Abstract

Objective

To cocreate and synthesize financial empowerment ideas for people living with acquired brain injury from multiple perspectives.

Design

We completed a qualitative descriptive study using focus-group methods. Content analysis was guided by deductive categorization across overlapping idea areas of educational products, human-interaction services, and advocacy approaches, followed by inductive idea subcategorization.

Setting

We held seven focus groups, five online and two in-person. Participants were recruited via community organization advertisements and convenience sampling. Four researchers analyzed transcripts using a triangulation approach.

Participants

Twenty-five adults (ages 18+) participated in seven different focus groups: 15 individuals living with acquired brain injury (five groups); 2 close others (one group); and 8 project advisory members (one group). Demographics varied across age, education, and time since injury; most were women.

Results

We generated 20 idea subcategories for financial empowerment after brain injury. Participants discussed ideas related to advocacy and service ideas more than products, but noted the salience of varied option availability to meet different needs across individuals. Participants living with brain injury identified seven unique ideas compared to the close other group and project advisory group.

Conclusions

Financial empowerment to address economic factors of financial capability and financial well-being after brain injury is important to brain injury rehabilitation, health, and well-being. Including lived experience voices provided unique ideas for addressing financial empowerment. Providing a spectrum of options and addressing contextualization factors could enhance the financial well-being of adults living with brain injury, which can contribute to brain injury recovery and improve community participation.

Keywords

Introduction

People living with the acute and chronic effects of acquired brain injury, as a diagnostic subgroup of people living with disabilities, are a financially disempowered, excluded, and vulnerable group.1–4 Changes after brain injury can lead to impaired financial activity capability and overall reduced financial well-being outcomes.1,2,4–6 Unsurprisingly, important clinical rehabilitation outcomes, such as goal-attainment, recovery, stability in social relationships, community and social participation, health, and general well-being, are all threatened by reductions in financial well-being.5,7 Therefore, addressing financial empowerment can be important to brain injury rehabilitation and recovery, but needs more evidence guiding what can be done.

Financial well-being is threatened after injury for many individuals and their families or dependents. In the fields of finance and economics, financial well-being is defined as an individual's, family's, or community's subjective or objective financial or economic outcomes, including being able to meet current and anticipated financial demands.1,8 Multiple studies have found that financial well-being outcomes are challenges reported by people living with brain injury, with financial or economic factors being one of the most prevalent unmet needs after brain injury in multiple studies.2,5,6,9 Specifically, qualitative and quantitative data demonstrate that after brain injury many people and their families experience a decline in their financial resources and threats to their financial safety.2,4,10 Qualitative studies have noted increasing financial costs and demands to manage health and disability factors.2,6,10

A salient part of financial well-being is financial capability, which can decline or become impaired after brain injury. Financial capability is defined as a person's financial-related knowledge (literacy), skills, abilities, attitudes, and applied behaviors. It encompasses money and finance management, accessing sources of funds or resources, planning ahead financially, making economic decisions, or seeking help or information when needed.8,11 Multiple qualitative and quantitative studies and case reports have highlighted financial capability declines and increased financial errors after brain injury, in both acute and chronic stages after injury.1,2,10,12–15

To adequately address brain injury rehabilitation, long-term health, and general well-being of adults living with brain injury, it is imperative to understand how to address financial capability and financial well-being and develop financial empowerment programs that meet the specific needs and contexts of people living with brain injury.7,13 Financial empowerment is a holistic framework of principles and approaches aimed to improve the financial well-being of individuals and families. It includes comprehensively addressing financial capability and financial well-being challenges across micro, meso, and macro levels. 16 Despite finance and economic life being identified in the World Health Organization's International Classification of Functioning, Disability, and Health as a major life activity and participation area, 17 there is very limited research about how to address the financial empowerment of adults living with brain injury, and no study from a lived experience perspective.18,19

Our study aimed to develop a broad mapping of innovative financial empowerment ideas that are meaningful and responsive to the needs of individuals living with brain injury, using a codesign approach and multiple perspectives. These ideas could then be used for recommendations of new intervention programs and research to address the financial empowerment of people living with brain injury.

Methods

Study design

We completed a qualitative descriptive focus-group study, 20 guided by content analysis. 21 This analysis approach was within a postpositivistic research paradigm and emphasizes counts of qualitative data and analysis, such as the counts of categories and subcategories across focus groups, in addition to supporting qualitative quotes and narrative. This study design supports the development stage of a cocreation or codesign and community-engaged approach. 22 Specifically, we used the approach to intervention development and evaluation proposed by Wang and colleagues, 23 where development of new innovations or interventions, such as new programs, approaches, or technologies, should allow for end-user engagement, collaboration, and sharing of perspectives and experiences.

