Abstract

This study seeks to offer a comprehensive and practical comprehension of the lessons that companies can derive from financial institutions to promote the adoption of blockchain technology for future growth. Utilising R3 Corda, the largest blockchain platform featuring prominent financial institutions, as a case study, this research collects a wealth of company-recorded videos, podcasts, webinars, and textual data that offer invaluable insights for this case analysis. This investigation strives to contribute to formulating a blockchain adoption framework, drawing inspiration from successful use cases in the financial sector. This research outlines the current institutional pressures, criteria for platform selection, a blockchain adoption checklist, and novel institutional arrangements, providing a structured approach for enterprises considering embracing blockchain solutions. This framework serves as a strategic guide, facilitating organisations in navigating the complexities of blockchain implementation and ensuring a seamless integration process that aligns with their unique goals and operational requirements. Hence, discerning how to judiciously select and participate in the right blockchain consortia/platform is paramount for fostering and managing new technological innovations as businesses undergo digital transformation.

Introduction

Amid the fourth industrial revolution, marked by the advent of transformative technologies like blockchain, Artificial Intelligence, the Internet of Things, and cloud computing (Al-Sulami et al., 2024; Lumineau et al., 2023; Schwab, 2016), the world is witnessing unprecedented changes. From social, mobile, analytics, biometrics, virtual reality, augmented reality, and digital twins, innovative technologies keep coming and significantly transforming the way we work and live, disrupting existing business models and processes and changing the digital landscape (Dhakshan et al., 2024; Gomber et al., 2018; Komulainen and Nätti, 2023). Blockchain has emerged as a buzzword since it gained mainstream attention in 2017 (Magnier and Barban, 2018), offering a novel approach to recording and sharing digital information. It is expected to be as revolutionary as the Internet (Tapscott and Tapscott, 2017), becoming the foundational technology (Iansiti and Lakhani, 2017) to reshape our society. It is estimated that blockchain could boost global GDP by $1.76 trillion by 2030 (PWC, 2020).

In recent years, the issue of blockchain adoption has attracted considerable interest among academics, policymakers, and practitioners (Toufaily et al., 2021) as an institutional innovation (Chloé and René, 2023). This technology has the great potential to enhance traceability and efficiency, enable better data access control, and preserve user privacy and identity authentication (Faisal et al., 2024). Scholarly literature on blockchain technology is evolving, emphasising the salient and strategic relevance of blockchain benefits in reducing costs, enhancing security, increasing transparency, and improving trust (Biais et al., 2019; Chen et al., 2023; Goldstein et al., 2019; Han et al., 2023; Iansiti and Lakhani, 2017; Yermack, 2017; Zachariadis et al., 2019).

Despite the promise, the practical realisation of blockchain’s transformative potential remains to be determined. It remains vague at present on how these transformational promises can be attained in reality (Al-Sulami et al., 2024), hampered by technical, organisational, and legal challenges, impeding widespread adoption (Bertino et al., 2019; Hughes et al., 2019; Karuppiah et al., 2023; Luthra et al., 2023; Sargent and Breese, 2023; Su et al., 2023; Vu et al., 2023; Yu et al., 2018). Therefore, there is a high interest in blockchain technology but slow adoption (Dehghani et al., 2022; Hassan et al., 2023; Komulainen and Nätti, 2023) in other industries besides the financial sector. For example, Toufaily et al. (2021) signal that it remains relatively unclear how the transformative potential of this technology can be realised in practice. Their study explains the status of blockchain technology adoption in the MENA (the Middle East and North Africa) region, ranging from non-adoption to planning and exploration of options and early-stage adoption. Early-stage adoption is evidenced in finance sectors in cheque registration, trade finance, and cross-border transactions.

Against this backdrop, this study aims to offer insights into what companies in various industries can learn from the successful experiences of blockchain adoption in financial institutions. The goal is to facilitate the expansion of blockchain adoption across sectors, enabling organisations to harness the newfound capabilities of blockchain technology for future growth.

Three observations motivated this study. Firstly, most academic studies on blockchain technology are conceptual (Angelis and Ribeiro da Silva, 2019; Janssen et al., 2020; Lo et al., 2019). Empirical investigations on blockchain adoption are still slight (Shahzad et al., 2024). Despite many potential promises, the adoption rate is still relatively slow, marked by notable hesitation in widespread implementation (Chloé and René, 2023; Komulainen and Nätti, 2023; Lu et al., 2024; Luthra et al., 2023). Secondly, organisations are more committed than ever to implementing blockchain in their business (Deloitte, 2020). It is suggested that case studies are urgently needed to uncover embedded insights for blockchain adoption, and more research is required to develop a theoretical understanding of how companies can leverage new blockchain capabilities to transform their businesses to succeed and strive for the future (Brennan et al., 2019; Moll and Yigitbasioglu, 2019). Thirdly, financial institutions are at the forefront of adopting and implementing blockchain technology across various domains, including banking, asset liquidity, payments, and trade finance (Han et al., 2023; World Economic Forum, 2020). Predictions indicate that digital banks on cloud-based platforms, accelerated by blockchain technology, will play a pivotal role in the future of financial services (Santander, 2020). Guided by these observations, this study addresses the research question: What insights can companies learn from the successful experience of blockchain adoption in financial institutions to foster widespread adoption in other sectors?

