Abstract

The objective of the paper is to trace out the effects of decommissioning of the Sellafield nuclear complex on the economy of West Cumbria. I seek to show how decommissioning expenditures are stimulating the formation of an agglomeration of advanced nuclear processing and engineering firms in the region and how this process is reinforced by a diverse array of emerging private and public institutions. With the aid of patent data, I indicate some possible pathways of industrial development in the region. I then proceed to examine how policy makers might enhance the developmental impacts of decommissioning especially in regard to measures focused on inter-firm network activities, training, and institutional infrastructures.

A region in transition

The aim of this paper is to examine economic shifts currently occurring in West Cumbria as a consequence of decommissioning of the Sellafield nuclear complex. I seek to show how the expenditures flowing from this process are stimulating significant local economic development effects as evident above all in the formation of an early-stage agglomeration of advanced nuclear processing and engineering firms. I am further concerned to elucidate a number of pressing policy issues raised by this situation and to suggest how policy makers might intervene in effective and positive ways.

In various parts of the world today, ageing nuclear power stations erected in the post-war years are coming to the end of their serviceable life and many of them are now subject to costly decommissioning (Laraia, 2018; Pasqualetti, 1990). These developments raise urgent questions about the effects of decommissioning on local communities. The situation in West Cumbria is of particular interest and significance given that Sellafield functioned until recently as the largest nuclear facility in Europe. Nuclear power generation at Sellafield ended in 2003 when a decommissioning programme was set in motion thus directly and indirectly destroying many established jobs in the locality. At the same time, decommissioning at Sellafield involves massive expenditures – currently exceeding £2.0 billion per annum – over a projected lifetime of several decades and is now stimulating positive economic responses in West Cumbria. In particular, as decommissioning has moved ahead, new entrepreneurial energies have been unleashed, and local governments together with other relevant parties have sought to formulate the attendant policy challenges in a series of ambitious plans in combination with a campaign to brand the region as ‘Britain’s Energy Coast’ (BEC, 2008, 2012).

Sellafield in geographic and historical context

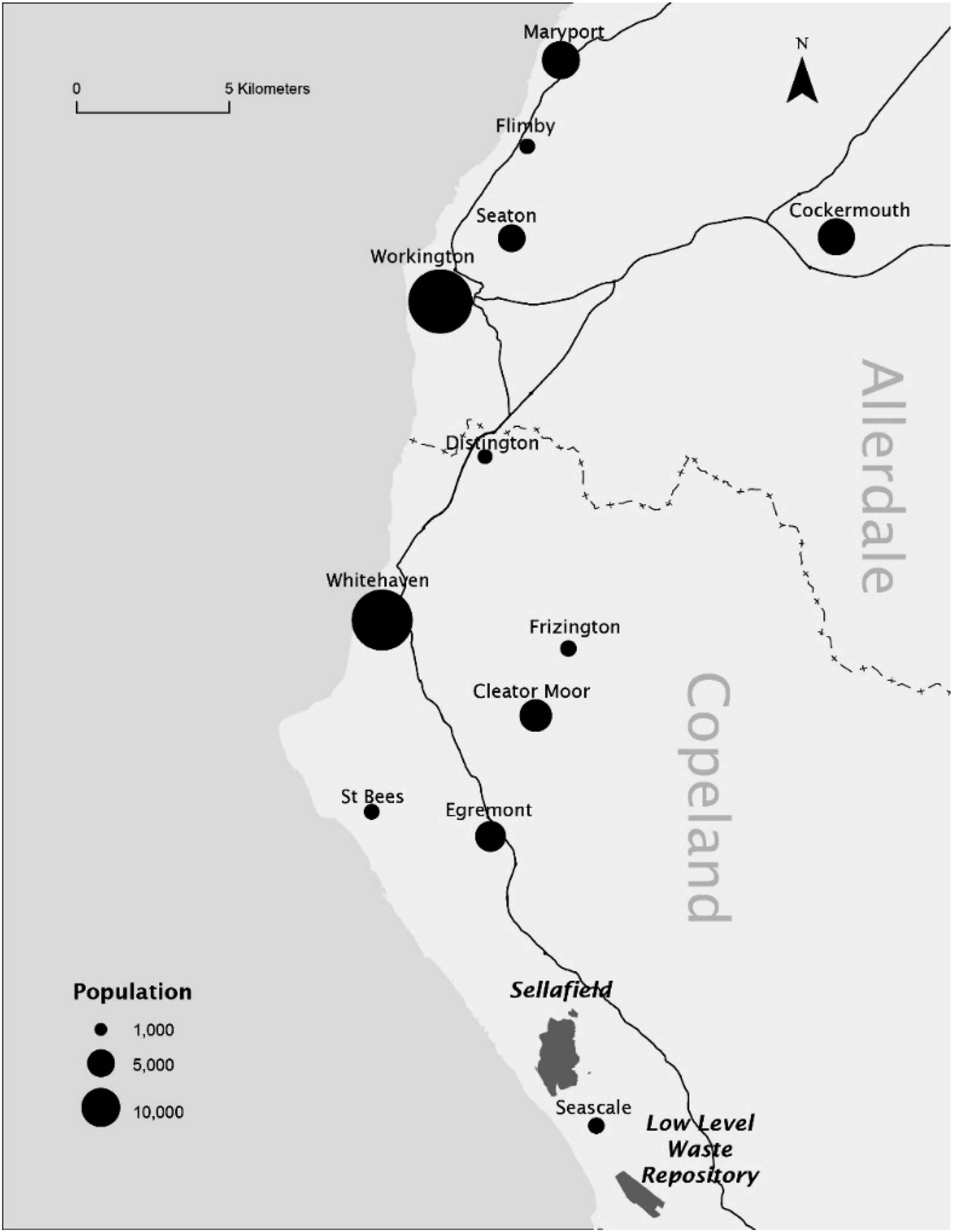

West Cumbria encompasses the most densely populated parts of the two former borough council districts of Allerdale and Copeland in the ceremonial county of Cumbria. These two districts were reorganised (along with Carlisle) on April 1st 2023 into the new Cumberland Council Area, but given their significance hitherto as reporting units for official statistics they are retained in this study as basic geographic points of reference. The region contains several small- and medium-sized towns (see Figure 1), the largest being Workington with 27,120 residents and the second largest Whitehaven with 24,900. It also has close relationships with several towns lying just beyond its immediate confines, above all with Carlisle in the north-east and Barrow-in-Furness in the south. At the same time, West Cumbria lies immediately to the west of the Lake District with its numerous recreational opportunities. The Sellafield complex itself is located in the south of the region between Egremont and Seascale. Urban centres and population in West Cumbria.

