Abstract

This paper examines how far patterns of external ownership affect benefits from industry geographical proximity. The case explores investments in energy and electricity supply in Wales. Geographically related benefits are examined through a Smart Specialisation lens, in the areas of innovation; firm-to-firm interaction; the labour market and public sector intervention. We find evidence that the ownership model or ‘home location’ of key firms is an important factor driving local economic benefits, and explore related policy implications. The case shows that the location of ownership is a key factor in firm innovative behaviour, and that the scale and nature of any benefits from industry geographical proximity will be dependent on where key decision centres lay. In spite of Wales’ comparative advantage in energy, the paper reveals no dynamic ‘melt’ of interactive and engaged firms and labour, but a functionally narrow, low value economic landscape. This leads to a request for more focus on the ownership and contextual factors that may drive the benefits of industrial proximity for places.

Introduction

Ownership, and specifically the location of ownership, could be an important factor in explaining the extent of geographical (and indeed a-spatial) proximity benefits accruing to firms and in understanding whether such benefits translate to improved regional performance. For example, patterns of ownership and ‘allegiance’ of capital have been shown to be important in debates around the regional economic benefits of externally owned capital (Phelps and Fuller, 2000: Phelps, 2009, and see also early work by Firn, 1975). Externally owned plants (and here we focus on ownership of capital outside of the region – see later) and firms in peripheral regions are known to behave differently from those domestically owned in their use (and payment) of labour, development of supply chain and other relationships and in the location and orientation of their innovative processes (McNabb and Munday, 2017). Also important might be the uses to which economic surpluses are put, in terms of taxation, re-investment or disbursement to firm owners, and importantly, whether the ultimate destination of such surpluses is ‘local’, or involves distribution or ‘repatriation’ to a non-local entity.

This paper discusses how far defined patterns of external ownership affect the benefits from industry geographical proximity. The case examined involves investments in energy and electricity supply in Wales. Wales has rich advantages in terms of access to wind and marine renewable resources and has recently seen strong increases in energy supply linked to renewables. Moreover, Wales as a region has seen considerable success in the attraction of inward investment (McNabb and Munday, 2017), but with virtually no consideration of inward investments in energy-related sectors, which in terms of capital investment are significant when compared to inward investment in manufacturing sectors. We consider how far the cluster of energy developments creates benefits from the concentration of related activity in the region, and then how far such benefits might translate to improved regional economic performance. We consider geographically related benefits through a Smart Specialisation lens in the areas of innovation; firm-to-firm interaction; the labour market and public sector intervention, and in each case seek to uncover whether the ownership model or ‘home location’ of key firms, organisations and institutions (both development and regulatory) are a factor in driving the nature of behaviours and local economic benefits. The paper contributes further through revealing that issues of ownership (and infrastructure) have been neglected somewhat in work around Smart Specialisation.

The next section outlines the connections between regional development policy, Smart Specialisation and capital ownership. This leads to an argument on why ownership might influence within-region innovation and other behaviours important for regional economic development prospects. The third section provides background and justification for the Welsh case focusing on the regional economic context and energy-related investment. The fourth describes how far different energy activities (differentiated by technology and ownership model) are oriented towards the development of within-region supply-chain links, knowledge and technology transfer and the development of high-trust relationships. The paper also comments on whether sustained energy investment has positively affected the Welsh labour market. The fifth section contextualises these findings within the wider debate around a Smart Specialisation approach in regions. The final section concludes and considers how far recent changes in Welsh policy on renewable energy might address some of the issues covered in the case.

Capital ownership, Smart Specialisation and regional development

The Smart Specialisation framework has evolved from analysis of how productivity is derived in private sector firms. The approach is founded on the recognition that private sector enterprises may be best placed to identify growth opportunities in an economy. Consequently, the process of ‘entrepreneurial discovery’ in the private sector might serve to inform public policies for innovation. The Smart Specialisation approach also argues that innovating entrepreneurial businesses should work closely with higher education institutions, state policy makers and delivery partners such that new investments are embedded in places to maximise local economic potential, but at the same time link to international trade flows, international ideas and investment finance.

Smart Specialisation has gained a central importance in European Union regional economic policy debates (McCann, 2015; McCann and Ortega-Argilés, 2015) with its focus on the ability of the private sector to evolve growth opportunities, and on the hope that the innovative processes adopted by leading firms might be replicated in state innovation policy, and in both private and public sector investments better reflecting regional economic potential and then improve trade, knowledge flows and economic growth.

The concept is held to move beyond former cluster and other policy as its ‘smartness’ lies in the ‘entrepreneurial discovery’ of relevant key sectors, activities and competencies by knowledgeable actors from across the civic and private spectrum, with this reducing the chances of policy effort being wasted on activities where there are no true regional comparative advantages (Boschma, 2014). Also, the concept is held to take account of the potential economic evolution and ‘knowledge ecology’ of the context region (McCann and Ortega-Argilés, 2015): thus Smart Specialisation is embedded, not parachuted in. Importantly however, the concept is admitted (in theory at least) to have limited application, being unsuited to large core regions where all activities are likely present, or to small, isolated regions where agglomerative economies are not applicable due to issues of population, economic scale or connectivity (McCann and Ortega-Argilés, 2015).

