Abstract

Prior literature has identified several outsourcing motivations, such as cost reduction and access to expertise, and deciphered the influence of these variables on outsourcing decisions. In another stream of outsourcing studies, researchers have gauged the degree of outsourcing, unearthing how companies may choose to outsource a set or processes instead of the whole business function. In this article, we draw on both of these streams of outsourcing research to study the relationship between outsourcing motivations and the degree of outsourcing within a particular business function. We probe the effect of nine motivation items on outsourcing decision through an empirical study using survey data gathered from 337 small and medium-sized enterprises. We find that cost reduction, a focus on core competence and business/process improvements are all associated with a higher degree of outsourcing, but interestingly, access to expertise is negatively associated with the degree of outsourcing. This finding suggests that companies that outsource mainly to acquire external expertise outsource only a limited number of processes within a specific business function. Our main theoretical contribution lies in uncovering the dynamic nature of outsourcing motivations, meaning that as companies outsource a larger degree of their business processes, some motivation items become more accentuated and others fade in importance.

Introduction

Business process outsourcing (BPO) is an act of delegation of one or more information-intensive business processes to a third-party provider (Borman, 2006; Luo, Zheng, & Jayaraman, 2010). Companies commonly outsource processes in non-core business functions, such as finance and accounting, call centres and human resources, to third-party service providers for various reasons. The extant literature identifies a plethora of these outsourcing motivations, the most widely cited being access to expertise (Currie, Michell, & Abanishe, 2008; Lam & Chua, 2009), cost reduction (Borman, 2006; Saxena & Bharadwaj, 2009) and scalability (Redondo-Cano & Canet-Giner, 2010). To complement and synthesize these studies, recent reviews of outsourcing literature (Lacity, Khan, & Yan, 2016; Lacity, Khan, Yan, & Willcocks, 2010; Lacity, Solomon, Yan, & Willcocks, 2011) offer a systematic and holistic summary of evidence behind the effects of the most important motivation items on outsourcing decisions. These company-level analyses have improved our understanding of how companies differ in their motivations to outsource business processes.

The BPO market has been growing steadily in recent years, reaching estimated US$322 billion by the end of 2016 (Snowden & Fersht, 2016), as cloud computing and other emerging technologies offer new opportunities to BPO providers to consolidate and grow their business (Singh & Tornbohm, 2016). Developments in the outsourcing market have enabled greater flexibility in designing outsourcing deals. For example, in accounting, cloud computing provides a platform where two parties (a client company and an outsourcing service provider) can jointly access the data and workflow in real time. Endowed with greater transparency and control through, this new breed of accounting information systems (AIS) allows the outsourcers to make outsourcing decisions on a task level instead of outsourcing the whole business function (Asatiani, Apte, Penttinen, Rönkkö, & Saarinen, 2014). For example, in accounting outsourcing, some may outsource a particular payroll-related task (e.g. payroll calculations), while others may choose to outsource the preparation and submission of financial statements.

This emerging complexity and flexibility in outsourcing calls for a revised understanding of outsourcing motivations, which requires us to delve deeper from a company-level analysis into a task-level analysis. Tangential to our research, Dibbern, Chin, and Heinzl (2012) challenged the modular view of outsourcing, where an outsourcing decision on one process is viewed as independent from decisions on other processes. Dibbern and colleagues observed a systemic influence on outsourcing motivations in information systems (IS) outsourcing. We argue that a similar phenomenon can be observed in BPO. While business functions such as accounting may have a modular structure, motivations to outsource a particular process are not independent of the context of other processes. Therefore, we theorize that motivations to outsource particular processes within a business function are related to the degree of outsourcing. Motivated by the recent developments in outsourcing markets and our limited current understanding of the link between outsourcing motivations and the degree of outsourcing, our main research question is as follows:

Research Question What is the relationship between motivations to outsource and the degree of outsourcing?

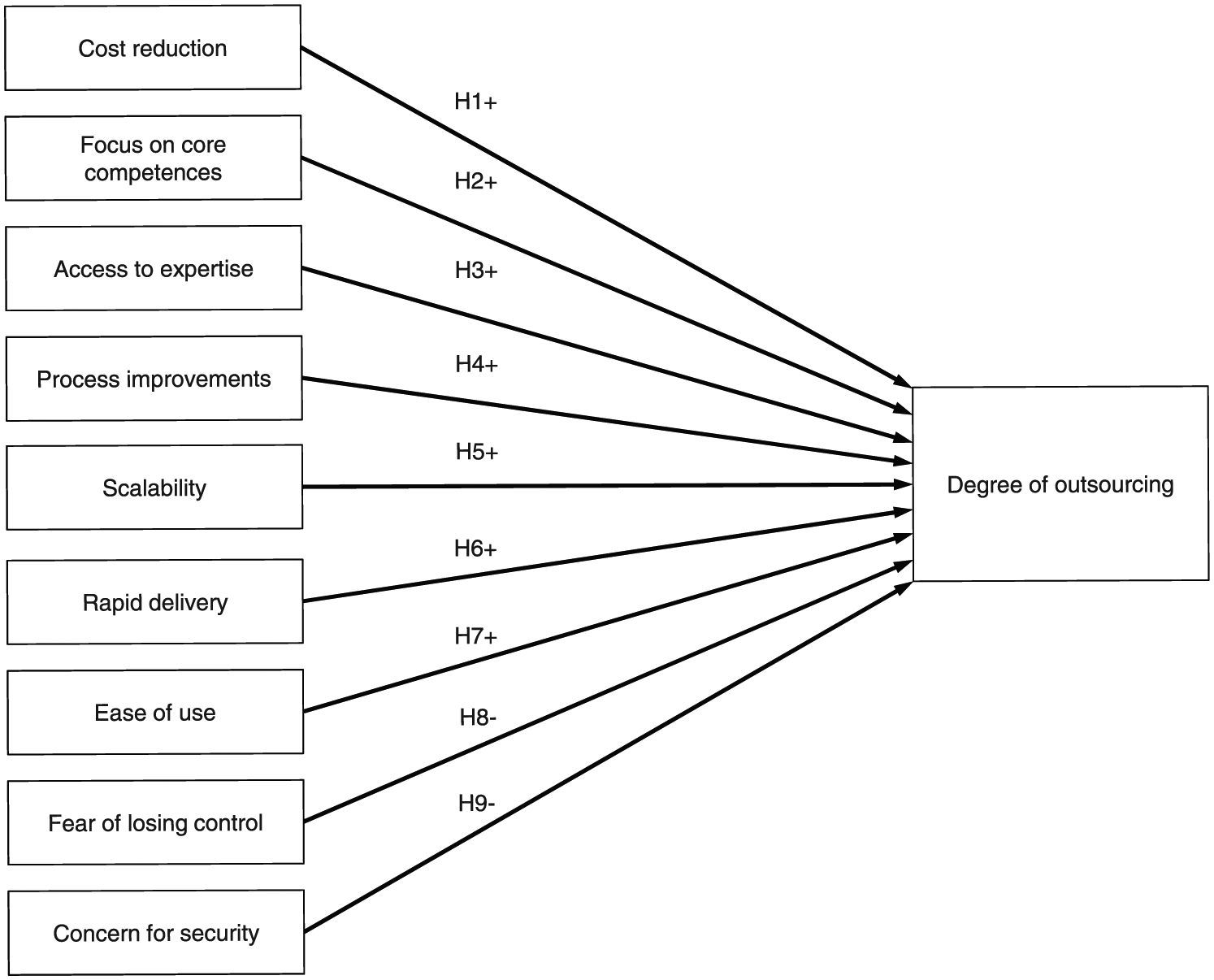

To address this research question, we reviewed the existing literature on outsourcing motivations to build a conceptual model with nine motivation items: cost reduction, focus on core competence, access to expertise, process improvements, scalability, rapid delivery, ease of use, fear of losing control (negative) and concern for security (negative). We collected empirical data on the outsourcing of accounting functions and the outsourcing motivations in 337 Finnish small and medium-sized enterprises (SMEs). Our results show that companies that outsource more tasks seek to focus on core competence, whereas companies that outsource only a limited number of tasks mainly seek external competence and assurance.

The remainder of the article is organized as follows. After this introduction, we proceed with a literature review on outsourcing motivations. In the third section, we build our conceptual framework, which consists of a set of motivation variables and the degree of outsourcing. In the fourth section, we present our empirical study. In the fifth section, we report the aggregate-level findings of our empirical study, and, in the sixth section, the process group-level findings. In the remaining sections, we discuss the findings and avenues for further research.