Recent developmental trends in West Cumbria are all the more arresting in view of earlier incarnations of the region as a peripheral coal and iron mining district that fell into prolonged depression in the period between the two world wars, followed by continuing deterioration in employment levels and social wellbeing through the post-war decades. It was precisely this prolonged crisis combined with the region’s peripheral location that motivated governmental efforts to develop the Sellafield site by setting up the Windscale Works in 1947 to process plutonium and to launch the Calder Hall nuclear power station in 1954. Several additional research and development facilities were built on the site, and in 1959 a Low-Level Waste Repository (LLWR) for the storage of discarded nuclear materials was set up a few miles to the south. Sellafield functioned in this basic configuration until the early years of the twenty-first century when – along with the transfer of ownership of the site and its custodian (Sellafield Ltd.) from British Nuclear Fuels (BNFL) to the Nuclear Decommissioning Authority (NDA) – decommissioning was initiated and a new regional trajectory of development came into view.

Conceptual preliminaries

In contrast to its economically marginal status over much of the twentieth century, West Cumbria appears now to be on the threshold of a comparatively new socio-economic order rooted in the decommissioning process. An initial if frankly hyperbolic intimation of this order is represented by the burgeoning high-technology regions now widespread on the economic landscape of the contemporary world (Castells and Hall, 1994; Scott, 1993). There is a mountain of literature on these and other types of industrial regions, but little has been written about the developmental impacts of nuclear decommissioning. Among the few and largely atheoretical attempts to deal with this problem are studies by Haller et al. (2017), IAEA (2011), and OECD (2022).

In what follows, I shall highlight a few major themes in the literature on local economic development, paying special attention to processes of agglomerated regional growth, and these themes will subsequently be interwoven with discussion of the actual effects of decommissioning at Sellafield on the West Cumbrian economy. The essential argument goes back to Marshall (1919) and his theory of industrial districts or agglomerations representing dense economic clusters overlain by an ‘atmosphere’ representing a shared informal culture of production and work. The argument has since progressed through several iterations into the body of concepts often referred to nowadays under the rubric of ‘smart specialization’ (Foray, 2018; Balland. et al., 2019). These concepts acknowledge that a process of regional development may originate in any number of different circumstances, such as a historical tradition, a local resource base, a decommissioning project, or even a purely random incident. What is important for any understanding of the process is not so much the manner in which an initial developmental seed is planted but the local ramification of subsequent generations of interrelated, synergy-generating events (Braunerhjelm and Feldman, 2006). Central to the process is the unfolding of a network of production units forming a social division of labour, that is, a system of specialised but complementary firms. Small- and medium-sized firms (SMEs) are critical to the process, though large enterprises may play a significant role too. The whole is constituted as a constellation of inter-firm relationships and an associated labour market forming a distinctive spatial cluster (Scott, 1995; Storper, 1997).

The incentives leading to this sort of spatial concentration derive in the first instance from the mutual cost-reducing proximity of interacting producers together with access to an adjacent pool of workers endowed with industry-specific skills, know-how, and forms of habituation, that is, a localised system of economies of scale and scope (or, more specifically, agglomeration economies). Three further factors augment these benefits (cf. Duranton and Puga, 2004). First, the spatial concentration of producers makes it possible to provide shared fixed capital assets (such as infrastructural artefacts) at reduced individual cost. Second, the mutual proximity of employment locations and employees’ residences facilitates appropriate matching between job requirements and workers’ aptitudes. Third, the intensified transactional relationships between clustered firms tend to augment the circulation of critical information, thus enhancing learning and innovation. The cluster as a whole then typically evolves over time within a pattern of path-dependent internal adjustment where each stage of system development invariably materialises as a structured outgrowth (in terms of technologies, skills, products, and so on) of the previous stage (Martin and Sunley, 2006).

These advantageous outcomes are equivalent to what Ostrom (1990) calls ‘common-pool resources’, in other words, collectively produced assets that are freely available to suitably positioned parties. As such, they represent a basic foundation of regional competitive advantage, and because they are typically susceptible to market failure, they call for overarching institutional arrangements to enhance system performance (Boschma and Frenken, 2009; Farrel and Knight, 2003). As we shall see, a growing patchwork of institutions that partially function in this way is now taking definite shape in West Cumbria. These include not only local governmental authorities but also a corpus of associations, professional organisations, and advisory councils, each providing specialised kinds of collective support in matters of education, technical training, market intelligence, social integration, and other communal services. The end result is a re-energised socio-economic system comprising a regional mosaic of interdependent units of production, local labour market activities, and a framework of ambient institutions. In the best of all possible worlds, the path-dependent dynamic of the whole regional complex is then consolidated through intensifying competitive advantage, innovation, and entrepreneurial effort, including spin-off from existing firms (Klepper, 1996; Scott, 2006).

Drivers of West Cumbrian economic transformation in the 21st century

Sellafield Ltd. currently employs just under 11,000 individuals. The National Nuclear Laboratory (NNL) employs an additional 300 on the Sellafield site as well as a further 150 in an affiliated facility in Workington. A complementary labour force is also engaged directly at Sellafield in decommissioning tasks under the control of private contractors, many of whom are subsidiaries of international corporations. The nearby LLWR employs a further 250 individuals. Thus, in spite of the cessation of nuclear power generation at Sellafield, considerable if not increased quantities of government-funded work are still being carried out in and around the site, including not only decommissioning but also the storage and reprocessing of spent nuclear fuel and basic research on nuclear science and engineering. Decommissioning is projected to endure for at least several decades, a point that has been emphasised in any number of official declarations. 1

