Abstract

This article examines the evolving strategic choices of the Gulf Cooperation Council (GCC) states as they navigate renewable energy partnerships with two major global actors, namely the European Union (EU) and China, against the backdrop of the securitization of the fourth energy transition after 2022. The study situates Gulf decision-making within a transformed geopolitical context, where energy transition has become both an environmental imperative and a pillar of national security policy in Europe, China, and the Gulf. Using a comparative SWOT framework supported by original data on foreign direct investment, EPC contracting, and equipment supply, the analysis contrasts the EU’s technology- and regulation-driven model with China’s cost-competitive, rapidly deployable solutions. It explores how GCC states balance immediate needs for scalable, affordable green technologies, largely supplied by China, with future-oriented investments in European renewable markets to secure technology access and hedge against long-term hydrocarbon demand decline. The article also highlights the political, economic, and technological risks of overreliance on either partner. It concludes that the GCC’s green energy strategy reflects a broader balancing act in an era of great power rivalry, leveraging both EU and Chinese engagement to diversify partnerships, safeguard economic resilience, and maintain strategic flexibility in the era of global energy transition.

Keywords

Introduction

In recent years, international academic community has substantially increased its interest in studying the strategic partnerships between the Gulf Cooperation Council (GCC) member states and two major global actors, namely China and the European Union (EU), 1 paying specific attention to their cooperation in the field of renewable energy. Aisha Al-Sarihi (2025), Camille Lons (2024), Qi Wang (2025), Jonathan Fulton (2021), Li Chen Sim (Sim & Griffiths, 2024, 2025), and John Alterman (al-Sulayman & Alterman, 2023) highlight the evolving dynamics of these relationships, particularly as China emerges as a global leader in clean energy. By 2022, China’s investments in renewables reached $546 billion, outpacing the EU and U.S. combined, raising new questions about the triangulation of the Gulf’s interactions with China and Europe (Šekarić Stojanović & Zakić, 2024).

However, while recognizing the substantial contribution of recent research toward understanding the dynamics within this triangle, it is also important to acknowledge that many of these studies are motivated by a rather old understanding of the fourth energy transition, whereby it is treated as a purely economic process. Moreover, several studies remain narrowly focused, often examining only one dimension of cooperation between the GCC and China/EU, such as hydrogen cooperation with Europe or specific solar projects with China, without considering broader strategic trade-offs. Yet, the geopolitical context setting the boundaries of the energy transition discourse shifted dramatically after 2022 and this shift requires a more critical and broader approach. Previously, the attention on renewables had stemmed from the green agenda, advocated largely by the Europeans. As Russia’s 2022 invasion of Ukraine elevated energy security to the forefront of policy debates in Europe and beyond, for the first time, renewables came to be viewed not just as an environmental issue, but a pillar of national security. While the EU and China continue to expand their clean energy footprint in response to this new challenge, GCC states found themselves navigating between two competing green energy superpowers (Atlantic Council, 2024).

Against these rapid transformations, the purpose of this article is to explore how the GCC countries are navigating the pressures of the emerging energy “transition” order, with a particular focus on their interactions with the two major actors, the EU and China. The article leaves aside a third important strategic partner affecting the interests of the GCC hydrocarbon producers, namely the United States of America. This exclusion is due mainly to two reasons. First, the authors believe that, at current juncture, both the EU and China have emerged as more relevant partners in shaping the GCC’s transformation toward sustainable energy systems, and these two actors advocated this file in their recently flourishing engagement with the Gulf. Second, a detailed assessment of the evolving US role in Gulf energy geopolitics warrants a separate analysis, as it involves and coalesces with distinct strategic, political, and security considerations that extend beyond the scope of this article. Accordingly, the present discussion focuses exclusively on EU-GCC and China–GCC dynamics, comparing how the engagement with these two actors, each representing different models of global energy transition governance, affect the Gulf states’ strategic choices, energy security calculus, and economic diversification trajectories.

The article situates the triangular relationship within a broader trend whereby the fourth energy transition is increasingly securitized. 2 As understood by the authors, the fourth energy transition implies a systemic reconfiguration of the world’s energy production, distribution, and consumption patterns from fossil fuel–based systems toward low- and zero-carbon sources, with the overarching aim of ensuring long-term energy security under conditions of climate imperatives. It entails the decarbonization of energy supply chains alongside the diversification of energy mixes, technologies, and geopolitical dependencies to enhance the resilience, affordability, and sustainability of energy systems. In this context, the transition is not only a response to the need for reducing energy-related CO2 emissions and mitigating climate change, but also a strategic process to strengthen the reliability, accessibility, and sovereignty of energy supply while advancing broader developmental goals such as health, gender equality, and inclusive economic growth.

As pointed out earlier, one of the main changes that the conflict in Ukraine introduced to the new energy order was the securitization of the fourth energy transition. In line with the Copenhagen School of security studies, we understand securitization as process involving the transfer of a problem’s discussion from the sphere of ordinary political discourse to the realm of security issues, which empowers the relevant actors, predominantly the state or state elites, for the use of special/extraordinary measures (Buzan et al., 1998). In other words, securitization is “the move that takes politics beyond the established rules of the game and frames the issue either as a special kind of politics or as above politics.” (Buzan et al., 1998, pp. 23).

Recent research also started to underscore that the global energy transition is increasingly shaped by geopolitical risk transmission and financial market spillovers, rather than purely by technology and cost factors. Studies by Helmi et al. (2024) and Helmi et al. (2025) show that geopolitical shocks and global fear indices generate cross-market volatility and higher-order spillovers among MENA and global financial markets, directly affecting capital costs and investment confidence in renewable projects. For the GCC, whose partnerships with the EU and China involve large-scale financing and exposure to global supply chains, such spillovers translate into tangible vulnerabilities, including but not limited to project delays, fluctuating green technology prices, and financing uncertainty. As Lin and Zhang (2025) highlight, the geopolitics of critical energy minerals, which increasingly dominated by China, adds another dimension of strategic dependence. Thus, Gulf renewable cooperation with both Europe and China must be viewed within a broader framework of geoeconomic interdependence and risk contagion, where ensuring the resilience of energy transition requires not only diversification of partners and technologies, but also robust mechanisms for managing geopolitical and financial volatility.

The securitization of the fourth energy transition affected the Gulf region in at least three ways. First, leading oil producers like the UAE and Saudi Arabia doubled down on their own renewable investments to prepare for a post-oil world. Second, they faced a dilemma, as China, their top hydrocarbons customer, was on a path to accelerate its domestic energy transition, and produce most of the clean tech worldwide. While this trend will potentially reduce Chinese demand for Gulf oil, it also opens up new avenues for cooperation in renewables, hydrogen, and clean tech localization (DNV, 2024). Third, the GCC countries are trying to ensure that they will remain the “last man standing” at the hydrocarbon markets, that is, they will be able to sell their oil and gas resources as long as possible even if demand on them goes down. This strategy cannot be successfully implemented without introducing green technologies in the process of production and transportation of the Gulf hydrocarbons, particularly natural gas, which is considered as the “transition fuel” (Gürsan & de Gooyert, 2021). All three tasks are serious challenges for most if not all GCC member states. The only relative exception can be Qatar whose gas resources may be considered as a part of the ongoing energy transition, thus, allowing Doha to ignore the contemporary pressures for a longer period. Yet, even Qatar is developing certain elements of the green energy domestically, such as Ras Laffan and Musaieed solar power plants which are used by liquefied natural gas (LNG) plants to lower carbon emissions and maintain its competitiveness.

Meanwhile, China’s cost-competitiveness, state-backed financing, and familiarity with GCC governance models make it a more agile partner than the EU in many cases. Its firms are less selective and more willing to engage in large infrastructure deals, through no strings attached practices. Despite the ease of business and relative cost advantages, the China option is surrounded with several issues, including but not limited to geopolitical tensions arising from the return of great power politics, financial dependencies bred by Chinese business practices, controversial performance of the Chinese economy and limited tech transfer, which raise doubts about overreliance on China. Meanwhile, the EU, while often slower and more bureaucratic, offers technological depth, environmental credibility, and access to high-standards markets. For the Gulf, on balance neither partner is ideal on its own; hence, their goal is to balance partnership with both sides to maximize returns and enhance strategic flexibility (Alghannam, 2025; al-Sulayman & Alterman, 2023).

To evaluate these dynamics, this article employs a comparative SWOT analysis of the EU and China as potential partners for the GCC in renewable energy. While this framework cannot capture all nuances, it offers a structured way to assess the strengths, weaknesses, opportunities, and risks of each partnership. As such, it can provide insights that can potentially lay the groundwork for a more balanced and resilient green energy strategy in the Gulf (Kenton, 2025). The SWOT analysis is also preceded by an examination of data on foreign direct investments (FDI) from the EU and China in sustainable energy projects across the GCC member states. This section also explores the involvement of European and Chinese EPC (engineering, procurement, construction) contractors in these projects, as well as the dynamics of equipment supplies by different actors. The study further considers Gulf investments in green projects in Europe and China, as well as joint GCC–EU/China investments in sustainable energy in third countries.

The quantitative analysis in this study has certain limitations. Despite substantial efforts to gather information on these topics by such institutions as Columbia University and the European Council on Foreign Relations, 3 access to comprehensive data on GCC countries’ relations with China and Europe in the field of sustainable energy projects remains a challenge. The authors had to rely primarily on available open source data and official reports to construct an overall picture of Gulf–EU/China cooperation, though it is important to acknowledge it is impossible to compile all existing data. Nevertheless, the information collected is substantive and it will be indicative to identify key trends and address the primary research focus of the current study.

The Energy Security Doctrines of the EU and China after 2022 and the Interests of the Gulf Hydrocarbons Exporters

EU: Between Energy Security and Energy Transition

Before the start of the war in Ukraine in 2022, Russia was the European Union’s largest energy supplier, accounting for approximately 41% of gas imports, 26% of oil, and more than half of coal (Delivorias & De Martini, 2023). The EU’s sanctions against Moscow, coupled with the voluntary refusal of European companies to purchase Russian supplies, required urgent measures to replace these volumes. In May 2022, the European Commission presented the REPowerEU plan, which was essentially a comprehensive energy “reboot” strategy designed to eliminate dependence on Russian fossil fuels well before 2030. The plan outlined three main pillars: energy savings, accelerated development of renewable energy sources, and active cooperation with international partners to diversify import routes. Also in May 2022, the EU adopted a new External Energy Strategy, which emphasized the urgent need to conclude new supply agreements with alternative exporters (Delivorias & De Martini, 2023).

As a part of this strategic shift, the GCC countries had an opportunity to play a role in replacing the lost volumes of Russian energy. While in 2021 the total import of mineral fuels from the GCC to the EU was worth €25.1 billion, in 2022 it peaked at €65.5 billion and remained high at €58.4 billion in 2023. By 2024, fuel made up over 75% of the EU’s total imports from the region (Council of the European Union, 2025, February 3). Saudi Arabia, which had previously focused predominantly on Asian clients, became increasingly engaged with European oil refiners. In 2022, the Polish company Orlen brought Saudi Aramco on board as a strategic partner: the Saudis acquired a 30% stake in the Gdansk oil refinery and signed a long-term contract to supply between 200,000 and 337,000 barrels of oil per day (Koper & Banacka, 2022). Despite the fact that the deal had been in making long before the Russian invasion of Ukraine, its conclusion in 2022 could have never been more timely: the above-mentioned Saudi volumes partially replaced Russian oil, which Poland had entirely phased out. In July 2022, during the UAE President’s visit to Paris, a deal was signed whereby the Emirates would provide France with the necessary volumes of diesel fuel. This agreement became a symbolic gesture of support, allowing France to compensate for the loss of Russian oil products (Irish, 2022).

In the gas market, Qatar managed to maintain its position as one of the key suppliers of LNG to Europe. Historically focused on Asian markets, Qatar rose to become the second-largest LNG exporter to the EU in 2022 (after the U.S.), accounting for about 14% of total EU LNG imports (Zaretskaya, 2024). 4 In 2023–2025, Qatar’s share remained substantial, around 10% by value (European Commission, 2025). Qatari LNG cargoes were delivered to many EU countries, from Spain and Italy to Belgium and Poland, helping cushion the impact of Russian pipeline shutdowns. Other Gulf states, including the UAE and Oman, also offered their LNG to Europe (Rinke & Mohamed, 2022). Importantly, the GCC states were not just after increasing supply volumes. Indeed, the Arab Gulf monarchies sought to anchor long-term European demand for their energy resources by investing in European downstream infrastructure. The most vivid example is the aforementioned Saudi Aramco–Orlen case: beyond securing Poland’s long-term oil needs, the Saudi oil giant gained access to European processing and distribution capacities in Central Europe (Koper & Banacka, 2022).

