Abstract

To err is human and learning from mistakes is essential for finding viable solutions to grand societal challenges through development and innovation. Yet, public organizations often exhibit a punitive zero-error culture, and public employees are stereotyped as error and risk-averse. Little is known about the underlying behavioral mechanisms that determine civil servants’ likelihood of handling errors positively, namely reporting and correcting them instead of ignoring and hiding them to avoid blame. Based on the transactional theory of stress coping, we argue that individuals’ error-handling strategies relate to both rational and emotional evaluations of error-specific and consequential contextual factors. Using a conjoint survey experiment conducted with N = 276 civil servants in Germany (Obs. = 1,104), this study disentangles the effects of error-related, individual, and organization-cultural factors as decisive drivers of individuals’ error response. We find that error characteristics (type and harmfulness) determine error-handling behavior, which is revealed to be independent from organizational error culture and individual error orientation, providing important and novel insights for theory and practice.

Keywords

Introduction

Solving societal and organizational challenges requires an experimental and often pragmatic approach to problem-solving in policy-making and public management. The central prerequisite for finding viable solutions to complex problems is the capacity to learn from the inevitable mistakes along the way. Consequently, an organization's and its members’ capacity to handle errors constructively and proactively is an essential strategic resource for organizational learning and innovation (Argyris, 1991). Public organizations are often characterized as risk averse, only grinding into action if media attention and external pressure are high (Erlich et al., 2021), as well as incapable of handling errors proactively, instead seeking to avoid blame and conceal errors (Eldor & Harpaz, 2019; Hendy & Tucker, 2021; Osborne et al., 2020; Sørensen & Torfing, 2011). Of course, this perspective on public organizations’ capability of error management is stereotypical and negative. Often rooted in political rhetoric and medial bureaucracy bashing, public organizations face an uphill battle against negativity bias in the external assessment of their performance (Marvel, 2016; Piatak et al., 2024). Public organizations are typically held to higher standards than private organizations because they are responsible for providing services essential for the functioning of society, for serving the public interest, and for upholding public values. As public service provider, public administration is particularly likely to serve as political agents’ and voters’ scapegoats in case of performance failure, irrespective of causal responsibility (Nielsen & Moynihan, 2016). This antagonistic climate suggests that public organizations may indeed be incentivized to prevent and conceal errors as much as possible as a blame-avoidance tactic (Bach & Wegrich, 2019). However, and somewhat surprisingly, there is little empirical evidence about how public organizations and civil servants in particular handle errors, calling for empirical research (Tangsgaard & Fischer, 2024; van de Walle, 2016). To date, it is still unclear what factors affect their behavioral response when making mistakes, and what individual, contextual, and organizational factors determine whether civil servants handle errors constructively?

Typical examples of errors in the administrative workplace are, for instance, miscalculated tax reimbursements (Torjesen, 2022) or social benefits (Woodbury & Vroman, 2001), child abuse unrecognized by a social worker (van Ufford et al., 2022), mistakes in the formal execution of an election (Montjoy, 2008), errors in archival case management, and lack of due diligence in public procurement procedures (Simovart & Piirisaar, 2022). To understand the motivational mechanisms that determine individuals’ response to making such mistakes, it is essential to recognize that errors are associated with negative emotions (van Dyck et al., 2005; Zhao, 2011), which may complicate responding in a proactive, constructive, growth and solution-oriented way vis-à-vis avoidant, blame-deflecting, and destructive coping mechanisms. Scholarship on private sector error management often assumes that individuals will detect, share, and analyze errors rationally and with their employer's organizational best interest in mind. This perspective ignores the fundamental challenge posed by the affective component and emotional burden associated with making mistakes for the individual, as well as the particularly consequential nature of public sector errors for society at large. To date, research considering individual motives and emotions as potential barriers to positive error-handling behavior in the context of public administration is still scarce (but see cf. Dahl & Werr, 2018; Lei et al., 2016; Zhao, 2011). Prior research on error handling focuses largely on the private sector and little is known about civil servants’ response to making mistakes. This is surprising given the exceptionally high relevance and potentially high stakes associated with (inefficient) error management in public administration (Tangsgaard & Fischer, 2024).

While behaviors similar to error handling such as whistleblowing (Kang, 2023) have been analyzed in a public sector context before, the fundamental difference between transparently handling one's own mistakes and blowing the whistle on organizational wrongdoings and other people's failures impedes drawing upon the latter stream of literature for error behavior research. Therefore, we focus on investigating how civil servants decide to handle their own workplace errors, with a particular focus on the impact of error characteristics, asking: How do error characteristics determine civil servants’ error-handling behavior?

Following the transactional theory of stress coping (Lazarus, 1966) and prior research on error reporting behavior by Zhao and Olivera (2006), we argue that civil servants challenged with deciding on how to handle their mistakes will either react emotionally or conduct a cost-benefit evaluation to determine whether to hide or communicate their error, and whether to do nothing about it or correct it (Horvath et al., 2021; Patrician & Brosch, 2009). We argue that specific error characteristics determine individuals’ error handling and reporting behavior, and assess these assumptions with a unique vignette-based conjoint experiment conducted with 276 civil servants in Germany.

This study contributes to the literature in three ways, at least. First, we advance the emerging literature on error management in the public sector and contribute to the discourses on sector-specific risk behavior, organizational learning, service failure, and resilience (Eldor & Harpaz, 2019; Mikkelsen & Grønhaug, 1999; Osborne et al., 2020; Tangsgaard & Fischer, 2024; van de Walle, 2016; Weißmüller, 2021). We expand prior research on individual error handling in professional contexts with empirical evidence from the administrative core of the public sector (i.e., ministries, agencies, or citizen service provision centers). Second, prior research on error management primarily focused on meso or macro-level error response (van de Walle, 2016), while our study integrates both meso and micro-level determinants and outcomes from the lens of behavioral public administration scholarship. This is a considerable theoretical advancement. Third, we systematically analyze and contrast the effect of different types of errors and their consequences in context, revealing factors influencing the likelihood of positive error responses, which is of high practical relevance for public management.

The remainder of this study is structured as follows. In the next section, we review the literature on the behavioral foundations affecting individuals’ perception and response to errors. This review converges into ten hypotheses on the relationships between error type and consequences with individuals’ likelihood of reporting (vs. hiding) and correcting (vs. ignoring) mistakes. Then, we present the design and research procedure of our preregistered discrete choice experiment. After reporting the results, we conclude with a discussion of the implications of our findings for theory and practice and derive avenues for future research.

Theory and Hypotheses

Literature Review

Errors are unexpected but potentially avoidable deviations from targeted outcomes and, as such, errors differ from mere inefficiencies (Keith & Frese, 2005; Vanderheiden & Mayer, 2020). At the workplace, human errors originate from physiological, psychological, and cognitive limitations often in the context of fatigue, high workload, and ineffective information processing resulting in flawed decision-making (Helmreich, 2000). Work-related errors lead to poorer organizational performance and service failures (Stewart & Chase, 1999), but also to personnel anxiety, work strain, stress, and lowered psychological safety (Dimitrova et al., 2017). In general, individuals have different approaches to coping with making mistakes. These individual approaches are based on attitudes that are summarized as an individual's error orientation (Farnese et al., 2022). Individuals with a positive error orientation perceive errors as opportunities for learning and growth, allowing them to choose approach-oriented error-handling strategies (Harteis et al., 2008; Rybowiak et al., 1999). These individuals will reflect upon their errors, correct them, and learn from them to prevent similar mistakes in the future (Frese & Keith, 2015; Harteis et al., 2008). In contrast, individuals who have internalized a negative error orientation will perceive errors as a threat and will experience a high degree of psychological burden and frustration related to errors (Farnese et al., 2022); consequently, they tend to deny or hide errors (Edmondson & Lei, 2014; Zhao & Olivera, 2006).

Errors do not necessarily lead to negative outcomes but may instead serve as useful opportunities for learning and innovation (Cannon & Edmondson, 2005; Harteis et al., 2008). Yet, organizations are often ill-equipped to motivate their members to handle errors constructively so that employees may opt to hide mistakes and miss the opportunity to learn and recover from failures (Barach & Small, 2000; Catino & Patriotta, 2013). This is problematic because proactive error reporting is associated with higher organizational performance and serves as an essential part of effective risk management (Fischer & Weißmüller, 2024; Wang et al., 2019).

Organizational culture and practices significantly affect bureaucrats’ behavior because they set and socially reinforce professional norms that provide benchmarks for the appropriateness of individual behavior (Møller, 2021; Seidemann & Weißmüller, 2024). Prior research suggests that individuals’ logic for selecting appropriate error-coping strategies is affected by their organizational environment. Organizational cultures that are error-friendly are a necessary condition for sharing errors and learning from them (Catino & Patriotta, 2013; Lei et al., 2016; Sasou & Reason, 1999) because they provide a supportive and enabling environment. This is especially true for the public sector (Mahler, 1997), and in decisions under risk (Tangsgaard, 2021). On the organizational level, preventive (i.e., error aversion) and corrective (i.e., error management) cultures can be differentiated (Kupor et al., 2018). While error management culture (EMC) perceives errors as a source of informative feedback essential for learning and correction, error aversion culture (EAC) strictly aims at preventing employees from making mistakes (Cusin & Goujon-Belghit, 2019; Keith & Frese, 2005). Working in an error-averse culture means that errors are associated with fear and emotional strain, while an EMC entails a work environment of psychological safety with regard to making and talking about mistakes (King & Beehr, 2017) to foster organizational learning (Mikkelsen & Grønhaug, 1999). A positive organizational error culture can also strengthen positive individual attitudes toward errors and encourage related proactive behaviors (Hetzner et al., 2011; Tangsgaard & Fischer, 2024).

Public Sector-Specific Challenges to Error Management

Despite these benefits, prior research suggests that creating a positive error culture seems to pose a particular challenge for public organizations (Borins, 2001). Public bureaucracies often suffer from a punitive, risk-averse, and zero-error culture that inhibits their members from responding to errors proactively (Crosby et al., 2017; Sørensen & Torfing, 2011). Furthermore, mistakes in core public tasks such as the provision of healthcare or security can have dramatic consequences, eroding public trust. The societal expectation to safeguard public value and balance complex and partially conflicting goals for the benefit of society at large can result in less tolerance for errors (Tangsgaard & Fischer, 2024).

Furthermore, citizens’ negative reactions to governmental failure do also not help to produce a more positive error culture, especially when mistakes are more often recognized and debated than accomplishments (negativity and anti-public sector bias; Gilad et al., 2018; Marvel, 2015; Meier et al., 2019), especially anti-public sector bias goes together with higher expectations. Society tends to hold public organizations to higher standards than private entities (Jørgensen & Bozeman, 2007). The belief that these organizations should be more accountable, ethical, and efficient contributes to a decreased tolerance for mistakes. Additionally, public organizations are usually funded by taxpayers’ money. When mistakes occur in the management or allocation of public funds, there is a heightened sensitivity to accountability and the public may be less forgiving because they expect their tax money to be used responsibly and effectively (Marvel, 2016; van de Walle, 2016).

