Abstract

Angel investing has been transformed over the past two decades into a collective endeavour as angels have increasingly organised themselves into professionally-managed angel groups. A key role of the manager, typically termed the gatekeeper, is to undertake the initial screening of investment opportunities that the group attracts. We examine this activity through the lens of collective action using principal-agent theory to understand whether the gatekeeper (agent) acts in the best interests of the members (principal). Our study examines the gatekeeper’s approach to initial screening. Two different data gathering techniques were used to collect evidence from 21 gatekeepers representing 19 angel groups. First, verbal protocol analysis, which involved gatekeepers ‘thinking out loud’ as they undertook the initial screening of a potential funding opportunity, indicated that the majority did consider the shared interests of the members of the group, although in many cases this comprised only a small proportion of their overall comments. This could indicate the potential for moral hazard; however, the interview questions demonstrate that the gatekeepers focus on actions which increase the benefits for members. This requires that gatekeepers have a strong social relationship with group members to match their investment preferences with the types of investment opportunities that they ‘screen in’.

Introduction

The view that ‘entrepreneurship is embodied in the lone entrepreneur as if entrepreneurial acts could only be performed by single individuals’ (Lindgren and Packendorff, 2003: 96) is deeply entrenched in both academic and practical literatures, as well as in the media, and reflected in the dominance of research on the individual (e.g. entrepreneurial traits, personality, intrinsic motivation, cognitive skills and abilities) (Branzei et al., 2018). But the reality is that entrepreneurship is fundamentally collective (Dimov, 2007; Drakopoulou Dodd and Anderson, 2007; Johannisson, 2011). This individualised view is just as pervasive in the literature on other actors in the entrepreneurship process: their collective action practices have also been largely overlooked (Champenois et al., 2020; Teague et al., 2021).

Our focus is on the collective nature of angel investing. Business angels are high net worth individuals – typically cashed out entrepreneurs, corporate executives or business professionals – who invest their own money, either alone or with others, directly in unquoted businesses in which there is no family connection (Mason, 2006). Business angels play a critical role at the start of the entrepreneurial pipeline, providing the first external investment in ambitious start-ups, supplying them with the funding to make the transition from the concept and validation stages to revenue generation and early scaling. Many angel-backed start-ups go on to raise further rounds of finance from venture capital (VC) funds to accelerate their scaling process (British Business Bank, 2020). A small number of angel-backed companies have gone on to achieve ‘unicorn’ status, becoming anchor companies in their ecosystems. Other angel-backed firms do not offer or achieve the rapid growth required to attract VC investment. However, some of these businesses will be attractive strategic acquisitions for other companies (Mason et al., 2015).

Business angel investment activity has been transformed over the past two decades from an individual to a collective activity. Traditionally, angels invested informally, either on their own or with a few friends or business associates (Landström, 1992; Mason and Harrison, 1994; Wetzel, 1981). Over the past 25 years however, evidence suggests that angels have increasingly organised themselves into professionally managed groups with member numbers ranging from under 50 to upwards of 100 members (Gregson et al., 2013; Sohl, 2012; Mason et al., 2016). Yet, despite this fundamental transformation of the angel market, such groups have not attracted significant attention from scholars (Tenca et al., 2018). As Shane (2008) points out, angels who invest in groups are distinctive on a variety of dimensions, including demographics, amounts invested, investment instruments, terms of investment and follow-on investing. Bonini et al. (2018) confirm that the investment practices of members of angel groups are significantly different from those of unaffiliated angels. Mason et al. (2019) have identified several implications of the emergence of angel groups that undermine our understanding of the angel investment process which remains largely based on research on individual angels. Specifically, we lack evidence on how collective action – coordinated actions by individuals acting voluntarily to create value in the interests of the group (Castellanza, 2022; Olson, 1965) – influences the way in which business angel groups operate, and, critically, how this shapes their investment process and decision-making. The specific focus of this study is to investigate how collective action affects the way in which the initial screening stage is conducted, that is, the stage at which the gatekeeper selects those opportunities which they think will be of potential interest to their members.

Business angel groups: A collective action perspective

Studies of entrepreneurship as a collective phenomenon are characterised by both a proliferation of terminology and the variety of sites in which it occurs (Nordstrom and Jennings, 2015). Scholars have highlighted key distinctions between (i) collective actions undertaken by independent firms (e.g. to create, organise or protect common resources) (Doh et al., 2019; Meyer, 2020; Wigger and Shepherd, 2020), (ii) community-centred collective action by inter-dependent actors (Rae and Blenker, 2023), both placed-based, such as entrepreneurial ecosystems, and user-based communities and (iii) collective action by individuals, for example, working in entrepreneurial teams (Yang et al., 2020). Our focus is on collective action by individuals, that is ‘the conditions under which individuals might co-operate to pursue common goals because they believe that pooling resources and co-ordinating strategies with like-minded actors can achieve certain goals more efficiently’ (Johnson and Prakash, 2007: 226). This action is voluntary.

Collective action by individuals occurs across economy and society (e.g., studies of collective action in anthropology, political science and environmental management: DeMarrais and Earle, 2017). It is typically institutionalised through the creation of an informal or formal organisation (Hargreave and Van de Van, 2006). These organisations often require a co-ordinating mechanism in order to achieve their common goal. Group members may, therefore, enter into a contract with an individual to provide services for which they receive tangible or intangible remuneration to perform this ‘co-ordination’ or ‘orchestration’ role (Brown, 2015; Olson, 1965). This makes the concept of agency central to the understanding of collective action (Cleaver, 2007). The goals of the members – the principals – and the co-ordinator – the agent – are always intended to be similar. However, the interests of the two parties do not always correspond. Agents may be tempted to engage in self-serving behaviour rather than pursuing the group’s mission, strategic objectives and value-maximisation goals, giving rise to moral hazard in which the principal(s) cannot observe the relevant actions undertaken by the agent which might result in outcomes that are not in their interests, specifically adverse selection (Klonowski, 2015; Landström, 2023). This leads Johnson and Prakash (2007: 232) to observe that ‘agency conflicts are pervasive in collective endeavors’.