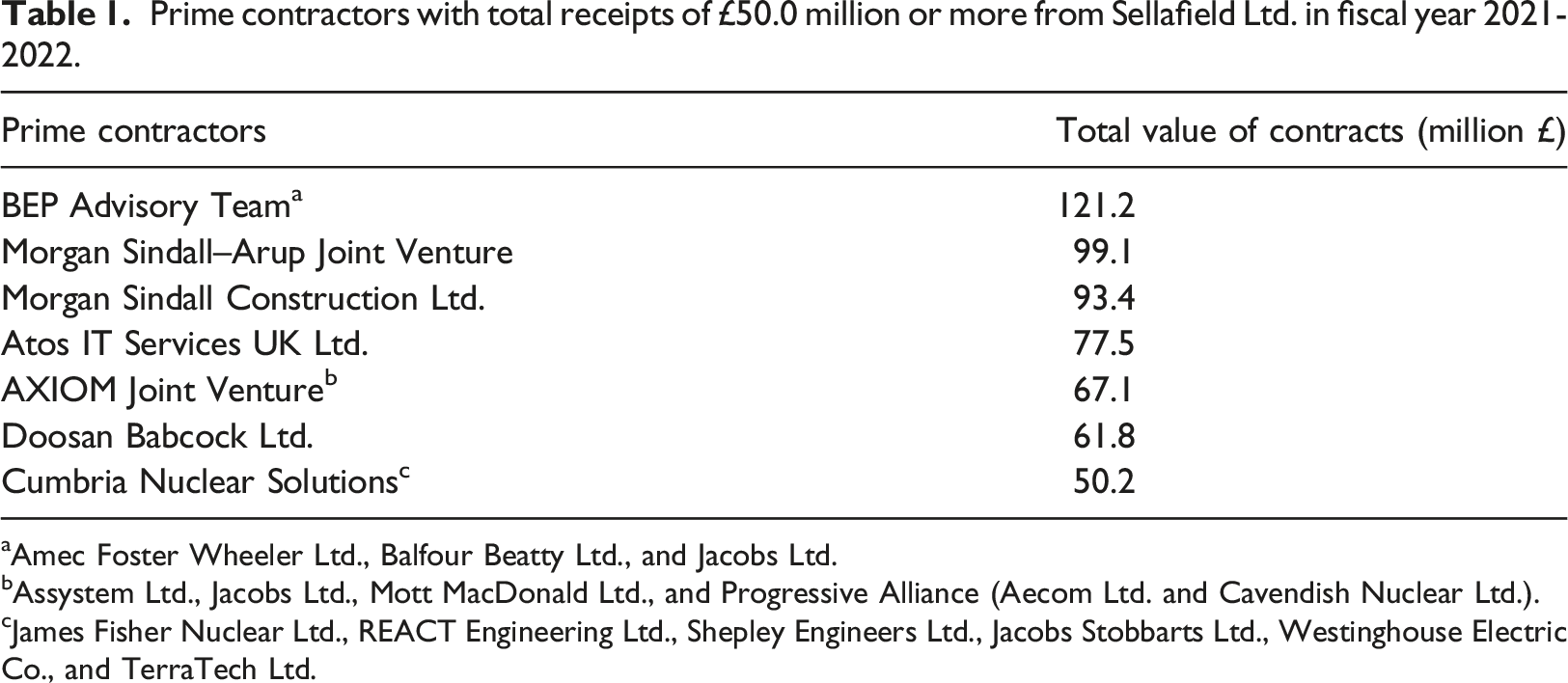

At the outset, the economy of West Cumbria is well served by the multiplier effects derived from the expenditures of the workers employed by Sellafield Ltd. Oxford Economics (2017, 2022) estimates that the company’s total wages bill in FY 2016-2017 was £472.4 million (in current values), 25.8% of which was apportioned to Allerdale and 55.9% to Copeland. In 2021 the wages bill was estimated at £598 million. Yet more important are the impacts of the money dispensed on decommissioning via Sellafield Ltd.’s supply chain. This money is a critical factor in the incipient formation of a new economy in West Cumbria. Detailed information on the supply chain is held in close confidentiality by Sellafield Ltd., but for present purposes a large data set covering all prime contract awards between FY 2017-2018 and FY 2021-2022 was acquired through the Freedom of Information Act. These data provide comprehensive information on the identity of all prime contractors and the amount that they received in any given year, and thus offer invaluable clues as to the business impacts of decommissioning.

Prime contractors with total receipts of £50.0 million or more from Sellafield Ltd. in fiscal year 2021-2022.

aAmec Foster Wheeler Ltd., Balfour Beatty Ltd., and Jacobs Ltd.

bAssystem Ltd., Jacobs Ltd., Mott MacDonald Ltd., and Progressive Alliance (Aecom Ltd. and Cavendish Nuclear Ltd.).

cJames Fisher Nuclear Ltd., REACT Engineering Ltd., Shepley Engineers Ltd., Jacobs Stobbarts Ltd., Westinghouse Electric Co., and TerraTech Ltd.

At least some of the work carried out by these and other prime contractors is performed directly on the Sellafield site, though most of it appears to be done off-site, partly in West Cumbria itself but for the most part elsewhere. Off-site locations within West Cumbria, as designated in the supply-chain data, are represented in some cases by physical production and research facilities, and in others by little more than an office or some equivalent arrangement. If we rely simply on the addresses attached to supply-chain awards, it would appear that as much as 28.0% of Sellafield Ltd.’s total spending in FY 2021-2022 was absorbed in West Cumbria. However, my own enquiries in interviews with representatives of local firms suggest that some unknown and probably major share of supply-chain awards directed to West Cumbrian addresses is actually transferred to more distant locations (cf. Cabras and Mulvey, 2012). Oxford Economics (2022) juggles with the same data but in the end provides only an ambiguous assessment of what fraction of supply-chain spending remains in West Cumbria. Whatever its actual magnitude, this fraction nevertheless has tangible effects on the local economy, and much of the discussion that follows is an attempt to identify how these effects are currently unfolding on the economic landscape.

