Abstract

An important stream of research has suggested that there is a significant relationship between the board of directors, through its strategic role, and organizational performance. However, this presumed relationship appears to be more complex, given the conceptual distance between the cause and the effect. This distance is discernible in the omission of intermediate variables explaining the operation of this relationship, that is, (i) a variable reflecting an intermediate-level output, here board effectiveness and (ii) a variable reflecting the mechanisms that enable production of the output, particularly the board’s strategic use of management accounting information (MAI) deriving from the budget or financial and non-financial performance indicators. This study aims to revisit the link conceptually and empirically between strategic board involvement and organizational performance by simultaneously integrating strategic use of MAI and board effectiveness in an integrative model. Using survey data taken from a sample of 185 board of directors, the results suggest that the strategic use of MAI plays a crucial role, particularly in terms of performance indicators, to cement strategic board involvement and improve board effectiveness and organizational performance.

Keywords

Introduction

Past research has examined the relationship between strategic board involvement and organizational performance. Andrews (1980) was one of the first researchers to consider the existence of this presumed relationship arguing that a strategically involved board leads to clearer oversight of the organization’s objectives and policies. His pioneering study, together with other empirical studies, suggests that strategic board involvement has a positive influence on organizational performance (Judge and Zeithaml, 1992; Siciliano, 2005; Zhu et al., 2016). Some researchers, however, are of the opinion that the literature has not presented any clear explanation of what a board really does or how it influences organizational performance (Huse et al., 2011). Also, despite the consensus as to the existence of the board’s strategic role, the way it should perform that role is not always clear, and this leads to greater ambiguity (Hendry and Kiel, 2004). Some studies even suggest a negative relationship between strategic board involvement and performance (Hitt et al., 2001; Jensen, 1993; Johnson et al., 1993). Organizational performance could indeed be negatively affected by an over-involved board that oversteps the boundaries of its strategic role and interferes with the organization’s day-to-day management (Judge and Zeithaml, 1992). These contradictory findings indicate that this cause-and-effect relationship needs to be examined further (Machold and Farquhar, 2013).

One possible explanation for these inconclusive, perhaps contradictory results, relates to the conceptual distance between the cause (strategic board involvement) and the effect (organizational performance). In other words, intermediate steps between this cause and this effect that add complexity to the passage from one to the other may have been omitted. This conceptual distance is discernible in the absence of intermediate variables explaining the articulation of the presumed relationship, namely, (i) a variable reflecting an intermediate-level output, here board effectiveness and (ii) a variable reflecting the mechanisms that enable the achievement of the output, particularly the board’s strategic use of management accounting information (MAI) deriving from the budget as well as financial and non-financial performance indicators. The main purpose of this study is thus to enrich the presumed relationship between strategic board involvement and organizational performance by also considering these two intermediate variables simultaneously. More specifically, the goal is to revisit this relationship by proposing an integrative model based on two main mediation paths.

Using survey data taken from a sample of 185 board of directors of Canadian organizations, our results show that strategic board involvement does not contribute directly to organizational performance, but instead indirectly through the strategic use of MAI and board effectiveness. Interestingly, the influence of MAI operates mainly through the strategic use of information from financial and non-financial performance indicators, and less from the monitoring of budgets.

This study contributes to the current literature in several ways. First, it examines the presumed relationship between strategic board involvement and organizational performance from a renewed angle. Because this relationship is founded on sometimes contradictory conclusions, this study narrows the conceptual distance by taking into consideration an information dynamic through the board’s strategic use of and including board effectiveness as an intermediate-level output. Although specific streams of research have examined the influence of board involvement, MAI or board effectiveness on organizational performance, they remain mostly disconnected. No holistic approach has been presented to articulate in a global framework the simultaneous links between these variables.

Second, this study helps integrate knowledge from two disciplines that have developed in relative isolation, namely, corporate governance and management accounting. The governance literature focuses on the use of information outside the organization’s boundaries, that is, in the board, but says little about the internal mechanisms that produce that information and how this information is used strategically by board members. On the other hand, the accounting literature typically conceptualizes the use of MAI inside the boundaries of the organization, examining the mechanisms ensuring the coherence of managerial behaviors and decisions with the organization’s goals and strategies. However, a board of directors differs from the typical organizational setting in that it consists of executive directors and independent directors who do not have the same level of knowledge concerning the organization’s activities, or the same proximity to its day-to-day operations.

The structure of this study is as follows. First, the conceptual framework is described and followed by the formulation of the hypotheses. The following section presents the methodology, including data collection and sample definition, measurement of the constructs and their validity and reliability, and an explanation of the statistical tests. Subsequently, the results of the analyses are presented. Lastly, the conclusion integrates theoretical and practical implications of the results, defining the study’s limitations, and proposing avenues for future research.