This research contributes in two primary ways and is potentially valuable for scholars, practitioners, and policymakers. Firstly, this study develops a blockchain adoption framework that constitutes institutional pressure, platform selection criteria, blockchain adoption checklist, and new institutional arrangement. This framework addresses intricate real-world business challenges, fostering cost reduction, enhanced trust, and improved operational efficiency. The research contends that valuable insights can be gleaned from the successful early adoption of blockchain in financial institutions. It serves as a blueprint for other sectors to expand their applications, gain societal legitimacy, and establish new standards. Secondly, employing a case study approach focussing on R3 Corda, the research augments existing blockchain adoption literature by showcasing successful use cases within financial institutions. This extends the discourse on blockchain adoption, offering insights applicable to a broader array of institutional contexts. The study emphasises the imperative for society to prioritise upskilling and reskilling efforts, advocating a purposeful and proactive response to emerging technological tools. In essence, this research not only contributes to the theoretical foundation of blockchain integration but also serves as a practical roadmap for organisations seeking to harness the transformative potential of blockchain technology in an increasingly digitised and interconnected world.

As such, this study intends to address the gap identified in existing research: the adoption of blockchain in organisations is still in its infancy, and studies in this area are limited (Lu et al., 2024). Despite growing interest from academics, politicians, and practitioners in blockchain technology adoption, there remains a significant ambiguity about how its transformational promises can be realised in practice. Specifically, there is a lack of studies on the factors that affect blockchain adoption (Al-Sulami et al., 2024). To bridge this gap, the research objectives of this study are as follows: • To identify and analyse the key lessons companies can learn from financial institutions regarding adopting blockchain technology. • To formulate a comprehensive framework for blockchain adoption, inspired by successful use cases in the financial sector. • To develop a detailed checklist that enterprises can use to ensure they have considered all necessary factors for successful blockchain adoption. • To improve understanding how businesses can thoughtfully select and participate in the right blockchain consortia/platform to foster and manage new technological innovations to support their digital transformation journeys.

These objectives aim to provide a structured and comprehensive approach to investigating the adoption of blockchain technology, drawing on practical lessons from the financial sector and offering actionable insights for businesses.

This study arranges the paper into six sections. Section one explicitly elucidates this study’s background, purpose, motivation, and contributions. This is followed by reviewing the relevant emergent blockchain technology literature to reveal this technology’s disruptive and transformative nature. Section two first outlines blockchain concepts, then explicates blockchain technology’s emergence and recent development. Following that, this sector also illuminates its applications in the financial industry. Section three delineates the relevance of the research case and expounds upon the methodology employed in this study. Section four presents the findings, followed by section five, which discusses the theoretical understanding and practical implications of this study and further concludes with the limitations of this study for further research in the last section.

Literature review

Blockchain concepts

The definition of blockchain technology remains elusive due to its evolving nature, with various scholarly perspectives offering nuanced interpretations of its characteristics and potential benefits. Yermack (2017) conceptualises blockchain as a sequential database or a giant spreadsheet, presenting an alternative to traditional financial ledgers. Su et al. (2023) define it as a distributed data structure facilitating data sharing through a peer-to-peer network. Ølnes et al. (2017) see it as a foundational technology for exchanging information and transacting digital assets in distributed networks. Moll and Yigitbasioglu (2019) emphasise blockchain’s role in creating an immutable distributed ledger to enhance data quality. Gomber et al. (2018) position blockchain as a FinTech innovation involving new technical competencies and business models, falling into Pisano’s ‘architectural innovations’ that combine radical innovation (new technical competencies required) and disruptive innovation (new business models needed) (Pisano, 2015). Hinings et al. (2018) highlight blockchain’s contribution to digital transformation, introducing novel actors, structures, practices, and values that impact existing organisational rules. Jayasuriya and Sims (2023) foresee significant transformations in accounting and management practices across industries.

In essence, blockchain emerges as an innovative technology with the potential to disrupt established business models and processes, prompting transformations in organisational structures, practices, and values. This disruption opens doors to new opportunities for commercialising products and services. The technology facilitates innovative methods of recording, sharing, validating, and managing information, offering benefits such as cost reduction, process automation, operational simplification, and automated compliance. Blockchain stands as a catalyst for reshaping industries and unlocking unprecedented opportunities for progress and efficiency.

The following section briefly outlines the development of this technology.

Emergence and recent development of blockchain technology

Blockchain technology, initially introduced by Nakamoto (2008) to validate Bitcoin ownership without intermediaries (Yermack, 2017), has evolved into a versatile tool with the potential to transfer various forms of value, such as finance, votes, intellectual property, health data, music, and ideas (Tapscott and Tapscott, 2017). Its progression from blockchain 1.0, focused on cryptocurrency transactions, to blockchain 2.0 with smart contracts, and further to blockchain 3.0, expanding into non-financial applications, signifies a transformative journey. Progressively, the technology is advancing towards blockchain 4.0, which integrates blockchain and artificial intelligence (Han et al., 2023).

Blockchain’s adaptability is evident in its design options, catering to diverse business purposes. It can manifest as a public blockchain with open access, a private blockchain restricting entry to authorised users, or a consortium where multiple firms collaborate to address specific challenges (Buterin, 2015; Han et al., 2023). The technology’s uniqueness lies in its distinct artefacts, including the distributed ledger, consensus mechanism, encryption mechanism, smart contract, and immutable audit trail (Du et al., 2019). These elements collectively generate and maintain decentralised consensus, fundamentally enhancing transparency and trust and reshaping the dynamics of the global economy (Shahzad et al., 2024).