Economic and social shifts in West Cumbria

An emerging cluster

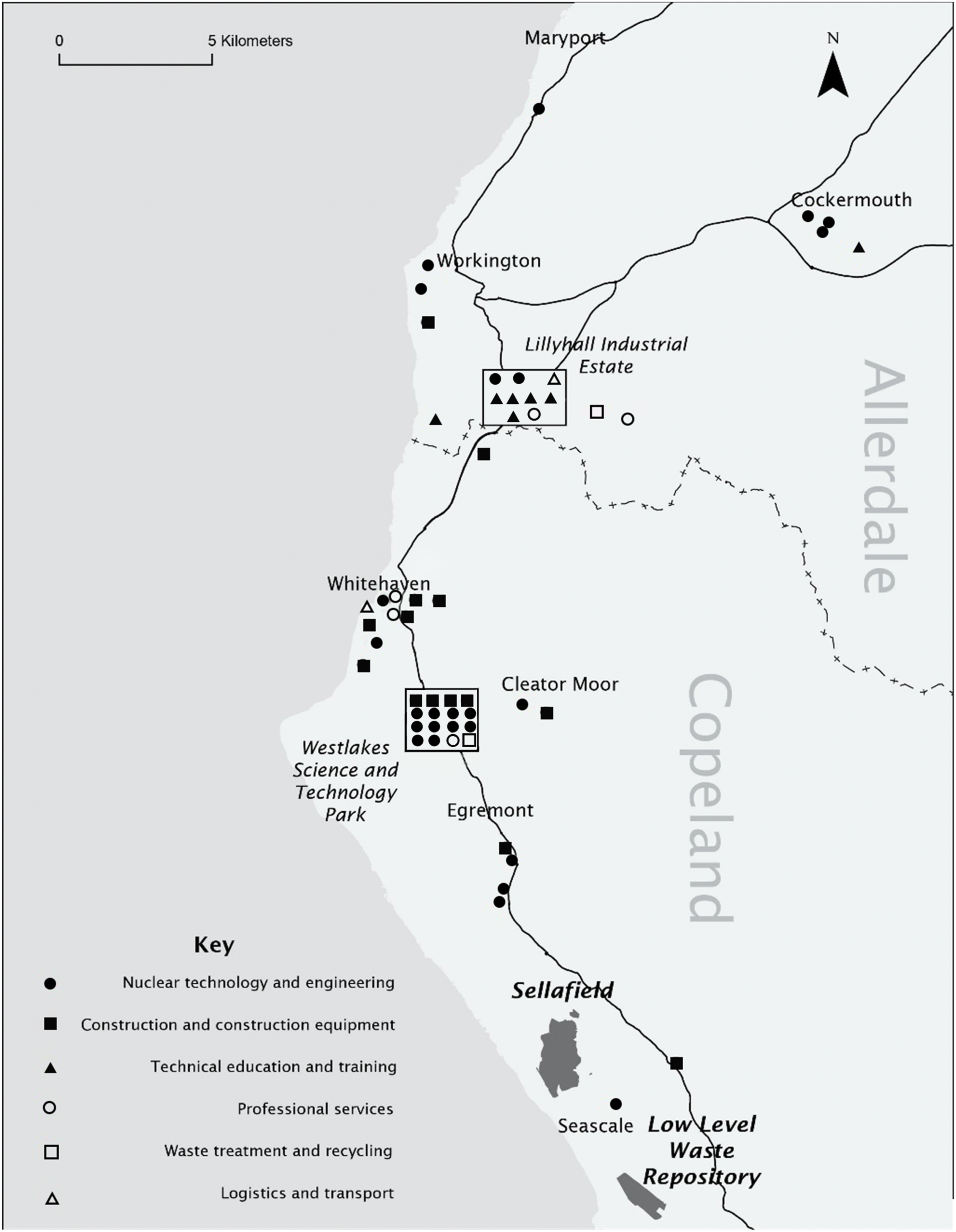

Today, West Cumbria is poised at the threshold of a potentially radical change of economic pace. Figure 2 presents a map indicating the main aspects of this situation. The map shows the geographic distribution of all those supply-chain vendors with a physical presence in West Cumbria who secured a total of £20,000 or more (in constant values) from Sellafield Ltd. for products and services between FY 2017-2018 and FY 2021-2022, though again, some non-negligible portion of the amounts received will undoubtedly have leaked out of the region via offsets and subcontracting orders. Note that the large multinational contractors operating directly on the Sellafield site are not included in Figure 2 since their presence on the site is contingent on specific contracts and therefore more or less provisional. The 59 vendors shown in the figure (mainly SMEs together with a few large producers and a group of educational institutes and research centres) represent a total annual value of supply-chain awards of £279.2 million. Most of these vendors occupy locations in the Lillyhall Industrial Estate and the Westlakes Science and Technology Park, and significant concentrations also occur in Whitehaven, Workington, and Cockermouth. A further nine firms in Carlisle accounted for an annual £4.9 million of awards, and six firms in Barrow-in-Furness for just under £1.0 million. West Cumbrian firms and education/training establishments with significant participation in the Sellafield Ltd. supply chain between FY 2017-2018 and FY 2021-2022.

Of all the firms shown in Figure 2, a total of 25 are engaged in nuclear technology and engineering while 14 offer specialised construction services and construction-equipment rentals. Other firms depicted are specialised in waste treatment and recycling, logistics and transport, and professional advice and assistance. Among the more technologically advanced are Createc Ltd. (Cockermouth), RAICo Ltd. (Whitehaven), React Engineering Ltd. (Cleator Moor), and Resolve Robotics Ltd. (Cleator Moor); and these constitute a small but dynamic sub-cluster focused on artificial intelligence and robotics. 2 Forth Engineering Ltd. in Maryport and Shepley Engineers Ltd. in Whitehaven also provide sophisticated engineering services. In addition, numerous local firms not mentioned in the supply-chain data provide direct and indirect inputs to prime contractors. One illustration of this remark is that West Cumbria is currently home to upwards of 250 engineering firms of all types (mechanical, civil, electronic, automotive, etc.), though only a handful of these are explicitly recorded in the supply-chain data. A further illustration is that a reserve of potentially useful expertise can be found in the perhaps unusually large number of knowledge-intensive business-service firms in the region.

Even though some definite intra-regional subcontracting activity can be detected, a well-developed system of interactions linking multiple firms into a robust agglomeration has still to make its appearance in West Cumbria. A new initiative that may possibly mitigate this lacuna is the programme (designated ‘Swimming with the Big Fish’) recently established by Solomons Europe Ltd. with the objective of bringing local SMEs into relationship with large Sellafield prime contractors, thereby helping to bridge the gaps in information flow, technology transfer, and project development that often separate firms with different strategic horizons from one another. An additional contribution to the local economy is the Game Changers programme, managed by FIS360 Ltd. under the auspices of the NNL, with the objective of funding commercialisable research into nuclear technology by small entrepreneurial firms. Only a handful of West Cumbrian firms have so far received funding from the Game Changers, but plans are currently under way to reach out more effectively to the local industrial community.

Education, training, and research: Facilities and programmes

Figure 2 reveals that several educational institutions besides private firms are caught up in the decommissioning supply chain. As argued earlier, successful industrial clusters comprise not only units of production and their interactions but also complementary hard infrastructures and soft overhead social capital that help to sharpen system operation. Despite the recency of West Cumbria’s economic transformation, the region has already acquired a multifaceted array of these supporting amenities, including the education, training, and research capabilities concentrated above all in the Lillyhall Industrial Estate near Workington and the Westlakes Science and Technology Park near Whitehaven (see Figure 2).

Lillyhall Industrial Estate, established by the Borough of Allerdale in the 1960s, contains an especially dense and diverse concentration of educational and training establishments in addition to a heterogeneous collection of commercial enterprises. Four establishments, each of them directly and indirectly concerned with nuclear issues, merit special mention: • The Energy Coast University Technical College dedicated to academic and technical education for 14- to 19-year-olds. • Lakes College, concentrating on T-level

3

training. A branch of the National College for Nuclear is incorporated into the college and provides courses on engineering and applied science. • Gen2 Engineering and Technology Training Ltd., which runs academic programmes, short vocational courses, and the Cumbria Apprenticeship Programme, all of them with an emphasis on nuclear issues. • The Workington Campus of the University of Cumbria located in the Energus Centre where exhibition and conference spaces are also available for public use.

A wide palette of vocational and academic courses tailored to the requirements of West Cumbrian employers is offered by these establishments. Most of them also run local job placement services. The supply chain offers substantial funding to the same establishments, as indicated by the £3.1 million given to Energus and the £485 thousand received by the Lakes College over the last 5 years. Sellafield Ltd. is an important employer of the graduates of these establishments.

The Westlakes Science and Technology Park is the site of many advanced nuclear research and business activities but is somewhat less well-endowed with academic facilities than the Lillyhall Estate. Even so, the University of Central Lancashire maintains a campus in the park with an extensive choice of courses emphasising medicine and nursing, including nuclear health. In addition, the Westlakes Dalton Nuclear Institute, which is owned and operated by the University of Manchester, houses cutting-edge research and academic capabilities. The Institute is mainly dedicated to research in radiation science with special reference to decommissioning, but it also offers a doctoral programme in a joint venture comprising the Universities of Manchester, Liverpool, and Lancaster. Some 25% of the Institute’s revenue is generated by commercial relations and collaborative projects with external partners, including Sellafield Ltd. and diverse private firms. Elsewhere in the park, nuclear research is carried out in large facilities belonging to major corporations such as Atkins Ltd., Cavendish Nuclear Ltd., and Delkia Ltd.