Review of outsourcing motivations

The outsourcing research has focused on two main areas: the decision to outsource and outsourcing outcomes. The stream of literature on the decision to outsource addresses questions of why outsource (motivations), what to outsource (what type of processes; transaction attributes) and how to outsource (e.g. how much to outsource; how to implement control mechanisms) (Dibbern, Goles, Hirschheim, & Jayatilaka, 2004; Lacity et al., 2011). The stream on outsourcing outcomes has sought to improve our understanding of how outsourcing impacts business performance, which factors contribute to the perceived success of outsourcing arrangements and how outsourcing impacts the quality of the relationships between outsourcing parties (Chou, Techatassanasoontorn, & Hung, 2015; Lee & Kim, 1999).

We focus on outsourcing decisions and, more specifically, on outsourcing motivations (why and what to outsource). The existing literature has identified a plethora of motivations, ranging from cost reduction to business transformation (Mani, Barua, & Whinston, 2010). In a series of articles, Lacity et al. (2010), Lacity et al. (2011) and Lacity et al. (2016) systematically reviewed the body of literature on outsourcing. Lacity et al. (2011) observed a total of 19 main outsourcing motivations used in the literature. However, when the authors analysed the findings on the effect of motivations on the decision to outsource, they found that only a fraction of outsourcing motivations received consistent empirical support (Lacity et al., 2016; Lacity et al., 2011). These motivations were cost reduction, access to skills/expertise, focus on core competence, business process improvements, scalability, rapid delivery and concern for security (negative effect). An exploratory, qualitative pre-study on contextual BPO motivations conducted by the authors of this article largely supports these findings (Asatiani & Penttinen, 2016).

Existing research has analysed BPO motivations in various contexts, focusing on specific industries (e.g. Currie et al., 2008; Lam & Chua, 2009), geographical locations (e.g. Martinez-Noya, Garcia-Canal, & Guillen, 2012) and business processes (e.g. Redondo-Cano & Canet-Giner, 2010). Many of the existing studies treat motivation as a static concept with a straight, linear effect on outsourcing. These studies test the relationship between outsourcing decisions and motivations without considering the degree of outsourcing within a business function. However, other studies tend to view an outsourcing decision as a choice among only three options: selective outsourcing, total outsourcing and total insourcing (e.g. Dahlberg, Nyrhinen, & Santonen, 2006; Lee, Miranda, & Kim, 2004). We believe that such an oversimplification of the outsourcing arrangement prevents us from fully understanding how outsourcers match their motivations with a particular outsourcing configuration.

Among the few studies that address the influence of motivations on the degree of outsourcing, Gewald and Dibbern (2009) studied transaction process outsourcing by banks and compared motivations among organizations that had already outsourced, those that planned to outsource and those that had decided against outsourcing. The authors found that organizations that had already made the decision to outsource portrayed a more balanced recognition of motivations than organizations that had decided against BPO. Closer to the scope of this article, Redondo-Cano and Canet-Giner (2010) studied the outsourcing of R&D activities in the agrochemical industry and measured both the degree of outsourcing and motivations. They observed that in cases of highly outsourced functions, companies were motivated by the lack of resources and production capabilities, whereas in cases of functions with a lower degree of outsourcing, outsourcers were motivated by acquiring and maintaining knowledge that was important to the core of their business while increasing the economic efficiency of non-core components of the function.

Weigelt (2009) studied the relationships among companies’ degree of outsourcing, integrative capabilities and market performance in the context of business process-enhancing technologies. Weigelt’s findings suggest that a greater reliance on outsourcing (high degree of outsourcing in a given function) leads to impediments in integrative capabilities and market performance. In a later study, while evaluating outcomes of outsourcing, Weigelt and Sarkar (2012) observed that companies outsourcing business processes that are reliant on emerging technologies have to make the trade-off between efficiency and adaptability that occurs when the degree of outsourcing increases. The authors concluded that differing objectives (in this case, efficiency and adaptability) require divergent governance structures (Weigelt & Sarkar, 2012), and therefore, the degree of outsourcing should be adjusted according to the objectives of the company. These findings further indicate the need for a deeper understanding of how motivations interact with outsourcing decisions regarding the degree of outsourcing in a particular business function. Although a few studies have investigated the relationship between motivations and various outsourcing configurations (cited above), we note a lack of a comprehensive understanding of how individual motivation variables interact with the degree of outsourcing.

Hypothesis development

To study the relationship between motivations and the degree of outsourcing, we put forward nine hypotheses. We selected a set of motivation variables for our analysis based on the reviews in existing literature and our pre-study (AAsatiani & Penttinen, 2016). We selected motivation variables that have been extensively studied, with empirical results supporting the effects of these motivations on outsourcing decisions. To identify these motivation variables, we consulted the literature reviews on outsourcing (Lacity et al., 2016; Lacity et al., 2010; Lacity et al., 2011). These reviews provide an extensive analysis of the outsourcing motivations research and present a summary of motivations used in the current literature.

The final set of variables included nine motivation items: (1) cost reduction, (2) focus on core competence, (3) access to expertise, (4) process improvements, (5) scalability, (6) rapid delivery, (7) ease of use, (8) fear of losing control (negative) and (9) concern for security (negative). Table 6 in Appendix A presents a summary of the selected outsourcing motivations in comparison with the existing literature and the pre-study.

Cost reduction is one of the most cited and examined motivations for BPO (Lacity et al., 2016). Cost reduction describes the client company’s desire to reduce or control the costs of a business process (Borman, 2006). The rationale behind cost reduction through outsourcing lies in economies of scale (Poppo & Zenger, 1998), where specialized market agents can minimize production costs by developing production capacity and by aggregating demand across several buyers. From this, we can assume that a BPO service provider (a specialized market agent) possesses superior production capabilities for non-core business processes compared with the outsourcer company. Therefore, we argue that companies that are highly motivated by cost reduction will pursue a higher degree of outsourcing. Our first hypothesis, therefore, reads as follows:

Hypothesis 1. A higher level of motivation to reduce costs through BPO leads to a higher degree of outsourcing.

Focus on core competence describes the client company’s desire to outsource non-core tasks in order to focus on the core part of the business (Premuroso, Skantz, & Bhattacharya, 2012). An example of such a non-core task is accounting, which lies outside the core business activities for the majority of companies. Outsourcing such processes allows a company to reallocate freed-up resources to more productive and/or value-generating tasks (Gewald & Dibbern, 2009). In contrast, for a third-party service provider, the outsourced tasks are a part of the core business (e.g. an accounting firm’s core competence is accounting). Thus, the providers possess superior competence needed to complete said tasks. Therefore, we argue that companies seeking to focus on their core business will outsource more business processes:

Hypothesis 2. A higher level of motivation to focus on core competence through BPO leads to a higher degree of outsourcing.

Access to expertise refers to an outsourcer’s desire to access a service provider’s expert knowledge that is not available internally (Lacity et al., 2016). Outsourcing to access expertise is justified when a company lacks internal expertise in a particular area and is unable or unwilling to develop the needed skills in-house (Lam & Chua, 2009). Developing specialized knowledge and assets internally requires considerable investments (Jacobides, 2008). In contrast, BPO service providers are able to provide highly qualified assets (e.g. payroll and tax specialists) by focusing on specialized resources and performing a continuous development of production capacity (Gewald & Dibbern, 2009). Therefore, we posit the following hypothesis:

Hypothesis 3. A higher level of motivation to access expertise through BPO leads to a higher degree of outsourcing.

Process improvements describe the client company’s desire to engage a BPO service provider to improve and develop a business process (Lacity et al., 2011). The motivation to outsource in order to reap process improvements is often associated with the desire to seek efficiency and effectiveness gains (Buco et al., 2004; Gewald & Dibbern, 2009). Arguably, third-party providers are able to better organize the outsourced processes due to asset specialization, extensive experience and economies of scale. Therefore, a higher degree of outsourcing could carry higher potential for efficiency gains (Weigelt & Sarkar, 2012). Based on the above, we propose the following hypothesis:

Hypothesis 4. A higher level of motivation to improve a process through BPO leads to a higher degree of outsourcing.