In recent years, industries spanning finance, manufacturing, supply chain, healthcare, education, insurance, and government have increasingly explored blockchain’s potential (Al-Sulami et al., 2024). The academic literature is burgeoning with scholars exploring diverse applications, such as custody for renewable energy credits and carbon credits (Ashley and Johnson, 2018), e-health systems (Casado-Vara and Corchado, 2019), RoboJudge (Castell, 2018), sustainable and traceable supply chain (Chang et al., 2019; Friedman and Ormiston, 2022; Karuppiah et al., 2023; Kordestani et al., 2023; Rehman Khan et al., 2022), corporate governance (Yermack, 2017), global value chains (Chen et al., 2022; Faisal et al., 2024; Hassan et al., 2023), collaborative and sustainable innovation in manufacturing (Benzidia et al., 2021; Wan et al., 2022), pension operation reforms (Sarker and Datta, 2022), the sharing economy (Pazaitis et al., 2017), incentivised blockchain-based online social media (Delkhosh et al., 2023), volatile crypto market using token incentives (Chen et al., 2023), and digital advertising (Kim et al., 2023).

However, financial institutions stand at the forefront of blockchain exploration and adoption, leveraging the technology to streamline operations and enhance efficiency and trust. The following section provides an in-depth exploration of blockchain applications within the financial sector.

Blockchain application in the financial sector

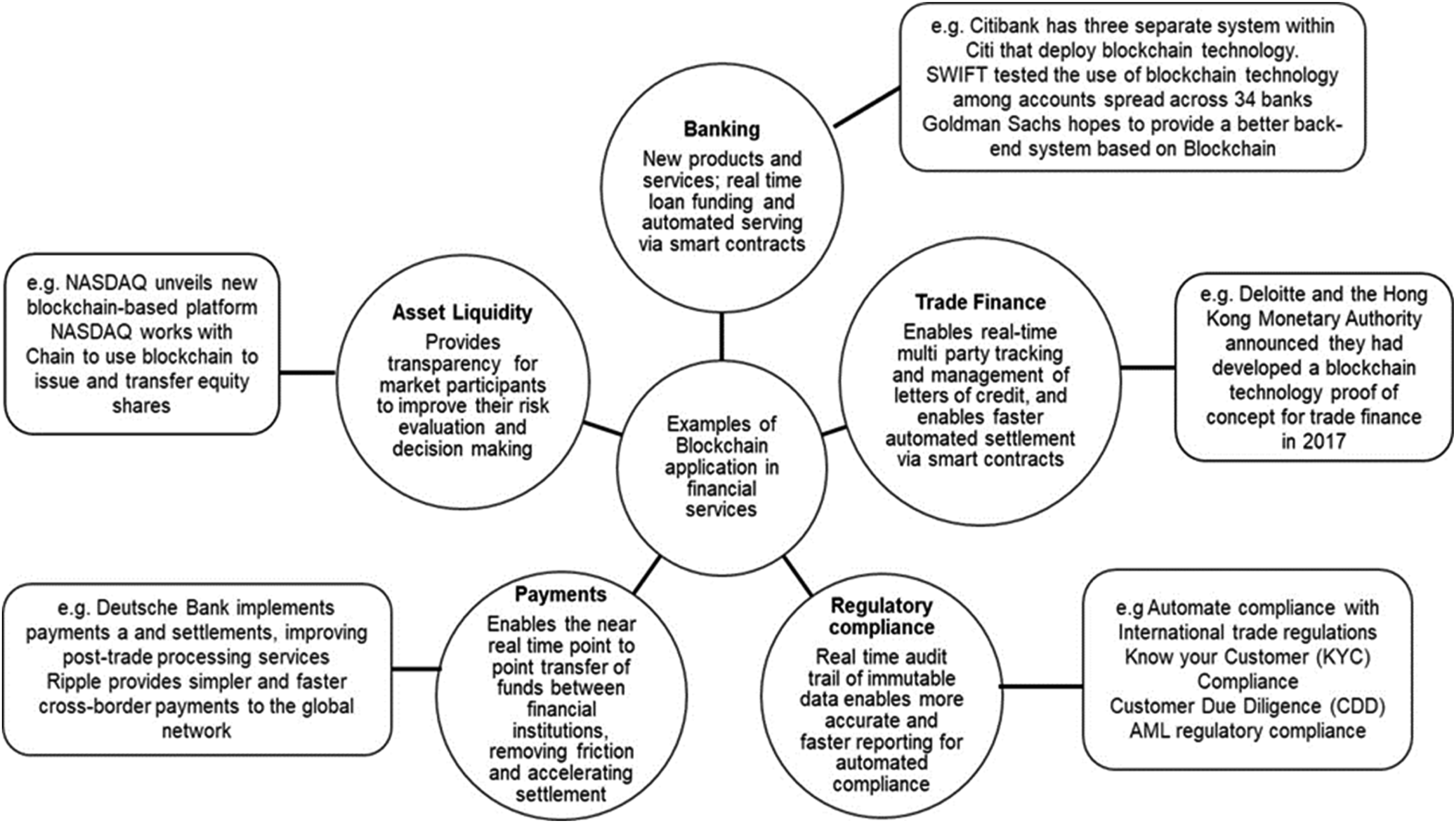

As early adopters of blockchain technology, financial institutions have spent substantial time and investment exploring the technical and functional aspects of the technology in the emerging field of Fintech in the financial service industry. This pioneering effort aims to harness the immense potential inherent in blockchain, propelling the financial service industry towards a future marked by efficiency, transparency, security, and trust (Gan and Lau, 2024). The journey of blockchain adoption in the financial sector has traversed various facets, encompassing banking, trade finance, regulatory compliance, payment systems, and asset liquidity, as illustrated in Figure 1 (see below for some examples). Examples of blockchain applications in financial services (sources: McWaters et al., 2016; Vysay & Kumar, 2019; World Economic Forum, 2020).