Conceptual framework

Overview of the conceptual model

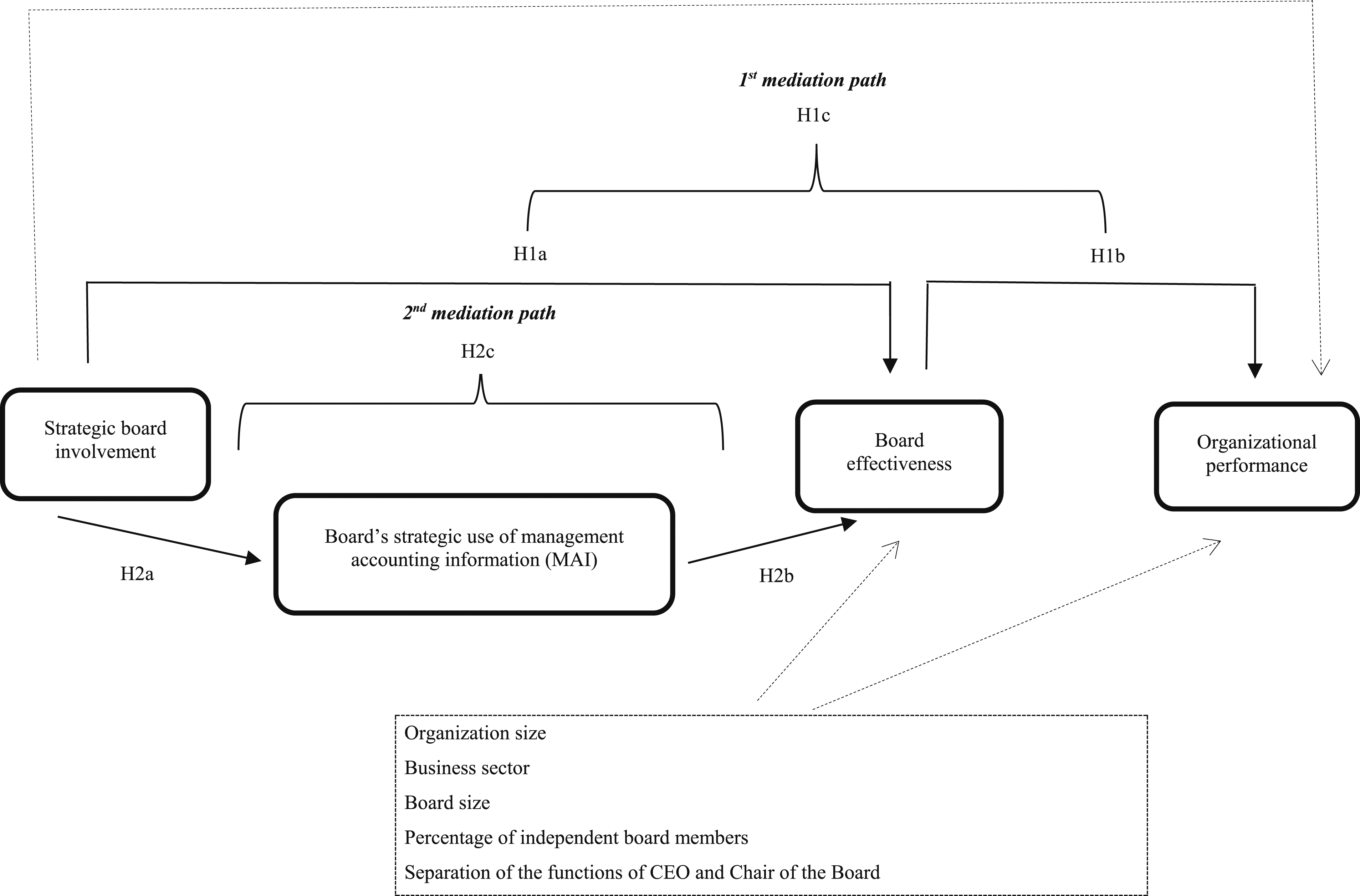

Figure 1 provides an overview of the conceptual model, designed to enhance the understanding of the presumed relationship between strategic board involvement and organizational performance by introducing two mediation paths. Conceptual double mediation path model.

The first, larger mediation path (H1) presents board effectiveness as a variable reflecting an intermediate-level output. This path thus bridges the gap between two isolated streams of research. The first stream suggests that an effective board contributes to value creation and organizational success, notably through efficient execution of directors’ tasks (Forbes and Milliken, 1999; Payne et al., 2009). The second stream posits that strategic board involvement is an explanatory factor in board effectiveness because it can improve the quality of decisions (Stiles and Taylor, 2001; Westphal, 1999). In sum, board effectiveness may act as an intermediary between strategic board involvement and organizational performance.

The second, smaller mediation path (H2), inside the first, examines the board’s strategic use of MAI as an ongoing process that leads to the production of output. Once again, our model bridges the gap between two different streams of research. The first group of studies suggest that greater board involvement is conducive to the strategic use of accounting information (Brennan et al., 2016). Indeed, the strategic use of MAI conveys knowledge to directors, which reduces information asymmetry between them and top management while also meeting their information needs in order to maintain and personalize their level of involvement (Hendry and Kiel, 2004; Judge and Zeilthaml, 1992). The second stream proposes that the use of MAI supports decisions and questions concerning current strategic issues, which results in improved board effectiveness. In sum, the board’s strategic use of MAI appears to act as an intermediary between strategic board involvement and board effectiveness.

The conceptual model also examines the potential influence of the variables studied in past governance and management accounting literature. In this study, control variables are put into two categories, relating to (i) the organization and (ii) the board. Two variables are used to control organizational characteristics, namely, size and business sector (Zona and Zattoni, 2007). Regarding the board characteristics, three common variables are considered, namely, size, percentage of independent members, and separation of the functions of CEO and Chair of the board (Finkelstein and Mooney, 2003).

Key concepts

Strategic board involvement

The concept of involvement is generally defined as a subjective psychological state reflecting the importance and personal relevance of an object or event (Barki and Hartwick, 1989). In a context of boards, strategic involvement relates to the amount of attention directors pay to components of the strategy formation, ranging from the formulation to the implementation of strategy (Judge and Talaulicar, 2017; Judge and Zeilthaml, 1992). For strategy formulation, the board questions and improves the proposed new strategic options, and facilitates the organization’s choice of strategy (Huse, 2007). The board’s involvement in strategy implementation, meanwhile, relates to defining the milestones needed to assess progress towards the adoption of strategy and evaluate organizational performance (Zhang, 2010).

Board’s strategic use of MAI

In this study, the board’s strategic use of MAI is defined as formal financial and non-financial information supplied to the board on a recurrent basis and used by the board to oversee the organization’s strategic plan (Massicotte and Henri, 2021). The strategic use of MAI deriving from the budget or financial and non-financial performance indicators is founded on two main dimensions: (i) monitoring strategic plan implementation and (ii) questioning the strategic plan. The board’s monitoring of strategic plan implementation consists of assessing and measuring progress in the application of the organization’s strategies (Davies, 1991). This dimension mainly concentrates on the use of MAI to provide support to strategy implementation. The board’s questioning of the strategic plan is the activity of determining whether the strategic plan’s fundamental orientations should be adjusted in light of past events, and systematically and continuously checking that the assumptions underlying the strategic plan are still valid (Schreyögg and Steinmann, 1987). It is based on the information reported to the organization in support of emerging new strategies.

Board effectiveness

It is commonly recognized that an effective board has the ability to perform its control and service tasks effectively (Forbes and Milliken, 1999; Mooney et al., 2021). More specifically, effectiveness in the performance of directors’ control tasks is generally defined as protecting the interests of shareholders and other stakeholders through the oversight of top managers’ behavior, while effectiveness in the performance of service tasks relates more to advice and support given by directors to top management on matters relating to the organization’s strategy (Finkelstein and Mooney, 2003).

Organizational performance

The models examining organizational performance have progressively taken into consideration (i) effectiveness through the attainment of goals (goal model), (ii) effectiveness through the resources and processes necessary to achieve those goals (system model), and (iii) satisfaction of the organizations’ stakeholders (strategic constituencies model) (Henri, 2004). Since none of these models captures the entirety of organizational performance, this study draws on all three of the above models (Su et al., 2015). As a result, this conceptualization considers two dimensions of performance: (i) the coverage of the financial and non-financial dimensions of performance and (ii) the relative nature of performance, through a process of comparison with an internal benchmark (the organization’s goals) and an external benchmark (the competition).

