Abstract

Ireland's policies towards US-owned global digital intermediaries (Big Tech) have emerged as an international political issue and received global media attention. So far, political and media focus has been on the impact of Ireland's tax policies on the revenue-raising ability of other European states and perceptions of light touch regulation of those corporations based in the Republic. The current paper will focus on how Ireland's switch to a focus on capital allowances for the sizeable American tech corporations has enabled the latter to sustain their dominance in the digital transition through incentivizing and subsidizing their switch to assetization as a means of deriving investment. Assetization enables investment and profits based on present and future rents from intellectual property. We argue here that the assets and intellectual property of the tech giants are emblematic of a broader process of political–economic restructuring and information monopoly building. The evidence for this resides in Ireland's bumper rise in corporate tax from 2015. Ireland's facilitation of assetization is the end process of some broader institutional transformations that structure economic power.

Keywords

Introduction

Ireland's policies towards US-owned global digital intermediaries (Big Tech) have emerged as an international political issue and received global media attention. So far, political and media focus has been on the impact of Ireland's tax policies on the revenue-raising ability of other European states and perceptions of light touch regulation of those corporations based in the Republic. The current paper will focus on how Ireland's switch to a focus on capital allowances for the sizeable American tech corporations has enabled the latter to sustain their dominance in the digital transition through incentivizing and subsidizing their switch to assetization as a means of deriving investment. Assetization enables investment and profits based on present and future rents from intellectual property. We argue here that the assets and intellectual property of the tech giants are emblematic of a broader process of political–economic restructuring and information monopoly building. The evidence for this resides in Ireland's bumper rise in corporate tax from 2015. Ireland's facilitation of assetization is the end process of some broader institutional transformations that structure economic power.

For digital companies, the Intellectual Property regime change and assetization enable digital business models that give them exclusive access to the key factors of production, allowing the future creation of monopolies in adjacent areas of digital services. Hence, what Pagano (2014) calls intellectual monopolies, the lengthening and strengthening of intellectual property rights and their designation as capital assets, are the outcomes of multiple institutional adjustments that re-engineer value creation. The Irish capital allowances system subsidizes this monopoly building through tax exemptions on intangible assets, thus freeing up capital for investment and legitimating institutional changes. The Irish intervention instantiates broader institutional transformations occurring within the US.

The paper takes a political economy approach that draws on state theory, historical institutionalism and the political economy of communications to position Ireland within the broader dynamics of the development of digital capitalism. Central to this is how Ireland has positioned itself as an attractive location for global I.P.-based industries looking for a European base. Whether it be pharmaceuticals, financial services or communication technologies, the State has created an environment wherein infrastructure, policy, and education environments are complementary, but, most significantly, capital assets are heavily subsidized and, to a certain extent, inter-corporate value shifting is hidden. In short, the Irish policy framework encourages and facilitates a process of assetization, I.P. hoarding and rent-seeking in large tech corporations.

The paper will outline the conceptual framework and then evaluate the proposition that Ireland should be considered an I.P. competition state. It will argue that Ireland's strategic courting of I.P.-based global industries is symptomatic of a significant change in the political economy, for example, the switch of focus to rent extraction. An overview of the political, economic, legal, and policy factors driving assetization will be given to help understand this transformation. The paper will then consider the historical use of I.P. in Ireland's tax strategy towards Apple and Google as historical case studies of how I.P. has been used to shift value within industries. It will then consider how Ireland's current policy towards capital allowances incentivizes FDI with an I.P.-based focus. Lastly, it will consider how the consequences of incentivizing I.P. industries contribute to the intellectual monopolies of corporations with a base in Ireland and the broader implications for the digital tenants of the rentier platforms.

Conceptual framework

The theoretical framework draws on political economy, state theory, and historical institutionalism. The political economy of communication analyzes the social and power relations that structure the production, distribution, and consumption of communications resources, including the relationship between State, market, and society (Mosco, 2009; Schiller, 2000). A key element of the political economy approach is analyzing the State as an institution and mediator of power relations in global resource distribution (Jessop, 2013).

To locate Ireland's policies towards big tech in a broader political–economic context, it is necessary to consider interrelated concepts of digital labour, value creation, commodification, rent, intellectual property, assetization, enclosure and wealth extraction. The recent political–economic literature from Marxian and Heterodox traditions is particularly relevant (Birch, 2020; Christophers, 2020; Mazzucato, 2018; Rikap, 2023). The critical political economy of digital media traditions provide a framework for understanding how a few tech corporations have emerged as an oligopoly in digitalization (Bilic et al., 2021; Fuchs, 2024).

Lastly, historical institutionalism analyses reproducible and recurrent patterns of behaviour, thinking, and resource distribution across space and time (Bannerman and Haggart, 2015). It evaluates the interplay of ideas, institutions, and interest groups in the constitution of social life over time. It is mainly concerned with how institutions (formal and informal rules) are strengthened and weakened and the broader power dynamics that result from that strengthening and weakening.

