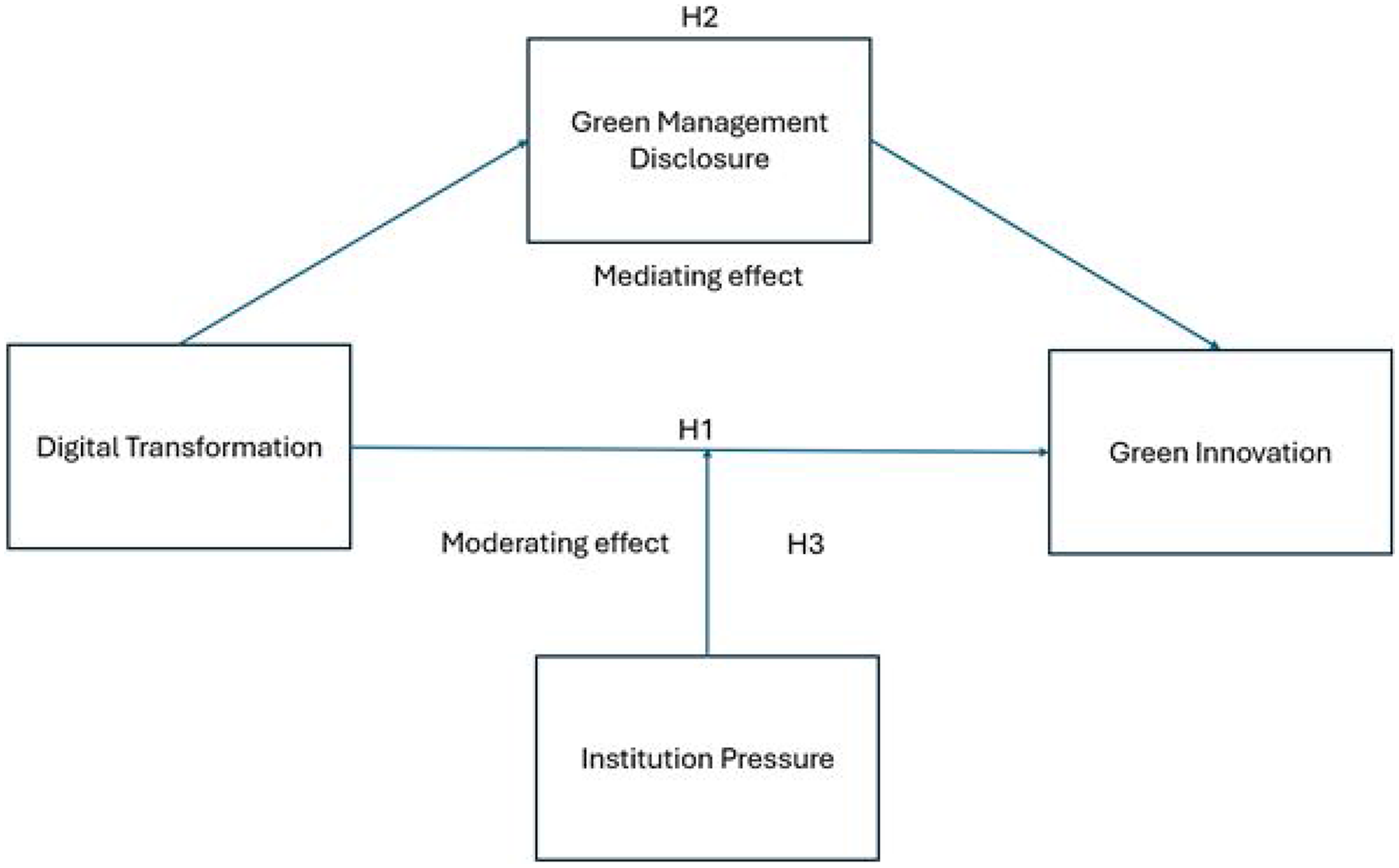

To improve managers’ utilization of digital transformation for green innovation, a mediator and a moderator are introduced to discuss further the mechanism between digital transformation and green innovation.

Green management disclosures are firms’ disclosures of management-level green practices, such as adopting the Environment protect system and progressing toward the EP goal. It is a form of environmental disclosure that helps managers understand the impact pathways of digital transformation on green innovation, thereby implementing the green innovation strategy effectively.

Institutional pressure is widely applied to investigate and achieve green innovation. He and Su (2022) stated that regulatory pressure can positively influence the progress of such innovation. Qi et al. (2021) also found that strict emissions policies prompt firms to adopt green technology. This paper mainly focuses on the institutional pressure on firms in a macro environment. Notably, institutional pressure also exists at the micro-level. According to Liu et al. (2010), industrial isomorphism exerts informal institutional pressure, influencing firms’ behaviors. Introducing the moderating role of industry-level institutional pressure to the research can help managers analyze the industrial environment to improve their utilization of digital transformation for developing green innovation.

This study makes the following contributions. First, the relationship between digital transformation and green innovation was examined and proven through empirical testing and robustness checks in response to the call by Sousa Jabbour et al. (2018). Following Takalo and Tooranloo (2021) study, samples were collected from 75 industries to further prove the universality of the relationship. Meanwhile, multiple theories were applied to demonstrate the positive relationship, including the upper echelon, social exchange, and absorptive theories. This allowed us to enrich the theoretical foundations of the research topic and widen its scope. Second, a new mediator and moderator were introduced to renew the transmission mechanism between digital transformation and green innovation. Based on the signal and stakeholder theories, green management disclosure was introduced as a mediator owing to its information exchange ability. This step refined the transmission mechanism from digital transformation to green innovation. Furthermore, green management disclosure and green practices showed a mutual positive influence. The study found a negative moderating role of industry-level institutional pressure, further clarifying the influence of institutional pressure on green innovation.

These findings can help managers better promote green practices through digital transformation to achieve sustainable development and obtain legitimacy. The study provides two practical managerial suggestions. First, firms should expedite their digital transformation efforts to enhance green practices, such as by improving internal communication systems, building coordinate networks, and enhancing knowledge acquisition ability (Feng et al., 2022; Tian et al., 2023; Warner and Wäger, 2019). This can enable firms to support green innovation, green management disclosure, and even more green practices. Second, in light of the negative moderating effect of institutional pressure, top managers should collect peer information to avoid the uncritical imitation of peer practices and strategically focus on the green innovation strategy that is the most suitable for firm internal environment (Sousa and Voss, 2008). Additionally, managers should accelerate the implementation of green practices to bolster the firm’s industry-level legitimacy, thereby mitigating the negative impact of institutional pressure (DiMaggio and Powell, 1983).

The remainder of this paper is structured as follows. The literature review is presented in the next section. This is followed by a discussion of the theoretical analysis and proposed hypotheses. After, data sources, variable definitions, and empirical models are introduced. Then, the empirical results and robustness tests are shown. The discussion section includes theoretical contributions, managerial implications, and research limitations. Finally, the conclusion is provided.

Literature review

Research on the digital transformation of firms

With the development of digital technology, such as 5G, big data, cloud computing, cloud storage, and digital platforms, corporate digital transformation has achieved increasing popularity, attracting attention from the academic world. Digitalization is a transformation that integrates digital technologies into firm operations and leads to the development of new organizational structures, business models, improved consumer interaction, and a collaborative approach (Hess et al., 2016).

On the one hand, digital transformation can benefit firms in multiple ways. Dynamic capability is an ability that enables firms to maintain their competitive advantage in rapidly changing environments (Teece et al., 1997). Digital transformation can improve firms’ ability to collect and integrate information while maximizing their existing abilities to react rapidly to the external environment, thereby enabling firms to develop dynamic capability (Ellström et al., 2021). Digital transformation allows firms to perform omnichannel selling, through which they can explore client groups and promote consumer shopping experience (Savastano et al., 2019). Digital platforms and cloud storage are key factors that enable firms to improve their absorptive ability. This ability is a learning mechanism for adapting to external knowledge and improving firm process innovation (Trantopoulos et al., 2017). Corporates can form a value-added network using digital technology, thereby benefiting from each other’s knowledge (Evens, 2010). Moreover, within corporates, digitalization can involve integrating different technologies to build a robust management or operating system and embedding it within their original organizational structure (Nadkarni and Prügl, 2021). Thus, digital transformation helps companies build competitive advantage, particularly in traditional industries, leading to improved performance (Zhai et al., 2022). However, digital transformation often requires substantial pre-investment at the initial stage. This requirement may influence short-term performance and benefit long-term returns (Jardak and Hamad, 2022).

On the other hand, digital transformation poses certain challenges for firms. One of these challenges is developing a suitable organizational structure. Li et al. (2021) argue that managers should oversee cognitive renewal, cultivate business team dynamics, and enhance organizational capacity. In manufacturing industries, the adaptation of the Internet of Things requires firms to establish new corporate entities to manage these technologies, and the collaboration between new and old corporate entities is also challenging (Bilgeri et al., 2017). Baptista et al. (2020) emphasized that workplace digitalization can significantly influence an organization’s basic digital/human configuration. Digitalization reduces corporate hierarchical levels, resulting in flatter corporate structures (Mirković et al., 2019). Digitalization influences not only organizational structure aspects but also corporate business models. It expedites the iteration of products and the erosion of property rights, forcing firms to adopt new, fast-growing business models (Nadkarni and Prügl, 2021). Chanias et al. (2019) also argued that digitalization changes business products and processes, thereby leading to entirely new business models to a certain extent. For example, by enabling rapid prototyping, 3D printing has vastly shortened the process applied in traditional business models (Rayna and Striukova, 2016).

Research on firms’ green innovation

According to Henderson (2006), innovation is the creation of new products and processes that enable firms to obtain an advantage in the market. Nowadays, the concept of sustainable development has gradually become common social sense, and companies are increasingly adopting sustainable values and undertaking efforts toward fulfilling corporate social responsibility (Magon et al., 2018). Green innovation is widely applied by firms as a critical strategic tool that can help them achieve sustainable goals (Weng et al., 2015). Green innovation consists of green process and green product innovation. Reducing resource waste and eliminating pollution during production are the main aims of green process innovation. In contrast, green product innovation ensures sustainable use and recyclability of the designed products (Xie et al., 2019).