Numerous other business enclaves exist in West Cumbria though none of them incorporates education, training, or research capacities at levels of technical competence equivalent to those available at the Lillyhall Industrial Estate and Westlakes Science and Technology Park. By contrast, the projected Industrial Solutions Hub in Cleator Moor (see below) will doubtless add materially to the region’s fund of technical proficiencies once it comes into operation.

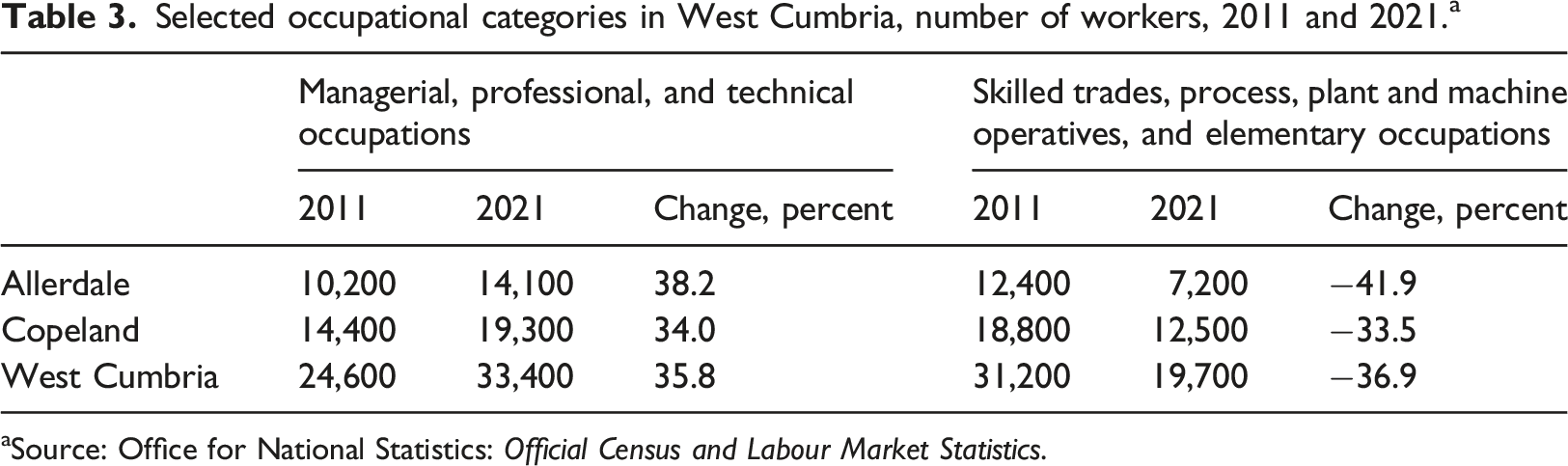

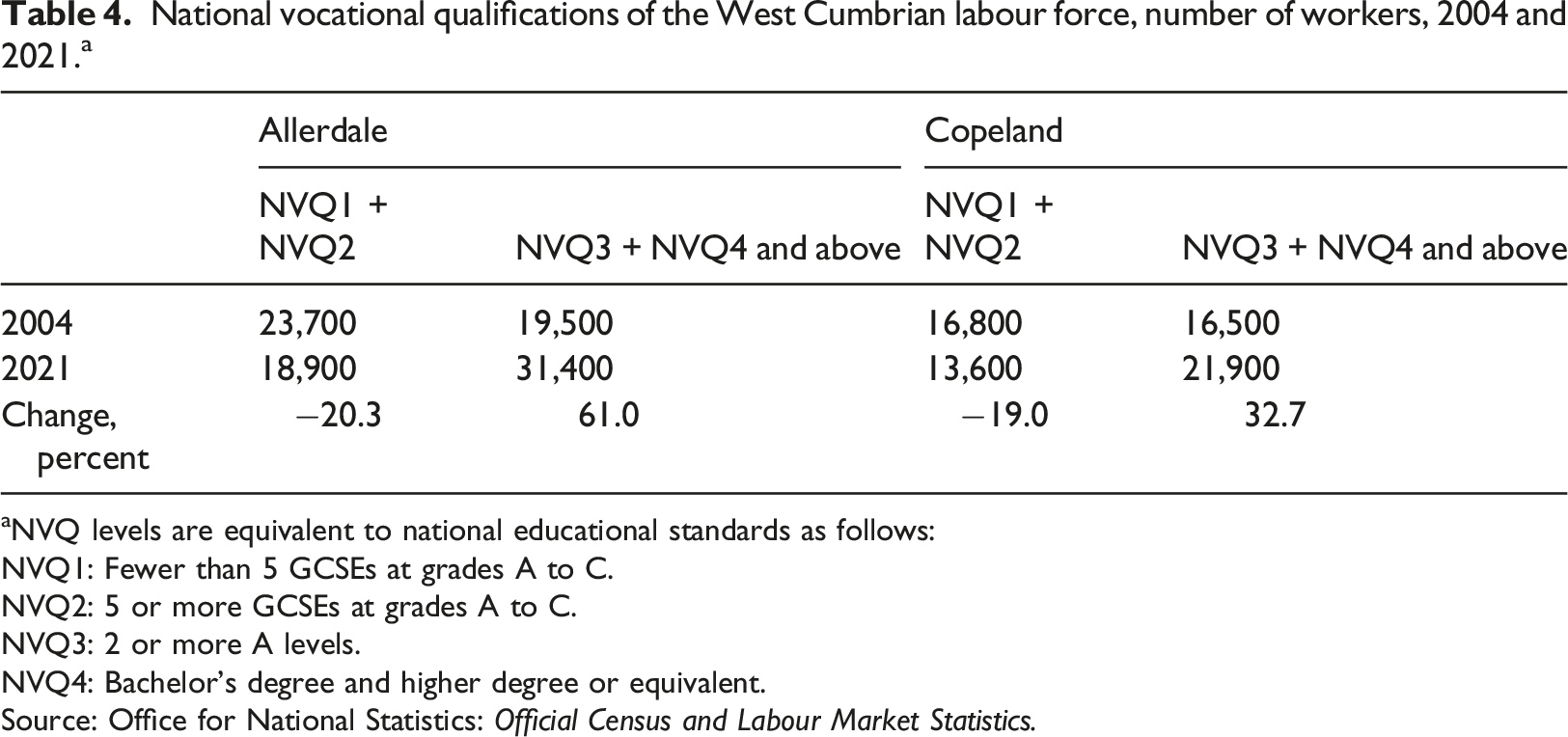

Population, occupations, and skills

In response to these developments, West Cumbria has experienced a wave of population growth and skills-upgrading that stands in sharp contrast to its earlier history of economic failure. The Sellafield complex has always sustained a cadre of highly qualified, well-paid employees, but recently, and no doubt due at least in part to decommissioning, there have been significant advances in the size and quality of the region’s overall labour force.