Digital labour, knowledge, commodification and assetization

The current paper concerns the economic structure of global digital technology corporations and how they sustain dominance. The key is tracing how socially produced knowledge is privatized, commercialized to extract rent and assetized to attract capital investment in those rent-seeking activities. Political economy scholars and heterodox economists have redirected attention to the origins of use value in digital labour (Fuchs, 2024; Jarrett, 2022; Mazzucato, 2018). Digital labour within and contracted by digital corporations is one of the least studied aspects of those corporations’ ascendance to digital dominance, with the role of tech workers being the least considered element (Dorschell, 2022). To focus on tech workers is not to propose that value arises purely from their work. Bilic et al. (2021) demonstrate how Google and Facebook have enclosed publicly funded science, research, and Free Software and Open Source inputs into their commodity forms. Mazzucato (2018) illustrates the same process by Microsoft and Apple. Tech workers who write the code for websites, apps, and software draw on existing resources to create a commercial product that is monetized in different ways. This, alongside an assemblage of digital labour, becomes the basis for extraordinary profits and cycles of investment that have allowed a few prominent companies to become global gatekeepers. High fixed costs, economies of scale and scope and positive network externalities characterize digital goods and services. The value resides in the assemblage of labour that develops goods and services that mediate symbolic agency and connection for users in a mediated environment. The monetization of knowledge inputs, user attention and data are vital logics that are subsequently imprinted on the affordances of digital goods and services.

Tech workers’ extant knowledge and know-how combined with additional knowledge, labour, and data are significant inputs into the production of commercial digital goods and services. As Bilic et al. propose, these products are often provided to users free of charge and are best considered as ‘pre-commodities’. Pre-commodities build on publically produced user value and achieve scale as free and privately funded social utilities. Scale and use deliver users’ attention and data, which is, following data analysis, further commodified (intermediate commodities) and marketed to the advertisers of products of third parties who produce final commodities. In this last regard, digitalization expands markets and goods and accelerates consumption (Schiller, 2000). Tech workers such as software engineers and data analysts utilize knowledge resources and know-how to produce highly valued technology monetized across this commodity chain. They are paid a wage for their present labour time, whereas the corporation appropriates the future productivity of their intellectual investment as a means of future production. Pre-commodities are also modular by design; tech modules are made separately but can be integrated and updated across an ecosystem of products. Corporations capture and control the future and scalable value of salaried tech workers’ knowledge resources as input in the form of intellectual property (Bilic et al., 2021).

Corporations extract value by separating socially produced intellectual resources into a product and intellectual property (in the legal form of patents, copyrights, and trademarks) whilst only paying labour for the present product output. They can reduce production costs, shape the affordances of future software development (e.g. algorithms designed for attention and data capture) and extract future value and inputs. Intellectual resources, as means of production, now appear as intellectual property to be owned, controlled, licensed and capitalized by the corporation. This flexibility is used in mobility and the ability to move I.P. where labour is cheaper, taxes lower, or both. Only the largest corporations can structure their economic organization this way, so smaller companies are disadvantaged and made ripe for acquisition.

Under financialized capital conditions, this I.P. can also be valued as a financial form or an intangible asset (Birch, 2020). Because of its monopolization as a modular input to the means of production, it enables corporations to extract value from its historical, present and future profitability. This flexibility and mobility enable the strategic movement of IP-based assets to areas with higher asset/capital incentives. The legal form abstracts value from labour, and the financial form further abstracts value from the place and time of its production. What becomes clear is that the code that software engineers produce blurs the boundaries between commodity, input, and asset and is manifested through property and contract law as all three.

The chain of commodities that starts with commons or publicly produced value and labour becomes monetized as an asset whereby multiple forms of rent are extracted: I.P. rents, data rents, attention rents, connection rents, and intermediation rents, amongst others (Mazzucato, 2023). Here, it is clear that the logic of software production and the affordances of digital forms mediate rentier capitalism. Christophers (2020) defines rent as ‘income derived from the ownership, possession or control of scarce assets under conditions of limited or no competition’. Corporations control knowledge and build technological forms based on exclusive access to knowledge and information. For example, pre-commodities extract public value and are offered free. They are then subsequently commercialized and upgraded via monetization and can become key intermediaries or gateways in the network of the Internet. Through the logic of datafication, they constantly mine new data as raw material for knowledge production. According to Christophers, these technological forms are ‘a digital infrastructure for generating intermediation-based rents for its owner’. Corporations can structure the business so that I.P. (legal form) and assets (financial form) are located where rents in the form of tax evasion or available capital incentives can also be extracted. Intellectual property is the basis of further value extraction and rent-seeking.

