Abstract

In today’s competitive market, SMEs need to realize that accounting information system (AIS) can enhance management control effectiveness (MCE) - one of the areas necessary for their survival and success. This paper aimed to measure the influence of AIS success on MCE among SMEs of Yemen, a less developed country, as research and knowledge are very limited in such context. Data were collected from 315 SME owners and managers via a questionnaire. SmartPLS 3 software was employed for data analysis. The results concluded positive links between AIS success and MCE. Specifically, the results revealed that AIS information quality, system quality, and usage positively impact MCE; quality of information and system are essential drivers of AIS usage and satisfaction; user satisfaction positively influences AIS usage. Interestingly, the quality of service showed to be insignificant in the context of AIS. Moreover, user satisfaction showed no significant impact on MCE. This research is deemed one of the first to introduce empirical evidence on the influence of AIS success on MCE among SMEs in Yemen, as a less developed country context.

Introduction

Information systems (IS) are work systems that allocate their operations and activities to process information, i.e., capturing, transporting, stocking, retrieving, processing, and displaying information (Alter, 2008). Livari (2005) interpreted an IS as a computer-based system that offers users information on certain issues in a specific organizational context. Each firm employs various IS, particularly computerized ones, to help them run their operations and achieve their objectives. Every firm strives to improve the effectiveness and productivity of the institutional management process by implementing an information system or technology (Syahidi and Asyikin, 2018; Al-Hattami, 2021b). Accounting information system (AIS) is a computerized IS concerned with the firm's financial and economic activities. According to Al-Hattami et al. (2021b), AIS is a computer-based software application to input and process financial data to generate financial information. Grande et al. (2011) identified AIS as a technological tool developed to manage and control issues related to the firm's financial and economic activities. Nicolaou (2000) also described AIS as a computer-based system that boosts control and collaboration within a company. AIS is generally the firm's lifeline, and there cannot be coordination, integration, or control of business operations without it (Das, 1989; Al-Hattami and Kabra, 2019; Sarwar et al., 2021).

On the other hand, firms cannot maintain a robust competitive place and attain value without a planning and follow-up process (control) (Nilsson and Stockenstrand, 2015). Control is a management concept that ensures the success and sustainability of businesses (Głodziński, 2012; Alomari et al., 2018). In every firm, the control process is carried out regularly as part of its activities to achieve its objectives and improve its performance (Voss and Brettel, 2014). The control process is often one of the critical management functions, which aims to monitor and measure actual performance and compare it to planned (Almbaidin, 2014). Berry et al. (1991) identified management control as a ‘functionalist perspective’ that concentrates on those activities needful for the firm to remain cohesive and survive as an entity. Its purpose is to direct and control organizational activities to attain the corporate goal and determine its competitive advantage. It is the prominent tool managers must take to plan, budget, analyze, measure, and evaluate helpful information for appropriate decision-making (Alomari et al., 2018).

Managers utilize various types of information to perform effective control. Conducting an effective control process demands having credible, sufficient, comprehensive, and timely information, particularly in contemporary business dynamics marked by globalization and rapid market shifts (Harris, 2018). AIS can provide such information (Sajady et al., 2008; Almbaidin, 2014; Al-Fasfus and Shaqqour, 2018). Literature confirms the importance of IS/IT, including AIS and its benefits to the firms covering various management functions, particularly the control process (Sajady et al., 2008; Almbaidin, 2014; Alomari et al., 2018; Harris, 2018). An efficient AIS keeps users from making errors, processes data fast, and produces meaningful reports (Sarwar et al., 2021). AIS functions enable reporting data and information to internal and external stakeholders and monitoring activities (e.g. asset protection and limit actions of individuals) (Guragai et al., 2017). AIS is also important for improving the firm's capability to resist and control competition (Ritchi et al., 2019). Indeed, AIS is the lifeblood of the business where it is no longer reasonable for any company to work or control its business without such a system (Sajady et al., 2008; Das, 1989). This earns the success of AIS more interest and search (Granlund, 2011; Grabski et al., 2011; Al-Hattami, 2021b).

Appiah et al. (2014) stated that AIS has actually become the underlying source for successful enterprises regardless of their size and geographical regions. AIS has become a widely spread business system; it is no longer exclusive to large enterprises. Though large enterprises have paved the way for the introduction and application of AIS, it is growingly crucial for SMEs to manage their collective intellect. The success of IS is one of the most widely adopted variables in IS research (Wang and Yang, 2016). Understanding the value of systems and the impact of management operations and investment in them necessitates measuring their success (DeLone and McLean, 2003). However, studies focused on measuring AIS success are very limited, especially in the SMEs context of the least developed countries (LDCs) such as Yemen. Pešalj et al. (2018) further observed that these enterprises had received little attention in the literature related to the use of management control systems. Other recent research has also disclosed that the investigation of IT/IS success, especially AIS in LDCs, is still very limited (Al-Hattami, 2021b; Aboaoga et al., 2020; Andoh-Baidoo, 2016; Homaid, 2021).

The scarcity of research focusing on the role of AIS success among SMEs in LDCs represents a significant gap in the literature that is important to address. Even though the vital role of AIS in the success and survival of SMEs by boosting management control effectiveness (MCE), many SMEs are still ignorant of this role. The actual contribution of AIS success to MCE remains unclear among SMEs in LDCs, and research is so limited to provide helpful guidance. Therefore, the present paper aims to bridge this research gap by examining AIS success and its impact on MCE in SMEs of Yemen. The selection of Yemen is explained by being one of the LDCs (UNCTAD, 2017; Homaid, 2021). Moreover, to our best knowledge, no study has examined the influence of AIS success on MCE among SMEs in such countries. Additionally, there is a need to focus on the SMEs sector in such countries, as this sector is exceedingly regarded as an essential contributor to job creation, minimize poverty, and economic development (UNCTAD, 2017; ILO, 2018; Mohammad, 2018; Alhakimi and Mahmoud, 2020; Fan et al., 2021).

As several earlier research in various contexts and systems (Floropoulos et al., 2010; Balaban et al., 2013; Ghobakhloo and Tang, 2015; Ojo, 2017; Ouiddad et al., 2020; Lwoga et al., 2020; Al-Okaily et al., 2021; Li and Wang, 2021), the present paper is based on DeLone and McLean (2003) (D&M) model and intended to examine the influence of AIS success on MCE among SMEs in Yemen. Consequently, the study question for this paper is: What is the influence of AIS on MCE among SMEs in Yemen?

The rest of the paper contents are Background, Model and Hypotheses of the Study, Methods, Analysis and Results, Discussion, Implications for Theory and Practice, Conclusion, and Limitations and Future Research.

Background

European Commission (EU, 2005) defines SMEs as enterprises with fewer than 250 people. Many countries adopt this definition to identify their SMEs (Ramdani et al., 2021). However, some countries such as Oman and Saudi Arabia define SMEs as those having less than or up to 100 employees (MoCI, 2012; Ahmad, 2012). In Egypt and Yemen 1 , such enterprises are defined as those having up to 50 people as a maximum (SMEPol, 2003; YMIT, 2014). Hence, the SMEs definition varies across countries. Notably, SMEs are not smaller versions of large business entities. They are entities that have an independent form and intellect (Harris, 2018; Wang and Yang, 2016). In comparison to large businesses, SMEs adapt better to market changes and fresh customers’ needs, and their regulatory structure allows for faster decisions. Further, these businesses have high flexibility to adapt to technological changes and promote better income distribution than large businesses (Pilar et al., 2018).