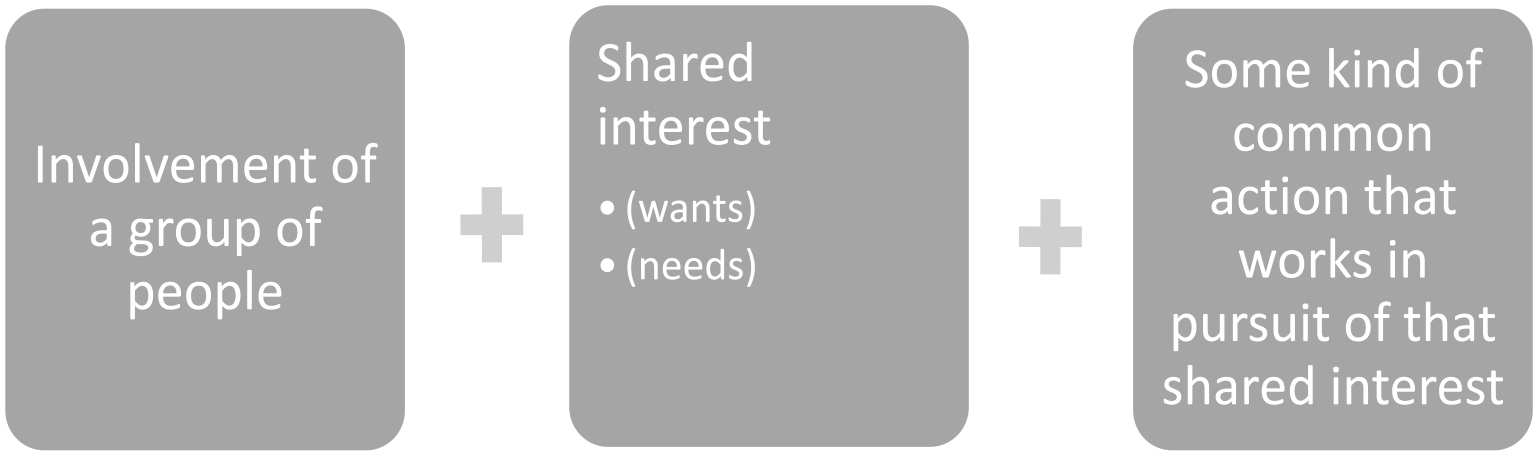

Meinzen-Dick et al. (2004: 200) define collective action as ‘the involvement of a group of people, . . . a shared interest within the group, and . . .. some kind of common action that works in pursuit of that shared interest.’ Business angel groups exhibit these features. They involve a clearly defined group of people, in this case, angel investors who decide that it is in their self-interest to collaborate as a group to invest in entrepreneurial businesses to maximise the benefits to themselves. Angel group members have a shared interest in improving the quality and quality of deal-flow, making better investment decisions, enhancing the post-investment support of their investee companies and ultimately achieving exits that generate significant capital gain (Mason and Botelho, 2014). These outcomes are more effectively achieved by investing collectively rather than individually (Paul and Whittam, 2010; Shane, 2008). Membership of an angel group enables individuals to develop a diversified portfolio of investments (by investing, say £100,000 across five businesses alongside other group members rather than in a single business in which they are the only investor). The visibility of angel groups and their networks generates a larger and better quality of deal flow. The administrative support enables more efficient management of the various stages in the investment process. Pooling the knowledge and expertise of group members offers a wider set of insights and interpretations, provides more effective screening and selection of investments, assists individual members to test and validate the accuracy of their own judgements and enhances the collective ability of the group to provide more effective post-investment support. Novice and less-experienced angels derive particular learning benefits from membership of angel groups. Transaction costs are reduced and efficiency is increased as groups build up knowledge that enables the development of effective due diligence procedures and standardised investment documents. All of these features contribute to risk reduction. Angels also highlight the social benefits arising from networking with other angels. These benefits – notably increased overall investment, portfolio diversification (with a moderate level of diversification having a beneficial impact on returns), better quality deal flow, access to superior information and the expertise of other angels, and lower due diligence and transaction costs – have been identified in several studies (Antretter et al., 2020; Bonini et al., 2018; Kerr et al., 2014).

A further shared benefit is that by pooling their financial resources angel groups have the ‘deeper pockets’ required to be able to make both larger initial investments and follow-on investments. This enables members to invest in deals that they could not invest in on their own. Investing as a group also reduces the power asymmetries with VC funds who, as follow-on investors in a business, can largely dictate investment terms, notably the valuation and deal structures that they offer to angels (Hellmann and Thiele, 2015). This has been described as a ‘burned angels’ problem (Leavitt, 2004). One angel, quoted by Shane (2008: 175), commented that ‘you are more likely to get crushed by venture capitalists in a later round if you invest as an individual.’ Angels are particularly vulnerable in the event of down rounds where their shares are re-priced below the initial price that they paid and their shareholding is diluted if they are unable to ‘follow their money’. This was particularly evident during and after the dotcom crash and was a significant driver for the creation of angel groups (Mason et al., 2016).

Common action is conducted to pursue these shared interests of the group. Angel groups organise their investment activities in a variety of ways (Sohl, 2007). However, there is typically a co-ordinator – termed the ‘gatekeeper’ (Paul and Whittam, 2010) – who undertakes the external-facing functions, notably building networks to attract deal flow, orchestrating the internal functioning of the group, working with members, particularly the core members of the group, facilitating the investment process, managing information flows and reporting on the performance of investee businesses. Some groups are member-led with a founding member taking on the gatekeeper role. In other cases, particularly larger groups where the gatekeeper role is too onerous for a member-gatekeeper to perform, the group hires a professional manager who may be supported by administrative staff to handle day-to-day work. Groups often evolve from being member-led to manager-led as they increase in size (Paul and Whittam, 2010). Paul and Whittam (2010: 246) observe that gatekeepers have a variety of industrial, commercial and professional backgrounds which does ‘not lend themselves to easy categorisation’. The variety of backgrounds of gatekeepers is confirmed by Mason et al. (2013). Just under half reported that they had worked in banking, accountancy or corporate finance, giving them experience of working in financial roles with growing businesses. Just over half (52%) had entrepreneurial experience. These experiences provide a strong indication for an economic drive embedded in the gatekeeper role.

The key responsibility of gatekeepers is to undertake the initial screening of investment opportunities that the group receives, assessing their fit with the group’s investment criteria (Paul and Whittam, 2010) and deciding which of them have sufficient merit to be of potential interest to members of the group. This will often involve meeting with entrepreneurs. As Paul and Whittam (2010) note, members depend on the gatekeeper to conduct initial assessments of potential investment opportunities so that ‘they do not have to get involved in the messy work of screening hundreds of candidates . . .’ (May 2002: 339). Those opportunities that pass the gatekeeper’s screening process are then invited to pitch to the group. Gatekeepers often work with entrepreneurs to help them prepare, improve and refine their pitches (Harrison and Chen, 2022). For those opportunities that attract sufficient interest from members a subset is typically established to undertake due diligence in order to decide whether or not to recommend it to the wider group to invest. It is important to emphasise that the angel group does not invest as an entity: each member makes their own investment decision and makes their own investment. 1 Hence, each investment that a group makes will normally comprise a different mix of angels. However, some groups operate a ‘side-car fund’ – a pooled investment vehicle that raises investment from passive investors to invest alongside the angel group, giving it greater financial firepower. Members cover the group’s running cost – typically in the form of an annual membership fee but may alternatively or additionally comprise a charge on each investment that is paid by either the entrepreneur or the investor and a performance fee levied at exit. Investors in sidecar funds are charged a management fee and sometimes also a performance fee. Some groups also attract corporate sponsorship. The members who perform specific roles in the investment process on behalf of the group, such as undertaking due diligence or as lead investor, do not normally receive remuneration.

The gatekeeper’s orchestrator role in angel groups creates potential agency problems. The gatekeeper (agent) is expected to perform their role of selecting investment opportunities on behalf of the members (principal) that they will find attractive to invest in. It is essential for the group to flourish that the members are satisfied with the quality of the investment opportunities that they receive and goodness of fit with their investment preferences. However, gatekeepers may act in their own self-interest, substituting their preferences for those of the principals (Johnson and Prakash, 2007), applying their own investment criteria to their investment selection, or putting forward deals that interest them, or that they have connections with, rather than based on the collective investment preferences of the group. This misalignment of interest can create moral hazard. However, the evidence for moral hazard – which is anecdotal – is inconsistent. But even if the gatekeeper does not act in their own self-interest in screening investment opportunities there may nevertheless be a misalignment of judgement between them and the members of the group on what constitutes a ‘good’ investment opportunity.

Misalignment would be expected to be reduced if gatekeepers invest alongside group members. Having ‘skin in the game’ reduces information asymmetries and aligns the interests of the gatekeeper with those of their members thereby, reducing moral hazard (Croce et al., 2020; White and Dumay, 2020). Conversely, if gatekeepers invest in opportunities outside of the group this would be expected to increase the risk of moral hazard. Gatekeepers might not share the deals that they invest in with the group and prioritise their efforts on their own investments rather than those of the group. Gatekeepers might present opportunities to their members that they have previously invested as this would allow these ventures to raise additional funding, instead of ‘offering’ investment proposals that are more suitable to their members. One of the gatekeepers interviewed by Paul and Whittam (2010: 247) commented that ‘you have to invest in all or none otherwise that would be a conflict of interest’. However, there was no consensus amongst their interviewees whether gatekeepers investing alongside members creates a conflict of interest. Moreover, gatekeepers may initially invest in the group’s deals – when the group’s investment capacity is limited – but stop investing as the membership grows in size. In contrast to member-gatekeepers, manager-gatekeepers may not have the personal wealth to make investments (Paul and Whittam, 2010).