This study was approved by the Bannatyne Health Ethics Board (University of Manitoba; ethics number: HS25274 (H2021:417)). All participants completed an informed consent process prior to study participation, where the consent process was done in a way that acknowledged different consent needs of people living with brain injury and included meeting with a study staff person or researcher synchronously in-person or online to go over the consent forms and discuss any questions. The Standards for Reporting Qualitative Research guided the reporting of our study. 24

Recruitment and sampling

We recruited three distinct types of focus groups: (1) groups with participants who were living with brain injury (i.e., ABI groups); (2) caregivers of adults who live with brain injury (i.e., CG group); and (3) members of our project advisory group (i.e., PAG group).

Over a three-month period (i.e., March–May 2022), people living with brain injury or caregivers were recruited through local community organizations advertising the recruitment poster in physical spaces or social media or sharing study information with their contact email lists. The principal investigator (LE) also attended multiple online community organization meetings open to people living with brain injury to provide information about the study.

For participants’ living with brain injury and caregivers the inclusion criteria were: (1) aged 18 years or older; (2) self-reported diagnosis of acquired brain injury (e.g., traumatic brain injury, stroke, nontraumatic brain injury

All brain injury survivor and caregiver participants were given a $20 gift card honorarium. The study funds also paid for participant parking, public transportation, or taxi costs to decrease any financial burden to access in-person focus groups, and research staff assisted participants with booking any needed taxi services to further support participation and accessibility.

Members of the project advisory group were emailed by the principal investigator to signify their interest in participating in the focus group for this study. The project advisory group had been a project team for two years at the time of the study. At the time of this focus group study, this group had completed two related studies1,2 and had been involved in the development of the overall financial empowerment program project. The project advisory group included one person who lives with brain injury who also had volunteer experience with community brain injury organizations, one staff member from a community brain injury organization, and six researchers with expertise related to brain injury, financial empowerment, or both. Of the six researchers in the project advisory group, at least two also had lived or family-related brain injury experience. We included a focus group of our project advisory group as a comparison to focus groups of people who had lived experience (i.e., brain injury or caregiver groups). In this way, we could compare which ideas or idea categories were uniquely identified by those with lived experience versus our project advisory group.

Data collection

Data collection was completed in January 2022 for the project advisory group and April through June 2022 for people living with brain injury or caregiver focus groups. We collected background and demographic information individually from all participants prior to or after the day of their focus group.

We completed seven focus groups. Five discussion group meetings were with people living with acquired brain injury, one discussion group meeting with caregivers, and one discussion group meeting with the project advisory group. We held five groups online using a video meeting platform (i.e., ABI-1, ABI-4, ABI-5, CG-1, and PAG-1) and two groups in-person (i.e., ABI-2 and ABI-3). We collected background data and demographic data from each brain injury-survivor or caregiver group participant via a phone call with each person and a structured demographic information questionnaire. The project advisory group participants’ demographic information was collected through their online profiles and email contact. All focus groups were audio recorded and transcribed verbatim, without noting which specific person in each focus group was speaking (i.e., each focus group was a unit of data).

All focus groups were 1–1.5 h in length, and each brain injury survivor or caregiver group included 2–5 people per group to allow for adequate time for participants to contribute to the group discussion but limit participants’ fatigue and time-burdens. Our focus group discussion guide included one overall question: what are your ideas of what could be done to help adults living with brain injury with these challenges? This question was presented while discussing seven financial empowerment challenges faced by people living with brain injury previously identified in past studies1,2,13; the seven challenges are listed in Supplement A. Each group discussed ideas for one financial capability or well-being challenge at a time until either all seven challenge areas had been discussed or the 1.5 h focus group maximum time was reached. To ensure equitable participation, the trained group facilitator used strategies to monitor power imbalance or discussion dominance, promote turn-taking, and encourage participation from every participant. Two researchers or research staff participated in each focus group: one to facilitate group discussion and the other to manage technology or other participant-related needs during the group session.

Data analysis

The data analysis of the transcribed interview data was guided by deductive and inductive content analysis. 21 Our analysis process was further guided using the framework approach to analysis outlined by Gale and colleagues. 25 Data analysis was done at the level of each focus group versus at the words and analysis per individual in each group.

Our data analysis was first deductive in that we divided data into categories related to the taxonomy of financial programs and then inductive to generate more specific program ideas within each category (i.e., subcategories). Deductive categories were three overlapping program types: informational or educational products (i.e., consumed or used without direct human-interaction or relationship involved); human-interaction services; and advocacy products or efforts (i.e., actions to generate public or policy support for financial empowerment). 19 Aligned with content analysis, we recorded the number of focus groups that discussed each category and subcategory. At least two researchers independently coded each focus group transcript into deductive categories and inductive subcategories; all four authors then met to discuss disagreements and reach agreement on data coding and categorization.