One stream of current research addresses factors that influence green innovation in firms. Innovation needs corresponding knowledge storage, whereas green innovation is a new subject. Therefore, a firm’s dynamic capability and absorptive ability play significant roles in the innovation process (Huang and Li, 2017). A suitable organizational culture can also promote green innovation, particularly in terms of green organizational culture (Wang, 2019). According to Li et al. (2022), CEOs’ characteristics influence green innovation development. These characteristics include their overseas experience, voluntary workplace green behavior, and potential relationship networks. Moreover, Tian et al.’s (2023) study assesses the role of leaders in green innovation by discussing the impact of digital leadership.

The external environment also impacts green innovation. Green credit and government subsidies can fund firms to resolve the financial dilemma brought on by large green innovation investments (Gao et al., 2023). Li et al. (2024) also find that digital construction policy can benefit green innovation through higher market information accessibility and lower operation risk. Public awareness of sustainable development leads to different inspection levels of corporate social responsibility, which indirectly influences firms’ green innovation process (Liao et al., 2020). Hsu et al. (2022) applied the O-ring theory to the supply chain and found that one mistake made by one company in the supply chain will influence other participants. Thus, similarly, business partners in one supply chain will push others to develop green innovation for improved green performance.

The effect of green innovation on firms is also widely discussed. The most significant and direct effect is corporate financial performance improvement (Leenders and Chandra, 2013). Additionally, Woo et al. (2014) highlighted that green innovation positively influences labor productivity, taking into account the interests of enterprises and customers. Green innovation can improve customer interaction, helping firms accumulate customer resources and thereby promote sustainable corporate development (Burki et al., 2018).

Research on the relationship between digitalization and green innovation

Various types of studies have investigated the relationship between digitalization and green innovation, with some focusing on the macro-level environment. At the country level, digitalization can change industry structure and enhance market potential and economic openness to promote the green innovation level (Luo et al., 2023). A city with a high degree of digitalization and a strict environmental policy can significantly boost local green innovation (Filiou et al., 2023). In the manufacturing industry, the degree of application of digital technology and digitalization expenditure are two key factors that promote green innovation (Yin et al., 2022). Liao et al. (2024) also indicated that the digital economy can promote efficient industrial green innovation via access to external knowledge resources.

Research on the effect of digitalization on green innovation at the firm level has been relatively limited. The dynamic capability theory and resource-based view are two significant theories applied to explain the relationship between digitalization and green innovation (Ning et al., 2023). Lin and Xie (2024b) found that digital transformation can positively influence green innovation by improving management efficiency. Feng et al. (2022) stated that corporate-level digital transformation can enable firms to change existing business processes or products and obtain related knowledge from external environments. These aspects are vital for firms to implement green innovation. Based on the natural resource orchestration theory, Riaz et al. (2024) highlighted that green intellectual capital, green information systems, green management initiatives and green technology adoption can be enhanced by digital transformation, thereby promoting green innovation.

To further explore the mechanism underlying the relationship between corporate digital transformation and green innovation, the mediator factor is applied widely. According to Gao et al. (2023), green innovation is a long-cycle, high-risk, and expensive project, necessitating external funds. They found that government subsidies serve as a mediator factor. Other studies have reported that digitalization helps firms obtain green credit and relieve financial constraints to achieve green innovation (Gao et al., 2023). Tang et al. (2023) proved the mediator effect of collaborative networks brought by digital platforms on the abovementioned relationship.

Certain factors play a moderating role in the relationship, including firm size and location (He and Su, 2022). Lin and Xie (2024a) comprehensively discussed the moderating role of board characteristics. They found that size, gender diversity, and education level all positively moderate the relationship between digital transformation and green innovation. Gao et al. (2023) stated that firms that originally had high CSR scores will receive pressure and resources from stakeholders, thereby pushing green innovation further. He and Su (2022) found that the effect of digitalization is strengthened by external contingencies, such as regulation.

Although existing papers examine the multiple mechanisms between digital transformation and green innovation, certain moderating and mediating factors still require examination, such as green management disclosure. Existing research focuses on high-polluting industries, which cannot prove the universality of results. Based on the institutional theory, the impact of formal institutional pressure, such as government regulation, has been widely discussed. However, whether informal institutional pressure can positively influence green innovation remains to be explored.

Thus, this paper comprehensively explains the effect of digitalization on corporate green innovation and provides a solid research foundation to address the research gap in the literature. Thus, in this study, I further examine the mechanisms underlying the relationship between digital transformation and green innovation in firms by investigating the mediator role of green management disclosure. This investigation reveals another channel through which digital transformation promotes green innovation by improving information sharing. Furthermore, the mechanism shows the internal interaction between green practices. Subsequently, I apply the institutional theory at the industry level to investigate how normative pressure from peers influences a firm’s green innovation. This study extends the application scope of the institutional theory in this research field.

Theoretical analysis and research hypothesis

Relationship between digital transformation and green innovation in firms

The dynamic capabilities theory can be applied to explain the mechanism underlying the impact of digital transformation. Dynamic capabilities refer to a firm’s ability to adapt to various business environments to maintain its competitive advantage (Teece et al., 1997). The emergence of the concept of sustainable development has transformed firms’ external environments. For example, industry leaders advocate for a sustainable supply chain, and governments impose environmental regulations. These changes force firms to create an effective tool to develop their dynamic capabilities to adapt to the rapidly changing environment. Digital transformation is a form of organizational transformation that integrates digital technologies (Liu et al., 2010); thus, it is an effective tool for optimizing a firm’s internal resource allocation process (Michaelis et al., 2021). Additionally, digitalization transformation can accelerate information sharing within the firm and reduce information barriers between departments (Mooi and Frambach, 2012). Thus, it can enable the firm to rapidly change investment directions to crucial fields, such as green innovation. Brown et al. (2012) found that sufficient R&D expenditures can improve green innovation, further proving that digital transformation benefits green innovation through the centralization of capital resources. Furthermore, digital transformation can promote firms’ ability to strategically respond to external environments. Warner and Wäger (2019) further indicated that digital transformation could accelerate strategic renewal by rebuilding business models, collaborative approaches, and organizational cultures.

According to the absorptive capacity theory, absorptive ability refers to a firm’s ability to utilize external knowledge and information resources to gain competitive advantage (Bilgili et al., 2016). Digital technology, such as 5G and big data, enhances firms’ ability to search for external knowledge and information, thereby boosting green innovation. Ning et al. (2023) also stated that digital transformation can improve firms’ absorptive ability to promote green innovation. Ng and Wakenshaw (2017) stated that information is a valuable resource that can influence top managers’ decision-making processes. Sufficient information can reduce information asymmetry, thereby pushing firms to implement suitable strategies. Digital transformation can also collect information from the buy-side through big data, thereby designing market-oriented green innovation. Woo et al. (2014) stated that green innovation should consider buy-siders’ opinions to balance profit and green development and therefore continuously implement green innovation strategies. From the perspective of knowledge acquisition, accessible external knowledge resources can help corporations realize technological innovation, optimize industry structure, and increase energy utilization efficiency, thus achieving green innovation (Fu et al., 2020; Liao et al., 2024; Roszkowska, 2017). In addition, Liao et al. (2024) stated that the utilization rate of external knowledge resources is positively related to the digital economy and can promote green innovation efficiency.

According to the social exchange theory, knowledge sharing is a reciprocal and mutually rewarding process (Cook and Emerson, 2003). Digital transformation enables firms to undertake knowledge sharing. For example, firms can effectively build collaborative networks via digital platforms. As a result, they can obtain related innovation knowledge while reducing trial-and-error costs, thus saving resources and inspiring innovation (Tang et al., 2023). Salehi and Sadeq (2023) pointed out that the scope of digital technology, such as databases and digital conference systems, can enhance knowledge sharing, thereby promoting firm innovation. A collaborative network can also develop new multiple innovation models, such as crowdsourced design, collaborative R&D, and value-added development. These models offer firms the opportunity to undertake collaborative creation. In the network, new participants can access sufficient innovation factors that inspire the innovation enthusiasm of the entire network.

Furthermore, digital transformation can be influenced by a manager’s leadership. Digital leadership is one of the dynamic capabilities developed through digital transformation, which can be expressed in four abilities: digital thinking, digital detecting, digital reserve, and digital social abilities. These four abilities enable leaders to develop long-term strategies, make the right decisions in a dynamic environment, improve communication efficiency, and recruit high-quality employees (Tian et al., 2023). With the concept of sustainable development becoming mainstream, digital leadership can be defined as leadership that pushes corporations to embrace and utilize digital technology appropriately to achieve green goals (Tian et al., 2023). According to the upper echelons theory, leadership influences firm outcomes (Bantel and Jackson, 1989). Therefore, digital leadership can help firms achieve green innovation and stay updated on market trends and environmental protection regulations (Tan and Zhu, 2022). Thus, green innovation can achieve a balance between profit and green development. Digital leadership can also be expressed through digital thinking. Digital thinking provides firms with multiple perspectives for establishing a green strategy direction, such as green management systems and green process innovation, to promote green innovation. Digital leadership can effectively achieve the integration of information and communication technology into the organizational framework, changing communication ways and work patterns (Passmore, 2017). Therefore, firms can develop green innovation at relatively low costs and cultivate a green innovation culture within their organization (Priscilla et al., 2016). Accordingly, the following hypothesis is proposed: Conceptual model.

Digital transformation can help firms implement green innovation.

Mediating role of green management disclosure

Green management disclosure refers to firms’ voluntary disclosure of management efforts toward achieving sustainable development and solving environmental problems (Clarkson et al., 2008). The institutional theory holds that firms, as social subjects, will take action to seek legitimacy (DiMaggio and Powell, 1983). With sustainable development becoming mainstream, firms’ disclosure of environment-related information is an effective way to obtain legitimacy (Hummel and Schlick, 2016).