Scalability describes the outsourcer’s desire to scale up/down a process depending on the demand (Currie et al., 2008; Lacity et al., 2016). Again, due to the economies of scale, BPO providers are able to provide the level of scalability, which outsourcers normally cannot achieve internally. BPO providers possess a large pool of specialized assets that could be allocated to a task on an on-demand basis, whereas client companies would have to invest time and resources in order to scale up the operations of any given business function. In contrast, scaling down involves the costly reallocation and/or downsizing of human resources, which could be a painful process. Therefore, we hypothesize the following:

Hypothesis 5. A higher level of motivation to scale a business process through BPO leads to a higher degree of outsourcing.

Rapid delivery describes the outsourcer’s motivation to speed up the delivery of services by outsourcing its components (Lacity & Willcocks, 2016). As BPO providers can devote greater resources to completing a task, client companies expect faster delivery compared with an in-house arrangement (Bandyopadhyay & Hall, 2009; Freytag, Clarke, & Evald, 2012). Thus, we posit the following hypothesis:

Hypothesis 6. A higher level of motivation to achieve rapid delivery through BPO leads to a higher degree of outsourcing.

Ease of use refers to the outsourcer’s desire to simplify the interaction with a business process and/or its output through, for example, improved customer support or enhanced software. Improving the ease of use of a business process through outsourcing may also decrease the level of frustration associated with that specific business process (Lacity et al., 2016; McKenna & Walker, 2008). It is assumed that, in order to stay competitive, BPO providers are incentivized to focus on delivering superior customer service to their clients. Therefore, outsourcers would expect a better service from external BPO providers compared to their in-house equivalents. We included this motivation factor in our conceptual framework based on our pre-study conducted within the same population of SMEs (AAsatiani & Penttinen, 2016). We hypothesize the following:

Hypothesis 7. A higher level of motivation to achieve ease of use through BPO leads to a higher degree of outsourcing.

In addition to the above-presented motivations for outsourcing, we include two motivation variables that deter outsourcing. Here, our goal is to examine whether these motivations restrict companies from outsourcing a larger number of business processes—in other words, leading to a lower degree of outsourcing.

Fear of losing control describes the concerns that the client company might have regarding maintaining control over the outsourced tasks (Lacity et al., 2016). Transferring control over a number of tasks to a third-party provider has been identified as a significant risk factor that may result in subpar performance and disruption in internal processes of a company (Sanders, Locke, Moore, & Autry, 2007). McKeen and Smith (2011) found that the fear of losing control is an important factor in guiding organizations to choose internally controlled shared service centres over outsourced ones. Moreover, Bhagwatwar, Hackney, and Desouza (2011) observed that the desire to regain control over tasks was one of the major factors contributing to backsourcing. Building on the negative impact of fear of losing control on outsourcing decisions, we thus hypothesize the following:

Hypothesis 8. A higher level of fear of losing control over the business process leads to a lower degree of outsourcing.

Concern for security encompasses the client company’s concerns regarding the privacy and safety of data and/or intellectual property associated with the outsourced tasks (Lacity et al., 2011). Security considerations constitute an important part of the outsourcing decision and contribute to the subsequent success of the outsourcing project (Nassimbeni, Sartor, & Dus, 2012). Concern for security is negatively related to a company’s desire to outsource (McIvor, Humphreys, McKittrick, & Wall, 2009). In their review of the BPO literature, Lacity et al. (2011) proposed, ‘the more concern for security or intellectual property, the less likely a client firm chose outsourcing’. Following this proposal, we posit the following hypothesis :

Hypothesis 9. A higher level of security concerns over the business process leads to a lower degree of outsourcing.

Thus, we hypothesize that the nine motivation variables identified in earlier reviews (Table 6) affect the degree of outsourcing within one business function. Figure 1 presents a summary of our hypotheses.

Summary of hypotheses.

Empirical study

We study BPO in the context of accounting, which is suitable for this research for three reasons. First, in most countries, regardless of the type of business or industry, companies are mandated by law to record their transactions and conduct the associated accounting processes, such as financial and tax reporting. Companies that employ people need to make salary calculations and payments, and again, they need to record those salary payments in their bookkeeping. Thus, every company faces a decision whether to conduct these processes in-house or outsource them to accounting firms. Indeed, outsourcing is a common practice, especially among SMEs (BDO Finland, 2015). This proliferation of accounting outsourcing has led to a well-developed accounting outsourcing market. Second, accounting practices offer a clean, well-defined, documented and standardized environment to study. The boundaries of the processes are well defined, and the outcomes are often standardized (e.g. financial statements or tax reports). The outsourcing decision makers can be clearly defined, and they are able to recognize these processes easily. All the above allow the use of more controllable data collection methods and contribute to the content and face validity of the responses. Third, the accounting function is well suited for modularization as it includes a variety of processes related to sales, purchases, payroll, payments and reporting. The work needed to accomplish these processes can be split between a client company and an accounting firm (BPO provider). In fact, it is common for companies to selectively choose a set of accounting processes to outsource, instead of merely opting for full outsourcing.

The accounting function can be divided into five major parts: sales recording, purchases recording, payroll processing, preparation of interim and annual reports, and payments (Everaert, Sarens, & Rommel, 2007, 2008). We operationalize the accounting function through a set of 22 processes (Table 7, Appendix B) that could potentially be outsourced to an accounting firm. All of these processes fall under one of the five major parts of the accounting function. Practitioners in the accounting industry in Finland use the same (or similar) set of processes to make outsourcing arrangements between a client and an accounting firm. Furthermore, the set of 22 processes is aligned with the standard contract terms between service providers and client companies recommended by The Association of Finnish Accounting Firms. Therefore, the decision makers in companies that have undertaken any degree of accounting outsourcing are familiar with this set of 22 processes.

Data collection

We collected the data in Finland, where accounting outsourcing is a €960 million industry, with almost 4300 service providers on the market (The Association of Finnish Accounting Firms, 2017). There are 356,790 enterprises in Finland, the majority of which are micro-enterprises (89.2%) with less than five employees, and non-micro SMEs (10.6%) with less than 250 employees (Statistics Finland, 2017). The micro-enterprises and SMEs are the major consumers of accounting outsourcing services in Finland. Accounting in Finland is highly regulated and standardized across all industries, yet accounting outsourcing market is highly competitive. The majority of accounting outsourcing contracts operate based on some version of the service agreement (see Table 8 in Appendix B) provided by The Association of Finnish Accounting Firms (2014). Further facilitating outsourcing of accounting processes, there are currently 18 major, distinct AIS on the Finnish market (The Association of Finnish Accounting Firms, 2015).

We collected survey data on SMEs. We refer to the definition set by the European Commission, which states that an SME is a company with no more than 250 employees and an annual turnover of less than €50 million (European Commission, 2003). The study was conducted in cooperation with the Federation of Finnish Enterprises, the largest business federation in Finland, which unites more than 116,000 enterprises (The Federation of Finnish Enterprises, 2016). The Federation focuses particularly on SMEs.

A representative of the Federation distributed the survey questionnaire through email. The email message included a cover letter signed by both the representative of the Federation and the authors of this article, and it contained a web link to the survey instrument. The cover letter included an invitation to participate in the study, a brief explanation of the purpose of the research and a statement regarding the anonymity of the responses. Both the cover letter and the survey questionnaire were written in Finnish by a native speaker (one of the authors) and were reviewed by all three authors and the representative of the Federation.

