Abstract

How do failure events affect subsequent new venture creation? The existing literature seems to point in two opposing directions. While the information perspective suggests that failure events undermine collective beliefs about market viability, the competition view implies that failures may foster entrepreneurship via easing competition in both factor and product markets. To address this question, we adopt an inductive approach and analyse registry data in Norway. Based on the firm-level microdata, we construct an industry-region-level marketspace to analyse the number of firm failures and new ventures in different markets. Results show that failures of existing firms generally lead to more venture creation in the same market, albeit being contingent on industry features. And such effect is mainly ‘pulled’ by product market vacuum, rather than ‘pushed’ by factor abundance. However, we also observe that ventures that are created following failure events are less likely to survive.

Keywords

Introduction

New venture creation has long intrigued entrepreneurship scholars and policymakers (Barbieri and Rizzo, 2023; Delgado et al., 2010). While prior literature has explored various external conditions that foster or impede regional entrepreneurship (Acs et al., 2014; Stam and Van de Ven, 2021), one line of recent inquiry focuses on how prior failures of existing firms affect subsequent creation of new ventures (Soublière and Gehman, 2020). The conventional view suggests that failure events undermine entrepreneurial effort, as they undermine collective beliefs about the viability of a particular market (Johnson et al., 2021). That is, failure events act as an information signal that entrepreneurs and their stakeholders make use of to evaluate market potentials (Chai et al., 2022; Pontikes and Barnett, 2017). While this information perspective is plausible, it overlooks the competition effect (Kilduff et al., 2010) stemming from firm failures. First, failures may reduce competition in the factor market, as failed firms instantaneously release floating resources (labours, capital and channels) and entrepreneurial talents which can be used to create new ventures in the same field (Delacroix and Carroll, 1983; Mason and Harrison, 2006; Stuart and Sorenson, 2003). Second, failures can also ease competition in the product market (Chen and Miller, 2012), opening up more market gaps for entrepreneurship (Davidsson, 2015; Shane and Venkataraman, 2000). As a result, failure events may foster new venture creation, given their role in reducing the competition of factors and products.

To advance understanding of the actual effect of failure events on entrepreneurship, we employ an inductive approach (Schwab and Zhang, 2019) and conduct large-scale exploratory research. Specifically, based on firm-level microdata in Norway, we establish an industry-region-level marketspace to examine the number of firm failures and new ventures. Our results show evidence for a net positive relationship between these issues: when there are more prior firm failures in a market (as represented by a region-industry mix), more new ventures will be created. The effect is also found to be contingent on industry features, which influence the relative importance of the ‘information’ and ‘competition’ effects. By adopting this focus, this article contributes to research on new venture creation in general (Davidsson et al., 2020), and the role of failure events in entrepreneurship in particular (Soublière and Gehman, 2020). While prior studies mostly emphasise failure events as a negative signal for market actors (Chai et al., 2022; Pontikes and Barnett, 2017), we balance it by stressing that firm failures will also release market resources which can enable new venture creation. As such this study illustrates the two opposite mechanisms (i.e. information and competition), through which failure events may affect entrepreneurship. Moreover, our empirical context also enriches understanding of entrepreneurship in Norway given the dearth of evidence systematically examining the effect of failures in the Norwegian marketspace.

Endeavouring to understand potential mechanisms, we further explore whether these new ventures are pulled by product market opportunities, pushed by resource abundance in the factor market, or involve both issues. While firm failures can help reduce competition in both product and factor markets (Barney, 1986; Hoberg and Phillips, 2010), it remains unclear which one will be the driving force for entrepreneurship. To shed light on this, we analyse the founding features of new ventures. We assume that if they are driven by abundant resources available in the factor market, new ventures that are created following failure events will easily scale up their organisations (Kroezen and Heugens, 2019; Thakur, 1999); if being driven by more opportunities in the product market, they will easily scale up market revenues after entry (Gilbert et al., 2006). Our results show that these new ventures in the ‘tainted’ market have smaller organisational scales (i.e. fewer employees and less equity), but garner significantly larger market revenues at their first year of establishment. While not conclusive, this suggests that the positive association between failure events and new venture creation may be driven largely by the product market competition effect, rather than by the factor market competition effect. Meanwhile, their smaller organisational scales also hint the effect of information signalling: as entrepreneurs (and/or the factor markets) are concerned about the viability of a market with many failures, new businesses will be started with caution. Finally, emphasising distinction between short- and long-term performance (Wennberg et al., 2011), we also examine how these ventures perform in the long run. By analysing survival rates, we find that when ventures are created subsequent to more firm failures, they are more likely to fail. Altogether, our research suggests an interesting pattern: when many firms fail, they will leave a vacuum in the product market that attracts the creation of new ventures. Because of the temporary market vacuum, these new ventures can usually achieve a good short-term performance. However, they are likely to eventually, because a market with many failures may have some fundamental and structural issues, such as lack of supporting industries or demand (Delgado et al., 2010; Porter, 2008). These issues are less explicit on the surface but will be made manifest in the long term. To a certain extent, this may reflect the general short-termism of many entrepreneurs in the market (Lumpkin et al., 2010). While they all aspire to be phoenix rising from the ashes, oftentimes they end up quickly burning themselves.

Literature

A central objective of entrepreneurship research is to understand how social and economic conditions promote or impede new venture creation (Acs et al., 2014; Shane and Venkataraman, 2000). Scholars have identified an extensive list of external antecedents to the formation of new ventures including cluster structure (Delgado et al., 2010), tax policies (Friske and Zachary, 2019) and regional opportunities (Verheul et al., 2009). Beyond those structural factors, studies have emphasised the important role of vital events in shaping the creation of new ventures (Johnson et al., 2021; Li et al., 2022). Specifically, scholars argue that failure events can substantially influence the extent to which entrepreneurs perceive and exploit entrepreneurial opportunities (Jenkins and McKelvie, 2016; Pontikes and Barnett, 2017; Soublière and Gehman, 2020). Such emphasis is natural, since market actors tend to make decisions by considering the fates of other similar actors (Kim and Miner, 2007). However, existing theories appear to provide opposing views on how failure events may influence new venture creation. While the information view contends that failures render a market undesirable (Chai et al., 2022; Sutton and Callahan, 1987), the competition perspective suggests that failures in a market may help ease competition for factors and products (Chen and Miller, 2012; Kilduff et al., 2010).

The information effect of failure events

On one hand, failure events may act as an information cue about the underlying quality of a market. New venture creation in a market hinges on how nascent entrepreneurs perceive its quality or viability. Promising markets attract more entrepreneurs, whereas unfavourable conditions discourage new venture entry (Davidsson et al., 2020; Priem et al., 2012). In addition to a thorough industry analysis (Porter, 2008), entrepreneur perceptions of a market are highly dependent on how existing firms perform (Xie et al., 2020). While the precise performance of existing firms may be less observable, their failures or bankruptcies are undoubtfully a very salient indicator of poor performance, which is often widely discussed and exaggerated by public media (Pontikes and Barnett, 2017). When many existing firms fail, they collectively signal that the market may be experiencing certain structural problems (Chai et al., 2022; Sutton and Callahan, 1987). Such information shapes consensus views about market viability, which undermines the incentives of nascent entrepreneurs to pursue opportunities in this market (Johnson et al., 2021; Pontikes and Barnett, 2017). Moreover, failure events in a market can also influence the perception of key stakeholders or factor providers such as suppliers, employees and investors (Soublière and Gehman, 2020). When these key stakeholders are concerned about market prospects, it will become more difficult to convince them to support entrepreneurial endeavours that indirectly impede new venture creation.

The competition effect of failure events

On the other hand, however, failure events also lead to reduced competition, which may foster entrepreneurial effort. Firms in the same market compete with each other in terms of acquiring resources (Barney, 1986) and selling products (Hoberg and Phillips, 2010). In the factor market, firms strive to gain more valuable resources such as labour, capital and partnerships, at more reasonable costs (Scheve and Slaughter, 2001). However, because resources are limited, competition intensifies as the number of similar firms increases (Dobrev et al., 2001). In the product market, firms compete with one another in selling similar products to a similar set of customers. The product market competition is intensified when there are more firms that have similar resources and target at common markets (Chen and Miller, 2012). Failures of existing firms, in turn, may decease competition intensity in both factor and product markets. First, failed firms will release their resources back to the factor market such as labour (e.g. managers, engineers and frontline workers), capital (equity and loan facilities) and even other institutional resources (Kroezen and Heugens, 2019; Stuart and Sorenson, 2003). Failures bring more market-specific resources available for nascent entrepreneurs, who will find it easier to launch new ventures in the same field. For instance, when a restaurant in Oslo ceases to operate, its managers, chefs and waiters may become available resources in the market; this will ease the process of resource acquisition when creating a new restaurant. In addition, failures also release entrepreneurial talents such that former employees in the failed firms may turn to become entrepreneurs (Spigel and Vinodrai, 2021; Stuart and Sorenson, 2003) or former entrepreneurs who failed can restart new businesses as serial entrepreneurs (Mason and Harrison, 2006). As such, the factor resources and entrepreneurial talents released by failed firms may act as a ‘push’ force for new venture creation. Meanwhile, in the product market, failed firms automatically create a market gap as their pre-existing customers will be left underserved. The more firms fail in the market, the larger the gap created. As new ventures are mostly established to address market gaps (Davidsson et al., 2020; Priem et al., 2012), the vacuum left by failed firms may act as a pull force that fosters entrepreneurial entry. If a Sushi restaurant in Oslo closes, for example, the market demand for Japanese food may be underserved and so, drive more entrepreneurial effort in this field. 1 As a result, markets may show substantial entrepreneurial resilience (Huggins and Thompson, 2015), with greater levels of entreneurial activity arising from prior failures.