In this article, we consider this potential agency problem in the operation of angel groups. Early studies of business angels adopted an agency perspective but in the context of the investor-entrepreneur relationship (Landström, 1992; Fiet, 1995; Kelly and Hay, 2003; Van Osnabrugge, 2000); however, it has not previously been applied to the study of angel groups. Our research question is therefore, as follows: does the approach taken by the agent reflect the interests of the principal? Or is there a misalignment of interests? This question is examined in the context of the initial screening stage of the investment process. The specific research questions are as follows. First, to what extent do gatekeepers reflect and demonstrate their group’s collective interests when undertaking the initial screening of investment opportunities? Second, what actions do gatekeepers take in the pursuit of the shared interests of the group? The challenges of conducting empirical research on collective action have been highlighted in the broader literature on account of the complexity of interactions. We examine these questions using a real-time methodology of how angel group gatekeepers perform the initial screening of investment opportunities on behalf of group members, complemented by interviews with a sample of gatekeepers.

Methodology

We adopt a practice perspective, an activity-oriented approach that is a means of developing detailed insights into complex actions, processes, relationships and interactions of practitioners. It focuses on understanding what people really do (Teague et al., 2021; Thompson and Byrne, 2022; Thompson et al., 2022), in this context, the ‘doing’ involved in making investment decisions. As Gartner et al. (2016: 813) note, this is ‘a valid means of understanding how people do things on an individual basis, a collective level and the actions that navigate the space between the two’.

The study was undertaken in Scotland and Northern Ireland. It is based on data gathered from 21 gatekeepers of 18 angel groups based in Scotland and one angel group in Northern Ireland. In three groups, the gatekeeper role was shared by two individuals. In two cases, these individuals were interviewed separately; in the third, both gatekeepers were present. The participating groups included all 16 of the members of LINC Scotland (recently re-branded Angel Capital Scotland) – the business angel trade association – that were publicly listed on its web site at the time that the research was undertaken. Two additional groups were identified through media and snowballing. LINC Scotland estimated that these groups collectively had about 700 investors in total. Of the 18 Scottish-based angel groups interviewed for this study, one-third (six) were three years old or less. Membership ranged from less than 10 to over 400. Scotland has eight of the UK’s most active angel groups (Young Company Finance, 2022) and so is a particularly appropriate geographical context in which to undertake the study. Securing the participation of such a high proportion of angel groups in the Scottish market was a considerable achievement. In many cases the initial response was not positive and follow-up approaches were required. The consequence was that the recruitment process took 3 months. It started with an initial email to the gatekeeper to request an interview. In several cases, it was not possible to identify the gatekeeper, but in these cases the recipient of the email forwarded it to the relevant individual. In 19 cases data were gathered in face-to-face meetings and two were conducted online. They ranged in length from 37 to 93 minutes, with the average being about 1 hour. All respondents agreed that the discussions could be recorded for later transcribing. The face-to-face meetings took place at a location of the interviewee’s convenience. Venues included the group’s office, coffee shops and in the office of one of the authors. We agreed with participants that information on individual groups would not be disclosed and that findings would be aggregated.

It is widely acknowledged that there are inconsistencies between attitude and behaviour (Ajzen et al., 2018; Kraus, 1995). It therefore, cannot be assumed that there is a relationship between what people say they do and what they actually do. Hence, as entrepreneur-as-practice scholars note, actions cannot be fully put into words. Accordingly, there is a need to move beyond an exclusive reliance on conventional interviewing – which has the risk that it becomes an artificial conversation – with a wider methodological repertoire of more immersive data collection techniques that get participants to reveal the more tacit elements of their practice (Liuberté and Feuls, 2022; Thompson and Byrne, 2022; Thompson et al., 2022). This issue has also been acknowledged in angel research, with previous studies of business angel decision-making highlighting inconsistencies between what investors say they do and the actions that they take (Mason and Botelho, 2016). Accordingly, we tested how gatekeepers would behave in a hypothetical – albeit realistic – situation. In this study we used verbal protocols (Ericsson and Simon, 1993), a real-time technique asks participants to ‘think out loud’ while they perform a routine task, in this case the initial screening of an investment opportunity. It is important to emphasise that although it was a hypothetical situation, it required gatekeepers to accurately simulate how they performed the initial appraisal of investment opportunities. Verbal protocol analysis (VPA) has been used successfully to examine the decision-making process of both venture capitalists and business angels (Hall and Hofer, 1993; Harrison et al., 2015; Mason and Stark, 2004) and has also been applied in a variety of other academic contexts (Green, 1998).

Each respondent was shown a current real investment opportunity which was sourced from a business angel network in England. The selection of an English case was intended to minimise the risk that the Scottish gatekeepers would be familiar with the business. It was given a fictitious name to protect its anonymity. The angels were asked to read the opportunity in the same way that they would normally read an investment proposal but verbalise their thoughts as they did so. The instruction given was to say aloud the thoughts that came into their mind. Respondents were not required to provide any explanations or verbal descriptions (Ericsson and Simon, 1993). One of the authors was present as each respondent performed this task and prompted them to think aloud if they lapsed into silence for more than 10 seconds. A short de-briefing session was then undertaken with each investor after completion of the evaluation which asked them to reflect on how the group membership affected their approach to initial screening.

