Abstract

The macromarketing literature has devoted substantial attention to marketing systems including those in emerging and developing countries. However, the market development of ‘endogenous’ products, which are products that are rooted in Africa’s natural- and socio-cultural resources and systems, is still understudied. Drawing on the 4As-framework and an exploratory qualitative study that examines market growth constraints for a product in Benin, this paper develops a descriptive theoretical model of market development for African endogenous products. The findings show that markets can be developed through endogenous marketing systems, because traders are familiar with the products and, once markets in easy-to-reach areas become saturated, they advocate their use in new market areas. Through this process, markets potentially grow from urban to peri-urban and rural areas. Because endogenous products have an inherent competitive advantage over foreign products, they deserve support in development policies next to the large commodities that typically characterize Africa’s production portfolio.

Introduction

Exploiting the nutritional-, medical- and economic potential of endogenous products is an opportunity to promote African economies and combat malnutrition (Ayenan and Ezin 2016; Chivenge et al. 2015). Endogenous African products stem from within the natural, socio-cultural and economic systems in Africa (Ingenbleek 2019) and include in particular neglected and underutilized food products, such as leafy vegetables, legumes, fruits and edible roots that have been maintained for their cultural and traditional value (Dansi et al. 2012; Gruère, Nagarajan, and King 2009). They, therefore, not only increase consumers’ quality of life as they diversify diets, but they may also help to improve food security because they provide vital nutrients (Manap 2015). Because they draw on Africa’s rich diversity of natural resources (Meredith 2014) they constitute a source of sustainable competitive advantage for African firms (Ingenbleek 2019) and can play a crucial role in the income generation of small-scale farmers in Africa (Dansi et al. 2012). By enlarging the demand for endogenous products, Africa’s heritage is therefore leveraged to help shape its future.

In many African countries, the marketing of endogenous products is however constrained by, among other factors, infrastructure, facilitating technologies, legal frameworks and institutional regulations that increase transaction costs (e.g., Adekambi, Ingenbleek, and van Trijp 2015; Arnould and Mohr 2005). As a result, markets are often fragmented, with the preferences and available products and services differing between communities (e.g., Layton 2009; Wooliscroft and Ganglmair-Wooliscroft 2018). Such market fragmentation prevents the development of economies of scale (Redmond 2018; Sheth 2011) and hinders the development of marketing systems, quality of life and economic growth, as consumers have access to less diverse product assortments (Layton 2009).

Market fragmentation can be reduced through market creation (Ingenbleek 2014; Layton 2019). Markets are created through the expansion of market infrastructure that enables and governs market exchanges such as regulations, technologies and roads and then developed through business activities (Kotler and Armstrong 2010; Lee, Struben, and Bingham 2018; Tedlow 1996). Infrastructural boundaries are expanded through, governmental investments (most often) that allow businesses to expand distribution networks at lower costs than before (Tedlow 1996). Within the extended infrastructural boundaries, markets are developed by companies using marketing instruments (e.g., Kotler and Armstrong 2010) that help businesses to reduce differences in information, quantity, quality, and price of their products between markets and effectively implement their standardized marketing strategy (e.g., Kotler and Armstrong 2010; Perreault and McCarthy 2002).

Our study focuses on this second step of market creation, which we refer to as market development (Ansoff 1957). Market development, sometimes labeled market formation (Lee, Struben, and Bingham 2018), or market shaping (Nenonen, Storbacka, and Windahl 2019) establishes or intensifies connections in the stages of the marketing system towards the consumer-end (e.g., O’Connor and Rice 2013; Redmond 2018; Sredl, Shultz, and Brecčić 2017). To ensure a stable supply for consumers and retailers it also requires changes in the deeper layers at the supply-side of the system (e.g., Layton 2007, 2015; O’Connor and Rice 2013). Because of these profound consequences for marketing systems, market development is also a macromarketing phenomenon.

The marketing literature has provided useful insights in market development from three different angles. Firstly, several authors address market development as an issue that foreign companies will be faced with when entering African markets (e.g., Prahalad and Hammond 2002; Sheth 2011). However, African businesses that aim to increase the uptake of endogenous products will find few relevant insights into this stream of literature, as it focuses on resource-rich foreign businesses. Secondly, subsistence marketplaces literature provides insights into the behaviors of consumers and entrepreneurs who live close to or under the monetary poverty line (e.g., Chikweche and Fletcher 2010; Viswanathan, Rosa, and Ruth 2010). This stream of literature helps mainly to understand how consumers and entrepreneurs cope with scarcity within isolated local markets but provides few implications for local businesses to grow beyond local marketplaces. Thirdly, the macromarketing literature shows how marketing systems emerge and develop to fulfil the needs and improve the welfare of society (e.g., Layton 2007; Wooliscroft and Ganglmair-Wooliscroft 2018), including marketing systems in challenging places such as in emerging and developing countries (e.g., Godinho et al. 2017; Hounhouigan et al. 2014; Viswanathan, Rosa, and Ruth 2010). This stream of literature has however not yet theorized how marketing systems change when fragmented markets are aggregated in a process of market development.

This study aims to empirically develop a descriptive model of market development for endogenous products using a qualitative approach. The study combines the 4As-framework as the basic theoretical structure for market development (Prahalad and Hammond 2002; Sheth and Sisodia 2012) with supply chain management perspectives that can provide insight into reducing supply constraints of endogenous products (e.g., Porter 1990).

The study analyses the causes of the current fragmented market situation of Kersting Groundnut (KG) a typical endogenous product in Benin (West Africa). KG, latin name - Macrotyloma geocarpum, is a tropical legume that is particularly adapted to drought areas, less susceptible to pest attack, has a high protein-content and is richer in amino acids, such as lysine and methionine than most of the other legume crops in West Africa (Ayenan and Ezin 2016; Chivenge et al. 2015). Benin constitutes an appropriate research context for this study, as the country shows characteristics typical of African markets (Nguyen and Dizon 2017). The cultural- and demographic composition of Benin is complex, consisting of more than 40 ethnic groups with different languages, cultural habits and religious affiliations (World Population Review 2018). In addition, accessibility of basic infrastructure, resources and education varies significantly within the country. While paved roads and other public infrastructure, such as electricity supply, are relatively good in urban cities, rural and smaller communities hardly possess them (Dominguez and Foster 2011).

This study makes three contributions. This study is the first to conceptualize a market development model for endogenous products in Africa. By conceptualizing market development in Africa, the study provides insights into the stages of market development, the conditions of occurrence of these stages, and it gives guidance on supply development to fulfil market demand. As such, it also contributes to the thinking on African endogenous businesses (Ingenbleek 2019) in that it explains how such businesses may cope with market fragmentation without investing the large marketing budgets that multinationals can invest. The second contribution of this study is that it adds to the use of the 4As-model in market development. The paper provides insights on how a market development strategy can build on existing marketing systems by using the 4As in a stepwise process of market development. These steps vary in the emphasis they place on particular elements from the 4As-model, starting with improving access to the product in central market areas, followed by greater affordability in these places for the product. The greater affordability in turn stimulates the dissemination of the product to more peripheral regions by first increasing awareness among new consumer groups and then acceptance. Such contingencies within the 4As-model go beyond those recognized by Sheth and Sisodia (2012). As a third contribution, the study explicitly extends market development thinking with supply chain management ideas, thereby, creating a model relevant for other locally produced ‘indigenous products’, for which a stable supply cannot be taken for granted.

The Potential and Challenges of Endogenous Products

Existing studies contend that the economic potential of endogenous products is underestimated and underexploited due to a lack of research and a lack of interest from farmers (Chivenge et al. 2015; Gruère, Nagarajan, and King 2009). Most support in terms of research and agricultural inputs goes traditionally to main staple foods and to agricultural commodities demanded on the world market. This puts the position of endogenous products under pressure (Chivenge et al. 2015). The declining production of endogenous products, particularly threatens nutrition and food security of poor consumers in Africa because these products may contain nutrients that the common staple foods don’t provide (Chivenge et al. 2015).

Another factor that contributes to the relatively weak market position of endogenous products, is that farmers often lack access to profitable markets for these products (Chivenge et al. 2015; Gruère, Nagarajan, and King 2009). Endogenous products are marketed locally, or through the typical African marketing systems that consist of different levels (e.g., Fafchamps 2003). The farmers producing endogenous products depend upon a small number of petty traders to sell their harvest and receive market information, as they live in remote areas (e.g., Adekambi, Ingenbleek, and van Trijp 2015). Petty traders collect small amounts of harvest from several farmers at village level and sell it to bigger traders that operate at regional level. The latter sell their stocks to wholesalers in central markets and from there, the process of distribution reaches the most remote consumers using a fine-grained network of sellers and resellers (e.g., Arnould and Mohr 2005). Because distribution challenges and information asymmetry are widely present in such systems, the development of the markets for endogenous products is constrained by transaction costs (e.g., Fafchamps 2003) that can easily exceed the potential selling prices, especially if transport is difficult and unpredictable due to infrastructural barriers.

Market Development in Africa

As one of the four growth strategies in Ansoff’s classic model (1957), market development is “a strategy in which the company attempts to adapt its present product line (generally with some modification in the product characteristics) to new missions” (Ansoff 1957, 114). Market development is also a macromarketing phenomenon as market development occurs through changes in marketing systems. Layton (2007) contends that marketing systems change by integrating new networks of actors / entities, linkages, and relationships that ensure flow of exchanges (information, finance, possession, ownership and risk). Sredl, Shultz, and Brecčić (2017) specify that marketing systems change following three phases, emergence, growth and institutionalization.