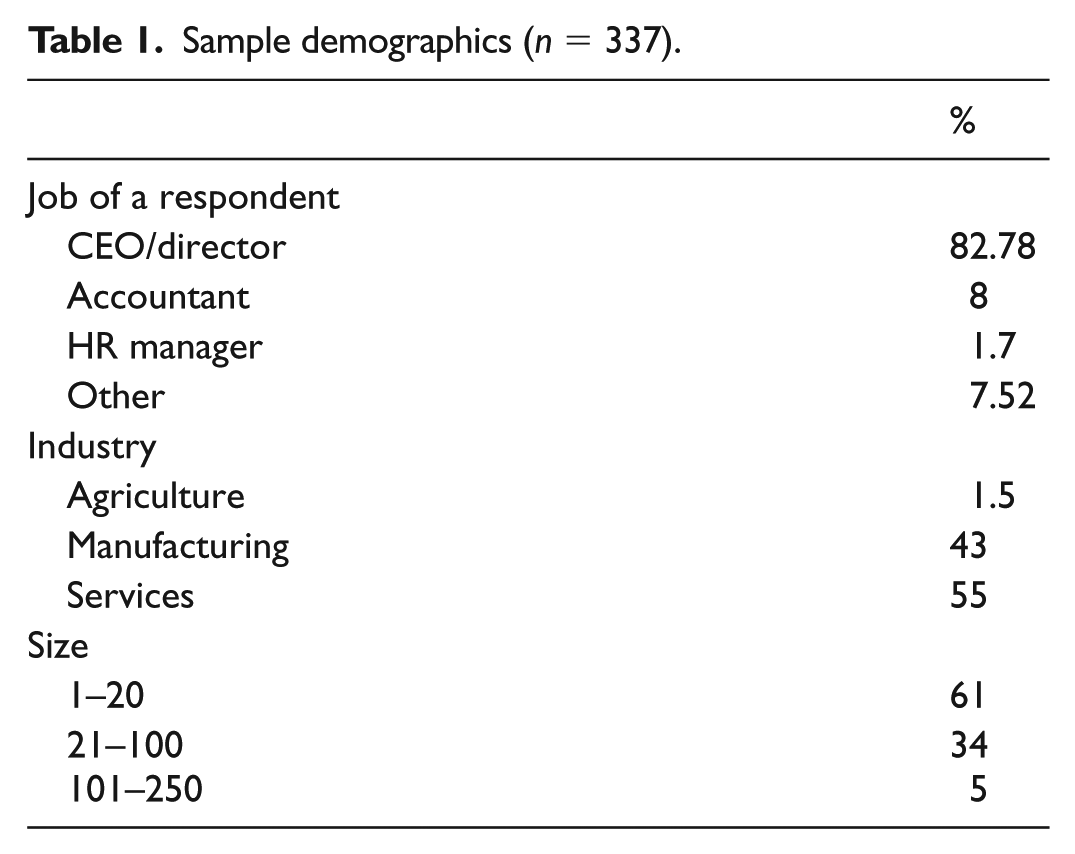

The survey was sent to a random sample of 5000 SMEs selected from the Federation’s member database. The survey was open for 4 weeks. In addition to sending the original invitation to the survey, the representative of the Federation distributed two follow-up messages during this period. In total, 460 complete responses were returned, for a response rate of 9.2%. As we were interested in studying the degree of outsourcing, we excluded companies that did not outsource any of the 22 accounting processes. We also excluded the companies that fell outside of the European Commission’s definition of an SME. The final sample used for our analysis includes 337 responses. Table 1 presents the sample demographics summary.

Sample demographics (n = 337).

The survey included three parts: (1) background questions, collecting the basic information about the SME and the respondent’s role in it; (2) outsourcing questions, enquiring about the accounting outsourcing arrangements of the SME; and (3) outsourcing motivation questions, addressing general and process-specific motivations for outsourcing. The English translation of the survey questions used for this study is provided in Appendix C.

Measures

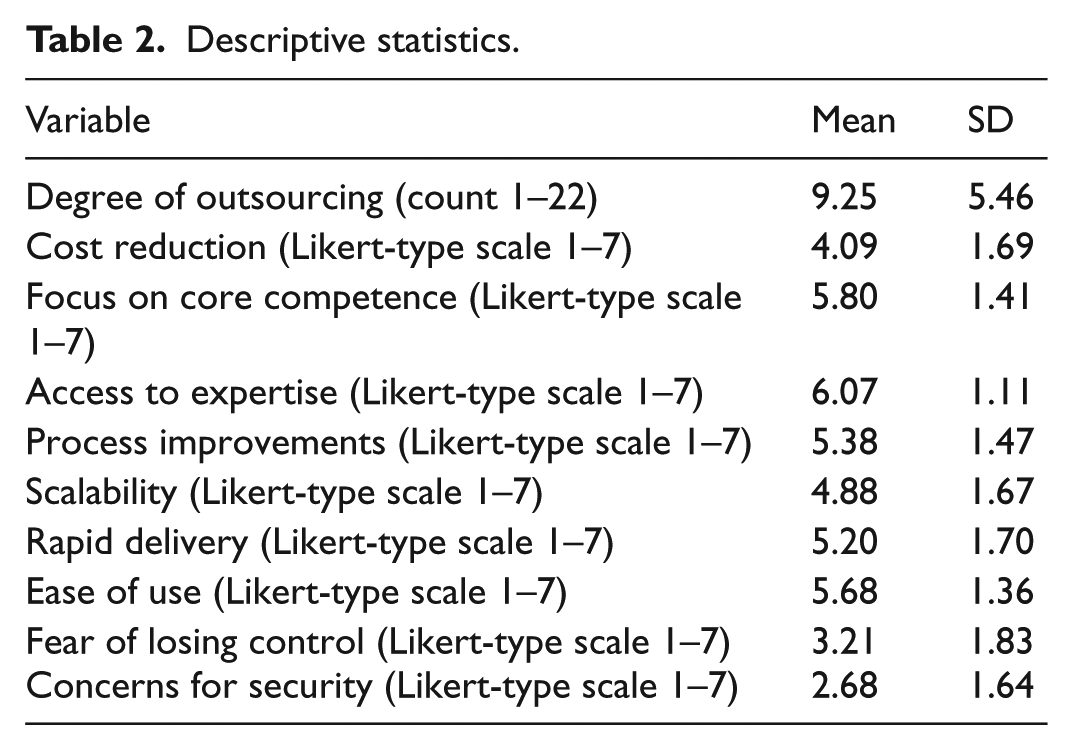

In this study, all motivation variables were measured on a seven-point Likert-type scale ranging from ‘No influence on the outsourcing decision’ to ‘Very strong influence on the outsourcing decision’. The dependent variable, ‘degree of outsourcing’, was derived based on the 22 survey items corresponding to the accounting processes (Table 7) outsourced by a respondent. Therefore, the dependent variable represented the sum of outsourced processes and thus was measured on a scale of 1 to 22. As we are studying the effect of motivations on the degree of outsourcing, measuring the dependent variable based on the count of outsourced processes was justified.

Based on the literature review, we measured nine motivation variables: (1) cost reduction, (2) focus on core competences, (3) access to expertise, (4) process improvements, (5) scalability, (6) rapid delivery, (7) ease of use, (8) fear of losing control and (9) concern for security (Table 2). Correlation coefficients for all model variables are shown in Table 9 in Appendix D. In addition to the main variables, we selected six control variables: (1) use of cloud-based IS for accounting, (2) company size by employees, (3) turnover, (4) age of the company, (5) multinational operations and (6) industry.

Descriptive statistics.

In addition to measuring overall motivations against the degree of outsourcing, we asked the respondents to indicate the most important outsourcing motivation for each process that they had indicated to outsource. This was done through a drop-down menu of the seven positive motivation items.

Findings and analysis—aggregate level

The objective of our research is to study the degree of BPO. Thus, the topic area falls under the study of event frequencies, and a count data analysis is an apt method to analyse such problems (Kauffman, Techatassanasoontorn, & Wang, 2012). We adopt a negative binomial model that allows our dependent variable, degree of outsourcing, to be more dispersed, which is often the case in the SME context.

