Abstract

Although new digital monetary instruments (e.g., cryptocurrencies) have emerged and proliferated, there is little academic research concerning consumer perspectives on these instruments or the effects of these instruments on consumers’ moral judgments. The present research addressed this gap in the literature by addressing the following research question: Is the morality of tax evasion judged differently when tax evasion is undertaken with cryptocurrency vs. traditional financial instruments (e.g., stocks)? In two online experiments, we exposed participants to a tax evasion scenario with either cryptocurrency or stock trading. The results of Study 1 showed that tax evasion is perceived as being less wrong when it is carried out with cryptocurrency trading rather than stock trading. Study 2 replicated Study 1 and tested an explanatory mediating mechanism hypothesized to underlie the main effect. A mediation analysis showed that the effect of cryptocurrency (vs. stock trading) on the perceived wrongness of tax evasion is partially mediated by the observer's positive (vs. negative) affective evaluation of the person committing tax evasion. This paper also discusses the theoretical, practical, and societal implications of the present results, including the likelihood that people's attitudes toward moral transgressions and crimes will be more lenient when these acts are conducted with new, innovative, and exciting instruments.

Introduction

Over the past decade, financial crimes and murky business practices have directed public outrage toward the lack of moral and judicial judgment in financial markets (e.g., BBC Panorama, 2020; Cohan, 2015; Eisinger, 2014; Winneker et al., 2020). Moreover, new financial technologies (a.k.a. fintech) can lead to new moral dilemmas. A prominent example is the dilemma of cryptocurrency. On one hand, cryptocurrencies yield certain benefits to users, such as flexibility, privacy, and the fact that one does not need a bank account to use them (Scharding, 2019), and have grown increasingly popular. There were at least 22,932 different cryptocurrencies in circulation in March of 2023 with a “total market capitalization of $1.1 trillion” (e.g., Hicks, 2023), and it has been estimated that 4% of the population across all developed countries uses cryptocurrencies (Cryptocurrency Ownership Data, 2023). On the other hand, the obvious downside of cryptocurrencies—owing especially to their anonymity—is that they open doors to criminal and unethical behaviors. Despite increased regulatory actions, many illegal underground markets (e.g., drugs, weapons, and human trafficking) use cryptocurrencies as their main forms of payment (e.g., Almaqableh et al., 2023; Bahamazava & Nanda, 2022; Dearden & Tucker, 2023). Even the digital currencies introduced by large global companies (e.g., Open AI:s WorldCoin) have raised concerns about their potential to facilitate money laundering and other harmful consequences (Partington, 2019; Pettersson Ruiz & Angelis, 2022; Wronka, 2022).

Notwithstanding the proliferation of cryptocurrencies, there is little academic research on their general influence on consumer behavior and virtually no empirical research on consumers’ ethical responses to them. Indeed, a recent literature review on the ethics of cryptocurrencies concluded that, compared to other forms of money, there is a lack of academic research on the ethical consequences of cryptocurrencies in terms of consumer behavior and societal implications (e.g., effects on illegal activities; Sousa et al., 2022). We addressed this gap in the literature by exploring consumer judgments of (other people's) moral transgressions with cryptocurrencies. Specifically, we empirically investigated the effects of cryptocurrency usage on consumers’ moral judgements of tax evasion by posing the following research question: Is the morality of tax evasion judged differently when tax evasion is undertaken with cryptocurrency vs. traditional financial instruments (e.g., stocks)? Tax evasion forms an appropriate empirical context because it is one of the most prominent examples of immorality connected to cryptocurrencies on a macro level (e.g., Dierksmeier & Seele, 2018; Nawaz et al., 2023: Nguyen, 2022).

To address the research question, we conducted two scenario-based online experiments. Experiment 1 examined how moral judgment of tax evasion varies between monetary instruments. The results demonstrated that consumers judge tax evasion with cryptocurrency (vs. stocks) trading to be significantly less (vs. more) wrong. Experiment 2 explored the observer's evaluation of the person committing tax evasion as a potential mediator of the currency's effect on the observer's moral judgments. The results showed that the tendency to cast a more negative moral judgment on tax evasion via stocks (vs. cryptocurrency) may be explained by the observer's less positive character evaluation of the stock-trading person (vs. the cryptocurrency-trading person).