To reiterate, there are competing views on the role of failure events in entrepreneurship. The information signal perspective suggests that failure events undermine new venture creation because they reduce collective beliefs about market viability. Supporting this, Pontikes and Barnett (2017), for instance, show that software companies are less likely to enter into market categories where more firms failed. Conversely, however, the competition view implies that failure events may foster the formation of new ventures as they ease competition in both factor and product markets. In line with this, Kroezen and Heugens (2019) suggest that new craft breweries are likely to be created in the locations where existing ones have left the area. While these previous studies are informative, they appear to point in opposing directions. More importantly, as most of them focus on specific industries, it is still uncertain how failures affect entrepreneurship in the generic, broad context. To shed more light on this from a more general perspective, we investigate the following research question: How will failures of existing firms influence subsequent new venture creation in the same markets?

Data and measures

To address the research question, we adopt an inductive approach by analysing the dynamics of a comprehensive sample of Norwegian firms (Berzins et al., 2019). Our main database, filed from Norwegian registry archives, tracks all firms operating in Norway, with information about their basic accounting statements, employment, industry code, region information and corporate governance information (Luzzi and Sasson, 2016). As such, this database provides quite a complete coverage on industry and organisation demography in the country. While the database includes all types of entities, we focus on limited companies – AS (the private limited companies) and ASA (public limited companies) (Berzins et al., 2019), as the other special types of entities are often regulated or arranged differently (e.g. ANS – general partnerships, BRL – housing cooperative or STI – foundations). Our sample, therefore, includes the whole universe of limited companies in Norway. The sampling period is 2000–2016. As we put 1-year time lag between dependent and explanatory variables, we start to observe new venture creation from 2001. After omitting observations with missing information, our dataset includes roughly 200,000 active firms per year, ranging from about 130,000 in 2000 to 260,000 in 2016.

Key measures

New venture creation

To investigate new venture creation, we count the number of new establishments in each industry of each region at each year. While estimating the counts of new ventures is the standard method in organisational sociology, prior research usually distinguishes them only by regions (Friske and Zachary, 2019; Sorenson and Audia, 2000; Stuart and Sorenson, 2003). That is because most studies focus on a single industry. Because we include all industries in Norway, it is necessary to consider industry heterogeneity. As such, we measure new venture creation at the intersection of region and industry. We use municipalities in Norway as regional units. Norway is currently divided into 11 counties (fyler) and over 400 municipalities (kommuner). Large cities like Oslo are both a county and a municipality. We opt to use municipalities because they are the specific government units responsible for most economic and social activities (Blom-Hansen et al., 2006). We define industries according to two-digital industry codes in Norway’s system, because this middle range of aggregation gives a more useful rendering of industry structure. By contrast, aggregation at the one-digital level is too broad, such that many heterogeneous industries are put under the same code (e.g. manufacture of textile and manufacture of furniture). Codes with three or more digitals generate too many industries, many of which include only a very limited number of firms. Therefore, we measure the number of new establishments registered in each two-digit industry in each municipality at each year t. By doing so, our primary regression sample includes over 137,000 industry-region-level observations for about 13,400 unique industry-region cells over the whole period.

Failure rate in the prior year

We count the number of failure events in each industry of each region at each year t−1. Firm failure occurs at year t−1 when a firm no longer exists in the database since t−1 (Dobrev et al., 2001; Pe’er and Keil, 2013). However, since the total number of failures may be largely correlated with population size, we create a scaled variable, failure rate, measured as the number of failure events divided by the number of active firms in each industry-region cell each year. This helps rule out the potential confounding effect of population size from estimating the effect of failure events. To avoid simultaneity, we add 1-year time lag between failure rates (measured at year t−1) and new venture creation (measured at year t).

Control variables

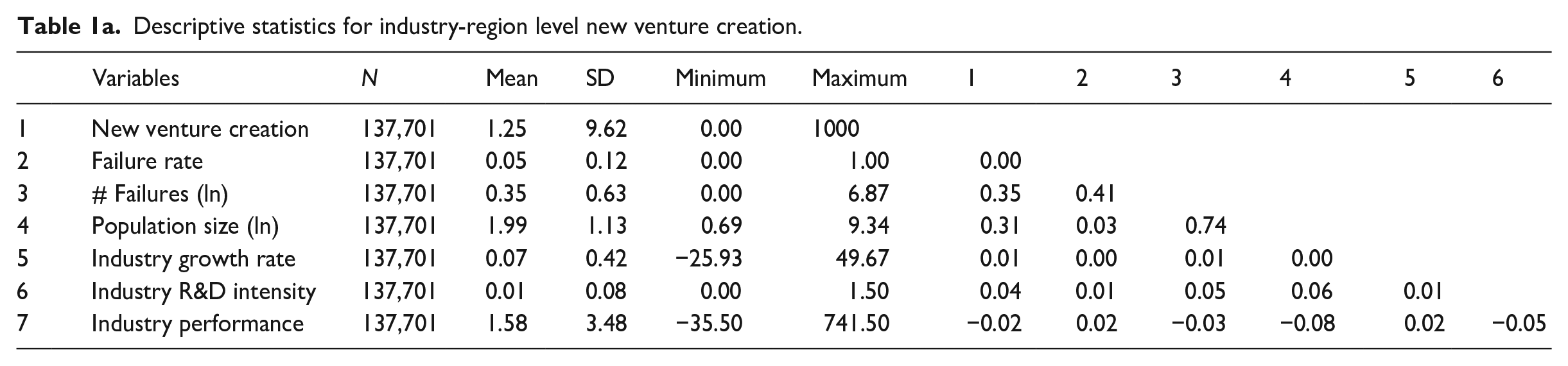

In estimating new venture creation, we control for a set of industry-region level variables. We include population size, measured as the number of active firms at year t−1 (Sorenson and Audia, 2000). 2 To control for industry performance and potential, we use industry growth rate (based on the change rate of industry-region-aggregated annual revenues from year t−2 to t−1) and industry performance (average return on assets: industry-region-aggregated revenues divided by aggregated total assets at t−1) (Zhou et al., 2017). 3 We also control for industry R&D intensity, measured as the total R&D expenditures divided by total revenues in each industry-region cell. While high R&D industries are often characterised by a higher rate of entry and exit, higher R&D intensity might also create a higher barrier for potential entrants. Year fixed-effects are included to account for time-related heterogeneity. As we use industry-region fixed effects estimation models, time-invariant variables at the industry or region level are mechanically omitted. Table 1(a) reports descriptive statistics and correlations. 4

Descriptive statistics for industry-region level new venture creation.

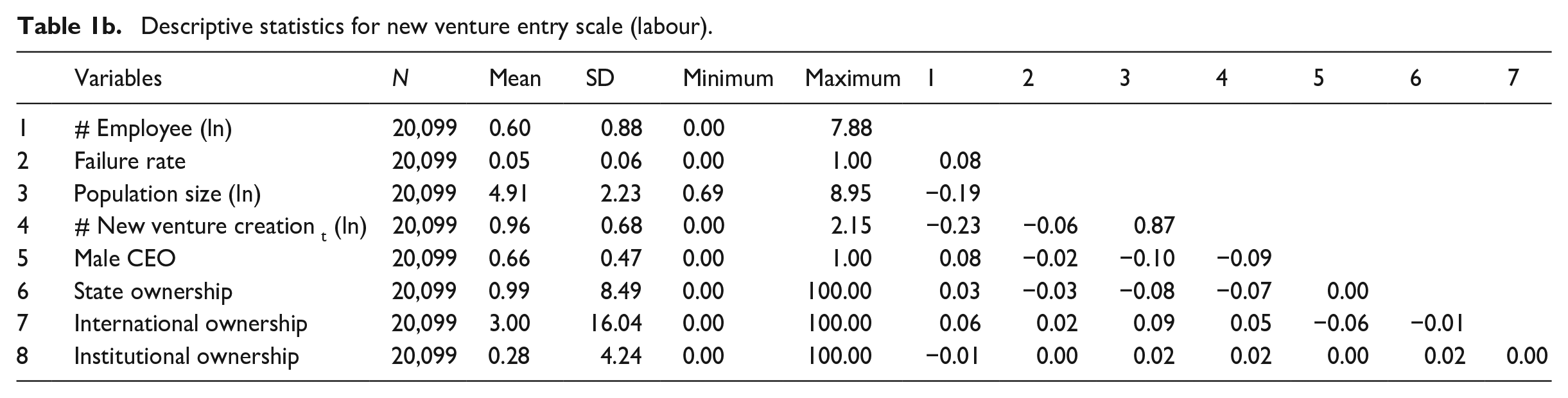

Descriptive statistics for new venture entry scale (labour).

