Abstract

Employing an institutional – FDI – economic growth lens the purpose of this paper is to identify and explain the impacts of Chinese FDI (CFDI) on host countries’ economic growth. While extensive research has been undertaken regarding determinants of CFDI, little is known about the actual outcomes of CFDI in recipient countries. Based on a sample of 22 countries over the period 2003–2018, our results identify that while general flows of FDI exhibited positive impacts on host countries’ economic growth, CFDI had a negative effect on host country economic growth. From the host country perspective, given the emphasis that is placed on FDI as an instrument of growth and development, our findings raise questions about what host countries are actually gaining from CFDI and the potential implications of whether pursuing the ‘Beijing Consensus’ as opposed to the ‘Washington Consensus’ is really in the long-term interests of countries.

Keywords

Introduction

This paper explores the impact of Chinese foreign direct investment (CFDI) on host countries’ economic growth with reference to the Belt and Road Initiative (BRI). As the world’s second largest FDI investor (UNCTAD, 2019), a significant body of research investigating the determinants of CFDI has been undertaken (Buckley et al., 2007; Kolstad and Wiig, 2012; Ross, 2015; Ross et al., 2019). However, there is now a requirement to better understand the impacts that CFDI is having on host country economies as opposed to simply explaining cross-country flows of CFDI (Buckley et al., 2018; Fu and Bolaky, 2020; Li et al., 2022). Moreover, while a range of extant literature has found linkages between FDI and economic growth (Li and Liu, 2005; Makki and Somwaru, 2004; Nair-Reichert and Weinhold, 2001), there is little if any empirical research demonstrating the actual impact of CFDI on host countries’ economic growth. This lack of empirical research is surprising given the exponential growth in CFDI following the inception of the Belt and Road Initiative in 2013. While FDI projects are generally viewed with optimism, given the potential to deliver investment, jobs, transformational infrastructure projects and general economic development, as of 2018, OECD data reported that China’s non-performing assets 1 in the BRI alone had reached $101.8 billion leaving a gap in our understanding about the impacts of Chinese investments on host country economic development.

China’s position today as an economic superpower and major international investor can largely be traced back to a series of policy reforms commencing in 1978, which sought to tackle key barriers curtailing China’s economic development. Internally, the establishment of market incentives in agriculture and industry promoted productivity and income growth; while limited, but targeted external liberalisation of trade and investment, between 1978 and 1984 via the ‘Open Door’ reforms attracted capital inflows from foreign investors, providing advanced technologies critical to China’s development (Chen et al., 1995). Throughout this period foreign investors were also encouraged to establish production facilities in China’s newly created experimental Special Economic Zones. China has subsequently, since 1993, been the second largest recipient of FDI globally (UNCTAD, 2022), experienced an average GDP growth rate of 9.4% (World Bank, 2020a) and become the world’s largest exporter of goods and services (World Bank, 2020b).

China’s exposure to FDI provided a major stepping stone for its integration into the global economy. Inward FDI flows brought knowledge of global markets, enabling the expansion of Chinese foreign trade and exposed Chinese firms to international competition, which provided the catalyst for improvements in management and production techniques to drive competitiveness (Chen et al., 1995). Building upon the seminal open door reforms the Chinese government’s ‘Going Global’ policy was implemented in the latter part of the 1990s, and actively encouraged specific Chinese firms to expand their global presence and invest overseas (Buckley et al., 2007). Further integration into the global economic system in 2001 via accession to the World Trade Organisation helped China transform its FDI position, and by 2016, Chinese outward investment flows surpassed its inward flows of FDI, charting China’s route to becoming the world’s second largest global investor (UNCTAD, 2019).

Consequently, with China set to become the world’s largest economy by 2028 (CEBR, 2020), this paper specifically seeks to enhance our limited understanding of the role CFDI has on host country economic growth. In doing so, our paper can make a number of contributions. First, utilising a panel data set between 2003 and 2018 for 22 Eurasian countries, we are able to add to the very limited empirical literature on the impacts of CFDI on host countries’ development. Second, as China looks to extend its sphere of influence economically and geopolitically in the form of the BRI, we also model China’s exponential growth in FDI from 2013 to 2018, to account for the effects of the BRI on host countries’ economic growth. Third, after controlling for country level effects, our modelling reveals that while overall global flows of FDI do exhibit positive effects on host countries’ economic growth, this is not the case for Chinese investments. Fourth, from the host country perspective, given the emphasis that is placed on FDI as an instrument of growth and development, our findings raise questions about the efficacy of CFDI, what host countries are actually gaining from CFDI, and the potential implications of whether pursuing the ‘Beijing Consensus’, as opposed to the ‘Washington Consensus’ is really in the long-term interests of countries. The remainder of the paper is structured as follows. The Literature review and conceptual framework section outlines the theoretical and conceptual approach. The Data, variable measurement and empirical approach section outlines the data and econometric method. The empirical results are presented in the Results and discussion section, which is followed by the Conclusion and directions for future research.

Literature review and conceptual framework

The role of FDI in economic growth theory

Historically, FDI theory from the field of international business has been utilised to explain firm level investment decisions and differences in cross-country flows of FDI (Buckley and Casson, 1976; Dunning, 1993; Hymer, 1976; Knickerbocker, 1973), yet while an extensive range of studies cite the positive effects that FDI can potentially have on economic growth and development (Borensztein et al., 1998; Li and Liu, 2005), the concept of FDI is seldom formally integrated into theoretical models of economic growth. However, theoretically the role of FDI as a determinant of economic growth can be found embedded within the respective exogenous and endogenous growth models developed by Solow (1956) and Romer (1986) in relation to capital accumulation. Solow suggests economic growth is achieved through the accumulation of factors of production such as capital and labour. According to Solow’s theory, flows of FDI into a host economy raise the capital stock which enhances economic growth. However, Solow’s model limits the extent to which capital accumulation, and hence, FDI can affect output growth, as capital is considered subject to diminishing returns; whereby increases in capital accumulation may only grant short-term increases in economic growth (Solow, 1956). However, FDI is widely accepted to encompass more than simple flows of capital, offering a package of advanced resource transfer effects, which can directly increase the rate of economic growth by raising the level of capital, thereby limiting the degree to which capital experiences diminishing returns. Thus, FDI can drive economic growth by increasing the amount and efficiency of capital in a host economy.

While both exogenous and endogenous growth models emphasise the importance of capital accumulation: the endogenous growth model developed by Romer (1986) asserts that economic growth is primarily driven by both the stock of human capital and technological development. The higher the level of human capital, the greater the level of technological progress, and hence the greater increase in total factor productivity (Al Nasser, 2010; Borensztein et al., 1998). Thus, if long-run growth is taken as a function of technological progress, FDI can increase the rate of economic growth in a host economy through a package containing physical capital, technology transfer, human capital and other spill-over effects such as R&D expenditures (Mahembe and Odhiambo, 2014), contributing not only to the growth and success of local firms, but which have also been found to be one of the most significant growth-inducing effects of FDI (Liu, 2008).