The idiosyncratic employment systems of many public organizations may posit another particular challenge for error management because civil servants’ comparatively high job security makes errors less consequential with regard to their career advancement. This posits a challenge for motivating and incentivizing positive error responses: Individuals with high moral engagement and public service motivation may feel more encouraged to engage in proactive error-handling behavior while morally disengaged individuals with low work involvement and motivation may be stimulated to hide and disregard errors (van Roekel & Schott, 2021). Error handling requires effort and relies on individuals’ use of discretion while simultaneously causing emotional strain—particularly in a punitive organizational error culture. Zhao and Olivera (2006) note that an individual's error response is not a simple and independent choice between, for example, reporting an error or not but rather relates to an array of possible behavioral response strategies. Response strategies may relate to individual behaviors (e.g., hiding errors), behaviors that can be performed individually or as a team (e.g., analyzing error origins, correcting errors, learning from errors collectively), or behaviors that are interactive and relate to other individuals in the form of acts of communication (e.g., sharing the information about an error with colleagues). In the following, we focus on four of these options, which form contrasting pairs, namely hiding vs. reporting an error as a communicative response strategy, and ignoring vs. correcting an error as an action-oriented response strategy. These are individual behaviors so that they can be tested in a survey setting, whereas the team and interactional behaviors would rather need to be tested in group settings. This focus closes an important research gap because prior research on factors that cause the aforementioned variety in error response remains inconclusive although these studies do point toward the decisive role of individual employees’ psychological and motivational dispositions as predictors for error response. For instance, Emby et al. (2019) show that individuals will only communicate errors transparently if they have sufficient self-efficacy. Self-efficacy and psychological safety are also positively related to the likelihood of learning from errors (Wang et al., 2019). Psychological distancing and self-controlling mechanisms (e.g., derived from the anticipation of punishment) are associated with defensive behavior and the tendency to hide an error whereas accepting responsibility and resolving errors in a rational and goal-oriented manner leads to positive changes in error-handling practice (Meurier et al., 1997). The motivation to detect and learn from errors can also be hindered by punitive leaders (Dahlin et al., 2018) and strict social hierarchies and institutional boundaries (Sasou & Reason, 1999), which are still prevalent characteristics of public bureaucracies worldwide.

Despite insights on individuals’ predisposition for error handling and organizations’ role in stimulating it, to date, the discourse lacks exploration of how specific error characteristics—that is, different error types and different error consequences—affect individuals’ error response.

Individuals’ Error-Coping Strategies—Emotional and Problem-Focused Responses

Errors cause stress, frustration, or even despair. People who realize that they have made a mistake often dread the potential consequences and experience increased emotional burden from the fear of losing face (Patrician & Brosch, 2009). The transactional theory of stress and coping provides a model to understand how individuals evaluate and react in such stressful situations (Lazarus, 1966; Lazarus & Folkman, 1984). The process of coping follows three steps: (1) cognitive appraisal of the situation and its evaluation as (ir-)relevant, positive, or stressful; (2) formulation of a coping response based on this assessment, and (3) response evaluation by reflecting upon the success of the selected coping mechanism while considering long-term effects to learn for future situations of error-induced stress.

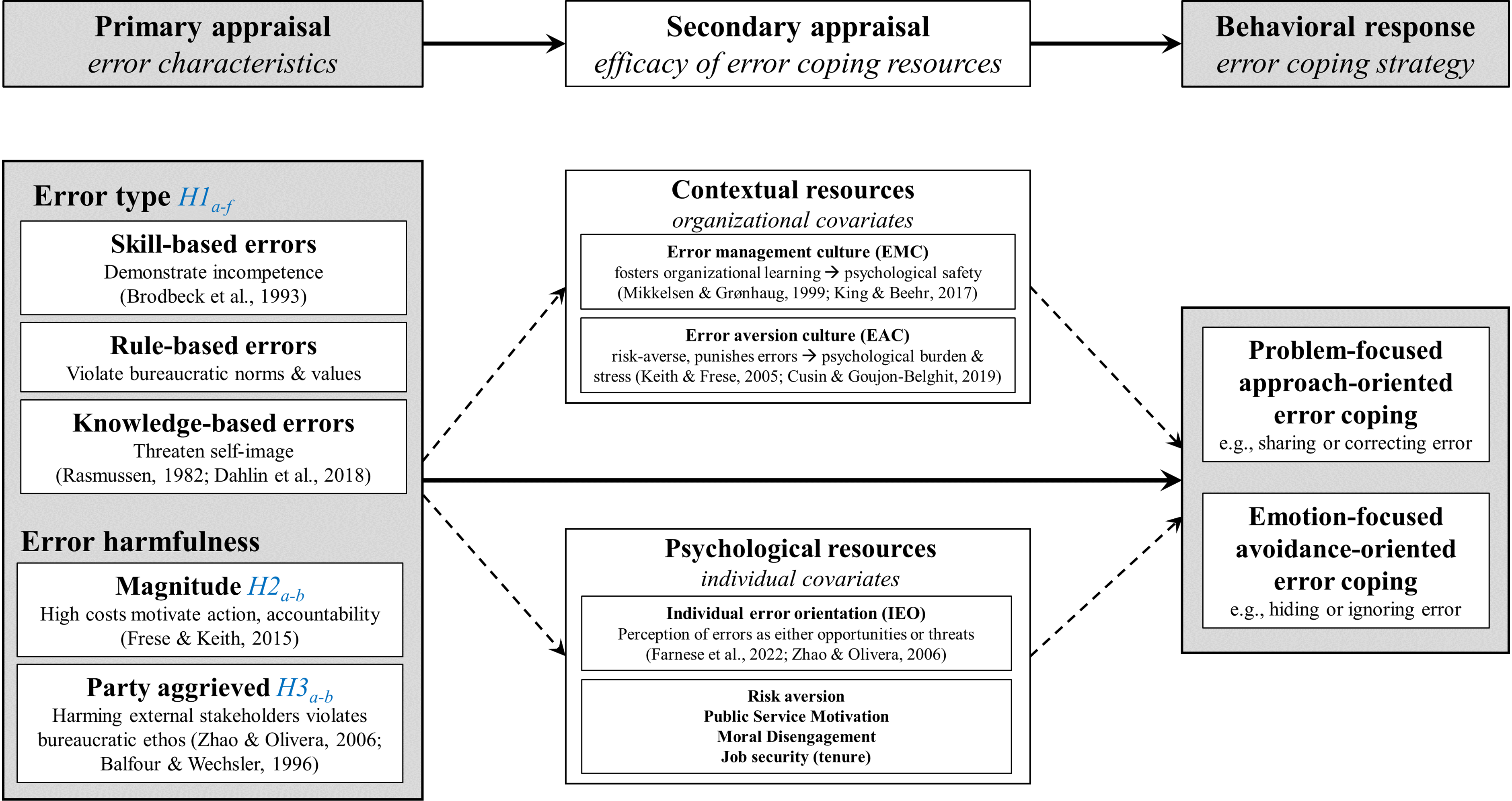

In this study, we follow Lazarus’ model and presume that making errors and deciding on what to do about them is a psychologically salient and stressful situation. Furthermore, we focus on the second step in this model: the actual behavioral response to errors. Coping behaviors are traditionally distinguished between problem-based or emotion-based behaviors, and approach or avoidance-related behaviors (Carver & Connor-Smith, 2010). The decision to hide or ignore an error is emotion-focused avoidance error coping because it is merely related to disengagement. In contrast, sharing and correcting errors is problem-focused approach-oriented error coping. Learning from errors can be an outcome of these behaviors within the specific context of organizational and individual resources that may facilitate and incentivize either of these behaviors, see Figure 1.

A conceptual model of transactional error coping behavior.

Emotional Error Coping

Rausch et al. (2017) suggest that errors are emotional events per se. They represent external and unsolicited feedback on an individual's workplace behavior and thereby stimulate negative emotions since, ultimately, errors are generally considered as signs of failure and under-achievement (Rausch et al., 2017). Work-related errors are particularly strongly related with negative emotions, for example, embarrassment, worry, disappointment, unhappiness, and fear (Basch & Fisher, 2000). While negative emotions function as potent psychological warning signals that may trigger reevaluation of individual behavior (Zhao, 2011), experiencing acute negative emotions actually reduces individuals’ cognitive capacity for making rational (i.e., goal-oriented) choices (Kuhl, 2001). Individuals who experience strong negative emotions are more likely to focus on emotional coping strategies first which help preserve their self-image (e.g., by hiding the error) instead of selecting problem-solving coping strategies, that is, fixing an error swiftly before much harm is done (Folkman & Lazarus, 1980). Therefore, preoccupation with negative emotions in error situations fosters irrational and potentially chaotic reactions that inhibit or delay effective error handling (Frese & Keith, 2015).

Problem-Focused Error Coping

Alternatively, coping theory suggests that if individuals are able to consider the outcome and impact of their errors in a less emotionally affected manner their error-coping strategies will rely on both self-related and other-related considerations. Rational individuals will conduct ex-ante cost-benefit evaluations to select their error response behavior (Zhao & Olivera, 2006). This perspective assumes that individuals are aware that different tangible and intangible costs and benefits arise from different error-handling behaviors. For instance, sharing knowledge about an error instead of hiding it might result in punitive action and financial losses, whereas in an organizational climate that cherishes proactive error communication sharing this error sharing might even result in higher validation by colleagues who appreciate the honesty and show gratitude for the opportunity to learn and develop (Fischer, 2022; Zhao & Olivera, 2006). We suggest that these cost-benefit assumptions determine which strategy an individual chooses to handle an error and that these assumptions rely on individual and organizational characteristics but also on the type of error that has occurred.

Error Type

The type of error may determine how individuals will handle it (Harteis & Gartmeier, 2017). We differentiate errors by type as skill-based (i.e., incorrect execution of a skill-related task, for instance, calculating social benefits incorrectly due to a mathematical error), rule-based (i.e., violating known rules, for instance, calculating social benefits by selecting the incorrect calculation model or wrong thresholds), or knowledge-based (i.e., not knowing enough, for instance, calculating social benefits incorrectly due to a lack of knowledge about the current legislation) (Dahlin et al., 2018; Rasmussen, 1982). Zhao and Olivera (2006, p. 1027) suggest that these different types of errors result in different error response strategies based on the emotions they trigger, for example“[k]nowledge-based mistakes may generate feelings of shame and may seem particularly threatening to one's self-image because they demonstrate incompetence.”

H1a: Error type affects the likelihood of reporting an error.

H1b: Error type affects the likelihood of correcting an error.

Brodbeck et al. (1993) suggest that errors on the intellectual level are particularly hard to handle and often require the support of colleagues or supervisors which may not only be time-consuming but also upsetting for employees on a personal emotional level (Brodbeck et al., 1993, p. 311). This might be especially true for public sector work, which is mainly knowledge-intensive work (Bos-Nehles et al., 2017). Hence, individuals may react with emotional and avoidance-oriented coping strategies to such errors. 1

In contrast, skills do have a lower importance in knowledge-intensive work and organizations, which is also true for the public sector. A good example is digital or innovation competences which are still underdeveloped in the majority of civil servants worldwide without significant consequences for these individuals (Kruyen & van Genugten, 2020). Therefore, we assume that civil servants do not mind sharing these types of errors but that they are also not highly motivated to solve them, as this would require effort, which is likely being avoided if no organizational pressure or normative incentives apply.

H1c: Skill-based errors are positively associated with the likelihood of reporting errors instead of hiding them.

H1d: Skill-based errors are positively associated with the likelihood of ignoring instead of correcting them.

