Abstract

This study explores the experiences of attempted frauds and victimisation which use largely telephone-based means of communication on predominantly over 75s in the United Kingdom. Using a postal survey targeted at the clients of a charity working mostly with this age group, two surveys were conducted during the 18-month life of the project, securing almost 2,000 responses, which sought to explore their experience of fraud as part of a wider evaluation of a fraud prevention initiative. The surveys were supported by 18 interviews with clients and 7 interviews with the charity co-ordinator and volunteers. The research found higher rates of victimisation than the norm for this group, combined with a large number of attempted frauds predominantly via the telephone, with 20% of respondents experiencing at least weekly attempts. The research highlights the first significant evidence of the fears, concerns, and anxieties among a minority of this group of frauds/scams and their impact on their daily lives. The paper also offers insights into telephone fraud and a typology of this crime.

Introduction

Some days, I have so many scam calls I could scream. I am disabled and I find these calls distressing as blocking calls does not work as they use different numbers. (Female 774 NV)

In recent years, the dominant discourse regarding fraud has become cyber-related, with a small but growing body of research rooted in how information and communication technology (ICT) such as websites, emails, social media, the dark web, hacking, and so on have become central to perpetrating large numbers of frauds (see, e.g., Cross and Lee, 2022; Jung et al., 2022; Leukfeldt and Holt, 2022; Reyns et al., 2019; Whittaker and Button, 2020). There is little doubt that cyber accounts for a significant volume of fraud, indeed the Crime Survey for England and Wales (CSEW) estimated 61% of frauds have a cyber element (ONS, 2023). The focus on cyber, however, has obscured the large numbers of frauds that are still perpetrated by the telephone either completely or partly (i.e., a phone call that leads to the victim switching on their computer). Telephone-based frauds are particularly prevalent among older adults, who tend not to use ICT as much and as the quote illustrates at the start of this article, they have a significant impact on them (ONS, 2021a). There has been very little research on telephone fraud and much of this small body of knowledge is based upon American studies from around 20 years ago. This type of fraud therefore deserves more attention, particularly as this paper will later show, that telephones are still a major vector of attack for older adults. This paper draws upon research on older adults based upon surveys and interviews and will provide unique insights into the bombardment of them with attempted telephone frauds and the impact these attempts have upon them.

This paper will explore telecommunications fraud by starting with a review of the limited literature in this area. It will examine the extent of telecommunications fraud, identifying the different types and developing a typology. The paper will then set out the methodology for this research before presenting the findings.

Telephones and crime

The advent of mass use of telephones in the post-war period was not accompanied by a wave of research on telephone crime. This probably reflected a smaller number of crime-orientated researchers at this time and a limited number of new crimes that emerged, compared with the advent of mass cybercrime more recently. Two areas of research on telephone crime have stimulated a small body of scholarly output, some based on abusive phone calls (Katz, 1994; Sheffield, 1989; Tseloni and Pease, 1998) and some based upon fraud (Reiboldt and Vogel, 2001; Sechrest et al., 1998; Shover et al., 2003; Titus and Gover, 2001). Compared with cybercrime, however, this output was relatively small. Before some of this research is considered, it would be useful to conceptualise and explore the nature of telephone fraud.

Telephone fraud

Fraud covers a wide range of behaviours ranging from staff exaggerating their expenses, to complex investment frauds perpetrated by corporations, to offenders impersonating official bodies to trick victims into making payments or revealing their important personal information. The essence of fraud is some form of deception which causes a loss to the victim or gain to the offender. The scope of this article is the frauds targeted at individuals via the telephone predominantly targeted at older adults. Some also call these frauds, scams, but as Button and Cross (2017) have noted scams also encompass unethical behaviours which are not necessarily illegal. To many professionals and the general public, however, frauds and scams are used interchangeably, and for this reason, the questions used for this research combined frauds and scams. Fraud and scams are therefore used throughout this paper to describe the illegal and unethical schemes promoted via the telephone that are designed to cause the victims either a direct or indirect financial loss. It is also important to understand what is meant by telecommunications and the typology of it.

Telecommunications is often a term that is used to precede certain types of fraud. This word is in reality as broad as cyber as it means the exchange of information over a distance via wire, cable, radio waves, and so on. As Ofcom (n.d.) (the UK regulator of communications) describes it, the ‘Conveyance over distance of speech, music and other sounds, visual images or signals by electric, magnetic or electro-magnetic means’. Telephones can also be wide ranging, covering landline-based phones which are used for predominantly voice-based communication; mobile phones which can be used for this and text messaging (SMS); and smartphones which in addition to voice and text messaging, add computing capacity, which can connect to the Internet. The latter type of phone is a means for a much broader range of cyber-frauds to occur. The advent of mass use of video calls through Skype, WhatsApp, Zoom, and Microsoft Teams during the pandemic adds yet another blurring dimension to this area. The focus of this paper is on frauds that use telephone calls via the voice using any of the three types of phones or SMS messaging. There are a wide variety of frauds and scams that use these communication means and these will now be explored using the following typology developed during this research, based upon the experience of the victims and the literature review of the offender’s modus operandi:

Sales talkers

The first type of telephone fraud which is very common is done by fraudsters who phone potential victims trying to sell them worthless goods or services. Telemarketing of bogus investments has become a major form of this type of fraud, often termed ‘boiler room’ frauds because of the high-pressure sales the fraudsters use (DeLiema et al., 2020; Shover et al., 2003, 2004). Investments are not the only products which are sold by this means; other common examples include consumer products, subscriptions to publications, lottery tickets, and charity donations.

Action talkers

Another variation on telephone fraud is fraudsters who call potential victims and present a convincing scenario, which causes them to pursue some form of action, such as switch on their computer and give control to the criminals, or pay a fee/transfer money. There are a variety of frauds that have occurred in this category. One common example is a phone call from someone claiming to be an Internet provider such as BT (in the United Kingdom), who then claims there are problems with the Internet and if they switch on their computer they can help improve speed, and that there might be monetary compensation for poor service. The unsuspecting victim then switches on their computer and often downloads software giving remote access to the fraudsters. Another common fraud in this category is where the victim is called by fraudsters impersonating the police or bank security to be told that there is a security issue with their account and they need to transfer their money to a ‘safe’ account. A more sinister variation is where individuals have been called by what they think is the police and told they have downloaded child abuse images, but because it is low level, if they pay a penalty, they will avoid prosecution (Button et al., 2020; Kerr et al., 2013).

Automated talkers

Another variation is robocalls, where automated voice messages target victims encouraging them to press a number on their phone. This connects them to a premium number or to a bogus call handler (Mailonline, 2016).

Receptive talkers

All of the examples above involve the fraudsters targeting the victim with a call, but there are some frauds that encourage the victims to call the fraudsters. Websites, emails, SMS messages, and so on create scenarios where the victims are encouraged to call a number, which is in reality the fraudster’s number. A common type of fraud in this area is the tech support scam, where the victim receives an email or visits a website that triggers a popup, which states there is some form of technical issue with their device and they need to call a number to resolve it. This ultimately leads to them being asked to pay for bogus products and/or reveal sensitive personal information (Miramirkhani et al., 2016).