Hypothesis development

First mediation path—Influence of strategic board involvement on board effectiveness

Past studies provide empirical evidence demonstrating a link between strategic board involvement and board effectiveness operating through the directors’ ability to work together to achieve their control and service tasks (Finkelstein and Mooney, 2003; Sundaramurthy and Lewis, 2003; Westphal, 1999). Conceptually, it is argued that this positive association can be explained by (i) the structure and formalization of the decision-making process and (ii) greater use of directors’ expertise.

More specifically, strategic board involvement enables the organization to better structure and formalize its strategic decision-making process (Pugliese et al., 2009; Zahra, 1990). Through a well-established decision-making culture in the board, the organization gives a formal structure to the board’s operation, the respective roles of the board and top management, and the way the board influences and supports strategic decisions (Pye and Pettigrew, 2005). One group of researchers has stressed the positive impact for strategy-related matters of the board’s working style and structure (Golden and Zajac, 2001; Huse, 2005). When the division of work between the board and top management is more clearly defined, information circulates better and that improves the decision-making process (Lockhart, 2012). In other words, a more formal, structured decision-making process improves the quality of strategic decisions, and thus contributes to board effectiveness (Sundaramurthy and Lewis, 2003; Westphal, 1999).

In addition to improving the quality of the organization’s decision-making process, strategic board involvement means the organization can capitalize on directors’ expertise (Adams and Ferreira, 2007). The existing research recognizes the importance of board members’ experience and knowledge for effective governance (Payne et al., 2009). Expertise is in fact one of the essential requirements for being a director (Cumming and Leung, 2021; Mooney et al., 2021). From a cognitive perspective, Rindova (1999) observes that strategic decision-making will improve with the expertise directors bring to the organization; This is because strategic board involvement makes maximum use of this expertise by requiring directors to make a significant contribution to strategy implementation. Motivated directors who consider strategy important will share and deploy their expertise more intensely, and in doing so improve board effectiveness (Finkelstein and Mooney, 2003; Sonnenfeld, 2002). Although over-involvement of board overstepping the boundaries of its strategic role and interfering with the organization’s day-to-day management could have adverse effect (Judge and Zeithaml, 1992), the following hypothesis is posited:

Strategic board involvement positively influences board effectiveness.

First mediation path—Influence of board effectiveness on organizational performance

Past studies have considered that the board plays an important role in value creation for the organization, and board effectiveness appears to be an antecedent of organizational performance (Crow and Lockhart, 2016; Judge and Zeithaml, 1992; Watson and Ireland, 2021). More specifically, an effective board contributes to the establishment of strong strategic foundation (Sundaramurthy and Lewis, 2003; Westphal, 1999). As well as being conducive to reaching sales and profit goals through the close monitoring of strategy implementation, directors help develop better long-term strategies. The ability to effectively manage risks also help the organization to do better than its competitors (Payne et al., 2009). By performing well in its control and service tasks, an effective board supports top management in anticipating threats to the organizational future and ensures the organization displays socially and environmentally responsible behavior (Federo and Saz-Carranza, 2018; Liao et al., 2021; Nekhili et al., 2021). As a matter of fact, more and more, boards are taking into consideration a wide range of stakeholders, not just the shareholders but also customers, employees, and suppliers (Desender et al., 2020; Shin and You, 2020). In other words, board effectiveness should translate into value creation for the organization, including an improvement in its financial and non-financial results (Van Den Heuvel et al., 2006). Although an effective board could not compensate for all potential organizational deficiencies or external market conditions, the following hypothesis is proposed:

Board effectiveness positively influences organizational performance. Combining the arguments from H1a and H1b, the larger mediation path (H1) includes an additional output variable, positioning board effectiveness as a mediating variable between strategic board involvement and organizational performance. Due to its ability to improve the quality of decision-making, strategic board involvement is considered an explanatory factor for board effectiveness, which in turn acts as an intermediary between strategic board involvement and organizational performance. In addition to reducing the conceptual distance between the cause and the effect, the importance of board effectiveness, as an additional output variable, is explained by the existence of its link with (i) strategic board involvement (Payne et al., 2009; Sundaramurthy and Lewis, 2003) and (ii) organizational performance (Forbes and Milliken, 1999; Zhu et al., 2016). In sum, strategic board involvement contributes to board effectiveness, which in turn improves organizational performance. More precisely:

Strategic board involvement indirectly and positively influences organizational performance through board effectiveness.

Second mediation path—Influence of the strategic board involvement on the board’s strategic use of MAI

One stream of research has demonstrated that the board cannot maintain and pursue its level of strategic involvement without using information (Heracleous, 2001; Zhu et al., 2016). In other words, greater strategic board involvement entails the use of various kinds of relevant information (Aram and Cowen, 1986; Huse, 2007). As a result, instead of relying solely on information from formal audits and certain regular updates, the board also refers to MAI (Parker, 2008; Zahra, 1990). Directors’ use of MAI to fulfill their strategic role differs from their use of MAI for a compliance role because the strategic role focuses on using information to create value for the organization, while the compliance role focuses mainly on accountability. For example, as well as using information from regular budget and key performance indicators to monitor and validate goal attainment, directors also use this information to discuss strategy implementation and question future orientations (Massicotte and Henri, 2021). Conceptually, greater board involvement is thus conducive to the use of MAI for strategic plan oversight, notably considering the need to set up a feedback system and to reduce information asymmetry.

More specifically, the board’s strategic use of MAI involves a feedback loop (Flamholtz et al., 1985) which can crystallize strategic board involvement. A feedback routine makes it possible to monitor the implementation of the strategic plan and question its contents for the future. The board’s strategic use of MAI makes this single and double feedback loop possible (Argyris and Schön, 1978). By referring to MAI to set and monitor financial and non-financial goals, the board makes strategic decisions about these goals to approve, reject, or reformulate the strategic proposals put forward by top management (Hendry and Kiel, 2004). The board can thus better oversee the implementation of the organization’s strategy (McNulty and Pettigrew, 1999; Zhang, 2010). The inherent feedback loop of MAI allows directors to maintain their involvement because they perceive the strategic dimension as important and relevant to them. This idea is supported by a substantial stream of research suggesting that feedback makes a positive contribution to individuals’ motivation (Flamholtz et al., 1985).