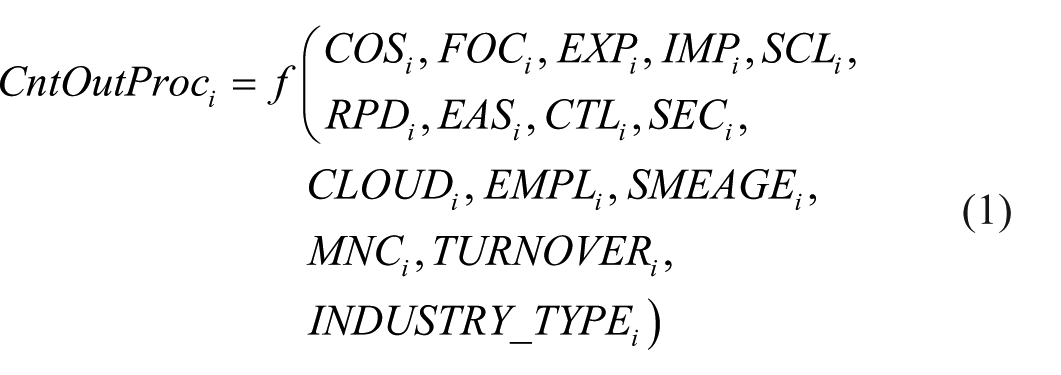

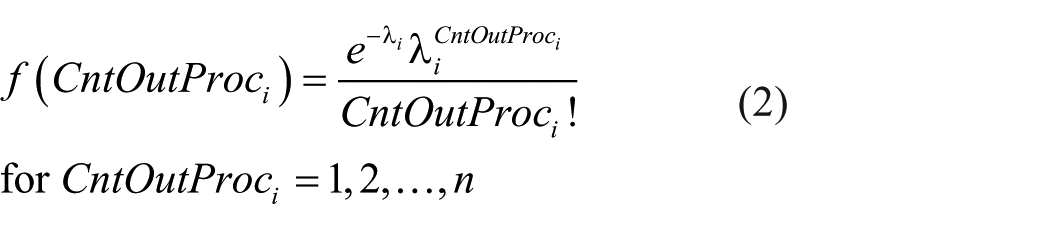

We let CntOutProci be a random variable capturing the count of outsourced processes by the company i. Then, we specify the following functional form, f, to model the number of outsourced processes

where variables COS, FOC, EXP, IMP, SCL, RPD, EAS, CTL and SEC refer to the company’s motivations, namely, cost reduction, focus on core competences, access to expertise, business improvements, scalability, rapid delivery, ease of use, fear of losing control and security concerns, respectively. Variables CLOUD, EMPL, SMEAGE, MNC, TURNOVER and INDUSTRY_TYPE are control variables in the model. CLOUD is a dummy variable for the cloud platform that takes a value of 1 if the company has cloud access and 0 otherwise. EMPL is the total number of employees in the company, SMEAGE captures the age of the company in years, MNC is a dummy for multinational company (which takes a value of 1 if it operates in more than one country and 0 otherwise) and TURNOVER captures the company’s annual turnover. Finally, INDUSTRY_TYPE is a dummy variable for the type of industry. Industry type is divided into three categories, primary, secondary and tertiary, where the primary sector serves as the basis for comparison.

Due to the special nature of our dependent variable, CntOutProc, we cannot apply the ordinary least squares method. Therefore, we view this process as a negative binomial 1 and model it as follows

where

where xi are variables specified in the function in Equation (1), and

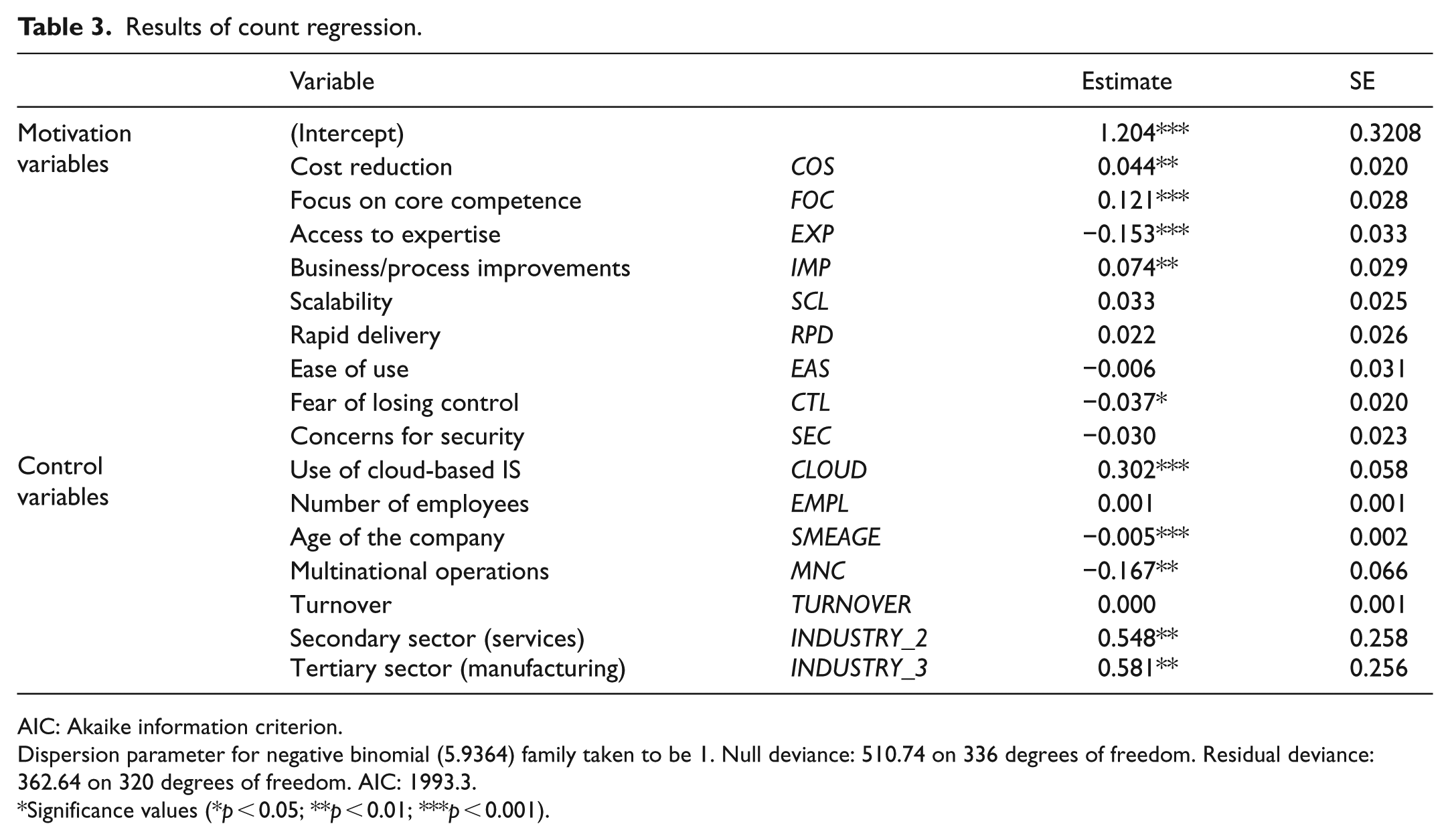

Aggregate-level results

The results of our model are summarized in Table 3. We observe a significant relationship between the degree of outsourcing and five motivation variables (Table 1). We find a significant relationship between motivation to reduce costs and an increase in the degree of outsourcing. Thus, Hypothesis 1 is supported. As expected, a stronger motivation to reduce and control costs leads companies to outsource a larger number of tasks. In line with Hypothesis 2, we observe a strong relationship between companies’ desire to focus on the core business and a higher degree of outsourcing. According to the results, the motivation to focus on core competence appears to be the strongest driver of the degree of outsourcing. We observe a significant positive relationship between process improvement and a higher degree of outsourcing. This result supports Hypothesis 4. We also observe a significant negative relationship between the degree of outsourcing and fear of losing control. Thus, Hypothesis 8 is supported. The factor appears to play a negative role in determining the degree of outsourcing.

Results of count regression.

AIC: Akaike information criterion.

Dispersion parameter for negative binomial (5.9364) family taken to be 1. Null deviance: 510.74 on 336 degrees of freedom. Residual deviance: 362.64 on 320 degrees of freedom. AIC: 1993.3.

Significance values (*p < 0.05; **p < 0.01; ***p < 0.001).

We observe a statistically significant relationship between access to expertise and the degree of outsourcing. However, contrary to our expectations, access to expertise is associated with a lower degree of outsourcing. This means that a stronger desire to access external expertise leads companies to outsource fewer processes. Therefore, Hypothesis 3 is not supported. This is a surprising and interesting result that warrants further discussion.

Concerning the control variables, we note statistically significant effects of the use of cloud-based IS and the age of the company (negative). A potential explanation for the effect of cloud-based IS could be the fact that cloud-based systems make it easier to disseminate digital information between the outsourcer and the outsourcing service provider. Also, these systems allow the design of optimal arrangements to increase collaboration and transparency by providing a platform in the form of a cloud-based AIS endowing companies with tools to more efficiently (re)allocate the accounting processes between the client company and the accountant. The finding that younger companies seem to outsource a larger degree of processes probably stems from the need to focus on the growth of the business in the nascent phases of the company resulting in a relatively strong need to outsource non-core business processes.