Texters for money

SMS messages that impersonate organisations asking for fees are also common. One of the most frequent is text messages that claim to be from a courier and provide a link for a small payment to be made to ‘secure’ the delivery of a parcel (Button et al., 2020).

Texters for action

A variation on the text for money is one that seeks personal information or provides a link to a website that downloads malware (Button et al., 2020).

Research on telephone frauds

The aforementioned examples illustrate the diversity of telephone frauds. There has been, as already noted, surprisingly very little research that has specifically looked at telephone-related fraud. The vast majority which has is American and largely undertaken over 20 years ago. Some studies have explored the dynamics of telemarketers involved in selling bogus products and services over the telephone (Doocy et al., 2001; Shover et al., 2003, 2004). Exploring the impact and susceptibility of the victims of such frauds has also been examined, again largely in the United States (Alves and Wilson, 2008; Lee and Geistfeld, 1999; Policastro and Payne, 2015; Reiboldt and Vogel, 2001; Sechrest et al., 1998; Titus and Gover, 2001; Weiler, 1995). Preventive measures have also been explored by several authors (Aziz et al., 2000; Cohen, 2006; Fawcett and Provost, 1997; Hines, 2001; Lee and Park, 2023). Some authors have looked at specific types of frauds delivered via telephones, such as investment fraud (Barnes, 2017) and voice phishing (Choi et al., 2017; Lee, 2020).

There have, nevertheless, been a number of recent reports by reputable organisations that have illustrated telephone fraud and nuisance calls are a major problem. Ofcom (2021) (the regulator of communications in the United Kingdom) conducted a prevalence survey of the adult population, securing data on exposure to some form of suspicious messaging, and found that 71% had experienced a suspicious text message, 43% a call on a mobile, and 41% a call on a landline telephone. For those aged 75+, landlines were the most common means of communication, with 61% for landlines compared with 55% for text messages. A report by the Sussex Elders Commission (2016: 14) drawing upon a survey of 1,434 older adults in Sussex found that 15.2% worried when the phone rang. The report noted: Persistent, unwanted calls lead to anxiety and fear and often to people not picking the phone up and missing family or care and health-related calls.

In a smaller study evaluating call blockers, 94% of applicants reported receiving fraud/scam or nuisance phone calls in the previous 6 months (Rosenorn-Lanng and Corbin-Clarke, 2020). There is therefore some strong evidence of a problem of telephone frauds and this paper contributes further to this evidence by providing some unique findings from a study of adults largely over 75s and their experiences of telephone fraud. It also offers insights into the fear of fraud.

The impact of fraud victimisation has been shown in a growing body of research illustrating issues from financial loss, anxiety, stress, and mental health problems to feelings of and attempts at suicide (Button et al., 2014; Cross, 2016; DeLiema et al., 2021; Kemp and Erades Pérez, 2023). There has been very little research, however, that has explored the fear of fraud, particularly for those who have not been victims and for older adults. Cross and Lee (2022) have noted the fear among largely female romance fraud victims, while Brancale and Blomberg (2023) noted some fears among older adults in retirement homes in the United States concerning fraud, often linked to other concerns. There is a much deeper base of research on the wider fear of crime, particularly among older women (LaGrange and Ferraro, 1989; Ollenburger, 1981; Warr, 1984). However, even though some of these studies touched upon frauds such as ‘cons’ and ‘consumer frauds’, the risk and exposure to fraud are much more significant than when many of these studies were undertaken, with the advent of the Internet, social media, email, and cheap telephone calls to name some. Cybercrime fear has secured much more interest recently (Brands and Van Doorn, 2022; Cook et al., 2023; Virtanen, 2017). However, while there is an overlap of some cybercrimes with frauds there are many frauds that are not cyber-perpetrated. Cybercrime covers a much wider range of offences beyond fraud such as cyber-bullying, stalking, and others (Ibrahim, 2016). The fraud-related studies in cybercrime also tend to focus on a very narrow range of finance-related cybercrimes such as hacking, phishing, identity-related frauds, and online shopping, and for older adults, a significant number do not use the Internet (see later). Telephones and their impact are clearly missing from this literature. This paper will therefore explore the impact of fraud and attempted frauds, particularly by the telephone on older adults. It will focus in particular on any fears and concerns that emerge from telephone fraud.

Methods

This research was the result of a commission from a UK charity, which works with largely (but not exclusively) over 75s to improve their social connections and reduce loneliness. The main purpose of this research was to evaluate a fraud awareness campaign initiated with the aim of increasing their ability to identify and deal with potential frauds/scams and ultimately reduce victimisation. The findings of the evaluation are beyond the scope of this paper and will be published separately. This paper focuses upon their experience of telephone-based fraud and fears related to that.

It is also important to note some of the challenges of conducting this research. First, the beginning of this project was towards the end of the COVID pandemic. Many of the charity clients were vulnerable, and in the context of the post-pandemic period, face-to-face interviews were difficult to arrange. As a consequence, all interviews were conducted online or via the telephone. Second, as the project progressed it was clear that for a small minority of clients, the mere mention of the word fraud and scams caused significant concern and anxiety, meaning that many were reluctant to participate.

As the project was primarily constructed to evaluate the charity fraud prevention initiative the plan was to survey and conduct interviews before execution of the project to secure baseline data, allow a period for implementation, and then conduct another survey and further interviews 6 months after the implementation. A control group was also included for this purpose (and will be referred to in the presentation of data in this paper), but the differences for this group are not explored as these relate to the evaluation of the initiative. Two postal questionnaires were sent to the charity’s clients: one distributed between January 2022 and March 2022 (6,595 sent, 1,177 usable responses – 17.8% response rate) and a second between November 2022 and February 2023 (4,053 sent, 820 usable responses – 20.2% response rate). The survey and interviews in both phases targeted the same group – all the clients of the charity, although the second survey would have picked up some new respondents who were not clients in the first survey, this is likely to be a small number. There was also a high turnover of clients due to deaths, movement to care homes, and long-term hospitalisation, exacerbated further due to COVID. Indeed, in the first survey, the records of the charity had not kept up to date due to COVID deaths and this explains the significant decline in the population between the two surveys. Postal questionnaires were used because many of this age group do not use modern technology and telephones were a major source of fraud attempts and deemed to be unlikely to secure a good response rate. It was also felt they could cause distress to the participants because anonymous calls are such a source of fraud/scams. A response rate of 20% might seem low but responses to postal surveys are in serious decline in general and given the feelings of many of the older adults this can be considered a very good response rate for this age group (Stedman et al., 2019). In addition to the two surveys, 18 interviews were conducted with older adults in the two periods above. These were sourced via the charity who used their coordinators to ask for volunteers whose information was then passed to the research team to contact. Some of these may also have completed the postal questionnaires. Five interviews were also pursued with volunteers who work for the charity to support their activities at the end of the project (November 2022 to April 2023). The main coordinator was also interviewed before and after the implementation of the project. The interviews and questionnaires directed at the clients explored personal demographics, lifestyle and satisfaction, fraud awareness, security behaviours, trust with communications, experience of fraud, and impact of frauds. The postal questionnaire had 27 questions, and the semi-structured interview schedule had 12 broad questions. Once the postal questionnaires were returned, the responses were entered into online surveys and the quantitative data were then extracted into an Excel sheet and analysed. The qualitative data were manually typed into another Excel document and coded along with the interviews, which were transcribed and assessed using thematic analysis. Prior to conducting the research, the project received ethical approval from the university ethics committee.