The present research contributes to two lines of literature. First, it contributes to the literature on consumer attitudes and behaviors relating to monetary instruments (e.g., Folkinshteyn & Lennon, 2016; Pieters, 2013; Wang & Wolman, 2016). In particular, the present findings contribute to the stream of research on ethical or moral judgments (Greene, 2014; Grym & Liljander, 2016; Horberg et al., 2011; Teper et al., 2015) related to monetary instruments by extending and updating the range of studied monetary instruments from traditional non-digital instruments (e.g., cash, checks, money orders, debit/credit cards, and investment securities) to the fully digital, contemporary instrument of cryptocurrency. Second, this research contributes to the emerging literature on cryptocurrency (e.g., Almeida & Gonçalves, 2023; Bhimani et al., 2022; Johnson et al., 2023; Vidal-Tomás, 2022). To our knowledge, this paper is one of the first to address general consumer responses and specific moral judgments relating to the use of cryptocurrencies.

Conceptual Development

Moral Judgment

Morality is related to the wrongness and harmfulness of a given act (Schein & Gray, 2018). Consumers’ moral judgments are influenced by many dispositional factors, such as their political and religious views (Haidt, 2012), social statuses (Lammers et al., 2010), moods (Forgas, 1995; 1987), and emotions (e.g., anger and guilt; Polman & Ruttan, 2012).

Scholars have demonstrated that the evaluation of a particular action alone does not explain the perceived wrongness of that action (Baron & Ritov, 2004; Cushman, 2008; Shultz et al., 1986; Zelazo et al., 1996). Cushman (2008) provided an example wherein two persons engage in drunk driving; one of these persons hits a pedestrian with their vehicle, while the other hits a lamppost. Both drivers engage in the same action (drunk driving), but the wrongness of action is judged very differently depending on the severity of the outcome.

Aside from evaluations of outcome (i.e., harmfulness), judgments of the wrongness of action are also influenced by factors such as guilt, intentions, and punishment associated with the action (Cushman, 2008). For example, moral responsibility, blameworthiness, and deserved punishment are relevant components of moral judgment according to the tradition of attribution theory (e.g., Cushman, 2008; Fincham & Jaspars, 1979; Shultz et al., 1981).

The Instrument of the Performed Action Shapes Moral Judgments

The aforementioned scenario (drunk driving) is a typical example in research on moral judgments, as it focuses on the influence of an action's explicit outcomes on moral judgments of that action. Likewise, there is an abundance of prior research on the influence of the performer of an action on moral judgments of that action. Most notably, research informed by attribution theory has established that when a wrongful action is performed by the observer, the observer will perceive the action as less wrong than if it were performed by someone else (Graham & Weiner, 1996; Heider, 1944; Kelley, 1967).

In contrast to the harmful outcomes or performers of actions, there is much less research on the influence of the instruments of transgressive actions on moral judgments of these actions. For example, would we judge an armed robbery (in which a robber threatens a victim) differently if the threat were executed with a knife vs. a gun? In the present research, the monetary instrument used to perform tax evasion was considered such an instrument. Meanwhile, the act itself (tax evasion), the action's harmful outcome (stealing from society), and the performer of the action (a friend of the observer) were held constant across the experimental conditions.

There is no single theory that can predict how a monetary instrument (cryptocurrency vs. stock) will influence moral judgments of the wrongness of actions performed with that instrument (tax evasion). Instead, two alternative effects (or directions of effect) can be conceived based on two different theories.

First, moral imagination, as conceptualized by Schwartz and Michael Hoffman (2018), plays a crucial role in ethical decision-making by enabling individuals to perceive and evaluate situations from multiple perspectives. This cognitive process involves reframing scenarios to uncover new possibilities and assessing these alternatives through a moral lens. Schwartz and Hoffman emphasize that moral imagination enhances the stages of ethical decision-making, including awareness, judgment, intention, and behavior. They argue that moral imagination not only helps in recognizing ethical issues but also in creatively resolving them, leading to more ethically sound decisions. (Schwartz & Michael Hoffman, 2018).