In the context of Africa, market development first requires infrastructural investments in places that are remote and where the last mile distribution becomes too expensive. On the supply side, the same problem occurs with the first mile distribution from farming communities (e.g., Adekambi, Ingenbleek, and van Trijp 2015). Literature in development economics has paid attention to this phenomenon of remoteness and its consequences on input and output markets (Christiaensen, Demery, and Paternostro 2005). Remote communities have limited access to markets and public services and have not benefited from growth during the 1990s in many African countries (see Christiaensen, Demery, and Paternostro 2005).

Once infrastructural barriers are reduced, companies can try to overcome associated barriers, because different communities often have unique development paths associated with unique languages, cultural practices and preferences (e.g., Barth 1998). Once people migrate from rural areas to cities, these barriers may not directly disappear. Therefore, also in urban areas, companies may need active market development strategies. The BoP literature first developed the business case for such strategies in peri-urban and rural markets. Anderson, Markides, and Kupp (2010) suggest that to develop their markets in peri-urban and rural areas, companies need to be ‘part of the fabric’ of local communities, enabling them to develop bottom-up and sustainable market development strategies. This means that companies have to work with village-chiefs and religious leaders, promote local entrepreneurship, and engage in corporate social responsibility activities in the communities. Additionally, Schäfers, Moser, and Narayanamurthy (2018) and Sheth (2011) indicate accessibility and affordability as the first critical elements to be taken into account while developing a market at the BoP, suggesting a hierarchical process of market development. They recommend companies to attract, develop, and maintain relationships with ‘market makers’, namely, socio-political and faith-based institutions and opinion leaders. Once this is done, the next important thing is to convert non-users into users, by “informing, educating, and enabling customers through workshops, social media and channel development” (Sheth 2011, p. 174).

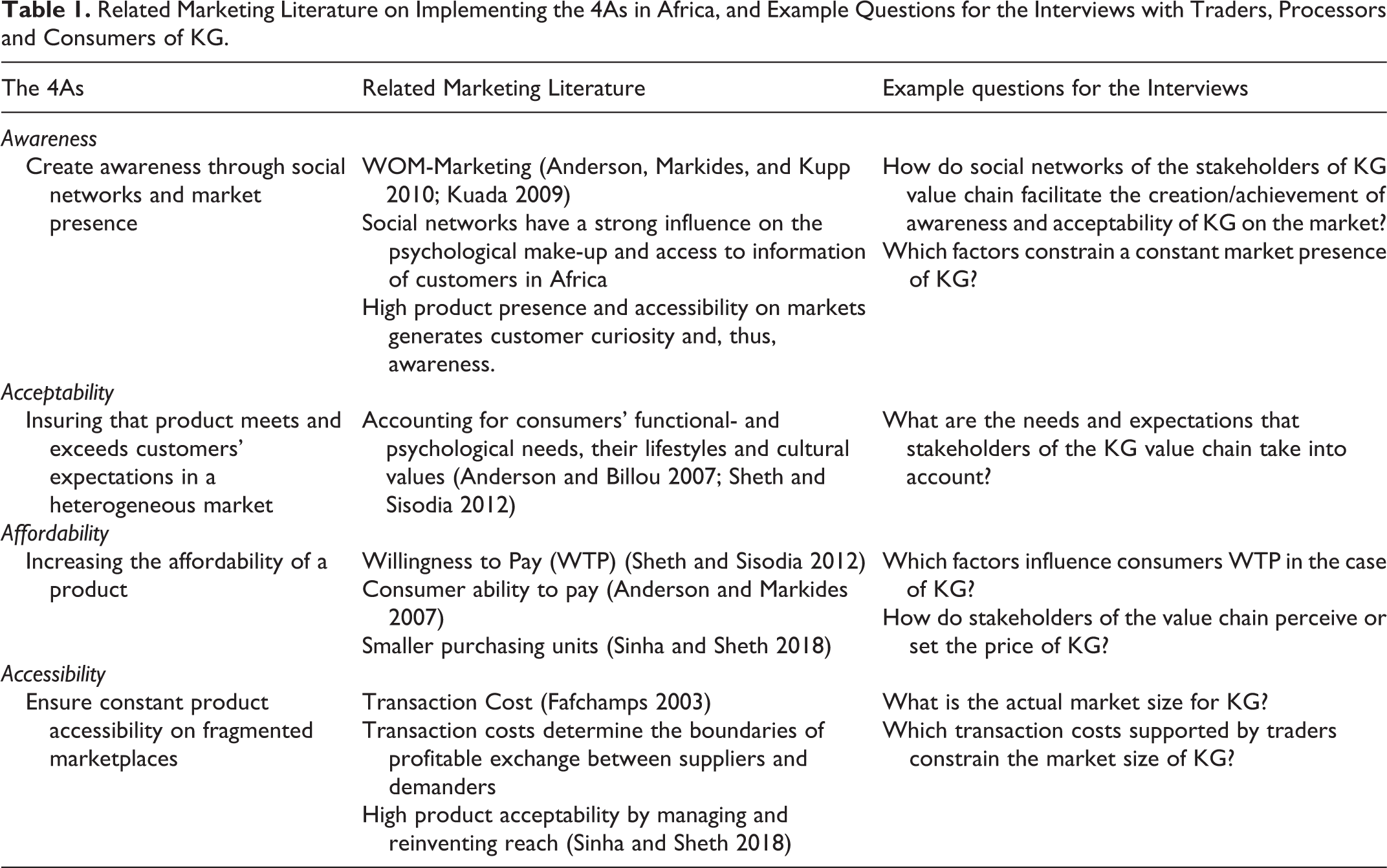

The conditions of marketing in African markets are much more about market-creation than a traditional segmentation, targeting, and positioning, also led to rethinking marketing instruments. Prahalad and Hammond (2002) and Anderson and Markides (2007) in that respect, suggested the 4As: Affordability, Accessibility, Acceptability and Awareness, as an alternative for the traditional positioning-based 4Ps (price, place, product, and promotion). The idea of 4As was stretched further by Sheth and Sisodia (2012) as a more general marketing instruments framework, which we use as a framework for our market development case. We selected related marketing literature that helps to operationalize each market development instrument in the study on endogenous products in Africa (see Table 1). Below we discuss how the four market development instruments can contribute to the development of the market for endogenous products.

Related Marketing Literature on Implementing the 4As in Africa, and Example Questions for the Interviews with Traders, Processors and Consumers of KG.

The 4As-Framework

Awareness refers to the degree to which consumers acknowledge product characteristics and are persuaded to try and repurchase (Anderson and Markides 2007; Sheth and Sisodia 2012). According to Sheth and Sisodia (2012), awareness has two dimensions: product knowledge and brand awareness (e.g., knowledge on the positive associations with endogenous products). Creating awareness is important in Africa, because of limited access to communication media, remote location and high illiteracy level (e.g., Anderson and Markides 2007) many consumers depend on word of mouth (WOM) from social networks for product information (Kuada 2009).

Acceptability refers to the extent to which the product meets and exceeds customer expectations (Sheth and Sisodia 2012). It focuses on functional- and psychological needs of consumers, their lifestyles and cultural values (Anderson and Billou 2007; Sheth and Sisodia 2012). In Africa, product acceptability may vary between consumers, based on their social-cultural background (e.g., Barth 1998). In Africa, many low-income consumers constantly cope with resource scarcity and a fluctuating income. More emphasis is placed on basic needs, such as sufficient nutrients and long storability (Chikweche and Fletcher 2010). Thus, products that reduce consumers’ purchasing risk by providing consistency in quality through standardized attributes have a higher chance of being accepted and demanded in many African markets.

Affordability refers to the ability and willingness of consumers to pay for a product (Sheth and Sisodia 2012). Both the economic dimension (ability to pay) and the psychological dimension (willingness to pay) of the product affordability matter in market development (e.g., Sinha and Sheth 2018). To be affordable, product prices and maintenance costs must be adjusted to the low and inconsistent income of many consumers, and to the consumption patterns of consumers that are additionally shaped by their limited ability to pay (Anderson and Markides 2007). Thus, prices likely needs to be set at a level that enables a sufficient number of consumers to buy products, for example, by increasing supply, reducing production costs or providing smaller purchasing units (Schäfers, Moser, and Narayanamurthy 2018; Sinha and Sheth 2018).

Accessibility refers to the extent to which customers are able to acquire and use the product in an uninterrupted way (Dadzie et al. 2017; Sheth and Sisodia 2012). Accessibility has two dimensions, availability and convenience (Sheth and Sisodia 2012). Accessibility is important for endogenous products due to poor transport infrastructure, disconnected marketplaces and shortages of formal distribution channels, such as supermarkets that many consumers cope with in Africa (e.g., Sheth 2011). Accessibility is also important for endogenous products as these products are often produced on a small-scale. To ensure accessibility, market supply needs to be increased by decreasing distribution and production costs and market linkages need to be strengthened between consumers and actors in the supply chain up to farmers.

Strengthening the Supply Chain

We use Porter’s (1990) diamond model on value chain to help identify factors that influence supply chain efficiency (see Arnould and More (2005) for another application of this model in an African production context). Within supply chains of agri-food sectors, such as those of endogenous products, individual farmers may take the role of ‘firms’ in Porter’s model. The model draws attention to four attributes of competitiveness from an industrial sector: (1) firm strategy, structure and rivalry, (2) factor conditions, (3) related and supporting industries, and (4) demand conditions. These factors may increase insight in constraints of the supply of endogenous products.