Proponents accept that the move from what was originally a sectoral theory to a regional and policy tool is problematic (see Baier et al., 2013; McCann and Ortega-Argilés, 2015). One problem with the concept is that it is closely related – at least in the perception of regional stakeholders and indeed some academics – to former or still extant regional development and innovation strategies based on regional comparative advantage, clusters and related variety (Asheim, 2013; Baier et al., 2013). This raises the spectre of regional policymakers simply couching existing policies in a ‘SmartSpec wrapper’ whilst continuing to favour existing regional lobby groups, industries and researchers, rather than undergoing a real process of entrepreneurial discovery. The potential for rent seeking to soften or destroy the benefits of such policies is then strong (Asheim et al., 2011; Pugh, 2014).

Our contention is that if regions are oriented to large, non-locally owned ‘anchor firms’, such rent seeking may have even more severe consequences. This is because evidence for knowledge spillovers and positive innovative impacts from non-domestic firms is weak, or at least mixed (Bishop and Wiseman, 1999). Where smaller states (even in the West) might have a lack of critical mass or absorptive capacity, and where much of their new investment originates outside the economy and is perhaps resource rather than market-seeking, such spillovers may be still more limited (Görg and Greenaway, 2001).

This could be a critical problem for smaller states and more economically peripheral regions. The paucity of a local base of strategic decision-making is a commonly cited issue in the regional economic development literature. Firn (1975) for example, revealed, how in the case of externally owned branch plants, that strategic decisions tended to be made by specialists in the parent organisation. In consequence a region with a significant branch plant presence could lose control to other areas and with an intraregional swap from ‘entrepreneurship’ activity towards ‘management’ activity. Firn noted that this could have longer term developmental implications, and we suggest this would link at very least to characteristics of innovation systems. The factors driving innovation systems have been shown by authors such as Isaksen (2015) and Tödtling and Trippl (2005) to be quite different in regional innovation systems characterised by being organisationally thin or thick. It may be the case that the presence of thin or thick systems tells us something about, or is even in part consequent on, the ultimate ownership of capital in regions. Thin systems might be identified, for example, with branch plant economies where ultimate ownership of facilities even in strong growth sectors rests elsewhere. In cases of organizationally thin research and innovation systems, development might be more based on connections to external expert milieus and imports of new technologies, and with this route providing regional firms with new competences and solutions. In these cases, new development paths are driven by ‘solutions’ successful in other regions. Alternatively, in organizationally thick regional innovation systems development paths might be spurred more by indigenous spin-offs from knowledge institutions working closely with the regional industry base, and with this resulting in more likelihood of extant regional industries diversifying into new areas. Critically here it might be external to the region capital ownership in industry that may contribute to development paths linked to ‘thin’ regional innovation systems, and more dependence on external technology provision. Where capital is locally owned and controlled and firms have a deeper functional base in a region, this would seem to one precondition for more ‘thick’ regional innovation systems.

Indeed, even if inward investors to regions do develop relationships which positively impact regional innovation or lead to labour market and other co-location synergies, it is clear they might do so in ways different to nationally- or regionally domestic firms (Knell and Srholec, 2005). Accounting for such ownership issues would seem to be a key element in understanding the strengths and weaknesses of a Smart Specialisation approach. More generally a paucity of work on ownership and infrastructure in research on Smart Specialisation needs to be addressed.

Case: Energy in the periphery

Here the focus is on the energy and electricity supply sector in Wales. There are a series of reasons why this case is of interest in the context of the above review.

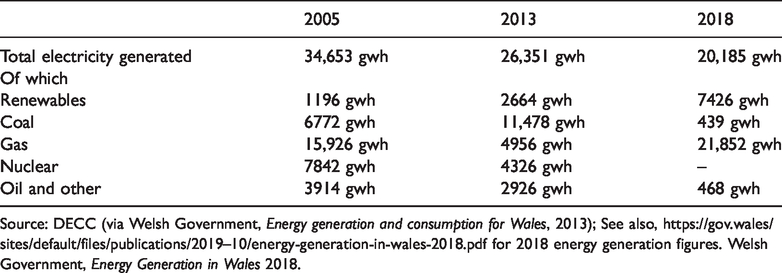

Firstly, Wales has a strong and enduring (properly ‘Ricardian’) comparative advantage in the energy sector (and more broadly in resource extraction and resource processing) as evidenced by the continued exploitation of (surface) coal, tentative exploration for shale gas and the development of a major liquefied natural gas (LNG) terminal at Milford Haven. The region has for many years had significantly more per-capita electricity generation capacity than the UK average (Jones, 2010). It is a test bed for novel energy technologies, and remains a likely home for a new-generation nuclear power station. Table 1 provides some key facts on energy output within the Welsh economy.