Despite the theoretical efficacy of Solow and Romer’s respective growth models, empirical findings highlight the complexity of the relationship between FDI and economic growth. For example, while a number of studies support a link between FDI and economic growth, highlighting the importance of FDI for technology transfer and its superiority over domestic investments for inducing growth (Al Nasser, 2010; Borensztein et al., 1998; Hansen & Rand, 2006; Li and Liu, 2005), the positive impact of FDI on economic growth is not uniform. A number of studies find no effects or positive effects dependent upon a countries stage of development (Johnson, 2006; Herzer et al., 2008; Carkovic and Levin, 2005), while Liu (2008) highlights the effects of FDI spill-overs can be both positive and negative. Just as FDI may introduce new technology into a host economy and increase productivity, simultaneously MNCs can also lead to the closure of local firms and higher unemployment potentially reducing host country growth (Jordaan, 2012; Ram and Zhang, 2002).

The complexity of drawing links between FDI and economic growth is highlighted by the empirical literature, and the reality that the growth effects of FDI may be shaped by a number of factors beyond simple capital accumulation (Zhang, 2001). Much of the literature which finds a positive link appears contingent upon conditions within the host economy (De Mello, 1997), while Zhang (2001) contends that country-specific conditions cast doubt over the general hypothesis that increased FDI simply leads to economic growth. Further still, Borensztein et al. (1998) identifies a positive link between FDI and growth, but crucially highlights the importance of a host economy’s capacity to sufficiently absorb growth-inducing spill-over externalities. In particular, a number of studies have highlighted the important role of host country institutions as a determinant of cross-country FDI flows (Bailey, 2018; Ross, 2015, 2019; Ross et al., 2019) either creating or deterring a positive investment environment.

Institutions and transaction cost theory

North (1990) proposed that institutions are the rules of the game upon which society is based. Comprising both formal (laws and regulations) and informal structures (values and norms) institutions create and develop the governance infrastructure which underpins the incentive structure of any society (Ross, 2019). As noted by Thirwall (2011: 118), ‘growth cannot take place in an institutional vacuum’. Thus, institutions have the potential to either bolster or impede economic growth. In contrast to the mixed empirical findings regarding the link between FDI and economic growth, institutions are widely accepted as yielding a strong positive impact on economic growth. Thus, on this basis, it might be implied that institutions are at least equally as important, if not more important than traditional location factors assigned to explaining FDI location choice. However, in the case of CFDI, this relationship is arguably less strong given the significant levels of CFDI taking place in locations which are often considered to have weak institutions (Ross et al., 2019).

Chinese outward foreign direct investment

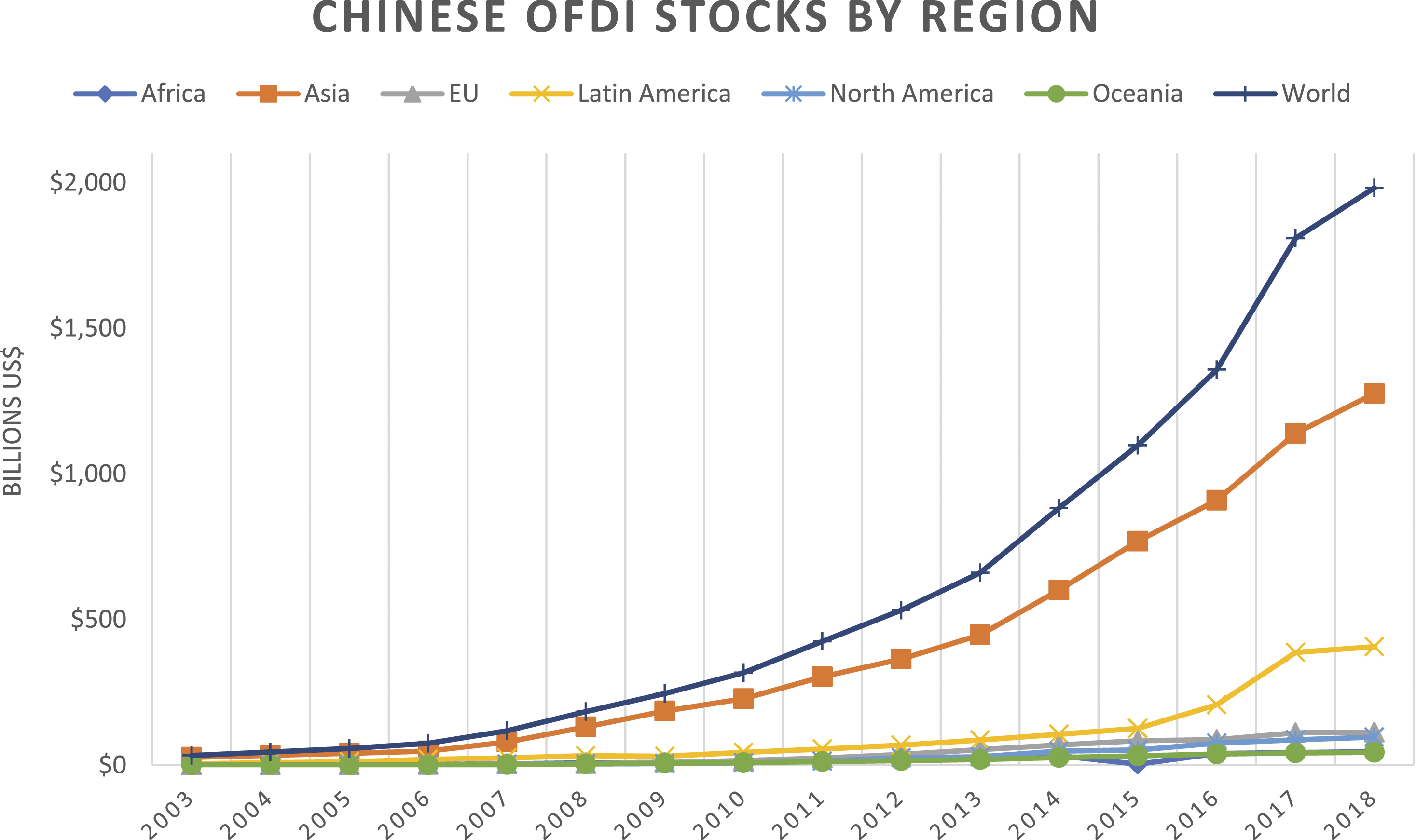

In recognition of China’s position as the world’s second largest investor an extensive body of empirical studies have been undertaken to better understand the cross-country determinants of CFDI. Yet, while we now have a better understanding about the determinants of CFDI, given China’s status as an economic superpower, very limited empirical research documenting the impacts of CFDI on host countries economies has been undertaken. This is somewhat surprising given the exponential growth in CFDI following its accession to the WTO in 2001, and which also reflects that countries are increasingly open to receiving greater amounts of Chinese investment. Moreover, if the positive correlation between FDI and economic development are deemed to hold, then the appeal of increased FDI flows arising from China’s Belt and Road Initiative (BRI) is likely to be of significant interest to participant countries. As Figure 1 highlights the stock of Chinese outward FDI by region demonstrates, since the inception of the BRI in 2013, China’s outward investments have grown substantially, which again highlights the need to better understand the impact CFDI is having on host countries. Chinese outward FDI Stocks by region. Source: MOFCOM (2018) statistical bulletin of China’s outward foreign direct investment.