The financial industry has reached a significant milestone where the maturity of blockchain technology aligns with a refined understanding of its optimal utilisation (Jessel, 2020). Projections from Bernstein estimate that the next 5 years could witness the tokenisation of assets worth $5 trillion on the blockchain, revolutionising their issuance, management, transactions, and redemption processes (Ledesma and Godbole, 2023). The benefits are manifold, ranging from expedited payments and cost reductions for banks to heightened security and increased transaction volumes with added efficiency (Lu et al., 2024). Enhanced efficiency, transparency, security, and trust across networks have spurred financial institutions to embark on blockchain projects (Gan and Lau, 2024). The technology enhances confidence among stakeholders by providing reliable and transparent accounting data, contributing to the establishment of immutable ledgers and fortification against fraud (Basly and Saunier, 2024; Judijanto et al., 2024), and the enhancement the robustness of financial forensics to support the fight against economic crimes such as money laundering (Gan and Lau, 2024).

Moreover, blockchain technology allows financial institutions to revamp their services, deliver innovative products, and meet evolving consumer demands. It transforms the financial services industry into a data-centric workstream, fostering the creation of multiple cost-effective financial products and services and saving time and resources while mitigating risks and administrative burdens (Shumsky, 2019).

Beyond financial transactions, blockchain facilitates alternative methods of recording and sharing contracts, obligations, and agreements between institutions and individuals (Brown, 2018; Han et al., 2023), streamlining processes and strengthening trust.

Recognising the transformative potential inherent in the successful field experience of financial institutions, this study aspires to develop a comprehensive blockchain adoption framework. This framework aims to guide non-financial industries, enabling them to unlock the value of blockchain technology as they undergo digital transformation.

This research contends that financial institutions, having paved the way as early adopters of blockchain, play a pivotal role in delivering value. Consequently, non-financial institutions can glean invaluable insights from the successful experiences of their financial counterparts. By assimilating and diffusing blockchain technology, non-financial industries can establish new industry standards, leading to social acceptance and legitimacy for innovative blockchain-enabled products and services, thus contributing to the growth of the digital economy.

The following section elucidates the research case’s relevance and outlines the method adopted in this study.

Methodology

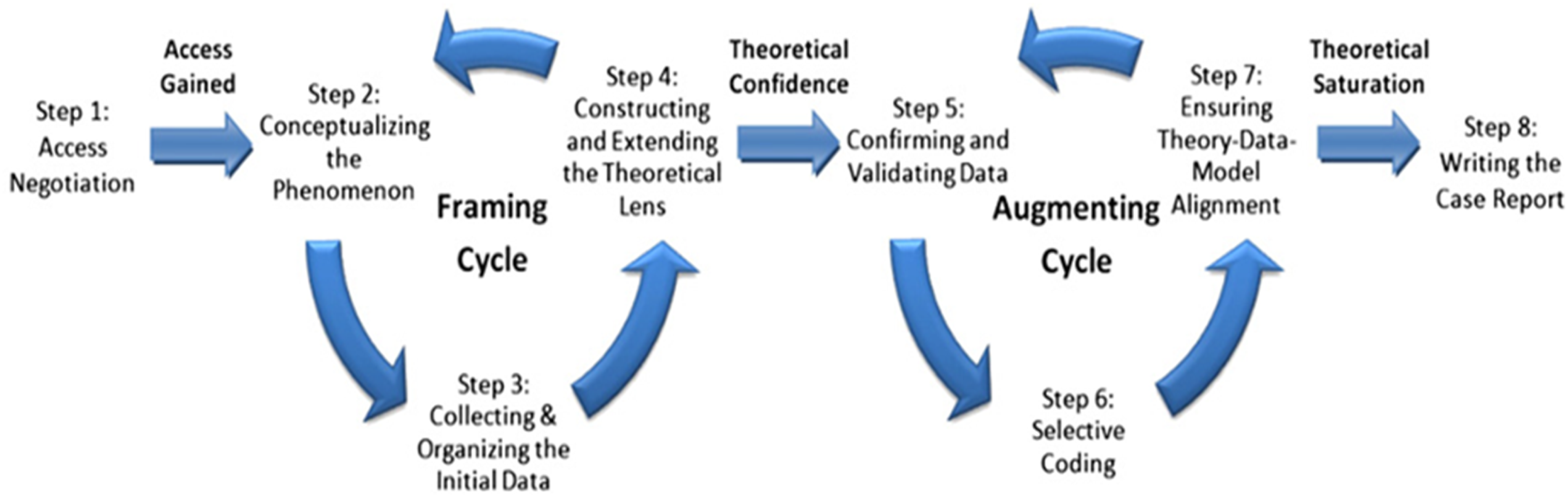

Following Pan and Tan’s (2011) structured-pragmatic-situational (SPS) approach for case studies (see Figure 2 below), this research undertakes a thorough examination of R3 Corda to enhance the methodological rigour of the investigation. Employing a case study methodology aligns with Eisenhardt’s (1989) assertion that it generates more profound insights and allows multiple levels of analysis (Yin, 2003) to help understand and promote blockchain adoption. A structured-pragmatic-situational approach adopted by this study (source: Pan and Tan, 2011:164).