Throughout this paper, older adults interviewed have been given a pseudonym. For the questionnaire, written responses for the first survey respondents have a number, either male or female, and whether they are a victim of fraud in the prior 6 months: NV = non-victim and V = victim. The second survey had a control group related to an evaluation that was also conducted so they have the additional letters of either C, they were in the control group, or N, they were not.

Findings

Demographics of participants

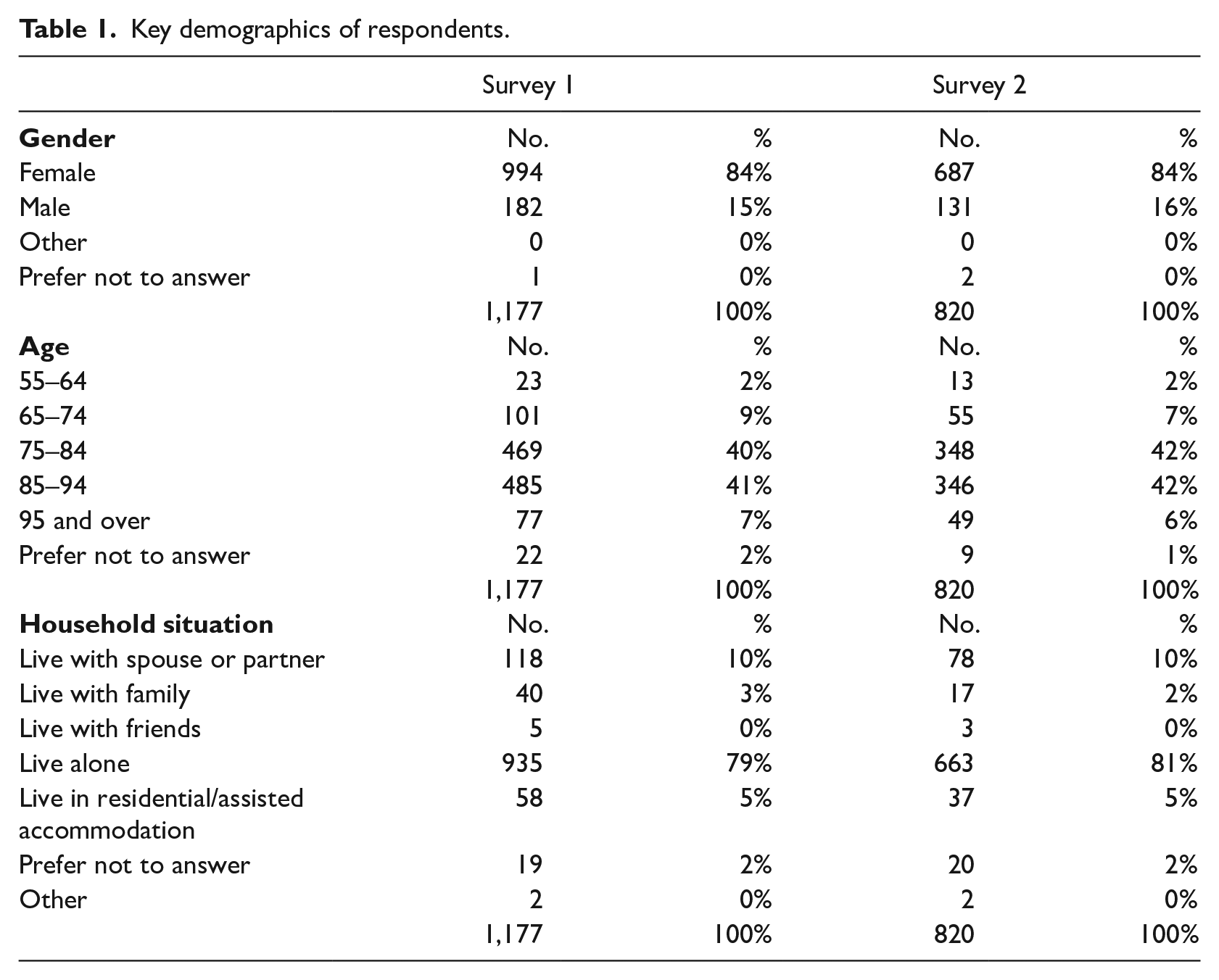

Table 1 illustrates some of the core demographics of the older adults who responded to the survey. The survey was very biased towards female respondents with both surveys recording 84% female respondents. Not surprisingly given the client groups, there is a clear dominance of over 75s with around 90% of responses.

Key demographics of respondents.

Respondents were also asked to indicate their household situation. In both surveys, around 80% of respondents indicated they lived alone. The next most common were those living with a partner with 10% of respondents in both surveys. Around 5% in both surveys lived in assisted accommodation, with a sprinkling of responses living alone.