SMEs generally form the majority of businesses and are very important in most countries. According to OECD (2014), SMEs contribute more than 55% of GDP and more than 65% of total employment in high-income countries. They also account for > 60% of GDP and > 70% of total employment in low-income countries. Thus, the quality of products and services they provide and their success and survival rates significantly influence the economies of those countries (Fernet et al., 2016; Nyathi et al., 2018; Perera and Baker, 2007).

IT/IS adoption and utilization can provide effectiveness, efficiency, innovation, growth, and competitiveness. These advantages offer SMEs opportunities to continue working and their success and survival (Consoli, 2012; Ghobakhloo et al., 2012; Nyathi et al., 2018; Ruiz and Collazzo, 2021). In return, this helps the country's economic development as the continuity and success of these enterprises contribute to it (Andoh-Baidoo, 2016; Ilavarasan, 2017; Qureshi, 2020). This is because these firms help create jobs, improve income distribution, reduce poverty and export growth (UNCTAD, 2017; ILO, 2018; Mohammad, 2018; Al-Hakimi and Borade, 2020; Al-Hakimi et al., 2021; Al-Hattami et al., 2021c).

AIS is one of the mechanisms used to ensure that such aspects are improved for firms. SMEs with IT solutions such as AIS are more likely to grow (UNDP, 2015). Adopting a computer-based accounting system has become critical, and it may be a crucial factor in the survival and success of SMEs (Ismail et al., 2003). There is a reasonable consensus on the importance of AIS for the continuity and survival of firms (Mohammad, 2018; Nyathi et al., 2018; dos Santos et al., 2018). This is because AIS is a critical regulatory mechanism crucial for effective decision management and business control (Nicolaou, 2000; Shuhidan et al., 2015; dos Santos et al., 2018; Ghasemi et al., 2019). Using AIS, it is possible to carry out the management control process effectively as AIS is a control system in nature. The more AIS is used, the better internal control measures (Shaiti, 2014; Sajady et al., 2008). It is possible to forecast future earnings, assess operations risk, and correct deviations with AIS (Grande et al., 2011; Salehi et al., 2010). Mitchell et al. (2000) argued that AIS could aid in the management of short-term issues, including spending, costs, and cash flow, by providing information to enhance the control process. Once short-term concerns are overcome, managers can concentrate on combining operational considerations with long-term strategic goals. These controls enable firms to protect assets, generate accurate information, and implement activities efficiently and effectively (Guragai et al., 2017). These advantages have been developed and tested in developed countries, and they should expand to SMEs of LDCs.

Compared to developed countries, SMEs operating in LDCs are lagging behind. According to many studies, SMEs have limited management information and poor control (Ismail and King, 2005). SMEs encounter disadvantages when employing management control as they typically lack the information systems needed to do so (Voss and Brettel, 2014). On the other hand, prior research has found that, among other things, inadequate accounting systems and poor record-keeping are among the key reasons for the failure of managing SMEs in such countries (Amoako, 2013; Nyathi et al., 2018; Kareem et al., 2019). In fact, inadequate or unsuccessful accounting systems are a primary factor in SMEs’ failure (Amoako, 2013; Mohammad, 2018; Arasti et al., 2014). On the contrary, successful AIS could help SMEs boost their opportunities for success and survival by offering managers/owners information relevant to effectively managing their business.

IS success model

DeLone and McLean (2003) modified their original IS success model, published in 1992 (DeLone and McLean 1992). This revised model provided an additional quality construct named “service quality,” as proposed by Pitt et al. (1995), as well as incorporating individual and organizational impact into a singular dimension called “net benefits” as suggested by Seddon (1997). These models, particularly the revised one, have gotten a lot of attention in the IS literature as they have been tested and validated in a lot of IS contexts (e.g. Jennex and Olfman, 2003; Floropoulos et al., 2010; Balaban et al., 2013; Stefanovic et al., 2016; Ojo, 2017; Ouiddad et al., 2020; Li and Wang, 2021; Al-Hattami, 2021b). The revised model provided a framework within which theories of evaluating the success/effectiveness of IS can be implemented. It was characterized by its division of model employed in 6 constructs “information quality, system quality, quality of service, user satisfaction, use/intention to use, and net benefits.” The authors explained this model as follows: the model starts with three constructs: information, system, and service quality. These three constructs positively boost system usage and user satisfaction. Finally, certain net benefits will be attained due to use and user satisfaction (DeLone and Mclean, 2003; Balaban et al., 2013; Ghobakhloo and Tang, 2015; Almazán et al., 2017). These net benefits can be in the form of individual benefits (Hsu et al., 2015), organizational results (Almazán et al., 2017), improving performance (Al-Hattami et al., 2021c; Al-Debei et al., 2013), management efficiency (Lee and Yu, 2012), or in the form of effective management control as in this research.