Especially in a bureaucratic work environment, errors that violate rules may cause tremendous stress in individuals given that rule violations—irrespective of whether they occur unintentionally—constitute serious violations of core principles of public administration, as procedural and legal certainty is an important pillar for citizens’ trust in government and the legitimacy of public organizations (Eriksen, 2023; van de Walle & Bouckaert, 2003). Rule-based errors are often seen as major failures and public organizations usually try to avoid that rule violations become public to avoid blame (Bach & Wegrich, 2019; James et al., 2016). This suggests that individuals who have made a rule-based error are likely to hide it but will try to correct it nonetheless:

H1e: Rule-based errors are positively associated with the likelihood of hiding errors instead of reporting them.

H1f: Rule-based errors are positively associated with the likelihood of correcting instead of ignoring them.

Error Harmfulness and Outcome

Errors are not only characterized by their type but also by their (expected) impact which may vary between neglectable and massive harm. Estimating the costs and benefits associated with selecting one particular error response strategy over another is particularly difficult in the public sector. Public sector agents are challenged by balancing complex and often conflicting goals (Simon, 1947/1997). Any cost-benefit evaluation implies that individual-level consequences have to be evaluated against organizational and even larger societal consequences. For example, individuals may choose to correct an error to avoid harm for the general public but may still not report and deny that the error occurred if they work in a negative error culture. Selecting an appropriate error response involves delicate consideration between one's own and other people's interests, and action is likely motivated by the expected harm associated with inaction (Frese & Keith, 2015).

Individuals who feel responsible for an error will experience more intense psychological costs (such as stress, see Lazarus, 1966; Lazarus & Folkman, 1984) if they expect their error to result in larger damage. Their emotional response is likely to affect their error behavior in this case, resulting in ineffectiveness (Frese & Keith, 2015) and a tendency to pursue self-preserving coping mechanisms instead of transparent error response strategies (Rausch et al., 2017). This also relates to the aforementioned blame avoidance in the public sector associated with the fear of punishment and being held accountable (Bovens et al., 2014).

H2a: Higher error harmfulness is positively associated with the likelihood of hiding errors instead of reporting them.

From the perspective of a cost-benefit analysis, however, higher prospective error harm may also motivate the person responsible for the error to take action and fix it while minor errors may be perceived as not being relevant enough to motivate action (Patrician & Brosch, 2009). We assume that higher expected error harmfulness will trigger action in public servants based on their professional norms and motivation. Public administration tends to attract employees with a particularly high regard for contributing to the public good and public service motivation (Ritz et al., 2016). Refraining from fixing an error would violate public servants’ professional norms and commitment to civic duty.

H2b: Higher error harmfulness is positively associated with the likelihood of correcting errors instead of ignoring them.

Furthermore, error harmfulness comprises two aspects that guide decision-making behavior: the magnitude of harm and the party aggrieved by the error's negative consequences. Commitment theories suggest that individuals base their decision-making behavior upon benchmarks of dissimilar levels of attachment toward other individuals in their environment (Balfour & Wechsler, 1996; Chordiya et al., 2017; Meyer & Herscovitch, 2001; Stazyk et al., 2011). Zhao and Olivera (2006) show that individuals—implicitly or explicitly—conduct cost-benefit evaluations to determine the effects of their professional behavior on both themselves and other people, including co-workers and their organization but also external stakeholders and society at large.

This is a particularly challenging issue for civil servants because public agencies are responsible for large amounts of taxpayers’ money and manage civil service processes that impact the lives of millions of people (Broadhurst et al., 2010, p. 356). Errors in public agencies may have detrimental effects on many citizens’ lives, as demonstrated by administrative scandals such as the Dutch childcare benefit scandal (Fenger & Simonse, 2024). Hence, in case of an external party being aggrieved the benefits of error correction may outweigh individual—psychological and tangible—costs associated with correcting the error and hence promote action.

H3a: Harming external—instead of internal—stakeholders is positively associated with the likelihood of correcting errors instead of ignoring them.

However, this explanation may not relate to the communication dimension of error handling because information sharing by itself will not help affected stakeholders. Rather, we argue, the fact that an error affects external stakeholders—in contrast to internal stakeholders—incorporates a higher likelihood of detection with potentially harsh consequences since affected citizens may reach out to the complaint management unit (Kang, 2023). Therefore, civil servants who know that their error aggrieves external stakeholders may assume that the psychological costs of reporting an error themselves are lower compared with the potential costs associated with the consequences of having an error discovered by a different party (Klofstad et al., 2022).

H3b: Harming external—instead of internal—stakeholders is positively associated with the likelihood of reporting errors instead of hiding them.

Materials and Methods

This section presents the sample and the preregistered experimental design used to assess our hypotheses. 2 To disentangle the factors determining individuals’ error response in context, we use a between-subjects randomized choice-based conjoint survey experiment, implemented with the software Qualtrics (Street et al., 2005; Weber, 2021). Experiments informed by behavioral approaches to administrative behavior using choice tasks are particularly powerful for investigating research questions that involve multidimensional choices involving a number of nuanced factors because conjoint experiments allow us to explicitly and systematically manipulate the different combinations of these factors that may determine individuals’ error response, that is, error types, error consequences in relation to the parties aggrieved, and the magnitude of harm done. Conjoint experiments are ideal survey experimental designs for this research topic because they reveal which attributes are most important for error response in a setting of complex and multidimensional choice options (Liu & Shiraito, 2023). By systematically randomizing each error-related factor, a conjoint experiment design solves the issue of composite treatment effects that would otherwise limit the explanatory power of classic experimental setups, allowing causal inference in contrast to mere correlational analyses (Hainmueller et al., 2014). The advantages of using a randomized controlled survey design is that it allows us to make causal predictions of isolated effects of individual stimuli while allowing for precise treatment manipulation. As an additional advantage compared to stated preferences in survey research, our experimental design reveals choice-based preferences instead of self-reported measures, which tend to suffer from social-desirability bias. Using this design, we directly respond to Harteis and Gartmeier's (2017) call for more experimental research into how individuals actually deal with errors. The data were analyzed with Stata, version 17, and R using the cregg package by Leeper (2020).

Sampling Procedure

Original data of active civil servants were collected in Germany in August 2021. We define civil servants as individuals who work in the core public administration, that is, ministries and local administration. Frontline employees from other professions (such as social workers, nurses, teachers, and the police) are purposefully excluded because these occupations incorporate very dissimilar job characteristics and a dissimilarly motivated workforce compared with core public administration. We employed a professional panel provider to source our sample. Respondents were remunerated with €1.50 for completing the online questionnaire. Incomplete responses were deleted rigorously from the dataset for quality control. Since respondents rated more than one vignette scenario, the data are clustered at the individual level of respondents. Consequently, our statistical estimates use robust clustering to account for the potential interaction of the error terms resulting from the conditional contribution to the regression estimates (Cameron et al., 2011). Following Bekker-Grob et al. (2015), we aimed at raising a final sample of at least N = 188 survey participants, each rating four tasks, because conservative effect size estimations prior to collecting the data indicate that this sample size is adequate for statistically reliably detecting even small effect sizes and intergroup correlations with a power level of 90% or higher for this study's design (Ellis, 2010; Stefanelli & Lukac, 2020). With a final and successfully balanced sample of N = 276 resulting in Obs. = 1,104, this aim was achieved (see Appendix C.7).

Conjoint Experiment Design and Dependent Variables

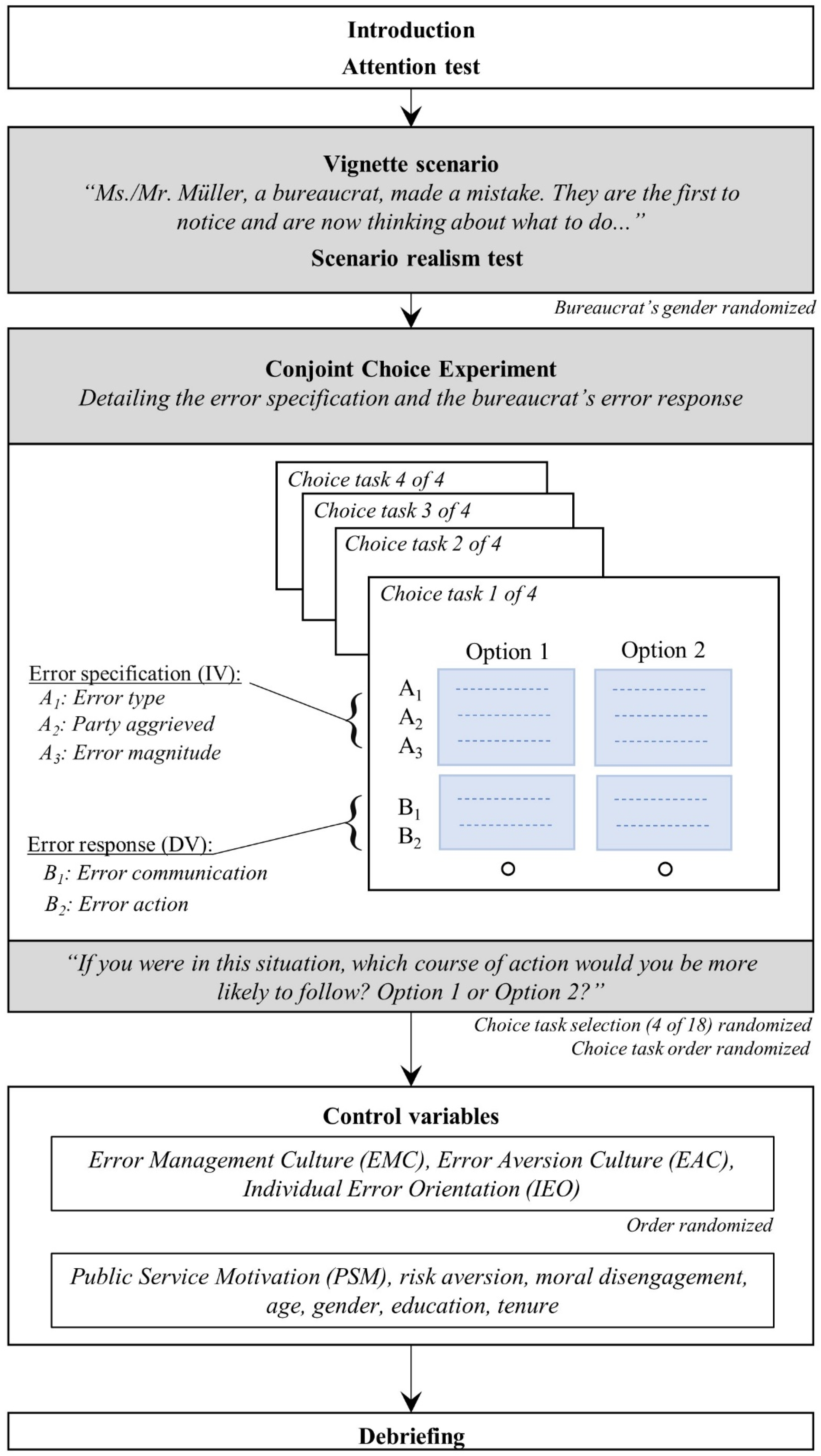

Figure 2 presents the process of our conjoint experimental design with the treatment array configuration in Table 1. After a general vignette scenario describing a typical setting in public administration in which an administrative error happens to a civil servant, respondents randomly received four out of 18 conjoint choice tasks, each consisting of the presentation of two sets of information that further specified the error and context (attributes A1 to A3) as well as prospective behavioral response strategies (attributes B1 and B2). These sets provided detailed information regarding the respective error type, the error consequences to be expected, the stakeholders aggrieved, as well as the magnitude of the expected harm resulting from the error. Respondents were then asked to indicate which of these two sets they were more likely to follow. Each study participant made four of these binary choices. With this setup, we follow best practice recommendations for the systematic configuration, distribution, and randomization of choice tasks to create an optimized orthogonal design (Rose & Bliemer, 2009; Weber, 2021). Figure 2 presents this process of our empirical treatment (see Appendix A and B for more detail on the treatment).