Second, theories on cognitive dissonance in moral judgments (Festinger, 1962; Mulder et al., 2009) consider the role of social norms in perceptions and evaluations of both actions and instruments. From this perspective, an act that breaches social norms (e.g., tax evasion) with an instrument that is aligned with social norms (e.g., stock investing) may be considered less wrong than if it were committed with an instrument that is less aligned with social norms (e.g., cryptocurrency trading). Indeed, cryptocurrency trading is likely to be perceived as less aligned with social norms by most people due to its novelty and unfamiliarity. Cognitive dissonance may arise if tax evasion with a norm-aligned instrument (e.g., stock investing) is perceived negatively (i.e., as morally wrong) while the instrument itself is perceived positively (i.e., as morally right). To avoid this dissonance, individuals may adjust their judgments of tax evasion with stock investing such that they perceive it as less wrong. In contrast, such dissonance may not arise if the instrument is judged less positively due to its low alignment with social norms, as in the case of cryptocurrency trading.

Alternatively, differences in moral judgments of tax evasion with two different instruments may arise from different affective evaluations of the persons assumed to typically use these instruments. Affective feelings may influence moral judgments (e.g., Hofmann & Baumert, 2010; Inbar et al., 2009), and the use of a particular monetary instrument by the wrongdoer may evoke the image of an unpleasant (vs. pleasant) person, which may in turn cause the observer to perceive the wrongdoing as more (vs. less) wrong. For example, in the context of monetary instruments, cryptocurrency users may be evaluated in more positive terms (e.g., innovative, smart, or tech-savvy) than stock traders (e.g., old-fashioned).

In summary, we pose two alternatives, competing hypotheses to address the research question:

Study 1

The first small pilot experiment (Study 1) explored H1 vs. H1alt on the main effect level. In other words, this study explored whether moral judgement of a wrongdoing differs between monetary instruments, such that tax evasion with cryptocurrency is perceived as more (vs. less) wrong than tax evasion with stock trading. The effect of monetary instruments on moral evaluation was investigated with a between-subjects randomized experiment, wherein participants were shown a scenario of tax evasion on investments made through either cryptocurrency or stock trading.

Method

Participants

60 participants, 30 per experimental cell, were recruited from the platform Prolific Academic (ProA), which has been shown to provide good-quality data (Peer et al., 2017). The cell size of 30 participants is a conventional cell size in consumer research, for smaller pilot studies. All participants were US citizens, aged 18–65 years (mean age = 39 years; 57% female). One participant was excluded for not finishing the questionnaire.

Design and Procedure

This study employed a simple between-subjects experimental design, with cryptocurrency trading and stock trading as treatment conditions. Each participant was presented with a tax evasion scenario (see Appendix 1 for full description), in which a friend of the participant was described as having made a profitable investment recently— but they had not paid taxes on the investment profits. For half of the participants (group 1), the scenario mentioned that the investment had been an investment in cryptocurrency (e.g., Bitcoin), while for half of the participants (group 2), the scenario said that the investment had been an investment in stocks. The online questionnaire platform (XXXXX) randomly assigned each participant to either group 1 or group 2, and presented the scenario to the participant accordingly.

Measures

The dependent measure was perceived wrongness of action measured on a 10-point scale (1 = did not act wrong, 10 = acted very wrong; Clifford et al., 2015). As control variables, we measured gender, educational level, employment status, yearly gross family income, and political orientation (10-point scale ranging from extremely liberal/left to extremely conservative/right).

The homogeneity of the participant characteristics was analyzed with a Pearson chi-square test. No statistically significant relationships were found between the treatment groups and the background variables of gender (p = .993), age (p = .108), educational level (p = .804), employment status (p = .539), income level (p = .053), and political orientation (p = .257).