Digital transformation integrates advanced digital technologies such as cloud storage, blockchain technology, and all-digital industrial servo systems that can improve information quality, thereby promoting green management disclosure (Zhang and Zhao, 2023). Firms’ digital transformation can build internal information networks within their organization. With the increasing transparency of internal information, principal-agent costs can be eliminated. This phenomenon reduces the likelihood of senior managers pursuing tenure performance to falsify the related information. Wu et al. (2022) also emphasized that enterprise digitalization can suppress the tendency of internal opportunism, improving the reliability of information disclosure.

Furthermore, digital transformation can enhance firms’ efficiency in sorting internal information. For example, digital technology upgrades unstructured data and promotes the flow and sharing of environment-related information. In addition, digital platforms and big data technologies can help firms establish various communication channels to external environments, thus improving the availability of their green management disclosure. Manita et al. (2020) further supported this idea by revealing that digitalization can help audit companies access firms’ data easily. Digital transformation can also build green information systems to analyze information and develop coordination and communication channels with stakeholders (Riaz et al., 2024).

Green management disclosure shows firms’ concept of and goal regarding EP, related system-building, and employment training, among others. Green management disclosure can influence firms’ green innovation through two mechanisms. First, according to the signaling theory, information asymmetry serves as a bad signal to stakeholders; it leads them to suspect that firms are ignoring stakeholder demands in favor of emphasizing only profit maximization (Bae et al., 2018). A firm’s voluntary disclosure of environmental management details also serves as a positive signal that the firm will strive for sustainable development in response to stakeholder demands. This situation can expand the financial channel of the firm, thereby promoting green innovation (Xiang et al., 2020). Barua and Chiesa (2019) also stated that firms’ reliable disclosure can positively influence the size of green bonds they receive to support green innovation.

Second, green management disclosure can intensify external environmental pressure. Lanoie et al. (1998) observed that capital markets and communities are significantly motivated to regulate pollution if they have access to data on polluters’ environmental conduct. This aspect increases firms’ reputation risk of polluting, which pushes them to implement green innovation. Additionally, firms’ disclosure behavior can attract environment-sensitive customer groups, whose demand for green products and high standards for green practices can push firms to implement green innovation (Hu et al., 2021). Thus, the following hypothesis is proposed:

Green management disclosure mediates the relationship between digital transformation and green innovation.

Moderating role of institutional pressure

The institutional theory posits three types of pressure: coercive, mimetic, and normative. These pressures push firms to adjust their actions to obtain legitimacy (DiMaggio and Powell, 1983). Ang et al. (2015) also stated that external institutional pressure regulates firms’ operation range and influences their strategic response. On the one hand, coercive pressure refers to formal and informal regulations in external environments. Wang et al. (2018) found that mandatory CSR disclosure imposes institutional pressure on firms, which constrains earnings manipulation and mitigates information asymmetry. Li et al. (2024) also found that digital construction policy can strongly promote green innovation by reducing operational risk and enhancing market information accessibility. Informal pressure is often exerted by vital stakeholders. Dai et al. (2021) pointed out that retailers with strong bargaining power will request their suppliers to improve their CSR to achieve the goal of building a sustainable supply chain. Thus, increasing environmental coercive pressure will push firms to become greener. Based on the previous discussion, digital transformation can also adjust companies’ strategies regarding and resource allocation to green development. Therefore, the impact mechanisms of digital transformation and coercive pressure overlap with each other. This phenomenon may weaken the relationship between digital transformation and green innovation.

On the other hand, mimetic pressure holds that firms in an uncertain environment will imitate others who perform better than them (Zsidisin et al., 2005). Sustainability is a recent development concept; however, firms hesitate to take action because of its long-term and high-cost characteristics. Huang et al. (2022) found that firms will adopt similar green practices and management systems to promote their ESG. However, such imitative behavior will only benefit firms to a certain degree. Due to contextual differences, firm best practices only work in specific contexts, and imitation can lead to suboptimal results (Sousa and Voss, 2008). For example, firm size and liquidity constitute the entry-level requirements for green innovation due to the long-term commitment and high-cost characteristics of the efforts needed. Small firms that unquestioningly imitate large firms will engage in misguided green behaviors, leading to failure. Wu et al. (2012) and Liu et al. (2010) found that mimetic pressure does not influence firms to build and adopt sustainable supply chain management. Zeng et al. (2017) also directly stated that mimetic pressure has negative moderating effects on building SSCM. Thus, the following hypothesis is proposed:

Institutional pressure negatively moderates the mechanism between digital transformation and green innovation (Figure 1).

Methodology

Sample selection and data sources

Chinese firms are appropriate research subjects for certain reasons. First, their green practices have accelerated because of government policies and regulations in the past decade (Huang and Lei, 2021). Second, according to the International Data Corporation’s statistics, China’s industrial internet regional platform and service market reached USD264 million in 2021, ranking second worldwide (Feng et al., 2022). Considering data availability and the launch of the Green List of International Patent Classification in 2010, our samples included A-share listed companies in China from 2011 to 2021. These samples exclude the ST and ST* companies and financial firms. Green innovation data were collected from the China Research Data Service Platform (CNRDS) database; other variables were gathered from the China Stock Market Accounting Research (CSMAR) database. After excluding missing values, 23,822 observations from 3021 firms were retained for analysis.

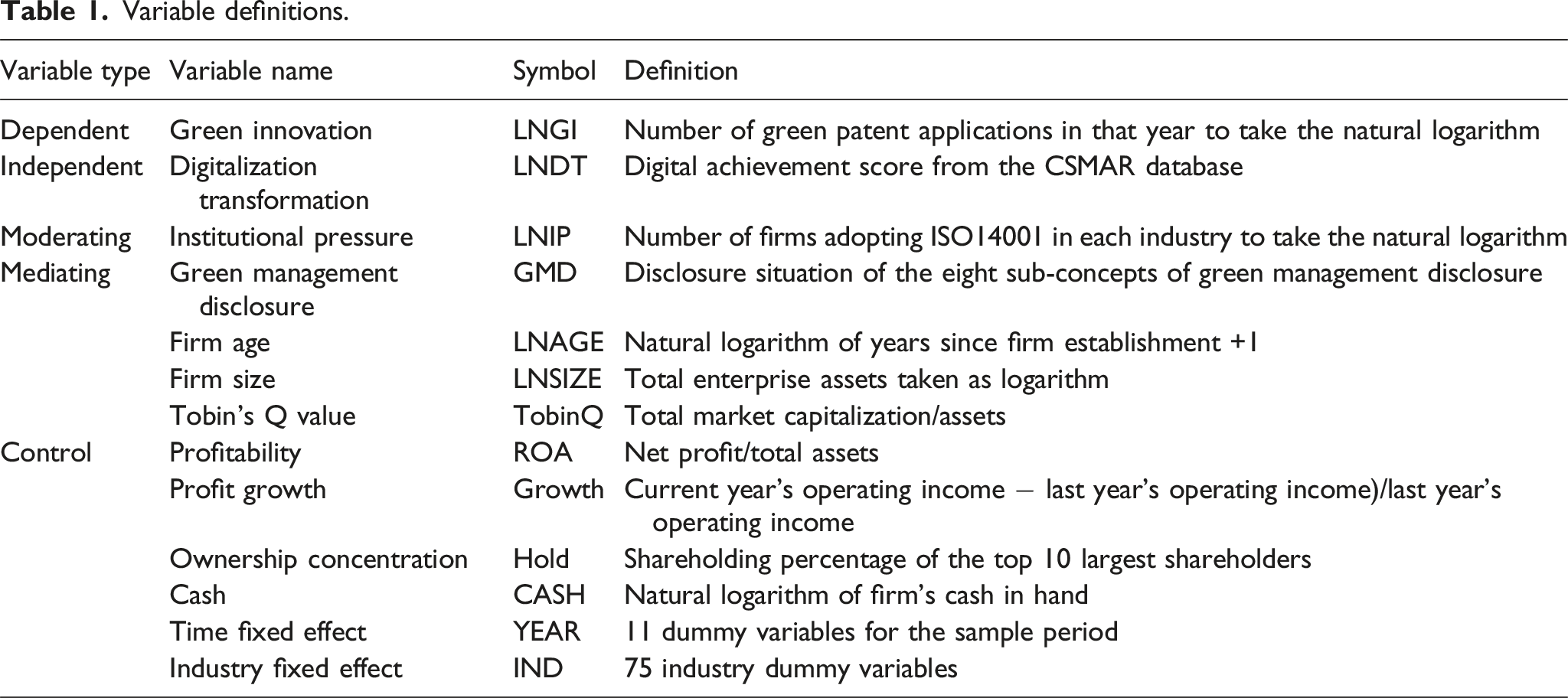

Variable definition

Dependent variable

A green patent constitutes an invention, a utility model, or a design patent (Lian et al., 2022). In this research, only utility and invention patents were applied to represent firms’ green innovation level. This is because product design cannot reflect firms’ green innovation situation (Lian et al., 2022). Drawing on Ning et al.’s (2023) study, a green patent application number can be used as a metric for companies’ green innovation. Because green patent authorization often requires 1–2 years after application, a green patent application is considered more appropriate for analysis. Moreover, a patent application from the listed company and its subsidiaries, joint ventures, and associates was considered to comprehensively assess the listed company’s green innovation situation. In this paper, the green patent application number was obtained from the CNRDS database. The natural logarithm of green patent application number +1 was taken to measure firms’ green innovation level.