Firm strategy, structure and rivalry defines how businesses are organized, define their corporate objectives and face competition. According to Porter (1990), companies with an advanced management and clearly defined goals are more competitive. Additionally, a competitive environment forces companies to improve and innovate to succeed in the market. This attribute may help improve the understanding of how the farmers of endogenous products are organized and what the strategic goal of producing them is.

Factor conditions include different production inputs that may or may not be available and thereby promote or impede the competitiveness of a sector. Porter (1990) distinguishes between basic resources like soil, climate or minerals and advanced resources, such as knowledge, infrastructure and capital. In the case of endogenous products, advanced resources may be critical for development of their supply, as for example Africa faces infrastructure problems (Pels and Sheth 2017; Sheth 2011).

Related and supporting industries evaluate the support that a sector receives from supplying businesses and governing institutions (Porter 1990). While suppliers enhance innovation by developing advanced input factors for businesses, institutions improve contextual conditions, like sufficient infrastructure and legal frameworks. With their informal value chains, endogenous products may suffer from a lack of development of advanced inputs and support from policy makers in many African countries (e.g., Ayenan and Ezin 2016; Dansi et al. 2012).

Demand conditions relate to factors that determine the potential of a market. They include factor, such as market size, growth and sophistication. According to Porter (1990), businesses that supply large and growing markets are more competitive. Supplying sophisticated markets with strict consumer requirements forces businesses to improve and innovate, increasing their competitiveness further. The market for endogenous products may be constrained by the limited knowledge on their processing and growth possibilities (e.g., Ayenan and Ezin 2016; Chivenge et al. 2015).

Jointly, the 4As-framework and Porter’s diamond model lead to the analytical model for African endogenous products sectors. We use these components as case study concepts (Yin 2013) in our analysis (see Table 1).

Method

We designed multiple-case studies to identify context-specific market and supply development instruments for KG in Benin (West Africa) (Yin 2013). KG is a seasonal crop that is harvested between November and December. KG is distinguished by three seed colors (white, red, and black) (e.g., Ayenan and Ezin 2016). The general processing method for KG is to boil the kernels (Adu-Gyamfi et al. 2011). Depending upon the recipe, various types of meat, vegetables and spices are added. The dish is traditionally served, with bread, yam, rice, or ‘gari’, a dish made of dried cassava flour (Adu-Gyamfi et al. 2011; Ayenan and Ezin 2016). The crop can also be further processed as flour for making cakes or used as infant food (Ayenan and Ezin 2016).

Case Selection and Description

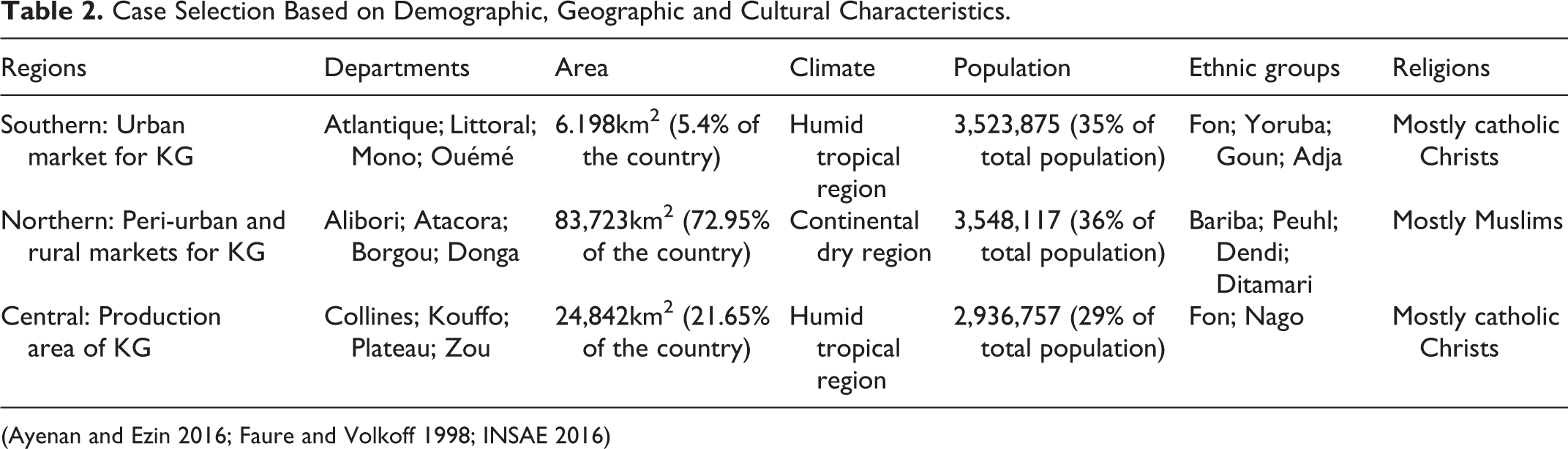

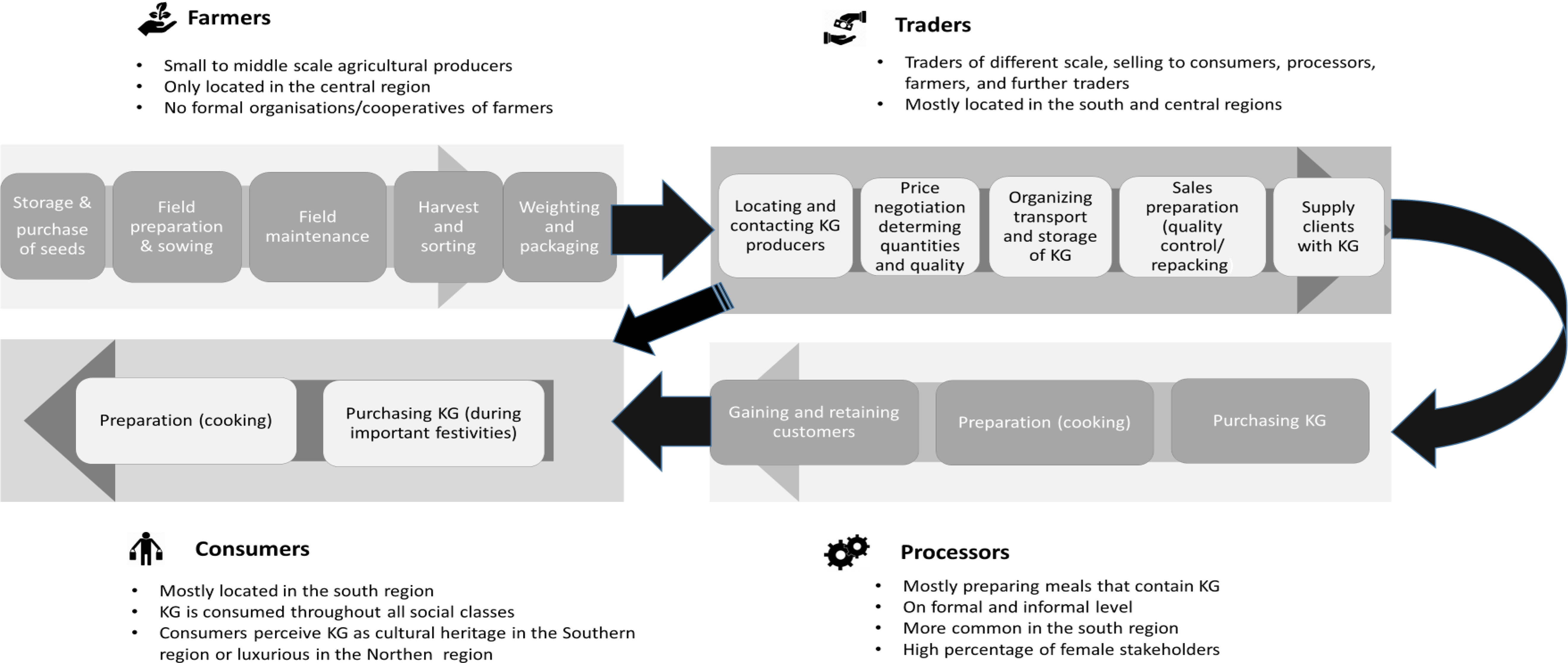

We used three regions of Benin as case studies representing respectively; an urban market, a rural market, and a production zone (Eisenhardt 1989; Yin 2013) (see Table 2 for case characteristics and Figure 1 for the supply chain). The Southern region of Benin is densely populated with a high urbanization rate, widely covered access to public services, such as electricity and piped water, has a relatively well developed transport infrastructure and contains three of the four largest cities of Benin (INSAE 2016; Nguyen and Dizon 2017). The Northern region is characterized by remote rural areas and a small number of urban centers, with 70% of the population living below the poverty threshold of less than US $2 a day (World Bank 2015). While the number of inhabitants is comparable to the Southern region, the Northern region is more than 13 times larger (INSAE 2016). As compared to the Southern region, the Northern region possesses few infrastructure and public services. The Central region is the main KG production region, because its soil- and climatic conditions are favorable to the growth of KG (Ayenan and Ezin 2016). This region constitutes a transition area between the Southern- and Northern regions in terms of access to public services, transport infrastructure and income level (World Bank 2015).

Case Selection Based on Demographic, Geographic and Cultural Characteristics.

Supply Chain of Kersting Groundnut in Benin.