Study design and experimental procedure.

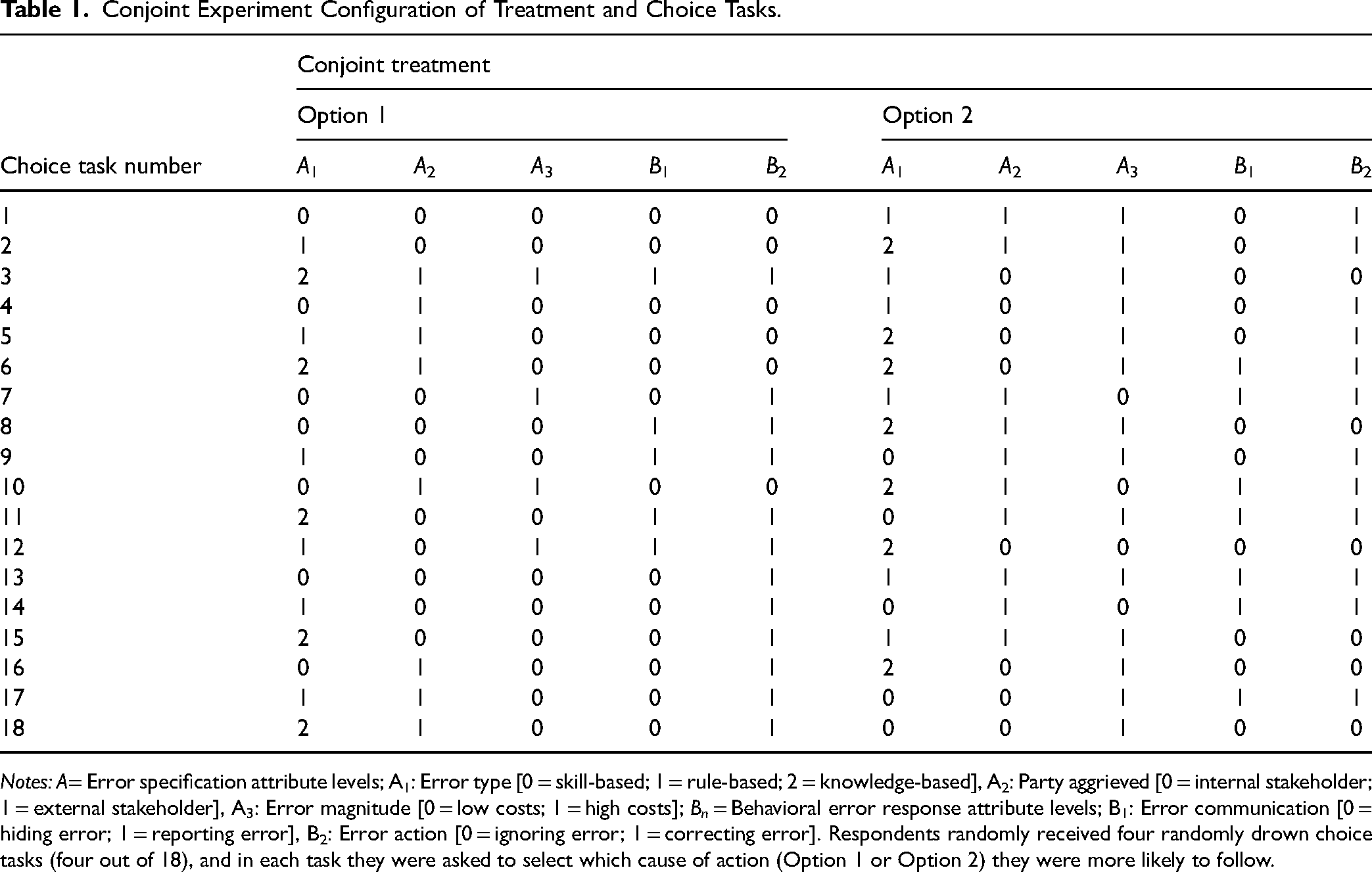

Conjoint Experiment Configuration of Treatment and Choice Tasks.

Notes: A= Error specification attribute levels; A1: Error type [0 = skill-based; 1 = rule-based; 2 = knowledge-based], A2: Party aggrieved [0 = internal stakeholder; 1 = external stakeholder], A3: Error magnitude [0 = low costs; 1 = high costs]; Bn = Behavioral error response attribute levels; B1: Error communication [0 = hiding error; 1 = reporting error], B2: Error action [0 = ignoring error; 1 = correcting error]. Respondents randomly received four randomly drown choice tasks (four out of 18), and in each task they were asked to select which cause of action (Option 1 or Option 2) they were more likely to follow.

Respondents were asked to read the information carefully and suitable attention tests were administered. The narrative of our experimental choice trials is nested in a description of a fictitious but realistic public administration agency in which an error occurred in the process of administrating a public tender. Study participants were asked to put themselves into the shoes of a street-level bureaucrat who had come to realize that they had caused an error and that they were the first person to realize that the error had happened. Besides the realistic description of the scenario of the vignette treatment, the ecological validity of the experimental design is supported by research by Hainmueller et al. (2014) who found that the effects detected in conjoint experiments reliably predict the effects of the same attributes in real world behavior, highlighting that conjoint designs are robust against social desirability response bias and exhibit particularly high predictive power for actual choice behavior.

In each of the four choice tasks, respondents were asked to choose between two choice options (“Option 1 or Option 2?”) to indicate which of the two response options presented was the one that they would be more likely to pursue if they were themselves the civil servant in the situation described. Combined with the systematic variation of conjoint attribute levels, this binary choice task response reveals the relatively more adequate error action and error communication behavior (our two DVs) as a response to the respective contextual conjoint error-specific attributes.

In each choice task, we systematically manipulate the information provided regarding the error itself—error type (skill-based, rule-based, or knowledge-based)—and its consequences—party aggrieved (internal stakeholder or external stakeholder) and magnitude of harm (low costs vs. high costs)—but also vary the proposed behavioral strategies on how to respond to the error, which constitute our two dependent variables (DVs), namely error communication (hiding vs. reporting the error) and error action (ignoring vs. correcting the error).

As discussed in the theory section, we focus on two dimensions of error-handling behavior (Cannon & Edmondson, 2005; Rybowiak et al., 1999; Zhao & Olivera, 2006), which are characterized by the individual having agency, factual responsibility, and opportunity to act upon their error 3 : communicative and action-oriented error handling behaviors. Both dimensions are modeled as two straight-forward questions with two distinct dimensional poles, that is, whether agents would either report or hide their error (error communication-dimension) and whether they would either correct or ignore their error (error action-dimension). The latter options represent avoidance-oriented error-coping behaviors, the former represent approach-oriented error-coping behaviors. During the conjoint experiment, each dimension's two items are coded as binary, mutually exclusive dummy variables.

This means that our dependent variables do in fact not ask respondents to indicate what they would do in absolute terms but the vignettes present potential error responses and ask respondents to indicate which potential error response they would prefer to perform. In doing so, we follow recent examples of empirical studies on deviant behavior in public personnel using vignette designs (e.g., Prysmakova & Evans, 2022) as well as best practices for conducting vignette experiments (Aguinis & Bradley, 2014). We exploit the central strength of vignette experiments: This vignette and dependent variable design inhibits social desirability response bias—which is essential in research on deviant behavior—by creating psychological distance between the respondent and the individual described in the vignette scenario, while still triggering context-dependent response with high internal and external validity under highly controlled experimental conditions (Aguinis & Bradley, 2014).

As presented in Table 1, the full factorial design (3 × 2 × 2 × 2 × 2) minus 12 implausible combinations results in 36 attribute sets that are combined into 18 choice tasks (Rose & Bliemer, 2009). To prevent halo, order, and response fatigue effects, we only administer four choice tasks per participant. The distribution and order of these choice tasks are randomized between and within participants. Randomization allows us to obtain an unbiased estimate of the effects of error-related, individual, and context-related stimuli.

Covariates and Control Variables

Based on the literature review, we complement our conjoint experiment with several important covariates and control variables associated with (a) organizational error culture to capture respondents’ prior experience and psychological benchmarks of how errors are typically handled in their professional work environment, as well as (b) individual error-related attitudes, behavioral motivations, and characteristics. All scale items were translated into German in a double-blind procedure to minimize researcher bias and increase reliability. Responses for all scale measures were provided on a 7-point Likert-type scale ranging from 1 (completely disagree) to 7 (completely agree) and they were mean-scored to form the respective variables.

Organizational Level

As discussed before, the literature distinguishes two types of organizational error culture: error management culture (EMC) which is characterized by a positive and proactive approach to errors, and error aversion culture (EAC) which is characterized as negative and avoidant toward errors and error management. Given that organizational culture may lead to internalization of certain heuristics and practices in the individual, we measure respondents’ prior exposure to both of these organizational cultures at their workplace with two scale-based variables (EMC and EAC) by van Dyck et al. (2005). These scales (see Appendix C for more detail and construct analysis) concern organizational error cultures and are not sector-specific, and hence do not impede the ecological validity of the measurement.

Individual Level

We capture between-respondent differences in motivation and traits, particularly individual error orientation (IEO) with Farnese et al.'s (2022) IEO scale (see Appendix C for more detail on all individual-level variables). Prior research emphasizes the relevance of public service motivation (PSM) as a control variable, because it is a meaningful predictor for moral and rule-breaking behavior (Ripoll, 2019), prosocial motivation (Schott et al., 2019), and public value orientation (Andersen et al., 2012), all of which may affect error responses. We use Kim's (2009) 12-item scale to capture PSM.

Given that risk preferences and moral motivation predict deviant behavior (Weißmüller, 2021), we reveal individuals’ implicit risk preference with a short version of Madden et al.’s (2009) Probability Discounting Questionnaire to estimate a characteristic probability discounting parameter (h) from ten systematically varied randomized hypothetical choice tasks between one smaller but secure vis-à-vis one larger but probabilistic option. The parameter h is a robust measure for probability discounting in predicting the degree to which individuals’ decisions are affected by the riskiness of their choices, for instance, when deciding upon whether to disclose that they had made a mistake. Moore et al.'s (2012) scale was used to capture moral disengagement (MD).

Lastly, to assess sample representativeness compared with the general population of civil servants in Germany, we measured respondents’ age in years, their gender, their level of education, and highest professional qualification, their years of work experience, whether they work at the street-level, held tenure and/or leadership responsibility, as well as their number of working hours to control for the different levels of work experience and involvement.