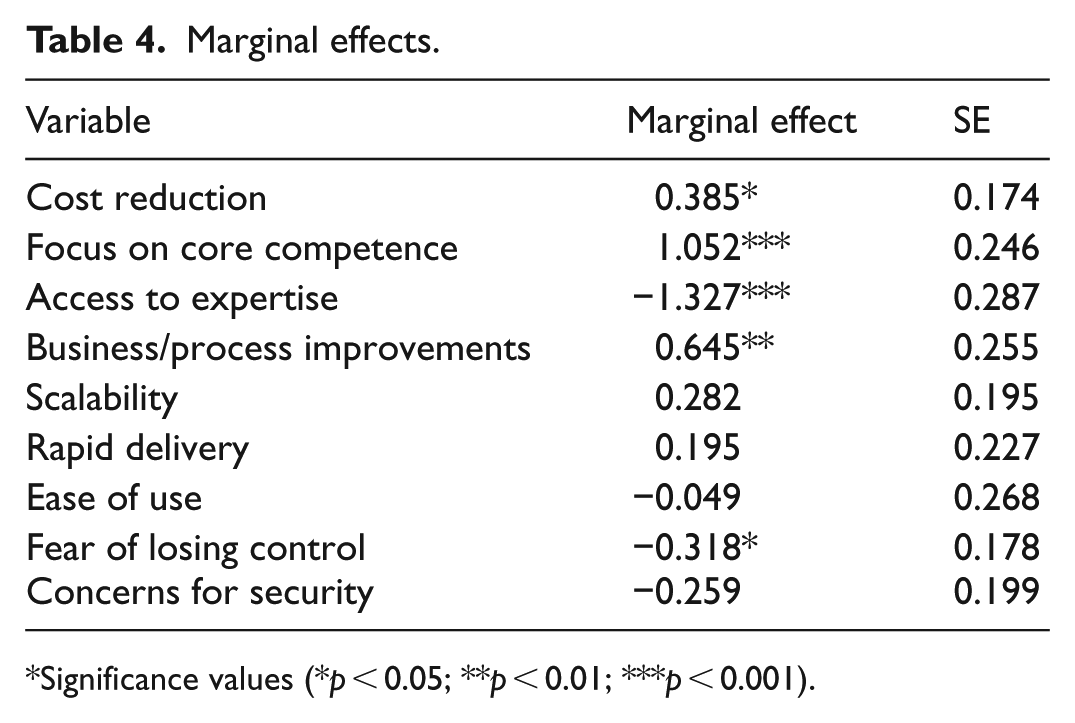

To aid in the interpretation of our results, we conducted additional analysis of marginal effects and visualized its results. We can get a better understanding of the model if we examine the marginal effects of the explanatory variables. The marginal effects analysis calculates the unit change in the predicted number of outsourced processes in response to a unit change in the explanatory variable by holding all other variables at their means. This allows us to gauge the sensitivity of the firms with respect to their motivations to outsource. The results indicate that the firms are more sensitive to motivation variables to focus on core competence and to access expertise (see Table 4). A unit change in a firm’s motivation to focus on core competence leads to the outsourcing of one more process (1.05), whereas a one-unit increase in the motivation to access expertise leads to more than a one-unit decrease in outsourced processes (–1.33). In practical terms, this means that the motivations to focus on core business and access to expertise have a major role in determining the number of outsourced processes.

Marginal effects.

Significance values (*p < 0.05; **p < 0.01; ***p < 0.001).

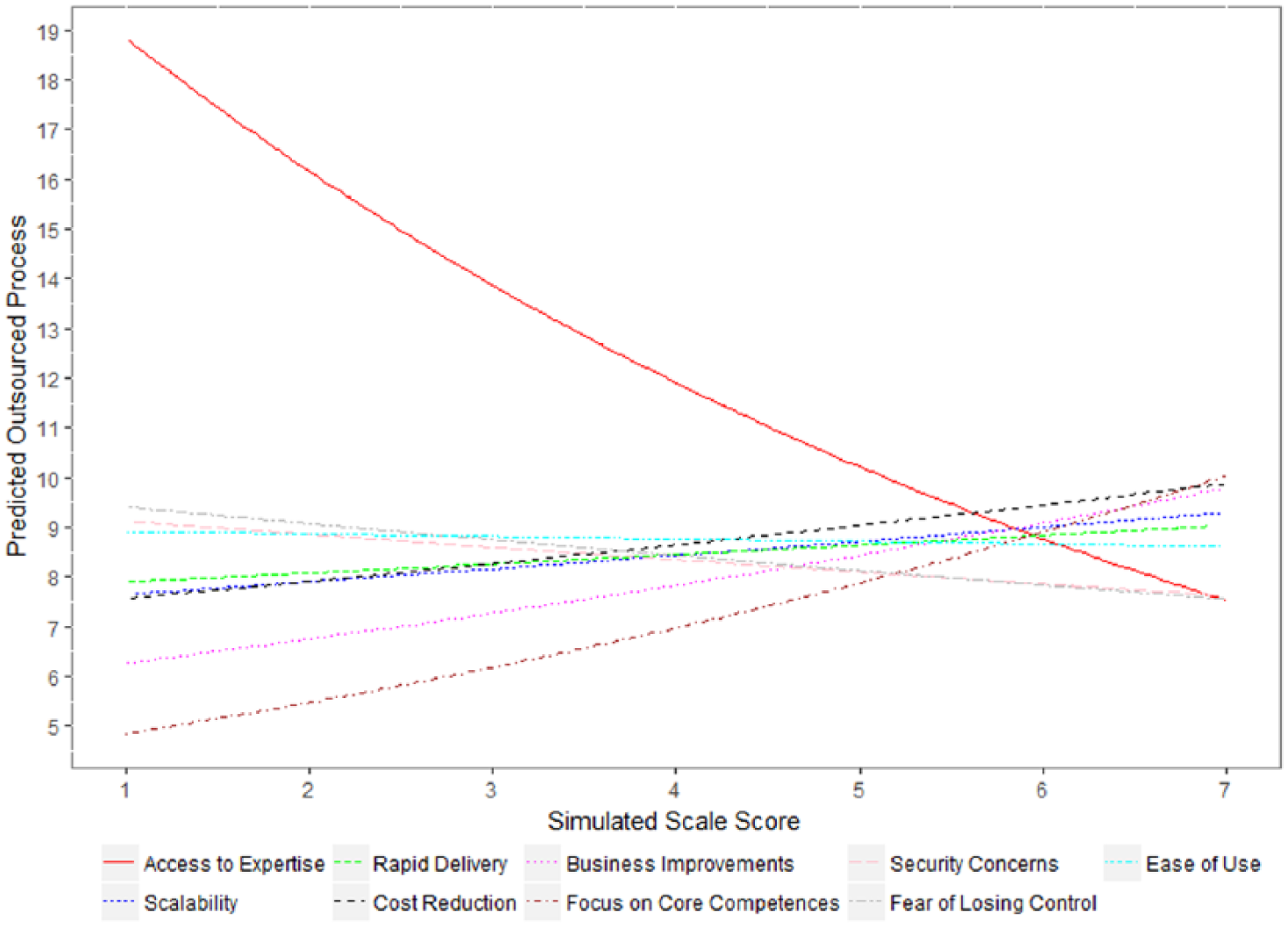

Furthermore, to demonstrate the sensitivity of the variables, we have visualized the results of the regression model using simulation (see Figure 2). The simulation is carried out for each of the motivation variables using parameters of the model from Table 3 by fixing other variables at their mean values. The visualization clearly demonstrates the size of the effect, confirming the conclusions drawn from the marginal effects table (Table 4), discussed above.

Simulated effect size based on the regression model.