Researcher reflexivity and strategies for rigor

To reflexively summarize our positionality that could influence this study, we (i.e., researchers/coauthors for this study) represented a diverse research team who have varied cultural, financial, racial, and professional education and experience backgrounds which include community health, rehabilitation, psychology, financial empowerment, and research education and experience. However, our research team had homogenous qualities that may be an influence on the research process and analysis: we all identified as heterosexual, cisgendered women in our early to middle adulthood; we all held or were working on advanced graduate research degrees; and we all resided in the same country (Canada) at the time of the study. Three of us were immigrants to Canada as adults from African or European countries and one of us (LE) is a third-generation white settler Canadian, which can influence our worldviews and perspectives of the study. As such to address reflexivity, we often discussed and made memos during individual analysis and agreement meetings about our own possible personal perspectives and biases that could be influencing data analysis.

We used multiple strategies to address study rigor and trustworthiness, including strategies for credibility, dependability, confirmability, and transferability. First, we generated an audit trail of study activities. Second, each involved researchers kept study journals during data collection and analysis to collect and document our observational fieldnotes, reflexive thoughts about the data collection and analysis, and memos during analysis. Second, we completed the analysis with triangulation of perspective (described above). After all data collection and analysis and in addition to multiple perspectives throughout the analysis process, we also met to discuss our findings with the project advisory group. To address transferability, we held multiple focus groups of people, purposively sampled to have experiences or knowledge related to brain injury, and aimed to have enough focus groups across the study to optimize data saturation. 26 However, we also acknowledged that as the focus on this study was possible ideas, it would be highly unlikely that total data saturation (i.e., no new information arising from new focus-groups) could be reached. Overall, breadth, possible utility, and comparison of collected idea subcategories using a triangulation of perspectives were used to examine saturation.