Nevertheless, the current “hydrocarbon honeymoon” between the EU and the GCC countries is unlikely to last. Brussels’s climate policy remains firmly in place (Sergeeva, 2023). Today, the EU’s energy strategy reflects a balance between urgent diversification of energy sources for geopolitical reasons and a long-term commitment to decarbonization and shift toward clean energy as per the green agenda. The EU has clearly stated that despite the conjectural increase in gas and oil imports, its longer-term trajectory toward a green economy remains unchanged. This means that demand for fossil fuels in Europe will steadily decline. According to analyst projections, EU gas consumption could drop by 25% from 2021 levels by 2030 due to energy efficiency measures and fuel substitution (Jaller-Makarewicz, 2025). After 2026, the financial charges as part of the Carbon Border Adjustment Mechanism (CBAM) will be gradually introduced, effectively taxing the import of carbon-intensive products with a large carbon footprint. All of these developments send clear signals to GCC countries: if they want to remain relevant energy partners for the EU, they must adapt to these new conditions and manage the green transition.

As a compromise, European actors and their counterparts have been moving toward comprehensive “energy partnerships” which include both traditional fossil resources and cooperation in the clean energy sector. In this context, the EU is indeed trying to draw Arab exporters into its climate agenda by encouraging them to invest in emissions reduction. For example, in 2022, France and the UAE announced the creation of a joint climate fund to finance decarbonization projects (Irish, 2022). The same year, Germany and the UAE agreed on the supply of “low-carbon” ammonia to Europe for use in power generation trials, as well as on a partnership between Masdar and RWE to develop offshore wind farms in the North Sea (Rinke & Mohamed, 2022). Even before 2022, the EU and GCC countries started to develop cooperation in the field of imports and production of advanced turbines for maximum efficiency and future fuel flexibility. For example, in 2024, Saudi Arabia awarded contracts for new combined-cycle plants at Taiba and Qassim (two phases each) featuring the latest Siemens Energy HL-class gas turbines and GE Vernova H-class turbines (Gulf Construction Online, 2024). These projects are explicitly hydrogen-ready combined-cycle facilities, aligning with Saudi Vision 2030 goals. A key aspect of this Saudi cooperation with the EU companies is the focus on local manufacturing and joint ventures. For instance, GE Vernova established the General Electric Saudi Advanced Turbines (GESAT) facility in Dammam as a joint venture with Saudi state-owned Dussur in 2017. GESAT has since manufactured over 200 gas turbine modules for power plants across 10 countries and trained a cohort of young Saudi engineers in gas turbine technology. Moreover, GE Vernova recently acquired Dussur’s stake in 2024, making GESAT a fully GE-owned entity (Reuters, 2024, September 2). Similarly, Siemens Energy is expanding its Dammam Hub to produce core components of its turbines locally (Siemens Energy, 2025). The UAE has also embraced advanced gas turbine technology to upgrade efficiency and reduce emissions. A landmark project is at Emirates Global Aluminium (EGA) in Jebel Ali, Dubai, where a 600 MW power block built around a Siemens H-class gas turbine was completed in 2021 (Aluminium International Today, 2021). In summary, geopolitics and decarbonization have become the two key forces shaping the post-2022 interaction between the EU and GCC states. The first factor, that is, geopolitical urgency, drives closer ties and expanded trade in fossil fuels. The second, that is, climate agenda, pushes for the reformulation of this cooperation on a more sustainable basis. In the short run, both sides have benefited: Europe has bolstered its energy security, and the Gulf states have gained new market shares and enjoyed windfall revenues from oil and gas sales, which remained high in 2022–2023. However, several challenges have yet to be addressed, perhaps the most important being how the Gulf states will adjust themselves to Europe’s energy transition in the long-run, in such a way that they do not jeopardize their own interests.

China: Different Motives, Same Outcome

In this context, China may appear to offer a more favorable partnership for hydrocarbon-exporting GCC states than the EU countries. Yet, as in the European case, seen from the Gulf demand security perspective, the China–GCC energy relationship is marked by a fundamental duality. In the short term, China remains one of the largest and most stable consumers of Gulf oil and gas from the Gulf. However, concerns over national energy security and supply resilience are prompting Beijing to accelerate its domestic energy transition and underwrite mega projects to expand the renewable electricity generation capacity, which eventually raises questions about the long-term trajectory of Chinese demand for fossil fuels.

Beijing has significantly intensified the implementation of its energy security doctrine, shaped by recent global shocks ranging from the COVID-19 pandemic to escalating geopolitical tensions (Kemp, 2021). These developments have prompted a reassessment of China’s energy import strategy. The 14th Five-Year Plan (2021–2025) reinforced China’s dual goals. On the one hand, Beijing wants to peak CO2 emissions by 2030 and achieve carbon neutrality by 2060. On the other hand, the strategy continues to prioritize energy efficiency, pollution reduction, and above all reliable access to energy. Under these circumstances, China’s chronic shortage of easily accessible domestic oil and gas reserves makes it structurally dependent on energy imports. By 2019, China had become the world’s largest crude oil importer, satisfying 75% of its demand through external sources, and one of the largest natural gas importers, meeting over 40% of its consumption via imports. This dependency is viewed in Beijing as a critical strategic vulnerability to be avoided in the future (Kemp, 2021).

China’s energy doctrine rests on several interrelated pillars. First, it seeks to increase domestic production of oil and gas, particularly natural gas, and expand strategic reserves to mitigate supply shocks (Erickson, 2022). Second, it aims to diversify external supply sources and transit routes to reduce reliance on any single supplier or chokepoint. Third, Beijing promotes long-term contracts and investment partnerships to convert buyer–seller relationships into deeper strategic alliances. Finally, the doctrine tightly links energy security with the transition to renewables, framing clean energy development as essential to reducing dependence on fossil fuels over the long term, without jeopardizing short-term supply security (Calabrese, 2025).

The global energy turbulence triggered by Russia’s invasion of Ukraine in 2022 further reinforced these principles. In response, China accelerated its efforts to build a resilient, multi-vector energy architecture. On the one hand, it pursued an aggressive policy with hydrocarbons, ranging from increased imports of discounted Russian oil to record long-term gas contracts with Middle Eastern suppliers. On the other hand, China accelerated its expansion plans in the renewables, which destined it to emerge as the worldwide leader in investments and capacity generation.

In this evolving framework for China’s energy diplomacy, the relations with the Gulf states occupy a critical position: the GCC countries, on the one hand, remain the main supplier of hydrocarbons to China, and, on the other, they emerge as important recipient of the Chinese green technologies and investments necessary to develop both their own sustainable energy resources and domestic technological base to develop it.

Moreover, while Gulf producers have traditionally ranked among China’s largest energy suppliers, their role has undergone a qualitative shift since 2020. Beijing is now embedding oil trade within long-term strategic partnerships, emphasizing integrated cooperation across the entire value chain—from upstream production to refining and distribution. By the mid-2020s, Gulf states accounted for over 40% of China’s crude oil imports (Calabrese, 2025). Saudi Arabia consistently competes for China’s top supplier position, while Oman, the UAE, and Kuwait also rank among China’s primary energy partners (Troderman, 2024). For both sides, this trade is seen as more than commercial, since it is surrounded by national security considerations (Calabrese, 2025).

The transformation from transactional trade to strategic partnership is especially evident in the China–Saudi Arabia energy relationship. For instance, the Yasref refinery in Yanbu, a joint venture between Sinopec and Saudi Aramco launched in 2016 with a 400,000 bpd capacity, was followed by a new framework agreement in 2025 to expand processing capabilities (Ministry of Commerce of the People’s Republic of China, nd). Meanwhile, Saudi Aramco began investing in Chinese petrochemical and refining infrastructure, including major projects on China’s eastern coast, thereby securing long-term crude supply contracts. The UAE has followed a similar pattern: Chinese firms have taken equity stakes in ADNOC concessions, and built key infrastructure like the Habshan–Fujairah pipeline, which enables the UAE to bypass the Strait of Hormuz for exports (al-Sulayman & Alterman, 2023).

Liquefied natural gas has also become a central pillar of China’s energy strategy. Moreover, as a cleaner transition fuel, LNG aligns with China’s dual goals of lowering emissions and enhancing security. Since 2020, China has significantly expanded LNG cooperation with Gulf states, particularly Qatar, the world’s leading LNG exporter. Following the global gas supply crisis of 2021–2022, China has sought to lock in long-term Qatari gas deliveries through multi-decade contracts.

In 2022, China imported approximately 18 million tons of Qatari LNG, representing over a quarter of its total LNG imports and 22% of Qatar’s global exports. In November of that year, QatarEnergy and Sinopec signed a historic 27-year supply agreement, which is the longest in industry history, marking a shift toward guaranteed, long-term cooperation. Interestingly, the deal not only included the purchase of LNG by China, but implied Chinese investments into the expansion of the Qatari LNG production facilities (Downs et al., 2023). A similar deal followed in 2023 between QatarEnergy and CNPC, covering 4 million tons annually and including joint participation in the North Field East expansion project. These agreements reflect China’s broader strategic shift away from spot market exposure toward energy security through long-term contracts and investments in the main suppliers (Downs et al., 2023).

However, hydrocarbons alone are increasingly insufficient as a long-term foundation for China–GCC energy relations. Much like the EU–GCC partnership, albeit for different reasons, China’s evolving strategy introduces new elements. Having studied the vulnerabilities exposed in Europe’s energy dependency on Russian gas, Beijing is determined to avoid excessive reliance on any one supplier or region, even the GCC. Since 2022, Chinese imports from alternative exporters, most notably Russia and, occasionally, Iran, have grown significantly. Western sanctions on these suppliers have allowed China to acquire discounted oil, enabling it to lower the average cost of its energy imports (Reuters, 2025, January 20). By 2024, Russia had overtaken Saudi Arabia as China’s top oil supplier, while Saudi exports to China fell by 9% to 78.6 million tons. In response, Gulf producers have begun offering China more favorable pricing and investment terms, seeking to preserve their market share amid growing competition (Reuters, 2025, January 20).

Moreover, China, mirroring the Western trends, also went through a securitization of energy transition in response to the new geopolitics of the post-2022 energy environment, which has catalyzed its leadership in renewable energy deployment. In 2022–2023, China surpassed the EU in both installed capacity and growth rate in renewables. For China, the shift toward clean energy is driven not only by climate concerns but also by its ambition to reduce strategic vulnerabilities tied to fossil fuel imports. According to current projections, China’s renewable energy share is expected to rise from 30% in 2024 to 55% in 2035 and 88% by 2050. Oil demand is forecast to peak by 2027 and decline by half by mid-century, substantially reducing China’s need for imported hydrocarbons (DNV, 2024).

These developments naturally are turning China into the production leader of equipment and materials needed globally for the sustainable energy development. Even on the eve of the Russian invasion of Ukraine, China accounted for 80% of solar and over 60% of wind components production in the world. “More specifically, China hosted 79% of global polysilicon capacity, 97% of wafer manufacturing and 85% of cell production” (Sim & Griffiths, 2025). Currently falling production cost of this equipment and materials only strengthen their competitiveness at the international market against European or American equivalents, and according to most projections, China is destined to lead in decarbonization globally.