Corporate and State lobbying shape the direction that I.P. law and policy have taken, resulting in monopolies on the use of knowledge that have become longer and stronger, with the Trade-Related Aspects of International Property (TRIPS) Agreement being a prime example (Frenkel and Dreyfuss 2015). The State recognizes these enclosures (tradeable commodities) through legislation, regulation, and the enforcement of exclusivity contracts. As Rikap observes, patent authorities may compel intellectual property licensing to third parties for royalties, but the access is restrictive and costly (2023). This de facto private ownership of knowledge and data can and does involve a global monopoly over its application. Once this occurs, firms’ capacities to absorb and learn from new knowledge will be structurally differentiated, leaving those at the frontier with the best chance of future innovation. Secondly, as knowledge is part of every production process, it can potentially be monopolized in any sector or industry across the economy. (Rikap, 2023 p116)

The second part of the process, assetization, is a relatively recent phenomenon and demands further scrutiny, given its importance to the current paper. Assetization refers to ‘anything that can be controlled, traded and capitalized as a revenue stream’ and has emerged as a critical dynamic in techno capitalism (Birch, 2020). Digital infrastructure, goods, and services are based on knowledge, know-how, and data manifested in code, codified as intellectual property, and further realized in finance as intangible assets. Chiapello clarifies that intangible assets ‘have no physical materiality; instead, they have legal and computational materiality ‘detached’ or ‘derived’ from some underlying physicality’ (Chiapello, 2024 pp45). Crucially, the production of intangible assets is a process that allows financial value to be extracted and circulated independently of global commodity chains. This latter factor has featured significantly in the economic power structure of tech corporations via the disintegration of value chains and their decision to base European operations in Ireland. Chiapello notes the blurring of distinctions between both financial and intangible assets. Tellmann et al. propose that in distinction to financialized capital, intangible assets involve a type of future making that is ‘not just as expected, speculated and calculated, but also as contracted, owned, controlled and de-risked at the same time’ (2024: 5).

As Birch and Munieza demonstrate, intangible assets, incorporating intellectual property, are legal constructs (contract and property law) enforced by state power. They value constructed monopolies and, subject to policy and law, can be valued through discount techniques that value future rents. Asset values are constituted by social actors that are both internal (corporate asset managers) and external (financial analysts, standards agencies). The dynamism and mobility of the asset form challenge their geographical governance and oversight. Value must first be produced and enclosed, and this is a site of multiple institutional struggles (scientific, legal, political and commercial). Assetization also involves the ‘problematization of temporality and politics in the making and claiming (future) value’ (Tellmann et al., 2024: 3). Assetization is a financial form that leverages future earning capacity, wherein that capacity is realized in the present through securitization/reduction of risk. The current paper aims to understand further and problematize state power's role in legitimizing, subsidizing and de-risking intangible assets as a significant aspect of the economic structure of tech corporations and their information monopolies.

I.P. law and policy

Intellectual property law creates the basis whereby knowledge can become a tradeable commodity, a monopoly, and is the basis for its assetization. Katharina Pistor demonstrates how intangible assets, assets that exist not in physical but legal form, are sometimes intellectual property rights and sometimes financial assets and often both. In short, intangibles are wealth-producing assets coded in the law of contracts and property with additional protections from the trust, corporate, or bankruptcy law (Pistor, 2020). Ultimately, they are protected by the power of coercive law and the State. According to Pistor, we must begin ‘with an inquiry into how value creation with and through law takes place, by whom and in whose interests, and what alternative options might be available’ (Pistor, 2020). What is important here is the recognition that property and value coded by law is a construct shaped by corporate legal power. This legal power can then proliferate by encoding in legal technology, which primarily instantiates US legal norms and practices (Sandvik, 2019). This is a prime example of the socio-cultural effects of knowledge monopolization and its materialization across adjacent sectors, as Rikap (2023) outlined.

Arguably, led by the commodification of digital labour, goods and services, the legal coding of property, and the financial recording of assets, innovation policies can also be captured by or structured for rent-seeking dynamics. Poorly designed I.P. policies that target income generated from intellectual property can incentivize value shifting within firms and reduce public budgets whilst enclosing knowledge and encouraging rent-seeking in services that structure data-driven development for private rather than public gain (Mazzucato, 2018). Following the same logic, R&D concessions do not cause research and development but allow companies with already large R&D budgets to subsidize it. Intellectual property regimes already guarantee temporary and longer-term monopolies on knowledge enforced by the law and the State, and policies that further provide concessions for intangible assets run the risk of incentivizing rent-seeking. In short, the geographical, temporal, and empirical challenges of governing intangible assets raise issues relative to value extraction, profit shifting, innovation lock-in and future knowledge monopolies.

The argument of this article, with Ireland as an example, is that I.P. law, tax laws and capital tax allowances incentivize investment in intellectual property rights as a means of structuring economic value within a company, whilst policy-derived subsidy also de-risks investment in ‘intellectual monopolies’ based on assetization/rent-seeking (Pagano, 2014). The reform of such situations can reside only in re-assessing where value originates, a blind spot of neoclassical economics and neoliberal policy. In an Irish context, the policy rationale underlining Ireland's capital, R&D, and innovation regime appears increasingly driven by the need to replace the outgoing low tax incentives with something equally attractive to IP-based global corporates.