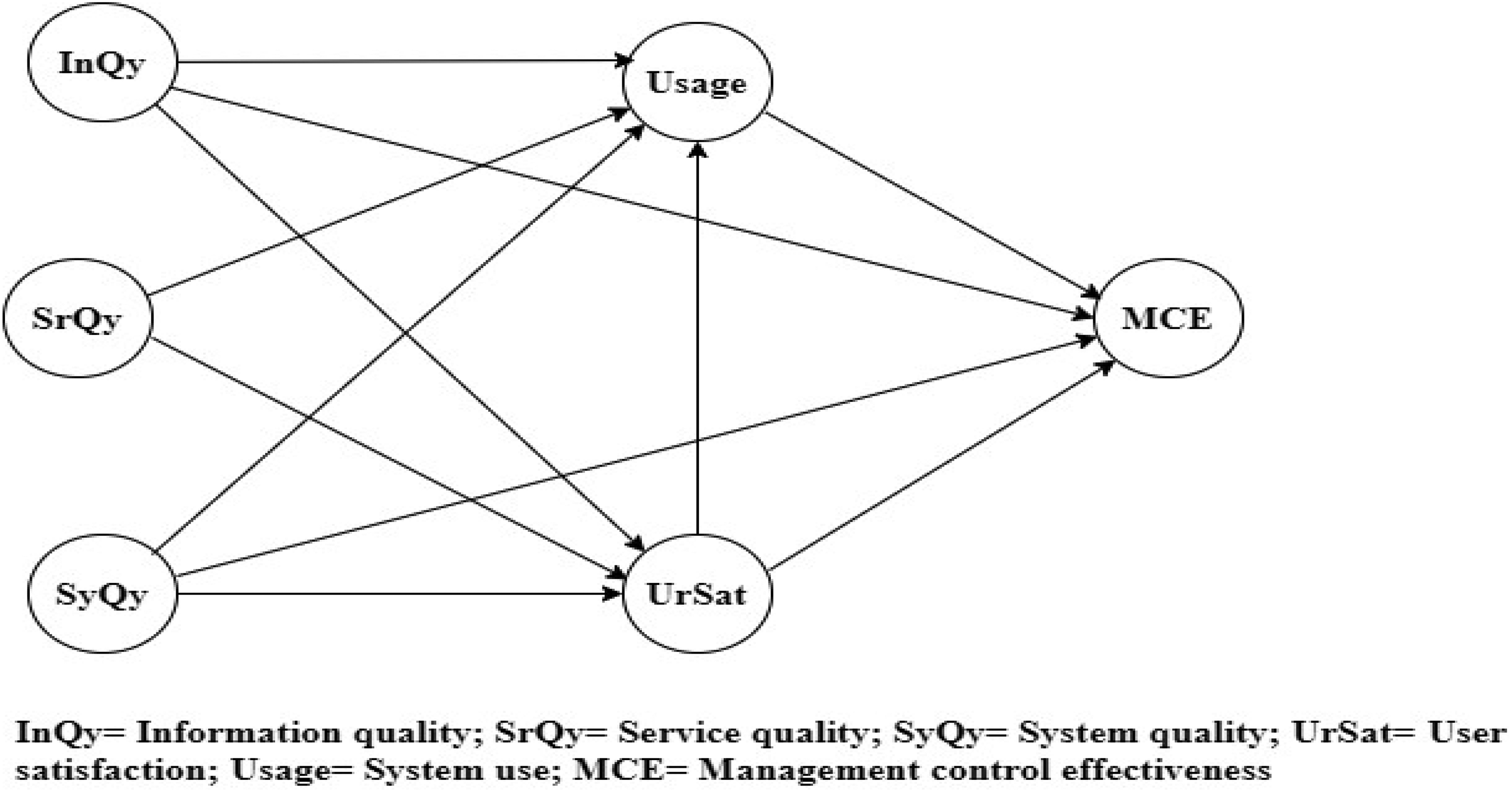

Model and hypotheses of the study

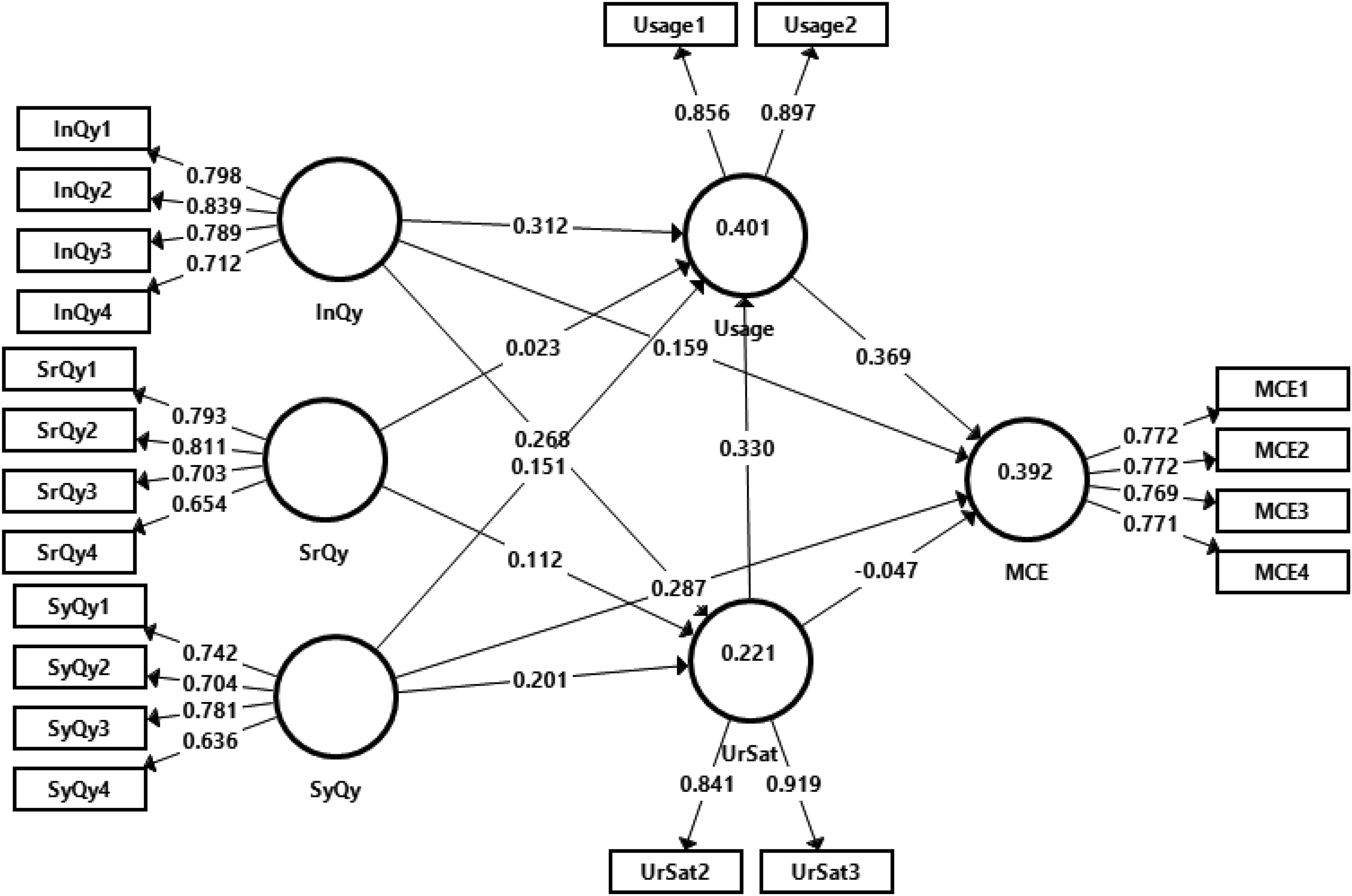

Based on DeLone and McLean (2003), the research model is built in Figure 1. The model, however, did not include the use intention construct because it is judged unsuitable in the context of SMEs where AIS usage is compulsory. Moreover, the reciprocal link between user satisfaction and usage was replaced by one-way causality, i.e., user satisfaction causes use and not vice versa. The feedback linkages from net benefits to UrSat and Usage were also excepted to avoid model complexity. Lastly, as the study aims to assay AIS success's influence on MCE in SMEs, the model was expanded by replacing the “net benefits” with “MCE.” The model was also expanded by examining the impact of AIS quality constructs (InQy, SyQy) on net benefits (i.e. MCE), as few IS studies take this into account.

Research model.

Information quality (InQy)

InQy issues have become too important for SMEs that want to improve performance, earn a competitive advantage or survive in today's business environment (Hussein, 2011). InQy is essential for administrative work; thus, ensuring timeliness, accuracy, and relevance are necessary (Petter et al., 2008). Poor accounting information can jeopardize managerial effectiveness, leading to failure (Shuhidan et al., 2015). Gorla et al. (2010) described InQy as useful user outputs, critical to decision-making and simple to comprehend, and outputs that meet users’ information requirements. Multiple indicators for InQy have been adopted in related empirical research, including completeness, timeliness, accuracy, and relevance (Abugabah and Sanzogni, 2010; Shagari et al., 2017; Al-Hattami, 2021b).