Findings and analysis—process group level

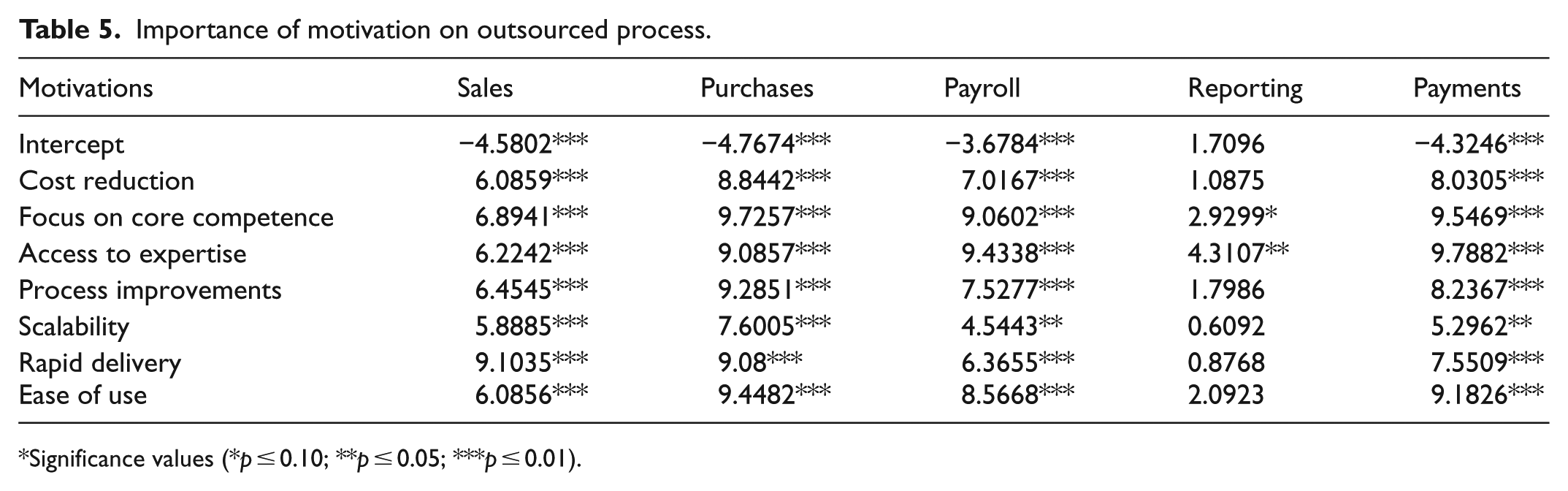

In addition to probing the relationship between outsourcing motivations and the degree of outsourcing, we looked into the most important outsourcing motivations for each major part of the accounting function. To group the accounting processes into distinct parts, we used the categorization by Everaert et al. (2007): sales, purchases, payroll, reporting and payments. In Table 10 in Appendix F, we have reported the responses to the main motivation items for each process (P1–P22) and process group (sales, purchases, payroll, reporting and payments).

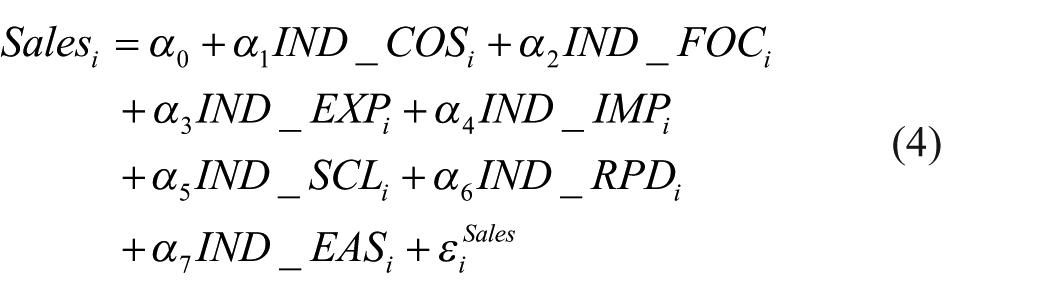

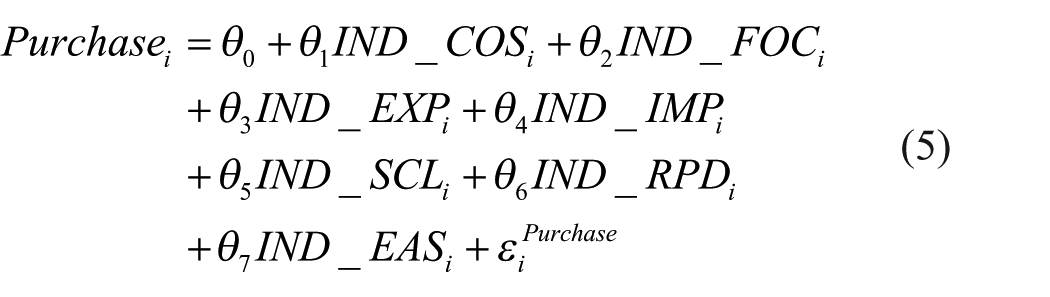

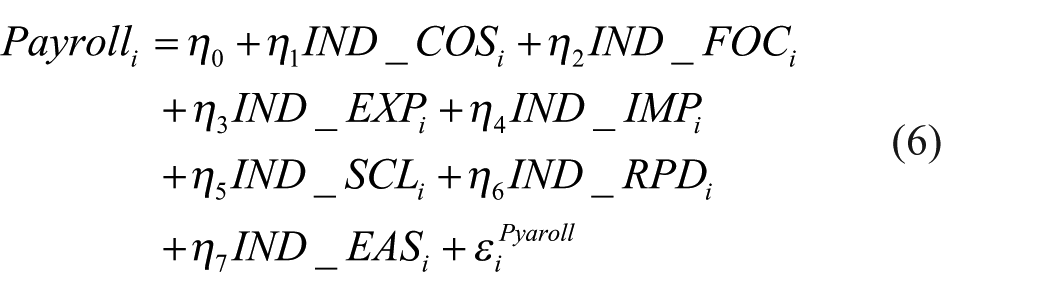

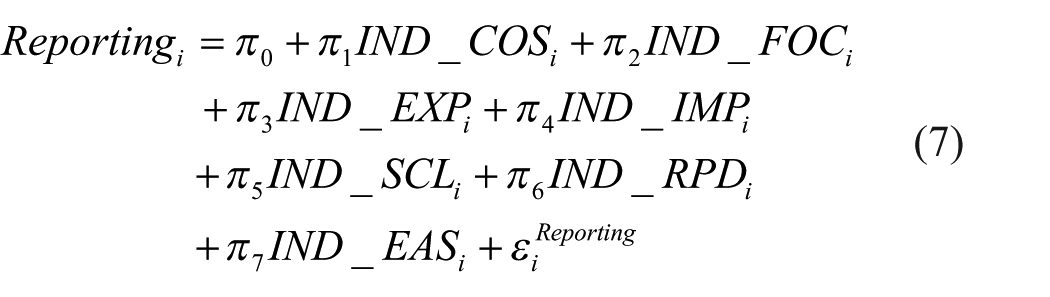

We use probit model to evaluate the relative importance of each of the seven motivations on each of the outsourced processes that are grouped into five major categories. Let Salesi, Purchasei, Payrolli, Reportingi and Paymenti be the outsourced process for the company i for processes pertaining to sales, purchase, payroll, reporting and payment, respectively (please see Table 7 in Appendix B for categorization of 22 outsourced processes into the five major categories). Let IND_COS, IND_FOC, IND_EXP, IND_IMP, IND_SCL, IND_RPD and IND_EAS be the indicator variables pertaining to the importance of cost reduction, focus on core competence, access to expertise, business improvements, scalability, rapid delivery and ease of use, respectively, that takes a value of 1 if the company i stated that individual motivation to be the most important for their outsourcing decision, otherwise it is 0. Thus, we model the following

The error term

Process group-level results

The results of our model are summarized in Table 5. Our results show that with exception of reporting, all the studied outsourcing motivations were positively associated with outsourcing of accounting processes. However, there are differences in the strengths of the effect. For example, while it appears that access to expertise is the most important motivation factor to outsource payroll and payments, focus on core competences seems to be the main motivation for outsourcing transaction-related processes. Concerning the processes within reporting, which were outsourced the most in our data set (see Table 10 in Appendix F), the results suggest access to expertise and focus on core competence are the main motivations for outsourcing those processes.

Importance of motivation on outsourced process.

Significance values (*p ≤ 0.10; **p ≤ 0.05; ***p ≤ 0.01).

Discussion

In this article, we set out to better understand the relationship between motivations to outsource and the degree of outsourcing within a business function in the context of SMEs. Our purpose was to critically analyse the outsourcing motivations cited in the existing literature and propose a conceptual basis for future studies. Next, we will present the implications of our research to theory and practice.