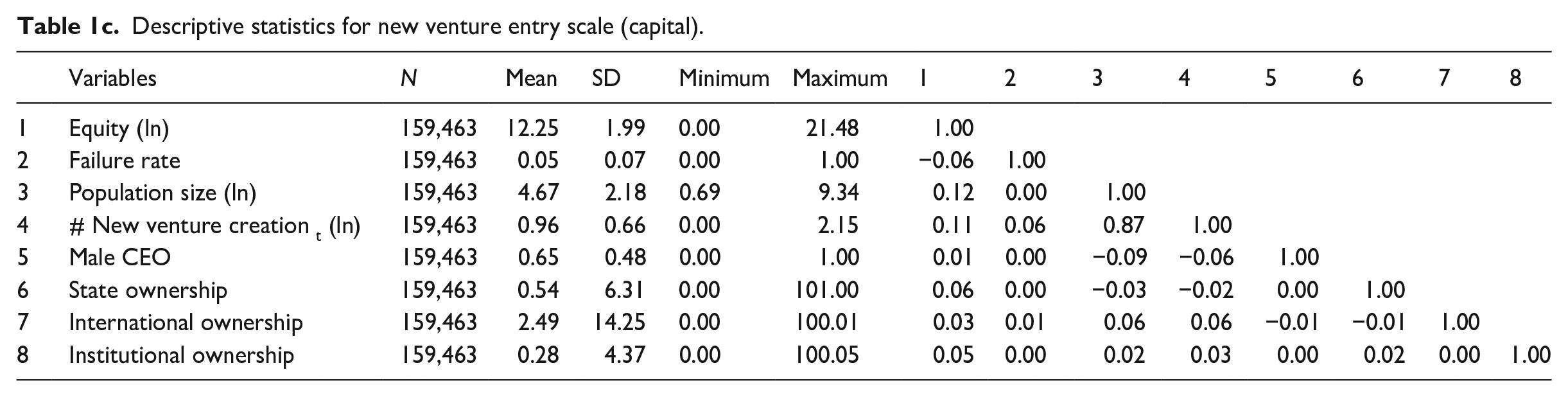

Descriptive statistics for new venture entry scale (capital).

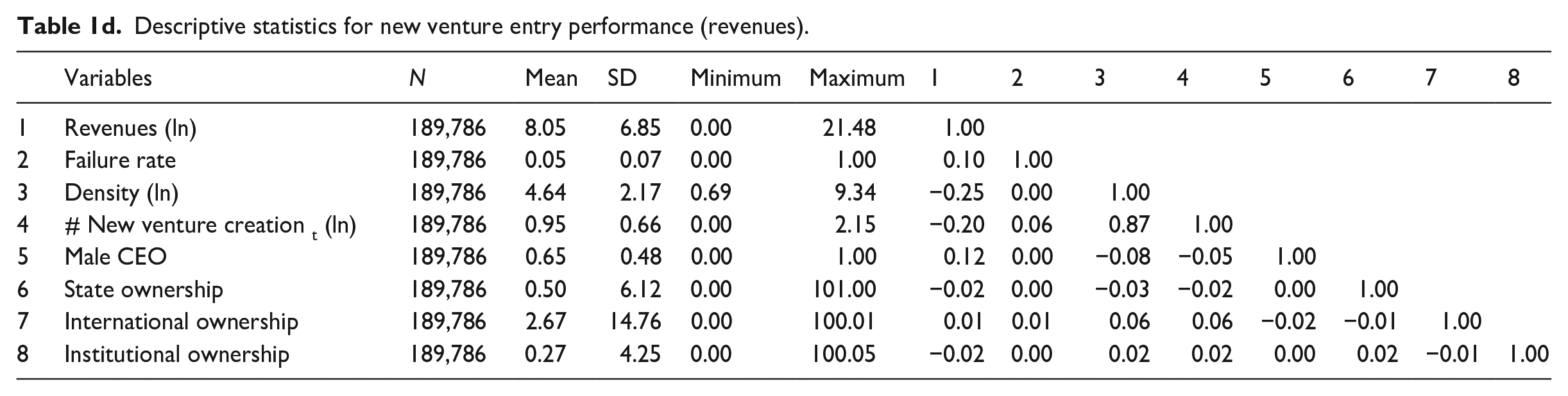

Descriptive statistics for new venture entry performance (revenues).

Estimation and results

New venture creation

The dependent variable, new venture creation, is a count measure with skewed distribution. We employ fixed-effects (or conditional) negative binomial regression (Stuart and Sorenson, 2003), which accounts for the possibility that some unspecified factors vary systematically with location and industry. It also helps cope with overdispersion and time dependence, as this estimator conditions on the total number of events in a particular industry-region cell.

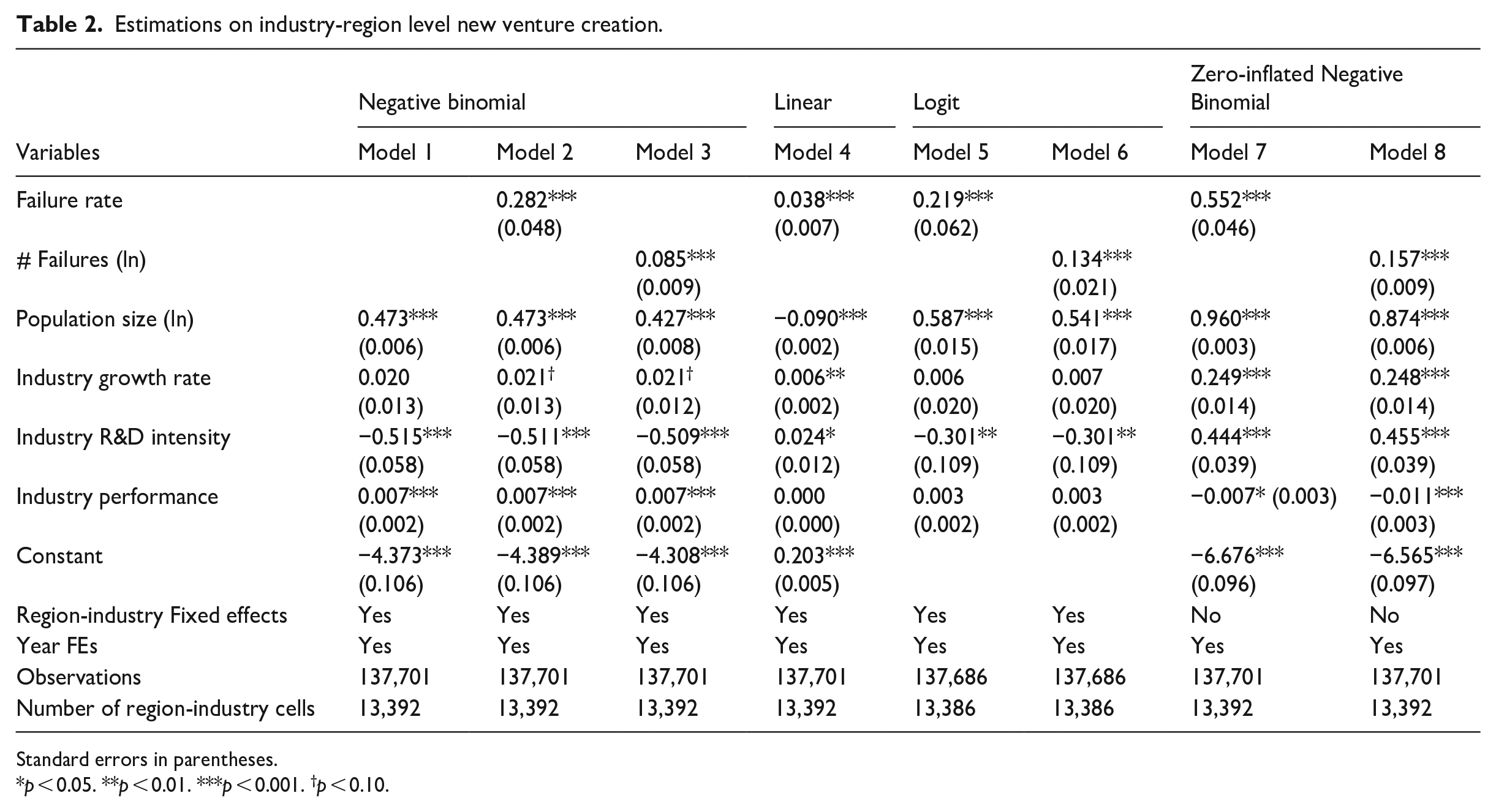

The results are presented in Table 2. Model 1 includes only control variables. The main effect of population size is positive, consistent with prior studies on population ecology (Sorenson and Audia, 2000; Soublière and Gehman, 2020). Industry performance is also positive, suggesting that more ventures are created when markets generate more returns. Interestingly, industry R&D intensity is negative, suggesting that more new ventures in Norway are created when industry R&D activities are lower. This may indicate that R&D intensity also escalates entry barrier for prospective entrepreneurs.