The Belt and Road Initiative

Unveiled in 2013 by Chinese President Xi Jinping, the Belt and Road Initiative (BRI) is expected to play a significant role in meeting China’s needs for continued economic development. A reconstruction of the Ancient Silk Road, the 21st Century BRI seeks to strengthen Beijing’s economic leadership via what some have labelled the most ‘ambitious infrastructure project in history’ (CEBR, 2019). In particular, the BRI seeks to revive the trade routes and cultural exchanges that linked the major civilisations of Asia, Europe and Africa, improving connectivity and co-operation on a transcontinental scale across more than 70 countries (World Bank, 2019).

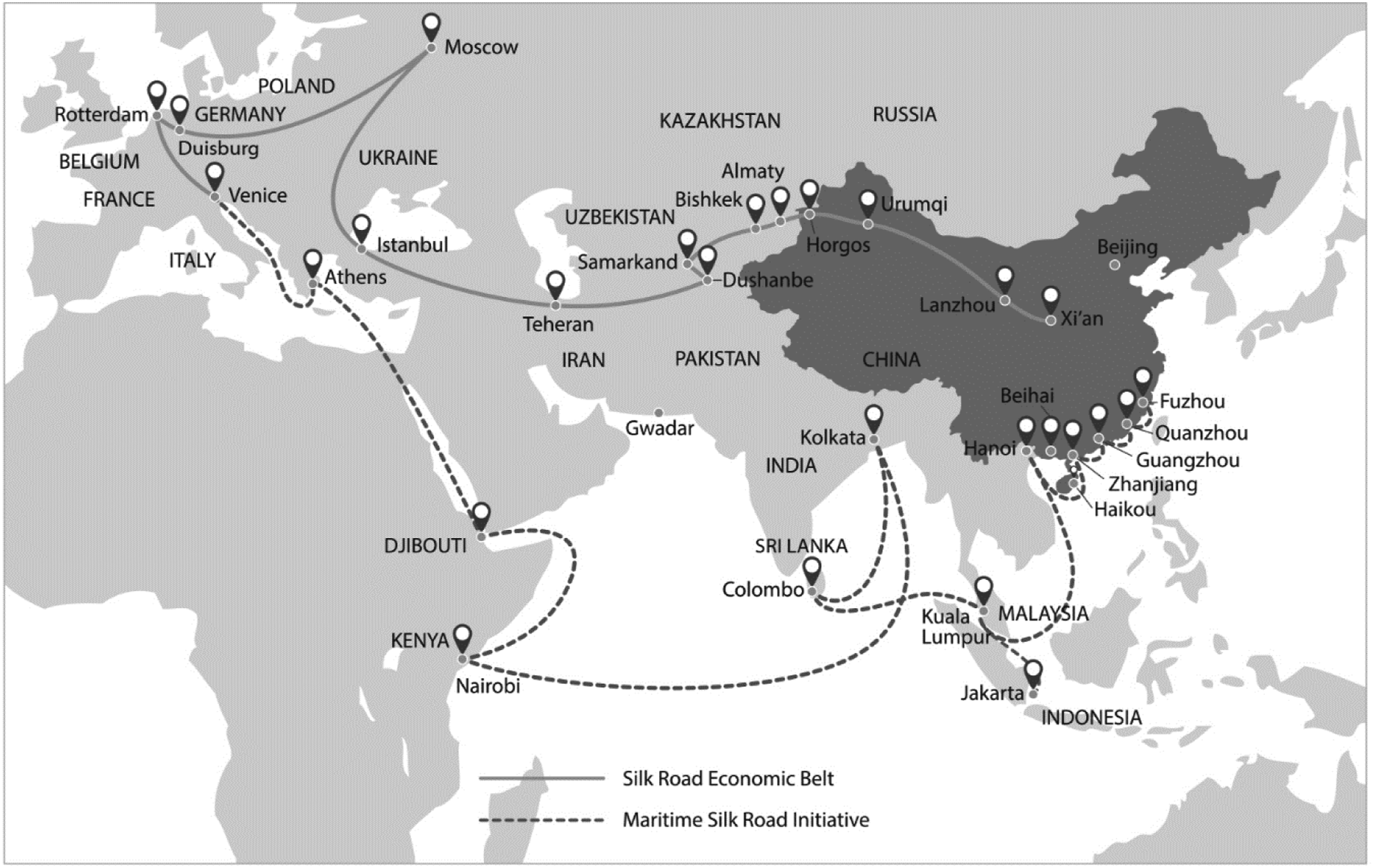

Although China’s economy is set to be the largest beneficiary of the BRI – gaining $1,777bn in GDP by 2040 – Beijing’s grand plan to connect East with West is forecast to increase global GDP by 4.2% over the same time period (CEBR, 2019). Achieved through six economic corridors the overland ‘Belt’ and a maritime ‘Road’ (see Figure 2), will connect China with South East Asia, Africa and ultimately Europe offering increased opportunities for trade, investment and jobs at a transcontinental level. It has been estimated that transportation projects along the BRI corridors could reduce travel times by 12%, and enhance international trade by between 4% and 12%, respectively (Konings, 2018; World Bank, 2019), while increased FDI flows arising from the BRI are expected to see GDP accrue 0.14% faster for some BRI corridor countries (World Bank, 2019). Key Chinese trading partners such as Indonesia and Vietnam have already seen increased BRI capital flows of $171bn and $152bn, respectively (CIMB, 2018). BRI geographic coverage. Source: Smith Freehills (2018).

The aforementioned theoretical literature on economic growth and FDI highlights the potentially positive role CFDI may have on host countries’ economic growth, both directly and following the inception of the BRI in 2013. With FDI acting as a conduit for growth via capital accumulation and technological progress, China’s BRI has the potential to deliver both of these factors to countries on the BRI routes, which otherwise might struggle to attract FDI from conventional sources of investment. Equally, from a policy perspective, it is not difficult to understand why countries may want to be involved in the BRI; as the nature of the BRI provides a unique opportunity to develop both physical and institutional infrastructure in host countries, both of which have strong linkages to higher levels of economic growth.