Construct Validity

All scale items exhibit high internal consistency and reliability (Cronbach's α = .744–.920; see Table 2 and Appendix C). We find that the EMC and EAC scales applied to our data have equally high internal consistency as in their original study by Van Dyck et al. (2005) pointing to the reliability of the measures with this study's data (EMC: Cronbach's α=.89 compared with .92; EAC: Cronbach's α=.88 compared with .92). Given that survey responses on topically closely related micro and meso-level variables may be subject to spillover effects in response behavior, we assess their construct validity, goodness of fit, and the distinctiveness of each scale measure and in tandem by conducting exploratory factor analysis (EFA). Convergent and discriminant validity were tested with SEM-based confirmatory factor analysis (CFA) to control for any common method bias that may be caused by latent unobserved factor(s) following best practice recommendations by Podsakoff et al. (2003) and Williams et al. (2010) using structural equation modeling (SEM) with the latent variable approach (see Appendix C for detailed results). Joint iterative CFA (maximum likelihood) with items from all four measures reveals that a four-factor model with EMC, EAC, and IEO fits the data significantly better than any collapsed model. CFA further showed excellent discriminant validity and high data-to-model fit, while SEM indicated no significant relationships of the study variables with a latent, unobserved marker which otherwise may indicate common method bias. EFA and CFA underscored the distinctiveness of the multi-factor model structure and polychoric correlation analysis revealed sufficient intercorrelation between the scale items within each scale measure; no latent factors were detected which indicates high construct distinctiveness and construct reliability.

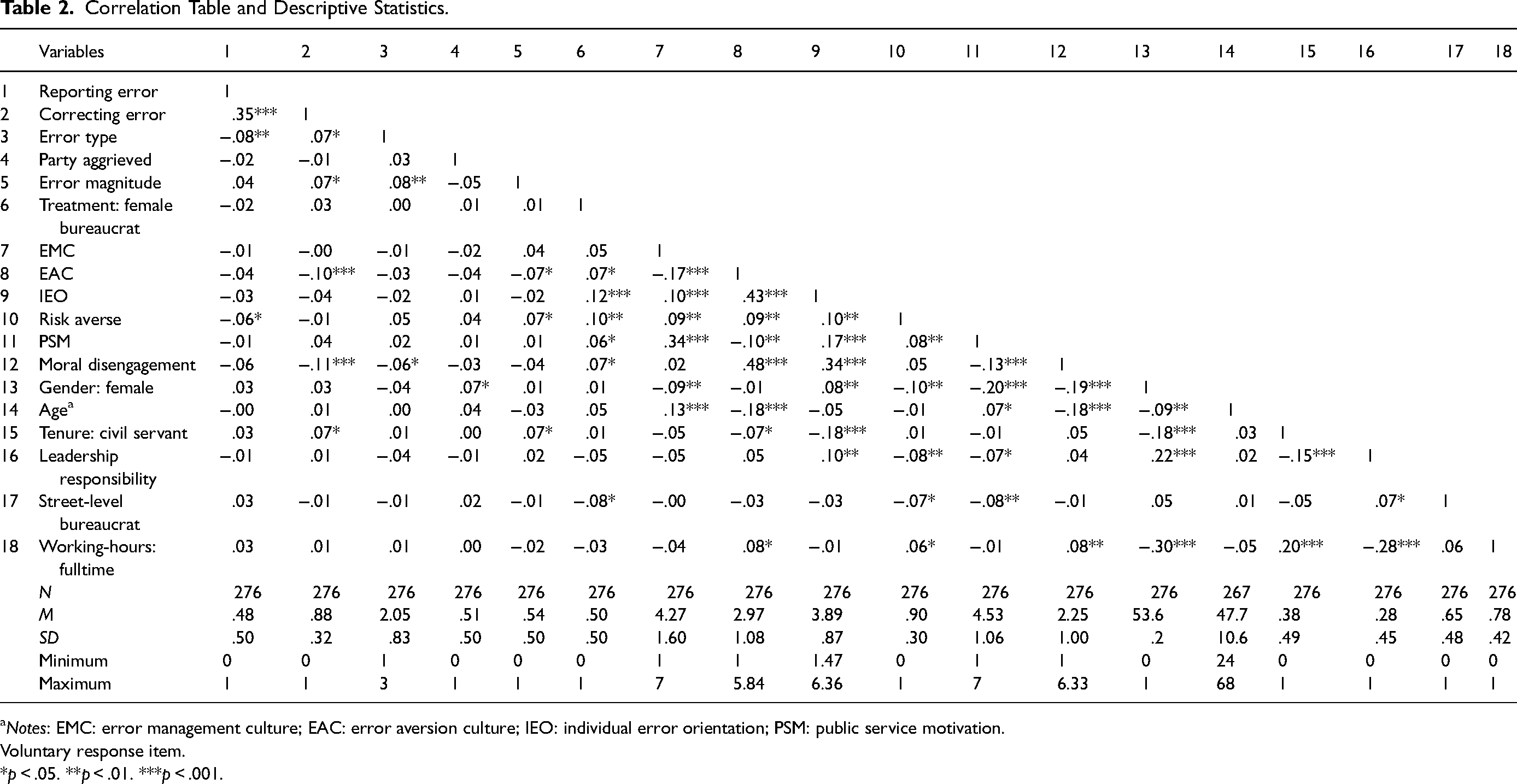

Correlation Table and Descriptive Statistics.

Notes: EMC: error management culture; EAC: error aversion culture; IEO: individual error orientation; PSM: public service motivation. Voluntary response item.

*p < .05. **p < .01. ***p < .001.

Results

Descriptive Sample Statistics

The link to our online experiment was distributed to a total of 454 individuals working in public administration, 61.5% (N = 276) completed the questionnaire. The final dataset comprises Obs. = 1,104 observations nested within N = 276 respondents. Table 2 presents the descriptive sample statistics and pair-wise correlations. 53.6% study participants are female, they are on average M = 47.7 (SD = 10.6) years old, predominantly risk averse (lnh: M=–0.81, SD = 0.91), civil servants (37.7%) or public sector employees with tenure (54.7%) who have M = 24.6 (SD = 12.1) years of work experience in total, and M = 19.9 (SD = 12.2) years of work experience in the public sector. Our sample represents a balanced mix of qualification-based public service job classifications, and 28.3% hold a leadership position. Most respondents (65.2%) are street-level bureaucrats who regularly interact with citizens. 78.0% of our sample work full-time. These characteristics indicate that our sample is, indeed, representative of the average civil servant in Germany. 4

Study participants perceived the error-related scenario provided in the vignettes as very realistic (M = 4.9, SD = 1.5), which supports the reliability and validity of our findings. 5 Post hoc power analysis reveals that the number of observations indeed allows us to reliably detect small-size effects and treatment effects (two-tailed) with a power (1–β) of 95.4 in these models.

Respondents report that on average their current workplace is characterized by an EMC (M = 4.27, SD = 1.60) instead of an EAC (M = 2.97, SD = 1.08). Study participants’ IEO is proactive in the sense that they tend to approach the risk associated with errors proactively M = 4.97 (SD = 1.12); they anticipate that errors may happen (M = 4.23, SD = 1.27) and feel below-average stress levels if errors occur (M = 3.26, SD = 1.21). Respondents score relatively high on PSM (M = 4.53, SD = 1.06), and exhibit low levels of MD (M = 2.25, SD = 1.00).

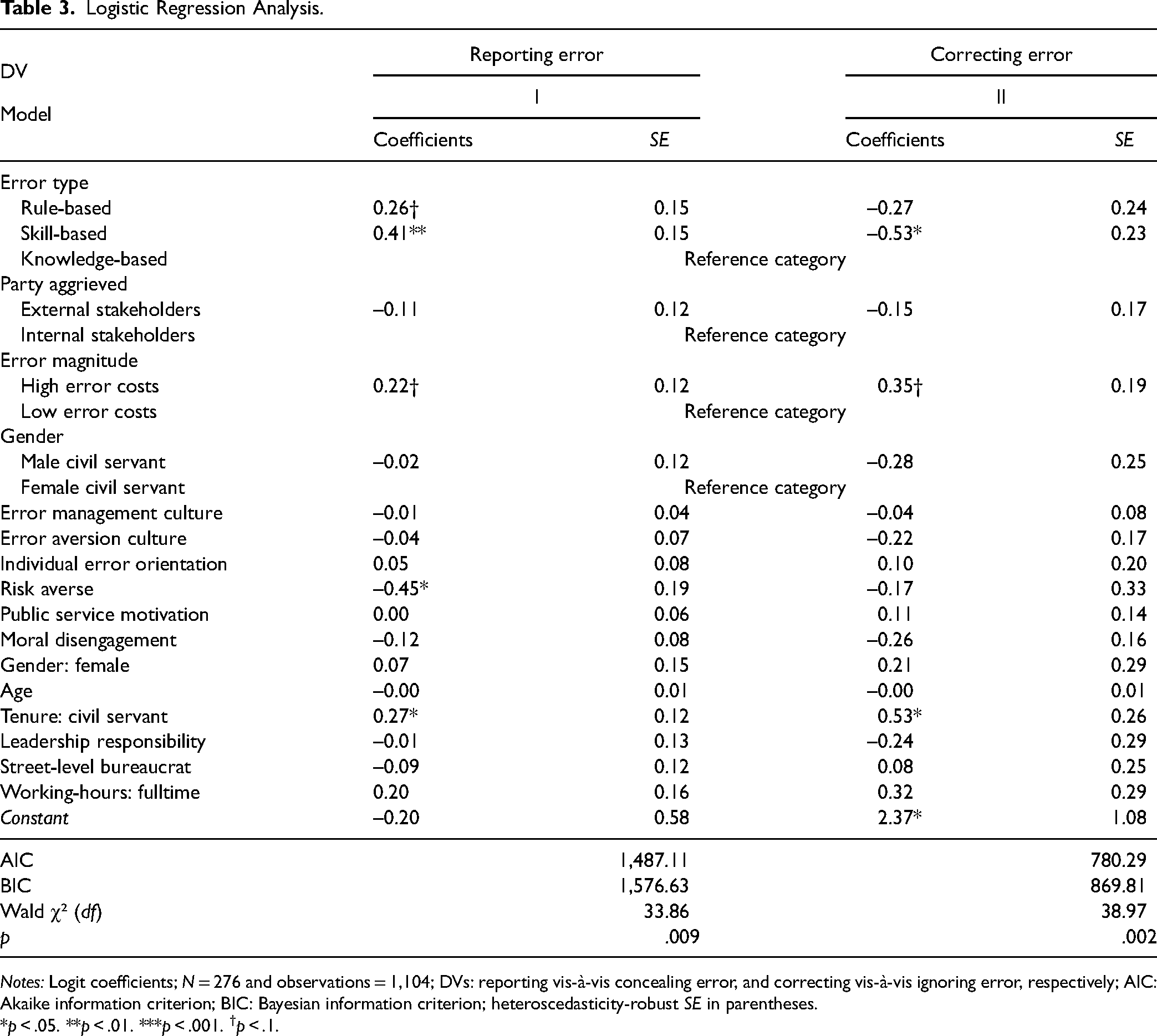

To develop a preliminary understanding of how these covariates and control variables may affect our variables of interest through correlation, we conducted logistic regression analyses with heteroscedasticity-robust standard errors (SE), see Table 3. Risk-averse individuals are significantly less likely to report errors (−39%; b = −0.45, p = .017) and respondents who are tenured civil servants are significantly more likely to both report (57%; b = 0.27, p = 0.021) and correct their errors (63%; b = 0.52, p = .045) in general, pointing to an enculturated civil service ethos, independent of PSM. Intriguingly, we find that organizational error cultures (EMC and EAC) as well as job-related attitudes such as PSM and MD do not significantly predict the likelihood of reporting and correcting errors per se, speaking to the importance of recognizing error type as a factor in driving error-coping strategies. We conducted the necessary exploratory analyses (see section below) to further reveal how error response to different types of errors is impacted by EMC, EAC, IEO, leadership responsibility, gender, and PSM.