Daily lives of participants

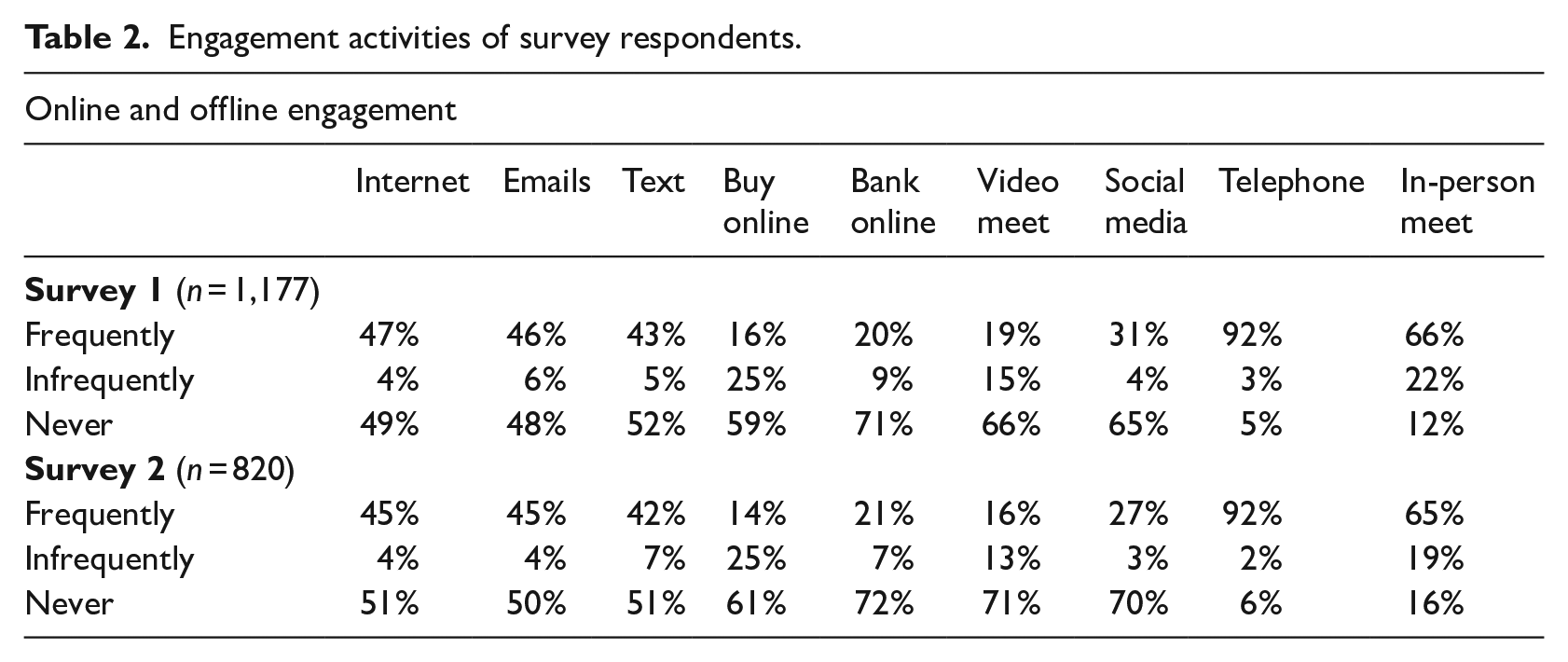

The survey respondents were asked about their daily lives and how often they used the Internet, email, text, banked online, met online, used the telephone, and met in person. They were asked to indicate the frequency with the categories daily, weekly (which was collapsed into frequently), monthly, yearly (which was collapsed into infrequently), or never (Table 2).

Engagement activities of survey respondents.

In both surveys, around 50% never used the Internet. The Office for National Statistics collects data on this, and in the most recent survey for 2020, of the over 75s, 39% had never used the Internet (43% of women and 33% of men). The survey respondents can therefore be considered less Internet-orientated than their wider age group (ONS, 2021a). Furthermore, around half the respondents never used email or texted. An even larger group never banked online at just over 70% in both surveys. Around 65–70% also did not use online video chat or social media. However, around 66% frequently met people in person and the most frequent method of communication was the telephone (92%).

There would therefore seem to be around a fifth of the sample very technologically engaged using the Internet, email, online banking, and social media regularly. There was then another 30% who used the Internet and some of the related technologies more conservatively, and about half disconnected from these technologies and relied on telephone and in-person meetings.

Victimisation

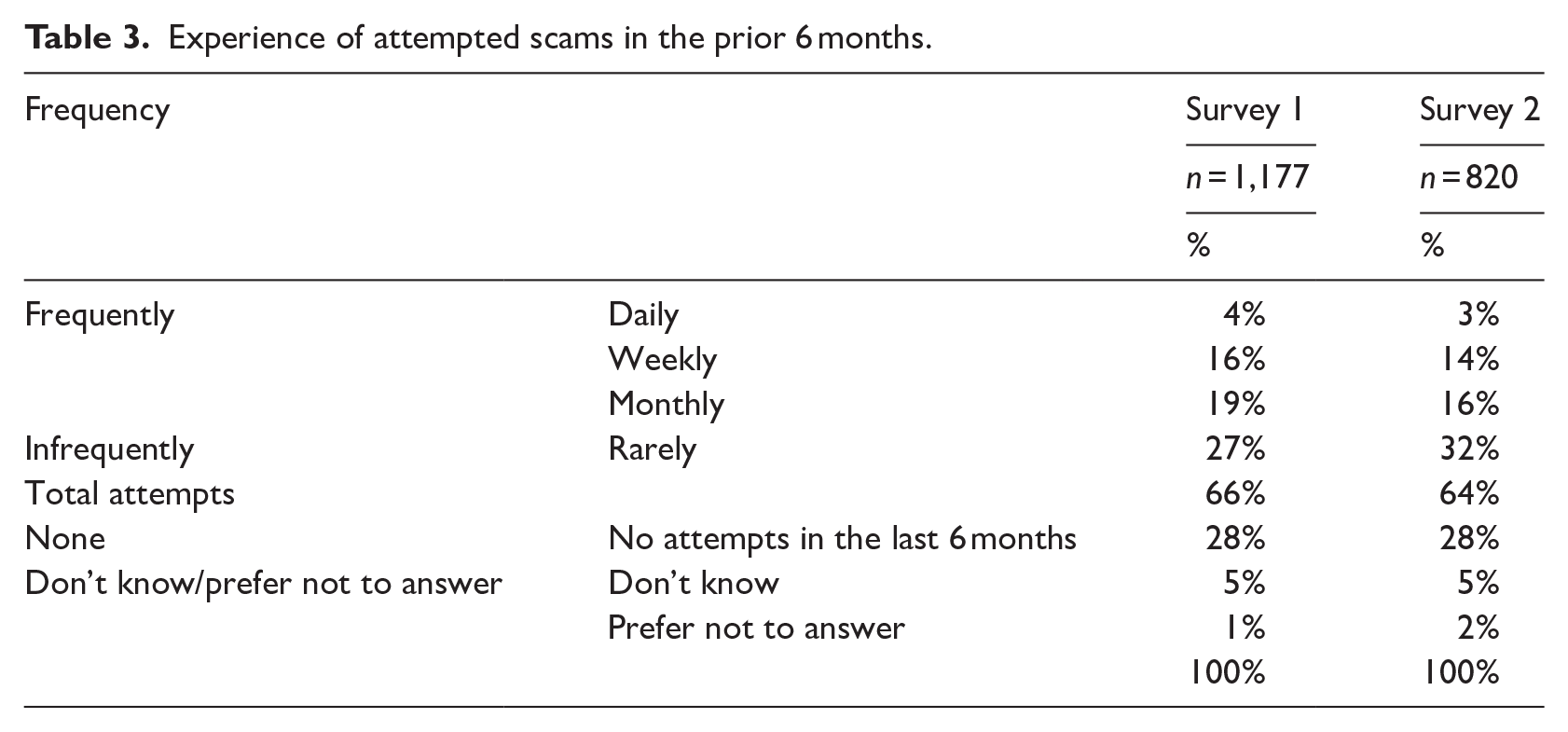

The research sought data on their experience of victimisation, asking in both surveys ‘In the past 6 months have you experienced being a victim of fraud/scam (in which you have actually lost money or revealed sensitive information as a consequence of the scam)?’ (Table 3). The letter accompanying the questionnaire defined fraud as ‘an attempt to secure information or money by deception, which is a criminal offence’, and scam as ‘a wider range of behaviours where the scammer may try to trick people by charging too much or getting them to buy goods and services they don’t need’. Six months was used rather than a year to enable a comparison to take place for the evaluation within the specified period sought by the charity.