Wales energy generation – Key facts.

Source: DECC (via Welsh Government, Energy generation and consumption for Wales, 2013); See also, https://gov.wales/sites/default/files/publications/2019–10/energy-generation-in-wales-2018.pdf for 2018 energy generation figures. Welsh Government, Energy Generation in Wales 2018.

The regional space brings a second benefit for our analysis in terms of the scope of electricity generation. Even where, as for electricity, final products are physically homogeneous, the method of production encompasses a range of techniques analogous to the product cycle cited as important for Smart Specialisation and evolution (Neffke et al., 2011), and with this production having important implications for the cost-competitiveness and market prospects (here of the electricity produced), and hence for the scale and characteristics of the capital employed in its creation, as well as for the behaviour and orientation of relevant actors (International Energy Agency, 2015). Electricity generation technologies employed (commercially or experimentally) in the region include:

fully mature and in terminal decline (coal); mature approaches with continuing innovative aspects (conventional and unconventional gas; hydropower; potentially nuclear – although with planned activity to develop a new nuclear reactor on Anglesey in North Wales stalled at the time of writing); technologies that are globally mature but regionally novel (onshore and offshore wind; Solar PV) Innovative and potentially disruptive technology (in-stream wave and tidal).

This range of technologies and approaches allows us to explore (qualitatively at least) whether the product (or rather plant/capital) cycle has an impact on the nature of proximity and related synergies or weaknesses, and to take a more sophisticated view on how the region sits within (and develops across) the relevant product space (Hidalgo et al., 2007).

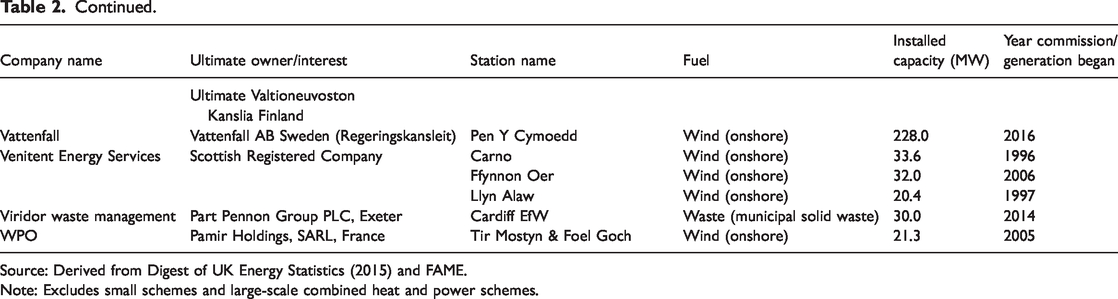

Third, the place of ownership in the regional electricity landscape is important for us. In the Welsh case this landscape (Table 2) is dominated by non-regional, largely multinational capital ownership. In this respect, external ownership here is external to the region and includes rest of UK firms. Table 2 shows that for Wales, large-scale within-region electricity generation is undertaken by large externally incorporated firms, including vertically integrated European energy companies, although identifying ultimate ownership is difficult here. In Table 2 just two of the firms have an identifiable Wales registered office (Calon Energy and Pennant Walters). The firms vary according to whether they actually have a registered office in another part of the UK or overseas. There has been an active debate in Wales (and other UK regions) on the regional economic consequences of external ownership (see most recently McNabb and Munday, 2017; Xu et al., 2019) but limited UK research analysing the specific effects of inward investment in electricity supply. Prior research has examined linkages between inward investment in power generation and economic growth (see, e.g. Khatun and Ahamad, 2015). Therefore in the discussion of the case, it is possible to comment on whether the model and location of ultimate ownership might be an important driver of the benefits arising regionally from location of capacity.

The ‘big’ energy generation landscape in Wales (2019).

Source: Derived from Digest of UK Energy Statistics (2015) and FAME.

Note: Excludes small schemes and large-scale combined heat and power schemes.

Fourth, Wales provides an interesting case due to the underlying consenting framework around energy development. In Wales, direct responsibility for economic development is devolved, but factors shaping the broader economic and regulatory environment are determined by UK government. Under the Wales Act 2017, further powers were devolved to the Welsh Assembly and Welsh Ministers in areas such as transport, energy and the natural environment. We note here that the Assembly had existing powers to legislate in planning but this had until 2017 excluded major energy infrastructure classed as over 50 MW installed capacity (onshore). However, the regional government (following the Wales Act 2017) has consenting powers for energy projects up to 350 MW capacity. This would still exclude powers over major energy infrastructure (such as, e.g. new nuclear capacity). This means that there are some limits in devolved capacity to change the energy mix in Wales within such multi-level governance, and it is important to note that it is the UK Government that is in control of the subsidy regime around electricity production. While, this somewhat restricts the Welsh Government’s room for manoeuvre, it has sought to actively encourage renewables development and encourage more local ownership of electricity generation projects. In this respect, Lesley Griffiths, the Minister for Energy, Environment and Rural Affairs was able to report in 2018 that: ‘We now have 778 MW of renewable energy capacity in local ownership, against our target of 1 GW by 2030. We expect all new energy projects to include an element of local ownership’ (Welsh Government, 2018: 3).