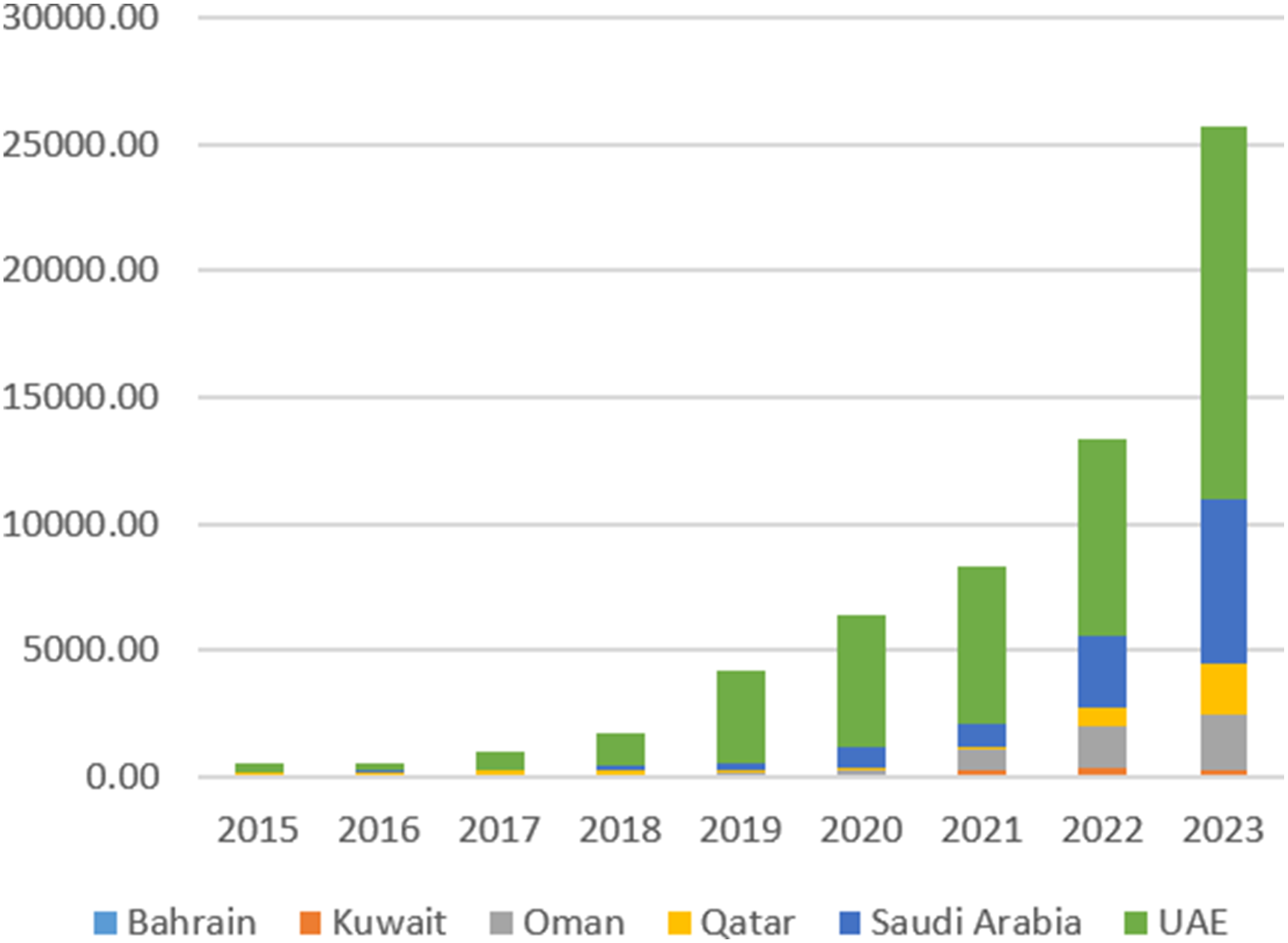

As China’s decarbonization progresses, hydrocarbons will gradually lose their centrality in China–GCC bilateral relations, opening up room for renewables and alternative energy as focal points of cooperation, including joint ventures in third markets. Recognizing the shifting grounds, Gulf states are increasingly engaging with China in renewable energy partnerships as well. While being latecomers to the race for sustainable energy resources development, in recent years, the Arab monarchies of the Gulf managed to achieve quite a progress (see Appendix 1, Graph 1). It comes as no surprise that to ensure the rapid growth of power generation capacities they need to rely on affordable Chinese equipment. As argued by Sim and Griffith, “China-based companies play very significant roles as suppliers of solar and wind equipment to the Gulf. In 2022 and 2023, for instance, the UAE imported 99.1% and 98.8% of its solar modules from China; comparative figures for Oman were 78.6% and 83.5%” (Sim & Griffiths, 2025). Chinese firms such as Jinko Solar and Huawei are involved in constructing major solar projects in the UAE and Saudi Arabia (Lons, 2024). Likewise, Oman has attracted several Chinese FDI since 2022 to establish local manufacturing in emerging energy sectors. These projects involve joint ventures or agreements between Chinese companies and Omani entities to build factories for batteries, electrolyzers, and solar photovoltaic modules. For instance, Chinese battery materials firm Hunan Zhongke Electric Co. Ltd. announced plans in mid-2025 to invest in a large lithium-ion battery anode materials factory in Oman (Yicai Global, 2025, June 5). In August 2025, United Engineering Services (UES) of Oman signed a Memorandum of Understanding with China’s Sungrow Hydrogen to establish a local facility for manufacturing hydrogen production equipment (Omanet, 2025, August 4). Moreover, Chinese solar manufacturer Hainan Drinda New Energy Technology teamed up with the Oman Investment Authority (OIA) in 2024 to launch Oman’s first photovoltaic cell production plant (Yicai Global, 2024, June 14).

Ultimately, this multi-tiered cooperation is consistent with China’s comprehensive energy security doctrine, one that combines short-term fossil fuel stability with long-term strategic investment in the “energy of tomorrow.” For the Gulf states, aligning with this model offers continued access to Chinese markets and technologies, while laying the foundation for sustained relevance in a post-oil global economy (al-Sulayman & Alterman, 2023).

The EU, China, and GCC Green Energy Partnerships: Political Momentum vs Practical Realities

Europe is a Window to the Future While China Is a Way to Live Today?