The selection of R3 Corda as the primary case study stems from its position leading the world’s largest blockchain ecosystem. Specifically crafted to meet the stringent requirements of major financial institutions like Royal Bank of Scotland, Barclays, Banks of America, HSBC, Commonwealth Bank of Australia, Morgan Stanley, Goldman Sachs, and UBS, R3 Corda stands out as a unique blockchain platform collaboratively designed and developed with active involvement from leading financial institutions and regulatory bodies. R3, alongside partners such as Microsoft, Intel, Accenture, HPE, Guardtime, Finastra, and Tradewinds, has successfully implemented blockchain applications in diverse sectors, including trade finance, insurance, banking, stock exchange, and bond markets. Its prestigious awards in 2023 as the best blockchain technology and most innovative use of blockchain in banking (R3, 2023) highlight its global leadership and recognition in the blockchain domain.

With R3 Corda as the focal point, the research team secured permission to leverage publicly available data from the company’s website as valuable investigative sources. Online resources such as recorded videos, podcasts, webinars, and blogs emerged as pivotal channels for data collection due to their accessibility, stability, and richness of information (Lincoln and Guba, 1985). This data collection approach aligns with contemporary studies by LeBaron et al. (2018), Skjælaaen et al. (2020), and Zundel et al. (2018), affirming the increasing viability of online sources to supplement or replace traditional methods like interviews and surveys.

Following Pan and Tan’s (2011) pragmatic case study procedures, the research systematically gathered substantial textual data from 34 senior executives at R3 and its affiliated financial institutions actively engaged in blockchain project design, development, and deployment. These participants, denoted as P1 through P34, were selected based on their extensive experience and profound understanding of blockchain adoption within financial institutions. Their insights, grounded in real-life experiences, serve as a crucial measure of their competence to offer rich perspectives on fostering blockchain adoption.

Various data types, including videos, podcasts, and webinar content, were transcribed into a textual format to analyse the diverse information collected. Nvivo 12, a qualitative data analysis software, was employed using a thematic analysis approach. Thematic analysis is a systematic process involving identifying, analysing, and reporting patterns within the data, facilitating the extraction of meaningful insights.

The entire data collection and analysis process was iterative until theoretical saturation was achieved (Eisenhardt, 1989; Glaser and Strauss, 1967). The initial open coding prioritised the data’s narrative, allowing for the emergence of initial categories. These codes were subsequently refined into themes, and the study further refined these themes to aggregate dimensions, forming a thematic framework. This framework provided a structured and comprehensive overview of emergent patterns and insights, enabling a deep understanding of blockchain adoption in financial institutions.

The thematic framework underwent validation through discussions within the research team to enhance credibility, and the coding and analysis underwent peer debriefing. Triangulation was employed by utilising multiple data sources, including videos, podcasts, and webinars, to corroborate findings from different perspectives and sources, thereby bolstering the study’s trustworthiness.