Furthermore, the board’s strategic use of MAI spreads knowledge to directors, reducing the information asymmetry between directors and top management while meeting their need for information to maintain and pursue their level of involvement (Heracleous, 2001; Judge and Zeilthaml, 1992). This spreading of information mitigates internal information asymmetry between members of the board, especially independent directors who do not have the same level of knowledge of the organization’s activities or the same degree of proximity to day-to-day operations as members of top management (Roberts et al., 2005; Rutherford and Buchholtz, 2007). Researchers acknowledge the importance of a detailed understanding of the organization’s internal management activities and issues, which they refer to as tacit knowledge (Forbes and Milliken, 1999). Explicit knowledge, in comparison, implies systematic expression and collective appropriation. It is easily codified and accessible to any director willing to put in the necessary time and effort to acquire it (Brennan et al., 2016; Dawson et al., 2010). Consequently, the board’s strategic use of MAI formalizes the strategic reality of the organization because it can help transform some tacit knowledge into explicit knowledge (Nonaka and Takeuchi, 1995). In other words, the board’s strategic use of MAI reduces information asymmetry by facilitating the transition from semiconscious knowledge to structured knowledge (Leonard and Sensiper, 1998), and this helps directors perform their strategic role. The transition from tacit to explicit knowledge through the strategic use of MAI enhances quality decision-making by the board (Brennan et al., 2016). Although strategically involved boards could (un)voluntarily overlook MAI, preferring to rely mainly on their collective experience or gut feelings, or because of cognitive boundaries and limited attention, the following hypothesis is posited:

Strategic board involvement positively influences the board’s Strategic use of MAI.

Second mediation path—Influence of the board’s strategic use of MAI on board effectiveness

The decision support role played by MAI reduces uncertainty in strategic decision-making (Zimmerman, 2000). In other words, the strategic use of MAI facilitates strategic decision-making and the attainment of predefined goals and objectives (Baines and Langfield-Smith, 2003). It also supports decisions and questions triggered by current circumstances, and thus supplies faster, more direct feedback (Nanni et al., 1992; Said et al., 2003). In a board setting, this means that the strategic use of MAI encourages challenges and questions when strategic decisions are being made (Brennan et al., 2016). Having said that, for closer monitoring of strategic plan implementation and questioning of strategy, top management supplies information to the board about meeting targets for financial and non-financial indicators (Parker, 2008; Zhang, 2010). Such strategic use of financial and non-financial information supports board effectiveness, via closer monitoring and better-informed questions about the strategic plan (Robert et al., 2005). More specifically, strategic use of MAI helps reduce the latitude of actions of top management and, thus, leads to positive tension between the containment of managerial opportunism and the pursuit of strategic opportunities (Ponomareva et al., 2019). Because the board consists of executive directors, and independent directors who do not have the same level of knowledge about the organization’s activities, the board’s strategic use of MAI can reduce information asymmetry between these two groups (Roberts et al., 2005; Rutherford and Buchholtz, 2007). It thus helps to improve the board’s cohesiveness as a group, and ultimately the board’s effectiveness in overseeing the strategic plan (Forbes and Milliken, 1999). Although information overload could have adverse effect by paralyzing the decision-making process, the following hypothesis is proposed:

The board’s strategic use of MAI positively influences board effectiveness. Combining the arguments that have led to H2a and H2b, a mediating effect of the board’s strategic use of MAI on the relationship between strategic board involvement and board effectiveness is now proposed. Among other factors, board effectiveness stems from active, ongoing board involvement in strategy implementation (direct link – H1a), but also from mobilizing the information potential of MAI (indirect link) (Crow and Lockhart, 2016). Greater board involvement notably leads to more use of relevant, varied MAI for strategic plan oversight purposes (Huse, 2007; Parker, 2008) and as a result, the board is better able to perform its strategic role. This activity of strategy monitoring and questioning through budget and performance indicators helps to improve board effectiveness. In short, strategic involvement by directors contributes to the board’s strategic use of MAI, which in turn supports board effectiveness. More precisely:

Strategic board involvement indirectly and positively influences board effectiveness through the board’s strategic use of MAI.

Methodology

Data collection and sample

A survey approach was used to test the above hypotheses based on a convenient sample of directors sitting on board of for-profit Canadian organizations. To form the sample, first, the Infomart database is consulted and the available information on directors of Canadian organizations listed on the Toronto stock exchange is extracted. Additional work was necessary to complete the identification of directors for some organizations. Then, using the Directory of certified directors maintained by the Collège des administrateurs de sociétés, 1 additional directors are identified, different from the first database, sitting on boards of for-profits Canadian organizations. The final sample consisted of 927 directors with full validated contact details. It is worth mentioning that for some boards of publicly traded organizations, the contact details for more than one director were available. In this case, only one director received the questionnaire following the prenotification step.

The questionnaire was first validated by means of a pre-test conducted with a group of five academic experts in governance and management control, and seven members of board of directors. It was then sent out anonymously in electronic form via email by the survey firm BIP 2 to board members previously identified. Administration of the questionnaire took place over a period of more than 2 months and comprised the following four stages: initial sending, first reminder (after 2 weeks), second reminder (after 4 weeks) and third reminder (after 6 weeks). To obtain a high response rate, BIP also made telephone reminders when the second reminder was sent out, offering the option of completing the questionnaire over the telephone. The questionnaire took about 20 min to complete and was sent out with an introductory email explaining the purpose of the study and offering all respondents the opportunity to receive a report which would allow them to compare their practices with the practices of other Canadian organizations.

A total of 192 questionnaires were returned, of which 185 were usable, giving a final response rate of 20%. This is comparable to the 10%–30% interval reported in recent governance studies and management accounting studies (Derdowski et al., 2018; Guenther and Heinicke, 2019). All the respondents occupied directorship positions. They were asked to answer all questions about one board of for-profits organizations of which they were (or had recently been) a member. 54% of the organizations concerned belonged to the industrial sector and 46% to the service sector; furthermore, 67% of them were small- and medium-sized firms (<499 employees) and 33% were large firms (>500 employees). Concerning the respondents themselves, 84% were aged 51 or older and 78% were male. In terms of their education level, 38% had a bachelor’s degree, 48% a master’s degree, 8% a PhD, and 6% had no degree. On average, respondents were members of 2.7 boards and had been directors for 16.9 years. Moreover, boards are on average comprised of 8.32 members, ranging between 3 and 25. An analysis of non-response bias was conducted to confirm the validity of the data. Comparison between the first and last 10% of respondents (the latter serving as a proxy for non-respondents) detected no significant differences in the answers received. The test performed gave no overall indication that non-response bias was a major issue in this sample. The classic test of comparing respondents and non-respondents on general parameters (such as their organization’s business sector and size) could not be validated due to the methodology used for this study: as respondents were asked to answer the questionnaire with a particular board in mind but not to name it, it was impossible to know the exact identity of the respondent’s chosen organization.

Construct measurement

Descriptive statistics.

Note: * Significant at 0.05 ** Significant at 0.01.