Results

The monetary instrument condition significantly affected the participants’ perceptions of the wrongness of tax evasion (F1,57 = 7.84, p < .01). Specifically, the perceived wrongness of tax evasion with cryptocurrency (M = 5.88, SD = 2.84) was significantly lower than that of tax evasion with stocks (M = 7.73, SD = 2.23; p < .05). This result supports H1alt, suggesting that tax evasion with cryptocurrency is perceived as less wrong than tax evasion with stocks. Conversely, this result rejects H1, which predicted that tax evasion with cryptocurrency would be perceived as more wrong than tax evasion with stocks. None of the control variables (income, gender, education, employment status, or political orientation) had any significant effects on perceived wrongness.

Discussion

The results of Study 1 showed that the monetary instrument of tax evasion affects moral judgement, such that tax evasion with stocks is perceived as more morally wrong than tax evasion with cryptocurrency. This finding fell in line with one of the two alternative hypotheses (H1alt) of Study 1. As a justification for this hypothesis, we noted that the use of a particular monetary instrument by the wrongdoer may evoke the image of an unpleasant (vs. pleasant) person, which may in turn cause the observer to perceive the wrongdoing as more (vs. less) wrong. Study 2 further theorizes upon this mediation mechanism.

Study 2

Individuals see and judge objects, thoughts, and other individuals through prototypes and stereotypes (Lakoff, 1986). When judging the actions of others, people tend not to judge each action alone but also shape their judgments based on associations and stereotypes pertaining to the action's performer (e.g., the little Hannah experiments; Darley & Gross, 1983). Such categorization and stereotyping effects have been widely demonstrated in relation to such factors as gender roles, ethnicity, and religion (Bar-Tal & Teichman, 2009; Czopp, 2010; Eccles et al., 1990; Hilton & Von Hippel, 1996).

Preliminarily, we theorized (H1alt) that if the monetary instrument used by the wrongdoer evokes unpleasant (vs. pleasant) associations about that person in the observer, then the observer may correspondingly perceive the person's wrongdoing as more (vs. less) wrong. Considering that our research empirically focuses on cryptocurrency vs. stock traders, it should be noted that stock traders are often linked with negative stereotypes (e.g., The Wolf of Wall Street). Conversely, it appears that no established stereotypes have been associated with cryptocurrency traders to date; alternatively, cryptocurrency traders may be associated with the positive stereotype of smart, tech-savvy experts of the new economy. Indeed, in a recent poll on the perceived honesty/ethics of various professions, stockbrokers were ranked fourth from last out of twenty professions; only 16% of the respondents rated the honesty/ethics of stockbrokers as high (Gallup, 2018). Thus, the use of stocks (vs. cryptocurrency) as a monetary instrument may lead observers to attach more (vs. less) negative stereotypical characteristics to the focal performer of the action. This may in turn lead observers to perceive greater wrongdoing when tax evasion is performed with stocks vs. cryptocurrencies. More formally, we hypothesize that the observer's affective evaluation of the focal performer's character mediates the main effect of cryptocurrency vs. stocks on the perceived wrongness of tax evasion, such that:

Method

Participants

One hundred and fifty-three participants were recruited through the same platform used in Study 1 (ProA). All participants were US citizens, aged 18–65 years (Mage = 33 years; 53.6% male, 45.8% female, < 1% other).

Design and Procedure

The design of Study 2 was identical to that of Study 1, except for the inclusion of the hypothesized mediating variable: the observer's affective evaluation of the focal actor's character.

Measures

The mediating variable—the observer's affective evaluation of the focal actor's character—was measured with three pairs of adjectives, which were bipolar in terms of positive vs. negative valence: agreeable vs. disagreeable (Hopper & Williams, 1973; Rydell & Durso, 2012; Scott, 1967; Um, 2013), constructive vs. destructive (Kammrath & Scholer, 2011; Scott, 1967), and positive vs. negative (Kammrath & Scholer, 2011; Scott, 1967). These pairs were measured with a nine-point semantic differential scale, in which a higher value denoted a more negative affective evaluation. This three-item scale had high reliability (α = 0.883). In the data analyses, we employed a variable that averaged each participant's responses to the three items of this scale.

The dependent and control variables in Study 2 were the same as in Study 1. No statistical relationships were found between the experimental groups and the background variables of gender (p = .305), age (p = .505), educational level (p = .0.067), political orientation (p = 463), employment status (p = .478), and income level (p = .768).