Findings

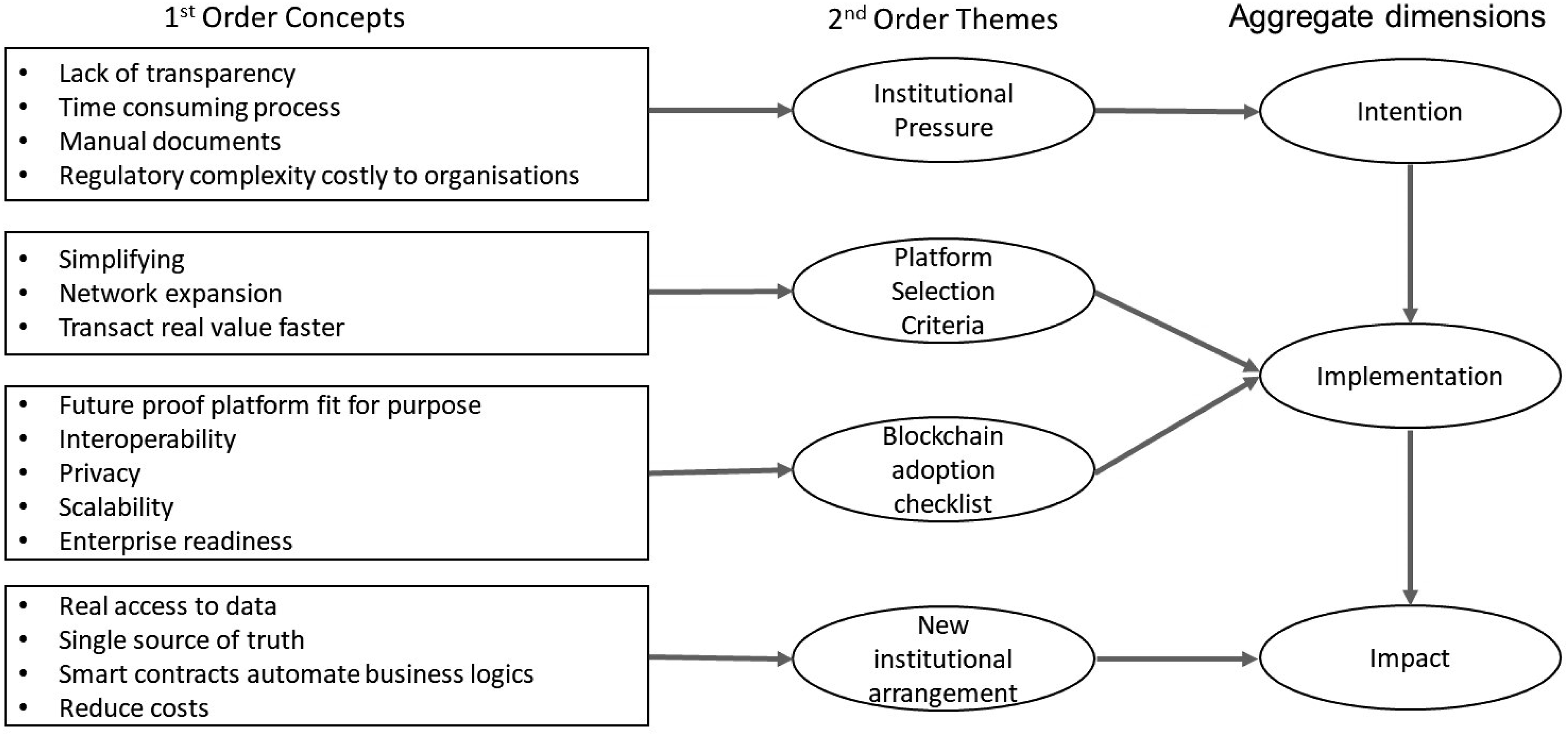

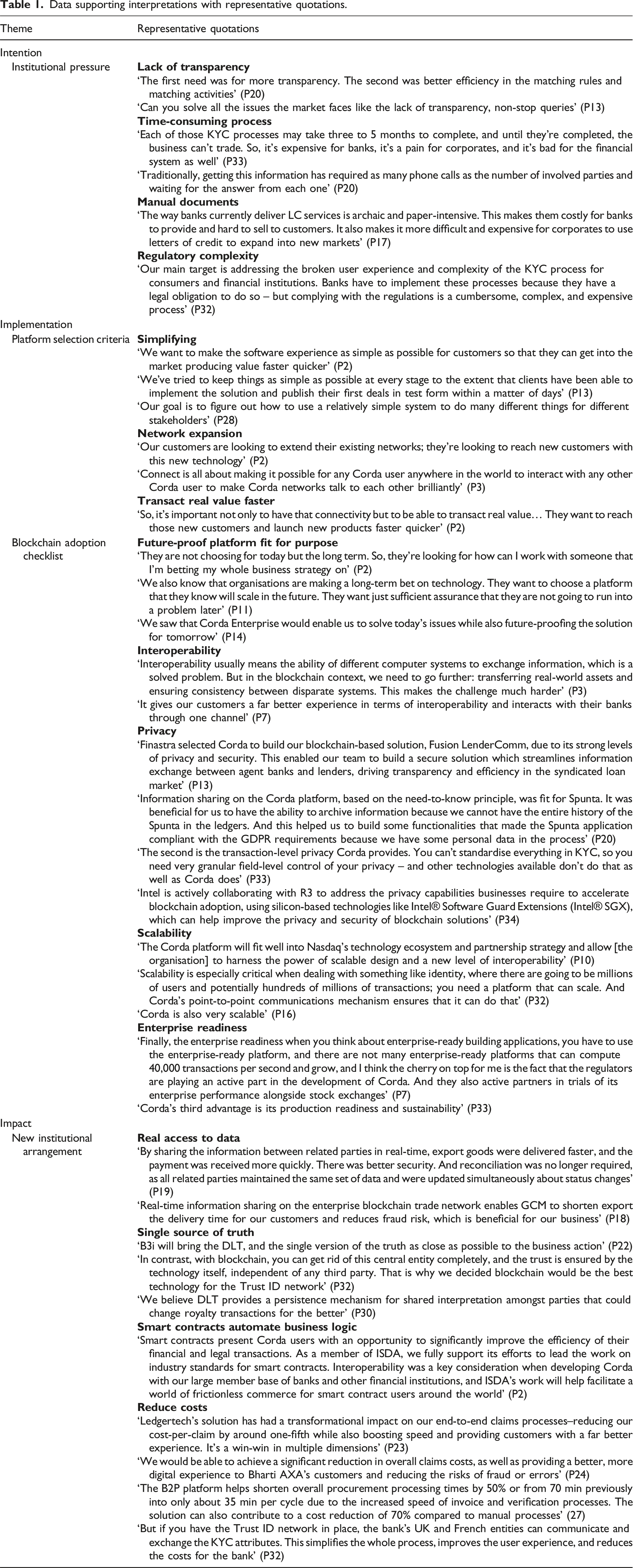

Drawing inspiration from Gioia et al.’s (2013) work, this study purposefully unveils the insights through a meticulously developed framework. This framework unfolds in a structured manner, employing a hierarchical data structure encompassing 1st order concepts, 2nd order themes, and aggregate dimensions explicating blockchain adoption (see Figure 3 below). To bolster the credibility and depth of the interpretations derived from this framework, the study presents supporting data in Table 1 below. The table functions as a repository of evidence, systematically aligning empirical data with the conceptual layers of the framework to establish a robust foundation for the key insights and foster transparency and credibility of its findings. Blockchain adoption framework. Data supporting interpretations with representative quotations.