Data Collection and Respondent Selection

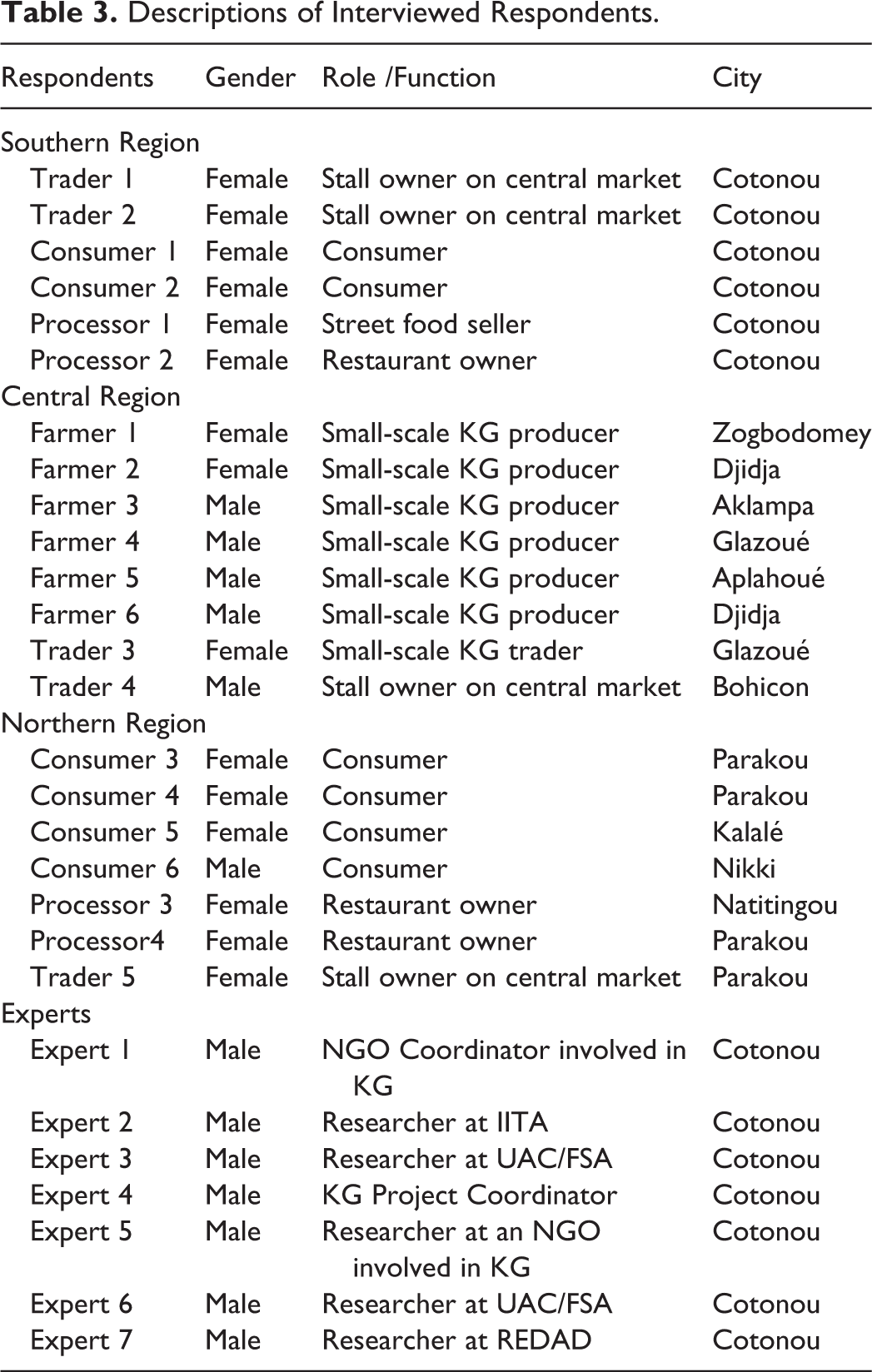

Twenty-eight qualitative interviews with experts and stakeholders of the KG value chain served as primary data sources of information (Table 3). Additionally, observations were recorded in notebooks to help triangulate the evidence and to allow the contribution of emergent questions and unique case features (Eisenhardt 1989). Within each case, we mostly selected either farmers in the production region or traders, processors, and consumers in the market regions. As in this study, farmers, traders and processors are also consumers of KG, we involved six respondents as mere consumers for corroboration purposes. KG farmers from rural areas were contacted through a local NGO with a high reputation among farmers (cf. Ingenbleek, Tessema, and van Trijp 2013). To select traders and processors, we visited open-air markets, supermarkets, restaurants and street sellers.

Descriptions of Interviewed Respondents.

We conducted interviews by using a semi-structured interview guide, based on the 4As-framework (See Table 1 for example questions). Before we started our interviews, we contacted experts at research institutes or NGOs and used their suggestions to further adapt our questions for the specific regions and stages of the KG value chain. Interviews usually started with explanations about the goal of the interview and the study. Subsequently, respondents were asked about their general knowledge of KG and about how they were involved in the value chain. To understand each stage of the value chain in depth, we continued with specific questions formulated for the respective stage that each respondent identified with (Eisenhardt 1989). We started with the expert interviews as they provide in-depth knowledge about the KG value chain, traditional value, current challenges and future market potential of the crop. To get a better idea of how the KG value chain is structured, questions to traders and processors mostly addressed their supply chain, client base and business challenges. Interviews with consumers focused on product knowledge, preferences and consumption patterns. Interviews with farmers deepened our understanding of the value chain and provided additional information about plant characteristics and cultivation methods. Interviews lasted approximately 45 minutes and were recorded. Depending upon the language skills of respondents, interviews were conducted in French, English or Fon - a widely spoken indigenous language in Benin. Because none of the authors spoke Fon, a local translator accompanied the research team during the field research. Interviews in Fon were transcribed into French by a local NGO employee, who spoke French and Fon (Eisenhardt 1989; Yin 2013). Afterwards, we translated all transcripts into English.

Data Analysis

To gain familiarity with each case and generate a preliminary theory, we started our analysis by conducting a within-case analysis of each region (Eisenhardt 1989; Yin 2013). We first grouped transcripts from the same region according to the different stages of the KG value chain present in that region, and read them multiple times to gain a clear understanding of their content (Eisenhardt 1989; Yin 2013). Subsequently, we marked text passages and statements that relate to the 4As-framework (e.g., accessibility) and detected similarities or divergences in statements. In a second round, we deepened our within-case analysis by comparing detected patterns between different stages of the KG value chain to detect cross-stage similarities and differences in statements (Eisenhardt 1989). Following these within-case analyses, we conducted a cross-case analysis by comparing the findings from the two market regions to check and extend our theory (Eisenhardt 1989).