Independent variable: Digital transformation level

Digital transformation is a form of organizational transformation that integrates digital technologies (Liu et al., 2010). Thus, the achievement of digital technology is an indispensable part of digital transformation. The digital achievement score focuses on firms’ technical achievement and can reflect their digital transformation level. Following Ling and Ge’s (2024) method, the digital achievement score from the CSMAR database was used to measure the digitalization transformation level. The digital achievement score is calculated using the following formula: (0.3668 × digital innovation standard) + (0.1174 × digital innovation paper) + (0.2354 × digital invention patent) + (0.1473 × digital innovation qualification) + (0.1331 × digital national award). This formula comprehensively evaluates firms’ efforts to achieve digitalization and their digital transformation level. The natural logarithm of the digital achievement score was taken to measure firms’ digital transformation level.

Moderating variable: Institutional pressure

Institutional pressure comes from firms’ desire for legitimacy in specific environments (DiMaggio and Powell, 1983). Thus, the more firms in an industry adopt the same environment-friendly management system, the more substantial is the institutional pressure imposed on firms. Drawing on Qi et al.’s (2021) research, selected firms adopting ISO14001 in each industry were considered in this study, and the natural logarithm was taken as the indicator of institutional pressure, obtained from the CSMAR database.

Mediating variable: Green management disclosure

Environmental disclosure is a tool that firms use to communicate with their external environment (Cho and Patten, 2007). Due to their information transmission role, environmental disclosures are widely used as mediators in sustainable development research (Iqbal et al., 2013; Kurniansyah et al., 2021). Green management disclosure also includes environment-related information. It reflects firms’ management efforts to achieve sustainable development (Clarkson et al., 2008). Xiao and Shen (2022) used the green management disclosure score from CSMAR as one of the indicators of environmental rating. The CSMAR database provides details of firms’ green management disclosure situation. It indicates whether firms’ disclosures include EP goal, EP concept, EP management system, EP training, EP honor, EP special act, EP emergency mechanism, and the three-simultaneity system. If the firms disclose one of the contents above, the score is 1 and 0 otherwise. Then, the values are added together to obtain the firms’ overall green management disclosure score.

Control variables

Variable definitions.

Empirical design

A two-way fixed effects model was applied to investigate the mechanism underlying the relationship between digital transformation and green innovation. Three regression models are often used for continuous panel data: pooled OLS, random effects model, and fixed effects model. The fixed effects model can effectively mitigate the omitted-variable bias by accommodating sample heterogeneity (Greene, 2001). In this research, industry and year effects were controlled. The effect of industry on green innovation has been widely evidenced by research, including the effects of difference in emission restrictions, various industrial regulations, and policies aimed at specific industries (Naveed et al., 2023; Yuan et al., 2021). These factors are usually ignored in research and are hard to control; hence, we should introduce industrial effects. From the empirical aspect, with the registration-based IPO system approved in 2019, the number of listed companies in China has grown significantly. Therefore, a third of the companies in the collected data have less than three observations over the sample period, resulting in insufficient data within groups. Therefore, effective estimation of individual effects cannot be supported. Furthermore, in models with a high degree of variability across firms, minimal within-firm variation will cause an overfitting problem. The average intra-group standard deviation of digital transformation is 0.187309, and the standard deviation across firms is 0.419399, which means that an overfitting problem is likely to occur. The control variables are all related to the characteristics of companies, which include financial performance, firm size, and ownership. Therefore, when we still control for the individual effects, the multicollinear problem will appear. The industry and year two-way fixed effect model is also widely applied in the literature (Feng et al., 2022; Ning et al., 2023). Additionally, an F-test was applied to test whether the intercepts are all equal to zero and thus confirm the existence of the industry and year effects. The results are 11.71, indicating that industry and year effects are significant at 1%. Therefore, the pooled OLS was not applied to the research. Moreover, the p-value of the Hausman test results is not supported by the random effects model. Therefore, the industry and year effects correlate with the dependent variables and are not a randomized disturbance term (Hausman et al., 1984). Accordingly, the fixed effects model is the best of the three models in the research. Finally, to address autocorrelation and heteroscedasticity issues, clustered and robust standard errors were applied.

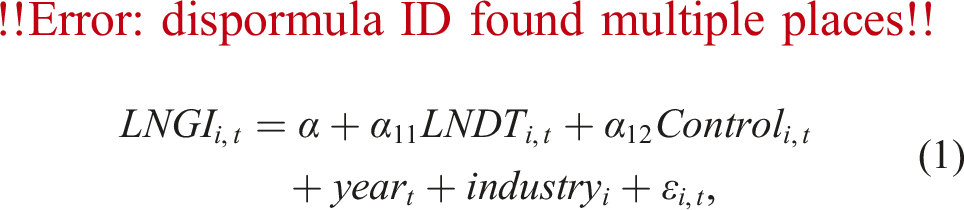

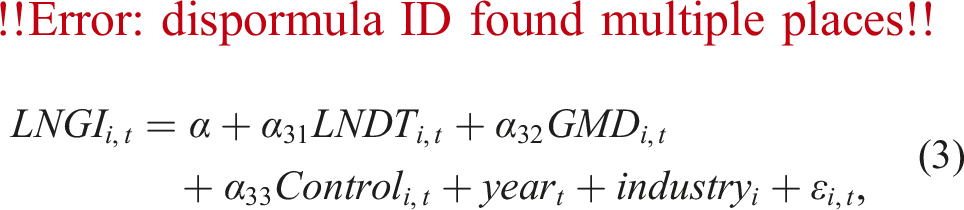

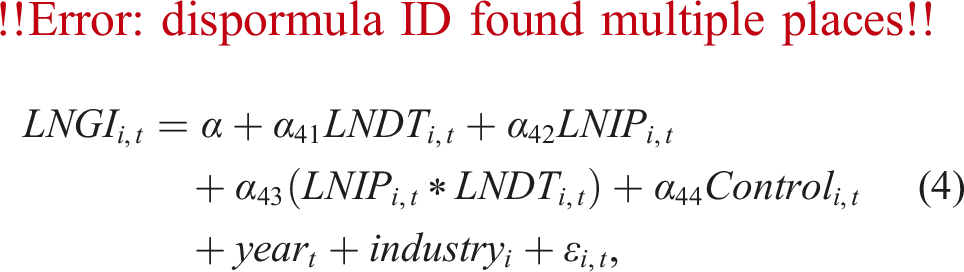

First, to examine the relationship between green innovation and digital transformation, equation (1) was applied as follows:

Empirical result and analysis

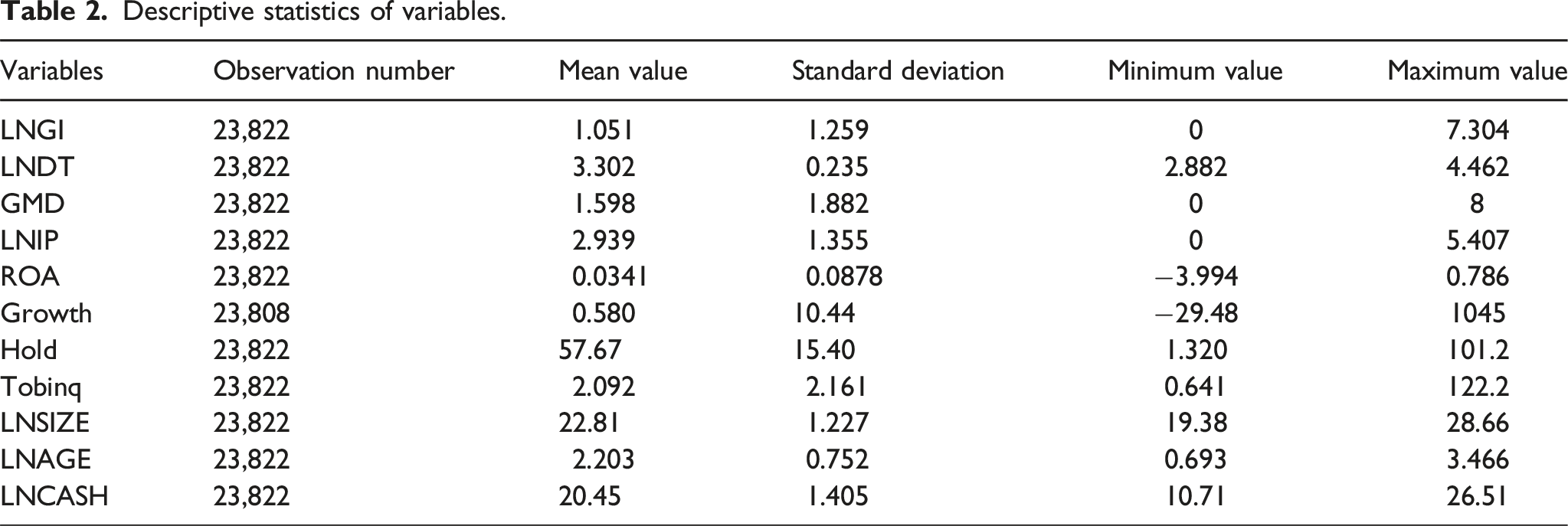

Descriptive statistics

Descriptive statistics of variables.