Results

First, we analyzed the main effect, as in Study 1. Again, the monetary instrument of tax evasion was found to significantly influence the observer's perceptions of moral wrongdoing (F1,15 = 6.90, p < 0.01). That is, tax evasion with cryptocurrency (M = 6.40, SD = 2.45) was perceived as less wrong than tax evasion with stocks (M = 7.41, SD = 2.30). This result replicated the main effect result of Study 1.

As a preliminary analysis of the mediating effect, a one-way ANOVA was conducted to address H2a and test whether the monetary instrument impacted the observer's affective evaluation of the transgressor's character. As predicted, the monetary instrument influenced the observer's affective evaluation of character (F1,15 = 4.026, p < .05), such that the transgressor who used cryptocurrencies was perceived less negatively (M = 4.98) than the transgressor who used stocks (M = 5.54).

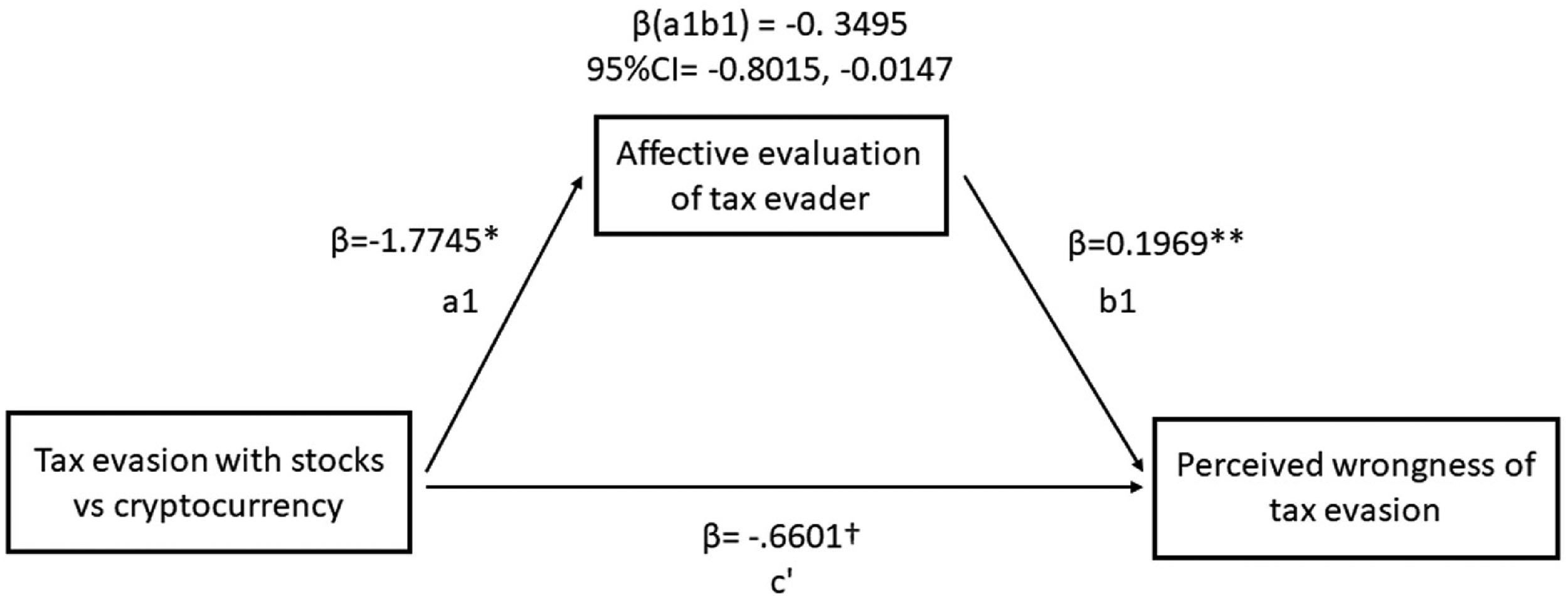

H2b hypothesized that as the observer's affective evaluation of the wrongdoer becomes more positive (vs. negative), the perceived wrongness of the act of tax evasion deceases (vs. increases). A formal mediation analysis was conducted using Model 4 of the Hayes PROCESS macro 3.4 (Hayes, 2013) in SPSS 26, with a bootstrap resampling of 5,000. Figure 1 presents the results of the mediation model. As anticipated, the path from the monetary instrument to the perceived wrongness of the action through the observer's affective evaluation of the performer's character was significant and did not include zero (indirect effect, B = −.3495, SE = .200; 95% CI = −.8015 to −.0147), thus supporting mediation (direct effect, B = −.6601, SE = .3499; 95% CI = -13513 to .0311). Specifically, the monetary instrument impacts the observer's affective evaluation of the performer, which affects the observer's judgement of the wrongness of the performer's actions.

Mediation model result (* < 0.05, ** < 0.01, †>0.05).

Discussion

The result of Study 2 replicated the main effect result of Study 1, thus supporting H1alt (i.e., tax evasion through cryptocurrency trading is perceived as less wrong than tax evasion through stock trading). Furthermore, this study tested the theorized underlying mechanism of this main effect through mediational analysis. Specifically, the mediational analysis provided evidence of the underlying mechanism of the monetary instrument's influence on the observer's affective evaluation of the transgressor. Consistent with H2a and H2b, the observer's affective evaluation of the transgressor mediates the effect of the monetary instrument on the observer's moral judgement of the transgressor's wrongdoing. That is, the use of cryptocurrency (vs. stocks) in tax evasion led to higher (vs. lower) affective evaluation of the tax evader (H2a), which in turn led the observer to perceive lower (vs. greater) wrongness of the tax evasion act (H2b).