Finally here, Wales is an interesting region because Smart Specialisation has been an important reference point for regional economic policy (Pugh, 2014; McCann and Ortega-Argilés, 2015). The Welsh Government was notionally a wholehearted and early adopter of the ‘SmartSpec’ approach (see Welsh Government, 2013). However, Pugh (2014) points out that government policy looks more like an adaptation of existing (notional) clusters and key sectors to a ‘SmartSpec’ world than a ‘clean sheet’ appreciation of current and potential strengths, with the risk that both the nuances and like local success of the policies are at risk. This government orientation is also relevant to our study, as the Welsh Government identified ‘key’ sectors, including energy and environment, overlap considerably with sectors dominated by firms that the government has identified as ‘anchor companies’ – understood by Welsh Government as major companies that are deemed important for increasing jobs and growing the economy. Typically these are global or international organisations with headquarters or a ‘significant corporate presence’ in Wales. However, it is largely the latter; in very large measure these are externally owned and controlled (e.g. Tata and Airbus, an exception being Admiral Insurance). The extent to which regional Smart Specialisation policies can be successful in sectors dominated by very large multinationals such as in energy is of interest. We seek here to contribute in terms of the role of external ownership in impacting on successful policy development and outcomes around Smart Specialisation.

In the case, the paper draws upon a series of researches into specific electricity generation technologies, places and facilities and their impacts; and into the regional development potential of novel innovative renewables. We summarise the projects that inform the case in Appendix 1 and firms/institutions involved. We accept some of the material is dated and since the research has occurred, the energy mix has continued to change in the UK and Wales, and the subsidy regime has also evolved (Table 1 reveals the near term evolution in the electricity production mix in Wales). However, while the energy mix has evolved patterns of external ownership of major electricity generation capacity in Wales have been more stable. This is the context for a recent Welsh Government focus on working towards higher levels of local ownership in new projects (Welsh Government, 2018).

Critically we are able, for this broad sector and in this region at least, to illuminate some of the actual processes and pathways along which synergies and positive (or negative) externalities might arise for related activities and industries (Puga, 2010). Our results are also comparable across technologies at different stages of development, which share a broad regulatory context but with important differences. We can then assess how far different sorts of geographical proximity might vary in importance for very specific activities, directly addressing the heterogeneity concerns of Bishop and Gripaios (2010).

Clearly there are limitations associated with a case study approach, and with the case formed from different elements of project research (summarised in Appendix 1) taking place at different times, and with some of the referenced work involving survey information from developers, and some not. In addition, our underlying project work was both ex post and ex ante, referring to projects and developments that are completed and operational; in construction or planning; or not yet begun. Our assessment of geographical proximity effects (and of production approaches and economic relationships more generally) is therefore made at different developmental stages: for some activities (notably marine renewables) they are the best estimates of participants and of the research team, supplemented where appropriate by evidence from elsewhere.

Case: The energy sector in Wales

Supply chain linkages

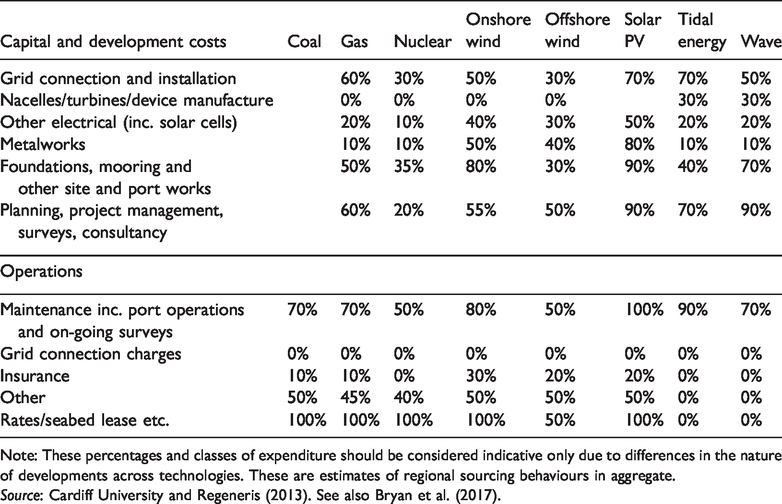

Firstly, for energy, the relative economic importance of both external supply chains and the development and construction phases is notable. Importantly, high value, manufacturing-linked capital spending is outside the region, and in many cases outside of the UK. Table 3 summarises the estimated regional purchasing propensities of selected technologies. For many categories of goods and services there is simply no supply capacity in Wales. Indeed where there is potential to source locally, the opportunity is often lost because externally owned developers and managing contractors have dedicated supply chains formed over many years.