Experience of attempted scams in the prior 6 months.

In both surveys, 8% of respondents had experienced a fraud in the past 6 months. The CSEW data for over 75s provides a victimisation rate of 5.8% in the prior 12 months, so the rate of victimisation was much higher among this group (ONS, 2023). This could be explained by the wider use of frauds/scams or repeat victims. Another very significant finding from this research was the sheer number of attempted frauds older adults experience. Over both surveys, the results were stable with at least two-thirds experiencing at least one attempt in the past 6 months. About one-third (32–40%) experienced frequent attempts (daily, weekly, or monthly). A small minority (3–4%) experienced a high rate of attempted daily victimisation. An increased frequency of attempted fraud not only increases the risks of successful fraud but, as will be shown later, also impacts on fear.

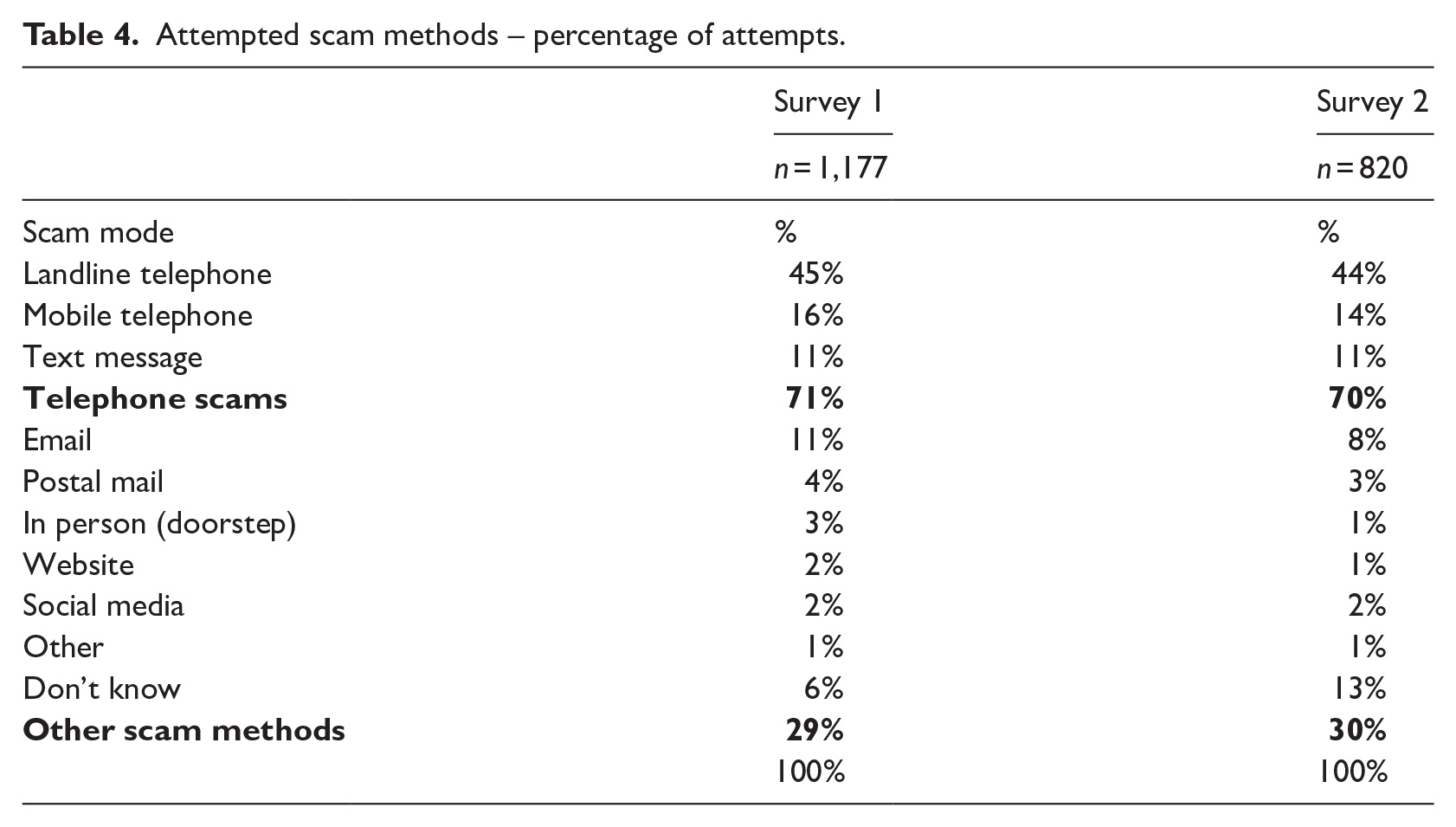

Fraud attempts by telephone

The telephone was the dominant method of communication for frauds/scams for this group. Nearly three-quarters of attempted frauds/scams involved landline or mobile telephones: 60% involved voice calls and 11% utilised text messages (Table 4). Attempted frauds were experienced via email, post, in person, a website, and social media, but at a much lower frequency. Considering that the telephone is the most common method of communication for older persons, telephone frauds/scams clearly pose the most serious threat to older adults.

Attempted scam methods – percentage of attempts.

Several interviewees talked about their experiences of attempted frauds. Jamie illustrated the sheer number of attempts he experienced: Well, I’ve had about 20 odd this year. Over 20. Yeah. Since 7 March I’ve had seven. I’ve not recorded one of them because I haven’t had time to do it all, but you can understand there’s so many of them (Jamie).

Several survey respondents also commented on the ubiquity of attempted frauds/scams: Telephone scammers seem to target areas full stop if I receive one call, then a few days later I received another and next door neighbours received them on the same days. (Male C53 NV) I receive suspected scam telephone calls on landline and mobile on average twice per day . . . I think we live in a very sad world and I have come to suspect everybody. (Male 160 NV) I get about 5 calls every day saying money taken out of my bank. I wish I could block them. (Female 1051 NV) I regularly have post office scams to say they have a parcel for me and I am not in to receive it. If you delve into it they say you owe £2.96. Follow it up you find they want your bank details to pay for it. I keep blocking it but always appears. It is a nuisance. (Female 298 NV)

Some respondents also indicated they were attempting to deal with the calls and also appreciated some were not all frauds, but the technology designed to help them was not effective as one respondent completing the questionnaire for their mother noted: My mum has dementia . . . She has received constant cold calling from Indian call centres. They are probably not scams but nuisance calls. The more you answer, the more they call. Every day numerous times a day. She has the BT number to direct nuisance calls to so they are blocked, but that fills up and you have to delete numbers to make room for more. They just keep coming. (N579 NV)