Findings

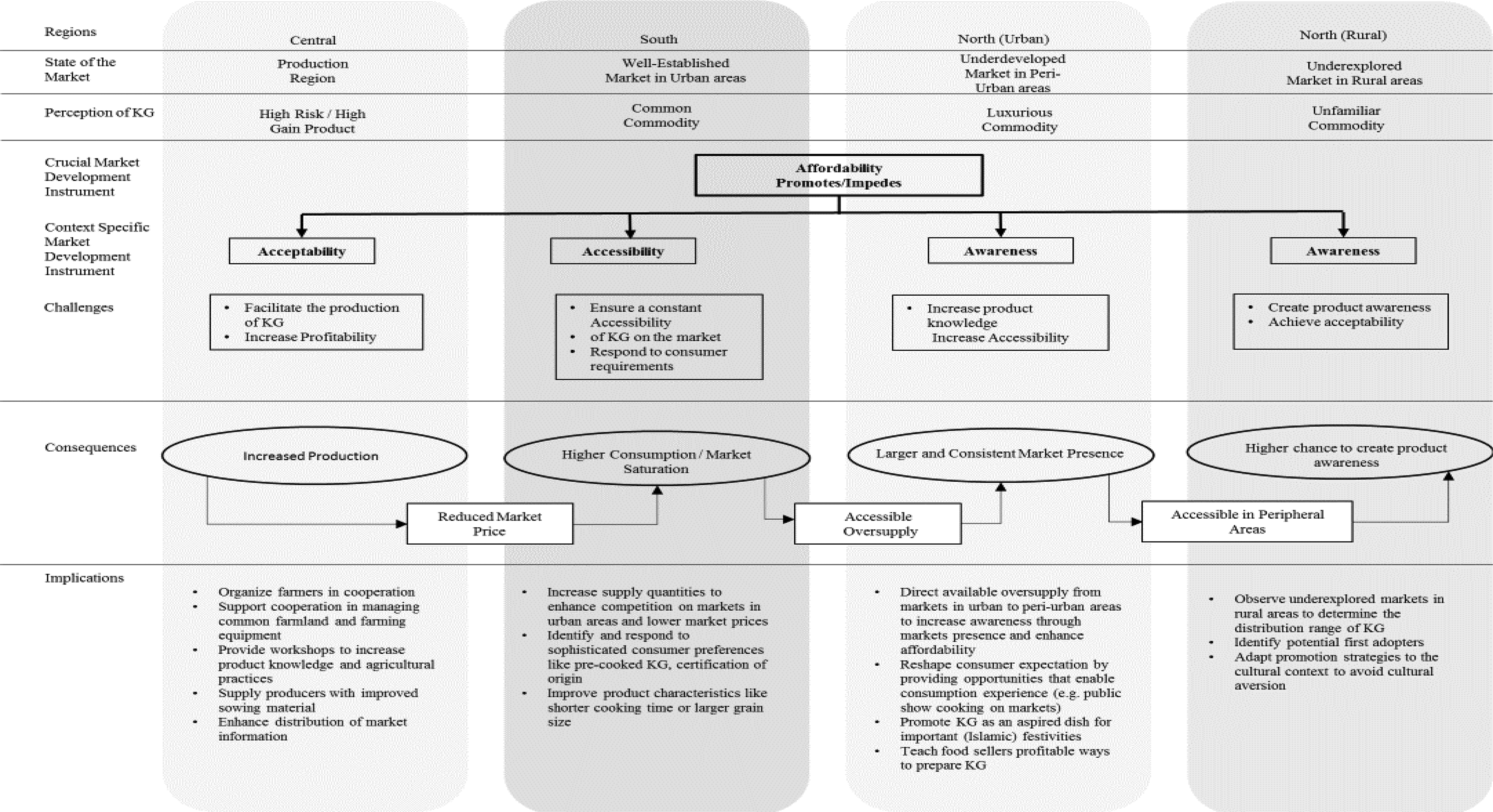

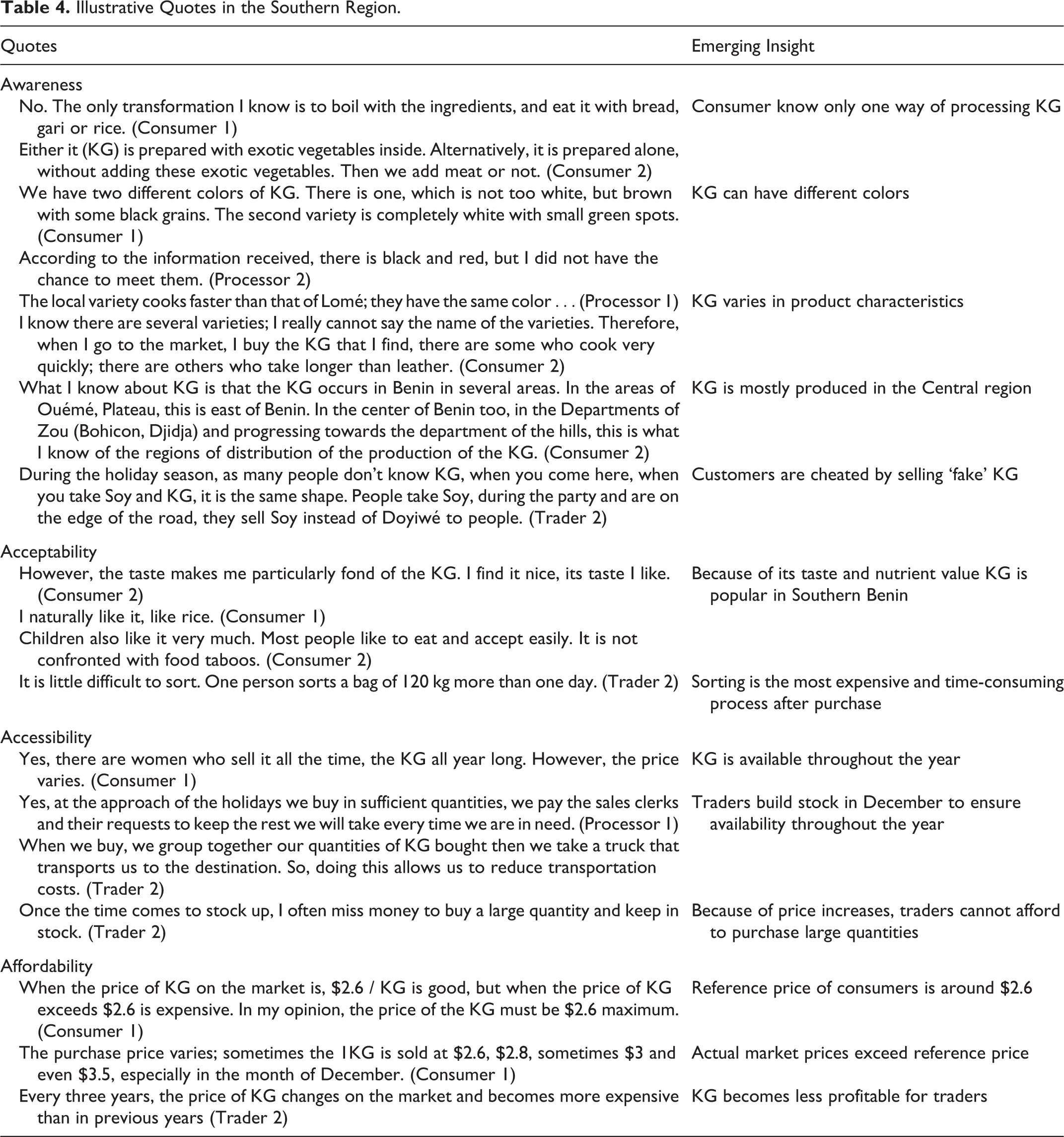

Figure 2 presents the state of the production and marketing of KG, as well as the crucial and contextual market development instruments for KG. As KG in the Central region is perceived as a high-risk – high-gain product due to its climatic sensitivity (long-lasting rainfall deteriorates the grains), high production-costs (seeds, field preparation, and harvest) and high market price, the supply of KG is decreasing. The decreasing market supply of KG reduces its affordability, because prices increase and in turn impedes its accessibility. The lower accessibility in turn hinders further market growth by limiting awareness and acceptability among potential new consumers. While consumers indicate that they are willing to pay approximately $2.6 per kilogram KG, the market prices range from $3 to $3.5 (e.g., Consumer 1 in Table 4). Because the average income of the Northern region is lower than in the other regions (World Bank 2015), KG is perceived as a luxury good that is only affordable during important festivities, while in the Southern region it is seen as a common food product. It is still purchased for special occasions, such as Christmas, but a trend towards more frequent consumption on weekdays is now hindered by the high prices.

Crucial and Contextual Market Development Instruments for Kersting Groundnut.

Illustrative Quotes in the Southern Region.

The Market in the Southern Region

The Southern region appears to be an established market for KG, with high demand for the crop (see Figure 1). Because of the cultural value, most respondents in the Southern region are aware of KG, known as ‘Doyiwé’. Informants described different types of KG that varied in color, grain size (big and small) and cooking attributes (e.g., Consumer 2 and Processor 1 in Table 4). Vendors were, however, selling white KG almost exclusively. Our observation is confirmed by Expert 7 who explained: “now, they prefer white KG, this is what is marketed. Nobody sells the black KG, nobody sells the red KG, and we have never seen it on the market.” Nevertheless, we observed that the white KG that is offered on markets always contained a small amount of black or red grains. Several respondents, e.g. Trader 2, described the existence of a ‘fake’ KG, which looks like KG (in terms of physical appearance) but is less tasty and takes longer to cook compared to KG (e.g., Trader 2 in Table 4). As Expert 3 stated, “especially during Christmas…other things are sold as KG, so there is contamination, a fraud around the resource and this is justified simply because it is expensive, and traders mix it a little to make profit.” Trader 2 was able to organize a sample of ‘fake’ KG.

KG is a highly accepted product in the Southern region as confirmed by Expert 3 “…everyone likes it, you’re not going to see anyone who can tell you, we don’t like it.” Consumers appreciate especially the appealing taste (e.g. Consumers 1 and 2 in Table 4). The crop is mostly consumed during Christmas and New Year as Expert 2 explained “…we consume it a lot during ‘end of the year’ ceremonies…” Processors and traders perceived KG as a profitable business due to its strong demand, as Processor 2 declared: “We sell more KG than other beans.”

However, KG acceptance is hindered by its long cooking time, which does not fit with the changing living conditions of modern urban consumers, as Expert 2 explained: “…consumers don’t have enough time to wait for a long cooking period, they need something quick.” For traders and processors, the time intense of removing trash and stones is perceived as an afflicting process (e.g. Trader 2 in Table 4).

While KG is harvested in December, respondents indicated that it is accessible on central markets in the Southern region throughout the year, which our observations from early March until the end of April confirmed (e.g., Consumer 1 in Table 4). During the harvest season, Trader 2, for example, sent an intermediary to the center of Benin, where she buys large quantities of KG from farmers to build stocks (e.g. Trader 2 and Processor 1 in Table 4). The crop can be found in many restaurants and is often offered by women selling cooked food on the roadside.

However, decreasing supply and lack of storage facilities appear as most constraining to KG accessibility. Respondents and experts agreed that the total quantity of KG available on the market is constantly decreasing as Consumer 2 explained: “…we notice that we have a continual reduction in the amount of KG that arrives in our markets.” According to traders, the ongoing price increase of KG prevents them from buying larger quantities and building stocks (e.g. Trader 2 in Table 4). Available quantities of KG are also limited by the fact that most traders don’t possess sufficient storage facilities to keep bigger stocks of the crops.

Overall, while the white KG is a highly known, accepted and strongly demanded food product in the Southern region, the key challenge for further developing its market is that, KG is not easily accessible throughout the year. Decreasing quantities available on the markets reduce KG affordability that in turn impedes consumers’ abilities to acquire and consume KG in an uninterrupted way.