Estimations on industry-region level new venture creation.

Standard errors in parentheses.

p < 0.05. **p < 0.01. ***p < 0.001. †p < 0.10.

Model 2 includes failure rate. It has a positive and significant effect on new venture creation (β = 0.282, SE = 0.048). It means that while holding all other variables constant, if failure rate increases by 10%, the number of new ventures will increase by about 2.86% (=exp(0.282 × 10%)−1). In Model 3, we replace failure rate with the absolute number of failures (the log of one plus the number of failures). The effect is also positive (β = 0.085, SE = 0.009). In Models 4–8, we employ alternative model specifications. In Model 4, we replace the dependent variable with the number of new ventures scaled by population size. As it is a continuous variable, we use linear fixed-effects estimations. In Models 5 and 6, we use fixed-effects logit regressions, instead of negative binomial, because the dependent variable is zero for a large proportion of observations. In Models 7 and 8, we use zero inflated negative binomial regressions. The results are all consistent with our prior findings.

Industry-level estimation

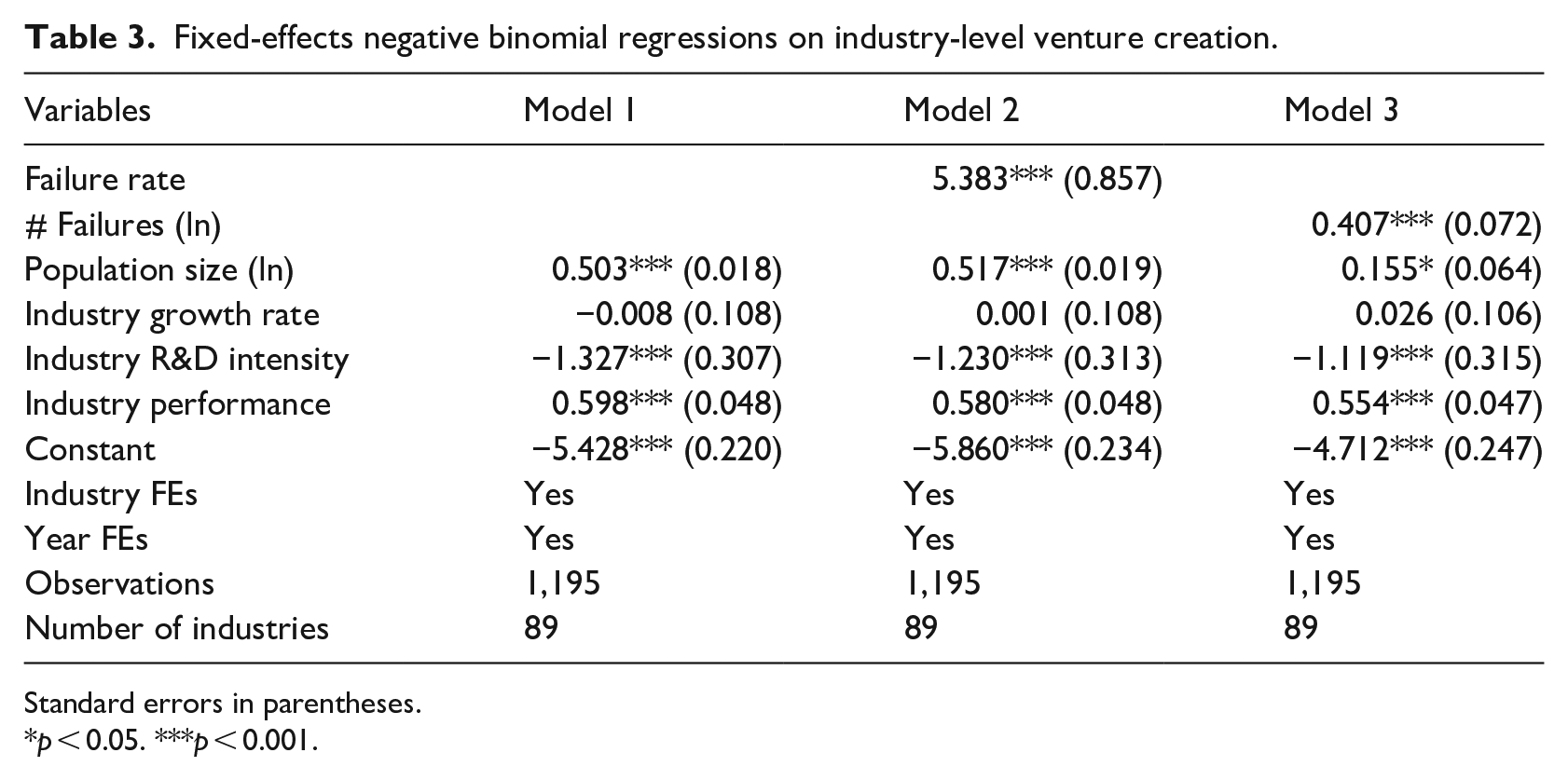

Moreover, it is possible that our unit of analysis (industry-region) is overspecified because failure events may spill over across regions. When more firms fail in a region, its neighbouring regions may also be affected. For instance, the employees released by failed firms in one city may flow to others thereby, affecting new venture creation beyond the focal city. This may be particularly so for small countries like Norway. As such, in this extensional analysis, we relax the assumption that the effect of prior failures is locally constrained. More specifically, we use only industries as the unit of analysis, so that the impact of failures in one industry would diffuse across the entire Norway. 5 Results from fixed-effects negative binomial regressions are reported in Table 3. The results are consistent with our findings above, as both failure rate and the number of failures in Models 2 and 3 are positively related to the likelihood of new venture creation. Overall, results in this section suggest that failures of existing firms in a market foster subsequent new venture creation.

Fixed-effects negative binomial regressions on industry-level venture creation.

Standard errors in parentheses.

p < 0.05. ***p < 0.001.