Some respondents just noted the problem asking for something to be done about them: I would like something to be done about nuisance phone calls, surely they could be banned. Somedays it is one after another and one of my worst complaints is Amazon. (Female 698 NV)

Some attempts were such that the older adults easily recognised them and terminated the phone call: I often get scams by phone, I recognise the woman’s voice. I ignore them. I had one day informing me that my bank had been scammed that morning. I started to laugh, what, I had been in my bank that morning and then you knew nothing about it. (Female N399 NV) The landline telephone is the greatest offender in my case. I regularly get calls with the sounds of a busy office in the background. I immediately put the phone down if I hear this. I receive these calls several times a week. Some callers are persistent and call again several times after I have put the phone down. I receive these calls despite having a nuisance call blocker on my line. (Female 1050 NV) I was almost taken in, where a phone caller purporting to be a Met police officer said my credit card had been cloned and been caught in attempted use in Oxford St. Perhaps I should contact my bank to check fraudulent payments. He asks which bank? I said Halifax (he should have known this if legitimate). I said I would ring them. ‘What phone will you use?’ My mobile being aware of the red lights of reported scams. You shouldn’t use your mobile it’s less secure he insisted. He rang off. It would have been easy to be taken in if I was not aware of scammers impersonating your bank. Publicity of scams of this sort is crucial. (Female 106 NV)

Some attempts were much deeper with the older adult almost succumbing to a major fraud: I am afraid of scams. I got caught by one pretending to be my daughter asking for money. I believed it was her as it was just a text. When I went to pay Nationwide told me it was not her but a scam. I felt quite sick by answering to a vile person. I did not lose any money due to Nationwide who told me it was a scam. (Female N51 V) I had a phone call telling me there were dangerous viruses on my computer which I fell for as not very confident about a wifi. They asked me to switch it on and they took it over and then demanded money to correct it 350 pounds to be paid by PayPal. They then proceeded to open a PayPal account in my name and expected me to transfer money to someone in British Columbia. It was only at this point that I realized, I was being tricked, they had gained my confidence and sounded so professional. I told them, I was going to report them to the police and put the phone down on them. They tried ringing back a couple of times, then gave up. I did report and fraud police I also had an expert check my computer for any bugs! (Female 944 NV) On 4 December 2020 I received a phone call proposing to be from BT with a message that my landline will be disconnected in one hour that it was compromised and to press one to speak to a person, which I did, unfortunately, but what was before the BT landline scam was known. I told the person that I was not with BT, whereupon he told me convincingly that BT had the overall licence but all networks. I became very anxious as my landline is my lifeline outside world, he then asked me to turn on my laptop again how did he know I even have a laptop was what has to be to do with a landline. I couldn’t think straight anymore, and I kept asking if he was a scammer, and each time the reply was convincing,,, After turning on his laptop and installing Team Viewer they spent two hours moving files around his computer giving the impression of professional activity. The victim was crying and terrified, and in this state, asked to transfer a large sum of money to a ‘police’ account which would then be transferred back, but they refused despite further pressure. This call left an impact, nonetheless . . . I was terribly upset but went to the bank immediately reported it . . . (had) flag put onto my accounts new cards passwords and I had my computer professionally cleaned. (Female 374 NV)

The toll of these attempts on some of the participants was significant as the opening quote to this article revealed and as this respondent said: (Telephone frauds) happen on a daily basis, calls numbers I’ve personally blocked after their last call was answered. So annoying as I am temporarily in a wheelchair with a broken foot and live on my own, but these scams calls are driving me CRAZY! (Female 481 NV)