The Market in the Northern Region

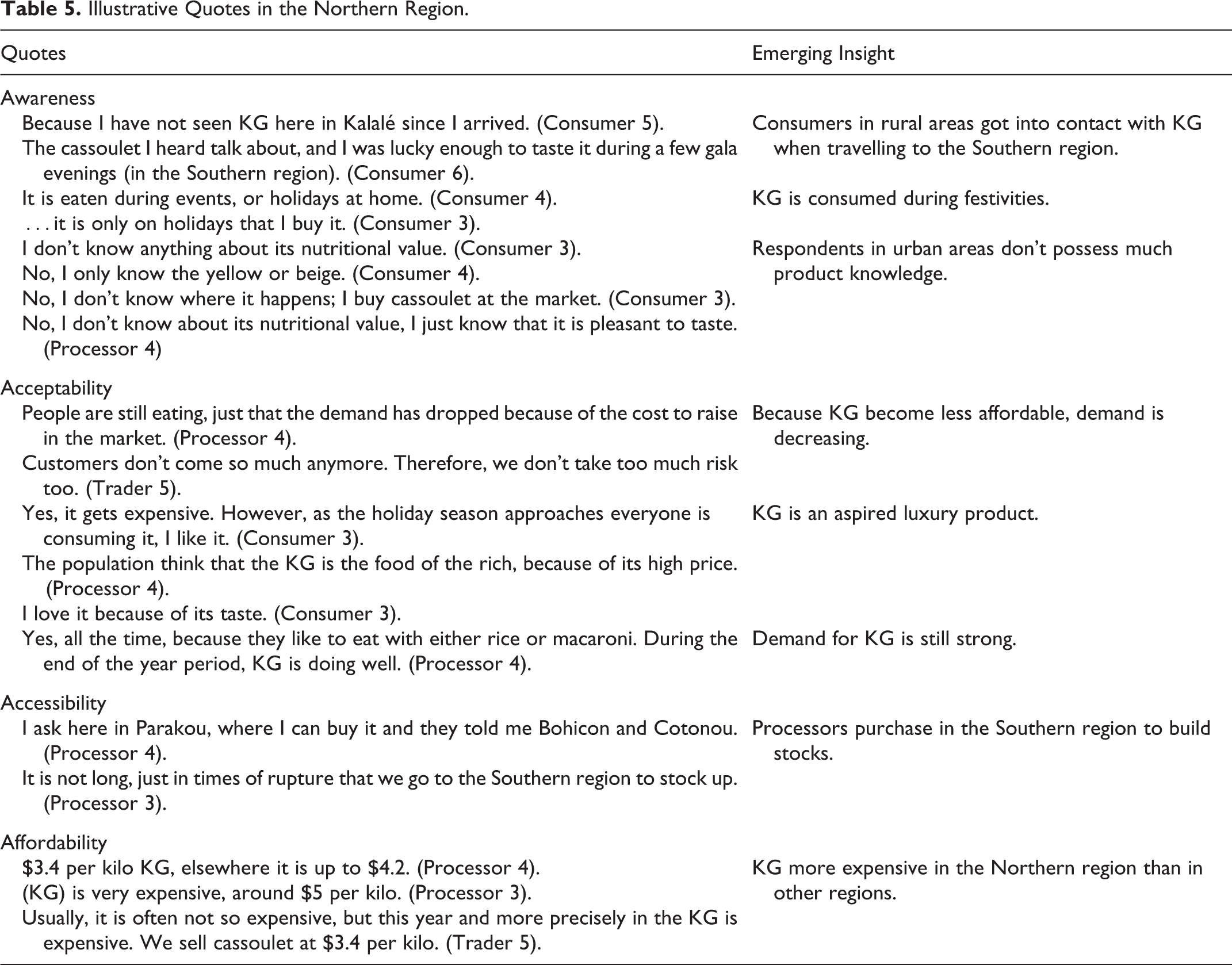

In urban areas of the Northern region, KG is known and accepted, as in the Southern region. As in the Southern region, the acceptability of KG is constrained by its cleaning, sorting, and cooking time and the accessibility of KG is further constrained by decreasing supply of KG. A difference appears between rural- and urban areas of the Northern region regarding the awareness, acceptability, and accessibility of KG (see Figure 1). The rural areas of the Northern region appear as areas in which consumers are not aware of KG. According to them, the crop is “something that they eat in the Southern region”. Respondents explained that they only came across KG when travelling to the South (e.g., Consumers 5 and 6 in Table 5). In contrast, in urban areas, consumers have a relatively lower awareness of KG, as compared to those in the Southern region. Urban respondents in the Northern region only know the white KG, known as “Cassoulet” (e.g., Consumers 3 and 4 in Table 5).

Illustrative Quotes in the Northern Region.

KG seems to be less accepted in rural areas, while it is relatively well accepted in urban areas of the Northern region. As the rural population does not perceive KG as inherent in their culture and consumption habits, the crop is not in demand, as explained by Consumer 5 “…we never come to ask (for KG), our preference is spaghetti and rice.” However, a positive consumption experience of KG seems to enhance KG acceptance in rural areas as consumer stated: “No, it’s not our staple food, it’s just consumed for fun, and now I can eat it for holidays.” Although, KG is perceived as a luxury product in urban areas of the Northern region (e.g. Consumer 3 in Table 5), the crop is well accepted and demanded, especially because of its pleasant taste. Processor 3 stated, “Customers like KG, when some of them come and miss it, they don’t buy anything else.” In the parts of the Northern region, where the crop is increasingly consumed, KG is frequently sold during “the sugar feast and the Tabaski”, important Islamic festivities (Consumer 4, see also Consumers 3 and 4 in Table 5).

Consistent with our observations, Consumer 5 indicated that KG is not accessible in rural areas (“No, I have never seen KG on the market”). In contrast, KG is relatively accessible in urban areas throughout the year with a few market women trading it in small quantities. Traders and processors visit markets in the Central- and Southern regions during the harvest season to build stocks (e.g. Processors 3 and 4 in Table 5). A remarkable observation was the low presence of KG in Northern urban restaurants. KG can only be found in upper-middle-class restaurants or gastronomy outlets that are specialized in dishes from the South.

In summary, the development of the market for KG in the Northern region is hampered by the lack of awareness. In rural areas, there is no awareness of KG, while in the urban areas, the awareness of KG is still lower than in the Southern region. In addition, the lower level of awareness of KG results in a lower level of acceptance of KG by consumers, and KG lower accessibility does not help to either increase its acceptability or demand.