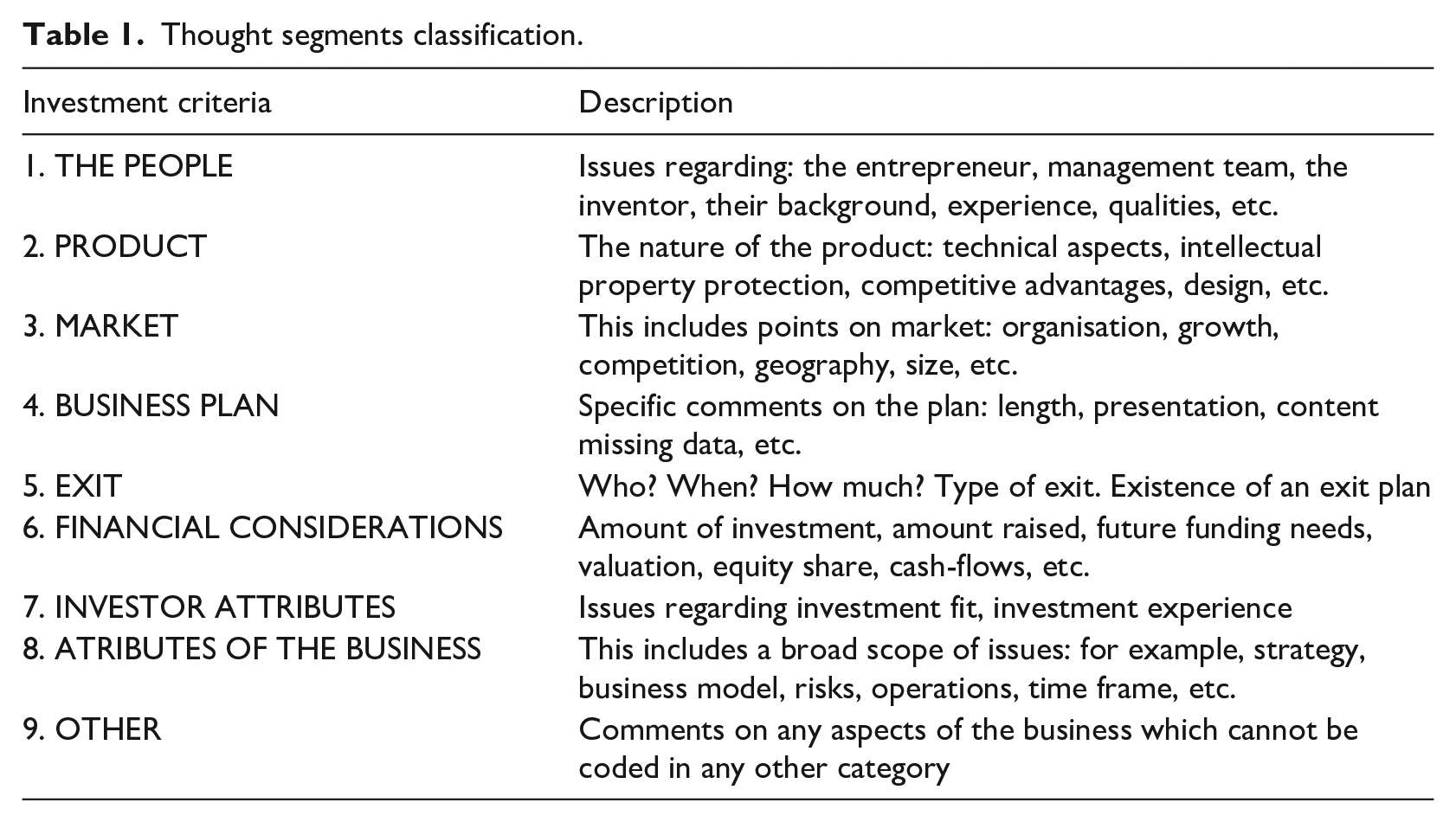

The verbalisations of each respondent were recorded and transcribed, and then the content was analysed in a two-step process. First, thought units were independently classified by the authors, using a well-established coding scheme (Botelho et al., 2023; Harrison et al., 2015, 2016; Mason and Botelho, 2016; Zacharakis and Meyer, 1995). This coding scheme focuses on the investment criteria utilised by angel investor while screening an investment opportunity (Table 1). The frequency counts for each of the investment criteria were aggregated and ranked. In the second step, the same thought units were coded according to the level of collectivism of each statement as indicated by the words: ‘we’, ‘us’, ‘members’, ‘investors’, ‘group’ and ‘angels’. The outcome was that every thought unit had two types of codes: (i) investment criteria; and (ii) if it reflected an individual or collective statement. This methodology provides a more reliable and richer understanding of the decision-making process of investors and the criteria used to evaluate investment opportunities than is possible from approaches using questionnaires, surveys and interviews (Shepherd and Zacharakis, 1999) which are subject to conscious or unconscious errors associated with post-hoc rationalisation and recall bias.

Thought segments classification.

Nevertheless, VPA has some limitations. Specifically, some respondents may be uncomfortable or self-conscious about thinking and speaking out loud which may distort their verbalisation. And it is impossible to entirely remove the effect of the artificiality of the situation. However, Ericsson and Simon (1993) argue that VPA is a valuable method for analysing decision-making as long as the following criteria are met: the information reported must be the focus of attention, the task is not highly routinised by habit, there must be only a short time between performance and verbalisation, verbalisation does not require excessive encoding, reports are oral, subjects are free from distraction, instructions are clear and completeness in reporting is encouraged. These conditions are all met in this study.

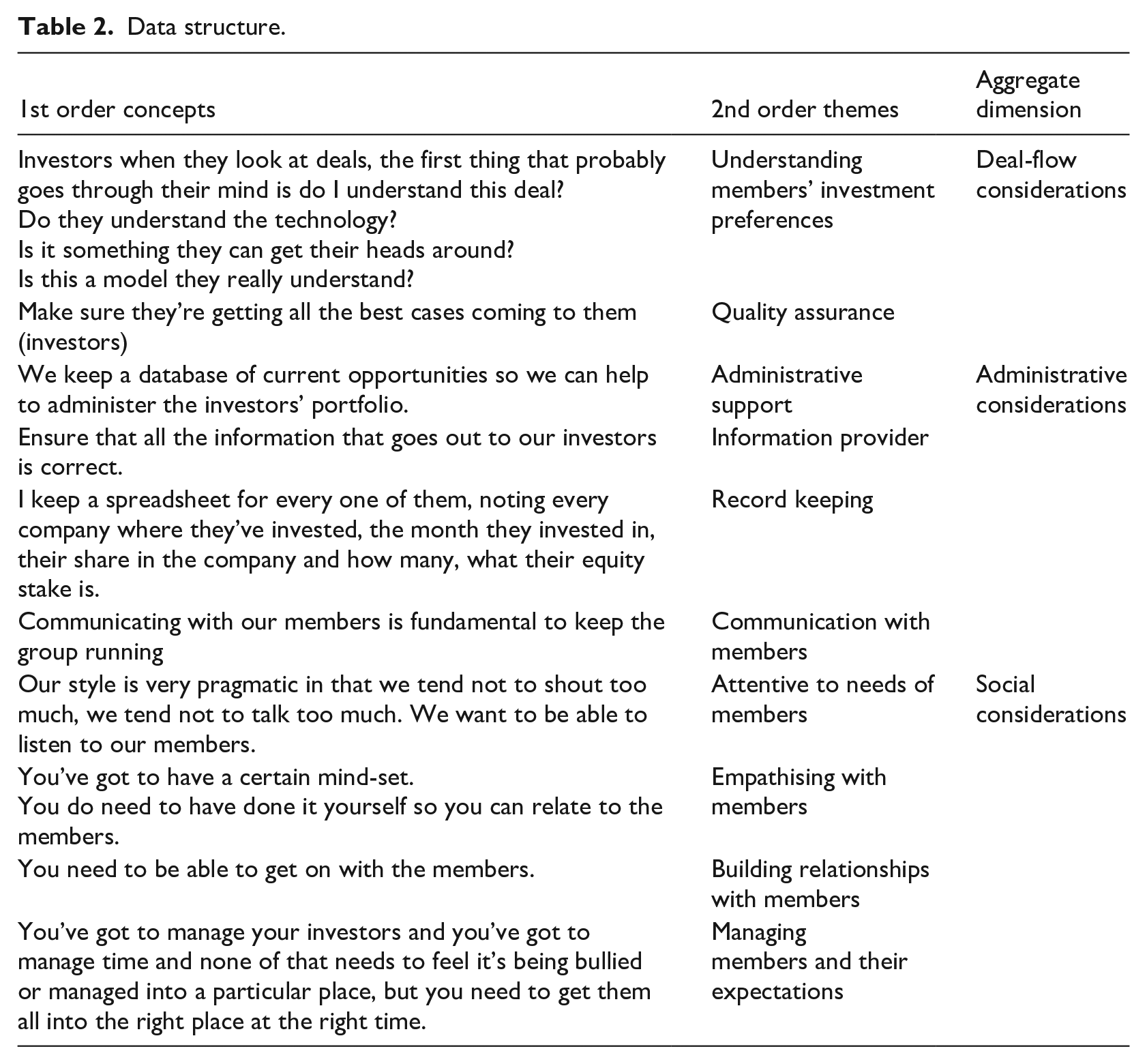

We complemented the verbal protocols by asking gatekeepers about the operation of the group, their management functions and role in the group’s activities, specifically the investment process. The purpose of these questions was to understand to what extent the gatekeepers recognise the collective nature of an angel group and whether they felt their role was focused on performing actions that enables the achievement of the shared interests of their members. This information complements the VPA data by providing a broader perspective of the gatekeeper’s activities and whether they are performed in the pursuit of a common goal that is aligned with member interests. These data were independently coded by the authors following the Gioia method (Gioia et al., 2013). This methodology was chosen as it enables the researcher to identify original insights on how participants perceive a particular phenomenon. In this case, the aim of the research was to identify those actions conducted by gatekeepers that reflect the collective nature of angel groups. Gioia et al. (2013) explain that this method was designed to enable the development of high-quality inductive research to enable researchers to rigorously generate new concepts. A coding scheme (Table 2) was developed to organise gatekeeper reflections on their roles, actions and interactions within their angel group.

Data structure.

This research design allows for an in-depth understanding of the collective nature of angel groups by focusing on the views of gatekeepers on their role and by capturing their decision-making approach. The combination of these two sources of data provides a unique perspective on how gatekeepers consciously think about their relationship with their members and whether and how their screening approach is shaped by the group’s membership.