Results

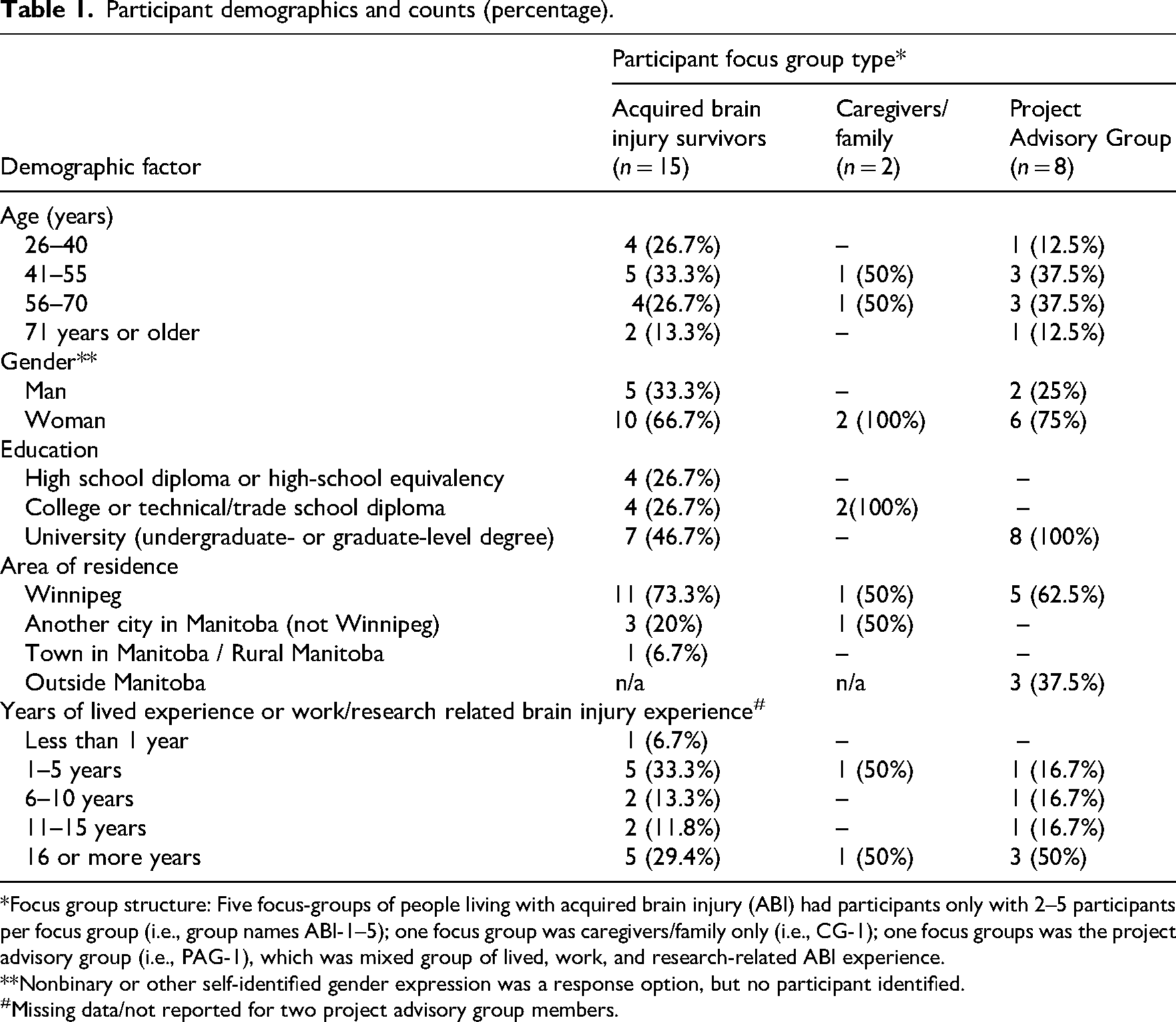

We included 25 people in this study across seven focus groups. Participants were a part of three focus group types determined by participant demographics: living with brain injury (i.e., in this paper coded/quoted as “ABI” groups), close other / caregivers (i.e., coded/quoted as “CG-1” group), or project advisory group members (i.e., coded/quoted as “PAG-1” group). Across the focus groups, there were 15 people living with brain injury who attended the five different focus groups (i.e., ABI-1, 2, 3, 4, or 5); two caregivers/ family members who attended an online focus group (i.e., CG-1); and eight project advisory group members who attended one online focus group (i.e., PAG-1). Group demographics are described in Table 1.

Participant demographics and counts (percentage).

*Focus group structure: Five focus-groups of people living with acquired brain injury (ABI) had participants only with 2–5 participants per focus group (i.e., group names ABI-1–5); one focus group was caregivers/family only (i.e., CG-1); one focus groups was the project advisory group (i.e., PAG-1), which was mixed group of lived, work, and research-related ABI experience.

**Nonbinary or other self-identified gender expression was a response option, but no participant identified.

Missing data/not reported for two project advisory group members.