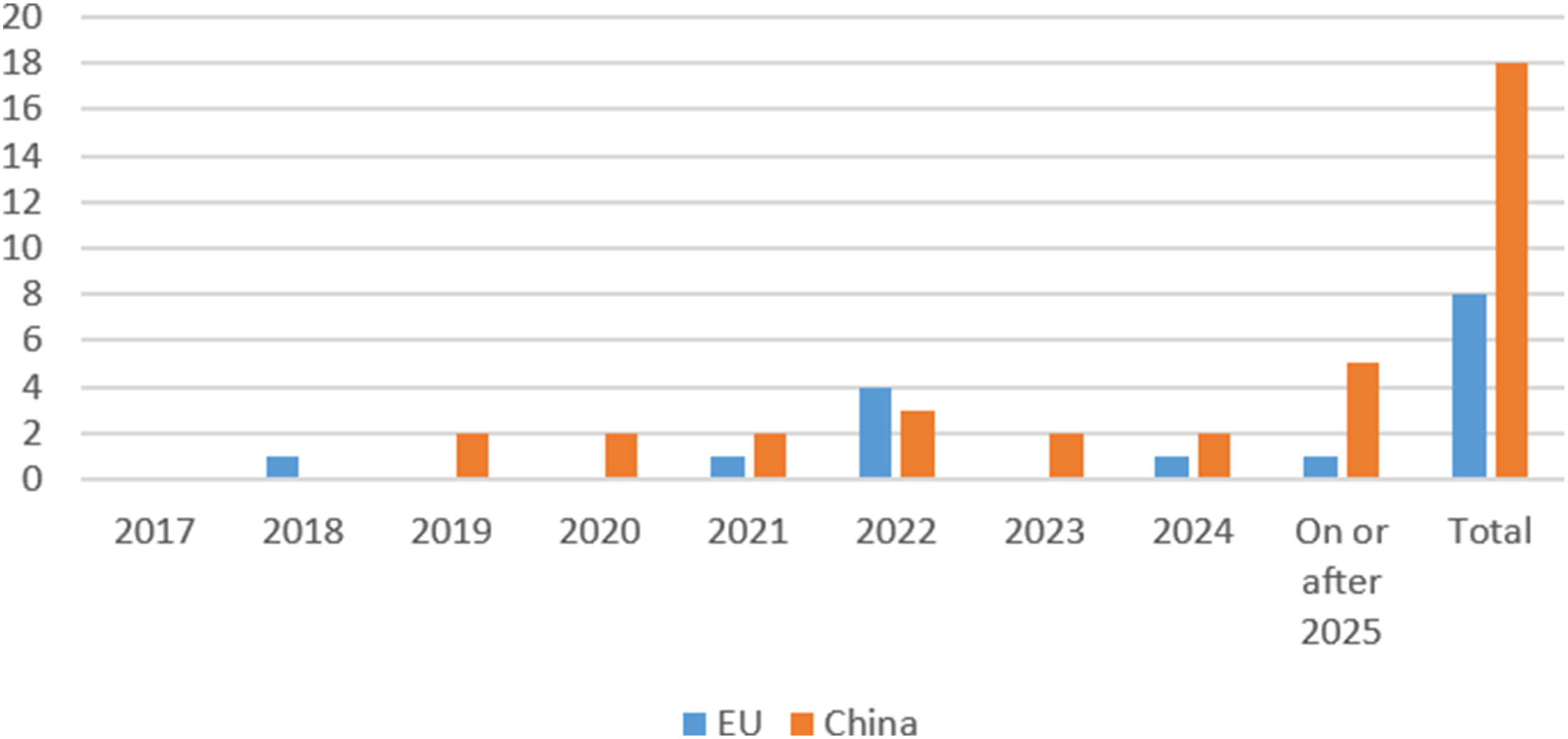

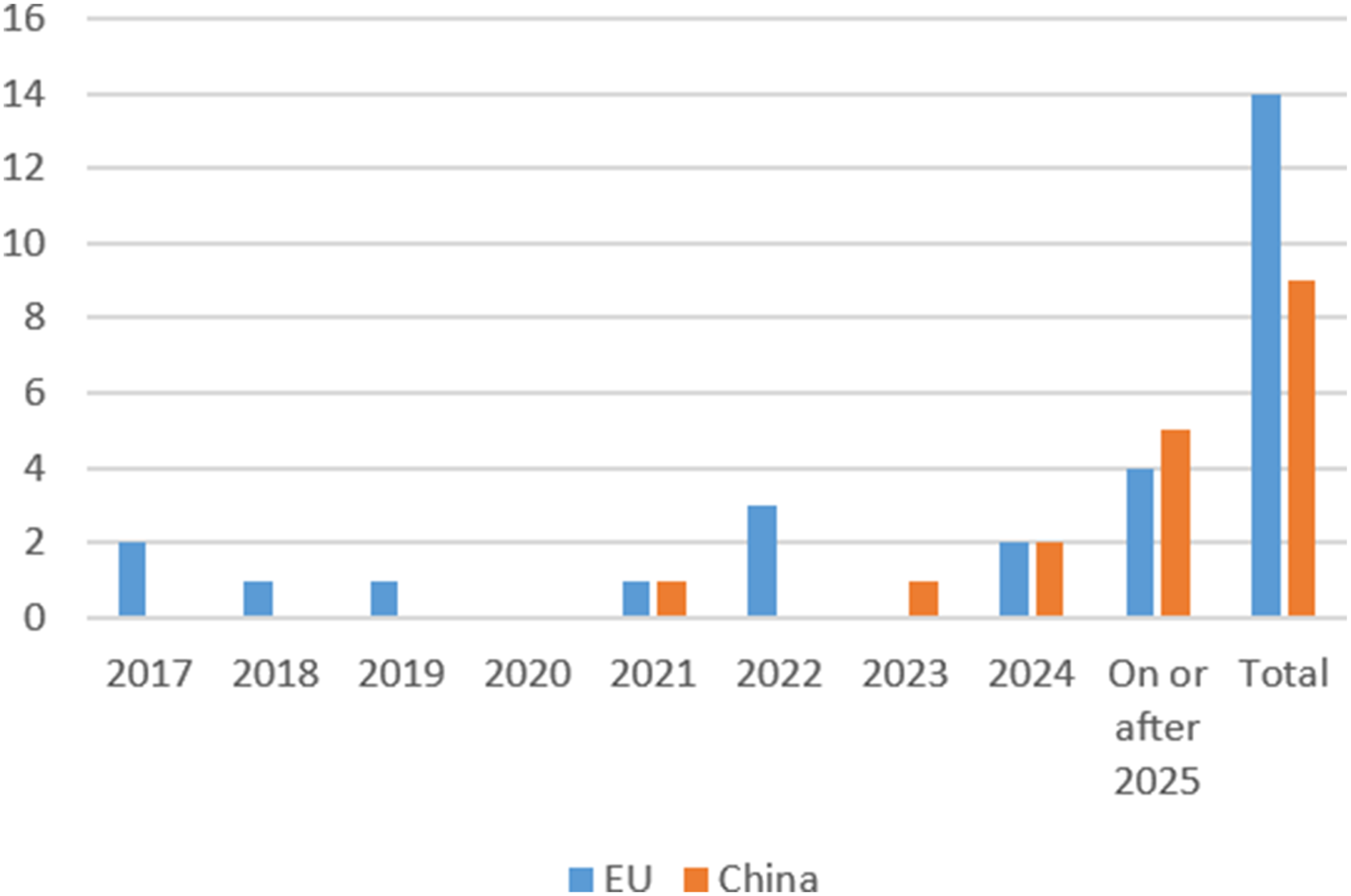

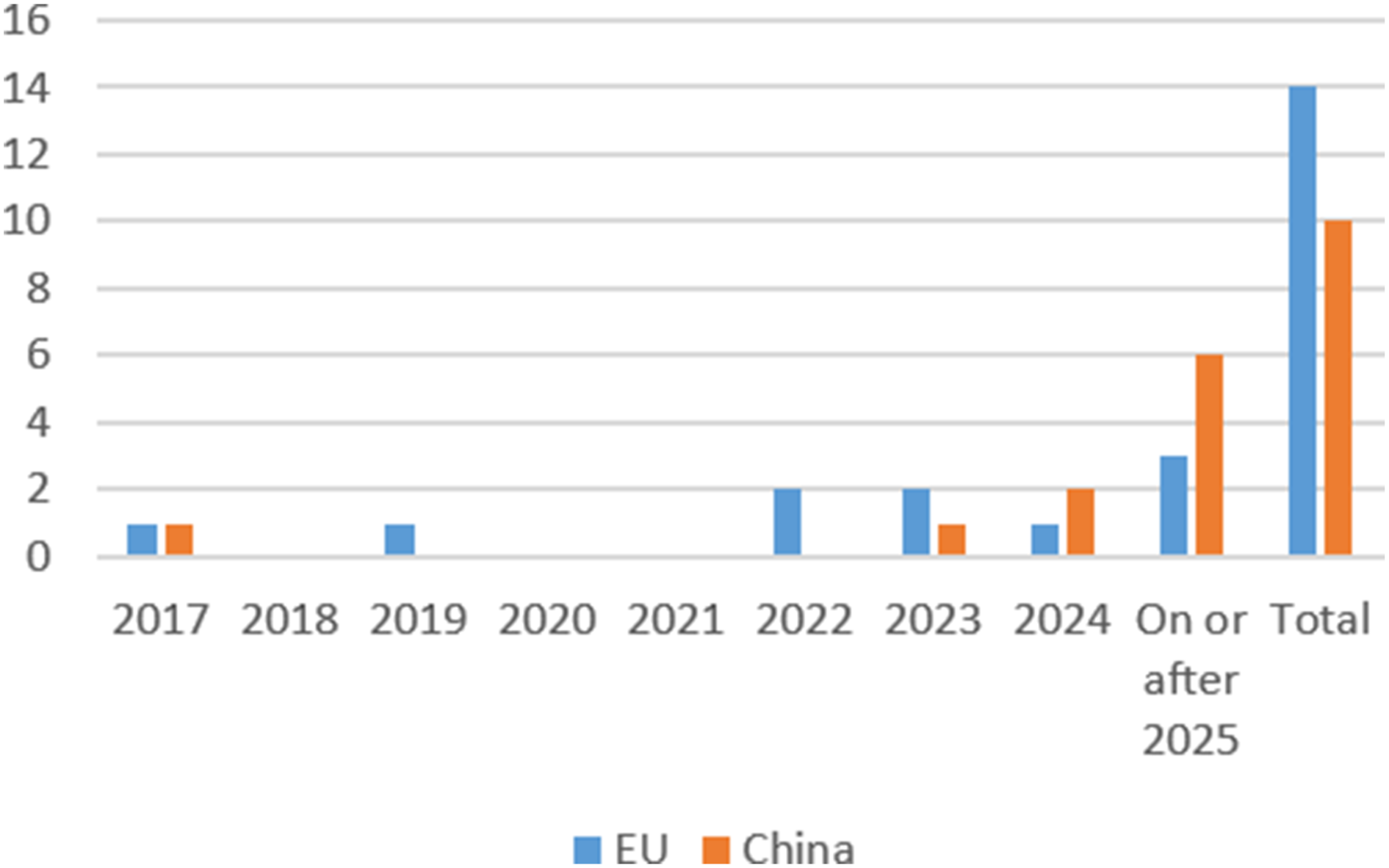

As previously noted, in recent years, analysts have been actively discussing China’s growing dominance as an external partner for the GCC countries in the development of sustainable energy resources. However, a more detailed analysis of the situation reveals that it is still premature to consider the Gulf states as a Chinese domain. An examination of the involvement of European and Chinese companies in the development of renewable energy in the GCC as investors, EPC contractors, and equipment suppliers offers a more nuanced picture whereby each of the two global actors, that is, the EU and China, has their own niche (see Appendix 1, Graphs 2–4).

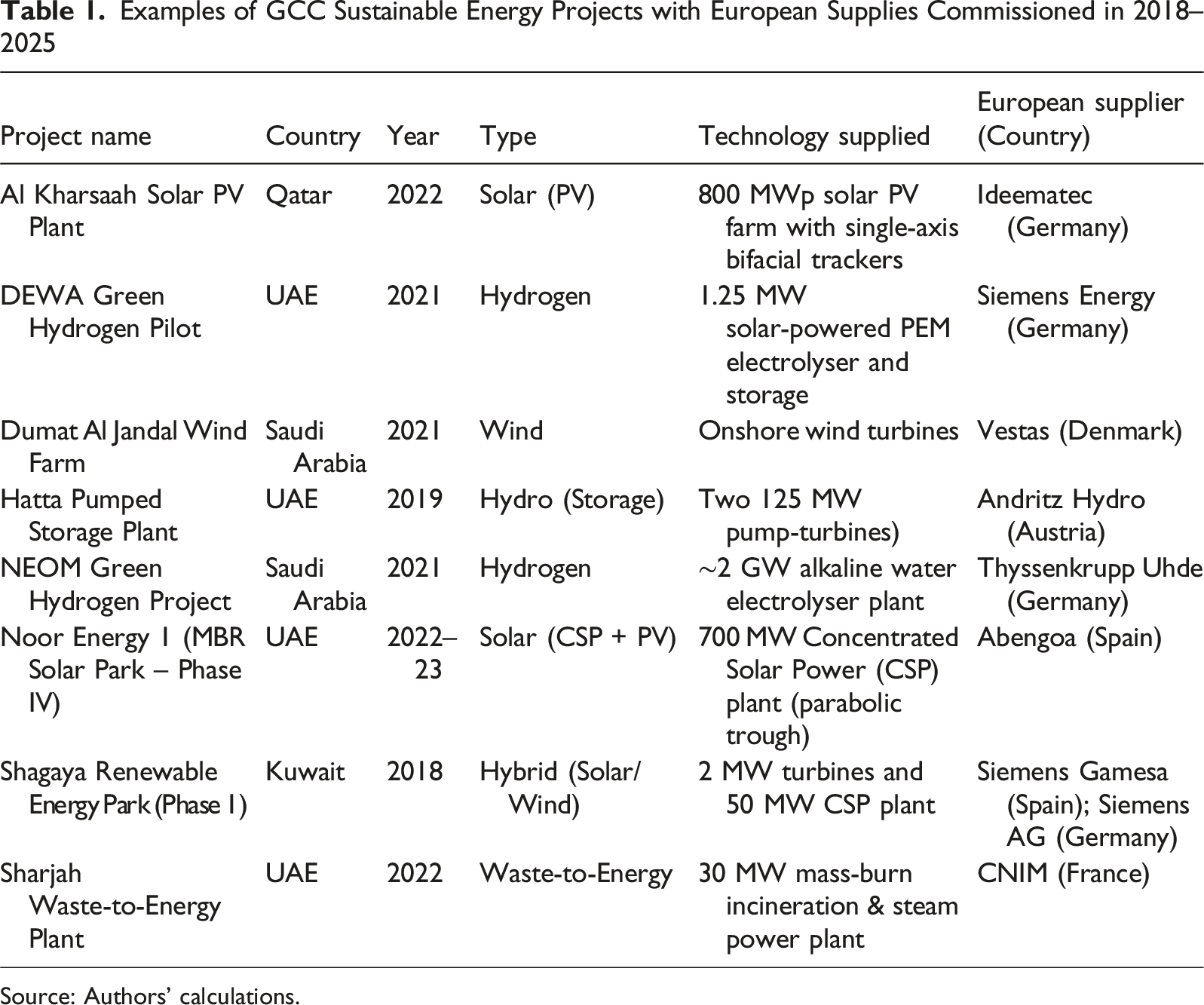

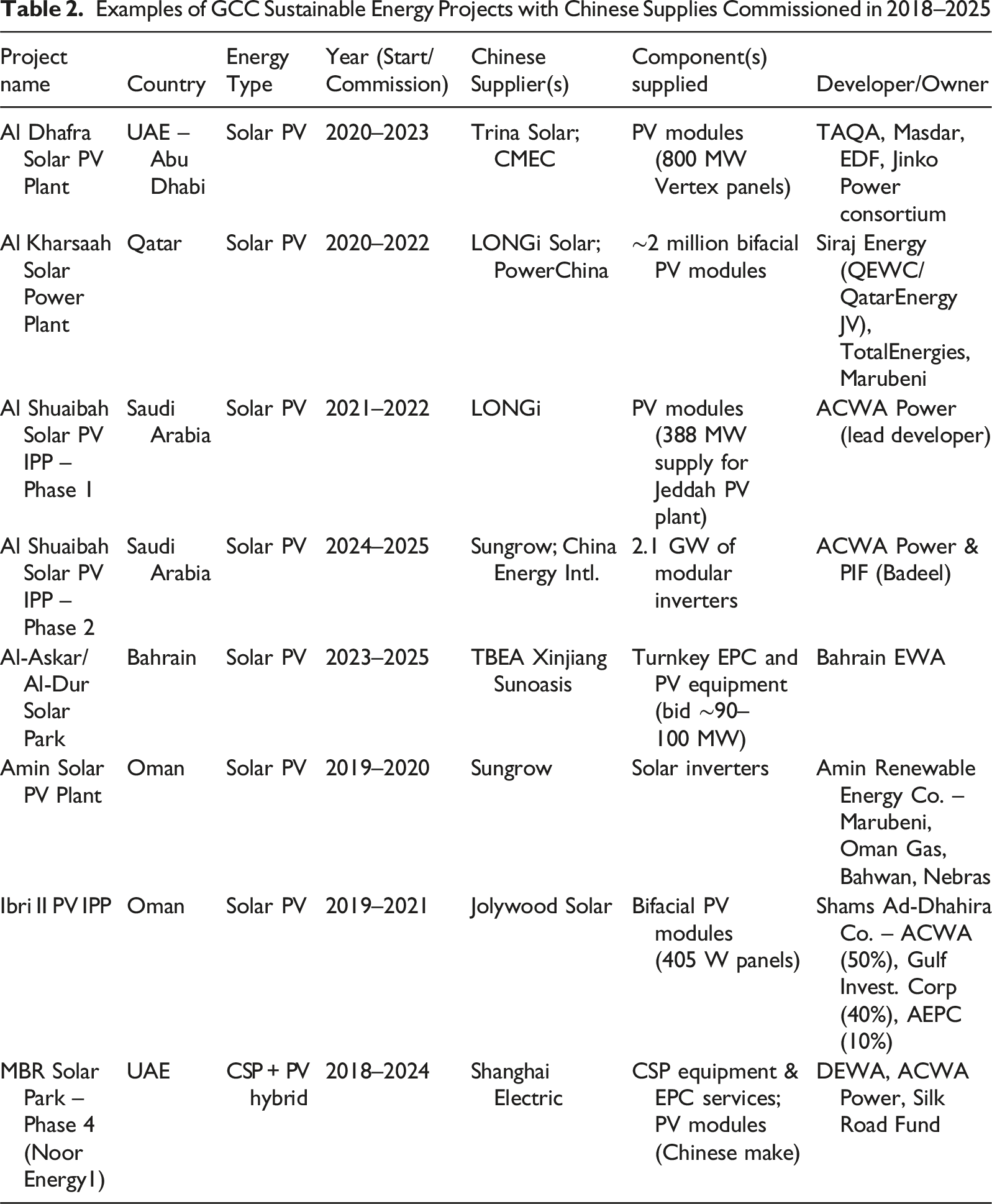

Beijing undoubtedly outpaces the EU in its role as an equipment supplier, which, as mentioned earlier, is due to its objective dominance in this segment of the global market (see Appendix 1, Graph 2). Yet even here there are nuances: European companies have occasionally supplied more technologically sophisticated equipment or products that fall outside of the typical range of Chinese exports list (see Appendix 2, Tables 1 and 2).

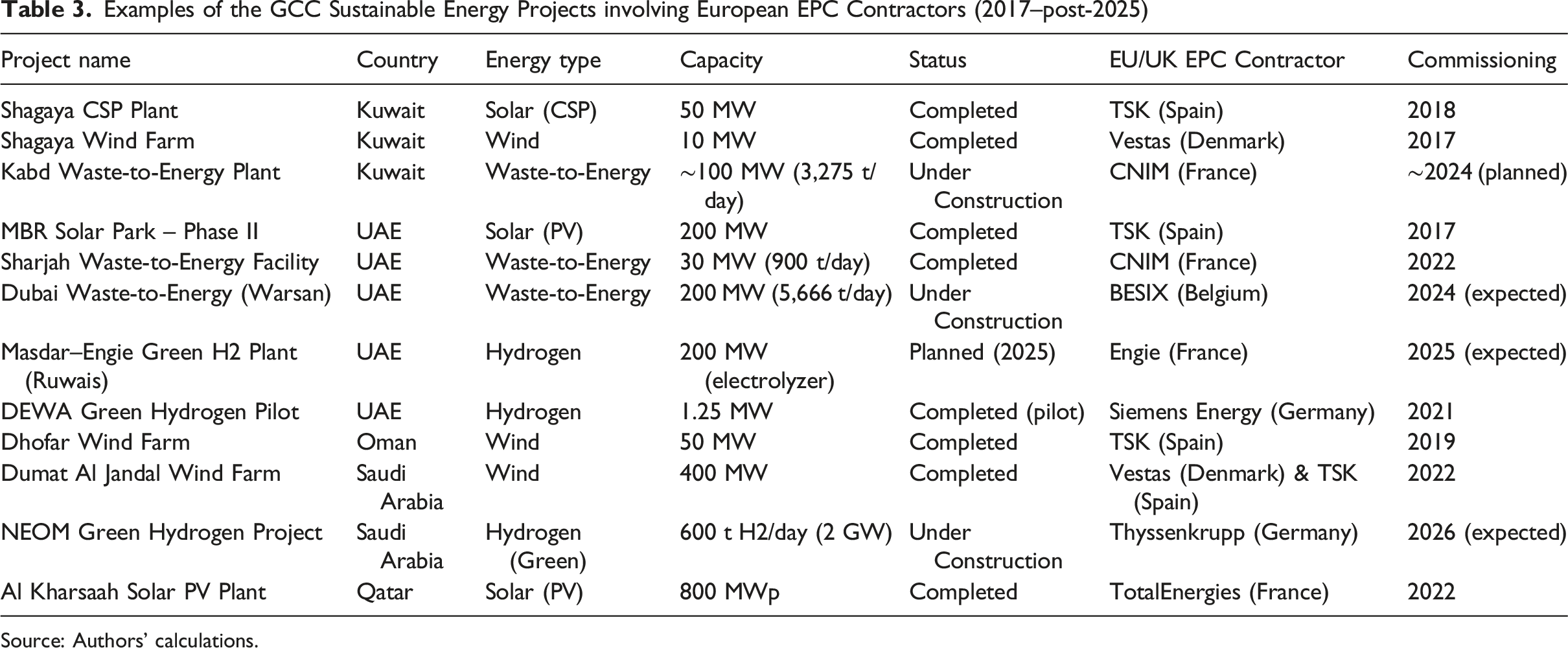

In terms of bilateral investments and EPC contracting, China is only recently taking the lead, and it remains to be seen whether it will be able to consolidate a dominant position (see Appendix 1, Graphs 3 and 4). Similarly, Beijing has an edge in areas where it has advantage in cost and manufacturing experience such as in solar and wind power. China may as well take over Europeans in product segments where it is less concerned than European players about the emergence of future competition from the GCC states themselves, since the latter is also seeking to prioritize the development of local technological capabilities as part of their vision plans. In all other areas, European firms can be even preferred by the Gulf actors, especially where cooperation involves advanced technologies or work in sectors whose development lies on the fringe of the current day and future (e.g., the development of hydrogen technologies) (see Appendix 2, Table 3).