However, while the BRI is understandably viewed with optimism in some quarters, given its potential to deliver investment, jobs, transformational infrastructure projects and general economic development, it is viewed with considerable anxiety by others in relation to non-performing assets and the implications of some countries not being able to meet their debt obligations (Ross, 2020). Furthermore, while empirical works documenting the determinants of CFDI are fairly extensive (Buckley et al., 2007; Kang and Jiang, 2012; Ross, 2015; Ross et al., 2019), studies examining the growth impacts of CFDI remain relatively scarce and untested.

Conceptual framework

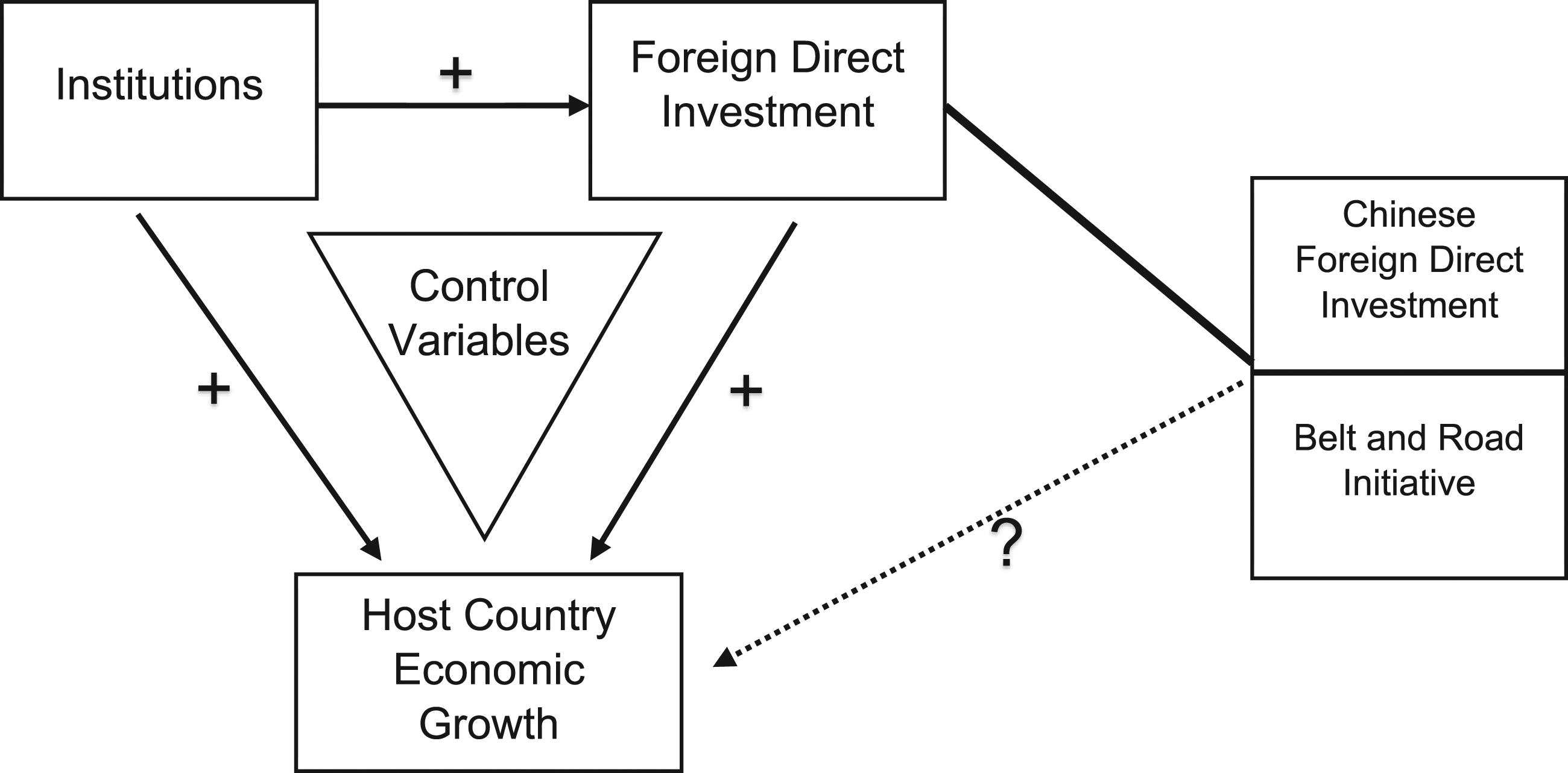

Synthesising the institutional, FDI and economic growth literature our paper proposes a conceptual framework as depicted in Figure 3 to aid our understanding and capture the impact of CFDI on host countries’ economic growth. Following the aforementioned theoretical and empirical literature, alongside the recognition at a policy level regarding the positive externalities associated with FDI, our framework expects that general inward flows of FDI will have a positive impact on host countries’ economic growth. Conceptual framework.

Nevertheless, FDI alone does not drive economic growth, and as long as countries demonstrate differences in cross-country flows of FDI and rates of economic growth, this indicates that local host country conditions must be important determining factors of differences in a country’s level of economic development. Therefore, our framework suggests that economic growth and inflows of FDI are contingent on host economies having sufficient capacity to absorb investments. This capacity relates to the institutional environment whereby countries with weak institutional capacity to design and implement an effective investment regime; and secondly, absorb FDI will struggle to attract and benefit from the positive externalities associated with FDI such as higher levels of economic growth. In general terms, countries with sound institutions are expected to demonstrate better economic performance (Butkiewicz and Yanikkaya, 2006).

However, given China’s patterns of FDI into countries that have not traditionally been considered as conventional investment locations by other investors, our framework reflects our gap in knowledge, in that it is unclear if current literature related to investment and economic growth hold in the case of CFDI. Specifically, with China forecast to become the world’s largest economy by 2028 (CEBR, 2020), and its global share of FDI outflows continuing to increase, a clearer understanding of what a host economy may gain from CFDI has become increasingly important. This is especially the case in light of China’s latest strategy for economic development – The Belt and Road Initiative, which has coincided with an exponential growth in Chinese outward investments. Our conceptual framework alongside a range of control variables is fully operationalised in the following section to explore the impacts of CFDI on host countries’ economic growth.

Data, variable measurement and empirical approach

In order to explore the impact of CFDI on host countries’ economic growth we employ panel data modelling over the period 2003–2018 for twenty-two 2 Eurasian and Middle Eastern countries. Further still, in order to account for the potential impact of China’s BRI, we separately model CFDI from 2013 to 2018, as a proxy measure for the impact of the BRI on host countries’ economic growth. The dependent variable is measured by annual rates of host country economic growth (HGRO), based on data obtained from the World Bank. The sample of predominately Asian countries reflects that the vast majority of CFDI outflows are focussed on the Asia region, while the inclusion of a number of economically and politically significant Middle Eastern countries reflects their proximity, as major regional powers in relation to BRI trading routes. Nevertheless, while the Middle East is of undoubted geostrategic importance to BRI trading routes, our predominant focus on Asian countries reflects that the Asian continent is the largest recipient of Chinese outward investment (Nedopil, 2021), and the focal point in China’s strategy for its own continued economic development. Therefore, by focussing our analysis on Asia, we can gain important insights into the impact of CFDI on host countries’ economic growth.