Results and discussion

Verbal protocol analysis

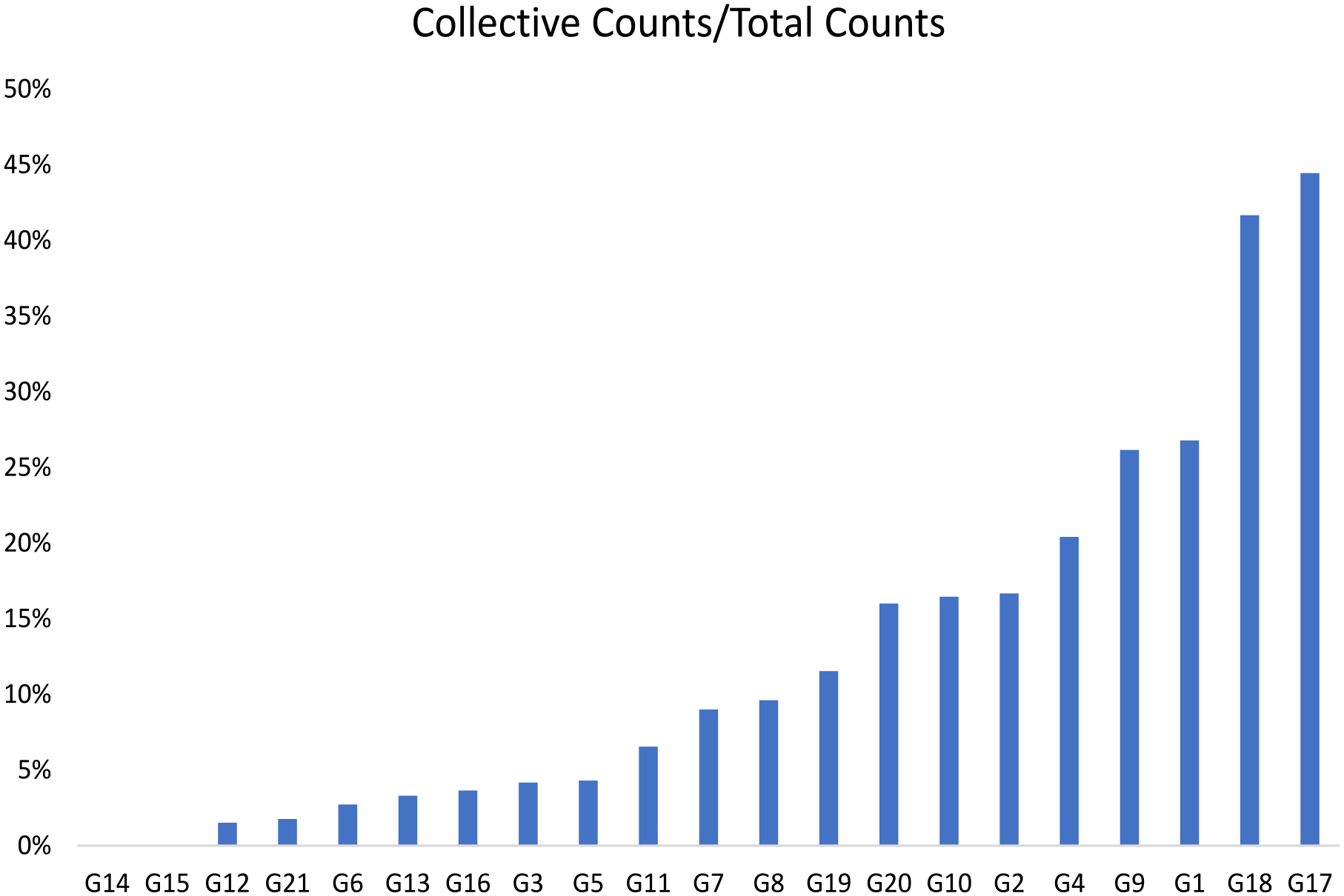

The transcripts for each of the 21 gatekeepers were divided into discrete thought units. A total of 1475 thought units were identified, of which only 136 (9%) related to shared interests with group members. These are thought units comprising statements that indicated that the gatekeepers were thinking about the group members. Figure 1 shows the collective counts per gatekeeper. It is apparent that there is considerable variation between gatekeepers in the extent to which their thought units reflected the shared interests of group members. Although the majority of gatekeepers (90%) expressed shared interests, in many cases these comprised only a small proportion of their overall comments. Indeed, more than half (57%) of the gatekeepers made fewer than 10% of their comments that reflected the shared interest of the group. There were just five gatekeepers who were very focused on their group’s shared interests, comprising 25% or more of their comments. These gatekeepers accounted for 38% of all the shared interest comments. The approach of one of these collective-oriented gatekeepers is captured as follows: ‘I like it because it’s a technology somebody could understand; I think they would quite like it so I would like to have the member’s opinion on it’ (GK17).

Mentions of collective views by the gatekeepers.

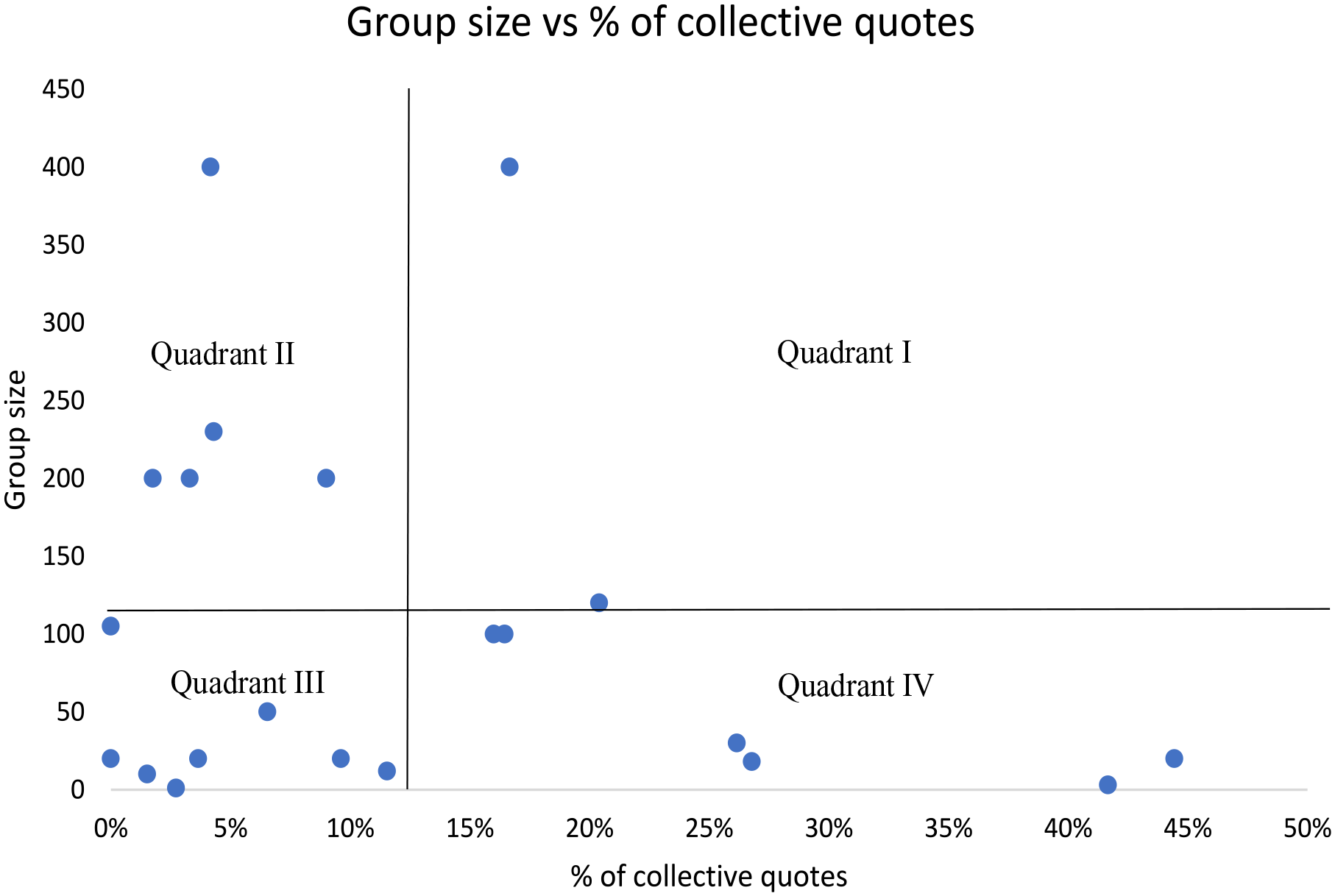

A possible explanation for the variability in the shared interest scores of gatekeepers being that it reflects the heterogeneity of the business angel population (Botelho, 2017; Sørheim and Botelho, 2016), angel groups and the backgrounds of gatekeepers. To better understand the impact of this heterogeneity on the collective approach of gatekeepers, we use a dispersion measure to cluster the results along two dimensions: shared interest scores and membership size (Figure 2). We have classified groups into four quadrants using half of the range of values as the threshold level. This approach follows Sarstedt and Mooi’s (2014) suggestion on how groups can be identified within data. To do so, we used the median score in each quadrant to examine whether the four quadrants are able to differentiate the sample on the basis of group size.