Logistic Regression Analysis.

Notes: Logit coefficients; N = 276 and observations = 1,104; DVs: reporting vis-à-vis concealing error, and correcting vis-à-vis ignoring error, respectively; AIC: Akaike information criterion; BIC: Bayesian information criterion; heteroscedasticity-robust SE in parentheses.

*p < .05. **p < .01. ***p < .001. †p < .1.

Given the nested structure of the data logistic regression analyses can be misleading, and average marginal component effects (AMCE) analysis is needed to test causal effects and the hypotheses with conjoint data. We explain these procedures below.

Analytical Procedure for Hypotheses Testing

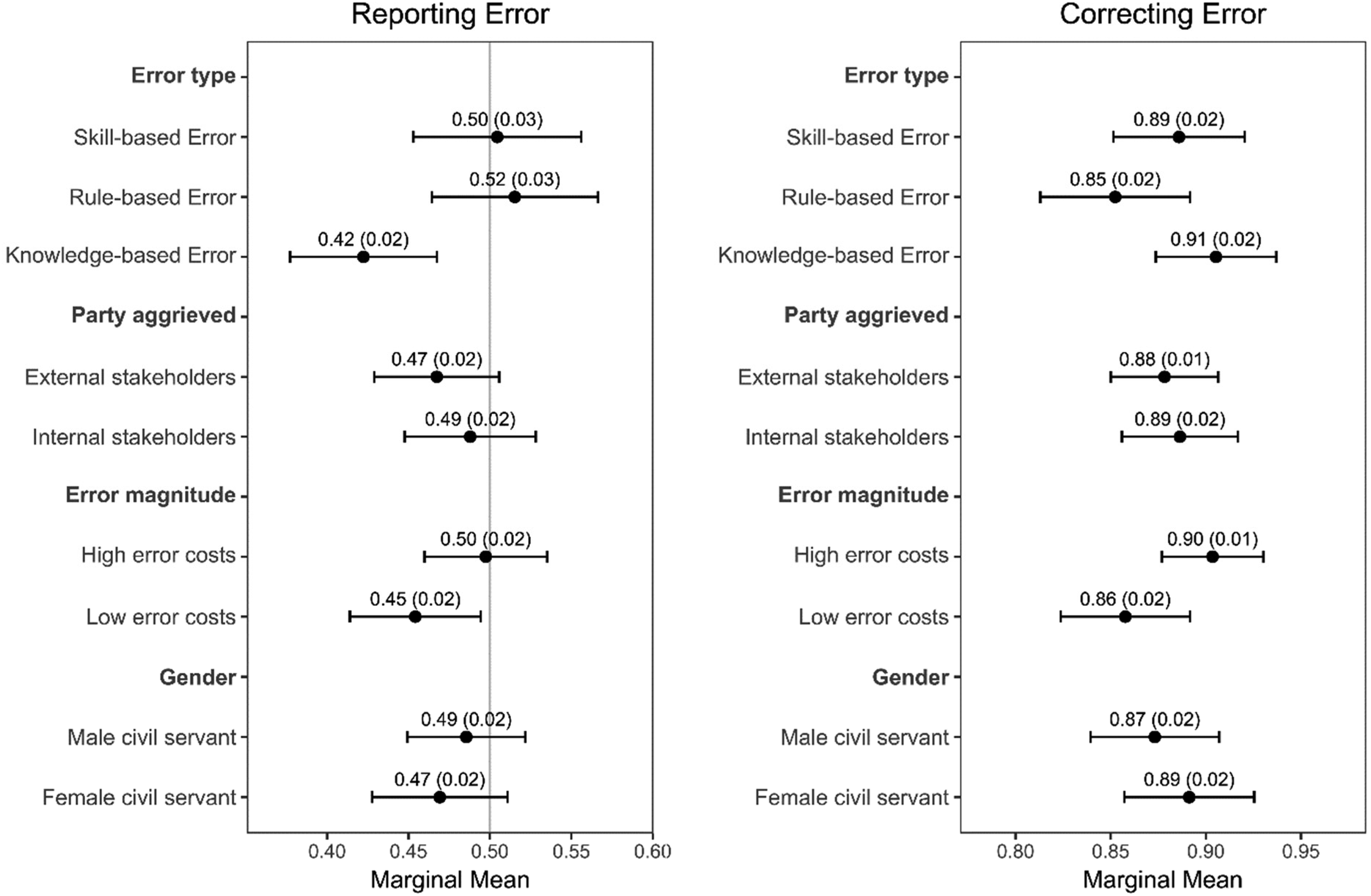

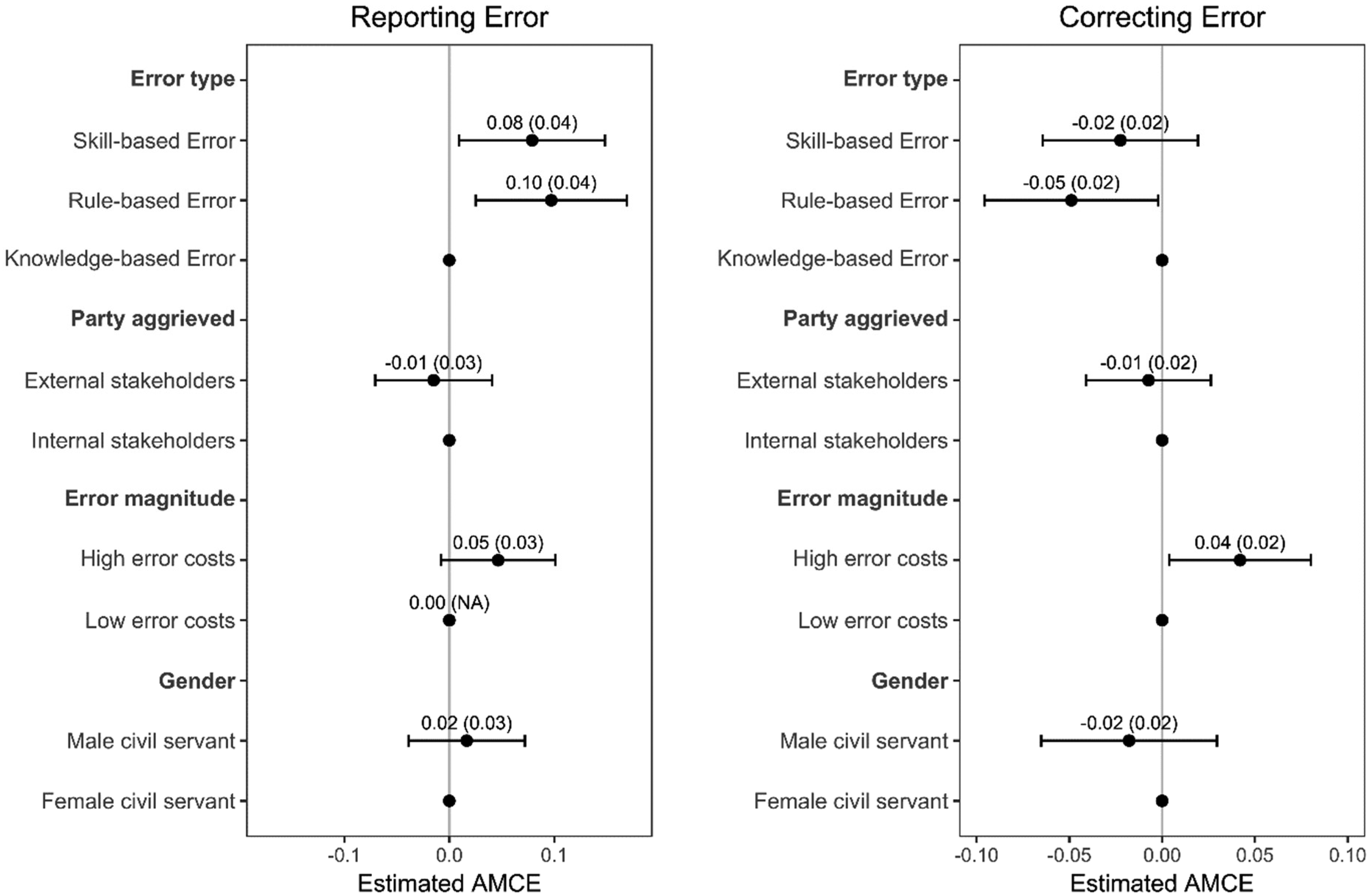

The conjoint design of our experiment allows us to test the impact of each error attribute on individuals’ error response while being able to randomize and independently vary each attribute's value at once. Following Hainmueller et al.'s (2014) and Bansak et al.'s (2023) formal explanations and best practices (e.g., Ghosn et al., 2021), we, first, describe the error attributes’ effects by estimating marginal means (95% CI, clustered SEs), see Figure 3. 6 Marginal means are statistically significant (p < .05) if their CIs do not intersect the vertical line at 0.5. Then, hypotheses are tested by assessing the effect size for each error attribute averaged over the joint distribution of all attributes (i.e., their AMCE) by estimating separate models for the two dependent variables of error response (i.e., error action: likelihood of reporting vs. hiding the error; and error communication: likelihood of correcting vs. ignoring the error). AMCEs have a clear causal interpretation namely the degree to which a given attribute level (i.e., the specific type of the error, the magnitude of harm, and the party aggrieved by the error) changes the likelihood of selecting the respective dependent variable choice option (e.g., reporting vs. hiding the error) in percentage points, relative to a baseline (Leeper et al., 2020).

Effects of error attributes on error responses (marginal means).

Effects of error attributes on error responses (AMCEs).

Following best practices, we explore the effect of covariates with sub-group analyses (e.g., respondents scoring high vis-à-vis low on IEO) by estimating distinct AMCE models and discuss them in the following sections (Ghosn et al., 2021; Hainmueller et al., 2014; Leeper et al., 2020).

Hypotheses Testing

All hypotheses focus on the relation between specific error attributes (i.e., type, magnitude of harm, and party aggrieved by the error). The subhypotheses H1a–f propose that civil servants will exhibit dissimilar strategies in handling different types of errors, that is, rule-based, skill-based, and knowledge-based errors.

The marginal means (Figure 3) reveal that civil servants are significantly less likely to report knowledge-based (0.42, SD = 0.02) and less harmful errors (0.45, SD = 0.02) instead of hiding them. Surprisingly, the likelihood of correcting instead of ignoring an error is significantly higher irrespective of error characteristics (all marginal means > 0.5). Investigating the AMCEs reported in Figure 4 quantifies these effects further: AMCE estimates reveal that, indeed, respondents are significantly more likely to report rule-based (AMCE = 0.10, p = .009) and skill-based errors (AMCE = 0.08, p = .027).6 This means that civil servants in our sample are 10% (respectively 8%) more likely to report these two types of error compared with knowledge-based errors. Study participants are significantly less likely to correct rule-based errors (AMCE = −0.05, p = .042) compared with knowledge-based errors while we find no significant AMCE difference for skill-based error correction (AMCE = −0.02, p = .294). This posits two important initial findings, which support the basic assumption behind the sub-hypotheses under H1: Error type matters for reporting and correcting errors because, firstly, different error types are associated with different error responses; secondly, error reporting will not automatically translate into error action in the form of actively seeking to correct the error; and, thirdly, people are more likely to report skill-based and rule-based errors. Hence, H1a, H1b, and H1c find support. H1d is rejected since the data reveal no significant AMCEs for skill-based errors on correction behavior. In contrast to the hypotheses, rule-based errors are the type of errors that is—comparatively—the most likely to be reported (AMCE = 0.10, p = .009) but also significantly more likely to be ignored (AMCE = −0.05, SE = 0.02), so that both H1e and H1f find no support.