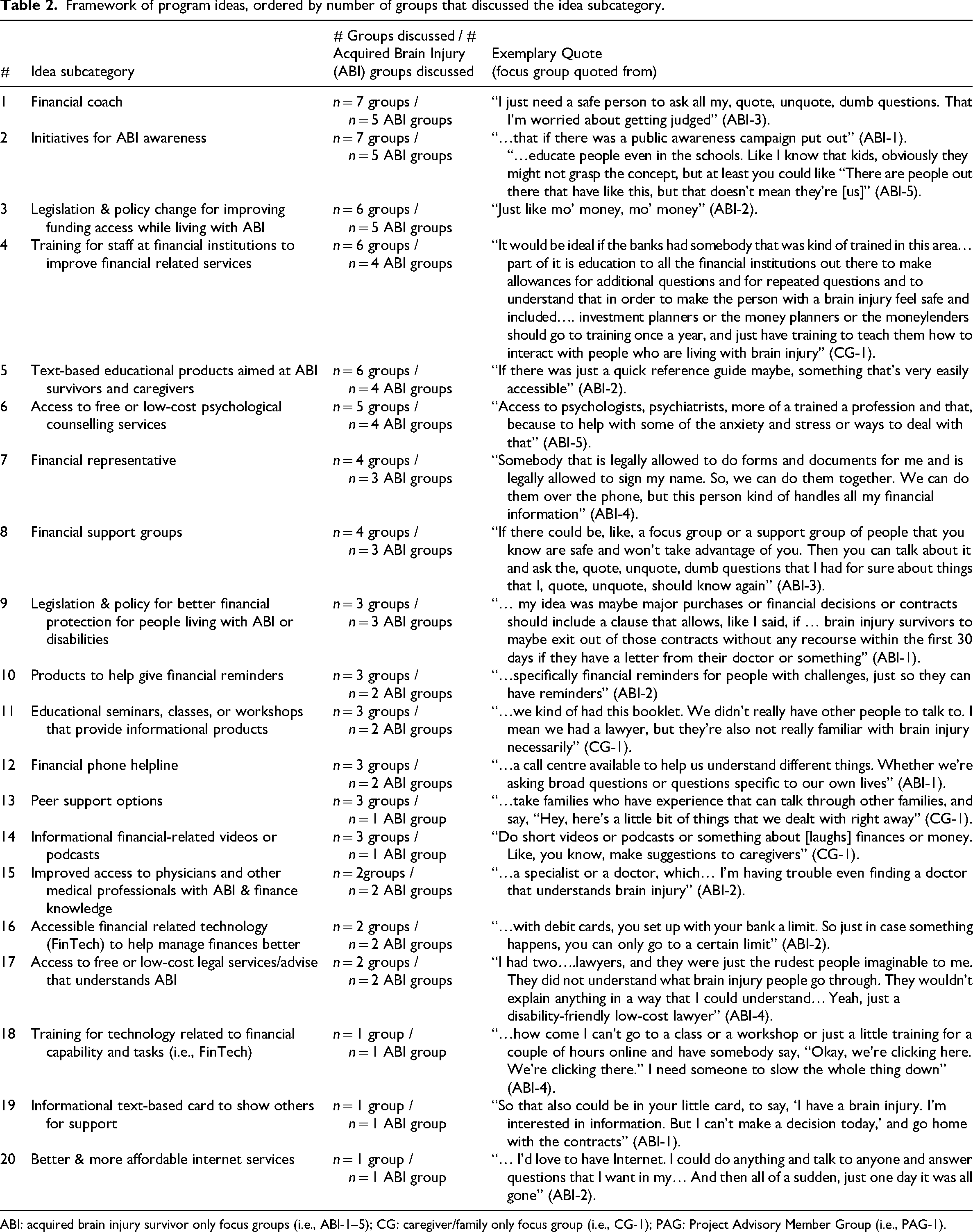

We developed 20 idea subcategories across the overlapping taxonomy of program type categories (i.e., products, services, advocacy, and combinations of these). These subcategories were based on discussions across all groups, and the comparative ideas discussed between the groups (Table 2 and Supplement B).

Framework of program ideas, ordered by number of groups that discussed the idea subcategory.

ABI: acquired brain injury survivor only focus groups (i.e., ABI-1–5); CG: caregiver/family only focus group (i.e., CG-1); PAG: Project Advisory Member Group (i.e., PAG-1).