Independent and control variables

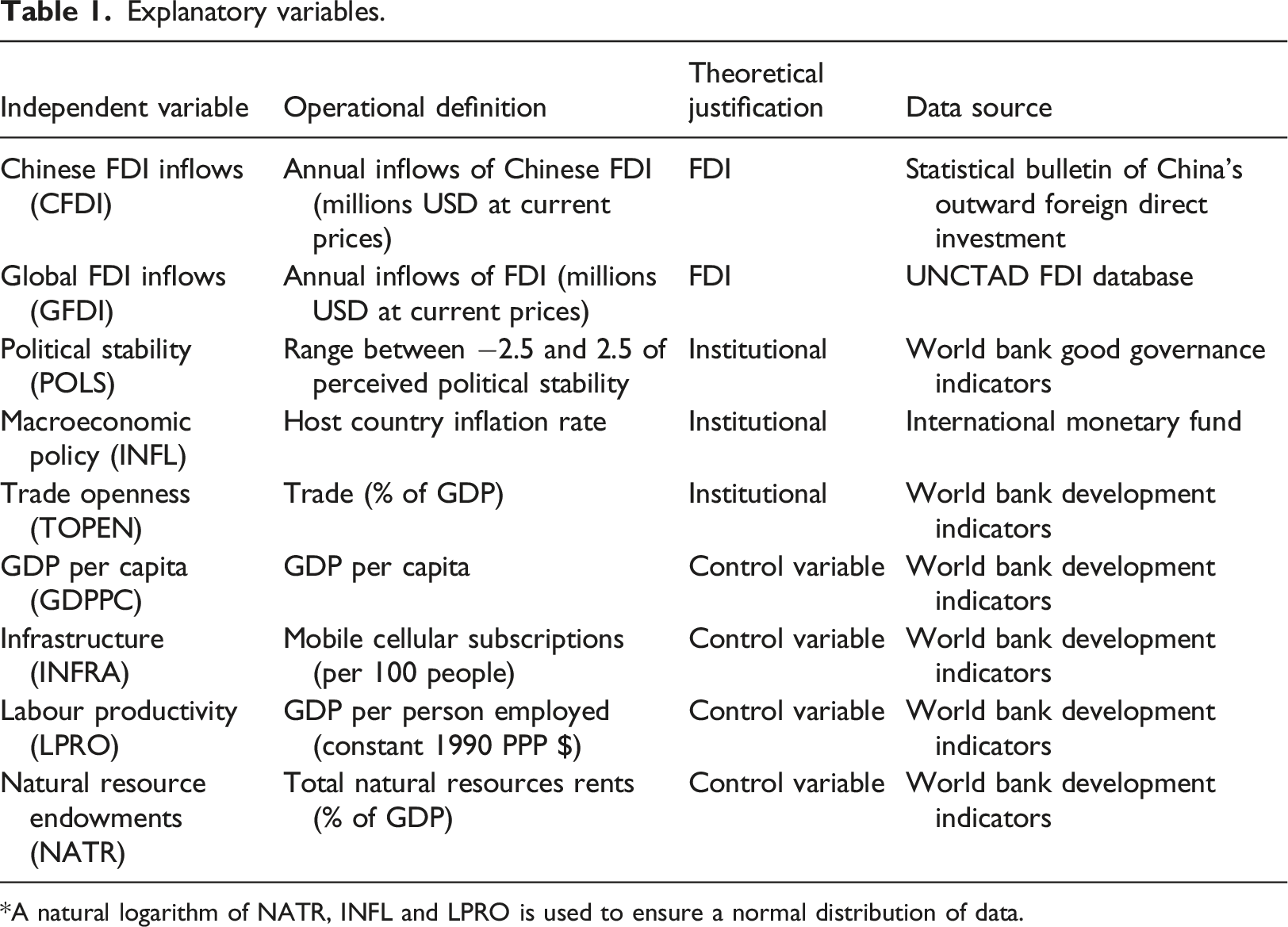

Explanatory variables.

*A natural logarithm of NATR, INFL and LPRO is used to ensure a normal distribution of data.

Robust institutions create predictable parameters and reduce the risks associated with undertaking economic transactions (Ross, 2019). While the role of institutions and their impacts can take many different forms, it is a country’s political environment that informs and shapes the overall institutional framework in which individuals and firms must act. Indeed, a number of studies have highlighted the role of political stability as a key variable when analysing the effects of institutions on economic growth (Acemoglu et al., 2005; Nawaz et al., 2014; Siddiqui and Ahmed, 2013), while Aisen and Veiga (2013) highlight that political instability leads to sub-optimal macroeconomic policies negatively affecting economic performance. We expect therefore that political stability (POLS) in a host country will positively influence a country’s level of economic growth. Our measure of political stability is taken from the World Bank’s good governance indicators, whereby the POLS variable is assigned a value ranging from −2.5 (poor performance) to 2.5 (excellent performance) with the expectation that a higher value would positively contribute to a country’s level of economic growth.

In addition to the political environment, sound economic policy delivered via economic institutions is required to foster economic growth. Macroeconomic stability is thought to provide confidence in both consumer and supplier markets, and therefore encourage economic transactions. We include the host country inflation rate (INFL) as a measure of economic stability and sound macroeconomic policy, whereby steady and predictable rates of inflation enable long-term planning in relation to consumer purchasing power and firm level profit expectations.

Finally, in relation to the role of institutions and economic policy, empirical evidence broadly shows that in the long-run, countries’ economies which are more open experience higher rates of economic growth (Chang et al., 2009; Freund and Bolaky, 2008; Lee et al., 2004). Trade openness represents the degree to which a country is integrated into the world economy, and reflects the relative ease with which a country enables international trade to take place. Therefore, given that a country’s degree of trade openness is largely driven by government policy, its inclusion as a variable is an assessment of the potential for economic growth via trade liberalisation, whereby the more open an economy and its markets are for trade, the greater the potential for higher levels of economic growth. Indeed, China’s own export led growth success has in large part been achieved due to trade liberalisation over the last four decades. We measure trade openness in terms of total trade as a percentage of GDP (TOPEN).

Control variables

In addition to our independent variables and to reflect the complex nature of the economic growth process we include a number of control variables that we think are likely to influence host country growth based on previous empirical findings and data availability. GDP per capita (GDPPC) as a variable has been widely cited (Buckley et al., 2007; Duanmu and Guney, 2009) to reflect the size and wealth of the host country market. While GDP per capita does not address income inequality, it is indicative of average wealth distribution, potential investor returns, but fundamentally the amount of money available for domestic spending to drive economic growth.