The I.P. competition state

As a competitive state, Ireland excels in attracting foreign direct investment (FDI) (Murphy and Kirby 2007, Kirby and Murphy 2011). As the most globalized nation in the 2000s, its economic boom from 1994 to 2007 was based on a commitment to neoliberal policies of liberalization, re-regulation, and privatization overseen by a series of centre-right coalitions. The Irish political economy remains geared towards attracting FDI as a key growth mechanism. This is achieved through low corporation tax, which has attracted primarily US corporate profit shifting to Ireland. This practice has positioned Ireland as an ‘emerging transnational accumulation regime of rentier character’ (Egan, 2023). However, with the recent OECD tax reforms, low tax is no longer the only incentive for investment. Ireland also offers generous capital allowances for the intellectual property of critical global industry sectors, such as technology, finance, and pharmaceuticals.

Ireland has transformed into an IP-based competition state, wherein intellectual property-based companies are located there in return for significant subsidies, support, and privacy. While this approach has successfully attracted inward investment, it has also led to the concentration of policies on the competitive provision of varied IP-based subsidies to international firms. This, in turn, has locked the State into supporting business strategies based on related dynamics of privatization, information/platform monopolies, enclosed innovation spaces, rent-seeking, and wealth extraction. Egan argues that most investment passing through Ireland is ultimately ‘phantom’, and productive activity happens elsewhere. Ireland appears to be ‘a staging post in the corporate circuit of capital’ (2023 p545).

Various journalistic accounts detail how the Irish State attracts multinational corporations for inward investment. These are summarized as follows: (1) engaging in aggressive tax competition (Reuters, 2013), (2) lack of transparency and enforcement regarding the tax dealings of multinational corporations (Murphy, 2013), (3) a close relationship between politicians, state agencies, tax advisors, accountancy firms and the legal offices of corporations in Ireland (Drucker, 2013), (4) offering light touch regulation in exchange for investment (Irish Times 2020), and (5) providing private corporate access to the upper echelons of state power (Irish Independent, 2014). These incentives inflect a position of dependent development that undermines the autonomy of the Irish State and its position within the E.U. (Jacobsen, 1994). State capacity is directed towards enabling the accumulation regime of digital intermediaries. The general articulation of policy based on attracting capital circumscribes state intervention in the economy more generally. For example, Egan (2023) explains Dublin's ongoing housing crisis as an outcome of the inflationary effects of labour migration, that is, multinational corporate employees. The policy prioritizes private rental property for mobile corporate employees. As investment moves to rental properties, the media have coined the term ‘Generation Rent’ to apply to those locked into continuous rent paying due to a lack of affordable housing to purchase. As the housing charity threshold notes, Generation Rent is ‘a term used to capture a broad range of inequalities in access to housing, secure employment, and welfare support amongst younger households (Threshold, 2023). Public investment choices are subordinate to foreign direct investment goals even as the latter reproduces the logic of rent.

Digital intermediaries in Ireland: Google and Apple

The flagship of Ireland's economic policy is attracting foreign direct investment through low corporation tax. With a tax rate of 12.5%, it is one of the lowest in the European Union. Combined with the access Ireland gives to European markets, its English-speaking population and infrastructural development, Ireland has become a location of choice for many US corporations. The decisions of large ICT and digital service companies such as Microsoft, Apple, Facebook, Google, and Amazon have partly been an outcome of these dynamics. However, another key attraction was the ability to move profits to tax havens via vehicles such as the ‘Double Irish’.

What initially came to prominence concerning both Google and Apple's tax dealings in Ireland, latterly labelled by the OECD as Base Erosion Profit Shifting (BEPS), was their utilization of a global tax system that enabled global companies to manifest myriad presence across different states. The source of their profits, intellectual property, resided in those countries with low to zero tax rates or, in some cases, remained stateless. The combination of complex international tax laws, the peculiarities of Irish tax laws and the intangible nature of goods based on intellectual property were of more significance to their ability to lower their tax below the original Irish 12.5% tax rate. The global tax system enabled, both legally and through extant loopholes, a situation where global companies could route their taxes through myriad companies based in different jurisdictions and potentially render themselves stateless for tax. The technology companies located their sales subsidiaries in Ireland to rinse out their global tax commitments.

It is difficult to estimate the contribution that this extended global tax holiday (the E.U. Commission valued Apple's tax foregone, 2004–2014, at 15 billion Euro) has given to the tech corporations that have taken advantage of it. However, it is clear that the tax foregone and the resultant working capital of these companies have contributed to significant cash reserves and have implications for their continued high spending in R/D, mergers and acquisitions and the accumulation of I.P. In its testimony to the US Senate sub-committee on tax affairs, Apple argued that its Irish subsidiaries AOI and ASI contribute a proportion of their foreign cash holdings to the high-cost R&D activities, mainly carried out in the United States (Forbes, 2013).