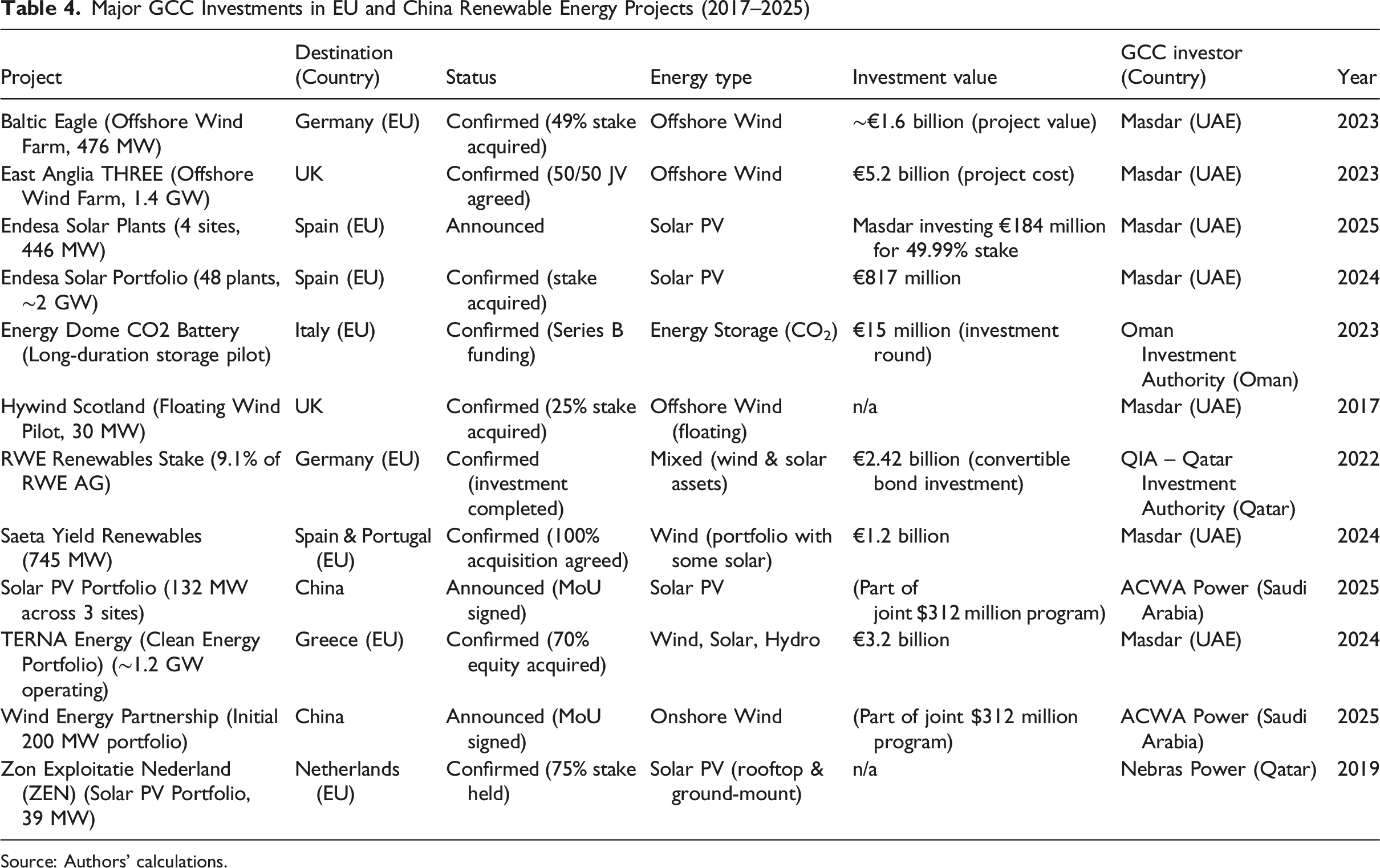

Of particular interest is the dynamics of investments by GCC countries in sustainable energy projects in the EU and China, as well as in joint projects located in third countries. In the latter case, the logic followed by the Arab monarchies of the Persian Gulf mirrors their behavior in the domestic market. When investing in the development of renewable energy projects in third countries, considering that they lack the necessary technologies and manufacturing base, countries like the UAE and Saudi Arabia turn to Chinese suppliers and constructors (Sim & Griffiths, 2025). In the realm of joint investments, the Gulf countries so far have more experience of cooperation with European partners, while cooperation with China is only a recent trend which may gain traction over time (see Appendix 2, Tables 5 and 6 further down).

When it comes to Gulf investments in the EU and China, the situation is even more telling: unlike in the traditional oil and gas sector, GCC countries are in no rush to invest heavily in renewable energy projects in China, while they are actively doing so in Europe (see Appendix 2, Table 4). This behavior can be explained by a number of factors. First, investments in Western companies allow Gulf countries to gain access to advanced technologies. Second, unlike China, where the decline in demand for oil and gas remains a distant and, so-far, largely hypothetical scenario, the EU’s transition to new energy sources and the reduction in hydrocarbon demand appear to be an objective reality. In this context, investing in European renewable energy projects serves as a form of risk hedging against future profit losses. Last but not the least, in the case of China, investing in renewables may, on the contrary, run counter to the interests of the GCC oil and gas producers by accelerating the onset of a new energy era.

In other words, the Gulf’s cooperation with Europe is driven by considerations of the future, whereas its engagement with China is shaped by the needs of the present. That said, any discussion of the slow progress in GCC investments in China’s renewable energy sector should still be framed with the words “for now.” The process of mutual integration, though gradual, is indeed underway. Thus, the most prominent player is Saudi Arabia’s ACWA Power. In December 2024, ACWA Power announced its entry into China’s renewable energy market with a portfolio exceeding 1 GW of solar and wind energy projects. These projects, located across several Chinese provinces, will be jointly owned by ACWA and leading Chinese industry players. By the end of 2025, ACWA plans to increase its installed capacity in China to 1.3 GW, and by 2030, to invest up to $50 billion to create 20 GW of renewable capacity and green hydrogen production facilities (El-Shaeri, 2024). The UAE’s Masdar has also announced plans to acquire stakes in solar power plants in China to capitalize on the growth of this market. In 2024, Masdar and the Silk Road Fund signed an agreement to jointly invest up to 20 billion yuan ($2.8 billion) in renewable energy projects globally, including potential ventures within China, although, so far, these intentions are staying only on paper (Roy, 2024). Yet, the investment flows can be potentially bidirectional. It is also worth noting innovative projects, such as Chinese companies’ involvement in Gulf states’ implementation of energy storage systems. For example, in 2023, China’s VRB Energy supplied a large vanadium redox battery system for a solar farm in the UAE. Conversely, Gulf funds are investing in Chinese climate startups and research. Qatar is co-financing R&D to improve solar panel efficiency in cooperation with Tsinghua University. Thus, there are signs that cooperation between China and the GCC could cover the full spectrum of green energy, from capacity building in solar and wind power stations to advanced manufacturing and development of hydrogen economy.

GCC–European Union: Green Energy Partnership in Principle and Practice

As mentioned earlier, Europe’s appeal is largely defined by its clear institutional framework and forward-looking orientation. After February 2022, the political dialogue between Europe and the Arab monarchies of the Gulf intensified, and by 2023–2024, the EU began to view the Gulf not merely as a fossil fuel supplier, but also as a prospective partner in the global energy transition. This strategic shift was institutionalized through several key initiatives and policy documents. The European Commission’s 2023 External Energy Strategy explicitly recognized the Gulf states as pivotal partners, citing their substantial hydrocarbon reserves alongside their expanding clean energy capacities. The culmination of this growing political engagement was the first-ever EU–GCC summit, held in Brussels on 16 October 2024, with the participation of senior leaders from both blocs. The summit’s joint communiqué emphasized intentions to deepen cooperation in energy security, efficiency, renewables, and hydrogen, while underscoring the need to ensure global energy market stability. In essence, a comprehensive political framework was set in the making to bridge traditional energy security priorities with the imperatives of climate action (Levesque, 2024a, October 18). In 2024, Sharif Al Olama of the UAE Ministry of Energy also underscored that a close partnership is forming between the EU and GCC in two critical areas: climate mitigation and sustainable economic transition. In this way, the strategic priorities of both sides align to support deeper cooperation in the green energy domain (Levesque, 2024b).

In recent years, this cooperation has become more concrete through joint initiatives and projects targeting renewables, decarbonization, and clean technologies. The EU–GCC Clean Energy Network, launched in the 2010s, facilitated early collaboration on solar and wind power, energy efficiency, and emissions management. In August 2023, this cooperation was elevated through a new 3-year initiative, “EU–GCC Cooperation on Green Transition,” funded by the EU. The project aims to create a shared platform for exchanging expertise, promoting technology transfer, and encouraging European companies to work with Gulf counterparts, particularly in climate policy, hydrogen, and sustainable urban development (European External Action Service, 2024a, April 18).

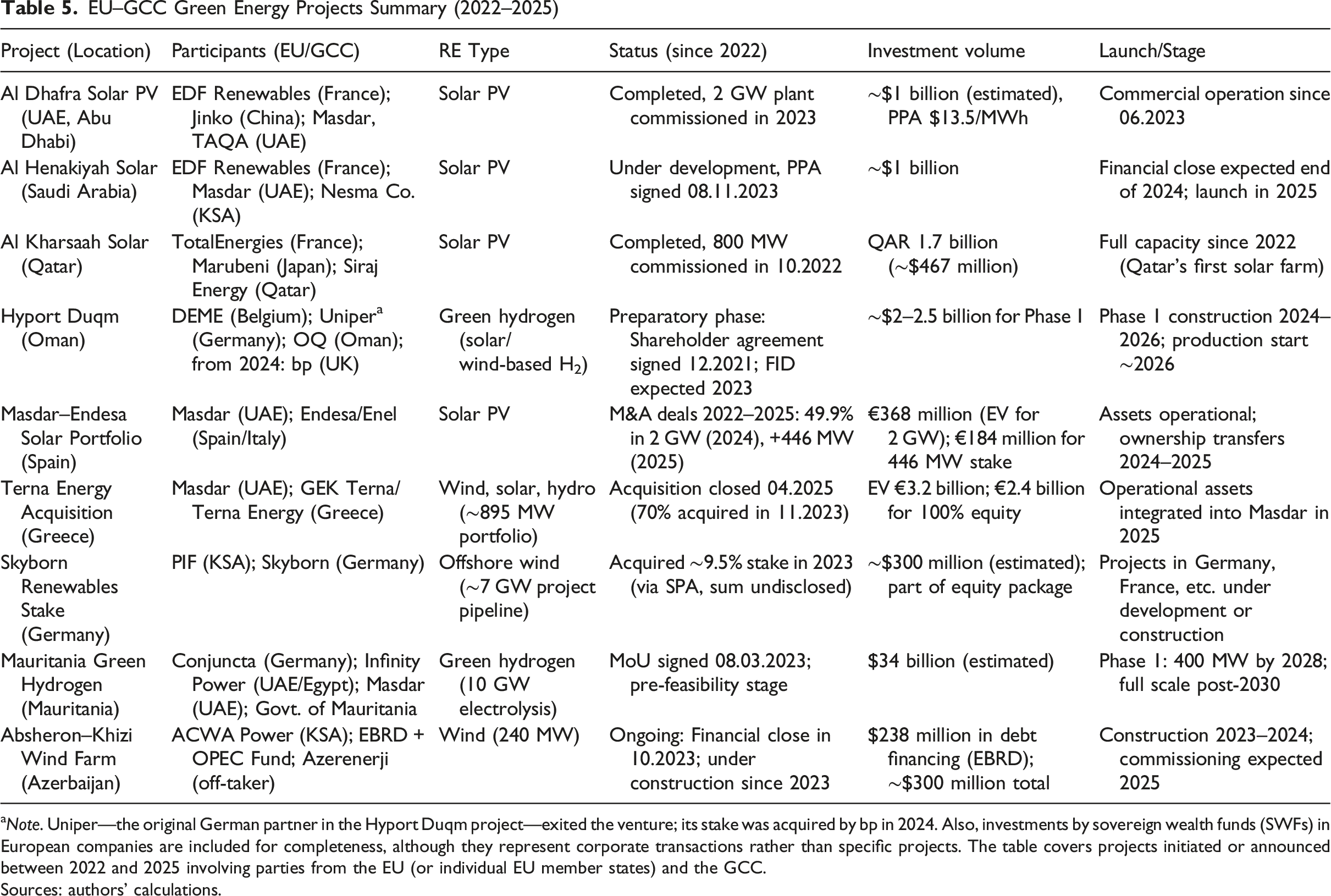

Beyond institutional dialogue, specific joint investments and commercial projects are emerging (see Appendix 2, Table 5). European companies are active in renewable energy developments across the Gulf, while Gulf sovereign wealth funds are acquiring clean energy assets in Europe. For example, Siemens is supplying hydrogen technology for the UAE pilot projects, and Eni is partnering in solar initiatives in Algeria and Oman. Masdar, the UAE’s state-owned renewable energy company, is especially prominent in this field, through investments in solar and wind farms not only in the Middle East but also in Spain, Greece, the UK, and elsewhere. In 2023, Masdar acquired a stake in Spanish solar plants and entered Greek firm Terna Energy’s capital. These investments align with the EU’s Global Gateway strategy, which seeks international partners for green transition (European External Action Service, 2024b).