Group size versus % of collective quotes.

It might have been expected that the gatekeepers of smaller angel groups would have a stronger collective mindset which would be reflected in a higher number and proportion of shared interest thought units. This would be consistent with the literature on the effects of group size in various contexts. For example, Wheelan (2009) found that larger groups have greater difficulty establishing trust amongst their members. Other studies (Bales and Borgatta 1955; Kelley and Thibaut 1954) have found lower member satisfaction and cooperation as an effect of larger group size (Kerr, 1989; Sato, 1988). Studies have also found that group size has an effect on cohesion, trust, commitment, and sense of belonging (Soboroff, 2012). However, the majority of angel groups (38%) are in quadrant 3 (low shared interest score, small group size) on account of their low shared interest scores (below 10% of shared interest scores) and small size of membership (smaller than 100 members) and 61% of groups are in quadrants 2 and 3 (low shared interest scores), indicating that regardless of group size the vast majority of gatekeepers are not focused on their group’s shared interests. Moreover, no relationship between size of group and thought units relating to shared interests was identified 2 (Figure 2). Nevertheless, when compared with their counterparts in smaller groups, gatekeepers of bigger groups are less likely to score above the median of shared interest thought units. Only 29% of the gatekeepers of large groups were in the first quadrant (high shared interest score, high group size) while 43% of the gatekeepers of smaller groups were in the fourth quadrant (high shared interest score, small group size). The thought units that reflected a shared view were classified according to the specific investment criterion coding scheme used in previous VPA studies. The coding scheme consisted of eight codes related to specific investment criteria, with two further codes used when the thought unit referred to an action or to something other than an investment criterion. Each of the eight investment criteria had further layers of coding.

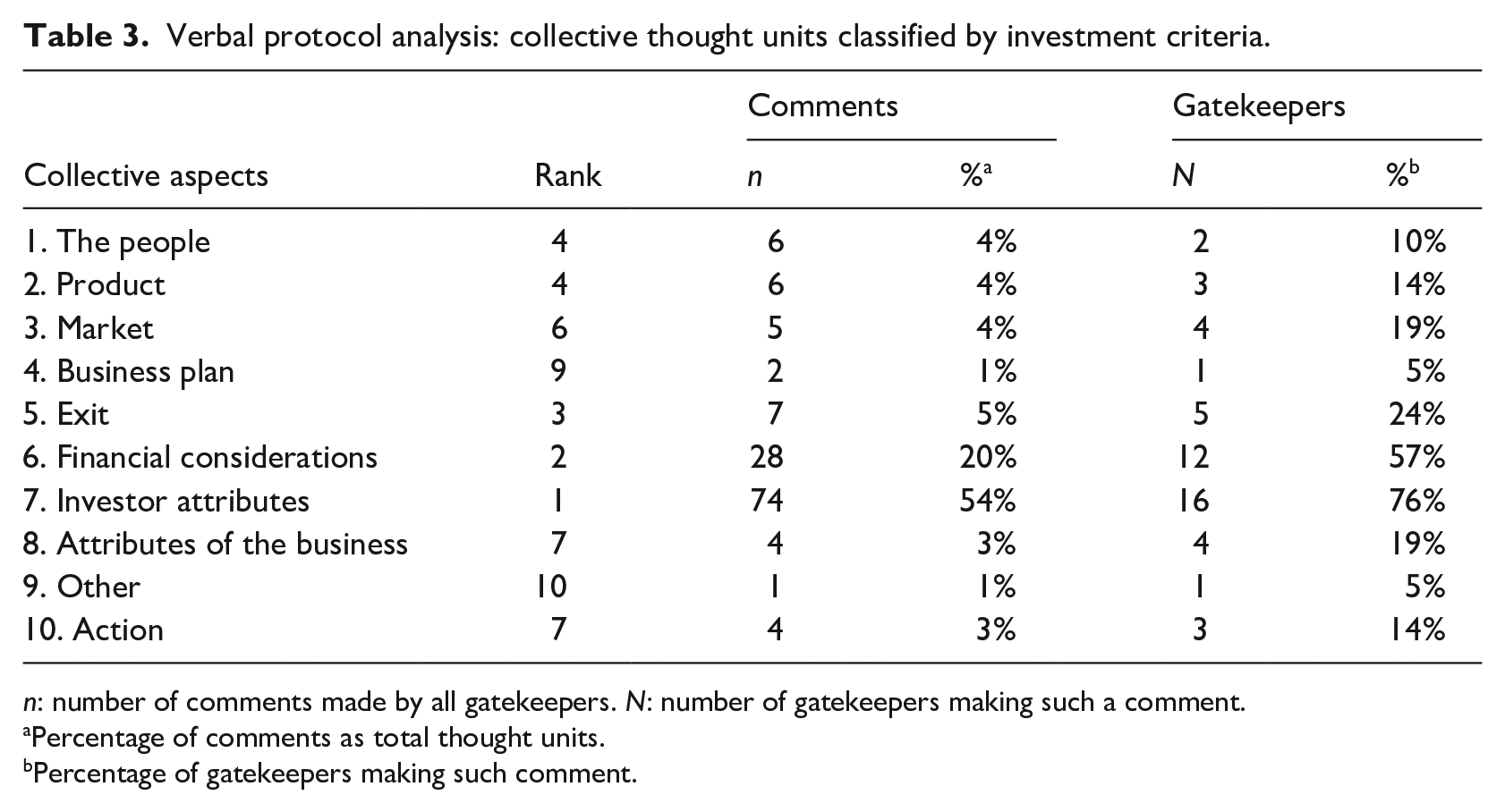

Previous VPA studies of the initial screening process have shown that business angels take into account a wide range of criteria when considering opportunities at the initial screening stage (Mason and Rogers, 1997; Mason and Stark, 2004). In contrast to these studies, the thought units of gatekeepers that related to shared interests of the group were concentrated around a narrow range of investment criteria. The first level coding revealed that just three investment criteria accounted for around 80% of these thought units with investor attributes the most significant criterion followed by financial considerations and exit (Table 3).

Verbal protocol analysis: collective thought units classified by investment criteria.

n: number of comments made by all gatekeepers. N: number of gatekeepers making such a comment.

Percentage of comments as total thought units.

Percentage of gatekeepers making such comment.

One possible explanation why gatekeepers focus on these three investment criteria is that they find it easier to incorporate into their own screening processes the objective views of their members regarding the types of businesses in which they would have investment interest, such as sector, amount requested, location, valuation, number of funding rounds and exit plan. This objective approach can be illustrated by the following quote from a gatekeeper: ‘the amount that they’re looking for is not unmanageable in terms of where we are, then looking to take it from more than one investor so it does fit in our sweet spot’ (GK1). And at the same time, it could also reflect the subjective nature of other investment criteria, notably the people, which was mentioned by only two gatekeepers. Moreover, in these cases, the references that the gatekeepers made were to objective features of the entrepreneur/people rather than their character or personality. One of the gatekeepers commented that ‘it is always better if the members can see that the founders have put some of their own money in’ (GK8). A similar approach was evident in the comments regarding the business plan, with gatekeepers focusing on its presence rather than presentational or content issues. An illustrative quote was as follows: ‘our members must see and check the business plan, that is our starting point’ (GK11).