Finally, the control variables were measured as follows. Organization size was measured using the number of full-time or equivalent employees, with a log-transformation to adjust for asymmetry (Payne et al., 2009). Business sector was a binary variable coded 0 if the organization belonged to the industrial sector, and 1 belonged to the service sector (Zona and Zattoni, 2007). Board size was measured by counting the total number of board members, with a log-transformation to adjust for asymmetry (Zahra et al., 2000). The percentage of independent board members was measured by taking the number of independent directors as a percentage of total board members (Mallette and Fowler, 1992). The separation of the functions of CEO and Chair of the Board was a binary variable coded 0 if the CEO was also the Chair of the board, and 1 otherwise (Finkelstein and D’Aveni, 1994).

Construct validity and reliability

Various thresholds were used to demonstrate the validity and reliability of constructs. Cronbach’s Alpha and composite reliability scores above 0.70 were required to be considered acceptable (Fornell and Larcker, 1981; Nunnally, 1978). For variance extracted, the threshold was 0.50 (Hair et al., 1998). For the goodness-of-fit indexes resulting from first and second order confirmatory factor analysis, the following thresholds were used: (1) the non-normed fit index (NNFI) > 0.90 (Tabachnick and Fidell, 2001), (2) the comparative fit index (CFI) > 0.95 (Hu and Bentler, 1995), and (3) the root mean square error of approximation (RMSEA) < 0.10 (Hu and Bentler, 1999). A second order confirmatory factor analysis was conducted on the organizational performance construct since it converged on two dimensions. The discriminant validity was assessed using a statistical test indicating one measure’s capacity to provide different results from other measures (Anderson and Gerbing, 1988; Fornell and Larcker, 1981). For the purposes of this test, the variance extracted for each construct was compared with the squared correlation between latent constructs (Fornell and Larcker, 1981). To support discriminant validity, the variance extracted for each construct had to exceed the squared correlation. Harman’s (1967) single-factor test was conducted, which did not reveal the presence of a single factor, suggesting that the variables are distinct constructs.

Appendix 1 presents the results of the construction validation process. Re-specification was only necessary for two constructs which had insufficient R2 on one item (<0.40), namely, strategic board involvement (1 item eliminated) and board effectiveness (1 item eliminated). After these minor re-specifications, all constructs were above the recommended thresholds for Cronbach’s Alpha, composite reliability and variance extracted, showing acceptable fit to the model with adequate R2. All item coefficients were statistically significant (p < .01).

Statistical tests

First, structural equation modeling was used in view of the conceptualization of multiple, interdependent relationships of dependence, and the presence of latent variables that were not directly observable (Mueller, 1996). The LISREL 9.30 software was used to analyze the data for this study. Composite indexes, and a partial disaggregation approach, were used to represent all the latent constructs in three respective indexes (Bagozzi and Heatherton, 1994; Landis et al., 2000). Moreover, structural equation models require that the function that represents the entry matrix be reversible, that is, the function must possess an inverse function. This is not the case when some conditions are violated; one of the main violations is the presence of multicollinearity (Roussel et al., 2002). The current models do not contain problematic correlations between constructs that could lead to multicollinearity issues.

In terms of statistical power, the existing literature suggests that a sample size of between 100 and 200 observations, or 5 to 10 observations per parameter, is adequate for testing small and medium structural equation models (Anderson and Gerbing, 1988; Bentler and Chou, 1987). In this study, the sample size is adequate for testing the proposed model (n = 185), although the number of observations per parameter (4.21) is slightly below the suggested rate. A sensitivity analysis consisting of running a simplified model without the four non-significant control variables shows that the initial results are unchanged, with a rate of 5.61 observations per parameter.

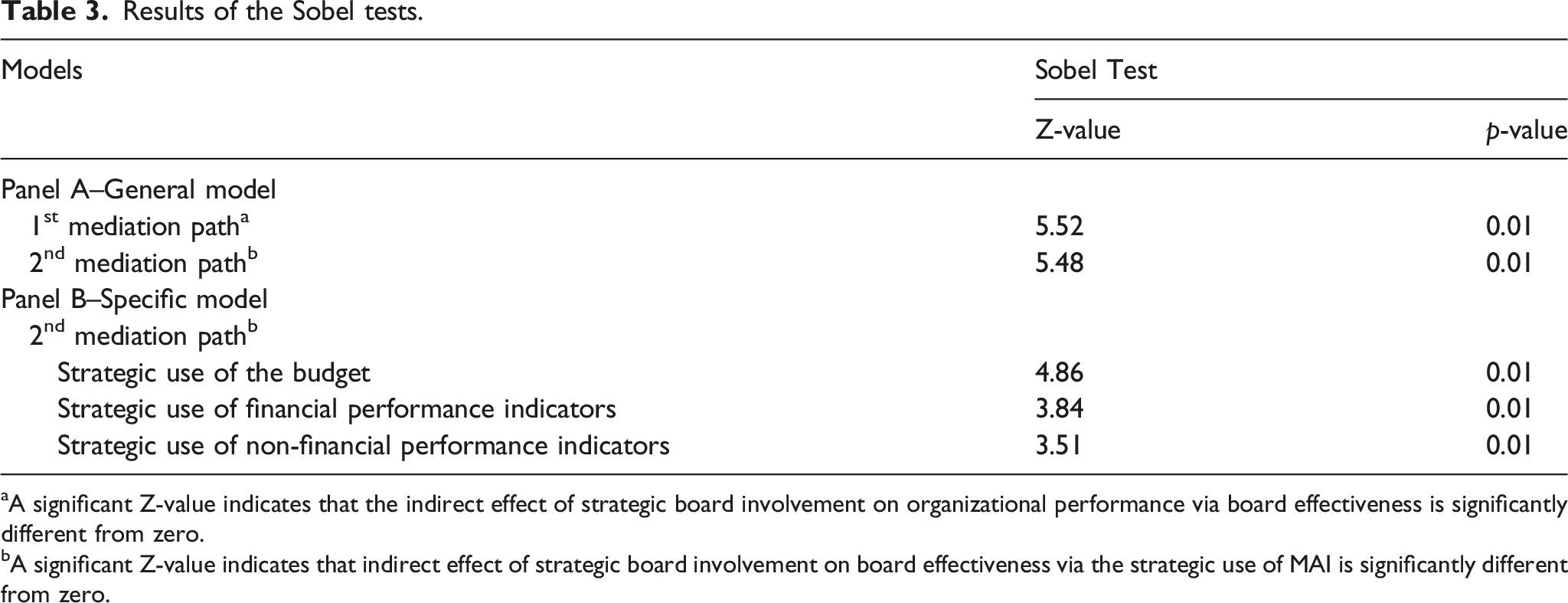

In addition to the analysis of direct and indirect effects included in LISREL, given the importance of the mediation effects in the conceptual model, a further test was conducted for the two mediation paths. The Sobel test is used to determine whether a mediator causes the independent variable’s influence on the dependent variable (Sobel, 1982). In other words, this test determines whether the diminished effect of the independent variable, once the mediator is included in the model, constitutes a significant reduction, and thus the test determines whether the mediation effect is statistically significant.