Hypothesis H2a presumed that civil servants would be more likely to hide—instead of report—errors that may cause much harm in the form of creating high subsequent costs as a mechanism of self-preservation and to avoid blame. This hypothesis finds no support (AMCE = 0.05, SE = 0.03, p = .095). Yet, the data show that higher error harmfulness significantly increases the likelihood of correcting the error by 4% points (SE = 0.02), supporting H2b. Indeed, respondents are significantly more likely (AMCE = 0.04, p = .033) to correct high-cost errors compared with low-cost errors. This effect is independent from the type of stakeholder aggrieved (reporting: ACME = −0.01, SE = 0.03; correcting: ACME = −0.01, SE = 0.02), so that H3a and H3b find no support.

Exploratory Analyses

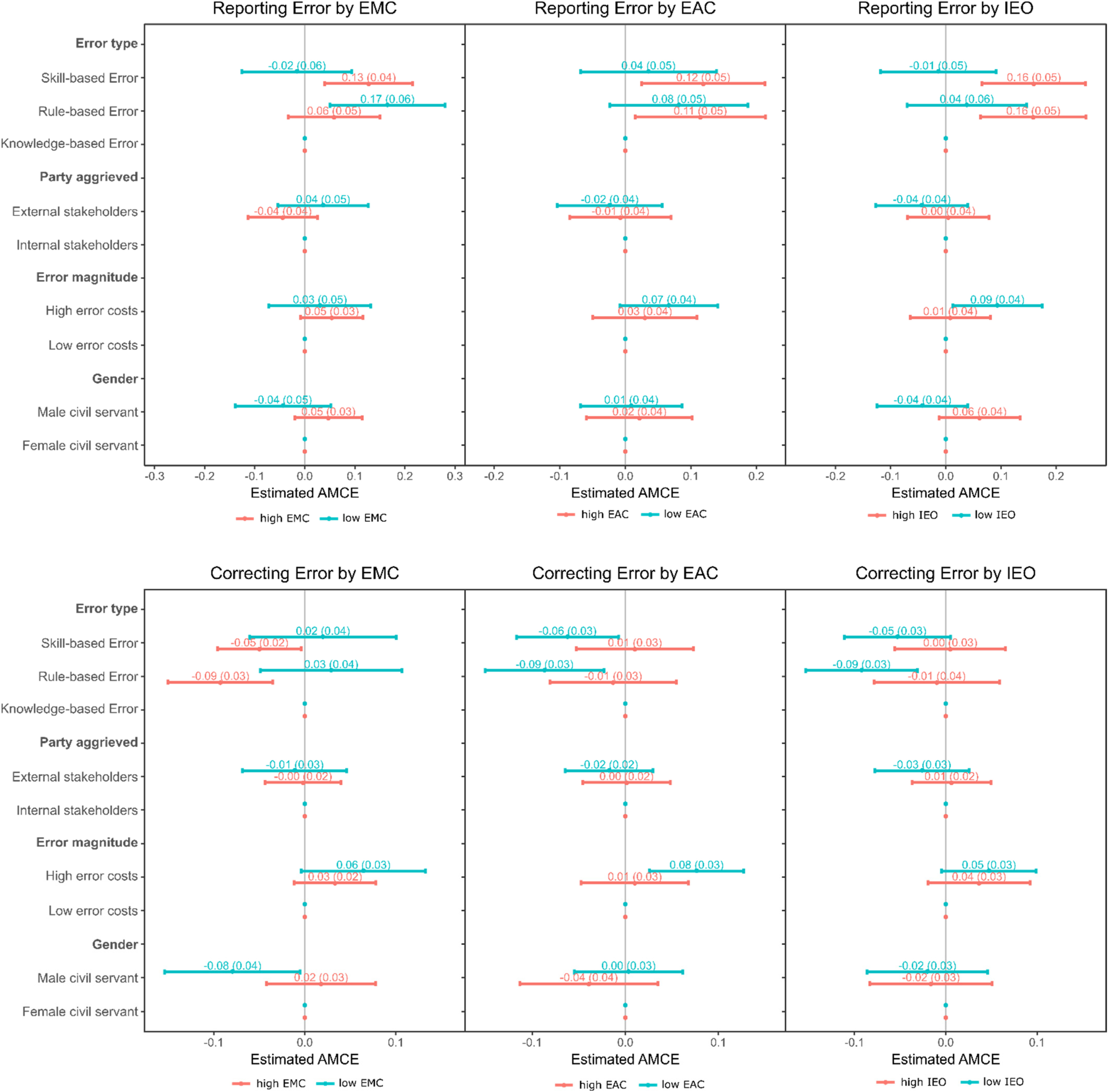

Given the mature state of research on the presumably strong impact of organizational error cultures (EMC and EAC) and IEO, exploratory analyses were conducted to qualify the robustness of the findings, based on sub-group AMCE analyses because the nested structure of the conjoint data does not allow for including control variables directly in the AMCE estimation models. Figures 5 and 6 present the AMCE estimates by subgroups split by below and above-sample average groups (i.e., “low EMC” are respondents with below-sample average scores on the EMC scale), by dependent variable.

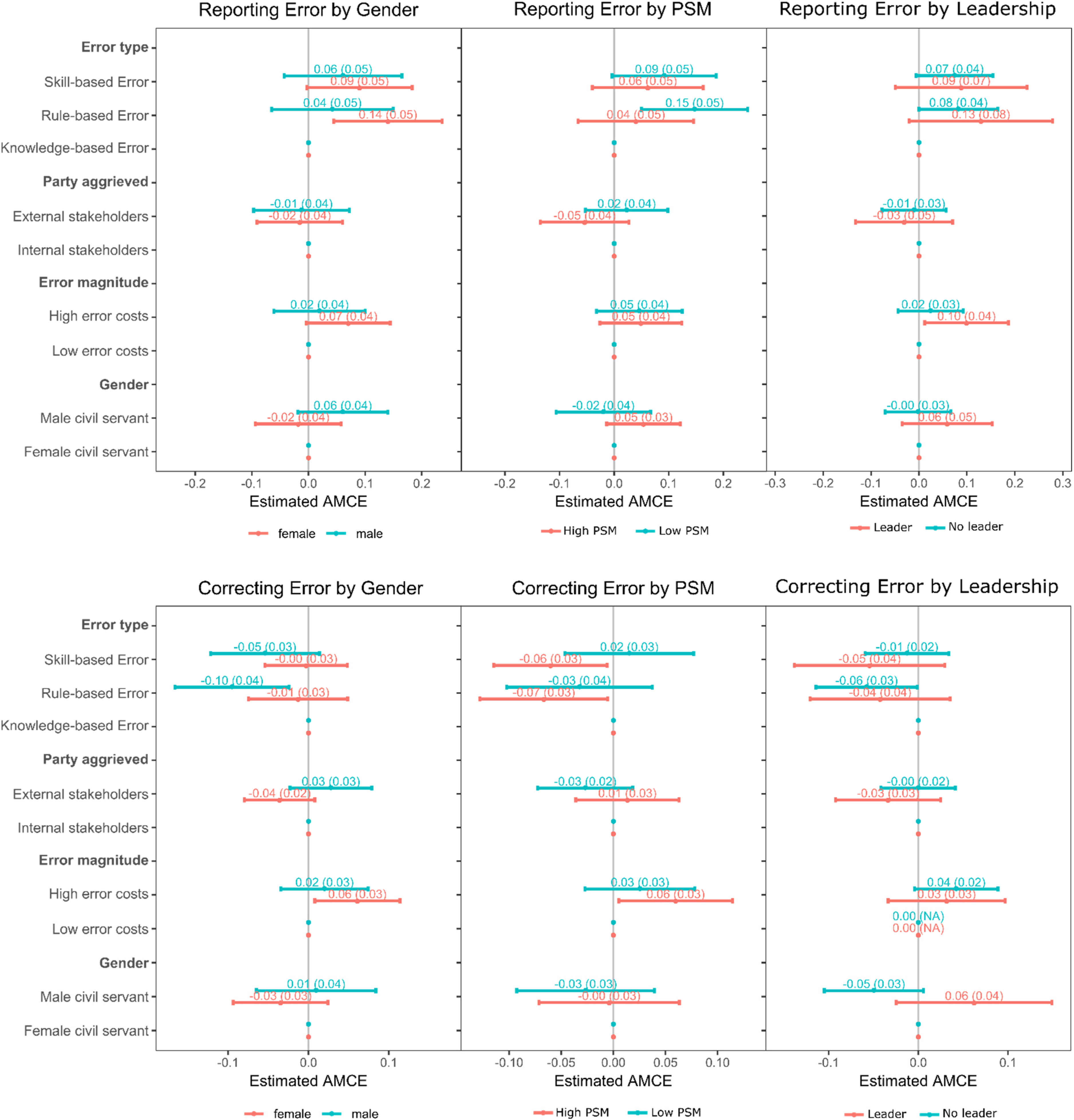

Subgroup analysis of AMCE, by EMC, EAC, and IEO (exploratory analysis).

Subgroup analysis of AMCE, by gender, PSM, and leadership responsibility (exploratory analysis).

These results show that error-type effects on reporting behavior are consistent across high vs. low organizational EMCs and EACs but, surprisingly, individuals with low IEO are more likely to report errors (skill-based and rule-based: + 16%, SE = 0.05). Furthermore, high IEO individuals are 9% (SE = 0.04) more likely to report errors with large expected harm. With regard to error action, individuals working in low-EMC or low-EAC organizations are significantly less likely to correct errors (−5% to −9% [SE = 0.03], respectively), depending on error type. Yet, higher error harmfulness increases the likelihood of error correction by 8% (SE = 0.03) for individuals working in high EAC organizations. Further exploring the impact of personal characteristics (Figure 6), the empirical evidence shows that men are 14% (SE = 0.05) more likely to report rule-based errors and they are more likely to correct the error if expected harm is high (+6%, SE = 0.03). This corresponds with what Prysmakova and Evans (2022) found concerning gender and whistleblowing, namely that women are less likely to report failures of their supervisors than their male colleagues. One conclusion could be that women still fear more severe consequences when reporting errors and wrongdoings and would behave differently due to societal biases concerning gender-stereotypical expectations of behavior.

Similar effects are observed with regard to high PSM (reporting rule-based errors: + 15%, SE = 0.05; correcting high-cost errors: + 6%, SE = 0.03). Low-PSM individuals are more likely to ignore errors (−6% to −7%, SE = 0.03), revealing a bright and dark side of PSM. Given that errors typically create problems that will have to be solved by leadership personnel, it is not surprising that respondents without leadership responsibilities are more likely to report high-cost errors (+10%, SE = 0.04) but no significant effects on error correcting behavior are observed.