Technology transfer is also a vital element. European companies are supplying critical components for major renewable projects in the Gulf, such as Thyssenkrupp Nucera’s electrolyzers for the $8.4 billion green hydrogen facility in Saudi Arabia’s NEOM (Petrova, 2023). ACWA Power, Saudi Arabia’s renewable energy giant, has partnered with Denmark’s Topsoe on CO2 capture and Italy’s Snam on exploring hydrogen exports to Europe (al-Mosalam, 2025). These examples illustrate a synergistic model in which the EU contributes technology and expertise while the Gulf provides capital, infrastructure, and demand. An important trend is joint EU–GCC investment in third countries, particularly across Africa and Asia. These projects combine EU technology and standards with Gulf financial resources to support clean energy access and future green fuel supplies for Europe.

Flagship green energy projects since 2022 span solar farms in the Gulf, Gulf capital flowing into European renewables, and emerging hydrogen ventures in Africa and Asia (see Appendix 2, Table 5). These initiatives support Europe’s decarbonization goals while helping the GCC diversify for the post-oil era. In coming years, an expansion of green hydrogen, offshore wind, and interconnectors is expected, deepening the strategic dimension of this partnership (Procopio & Čok, 2024).

Meanwhile, European commercial banks have become key financiers of large Gulf renewable energy projects since 2022. Thus, BNP Paribas and Crédit Agricole were among the six lenders providing $600 million in project financing for Abu Dhabi’s 1.5 GW Al Ajban solar PV plant, alongside HSBC, Standard Chartered, and others (Norton Rose Fulbright, 2024, April 30). Collectively, European commercial banks are providing long-tenor loans and expertise for Gulf mega-projects in solar, wind, and green hydrogen, ranging from NEOM’s futuristic hydrogen venture to UAE’s Al Ajban and Oman’s Manah solar farms (Muscat Daily, 2024, January 13). European public financial institutions and export credit agencies are also increasingly supporting Gulf renewable initiatives through risk mitigation, diplomatic agreements, and third-country collaborations, although multilateral lenders like the EBRD and EIB have only a limited direct footprint in the wealthy GCC states. However, key challenges remain before full scale cooperation and expansion of trade relations. The commercial viability of large-scale clean energy exports from the Gulf to Europe is still uncertain. Green hydrogen remains costlier than gray hydrogen, and competitiveness depends on scaling, cheaper renewables, and supportive infrastructure. The EU is introducing support mechanisms, such as Carbon Contracts for Difference and the Innovation Fund, with a target of importing 10 million tons of green hydrogen by 2030. But if demand underperforms, or if domestic or U.S. production proves cheaper, Gulf suppliers may struggle to secure buyers in the European markets (Cantini, 2023).

Energy price volatility also shapes the prospects of cooperation between the parties. High oil prices provide Gulf states with capital for green investments but reduce pressure for transition. Likewise, low prices could delay EU incentives for decarbonization, and scuttle capital accumulation in the Gulf, which could be channeled to green investments. Predictability is thus essential, requiring policy coordination, including through the EU–OPEC dialogue (Levesque, 2024a, October 18).

Technical and regulatory barriers persist. For instance, Gulf solar projects face challenges from extreme heat and dust. Hydrogen electrolysis is costly due to water desalination. Transporting clean energy, via interconnectors, hydrogen pipelines, or liquefied products, requires massive investment and political stability. Moreover, EU regulations (CBAM, delegated acts, hydrogen rules) impose high environmental and compliance thresholds. GCC states must align their standards and legal frameworks to gain access, yet this alignment is often slow or economically unfeasible (Levesque, 2024a).

Finally, competition for green markets is intensifying. Asian economies, China, India, Japan, South Korea, offer larger and less-regulated alternative markets. If entry into the EU markets becomes too burdensome, Gulf exporters may reorient toward Asia. Similarly, Europe is diversifying its own supply sources of green energy whereby North African or Mediterranean producers, for instance, are emerging as potentially more favorable alternative suppliers (TRENDS Research & Advisory, 2025).

Despite a dynamic political framework, implementation often lags. Since 2022, numerous joint plans have been announced, yet investment projects remain limited in scale. Much activity remains at the expert dialogue and institutional support level, with major infrastructure developments progressing slowly. In short, while political rhetoric emphasizes the emergence of a “green bridge” between Europe and the Gulf, turning this into a robust investment alliance will require addressing regulatory mismatches, aligning economic incentives, and developing credible, long-term demand guarantees. Only then can the EU–GCC green partnership evolve from paper into practice.

GCC–China: Drive and Determination

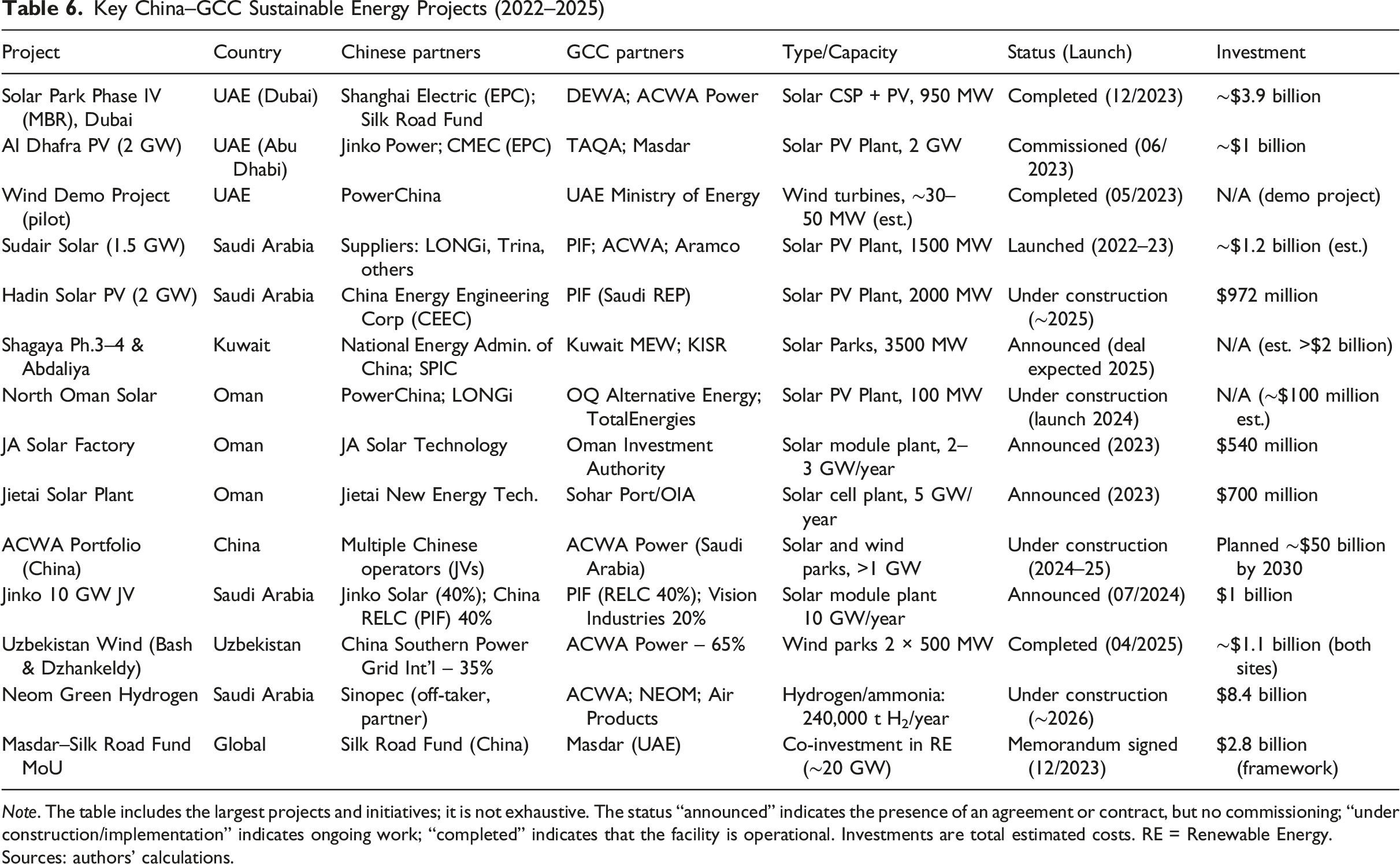

The period from 2022 to 2025 marked a qualitatively new phase in energy cooperation between China and the GCC countries (see Appendix 2, Table 6). Record-breaking solar and wind power plants have been launched or announced, from massive parks in the deserts of the UAE and Saudi Arabia to the first wind farm in the Emirates. Joint production of solar panels and components is under planning, both within the Gulf (Oman, Saudi Arabia, and UAE) and beyond (Chinese–Saudi projects in Asia).

This cooperation is driven by mutual interests. Gulf countries gain access to necessary equipment and reliable contractors to help achieve their ambitious goals (30–50% clean energy by 2030), while China expands its presence in Middle Eastern markets, exports equipment, and signs long-term contracts. According to available data, about one-third of China’s direct investment in Saudi Arabia from 2021 to 2024 went into clean technologies (solar, wind, energy storage) (El-Shaeri, 2024). As a result, China has become a key energy transition partner for all GCC states, from the major players, namely Saudi Arabia, and the UAE, to those just beginning their green journey such as Kuwait, and Bahrain, and to those trying to find their special way as Oman and Qatar.

The projects listed in Table 6 (Appendix 2) demonstrate that this alliance of capital and technology is accelerating global decarbonization. In the future, China–GCC cooperation in green energy is set to expand, with new solar mega-projects in Kuwait, hydrogen exports from Oman and Saudi Arabia to Asia, and power grid integration on the agenda (Ministry of Electricity, Water and Renewable Energy of Kuwait, 2025). This partnership is becoming a prime example of synergy between emerging economies in the global energy transition.

Yet, China’s partnership with the GCC in green energy, despite its logistical and strategic appeal, is not without challenges. Traditionally, scholars focus their attention on (geo)political and technological risks. Thus, one of the widely discussed primary risk factors is external pressure from the United States and its Western allies, which are increasingly concerned about China’s growing influence in critical energy infrastructure. The use of Chinese equipment, especially in strategic projects, raises cybersecurity and supply chain dependency concerns, especially when dual use components are concerned. Moreover, some Chinese energy technology manufacturers are already under U.S. sanctions, which may complicate equipment deliveries, maintenance, and access to international financing. Under these circumstances, Gulf countries will have to carefully navigate between two global power centers, avoiding confrontation and maintaining access to both Western markets and Chinese investment and technology.

The technological dimension of cooperation with China is also believed to pose threats. Although Gulf states have broad access to Chinese equipment and engineering services, China is not always ready to share critical know-how or co-develop joint research platforms. This situation risks locking GCC countries into the role of technology importers and assemblers, rather than developers, reducing the long-term resilience of their energy transition. Additionally, there may be frictions over equipment quality, project timelines, or contractual conditions, especially in large-scale infrastructure ventures. Any failure or delay could damage China’s reputation as a reliable partner and erode trust in the “Chinese decarbonization” model, particularly in the eyes of Gulf elites striving for technological sovereignty, which has been an important component of the recent developmental model adopted by these countries as part of their vision plans.