The blockchain adoption framework presented in this study comprises three essential dimensions: intention, implementation, and impact, offering a comprehensive understanding of blockchain adoption that extends beyond the financial sector. Non-financial institutions can draw valuable insights from the successful experiences of financial counterparts in harnessing blockchain technology to deliver tangible value.

In the realm of intention, businesses looking to foster blockchain adoption must first determine their institutional pressures and current challenges. The empirical evidence from this study highlights prevalent issues faced by financial institutions, including lack of transparency, time-consuming processes due to numerous intermediaries, manual documentation, human errors, and regulatory complexities. By extrapolation, non-financial institutions grappling with similar challenges can consider blockchain a potential solution. This technology offers avenues to enhance transparency, streamline processes, and build trust, thereby reducing costs, fraud, counterpart risks, and settlement times.

Moving to the implementation dimension, this study unveils critical considerations for businesses selecting appropriate blockchain platforms. Drawing from successful field experiences in the financial sector, this study reveals the blockchain platform selection criteria and blockchain adoption checklist, which are potentially valuable for non-financial institutions when they decide to adopt blockchain technology to provide innovative products and services. Businesses often look for simplicity, connection, and transaction when selecting a blockchain platform. Companies don’t want to create yet another complex process that their customers have to go through; instead, they want to enhance and streamline what they are already doing. The emphasis is on avoiding additional complexities and instead enhancing existing processes. They can choose a blockchain platform that is as simple as possible so that they can get their hands on it quickly to offer new products and services, which allows them to expand their networks to unlock new opportunities and transact real value faster. Further, the study introduces a blockchain adoption checklist, urging businesses to align platform choices with long-term strategic goals, assess interoperability with legacy systems, evaluate privacy and scalability features, and gauge enterprise readiness. For example, the R3 Corda platform is designed to be the future-proof blockchain platform, allowing data and digital assets to move without friction in an open network protected with Corda’s unique privacy mode: permission admission, authenticated nodes, and data shared on a need-to-know basis. It has incorporated a backward approach to feed customer feedback and end-user points into its blockchain design to address the issues of interoperability, privacy, scalability, and enterprise readiness to ensure its platform can align incentives between people to meet diverse customer needs. R3 team focused on learning from its broader client base not only what they’re using Corda for but what problems they are trying to solve to design the system that fits their customer’s overall business strategy in the long run.

Finally, the impact dimension highlights the transformative effects of adopting the right blockchain technology, revealing the business values of adopting appropriate blockchain to leverage the new capabilities of this technology to deliver their products and services cheaper, quicker, and faster. For example, blockchain technology is successfully adopted for cross-border payment at MasterCard, syndicated loans at NatWest and Finastra, premium payments and claims handling at the insurance sector at ACORD, digital debt capital market at Agora, procure-to-pay at Siam Commercial Bank, B3i′s reinsurance solution, stock exchange at Nasdaq, etc. These applications lead to unlocking new opportunities, process automation, enhanced transparency, reduced settlement times and costs, error and fraud mitigation, and real-time data provision with a single source of truth. Blockchain fundamentally alters information recording, validation, and sharing, paving the way for decentralised protocols that significantly improve efficiency and trust.

Discussion

This section explicates the theoretical and practical implications of this study.

Theoretical contribution

The blockchain adoption framework developed by this investigation serves as a valuable resource for companies seeking to explore blockchain applications and leverage the technology’s potential value beyond the financial realm. It provides a structured guide for understanding and implementing blockchain adoption, enabling organisations to navigate the complexities of this transformative technology successfully. The framework stands as a meticulously constructed roadmap, offering a structured pathway for companies to comprehend, embrace, and effectively implement blockchain solutions within their operational frameworks. By distilling complex concepts into actionable insights, it empowers organisations to transcend the traditional boundaries of their industries and unlock new realms of possibility through blockchain innovation.

This framework helps non-financial institutions to learn from the successful blockchain use experiences in financial institutions, understanding what factors motivate blockchain adoption and how to adopt blockchain appropriately to offer new products and services, thus unlocking new opportunities to sustain businesses. It addresses institutional pressures, helping companies understand current business problems. The platform selection criteria focus on what businesses aim to achieve with blockchain technology. The blockchain adoption checklist assists companies in evaluating the selected blockchain platform, ensuring it is future-proof, fits overall business strategies, and aligns incentives among stakeholders. New institutional arrangements explicate the benefits of using blockchain to create value.

Through a comprehensive examination of intention, implementation, and impact, this framework provides a holistic perspective on the multifaceted journey of blockchain integration. It equips companies with the tools to articulate clear objectives, design robust implementation strategies, and assess the tangible outcomes of blockchain adoption within their unique organisational contexts. Moreover, this framework serves as a catalyst for innovation, inspiring companies to explore novel applications of blockchain technology beyond conventional use cases.