Implications for theory

Even in the early days of outsourcing, researchers proposed that while efficiency-focused motivations have a major role in outsourcing decisions, strategy-focused motivations could also play a key part in the decision to outsource particular functions (McLellan, Marcolin, & Beamish, 1995; Gambal, Kotlarsky, & Asatiani, 2018). More recently, Weigelt and Sarkar (2012) outlined two main desired organizational outcomes of outsourcing, which are broadly referred to as efficiency and adaptability. We observe a similar trend in our findings, where the dividing line among motivations is drawn between the desire for efficiency (related to utilization of supply-side economies of scale) and the desire to seek for external expertise (drawing on the access to specialized resources on the market). Our key contribution lies in uncovering the differences in the relationship between these groups of motivations and the degree of outsourcing. We would like to highlight two specific theoretical implications.

Our first theoretical implication concerns the strength of various motivations and the degree of outsourcing. As hypothesized, the three motivation variables associated with efficiency (cost reduction, focus on core competence and business/process improvements) turned out to be positively related to the degree of outsourcing. These efficiency-related benefits of BPO emerge mainly as a result of the supply-side economies of scale and scope (Poppo & Zenger, 1998). Therefore, for a company to be able to fully harness these benefits, a larger degree (scale) of the processes within the specific business function should be outsourced. Following this reasoning, a sound theoretical argument drives the strong positive relationship between efficiency-related motivations and the degree of outsourcing.

Interestingly, our results suggest that not all motivation items work in the same way: Although a motivation variable may drive the overall decision to outsource, it may be negatively associated with the degree of outsourcing. This was the specific case of the motivation variable access to expertise in our study. While the motivation to access expertise through outsourcing has been found in earlier literature to explain the overall decision to outsource (Lacity et al., 2016), in our study companies that strongly sought to gain external expertise to the business function ended up outsourcing fewer processes. We discuss this finding from the perspective of company resources. By gaining access to expertise through outsourcing, companies seek to complement their resource based on the specific processes for which they lack internal competence (i.e. cannot perform themselves). Theoretically, compared to efficiency seeking through outsourcing, this type of resource complementing is clearly targeted to a smaller number of processes. Thus, based on the argumentation above, it seems reasonable to find a negative relationship between access to expertise and the degree of outsourcing.

Building on these observations, the second main theoretical implication from our results is a suggestion of systemic influence on the interaction between outsourcing motivations and the degree of outsourcing. In other words, analysing motivations on the scale of the whole function provides greater insights to the interaction between motivation factors and outsourcing, than merely studying the motivations behind outsourcing each individual process. Our findings suggest that when looking at outsourcing motivations of a given process or a group of processes within a larger business function, the relationship between motivations and decision to outsource remains more or less the same across the spectrum of processes. Therefore, taking a modular view on outsourcing (i.e. analyse outsourcing motivation for each task or a small group of tasks within a function) could lead to a conclusion that all outsourcing decisions are equally influenced by a set of common outsourcing motivations. However, when looking at the bigger picture of outsourcing of a whole business function (in our case, accounting), we observe the clear relationship between the strength of certain motivations and the degree of outsourcing. This calls for more systemic analyses of outsourcing, echoing the observations made by Dibbern et al. (2012) on IS outsourcing.

We argue that, contrary to earlier research (e.g. Dahlberg et al., 2006; Lee et al., 2004), outsourcing should not be viewed as a single decision with a fixed set of outcomes. Instead, we need to study this decision beyond the decision point and focus on how the outsourcing decision determinants affect the outsourcing arrangement resulting from the decision. Our central claim is that the strength of various motivations defines the degree of outsourcing. However, these motivations may have a varying effect on the degree of outsourcing, where one set of motivations facilitates a higher degree of outsourcing, another set has the opposite effect and a third set has no or little effect on the extent of outsourcing (see Figure 2).

The implication of our approach is that one cannot study or compare various outsourcing decisions without considering the relationship dynamics between outsourcing motivations of the decision-making entity and the degree of outsourcing of a given business function. While the majority of the existing research (as demonstrated by Lacity et al., 2016; Lacity et al., 2011) focuses on studying the role of motivation in making outsourcing decisions, very few studies analyse the relationship between the articulated motivations and the configuration (in our case, the degree of outsourcing) of the outsourcing contract. Our study demonstrates the potential knowledge gains from studying outsourcing arrangements from the perspective of motivations and possibly other sourcing determinants, such as transaction attributes.

Implication for practice

Uncovering the nature of the relationship between motivations and the degree of outsourcing yields insightful implications for practitioners. Outsourcing service providers should understand that their customer companies have differing motivations to outsource their business processes and that the degree of outsourcing is one dimension that can be used to analyse these differences. According to our results, companies seeking access to expertise outsource only a limited set of tasks, whereas those seeking efficiency gains outsource a larger set of tasks. Outsourcing service providers could take this into account when designing their market offerings. For example, when entering into negotiations to renew the contract of an existing customer, the service provider should analyse the past behaviour of the customer and build arguments for continuing the contract accordingly. Outsourcing service providers can also develop service packages tailored to different segments of the market and thus make their sales processes more efficient.

Moreover, information system providers may use the findings of this study to build systems with features that enable both efficiency and integration of expertise. For customers that outsource a larger set of tasks, ensuring the efficiency of the outsourced processes is important, whereas easy integration of expertise is important for customer companies that outsource only a limited number of tasks.

Companies that are considering outsourcing should carefully reflect upon their motivations and evaluate which of the processes should be outsourced, in correspondence with their objectives. Many cloud-based information systems allow a more granular division of tasks between the outsourcing service provider and the customer company, which enables more alternatives for organizing business processes.

Limitations and opportunities for further research

We note three main limitations to our findings. First, we limited our empirical setting to the context of accounting. While accounting offers a somewhat clean and controllable study setting, further research could explore the relationship between outsourcing motivations and the degree of outsourcing in a broader context. Researchers could ask, for example: Does the composition of the business function influence the degree of outsourcing and the associated motivation variables? Furthermore, empirically, we focused on SMEs, which have more limited access to resources and have fewer layers of hierarchy than larger firms. Clearly, we must assume the outsourcing behaviour and motivations to be different in larger firms compared to SMEs. Therefore, here, we restrict ourselves to making theoretical and practical knowledge claims on SMEs’ outsourcing behaviour. Further research could look into the differences between large and small firms in terms of their outsourcing motivations and degree of outsourcing. Second, in this study, we only focus on the degree of outsourcing omitting specific outsourcing configurations and their interaction with outsourcing motivations. Further studies could focus on identifying and characterizing common outsourcing configurations within a business function and analyse the potential interdependencies between different processes and motivations to outsource. Third, while the motivation items used in this study have strong empirical support from earlier research, due to the nature of our empirical study (survey), the items had to be simplified, condensed and measured on seven-point Likert-type scales. In reality, the motivations driving an outsourcing decision might be more complex calling for studies using data collection methods that allow for more in-depth probing. Further research could, therefore, take a more qualitative stance and critically review the results of our study.

Conclusion

We draw on two streams of outsourcing literature—outsourcing motivations and degree of outsourcing—to probe the relationship between motivations and degree of outsourcing. Relying on a rich data set with responses from 337 companies, we find that cost reduction, a focus on core competence and business/process improvements are all associated with a higher degree of outsourcing, but interestingly, access to expertise is negatively associated with the degree of outsourcing. This finding suggests that companies that outsource to acquire external expertise are more selective. These companies outsource only a limited number of processes within a specific business function. Our main theoretical contribution lies in uncovering the dynamic nature of outsourcing motivations, meaning that as companies outsource a larger degree of their business processes, some motivation items become more accentuated and others fade in importance. Furthermore, our enquiry on process group-level outsourcing revealed that while four of the process groups (sales, purchases, payroll, payments) portrayed a balanced set of motivations across the seven motivation items, outsourcing of processes in one process group (reporting) was motivated by access to expertise. Our empirical findings open avenues for further studies probing the nature of the relationship between outsourcing motivations and the degree of outsourcing.

Footnotes

Appendix A

Appendix B

Appendix C

Appendix D

Appendix E

Appendix F

Acknowledgements

We thank the Federation of Finnish Enterprises for the opportunity to survey their members. We are grateful to the Senior Editor and the two anonymous reviewers whose comments and support helped us improve the manuscript. We also thank the HSE Support Foundation for partially funding this project. Our pre-study based on qualitative data was presented in a paper session at ECIS 2016 and we wish to thank the participants of that session for their feedback.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was partially funded by the HSE Support Foundation.