Yet, when it comes to the green energy cooperation, the major source of challenges for the GCC states is often underestimated: the economic factors. As Table 6 (Appendix 2) details, Chinese companies are on a trajectory toward providing capital, equipment, and engineering expertise for many flagship Gulf projects, from vast solar parks to planned green hydrogen plants. While this alignment accelerates the Gulf’s energy transition, an overdependence on China presents certain economic vulnerabilities. First, there are investment and funding risks. China’s years of double-digit GDP growth have slowed to mid-single digits; GDP growth is forecast around 4–5% in 2024–2025 (Ellis, 2025). This cooldown, exacerbated by the property sector crisis, means Chinese state investors and banks may become more cautious. Thus, BRI investments peaked around 2018 and have been moderate ever since (Nouwens, 2023). For GCC projects counting on Chinese capital in the form of equity stakes, loans, or joint funds, a Chinese slowdown or financial shock could dry up promised financing.

Second, as the world manufacturing hub of the clean energy technologies, China’s internal disruptions can quickly ripple outward. The Covid-19 pandemic was a warning signal: Chinese the lockdowns in factories and port closures led to equipment delivery delays globally, while soaring shipping costs hit project timelines (Rivero, 2021). Additionally, fast-rising Chinese demand for raw materials caused global shortages, negatively affecting prices: from 2020 to 2022, prices for solar-grade polysilicon, lithium, steel, and other inputs roughly doubled. These cost spikes raised solar and wind project costs by 20–30% in many markets, forcing some developers to postpone projects (International Energy Agency, 2023).

Third, as it was mentioned before, the GCC’s ability to invest in renewables is linked to its hydrocarbon revenues, and China is the world’s largest oil importer, and a major buyer of GCC oil and gas (Alghannam, 2025). An economic downturn in China could contribute to an oil glut or price drop, thereby shrinking GCC export earnings. This, in turn, squeezes the funding available for renewable projects, many of which are state-funded or backed by sovereign wealth derived from oil. Thus, economic modeling by the IMF shows that a global slowdown led by China would significantly dent both hydrocarbon and non-hydrocarbon GDP in the GCC (Ando, 2024).

Finally, by leaning so much on one partner, GCC nations may neglect development of alternative capabilities and options. If Chinese firms always win the contracts and supply the equipment, local companies may not grow their expertise, and relationships with other international providers may weaken. This concentration risk means that if the Chinese source is suddenly unavailable, the Gulf may find itself with insufficient alternative suppliers or homegrown talent to compensate.

Comparative SWOT Analysis of the EU and China as Partners of the GCC in the Renewable Energy Sector

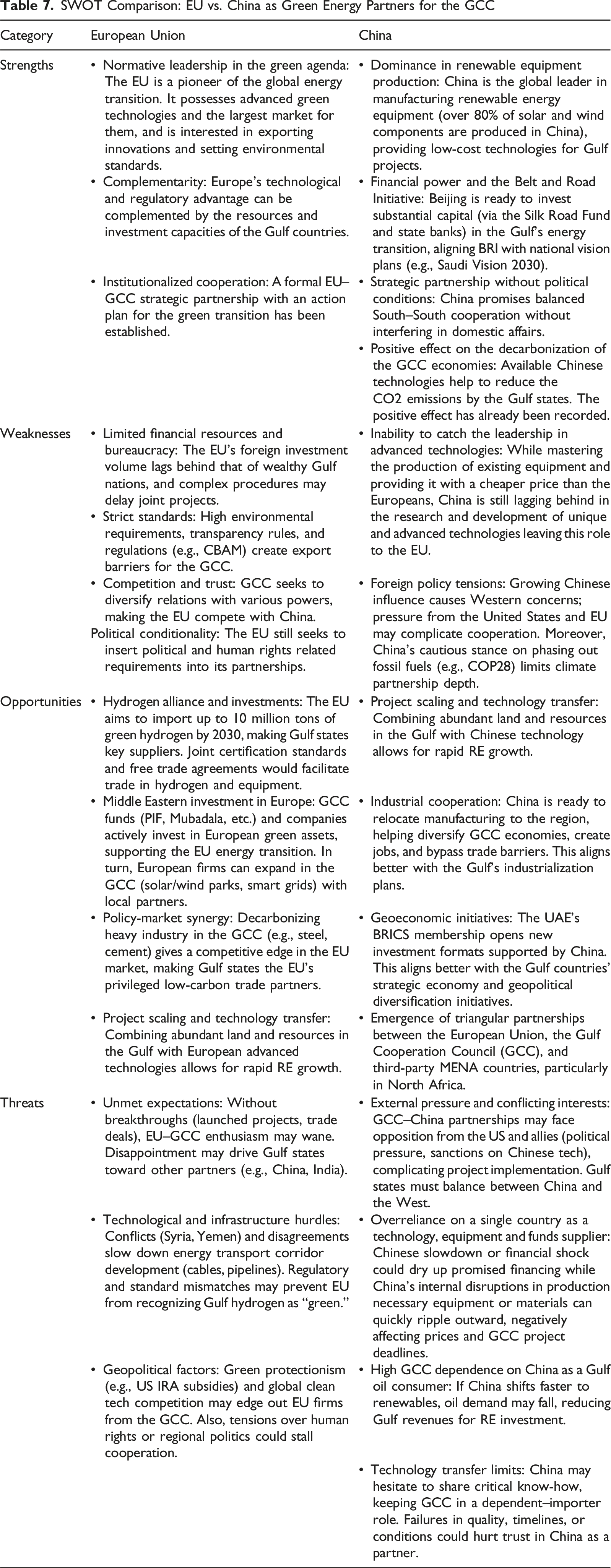

Based on the foregoing, the next section will discuss whether the EU or China is the more attractive partner for the GCC states. Table 7 (Appendix 2) presents a comparative SWOT analysis, based on the authors’ own expert assessment, of the EU and China as potential strategic partners for the Gulf countries in the development of renewable energy. Each category highlights the key characteristics of the two partners (see Appendix 2, Table 7).

For the Arab Gulf states, the European Union represents a natural partner in advancing the green agenda, owing to its global leadership in climate change mitigation and its expertise in high-tech development. The EU’s appeal to the GCC lies in the convergence of opportunities for the GCC member states showcasing as the most technologically advanced countries and a values-driven approach to the energy transition. The EU offers cutting-edge technologies in renewable energy and energy efficiency, a mature clean energy market, and a comprehensive regulatory framework. These assets complement the Gulf states’ strengths, namely abundant financial resources derived from hydrocarbon revenues, vast territories suitable for solar and wind development, and the demand for modern technologies and expertise. Together, these capabilities can produce a synergistic effect that accelerates the energy transition and benefits both regions.

However, several limitations hinder the full realization of the EU–GCC partnership’s potential. First, the EU trails behind China and some of the wealthiest oil-exporting states in terms of financial capacity to fund major projects in that realm. Despite the Global Gateway initiative, European funding for green energy projects remains relatively modest. Faced with pressing timelines and abundant capital, Gulf states often prefer to secure more agile financing from Asian institutions rather than endure the lengthy EU funding approval processes. Second, the EU’s high environmental, legal, and regulatory standards are often seen in the Gulf as cumbersome. To export hydrogen or ammonia to Europe, producers must comply with stringent technical criteria and provide transparent emissions data. For GCC monarchies accustomed to less regulated partnerships, such as those with China or India, this adds friction and reduces flexibility. Third, the EU’s geopolitical presence in the Gulf is limited. Unlike the United States, Europe lacks a robust military presence or long-term security agreements with GCC countries, except for the presence of individual EU members through bilateral arrangements. While this does not directly impact renewable energy cooperation, it contributes to a lower overall level of trust and strategic engagement.

By contrast, China has emerged as a fast-moving and pragmatic partner for the GCC states in the renewable energy sphere. Its appeal stems from a unique blend of economic strength, technological leadership, and a policy of non-interference. The foundations of China–GCC cooperation are clear: China is the world’s largest importer of oil and gas, while the Gulf states are among its principal suppliers. Simultaneously, China is investing heavily in its domestic and global green energy capacities and holds dominant positions in the production of solar panels, wind turbines, batteries, and related technologies. This makes Chinese solutions especially attractive for the Gulf, offering a turnkey package, from financing and equipment to project execution, for rapidly scaling renewable infrastructure, such as solar farms and electric vehicle systems.

In practice, unsurprisingly, China–GCC cooperation has progressed at a remarkable pace in recent years. As much as Gulf policymakers are increasingly cognizant of the associated risks, China’s attractiveness to the GCC remains very high, particularly in the short and medium term. It offers fast, large-scale, and politically uncomplicated solutions to many of the Gulf’s energy transition needs. Beijing has demonstrated a growing willingness to invest hundreds of millions of dollars and provide access to technology, as illustrated in Table 6 (Appendix 2). As a result, China is seen as a convenient and pragmatic partner in an increasingly multipolar global system.

The comparative SWOT assessment of the EU and China as green energy partners illustrates that the GCC’s partnership strategies should be multidimensional, with distinct priorities in the short and long term. In the short term, the most decisive dimensions lie on the Chinese side, notably its strengths in low-cost renewable equipment manufacturing, project financing under the Belt and Road Initiative (BRI), and its politically non-intrusive approach. These attributes align closely with the Gulf states’ immediate needs to scale up renewable capacity, develop local industrial bases, and deliver visible progress on national transition agendas such as Saudi Vision 2030 or UAE Net Zero 2050. The EU’s weaknesses, particularly its bureaucratic inertia, complex regulatory mechanisms, and political conditionality, limit its responsiveness to these short-term imperatives. As a result, the GCC’s pragmatic calculus favors Chinese engagement to secure rapid infrastructure deployment, local job creation, and technology transfer that underpins domestic legitimacy and diversification goals.

In the long term, however, the balance of strategic value tilts toward the EU’s strengths and opportunities. Europe’s technological and regulatory leadership, experience in hydrogen markets, and potential to establish joint certification and carbon-pricing mechanisms are critical for the Gulf economies’ integration into the emerging global low-carbon trade regime. As international climate governance and green trade standards consolidate, alignment with EU norms becomes a prerequisite for maintaining market access, export competitiveness, and credibility in sustainable finance. Moreover, the EU’s focus on transparency, energy efficiency, and innovation ecosystems supports the GCC’s ambition to achieve technological sovereignty and resilience beyond the replication of imported models.

Hence, the GCC’s optimal strategy is to act in a sequenced and adaptive manner: leveraging China’s short-term advantages in cost efficiency and industrial scalability while cultivating Europe’s long-term potential as a source of regulatory legitimacy, innovation, and market integration. This dual-track approach operationalizes the Gulf’s broader hedging and diversification doctrine, ensuring flexibility amid systemic uncertainty. By combining China’s pragmatic industrial engagement with the EU’s normative-technological edge, the GCC enhances its energy security, transition resilience, and strategic autonomy, which will help secure both immediate gains and long-term positioning in the post-hydrocarbon global order.

Faced with these asymmetries, the GCC’s strategic calculus increasingly relies on multi-vector engagement: cooperating with the EU to gain legitimacy, regulatory compatibility, and access to cutting-edge decarbonization tools, while deepening ties with China to accelerate infrastructure development, attract capital, and expand manufacturing capacity. This hedging posture allows Gulf states to mitigate the risks of overdependence on either partner, balancing Europe’s normative and technological assets with China’s financial and industrial pragmatism. Moreover, it enhances energy security by diversifying technology sources, export markets, and geopolitical alignments, which will effectively transform the GCC’s traditional focus on “security of demand” for hydrocarbons into a broader quest for technological sovereignty and transition resilience. In this sense, the EU-plus-China dual engagement functions not as a zero-sum choice but as a strategic instrument for Gulf states to secure autonomy and flexibility in an increasingly fragmented global energy order.

The opportunities identified in both the EU and Chinese dimensions of the SWOT table illustrate complementary avenues through which the GCC can advance its energy transition, diversify its economies, and consolidate energy security. The EU’s opportunities, notably the development of a hydrogen alliance, investment interdependence, and policy-market synergies, correspond to the Gulf states’ long-term ambition to position themselves as global exporters of low-carbon energy carriers. Europe’s projected import demand for green hydrogen beyond 2030 aligns directly with Gulf investment in large-scale solar and wind capacity, as well as ammonia conversion facilities. Joint certification schemes and harmonized regulatory frameworks with the EU could enable Gulf hydrogen to access premium low-carbon markets, while Gulf sovereign wealth funds’ investments in European green assets create reciprocal channels of interdependence. Moreover, EU–GCC collaboration in the decarbonization of heavy industry (e.g., aluminum, steel, or petrochemicals) offers the Gulf producers a route to maintain competitiveness under the EU’s Carbon Border Adjustment Mechanism (CBAM) and similar future trade regimes. Thus, the EU’s opportunities are primarily institutional and regulatory, which can potentially embed Gulf economies within the architecture of the global green economy and enhance their long-term energy and economic resilience.

By contrast, China’s opportunities are primarily industrial and financial. Beijing’s readiness to scale projects rapidly, relocate manufacturing to the Gulf, and integrate energy cooperation within broader BRI corridors provides the GCC with immediate pathways for capacity expansion and industrial diversification. These opportunities align strongly with the Gulf visions of localized production, job creation, and the embedding of supply-chains. Additionally, China’s support for BRICS and related multilateral formats offers the Gulf countries alternative platforms for financing and investment, which can insulate them, at least partially, from Western regulatory constraints. In this sense, China’s opportunities strengthen short-to medium-term transition pragmatism, enabling the GCC to implement tangible projects that build domestic legitimacy and reduce the cost of the energy shift.