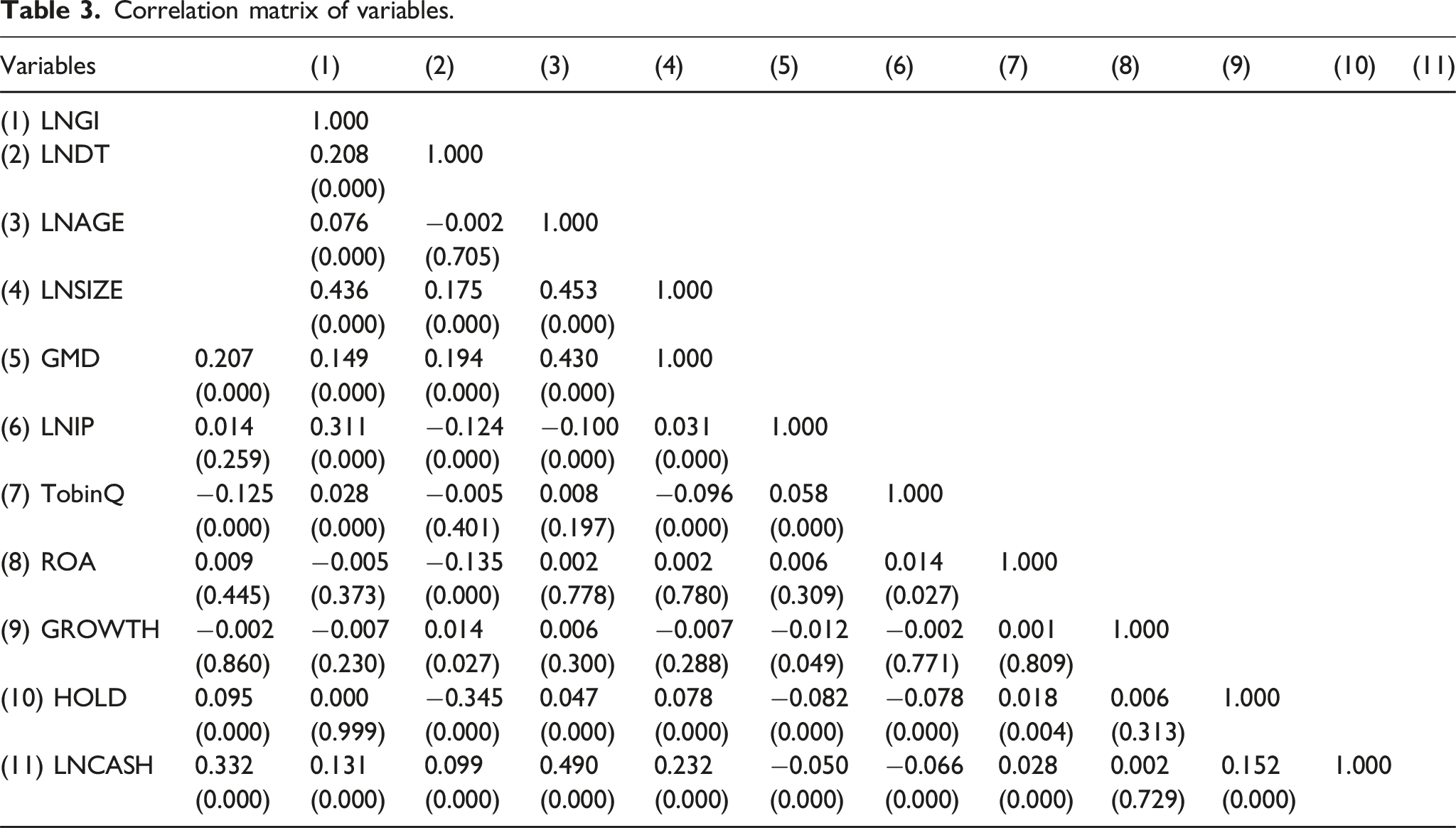

Correlation matrix of variables.

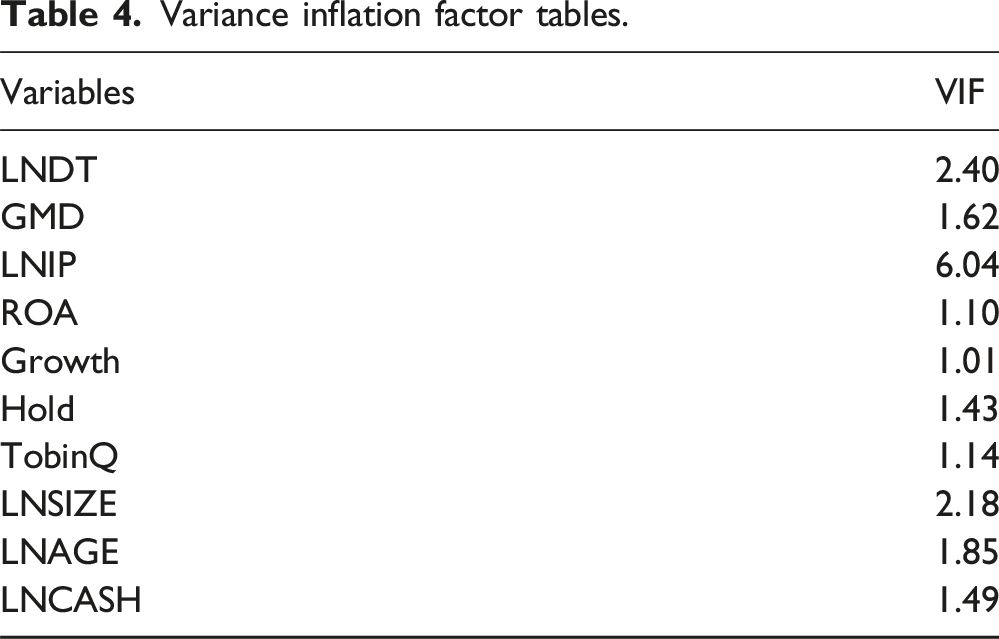

Variance inflation factor tables.

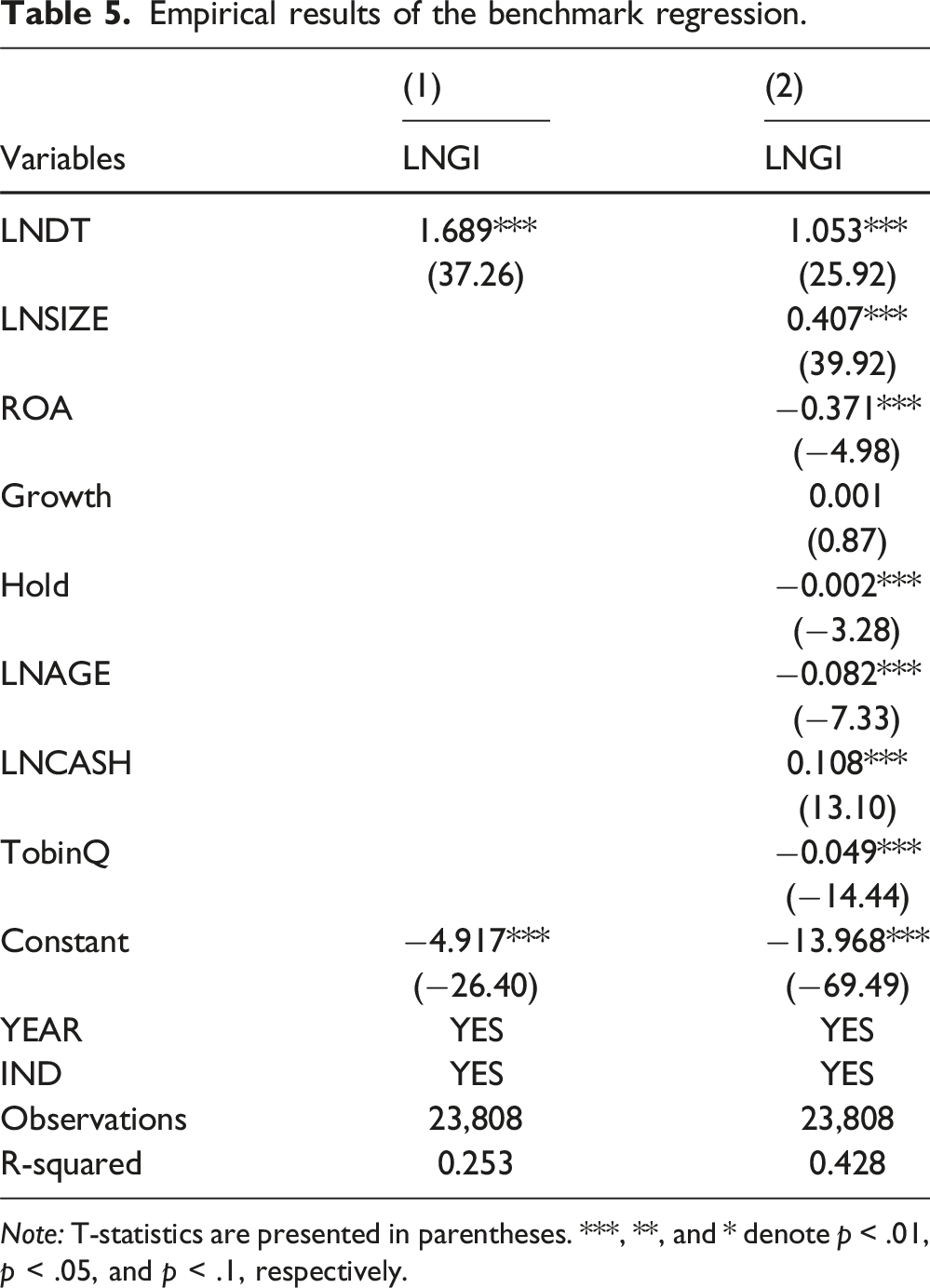

Benchmark regression result

Empirical results of the benchmark regression.

Note: T-statistics are presented in parentheses. ***, **, and * denote p < .01, p < .05, and p < .1, respectively.