Local sourcing propensities under different technologies.

Note: These percentages and classes of expenditure should be considered indicative only due to differences in the nature of developments across technologies. These are estimates of regional sourcing behaviours in aggregate.

Source: Cardiff University and Regeneris (2013). See also Bryan et al. (2017).

Turbines and related components are typically the highest value element in development spend. The case of on-shore wind is indicative. The average spend per Megawatt (MW) of installed capacity in Wales during the development and construction phase was around £1.25 m (£2012) (Regeneris and Cardiff University, 2013a). However, regional purchases averaged around £0.4 m per installed MW. This pattern is repeated in other technologies mentioned in Table 3. This reflects a limited supply side, the significance of scale economies in some parts of the dedicated manufacturing sector, but also reflects patterns of ownership in managing contractors and developers.

In many of the technologies embraced in Table 3 much of the life cycle spending is focused in the development and construction phase as opposed to the operational stage. This leads to labour market consequences considered later. It is during operational phases when the complex within-region relationships are developed between firms, their commercial partners, the public sector and indeed regional residents. For many private and third sector developers, the operational phase of the energy development (usually conceptualised and financially planned according to the length of the relevant subsidy) would imply a significantly reduced level of local staffing and interest. For established technologies and both large and small developers, both private and otherwise, once the turbines were erected (on land, in buildings, in rivers or at sea) they were effectively static and unalterable capital for the period of the relevant subsidy and interest moved to the next project, inside the region or outside.

Again on-shore wind is a good case. It was revealed above that the estimated capital spend per MW installed on-shore wind in Wales was around £1.25 m. This compared to £30,000 per annum per MW installed during operations and maintenance (a period lasting 20–25 years). This ratio of operational and maintenance costs to development and construction varies, and with some technologies such as biomass and coal requiring more material handling during operations. However, with renewables the differences are noticeable with technologies such as wind and solar supporting little economic activity in the region once installed. This pattern is also evident in newer evolving technologies. For example, tidal stream and wave technologies capital costs during development and construction were estimated between £4.2 and £5.0 m per installed MW of capacity and with operational costs of between £165,000 and 175,000 per annum per MW installed (see Regeneris and Cardiff University, 2013b). Local purchasing propensities of energy projects in Wales tend to be higher during operational phases (excluding any repowering) but then the sums of money involved are far smaller. The conclusions above might be different in emerging technologies around smaller scale development such as micro-hydro schemes where there is a greater propensity to source items such as turbines locally (see Bere et al., 2017).

The overarching production reality means that whilst Wales features a number of shared suppliers and input sources these were typically outside the energy industry per se, relating to specialised professional services in planning, environmental surveys, law and lobbying; in haulage and in construction services. The region is significantly lacking in large ‘Tier 1’ construction contractors, and a number of such companies serviced a number of energy developments. Interestingly several developers, across private and third sectors, claimed to prioritise local suppliers over sometimes-cheaper non-regional alternatives, and with an explicit local economic development rationale. Such behaviours were less evident among larger and multinational developers, although in all cases developers emphasised their desire to purchase locally where possible – and indeed to convince local companies of the opportunities on offer in supplying to (especially) on-shore wind. Almost all such supplier development related to construction phases, with modest operational requirements being met in-house or rolled into warrantied support obtained from non-local turbine manufacturers.

There was very little opportunity with mature technologies such as gas and wind power for regional input into any innovative product or technological development, with these occurring outside the region (and usually outside the UK) either inside or outside relevant firms. Would-be developers of more novel technologies emphasised the potential for regional partnerships, although this was couched largely in terms of research partnerships with higher education, or joint lobbying for infrastructure improvements (e.g. access to the electricity grid).

In summary then, whilst a number of shared input suppliers were evident, these relationships were restricted to time-limited development, rather than operational phases. The development of a regional ‘supply side’ would then occur largely outside the identified energy industry and reliant on an ongoing stream of new projects.

Labour market effects – In debates around the advantages of Smart Specialisation, the existence of explicit and also more subtle labour market effects are important. In the case explored in this paper labour market effects are moderated by the relatively small numbers of people directly involved in the electricity supply sector during operations. For example, the Business Register and Employment Survey from the ONS revealed that employment in the whole electricity production, distribution and transmission sector in Wales was around 4500–5000 people in the period 2016–2018, with the numbers in electricity production varying between an estimated 1000–1500. Then in considering the labour market context the following points are relevant.