From profit shifting to value shifting

Ireland's 12.5% corporate tax rate has been a source of disquiet amongst its European partners for some time. As detailed by Stewart, as early as 2007, the French government supported plans within the European Commission to develop a Common Corporate Tax Base focussed on lessening the effects of ‘harmful tax competition’ (Stewart, 2013). In 2007, the German finance minister also criticized Ireland and articulated its support for tax harmonization. In the context of the loans given to the Irish State, in the wake of the banking collapse, both Nicholas Sarkozy and Angela Merkel attempted to make Ireland's tax rate a condition of the EU/IMF loans. The subsequent revelations about the tax dealings of Google, Apple, Microsoft and Facebook have directed attention to the particular dynamic of global tax, tax laws and the new intermediaries of the global industrial structure of digital media. However, a so-called Google Tax, a European attempt to tax tech company profits at the point of sale, has yet to materialize even as national attempts persist.

Ireland nominally signed up for E.U. and OECD tax reforms and increased its tax rate by 2.5% in 2024. The BEPS, which attracted large corporations, is widely perceived as discontinued. In addition, in 2018, the US introduced the Tax Cuts and Jobs Act, which essentially allowed corporate taxes abroad to be taxed at the rate of the states in which the corporations were active. However, the focus on profit obfuscates the central dynamic of value shifting occurring through the privatization of knowledge, trading it as a commodity and valuing it as an asset.

R&D and capital allowances

Despite the shutting down of tax loopholes, there continues to be a significant difference between GDP and indicators of ‘real’ economic activity in Ireland, which Paul Krugman labelled in 2015 via his Twitter account as ‘Leprechaun economics’. In 2015, Apple relocated around $250 billion in intellectual property assets to Ireland, resulting in a 50% increase in tax revenue and a 26.5% GDP growth. This is better labelled I.P.-based value shifting. From their international headquarters in Ireland, multinational corporations like Apple have been setting up manufacturing (hardware) overseas, licensing their I.P. from Ireland and shifting their intangible assets there.

According to the E.U.'s Tax Observatory, an independent research lab based in the Paris School of Economics, Ireland and Holland continues to operate as the key tax shelters for I.P.-based multinationals operating in the European economy (European Tax Observatory, 2024). This is achieved through further tax planning strategies for I.P.-based businesses in Ireland. In 2024, the Observatory labelled Ireland a tax haven, the world's number one tax haven, according to its 2024 report; …corporate tax revenues of Ireland have exploded since 2015…. Some of this growth may reflect the relocation of activities to Ireland, i.e., standard tax competition for capital. However, a large fraction probably reflects the rise of profit shifting to Ireland, mainly due to the relocation of intangible assets following BEPS, the Tax Cuts and Jobs Act, and the introduction of capital allowances. Whatever the reason, this increase illustrates how, absent tax coordination and minimum taxation, tax havens can generate high amounts of tax revenues by choosing meagre tax rates.

Another significant tax-based incentive to encourage Irish-based companies to invest in R&D is the R&D tax credit. In certain situations, credit allows them to receive up to 30% of their R&D expenditures (capital and revenue) as a tax credit or as cash (Irish Revenue, 2021). According to Christensen and Clancy, utilizing R&D tax credits offered by Ireland's tax code permits Apple and other businesses to pay tax on R&D operations at a rate of 3%.

In 2015, the tech companies began on-shoring their I.P. and sales profits to Ireland because of the capital allowance and R&D credits, which essentially allow them to reduce their tax liability. This is a significant departure from the Double Irish. Since that year, the Irish corporate tax revenue has increased tenfold. In a report for the European Left Group, Christensen and Clancy labelled the tax relationship between the Irish State and Apple as the ‘Green Jersey’ deal. Aside from the on-shoring of sales and I.P. to Ireland, the essential features include the following:

Sales profits are booked in Ireland, but the expenditure the company incurs in the one-off purchase of the I.P. license(s) can be written off against the sales profits by using the capital allowance program for intangible assets; It is beneficial for the company to complement the tax write-off by continuing to use an offshore subsidiary but no longer for outbound royalty payments. The role of the offshore subsidiary is to store cash and provide loans to the Irish subsidiary to fund the purchase of the I.P. The expenditure on the I.P. is written off, but so too are the associated interest payments made to the offshore subsidiary, which thus accumulates more cash that goes untaxed. (Christensen and Clancy, 2018: 6)

Arguably, Ireland is incentivizing assetization, which becomes the basis for potential value shifting, shoring up intellectual monopolies, and rent-seeking within digital ecosystems.