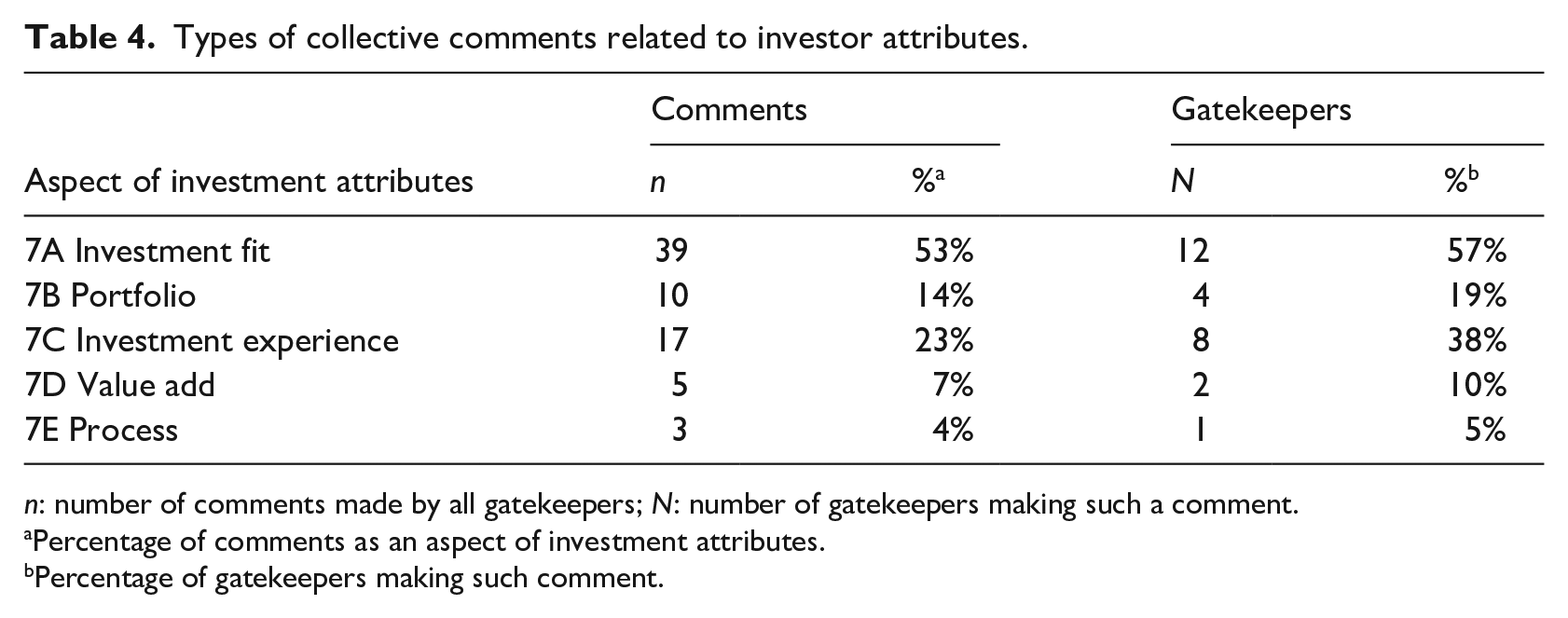

Investor attributes is the top investment criteria mentioned by gatekeepers (see Table 3). Disaggregating further (Table 4) reveals that the highest share of comments related to investment fit (how suitable is the opportunity to the investment preferences of group members), which accounts for just over half (53%) of all collective action comments on investor attributes, and is mentioned by more than half of all gatekeepers (57%). This is followed by the investment experience of members, comprising 23% of investor attributes comments, and mentioned by 8 gatekeepers (38%). The investment portfolio of members was also an important consideration for gatekeepers, accounting for 14% of investor attributes comments and mentioned by 4 gatekeepers (19%). Once again, this indicates that gatekeepers focus on objective factors, specifically investor preferences (fit) but also their investment experience and investment portfolios. This highlights that all three dimensions identified during the interviews (see Table 2) are interrelated: in order to be able to understand in what their members may wish to invest, gatekeepers have to develop social relationships with them while keeping detailed records of their preferred previous investments.

Types of collective comments related to investor attributes.

n: number of comments made by all gatekeepers; N: number of gatekeepers making such a comment.

Percentage of comments as an aspect of investment attributes.

Percentage of gatekeepers making such comment.

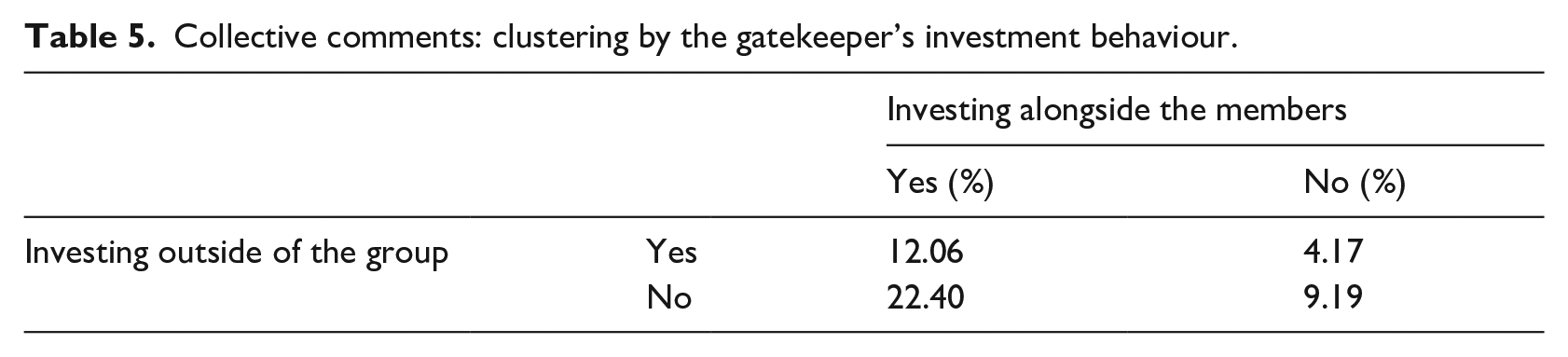

To further understand the possibility of misalignments of interest we examined whether gatekeepers have invested alongside the group members or invested independently of the group. The expectation is that gatekeepers who have invested alongside the group members should present higher levels of shared interested than those who have not. In contrast, gatekeepers who exclusively invested in opportunities outside of the group would exhibit a lower level of shared interest. Our results support these expectations (Table 5). Investing alongside the group increases the collective action score: in other words, gatekeepers who have invested with group members are more likely to think about them when screening investment opportunities. Furthermore, gatekeepers who invest exclusively with the group have the highest collective action score. In contrast, gatekeepers who invest exclusively outside of the group and do not invest with the group, have the lowest collective action score, indicating that they are less likely to think about the members than gatekeepers who invest with the group. This suggests that gatekeepers in this category are more likely to prioritise their own interest rather than the group’s interests.

Collective comments: clustering by the gatekeeper’s investment behaviour.

Interview evidence

The majority of respondents (62%) did not acknowledge the collective nature of their gatekeeper activities when asked about their role and skills to perform the role. Their responses were dominated by an emphasis on their own investment experience in shaping their activities rather than on their interactions with the members and consideration of their interests. For example, one participant stated that ‘my previous experience as a successful entrepreneur allowed me to be fully prepared to play this role’ (GK8). Other participants focused on their personal skills and knowledge in performing their activities on behalf of the group. One gatekeeper commented that ‘in everything I do for the group, I need to have financial awareness, financial and commercial awareness which is really handy’ (GK15).

The other gatekeepers (38%), in contrast, did show clear signs of strong collective awareness. Three main dimensions of their collective action were apparent (Table 2). The first is deal-flow considerations. These gatekeepers recognised their need to understand the investment preferences of their members in order to select the types of investment opportunities to be presented to the group that would be of potential interest to them. Additionally, they understood that their members saw them as a means of ensuring that the investment opportunities presented to the group would be of a high quality. The second dimension identified by these gatekeepers was administrative considerations. This focused on management activities that generate benefits for members of the group, notably the management of information. Significantly, these benefits go beyond managing the investee companies in the portfolio to include managing information on opportunities and investments on behalf of members. 3 The third dimension of the collective nature of the gatekeeper role was social. This focused on generating a sense of community amongst the group members. Gatekeepers described this dimension as a relationship building process that enabled them to empathise with members and understand their broader expectations of membership.