The Production of KG in the Central Region

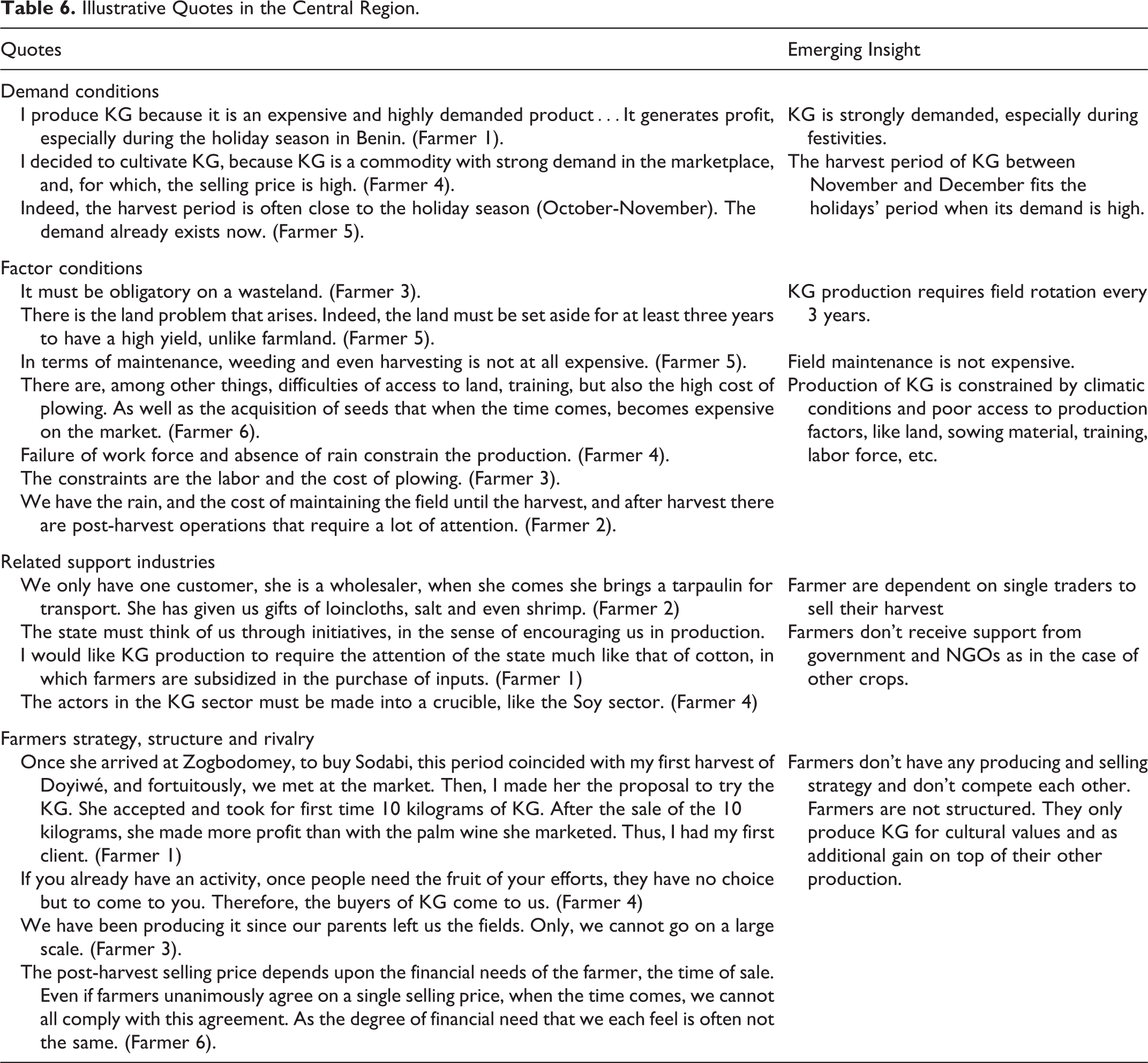

The findings indicate that the production of KG is constantly decreasing in the Central region, the only area of Benin in which KG production takes place (see Figure 1). Respondents don’t seem to have any strategy of producing and commercializing KG. Farmers perceive KG as an additional gain, while other cash crops, like maize, cotton, soybeans or Bambara Groundnut, provide their main source of income. Farmers emphasize the production of KG as a cultural heritage, and its high market price as motivations to produce the crop, as explained by Farmer 6: “producing and marketing KG allow us to cover many of our expenses,”, and Farmer 3: “We have been producing it since our parents left us the fields.” In terms of structure, we observed that farmers have no formal organizations, and grow KG in small-scale next to larger production of other agricultural products, such as maize. Although, farmers are deeply embedded in their communities, which often include other KG farmers, they are not organized in associations or cooperatives. In addition, KG farmers don’t perceive any rivalry or competition, because of the exceeding market demand and the small share of KG in total agricultural production. Consequently, they are less motivated to innovate or improve their production to achieve a competitive advantage.

Although, production knowledge varies significantly between farmers and results in large differences in harvest quantity and quality, respondents indicated that other shared factor conditions, which promote the production of KG, relate to the fact that the plant is resilient to diseases and pest attacks and, therefore, does not require the application of pesticides. In addition, KG does not demand a lot of field maintenance, as Farmer 5 explained: “In terms of maintenance, weeding (…) is not expensive at all.”

Factor conditions that impede the production of KG can be categorized into production-risks and production-costs. Production-risks comprise the sensitivity of KG to soil humidity and fluctuating quality of available sowing material. The plant is not resilient to heavy rainfall, as explained by Expert 7: “If there is a lot of water, it rots”. Because climatic conditions are becoming less predictable, the risk of harvest losses increases, and farmers switch to more resilient crops, as Expert 2 explained: “…farmers go to Bambara Groundnut that can withstand and gives higher yields than KG, which is more sensitive for too much or too less rain.” When poor harvests force farmers to sell their entire yield, they cannot keep seeds as sowing material for the next season. The acquisition of new sowing material on the market is not only expensive, but also does not allow estimating germination rates or yield of the seeds (e.g. Farmer 6 in Table 6). As the quality of the seeds is unstable, farmers regularly face crop failure, as Farmer 1 mentioned: “Sometimes we buy the seeds at the market and after sowing it does not grow.” With the lack of access to certified seeds, some farmers try to store a part of their harvest as sowing material for the next season (e.g. Farmers 1 and 4 in Table 6). To prevent post-harvest pest (bruchid) attacks, most respondents put the seeds in plastic containers and add ash, pesticides, peppers or hot sand (e.g. Farmer 5 in Table 6). However, as Expert 7 stressed: “…the hot sand does not make any sense, as it can kill the seed.” Some practices used by farmers on the seeds to avoid pest attacks, can reduce the germination rate of the seeds.

Illustrative Quotes in the Central Region.

Production costs are related to the access to farmland and labor force. Young people from the Central region migrate to urban areas in the Southern region searching for better income opportunities (Nguyen and Dizon 2017), and, thus, labor force becomes an increasingly scarce production factor as stated by Farmer 6: “…labor force is very difficult to find…” At the same time, KG field preparation is labor-intensive, as plant residues should be ploughed into the soil. As a result, field preparation for KG is four times more expensive than ploughing empty fields, as confirmed by Expert 6: “…ploughing is $0.04 for a 20 m ridge (of empty field) while for KG the ploughing is $0.17”. The cultivation area of KG is further constrained by the lack of tractors and other facilitating equipment, as substitutes to labor force. Farmers end-up using basic tools, like pickaxes, to harvest KG in small-scale production. The access to farmland is further complicated, because the yield quantity of KG decreases when the plant is cultivated on the same farmland for more than three years (e.g. Farmers 3 and 5 in Table 6). Expert 3 confirmed this fact: “If you go over three years, it leaves substances that no longer facilitate good soil performance”. Therefore, the cultivation of the plant requires large farming areas to cope with decreasing yield of KG in ‘spent’ land and that is often either not accessible or too expensive (e.g., Farmers 5 and 6 in Table 6).

The findings also indicate that related and supporting industries virtually don’t exist. As mentioned above, farmers have no specialized suppliers of sowing material and other agricultural inputs like fertilizer. Farmers emphasized that they do receive no support from the government for KG in contrary to farmers of cotton or cashew nuts. Non-governmental organizations have recently become involved in the KG value chain. The same accounts for scientific institutions that just recently started with the collection and characterization of KG samples from West Africa (Ayenan and Ezin 2016).

The current demand conditions of KG are appealing. All farmers indicated KG as a very profitable crop due to its high selling price and strong market demand (e.g. Farmers 1 and 4 in Table 6). In terms of market growth and sophistication, the findings show that KG offers many possibilities to increase the value for consumers. KG characteristics including cooking time and grain size fluctuate, and its value chain only contains minor value-adding processes, like cleaning and sorting. This provides potential for branded products that ensure standardized product characteristics and, thereby, reduce the risk perception of consumers when purchasing KG.

Overall, KG is produced because of its strong market demand and cultural value. Although, KG is perceived as profitable, risky and costly factor conditions and the absence of related and supporting industries impede its production. As KG production satisfies market demand, KG farmers don’t show any rivalry among themselves, but also don’t innovate by organizing groups amongst themselves and developing strategies together that increase their competitiveness.