DeLone and McLean (2003) argued that the higher InQy produced by an IS, the more user satisfaction and system usage. This argument has been supported in many contexts of IS (Wang and Liao, 2008; Lee and Yu, 2012; Ojo, 2017; Almazán et al., 2017; Himang et al., 2019; Fadhel et al., 2018; Ouiddad et al., 2020). Although InQy is also a key determinant of net benefits, DeLone and McLean model did not indicate the association between InQy and net benefits (DeLone and McLean, 2003; Petter et al., 2013). However, few studies considered this association and concluded a significant association between InQy and net benefits (e.g. Gorla et al., 2010). Consistent with the preceding, this study builds its hypotheses related to InQy in the context of AIS. But before that, it should note that most of the past studies that examined InQy relationships were conducted in developing and developed countries. In LDCs, such as Yemen, studies about InQy relationships in SMEs are very limited. Therefore;

Service quality (SrQy)

IS researchers recently adopted the SrQy tool, which has proven its validity in many areas such as marketing (Pitt et al., 1995; Chen and Cheng, 2009; DeLone and Mclean, 2003). SrQy simplifies business processes, improves perceived value, and boosts retention (or continuity) (Akter et al., 2011). Providing a fast and reliable service according to the user's needs may provide a better product or service to customers (Shagari et al., 2017). Gorla et al. (2010) presented a scale consisting of four indicators for SrQy, including service reliability, responsiveness, assurance, and empathy. SrQy can also be measured by promptness, responsiveness, security, and comprehension (Chen and Cheng, 2009).

DeLone and Mclean (2003) state that SrQy positively impacts IS user satisfaction and usage. Many other studies in different contexts have proved this positive impact (e.g. Ojo, 2017; Wang and Yang, 2016; Balaban et al., 2013; Alfaki, 2021). However, there is a scarcity of studies that examine such an impact in AIS context of SMEs in LDCs. Therefore, this research investigates this impact in the AIS context of Yemeni SMEs; hence, it assumes that:

System quality (SyQy)

The term “system quality” indicates how well a system is in terms of its operational properties (Jennex and Olfman, 2003; DeLone and McLean 1992, 2003; Petter et al., 2013). It is the degree to which the system's functionalities can best meet user needs, with as little difficulty and as few problems as possible (Chen et al., 2015). A set of indicators were proposed for SyQy: ease of use, response times, flexibility, and reliability (DeLone and McLean 1992, 2003; Petter et al. 2008). Abugabah and Sanzogni (2010) adopted correctness, reliability, integration, and response time. SyQy can also be gauged by accessibility, reliability, ease of use, and flexibility (Prybutok et al., 2008; Al-Hattami, 2021b).

Both DeLone and McLean model (2003) and earlier research (e.g. Iivari, 2005; Hsu et al., 2015; Himang et al., 2019; Wang and Yang, 2016; Fadhel et al., 2018) report a positive influence for SyQy on user satisfaction and usage. Despite the vital relationship between SyQy and net benefits, DeLone and McLean model did not indicate this relationship (DeLone and McLean, 2003), and only a very few studies considered this relationship and revealed a positive association between SyQy and net benefits (e.g. Wei et al., 2009). Existing literature has not sufficiently examined SyQy impacts in the AIS context of SMEs in LDCs such as Yemen to the best of our knowledge. Therefore, this study proposes that:

User satisfaction (UrSat)

UrSat is a metric that assesses users’ perceptions of the system, and it is one of the most constructs that are gauged repeatedly to the success of IS (Jennex and Olfman, 2003; Ghobakhloo et al., 2012; Al-Hattami, 2021a; Al-Hattami et al., 2021a). This construct refers to how satisfied the individuals are with the IS's ability to meet their information necessities (Morris et al., 2002). Users feel satisfied with the system when it is needful to complete their tasks (Le et al., 2018). It can be measured by hardware and software satisfaction, the system's capability to get the job done, increase productivity, and meet user necessities (DeLone and McLean, 1992). It can also be measured by overall satisfaction, support, and meeting expectations (Floropoulos et al., 2010).

DeLone and McLean (2003, 1992) reported that user satisfaction and usage are supposed to be reciprocally interrelated. Iivari (2005) argued that a study should be conducted to adequately assess this reciprocal relationship in which user satisfaction and usage are tracked over time. The satisfaction factor generally locates the user's response to the effectiveness of IS usage, as well as being the basis on which the beneficiary depends in using the system (i.e. user satisfaction drives usage instead of vice versa) (Bikson and Gutek, 1983; Seddon, 1997; Baroudi et al., 1986). Therefore, this research is confined to a single path (i.e. UrSat -> Usage) (Almazán et al., 2017; Lin et al., 2006; Ghobakhloo and Tang, 2015). The literature also argues a positive influence for user satisfaction in attaining net benefits (Hassanzadeh et al., 2012; Al-Debei et al., 2013; Al-Okaily et al., 2021; Al-Hattami et al., 2021a; Li and Wang, 2021). Accordingly, in the AIS context of Yemeni SMEs, it can also be supposed that:

System use (Usage)

The use construct is considered the most applicable metric of success when system use is required (Jennex and Olfman, 2003). It depicts the extent to which users avail IS capabilities and how they do so (Petter et al., 2013; Balaban et al., 2013; Urbach and Müller, 2012). Specifically, the attitude toward usability identifies IS use. Usability is gauged by frequency of usage, depth of usage, and the possibility of self-report of the system (Le et al., 2018). According to Ismail (2009), the use of the system reflects the recipient's consumption of information systems outputs such as regular use, duration of use, number of queries, and frequency of reporting requests. This construct can also be gauged by dependency and frequency of usage (Wang and Liao, 2008) or frequency of usage, time spent in use, and the extent of use (Ouiddad et al., 2020).

When a firm is committed to implementing and using an IS, the firm often does so as some kind of positive organizational effect is desirable, such as profitability or productivity improvement. However, only a few research have looked into the impacts of a particular IS on the firm (Petter et al., 2013). Salehi et al. (2010) indicated the effectiveness of AIS as successful system utilization, which assures the user's needs. They defined the success of AIS use as being profitably applied to the field of interest, widely utilized by satisfied users, and increased their performance quality. DeLone and Mclean (2003) determined the use construct as an essential factor for IS success. They argued that system use could enhance net benefits. Many other researchers have supported this argument. For example, Almazán et al. (2017) and Ojo (2017) revealed a positive link between system usage and net benefits. Stefanovic et al. (2016) and Ghobakhloo and Tang (2015) also concluded a significant impact for system use on net benefits. These net benefits can be in the form of perceived usefulness, time and cost-saving, decision-making quality, among others (Floropoulos et al., 2010; Al-Hattami, 2021b; Ouiddad et al., 2020). The current study replaced the net benefits with MCE as the first study, especially in the AIS context of SMEs in LDCs such as Yemen. Based on that, the last hypothesis is:

Net benefits _ MCE

The major advantages gained from increased use and satisfaction when reacting with IS are net benefits (Al-Hattami, 2021b). This construct represents the overall dependent variable of the D&M model, which plays a vital role in information systems research (Urbach and Müller, 2012). It is a combination of individual and institutional impacts, where the effect can be gauged by reducing costs, improving productivity, performance, decision-making efficiency, economic development, among others (Petter et al., 2008; Petter et al., 2013; Wei et al., 2009; Le et al., 2018; Al-Hattami, 2021b; Al-Hattami et al., 2021c).