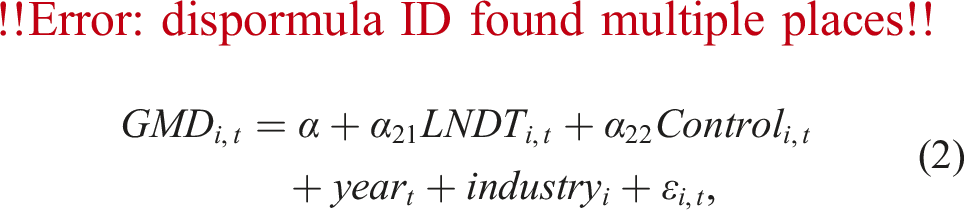

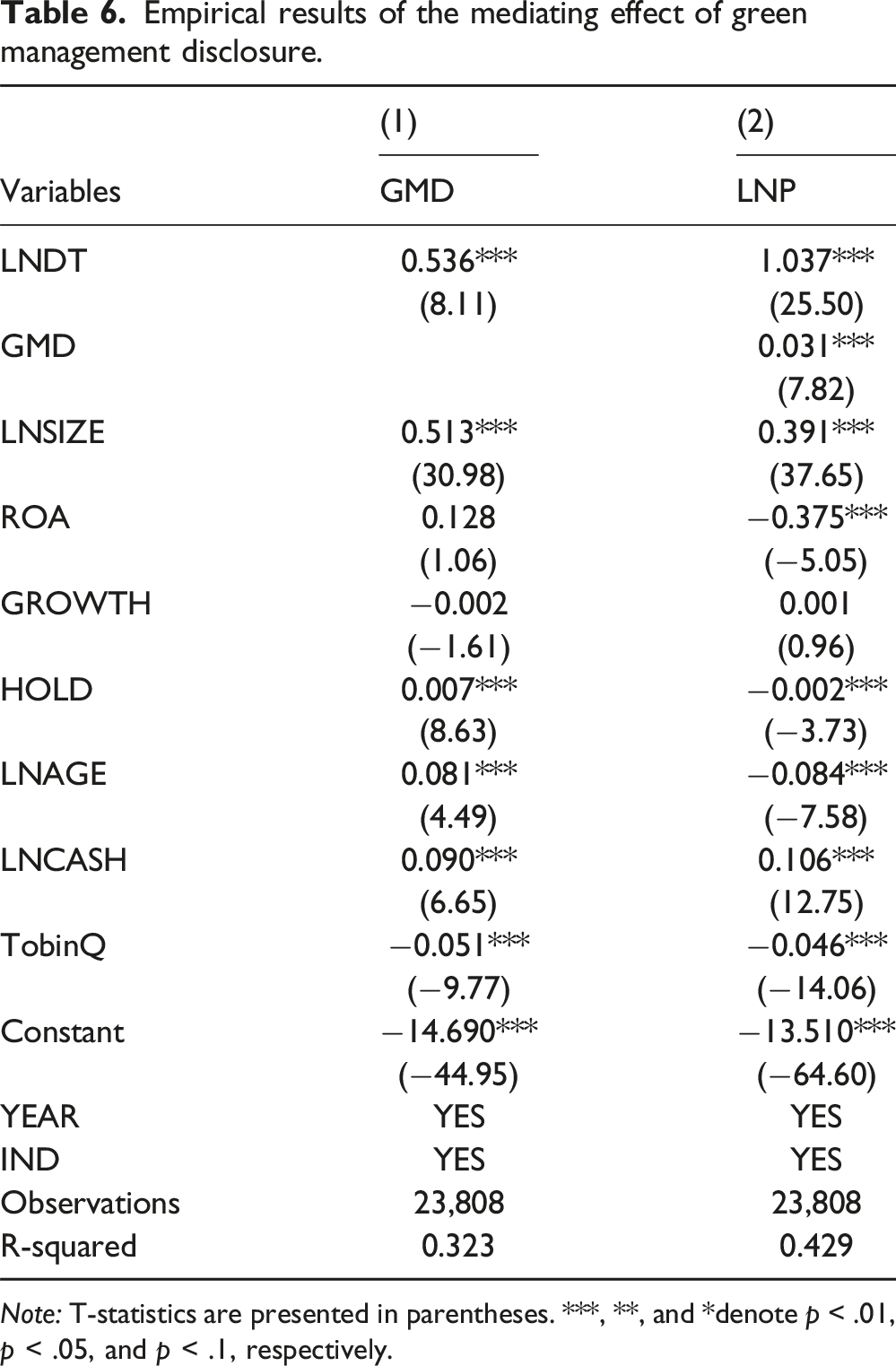

Examination of the mediator role of green management disclosure

Empirical results of the mediating effect of green management disclosure.

Note: T-statistics are presented in parentheses. ***, **, and *denote p < .01, p < .05, and p < .1, respectively.

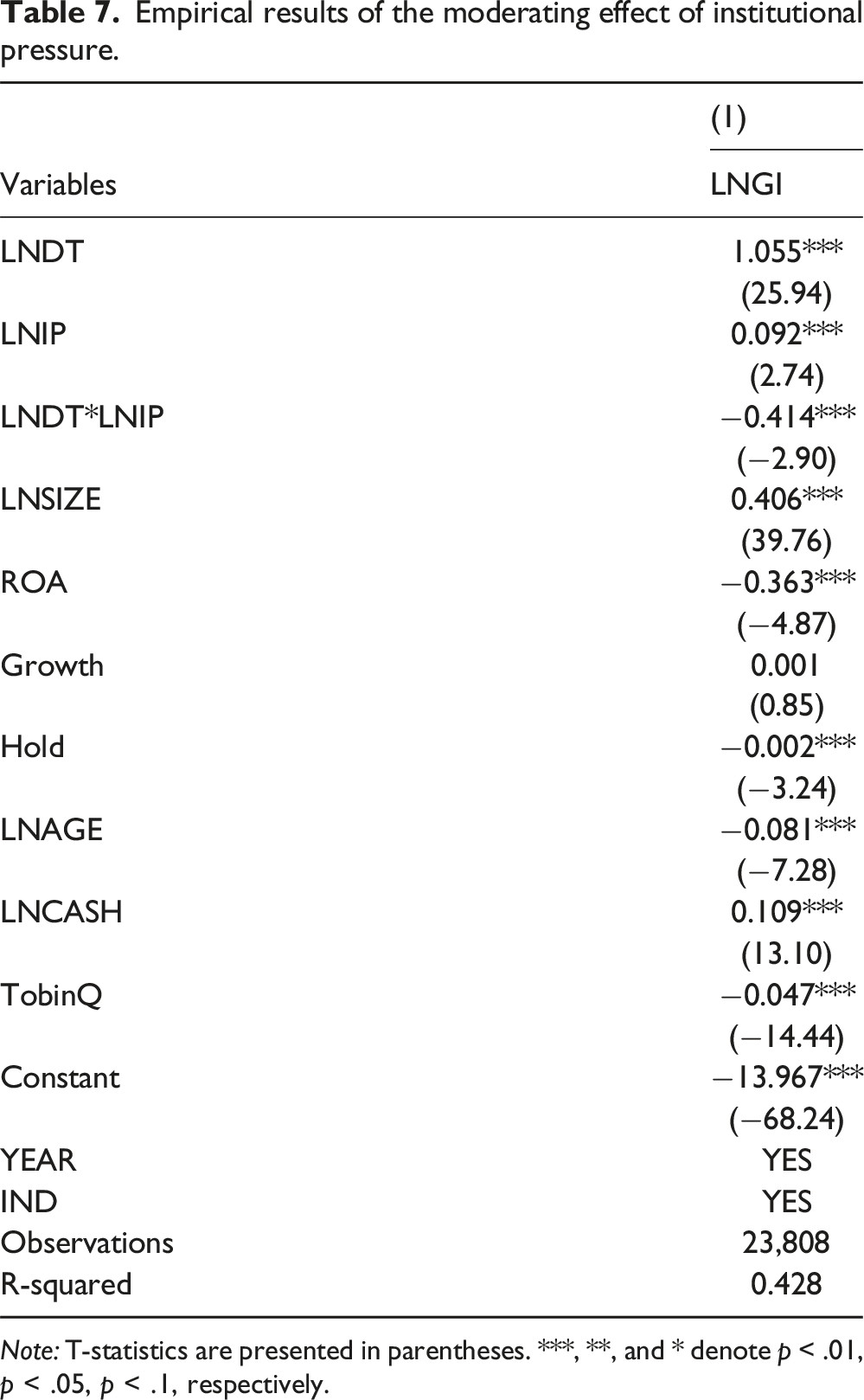

Examination of the transmission mechanism of institutional pressure

Empirical results of the moderating effect of institutional pressure.

Note: T-statistics are presented in parentheses. ***, **, and * denote p < .01, p < .05, p < .1, respectively.