Results

Descriptive statistics

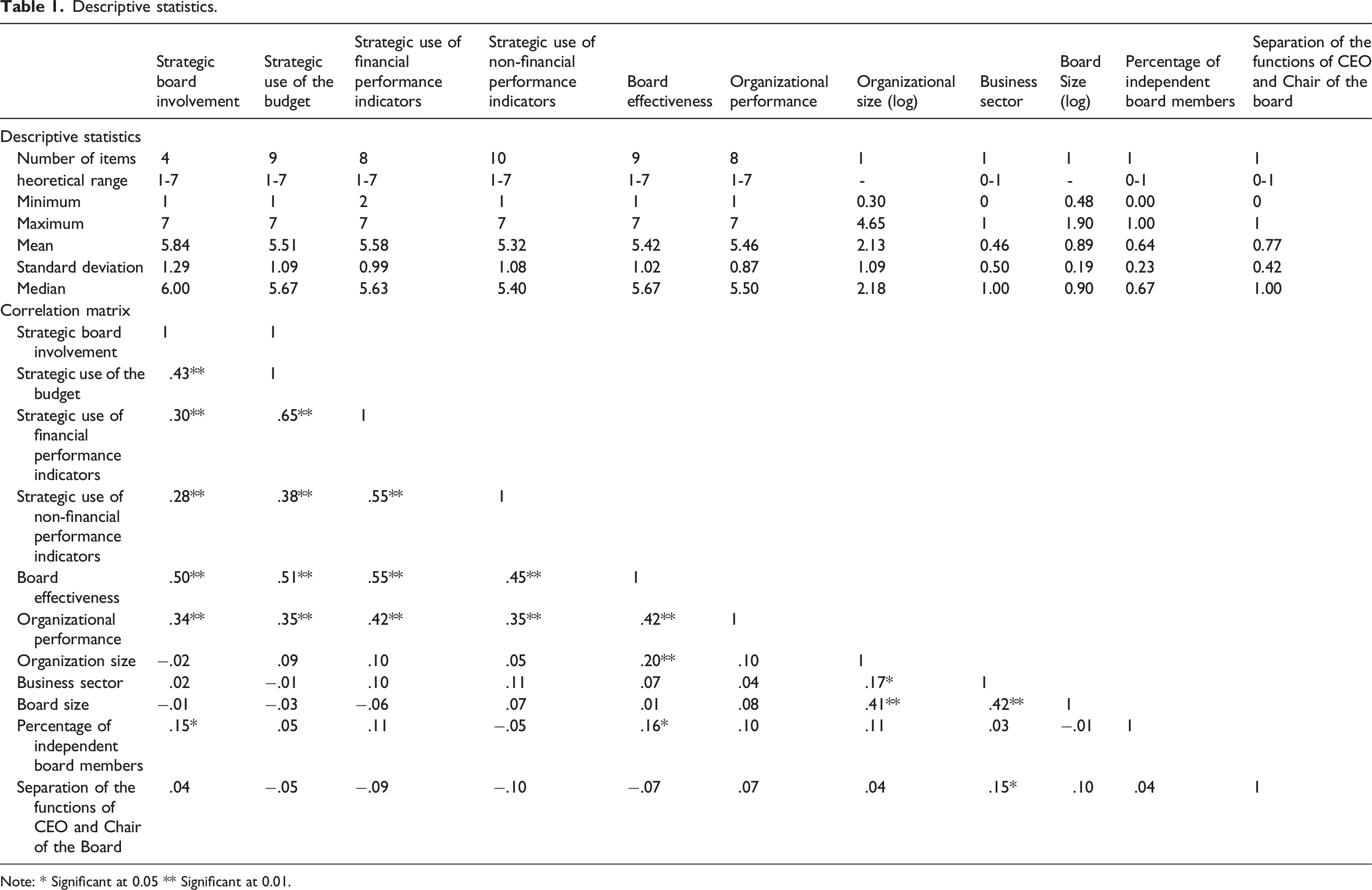

Table 1 presents the descriptive statistics for the constructs and the correlation matrix. The results suggest the board’s strategic use of MAI is moderately high, particularly with the budget and financial performance indicators, and slightly less with the use of non-financial indicators. It is worth mentioning the presence of positive and significant correlations between the model’s constructs. More specifically, the coefficients are moderately low between strategic board involvement, MAI, board effectiveness and organizational performance, but moderately high between specific types of MAI, namely, budget, financial and non-financial performance indicators. These latter statistics are expected considering that they are part of a global management control package (Malmi and Brown, 2008).

Hypotheses testing

Standardized results of the structural equation models Panel A – General model.

Note: *p < .05; **p < .01; n.s. - not significant.