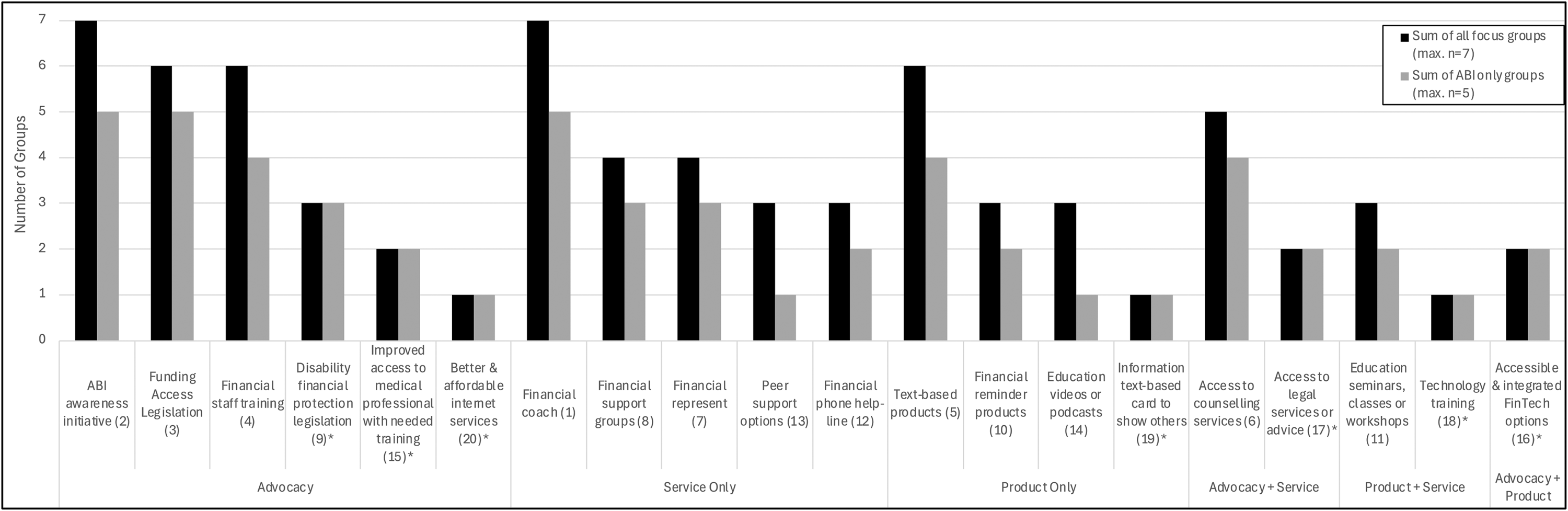

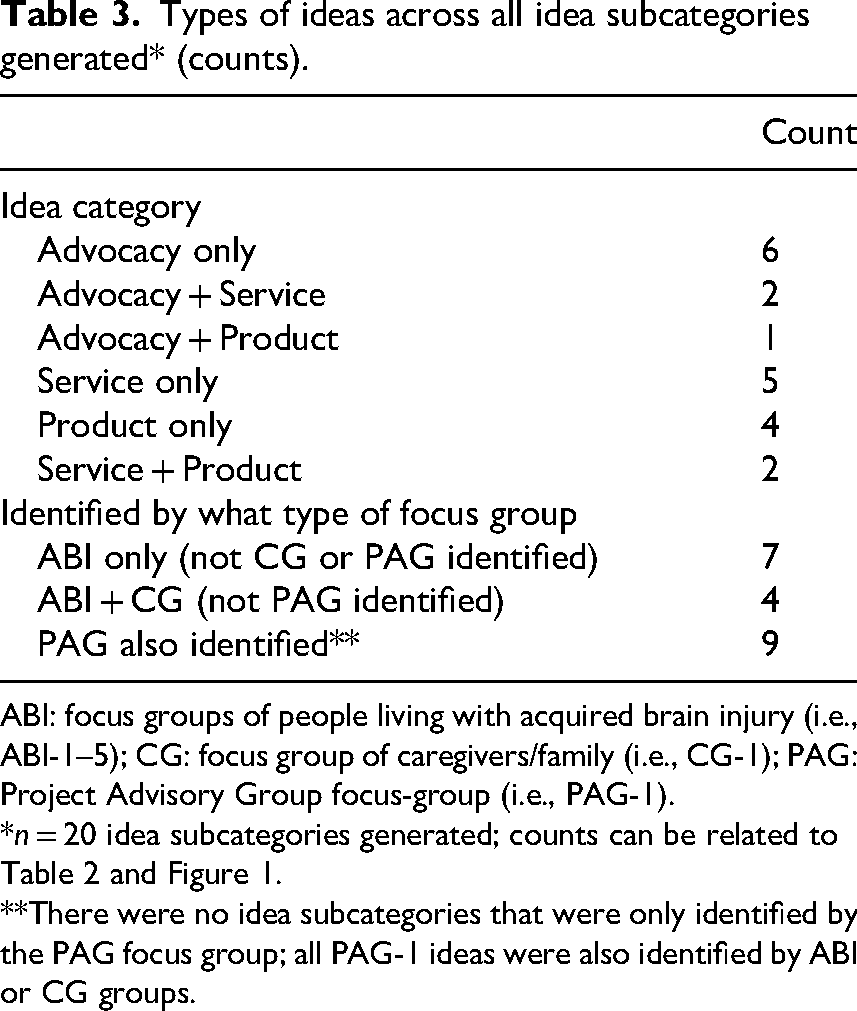

Across the 20 financial empowerment idea subcategories, nine included elements of advocacy, nine included elements of services aimed at people with lived experience, and seven included elements of a product aimed at people with lived experience (Table 3 and Figure 1). The five brain injury focus groups identified seven unique idea subcategories that were not identified by the caregiver or project advisory group focus groups.

Number of focus groups that discussed ideas, categorized by type of idea (advocacy, products, services).

Types of ideas across all idea subcategories generated* (counts).

ABI: focus groups of people living with acquired brain injury (i.e., ABI-1–5); CG: focus group of caregivers/family (i.e., CG-1); PAG: Project Advisory Group focus-group (i.e., PAG-1).

**There were no idea subcategories that were only identified by the PAG focus group; all PAG-1 ideas were also identified by ABI or CG groups.

Further to our inductive data analysis and to address our aim to identify ideas that are sensitive and meaningful to those living with brain injury, we also generated five data categories that were not specific to an idea subcategory but instead were factors that highlighted important contextualizing considerations for any financial empowerment program that might be developed.

First, five groups (ABI-1, 2, 4, 5; PAG-1) discussed the need for offering varied and individualized program options as the financial empowerment, learning, and program engagement or accessibility needs for people living with brain injury are diverse: I think it's very difficult because I think that someone with a brain injury, they’re at different levels of the injury and there's different levels of comprehension, different levels of their ability to self-care and to take care of themselves….Well, the thing I know about brain injuries is every single one of them is different than the next, every single one of them. (ABI-2)

The discussions in focus groups highlighted that a one-size-fits-all approach would not be effective to a broad spectrum of people living with brain injury, and that having varied information that might be easier to access, that can be adapted as needed, and that can be targeted to the right people at the right time would be more helpful: “I need to know what I need to know when I need to do it at that time; timing is critical” (ABI-4).

Second, five groups of people with lived experience (ABI-1,3,4,5; CG-1) also discussed the importance of programs having intentional outreach to people living with brain injury as often people were experiencing brain injury symptoms or changes that made it hard to be aware or focus on financial-related issues, until possibly too late or after a financial crisis is already present. This outreach was discussed as being a phone call or specific email to push-out the financial-empowerment-related information or program opportunities to people living with brain injury: I think both because I didn’t realize that it was valid to be so nervous about finances and to be irresponsible. Like, I made bad decisions at the beginning, and I didn’t know that that was a symptom of brain injury…Just I would say that [for] the people that have brain injury, that they contact us and not us contacting [them]. (ABI-3)

Another group further discussed intentional outreach to connect people to information needed: Yeah, I think one of the key things is just being presented with the knowledge of what you can access, what needs to be accessed, or what is possible for you to access, is really the key thing. Because you think of it as this, you have a brain injury, it's like one day you have a total disconnect. (ABI-5)

Third, five groups (ABI-1, 2, 4, 5; PAG-1) highlighted programs, particularly financial services, needed to be developed or provided by people knowledgeable about finance but have a particular ability to understand how best to work with adults living with brain injury or related disabilities. The people providing services need to have empathy about brain injury and disability as well as accurate financial-related information: “If you’re dealing with someone that has a brain injury or a disability, being able to explain in it a different way” (ABI-4). As another group further delineated: I think you need to be able to work with professionals that understand brain injuries. Brain injuries can be so diverse. So, you need to make sure that if you’re a client accessing the service and you’re going to look for financial information, you want to be comfortable with who you’re seeing and know that, okay, they’re going to understand if my eyes start to close. They’re going to understand if I show up with sunglasses. They’re going to understand if I have to cancel at the last minute. They’re going to understand if I need to be virtual or over the phone because today, I can’t function. (ABI-1)

Further, groups highlighted how the right person providing programs would also need to be trusted, unbiased, and fiduciary: “But in regards to managing the finances and money, you really have to have someone that you can trust” (ABI-2).