These findings are consistent with the existing angel literature that highlights the benefits of being part of an angel group (Mason and Botelho, 2014) and describes the gatekeeper role (Mason et al., 2016; Paul and Whittam, 2010). However, by identifying and conceptualising the actions that gatekeepers take that reflect the group’s shared interests – which we classify along three dimensions – our findings expand the insights of previous studies. Whereas such studies have focused on the overall benefits provided by angel groups for their members, our research conceptualises the actions undertaken by the gatekeepers in the pursuit of the shared interest of the members. Our specific contribution is to distinguish the separate actions of gatekeepers for the collective benefit of the members from those that are undertaken to benefit the growth and sustainability of the organisation (group).

Discussion

The results from this study could be interpreted as indicating that most angel groups are led by a gatekeeper driven by their own self-interest not informed by the shared views of their members. In other words, they do not perform their role with a collective mindset. First, our VPA results show that only a very small number of thought units (9%) reflected the group’s shared interests. Additionally, most gatekeepers (57%) made very few comments that reflected the interests of their members while screening an investment opportunity. Second, less than half of the gatekeepers (38%) recognised the collective nature of their role. However, these findings should not be interpreted as indicating the failure of the collective action model (Meinzen-Dick et al., 2004) to correspond to how angel groups operate. Rather, the findings suggest that in an angel group context, gatekeepers do not consider what they think the members want but what they think they need, which in this context is a supply of good investment opportunities. By using their own experience, rather than the desires (wants) of their members, gatekeepers aim to maximise the potential for their members to make investments in high quality businesses.

This enables us to suggest a variation from the original model of collective action which divides the shared views into wants and needs. Knowing what members want allows gatekeepers to recognise in their screening what might attract them to invest. Figure 3 depicts this variation to the original model. Additionally, most gatekeepers might not consciously verbalise their focus on the group’s shared interest as the investment preferences of members are already embedded in their screening approach. This is consistent with previous research that has identified cognitive biases in business angel decision-making (Harrison et al., 2015; Huang and Pearce, 2015). In summary, we do not find any evidence concerning the activities of gatekeepers that confirms the existence of moral hazard. Rather, the evidence indicates that the actions of gatekeepers focus on what they think are the group’s best interests

Collective action framework.

Conclusion

The growing recognition that entrepreneurship is a collective endeavour has not permeated the entrepreneurial finance literature where the individual continues to be the unit of analysis in studies of investment decision-making. This is particularly the case in studies of business angels, even though the emergence of angel groups over the past 25 years has transformed angel investing from an individual to a collective activity. Our focus in this article has been on the manager of the angel group – termed the gatekeeper – whose key role is to undertake the screening of investment opportunities where they are deciding which deals to reject and which to select for their members to consider in detail. Specifically, we consider whether the gatekeeper role creates an agency conflict in angel groups: does the approach taken by the agent (gatekeeper) reflect the interests of the principal(s) (members)? This would occur if the gatekeeper pursued self-serving behaviour, selecting investment opportunities based on their own preferences rather than those of the group, generating moral hazard.

Our first research question asked to what extent do gatekeepers reflect and demonstrate their group’s collective interests when undertaking the initial screening of investment opportunities? Using VPA, we find that gatekeepers do not consciously reflect the shared interests of group members while screening investment opportunities. Our second research question asked: what actions do gatekeepers take in the pursuit of the shared interests of the group? Responses to questions about their activities indicated that their focus is on providing benefits to their members. Nevertheless, their comments that reflected the shared interests of the group largely refer to objective investment criteria – investment fit with member interests, financial attributes of the business seeking finance and the exit. Whereas this could be interpreted as moral hazard, with gatekeepers acting in their self-interest, our analysis makes an important distinction between the collective actions that gatekeepers undertake that generate benefits for the organisation and those that benefit the members. Hence, although it might seem that the agent (gatekeeper) is not reflecting the shared interests of the group, they are acting in the best interest of the principal (members) by selecting what they consider to be high quality investment opportunities. Accordingly, we suggest that, following the distinction made by Campbell (1998), gatekeepers think about what they believe the group needs (satisfaction) rather than what their members want (desire) when undertaking the initial screening of the group’s deal flow. The way in which this translates into practice is that gatekeepers of angel groups focus on offering their members what they believe are good investment opportunities rather than the types of opportunities that their member might want. Gatekeepers justify this approach on the basis of their own investment experience. We further note that the commitment to the group is influenced by whether gatekeepers exclusively invest alongside the group or invest independently of the group. Gatekeepers who invest alongside the group have higher collective action scores than those who invest independently of the group.

We contribute to the collective action literature in three ways. First, we show that it is a suitable framework to examine angel group activity. Second, we identify the potential agency conflict that is created when a group appoints a co-ordinator (or orchestrator) to achieve their common goal. Third, we offer a more nuanced perspective on the actions that the gatekeepers undertake on behalf of the group. We find no evidence of moral hazard in which gatekeepers pursue their own self-interests when deciding what investment opportunities should be presented to the collective. However, we suggest that the concept of shared views requires to be divided in two dimensions: (i) wants; and (ii) needs. This allows for the differentiation of what the individual members believe they require (want) and what a decision maker of the collective (gatekeeper) considers to be the best for the group (needs). Commitment to the group is also influenced by whether gatekeepers invest exclusively with the group.

Our research provides clear evidence that collective action can be used as a suitable conceptual framework for angel group research, opening an avenue for future research. The main focus of this study is on the screening stage which is undertaken by the gatekeeper and so focuses on the action of gatekeepers. It does not look at member interactions. Hence, future research should explore the interactions between members, such as those that occur during pitching events, the due diligence process and in post-investment activities. Do investors focus on their own experience and opinions, or do they generate a joint ‘voice’ that reflects shared interests? And does the opinion of a more experienced investor influence other members? And what is the impact of the various digital tools that angel groups adopted during the Covid pandemic and have subsequently retained (Mason, 2022) on the interactions between gatekeepers and their members and between members? Has this weakened collective action?

Bonnet et al. (2022) have noted that the ‘survival and success of an angel group essentially depends on volunteer and member involvement in group management activities.’ A second line of research should therefore, evaluate whether the recruitment process of angel groups follows a strict protocol that focuses on those who are likely to share the interests of existing members. As groups typically only consider investment opportunities if there is relevant expertise within the group this approach could have significant implications for their investment capabilities (e.g. sector expertise, location, connections and capital availability).

Third, future research should look at the impact of group size on the development of shared interest. This study was not able to identify a statistically a significant relationship between size and shared interests. However, our findings indicate that gatekeepers of smaller groups are more likely to make higher shared interest comments. Hence, future studies could evaluate whether, and in what ways, group size has an influence on the pursuit of shared interests. And the effect of the group’s operational mode – which is likely to be related to size – should also be explored for its effect on collective action. Specifically, in the case of groups with an operational model that comprises core and peripheral members, in which the gatekeeper working closely with the inner core, it might be more appropriate to view the gatekeeper as being a principal. This suggests that in at least some angel groups the relationship is one of principal-principal rather than principal-agency (Chrisman et al., 2018; Young et al., 2008).

Fourth, future studies should look at other stages in the investment process to evaluate whether the common actions of both the gatekeeper and the members in the pursuit of shared interests become more significant. For example, during the post-investment stage does the interaction with the investee companies reflect the group’s shared interests? And is the pursuit of an exit based on the shared interest of all the group members who invested. Specifically, how do the entrepreneurs, angel investors and any other investors (e.g. VC funds) achieve a shared interest in the exit decision and to what extent does this involve collective action to achieve this outcome (Botelho et al., 2021)?

Finally, angel investing is a now a global activity. But in the light of differences between countries – especially between developed, emerging and developing countries – notably in composition of the angel population, institutions and cultural values (Harrison, 2017) – there is a need for research to examine how forms of collective action amongst angels might vary across the globe. Collective action between angel groups in different countries has also been identified as a key requirement to enable business angels to make cross-border investments (Mason et al., 2022). Accordingly, further research should examine the forms of collective action between angels groups in different countries and how they facilitate cross-border angel investing.

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This paper arises from research funded by the ESRC under its Co-funded Pilot scheme. The co-funders were NESTA, BVCA, Lloyds-TSB and Invest NI.