First mediation path

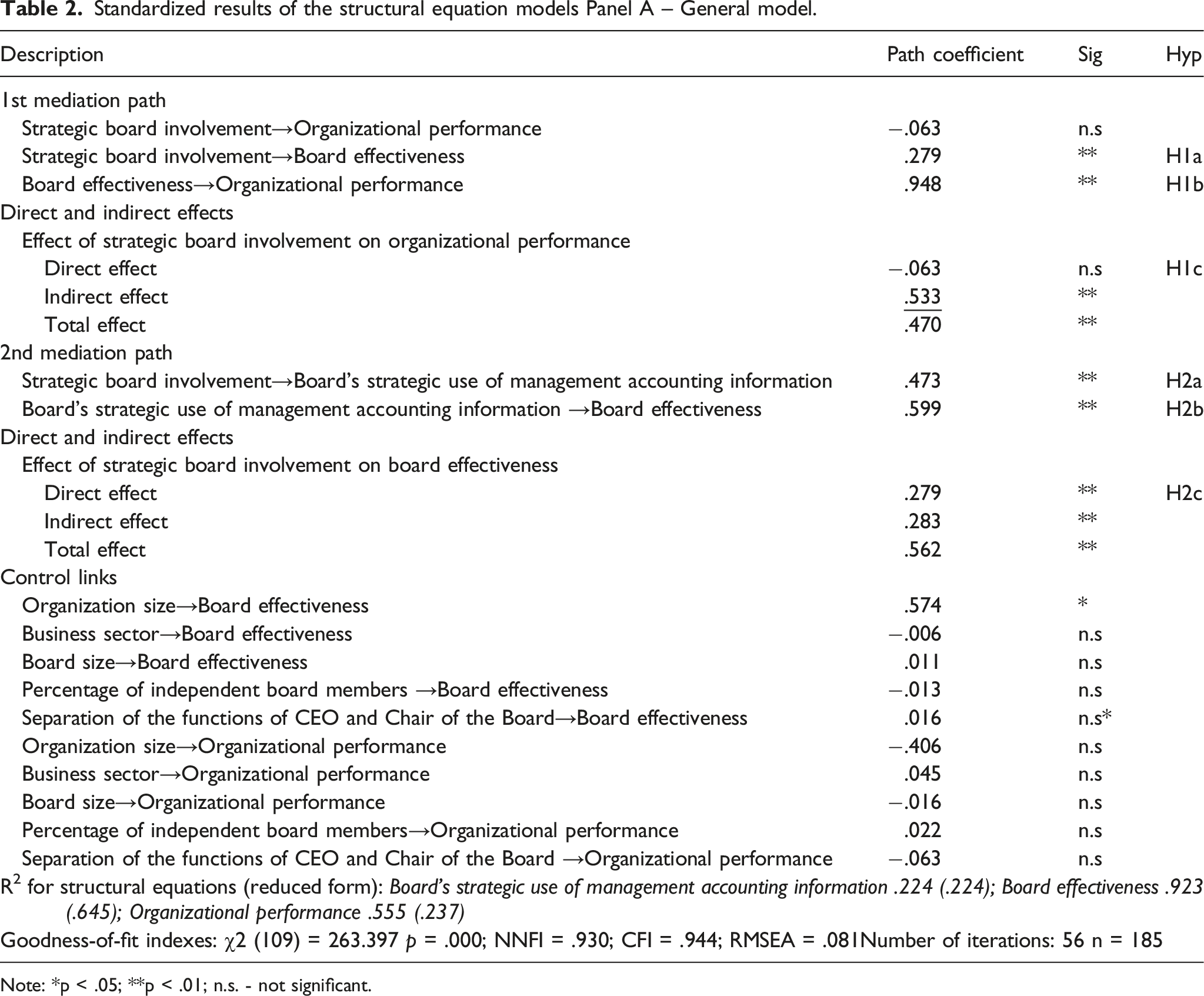

Overall, the results given by the general (Panel A) and specific model (Panel B) support the existence of an indirect positive, significant connection between strategic board involvement and organizational performance via board effectiveness.

More specifically, the results of both models suggest a positive, significant direct link for the two components of the first mediation path, that is, (i) the link between strategic board involvement and board effectiveness (0.279/0.351; p < .01) and (ii) the link between board effectiveness and organizational performance (0.948/0.939; p < .01). These results support hypotheses H1a and H1b. Also, analysis of total effects for both models lead to two findings that support H1c and suggest a full meditation relationship. First, there is a weak and negative, but not significant direct link between strategic board involvement and organizational performance. Moreover, the total effect (0.470/0.524; p < .01) is explained entirely by the presence of a significant positive and indirect link (0.533/0.579; p < .01), which has been alleviated by the negative direct link. Also, the indirect link is mainly driven by the coefficient of the path between board effectiveness and organizational performance which is approximately three times more important than the path between board involvement and board effectiveness. Overall, these results suggest that for every additional unit increase in board involvement (e.g., one degree of involvement on our measurement scale), organizational performance is expected to increase approximately by 0.5 unit on our measurement scale (e.g., 0.533/0.579 times the standard deviation of organizational performance) through improvements in board effectiveness. Considering all variables in the models, including mediators and error terms, the R2 of organizational performance is .237/0.302, which may be considered a small increase for policy purposes.

Second mediation path

In general, the results reflect a positive, significant indirect link between strategic board involvement and board effectiveness via (i) the strategic use of MAI generally by the board and (ii) specifically, the strategic use of financial and non-financial performance indicators. However, the presence of an indirect relationship via the budget is less conclusive.

More specifically, the results of the general model (Panel A) suggest that strategic board involvement positively and significantly influences the board’s strategic use of MAI (.473; p < .01) which in turn positively and significantly influences board effectiveness (0.599; p < .01). Contrary to the first mediation path, these two paths contribute relatively equally to the indirect effect. The results of the specific model (Panel B) generally concur with this for both components of the mediation path. As expected, strategic board involvement positively and significantly influences the strategic use of (i) the budget (0.517; p < .01), (ii) financial performance indicators (0.436; p < .01), and to a lesser extent (iii) non-financial performance indicators (0.381; p < .01). The results also suggest that the strategic use of financial performance indicators (0.337; p < .01) and non-financial performance indicators (0.208; p < .01) positively and significantly influences board effectiveness. No significant result was found concerning the budget. In sum, these results provide overall support for hypotheses H2a and H2b.

A total effect analysis results in two findings that suggest the presence of partial mediation, which supports hypothesis H2c. First, as discussed earlier, both the general and specific model (Panel A and B) show a direct link between strategic board involvement and board effectiveness (0.279; p < .01/0.351; p < .01). The total effect is also explained by the presence of a significant indirect link in both the general model (0.283; p < .01) and the specific model (0.266; p < .01). In both cases, and contrary to the first mediation path, the total effect is approximately explained equally by both direct and indirect components. In the specific model (Panel B), as discussed earlier, an indirect link is found for the use of financial and non-financial performance indicators, but not for the use of the budget. Overall, these results suggest that for every additional unit increase in board involvement (e.g., one degree of involvement on our measurement scale), board effectiveness is expected to increase approximately by 0.6 unit on our scale (e.g., 0.562/0.617 times the standard deviation of board effectiveness), approximately half directly (0.279/0.351) and half indirectly through improvements in the strategic use of management accounting information (0.283/0.266). Considering all variables in the models, including mediators and error terms, the R2 of board effectiveness is 0.645/0.768, which might be considered a large increase for policy purposes.

Results of the Sobel tests.

aA significant Z-value indicates that the indirect effect of strategic board involvement on organizational performance via board effectiveness is significantly different from zero.

bA significant Z-value indicates that indirect effect of strategic board involvement on board effectiveness via the strategic use of MAI is significantly different from zero.

Additional testing

Another structural model has been analyzed in which organizational performance is considered as an ordinal variable instead of a continuous variable. The results remain virtually unchanged in terms of model fit, statistical signification, and path coefficients (except for some indirect effects that are slightly smaller). The results of this test are presented in appendix 2 and support the main conclusions.

Discussion and conclusion

The main purpose of this study was to revisit conceptually and examine empirically the presumed relationship between strategic board involvement and organizational performance by considering additional intermediate parameters. Overall, the analyses show that the relationship between strategic board involvement and organizational performance is more complex than reported in the past literature, given the conceptual distance between the cause and the effect. In fact, strategic board involvement does not contribute directly to organizational performance. Instead, the relationship operates indirectly, through board effectiveness. Due to its ability to improve the quality of decisions, a board with good involvement in its strategic role is more effective in its actions. This suggests that board effectiveness acts as an intermediary between strategic board involvement and organizational performance. In other words, through its advisory role focusing on strategy, the board plays an important part in the organization’s value creation; and board effectiveness positively influences organizational performance.