Fourth, the need to consider financial related activities and potential financial challenges early after brain injury was discussed by two focus groups (ABI-5; PAG-1), as these issues can be significant life issues immediately after brain injury and can be present for a long-time after sustaining an brain injury: “…whether or not there are any programs out there to help you financially coming out of the situation…I was told, “Within two weeks, go find your own place to live that's safe for you.” This was coming from the hospital” (ABI-5).

Last, one group directly highlighted that financial-related programs aimed at people living with brain injury be funded by private or public sources or be made free or low-cost for the person living with brain injury: “…so then the service is free because not everyone has the ability to pay for private service” (ABI-1). This focus-group further discussed how it would be beneficial to have financial programs built into already established rehabilitation or community programs directed at people living with brain injury. Although low-cost was only discussed directly by this one group (i.e., ABI-1), other results presented have highlighted the need for free or low-cost options specific to counselling services (five groups; brain injury-1,2,3,5; CG-1) or free and low-cost legal services (two groups; ABI-2,4).

Discussion

Addressing financial empowerment is complex, as managing finances in current economic environments is complex. Our results identify 20 idea subcategories for financial empowerment for those living with acquired brain injury generated from the perspective of those with lived, work, or research-related expertise. Participants, particularly those with lived experience, also highlighted five contextualizing considerations for all program ideas. These results provide potential useful considerations to address financial empowerment for people living with brain injury. This is salient as financial capability and financial well-being challenges have been a consistent unmet need of people living with brain injury.2,9,12,14,15

Our finding related to needing a comprehensive approach to financial empowerment is advocated by many other financial well-being and empowerment groups and literature.3,16,19,27 As discussed in our focus groups, a comprehensive approach needs to include advocacy for systemic and social equity changes, approaches that can often have more influence on addressing financial empowerment than only individual-focused products and services.3,16,19 Advocacy for disability funding or benefits, at levels adequate to support a livable standard of living, has been long-standing issues in many jurisdictions or countries. 28 Further, all focus groups in our study identified how advocacy to improve public awareness about brain injury and disability, especially invisible disability, could indirectly address financial empowerment. As social, institutional, or systemic factors can be facilitators or barriers to financial access and financial inclusion, advocating for meso and macro-level improvements could have widespread financial empowerment outcomes related to access and inclusion for many people living with disabilities.28–30

Interestingly, focus groups with lived experience identified needed advocacy to improve access to professionals who are better able to connect them with their needed financial resources. For example, participants living with brain injury in two groups specifically highlighted the need for access to health or rehabilitation professionals with good brain injury as well as finance-related training and knowledge. Health professionals, historically primarily physicians, have been the “gatekeepers” to insurance and governmental benefits within many care/support systems and governmental benefits systems around the world.31,32 However, there can be many issues to accessing health and rehabilitation professionals who are aptly prepared to address the financial needs. Some groups have developed or advocated for medical-financial partnerships or specialized medical-financial specialists to holistically support the needs of people accessing care, but more research is needed to examine if health care professionals are aptly prepared to address financial issues and outcomes of financial partnerships or specialists as part of rehabilitation teams. 33

Despite a spectrum of comprehensive ideas being identified by our focus groups, many of the identified financial product and service approaches have not been adequately studied in brain injury populations.

18

For example

Last, our comparative analysis across group types highlights the importance of including lived experience perspectives in the idea generation and design of new interventions. 22 Our lived experience groups (i.e., brain injury and caregiver groups) generated 11 unique idea categories and had more breadth and depth in discussions related to contextualizing factors for financial empowerment program options. This finding aligns with current calls for growth for codesign or codevelopment approaches in program and intervention development and research.22,23,36 While recent financial empowerment-related research and program development specific to financial safety and cyberscams has prominently involved the voice of lived experience, 10 it is imperative that continued financial empowerment program development and research continue to involve the voice of people with lived experience.

