Abstract

This article invites 2 experts having knowledge of financial management: one from within the dental fraternity and one from outside to assist the orthodontists (academic and practitioners alike) to help provide some guidance to sail through these turbulent times. With the COVID-19 pandemic, we are witnessing an unprecedented moment in history that has impacted the entire globe at a never before seen scale. This coronavirus has resulted in a double black swan event where there is a health and financial pandemic at the same time. As orthodontists, you are also corona warriors and part of the first line of defense! But even you would be facing a decrease in patients and earnings, maybe even an increase in your expenses as you are battling through this pandemic. These turbulent times have greatly affected businesses and livelihoods, and everyone wants to know the best thing that they can do to manage and optimize their personal finances.

The Dental/Orthodontic Perspective

The following statements and inputs are by no means nonexhaustive but only represent the basic things that an orthodontist can do to tide through their troublesome times and manage their practice.

Origins of group buying can be traced to China, where it is known as Tuán Gòu (Chinese: 团购), or team buying. You can make a group of fellow dentists in your area and buy collectively, while demanding a steep discount from the company/dealer.

Nondental/Orthodontic Perspective

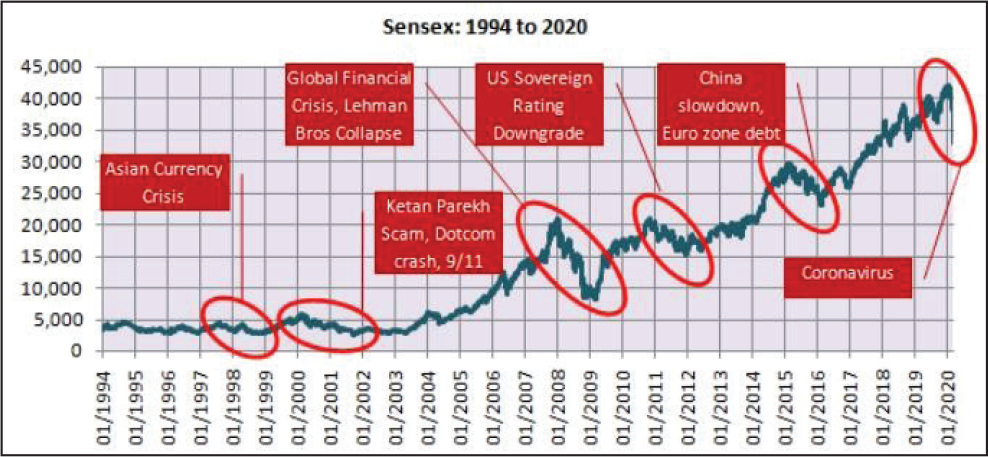

Even though this is an unprecedented double whammy, crashes in the financial markets are not uncommon (Figure 1).

Each financial market crisis brings with it a chance to learn and the most important learning of all is “stick to the basics.” If one has his/her basics in place, his/her financial foundation can withstand any turmoil and even capitalize on it!

Following are some basic financial planning mantras that can help you navigate this current crisis and any future ones that may arise on your road toward a secure future.

Having an “emergency fund” is often the simplest and most overlooked aspect of personal finance. In a crisis like this, many could be facing salary cuts in academic institutions, along with private practitioners who would be facing a drop in their clinic revenues. One should ALWAYS have at least 6 months’ worth of their household expenses in a safe and liquid instrument (like liquid funds) so that times like these do not have them worrying and selling long-term investments at losses to pay for basic expenses. For those of you who have their own clinics, your emergency fund should cover 6 months of business expenses as well, as your staff depends on you. “Health insurance” is essential as you do not want to spend your hard-earned savings and investments in medical expenses. Most people have this point covered; however, some are under insured and do not even know it, while others may have outdated policies that do not provide the coverage that is required. There are now COVID-specific policies also available that could be looked into. Independent practitioners should also get health insurance for their employees and support staff as this is essential for the peace of mind, safeguarding your business. There are many economical group insurance policies available today. While most of us have health insurance figured out, “term insurance” still remains a challenge. We refuse to accept our own mortality and think that nothing bad can happen to us. Many think that they are safe because they are covered with their LIC Policies. These policies have a very poor sum assured, and even if you have multiple such policies, just add them up; they will not be sufficient for your family in the case of a mishap. If you do not have term insurance, buy a simple vanilla term plan that has the coverage of at least 12 to 15 times your annual income. “Asset allocation” is the single biggest factor that determines long-term returns and makes sure that one’s portfolio is balanced enough to sail through choppy waters. Asset allocation is a fundamental of investing where an investor sets a fixed percentage of exposure to different asset classes such as equity, debt, real estate, and gold based on goals, risk tolerance, and investment horizon.

Many that I have noticed are overexposed to property. They face the issue that their capital is tied to ill-liquid assets and is not available to them at a time of need. The risk-takers are generally overexposed to equity. They see their portfolios majorly in the red and panic. Many even make the mistake of selling equity investments to protect themselves from further loss. The conservative ones have most of their money in fixed deposits and gold, and they miss great opportunities to multiply their wealth.

But if one has carefully decided an asset allocation that suits them and has appropriate exposure to the different asset classesproperty, equity, debt (fixed income), and goldthey will not face any problems and even stand to capitalize on market crashes by re-balancing their allocation and investing more in equity to generate greater returns in the long run.

With basics in place, you and your family are safe and secure. With safety out of the way, following are some of the things that you should keep in mind and follow right now.

Don’t panic: The most important thing is to not get carried away by headlines and make knee-jerk reactions in panic. Long-term investors should not panic and redeem their investments in a hurry in the current market. Do not convert your notional losses into actual ones. Remember that you have invested in equity only for the long run, and you must not let short-term volatility affect your overall financial plan. Markets go through these cycles sometimes, and the true test of an investor is to focus on his/her goals and stay invested.

Stick to your asset allocation. Be patient. Stay invested.

Do not stop your SIPs: The main reason we invest via systematic investment plans (SIPs) is to use rupee-and-cost averaging to accumulate greater units in such market conditions. So, unless you are facing grave troubles due to job loss or salary cuts or have an emergency, and you need the capital right now, please do not stop your SIPs. Rather, use this opportunity to top up and increase your monthly SIPs. Market crashes are the best time for your SIPs as you get more units that increase your long-term returns. Invest in equity: In hindsight, one sees that all crashes are excellent buying opportunities, so if you have ample liquidity and your asset allocation allows it, seize the opportunity and invest inequity mutual funds. However, keep in mind that one must stagger the lump sum amount in 3 to 4 tranches as no one can predict the exact bottom. In the long run, it is not going to matter whether you invested with Sensex at 32,000 or 30,000, but whether you invested in equity at all. Another good option is investing with a liquid to equity systematic transfer plan over 20 weeks. Review asset allocation: As exciting as the markets may seem to enter into equity or as scary as they may seem to exit, do not violate your asset allocation. If your predecided asset allocation has altered because of the market correction, use this opportunity to re-balance it! If you have been investing without keeping asset allocation in mind, use this opportunity to start and become a better, more disciplined investor.

It is always advisable to speak to a financial advisor who can provide the guidance and support needed through these turbulent times and walk with you on your financial journey toward a secure future.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.