Discussion

This study set out to explore what factors determine bureaucrats’ response to making mistakes, with a specific focus on the impact of error types and consequences, but also considering important micro- and meso-level factors that explain individual error-coping mechanisms in context.

First, the experimental data show that error characteristics significantly affect error response and the likelihood of coping by either approach-oriented (i.e., reporting and/or correcting) or avoidance-oriented behavior (i.e., hiding and/or ignoring), significantly expanding prior research on error and risk behavior (Møller, 2021; Tangsgaard & Fischer, 2024; Weißmüller, 2021). We find that error type matters in that bureaucrats in our sample are significantly more likely to report rule-based and skill-based errors than knowledge-based errors. Intriguingly, this higher tendency to report errors does not automatically translate into error correction as, for example, respondents are less likely to correct skill-based errors. Furthermore, higher error harmfulness increases the likelihood of correcting an error (but not of reporting it), suggesting that higher prospective error costs motivate approach-oriented action and a higher likelihood of pursuing a productive error-coping strategy. In contrast, the party aggrieved—external stakeholders vis-à-vis the decision-maker's organization—did not significantly affect error-coping behavior.

Second, this study advances scholarship with its novel micro-level exploration of error behavior (van de Walle, 2016), going beyond meso and macro-level antecedents, such as organizational structure, incentives, management support (e.g., Dahl & Werr, 2018), and organizational culture (e.g., Jafree et al., 2015), while simultaneously recognizing the impact of organizational work culture and individual dispositions. We find that the magnitude of harm for parties aggrieved by the error will inspire action (i.e., both reporting and correcting the error), which resonates with prior research by Patrician and Brosch (2009). Findings show that these situational outcomes are in fact stronger predictors of error behavior than more general stated individual preferences or organizational characteristics. This suggests that the cost-benefit evaluation that precedes error behaviors is primarily informed by the specific type of the error as well as its expected consequences, marking error behavior as highly versatile and idiosyncratic, combined with intuitive reactions based on psychological traits, such as risk-aversion (Dahlin et al., 2018; Emby et al., 2019; Wang et al., 2019).

Third, we find that error communication and error action are psychologically distinct to some degree because error characteristics affect them in different ways. This novel insight expands prior concepts of error-coping behavior but also has methodological implications: error behavior should be measured with specificity and (at least) a bifurcated distinction between communication and action to assure measurement precision and research validity. Our approach to distinguish between communication and action has proven to be useful in this regard.

Fourth, bureaucrats report rule-based and skill-based errors more often than knowledge-based errors and there is a difference with regard to the likelihood of correcting them. This resonates with Argyris’s (1991) and Brodbeck et al.'s (1993) argument that, for highly professionalized and specialized knowledge workers—such as German bureaucrats in the core administration—making knowledge-based errors triggers negative emotions because they demonstrate a lack of expertise and hence damages their professional identity more strongly than making other types of mistakes, resulting in a stress-induced avoidant coping reaction (Lazarus & Folkman, 1984). However, the comparison of bureaucrats with and without leadership roles shows that a higher hierarchical position and related responsibilities do not increase the likelihood of reporting and even reduces the likelihood of reporting high-cost errors. Admitting errors may be less risky for followers compared with leaders. We encourage future research into the sector-specificity of our findings and whether public sector workers with more skill-based professions will logically respond similarly to these types of errors. More research into the qualia of rule-based errors (i.e., whether they are perceived as red or green tape, see DeHart-Davis et al., 2013) will clarify whether the observed heterogeneity in stimuli effects originates from bureaucrats’ internalized concept of rules and the relevance of rule abidance vs. pragmatic improvisation (Houtgraaf et al., 2024; Weißmüller et al., 2022), or from concerns about being personally held accountable. This open question links with the finding that the locus of harm—that is, whether an error affects external or internal stakeholders—does not influence the likelihood of correcting an error may be specific to the public sector because bureaucrats are responsible for avoiding harm to the general public and are encouraged to prioritize societal over self-serving interests (Esteve et al., 2016; Schott et al., 2019). We also encourage future research to analyze whether different types of external parties aggrieved (e.g., citizens vs. noncitizens, citizens vs. companies, and citizens with different sociocultural backgrounds) would result in dissimilar error behaviors given that perceived citizen deservingness leads to systematic discriminatory bias in bureaucratic behavior (Jilke & Tummers, 2018; Moynihan et al., 2015; Weißmüller et al., 2022).

Fifth, surprisingly, organizational error cultures have a weaker impact on error behavior than suggested by prior (qualitative) research. Organizational EMC (high EMC) fosters error reporting but individuals working in an error-averse organization (high EAC) are also likely to report errors, but less likely to correct them. This finding substantiates van Dyck et al.'s (2005) suggestion that the supportive and learning-oriented climate of an EMC would lead to more error reporting. In summary, in our data, organizational error culture does influence individuals’ behavior when deciding what to do about their own mistakes but to a limited extent. The size of these effects may relate to the fact that we sampled seasoned bureaucrats, that is, highly professionalized and motivated (high PSM, low MD) knowledge workers. We find mixed patterns for the relationship between PSM and error response. Low PSM is related to more reporting of skill-based errors but no higher likelihood of correction. High PSM is associated with a higher likelihood of reporting rule-based errors but only when coinciding with high expected harm. This approach-oriented error behavior speaks to the main-stream PSM discourse stressing that self-sacrifice and individuals’ orientation toward the public interest will motivate approach-oriented error behavior. Professionals with highly specialized profiles, high commitment and experience (i.e., those who are good at their job) are notoriously ill-equipped to learn from making mistakes due to the learning dilemma of smart people (Argyris, 1991): People who are good at their job only seldomly make mistakes and they hence lack the opportunity to learn how to learn from and positively act upon failure, exacerbating the amount of stress-induced avoidance in case errors actually do occur. This paradox of single vs. double-loop learning capacity may also explain the observed patterns of error responses for high-PSM respondents and leaders in our sample.

Overall, error type is a strong predictor of error behavior while IEO and organizational error cultures have only small effects, mitigated by error type, if any. One explanation is that the situation presented in the experimental vignette scenario calls for an immediate error response. Urgent responses usually coincide with quick and intuitive decision making which relies on deeply internalized heuristics and values as benchmarks to guide behavior, while less time pressure gives room for deliberation prior to making a decision (dual process theory, see e.g., Chaiken & Trope, 1999; Stanovich & West, 2000). This also explains why our results contrast with prior qualitative research by Møller (2021) that suggested that organizational culture should impact judgment more strongly but only if socio-dynamic calibration processes in the form of deliberation can take place. In less urgent situations, error response may be more likely to rely on cognitively elaborate cost-benefit analyses into which organizational culture feeds in as internalized normative beliefs (see e.g., Ajzen’s (1991) theory of planned behavior).

Our study highlights that public administration (at least in Germany) may not be the stereotypically risk and error-averse work environment that it is often conceptualized to be (Crosby et al., 2017; Sørensen & Torfing, 2011). On average, our sample reports experiencing error-friendly work climates which substantiates prior findings by Brewer and Lam (2009). Nevertheless, individual traits still matter. Our representative sample of bureaucrats is predominantly risk-averse, a trait that correlates strongly with avoidant error behavior and a peculiar shyness toward sharing their errors with others. In contrast with Tepe and Prokop (2018), who found that risk-averse students of public administration do not behave risk-aversely, our results revealed risk propensity combined with controlling for MD and PSM indicates that bureaucrats do not hide their errors based on immoral intent but because their risk-aversion amplifies the stress induced by making mistakes, and independently so from organizational culture. In line with prior research by Weißmüller (2021), who found that risk aversion is associated with public sector socialization and self-selection into public employment (Seidemann & Weißmüller, 2024), we infer that the strong risk-aversion–error behavior relationship is indicative of a social learning process associated with building a professional identity in the particular rigid rule-based system of German administration. This is a call for action for public personnel management and public leaders. Learned risk aversion as a professional norm hinders error reporting. If errors are corrected but not shared, organizational learning cannot take place, and errors will inevitably be repeated, stunting innovation, and development (Argyris, 1991; Barach & Small, 2000; Catino & Patriotta, 2013; Frese & Keith, 2015; Wang et al., 2019). Future research nested in other administrative traditions is encouraged to assess the culture-specificity of these novel findings and the degree to which they generalize beyond the rule-focused Rechtsstaat tradition-logics of German public administration (Bach & Veit, 2017; Ziekow, 2021).

Limitations

One limitation of the current study is that the range of potential error responses was limited and demanded an immediate response. While the vignette scenario was deemed realistic and created sufficient variation and arousal (Hughes & Huby, 2004), conjoint experiments come with high internal validity but lower ecological validity. One potential avenue to develop our theoretical and empirical model further is to investigate longitudinal effects in error handling as a learning process over time. For instance, by examining learning processes and adjustment to recurring errors. Another limitation relates to the fact that we conducted a survey experiment in which participants faced no real-life consequences from opting for a particular error handling behavior. Although stakes are low, this setting is realistic for our target population because Germany's tenure-based employment system means that civil servants’ performance usually exhibits only a minor influence on their renumeration or further career development. Replication studies in more punitive, nontenured, job-based administrative systems (such as those informed by the Anglo-Saxon tradition of public administration) are needed to assess the context-specificity of our findings.

Practical Implications

Error behavior strongly depends on the error type and its expected harmfulness. What can practitioners do since these characteristics may largely evade their control? Our data suggest that employees are more likely to report rule-based and skill-based errors and are (indicatively) less likely to correct rule-based errors. Consequently, public managers may want to consider implementing error management systems and risk mitigation strategies that are particularly targeted at buffering these types of errors. For instance, implementing the four-eye principle and regular training to avoid rule-related errors, making sure employees receive sufficient training on procedures to avoid these types of errors (as shown by Spreen et al., 2020), and implementing error feedback systems that reduce shame and anxiety related to making and reporting one's own mistakes, for example, anonymous reporting systems and peer-feedback.

The evidence shows that bureaucrats are (in general) likely to correct errors but only report them under certain conditions, which serves the public interest but does not help the organization to learn from mistakes. Leaders have the power to set positive benchmarks for their followers’ behavior. To enhance the likelihood of error reporting, leaders should serve as role models and foster employees’ sharing behavior by committing to bilateral transparency, explicating the goal of continuous improvement, co-creation, and adequate recognition for proactive error-sharing behavior (Argyris, 1991; Tavares et al., 2021).

Strategic recruitment and training may also play a bigger role in making public administrations more error-savvy than previously anticipated. For instance, human resource managers are encouraged to strategically recruit talent with lower risk-aversion or highly positive IEO for error-prone tasks and positions that are high-risk/high-gain, such as in innovative processes and organizational development, tasks associated with implementing new technologies, and in cases in which organizational interest in reporting errors is particularly high, such as in sensitive interactions with stakeholders. Furthermore, policy-makers and public managers should critically assess whether current staff training programs sufficiently recognize that effective error training should equip their workforce with training in both appropriate behavioral strategies to correct and communicate about errors to facilitate learning from mistakes and mitigate organizational risks.

Supplemental Material

sj-pdf-1-arp-10.1177_02750740241267941 - Supplemental material for What Determines Civil Servants’ Error Response? Evidence From a Conjoint Experiment

Supplemental material, sj-pdf-1-arp-10.1177_02750740241267941 for What Determines Civil Servants’ Error Response? Evidence From a Conjoint Experiment by Caroline Fischer and Kristina S. Weißmüller in The American Review of Public Administration

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.