De alio and de novo ventures

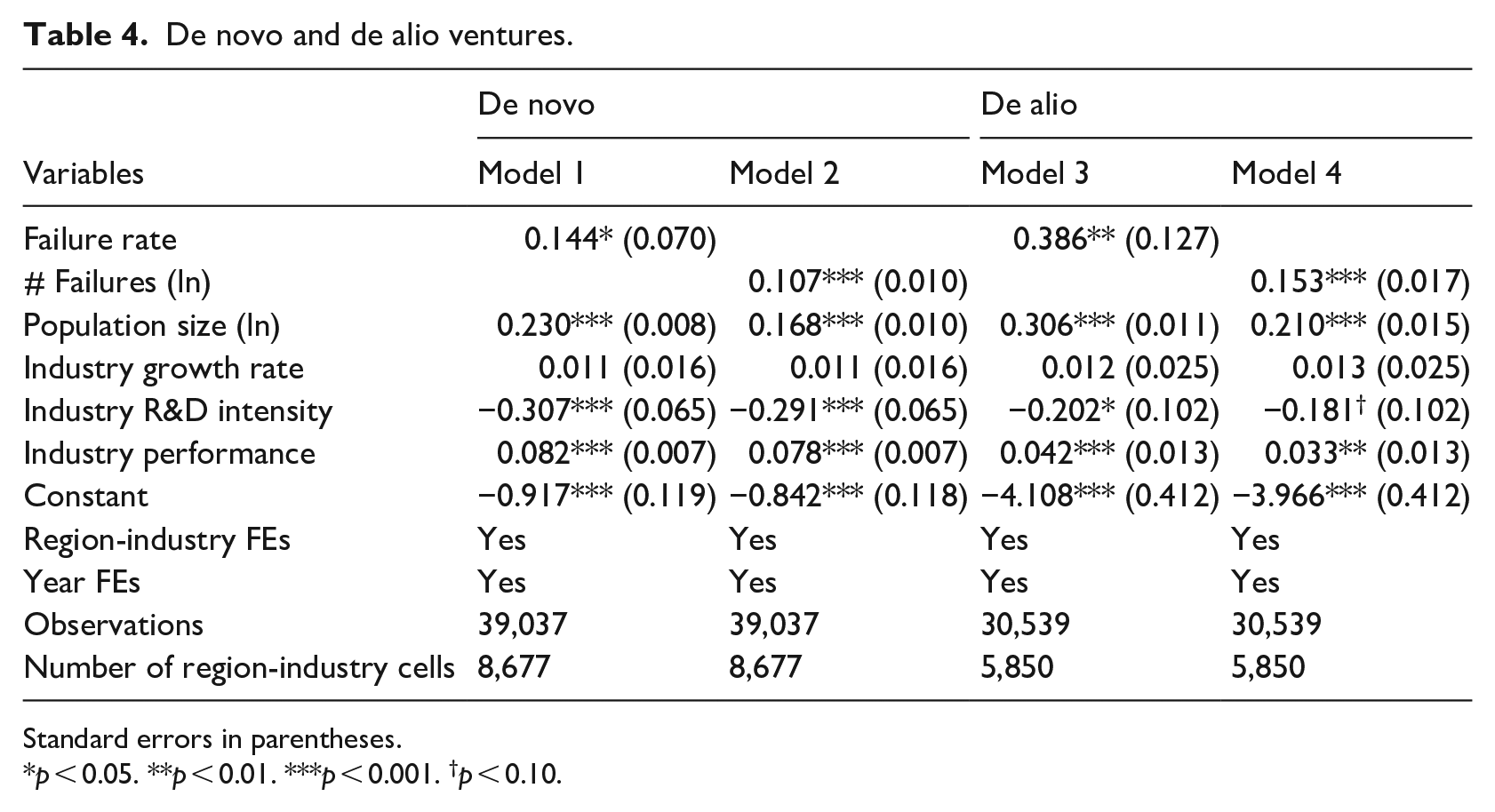

As discussed earlier, failed firms may release both production factors and entrepreneurial talents that spur new venture creation (Mason and Harrison, 2006; Spigel and Vinodrai, 2021). As such, some ventures may be closely associated with previous failures (i.e. serial entrepreneurs), while others not. Ideally, we would like to focus upon this by tracking the same individuals. But our data provide no identity information about founders and directors, which prevent a detailed analysis. Yet, the data do provide information about whether each new venture is an independent entity or part of other entities. The former is often noted as de novo ventures and the latter as de alio (Wang, 2021). Our assumption is that serial entrepreneurship is less likely to be observed in de alio than de novo. Among ventures with sufficient information about their independence, about 25% are de alio and 75% are de novo. We then separately estimate the number of new de alio ventures and the number of new de novo ventures being created each year, using the same estimation approach. The results are reported in Table 4. For both types of new ventures, prior failures show a positive effect. While inconclusive, these findings suggest that prior failures may lead to both more de alio ventures where serial entrepreneurship is less relevant, and more de novo ventures where serial entrepreneurship is more prevalent.

De novo and de alio ventures.

Standard errors in parentheses.

p < 0.05. **p < 0.01. ***p < 0.001. †p < 0.10.

Market heterogeneity

While our estimation above focuses on the net effect of failures on entrepreneurship, it is definitely not unconditional. As the relative forces of ‘information signalling’ and ‘competition’ may be manifested differently across markets or industries, the net effect of failures may change accordingly. To shed more light on heterogeneity across industries, we conduct two sets of additional tests.

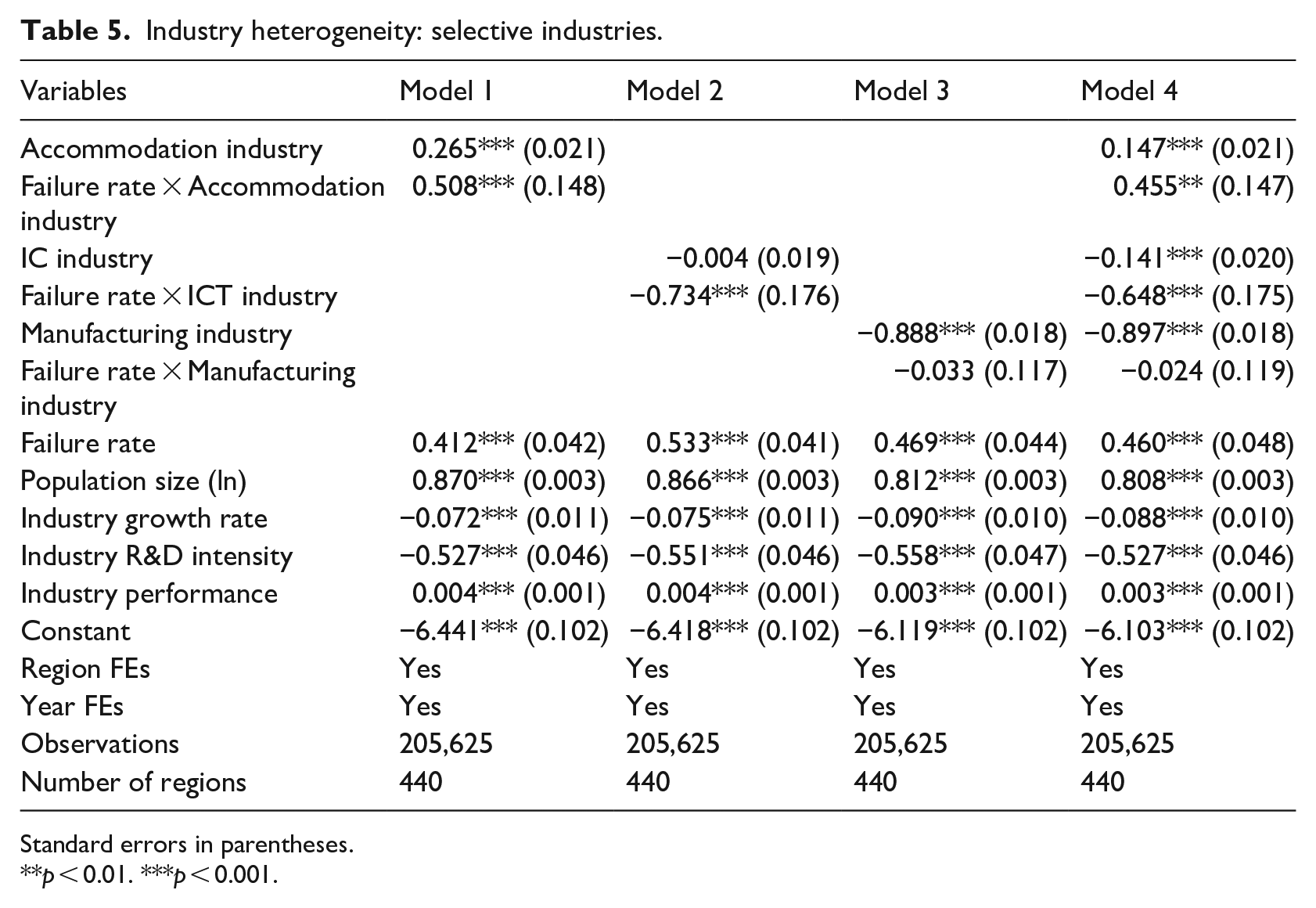

First, we suspect that the information signalling effect may be more prominent in tech industries with higher-level innovation (e.g. Information and communication technology (ICT)) (Pontikes and Barnett, 2017), such that the net positive effect of failures on new venture creation will become weaker (or even turn negative). By contrast, prospective entrepreneurs in the traditional industries with lower-level innovation (e.g. accommodation) may be less sensitive to market signals as they mostly pursue ‘lifestyle businesses’. In such industries, information signals may become less relevant. To test this idea, we code selective industries based on the Norwegian standard industry classification (ssb.no/en/klass/klassifikasjoner/6). Specifically, we identify industries in the accommodation if their two-digit industry codes are 55 or 56, and industries in the ICT if their codes range between 58 and 63. Moreover, we also use generic manufacturing industries (codes between 10 and 33) for comparison. We then interact failure rate with the three industry dummies. The results from region fixed-effects estimations are reported in Table 5, which are mostly consistent with our conjecture. The interaction with accommodation is positive, suggesting a stronger competition effect (or lesser signalling effect) in accommodation industries; the interaction with ICT is negative, suggesting a stronger signalling effect (or weaker competition effect) in information and communication industries. In comparison to the specific accommodation and ICT industries, the interaction of manufacturing and failure rate is non-significant, suggesting no significant differences between generic manufacturing and non-manufacturing industries.

Industry heterogeneity: selective industries.

Standard errors in parentheses.