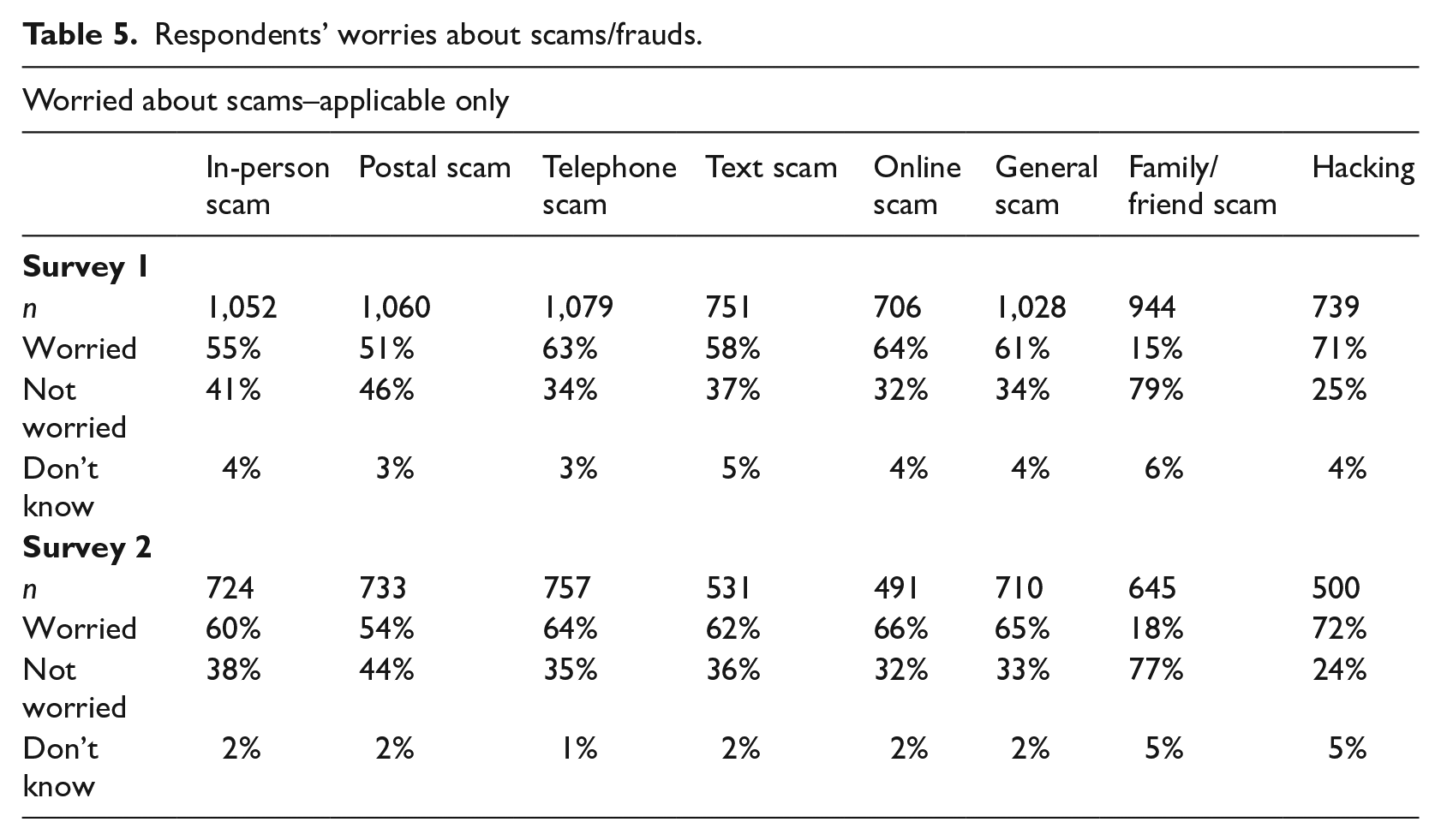

In addition to the qualitative comments above, quantitative data from the surveys highlighted some with significant worries over fraud. Respondents rated how worried they were about a variety of fraud types of fraud using the scale: 1 very worried, 2 fairly worried, 3 not very worried, and 4 not at all worried (Table 5). The respondents were least worried about being defrauded by a friend or family member (15% in the first survey and 18% in the second survey). The highest levels of concern were associated with hacking, online frauds/scams, and telephone frauds/scams. At 61–65%, the portion worried about frauds/scams in general is very close to the results from the very large CSEW, which found that 62% of adults aged 75–84 are worried about fraud and 64% are worried about the security of their personal information (ONS, 2021b).

Respondents’ worries about scams/frauds.

Older adults’ feeling of safety

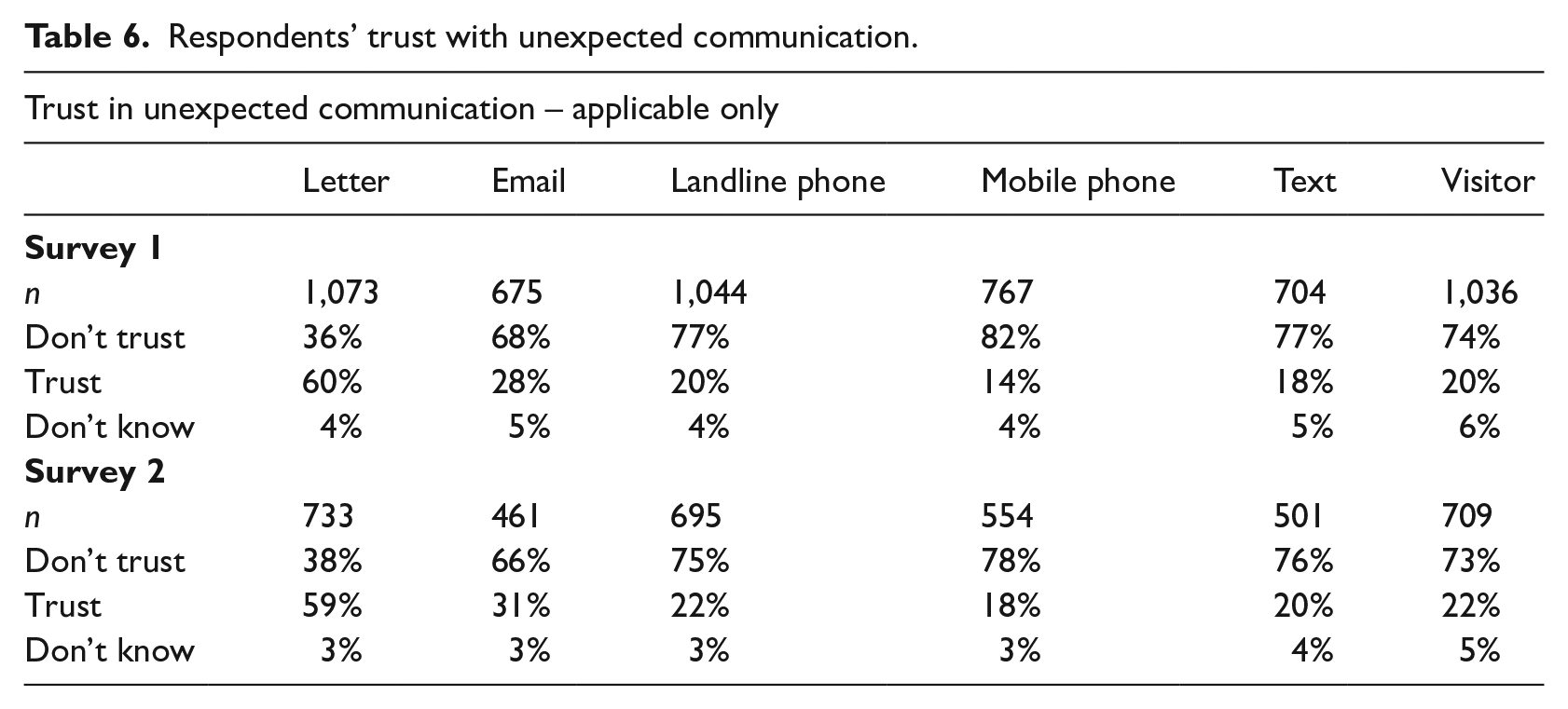

The survey sought data on how safe the respondents felt doing a variety of activities. Relating to telephones, it is also important to note a significant minority felt unsafe using the telephone (Table 6). In Survey 1, 24% and in Survey 2, 25% indicated they felt unsafe answering the telephone. These feelings of not feeling safe were also complemented by respondents’ trust with different forms of unexpected communication. Around three-quarters of respondents in both surveys did not trust unexpected communications on landlines and mobile phones. They were the most untrusted forms of communication.

Respondents’ trust with unexpected communication.

The qualitative comments from the survey and interviews also illustrated the concerns of older adults. Below some quotes from the survey and interviews are presented. Virtually all these quotes are from participants who had not experienced being a fraud/scam victim within the prior 6 months. The experience of attempted frauds/scams and general perceptions of the problem would seem to lead to substantial concerns among a significant minority of the respondents.

I’m always nervous about cold or strange phone calls – I normally give as good as I get – the same with strange emails. I just delete. I think I can handle post. If in doubt I speak to one of my daughters. (Male 448 NV) It still leaves me very wary, especially phone calls not listed in my phone and people at the door. It’s quite frightening to see how clever the scammers are. I do not have any telephone banking etc. (Female C44 NV) I hate the telephone scam calls. Even though I hang up quickly I feel frightened and disturbed for quite a while. I have also got phobic about ordering anything using my phone or computer. If I want to buy something I have to do it through my very patient daughter or I am anxious. (Female 109 NV) When refusing to divulge my details on the phone to someone wanting to ‘confirm’ my bank details, they become antagonistic and aggressive. This leaves me shaking and doubting myself – I just put the phone down. It is very upsetting being a victim of such bullying. I don’t want to think of myself as a victim just because I am elderly. (Female 159 NV) I often feel very insecure when I receive phone or mobile messages, I try to ignore them but they make me feel not safe in my own home. (Female 837 NV) I find ‘silent calls’ a bit unnerving but will not let them control my life: I block numbers. (Female 615 NV)

Discussion

This paper has provided the first in-depth exploration of the experiences of largely telephone-based fraud against older adults in the United Kingdom. It is important to note the participants for this project are not representative of older adults in the United Kingdom. It is based upon older adults who are supported by a charity with an aim to help the lonely. Some caution must therefore be considered in assessing the findings. However, with over 3 million older adults living alone in England and Wales (ONS, 2022), and the reality that a charity like the one in this research does not have the capability to help all lonely older adults, the authors are confident that the findings are representative of a much larger group of older adults than the charity client list. Further, as one co-ordinator noted to the researchers, their clients are the lucky ones as they are receiving support; there are many lonely older adults who are not. Nevertheless, it is clear that more research on a more representative sample of older adults is required.