After looking into Microsoft's cost-sharing plans and its operations in Ireland, Curtiss and Avi-Yonah suggest they do not fully comply with the most recent version of the US tax code. Microsoft revealed in an August 2017 hearing held in Australia that it had significantly changed its cost-sharing agreement (CSA) that year in order to consolidate its overseas intellectual property under its Irish affiliate, ostensibly eliminating its affiliates in Singapore and Puerto Rico from the CSA. As late as 2021, filings in Ireland showed that Microsoft Ireland Operations Ltd. (MIOL) reported about $28 million in revenue per employee — a remarkable figure that is about 3,435 per cent times the U.S. figure reported in SEC filings……… According to MIOL's income statement included in the credit report, it expensed 82 per cent of that revenue as operating costs separate from the cost of sales and administrative expenses. This expense is believed to consist primarily of a royalty to MIR for the license of the OEM- related technology I.P. it obtained through the CSA.

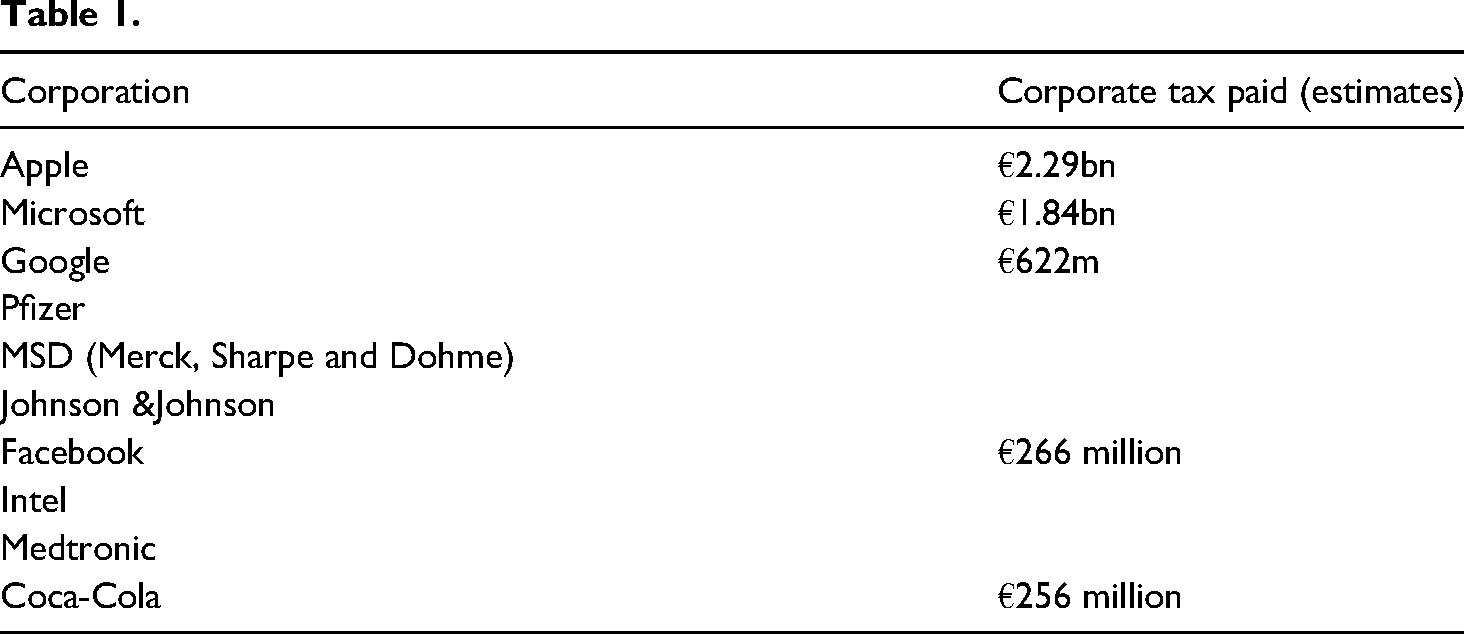

Ireland is the third-largest recipient of corporate taxes from US multinational corporations worldwide. It has seen a doubling of its corporate tax revenues since 2015. Due to the concentration of payments, half of all payments came from just 10 companies (Irish Revenue 2021). There is a public interest in identifying the actual payers of these corporate taxes and the source of those profits. However, corporations do not publish detailed accounts per country, and Irish revenue exempts corporations from doing so. In 2021, Eoin Burke Kennedy, economics correspondent with the Irish Times (2020), estimated the likely companies to be as follows (see Table 1).

A working paper from the Irish Fiscal Advisory Council (2023) endorses this speculative list:

'We find that just three groups accounted for around a third of all corporation tax revenues in 2021. This share remained high and close to a third throughout the five years, from 2017 to 2021. Furthermore, just two sectors—ICT and pharma-chem—accounted for a substantial share of the corporation tax paid by the top ten groups during this time'.