The literature supports the significance of IS, including AIS, and the benefits they introduce to businesses. According to Sajady et al. (2008), AIS's benefits may be measured by how well it improves accounting information quality, decision-making process, internal control, performance, and transactional efficiency. Wang and Liao (2008) argued, in their work on eGovernment systems, that “time-saving” and “making the job easier” form net benefits, while Prybutok et al. (2008) adopted improving performance and overall satisfaction as indicators of net benefits. Borena and Negash (2016) used satisfying customers, increasing overall productivity, and increasing competitive advantage in a banking system context, while Al-Hattami (2021b) adopted “usefulness” and “time and cost-saving.” In other contexts, Al-Debei et al. (2013) substituted “net benefits” with “job performance,” Lee and Yu (2012) with “management efficiency,” Almazán et al. (2017) with “organizational results,” and Aboaoga et al. (2020) with “User's perception of IS success.” In this paper, the net benefits of AIS are reflected by MCE.

Methods

Measurement

All study constructs’ indicators/items have been adapted based on the available literature (see Appendix A); some minor amendments have been made to the indicators driven from the literature, emphasizing AIS. These indicators have been measured via a Likert scale of five-point that ranged from “1 - strongly disagree” to “5 - strongly agree.” Four demographic questions on gender, education, Job, and expertise have also been included. Researchers can learn more about their participants by asking demographic questions in a survey. These questions provide context for the gathered survey data (Allen, 2017).

Data collection

This research is quantitative as a closed-ended questionnaire has been employed for data collection (Creswell and Creswell, 2017). As the questionnaire's items entirely count on prior research, only closed-ended questions were adopted, as they are easy to answer and facilitate the statistical analysis process (Mooi et al., 2018; Saunders et al., 2016). Yemeni SMEs, which are amounted to 28167, made up the study population (Al-Fahim et al., 2015). According to Krejcie and Morgan (1970), the required minimum sample size of 28167 units, at a margin of error of 5% and a confidence level of 95%, is 379 units. However, due to the situation in Yemen and the Coronavirus crisis, the researchers targeted only 323 units. Newman and McNeil (1998) reported that a sample size ranging from 300 to 400 is large enough and appropriate. A stratified random sampling method was employed in this paper since it provides a representative sample (Ros and Guillaume, 2019). Accordingly, 323 SMEs from various industries (trading, manufacturing, and services) were targeted (only those applied AIS). Specifically, owners and managers of those enterprises were targeted.

As a first stage, a pilot study was driven. Its goal was to see if the questionnaire items were valid and reliable and the response rate. This pilot study was performed via a questionnaire distributed to 65 randomly selected pilot samples; only 41 answers were received (i.e. a 63.1% response rate). The results demonstrated that all questionnaire items were valid and reliable, implying that the constructed survey is a reliable tool for determining the quality of the proposed model. Concerning the response rate, it can also be considered reasonable.

After that, a mix of online (Google Docs) and offline (manual) delivery were used to distribute 550 questionnaires to SMEs’ owners and managers. Of 331 responses were received (i.e. a response rate of 60.2%); of these, 315 were deemed valid responses, i.e., complete and valid for analysis. The sample consisted of 55 females (17.5%) and 260 males (82.5%). Concerning educational level, 45 participants were enrolled in School/Diploma degrees (14.3%), 194 of them were enrolled in Bachelor degrees (61.6%), while the rest were enrolled in Postgraduate degrees (24.1%). Regarding job positions, 245 participants were managers (77.8%) and 70 were owners (22.2%). Lastly, for the expertise, 52 participants had less than five years (16.5%), 115 of them had 5–10 years (36.5%), while the remaining had above ten years of expertise (47%).

The research model was estimated employing SmartPLS 3 software. In the next section, the measurement model and the structural model are estimated.