However, both partnerships also contain significant threats that shape the GCC’s hedging behavior. Regarding the EU, the main threats arise from underperformance and regulatory challenges. It is of key importance for the Europeans to sustain the high level of involvement into the Gulf renewable projects amid growing China presence (both in form of the FDIs and EPC contracts) and consider the ways to raise in the volume of spare parts supplies. Without it, the enthusiasm for deepening EU–GCC partnership may erode, leaving space for Asian partners. Moreover, divergent definitions of ‘green’ hydrogen that can be considered acceptable for the EU economies and environmental standards could prevent Gulf exports from being recognized as sustainable in European markets, an outcome which may undermine the GCC’s strategic positioning. The EU’s tendency toward “green protectionism,” exemplified by CBAM and subsidy competition with the U.S. Inflation Reduction Act, also risks marginalizing non-European producers.

Regarding China, threats are more systemic and geopolitical. Overreliance on China as a supplier of renewable technology and as a major oil consumer creates dual vulnerabilities: a slowdown in the Chinese economy or disruptions in its manufacturing chain could delay Gulf projects, while an accelerated Chinese shift toward renewables could reduce hydrocarbon revenues essential for funding the Gulf transition. External political pressures, especially from the United States and the EU, may also complicate GCC–China cooperation, forcing Gulf states to manage exposure to sanctions and technological restrictions. Furthermore, China’s limited willingness to transfer core technologies could leave the Gulf economies in a dependent, importer position, constraining their pursuit of technological sovereignty.

Taken together, these opportunities and threats illustrate the GCC’s complex strategic landscape. Europe offers long-term institutional and regulatory integration, essential for global competitiveness, but it may be slower to materialize. China provides short-term industrial dynamism and financial liquidity, yet it may come at the cost of higher dependency and geopolitical risk. The Gulf’s challenge, therefore, is to exploit both sets of opportunities while mitigating their respective threats through a balanced diversification strategy, anchored in selective technology transfer, multi-market export orientation, and active participation in both Western and Asian decarbonization frameworks. This calibrated approach enhances not only energy transition progress but also the strategic autonomy and systemic resilience of the GCC countries in an increasingly fragmented global energy order.

Conclusion

The energy transition is becoming not only an economic necessity or technological trend but also a subject of active foreign policy maneuvering, where cooperation and competition are deeply intertwined. In this context, the external partnerships of the GCC states with the European Union and China reflect two different strategic approaches to the region’s “green” future. The European Union promotes norm-based cooperation centered around rules, certifications, and climate standards. In contrast, China acts more pragmatically, offering concrete investments, equipment, and EPC contracts, making it especially attractive to Gulf countries seeking rapid implementation of large-scale projects.

However, neither external partnership vector is free of limitations and potential risks. In the EU’s case, excessive regulatory rigidity, especially around hydrogen certification, rules of origin, and carbon footprint, creates real barriers for Gulf exports and slows the development of joint initiatives. China, meanwhile, though more flexible and better funded, reproduces a dependency on external technologies and may limit the transfer of critical know-how. Moreover, in a world of intensifying global competition for energy influence, any deepening of ties between Gulf states and Beijing may be seen as a threat by the U.S. and EU, leading to the further securitization of the energy transition itself, as part of the securitization of China question and return of great power politics.

Indeed, while there are a host of technological or energy markets related factors that will determine the evolution of the Gulf region’s relationship with China and the EU, a major determinant will be the broader geopolitical considerations and systemic shifts. As part of the return of great power competition, there is a major internal debate within the West as to how to reformulate the relations with an increasingly assertive China and develop a unified strategy. Considering its opposition to the Chinese expansion in economics and other fields, the United States has been pressing hard on its allies in different parts of the globe and European powers to reformulate their relationship with China and its expanding presence in the neighboring regions. While there appeared to be a deep transatlantic divide on the China question, since the new geopolitical realities in the wake of the COVID-19 pandemic and Russian invasion of Ukraine, a more critical thinking toward China also gained ground in Europe. The U.S., keen on decoupling Western economies and its partners from China both in terms of production and technology, will continue to put pressure in that realm. Europe is increasingly debating its disengagement from China and approaching it in a more strategic manner. Since the launch of the European Commission’s strategic outlook paper on EU-China relations in March 2019, China has been viewed as not only a partner but also a rival and systemic competitor (European Commission, 2019). Nonetheless, it will be hard to achieve a complete decoupling, considering the current level of mutual integration of economic and financial markets. Therefore, the European leaders tend to avoid the language of decoupling, and instead emphasize de-risking in a way to reduce the dependency on China and increase coordination with other potential partners (Von Der Leyen, 2023).

While China emerges as economic powerhouse, the multi-faceted economic engagement between the Gulf and China will most likely continue. Similar to Western capital flowing into Chinese markets, and production moving there in such industries as solar, automobiles, chemicals or emerging technologies, the Gulf, too, will continue to deepen its partnership with China in all economic spheres. However, parallel to the securitization of technological partnerships, a more coercive Western policy on China may eventually transform cooperation in energy from a purely technical or environmental issue into a strategic matter of international rivalry. If the West were to take a tougher line on China, it might put the Gulf countries in a difficult position, but in any case they will be opting for balancing their ties with both sides, and the cooperation in green energy transition presents the best case study for this behavior.

To navigate the competing pressures between the EU’s regulatory model and China’s pragmatic industrial approach, GCC policymakers will be best advised to stick to a flexible, multi-level strategy that institutionalizes hedging as a tool for both risk management and value creation. In the short term, Gulf states should leverage Chinese financing and industrial capacities to accelerate renewable deployment and build domestic manufacturing ecosystems, while simultaneously engaging the EU to secure technology transfer, certification compatibility, and access to low-carbon export markets. Establishing hybrid partnerships, where, for instance, Chinese capital supports projects adhering to EU environmental standards, could bridge normative and pragmatic models. Policymakers should also prioritize technology localization, regulatory alignment, and joint research and development centers to reduce long-term dependency. On the governance side, developing sovereign green funds and regional transition frameworks, for instance through the GCC Secretariat, could help coordinate national efforts, mitigate exposure to supply chain shocks, and ensure resilience against geopolitical volatility in both Western and Asian markets.

From a research agenda perspective, future studies could explore how the financialization and securitization of the energy transition are reshaping Gulf strategic behavior. Similar to recent work by Helmi et al. (2024, 2025) and Lin and Zhang (2025), scholars could analyze how geopolitical risk indices, green finance dynamics, and critical mineral supply chains jointly influence Gulf investment decisions. Comparative analyses of intra-GCC approaches to managing technology dependence, critical mineral sourcing, and green hydrogen certification could also provide valuable policy insights. Ultimately, deeper interdisciplinary inquiry, linking political economy, finance, and security studies, will be essential to understand how the GCC can sustain strategic autonomy and energy transition resilience amid an increasingly multipolar and risk-prone global order.

Footnotes

Acknowledgements

Open Access funding provided by the Qatar National Library

Funding

The authors received no financial support for the research, authorship and/or publication of this article. Open Access is made available through the funding provided by the Qatar National Library.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Notes

Author Biographies

Graphs

Electricity Generations by Renewables in the GCC Member State in 2015–2023 (GWh). Source: IRENASTAT: https://pxweb.irena.org/pxweb/en/IRENASTAT

Major GCC Renewable Energy Projects with the Supply of the EU and Chinese Equipment Commissioned in 2017–post-2025. Sources: Author’s calculations

Major GCC Renewable Energy Projects with the EPC Participation of the EU and Chinese Companies Commissioned in 2017–post-2025. Sources: Author’s calculations

Major GCC Renewable Energy Projects with the European and Chinese FDI Commissioned in 2017–post-2025. Sources: Author’s calculations

Tables

Examples of GCC Sustainable Energy Projects with European Supplies Commissioned in 2018–2025 Source: Authors’ calculations.

Project name

Country

Year

Type

Technology supplied

European supplier (Country)

Al Kharsaah Solar PV Plant

Qatar

2022

Solar (PV)

800 MWp solar PV farm with single-axis bifacial trackers

Ideematec (Germany)

DEWA Green Hydrogen Pilot

UAE

2021

Hydrogen

1.25 MW solar-powered PEM electrolyser and storage

Siemens Energy (Germany)

Dumat Al Jandal Wind Farm

Saudi Arabia

2021

Wind

Onshore wind turbines

Vestas (Denmark)

Hatta Pumped Storage Plant

UAE

2019

Hydro (Storage)

Two 125 MW pump-turbines)

Andritz Hydro (Austria)

NEOM Green Hydrogen Project

Saudi Arabia

2021

Hydrogen

∼2 GW alkaline water electrolyser plant

Thyssenkrupp Uhde (Germany)

Noor Energy 1 (MBR Solar Park – Phase IV)

UAE

2022–23

Solar (CSP + PV)

700 MW Concentrated Solar Power (CSP) plant (parabolic trough)

Abengoa (Spain)

Shagaya Renewable Energy Park (Phase 1)

Kuwait

2018

Hybrid (Solar/Wind)

2 MW turbines and 50 MW CSP plant

Siemens Gamesa (Spain); Siemens AG (Germany)

Sharjah Waste-to-Energy Plant

UAE

2022

Waste-to-Energy

30 MW mass-burn incineration & steam power plant

CNIM (France)

Examples of GCC Sustainable Energy Projects with Chinese Supplies Commissioned in 2018–2025

Project name

Country

Energy Type

Year (Start/Commission)

Chinese Supplier(s)

Component(s) supplied

Developer/Owner

Al Dhafra Solar PV Plant

UAE – Abu Dhabi

Solar PV

2020–2023

Trina Solar; CMEC

PV modules (800 MW Vertex panels)

TAQA, Masdar, EDF, Jinko Power consortium

Al Kharsaah Solar Power Plant

Qatar

Solar PV

2020–2022

LONGi Solar; PowerChina

∼2 million bifacial PV modules

Siraj Energy (QEWC/QatarEnergy JV), TotalEnergies, Marubeni

Al Shuaibah Solar PV IPP – Phase 1

Saudi Arabia

Solar PV

2021–2022

LONGi

PV modules (388 MW supply for Jeddah PV plant)

ACWA Power (lead developer)

Al Shuaibah Solar PV IPP – Phase 2

Saudi Arabia

Solar PV

2024–2025

Sungrow; China Energy Intl.

2.1 GW of modular inverters

ACWA Power & PIF (Badeel)

Al-Askar/Al-Dur Solar Park

Bahrain

Solar PV

2023–2025

TBEA Xinjiang Sunoasis

Turnkey EPC and PV equipment (bid ∼90–100 MW)

Bahrain EWA

Amin Solar PV Plant

Oman

Solar PV

2019–2020

Sungrow

Solar inverters

Amin Renewable Energy Co. – Marubeni, Oman Gas, Bahwan, Nebras

Ibri II PV IPP

Oman

Solar PV

2019–2021

Jolywood Solar

Bifacial PV modules (405 W panels)

Shams Ad-Dhahira Co. – ACWA (50%), Gulf Invest. Corp (40%), AEPC (10%)

MBR Solar Park – Phase 4 (Noor Energy1)

UAE

CSP + PV hybrid

2018–2024

Shanghai Electric

CSP equipment & EPC services; PV modules (Chinese make)

DEWA, ACWA Power, Silk Road Fund

Examples of the GCC Sustainable Energy Projects involving European EPC Contractors (2017–post-2025) Source: Authors’ calculations.

Project name

Country

Energy type

Capacity

Status

EU/UK EPC Contractor

Commissioning

Shagaya CSP Plant

Kuwait

Solar (CSP)

50 MW

Completed

TSK (Spain)

2018

Shagaya Wind Farm

Kuwait

Wind

10 MW

Completed

Vestas (Denmark)

2017

Kabd Waste-to-Energy Plant

Kuwait

Waste-to-Energy

∼100 MW (3,275 t/day)

Under Construction

CNIM (France)

∼2024 (planned)

MBR Solar Park – Phase II

UAE

Solar (PV)

200 MW

Completed

TSK (Spain)

2017

Sharjah Waste-to-Energy Facility

UAE

Waste-to-Energy

30 MW (900 t/day)

Completed

CNIM (France)

2022

Dubai Waste-to-Energy (Warsan)

UAE

Waste-to-Energy

200 MW (5,666 t/day)

Under Construction

BESIX (Belgium)

2024 (expected)

Masdar–Engie Green H2 Plant (Ruwais)

UAE

Hydrogen

200 MW (electrolyzer)

Planned (2025)

Engie (France)

2025 (expected)

DEWA Green Hydrogen Pilot

UAE

Hydrogen

1.25 MW

Completed (pilot)

Siemens Energy (Germany)

2021

Dhofar Wind Farm

Oman

Wind

50 MW

Completed

TSK (Spain)

2019

Dumat Al Jandal Wind Farm

Saudi Arabia

Wind

400 MW

Completed

Vestas (Denmark) & TSK (Spain)

2022

NEOM Green Hydrogen Project

Saudi Arabia

Hydrogen (Green)

600 t H2/day (2 GW)

Under Construction

Thyssenkrupp (Germany)

2026 (expected)