This study has limitations that should be considered. As with all qualitative studies that inherently use smaller samples, the transferability may be limited, as different samples or different researchers involved in analysis could lead to different overall subcategories of ideas. Particularly, we experienced difficulties in recruiting caregivers for this study, as our data collection was during the later years of the COVID-19 pandemic, when research has demonstrated some caregivers were busy, stressed, or exhausted managing caregiving duties. 37 Further, although we included a mix of adults living with brain injury across years since injury, ages, and education levels, our sample included more women and no people that identified as nonbinary, which may introduce a gendered bias. Further, this research was conducted within a specific context of one province in Canada, which represents specific environmental and geopolitical contexts. As we collected and analyzed data from a focus-group unit of data, and not individual responses, future research should examine financial empowerment for individuals with brain injury from an intersectional perspective, including critical analysis on income, race/ethnicity, gender, and disability. Last, our study did not examine the potential outcomes of any of the ideas generated in the focus groups. Thus, research is needed to examine the effectiveness and outcomes of the presented financial empowerment ideas when used with people living with brain injury.

People living with brain injury, as a diagnostic group related to disability, are a group of people who require unique ways to address their financial capability and financial well-being related to financial empowerment, but how to address financial empowerment has largely been ignored for this population.2,18,19,27 This study is part of the foundational work to examine the unique needs and ways to address financial empowerment after brain injury while working within a model of upholding, as much as possible, people living with brain injury's autonomy and control over their own finances, as a conduit to control over their own lives. If financial empowerment needs are not met, we risk becoming paternalistic by formally or informally removing the rights of people to manage their own finances or make their own financial decisions which then limits their autonomy. Thus, comprehensively addressing financial empowerment after brain injury should be a salient goal of long-term brain injury rehabilitation and advocacy efforts to promote community participation and long-term health and well-being.

Clinical messages

While discussing their experiences and ideas of how to address financial challenges after brain injury, focus group participants endorsed many financial capabilities or financial well-being challenges while living with brain injury; these are often dependent on an interaction between the person and environmental factors that are within a context of brain injury disability.

People with lived experience identified 20 different idea subcategories that could help address financial capability or financial well-being challenges (i.e., financial empowerment ideas).

Participants highlighted that a variety of brain injury-sensitive financial empowerment options are needed to meet the diverse needs across different individuals living with brain injury.

A salient advocacy idea discussed by multiple focus groups was to ensure health and rehabilitation professionals are adequately knowledgeable about client finance and finance related to disability experience.

Supplemental Material

sj-docx-1-cre-10.1177_02692155251382507 - Supplemental material for Promoting financial empowerment after brain injury: Findings from focus groups

Supplemental material, sj-docx-1-cre-10.1177_02692155251382507 for Promoting financial empowerment after brain injury: Findings from focus groups by Lisa Engel, Kafayat Adedotun, Roheema Ewesesan and Ibiyemi Arowolo in Clinical Rehabilitation

Supplemental Material

sj-docx-2-cre-10.1177_02692155251382507 - Supplemental material for Promoting financial empowerment after brain injury: Findings from focus groups

Supplemental material, sj-docx-2-cre-10.1177_02692155251382507 for Promoting financial empowerment after brain injury: Findings from focus groups by Lisa Engel, Kafayat Adedotun, Roheema Ewesesan and Ibiyemi Arowolo in Clinical Rehabilitation

Footnotes

Acknowledgements

The authors would like to acknowledge that this project was conducted on Treaty 1 territory and on original lands of the Anishinaabeg, Cree, Anisininew, Dakota, and Dene peoples, and on the homeland of the Red River Métis. The authors acknowledge the immense past and current harms to Indigenous people in Canada and work toward, both in and out of this project, to action for reconciliation and collaboration. The authors would also like to acknowledge the staff and board of directors of the Manitoba Brain Injury Association (MBIA) and other local community organizations who helped with dispersing recruitment materials for this study. The authors are thankful to the MBIA for assisting in arranging space for in-person focus groups.

Ethical considerations

This study was approved by the Bannatyne Health Research Ethics Board at the University of Manitoba (Winnipeg, MB, Canada; ethics number: HS25274 (H2021:417)).

Consent to participate

All participants in the focus groups completed written informed consent prior to participating in the study; in cases where the participant was not able to provide a written signature, an audio recording of their verbal consent to participate was created in lieu of written consent (a process approved by the HREB to remove possible e-signature or signature barriers to participation).

Author contributions

Lisa Engel was the primary developer of this study and the larger project it is a part and led the team in developing the study protocol, obtaining ethics approval, data collection, analysis, and manuscript writing/editing (including being the primary author of the manuscript as submitted). Kafayat Adedotun participated in data collection and analysis, writing of some sections of the manuscript initial draft, and editing the manuscript. Roheema Ewesesan participated to develop the study protocol, obtain ethics approval, data collection, analysis, and editing the manuscript. Ibiyemi Arowolo participated to develop the study protocol, obtaining ethics approval, project management, data collection, analysis, and editing the manuscript.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was funded in part by the Government of Canada's Social Development Partnerships Program (Disability component; project/contract number: 16684730). The opinions and interpretations in this publication are those of the author and do not necessarily reflect those of the Government of Canada. Dr. Engel's research program has also been funded in part by the Canadian Institutes of Health Research (CIHR) and funds internal to the University of Manitoba.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.