Analysis and results

Measurement model

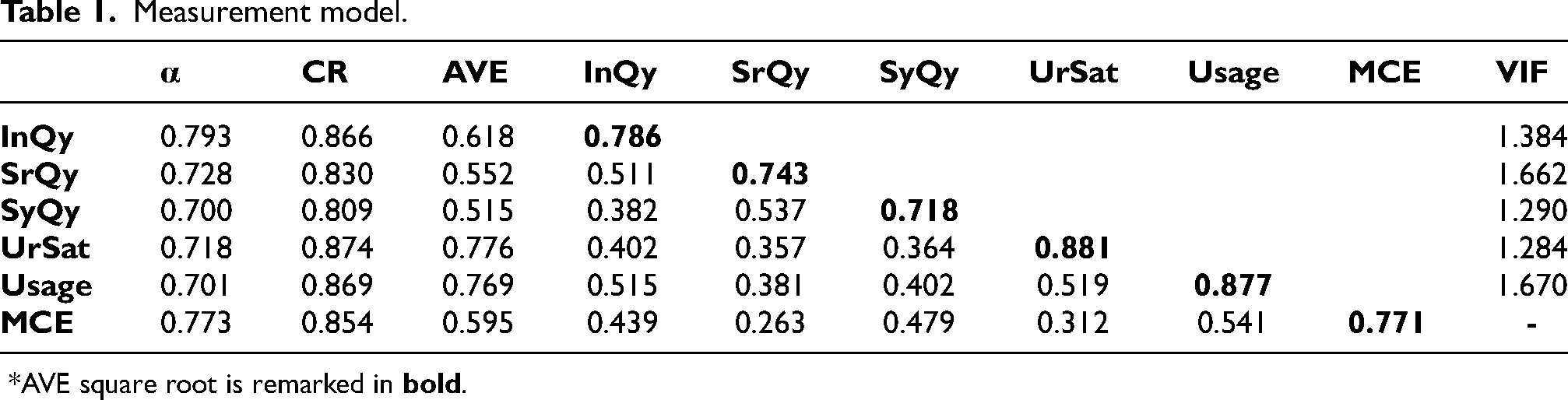

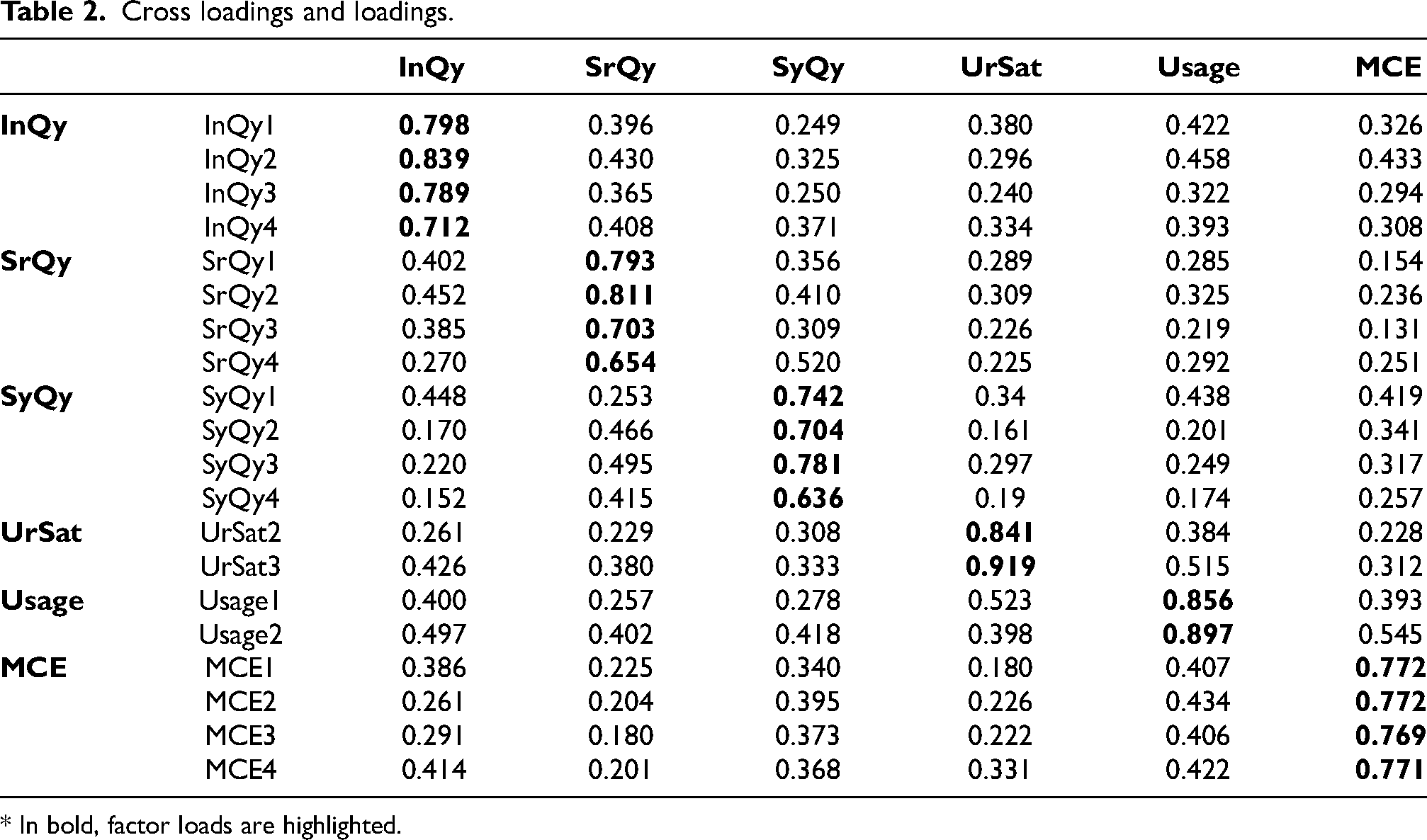

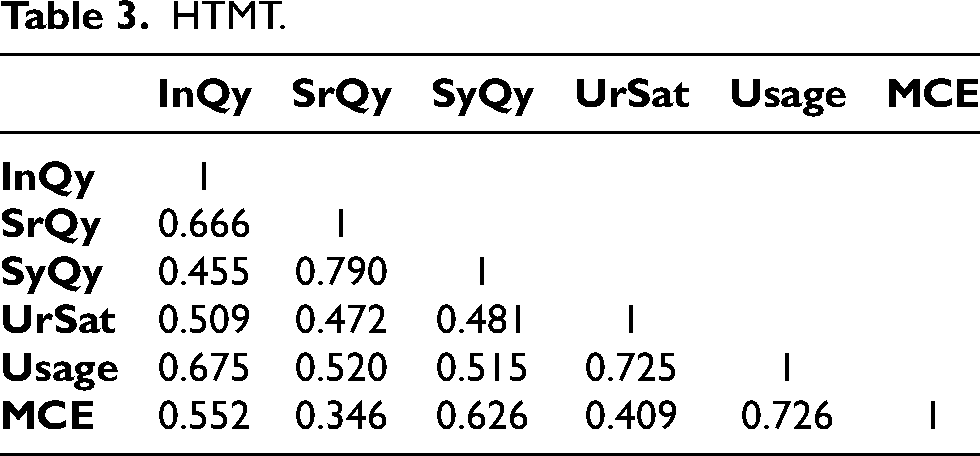

In the measurement model, validity and reliability are investigated. Validity and reliability tests are among the most critical tests performed in empirical IS research. Validity varies into several types, the most important of which are discriminant validity and convergent validity. The typical measurements of discriminant validity are (Fornell and Larcker, 1981; Hair et al., 2017): (1) each construct's correlation values ought to be smaller than the square root of AVE (see Table 1), (2) the loadings ought to be above the cross-loadings (see Table 2), and (3) HTMT ought to be lower than 0.90 (see Table 3). Given that all conditions have been met, it is safe to conclude that all constructs have discriminant validity. The average variance extracted (AVE) for each construct, which should be above or equal to 0.50, can be used to check for convergent validity (Fornell and Larcker 1981). This condition was achieved as shown in Table 1, meaning that the constructs have convergent validity. Cronbach's Alpha (α), composite reliability (CR), and loadings should verify to evaluate the reliability. Based on Hair et al. (2017), the reliability can attain when both α and CR score ≥ 0.70. According to Bagozzi and Yi (1988), the used constructs meet the reliability criterion when their loadings are ≥ 0.60. As shown in Tables 1 and 2, α, CR and the loadings were met. As a result, the measuring tool demonstrated a high level of indicator reliability.

Measurement model.

*AVE square root is remarked in

Cross loadings and loadings.

* In bold, factor loads are highlighted.

HTMT.

This study also investigated Common Method Bias (CMB) and multicollinearity issues. CMB most commonly occurs when all data (dependent and independent variables) are gathered employing the same method, potentially leading to artificial inflation of relationships (Podsakoff and Organ, 1986; Jordan and Troth, 2020). As the highest correlation among the fundamental constructs was r = 0.790, the correlation matrix did not refer to any exceptionally correlated variables (see Table 3). The evidence of bias in the common method usually leads to very high correlations (r ≥ 0.90) (Hair et al., 2010). Any study could also have a multicollinearity issue, but it is undesirable. VIF is commonly employed to quantify and assess the multicollinearity score. A VIF of > 5 is considered an indicator of a multicollinearity issue (Hair et al., 2017). Table 1 showed that all values of VIF are lower than the critical threshold of 5, indicating no multicollinearity issue in this study.