The relationship between strategic board involvement and organizational performance is not only mediated by board effectiveness, but also by the informational mechanisms supporting board members. The results revealed that the board’s strategic use of MAI also acts as an intermediary between strategic board involvement and board effectiveness. In fact, an effective board cannot maintain and pursue its level of strategic involvement without using detailed information produced by MAI. In other words, the board’s contribution to value creation lies mainly in its active, continuous involvement in strategy, which mobilizes the information potential of MAI.

The analyses also revealed that the influence of MAI operates mainly through the strategic use of information from financial and non-financial performance indicators, and less from the monitoring of budgets. This could be explained by the budget’s shorter term focus, which prevents the board from fully embracing the organization’s long-term issues and priorities. The information derived from the budget may be considered by board directors as useful for accountability than strategic purposes. It is also possible that the strategic use of this MAI may be partial, that is, not fully embedded in the board’s routines. In other words, information from the budget may occasionally be used strategically, but it is used more frequently for accountability purposes, which offsets the potential effect. The role of this MAI deserves to be examined in more depth in a future study.

Theoretical and managerial implications

A certain number of important theoretical and managerial implications can be deduced from these results. From a theoretical perspective, this study fills a certain gap in the governance and management accounting literature.

First, it adopts a renewed angle to examine the presumed relationship between strategic board involvement and organizational performance. Given that this relationship is currently founded on somewhat contradictory conclusions, this study suggests that the conceptual distance can be reduced by taking into consideration an information dynamic, through the board’s strategic use of MAI, and including board effectiveness as an intermediate-level output. A holistic approach is proposed to conceptualize the simultaneous links among strategic board involvement, MAI, board effectiveness and organizational performance. A double-path mediation model is tested to empirically support to role of MAI and board effectiveness and reconcile disconnected streams of research.

Second, this study helps to integrate two disciplines of research that have developed in relative isolation. On the one hand, the governance literature, focuses on information outside the organization’s boundaries, that is, in the board of directors (Brennan et al., 2016), but does not always examine the MAI. The accounting literature, on the other hand, conceptualizes the use of MAI inside the boundaries of the organization by examining the coherence between organizational actors’ behaviors and decisions and the organization’s strategies and goals. However, a board of directors differs from the typical organizational setting in that it consists of executive directors and independent directors who do not have the same level of knowledge concerning the organization’s activities, or the same proximity to its day-to-day operations. Also, the board’s role differs from the top management’s role in that the former governs the organization whereas the latter manages it. Directors thus form a special group with different information needs. This study thus bridges the gap by examining the board’s use of three MAI to support the actions required for strategic plan oversight.

From a more managerial perspective, this study first highlights the importance of board of directors as a mechanism creating value for the organizations, not only through its fiduciary role concentrating on compliance, but just as importantly, and perhaps even more so, through its advisory role concentrating on strategy. The positive influence of board of directors on organizational performance should help to alter the perception held in some circles and by some top managers that the board is a necessary evil. This study also shows that the board’s contribution to organizational performance is reflected in its ability to be effective in its control and service role. In doing so, directors need to be fully aware of the importance of not only governing the organization well, but also governing themselves well as a group. Finally, this study could raise directors’ awareness of the potential of MAI. Regular reporting by top management to the board, in the form of information from the budget and performance indicators, is potentially useful for directors, not only to execute their compliance and accountability role, but also for their strategic and advisory role. The MAI is crucial to the strategic role expected of directors, particularly for periodic monitoring and questioning of the strategic plan. The strategic use of MAI helps board members become or remain strategically involved and contributes to improved effectiveness of the board as a work group.

Limitations and future research

Despite making noteworthy theoretical and managerial contributions, this study is subject to potential limitations in terms of internal and external validity.

First, for any proposed structural model, there is the possibility that different structural models tested with the same data may suggest different relationships between the latent constructs and reflect equivalent levels of goodness-of-fit (MacCallum et al., 1993). The potential existence of an equivalent model is problematic and is one limitation of the results reported here. Second, no clear evidence of causality can be established from the data obtained through cross-sectional analyses. That evidence should instead be considered to lie in the results’ compatibility with the theoretical arguments in this study and the relationships in the hypotheses. Even using a tried-and-tested methodology under rigorous conditions together with several statistical tests, the test results cannot be considered definitive. Third, the homogeneity of the sample formed from the data collection is itself a limitation, since only directors from private and listed Canadian firms completed the questionnaire, which means the profiles of the respondents have a certain degree of homogeneity. In addition, considering the convenience sampling approach used, the results cannot at this point be generalized to all boards of for-profit organizations.

Also, the size of the sample resulting from the data collection is a potential limitation. Although the sample size and the number of observations per parameter are acceptable, it would have been useful to have a higher response rate. It should be remembered, however, that board members are busy professionals with many demands on their time, and it is becoming more and more difficult to persuade them to participate in surveys of this kind. In addition, due to the difficulty in obtaining information regarding boards, as a single respondent was used. Relying on a single respondent is a limitation to this study, and future research should try to extend the results and add additional information by considering multiple respondents from the same board. Furthermore, although the overall structural model displays convincing goodness-of-fit indexes, the effects of variables on organizational performance could be perceived as somehow low for policy purposes. It is worth noting that the context of organizational performance is broad and complex. Corporate governance represents only one aspect of the organizational reality that might influence performance along with organizational capabilities, strategic considerations, operational aspects, risk management, organizational culture, to name a few. Lastly, although the conceptual model covers a broad range of control variables related to the organization and the board, other potential control variables could have been included, such as capital structure, CEO characteristics, and the age of the organization.

The results of this study open the door to several further areas of research. Additional research could include more qualitative work to add more nuance to the specificities of information produced by the three MAI considered, particularly the budget. A complementarity approach could also be considered, to understand links between the MAI themselves. Finally, it would be interesting to broaden the consideration of MAI applied to the board, for example by examining their role as influencer of top management behavior, and thus incorporate other MAI such as incentives.

Supplemental Material

Supplemental Material - Revisiting the impact of strategic board involvement on organizational performance

Supplemental Material for Revisiting the impact of strategic board involvement on organizational performance by Steeve Massicotte and Jean-François Henri in Journal of General Management

Footnotes

Acknowledgments

The useful contributions of the participants at the 2019 8e Atelier de recherche de l’Association de Contrôle de Gestion (ACG) are acknowledged. The support from the Collège des administrateurs de sociétés (CAS) and the Chaire de recherche en gouvernance de sociétés of l’Université Laval are also acknowledged.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this study.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this study.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.