**p < 0.01. ***p < 0.001.

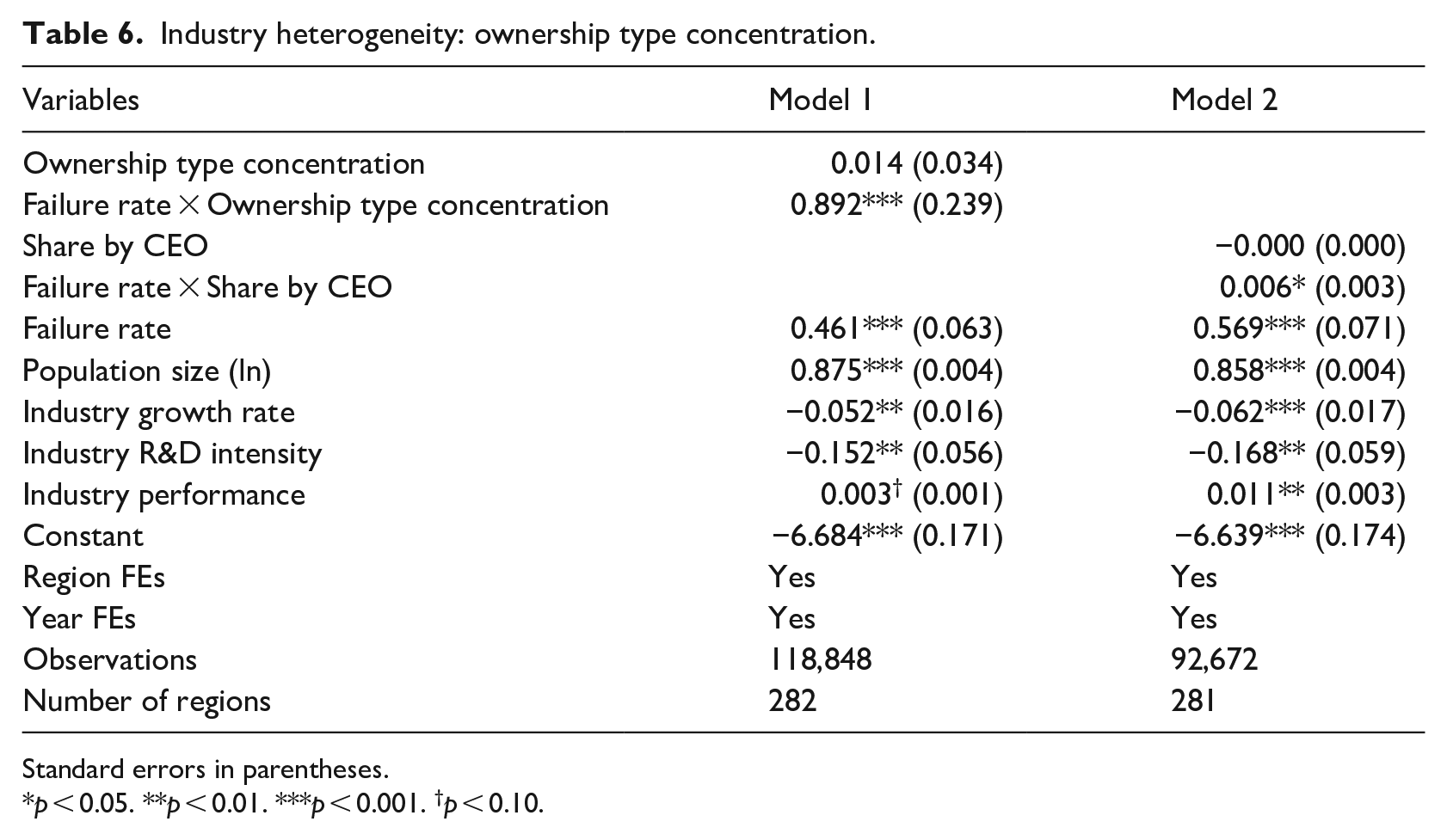

Second, it is also possible that the signalling effect of failure events is more prevalent when venture creation involves multiple stakeholders (e.g. private investors or institutional investors). When being accountable to diverse market audiences, entrepreneurs will be more risk averse and make more elaborate information searches (Vieider, 2009). As such, we suspect that the information signalling effect is stronger in industries characterised by more stakeholder involvements. While our data do not include a precise measure of multiple stakeholders, we develop a closest possible proxy. Specifically, for each firm, we calculate the Herfindahl index of its ownership type. Firms may have different types of ownership such as personal, state, institutional, and international in the database. The Herfindahl index indicates how concentrated their ownership is on certain types of owners. We then calculate ownership type concentration as the mean Herfindahl index across all firms for each industry-region cell each year. A larger value suggests that firms in the industry-region cell mostly have concentrated ownership (and hence less exposure to multiple types of shareholders), whereas a lower index suggests that its firms are owned more equally by multiple types of shareholders. We then interact it with failure rate.

The results are reported in Model 1 of Table 6. The interaction term is positive (β = 0.892, SE = 0.239). This suggests that when firms in a market involve more concentrated ownership, the positive effect of failures is stronger (i.e. a stronger competition effect). By contrast, when firms involve less concentrated ownership (more exposure to multiple types of shareholders), the net positive effect of failures is weaker (i.e. a stronger signalling effect). Moreover, in Model 2, we use the share by CEO as another proxy. The assumption is that if CEOs own a larger share, they will involve fewer external stakeholders, such that the signalling effect is weaker (and hence a stronger positive effect of failures). Indeed, we see a positive effect for the interaction term between share by CEO and failure rate in Model 2. Altogether, these findings provide consistent patterns, which hint that when industries are exposed less to multiple external stakeholders, the signalling effect of failures become less relevant such that the net positive effect of failures will be stronger.

Industry heterogeneity: ownership type concentration.

Standard errors in parentheses.

p < 0.05. **p < 0.01. ***p < 0.001. †p < 0.10.

New venture entry scale and performance: Exploring the competition mechanisms

In addition to estimating the effect of failures on new venture creation, we turn next to the founding features of new ventures to analyse their entry scale and performance. By so doing, we endeavour to explain the positive relationship between them. Specifically, this relationship may be explained by at least two mechanisms – factor and product market competition.

Entry scale: factor market competition effect

When many firms fail more resources (e.g. labour and capital) may be released back to the factor market, which pushes new venture creation. If this is the case, it will be easier for new ventures to scale up their acquisition of labour and capital. To test this possibility, we use two proxy measures of entry scale: (1) the number of employees 6 and (2) the amount of total equity acquired by a new venture at its first year of establishment. They are both firm-level measures. We use their logarithm transformation (plus one) to reduce skewness. Tables 1(b) and 1(c) report descriptive statistics and correlations for the labour and capital estimation samples, respectively.

Entry performance: Product market competition effect

When many firms fail, this leads to market vacuum, which pulls more new ventures into being created to fill the gap. If so, these new ventures might be able to deliver a better market performance, at least in the short run. To examine this possibility, we gather information on new venture market revenues at their first year of establishment, as a proxy of their entry performance. As the measure is skewed, we use its logarithm transformation (plus one) in regressions. Table 1(d) reports descriptive statistics and correlations for the sample analysing market revenues.

Additional control variables

In estimating the entry features of new ventures, we also include a set of additional controls. First, population size is included, accounting for overall crowdedness or competition in the market. We also control for the gender of CEO (male CEO), as female and male entrepreneurs may behave and perform differently (Robb and Watson, 2012). To account for heterogeneity in capital structure, we include shares of state ownership, international ownership and institutional ownership in new ventures. We also control for the number of new ventures created in the same industry-region cell at the same year t as the focal firm, which may escalate competition for available resources and market shares. Year fixed-effects are also included to account for temporal heterogeneity.

Estimation and results

We employ the industry-region fixed-effects approach to predict new venture entry scales and entry performance. Since those variables are continuous measures, we use a generalised least squares estimator (Soublière and Gehman, 2020), instead of the negative binomial estimator. We also cluster standard errors at the region level to account for potential heteroscedasticity. 7