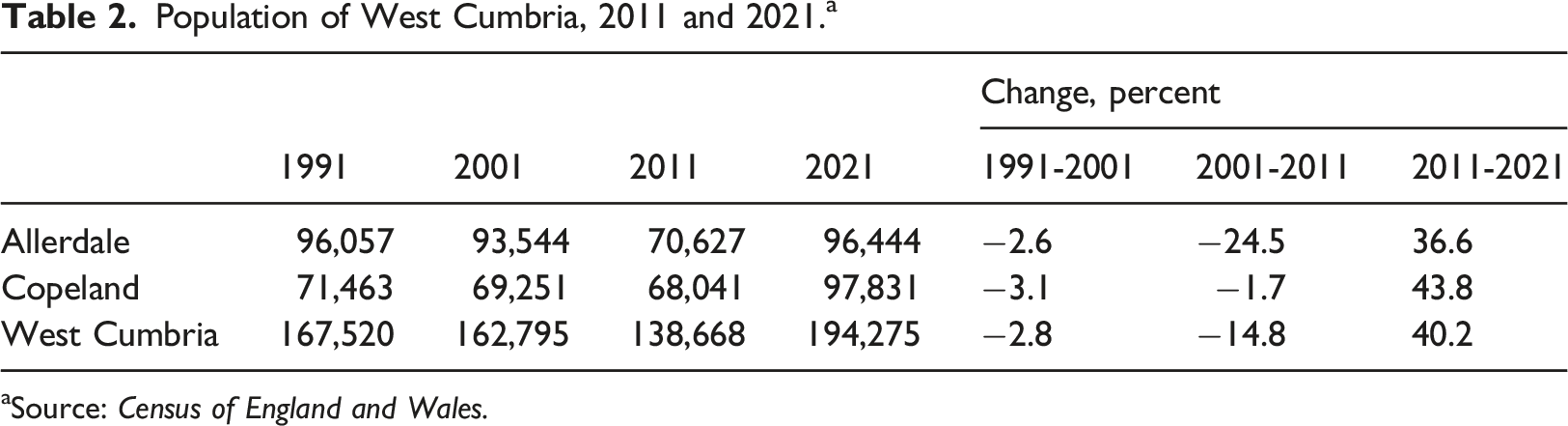

Population of West Cumbria, 2011 and 2021.a

aSource: Census of England and Wales.

Selected occupational categories in West Cumbria, number of workers, 2011 and 2021. a

aSource: Office for National Statistics: Official Census and Labour Market Statistics.

National vocational qualifications of the West Cumbrian labour force, number of workers, 2004 and 2021. a

aNVQ levels are equivalent to national educational standards as follows:

NVQ1: Fewer than 5 GCSEs at grades A to C.

NVQ2: 5 or more GCSEs at grades A to C.

NVQ3: 2 or more A levels.

NVQ4: Bachelor’s degree and higher degree or equivalent.

Source: Office for National Statistics: Official Census and Labour Market Statistics.

In spite of the continued existence of residual pockets of poverty and deprivation, West Cumbrian society has clearly been subject to deeply rooted social transformation over the last decade or so as evidenced by rising population numbers and strong improvements in the aptitudes of the labour force. Wages and salaries in West Cumbria have also emphatically moved upwards in recent years and are now generally above national levels. On the basis of median weekly pay, residents of Allerdale in full-time work earned 5.7% more than the national level in 2021 and residents in the more technologically advanced and productive economic environment of Copeland earned as much as 41.7% more. Between 2008 and 2021, the ratio of median female to male weekly pay in Allerdale remained more or less stable at approximately 0.72, but in Copeland the ratio grew substantially from 0.69 to 0.83. 4

Pathways to cluster upgrading and the consolidation of social capital

The shape of things to come?

The discussion so far describes West Cumbria as an early-stage innovation region with rising economic expectations emerging out of the primary stimulus of nuclear decommissioning. As such, West Cumbria represents a particularly significant instance of a syndrome that is now becoming evident in a number of different countries around the world. Analogous situations include both the Hanford Nuclear Site in the USA where decommissioning is creating new employment opportunities in the surrounding Benton and Franklin Counties (Novakovich, 2022), and the Fukushima Daiichi Nuclear Power Plant in Japan where an extensive industrial infrastructure project is advancing under the auspices of the Fukushima Innovation Coast Promotion Organization (OECD, 2022). A similar initiative is moving forward in Europe at the former nuclear site of Fessenheim on the Franco-German border where the construction of a ‘Novarhena’ hub for the commercialisation of hydrogen-energy technologies is envisaged (Préfet Du Haut-Rhin, 2021). Likewise, the developing science city of Dubna in Russia has also been cited as a cluster that owes it origin to spin-offs from the Joint Institute for Nuclear Research (Khozyainov and Yakushina, 2020).

As it happens, few, if any, of these cases have advanced sufficiently far for meaningful lessons to be drawn from them as to the logic of industrial cluster formation in response to nuclear decommissioning. In order to advance the argument further, we must now call on supplementary notions of regional evolutionary change above and beyond the conceptual apparatus already adduced. These notions propose that the temporal order of industrial agglomerations is typically marked by hysteresis or path-dependence where forward evolution is closely structured by pre-existing states of play (Martin, 2010). The implication of this claim for the West Cumbrian economy is not only that it is predisposed to a future rooted in nuclear technology and engineering but also that its developmental trajectory is likely to have been in some degree foreclosed by what has already happened since the early 2000s.

One way in which we can identify likely evolutionary possibilities implicit in the current situation is by examination of germane patent-citation patterns, which, in the present instance, are represented by composite national data on nuclear-technology patents. On this basis, we are able in some degree to make informed assessments as to how existing nuclear technologies might evolve into more diversified structures of production (cf. Jieun et al., 2021). In practical terms, this entails exhaustive indexing of so-called forward patent citations. The forward citations are then presumed to detect the likelihood that the substantive elements described in the citing patent will generate particular kinds of technological spin-offs (embodied in some commercial application). The details of this exercise are presented in the Appendix where relevant statistics and explanatory notes are laid out, and only the most salient points are dealt with here. The statistics presented in the Appendix are taken from the website of the United States Patent and Trademark Office 5 ; they represent counts of forward citations by patents classified under ‘Nuclear Physics and Engineering’ as defined by the Cooperative Patent Classification (CPC). American patent data are used here because of their comprehensiveness, and it is probably not too much of a distortion to assume that British patenting patterns run more or less in parallel.