First over the life cycle of electricity generation projects in Wales, much of the employment effect occurs during development and construction. Gas generation provides a good example. It is estimated that around 2000 person-years of Welsh employment were connected to the development of a 500 MW installed capacity gas-fired power station in Wales; this compared to 0.3 full time equivalents (FTEs) per annum per installed MW during the operational phase (around 150 Welsh jobs per annum – see Cardiff University and Regeneris, 2013). Indeed for seven different electricity generation technologies (excluding coal and biomass) Welsh employment supported per MW installed during operational phases varied between an estimated 0.3 FTEs per annum per MW installed (gas) to an expected 0.9 FTEs per MW installed in connection with emerging tidal stream technologies.

Second, regional skills spillovers during development and construction (i.e. in some areas of planning and development, and in civil engineering) are limited because construction is led by transient managing contractors and labour forces, and specialist teams with no enduring regional base. New electricity generating capacity potentially creates new demands for particular skill sets at a local level and this has certainly been one of the desires of Welsh Government in terms of renewables development. However, the scale and nature of this demand, and how these needs are met by local workers, are not straightforward.

Factors that influence the need for labour and skills in development and construction phases and the scope to source these from the local labour market include on the demand side: the scale, nature and duration of the development, including how specialist are the construction and manufacturing inputs; the extent to which manufacturing, construction and assembly occurs on- or off-site (and typically with high value components produced off-site); the nature of procurement processes, including the origin of the managing contractors and key sub-contractors (and these are often external). Sitting alongside demand are supply side factors including: the character of the local economy of the development site; the associated labour market; how far developers and managing contractors, and then operators, local agencies and colleges seek to engage with the local supply chain and local workforce.

The above demand and supply side factors noted, the more subtle labour market effects (and new skills development and educational provision) are heavily shaped by the size, duration, location and ownership of the scheme. Larger schemes (e.g. the construction of the RWEnpower gas-fired power station in Pembrokeshire in 2012) require more labour input on or close to the construction site. Likewise, in practice it is typical in the Welsh case for much of the on-site employment during construction to be filled by workers from other parts of the UK or Europe. The origin of the contractors and the nature of the work mean that there can be limited opportunities to recruit locally, even if the skills are available locally. Whilst Wales undoubtedly has strength in some aspects of the supply chain, these firms are often not located geographically close to new developments.

There are commonalities between factors influencing the ability to source workers and skills locally during development and construction and then in the operations and maintenance phases of electricity generation projects. In Wales, there has been interest in developing employment in the electricity generation sector and with this partly linked to its general high skill content, and then relatively high earnings. For example, Cardiff University and Regeneris (2013) found that average remuneration across 12 power stations in Wales varied between £42,000 and £63,000 in 2012, well above regional average pay at that time. It also confirmed that the power industry employs relatively more professional, associate professionals, skilled trades and sales and customer service occupations, and that around 27% of all energy and utilities jobs in Wales are occupied by workers with NVQ 4+ qualifications (i.e. degree level or higher).

There have been some developments in Wales to improve the supply of skills to power station operators. For example, in the case of onshore wind, North Wales’ Coleg Llandrillo’s marine and built environment centre has a new wind turbine training centre. The college has also collaborated with RWE npower and Vattenfall (a wind developer) to design apprenticeship programmes linked to wind energy and ISOFab, a mechanical engineering contractor, and Vattenfall delivered a 3-year apprenticeship scheme training four apprentices as wind turbine technicians for Pen y Cymoedd wind farm near Neath. In Wales, EU Skills (working with RenewableUK) also developed a bespoke Modern Apprenticeship in Wind Turbine Operations and Maintenance.

Innovative knowledge transfer – The above-noted focus on the planning and construction phase of energy developments was influential in the type, strengths and duration of relationships developed within the region by energy companies and energy-interested communities. Energy industry stakeholders in Wales have been shown to have a strong interest, and often shared involvement, in developing a more positive ‘institutional context’ for renewables in particular, i.e. in government lobbying and joint conferences. Such activities typically excluded fossil and nuclear developers (multinationals with cross-technology interests were represented by their renewables arms). This interesting sector division was somewhat related to the evolving subsidy contexts, but much more related to the (moral) value systems of non-commercial stakeholders, and the support of the regional government that was strongly focussed on renewables development to address climate targets (Welsh Government, 2012, 2018).

This shared lobbying and network development – social rather than technological innovation perhaps – appears by far the most notable cross-organisation activity. The region was host to a very narrow range of ‘resource-seeking’ activity and, for most multinational actors, limited organisational scope. There were few clear instances of technology transfer, shared learning or cluster-type developments with the sector characterised by the application of well understood technology, largely by non-regionally located developers with limited embeddedness. Indeed, there is a common practice by some developers of furthering projects solely to obtain planning permission and/or a guaranteed long-term generation subsidy before selling the facility to financial funds as a portfolio investment, with clear and negative implications for the kinds of relationships developed within the region.