Labour productivity (LPRO) calculated as GDP per person employed for a given country assesses the efficiency of production and output per worker within an economy. Considered a critical factor for all economies labour productivity reflects the interaction between human capital, quality of labour resources and technology. Labour productivity affects a country’s competitiveness in the global economy, whereby an increase in labour productivity should grant an increase in economic growth (Auzina-Emsina, 2014; Korkmaz and Korkmaz, 2017).

To control for host country natural resource endowments (NATR), we use total natural resource rents as a percentage of host country GDP. Limited consensus exists regarding the links between the natural resource endowment of a particular country and its consequent growth. A meta-analysis conducted by Havranek et al. (2016) cited that approximately 40% of empirical studies find a negative link, 40% find no effect and 20% find a positive correlation. Natural resources, however, represent important building blocks for production and hence growth. Indeed, Chinese investment projects are known to actively pursue resource-rich locations to ensure the steady supply of raw materials required to sustain domestic Chinese growth (Ross, 2015; Ross et al., 2019).

The links between infrastructure and economic growth are widely recognised to be important and cover a range of areas including physical infrastructure and telecommunications (Bougheas et al., 2000; Demirham and Masca, 2008; Donaldson, 2018). Good quality infrastructure can be expected to reduce transaction costs, but it also increases the efficiency of operations driving productivity and economic growth. As with many other cross-country studies, and those that specifically or predominantly address developing and emerging market countries, our paper is confronted by the lack of homogenous and complete data across sample countries. Therefore, following a number of other studies (Ross, 2015; Kang et al., 2018) we control for host country infrastructure and telecommunications via mobile cellular subscriptions (INFRA). In the following section, we present our empirical model.

Empirical model

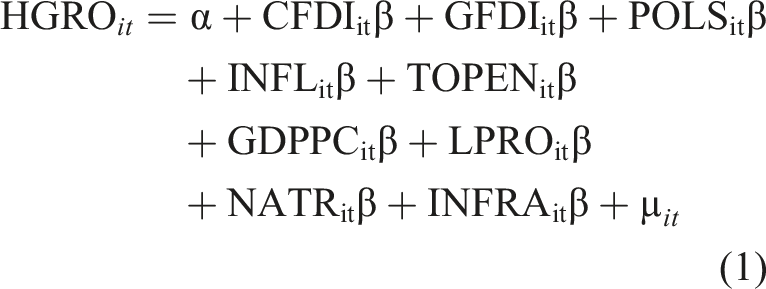

On the basis of our conceptual framework and variables selected a basic Ordinary Least Squares regression (OLS) can be utilised to assess the impact of Chinese outward foreign direct investment on host countries’ economic growth. The OLS model is expressed as

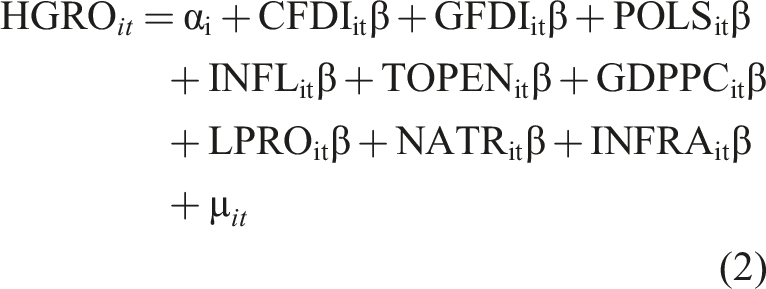

From an empirical specification perspective, when selecting an individual effect model, one must decide between a fixed or random-effect model. Fixed and random-effect models differ in the way the individual specific error component is modelled. In the fixed-effect model, it is assumed to be part of the intercept, while in the random model, it forms part of the error variance. The choice of whether to estimate coefficients using a fixed or random-effect model was made using the Hausman Test, which tests if the u

i

are uncorrelated with the independent variables. In this case, the Hausman test produced a χ2 result of 34.809 indicating we reject the null hypothesis and that it is appropriate to use the fixed-effect model.