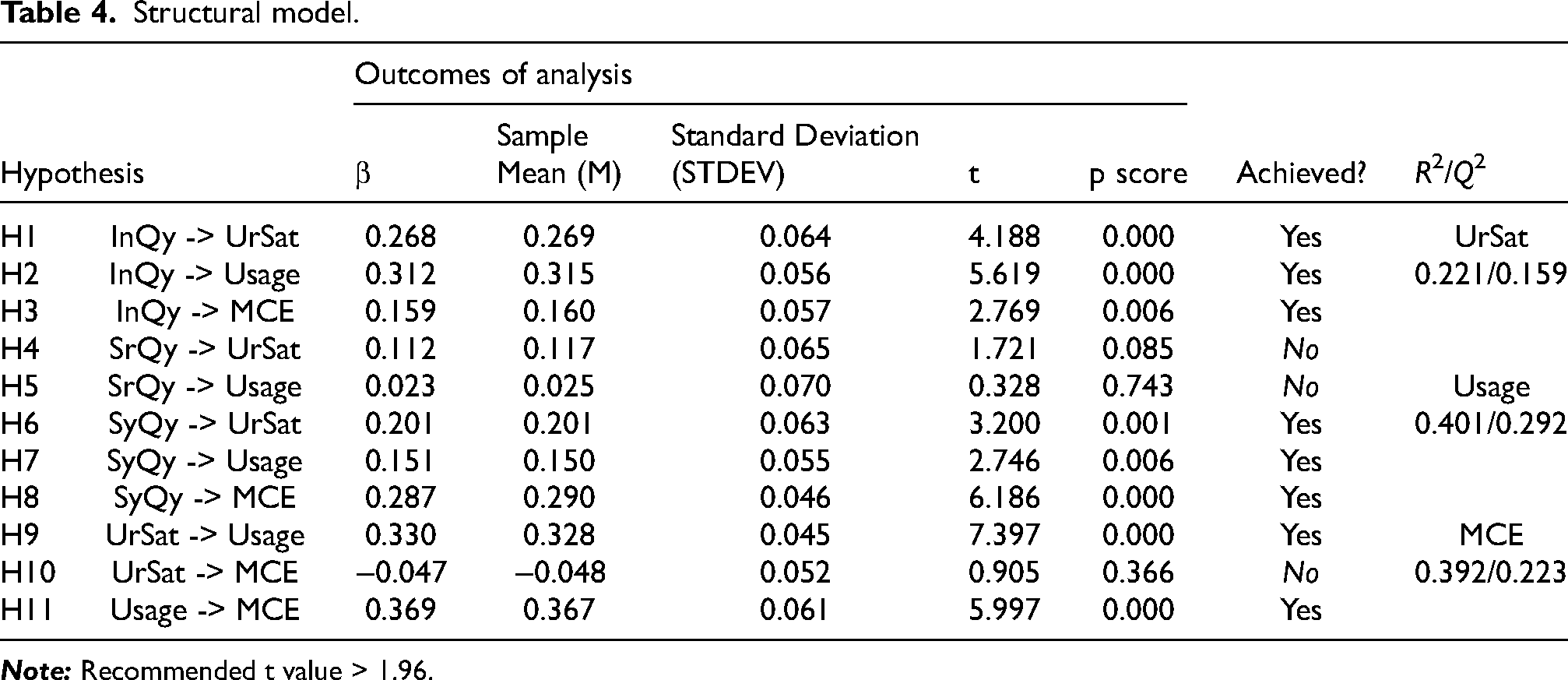

Structural model

The structural model is checked after the measurement model has been confirmed to be correct. Figure 2 depicts the structural model's results, which are also reported in Table 4. The structural model looks at R squares, hypothesis testing, Q2 (predictive relevance), and model fit. First, the variance (R squares) demonstrated by the model is: 0.221 for UrSat, 0.401 for Usage, 0.392 for MCE, which are within the model's predictive strength's permitted ranges (Falk and Miller, 1992). The scores of t and p are employed to determine the significance of β values. Table 4 displays three weak t and p scores (i.e. t < 1.96 and p > 0.5), thus are not significant. Therefore, the corresponding hypotheses (H4, H5, and H7) are unsupported. In SmartPLS, the Q2 is assessed using the blindfolding procedure. The Q2 values greater than 0 suggest that the model is predictive (Hair et al., 2017). Table 4 showed that all Q2 scores are greater than 0, implying the model's predictive power. The Goodness of Fit (GoF) index was created as an overall model fit assessment. GoF is identified as “how well the specified model reproduces the observed covariance matrix among the indicator items” (Hair et al., 2014, p. 576). GoF is calculated employing this formula: GoF = √ (average of AVE * average of R2) (Tenenhaus et al., 2005). A GoF of > 0.25 indicates a good level of overall model fit (Wetzels et al., 2009). This research yielded a GoF of 0.464 [√ (0.6375 * 0.338)], implying a good level of overall model fit for SmartPLS-SEM.

PLS results.

Structural model.

Discussion

This study purposed to measure the influence of AIS success on MCE, drawing on the Delone and McLean (2003) model. Using bootstrapping process with 5000 samples in SmartPLS 3, nine of the eleven developed hypotheses were supported. According to the results, all paths of the proposed model, except for SrQy and UrSat -> MCE, significantly improve MCE in an AIS context of Yemeni SMEs. The study results did not corroborate previous ones on SrQy and its positive impact on UrSat and Usage (Balaban et al., 2013; Ojo, 2017; Wang and Yang, 2016). Even though these results support certain other studies (Ghobakhloo and Tang, 2015), they disagree with D&M commendations, which state that SrQy is necessary for determining IS success. As a result, such results call into question DeLone and McLean's argument that SrQy is a critical determinant in IS success. However, the fact that AIS use is mandatory in SMEs can explain these inconsequential results (H4: β = 0.112, t = 1.721, p > 0.05; H5: β = 0.023, t = 0.328, p > 0.05). That is, regardless of the quality of service, AIS, a mandatory system required to carry out tasks, will be used. Accordingly, it is plausible to conclude that information and system quality are greater drivers of success than service quality in the AIS context. For UrSat -> MCE (H10), it was also shown as an insignificant path (β = −0.047, t = 0.905, p > 0.05). This means that user satisfaction with AIS has no impact on MCE. As user satisfaction in the organizational setting represents individual impacts of IS, tracing the causation path from UrSat to MCE is fruitless. This result can also be justified by the mandatory nature of AIS, which may make the UrSat construct irrelevant in achieving MCE. This result supports Ojo (2017) and Al-Hattami (2021a), who reported that UrSat does not influence net benefits.

In line with the suggested correlations of the D&M success model, the study revealed that InQy positively impacts UrSat and Usage among SMEs (H1: β = 0.268, t = 4.188, p < 0.001; β = 0.312, t = 5.619, p < 0.001). This indicates that AIS's updated, accurate, complete, and relevant information is essential for usage and user satisfaction. Such results were previously confirmed in relevant IS research such as Ouiddad et al. (2020) and Lee and Yu (2012). The paper further found that InQy has a positive influence on MCE (H3: β = 0.159, t = 2.769, p < 0.05). This corresponds to expectations, as information is a product of usage and is in direct service for benefits emerging from AIS use. That is, InQy affects use and satisfaction as intermediate variables and directly impacts MCE. To our knowledge, very few studies have experimentally assessed the correlation between InQy and net benefits within the D&M model (e.g. Balaban et al., 2013; Gorla et al., 2010).