An exception was that of small and especially community-owned in-stream hydropower, where a number of developers, operators and supporting companies join with communities across a range of projects to improve success rates and to exchange learning. As well as the purposeful development of within region supply chains, this sub-sector reveals instances of cross subsidisation between different actors to address cash flow and investment bottlenecks, including the provision of soft loans between organisations. For not-for-profits, technology mattered less – as long as it was renewable – with lessons learned by (e.g.) Solar PV installation applicable and communicated to hydro and wind developers and vice versa. Not for profit energy development was very small in scale however (certainly less than 1% of commercial renewables in terms of MW installed) and involving only a few dozens of people and organisations: it is not clear whether such behaviours are ‘scalable’ or would emerge in a fully commercial context.

Extra-regional relationships and commercial drivers – Debates around the regional economic development benefits of inward investment are cognizant of the national and international supply and competitive contexts within which firms operate. The evidence from the energy sector in Wales is that extra-regional relationships are dominant in driving firms’ behaviours, and that this has consequences for the importance and development of local relationships and opportunities. Most large energy developers are not regionally (or even UK owned – see also Table 2) and place few higher order occupations within the region, whilst devolving a low level of autonomy to Wales).

Also importantly, enabling price support for electricity has been a non-devolved (i.e. UK Government) responsibility. This means UK Government was the sole arbiter of the viability of renewable developments, and the incentive to engage with the regional public sector was lessened (for small and community, as well as large commercial developers) – although planning issues required ongoing and often fraught dialogue and negotiation. The dominance of national aspects was clear across the energy supply landscape. For example, decisions on new nuclear development (at Wylfa on Anglesey, and with this currently on hold) were made wholly outside the region – in terms of investment and financing, enabling electrical grid upgrades and planning permissions. This is not to say of course that the support of local communities is not important, or that local supply chain opportunities will not arise, but the regional position, economically and politically, is still a largely ‘passive’ one.

The above elements suggest that whilst geographic proximity has some benefits in the energy sector in Wales, that these are limited by both the ownership of key developers and operators, and by the investment and political context within which UK energy operates. While energy is a very particular economic sector in its investment activity, it shares several characteristics and outcomes with other within-region utility, manufacturing and service activities. Such elements could have strong implications for the effectiveness of Smart Specialisation and ‘allied’ policies in poorer, peripheral regions elsewhere.

Discussion

Studies seek to establish the existence and nature of geographic externalities for firms under different banners. This study of one industry, taking many forms in one region, suggests such externalities exist, but may be strongly mediated by forces and structures that have attracted limited attention. These factors are important in policy design at regional level.

First the case reveals that the location of ownership as an important factor in firm innovative behaviour. Multinational energy companies (whether UK or overseas based) concentrate innovative and R&D behaviours in select locations often unconnected to where their capital is actually employed, and access (and purchase) enabling technology at a continental scale. This may severely limit the innovative ‘space’ in regions, populations or networks where multinationals are important economic actors. Ownership has other implications. Here this included a functionally and temporally limited interest in the case region, with negative implications for network development; a (related) lack of autonomy enjoyed by local commercial entities; the prospect of rapid and even frequent changes of ownership; and as a result lessened contact between owners and suppliers, local government and affected communities. Non-local ownership might then impact the location where the benefits of innovation occur. The assumption, explicit or otherwise, in some Smart Specialisation studies is that benefits from geographical proximity transmit to the locality through increased wages, or more competitive and innovative ‘local’ firms. The potential for there to be a differential outcome, with non-local firms capturing the benefit of innovative network behaviour, or in the form of increased returns to capital, and then repatriating these to the firm’s ‘home’ region or shareholders, should not be discounted.

Building upon the above it is suggested, second, that the scale and nature of any benefits from industry geographical proximity will be strongly dependent on where key decision making centres lay. Firms with scarce resources cannot apply equal interest and staff time to relationship management, lobbying and supply chain development in Mid-Wales, Cardiff Bay, London and Brussels for example. In this case (and in common perhaps with other energy intense industries) the local context suffers because key regulatory and subsidy conditions are set nationally. Similarly, where key labour and other inputs can be sourced nationally or internationally and, in both development and operational phases, supplied peripatetically, the role of both the labour and intermediate product markets in communicating knowledge and innovation across the locality at least must be questioned, as must the often-implied framing in studies which assume that workers live and spend where they work.

Third, the type of industry and type of product may matter greatly – a key driver in firm behaviour in the regional energy case was the certain and extended life of employed capital, as well as its low maintenance requirements. With the exception of biomass (and nuclear, somewhat), few new energy developments will require many employees or factor inputs in the operational phase. Once operational, capital in our case was technologically ‘fixed’ for decades by the cost ineffectiveness of renewal before the grandfathered, guaranteed subsidy period is over (usually 20–25 years). In the case of other technologies this is potentially much longer (e.g. contract for difference negotiations for electricity generated by nuclear). Therefore agglomeration or innovative benefits, which do not happen at the start, are unlikely to happen at all.