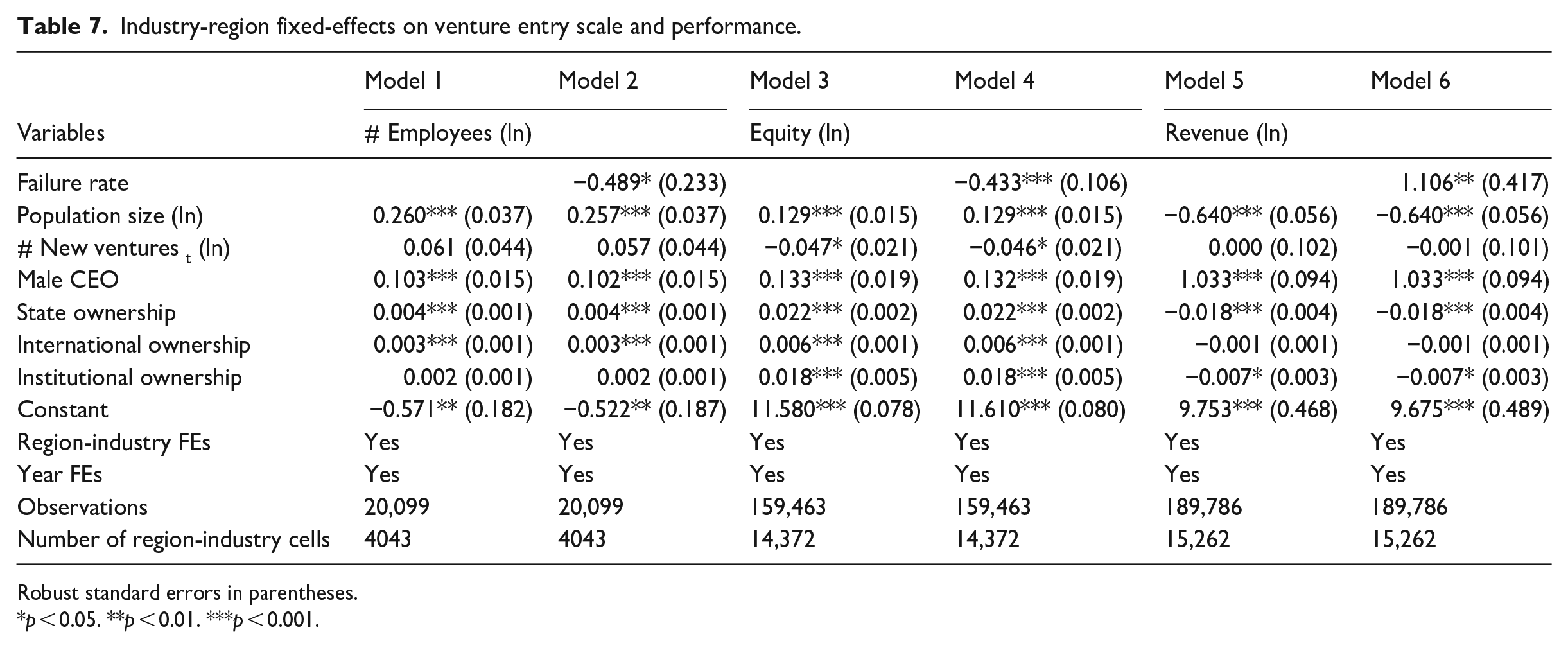

Results are reported in Table 7. Models 1, 3, and 5 show results with only control variables. In Model 2, we add failure rate to predict employment scale, which has a negative and significant coefficient (β = −0.489, SE = 0.233). It suggests that new ventures hire fewer employees, when being created after more prior failures in the market. More precisely, as failure rate increases 10%, the number of employees at the new venture founding stage decreases by about 4.8% (=1−1/exp(0.489 × 10%)). In Model 4, we add failure rate to predict capital scale, which has a negative and significant coefficient (β = −0.433, SE = 0.106). This suggests that new ventures acquire less equity, if being established after more failure events. More precisely, as failure rate increases by 10%, the amount of equity at new the venture founding stage decreases by about 4.2% (=1−1/exp(0.433 × 10%)). Altogether, the results indicate that new ventures that are created after more firm failures will have a smaller entry scale. This is opposite to what would be expected from the factor market competition argument.

Industry-region fixed-effects on venture entry scale and performance.

Robust standard errors in parentheses.

p < 0.05. **p < 0.01. ***p < 0.001.

In Model 6, we estimate the effect of failure rate on market performance, which has a positive and significant effect (β = 1.106, SE = 0.417). More precisely, as failure rates increases by 10%, a new venture’s first-year market revenues increase by about 11% (=exp(1.106 × 10%)−1). It suggests that new ventures deliver a better entry performance, when being created after more failures in the market. This finding is consistent with the product market competition explanation: prior failures reduce product market competition which pulls new ventures into being created to fill the underserved market demand. Taken together, we find that ventures created after higher numbers of failures tend to be smaller scale but gain greater short-term revenues. This suggests that the failure-induced new venture creation is mainly pulled by the gap in the product market, rather than pushed by the resource abundance in the factor market. Meanwhile, their smaller entry scales may also hint the information signalling effect of failure events. Although entrepreneurs are likely to enter the market with more prior failures, they may also be cautious in exploiting it as they refrain from substantial investment in labour and capital resources.

Long-term performance: Survival

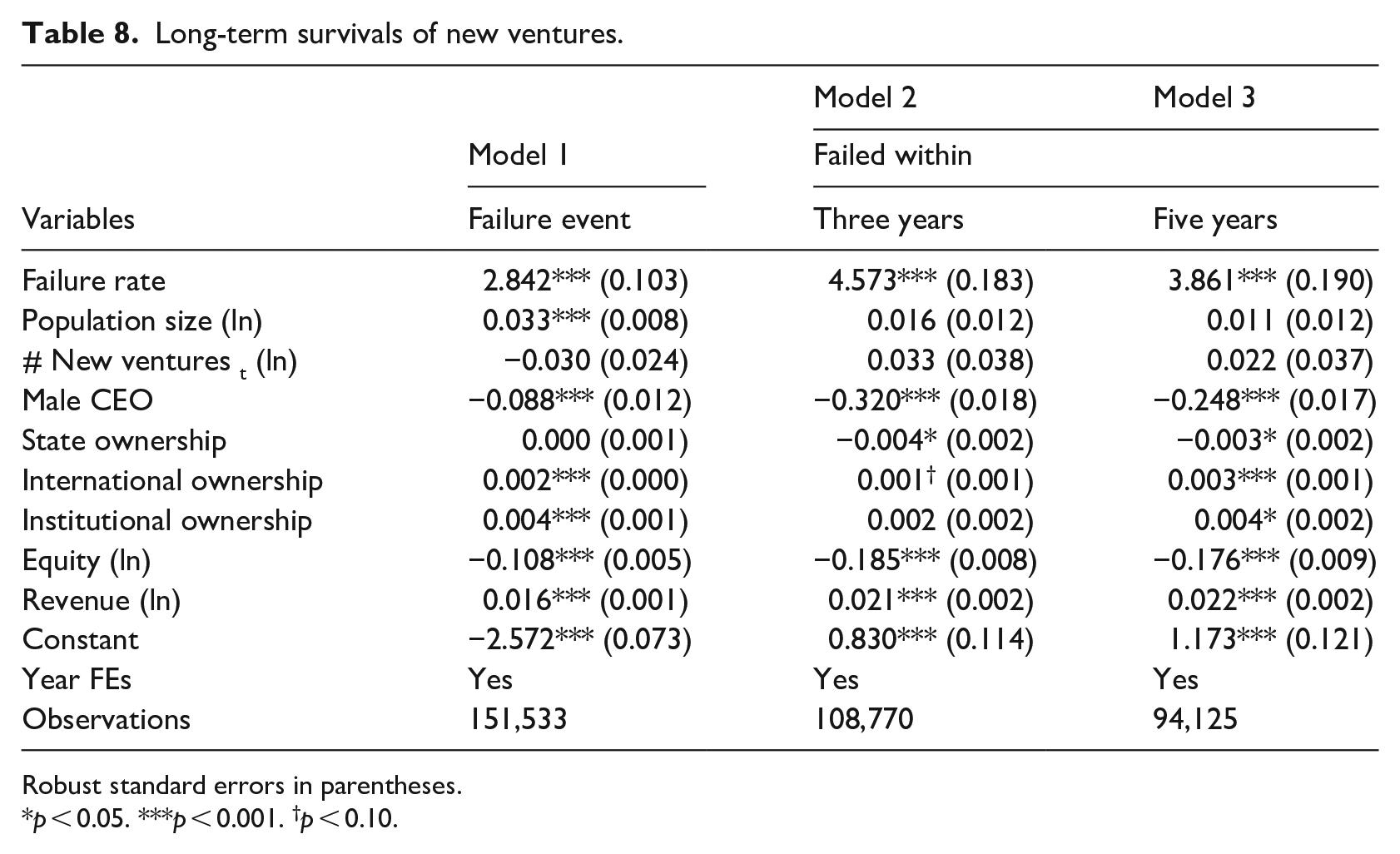

Finally, it is interesting to see how these ventures perform in the long term, given that short-term performance may not necessarily guarantee long-term success (Wennberg et al., 2011). Prior studies on non-consensus entrepreneurship suggest that ventures created following more failures are more likely to survive (Pontikes and Barnett, 2017). They argue that because failure events lead to a negative perception of market viability, entrepreneurs attempting to enter the tainted market will face more scrutiny from stakeholders. This scrutiny may heighten the selection threshold for entry so that those ventures finally created will be better suited to the market. However, it is also possible that there are some fundamental and structural problems in the market (Agarwal et al., 2002; Porter, 2008), such that the newly created ventures are also more likely to fail.