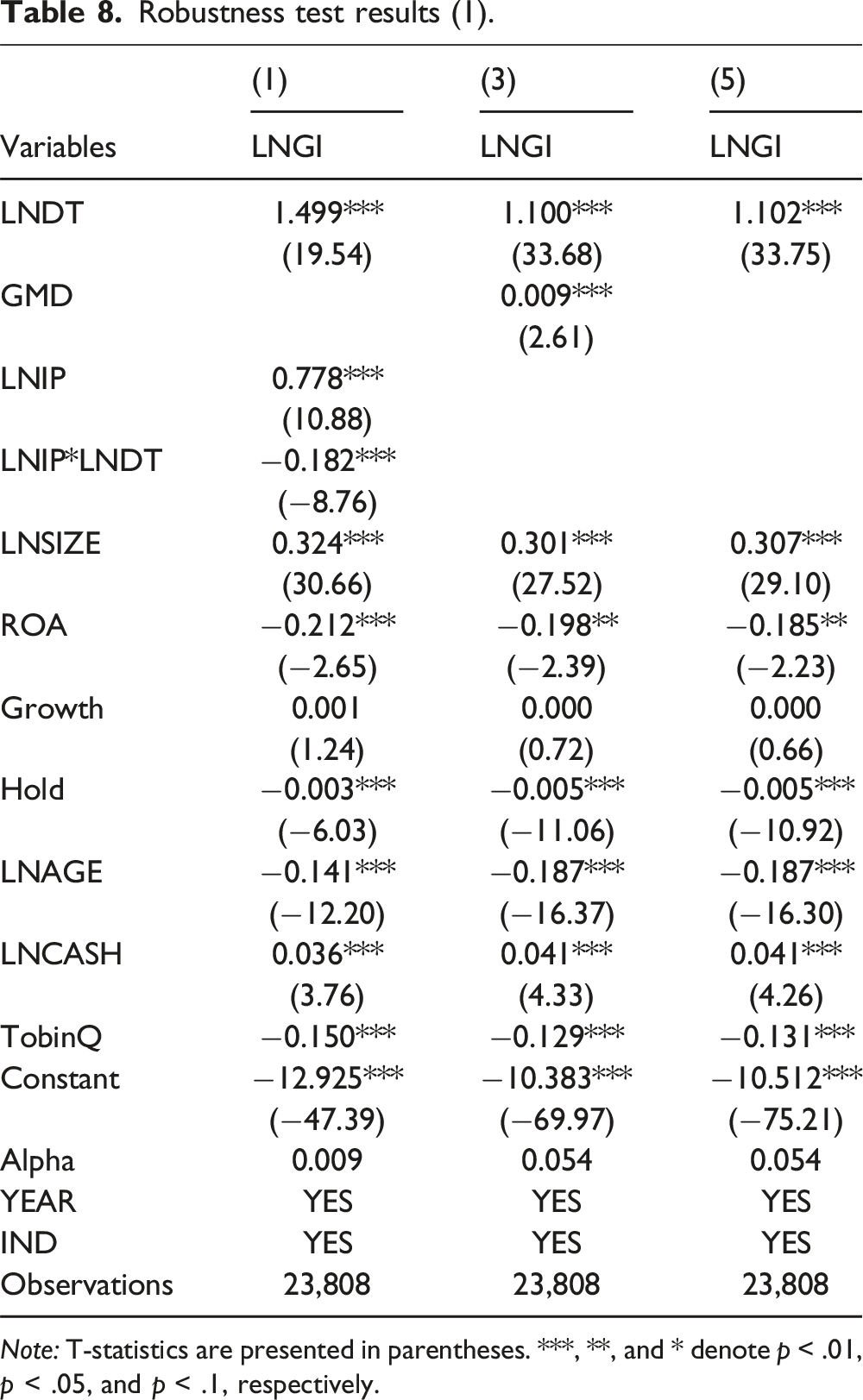

Robustness test

Negative binomial model regression model

Robustness test results (1).

Note: T-statistics are presented in parentheses. ***, **, and * denote p < .01, p < .05, and p < .1, respectively.

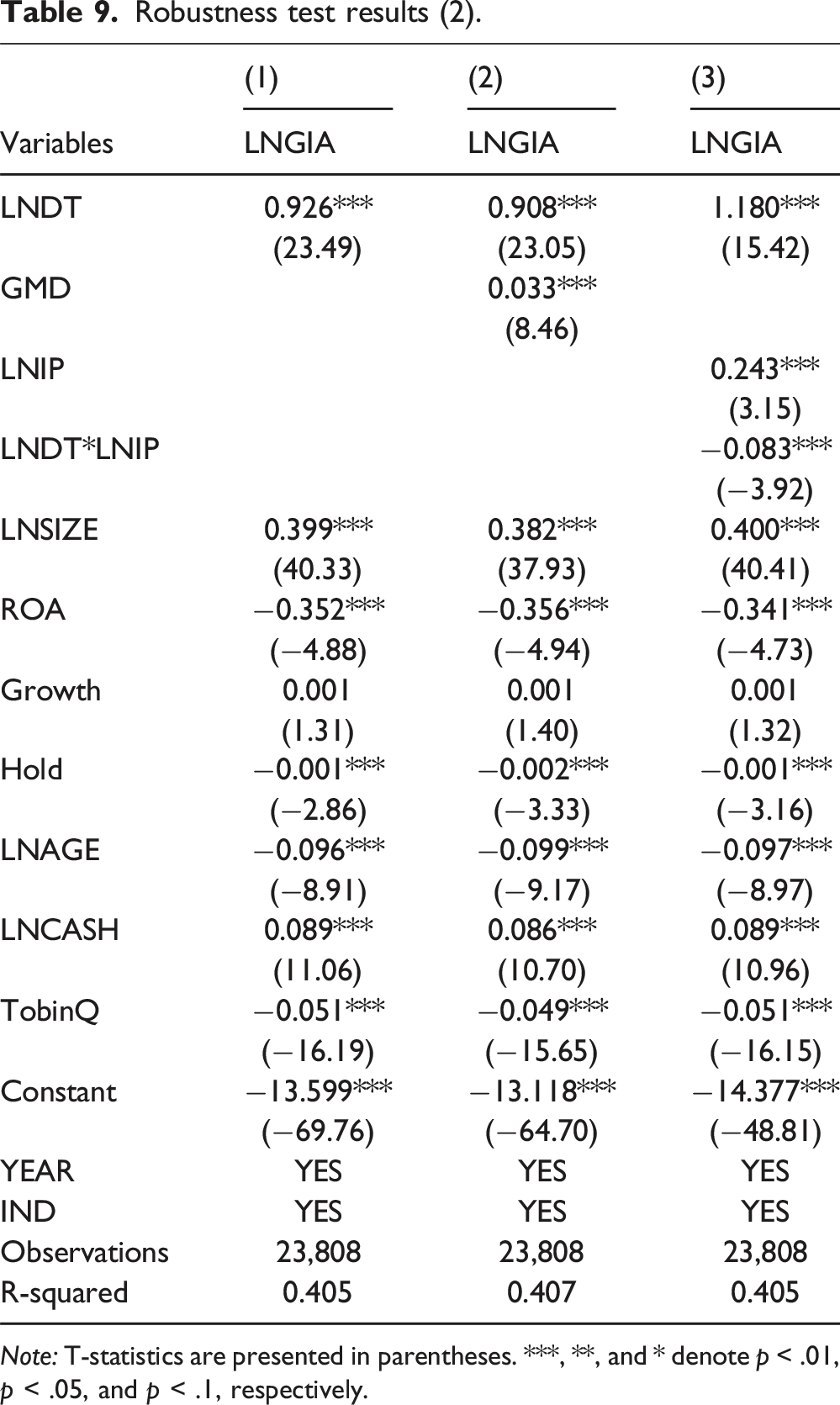

Test results after remeasuring green innovation level

Robustness test results (2).

Note: T-statistics are presented in parentheses. ***, **, and * denote p < .01, p < .05, and p < .1, respectively.

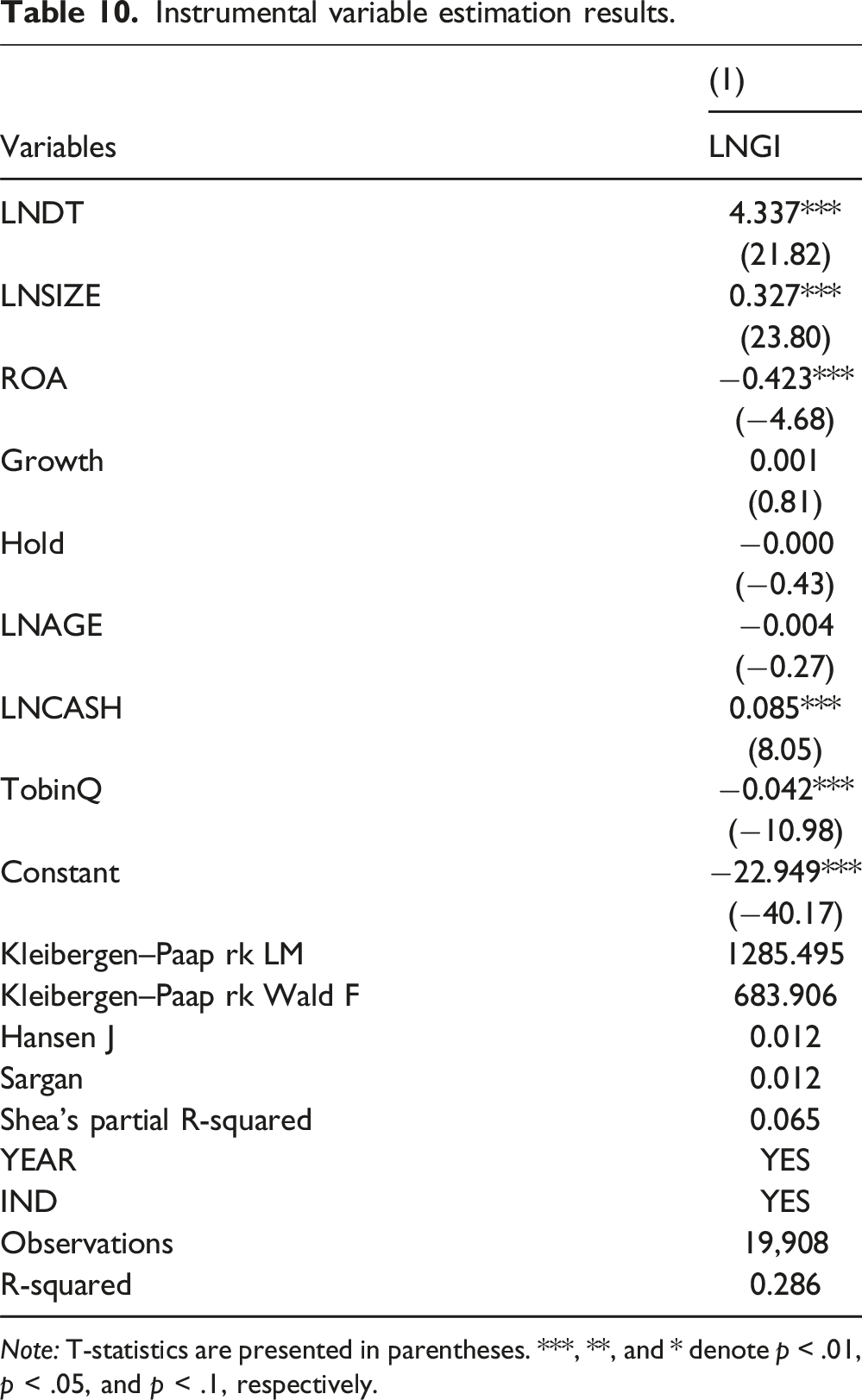

Endogenous problem

Missing variables or reverse causality may have caused endogenous problems. Thus, instrumental variables (IV) were adopted to further examine the relationship between digital transformation and green innovation. Drawing on the research conducted by Ning et al. (2023) and Qiu et al (2020), this study used the lag value of digital transformation in a period as an IV. Following Feng et al.’s (2022) study, internet users in cities and companies were also set as an IV. A one-term lagged value of digital transformation will correlate with digital transformation itself because the development of digital transformation is based on the previous basic. Accumulating experience, skill, and high-quality employees will promote the following development. Meanwhile, Jardak and Ben Hamad (2022) also discuss the autocorrelation characteristics of digital transformation. The one-term lag value of digital transformation is also unrelated to green innovation. The characteristics of digital transformation include real-time knowledge sharing and collaborative networks, and both can achieve timely innovation (Salehi and Sadeq Alanbari, 2023). Additionally, digital transformation can enable corporations to build prompt feedback loops, thereby better-adjusting innovation direction to respond rapidly to environmental metrics. Meanwhile, digital transformation includes adopting technologies such as digital twins, which can significantly promote the efficiency of green innovation (Fukawa and Rindfleisch, 2023). Thus, the lag impact on digital transformation for green innovation will be limited.