Fourth, comparative geographic advantage may bring limited economic advantage – as well as types of industry, one must consider types of places. Commentators have already noted the potentially limited application of Smart Specialisation to weaker regions. Wales has, quite rightly from a Smart Specialisation perspective, identified energy and environmental services as a sector of interest, based on a strong geographic resource advantage. This approach ignores the weaknesses in the regional economy that means investment from outside will reinforce Wales’ position as a resource periphery, with products and value expropriated via inward investments (including rest-of-UK) for the gain of richer core regions. The implication here is that the identification of regional specialisms should be tempered (if not driven) by a consideration of key regional cross-industry (and indeed perhaps cross-society) competencies and weaknesses, which will critically affect the development impact of key sectors.

The case then points to a number of factors that fundamentally shape the nature of economic relationships at the regional scale. Despite Wales’ longstanding and immovable comparative advantage in energy, we find not a dynamic ‘melt’ of interactive and engaged firms and labour, but a functionally narrow, low value and, outside of some third sector players, economically uninteresting landscape. This finding has implications for the study of the economic benefits of industry proximity.

In part selected of the problems identified can be connected to emerging policy changes in Wales with explicit targets now set for local ownership in new energy projects (see Energy Generation in Wales, 2018: 12–13). Moreover, in more recent post Brexit planning in Wales for a new regional investment framework, the need for an element of local ownership in new energy projects from 2020 has also been highlighted, such that projects create local economic opportunity in addition to meeting renewable energy targets. This type of policy development is welcome, but we would argue that more still needs to be done in the region to engage communities with opportunities from renewable electricity generation that move beyond simple community benefit packages around projects, and move towards local communities sharing the risks and rewards from shared ownership in larger projects. This is important because our (and other) evidence shows that where local ownership and control of renewables infrastructure is a feature – in this case, mostly in-stream hydropower – wider behavioural changes required for climate transition (in energy use and efficiency, transport etc.) can be driven by both the development of bespoke local infrastructure and education funded by renewables income, and by the very fact of communities becoming climate-aware via deep engagement in the renewables development process (Bere et al., 2017).

Answers to the wider problems elucidated in the case are difficult. We have revealed that external ownership comes with limitations, but then for a small region if capital is not derived from inward investment where is it to come from? Wales as a nation remains very reliant on inward investment from both overseas firms and rest of UK firms. Other important issues here are then how far organisations such as the Welsh Government can work to encourage high levels of local sourcing in electricity production projects, and indeed how far local authorities and Welsh Government take more of a role as direct investors in projects which would provide them with more leverage to promote regional development outcomes from energy investments.

Conclusions

To conclude, there is a continuing focus in policy on the potential for geographic proximity to bring economic and competitive benefits to firms and places. Such concepts are important in developing EU regional development policies that focus on Smart Specialisation. This builds on past and existing approaches that conflate the success of firms with the success of places, and, by implication at least, suggest that proximity brings important economic dividends either directly – for cities and larger urban areas, growth poles or employment sites – or indirectly – for example hinterland and rural regions that benefit from urban demand for rural labour, along supply chains or through other ‘spread’ effects. This policy focus is despite continuing academic debate and uncertainty about the origin, scale and nature of such proximity benefits, and a limited debate on how such benefits might be mediated by contextual factors hitherto considered unimportant.

In the case a strong argument was made that potential proximity benefits will be significantly reduced by a number of factors either rarely considered, or difficult to account for, within place-development policies. Specifically, firm and capital ownership is a key factor. There is much evidence that inward investors are productively and behaviourally different to local firms; often more productive and more innovative. What works, in terms of inward investment interactions and technology transfer, to increase levels of value added and income in more prosperous regions may not work in poorer regions, especially within a context of oligopolistic and geographically specialised firms in a context of inter-regionally mobile labour and internationally mobile capital (in terms of both stock and dividend flow).

Innovation opportunities, in both technological and ‘social’ senses are lumpy, and very product or capital dependent, and the need for a firm focus on product evolution and lifecycles in agglomeration studies is reinforced. The case also suggests that proximity studies may miss important benefits if they cannot properly account (econometrically or otherwise) for the relatedness of activities across the economy – inter-sectorally – with our case finding much more input sharing outside the energy sector – for example, in logistics, professional services and construction – than within.

To summarise there is a call for more focus on the ownership and contextual factors that may drive the benefits or otherwise of industrial proximity for places. In particular, the sorts of conceptual frameworks that make sense for already successful locations might not apply to or explain poor, resource-intense peripheries due to a series of long-standing economic structural factors and weaknesses that indeed explain their current condition. Innovation is a factor of production, as is labour or capital. Conditions may simply not be suitable for its creation in many places. It may be created, in part, by proximity but the benefits may be captured not by local workers, or between companies in Wales, but rather by remote owners of capital. Such possibilities should be more fully considered in both theory and practice.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.