3

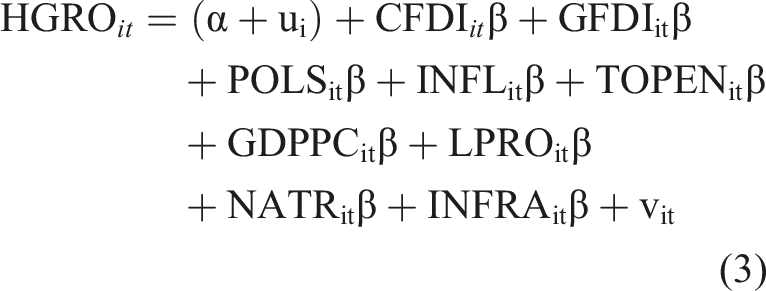

The fixed-effect model can be expressed as

Results and discussion

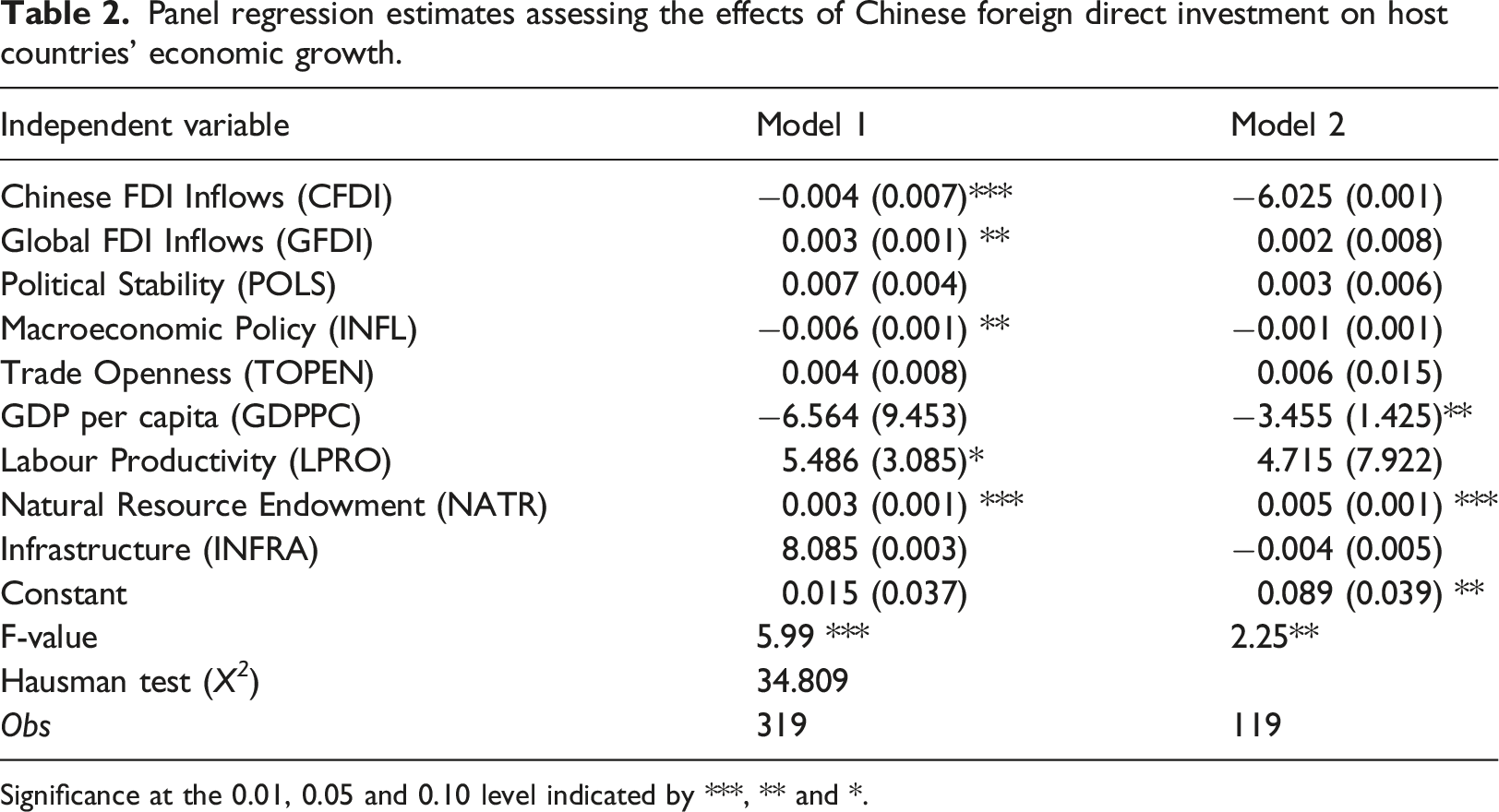

Panel regression estimates assessing the effects of Chinese foreign direct investment on host countries’ economic growth.

Significance at the 0.01, 0.05 and 0.10 level indicated by ***, ** and *.

The empirical results from model 1 highlight as predicted that host countries’ economic growth is positively impacted by both aggregate inflows of FDI (GFDI); and secondly, a robust institutional environment. In particular, the findings indicate that economic institutions that can provide macroeconomic stability (INFL) which reduces the risks associated with economic transactions, and provides confidence for long-term investment exhibit positive effects on economic growth. Additionally, our control variables also demonstrate that while FDI and institutions are important drivers of economic growth there are a range of other significant determinants including host countries’ labour productivity (LPRO) and natural resource abundance (NATR) that can facilitate economic growth.

However, the most revealing result concerns the statistically significant (0.01) negative impact of Chinese foreign direct investment (CFDI) on host countries’ economic growth. Yet, as model 2 highlights, we do not find statistically significant findings to indicate that China’s Belt and Road Initiative (BRI) per se is having a negative effect on host countries’ economic growth. Nevertheless, the contradictory findings between the positive impact yielded by general overall FDI inflows on economic growth, which is consistent with previous studies (Al Nasser, 2010; Borensztein et al., 1998; Hansen & Rand, 2006; Li and Liu, 2005), as opposed to the negative impact of CFDI on host countries’ economic growth raises concerns about the efficacy of CFDI for recipient countries. Consequently, the remainder of this paper will focus on trying to better understand why CFDI appears to exhibit negative effects on host countries’ economic growth, alongside a consideration of the long-term geostrategic implications of CFDI. Indeed, while there is little empirical research to draw on regarding the impacts of CFDI on host countries’ economic growth beyond this paper, there are a number of factors that may potentially explain the negative role of CFDI on host economies’ economic growth.

First, China is not a conventional investor, and as a result does not follow the same investment rules and protocols, as those traditionally associated with private sector firms emanating from predominantly western free market economies. For example, with approximately 80% of CFDI undertaken by SOEs (Du, 2014), CFDI is susceptible to a degree of political influence that is not generally associated with foreign investments emanating from more so-called market-based economies. Where private shareholder owned firms tend to select investment projects to maximise profitability and/or market-share, with metrics of success that are relatively easy to understand, SOEs may hold a wider set of organisational goals, such as geopolitical aims that go beyond financial performance, and therefore are harder to measure in terms of successful outcomes. Indeed, we know that China has invested significantly in strategic transportation and energy infrastructure projects in order to secure its supply lines, and meet domestic resourcing requirements, which may have sub-optimal economic outcomes for both the host country and investor. However, these investments may meet the geopolitical aims and objectives of the project, thus may be considered a success in a way it would not for a private sector business dependent on economic performance. Equally, with many of China’s strategic FDI projects acting as simple transit corridors for supplies, and which are often staffed with imported Chinese labour, few jobs and the associated multiplier effects traditionally associated with FDI packages are being generated in host countries. Such investments may well be in the interests of China, but not necessarily the host country.

Second, while there is evidence to suggest greater internal scrutiny of CFDI projects is now taking place in relation to financial performance (Kynge and Wheatley, 2020; Ross et al., 2019), the executives of Chinese SOE’s are additionally constrained by government directives and political influence. SOE managerial behaviour and career prospects are primarily driven by how well SOE executives comply with governmental directions to meet the goals of the state (Du, 2014). Equally, studies have highlighted that when financial performance and political matters conflict, the executives of Chinese SOEs will select state interests over financial interests and the interests of other non-state stakeholders (Conyon and He, 2008; Yang et al., 2012) such as other countries.

Third, some recipient countries are starting to feel the negative effects of Chinese FDI financing gone wrong; whereby less stringent investment conditions such as those imposed by the IMF, and the lure of initially abundant capital particularly in areas of capital infrastructure is not delivering the economic gains predicted, consequently leaving the host country recipients beholden to their Chinese creditors. This has led some to accuse the Chinese government of conducting ‘debtbook diplomacy’ (Parker and Chefitz, 2018) with debt defaults being used to acquire strategic assets or political influence over debtor nations in return for debt relief.

While Brautigam (2020) challenges the notion of Chinese ‘debt-trap diplomacy’ concerns have been raised about the motives and impacts of CFDI in less developed countries (Du, 2014). The most well documented example of so-called Chinese ‘debtbook diplomacy’ relates to the construction of Hambantota port in Sri Lanka, which on completion failed to generate the economic returns expected leaving the Sri Lankan government unable to repay its debts to China. This led to China’s ‘acquisition’ of Hambantota Port in Sri Lanka on a 99 years lease, as the quid pro quo for the Sri Lankan government’s inability to service its debt repayments to China for the port’s $1.3 billion construction cost. Sri Lanka’s inability to repay its debts was subsequently linked to its weakest economic performance for 16 years and a significant depreciation of the Sri Lankan rupee (Kuronuma, 2018). Of course, one may argue that when debt cannot be repaid, a debtor is beholden to its creditor, and that is no different in relation to CFDI projects. However, the issue in question is that in reality the creditor is ultimately the Chinese state, whereby CFDI potentially acts as Trojan horse with which China can extend its sphere of influence, and in some cases impact the national sovereignty of certain host countries.