General Discussion

Contributions to the Literature

Given the increasing proliferation of cryptocurrencies in markets and the lack of studies on consumer perceptions of cryptocurrencies, the present research set out to explore whether moral transgressions are judged differently when committed with cryptocurrencies vs. stocks. The two present studies showed that people tend to judge tax evasion as less wrong when it is performed with cryptocurrencies vs. stocks. This result is somewhat surprising given the government and media attention paid to cryptocurrency as a means of money laundering (e.g., Rooney, 2019), fraud (e.g., OneCoin; Bartlett, 2019), and other illegal activities. Furthermore, this relationship is explained by the perceived character image of the person performing tax evasion.

Our results provide four contributions to five streams of literature. First, they extend upon the literature on consumer attitudes toward monetary instruments in general (e.g., Ching & Hayashi, 2010; Schuh & Stavins, 2010; Simon et al., 2010). Second, they extend upon the literature on moral judgment (Cushman, 2008; Fincham & Jaspars, 1979; Schein & Gray, 2018; Shultz et al., 1981). This paper adds cryptocurrencies to the list of monetary instruments studied in these streams of research, which also includes cash, checks, money orders, debit/credit cards, and investment securities. In essence, the two present studies show that compared to the use of a more traditional monetary instrument (stocks), the use of cryptocurrencies to perform a moral transgression causes consumers to perceive the transgression as less wrong.

Third, we found evidence of an underlying mechanism for the discovered effect, which is new to the literature on moral judgments. That is, our results indicate that a monetary instrument may shape the perceived wrongness of an action conducted with the instrument by evoking positive vs. negative stereotypical affective evaluations of persons who use the instrument. In the present case, more negative associations were evoked with the stock trader (even when they were a friend of the observer) than with the cryptocurrency trader. While prior research has revealed the effects of stereotypes on moral judgments in general—particularly with respect to gender roles, ethnicity, and religion (Bar-Tal & Teichman, 2009; Czopp, 2010; Eccles et al., 1990; Hilton & Von Hippel, 1996)—research on instrumental and situational triggers is lacking. The present findings add to the literature on moral judgments and the manner in which instrumental cues (e.g., monetary instruments) can evoke negative associations of character.