To address this question, we conducted an additional analysis for venture survival. More specifically, we used maximum likelihood estimation Weibull hazard rate models to predict the failure likelihood of different new ventures (Delmar and Shane, 2004), and report robust standard errors clustered at the industry-region level. Consistent with our operationalisation above, new ventures are defined as failures at the year when they cease to exist in the database. The results are presented in Table 8. In Model 1, failure rate at their entry period has a positive effect on the failure speed of new ventures (β = 2.842, SE = 0.103). It suggests that new ventures are more likely to fail, if they are created right after more prior failures in the market. In Models 2 and 3, we use logit models to estimate the likelihood that new ventures fail within three and five years, respectively. Both show results that are consistent with the hazard rate analysis, as failure rate show a significant and positive effect on the failure of focal ventures. Taken together, we observe that when ventures are created after more failures of existing firms, they are likely to deliver a better short-term performance, but at the same time to end up with long-term failures.

Long-term survivals of new ventures.

Robust standard errors in parentheses.

p < 0.05. ***p < 0.001. †p < 0.10.

Discussion

Analysing a large-scale sample of firms in Norway, this article explores how failures of existing firms influence subsequent new venture creation. While existing theories points in opposing directions, our empirical results show solid evidence that when there are more failure events in the market, there will be more new ventures created. Although it seems counterintuitive from the information perspective, this finding is consistent with the competition-based argument: firm failures ease competition for limited market resources; this fosters entrepreneurship effort. However, this effect is not unconditional as industry features are found to shape the relative forces of information and competition. Our additional investigation suggests that the effect may be driven by the competition effect in the product market rather than that in the factor market. Ultimately, we find that new ventures created after many failure events can deliver better short-term market performance but they are also less likely to survive in the long term. These results provide important implications for theory and practice.

Failure events and new venture creation

Our findings reveal a nuanced understanding of the role of failure events in entrepreneurship. The conventional assumption in prior literature is that failure events act as a salient and strong negative signal about the viability of a market (Chai et al., 2022); this undermines entrepreneurial effort (Pontikes and Barnett, 2017; Soublière and Gehman, 2020). In contrast, our study introduces the competition perspective to emphasise that failures may foster new venture creation through reducing competition intensity in both factor and product markets (Chen and Miller, 2012; Kroezen and Heugens, 2019; Thakur, 1999). Our large-scale analysis of Norwegian firms shows evidence supporting the prevalence of the competition perspective: there will be more new ventures in the market where many existing firms have failed. Our findings are in contrast to those of Pontikes and Barnett’s (2017) research that emphasises the information perspective. Specifically, they find that entrepreneurs follow the waves, so that failure events will discourage entrepreneurial entry. The contrast may be related to differences in our empirical design: while we analyse new venture creation in all industries of Norway, Pontikes and Barnett (2017) focus on market entry of U.S. software firms. First, it is possible that the software market has greater uncertainty, such that the information side of failure events is more profound in guiding the next move by entrepreneurs. However, in other markets with relatively lower uncertainty, the role of information may be subtle. Supporting this, our extensional analyses suggest that the effect of failure events in the Norwegian ICT industries is less positive (or more negative) than that in other industries. Second, their work in fact analyses the market segment entry (and exit) of incumbent firms, rather than the creation (and failures) of completely new establishments. Different from new venture creation, market entry of incumbents may be more subject to the information cue of failure events, as their moves have to be better justified to extant market stakeholders (York and Lenox, 2014). Given those considerations, we believe our research has broader generalisability in new venture creation. However, more dedicated research is needed to discuss additional important contingencies.

Factor and product market competition

We also endeavour to explore possible mechanisms, by distinguishing the competition effect in factor and product markets. On the one hand, we find new ventures that are created after more failure events will have greater market revenues at the entry stage. It suggests that prior failures reduce competition in the product market, leaving more market vacuum, which allows new ventures to scale up revenues in a short period. On the other hand, however, we find that these new ventures tend to hire fewer employees and acquire less equity during their entry. This is opposite to what would be expected from the competition effect in the factor market. If failures ease competition for acquiring factor resources, new ventures would be more likely to build a larger organisation scale in terms of labour and capital. Altogether, the findings suggest that these new ventures are mainly ‘pulled’ by the product market vacuum, rather than ‘pushed’ by the factor abundance. Moreover, the fact that such type of ventures can garner larger revenues with fewer resources during the entry stage also implies that these ventures are in fact more productive, at least in the short term. Nevertheless, it is still plausible that failures of existing firms will release more resources (e.g. labour, capital, distribution channels and supplier relations) back to the factor market, which can be utilised by nascent entrepreneurs. The fact that these entrepreneurs refrain from substantial resource acquisition may suggest that they (and/or the factor markets) are more cautious in exploring the focal market vacuum (i.e. more conservative moves), after observing many failure events in the market. This also hints the relevance of the information signalling effect in the market. In other words, while the net effect of failures is found to be positive, it only suggests that the competition effect is relatively stronger than the information effect. Yet, it does not mean that failure events provide no information cues at all. Indeed, smaller entry scales indicate that entrepreneurs (and/or the factor markets) are in fact subject to the negative signalling effect stemming from prior failures.

Short- and long-term performance

Our study highlights the contrast between short- and long-term performance of these new ventures. Although new ventures that are created after many failure events show strong short-term performance, they are significantly less likely to survive in the long run. As discussed above, strong performance in the short run may be largely enabled by the product market vacuum resulting from the dissolutions of existing firms. However, lower long-term survival rates may also suggest that the market with many failure events has some fundamental and structural issues. These issues can be unhealthy competition, lack of sophisticated demand, and lack of supporting industries (Porter, 2008).

Because these issues are often implicit or invisible on the surface, nascent entrepreneurs who are attracted by the more explicit market vacuum may overlook them. Whereas market vacuum acts as a dominant force for venture’s short-term performance at the entry stage, the impact of structural issues intensifies over time, which ultimately erodes their chances of long-term survival. In other words, this may reflect the short-termism or irrationality of many entrepreneurs (Lumpkin et al., 2010). While they all aspire to become phoenix rising from the ashes, oftentimes nirvana does not materialise. Indeed, there are some anecdotal cases for that. Since 2018, for instance, the low-cost airline company Norwegian Air Shuttle (NAS) has been struggling close to bankruptcy and narrowing its market scope over time, which left some flight routes underserved. Being attracted by the market opportunity (at least partially), Flyr was established in August 2020 by a team of NAS veterans and co-founders. While Flyr enjoyed early success on popular routes, it unfortunately filed for bankruptcy in January 2023 (Nikel, 2023). There might exist some fundamental issues in Norway’s low-budget airline market, which were overlooked by Flyr’s founders.

Limitations and future studies

While our study shows interesting results, it is not without limitations. First, we see a potential concern about the identification of failures and new venture creation (Jenkins and McKelvie, 2016). We follow prior research to define failure when a firm is inactive (Dobrev et al., 2001; Pe’er and Keil, 2013). While most of inactive firms do cease to operate, a few of them may be acquired by others or closed due to retiring entrepreneurs, which we cannot detect from the available data. Similarly, some new ventures may be established by incumbents, which are hidden in the complex ownership chains.

Second, as we have no identity information about entrepreneurs or founders, we cannot identify whether new ventures are closely associated with prior failures. The positive relationship we observed may be partially explained by some serial entrepreneurs who failed and restart new businesses (Mason and Harrison, 2006), or some employees who lost their jobs and turn to entrepreneurship (Spigel and Vinodrai, 2021). But they may have very different implications for venture performance and regional development. We leave it to future studies.

Third, our findings are based on the analysis of firm dynamics within only one country. While we believe that similar competition effect is evident in most other contexts, it is still uncertain whether failure events would exert exactly the same influence on new venture creation as we observe in Norway. As entrepreneurship is largely dependent on formal and informal institutions (Stam and Van de Ven, 2021), it is therefore interesting to replicate our study in different countries.

Fourth, our analysis may be subject to the potential endogeneity concern (Cho and Orazem, 2021). Specifically, both firm failure and creation may be contingent on other unobserved factors. In our empirical design, we have tried to address the concern by employing fixed-effects estimation and putting time lags between them. However, we understand that the endogeneity concern is never fully resolved.

Finally, while we focus on the overall pattern, we have downplayed heterogeneity across regions and industries. Industries differ in their technological regimes such as opportunities, appropriability, cumulativeness, and knowledge base conditions (Malerba and Orsenigo, 1997); regions vary in terms of factor, demand, competition and infrastructure conditions (Porter, 2008). As such, it is interesting to consider how these conditions shape the relationship between failures and entrepreneurship.

Conclusion

Our study deepens understanding of how failures of existing firms affect subsequent new venture creation. While the conventional information view suggests a negative signalling effect, we find solid evidence for the opposite after analysing all industries in Norway. We also show that this may be driven by the product market competition effect: failed firms leave more entrepreneurial opportunities, which attracts the formation of new ventures. Finally, our study warns that such entrepreneurial opportunities may be a trap as new ventures exploiting them are more likely to end up failing.

Footnotes

Acknowledgements

I would like to thank the Center for Corporate Governance Research for providing high-quality Norwegian administrative and accounting data that enables this work.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.