The table given in the Appendix shows the incidence of the top 25 technological categories (out of a total of 127) in terms of forward citations from nuclear physics and engineering patents. Medical or veterinary science represents the most common type of forward citation, though given the relatively underdeveloped state of health research in West Cumbria, this type of activity would seem to offer only limited synergistic spin-off possibilities. Citations to nuclear physics and engineering rank high in the given list, and these technologies are, of course, well represented in West Cumbria’s new economy. Substantial numbers of forward citations refer more specifically to measuring and testing, climate change applications, electric/electronic techniques, and engineering, all of which represent very plausible windows of opportunity for West Cumbria given its current state of development. Machine tools and nanotechnology, too, are not beyond the bounds of conceivable evolutionary outcomes for the region. An OECD (1993) report on observed spin-offs from nuclear industries in different parts of the world highlights technologies that have much in common with those mentioned here, notably, testing, engineering, electronic components, environmental technologies, and material handling. The broad implications of these remarks are that while any future technological trajectory in West Cumbria will almost certainly exhibit unpredictable shifts, sectors focusing on one form or another of engineering, measuring, testing, or electronics, with roots in nuclear technology, are perhaps most likely to come to the fore.

The same kinds of technologies form the basis of an enormous variety of industrial and commercial applications. Products and services like waste treatment, cleantech, carbon capture, climate control, fuel cells, photovoltaics, health and safety, cybernetics, and robotics, to mention only some of the more obvious cases, all represent possible lines of application in West Cumbria, as does, to be sure, the continued environmental remediation of the Sellafield site. The already large number of engineering firms that exist in the region also constitute an important reserve of capabilities that may eventually be brought into a network of interdependencies structured by these technologies. Several other dimensions of the local economy present further potential linkages to the nuclear industry, most notably the extensive Robin Rigg Wind Farm in the Solway Firth, together with the proposed small modular reactor at Moorside and the long-standing scheme to harness the tidal energies of the Solway. The production of nuclear submarines by BAE Systems Ltd. in Barrow is likewise apt to provide market outlets for independent firms in Cumbria’s emerging nuclear and engineering industry. Moreover, the proposed Woodhouse Colliery just to the south of Whitehaven has now received official authorisation. When operational, the Colliery will produce high-grade coking coal and will no doubt contribute to the emerging new energy cluster in West Cumbria, though its local net impacts have been very negatively assessed by environmental advocacy groups. It is apposite here to reiterate the point that production, interlinkage, innovation, and local labour markets exert mutually reinforcing pressures in agglomerated path-dependent sequences so that individual firms tend to evolve within the framework of an overarching region-based technological paradigm. In the same way, West Cumbria appears now to have entered a conjuncture leading to a coalescing regional complex of nuclear, engineering, and related industries. The economy of West Cumbria will almost surely be propelled forward in this overall configuration, and we can plausibly argue that the region will henceforth follow a more benign evolutionary course in human and environmental terms than was the case when it was dominated by what the poet Norman Nicholson referred to as the ‘Toadstool Towers’ of Sellafield.

The public dimension: Institutions, collective action, and policy

The notion of a collective order has already been mentioned several times, but its full import in regard to the viability of West Cumbria’s economy in the era of decommissioning remains to be more fully explored. Of special note is the fact that the region’s economy has of late been the scene of growing institutional networks. These play a potentially crucial role in integrating evolving spatial structures of production into efficient systems while simultaneously helping to dampen the negative externalities and diseconomies that are almost always accessory to any structure of this type. This order of things is in part sustained by educational and research services, but its sphere of operation also includes a heterogeneous body of social and political structures geared to system coordination and remedial action.

There is a long tradition in West Cumbria, going back to the 1920s, of public intervention to resolve regional problems and predicaments, and many different organisations have come and gone with this objective in view. As new opportunities for economic growth brought on after the 1990s by the decision to decommission Sellafield come into view, corresponding changes in local government policies and the institutional environment are being increasingly brought to bear on the local economy. The NDA and many business interests are implicated in these efforts as well. The energies thus mobilised bore early fruit in a ‘Masterplan’ published in 2008 and a subsequent ‘Blueprint’ in 2012 (BEC, 2008; BEC, 2012), both of them laying out ambitious projections about the developmental implications of Sellafield’s shifting status. These early stirrings of a public response to decommissioning set the scene for unprecedented shifts in perceptions of the local area and for enhanced investor confidence. One of the more conspicuous outcomes of this rising tide has been the rapid recent expansion of the Westlakes Science and Technology Park (currently managed by Building Extraordinary Communities Ltd. 6 ) with its advanced architectural set pieces and manicured grounds quite unlike anything in the rest of the West Cumbrian landscape.

Local governments and the NDA continue to provide important resources in support of regional development, not only in the economic arena but also in matters of social and urban wellbeing, as illustrated by Sellafield’s generous Social Impact Program dedicated to fostering family and community welfare. Other institutional sources of assistance to the region include the Cumbria Local Enterprise Partnership (CLEP), a county-wide organisation that has been active since 2016, and the Cumbria Business Growth Hub which was established by the Cumbria Chamber of Commerce in 2012. Both of these organisations are active in promoting business performance by means of financial and advisory support for SMEs, with special emphasis on industrial innovation. CLEP has also played a significant leadership role jointly with the borough council of Copeland and the NDA in sponsoring the £22.5 million Town Deal to upgrade the Leconfield Industrial Estate in Cleator Moor where the new Industrial Solutions Hub will be completed to carry out scientific and engineering activities devoted to nuclear decommissioning. 7 Amongst the additional benefits that are expected to be brought to the region by CLEP or its successor – as well as by initiatives set in motion by the Northern Powerhouse Partnership – are significant investments to correct longstanding inadequacies of road and rail communications.

These concrete contributions to the collective resources of the West Cumbrian agglomeration are supplemented by institutional structures that strengthen associative relationships stimulating information exchange and collaborative interaction. The Northern Nuclear Alliance, for example, brings together companies at all levels in the supply chain in events that facilitate discussion and learning about technological and business trends in the nuclear industry. The alliance serves the nuclear industry throughout the northwest of England, and it has a strong nucleus of members in West Cumbria. Similarly, but on a more limited scale, the Northern Branch of the Nuclear Institute disseminates technical know-how and employment information amongst engineers and scientists in the industry. Perhaps more than any other organisational entity in the region, Britain’s Energy Coast Business Cluster (BECBC) has striven to boost the circulation of information and to provide an inclusive forum of interchange for participants in the nuclear industry. BECBC brings together some 250 members comprising private firms, organisations, and governmental bodies. It sponsors what it identifies on its website as ‘networking, business support, industry introductions, events, opportunities, business promotion and marketing, and industry news’, 8 and, as such, it plays a unique role in reinforcing overall social capital in the region.

As insubstantial as these types of organisations may seem to be in comparison with more durable capital investments, they represent an indispensable dimension of any regional development programme. In their absence, vital bodies of local knowledge in such matters as markets, materials, technical expertise, managerial cultures, traditions, and habits of mind would almost certainly lose at least part of their edge and substance. Even a casual observer of recent trends in West Cumbria becomes at once aware of the implicit value of these and other organisational entities, especially in view of their relentless sponsorship of conferences, seminars, short courses, training programmes, exhibitions, and social events as aids to upskilling, exchange of know-how, and regional cohesion.