Fourth, this research contributes to the emerging literature on cryptocurrencies (e.g., Almeida & Gonçalves, 2023; Bhimani et al., 2022; Johnson et al., 2023; Vidal-Tomás, 2022). To our knowledge, the present studies are among the first to address consumers’ moral judgments of cryptocurrencies, extending upon the previous studies that have addressed consumer perceptions of cryptocurrencies in general. The finding that tax evasion is perceived as less wrong when committed through cryptocurrency trading vs. stock trading and the mediating effect of character evaluation are new to this literature as well. The mediating effect is especially interesting because it implies that despite the negative publicity surrounding the use of cryptocurrency to commit criminal activities (e.g., drug, weapon, and sex trafficking), consumers may still associate cryptocurrency users with more positive images in comparison to stock traders. Alternatively, cryptocurrencies are so new and unfamiliar to most consumers that they do not yet have any strong prototypical associations with cryptocurrency users.

Finally, the present research also adds to the literature on tax evasion and tax morale (Alm et al., 1995; Di Gioacchino & Fichera, 2020; Kemme et al., 2020; Luttmer & Singhal, 2014). While previous research has indicated that tax evasion vs. morale is influenced by moral judgments (Bobek et al., 2013; Luttmer & Singhal, 2014; Nordblom & Žamac, 2012; Traxler, 2010), our results contribute the insight that consumer perceptions of the wrongness of tax evasion also depend upon the monetary instrument with which the taxable income is accumulated. Although the experimental setting exposed consumers to a scenario involving tax evasion by a friend, the consumers’ responses likely reflect their own values concerning the acceptability of tax evasion.

Societal Implications

Given that cryptocurrencies are relatively new, strong stereotypes of cryptocurrency users or investors have yet to be depicted in the news or in fiction. Conversely, many films have depicted stockbrokers as villains (e.g., the 1987 film Wall Street, the 2013 film The Wolf of Wall Street, and the 2015 film The Big Short). The familiarity of these images (a.k.a. the Wolf of Wall Street effect) may explain why tax evasion with stocks is perceived differently from tax evasion with cryptocurrencies.

There is an inherent risk to society if people judge financial crimes as less severe (i.e., less wrong) when they are committed with monetary instruments that are new or outside the established norms. New technologies (e.g., cryptocurrencies) may change consumer perceptions of old crimes (e.g., tax evasion), thus directing consumer attitudes toward the perception that these crimes are less morally wrong and that their perpetrators are more amicable, as demonstrated by this paper. This may in turn cause some crimes to appear more permissible in the eyes of the public by altering the norms surrounding these crimes, especially norms and perceptions concerning the perpetrators of these crimes.

Even researchers know very little about cryptocurrency users. In general, there is a scarcity of publicly available information on cryptocurrencies, their initiators, their producers, and their users. This is partly due to the pseudo-anonymous, decentralized design of cryptocurrencies. In other words, cryptocurrency users are not registered by name or identified in any way. Furthermore, there is no central authority to keep records of cryptocurrency users or transactions. So-called cryptocurrency wallet programs can be installed by anyone, and they are immediately connected to the peer-to-peer network (i.e., the blockchain) that facilitates cryptocurrency transactions. For this reason, cryptocurrency transactions between wallet programs are not analogous to person-to-person currency transactions conducted through the banking system.

Voltaire (Beccaria, 1872, p. 20) argued that equal crimes should be judged equally independent of the characteristics of the criminal. Kant formulated very similar arguments in his principle of equality in Groundwork of the Metaphysics of Morals (published in 1785). From these roots to modern moral foundation theory (Graham et al., 2013; Haidt, 2012), the idea that an equal punishment should fit an equal crime has been well established. However, the present research shows that simply altering the instrument of a crime, ceteris paribus, can change the way in which people judge the crime or at least the criminal.

In a legal context, decades of research have already shown that criminal sentencing is affected by external, legally irrelevant factors, such as family background, ethnicity, facial features, and socioeconomic status (e.g., Daly, 1987; Greenberg, 1977; Steffensmeier & Demuth, 2006; Wilson & Rule, 2015). The present research explored the antecedents of criminal sentencing: the moral judgement of a moral transgression and the manner in which this judgment is affected by seemingly external or irrelevant factors. The results of this research may serve as a warning for public policy makers and tax authorities to look beyond the mere tax code or written law when formulating policies and regulations to mitigate the risks that may be posed by new technologies (in this case, monetary technologies). This and any future research on this subject may also serve as a reminder of how easily our intuitions on moral and ethical choices are influenced by the application of old rules of thinking to novel, modern circumstances.