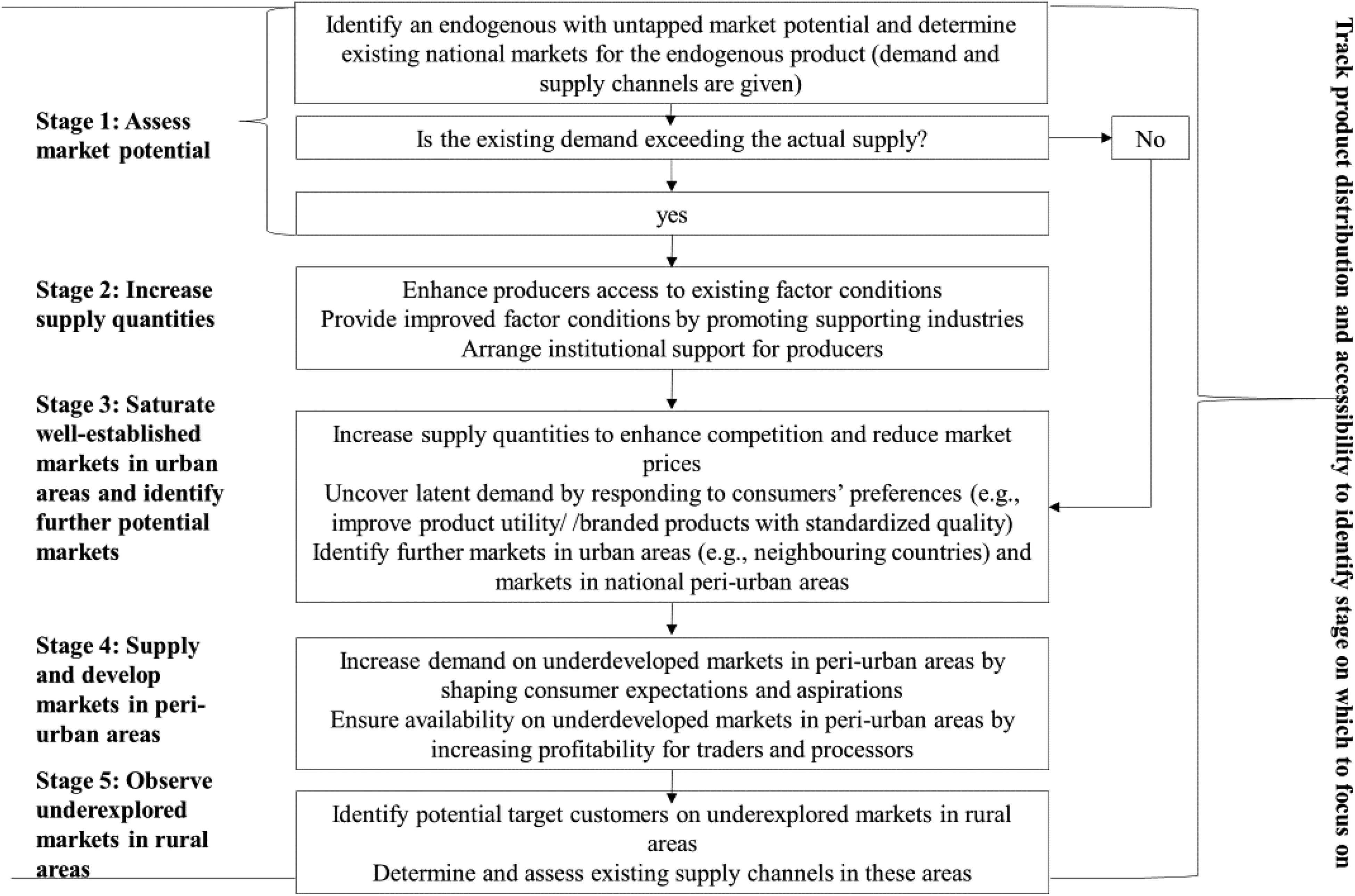

A Market Development Model for Endogenous Products

By analyzing the market for KG in Benin, this study provides insights into the untapped market potential of the crop, which is the starting point of any market development strategy (Ansoff 1957). The findings suggest that the market development of endogenous products can build upon the existing, mostly informal, trading systems, through which such products are traded traditionally (Fafchamps 2003; Layton 2007, 2015; Sredl, Shultz, and Brecčić 2017). Endogenous products are well known to local traders, and close to their cultural heritage and understanding (e.g., Chivenge et al. 2015; Dansi et al. 2012). This became apparent in the case of KG from the involvement, through which traders spoke about the product as ‘Doyiwé’ in the Southern region and ‘Cassoulet’ in the Northern region, such that an imported product or products supplied by multinationals would not be part of such cultural associations (e.g., Godinho et al. 2017). Traders can also act as endorsers, thus, extending awareness, acceptability and accessibility of endogenous products, as soon as their well-established markets in urban areas are saturated. In fact, during our data collection, we saw that due to the decrease in supply the accessibility of KG actually declined. Despite the benefits of the crop, the market for KG did not develop, but rather KG moved out of the capillaries of the system, in which it once went or could potentially go. As the marketing system is still in place, this process can be halted and even reversed, if KG production goes up and accessibility increases (e.g., Redmond 2018; Sredl, Shultz, and Brecčić 2017). Consequently, KG will become affordable and once the urban markets become saturated, traders will bring the product to peri-urban and rural areas. Where the product is less known, they may create awareness by persuading smaller traders to purchase the product and bring it to attention of new customers. Ultimately, every corner of the marketing system can be reached through this process, up to limits at which distribution costs exceed profitability (e.g., Layton 2007; Redmond 2018).

The development of a market for endogenous products can, therefore, be stylized in a five-stage model (Figure 3). In the first stage, the market potential of endogenous products is evaluated by identifying untapped markets that can potentially be reached through the trading system. The market boundaries are not simply a matter of drawing the borders of a map, because distribution costs may be highly dependent upon available infrastructure (e.g., Fafchamps 2003). In the case of KG, the crop is, for example, produced in the Central region, transported to the markets in the South, from where it is often brought by traders to the North, and is potentially distributed further in surrounding areas.

Model for Market Development for Endogenous Products in Africa.

In the second stage, the accessibility of KG is ensured, by increasing the supply of endogenous products to ‘fill up’ the trading system to fulfill the demand in urban areas. In the case of KG, these are the urban markets in the South of Benin, but also for other endogenous products the trade routes are likely to lead to central markets that are usually found in capitals or other central cities (e.g., Fafchamps 2003). The study shows that the production of KG is the most important constraint to develop a market, due to factor conditions.

In the third stage, the affordability of KG is increased because the increased supply allows traders to purchase larger quantities, and thereby, reduces their distribution costs (e.g., Fafchamps 2003). The market price for endogenous products will continuously decrease and markets in the urban areas become saturated. Thus, at this stage, endogenous products become affordable and margins in the urban, saturated markets decrease.

In the fourth stage, traders start creating awareness on new market space. For KG, and again most likely for other African endogenous products, new market potential will be identified in, for example, peri-urban areas and urban areas in neighboring countries (Anderson, Markides, and Kupp 2010; Ansoff 1957; Sarasvathy and Dew 2005). To increase awareness of consumers, social networks and people with central- and leading roles in such networks as traders and processors in the case of KG may be involved to spread product knowledge through WOM (e.g., Kuada 2009).

In the last stage, the acceptability of endogenous products is achieved on the market in rural areas of which the market potential is assessed by identifying suitable target consumers and available marketing channels (e.g., Anderson, Markides, and Kupp 2010; Sarasvathy and Dew 2005). The businesses that trade endogenous products increase acceptance by engaging traders and other stakeholders in rural markets and by adapting to cultural differences. As such, depending on the stage, one “A” gets more emphasis than the others. This finding differs from Sheth and Sisodia’s (2012, p. 34) suggestion that A’s are either independent or can be used in pairs of two.

Implications

Practical Implications

Our study has several practical implications to stimulate the growth of endogenous products. Firstly, to assess the market potential for endogenous products, entrepreneurs or researchers acting on their behalf may follow the traders of these products to see where they end up and investigate why they are not traded further. This investigation will help to understand the current boundaries of endogenous products’ market through the traditional trading system and to identify marketing systems’ linkages that need to be created or strengthened to gain in economies of scale (Redmond 2018; Sheth 2011; Sredl, Shultz, and Brecčić 2017). Secondly, to reduce the costs and risks that constrain the supply of endogenous products, farmers may group themselves in cooperatives to reduce costs, improve access to farm inputs, and organize joint marketing. Research institutes can improve seeds, label the varieties and develop best farming practices that NGOs can disseminate through cooperatives and traders.

Thirdly, once the supply of endogenous products increases, traders can use the available infrastructure more optimally by aggregating demand and by taking advantage of established traditional channels (Sheth 2011). Identifying and responding to sophisticated preferences of urban consumers, for example through processing, branding and origin certification, may strengthen the position of endogenous product businesses on the increasingly competitive urban markets. Fourthly, to increase awareness among peri-urban consumers, traders may strengthen the presence of endogenous products by directing available oversupply from urban to peri-urban markets (Anderson and Billou 2007; Sheth and Sisodia 2012). They may also organize cooking events where they present preparation methods and offer tasting samples and involve opinion leaders like owners of well-known restaurants (Sinha and Sheth 2018). Fifthly, to increase acceptance in rural areas, trading and processing businesses may see endogenous products as investment opportunities for which they should determine the distribution range and identify potential first adopters. Next, they have to adapt promotional strategies to the cultural context to avoid cultural aversion, by promoting the products as a desirable dish for special occasions for example. Teaching food sellers, profitable ways of preparing the products and providing sales incentives to traders may further increase accessibility (Sinha and Sheth 2018).

Implications for Macromarketing and African Endogenous Business Research

This paper has several implications for macromarketing. First, market development is a process that takes place through marketing systems. Our study suggests that formal players in the system that intend to develop a market for endogenous products, can build their market development strategies also on informal actors such as traders who contribute to creating awareness about the products, acceptance, and affordability by increasing access. While other authors have acknowledged that formal and informal marketing systems may exist alongside each other (e.g., Godinho et al. 2017), our study suggests that they can be strongly interconnected and help each other to thrive.

Second, by developing markets for endogenous products, our study implies that the marketing systems providing these products have an impact on societies. This is because endogenous products are directly related to regions or ecological zones where they may grow best. As such, they are likely to be rooted in culture, consumption habits and special occasions. The development of endogenous products may therefore contribute to cultural heritage of specific regions or countries. This is an important implication from our study because several authors have suggested that globalization of the economy in fact puts traditions and culture in developing and emerging economies under pressure due to the increased adoption of “Western” lifestyles and consumption patterns (e.g., Witkowski 2005).

Ingenbleek (2019, p. 201) called in that respect for more research on African endogenous businesses, which are businesses that aim to “create and sustain competitive advantage by integrating Africa’s endogenous natural resource advantages and the economic, social and cultural systems that build on them with modern business practices.” Endogenous products and services can be seen as the outputs of endogenous businesses. The KG case is in that respect typical as it uniquely grows in a particular ecological zone in West Africa. Ingenbleek (2019) further explains how Africa’s main North-South axis gave as one of the biogeographic factors rise to the typical traits of Africa’s marketing system. Our study shows that Africa’s geographic characteristics have provided the continent with unique products that offer not only economic, but also cultural and social types of value. The combination of natural, cultural and social aspects of endogenous products makes these products difficult to imitate by foreign competitors and thus creates a basis for sustainable competitive advantage. Furthermore, the model for market development created in this study shows how endogenous businesses can build on traditional marketing systems to develop the markets for their products with strategies that are also logically explained by the 4As-framework and underlying marketing theories.

Limitations and Future Research

By dividing Benin into three different regions, the study does not reflect the diverting conditions within each region. We also conducted our field research after an exceptionally low KG harvest, which probably explains the low accessibility and high price we observed. Future research can overcome these limitations by longitudinal analyses. Although our model is developed in the specific context of KG, it is theoretically generalizable and can suit further theory development and testing on African endogenous business. The empirical generalizability can be strengthened by examining other cases such as Bambara groundnut and sesame. Likewise, the model can be used to design interventions in the 4As-domains to stimulate market growth. Finally, cross-sectional and longitudinal consumer surveys may help to validate the model.

Conclusion

The present study created a model for market development of endogenous African products, products that have a strong basis for competitive advantage because they are rooted in endogenous natural resource advantages and the economic, social and cultural systems that build on them. The case of KG shows that supply is the most constraining factor in the organic four-stage growth process of market development. While most investments therefore still go to big cash crops and staple foods, endogenous products like KG may miss the momentum to obtain a permanent foothold in Africa’s rapidly growing urban and peri-urban markets. Hence, endogenous products deserve more attention in the African development agenda.

Footnotes

Acknowledgments

The authors thank Patrice Sewade and Sojagnon Association for their help for data collection.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors thank NWO/WOTRO, for funding this project (Food & Business Applied Research Fund, Project Doyiwé, no. W 08.270.344).