Further, the results of this study enrich the extant emerging blockchain literature in general and blockchain adoption in particular, expanding its applications in much broader fields to create more value. Blockchain offers significant benefits and new capabilities, such as improving operational efficiency through automated document management and reconciliation, reducing settlement time with smart contracts, mitigating counterparty risk via codified agreements executed in a shared immutable environment, increasing transparency and visibility, reducing fraud, and enhancing regulatory efficiency. These benefits will become more salient when more organisations adopt the technology appropriately with the right intention. When the use of blockchain technology becomes the industry norm, businesses can transact anything of value without friction.

Essentially, this framework is grounded in real-world insights. It draws upon the experiences of pioneering financial organisations that have successfully navigated the challenges of blockchain adoption through the R3 platform, distilling their collective wisdom into actionable guidelines that offer solutions to common obstacles encountered during blockchain adoption. As a result, organisations that wish to embark on their blockchain journey can benefit from the themed practices outlined in this framework, accelerating their path to successful implementation and realising the potential of blockchain technology.

Practical implications for general management

Practically, the findings of this study offer valuable insights for organisations seeking to adopt blockchain technology, guiding them in understanding how to effectively implement this technology to address existing business challenges and generate value. The technology can help businesses simplify business processes, improve user experience, enhance trust, and reduce costs if used properly.

Firstly, it’s essential for managers to conduct a thorough analysis of the specific business problems they aim to address and then decide whether blockchain is the best solution because different blockchains have different implications. For instance, the public blockchain is costly and slower to reach consensus, while the private blockchain is more cost-effective because users need to be permitted to participate. The blockchain consortia require effective collaboration between business partners.

Secondly, general managers should promote education and awareness among top executives to facilitate informed decision-making and communicate the value generated by blockchain initiatives to stakeholders, ensuring transparency and building confidence in the technology. As digital transformation becomes increasingly imperative across industries, it is essential for companies to invest in talent with the necessary digital skills to navigate technological advancements and leverage data effectively. Moreover, organisations’ managers need to compare and select the right and best blockchain platform to meet their business needs to work with and drive the companies forward by exploring consortiums and partnerships to address challenges and promote blockchain standards collectively.

Thirdly, general management should ensure that blockchain adoption aligns with the organisation’s overall strategic goals and objectives to mitigate risks related to technology, security, regulatory compliance, and potential disruptions to existing business models. Organisations need to be agile and check whether the platform is future-proof, focussing on long-term business success that fits the overall business strategy. Further, organisations also need to check whether the platform addresses the issues of interoperability, privacy, scalability, and enterprise readiness to capture value by using blockchain technology. Further, organisations can position themselves at the forefront of industry advancements by embracing blockchain technology and fostering an adaptive, agile, open, and learning-centric culture.

By incorporating these practical considerations into general management practices, organisations can confidently navigate the complexities of blockchain adoption. They can address real-world business challenges, enhance competitiveness, and drive innovation in the evolving digital landscape. Through strategic alignment, informed decision-making, and proactive risk management, organisations can unlock the transformative potential of blockchain technology and pave the way for sustainable growth and success.

Conclusion

The blockchain adoption framework developed in this study represents a valuable resource for companies looking to explore blockchain applications and unlock the potential value offered by this transformative technology. To facilitate broader blockchain adoption and realise the societal benefits it can bring, organisations must collaborate closely with blockchain developers and regulators, drawing lessons from the experiences of financial institutions in addressing technical challenges such as privacy, interoperability, scalability, and regulatory uncertainty.

Furthermore, the C-Suite must champion the decision to embrace blockchain technology, as their leadership is crucial in ensuring alignment with organisational goals and garnering support across all company levels. This top-down approach empowers stakeholders at every level to understand the technology and ask the right questions throughout the adoption process, ultimately driving towards the desired outcomes. Moreover, society must prioritise reskilling and upskilling initiatives to adapt to the evolving digital landscape and remain relevant in the face of changing norms.

Limitations of this study and further research

While this study offers valuable insights into enterprise blockchain adoption, it is crucial to acknowledge its limitations. The insights drawn from this study primarily stem from empirical data collected from the R3 case, which represents a specific type of permissioned blockchain consortium formed by leading financial institutions. While these insights may be analytically generalisable to some extent, it’s essential to recognise that they may only partially encompass the complexities of blockchain adoption in diverse organisational, cultural, or industrial contexts.

Therefore, further investigation is necessary to enhance the generalisability of the findings. Future studies should explore blockchain adoption in institutions within similar or different industrial sectors. By examining how these organisations select blockchain platforms that align with their overall business strategies, future research can corroborate and expand upon the findings of this study. Additionally, future research activities are needed to explore the mass adoption of blockchain technology at the enterprise level across different sectors and jurisdictions.

Understanding how professionals adapt and respond to technological changes in the context of blockchain adoption will shed light on the evolving skill sets required in the digital age. Moreover, conducting multi-case studies to identify similarities and differences across various blockchain adoption scenarios would enrich the existing literature and provide a deeper understanding of the factors influencing blockchain implementation and success.

By exploring these avenues, future research can contribute to a more comprehensive understanding of blockchain adoption and its implications for organisations across different sectors and regions, thereby aiding companies in successful digital transformation.

Footnotes

Acknowledgements

We want to thank the Journal of General Management editors and three anonymous reviewers for their invaluable comments and suggestions, which helped improve this manuscript.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.