Internet users in the city are considered to represent the level of local internet infrastructure. According to Wu et al. (2023), based on a resource-based view, the local internet infrastructure level positively correlates with corporations’ green innovation. However, the city infrastructure is not related to the green innovation of the corporation; most antecedent factors of green innovation are internal (Khan et al., 2021a). External driving factors usually comprise environmental policy and external knowledge resources (Dangelico, 2016); thus, city internet users fulfill the instrument variable requirements.

Instrumental variable estimation results.

Note: T-statistics are presented in parentheses. ***, **, and * denote p < .01, p < .05, and p < .1, respectively.

In conclusion, the IVs are reliable and can be used to eliminate the endogenous problem. After introducing the IVs, the coefficient of LNDT is 4.337, significant at 1%. Therefore, the relationship between green innovation and digital transformation is reliable.

Discussion

The empirical result of equation (1) proves the positive relationship between digital transformation and green innovation. Digital transformation builds an innovation-friendly environment by integrating digital technology into firm operations and management. Specifically, digital transformation enables firms to implement flexible strategy shifting, strengthen their knowledge- and information-gathering ability, and bolster digital leadership, thereby promoting low-cost and high-efficiency green innovation (Feng et al., 2022; Tian et al., 2023; Warner and Wäger, 2019). This result is consistent with those obtained by Gao et al. (2023) and Xue et al. (2022) and contributes to the current literature on the universality of the relationship between green innovation and digital transformation.

H2 considers the mediator role of green management disclosure. Similar to Zhang and Zhao’s (2023) results, digital transformation was found to provide technological support for green management disclosure in this study. Signal and stakeholder theories also provide a strong theoretical foundation for the results. On the one hand, green management disclosure can serve as a good signal to the market and attract green innovation investments (Xiang et al., 2020). On the other hand, it can facilitate stakeholders’ monitoring of firms’ green management, thereby forcing firms to improve their green innovation (Hu et al., 2021; Lanoie et al., 1998) According to Hong et al. (2020), CSR disclosure can promote green innovation, which is consistent with our results. However, Li et al.’s (2018) result shows that green innovation promotes environmental disclosure due to external institutional pressure. Therefore, under external pressure, the mechanism between green innovation and environment-related disclosure requires further research.

The empirical result of equation (3) states that institutional pressure has a negative moderating effect on digital transformation and green innovation. This result differs from previous results. He and Su (2022) found that institutional pressure from government regulations can positively moderate the firm-level relationship between digital transformation and green innovation. The difference in these empirical results is attributable to two reasons. First, because of institutional pressure, firms will thoughtlessly simulate peers’ green innovation strategies, thereby leading to failure. Huang et al. (2022) found that firms will adopt similar green practices and management systems to promote their ESG. Moreover, Sousa and Voss (2008) stated that imitation often leads to suboptimal results due to contextual differences. Second, institutional pressure will force firms to reallocate their resources or change strategy directions (Ang et al., 2015). The impact pathway overlaps with digital transformation, and the slight difference is the passive or active form. As a result, institutional pressure negatively moderates the relationship between digital transform and green innovation.

Theoretical contributions and limitations

This study makes two main theoretical contributions. First, multiple theories were applied to analyze the relationship between digital transformation and green innovation. They include the dynamic capability, absorptive capacity, social exchange, and upper echelons theories. Digital transformation can cultivate absorptive and dynamic capabilities, improving knowledge acquisition and resource allocation and thereby promoting green innovation (Michaelis et al., 2021; Ning et al., 2023). Additionally, this study applied the social exchange theory to further explain knowledge sharing and acquisition mechanisms underlying digital transformation. The introduction of the upper echelons theory explained how digital leadership, as a component of digital transformation, influences green innovation progress through digital thinking, decision-making, and talent cultivation. These four theories elucidate the relationship between digital transformation and green innovation comprehensively compared with previous research and provide a solid theoretical foundation for further investigations. This paper also responds to Sousa Jabbour et al.’s (2018) call for future research to empirically examine how digital technologies influence a firm’s ability to implement sustainable development. Takalo et al. (2021) called for future research on multiple industries’ green innovation rather than focusing on high-polluting industries. In response, this study analyzed samples from all industries, except the financial industry.

Second, the impact mechanism between digital transformation and green innovation was enriched by the new mediator and moderator introduced in this study. The mediator role of green management disclosure was confirmed, revealing how information integration and exchange ability in digital transformation serves as an additional mechanism affecting green innovation.

Multiple mediators have been found previously, including government subsidies and financial constraints (Gao et al., 2023; Xue et al., 2022). Management efficiency was also found to enrich the transformation mechanisms between digital transformation and green innovation (Lin and Xie., 2024b). However, this study is the first to introduce green management disclosure—an environmental-related management disclosure—as a mediator. This mediator variable allows us to obtain a deeper understanding of the mediating effect of environmental disclosures. Subsequently, through the signal and stakeholder theories, the effect of green management disclosure on green innovation is mainly reflected in the increased visibility to capital market and stakeholders, forcing firms to push green innovation.

This study investigated industry-level institutional pressure and identified its negative moderating role. Previous research has mentioned multiple moderating factors, including corporate social responsibility and international opportunities (He and Su., 2022). However, institutional pressure has been mentioned sparingly. According to Tolmie et al. (2020), informal institutional pressure also exists, which is caused by social values, trust, and norms. Thus, in this paper, institutional pressure is measured by the number of firms adopting ISO14001 in each industry, which reflects industry-level informal institutional pressure. This finding shows that informal institutional pressure within the industry can also significantly influence a corporation’s green innovation. The negative moderating effect of institutional pressure is inconsistent with previous research (Hu et al., 2022; Qi et al., 2021). This difference may be caused by the impact mechanism of industry-level institutional pressure overlapping with digital transformation. Both can relocate firm resources and push firms to renew their green strategies. Thoughtless mimetic behavior caused by institutional pressure also disrupts green innovation progress. This finding reveals another impact of institutional pressure on green innovation.

Our research has certain limitations. First, the sample included only Chinese listed companies. Thus, further investigation is required to determine the universality of the results. For example, future studies can include SMEs and listed companies in other counties. Second, the transmission mechanism between digital transformation and green innovation should be further investigated. In this study, only the mediator role of green management disclosure and the moderating effect of institutional pressure were investigated. The effect of other possible factors such as firm culture or board characteristics is not apparent. Additionally, this research did not apply other transmission mechanisms, such as a mediated moderation model. Therefore, future research can explore more related factors that impact the relationship between digital transformation and green innovation via different mechanisms. Finally, the paper only discussed the impact of digital transformation on green innovation. Different dependent variables, such as the efficiency or quality of green innovation, are not considered (Lin and Xie, 2024b).

Managerial implication

Our research can provide the following practical suggestions to firms. First, firms should integrate digital technology into firm operations and adopt new organizational structures to accelerate their digital transformation (Hess et al., 2016). By doing so, firms can improve their information acquisition, system updating, and customer interaction (Xue et al., 2022). These benefits can also promote their green practices, including green innovation and green management disclosure. As a result, they can achieve sustainable development goals and gain societal legitimacy.

Second, green management disclosure’s mediator role has been revealed. Firms should build a comprehensive information disclosure system by utilizing digital transformation. A real-time information exchange platform is necessary, which can be realized through 5G and cloud computing (Ellström et al., 2021). An internal information exchange network is also necessary for quality information disclosure. 5G and blockchain can help firms build a transparent internal communications system (Nadkarni and Prügl, 2021) to avoid information asymmetry caused by agency problems, thereby improving information quality (Wu et al., 2022).

Third, the negative moderating effect of institutional pressure can be reduced in two ways. Top managers should focus on peer information collection to establish the overall plan for achieving green innovation and avoiding thoughtless imitation of peer behaviors. Comprehensively evaluating a firm’s internal environment can help build a suitable environment for green innovation (Sousa and Voss, 2008). Additionally, firms should accelerate the progress of their green practices to obtain legitimacy at the industry level (DiMaggio and Powell, 1983).

Conclusion

This study comprehensively investigates the relationship between digital transformation and green innovation in Chinese listed companies and confirms the mediator role of green management disclosure and institutional pressure at the industry level. The sample contains more than 3000 listed companies and 75 industries in China’s A-share stock market. The fixed effects model was applied to control for time and industry effects. These empirical results show that digital transformation has a significant positive influence on green innovation and reveal a new transmission mechanism: green management disclosure. Furthermore, this paper also reveals that industry-level institutional pressure negatively moderates the relationship between green innovation and digital transformation. Measurements of the independent variable were changed, and an econometric model was applied to test the robustness of the results, indicating that the results are consistent with previous studies. These findings provide the following suggestions for managers. First, managers should accelerate firm digitalization to make progress on green practices, including green innovation and environment information disclosure. Second, managers must maintain strategic focus, avoiding thoughtless imitation induced by institutional pressure. Meanwhile, digital transformation can be utilized to build better internal environments for green practices to obtain legitimacy.

Footnotes

Author contributions

Feng Jiang.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.