Is there any risk that people may judge crimes conducted with modern tools more leniently than the same crimes conducted with older tools? As we enter a new era of novel technologies, which can be used to commit crimes and other wrongdoings, it is difficult to precisely predict how these developments will impact the moral judgment of transgressors and transgressions. Old stereotypes appear to weigh on these judgments most heavily, possibly because newer stereotypes have not yet been formed. At present, high-speed, computerized stock index manipulation appears to result in milder convictions than bank robbery. For example, the recent LIBOR manipulation scandal led to only one conviction (Bray, 2016). Such stories shape people's beliefs and trust in the judiciary system and affect their moral judgment of financial crimes.

Limitations and Future Research Implications

The present research had two major limitations, which may affect future research directions. First, our study data were collected in autumn 2018 and thus reflect how cryptocurrencies were perceived at that time. As of 2023, cryptocurrencies and especially cryptocurrency trading are still considered a new phenomenon. However, the public visibility and discussion of cryptocurrencies have changed since 2018. For example, the value and trading volume of Bitcoin have come down from their highs in 2018 and skyrocketed once more in 2021. We do not know whether or how this might have affected people's perceptions and judgments of cryptocurrencies. However, as with any innovation, we recognize that people's attitudes toward cryptocurrencies may change rapidly with the emergence of new use cases, applications, and use experiences (e.g., Open AI:s WorldCoin) or with alterations in the sentiment of news coverage. Given this potential for fast-paced change, it would be worthwhile for future research to replicate the present study in order to address changing attitudes toward and knowledge of digital currencies as well as their impact on behavior. Nevertheless, we believe that the underlying mechanisms and dispositional behaviors revealed in the present research will not substantially change even if attitudes toward cryptocurrencies change in a positive or negative direction.

Second, our study data were collected in the United States, and geographical differences in the usage of digital monetary instruments may affect the impact of cryptocurrencies on consumers. Cryptocurrency investing and trading is largely dominated by users in the US, Russia, and the UK (Coin Dance, 2019). Other countries may also have large trade volumes, but it is suspected that users in other countries may use cryptocurrencies for very different reasons. For example, in 2018, the fourth-largest Bitcoin trading volume of 707 million dollars came from Venezuela, which also hit its hyperinflation peak of 1,698,488% for its ordinary currency in the same year (Stasio, 2019). Therefore, Venezuelans are likely to have used cryptocurrency as a haven for their savings in situations where their own currency was in free fall. Correspondingly, it can be assumed that the cryptocurrency-related attitudes and behaviors (including moral judgments) of people in such countries are significantly different from those of people in countries like the US. For example, the use of cryptocurrencies as a haven for money in a falling economy is a very different use case from the crypto day trading carried out in the UK. Therefore, we recommend that future research replicate the present studies and geographically extend them to a variety of countries beyond the US.

Concluding Remarks

The present experiments show that the instrument used to commit a moral transgression affects people's moral condemnation of that transgression. As to the explanatory mechanism of this effect, the second experiment demonstrated that the stereotypical image associated with the transgressor depends on the instrument used to commit the transgression. As two different murder weapons may invoke different images of a killer, the present results suggest that this psychological mechanism extends to the monetary instruments used to commit transgressions. Even if cryptocurrencies per se are associated with unethical issues (e.g., drug, weapon, and human trafficking), consumers may still consider the use of cryptocurrencies to decrease the perceived wrongness of other transgressions (e.g., tax evasion).

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Author Biographies

Appendix 1

“You meet a friend for lunch. They tell you about a new investment website online that operates in another country. During the last year, they got a hang of trading and started making steady profits on their investments. Eventually, they concentrated all their investments in

By the end of the year, they made 100% profit on their initial investment. The website does not provide automatic tax reporting to the government, and your friend decides not to inform the tax authorities on the profits.”