For SyQy paths, they were all positive and statistically significant. Specifically, SyQy was found to significantly impact UrSat and Usage (H6: β = 0.201, t = 3.200, p < 0.01; H7: β = 0.151, t = 2.746, p < 0.01). These results imply that reliable, flexible, easy to use, and accessible AIS could enhance usage and increase user satisfaction. These results align with other research (e.g. Hsu et al., 2015; Iivari, 2005). The results from this paper further found that SyQy has a significant impact on MCE (H8: β = 0.287, t = 6.186, p < 0.001). This indicates that, for SMEs to increase management control effectiveness, SyQy must be given further attention regarding accessibility, ease of use, flexibility, and reliability. To our knowledge, very few studies have experimentally evaluated the correlation between SyQy and net benefits within the D&M model (e.g. Wei et al., 2009).

As expected, hypothesis H9 was supported (β = 0.330, t = 7.397, p < 0.001), which states that UrSat has a positive impact on Usage. This demonstrates that users feel pleased with the features of AIS and are hence driven to use it. This result is in line with Lin et al. (2006), Ghobakhloo and Tang (2015), and Almazán et al. (2017).

For the last hypothesis H11, it was also supported (β = 0.369, t = 5.997, p < 0.001). Indeed, AIS InQy, SyQy, and UrSat impacted Usage, which in turn enhanced MCE. This result implies that successful AIS usage can create net benefits in terms of management control effectiveness for SMEs, even in LDCs such as Yemen. Importantly, the results showed that AIS Usage had the most impact on MCE (β = 0.369) as compared to InQy and SyQy (β = 0.159; β = 0.287). This indicates that, for SMEs to increase management control effectiveness, AIS Usage in terms of continued use and reliance on it, must be given utmost attention.

Implications for theory and practice

This paper promotes the limited knowledge on the influence of AIS success on MCE among SMEs in LDCs. Moreover, it contributes to IS theory by expanding and examining the D&M model in a different context and environment from prior studies. Indeed, this paper showed that the D&M model of IS success, with minor amendments, has agreeable predictive ability in the area of AIS success among SMEs in LDCs such as Yemen. The paper further contributes by finding that information quality (InQy) and system quality (SyQy) can operate as potential triggers for the emergence of net benefits (Here, MCE). While not being included in the theoretical arguments of DeLone and McLean (2003) on IS success, we can consider InQy and SyQy as one of the essential constructs for explaining the existence of net benefits from AIS use. Accordingly, by expanding the theoretical development in the field of AIS success, this paper could serve as a springboard for further investigation into the subject.

Practically, the research model can serve as an instrument for SMEs to predict and assess the success of implemented AIS applications. The model's empirical analysis and results could be valuable for SMEs’ managers/owners to understand the significant role of AIS success in increasing MCE. Additionally, since many Yemeni SMEs still rely on traditional manual accounting systems (Al-Hattami et al., 2021c), this research could help them understand the benefits of AIS and its significant impact on MCE. This, in turn, may encourage them to transform to AIS. In fact, using AIS, SME managers/owners can monitor and control various transactions, consider problems, take corrective action and make decisions. Moreover, it allows management to reveal deviations, analyze their causes and treat them.

On the other hand, this paper provides practical guidance for the government on the significance of AIS success among SMEs and its role in the country's economic development. SMEs are acknowledged to play a significant role in the country's economic development because they employ a substantial percentage of the workforce, contribute to GDP, reduce poverty, improve income distribution, among others (UNCTAD, 2017; ILO, 2018; Mohammad, 2018; Fan et al., 2021; Al-Hattami et al., 2021c). As a result, governments worldwide focus on growing the SME sector to promote economic development (Ilavarasan, 2017). Government support plays a significant role in improving the performance of these firms (SMEs). For example, from a technological aspect, government support plays an essential role in speeding up IT adoption among SMEs, particularly in emerging economies (Kareem et al., 2019).

Indeed, the research model shown in Figure 2 demonstrated that Yemeni SMEs could improve their management control effectiveness and succeed by utilizing AIS. This suggests that promoting AIS use among SMEs could effectively help this sector succeed and contribute to economic development in Yemen, an LDC. In this regard, the government could play a crucial role. Government should assist the adoption and use of AIS in SMEs to assure their success and survival, which would benefit the country's economic development. For instance, IS, including AIS, are notoriously expensive, particularly for SMEs (Kareem et al., 2019; Ruiz and Collazzo, 2021) in LDCs. This could have a negative impact on the adoption/using AIS in SMEs and benefit from them, leading to a failure (Mohammad, 2018). In Yemen, it has been reported that many SMEs have not yet adopted AIS in their business (Al-Hattami et al., 2021c). This could be due to different factors, the most important of which is the system's buying budget (Qureshi, 2020; Voss and Brettel, 2014; Consoli, 2012; Ghobakhloo et al., 2012; Ismail, 2009). In such instances, it is suggested that the government offer support, for example, a) offering financial assistance and/or giving low-interest or no-interest loans. b) Exempting from fees and taxes. c) Providing services of the Internet as well as a safe e-environment. d) Providing free AIS workshops and training programs. e) Enhancing research and development in the AIS field for SMEs.

Conclusion

AIS has become an essential part in all businesses as it supports data recording and financial reporting accurately and timely and plays a vital role in promoting MCE. This paper investigates the influence of AIS success on MCE in SMEs in LDCs, the Yemeni case. To this end, the D&M model developed by DeLone and McLean (2003) has been tested. When examining the literature, it was found that there is a lack of studies testing the D&M model to assess AIS success, especially in the SMEs context of LDCs such as Yemen. Therefore, this paper is of great importance to bridge the gap in the existing literature. Among eleven proposed hypotheses, AIS information quality, system quality, and usage positively influenced MCE. Quality of information and system positively influenced AIS usage and satisfaction, and user satisfaction positively influenced AIS usage. However, the study did not find any significant influence of service quality on AIS usage and satisfaction. Also, user satisfaction showed no significant effect on MCE. These results may assist SMEs to be more effective in the management control, more efficiently protecting their asset.

Limitations and future research

The current paper, like many others, has limitations. First, even though the research factors interpreted a large fraction of the variance in MCE, a portion of the variance remains uninterpreted. This could be due to other important factors not included in this paper, implying that more empirical and theoretical research is needed to recognize those factors. Second, the study results concluded that SrQy has no impact on UrSat and Usage; UrSat does not impact MCE. This justifies more research into retesting those associations in different contexts or scouting the mediating variables that may affect such associations. Third, the study targeted and defined SMEs as entities employing less than 50 based on the Yemen Ministry of Trade and Industry definition (YMIT, 2014). Therefore, the study results may not be generalizable to SMEs employing 50 and more; thus, further research is required. Lastly, this research has been conducted in a less developed Arab country. To promote generalization, making a comparison with various countries is welcome, with greater sample size and across a variety of languages and cultures.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.