From the Irish Times list, Coca-Cola is the only company not in the ICT/Pharma Chem sector. In a forensic analysis, tax accountant Sean Crotty identified the spike in corporate taxes as related to the transfer or the on-shoring of intellectual property to Ireland, where, he claims, up to 50% of profits can be tax deductible (Crotty, 2021). Again, this is legal, but only because of the abstractions of commodification, legal regime shifting and a lack of transparency. The designation, pricing and transfer of royalties all occur within the corporation (Schneider, 2021). Additionally, the Irish State offers a shield to full accountability on these matters, and there are no fundamental economic measures for valuing intellectual property as assets (Jarrett, 2022).

Because Irish revenue does not publish the specific tax paid each year by corporate groups, we rely on information from investigative journalism, NGOs and forensic tax accountants to trace value construction in the political economy. If intellectual property lies between a commodity and an asset, who other than the corporation is in a position to value assets? The value of assets partially comes from the legal ability to exclude competitors and arguably from its reverse engineering to move value. They also allow corporations to expropriate surplus and future surplus value from socially produced goods and privatize and monopolize innovation internally and through acquisition. Furthermore, given the low distribution cost/scalability of I.P.-based profits elaborated by Haskel and Westlake (2017), it is likely that large firms with established infrastructural power are experiencing the super profits that further arise from assetization. Profits from non-rivalrous code will, by default, outstrip physical or commodity-based growth. This is more than profit shifting; the fundamental contradictions emerge from the abstractions and contradictions of digital capitalism. These abstractions arise from commodifying knowledge/knowledge labour (organizational and legal form) and assetization (financial form). With each move, the value is coded by the legal system, not the market. This is why the Irish State can continue to claim that the tax arrangements in Ireland are all ‘perfectly legal’.

Additionally, poorly designed policies are an opportunity cost for public policy that may drive innovation and public purposes across myriad sectors of the economy and society. Mazzucato argues that policies like those in Ireland incentivize the wrong type of entrepreneurship. Citing William Baumol, I.P. policy can structurally favour ‘unproductive’ entrepreneurs who take advantage of their unique connections with the government to build regulatory protections, obtain public funding or public value for their use, or manipulate regulations policy to their advantage, thereby stifling competition and giving their businesses an advantage. This is, of course, a rent-seeking behaviour in economics. Public interest objectives are neglected in supporting rent-seeking innovation, whereas potentially productive and socially beneficial innovation sources are dissuaded.

Arguably, this state-driven competitive tax competition pursued in Ireland from 2000 to 2015 enabled a first-mover advantage for platforms. After that, the regime shifts in I.P. from a source of innovation to a source of investment guarantee, coupled with capital asset incentives (the Green Jersey deal) and the lack of transparency surrounding royalties, facilitate and incentivize the development of information monopolies. It designates I.P. as an asset that allows significant tax exemption that, by any measure, is a subsidy. As there are few benchmarks for designating the asset value of I.P., this is highly exploitable by firms. Additionally, the valuation of I.P. as assets, not innovation incentives, switches the firms’ focus to rent-seeking.

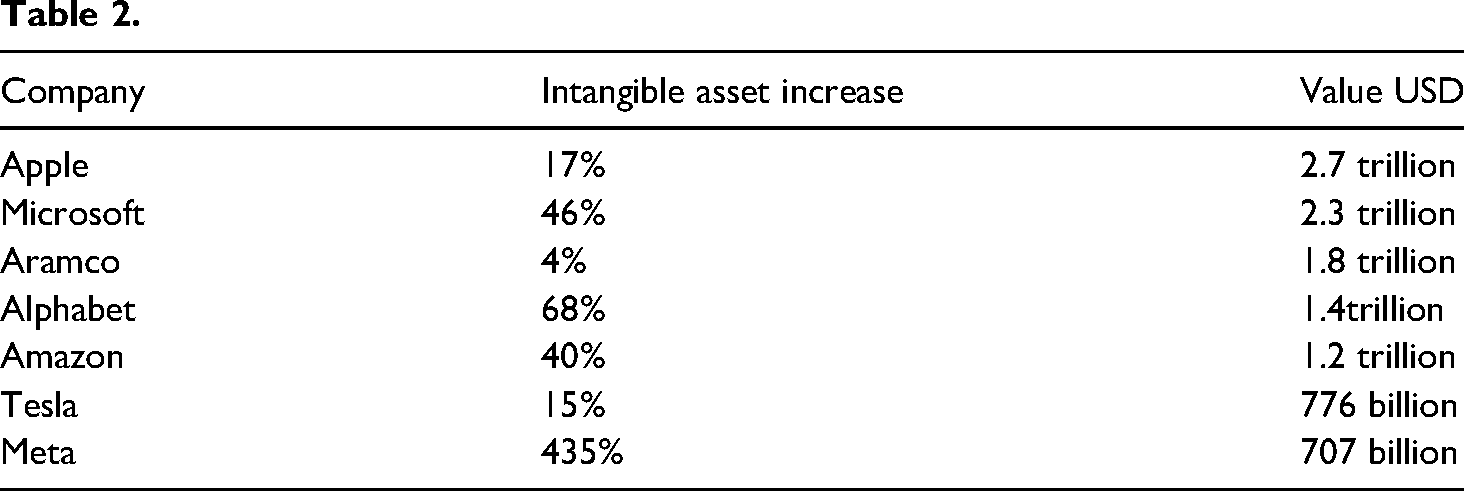

The Brand Finance Global Intangible Finance Tracker (GIFTTM) report annually tracks the intangible asset value of the largest corporations worldwide. The 2023 figures indicate the companies with the highest-valued intangible assets and the percentage increase in asset value year over year. Unsurprisingly, digital platform companies dominate this list (Table 2).