The research has shown that telephone-based frauds cause significant impact and fear among some older adults, particularly older single women. Such groups being fearful of crime in general is not new, there is extensive research illustrating that. However, what is new in this research is how the advent of mass telephone-based fraud has turned some of the most vulnerable in society to fear the only significant means many have of regularly communicating with friends, family, and official agencies. Some of these older adults rarely go out, do not use computers, and are lonely. Their only link to a social life is compromised. Not only this, frauds have often been labelled as a lesser ‘victimless’ crimes in the past, because many get their money back (Button et al., 2014; Cross and Lee, 2022). Several studies clearly show many impacts of fraud victimisation and this study shows that these impacts also extend to non-victims, with clear negative impacts on their lives (Button et al., 2014, 2021; Cross, 2016, 2018; DeLiema et al., 2021; DeLiema and Witt, 2022). It cannot be naturally assumed that fraud as a crime creates fear, so research is needed to prove this and this paper like the research of Cross and Lee (2022) shows fear of fraud is an issue among this age group for victims and non-victims.

The impact of attempted fraud calls on the older adults in this survey, given the vast majority were women and living alone, is not surprising when the small but important literature on obscene calls is revisited. For example, research has shown that obscene calls for women can be seen on a par with burglary in generating fear, upset, and worry (Clarke, 1990). Some writers have compared obscene phone calls to assault (Warner, 1988), terror (Villa-Nicholas, 2018), and even rape (Hott, 1983). Research on such calls has noted a wide range of impacts, including violation, paranoia, revulsion, stress, shock, anger, self-blame, and of course fear (Sheffield, 1989; Smith and Morra, 1994). Research has also shown that such calls lead to elevated fear of burglary and sexual crime (Tseloni and Pease, 1998). Warr (1984) argued the reason for this greater fear of most physical crimes for women is underpinned by fear of rape, that is, scenarios such as burglary, robbery, and so on could potentially lead to a sexual attack. An obscene phone call clearly has a sexual connotation, an interaction with an offender, who also clearly, at the very least, knows their phone number and possibly their address. There is a clear progression to understanding how these calls can contribute to fears of crimes of intrusion, such as burglary, voyeurism, and sexual attacks.

Turning back to the attempted frauds by telephone, they may not be sexual in orientation but they do involve an interaction with an offender who may or may not know where the victim lives. The offender may suggest they do or the victims simply perceive they must know. Once the victim can imagine a scenario where the offender knows where they live, this can lead to fears of not just other fraud attempts occurring, but other crimes too. The reasons for greater fear among women were not something this project set out to consider, so the Warr thesis, however attractive, needs to be treated with caution. More research needs to be conducted not just to confirm if women are more fearful, but why, on a more representative sample.

The research also highlights how older technologies like landline telephones are still being used on an industrial scale to conduct frauds. These telephone calls have become for some older adults something they experience on a daily or weekly basis. Even though many older adults understand these are frauds and quickly hang up, for some, these attempts have significant impacts. Researchers have begun to grasp the significant impacts of frauds where there is a financial or information loss, but the impact of attempted frauds (by whatever means) on victims has not been seriously investigated (Button et al., 2014, 2021; Cross, 2016, 2018; DeLiema et al., 2021; DeLiema and Witt, 2022). These findings clearly show that more research needs to be conducted to explore the impact of attempted frauds on individuals’ fear of crime and quality of life among all age groups.

Another interesting issue that arises relates to the future. This study and ONS data illustrated earlier show only a small minority of this generation of older adults are digital natives. Dealing with telephone-based frauds is relatively simple to cope with for the most vulnerable, as call blockers and ultimately removal of telephones can take away the opportunities for victimisation. However, as younger generations get older and become the new older adults with their much more diverse use of communication technologies, with the associated risks of ageing and fraud combined, such as loneliness and mild cognitive decline, the risks of fraud, attempted frauds and fears look to be a potential timebomb, unless planning for this begins now. The lonely 75-year-old, with mobility problems with their routine activities of searching social media for friendship, buying their consumer goods from websites, and banking online is likely to face many more risks of fraud and greater chances of victimisation in the future (Holtfreter et al., 2008).

Conversely, there might be a reason to be less pessimistic. The future digitally skilled and active older adults might be less lonely, they might have access to better technologies to prevent victimisation and they might be better equipped to deal with the world of mass volume fraud after a lifetime of experiencing attempts and actual frauds. Predicting the future is always difficult, but any attempt needs a larger base of research on the issues raised in this article.

What is overwhelmingly clear is much more research needs to be undertaken on fear, fraud attempts, and non-cyber means of conducting fraud among older adults and other groups. Cyber has rightly grabbed the attention of researchers, funders, and policy-makers, but we must not forget that in the huge volume of fraud that occurs significant harms are still being perpetrated through more traditional means of communication. A priority should be a survey of older adults and given the experience of this research needs to be conducted face-to-face or by postal means, rather than by telephone, which as this paper has shown, is such a source of anxiety. Indeed, the CSEW, which is now conducted via telephone should consider the implications of this research for how it secures data from this demographic.

The implications of this research also highlight a relatively simple solution to tackle this problem. There are numerous call blockers that one can purchase that vary in their effectiveness. The government and counter-fraud community should identify standards to distinguish the most effective and promote those that meet this standard. Furthermore, funding the fitting and training of older adults on how to use them (not just giving them) should be a priority and a cost that would be sure to reap not only benefits in less fraud but also secure a safer home environment for those using them, as was found by Rosenorn-Lanng and Corbin-Clarke (2020).

Conclusion

This paper has explored the experience of older adults and largely telephone-based fraud. Drawing upon survey and interview data from a large number of clients of a UK charity which works mainly with over 75-year-olds who are lonely, it has illustrated some significant findings, which to date have not been exposed by researchers. These include the significant number of attempted frauds this group experiences largely by telephone, which for a small minority occur on a daily and weekly basis. The study has also illustrated significant fears and concerns among a significant minority in this group which arise not just from victimisation, but attempted frauds. This sample is not representative, but in England and Wales there are over three million older adults living alone (ONS, 2022), which if they are experiencing the same problems from this sample on a similar scale could illustrate an epidemic of worry. It is therefore important more research is conducted to determine the full extent of these problems and policy-makers implement relatively simple solutions to address it.

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors are grateful to the charity Re-engage for the funding for this research.