Towards an augmented development agenda

The current conjuncture in the West Cumbrian economy can be described in terms of an agglomeration of private productive assets interwoven with webs of common-pool resources and agencies of social management. The ongoing socio-economic transformation of the region rests on three principal foundations; namely, first, nuclear decommissioning and the corresponding money outflow from Sellafield Ltd; second, the concomitant beginnings of an agglomeration of technologically advanced enterprises; and third, a body of institutions affording diverse resource-allocation and policy services. This tripartite structure of forces has opened up unprecedented potentials for regional growth. We may ask how viable is this regional constellation of people, relationships, and organisations in its current stage of emergence?

The abundant stream of money from decommissioning activities will undoubtedly continue far into the foreseeable future. Yet, even if this situation represents an unquestionably positive state of affairs for West Cumbria, it is simultaneously charged with hidden hazards. On the one hand, it underpins expectations of steady long-term cash flow through the supply chain. On the other hand, as things now stand, most of the money dispensed in this manner is shunted out of the region. Crucially, there may be grounds for supposing that undue local dependence on Sellafield Ltd.’s supply-chain expenditures might also prove to be a source of deleterious system rigidities. The point to be stressed here is that producers facing a monopsonistic (or quasi-monopsonistic) buyer are susceptible to forms of lock-in that may compromise their organisational flexibility and, specifically, hinder their capacity for effective adjustment to wider national and international market trends, especially if lock-in persists over some extended period of time. There is therefore much to be said for two complementary strategies designed to underpin West Cumbria’s industrial revival. The first and most obvious desideratum concerns the need for further build-up of localised socio-economic capacities by allocating a much greater proportion of decommissioning funds to actual and prospective West Cumbrian entrepreneurs and social organisations (as recommended by the Committee of Public Accounts, 2018). The other turns on the more problematical suggestion that aggressive efforts to cultivate wider markets by local firms – both individual units and groups – will be necessary if more robust modes of economic development are to come forth. Any successes in this regard will in and of themselves magnify agglomeration economies by creating additional organisational spaces for the accommodation of new entrepreneurial and innovative energies.

The overall pertinence of these remarks for policy-making in support of West Cumbria’s economic ambitions can be summarised in the proposition that heavy-handed attempts to steer the economy into preconceived channels of development are liable to be much less effective than measures devoted to encouraging entrepreneurship in general and the accumulation of useful common-pool resources. The policy imperatives implied by this advocacy are many and various, for example, augmented support for relevant types of education and training, subsidies for research into shared technological bottlenecks, accelerated transfers of technology and know-how to SMEs, public funding for enhancement of job search and recruitment processes, effective encouragement of creative inter-firm relationships, investment in critical infrastructural facilities, consolidation of industry-specific social networks, and assistance to producers for contesting national and international markets, to mention only a few of the more pressing exigencies, though taking on these tasks will be a major challenge to existing institutions. At the same time, a typical Achilles heel of emerging agglomerations is the difficulty faced by SMEs in raising capital, a weakness that is sharply evident given the contributions that SMEs so often make to the lifeblood of vibrant, innovative clusters. Injections of public finance into new firm formation and entrepreneurial inventiveness are hence a potent means of buttressing competitive advantages. Local governments, the Cumbria Local Enterprise Partnership, the Cumbria Business Growth Hub, the NDA, and other public agencies in Northwest England are already taking appropriate steps in these directions, and more generous public allocation of resources to these ends will no doubt pay dividends in terms of developmental response. Initiatives of these sorts fit well within the national Levelling Up policy framework, though as Sunley et al. (2022) point out, the framework appears ill-equipped to deal with ‘place-based collaborative learning about the potential of new technologies and practices’, especially in areas that ‘lack political significance’.

As the preceding argument has emphasised, a viable policy agenda for remedial intervention in any regional agglomeration is well advised to search out specific points of system fragility and collective opportunity that lend themselves to public intervention rather than to focus on forward programming directed to prescribed end points. Given careful attention to these matters, there is every reason to suppose that the regional economy will progress through flexible evolutionary pathways – via multiple experiments, with their attendant failures and successes – that facilitate system adjustments to contingencies and risks as they arise. The growth pains of other advanced-technology agglomerations, from Silicon Valley to Bangalore, offer many tacit clues as to relevant strategic postures (Scott, 1995; Storper, 1997). Not least of the challenges faced as the West Cumbrian economic transition fostered by decommissioning moves head is the question of social justice and the need for due policy attention to left-behind fractions of the local population (Newell and Mulvaney, 2013).

A promising but still uncertain future

The West Cumbrian economy has undergone a remarkable, if still somewhat amorphous, transformation over the last couple of decades. This historical turn is equivalent to the reconstruction of West Cumbria as an early-stage innovation region primed for future growth.

Yet, this statement must be promptly qualified. It is by no means inevitable that the economy will conform to a benign growth model where a steadily expanding mosaic of agglomerated in production activities, labour market activities, and institutional responses condenses out as an island of high productivity and competitiveness. This remark stems not only from the reservations already expressed about the region’s current prospects but also from the possibility that any number of contingencies might compromise the formation of the common-pool resources essential to any durable region-wide dynamic of intensifying competitive advantage and market contestation. Competitive threats from outside are a further cause for concern. Well-developed clusters of nuclear research and production activities are already present in other parts of the country – above all in Warrington and the Southwest Nuclear Arc running from Oxford through Bristol to Bridgewater – and these may well eventually pose a competitive threat to the onward march of West Cumbria’s fortunes. Moreover, and especially in view of the rival claims to public spending by these and other regions, there is no reason to suppose that the monetary flows that have hitherto sustained much of West Cumbria’s growth will continue as an iron-clad certainty, a point that is underlined by the recent decision not to site the government’s planned prototype fusion reactor in the region.

Notwithstanding these caveats, a positive assessment of West Cumbria’s economic expectations can be very reasonably advanced. A preliminary accumulation of assets in the matter of technologies, production capacities, infrastructural resources, and institutional arrangements is already functioning in place, and a sizable labour force endowed with advanced skills has assembled in the region. Additionally, in a world where nuclear technologies play a key role in the search for new commercial outlets like alternative energy, low-carbon production, environmental remediation, innovative electronic contrivances, and advanced engineering products (including robotics and artificial intelligence), West Cumbria’s economy is credibly positioned at a point of take-off. In the best of all possible worlds, the region’s burgeoning cluster of nuclear and engineering industries will also adapt to alternative market niches thus reducing the relative weight of its dependence on decommissioning. A positive factor underlying this optimistic appraisal is that a significant segment of West Cumbrian society is by all accounts reconciled to the idea that the nuclear industry, whatever form it might take, will remain a more or less permanent feature of the local economy (Haraldsen, 2018; Wylie et al., 2020). An urgent need now is for some fine-tuning of the currently diffuse political leadership in the region and more decisive articulation of a set of overarching policy goals judiciously designed to contend with the many challenges that have been shown to characterise the current situation. Is it beyond the bounds of reason to imagine that a modest West Cumbrian Science City might actually be in the making under the Lakeland fells?

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.