Of course, Ireland's favourable subsidization of capital investment is one aspect of institutional arrangements supporting the significant revenues and growth of the dominant technology companies. Another side of the coin is the US suppression of interest rates from 2009 to 2022. The US kept interest rates close to zero, encouraging investment funds’ interest in business models that promised transformative technological outcomes. This, allied with the US commitment to shareholder value above all other values, including public and social values, created the institutional basis for massive investment in companies based on intangible assets. The 0% interest rates in the US and the reduced tax rates in the Irish Republic enabled massive sizeable investments and equally voluminous dividends for investors, which enabled the digital monopolies that are the focus of so much policy activity in the present. Additionally, large tech companies have benefitted through the historical absence of regulation, which is well documented.

Conclusion

The Irish government has actively facilitated the digital dominance of US-based digital corporations through tax breaks and favourable policies, supporting their internationalization and expansion strategies. While this has brought in significant tax revenues and enhanced the State's appeal to foreign direct investment, it has also facilitated a form of digital capitalism that extracts value from various social spheres and perpetuates a winner-takes-all economy. Furthermore, by positioning itself as an attractive location for global I.P.-based industries, Ireland is actively bolstering the intellectual monopolies of big tech and pharma companies. Intellectual monopolies are perpetuated through enclosing intellectual labour, designating critical aspects of value as residing in that property, and attracting investment and speculation in these monopolies. Ireland's current state-corporate nexus enforces restrictive IPRs, legitimizes assetization, subsidizes assetization, and facilitates inter-corporate trading and the internal pricing of intellectual property that makes techno-scientific corporate profits so malleable. By enabling this mode of accumulation, the Irish government contributes to a larger dynamic wherein value generation is subjugated to the logic of rent and monopolization, and inequality is exacerbated in the distribution of surplus value from socially productive activities to capital. Furthermore, Microsoft, Alphabet, Meta, and Apple are at the forefront of A.I. development, and Irish state policies will perpetuate their dominance in these spheres of activity.

Intangible assets offer a form of monopoly on future factors of production that are central to innovation in digital goods and services. Low interest rates and capital allowances structure the investment by large investment funds into asset-rich corporations that are near-monopolies in crucial infrastructure and ecosystems of digital mediation. Investment funds such as Blackrock and the Vanguard Group are increasing their shares in Big Tech companies in parallel with those corporations’ processes of assetization and the State's de-risking of assetization. Three of Apple's most significant shareholders are Vanguard, Blackrock and Berkshire Hathaway. Blackrock Incorporated's top holdings are in Microsoft, Apple, NVIDIA, Amazon and Meta (Fintel, 2024). What is occurring is the parallel encroachment of asset investment companies on digital infrastructure, services and goods to complete their asset portfolios. This will exacerbate the rentier dynamics that have characterized the digital economy and deepen them in the context of A.I. development. It also deepens the investment chokehold that big tech has on many sectors of the digital economy, a chokehold that originates from their intellectual monopolies. This centralization of political, economic and media power also challenges the ability of democratic governments to govern. To return to the communicative implications of this, the autonomy of Irish media sectors and their ability to compete within the infrastructure of digital media are circumscribed by the monopolistic powers of the Big Tech. More value will be extracted from media, whereas the rents for attaining attention will continue to rise. At a democratic level, media's informational, expressive, dialogical, creative and educational dimensions are pulled closer to the private logic of digital capitalism. In contrast, public logic of access, public service, cultural expression and shared communicative space are de-emphasized.

From the Irish State's perspective, it raises significant questions about the appropriateness of a state institutional structure that appears captive to the geopolitical steering of United States corporations and their mode of development. Ireland's facilitation of assetization is just the end process of some broader institutional transformations. However, it contradicts the E.U.'s goals to become a geopolitical actor in the digital economy. Because of Ireland's relationship with the Big Tech, the European Commission, in 2022, based oversight of its centrepiece Digital Services Act in Brussels, not Dublin. Ireland will forego investments and employment because it is not configured to direct state capacity to public interest objectives. In the short term, Ireland generates significant but precarious tax revenue and some local but highly mobile employment. In the longer term, assetization and rent-seeking exacerbate the deepening inequality and stagnation associated with a techno-economic system built on wealth extraction and the negation of public value, a system that seeks to stretch its logic into all social and economic domains long into the future.

Footnotes

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.