Fourth, when writing about the geostrategic implications of the Belt and Road Initiative, Ross (2020) comments on the ability of Chinese SOEs to sustain losses that would be anathema to private companies and its shareholders. Importantly, this highlights the issues of competition in imperfect markets, whereby private investors are unable to justify short to medium-term losses to their shareholders – a calculus that is far less relevant for state-backed geopolitical investors and ultimately gives them a competitive advantage. Indeed, Chinese SOEs benefit from financial and non-financial incentives in the form of government subsidies, privileges and immunities that are not available to the same extent for privately owned competitors (Szamosszegi and Kyle, 2011). Fundamentally, the lack of a level playing field is not fair in the first instance for non-SOE actors; and secondly, from a host country perspective, it is likely to crowd out alternative investors, who may actually provide more effective and efficient FDI, which as our empirical results demonstrate does drive economic growth.

Fifth, in trying to account for the effects of the BRI on host countries’ economic growth, we separately modelled CFDI from the BRI’s inception year in 2013. While our BRI variable is only a proxy measure, reflecting the limited way in which aggregate BRI impacts can be measured, more than 90% of BRI projects have involved Chinese companies, and 97% of funding for the BRI originates from Chinese state banks (HSBC, 2018) which correlates with the exponential growth in CFDI since 2013. Although the negative coefficient was not statistically significant, it nevertheless does not show the BRI having a positive impact on host countries economic growth.

Understandably, while the BRI is viewed with optimism by some, given its potential to deliver investment, jobs, transformational infrastructure projects and general economic development, it is viewed with considerable scepticism by others because of the implications of some countries not being able to meet their debt obligations. As of 2018, OECD data reported that China’s non-performing assets in the BRI have reached $101.8 billion. Moreover, with China’s overseas development lending collapsing from $75bn in 2016 to just $4bn in 2019 (Boston University Global Development Policy Center, 2020) by its two largest overseas lenders – the China Development Bank and the Export-Import Bank of China – whose activities fall under the direct control of China’s state council (Kynge and Wheatley, 2020), this signifies that Beijing is having to rethink the scale and scope of its external lending in order to avoid being at the centre of recipient countries’ looming debt crises and the inevitable hardships this will extoll on host countries.

The BRI promised much in terms of economic outcomes for participant countries, yet in reality many of these positive externalities have failed to materialise or are at least difficult to directly measure. For a conventional economic project and private sector investor, this would signify failure, but the BRI is not a conventional economic project, but rather a geopolitical powerplay. Moreover, as China increasingly utilises and exercises its soft power to embed its ideological perspectives and global reach, the BRI and CFDI more generally brings into sharp focus the global geopolitical implications and outcomes of countries pursuing the Beijing, as opposed to the Washington Consensus.

Conclusion and directions for future research

Utilising a framework underpinned by an institutional – FDI – economic growth lens, this paper is to the best of the authors’ knowledge one of first to investigate the relationship and impact of CFDI on host countries’ economic growth. Our findings specifically highlighted that while general inflows of FDI exhibit a positive impact on host countries’ economies, Chinese foreign direct investment (CFDI) by contrast was found to have a negative impact on host countries’ economic growth. Of course, time series data is never complete and as more data becomes available our model can be tested further and updated if required. Nevertheless, as highlighted in our discussion, the results raise legitimate concerns about the efficacy of CFDI for recipient countries, and the long-term geostrategic implications of CFDI.

From the host country perspective, the results imply that China is not a conventional investor, but rather many of its investments take on a geostrategic dimension, that are not subject to the same economic performance constraints as private firms. Therefore, host countries need to better understand that they may not get the same transfer effects and externalities traditionally associated with conventional FDI. In short, China judges its success by different means, and while some investments may be in the interests of China, they are not necessarily in the economic interests of the host country.

From the Chinese perspective while many western observers and governments have criticised the financial and non-financial support provided by China to its companies, this may be considered somewhat hypocritical in that most embassies and consulates provide soft support for their country’s overseas businesses and potential investors. However, what is different and what countries fear is the scale of China’s support for its companies – it is unparalleled, and for the time being unchecked. Of course, this is not China’s problem, but rather a problem that must be confronted by China’s geopolitical rivals.

Nevertheless, CFDI projects undeniably enable China to extend its economic and geographic spheres of influence irrespective of the questionable economic viability of some projects (Ross, 2022). Consequently, while our paper has advanced our understanding on the impacts that CFDI is having on host country economic growth, with China forecast to become the world’s largest economy in 2028, and as the world’s second largest investor, far more scrutiny needs to be undertaken to better understand the implications of CFDI on host countries’ economies beyond the scope of this paper. Indeed, this paper is a start not an end and while it provides some initial insights far more empirical analysis is required to be undertaken as more detailed data becomes available both at firm and country level. The most straightforward option is to extend the scope of this paper with a larger sample size or to give a specific geographic dimension to the study. However, as encountered in the writing of this paper, it is often difficult, especially in the case of developing countries to find sufficient and complete data over extended time periods in relation to independent variables. Second, given its importance in terms of scale and scope, more studies need to be conducted in relation to the BRI. Related, but separate is the difficulty of how to measure the presence, but particularly the impacts of the BRI – a challenge for this paper and others before it. Third, it is clear that the conventional theories of international business are not sufficient to explain the Chinese model of investment. In particular, current theory is unable to explain and account for the role of SOEs, in that some, if not all of an SOE’s objectives may be of a non-economic nature. That is, their objectives may be entirely geopolitical or geostrategic in nature. The consideration of an SOE theoretical lens is important because many of the up-and-coming future economic powerhouses appear to have similarly high levels of state intervention as China.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Selecting a fixed-effect or random-effect model.

In the fixed-effect model, the individual effect is captured by the intercept term α

i

, which means that every individual country has their own intercept and that the individual effect varies across groups. Thus, the fixed-effect model can be expressed as

where in the fixed-effect model, µ

i

are assumed to be fixed parameters to be estimated, ν

it

is the remaining stochastic disturbance, which is assumed to be independent and identically distributed IID (0

where the only difference µ

i

is now part of the error term and not the intercept. Therefore, the random-effects model meets all of the same assumptions as the fixed-effects model plus the additional requirement that the individual effect µ

i

is uncorrelated with the regressors in all time periods. Therefore, ν

it

are independent random variables with